Outside Candle Session Breakout [CHE]Outside Candle Session Breakout

Session - anchored HTF levels for clear market-structure and precise breakout context

Summary

This indicator is a relevant market-structure tool. It anchors the session to the first higher-timeframe bar, then activates only when the second bar forms an outside condition. Price frequently reacts around these anchors, which provides precise breakout context and a clear overview on both lower and higher timeframes. Robustness comes from close-based validation, an adaptive volatility and tick buffer, first-touch enforcement, optional retest, one-signal-per-session, cooldown, and an optional trend filter.

Pine version: v6. Overlay: true.

Motivation: Why this design?

Short-term breakout tools often trigger during noise, duplicate within the same session, or drift when volatility shifts. The core idea is to gate signals behind a meaningful structure event: a first-bar anchor and a subsequent outside bar on the session timeframe. This narrows attention to structurally important breaks while adaptive buffering and debouncing reduce false or mid-run triggers.

What’s different vs. standard approaches?

Baseline: Simple high-low breaks or fixed buffers without session context.

Architecture: Session-anchored first-bar high/low; outside-bar gate; close-based confirmation with an adaptive ATR and tick buffer; first-touch enforcement; optional retest window; one-signal-per-session and cooldown; optional EMA trend and slope filter; higher-timeframe aggregation with lookahead disabled; themeable visuals and a range fill between levels.

Practical effect: Cleaner timing at structurally relevant levels, fewer redundant or late triggers, and better multi-timeframe situational awareness.

How it works (technical)

The chart timeframe is mapped to an analysis timeframe and a session timeframe.

The first session bar defines the anchor high and low. The setup becomes active only after the next bar forms an outside range relative to that first bar.

While active, the script tracks these anchors and checks for a breakout beyond a buffered threshold, using closing prices or wicks by preference.

The buffer scales with volatility and is limited by a minimum tick floor. First-touch enforcement avoids mid-run confirmations.

Optional retest requires a pullback to the raw anchor followed by a new close beyond the buffered level within a user window.

Optional trend gating uses an EMA on the analysis timeframe, including an optional slope requirement and price-location check.

Higher-timeframe data is requested with lookahead disabled. Values can update during a forming higher-timeframe bar; waiting and confirmation mitigate timing shifts.

Parameter Guide

Enable Long / Enable Short — Direction toggles. Default: true / true. Reduces unwanted side.

Wait Candles — Minimum bars after outside confirmation before entries. Default: five. More waiting increases stability.

Close-based Breakout — Confirm on candle close beyond buffer. Default: true. For wick sensitivity, disable.

ATR Buffer — Enables adaptive volatility buffer. Default: true.

ATR Multiplier — Buffer scaling. Default: zero point two. Increase to reduce noise.

Ticks Buffer — Minimum buffer in ticks. Default: two. Protects in quiet markets.

Cooldown Bars — Blocks new signals after a trigger. Default: three.

One Signal per Session — Prevents duplicates within a session. Default: true.

Require Retest — Pullback to raw anchor before confirming. Default: false.

Retest Window — Bars allowed for retest completion. Default: five.

HTF Trend Filter — EMA-based gating. Default: false.

EMA Length — EMA period. Default: two hundred.

Slope — Require EMA slope direction. Default: true.

Price Above/Below EMA — Require price location relative to EMA. Default: true.

Show Levels / Highlight Session / Show Signals — Visual controls. Default: true.

Color Theme — “Blue-Green” (default), “Monochrome”, “Earth Tones”, “Classic”, “Dark”.

Time Period Box — Visibility, size, position, and colors for the info box. (Optional)

Reading & Interpretation

The two level lines represent the session’s first-bar high and low. The filled band illustrates the active session range.

“OUT” marks that the outside condition is confirmed and the setup is live.

“LONG” or “SHORT” appears only when the breakout clears buffer, debounce, and optional gates.

Background tint indicates sessions where the setup is valid.

Alerts fire on confirmed long or short breakout events.

Practical Workflows & Combinations

Trend-following: Keep close-based validation, ATR buffer near the default, one-signal-per-session enabled; add EMA trend and slope for directional bias.

Retest confirmation: Enable retest with a short window to prioritize cleaner continuation after a pullback.

Lower-timeframe scalping: Reduce waiting and cooldown slightly; keep a small tick buffer to filter micro-whips.

Swing and position context: Increase ATR multiplier and waiting; maintain once-per-session to limit duplicates.

Timeframe Tiers and Trader Profiles

The script adapts its internal mapping based on the chart timeframe:

Under fifteen minutes → Analysis: one minute; Session: sixty minutes. Useful for scalpers and high-frequency intraday reads.

