Bitcoin 30m Swing Trader Long/Short StrategyIntro

I want to share the results of my passionate hobby and the unstoppable chase for a profitable automated trading strategy. It has been created with the intention of trading only Bitcoin. Altcoins are not interesting for me, as I have discovered lots of issues with finding the right parameter values for experiencing a good performance. As altcoins typically follow the trend of bitcoin and characteristically have a high volatility that may cause stop-hunts, I decided to not over complicate this project. I was just aiming for a profitable trading strategy with an acceptable drawdown and enough confidence by a statistically significant number of trades beside a wide backtesting timespan (credits going out to TradingView: Deep Backtesting).

Total time spent on this is approximately 2 years.

Indicators used

RSI: Used for entries and trend reversal spots

MACD: Used for entry and exit optimiziation

ATR: Used for dynamic offsets in trend definition indicator

Custom trend indicator: Self-made indicator, based on simple price action of higher timeframes using pivot points to find support and resistance zones that have formerly been created

Strategy parameters

I have reduced the total parameters used to just a few. It took lots of working hours to find appropriate values along the trading algorithm and I don’t want to overcomplicate it to you.

This strategy is for those, who have been looking for a working strategy. No DIY kit.

Feel free to adapt Take profit or stop loss targets. But it’s not recommended to do so.

How it works

Entries:

I started with a kind of template that I have been using for strategies for a long time. This includes how to find the right Entries during a trend as well as spotting trend reverse opportunities. Here I combine simple indicators like RSI and MACD beside necessary trend conditions. If a target RSI Value is hit, it will enter a trade, after MACD histogram has stopped to fall/rise. Depends on long/short. While we are in a trade and trend reversed, it waits for a specific RSI target level to be hit, to reverse the trade. As simple as it is, it closes the open one and starts a trade in other direction.

Micro trend:

It starts to get more interesting when it comes to trend recognition, as it forms the core of the strategy and discovering appropriate values for it has been very hard. The final trend variable is defined by the responses over higher timeframes of my self-made trend indicator. Executed on the current timeframe, the trend indicator is quite interesting. But for a automated trading strategy it is necessary to deviate trading instructions from higher timeframes trends.

Macro trend:

The same process that happens for micro trend is also applied with much higher timeframes, like 3D or weekly. The basic assumption is, that if we are in a bull or bear run, where retail investors are flooding the markets, we are increasing our take profit targets respectively. This way we can catch bigger moves in bigger trends.

Exits:

Closing a trade generally happens when a TP target (in %) is hit, or the SL (in %) is hit. The strategy has a special treatment with SL’s. After it happens, the strategy is more careful about market conditions and typically waits for a countertrade. The third way of closing a trade has already been mentioned: the reverse trades. They happen during choppy market conditions. The strategy has also special awareness here and tracks, if reverse trades start to happen more often. After a while, it starts to be more restrictive in opening new reverse trades.

Performance

Capabilities and limitations:

As I have already mentioned the strategy is only optimized for bitcoin (Perpetual Futures). This does not mean, it can not be used on other markets, because the algorithm itself is universal appliable. A very hard task was about finding the right parameter values for the strategy performing like this. If you have a special wish to configure this strategy for a specific market, DM me. The strategy has been tested with different configurations on the following timeframes: 30, 15, 10, 5, 1. I have decided to publish the one for 30m TF, because its performance simply convinced me.

Repainting:

It has been tested lots of times against repainting.

Confidence:

The total backtesting performance reaches out to 2019-09-08. So the strategy has been managing to be successful since then, but this does not guarantee that the logic, this strategy follows, is going to continue this level in future.

Commission:

The algorithm is configured with 0.04% commission per trade, as it is on Binance (for Future Market orders).

Ordersize:

Its totally up to you, how much of your total equity should be traded. Nevertheless, I would personally recommend to not exceed 50% ordersize of your equity with this strategy. In the past, you would have had great performance beside a drawdown, that was from psychological point of view good to handle with. This strategy additionally uses STOP LOSSES, so you can never loose you whole ordersize at one trade.

Slippage:

You also must consider about getting slipped when trading this strategy on live markets. Statistically one could assume, that the slippage could be neutral, as it can be both positive or negative. It depends on your execution time, the exchange, on which you are executing trades and market conditions. But keep it in mind, as if you have too much slippage, this strategy would be unprofitable.

"stop loss" için komut dosyalarını ara

RSI Divergence Strategywhat is "RSI Divergence Strategy"?

it is a RSI strategy based this indicator:

what it does?

it gives buy or sell signals according to RSI Divergences. it also has different variables such as "take profit", "stop loss" and trailing stop loss.

how it does it?

it uses the "RSI Divergence" indicator to give signal. For detailed information on how it works, you can visit the link above. The quantity of the inputs is proportional to the rsi values. Long trades are directly traded with "RSI" value, while short poses are traded with "100-RSI" value.

How to use it?

The default settings are for scalp strategy but can be used for any type of trading strategy. you can develop different strategies by changing the sections. It is quite simple to use.

RSI length is length of RSİ

source is source of RSİ

RSİ Divergence lenght is length of line on the RSI

The "take profit", "stop" and "trailing stop" parts used in the "buy" group only affect buys. The "sell" group is similarly independent of the variables in the "buy" group.

The "zoom" section is used to enlarge or reduce the indicator. it only changes the appearance, it does not affect the results of the strategy.

Inverse MACD + DMI Scalping with Volatility Stop (By Coinrule)This script is focused on shorting during downtrends and utilises two strength based indicators to provide confluence that the start of a short-term downtrend has occurred - catching the opportunity as soon as possible.

This script can work well on coins you are planning to hodl for long-term and works especially well whilst using an automated bot that can execute your trades for you. It allows you to hedge your investment by allocating a % of your coins to trade with, whilst not risking your entire holding. This mitigates unrealised losses from hodling as it provides additional cash from the profits made. You can then choose to hodl this cash, or use it to reinvest when the market reaches attractive buying levels.

Alternatively, you can use this when trading contracts on futures markets where there is no need to already own the underlying asset prior to shorting it.

ENTRY

The trading system uses the Momentum Average Convergence Divergence (MACD) indicator and the Directional Movement Index (DMI) indicator to confirm when the best time is for selling. Combining these two indicators prevents trading during uptrends and reduces the likelihood of getting stuck in a market with low volatility.

The MACD is a trend following momentum indicator and provides identification of short-term trend direction. In this variation it utilises the 12-period as the fast and 26-period as the slow length EMAs, with signal smoothing set at 9.

