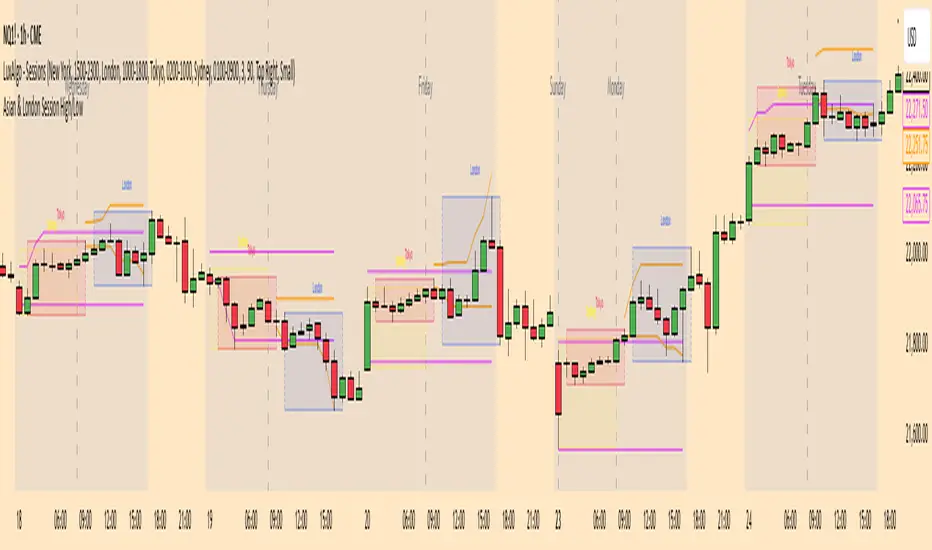

AP Session Liquidity with EQH/EQL and Previous DayThis indicator plots key intraday session highs and lows, along with essential market structure levels, to help traders identify areas of interest, potential liquidity zones, and high-probability trade setups. It includes the Asia Session High and Low (typically 00:00–08:00 UTC), London Session High and Low (08:00–12:00 UTC), New York AM Session High and Low (12:00–15:00 UTC), and New York Lunch High and Low (15:00–17:00 UTC). Additionally, it displays the Previous Day’s High and Low for context on recent price action, as well as automatically detected Equal Highs and Lows based on configurable proximity settings to highlight potential liquidity pools or engineered price levels. These session levels are widely used by institutional traders and are critical for analyzing market behavior during time-based volatility windows. Traders can use this indicator to anticipate breakouts, fakeouts, and reversals around session boundaries—such as liquidity grabs at Asia highs/lows before the London or New York sessions—or to identify key consolidation and expansion zones. Equal Highs and Lows serve as magnets for price, offering insight into potential stop hunts or inducement zones. This tool is ideal for day traders, scalpers, and smart money concept practitioners, and includes full customization for session timings, color schemes, line styles, and alert conditions. Whether you're trading price action, ICT concepts, or supply and demand, this indicator provides a powerful framework for intraday analysis.

"session" için komut dosyalarını ara

RTH Session Highs & LowsA Pine Script indicator designed to track and plot the Regular Trading Hours (RTH) session highs and lows on a chart, typically for U.S. equity markets (e.g., S&P 500, Nasdaq, etc.), which operate from 9:30 AM to 4:00 PM Eastern Time.

Session High & Low Lines:

During the RTH session, the indicator draws green and red horizontal lines that represent the highest and lowest price seen so far within that trading session.

These levels help traders identify intraday support (low) and resistance (high) levels.

New High/Low Markers:

Small triangle markers are placed:

Above the bar when a new intraday high is made (green triangle).

Below the bar when a new intraday low is made (red triangle).

This visually flags when momentum may be building or reversing.

Intraday Strategy Support:

Use the session high/low as dynamic support/resistance for scalping or breakout strategies.

For example:

Breakouts above session highs may indicate bullish strength.

Breakdowns below session lows may suggest bearish momentum.

Mean Reversion Tactics:

Prices approaching these lines and then rejecting can be used for mean reversion setups.

Combine with volume or candlestick patterns for confirmation.

Risk Management:

Set stops or targets relative to session highs/lows.

For instance, use session high as a stop-loss level in a short position.