Between fifteen and under sixty minutes → Analysis: fifteen minutes; Session: one day. Suits day traders who need intraday alignment to the daily session.

Between sixty minutes and under one day → Analysis: sixty minutes; Session: one week. Serves intraday-to-swing transitions and end-of-day planning.

Between one day and under one week → Analysis: two hundred forty minutes; Session: two weeks. Fits swing traders who monitor multi-day structure.

Between one week and under thirty days → Analysis: one day; Session: three months. Supports position traders seeking quarterly context.

Thirty days and above → Analysis: one day; Session: twelve months. Provides a broad annual anchor for macro context.

These tiers are designed to keep anchors meaningful across regimes while preserving responsiveness appropriate to the trader profile.

Behavior, Constraints & Performance

Signals can be validated on closed bars through close-based logic; enabling this reduces intrabar flicker.

Higher-timeframe values may evolve during a forming bar; waiting parameters and the outside-bar gate reduce, but do not remove, this effect.

Resource footprint is light; the script uses standard indicators and a single higher-timeframe request per stream.

Known limits: rare setups during very quiet periods, sensitivity to gaps, and reduced reliability on illiquid symbols.

Sensible Defaults & Quick Tuning

Start with close-based validation on, ATR buffer on with a multiplier near zero point two, tick buffer two, cooldown three, once-per-session on.

Too many flips: increase the ATR multiplier and cooldown; consider enabling the EMA filter and slope.

Too sluggish: reduce the ATR multiplier and waiting; disable retest.

Choppy conditions: keep close-based validation, increase tick buffer, shorten the retest window.

What this indicator is—and isn’t

This is a visualization and signal layer for session-anchored breakouts with stability gates. It is not a complete trading system, risk framework, or predictive engine. Combine it with structured analysis, position sizing, and disciplined risk controls.

Disclaimer

The content provided, including all code and materials, is strictly for educational and informational purposes only. It is not intended as, and should not be interpreted as, financial advice, a recommendation to buy or sell any financial instrument, or an offer of any financial product or service. All strategies, tools, and examples discussed are provided for illustrative purposes to demonstrate coding techniques and the functionality of Pine Script within a trading context.

Any results from strategies or tools provided are hypothetical, and past performance is not indicative of future results. Trading and investing involve high risk, including the potential loss of principal, and may not be suitable for all individuals. Before making any trading decisions, please consult with a qualified financial professional to understand the risks involved.

By using this script, you acknowledge and agree that any trading decisions are made solely at your discretion and risk.

Do not use this indicator on Heikin-Ashi, Renko, Kagi, Point-and-Figure, or Range charts, as these chart types can produce unrealistic results for signal markers and alerts.

Best regards and happy trading

Chervolino

"scalping" için komut dosyalarını ara

Digital RPM HUD — 4 Feeds + Confidence + Timeline (v3)🏎️ Digital RPM HUD — 4 Feeds + Confidence + Timeline (v3)

A performance-style trading dashboard for momentum-driven traders.

The Digital RPM HUD gives you an instant visual readout of market “engine speed” — combining four customizable data feeds (Trend, Momentum, Volume, Volatility) into a single confidence score (0–100) and a color-coded timeline of regime changes.

Think of it as a racing-inspired control panel: you only “hit the throttle” when confidence is high and all systems agree.

🔧 Key Features

4 Data Feeds – assign your own logic (EMA, RSI, RVOL, ATR, etc.).

Confidence Meter – blends the four feeds into one smooth 0–100 reading.

Timeline Strip – shows recent bullish / bearish / neutral states at a glance.

Visual Trade Cues – optional on-chart LONG / SHORT / EXIT markers.

Fully Customizable – thresholds, weights, smoothing, colors, layout.

HUD Overlay – clean, minimal, and adjustable to any corner of your chart.

💡 How to Use

Configure each feed to reflect your preferred signals (e.g., trend EMA 200, momentum RSI 14, volume RVOL 20, volatility ATR 14).

Watch the Confidence gauge:

✅ Above Bull Threshold → Market acceleration / long bias.

❌ Below Bear Threshold → Momentum loss / short bias.

⚪ Between thresholds → Neutral zone; stay patient.

Use the Timeline to confirm trend consistency — more green = bullish regime, more red = bearish.

⚙️ Recommended Setups

Scalping: Trend EMA 50 + RSI 7 + RVOL 10 + ATR 7 → Fast response.

Intraday: EMA 200 + RSI 14 + RVOL 20 + ATR 14 → Balanced signal.

Swing: Multi-TF Trend + MACD + RVOL + ATR → Smooth and steady.

