Bitcoin Polynomial Regression OscillatorThis is the oscillator version of the script. Click here for the other part of the script.

💡Why this model was created:

One of the key issues with most existing models, including our own Bitcoin Log Growth Curve Model , is that they often fail to realistically account for diminishing returns. As a result, they may present overly optimistic bull cycle targets (hence, we introduced alternative settings in our previous Bitcoin Log Growth Curve Model).

This new model however, has been built from the ground up with a primary focus on incorporating the principle of diminishing returns. It directly responds to this concept, which has been briefly explored here .

📉The theory of diminishing returns:

This theory suggests that as each four-year market cycle unfolds, volatility gradually decreases, leading to more tempered price movements. It also implies that the price increase from one cycle peak to the next will decrease over time as the asset matures. The same pattern applies to cycle lows and the relationship between tops and bottoms. In essence, these price movements are interconnected and should generally follow a consistent pattern. We believe this model provides a more realistic outlook on bull and bear market cycles.

To better understand this theory, the relationships between cycle tops and bottoms are outlined below:https://www.tradingview.com/x/7Hldzsf2/

🔧Creation of the model:

For those interested in how this model was created, the process is explained here. Otherwise, feel free to skip this section.

This model is based on two separate cubic polynomial regression lines. One for the top price trend and another for the bottom. Both follow the general cubic polynomial function:

ax^3 +bx^2 + cx + d.

In this equation, x represents the weekly bar index minus an offset, while a, b, c, and d are determined through polynomial regression analysis. The input (x, y) values used for the polynomial regression analysis are as follows:

Top regression line (x, y) values:

113, 18.6

240, 1004

451, 19128

655, 65502

Bottom regression line (x, y) values:

103, 2.5

267, 211

471, 3193

676, 16255

The values above correspond to historical Bitcoin cycle tops and bottoms, where x is the weekly bar index and y is the weekly closing price of Bitcoin. The best fit is determined using metrics such as R-squared values, residual error analysis, and visual inspection. While the exact details of this evaluation are beyond the scope of this post, the following optimal parameters were found:

Top regression line parameter values:

a: 0.000202798

b: 0.0872922

c: -30.88805

d: 1827.14113

Bottom regression line parameter values:

a: 0.000138314

b: -0.0768236

c: 13.90555

d: -765.8892

📊Polynomial Regression Oscillator:

This publication also includes the oscillator version of the this model which is displayed at the bottom of the screen. The oscillator applies a logarithmic transformation to the price and the regression lines using the formula log10(x) .

The log-transformed price is then normalized using min-max normalization relative to the log-transformed top and bottom regression line with the formula:

normalized price = log(close) - log(bottom regression line) / log(top regression line) - log(bottom regression line)

This transformation results in a price value between 0 and 1 between both the regression lines.

🔍Interpretation of the Model:

In general, the red area represents a caution zone, as historically, the price has often been near its cycle market top within this range. On the other hand, the green area is considered an area of opportunity, as historically, it has corresponded to the market bottom.

The top regression line serves as a signal for the absolute market cycle peak, while the bottom regression line indicates the absolute market cycle bottom.

Additionally, this model provides a predicted range for Bitcoin's future price movements, which can be used to make extrapolated predictions. We will explore this further below.

🔮Future Predictions:

Finally, let's discuss what this model actually predicts for the potential upcoming market cycle top and the corresponding market cycle bottom. In our previous post here , a cycle interval analysis was performed to predict a likely time window for the next cycle top and bottom:

In the image, it is predicted that the next top-to-top cycle interval will be 208 weeks, which translates to November 3rd, 2025. It is also predicted that the bottom-to-top cycle interval will be 152 weeks, which corresponds to October 13th, 2025. On the macro level, these two dates align quite well. For our prediction, we take the average of these two dates: October 24th 2025. This will be our target date for the bull cycle top.

Now, let's do the same for the upcoming cycle bottom. The bottom-to-bottom cycle interval is predicted to be 205 weeks, which translates to October 19th, 2026, and the top-to-bottom cycle interval is predicted to be 259 weeks, which corresponds to October 26th, 2026. We then take the average of these two dates, predicting a bear cycle bottom date target of October 19th, 2026.

Now that we have our predicted top and bottom cycle date targets, we can simply reference these two dates to our model, giving us the Bitcoin top price prediction in the range of 152,000 in Q4 2025 and a subsequent bottom price prediction in the range of 46,500 in Q4 2026.

For those interested in understanding what this specifically means for the predicted diminishing return top and bottom cycle values, the image below displays these predicted values. The new values are highlighted in yellow:

And of course, keep in mind that these targets are just rough estimates. While we've done our best to estimate these targets through a data-driven approach, markets will always remain unpredictable in nature. What are your targets? Feel free to share them in the comment section below.

"top" için komut dosyalarını ara

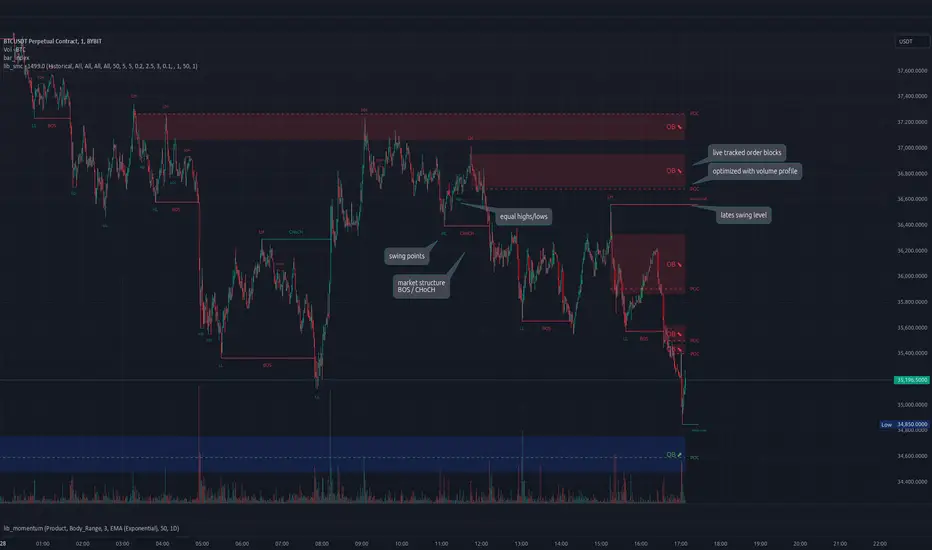

lib_smcLibrary "lib_smc"

This is an adaptation of LuxAlgo's Smart Money Concepts indicator with numerous changes. Main changes include integration of object based plotting, plenty of performance improvements, live tracking of Order Blocks, integration of volume profiles to refine Order Blocks, and many more.

This is a library for developers, if you want this converted into a working strategy, let me know.

buffer(item, len, force_rotate)

Parameters:

item (float)

len (int)

force_rotate (bool)

buffer(item, len, force_rotate)

Parameters:

item (int)

len (int)

force_rotate (bool)

buffer(item, len, force_rotate)

Parameters:

item (Profile type from robbatt/lib_profile/32)

len (int)

force_rotate (bool)

swings(len)

INTERNAL: detect swing points (HH and LL) in given range

Parameters:

len (simple int) : range to check for new swing points

Returns: values are the price level where and if a new HH or LL was detected, else na

method init(this)

Namespace types: OrderBlockConfig

Parameters:

this (OrderBlockConfig)

method delete(this)

Namespace types: OrderBlock

Parameters:

this (OrderBlock)

method clear_broken(this, broken_buffer)

INTERNAL: delete internal order blocks box coordinates if top/bottom is broken

Namespace types: map

Parameters:

this (map)

broken_buffer (map)

Returns: any_bull_ob_broken, any_bear_ob_broken, broken signals are true if an according order block was broken/mitigated, broken contains the broken block(s)

create_ob(id, mode, start_t, start_i, top, end_t, end_i, bottom, break_price, early_confirmation_price, config, init_plot, force_overlay)

INTERNAL: set internal order block coordinates

Parameters:

id (int)

mode (int) : 1: bullish, -1 bearish block

start_t (int)

start_i (int)

top (float)

end_t (int)

end_i (int)

bottom (float)

break_price (float)

early_confirmation_price (float)

config (OrderBlockConfig)

init_plot (bool)

force_overlay (bool)

Returns: signals are true if an according order block was broken/mitigated

method align_to_profile(block, align_edge, align_break_price)