Volatility Gauge:

Tracking how frequently new highs/lows are formed can help assess intraday volatility or range expansion.

Complement with Indicators:

Combine this with our "McGinley Dynamic Channel with Directional Shading" indicator or our "EMA Crossover with Shading" indicator to add context to breakouts or rejections.

matrixx Global Sessions + Good/Premium Spread ZonesSimple (enough) Script that allows you to visualize the major trading sessions, with some QoL stuff, Includes a "Monday Open" bar for reference when zooming out.

By default no one 'session' is turned on; instead, we have;

Good Zone - where spread tends to close up enough for (me) to trade in the 1-minute timezones

Premium Zone - where the tightest spreads tend to happen and I (you?) can get more aggressive with Stop Losses, and moment-to-moment trade accuracy.

The Monday Open - for reference.

You are able to go into the settings and turn these on and off at will, making any combination of 'zones' you prefer, and can colour code them, as well.

Points of Difference;

You can turn on and off any group or set of sessions for an overview;

Additionally, this is coded so that if there is a "Daylight Saving" or other localized timezone shift, it should be reflected correcty, as timezones are calculated based on each sessions' data, not arbitrarily with +/- as most of the other scripts that do similar to this one.

Monday Open

you can toggle sessions, or instead toggle the 'off hour' zones, at will

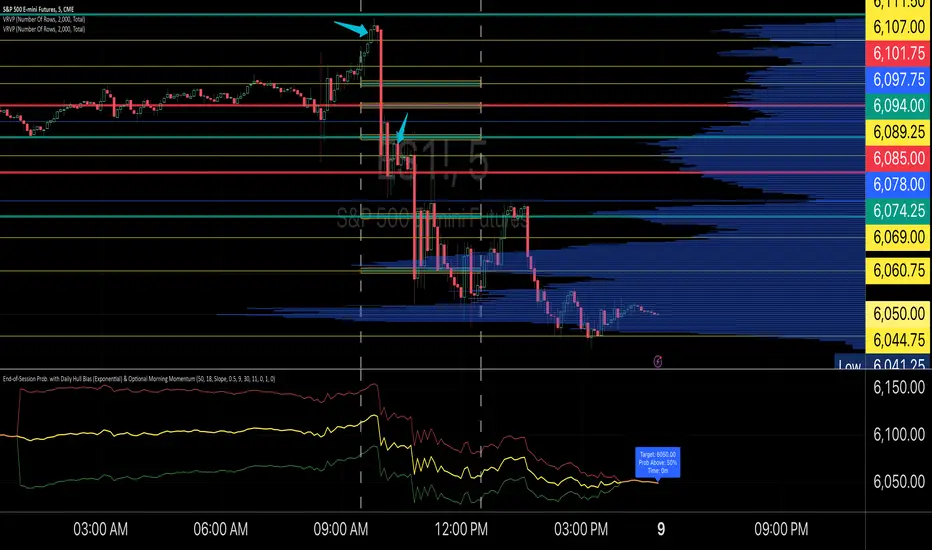

End-of-Session ProbabilityThis indicator estimates the probability that the market will finish the session above a specified target price. It blends a statistical probability model with directional bias and optional morning momentum weighting to help traders gauge end-of-day market expectations.

Key Features:

• Statistical Probability Model:

Uses a normal distribution (with a custom normal CDF approximation) scaled by the square-root-of-time rule. The indicator dynamically adjusts the standard deviation for the remaining session time to compute a z‑score and ultimately the probability that the session close exceeds the target.

• Directional Bias via Daily HullMA (Exponential):

A daily Hull Moving Average (calculated using an exponential method) is used as a big-picture trend indicator. The model allows you to select your bias method—either by comparing the current price to the daily HullMA (Price method) or by using the HullMA’s slope (Slope method). A drift multiplier scales this bias, which then shifts the mean used in the probability calculations.

• Optional Morning Momentum Weight:

For traders who believe that early session moves provide useful clues about the day’s momentum, you can enable an optional weighting. The indicator captures the percentage change from the morning open (within a user-defined time window) and adjusts the expected move accordingly. A multiplier lets you control the strength of this adjustment.