The DMI indicates what way price is trending and compares prior lows and highs with two lines drawn between each - the positive directional movement line (+DI) and the negative directional movement line (-DI). The trend can be interpreted by comparing the two lines and what line is greater. When the negative DMI is greater than the positive DMI, there are more chances that the asset is trading in a sustained downtrend, and vice versa.

The system will enter trades when two conditions are met:

1) The MACD histogram turns bearish.

2) When the negative DMI is greater than the positive DMI.

EXIT

The strategy comes with a fixed take profit combined with a volatility stop, which acts as a trailing stop to adapt to the trend's strength. Depending on your long-term confidence in the asset, you can edit the fixed take profit to be more conservative or aggressive.

The position is closed when:

Take-Profit Exit: +8% price decrease from entry price.

OR

Stop-Loss Exit: Price crosses above the volatility stop.

In general, this approach suits medium to long term strategies. The backtesting for this strategy begins on 1 April 2022 to 18 July 2022 in order to demonstrate its results in a bear market. Back testing it further from the beginning of 2022 onwards further also produces good returns.

Pairs that produce very strong results include SOLUSDT on the 45m timeframe, MATICUSDT on the 2h timeframe, and AVAUSDT on the 1h timeframe. Generally, the back testing suggests that it works best on the 45m/1h timeframe across most pairs.

A trading fee of 0.1% is also taken into account and is aligned to the base fee applied on Binance.

The best scalping strategyPullbacks are always the most difficult part of trading, and when this happens, we struggle to make a decision about whether to continue trading and wait for a recovery or reduce losses. Similarly, when the instrument has a good trend, it is often difficult to make a decision if we want to withdraw some profit. This strategy is aimed at facilitating these decisions, it looks for price impulses and, based on this, calculates the pullback of the price at which it is necessary to place limit buy orders (yellow lines) based on Fibonacci levels. We place the stop loss on the red line, on the blue and pink lines it is necessary to put a take profit of 50% each. The entry and exit indicator does not always correctly display the entry and exit points, so it is necessary to work with limit orders.

-In the settings, you can change the number of candles participating in the cycle, if the price is at the same level for a long time and limit orders do not work, then it is recommended to reduce the number of candles.

-The remaining parameters are still under development, it is better not to touch them. In the future, I plan to add a limit on the amount of loss as a percentage, for more fine-tuning of risk management

Откаты всегда являются самой сложной частью торговли, и когда это происходит, мы изо всех сил пытаемся принять решение о том, продолжать ли торговлю и ждать восстановления или сократить убытки. Точно так же, когда инструмент имеет хороший тренд, часто трудно принять решение, если мы хотим снять некоторую прибыль. Эта стратегия направлена на то, чтобы облегчить эти решения, она ищет ценовые импульсы и исходя из этого рассчитывает по уровням фибоначи откат цены, на которых необходимо разместить лимитные ордера на покупку (желтые линии). Стоп-лос размещаем на красной линии, на синей и розовой линии необходимо поставить тэйк-профит по 50%. Индикатор входа и выхода не всегда корректно отображает точку входа и выхода, поэтому необходимо работать с лимитными ордерами.

-В настройках можно менять количество свечей участвующих в цикле, если цена долго находится на одном уровне и не срабатывают лимитные ордера то рекомендуются уменьшить количество свечей.

-Остальные параметры до сих пор находятся в разработке, их лучше не трогать. В дальнейшем планирую добавить ограничение размера убытка в процентах, для более тонкой настройки риск менеджмента

AT_MR-15m-ALGO Strategy IndicatorsThis strategy includes systems based on the return-to-mean method.

It creates BUY-SELL signals by getting approval from volatility, trend, momentum, volume, incompatibility and artificial intelligence formations in the system.

Unaffected by Pump and Dump (extreme spikes and dips). In some cases, it can turn this into an opportunity.

Our loss rates in transactions are minimized by algorithms. In other words, it has minimized the loss rates in the position with the stop loss systems and artificial intelligence in it.

IMPORTANT NOTE:

1-) In order for our indicator to be used efficiently, it is necessary to optimize its parameters on a monthly basis. It is offered to you by optimizing regularly by our technical team every month so that it can work efficiently in variable market conditions. Non-optimized systems do not work efficiently in new market conditions.

2-) Strategy should definitely be used on 15-minute charts. Otherwise, it will lead to losses!!!

Turkish Information:

Bu strateji ortalamaya geri dönüş metodu üzerine kurulmuş sistemleri içerir.

Sistem içerisindeki volatilite, trend, momentum, hacim, uyumsuzluk ve yapay zeka formasyonlarından onay alarak AL-SAT sinyallerini oluşturur.

Pump ve Dump(aşırı ani yükselişler ve düşüşler) durumlarından etkilenmez. Bazı durumlarda bunu fırsata çevirebilir.

İşlemlerdeki zarar oranlarımız algoritmalar tarafından minimize edilir. Yani, içerisinde bulunan zarar durdurma sistemleri ve yapay zeka ile pozisyondaki zarar oranlarını minimuma indirmiştir.

ÖNEMLİ NOT:

1-) İndikatörümüzün verimli bir şekilde kullanılabilmesi için her ay düzenli bir şekilde parametrelerinin optimizasyonunun yapılması gerekiyor. Değişken piyasa koşularında verimli çalışabilmesi için her ay düzenli olarak teknik ekibimiz tarafından optimizasyonu yapılarak sizlere sunulmaktadır. Optimize olmayan sistemler yeni piyasa koşullarında verimli çalışmazlar.

2-) Strateji kesinlikle 15 dakikalık grafiklerde kullanılmalıdır. Aksi taktirde kayıplara yol açacaktır!!!

Kifier's MFI/STOCH Hidden Divergence/Trend BeaterMFI/STOCH Hidden Divergence/Trend Beater

General Idea:

My premise around this strategy was to make a general strategy for crypto that would help out with finding entry positions for when you’re bullish on a crypto and want to hold on for a while, and at the same time avoiding massive drops. Essentially a way to mix long term/ swing trading; I somewhat achieved my goal however it still requires a lot of logic tuning of the trend averages.

I’m a huge proponent of volume indicators and coupled with average closing price, I think this gives a really good idea of what is happening with the market. It gives an idea on the market and retail investor sentiment. This generally gives you logical entry positions (Although I don’t know how amazing that will work with all cryptos, there’s a fine line between a good strategy and one that just rides bubble market conditions, some would argue that’s still a success and others not)

How it works:

There are many components to the strategy that try to do different things:

First of all there are two types of entries, a MFI hidden divergence with a STOCH check, essentially it will only fire when a divergence is detected while STOCH is above 50%, however this might be changed in the future as due to the volatile nature of cryptos, the STOCH is not too effective. The second entry is a simple MFI/STOCH trend, if STOCH is above 50% and the trend is detected to be in a trending long, once a MFI crossover over the 50% line is detected an entry is placed, this is designed to get out profit where the divergence would otherwise be less accurate during strongly trending conditions.