Namespace types: OrderBlock

Parameters:

block (OrderBlock)

align_edge (bool)

align_break_price (bool)

method create_profile(block, opens, tops, bottoms, closes, values, resolution, vah_pc, val_pc, args, init_calculated, init_plot, force_overlay)

Namespace types: OrderBlock

Parameters:

block (OrderBlock)

opens (array)

tops (array)

bottoms (array)

closes (array)

values (array)

resolution (int)

vah_pc (float)

val_pc (float)

args (ProfileArgs type from robbatt/lib_profile/32)

init_calculated (bool)

init_plot (bool)

force_overlay (bool)

method create_profile(block, resolution, vah_pc, val_pc, args, init_calculated, init_plot, force_overlay)

Namespace types: OrderBlock

Parameters:

block (OrderBlock)

resolution (int)

vah_pc (float)

val_pc (float)

args (ProfileArgs type from robbatt/lib_profile/32)

init_calculated (bool)

init_plot (bool)

force_overlay (bool)

track_obs(swing_len, hh, ll, top, btm, bull_bos_alert, bull_choch_alert, bear_bos_alert, bear_choch_alert, min_block_size, max_block_size, config_bull, config_bear, init_plot, force_overlay, enabled, extend_blocks, clear_broken_buffer_before, align_edge_to_value_area, align_break_price_to_poc, profile_args_bull, profile_args_bear, use_soft_confirm, soft_confirm_offset, use_retracements_with_FVG_out)

Parameters:

swing_len (int)

hh (float)

ll (float)

top (float)

btm (float)

bull_bos_alert (bool)

bull_choch_alert (bool)

bear_bos_alert (bool)

bear_choch_alert (bool)

min_block_size (float)

max_block_size (float)

config_bull (OrderBlockConfig)

config_bear (OrderBlockConfig)

init_plot (bool)

force_overlay (bool)

enabled (bool)

extend_blocks (simple bool)

clear_broken_buffer_before (simple bool)

align_edge_to_value_area (simple bool)

align_break_price_to_poc (simple bool)

profile_args_bull (ProfileArgs type from robbatt/lib_profile/32)

profile_args_bear (ProfileArgs type from robbatt/lib_profile/32)

use_soft_confirm (simple bool)

soft_confirm_offset (float)

use_retracements_with_FVG_out (simple bool)

method draw(this, config, extend_only)

Namespace types: OrderBlock

Parameters:

this (OrderBlock)

config (OrderBlockConfig)

extend_only (bool)

method draw(blocks, config)

INTERNAL: plot order blocks

Namespace types: array

Parameters:

blocks (array)

config (OrderBlockConfig)

method draw(blocks, config)

INTERNAL: plot order blocks

Namespace types: map

Parameters:

blocks (map)

config (OrderBlockConfig)

method cleanup(this, ob_bull, ob_bear)

removes all Profiles that are older than the latest OrderBlock from this profile buffer

Namespace types: array

Parameters:

this (array type from robbatt/lib_profile/32)

ob_bull (OrderBlock)

ob_bear (OrderBlock)

_plot_swing_points(mode, x, y, show_swing_points, linecolor_swings, keep_history, show_latest_swings_levels, trail_x, trail_y, trend)

INTERNAL: plot swing points

Parameters:

mode (int) : 1: bullish, -1 bearish block

x (int) : x-coordingate of swing point to plot (bar_index)

y (float) : y-coordingate of swing point to plot (price)

show_swing_points (bool) : switch to enable/disable plotting of swing point labels

linecolor_swings (color) : color for swing point labels and lates level lines

keep_history (bool) : weater to remove older swing point labels and only keep the most recent

show_latest_swings_levels (bool)

trail_x (int) : x-coordinate for latest swing point (bar_index)

trail_y (float) : y-coordinate for latest swing point (price)

trend (int) : the current trend 1: bullish, -1: bearish, to determine Strong/Weak Low/Highs

_pivot_lvl(mode, trend, hhll_x, hhll, super_hhll, filter_insignificant_internal_breaks)

INTERNAL: detect whether a structural level has been broken and if it was in trend direction (BoS) or against trend direction (ChoCh), also track the latest high and low swing points

Parameters:

mode (simple int) : detect 1: bullish, -1 bearish pivot points

trend (int) : current trend direction

hhll_x (int) : x-coordinate of newly detected hh/ll (bar_index)

hhll (float) : y-coordinate of newly detected hh/ll (price)

super_hhll (float) : level/y-coordinate of superior hhll (if this is an internal structure pivot level)

filter_insignificant_internal_breaks (bool) : if true pivot points / internal structure will be ignored where the wick in trend direction is longer than the opposite (likely to push further in direction of main trend)

Returns: coordinates of internal structure that has been broken (x,y): start of structure, (trail_x, trail_y): tracking hh/ll after structure break, (bos_alert, choch_alert): signal whether a structural level has been broken

_plot_structure(x, y, is_bos, is_choch, line_color, line_style, label_style, label_size, keep_history)

INTERNAL: plot structural breaks (BoS/ChoCh)

Parameters:

x (int) : x-coordinate of newly broken structure (bar_index)

y (float) : y-coordinate of newly broken structure (price)

is_bos (bool) : whether this structural break was in trend direction

is_choch (bool) : whether this structural break was against trend direction

line_color (color) : color for the line connecting the structural level and the breaking candle

line_style (string) : style (line.style_dashed/solid) for the line connecting the structural level and the breaking candle

label_style (string) : style (label.style_label_down/up) for the label above/below the line connecting the structural level and the breaking candle

label_size (string) : size (size.small/tiny) for the label above/below the line connecting the structural level and the breaking candle

keep_history (bool) : weater to remove older swing point labels and only keep the most recent

structure_values(length, super_hh, super_ll, filter_insignificant_internal_breaks)

detect (and plot) structural breaks and the resulting new trend

Parameters:

length (simple int) : lookback period for swing point detection

super_hh (float) : level/y-coordinate of superior hh (for internal structure detection)

super_ll (float) : level/y-coordinate of superior ll (for internal structure detection)

filter_insignificant_internal_breaks (bool) : if true pivot points / internal structure will be ignored where the wick in trend direction is longer than the opposite (likely to push further in direction of main trend)

Returns: trend: direction 1:bullish -1:bearish, (bull_bos_alert, bull_choch_alert, top_x, top_y, trail_up_x, trail_up): whether and which level broke in a bullish direction, trailing high, (bbear_bos_alert, bear_choch_alert, tm_x, btm_y, trail_dn_x, trail_dn): same in bearish direction

structure_plot(trend, bull_bos_alert, bull_choch_alert, top_x, top_y, trail_up_x, trail_up, hh, bear_bos_alert, bear_choch_alert, btm_x, btm_y, trail_dn_x, trail_dn, ll, color_bull, color_bear, show_swing_points, show_latest_swings_levels, show_bos, show_choch, line_style, label_size, keep_history)

detect (and plot) structural breaks and the resulting new trend

Parameters:

trend (int) : crrent trend 1: bullish, -1: bearish

bull_bos_alert (bool) : if there was a bullish bos alert -> plot it

bull_choch_alert (bool) : if there was a bullish choch alert -> plot it

top_x (int) : latest shwing high x

top_y (float) : latest swing high y

trail_up_x (int) : trailing high x

trail_up (float) : trailing high y

hh (float) : if there was a higher high

bear_bos_alert (bool) : if there was a bearish bos alert -> plot it

bear_choch_alert (bool) : if there was a bearish chock alert -> plot it

btm_x (int) : latest swing low x

btm_y (float) : latest swing low y

trail_dn_x (int) : trailing low x

trail_dn (float) : trailing low y

ll (float) : if there was a lower low

color_bull (color) : color for bullish BoS/ChoCh levels

color_bear (color) : color for bearish BoS/ChoCh levels

show_swing_points (bool) : whether to plot swing point labels

show_latest_swings_levels (bool) : whether to track and plot latest swing point levels with lines

show_bos (bool) : whether to plot BoS levels

show_choch (bool) : whether to plot ChoCh levels

line_style (string) : whether to plot BoS levels

label_size (string) : label size of plotted BoS/ChoCh levels

keep_history (bool) : weater to remove older swing point labels and only keep the most recent

structure(length, color_bull, color_bear, super_hh, super_ll, filter_insignificant_internal_breaks, show_swing_points, show_latest_swings_levels, show_bos, show_choch, line_style, label_size, keep_history, enabled)

detect (and plot) structural breaks and the resulting new trend

Parameters:

length (simple int) : lookback period for swing point detection

color_bull (color) : color for bullish BoS/ChoCh levels

color_bear (color) : color for bearish BoS/ChoCh levels

super_hh (float) : level/y-coordinate of superior hh (for internal structure detection)

super_ll (float) : level/y-coordinate of superior ll (for internal structure detection)

filter_insignificant_internal_breaks (bool) : if true pivot points / internal structure will be ignored where the wick in trend direction is longer than the opposite (likely to push further in direction of main trend)

show_swing_points (bool) : whether to plot swing point labels

show_latest_swings_levels (bool) : whether to track and plot latest swing point levels with lines

show_bos (bool) : whether to plot BoS levels

show_choch (bool) : whether to plot ChoCh levels

line_style (string) : whether to plot BoS levels

label_size (string) : label size of plotted BoS/ChoCh levels

keep_history (bool) : weater to remove older swing point labels and only keep the most recent

enabled (bool)