• Visual Outputs:

The indicator plots quantile lines (approximately the 25%, 50%, and 75% levels) for the expected price distribution at session end. An abbreviated on-chart label displays key information:

• Target: The target price (current price plus a user-defined offset)

• Prob Above: The probability (in percentage) that the session close will exceed the target price

• Time: The time remaining in the session (in minutes)

How to Use:

1. Set Your Parameters:

• Expected Session Move: Input your estimated standard deviation for the full-session move in price units.

• Daily Hull MA Settings: Adjust the period for the daily HullMA and choose the bias method (Price or Slope). Modify the drift multiplier to tune the strength of the directional bias.

• Target Offset: Specify an offset from the current price to set your target level.

• Morning Momentum (Optional): Enable the morning momentum weight if you want the indicator to adjust the expected move based on early session price changes. Define the morning session window and set the momentum multiplier.

2. Interpret the Output:

• Quantile Lines: These represent the range of possible end-of-session prices based on your model.

• Abbreviated Label: Provides a quick snapshot of the target price, probability of finishing above that target, and time remaining in the session.

3. Trading Application:

Use the probability output as a guide to assess if the market is likely to continue in the current direction or reverse by session close. The indicator can help you decide on trade entries, exits, or adjustments based on your overall strategy and risk management approach.

This tool is designed to offer a dynamic, statistically driven snapshot of the market’s expected end-of-day behavior, combining both longer-term trend bias and short-term momentum cues.

High & Low Of Custom Session - Breakout True Open [cognyto]This indicator is based on the High & Low Of Custom Session - OpeningRange Breakout (Expo) created by Zeiierman.

It adds new functionality and enhances existing settings, targeting ES, NQ, and YM:

Manages session defaults to 12:00 to 13:00

New true opening fully customizable (default 13:00)

Manages timeframe visualization (default 15m and below)

Manages session draw length until the end of the current session (default NY)

Manages previous sessions, allowing the to be hidden

Improves timezone selection (default NY)

Following the strategy called Paradox detailed by DayTradingRauf, it works with indices like ES, NQ, and YM.

The rules consider three possible profiles:

First

AM session as consolidation (08:00-12:00)

Lunch hour range as consolidation (less than 100 points)

PM session breaking either side of the session range

Second

AM session trending lower (08:00-12:00)

Lunch hour range as consolidation (less than 100 points)

PM session trending higher

Third

AM session trending higher (08:00-12:00)

Lunch hour range as consolidation (less than 100 points)

PM session trending lower

After the session ends, the opening price at 13:00 is automatically drawn as it is a key point for the entry strategy.

The strategy can be monitored using a 5-minute or 15-minute timeframe as follows:

- Wait for a liquidity hunt (either the high or low of the lunch session range or AM is taken).

- If liquidity is taken, switch to the 1-minute timeframe and wait for a CISD (change in the state of delivery), where the price closes below an OB, or consider a breaker block or iFVG to enter the trade.

- Bullish entries should happen below the opening price at 13:00, and bearish entries should happen above.

- Consider a 1:2 reward ratio. However, runners can target the opposite side of the range that was not yet taken.

This indicator is for informational purposes only and you should not rely on any information it provides as legal, tax, investment, financial or other advice. Nothing provided by this indicator constitutes a solicitation, recommendation, endorsement or offer by cognyto or any third party service provider to buy or sell any securities or other financial instruments in this or any other jurisdiction in which such solicitation or offer would be unlawful under the securities laws of such jurisdiction.

Volatility Weighted Moving Average + Session Average linesHi Traders !

Just finished my Y2 university finals exams, and thought I would cook up a quick and hopefully useful script.

VWAP + Session Average Lines :

Volatility Weighted Average Price in the standard case is a trading indicator that measures the average trading price for the user defined period, usually a standard session (D timeframe), & is used by traders as a trend confirmation tool.

This VWAP script allows for altering of the session to higher dimensions (D, W, M) or those of lower dimension (H4, or even H1 timeframes), furthermore this script allows the lookback of data to be switched from the standard session to a user defined amount of bars (e.g. the VWAP of 200 bars as opposed to the VWAP of a standard session which contains 95 bars in M15 timeframe for 24/7 traded assets e.g. BTCUSD), lastly this script plots Session VWAP Average Lines (if true in settings) so tradaes can gauge the area of highest liquidity within a session, this can be interpreted as the fair price within a session. If Average lines are increasing and decreasing consistently like a monotonic function this singles traders interest is at higher / lower prices respectively (Bullish / Bearish bias respectively ?), However if Average lines are centered around the same zones without any major fluctuations this signals a ranging market.