-MFI is a great indicator, as a volume weighted momentum indicator I find it the most accurate of all, the STOCH however is a great indicator to get a general picture of simple market conditions and can filter out the emotional noise of retail investors.

-VWMA and an SMA (The bottom oscillator) gives an idea of the trend tacking into account of the volume, this serves as a more short term filter of the trend for filters.

-OBV checks are done between the OBV and an EMA of the OBV, to get the idea of a volume weighted long trend, which is important for crypto as there are massive rallies to go up due to retail greed, it’s great to jump onto it at the beginning, and get off before the stack of cards fall apart.

-ATR is used to detect when the market is relatively just ranging or moving sideways, which is where the hidden divergence entries are done, during predictable and profitable market conditions.

- Stop loss is based on the closest support of the entry, this is a nice medium of room to breath but also an actual stop loss.

Future plans and improvements:

Currently there’s a lot I want to improve, mostly the divergence detection and the overall sharpe ratio could be much better, but the current value of 0.5 gives me hope that the strategy is onto something. I also want to change TP from a percentage stop to something more dynamic but that might be too optimistic. The current plan is to paper trade test this either by manual or by a python bot, to see how it performs with some user input as well.

Khair Day trade with profit lossBest used when applied for intraday trading. Users can customize length and deviation to fit their needs. Works best for high volatility stocks.

This strategy only works intraday intervals, so it means when you try to apply it to day/week/month it won't show any entry or exits.

Bollinger band breakout with non-standard deviation along with profit targets and stop loss.

There are 2 profit targets that can be adjusted based on individual preference.

This strategy minimizes risk and only opens trades when the probability of profitability is higher.

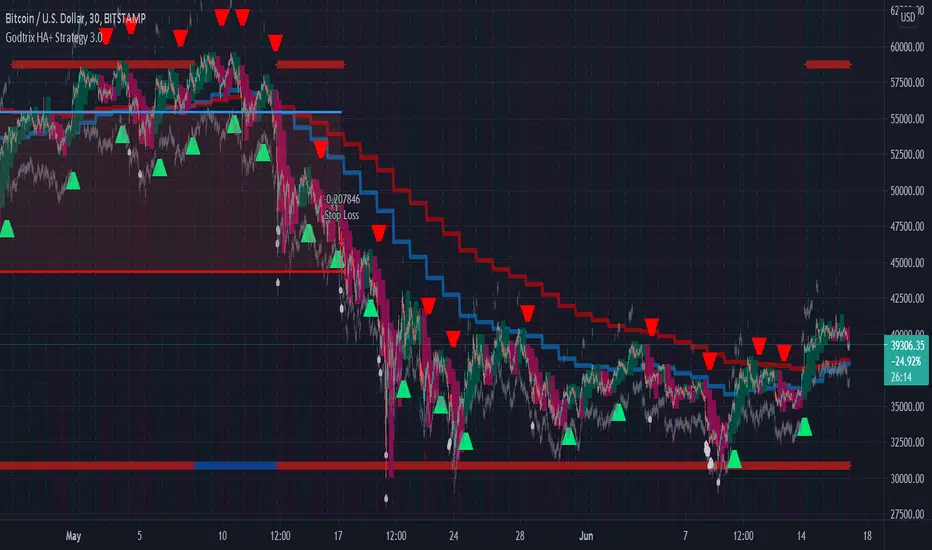

Godtrix's Crypto HA+RSI+EMA+ATH+DCA Strategy 3.0New Updates is here! Upgrade from previous version 2.0 (Please avoid using v2.0 as it's outdated.)

Great stability, Repaint bug fixes, and New features!

==================

| Introduction: |

==================

This is a Long Term Strategy, using compounding profit method, it can generate high returns, but it also risk for losses, this can be overcome if you set Stop Loss to over 25% for bitcoin & 60% for Altcoins.

Best profit plan with this strategy is you trade on Future leverage while you hold on to your coin, so that when price goes up, your coin value goes up, and at the same time, you trade with your leverage to earn even more, easily doubling up your total profit.

Benefits:

Fully customizable and you can easily personalized it and FINE TUNE it according to the market or coin you trading on.

The strategy is based on REAL PRACTICAL trading skills, so it works in real-world.

I fixed the "repainting" issue so the backtest it shows you IS ACCURATE when you run for real-time.

We all know one indicator is not going to help you win your trades, so this strategy combines ALL three: EMA for long+short term trend, HA for short term trend, RSI for entry/exit

This strategy is designed for LONG trade (Buy low, Sell high), not for SHORT trade.

This is not day trading, it is more to mid-term trading, where there's only few trades per month

Mainly is coded to work with 3Commas bot auto trading, so you only need to key in your Bot ID & Email Token.

Bot trading NOTE:

- You need to replace the Alert Message with this: {{strategy.order.alert_message}}

- And you'll need the Bot's webhook Url set with the Alert too.

- One Alert will work for both Buy and Sell Order

- If you using other Bot service, you can enter Custom Command in Input Settings too, it works on any bot service.

Lastly,

regarding the setting advice, I would say you try playing with different settings and your objective is to achieve a backtest result that has:

1) Profitable is > 80%

2) Losing trades is nearly 0 or below 25% of your winning trades. Trick is using far stop loss %

3) Net Profit be almost same or more than "Buy & Hold Profit"

==================

| Latest Updates: |

==================

=| Tidy Up Codings |=

- Group input fields so it'll be easier to understand and find the settings

- Upgrade code for obsolete 'transp' options

=| Repaint Issues |=

- Previous v2.0's RSI has repaint issue, creating false result against real-time data. I've fixed this.

- Also done fine-tuning other parts of the codes to prevent possible repaint issues.

=| Bot System |=

- Improved Custom Bot system, so that you're able to set dynamic order size/quantity with my custom keyword: and

Base Order Example:

{ 'message_type': 'bot', 'bot_id': 1234567, 'email_token': 'abcdefgh-1234-1234-1234', 'base_order': , 'delay_seconds': 0, 'pair': 'USDT_BTC'}

=| EMA Downtrend Exit |=

- Added option for you to decide whether to close position when detected EMA Long term downtrend.

=| EMA 2 (short term) is removed |=

- After several test, I've decided to remove this because it doesn't contribute to improving the results.