_check_equal_level(mode, len, eq_threshold, enabled)

INTERNAL: detect equal levels (double top/bottom)

Parameters:

mode (int) : detect 1: bullish/high, -1 bearish/low pivot points

len (int) : lookback period for equal level (swing point) detection

eq_threshold (float) : maximum price offset for a level to be considered equal

enabled (bool)

Returns: eq_alert whether an equal level was detected and coordinates of the first and the second level/swing point

_plot_equal_level(show_eq, x1, y1, x2, y2, label_txt, label_style, label_size, line_color, line_style, keep_history)

INTERNAL: plot equal levels (double top/bottom)

Parameters:

show_eq (bool) : whether to plot the level or not

x1 (int) : x-coordinate of the first level / swing point

y1 (float) : y-coordinate of the first level / swing point

x2 (int) : x-coordinate of the second level / swing point

y2 (float) : y-coordinate of the second level / swing point

label_txt (string) : text for the label above/below the line connecting the equal levels

label_style (string) : style (label.style_label_down/up) for the label above/below the line connecting the equal levels

label_size (string) : size (size.tiny) for the label above/below the line connecting the equal levels

line_color (color) : color for the line connecting the equal levels (and it's label)

line_style (string) : style (line.style_dotted) for the line connecting the equal levels

keep_history (bool) : weater to remove older swing point labels and only keep the most recent

equal_levels_values(len, threshold, enabled)

detect (and plot) equal levels (double top/bottom), returns coordinates

Parameters:

len (int) : lookback period for equal level (swing point) detection

threshold (float) : maximum price offset for a level to be considered equal

enabled (bool) : whether detection is enabled

Returns: (eqh_alert, eqh_x1, eqh_y1, eqh_x2, eqh_y2) whether an equal high was detected and coordinates of the first and the second level/swing point, (eql_alert, eql_x1, eql_y1, eql_x2, eql_y2) same for equal lows

equal_levels_plot(eqh_x1, eqh_y1, eqh_x2, eqh_y2, eql_x1, eql_y1, eql_x2, eql_y2, color_eqh, color_eql, show, keep_history)

detect (and plot) equal levels (double top/bottom), returns coordinates

Parameters:

eqh_x1 (int) : coordinates of first point of equal high

eqh_y1 (float) : coordinates of first point of equal high

eqh_x2 (int) : coordinates of second point of equal high

eqh_y2 (float) : coordinates of second point of equal high

eql_x1 (int) : coordinates of first point of equal low

eql_y1 (float) : coordinates of first point of equal low

eql_x2 (int) : coordinates of second point of equal low

eql_y2 (float) : coordinates of second point of equal low

color_eqh (color) : color for the line connecting the equal highs (and it's label)

color_eql (color) : color for the line connecting the equal lows (and it's label)

show (bool) : whether plotting is enabled

keep_history (bool) : weater to remove older swing point labels and only keep the most recent

Returns: (eqh_alert, eqh_x1, eqh_y1, eqh_x2, eqh_y2) whether an equal high was detected and coordinates of the first and the second level/swing point, (eql_alert, eql_x1, eql_y1, eql_x2, eql_y2) same for equal lows

equal_levels(len, threshold, color_eqh, color_eql, enabled, show, keep_history)

detect (and plot) equal levels (double top/bottom)

Parameters:

len (int) : lookback period for equal level (swing point) detection

threshold (float) : maximum price offset for a level to be considered equal

color_eqh (color) : color for the line connecting the equal highs (and it's label)

color_eql (color) : color for the line connecting the equal lows (and it's label)

enabled (bool) : whether detection is enabled

show (bool) : whether plotting is enabled

keep_history (bool) : weater to remove older swing point labels and only keep the most recent

Returns: (eqh_alert) whether an equal high was detected, (eql_alert) same for equal lows

_detect_fvg(mode, enabled, o, h, l, c, filter_insignificant_fvgs, change_tf)

INTERNAL: detect FVG (fair value gap)

Parameters:

mode (int) : detect 1: bullish, -1 bearish gaps

enabled (bool) : whether detection is enabled

o (float) : reference source open

h (float) : reference source high

l (float) : reference source low

c (float) : reference source close

filter_insignificant_fvgs (bool) : whether to calculate and filter small/insignificant gaps

change_tf (bool) : signal when the previous reference timeframe closed, triggers new calculation

Returns: whether a new FVG was detected and its top/mid/bottom levels

_clear_broken_fvg(mode, upper_boxes, lower_boxes)

INTERNAL: clear mitigated FVGs (fair value gaps)

Parameters:

mode (int) : detect 1: bullish, -1 bearish gaps

upper_boxes (array) : array that stores the upper parts of the FVG boxes

lower_boxes (array) : array that stores the lower parts of the FVG boxes

_plot_fvg(mode, show, top, mid, btm, border_color, extend_box)

INTERNAL: plot (and clear broken) FVG (fair value gap)

Parameters:

mode (int) : plot 1: bullish, -1 bearish gap

show (bool) : whether plotting is enabled

top (float) : top level of fvg

mid (float) : center level of fvg

btm (float) : bottom level of fvg

border_color (color) : color for the FVG box

extend_box (int) : how many bars into the future the FVG box should be extended after detection

fvgs_values(o, h, l, c, filter_insignificant_fvgs, change_tf, enabled)

detect (and plot / clear broken) FVGs (fair value gaps), and return alerts and level values

Parameters:

o (float) : reference source open

h (float) : reference source high

l (float) : reference source low

c (float) : reference source close

filter_insignificant_fvgs (bool) : whether to calculate and filter small/insignificant gaps

change_tf (bool) : signal when the previous reference timeframe closed, triggers new calculation

enabled (bool) : whether detection is enabled

Returns: (bullish_fvg_alert, bull_top, bull_mid, bull_btm): whether a new bullish FVG was detected and its top/mid/bottom levels, (bearish_fvg_alert, bear_top, bear_mid, bear_btm): same for bearish FVGs

fvgs_plot(bullish_fvg_alert, bull_top, bull_mid, bull_btm, bearish_fvg_alert, bear_top, bear_mid, bear_btm, color_bull, color_bear, extend_box, show)

Parameters:

bullish_fvg_alert (bool)

bull_top (float)

bull_mid (float)

bull_btm (float)

bearish_fvg_alert (bool)

bear_top (float)

bear_mid (float)

bear_btm (float)

color_bull (color) : color for bullish FVG boxes

color_bear (color) : color for bearish FVG boxes

extend_box (int) : how many bars into the future the FVG box should be extended after detection

show (bool) : whether plotting is enabled

Returns: (bullish_fvg_alert, bull_top, bull_mid, bull_btm): whether a new bullish FVG was detected and its top/mid/bottom levels, (bearish_fvg_alert, bear_top, bear_mid, bear_btm): same for bearish FVGs

fvgs(o, h, l, c, filter_insignificant_fvgs, change_tf, color_bull, color_bear, extend_box, enabled, show)

detect (and plot / clear broken) FVGs (fair value gaps)

Parameters:

o (float) : reference source open

h (float) : reference source high

l (float) : reference source low

c (float) : reference source close

filter_insignificant_fvgs (bool) : whether to calculate and filter small/insignificant gaps

change_tf (bool) : signal when the previous reference timeframe closed, triggers new calculation

color_bull (color) : color for bullish FVG boxes

color_bear (color) : color for bearish FVG boxes

extend_box (int) : how many bars into the future the FVG box should be extended after detection

enabled (bool) : whether detection is enabled

show (bool) : whether plotting is enabled

Returns: (bullish_fvg_alert): whether a new bullish FVG was detected, (bearish_fvg_alert): same for bearish FVGs