VWAP calculation :

VWAP is derived from the ratio of the assets value to total volume of transactions where value is the product of typical price (Average of high, low and close bars / candles) and corresponding bar volume, value can be thought of as the dollar value traded per bar.

How is VWAP used by Institutions / Market movers :

For some context and general information, VWAP is typically used by Market movers (e.g. Hedge funds, Mutual funds ,..., ...) in their trade execution, as trading at the VWAP equals the area of highest market volume, trading in line with the volume of the market reduces transaction costs by minimizing market impact (extra liquidity lowers spreads and lag time between order fills), this overall improves market efficiency.

In my opinion the script is best used with its standard settings on the M15 timeframe, note as of now the script is not functional on certain timeframes, however this script is not intended to be used in these timeframes, i will try fix this code bug as soon as possible.

Custom Trading Session HighlighterThe Custom Trading Session Highlighter is a simple yet powerful indicator that allows you to visualize specific trading sessions on your chart by highlighting the background within the specified time range. This indicator can be helpful for traders who want to focus on specific market hours or analyze the market behavior during certain time periods.

Features:

>Customizable start and end times: Input your desired trading session start and end times using the format "HHMM" (e.g., "0930" for 9:30 AM). The indicator allows you to select the time range in 30-minute intervals.

>Trading session background color: The specified trading session will be highlighted with a semi-transparent green color, making it easy to differentiate the session from the rest of the chart.

>Overlay: The indicator overlays on the price chart, so it doesn't take up any additional space on your screen.

How to use:

>Add the Custom Trading Session Highlighter to your chart.

>Configure the start and end times of the session you want to highlight using the input fields in the indicator settings.

>Observe the highlighted trading session on your chart to analyze market behavior within that specific time range.

Daily Session Windows background highlight indicatorIn intraday studies of stock indexes and Forex I have this weird habit of highlighting premarket, core session, lunch break and extended session with different backgrounds. If done by hand, this is tedious work that has to be repeated daily.

I think this feature should be built-in in TradingView. But it isn't.

For a few months now, I have been using this tiny indicator that does precisely that job. It saved me literally hours of focus time and mistakes. I have decided to revamp it and release it. I'm sure it can be useful to others.

Features:

Background color highlighting for premarket , core session , lunch hour and extended session of the trading day.

Session timing preset to match US session, but can be customized.

Can be enabled or disabled on a day of the week basis, including week-end.

Timezone is selectable, matches the chart's instrument but can be set independently to track a different timezone.

Not affected by the timezone you decided to assign to the chat's time scale.

Ready for stock indexes, but can be used to highlight Forex sessions too.

BTMM OFJ FOR BEST RESULTS PLEASE SWITCH TO LINE CHART OR DISABLE THE CHART CANDLES. BELOW IS A LINE WITH OPACITY TURNED DOWN TO 15%

ASIA, LONDON, AND NEW YORK SESSIONS CAN BE CUSTOMIZED (1ST 3 HRS DEFAULT)

VOLUME CANDLES CAN BE APPLIED WITH SUPPLY AND DEMAND OR MARKET MAKER METHOD. IN A STRONG TREND YOU WANT TO SEE REPEATED HIGH VOLUME CLUSTERS IN THE DIRECTION OFTHE TREND AND FADING LOW VOLUME ON THE RETRACE

BASICK KEY LEVELS WEEKLY INITIAL BALANCE (MONDAY+TUESDAY HIGHEST HIGH AND LOWEST LOW) YESTERDAY AND LASY WKHI/LO

QUICK APPLICATON

Pre and Market OpeningsPre and Market Openings is to enable you to quickly visualize the opening markets and how they could influence trading.

The below script has used the market time data from the below links:

Tokyo/Asia www.tradinghours.com

London www.tradinghours.com

New York www.tradinghours.com

The below script aims to plot:

Daily Asia Open

Weekly Asia Open

Daily London Open

Weekly London Open

Daily New York Open

Weekly New York Open

Using background colour it also shows market sessions (pre-market) for London and New York and regular for London, New York and Asia.

There is also plotted text for days of the week and sessions.