=| Heikin Ashi System |=

- Improved the chart display, now you'll see the HA candle 'shadowed' behind, so you'll see both actual price candle and HA candle at same time.

- Added the system that detect the HA candle sizes to decide specifically when it's suitable for Entry and Exit.

>> For "Entry/Exit Range"

- This means after HA is valid for Entry or Exit, how many following bars are allowed to stay valid so it will match other requirements to be completely fulfilled for Entry or Exit.

>> For "Crossing Interval"

- This means after detected HA line crossover, how many HA intervals is allow to Entry or Exit

>> For "Reversed Exit"

- This function let's you decide whether to close position if after HA bull (green candle) changed into HA Bear (red candle)

=| RSI A Entry |=

- Added option to avoid Entry during NTZ (No trade Zone)

- Also added the option to avoid next same condition RSI A entry too soon

=| RSI B Entry |=

- This function is for Entry if RSI is going very low, mostly due to bigger price drops in short time, it's good for buying DIP, however we'll never be able to know when a DIP ends, so do more test on this settings before put into real use.

- Added "avoid" options to help avoid getting Entry at "false" DIP, more like a short & fast pullback which causes RSI to drop very low but actually the price is near ATH or Recent High.

- Added option for Entry with Trailing Price Lower Buy combine with a limit order that grabs low price, so whichever it fulfill first.

=| New: Avoid Entry |=

- Well, it's a pain if you bought at the top, so I've added two options that will avoid buying near ATH and Recent High.

=| Time-limit Removed |=

- Sorry that I've missed look on the script policy which I'm not allowed to put a time-limit for public scripts.

=| System Improvements |=

- HA condition detection is optimized and bug fixed

- RSI values now reads accurately on each bar despite using higher timeframe, especially when moving to next interval

=| New: Dollar Cost Averaging (DCA) Orders |=

- Although DCA strategy is not appealing for Long term strategy, but I've added it for your extra options and flexibilities.

- The settings are quite straight-forward and standard, so I won't be explaining here.

=| New: Backtest Start & End Date |=

- This is very good function when you need more accurate result starting at specific date & time.

- Also if you set the date & time for your real trading starts, it'll much result the same as your actual trading records, which helps you to see clearer and make future decisions.

Any found bugs or flaws, please feel free to PM me, I can't get notifications from comments here below, so I'll not able to reply you the soonest possible, still not sure how to turn on notification for comments, anyone who knows can PM and teach me, lol... Thanks in advance!

Well, this is free version, hope it helps! Feedbacks are all welcome :)

(To Moderators: I've fully use the "f_security()" guideline, but instead of creating a separate function, I apply directly on all security() function. Please don't ban my script before fully check if I've truly fixed repaint. Thank you.)

BITSTAMP:BTCUSD COINBASE:BTCUSD COINBASE:ETHUSD BINANCE:BNBUSDT

Bollinger Band with RSI

Using combination bollinger band and RSI indicator as guide to predict price volatility and the best entry point. The strategy logic is pretty straightforward where we're interested with close price that touches the lower bollinger band ; there are only two scenarios that will happened after the price reaches the lower band; the price might rebound from the lower bollinger band or drop lower and continue downtrend. To confirm the price movement, we use a second indicator which is the RSI to further investigate the price trend. For example, if the price reaches the lower bollinger band but the RSI value is not in the oversold region, we can conclude that the price will go lower and continue downtrend. If the RSI value is in the oversold region, we can use this price area as our entry point.

Stop loss is necessary to avoid losing too much capital if the RSI value lingers too long in the oversold region.

Best take profit area is when the price rebound above the middle bollinger band area/upper bollinger band or when the RSI reaches overbought region; whichever comes first.

Long entry:

RSI < 30 & close price < lower bollinger band

Exit entry:

RSI > 70

Default stop loss: -25%

MACD 50x Leveraged Short Strategy with Real Equity

Hello there ,

Short version of the Macd Long strategy.

MACD Long strategy:

Adding margin: Forbidden or not specified. (Add Margin : No)

Position size: (for each trade) 1%

Stop-Loss: (2% Above Entry Level)

Long: macd crossunder

Exit: macd crossover

Or ofc touching the stop-Loss value as predicted.

These strategies are just examples.

The goal is to observe true equity and equity change.

Warning: This strategy simulation is for Short direction only.

Regards.

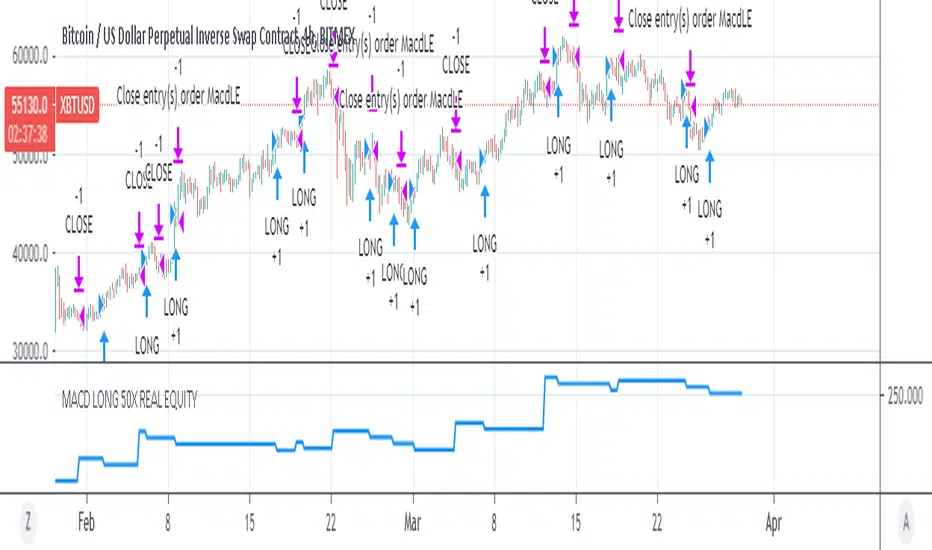

MACD 50x Leveraged Long Strategy Results with Real Equity Hello there.

I was looking for a way to simulate leveraged transactions in Tradingview and this script came out.

You can examine the equity graph without looking at the strategy results.

Thus, the facts will come to light.

Strategy parameters:

Adding margin: Forbidden or not specified. (Add Margin : No)

Position size: (for each trade) 1%

Stop-Loss: (2%)

Long: macd crossover

Exit: macd crossunder

Or ofc touching the stop-Loss value as predicted.

Warning: This strategy simulation is for Long direction only.

Regards.