OrderBlock

Fields:

id (series int)

dir (series int)

left_top (chart.point)

right_bottom (chart.point)

break_price (series float)

early_confirmation_price (series float)

ltf_high (array)

ltf_low (array)

ltf_volume (array)

plot (Box type from robbatt/lib_plot_objects/49)

profile (Profile type from robbatt/lib_profile/32)

trailing (series bool)

extending (series bool)

awaiting_confirmation (series bool)

touched_break_price_before_confirmation (series bool)

soft_confirmed (series bool)

has_fvg_out (series bool)

hidden (series bool)

broken (series bool)

OrderBlockConfig

Fields:

show (series bool)

show_last (series int)

show_id (series bool)

show_profile (series bool)

args (BoxArgs type from robbatt/lib_plot_objects/49)

txt (series string)

txt_args (BoxTextArgs type from robbatt/lib_plot_objects/49)

delete_when_broken (series bool)

broken_args (BoxArgs type from robbatt/lib_plot_objects/49)

broken_txt (series string)

broken_txt_args (BoxTextArgs type from robbatt/lib_plot_objects/49)

broken_profile_args (ProfileArgs type from robbatt/lib_profile/32)

use_profile (series bool)

profile_args (ProfileArgs type from robbatt/lib_profile/32)

lib_profileLibrary "lib_profile"

a library with functions to calculate a volume profile for either a set of candles within the current chart, or a single candle from its lower timeframe security data. All you need is to feed the

method delete(this)

deletes this bucket's plot from the chart

Namespace types: Bucket

Parameters:

this (Bucket)

method delete(this)

Namespace types: Profile

Parameters:

this (Profile)

method delete(this)

Namespace types: Bucket

Parameters:

this (Bucket )

method delete(this)

Namespace types: Profile

Parameters:

this (Profile )

method update(this, top, bottom, value, fraction)

updates this bucket's data

Namespace types: Bucket

Parameters:

this (Bucket)

top (float)

bottom (float)

value (float)

fraction (float)

method update(this, tops, bottoms, values)

update this Profile's data (recalculates the whole profile and applies the result to this object) TODO optimisation to calculate this incremental to improve performance in realtime on high resolution

Namespace types: Profile

Parameters:

this (Profile)

tops (float ) : array of range top/high values (either from ltf or chart candles using history() function

bottoms (float ) : array of range bottom/low values (either from ltf or chart candles using history() function

values (float ) : array of range volume/1 values (either from ltf or chart candles using history() function (1s can be used for analysing candles in bucket/price range over time)

method tostring(this)

allows debug print of a bucket

Namespace types: Bucket

Parameters:

this (Bucket)

method draw(this, start_t, start_i, end_t, end_i, args, line_color)

allows drawing a line in a Profile, representing this bucket and it's value + it's value's fraction of the Profile total value

Namespace types: Bucket

Parameters:

this (Bucket)

start_t (int) : the time x coordinate of the line's left end (depends on the Profile box)

start_i (int) : the bar_index x coordinate of the line's left end (depends on the Profile box)

end_t (int) : the time x coordinate of the line's right end (depends on the Profile box)

end_i (int) : the bar_index x coordinate of the line's right end (depends on the Profile box)

args (LineArgs type from robbatt/lib_plot_objects/24) : the default arguments for the line style

line_color (color) : the color override for POC/VAH/VAL lines

method draw(this, forced_width)

draw all components of this Profile (Box, Background, Bucket lines, POC/VAH/VAL overlay levels and labels)

Namespace types: Profile

Parameters:

this (Profile)

forced_width (int) : allows to force width of the Profile Box, overrides the ProfileArgs.default_size and ProfileArgs.extend arguments (default: na)

method init(this)

Namespace types: ProfileArgs

Parameters:

this (ProfileArgs)

method init(this)

Namespace types: Profile

Parameters:

this (Profile)

profile(tops, bottoms, values, resolution, vah_pc, val_pc, bucket_buffer)

split a chart/parent bar into 'resolution' sections, figure out in which section the most volume/time was spent, by analysing a given set of (intra)bars' top/bottom/volume values. Then return price center of the bin with the highest volume, essentially marking the point of control / highest volume (poc) in the chart/parent bar.

Parameters:

tops (float ) : array of range top/high values (either from ltf or chart candles using history() function

bottoms (float ) : array of range bottom/low values (either from ltf or chart candles using history() function

values (float ) : array of range volume/1 values (either from ltf or chart candles using history() function (1s can be used for analysing candles in bucket/price range over time)

resolution (int) : amount of buckets/price ranges to sort the candle data into (analyse how much volume / time was spent in a certain bucket/price range) (default: 25)

vah_pc (float) : a threshold percentage (of values' total) for the top end of the value area (default: 80)

val_pc (float) : a threshold percentage (of values' total) for the bottom end of the value area (default: 20)

bucket_buffer (Bucket ) : optional buffer of empty Buckets to fill, if omitted a new one is created and returned. The buffer length must match the resolution

Returns: poc (price level), vah (price level), val (price level), poc_index (idx in buckets), vah_index (idx in buckets), val_index (idx in buckets), buckets (filled buffer or new)

create_profile(start_idx, tops, bottoms, values, resolution, vah_pc, val_pc, args)

split a chart/parent bar into 'resolution' sections, figure out in which section the most volume/time was spent, by analysing a given set of (intra)bars' top/bottom/volume values. Then return price center of the bin with the highest volume, essentially marking the point of control / highest volume (poc) in the chart/parent bar.

Parameters:

start_idx (int) : the bar_index at which the Profile should start drawing

tops (float ) : array of range top/high values (either from ltf or chart candles using history() function

bottoms (float ) : array of range bottom/low values (either from ltf or chart candles using history() function

values (float ) : array of range volume/1 values (either from ltf or chart candles using history() function (1s can be used for analysing candles in bucket/price range over time)

resolution (int) : amount of buckets/price ranges to sort the candle data into (analyse how much volume / time was spent in a certain bucket/price range) (default: 25)

vah_pc (float) : a threshold percentage (of values' total) for the top end of the value area (default: 80)

val_pc (float) : a threshold percentage (of values' total) for the bottom end of the value area (default: 20)

args (ProfileArgs)

Returns: poc (price level), vah (price level), val (price level), poc_index (idx in buckets), vah_index (idx in buckets), val_index (idx in buckets), buckets (filled buffer or new)

history(src, len, offset)

allows fetching an array of values from the history series with offset from current candle

Parameters:

src (int)

len (int)

offset (int)

history(src, len, offset)

allows fetching an array of values from the history series with offset from current candle

Parameters:

src (float)

len (int)

offset (int)

history(src, len, offset)

allows fetching an array of values from the history series with offset from current candle

Parameters:

src (bool)

len (int)

offset (int)

history(src, len, offset)

allows fetching an array of values from the history series with offset from current candle

Parameters:

src (string)

len (int)

offset (int)

Bucket

Fields:

idx (series int) : the index of this Bucket within the Profile starting with 0 for the lowest Bucket at the bottom of the Profile

value (series float) : the value of this Bucket, can be volume or time, for using time pass and array of 1s to the update function

top (series float) : the top of this Bucket's price range (for calculation)

btm (series float) : the bottom of this Bucket's price range (for calculation)

center (series float) : the center of this Bucket's price range (for plotting)

fraction (series float) : the fraction this Bucket's value is compared to the total of the Profile

plot_bucket_line (Line type from robbatt/lib_plot_objects/24) : the line that resembles this bucket and it's valeu in the Profile

ProfileArgs

Fields:

show_poc (series bool) : whether to plot a POC line across the Profile Box (default: true)

show_profile (series bool) : whether to plot a line for each Bucket in the Profile Box, indicating the value per Bucket (Price range), e.g. volume that occured in a certain time and price range (default: false)

show_va (series bool) : whether to plot a VAH/VAL line across the Profile Box (default: false)

show_va_fill (series bool) : whether to fill the 'value' area between VAH/VAL line (default: false)

show_background (series bool) : whether to fill the Profile Box with a background color (default: false)

show_labels (series bool) : whether to add labels to the right end of the POC/VAH/VAL line (default: false)

show_price_levels (series bool) : whether add price values to the labels to the right end of the POC/VAH/VAL line (default: false)

extend (series bool) : whether extend the Profile Box to the current candle (default: false)

default_size (series int) : the default min. width of the Profile Box (default: 30)

args_poc_line (LineArgs type from robbatt/lib_plot_objects/24) : arguments for the poc line plot

args_va_line (LineArgs type from robbatt/lib_plot_objects/24) : arguments for the va line plot

args_poc_label (LabelArgs type from robbatt/lib_plot_objects/24) : arguments for the poc label plot

args_va_label (LabelArgs type from robbatt/lib_plot_objects/24) : arguments for the va label plot