As you can see from the picture below that these market openings can act as support and resistance:

BTC

ETH

Breakout Scalper (Session)This is a twist on my on my Breakout Scalper strategy that limits trading to a user-configurable session

Find the original "Continuous" version of the scalper here:

The breakout scalper is based on "slow" and "fast" donchian periods. In this version, the "slow" donchian is in fact the Day's high/low. This important difference means that we will always be entering our trades at the day's high or low, so you are exposed to the price making new highs/lows but not to oscillations within the day's range.

Furthermore, the scalper is modified to only enter trades after the start of the user-configured session. Any open trades are closed at the end of the user-configured session. The default session is set to 10:00 AM to 3:30 PM because that's when I like to trade.

NY Session 15 min ORB + Fib RetracementThis indicator builds a New York session Opening Range (ORB) and plots Fibonacci retracement levels based on that range.

What it does

Defines the Opening Range using the NY cash open (default: 9:30–9:45 ET)

Tracks the ORB high and low during that window

Locks the ORB once the window ends (recommended)

Draws Fibonacci retracement levels from the ORB range

Optionally fills the space between fib levels

Displays price tags for ORB levels and fib levels on the right side

Sessions

ORB window is configurable (default: 9:30–9:45 ET)

Fib levels are only shown during the selected plot session

(default: 9:30–16:00 ET)

Nothing plots outside the selected fib session

Prevents lines from connecting across trading days

Fib behavior

Fibs are calculated from the ORB high and low

Direction can be:

High → Low (default)

Low → High

Common fib ratios are included by default:

0.236

0.382

0.500

0.618

0.786

All ratios are user-editable

Visuals

ORB High = green line

ORB Low = red line

Fib levels = gray lines

Optional shaded fill between fib levels

Optional right-side labels showing:

ORB High / Low price

Fib ratio and exact price

Recommended use

Designed for intraday trading

Best used on NY session instruments (ES, NQ, SPY, QQQ, etc.)

Works well on lower timeframes (1–15 min)

Locking the ORB at session end is recommended for consistency

Notes

Indicator does not generate trade signals

Levels are intended as reference only

Always use proper risk management

Asia & London Session High/Low Description:

This indicator plots the highest and lowest points of the Asian and London trading sessions based on Eastern Time (ET).

Features:

Draws horizontal rays for session highs and lows

Automatically resets for each session

Perfect for I CT-style liquidity analysis , range breaks , and session-based trading setups

Clean chart : no labels or clutter, just the key session levels

Use it to identify liquidity zones , plan entries , and anticipate potential session raids in your trading strategy.

Padder Scalp - Manipulation Triangle + First 15m Session BoxThis indicator combines intraday manipulation detection with session‑based structure and key candlestick pattern labeling to support precision scalp trading.

1. Manipulation Candle Detection (Daily ATR‑Based)

The script calculates the Daily ATR(14) and compares each intraday candle’s range to it.

If a candle’s range is ≥ 20% of the daily ATR, it is flagged as a potential manipulation candle.

A purple triangle is plotted beneath any candle that meets this threshold, helping traders quickly spot abnormal volatility spikes that often precede liquidity grabs or engineered moves.

2. First 15‑Minute RTH Session Box (9:30–9:45 AM)

Designed for use on a 15‑minute chart, the script automatically identifies the first bar of the regular trading session (RTH).

When the 9:30–9:45 candle prints:

- Its high and low are captured

- A session box is created using those levels

- The box extends across the entire trading day

This provides a consistent structural reference point for opening‑range dynamics, liquidity sweeps, and intraday bias.

3. Automatic Box Extension

Once the first RTH candle is detected, the script draws a blue box from that candle’s high/low and continuously extends it to the right for the remainder of the session.

This creates a persistent visual anchor for:

- Breakouts

- Retests

- Rejections

- Mean‑reversion scalps

4. Candlestick Pattern Detection + Labels

The script identifies and labels four high‑value reversal/continuation patterns:

- Bullish Engulfing → green label above the candle

- Bearish Engulfing → red label below the candle

- Hammer → yellow label below the candle

- Inverted Hammer → orange label above the candle

These labels help traders quickly spot actionable price‑action signals without manually scanning every bar.