Low volatility Buy w/ TP & SL (Coinrule)The compression of volatility usually leads to expansion. When the breakout comes, it can ignite strong trends. One way to catch a coin trading in an accumulation area is to spot three moving averages with values close to each other. The strategy uses a combination of Moving Averages to spot the best time to buy a coin before its breakout.

Buy Condition

The MA200 is greater than the MA100

The MA50 is greater than the MA100

According to backtesting results, the 1-hour time frame is the best to run this strategy.

Sell Condition

Take Profit: the price increases 8% from the entry price

Stop Loss: the price drops 4% from the entry price

The strategy has a profitability of 40-60% (depending on the market conditions). Having a ratio of two between Take profit and Stop Loss helps keeping the strategy profitable in the long term.

Triple EMA Scalper low lag stratHi all,

This strategy is based on the Amazing scalper for majors with risk management by SoftKill21

The change is in lines 11-20 where the sma's are replaced with Triple ema's to

lower the lag.

The original author is SoftKill21. His explanation is repeated below:

Best suited for 1M time frame and majors currency pairs.

Note that I tried it at 3M time frame.

Its made of :

Ema ( exponential moving average ) , long period 25

Ema ( exponential moving average ) Predictive, long period 50,

Ema ( exponential moving average ) Predictive, long period 100

Risk management , risking % of equity per trade using stop loss and take profits levels.

Long Entry:

When the Ema 25 cross up through the 50 Ema and 100 EMA . and we are in london or new york session( very important the session, imagine if we have only american or european currencies, its best to test it)

Short Entry:

When the Ema 25 cross down through the 50 Ema and 100 EMA , and we are in london or new york session( very important the session, imagine if we have only american or european currencies, its best to test it)

Exit:

TargetPrice: 5-10 pips

Stop loss: 9-12 pips

TrendMaAlignmentStrategy - Long term tradesThis is another strategy based on moving average alignment and HighLow periods. This is more suitable for long term trend traders and mainly for stocks.

Candle is colored lime if : Lookback Period has at least one bar with moving averages fully aligned OR None of the bars in Lookback periods has negatively aligned moving averages (More than half are positively aligned).

Candle is colored orange if : Lookback Period has at least one bar with moving averages fully aligned in negative way OR none of the bars in lookback has positively aligned moving averages (More than half are negatively aligned).

If either of above conditions are met, candle is colored silver.

Moving average alignment parameters:

Moving Average Type : MA Type for calculating Aligned Moving Average Index

Lookback Period : Lookback period to check highest and lowest Moving Average index.

HighLow parameters:

Short High/Low Period: Short period to check highs and lows

Long High/Low Period: Longer Period to check highs and lows.

If short period high == long period high, which means, instrument has made new high in the short period.

ATR Parameters:

ATR Length: ATR periods

StopMultiplyer: To set stop loss.

ReentryStopMultiplyer: This is used when signal is green buy stop loss on previous trade is hit. In such cases, new order will not be placed until it has certain distance from stop line.

Trade Prameters:

Exit on Signal : To be used with caution. Enabling it will allow us to get out on bad trades early and helps exit trades in long consolidation periods. But, this may also cause early exit in the trend. If instrument is trending nicely, it is better to keep this setting unchecked.

Trade direction : Default is long only. Short trades are not so successful in backtest. Use it with caution.

Backtest years : limit backtesting to certain years.

Part of the logic used from study's below:

Other strategies based on these two studies are below (which are meant for short - medium terms):

Amazing scalper for majors with risk managementHello,

Today I am glad to bring you an amazing simple and efficient scalper strategy.

Best suited for 1M time frame and majors currency pairs.

Its made of :

Ema (exponential moving average) , long period 25

Ema(exponential moving average) Predictive, long period 50,

Ema(exponential moving average) Predictive, long period 100

Risk management , risking % of equity per trade using stop loss and take profits levels.

Long Entry:

When the Ema 25 cross up through the 50 Ema and 100 EMA. and we are in london or new york session( very important the session, imagine if we have only american or european currencies, its best to test it)

Short Entry:

When the Ema 25 cross down through the 50 Ema and 100 EMA, and we are in london or new york session( very important the session, imagine if we have only american or european currencies, its best to test it)

Exit:

TargetPrice: 5-10 pips

Stop loss: 9-12 pips

Hope you enjoy it :)

[HTI2] Hiubris Trend Indicator 2 StrategyThis is the Strategy version of the HTI2 Indicator

After testing several strategies for months and comparing them to the standard 'Buy and Hold' method, we've found the best performing strategy for BTCUSDT

We simplified it to make it more user-friendly (We've only added 1 optional exit: a % SL) and left all the inputs adjustable, so it can be optimized for ANY pair!

This is a Trend Indicator! This means that the '% Profitable Trades' is not the main focus, but catching every trend swing. When trying to catch every trend swing, naturally alot of the them might be unprofitable, especially in sideways markets. The idea behind this strategy is to catch all the significant trend movements, which are alot more profitable than all the 'sideway market' losses

For that reason, we recomment backtesting on Timeframes greater than 15min. Initially we suggest you backtest without a Stop-Loss, trying multiple combinations of the 2 inputs (Length 9 to 32 / Multiplier 2 to 12)

After you found a profitable enough combination, you should look at the 'Average Losing Trade' and the 'Largest Losing Trade', then try further improving the results by setting up a Stop-Loss accordingly (if needed)

In our case, we've found that having a 2% SL (on BTCUSDT) really helps alot with those sideways market trend swings. This also allows us to comfortably us a 10x leverage

*** When using the Re-Entry feature, make sure to change the order size to contracts! Do not leave is as '% of Account' !!! ***

Some of our backtesting results

BTCUSDT 30-5 30min, 2% SL vs 'Buy and Hold'

2019 - present 697.42% vs 250%

2018 - 2019 119.42% vs -75%

EURUSD 18-6 30min, 0.6% SL

2019 - present 12.4%

AMZN 13-2 30min, 2% SL

2019- present 279.44%

XAUUSD 18-3 30min, 1.75% SL

2019- present 53.43%

BA 20-6 30min, 1.5% SL

2019- present 251.35%

[BoTo] Pump&Dump StrategyThis strategy uses only long positions. It isn't used short positions, it doesn't use marginal trade, it doesn't use a pyramiding.

It is strategy uses only one indicator. Ourselves have constructed the indicator for cryptocurrencies. We called it 'Pump&Dump Ocsilator'. You can read as this indicator works here:

Not usual stop

Strategy uses 2 ways for closing of an unprofitable position. But it is possible to use only one way.