args_profile_line (LineArgs type from robbatt/lib_plot_objects/24) : arguments for the Bucket line plots

args_profile_bg (BoxArgs type from robbatt/lib_plot_objects/24)

va_fill_color (series color) : color for the va area fill plot

Profile

Fields:

start (series int) : left x coordinate for the Profile Box

end (series int) : right x coordinate for the Profile Box

resolution (series int) : the amount of buckets/price ranges the Profile will dissect the data into

vah_threshold_pc (series float) : the percentage of the total data value to mark the upper threshold for the main value area

val_threshold_pc (series float) : the percentage of the total data value to mark the lower threshold for the main value area

args (ProfileArgs) : the style arguments for the Profile Box

h (series float) : the highest price of the data

l (series float) : the lowest price of the data

total (series float) : the total data value (e.g. volume of all candles, or just one each to analyse candle distribution over time)

buckets (Bucket ) : the Bucket objects holding the data for each price range bucket

poc_bucket_index (series int) : the Bucket index in buckets, that holds the poc Bucket

vah_bucket_index (series int) : the Bucket index in buckets, that holds the vah Bucket

val_bucket_index (series int) : the Bucket index in buckets, that holds the val Bucket

poc (series float) : the according price level marking the Point Of Control

vah (series float) : the according price level marking the Value Area High

val (series float) : the according price level marking the Value Area Low

plot_poc (Line type from robbatt/lib_plot_objects/24)

plot_vah (Line type from robbatt/lib_plot_objects/24)

plot_val (Line type from robbatt/lib_plot_objects/24)

plot_poc_label (Label type from robbatt/lib_plot_objects/24)

plot_vah_label (Label type from robbatt/lib_plot_objects/24)

plot_val_label (Label type from robbatt/lib_plot_objects/24)

plot_va_fill (LineFill type from robbatt/lib_plot_objects/24)

plot_profile_bg (Box type from robbatt/lib_plot_objects/24)

Entanglement Penscript name: Entanglement Pen

For left traders, how to accurately find the bottom and top is very important, and there are various methods. I have shared the bottom type script composed of three bars before, but this type of bottom type is effective in a small range. So, this script is sharing " Entanglement Pen ", which can help us determine bottoms and tops on a global scale.

However, this script uses an approximate reduction method rather than the orthodox solution of entanglement.

After roughly finding the bottom and top, how to determine that these are the bottom and top that meet the definition of entanglement theory?

The main 2 methods of "approximate reduction" are:

(1) The price difference between the top and the bottom is large enough, that is: the lowest price at the top > the highest price at the bottom.

(2) The stock price before the top has continued to rise, that is: both the highest point and the lowest point are rising. In the same way, the stock price before the bottom has a continuous decline, that is: both the high and the low point are falling.

A big disadvantage of this script is that it needs to use future data. This is because:

When multiple bars meet the top definition in a short period of time, only the last bar is used, which is defined as a big top. So, when you see a top appear, you don't know it's not a real top, because it might be followed by a bar that also matches the definition of the top.

When displayed on the graph, bars that meet the top definition have a gray label, which is the small top. Each small top is a big top (with a blue label) at the beginning, and when another small top appears after it, it becomes a gray small top.

Regarding the limit on the number of bars by TradingView:

The logic of calculating the small top and the small bottom is relatively simple, it does not need to use future data, and the amount of calculation is small, so it is the default TradingView limit. (The limit is 2000 in the script, but in practice TradingView won't let us use such many bars)

The calculation logic of the big top and the big bottom is more complicated, and it needs to use future data. The calculation amount is very large, and only the most recent 150 bars can be calculated. The user can try to enter a larger value, but TradingView may report an error. If an error occurs, please enter a lower value. When loading for the first time, it takes a long time, which is indeed not common in general TradingView scripts, but please be patient.

The next version may add the alert function, that is: when the top and bottom appear, the alert function is called. But this only applies to small tops and bottoms, because when the alert is sent,, none of us know what data will be in the future.

Introduction in Chinese:

脚本名称:缠论笔

对于左侧交易者来说,如何准确地找到底部和顶部是非常重要的,方法也是多样的,之前已经分享了三根bar组成的底分型脚本,但这种底分型生效的范围较小,缺乏全局视野。所以,这次的脚本分享的是“缠论笔”,它能帮我们在全局尺度内确定底部和顶部。

不过,此脚本使用的是近似还原的方法,而非缠论的正统解法。

粗略找到底和顶之后,如何确定这就是符合缠论定义的底和顶呢?

“近似还原”的主要2个方法是:

(1)顶部与底部的价差足够大,即:顶部的最低价>底部的最高价。

(2)顶部之前的股价有持续的上涨,即:最高点和最低点都在上涨。同理,底部之前的股价有持续的下跌,即:最高点和最低点都在下跌。

这个脚本的一大缺点是:需要使用将来的数据。这是因为:

当短期内有多个bar都符合顶部定义时,只使用最后一个bar,定义为大顶。所以,当你看到一个顶部出现时,你不知道这不是真的顶部,因为它之后可能还会出现符合顶部定义的bar。

在图上显示时,符合顶部定义的bar有灰色的label,这是小顶。每一个小顶,刚开始时都是大顶(有蓝色的label),直到它之后又有小顶出现时,它就变成了灰色的小顶。

关于TradingView对bar数的限制:

计算小顶和小底的逻辑比较简单,不需要使用将来的数据,计算量较小,所以是默认的TradingView限制。(脚本中限制为2000,但实际上TradingView不会让我们使用那么多bar)

大顶和大底的计算逻辑比较复杂,需要使用将来的数据,计算量非常大,大约只能计算最近150根bar。用户可以尝试输入更大的数值,但TradingView可能会报错。若遇报错,则请输入更低的数值。初次加载时,需要等待较长时间,这确实在一般的TradingView脚本中并不常见,但还是请多些耐心。

下一版可能会增加alert功能,即:当顶部和底部出现时,调用alert函数。但这只适用于小顶和小底,因为警报发出时,我们谁也不知道将来的数据。

BjCandlePatternsLibrary "BjCandlePatterns"

Patterns is a Japanese candlestick pattern recognition Library for developers. Functions here within detect viable setups in a variety of popular patterns. Please note some patterns are without filters such as comparisons to average candle sizing, or trend detection to allow the author more freedom.

doji(dojiSize, dojiWickSize) Detects "Doji" candle patterns

Parameters:

dojiSize : (float) The relationship of body to candle size (ie. body is 5% of total candle size). Default is 5.0 (5%)

dojiWickSize : (float) Maximum wick size comparative to the opposite wick. (eg. 2 = bottom wick must be less than or equal to 2x the top wick). Default is 2

Returns: (series bool) True when pattern detected

dLab(showLabel, labelColor, textColor) Produces "Doji" identifier label

Parameters:

showLabel : (bool) Shows label when input is true. Default is false

labelColor : (series color) Color of the label border and arrow

textColor : (series color) Text color

Returns: (series label) A label visible at the chart level intended for the title pattern

bullEngulf(maxRejectWick, mustEngulfWick) Detects "Bullish Engulfing" candle patterns

Parameters:

maxRejectWick : (float) Maximum rejection wick size.

The maximum wick size as a percentge of body size allowable for a top wick on the resolution candle of the pattern. 0.0 disables the filter.

eg. 50 allows a top wick half the size of the body. Default is 0% (Disables wick detection).

mustEngulfWick : (bool) input to only detect setups that close above the high prior effectively engulfing the candle in its entirety. Default is false

Returns: (series bool) True when pattern detected

bewLab(showLabel, labelColor, textColor) Produces "Bullish Engulfing" identifier label

Parameters:

showLabel : (bool) Shows label when input is true. Default is false

labelColor : (series color) Color of the label border and arrow

textColor : (series color) Text color

Returns: (series label) A label visible at the chart level intended for the title pattern

bearEngulf(maxRejectWick, mustEngulfWick) Detects "Bearish Engulfing" candle patterns

Parameters:

maxRejectWick : (float) Maximum rejection wick size.

The maximum wick size as a percentge of body size allowable for a bottom wick on the resolution candle of the pattern. 0.0 disables the filter.

eg. 50 allows a botom wick half the size of the body. Default is 0% (Disables wick detection).

mustEngulfWick : (bool) Input to only detect setups that close below the low prior effectively engulfing the candle in its entirety. Default is false

Returns: (series bool) True when pattern detected

bebLab(showLabel, labelColor, textColor) Produces "Bearish Engulfing" identifier label

Parameters:

showLabel : (bool) Shows label when input is true. Default is false

labelColor : (series color) Color of the label border and arrow

textColor : (series color) Text color

Returns: (series label) A label visible at the chart level intended for the title pattern

hammer(ratio, shadowPercent) Detects "Hammer" candle patterns

Parameters:

ratio : (float) The relationship of body to candle size (ie. body is 33% of total candle size). Default is 33%.

shadowPercent : (float) The maximum allowable top wick size as a percentage of body size. Default is 5%.