Overall Purpose

This tool blends volatility‑based manipulation detection, opening‑range structure, and real‑time candlestick pattern recognition into a single, clean visual system.

It’s built for scalpers and intraday traders who rely on:

- Opening‑range levels

- Liquidity cues

- Manipulation signals

- Price‑action confirmation

to time entries with precision.

3 Trading Sessions [TickDaddy]Customizable 3 trading session indicator. Asia, Longdon, New York. Adjust times for each session, color, opacity. toggle if you want to see future sessions coming up.

HTCTS - Session & Time LiquidityHTCTS - Session & Time Liquidity

1. ภาพรวมการทำงาน (Overview)

อินดิเคเตอร์ตัวนี้ทำหน้าที่ 4 อย่างหลักพร้อมกัน:

Auto DST (ปรับเวลาตามฤดูอัตโนมัติ): คุณไม่ต้องมานั่งแก้เวลาเมื่อตลาดต่างประเทศเปลี่ยนเวลา (Daylight Saving Time) เพราะโค้ดอ้างอิง Timezone ของตลาดนั้นๆ โดยตรง (เช่น NY ใช้ America/New_York)

Session Bars: แสดงแถบสีเล็กๆ ด้านล่างจอเพื่อบอกว่าตอนนี้อยู่ใน Session ไหน (Asia, London, NY AM, NY PM, Thai) แทนการถมสีพื้นหลังซึ่งอาจจะรกตา

High/Low Levels & Sweeps: เมื่อจบ Session โปรแกรมจะตีเส้น High และ Low ของช่วงเวลานั้นทิ้งไว้ ถ้ากราฟวิ่งไปชนเส้นเหล่านั้น (Breakout/Sweep) เส้นจะเปลี่ยนเป็นเส้นประและขึ้นข้อความว่า "(Swept)"

1. Indicator Overview and Purpose (ICT/SMC Framework)

This custom Pine Script indicator is designed specifically for traders utilizing ICT (Inner Circle Trader) or SMC (Smart Money Concepts) methodologies. Its primary function is to simplify the analysis of Time & Price by automatically defining and tracking key market sessions, their resulting liquidity levels (High/Low), and detecting liquidity sweeps (Stop Hunts).

The indicator is designed to be Zero-Maintenance regarding time zones, as it automatically adjusts for Daylight Saving Time (DST) changes in major financial centers (London, New York).

2. Key Features and Logic

A. Automatic DST Handling (Auto-DST)

The script uses specific, location-based time zones for global markets instead of a fixed GMT/UTC offset.

Asia: Uses Asia/Tokyo.

London: Uses Europe/London (Automatically adjusts for BST).

New York (AM/PM): Uses America/New_York (Automatically adjusts for EST/EDT).

This guarantees that the session times displayed on your chart (regardless of your local time, e.g., Thailand GMT+7) always align with the actual opening and closing moments of the corresponding financial market.

HTF FVG + SessionsThis indicator combines multi-timeframe FVG A–C detection with intraday session boxes on a single chart.

It automatically finds bullish and bearish Fair Value Gaps on 15m, 30m, 1H, 4H, 1D and 1W timeframes.

Fresh FVGs are drawn in a transparent gold color, then dynamically shrink as price trades back into the gap.

Once price fully fills the gap, the FVG box and its label are automatically removed from the chart.

After the first touch, each FVG changes to a per-timeframe gray shade, making overlapping HTF gaps easy to see.

You can toggle each timeframe on/off and also globally enable/disable all FVGs from the settings panel.

Session boxes highlight Asia, London, NY AM, NY Lunch and NY PM using soft colored rectangles.

Each session box is plotted from the high to the low of that session and labeled with its name in white text.

A global “Show all session boxes” switch allows you to quickly hide or display the session structure.

This tool is designed for traders who want to combine FVG liquidity maps with clear intraday session context.

USD Session 8FX - LDN & NY (TF-invariant, Live + Table)What changed

Flexible session window

Removed the old fixed NY end-time selector.

Added new inputs so you can pick start time and length:

London: ldnStartSel (default 08:00) and ldnLenSel with options 45/60/90 minutes.

New York: nyStartSel (default 15:30) and nyLenSel with options 45/60/90 minutes.

The session string used by time(refTF, sess, tz) is now built dynamically as "HHMM-HHMM" from start + length (e.g., 1530-1630).