Way 1: if the indicator has distinguished a dump, then the long position needs to be closed when the candle is closed (for an example: to close a position when time 00:00 if you have chosen daily timeframe)

Way 2: the user himself chooses the size in settings of this script. Percent. If the user has chosen 100%, means isn't used absolutely. Because the price will never fall by 100%. If the user has chosen less than 100%, for example 5%, then the long position needs to be closed if the low of a candle was less than this price level of choosed stop-loss. But the position needs to be closed too when the candle is closed.

Strategy

A pump-signal: if the candle green and her body is 3 times more than norm

A dump-signal: on the contrary, if the candle red and her body is 3 times more than norm

For opening of a long position: it is necessary any pump-signal (if the position hasn't been open yet)

For closing of a long position: several ways:

1) Or any dump-signal is necessary

2) Or a stop-loss which was chosen by the user is necessary

Millionare tool1. No lag, proprietary algorithm gives signal when position is triggered.

2. Ideal for ones who have tight stop losses but book profits very soon and miss the BIG move.

3. Works on Intraday/ positional/investment long term

4. Works on INDEX/ EQUITY/ FOREX/ CRYPTO CURRENCY

5. Works in any market all over the world, USA,LONDON, JAPAN,INDIA etc

6. 5d,1m,3m ,6m,1yr,5yr no problem.

7. Ideal for trend traders who want to catch the biggest move

8. All human emotions/temptations, silly indicators are out, get the signal? take the entry. simple as ABC

9.Use a breakeven stop loss or max 0.3%, never have a big loss, only big profits

*BUY on long signal, book profits when content, or on next short signal, can initiate fresh shorts too.

*Works in all markets mentioned

*Its your best friend to catch the trend. money

Some examples-

1) postimg.org

2) postimg.org

3) postimg.org

4) postimg.org

5) postimg.org

MACDouble & StochRSI w/ safeties and variable time interval v0.3UPDATE:

IMPORTANT!!! MAKE SURE "RECALCULATE AFTER ORDER FILLED" IS CHECKED. I will have it on by default in the future.

This is a continuation of my previous scripts of two MACD indicators with a Stochastic RSI indicator.

New features:

- Alternate MACD time interval

You can now set the time interval for the second MACD indicator to a different resolution than the displayed chart.

Uncheck the box and select the desired interval. For example, if your chart is set to 15min then first MACD will be set at 15 min and you can select 5 min for the second MACD.

- Alternate StoRSI time interval

You can (and should) set the StochRSI to a different time interval as well. StochRSI hasn't worked great with previous versions. Now you can set it to a different time resolution as well. I strongly recommend you set it at a higher (slower) resolution; for example if your chart is set at 15min then you should test setting the StochRSI at 30 or 45min.

- ' True" StochRSI logic

Trading logic for StochRSI is now a true StochRSI, instead of just reading "k" and ignoring "d", K now has to be greater than D to buy and less than to sell.

- Safeties

A primitive but low risk safety in the form of an uptrend/downtrend price safety. If current close+high isn't greater than the previous close and high then the buy order will not be executed. The same applies for sell orders.

- Cap on losses from short positions

A stop loss safety set to 9000 for exiting sell positions. This will need refinement in the future but this puts a cap on losses from any sell position. At an initial currency of 10,000 this translates to 90.00. If it is giving you problems simply delete line 78 from the source code.

Please feel free to ask any questions or send me suggestions. This is still very much a work in progress and I'll try to polish up the rough spots but it is fully functional. With a slower StochRSI and the safeties I have gotten it to consistently outperform the old 2x MACD strategy script---typically by 3-fold.

S&D Light+ Enhanced# S&D Light+ Enhanced - Supply & Demand Zone Trading Strategy

## 📊 Overview

**S&D Light+ Enhanced** is an advanced Supply and Demand zone identification and trading strategy that combines institutional order flow concepts with smart money techniques. This strategy automatically identifies high-probability reversal zones based on Break of Structure (BOS), momentum analysis, and first retest principles.

## 🎯 Key Features

### Smart Zone Detection

- **Automatic Supply & Demand Zone Identification** - Detects institutional zones where price is likely to react

- **Multi-Candle Momentum Analysis** - Validates zones with configurable momentum requirements

- **Break of Structure (BOS) Confirmation** - Ensures zones are created only after significant structure breaks

- **Quality Filters** - Minimum zone size and ATR-based filtering to eliminate weak zones

### Advanced Zone Management

- **Customizable Zone Display** - Choose between Geometric or Volume-Weighted midlines

- **First Retest Logic** - Option to trade only the first touch of each zone for higher probability setups

- **Zone Capacity Control** - Maintains a clean chart by limiting stored zones per type

- **Visual Zone Status** - Automatically marks consumed zones with faded midlines

### Risk Management

- **Dynamic Stop Loss** - Positioned beyond zone boundaries with adjustable buffer

- **Risk-Reward Ratio Control** - Customizable R:R for consistent risk management

- **Entry Spacing** - Minimum bars between signals prevents overtrading

- **Position Sizing** - Built-in percentage of equity allocation

## 🔧 How It Works

### Zone Creation Logic

**Supply Zones (Selling Pressure):**

1. Strong momentum downward movement (configurable body-to-range ratio)

2. Identified bullish base candle (where institutions accumulated shorts)

3. Break of Structure downward (price breaks below recent swing low)

4. Zone created at the base candle's high/low range

**Demand Zones (Buying Pressure):**

1. Strong momentum upward movement

2. Identified bearish base candle (where institutions accumulated longs)

3. Break of Structure upward (price breaks above recent swing high)

4. Zone created at the base candle's high/low range

### Entry Conditions

**Long Entry:**

- Price retests a demand zone (touches top of zone)

- Rejection confirmed (close above zone)

- Zone hasn't been used (if "first retest only" enabled)

- Minimum bars since last entry respected

**Short Entry:**

- Price retests a supply zone (touches bottom of zone)

- Rejection confirmed (close below zone)

- Zone hasn't been used (if "first retest only" enabled)

- Minimum bars since last entry respected

## ⚙️ Customizable Parameters

### Display Settings

- **Show Zones** - Toggle zone visualization on/off

- **Max Stored Zones** - Control number of active zones (1-50 per type)

- **Color Customization** - Adjust supply/demand colors and transparency

### Zone Quality Filters

- **Momentum Body Fraction** - Minimum body size for momentum candles (0.1-0.9)

- **Min Momentum Candles** - Number of consecutive momentum candles required (1-5)

- **Big Candle Body Fraction** - Alternative single-candle momentum threshold (0.5-0.95)

- **Min Zone Size %** - Minimum zone height as percentage of price (0.01-5.0%)