Returns: (series bool) True when pattern detected

hLab(showLabel, labelColor, textColor) Produces "Hammer" identifier label

Parameters:

showLabel : (bool) Shows label when input is true. Default is false

labelColor : (series color) Color of the label border and arrow

textColor : (series color) Text color

Returns: (series label) A label visible at the chart level intended for the title pattern

star(ratio, shadowPercent) Detects "Star" candle patterns

Parameters:

ratio : (float) The relationship of body to candle size (ie. body is 33% of total candle size). Default is 33%.

shadowPercent : (float) The maximum allowable bottom wick size as a percentage of body size. Default is 5%.

Returns: (series bool) True when pattern detected

ssLab(showLabel, labelColor, textColor) Produces "Star" identifier label

Parameters:

showLabel : (bool) Shows label when input is true. Default is false

labelColor : (series color) Color of the label border and arrow

textColor : (series color) Text color

Returns: (series label) A label visible at the chart level intended for the title pattern

dragonflyDoji() Detects "Dragonfly Doji" candle patterns

Returns: (series bool) True when pattern detected

ddLab(showLabel, labelColor) Produces "Dragonfly Doji" identifier label

Parameters:

showLabel : (bool) Shows label when input is true. Default is false

labelColor : (series color) Color of the label border and arrow

Returns: (series label) A label visible at the chart level intended for the title pattern

gravestoneDoji() Detects "Gravestone Doji" candle patterns

Returns: (series bool) True when pattern detected

gdLab(showLabel, labelColor, textColor) Produces "Gravestone Doji" identifier label

Parameters:

showLabel : (bool) Shows label when input is true. Default is false

labelColor : (series color) Color of the label border and arrow

textColor : (series color) Text color

Returns: (series label) A label visible at the chart level intended for the title pattern

tweezerBottom(closeUpperHalf) Detects "Tweezer Bottom" candle patterns

Parameters:

closeUpperHalf : (bool) input to only detect setups that close above the mid-point of the candle prior increasing its bullish tendancy. Default is false

Returns: (series bool) True when pattern detected

tbLab(showLabel, labelColor, textColor) Produces "Tweezer Bottom" identifier label

Parameters:

showLabel : (bool) Shows label when input is true. Default is false

labelColor : (series color) Color of the label border and arrow

textColor : (series color) Text color

Returns: (series label) A label visible at the chart level intended for the title pattern

tweezerTop(closeLowerHalf) Detects "TweezerTop" candle patterns

Parameters:

closeLowerHalf : (bool) input to only detect setups that close below the mid-point of the candle prior increasing its bearish tendancy. Default is false

Returns: (series bool) True when pattern detected

ttLab(showLabel, labelColor, textColor) Produces "TweezerTop" identifier label

Parameters:

showLabel : (bool) Shows label when input is true. Default is false

labelColor : (series color) Color of the label border and arrow

textColor : (series color) Text color

Returns: (series label) A label visible at the chart level intended for the title pattern

spinningTopBull(wickSize) Detects "Bullish Spinning Top" candle patterns

Parameters:

wickSize : (float) input to adjust detection of the size of the top wick/ bottom wick as a percent of total candle size. Default is 34%, which ensures the wicks are both larger than the body.

Returns: (series bool) True when pattern detected

stwLab(showLabel, labelColor, textColor) Produces "Bullish Spinning Top" identifier label

Parameters:

showLabel : (bool) Shows label when input is true. Default is false

labelColor : (series color) Color of the label border and arrow

textColor : (series color) Text color

Returns: (series label) A label visible at the chart level intended for the title pattern

spinningTopBear(wickSize) Detects "Bearish Spinning Top" candle patterns

Parameters:

wickSize : (float) input to adjust detection of the size of the top wick/ bottom wick as a percent of total candle size. Default is 34%, which ensures the wicks are both larger than the body.

Returns: (series bool) True when pattern detected

stbLab(showLabel, labelColor, textColor) Produces "Bearish Spinning Top" identifier label

Parameters:

showLabel : (bool) Shows label when input is true. Default is false

labelColor : (series color) Color of the label border and arrow

textColor : (series color) Text color

Returns: (series label) A label visible at the chart level intended for the title pattern

spinningTop(wickSize) Detects "Spinning Top" candle patterns

Parameters:

wickSize : (float) input to adjust detection of the size of the top wick/ bottom wick as a percent of total candle size. Default is 34%, which ensures the wicks are both larger than the body.

Returns: (series bool) True when pattern detected

stLab(showLabel, labelColor, textColor) Produces "Spinning Top" identifier label

Parameters:

showLabel : (bool) Shows label when input is true. Default is false

labelColor : (series color) Color of the label border and arrow

textColor : (series color) Text color

Returns: (series label) A label visible at the chart level intended for the title pattern

morningStar() Detects "Bullish Morning Star" candle patterns

Returns: (series bool) True when pattern detected

msLab(showLabel, labelColor, textColor) Produces "Bullish Morning Star" identifier label

Parameters:

showLabel : (bool) Shows label when input is true. Default is false

labelColor : (series color) Color of the label border and arrow

textColor : (series color) Text color

Returns: (series label) A label visible at the chart level intended for the title pattern

eveningStar() Detects "Bearish Evening Star" candle patterns

Returns: (series bool) True when pattern detected

esLab(showLabel, labelColor, textColor) Produces "Bearish Evening Star" identifier label

Parameters:

showLabel : (bool) Shows label when input is true. Default is false

labelColor : (series color) Color of the label border and arrow

textColor : (series color) Text color

Returns: (series label) A label visible at the chart level intended for the title pattern

haramiBull() Detects "Bullish Harami" candle patterns

Returns: (series bool) True when pattern detected

hwLab(showLabel, labelColor, textColor) Produces "Bullish Harami" identifier label

Parameters:

showLabel : (bool) Shows label when input is true. Default is false

labelColor : (series color) Color of the label border and arrow

textColor : (series color) Text color

Returns: (series label) A label visible at the chart level intended for the title pattern

haramiBear() Detects "Bearish Harami" candle patterns

Returns: (series bool) True when pattern detected

hbLab(showLabel, labelColor, textColor) Produces "Bearish Harami" identifier label

Parameters:

showLabel : (bool) Shows label when input is true. Default is false

labelColor : (series color) Color of the label border and arrow

textColor : (series color) Text color

Returns: (series label) A label visible at the chart level intended for the title pattern

haramiBullCross() Detects "Bullish Harami Cross" candle patterns

Returns: (series bool) True when pattern detected

hcwLab(showLabel, labelColor, textColor) Produces "Bullish Harami Cross" identifier label

Parameters:

showLabel : (bool) Shows label when input is true. Default is false

labelColor : (series color) Color of the label border and arrow

textColor : (series color) Text color

Returns: (series label) A label visible at the chart level intended for the title pattern

haramiBearCross() Detects "Bearish Harami Cross" candle patterns

Returns: (series bool) True when pattern detected

hcbLab(showLabel, labelColor) Produces "Bearish Harami Cross" identifier label

Parameters:

showLabel : (bool) Shows label when input is true. Default is false

labelColor : (series color) Color of the label border and arrow

Returns: (series label) A label visible at the chart level intended for the title pattern

marubullzu() Detects "Bullish Marubozu" candle patterns

Returns: (series bool) True when pattern detected

mwLab(showLabel, labelColor, textColor) Produces "Bullish Marubozu" identifier label

Parameters:

showLabel : (bool) Shows label when input is true. Default is false

labelColor : (series color) Color of the label border and arrow

textColor : (series color) Text color

Returns: (series label) A label visible at the chart level intended for the title pattern

marubearzu() Detects "Bearish Marubozu" candle patterns

Returns: (series bool) True when pattern detected

mbLab(showLabel, labelColor, textColor) Produces "Bearish Marubozu" identifier label

Parameters:

showLabel : (bool) Shows label when input is true. Default is false

labelColor : (series color) Color of the label border and arrow

textColor : (series color) Text color

Returns: (series label) A label visible at the chart level intended for the title pattern

abandonedBull() Detects "Bullish Abandoned Baby" candle patterns

Returns: (series bool) True when pattern detected

abwLab(showLabel, labelColor, textColor) Produces "Bullish Abandoned Baby" identifier label