The label shown in the table (winTxt) auto-formats to HH:MM–HH:MM.

New time helpers

addMinutesHHMM() computes the end time from a "HHMM" start plus a minute length.

makeSess() produces the session string "HHMM-HHMM".

prettySess() converts "HHMM-HHMM" → "HH:MM-HH:MM".

(Kept on one line to avoid the “end of line without line continuation” error.)

Stability & UI fixes

Main table now uses table.new(f_pos(tablePos), ...) directly (no undeclared pos variable).

Trade Gate panel uses a properly initialized gatePosEnum before table.new(...) (fixes “Undeclared identifier”).

Minor cleanups; no logic changes.

What did NOT change

Scoring logic: returns → optional ATR normalization → weights → anti-USD vs USD-base averages → final score.

Thresholds: minAbsScore and live intrath alerts are unchanged.

VWAP Gate logic is the same (price vs VWAP consistency depending on USD Strong/Weak).

Freeze/Lock of values at session end is unchanged.

Alerts (session close bias, live threshold cross, and “Entry hint”) are unchanged.

Why this helps (practical impact)

Longer windows (e.g., NY 60/90, LDN 60/90) usually make the score more robust, filtering noise and reducing false signals—at the cost of a slightly slower signal.

You can now A/B test:

London: 45 vs 60 vs 90

New York: 45 vs 60 vs 90

without touching anything else; the indicator adapts automatically.

How to use

Choose Session (London / New York).

Set the start and length for that session.

The background highlight, the winTxt, and the entry/exit logic all follow the dynamic window.

Quick tips to reduce false signals

Try NY 60 or NY 90 and LDN 60 when volatility is choppy.

Keep ATR normalization ON (useATRnorm = true) for more comparable returns.

Consider raising minAbsScore slightly (e.g., from 0.12 → 0.15–0.20) if you still see noise.

Use the VWAP Gate panel: only act when Bias OK and at least one of the Top-3 pairs shows VWAP OK.

If you want, I can add quick presets (buttons) to jump between LDN 45/60/90 and NY 45/60/90, or plot two Scores side by side for direct comparison.

Multi-Session Viewer and AnalyzerFully customizable multi-session viewer that takes session analysis to the next level. It allows you to fully customize each session to your liking. Includes a feature that highlights certain periods of time on the chart and a Time Range Marker.

It helps you analyze the instrument that you trade and pinpoint which times are more volatile than others. It also helps you choose the best time to trade your instrument and align your life schedule with the market.

NZDUSD Example:

- 3 major sessions displayed.

- Although this is NZDUSD, Sydney is not the best time to trade this pair. Volatility picks up at Tokyo open.

- I have time to trade in the evening from 18:00 to 22:00 PST. I live in a different time zone, whereas market is based on EST. How does the pair behave during the time I am available to trade based on my time zone? Time Range Marker feature allows you to see this clearly on the chart (black lines).

- I have some time in the morning to trade during New York session, but there is no way I am waking up at 05:00 PST. 06:30 PST seems doable. Blue highlighted area is good time to trade during New York session based on what Bob said. It seem like this aligns with when I am available and when I am able to trade. Volatility is also at its peak.

- I am also available to trade between London close and Tokyo open on some days of the week, but... based on what I see, green highlighted area is clearly showing that I probably don't want to waste my time trading this pair from London close and until Tokyo open. I will use this time for something else rather than be stuck in a range.

Pre-London & London Session (Auto DST) MMMThis indicator automatically marks the Pre-London and London Open sessions for any trading day, with full U.S. Daylight Saving Time (DST) adjustment.

It’s ideal for traders backtesting Gold (XAUUSD) or other pairs sensitive to London liquidity, as it dynamically shifts between UTC-4 and UTC-5 to stay perfectly aligned with institutional session timing.