### BOS Configuration

- **Swing Length** - Lookback period for structure identification (3-20)

- **ATR Length** - Period for volatility measurement (1-50)

- **BOS Required Break** - ATR multiplier for valid structure break (0.1-3.0)

### Midline Options

- **None** - No midline displayed

- **Geometric** - Simple average of zone top/bottom

- **CenterVolume** - Volume-weighted center based on highest volume bar in window

### Risk Management

- **SL Buffer %** - Additional space beyond zone boundary (0-5%)

- **Take Profit RR** - Risk-reward ratio for target placement (0.5-10x)

### Entry Rules

- **Only 1st Retest per Zone** - Trade zones only once for higher quality

- **Min Bars Between Entries** - Prevent overtrading (1-20 bars)

## 📈 Recommended Settings

### Conservative (Lower Frequency, Higher Quality)

```

Momentum Body Fraction: 0.30

Min Momentum Candles: 2-3

BOS Required Break: 0.8-1.0

Min Zone Size: 0.15-0.20%

Only 1st Retest: Enabled

```

### Balanced (Default)

```

Momentum Body Fraction: 0.28

Min Momentum Candles: 2

BOS Required Break: 0.7

Min Zone Size: 0.12%

Only 1st Retest: Enabled

```

### Aggressive (Higher Frequency, More Signals)

```

Momentum Body Fraction: 0.20-0.25

Min Momentum Candles: 1-2

BOS Required Break: 0.4-0.5

Min Zone Size: 0.08-0.10%

Only 1st Retest: Disabled

```

## 🎨 Visual Elements

- **Red Boxes** - Supply zones (potential selling areas)

- **Green Boxes** - Demand zones (potential buying areas)

- **Dotted Midlines** - Center of each zone (fades when zone is used)

- **Debug Triangles** - Shows when zone creation conditions are met

- Red triangle down = Supply zone created

- Green triangle up = Demand zone created

## 📊 Best Practices

1. **Use on Higher Timeframes** - 1H, 4H, and Daily charts work best for institutional zones

2. **Combine with Trend** - Trade zones in direction of overall market structure

3. **Wait for Confirmation** - Don't enter immediately at zone touch; wait for rejection

4. **Adjust for Market Volatility** - Increase BOS multiplier in choppy markets

5. **Monitor Zone Quality** - Fresh zones typically have higher success rates

6. **Backtest Your Settings** - Optimize parameters for your specific market and timeframe

## ⚠️ Risk Disclaimer

This strategy is for educational and informational purposes only. Past performance does not guarantee future results. Always:

- Use proper position sizing

- Set appropriate stop losses

- Test thoroughly before live trading

- Consider market conditions and overall trend

- Never risk more than you can afford to lose

## 🔍 Data Window Information

The strategy provides real-time metrics visible in the data window:

- Supply Zones Count

- Demand Zones Count

- ATR Value

- Momentum Signals (Up/Down)

- BOS Signals (Up/Down)

## 📝 Version History

**v1.0 - Enhanced Edition**

- Improved BOS detection logic

- Extended base candle search range

- Added comprehensive input validation

- Enhanced visual feedback system

- Robust array bounds checking

- Debug signals for troubleshooting

## 💡 Tips for Optimization

- **Trending Markets**: Lower momentum requirements, tighter BOS filters

- **Ranging Markets**: Increase zone size minimum, enable first retest only

- **Volatile Assets**: Increase ATR multiplier and SL buffer

- **Lower Timeframes**: Reduce swing length, increase min bars between entries

- **Higher Timeframes**: Increase swing length, relax momentum requirements

---

**Created with focus on institutional order flow, smart money concepts, and practical risk management.**

*Happy Trading! 📈*

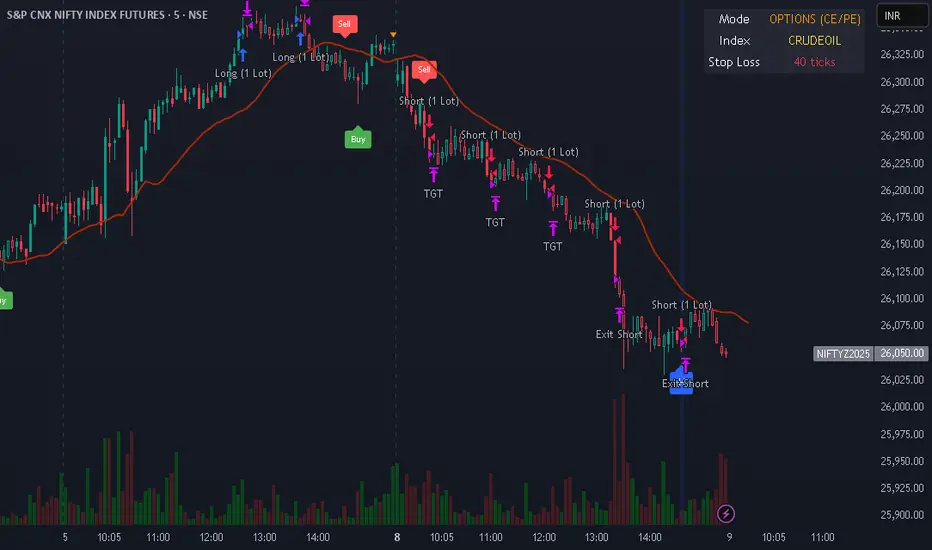

Intraday Options/Futures Naked By TradeEarnIntraday Momentum Strategy (Futures & Options)

Description: This strategy is designed for intraday momentum trading on Indian Indices (Nifty, BankNifty, FinNifty, Sensex) and Crude Oil. It combines Price Action (Impulse Candles) with strictly defined Momentum (RSI) and Trend Strength (ADX) indicators to filter out choppy markets and capture high-probability moves.

Key Features:

Instrument Flexibility: Supports both Futures (Long/Short) and Options Buying (Long CE/PE) modes.

Auto-Lot Sizing: Automatically calculates the correct Lot Size based on the selected Index (e.g., Nifty = 25, BankNifty = 15).

Rupee-Based Risk Management: Define Target, Stop Loss, and Trailing Stop directly in INR (Rupees) rather than points or percentages.

Choppiness Filter: Uses ADX > 20 to avoid trading in sideways markets.

Cooldown Mechanism: Incorporates a "Cooldown" period after every trade exit to prevent over-trading and whipsaws.

⚠️ Disclaimer (As per SEBI & RBI Guidelines)

Educational Purpose Only: This strategy/script is for educational and backtesting purposes only. It does not constitute financial advice, investment recommendations, or a tip to buy or sell any securities.