Parameters:

showLabel : (bool) Shows label when input is true. Default is false

labelColor : (series color) Color of the label border and arrow

textColor : (series color) Text color

Returns: (series label) A label visible at the chart level intended for the title pattern

abandonedBear() Detects "Bearish Abandoned Baby" candle patterns

Returns: (series bool) True when pattern detected

abbLab(showLabel, labelColor, textColor) Produces "Bearish Abandoned Baby" identifier label

Parameters:

showLabel : (bool) Shows label when input is true. Default is false

labelColor : (series color) Color of the label border and arrow

textColor : (series color) Text color

Returns: (series label) A label visible at the chart level intended for the title pattern

piercing() Detects "Piercing" candle patterns

Returns: (series bool) True when pattern detected

pLab(showLabel, labelColor, textColor) Produces "Piercing" identifier label

Parameters:

showLabel : (bool) Shows label when input is true. Default is false

labelColor : (series color) Color of the label border and arrow

textColor : (series color) Text color

Returns: (series label) A label visible at the chart level intended for the title pattern

darkCloudCover() Detects "Dark Cloud Cover" candle patterns

Returns: (series bool) True when pattern detected

dccLab(showLabel, labelColor, textColor) Produces "Dark Cloud Cover" identifier label

Parameters:

showLabel : (bool) Shows label when input is true. Default is false

labelColor : (series color) Color of the label border and arrow

textColor : (series color) Text color

Returns: (series label) A label visible at the chart level intended for the title pattern

tasukiBull() Detects "Upside Tasuki Gap" candle patterns

Returns: (series bool) True when pattern detected

utgLab(showLabel, labelColor, textColor) Produces "Upside Tasuki Gap" identifier label

Parameters:

showLabel : (bool) Shows label when input is true. Default is false

labelColor : (series color) Color of the label border and arrow

textColor : (series color) Text color

Returns: (series label) A label visible at the chart level intended for the title pattern

tasukiBear() Detects "Downside Tasuki Gap" candle patterns

Returns: (series bool) True when pattern detected

dtgLab(showLabel, labelColor, textColor) Produces "Downside Tasuki Gap" identifier label

Parameters:

showLabel : (bool) Shows label when input is true. Default is false

labelColor : (series color) Color of the label border and arrow

textColor : (series color) Text color

Returns: (series label) A label visible at the chart level intended for the title pattern

risingThree() Detects "Rising Three Methods" candle patterns

Returns: (series bool) True when pattern detected

rtmLab(showLabel, labelColor, textColor) Produces "Rising Three Methods" identifier label

Parameters:

showLabel : (bool) Shows label when input is true. Default is false

labelColor : (series color) Color of the label border and arrow

textColor : (series color) Text color

Returns: (series label) A label visible at the chart level intended for the title pattern

fallingThree() Detects "Falling Three Methods" candle patterns

Returns: (series bool) True when pattern detected

ftmLab(showLabel, labelColor, textColor) Produces "Falling Three Methods" identifier label

Parameters:

showLabel : (bool) Shows label when input is true. Default is false

labelColor : (series color) Color of the label border and arrow

textColor : (series color) Text color

Returns: (series label) A label visible at the chart level intended for the title pattern

risingWindow() Detects "Rising Window" candle patterns

Returns: (series bool) True when pattern detected

rwLab(showLabel, labelColor, textColor) Produces "Rising Window" identifier label

Parameters:

showLabel : (bool) Shows label when input is true. Default is false

labelColor : (series color) Color of the label border and arrow

textColor : (series color) Text color

Returns: (series label) A label visible at the chart level intended for the title pattern

fallingWindow() Detects "Falling Window" candle patterns

Returns: (series bool) True when pattern detected

fwLab(showLabel, labelColor, textColor) Produces "Falling Window" identifier label

Parameters:

showLabel : (bool) Shows label when input is true. Default is false

labelColor : (series color) Color of the label border and arrow

textColor : (series color) Text color

Returns: (series label) A label visible at the chart level intended for the title pattern

kickingBull() Detects "Bullish Kicking" candle patterns

Returns: (series bool) True when pattern detected

kwLab(showLabel, labelColor, textColor) Produces "Bullish Kicking" identifier label

Parameters:

showLabel : (bool) Shows label when input is true. Default is false

labelColor : (series color) Color of the label border and arrow

textColor : (series color) Text color

Returns: (series label) A label visible at the chart level intended for the title pattern

kickingBear() Detects "Bearish Kicking" candle patterns

Returns: (series bool) True when pattern detected

kbLab(showLabel, labelColor, textColor) Produces "Bearish Kicking" identifier label

Parameters:

showLabel : (bool) Shows label when input is true. Default is false

labelColor : (series color) Color of the label border and arrow

textColor : (series color) Text color

Returns: (series label) A label visible at the chart level intended for the title pattern

lls(ratio) Detects "Long Lower Shadow" candle patterns

Parameters:

ratio : (float) A relationship of the lower wick to the overall candle size expressed as a percent. Default is 75%

Returns: (series bool) True when pattern detected

llsLab(showLabel, labelColor, textColor) Produces "Long Lower Shadow" identifier label

Parameters:

showLabel : (bool) Shows label when input is true. Default is false

labelColor : (series color) Color of the label border and arrow

textColor : (series color) Text color

Returns: (series label) A label visible at the chart level intended for the title pattern

lus(ratio) Detects "Long Upper Shadow" candle patterns

Parameters:

ratio : (float) A relationship of the upper wick to the overall candle size expressed as a percent. Default is 75%

Returns: (series bool) True when pattern detected

lusLab(showLabel, labelColor, textColor) Produces "Long Upper Shadow" identifier label

Parameters:

showLabel : (bool) Shows label when input is true. Default is false

labelColor : (series color) Color of the label border and arrow

textColor : (series color) Text color

Returns: (series label) A label visible at the chart level intended for the title pattern

bullNeck() Detects "Bullish On Neck" candle patterns

Returns: (series bool) True when pattern detected

nwLab(showLabel, labelColor, textColor) Produces "Bullish On Neck" identifier label

Parameters:

showLabel : (bool) Shows label when input is true. Default is false

labelColor : (series color) Color of the label border and arrow

textColor : (series color) Text color

Returns: (series label) A label visible at the chart level intended for the title pattern

bearNeck() Detects "Bearish On Neck" candle patterns

Returns: (series bool) True when pattern detected

nbLab(showLabel, labelColor, textColor) Produces "Bearish On Neck" identifier label

Parameters:

showLabel : (bool) Shows label when input is true. Default is false

labelColor : (series color) Color of the label border and arrow

textColor : (series color) Text color

Returns: (series label) A label visible at the chart level intended for the title pattern

soldiers(wickSize) Detects "Three White Soldiers" candle patterns

Parameters:

wickSize : (float) Maximum allowable top wick size throughout pattern expressed as a percent of total candle height. Default is 5%

Returns: (series bool) True when pattern detected

wsLab(showLabel, labelColor, textColor) Produces "Three White Soldiers" identifier label

Parameters:

showLabel : (bool) Shows label when input is true. Default is false

labelColor : (series color) Color of the label border and arrow

textColor : (series color) Text color

Returns: (series label) A label visible at the chart level intended for the title pattern

crows(wickSize) Detects "Three Black Crows" candle patterns

Parameters:

wickSize : (float) Maximum allowable bottom wick size throughout pattern expressed as a percent of total candle height. Default is 5%

Returns: (series bool) True when pattern detected

bcLab(showLabel, labelColor, textColor) Produces "Three Black Crows" identifier label

Parameters:

showLabel : (bool) Shows label when input is true. Default is false

labelColor : (series color) Color of the label border and arrow

textColor : (series color) Text color

Returns: (series label) A label visible at the chart level intended for the title pattern

triStarBull() Detects "Bullish Tri-Star" candle patterns

Returns: (series bool) True when pattern detected

tswLab(showLabel, labelColor, textColor) Produces "Bullish Tri-Star" identifier label

Parameters:

showLabel : (bool) Shows label when input is true. Default is false

labelColor : (series color) Color of the label border and arrow

textColor : (series color) Text color

Returns: (series label) A label visible at the chart level intended for the title pattern

triStarBear() Detects "Bearish Tri-Star" candle patterns

Returns: (series bool) True when pattern detected

tsbLab(showLabel, labelColor, textColor) Produces "Bearish Tri-Star" identifier label

Parameters:

showLabel : (bool) Shows label when input is true. Default is false

labelColor : (series color) Color of the label border and arrow

textColor : (series color) Text color

Returns: (series label) A label visible at the chart level intended for the title pattern

wrap(cond, barsBack, borderColor, bgcolor) Produces a box wrapping the highs and lows over the look back.