Features:

🕑 Auto-detects whether the date falls under U.S. Daylight or Standard Time

🟧 Highlights Pre-London session (2 a.m.–3 a.m. EDT / 1 a.m.–2 a.m. EST)

🟩 Highlights London session (3 a.m.–5 a.m. EDT / 2 a.m.–4 a.m. EST)

⚙️ No manual adjustments needed — fully automatic for any backtest date

📈 Perfect for ICT, Smart Money, and liquidity-based session strategies

Recommended settings:

Chart timezone: New York

Works on all symbols and timeframes

Dr.Yazdani V063 Session OR + A-Lines

**ACD Indicator: Mark Fisher's Opening Range Breakout Strategy**

**Overview**

The ACD system, developed by legendary trader Mark Fisher in his book *The Logical Trader*, is a powerful methodology for identifying high-probability trade setups based on the market's opening range (OR). This indicator automates Layers 1 and 2 of the ACD strategy, helping you spot breakout opportunities, trend direction, and key support/resistance levels. Perfect for day traders, scalpers, and swing traders in forex, stocks, futures, or crypto.

**How It Works**

1. **Opening Range (OR)**: Calculated from the high/low of the first X minutes (default: 30-60 min) of major sessions (e.g., Tokyo, London, New York).

2. **A Levels**: Drawn at a percentage (default: 0.5% of OR range or ATR-based) above/below the OR. A breakout above A-Up signals a bullish setup; below A-Down signals bearish.

3. **C Levels**: Wider levels (default: 1-2% or ATR multiplier) for stronger confirmation. Breakouts here confirm trend strength and filter fakeouts.

4. **Pivot Ranges**: Includes daily and N-day pivots to gauge overall market bias (above pivots = bullish; below = bearish).

**Key Features**

- **Customizable Sessions**: Tokyo (00:00-01:00 GMT), London (08:00-09:00 GMT), New York (13:30-14:30 GMT) – adjustable.

- **ATR Integration**: Uses Average True Range for dynamic A/C levels (period: 14 by default).

- **Visual Alerts**: Color-coded lines (green for bullish, red for bearish) + optional labels for breakouts.

- **Pivot Display**: Show/hide daily or multi-day pivots with customizable colors.

- **Risk Management**: Built-in stop-loss suggestions based on OR width.

**Trading Rules**

- **Bullish Setup**: Price breaks and holds above A-Up → Enter long at C-Up confirmation. Target: Next pivot or 1:2 risk-reward.

- **Bearish Setup**: Price breaks below A-Down → Enter short at C-Down.

- **Avoid Fakeouts**: Wait for stabilization (e.g., close above/below level).

- **Trend Filter**: Combine with PMA (Pivot Moving Average) for Layer 3 confirmation (search "ACD PMA" in TradingView).

**Settings Guide**

- **OR Timeframe**: Session start time and duration (e.g., 30 min).

- **A Multiplier (%)**: Distance for A levels (default: 0.5).

- **C Multiplier (%)**: Distance for C levels (default: 1.0).

- **ATR Period**: For volatility-based levels (default: 14).

- **Show Pivots**: Toggle daily/N-day ranges.

This indicator balances supply/demand by analyzing volume and price action within the opening range. Backtest on your favorite pairs (e.g., EURUSD, BTCUSD) and adjust for your style. Not financial advice – always use proper risk management!

**Inspired by**: Mark Fisher's ACD Methodology. Open-source for community review. Questions? Comment below!

#ACD #OpeningRange #Breakout #DayTrading #FisherStrategy

Keks Key Level Fx SessionsThis script is designed to automatically plot and manage key levels for the major FX trading sessions (London, New York, and Asia). It helps traders identify the most relevant price areas that often act as support, resistance, or breakout zones during active market hours.

Key features:

Marks session highs, lows, and midpoints

Visualizes key intraday levels for better market structure analysis

Highlights potential breakout and retest areas

Works across multiple timeframes for flexibility

Clean and minimal chart design to avoid clutter

This tool is especially useful for traders who rely on session-based strategies, such as breakout trading, retests, or range trading, by providing a clear visual guide to the most important price zones.

Asian & London Session High/LowThis Pine Script v6 indicator plots the high and low of the Asian and London trading sessions on the chart before the New York session opens.

Asian session is defined from 00:00 to 08:00 (Europe/Sofia time).

London session is defined from 09:00 to 16:30 (Europe/Sofia time).

The session highs and lows are tracked live and updated as new candles form within the session time ranges.

At 16:30, when the New York session opens, all high/low values are reset to na to prepare for the next day.

Horizontal lines are plotted using plot.style_linebr to extend the lines until the next candle.

This tool helps traders identify key support/resistance zones formed during the most active pre-New York hours.