Risk Disclosure:

Market Risk: Trading in the stock market, especially in Derivatives (Futures & Options), involves a high degree of risk and the potential for significant financial loss. You may lose your entire capital.

No Guarantees: Past performance of this strategy (Backtest results) is not indicative of future results. Market conditions change, and algorithms may fail during live execution.

SEBI Registration: The creator of this script is not a SEBI Registered Investment Advisor (RIA) or Research Analyst (RA).

User Responsibility: By using this script, you acknowledge that you are solely responsible for your own trading decisions. Please consult a SEBI-registered financial advisor before deploying real capital. This script is not compliant with high-frequency trading regulations and is intended for manual or semi-automated analysis only.

Inyerneck Quiet Bottom Hunter v36 — Last Sorta-Working VersionQuiet Bottom Hunter v36 — Accurate Description (the sorta-working version that fires signals)

Overview

A mean-reversion bottom-hunting strategy for small-cap stocks (<$2B market cap). Designed to catch slow-bleed stocks that quietly bottom out and rebound 20–60%+. Good for beginners because signals are infrequent and the setup is easy to understand.

Timeframe

Daily (D) — best results on 1-day charts. Works on weekly too, but signals are rarer.

Triggers / Conditions (all must be true at bar close)

Drop from high ≥ 25% from the highest high in the last 100 bars (previous bars only — no repainting)

Volume ≤ 80% of the 50-day average (quiet accumulation, no panic selling left)

RSI(14) ≤ 38 (oversold territory)

Green/flat streak ≥ 2 consecutive days where close ≥ open (shows sellers are exhausted)

When all four line up → tiny green “QB” triangle below the bar

Firing Frequency

1–4 signals per month on an average small-cap stock (depends on market conditions). Some months zero, some months a handful. Not spammy, but not ultra-rare either.

Usage Parameters

Position size: 10% of equity per trade (default — change to 5–20% depending on risk tolerance)

Profit target: 40%

Stop loss: 12%

Hold time: usually 2–8 weeks

Best on low-float, high-volatility small caps (TLRY, SNDL, MVIS, SOUN, INHD, etc.)

Expected Performance (backtested on 2025 small caps)

Win rate: ~80–85%

Average rebound on winners: +30–40%

Some losers when the bottom isn't "quiet" enough

How to use

Add to daily charts of your small-cap watchlist

When “QB” arrow appears, buy at next open or market

Set 40% target / 12% stop or trail it

Wait for the rebound — no day-trading needed

Triple Screen Scalper [Pro] + Dynamic Risk Engine + Smart DCA🚀 Strategy Concept

This algorithm utilizes a Triple Screen methodology to filter market noise and align trades with the path of least resistance. Instead of relying on a single timeframe, it analyzes market structure across three distinct "horizons" to ensure high-probability execution:

The Tide (Long-Term): Analyzes the dominant directional flow and market bias on higher timeframes.

The Wave (Medium-Term): Measures the strength of the current momentum and pauses trading during weak or "choppy" market phases.

The Ripple (Short-Term): Pinpoints precise entry zones by detecting over-extended price action and mean-reversion opportunities within the larger trend.

The system is fortified with a Smart DCA (Dollar Cost Averaging) Engine that adapts to volatility. It does not blindly add to positions; it calculates "Risk Room" and "Trend Stability" before every additional entry, ensuring capital is deployed efficiently rather than recklessly.

⚙️ Configuration Guide (Variable Explanations)

💰 Position & Leverage

Trade Direction: Choose between Long, Short, or Auto. In "Auto," the system trades both directions based on the dominant trend.

Target Entry Leverage (x): The desired leverage for your initial entry.

Base Order Size (% of Equity): How much of your account balance is allocated to the very first trade of a sequence.

DCA Size Multiplier: Controls how much larger each subsequent order is compared to the previous one. A value of 1.0 means flat sizing; values above 1.0 increase the size of recovery orders.

KILL SWITCH: Max Effective Lev: A safety ceiling. If your total position's effective leverage exceeds this value, the strategy will force-close the position to prevent liquidation.

🚀 Profit Settings (Dynamic Exits)

Use Dynamic Profit?: If enabled, the take-profit target acts like a breathing lung—expanding during high volatility (to catch bigger moves) and contracting during quiet periods.

Gain Volatility Length: The lookback period used to measure recent market volatility.

Gain Multiplier: Scales the profit target. Higher numbers require a larger price move to hit profit; lower numbers take profit sooner.

Minimum Profit Floor %: A hard limit ensuring the target never drops below this percentage, even in extremely low-volatility markets.

📉 Trend & Momentum Filters

Trend Strength Threshold: Defines the minimum "velocity" required to trade. This filters out flat, ranging markets where trends are not established.

Momentum Sensitivity (K/D/Smooth): These variables tune the sensitivity of the entry trigger.

Lower numbers = Faster entries (more trades, potentially more noise).

Higher numbers = Slower, more confirmed entries.

Overbought / Oversold Levels: The specific zones (0-100) where price is considered statistically over-extended, triggering a reversal signal.

🛡️ Risk & DCA Settings

Enable Hard Stop Loss: A traditional safety stop based on a fixed percentage.

Max DCA Orders: The maximum number of times the strategy is allowed to "average down" on a position.

Require Trend for DCA?: If TRUE, the strategy will only add to a losing position if the broader market trend is still valid. If the trend breaks, it stops buying.

DCA Volatility Length/Multiplier: Controls the spacing between buy orders.

High Multiplier = Orders are spread far apart (safer for crashes).

Low Multiplier = Orders are closer together (faster recovery in normal dips).

Risk Scaling: A unique feature that pushes DCA orders further away as your leverage increases, protecting you from adding too much risk too quickly.

Base DCA %: The minimum distance required between orders, regardless of volatility.

⏱️ Timers & Cooldowns

Fast / Slow Cooldown: The minimum time (in seconds) the strategy must wait between realizing a profit and opening a new trade. This prevents "revenge trading" or entering twice on the same candle.

Position Cooldown: A specific timer applied after a large position is closed to let the market settle.

🎯 Daily S/R Targets

Enable Daily S/R: If enabled, the strategy will attempt to "snipe" exits at calculated daily support and resistance pivots.

Proximity Threshold: How close the price must get to a daily level to trigger an early exit.

⚠️ Risk Disclaimer

This script is an automated tool for analysis and execution assistance. It employs averaging techniques (DCA) which involve calculated risk. While the "Kill Switch" and "Risk Scaling" features are designed to mitigate exposure, users should thoroughly backtest and understand the "Multiplier" settings before deploying real capital. Past market structure is not a guarantee of future performance.