Parameters:

cond : (series bool) Condition under which to draw the box.

barsBack : (series int) the number of bars back to begin drawing the box.

borderColor : (series color) Color of the four borders. Optional. The default is color.gray.

bgcolor : (series color) Background color of the box. Optional. The default is color.gray.

Returns: (series box) A box who's top and bottom are above and below the highest and lowest points over the lookback

topWick() returns the top wick size of the current candle

Returns: (series float) A value equivelent to the distance from the top of the candle body to its high

bottomWick() returns the bottom wick size of the current candle

Returns: (series float) A value equivelent to the distance from the bottom of the candle body to its low

body() returns the body size of the current candle

Returns: (series float) A value equivelent to the distance between the top and the bottom of the candle body

highestBody() returns the highest body of the current candle

Returns: (series float) A value equivelent to the highest body, whether it is the open or the close

lowestBody() returns the lowest body of the current candle

Returns: (series float) A value equivelent to the highest body, whether it is the open or the close

barRange() returns the height of the current candle

Returns: (series float) A value equivelent to the distance between the high and the low of the candle

bodyPct() returns the body size as a percent

Returns: (series float) A value equivelent to the percentage of body size to the overall candle size

midBody() returns the price of the mid-point of the candle body

Returns: (series float) A value equivelent to the center point of the distance bewteen the body low and the body high

bodyupGap() returns true if there is a gap up between the real body of the current candle in relation to the candle prior

Returns: (series bool) true if there is a gap up and no overlap in the real bodies of the current candle and the preceding candle

bodydwnGap() returns true if there is a gap down between the real body of the current candle in relation to the candle prior

Returns: (series bool) true if there is a gap down and no overlap in the real bodies of the current candle and the preceding candle

gapUp() returns true if there is a gap down between the real body of the current candle in relation to the candle prior

Returns: (series bool) true if there is a gap down and no overlap in the real bodies of the current candle and the preceding candle

gapDwn() returns true if there is a gap down between the real body of the current candle in relation to the candle prior

Returns: (series bool) true if there is a gap down and no overlap in the real bodies of the current candle and the preceding candle

dojiBody() returns true if the candle body is a doji

Returns: (series bool) true if the candle body is a doji. Defined by a body that is 5% of total candle size

Delta Volume Candles [LucF]█ OVERVIEW

This indicator plots on-chart volume delta information using candles that can replace your normal candles, tops and bottoms appended to normal candles, optional MAs of those tops and bottoms levels, a divergence channel and a chart background. The indicator calculates volume delta using intrabar analysis, meaning that it uses the lower timeframe bars constituting each chart bar.

█ CONCEPTS

Volume Delta

The volume delta concept divides a bar's volume in "up" and "down" volumes. The delta is calculated by subtracting down volume from up volume. Many calculation techniques exist to isolate up and down volume within a bar. The simplest use the polarity of interbar price changes to assign their volume to up or down slots, e.g., On Balance Volume or the Klinger Oscillator . Others such as Chaikin Money Flow use assumptions based on a bar's OHLC values. The most precise calculation method uses tick data and assigns the volume of each tick to the up or down slot depending on whether the transaction occurs at the bid or ask price. While this technique is ideal, it requires huge amounts of data on historical bars, which considerably limits the historical depth of charts and the number of symbols for which tick data is available. Furthermore, historical tick data is not yet available on TradingView.

This indicator uses intrabar analysis to achieve a compromise between the simplest and most precise methods of calculating volume delta. It is currently the most precise method usable on TradingView charts. TradingView's Volume Profile built-in indicators use it, as do the CVD - Cumulative Volume Delta Candles and CVD - Cumulative Volume Delta (Chart) indicators published from the TradingView account . My Delta Volume Channels and Volume Delta Columns Pro indicators also use intrabar analysis. Other volume delta indicators such as my Realtime 5D Profile use realtime chart updates to calculate volume delta without intrabar analysis, but that type of indicator only works in real time; they cannot calculate on historical bars.

This is the logic I use to determine the polarity of intrabars, which determines the up or down slot where its volume is added:

• If the intrabar's open and close values are different, their relative position is used.

• If the intrabar's open and close values are the same, the difference between the intrabar's close and the previous intrabar's close is used.

• As a last resort, when there is no movement during an intrabar, and it closes at the same price as the previous intrabar, the last known polarity is used.

Once all intrabars making up a chart bar have been analyzed and the up or down property of each intrabar's volume determined, the up volumes are added, and the down volumes subtracted. The resulting value is volume delta for that chart bar, which can be used as an estimate of the buying/selling pressure on an instrument. Not all markets have volume information. Without it, this indicator is useless.

Intrabar analysis

Intrabars are chart bars at a lower timeframe than the chart's. The timeframe used to access intrabars determines the number of intrabars accessible for each chart bar. On a 1H chart, each chart bar of an active market will, for example, usually contain 60 bars at the lower timeframe of 1min, provided there was market activity during each minute of the hour.

This indicator automatically calculates an appropriate lower timeframe using the chart's timeframe and the settings you use in the script's "Intrabars" section of the inputs. As it can access lower timeframes as small as seconds when available, the indicator can be used on charts at relatively small timeframes such as 1min, provided the market is active enough to produce bars at second timeframes.

The quantity of intrabars analyzed in each chart bar determines:

• The precision of calculations (more intrabars yield more precise results).

• The chart coverage of calculations (there is a 100K limit to the quantity of intrabars that can be analyzed on any chart,

so the more intrabars you analyze per chart bar, the less chart bars can be calculated by the indicator).

The information box displayed at the bottom right of the chart shows the lower timeframe used for intrabars, as well as the average number of intrabars detected for chart bars and statistics on chart coverage.

Balances

This indicator calculates five balances from volume delta values. The balances are oscillators with a zero centerline; positive values are bullish, and negative values are bearish. It is important to understand the balances as they can be used to:

• Color candle bodies.

• Calculate body and top and bottom divergences.

• Color an EMA channel.

• Color the chart's background.

• Configure markers and alerts.

The five balances are:

1 — Bar Balance : This is the only balance using instant values; it is simply the subtraction of the down volume from the up volume on the bar, so the instant volume delta for that bar.

2 — Average Balance : Calculates a distinct EMA for both the up and down volumes, and subtracts the down EMA from the up EMA.

The result is akin to MACD's histogram because it is the subtraction of two moving averages.

3 — Momentum Balance : Starts by calculating, separately for both up and down volumes, the difference between the same EMAs used in "Average Balance" and

an SMA of twice the period used for the "Average Balance" EMAs. The difference for the up side is subtracted from the difference for the down side,

and an RSI of that value is calculated and brought over the −50/+50 scale.

4 — Relative Balance : The reference values used in the calculation are the up and down EMAs used in the "Average Balance".

From those, we calculate two intermediate values using how much the instant up and down volumes on the bar exceed their respective EMA — but with a twist.

If the bar's up volume does not exceed the EMA of up volume, a zero value is used. The same goes for the down volume with the EMA of down volume.

Once we have our two intermediate values for the up and down volumes exceeding their respective MA, we subtract them. The final value is an ALMA of that subtraction.

The rationale behind using zero values when the bar's up/down volume does not exceed its EMA is to only take into account the more significant volume.

If both instant volume values exceed their MA, then the difference between the two is the signal's value.

The signal is called "relative" because the intermediate values are the difference between the instant up/down volumes and their respective MA.

This balance flatlines when the bar's up/down volumes do not exceed their EMAs, which makes it useful to spot areas where trader interest dwindles, such as consolidations.

The smaller the period of the final value's ALMA, the more easily it will flatline. These flat zones should be considered no-trade zones.

5 — Percent Balance : This balance is the ALMA of the ratio of the "Bar Balance" over the total volume for that bar.

From the balances and marker conditions, two more values are calculated:

1 — Marker Bias : This sums the up/down (+1/‒1) occurrences of the markers 1 to 4 over a period you define, so it ranges from −4 to +4, times the period.

Its calculation will depend on the modes used to calculate markers 3 and 4.

2 — Combined Balances : This is the sum of the bull/bear (+1/−1) states of each of the five balances, so it ranges from −5 to +5.

The periods for all of these balances can be configured in the "Periods" section at the bottom of the script's inputs. As you cannot see the balances on the chart, you can use my Volume Delta Columns Pro indicator in a pane; it can plot the same balances, so you will be able to analyze them.

Divergences