⚠️ Disclaimer

This script is not a trading strategy and does not execute trades.

All signals are visual aids — always confirm with your own analysis and risk management.

RAF@SSET POWER-7 MA SuiteWhat it is

A clean, lightweight pack of seven moving averages (1m, 5m, 15m, 1H, 4H, 1D, 1W).

HTF lines are confirmed-only (no intra-bar wiggle), so what you see is what closed—no repaint on HTFs. Use it to anchor scalps to higher-timeframe structure without clutter.

Why you’ll like it

1m→1W in one look – see alignment from scalp to swing.

Confirmed HTFs – uses request.security() with lookahead_off and only plots closed values.

Zero fluff – just MAs, fixed colors, ultra-fast.

Your presets – default to my “Power-7” lengths (e.g., 233) or set your own.

SMA/EMA switch – pick your poison globally.

Inputs

Show/hide: 1m, 5m, 15m, 1H, 4H, 1D, 1W

Length per TF (defaults 233)

MA type: SMA / EMA

Color per TF

How it works (short)

Current-TF MA updates live.

Higher TF MAs (5m, 15m, 1H, 4H/“240”, 1D, 1W) only update when their candle closes. That removes “wiggle” and surprise shifts.

Tips

For scalping: trade off LTF, bias from 1H/4H/1D.

For swing: let 1D/1W set bias; use 1H/4H for timing.

Your current chart TF MA is live (by design). If you want it confirmed too, set your chart to the HTF you care about.

Built from my RAF@SSET workflow. Shoutout to everyone who keeps indicators simple and readable.

v1.0: First public release (Pine v6). Seven MAs (1m→1W), confirmed HTFs, fixed colors, SMA/EMA toggle.

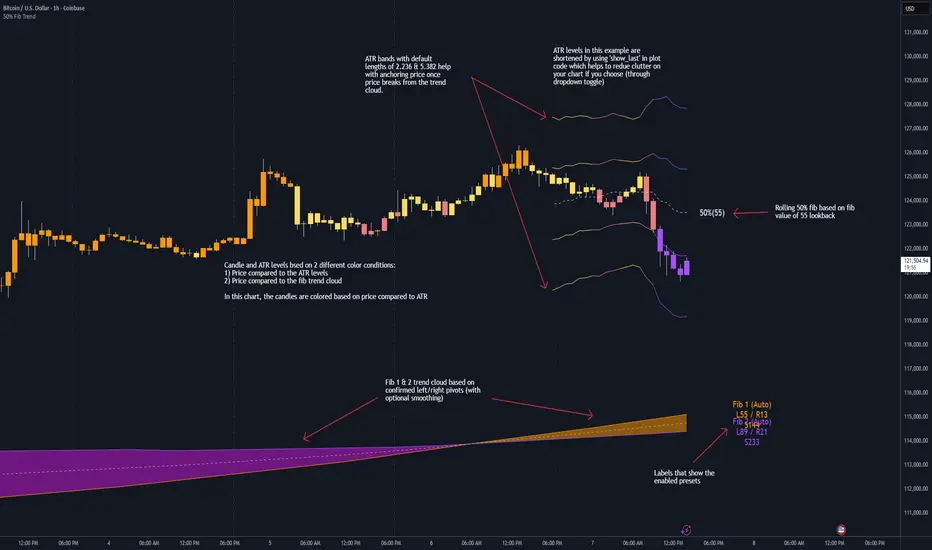

50% Fib Trend Cloud + ATR BandsThis indicator plots two structural 50% fibonacci midpoints from recent confirmed 'left/right' swings that form a *cloud* of equilibrium, then adds a rolling 50% fibonacci range midpoint based on a lookback window that's wrapped in ATR bands. Importantly, it solves a specific trading problem:

Structural midpoints (macro context) are powerful but can lag when price escapes prior ranges. Enter rolling 50% fib + ATR ➡️ which restores real-time balance & tolerance (micro context). Together they show where price is balanced structurally, where it’s balanced right now, and how much volatility to tolerate before acting.

➖➖➖

🔑 Why this is different

Most tools either draw a single midpoint (ex., daily 50%) or ATR bands around a moving average. This script fuses dual swing-based 50% midpoints (structure) + a rolling 50% with ATR (flow), so you don’t lose context when price escapes prior ranges. The cloud tells you who’s in control (fast vs. slow structure). The rolling 50% + ATR tells you how far is “too far” now.

➖➖➖

🧠 What it does (at a glance)

🔸Structural Equilibrium × 2 (Fib1/Fib2)

Two independent 50% midpoints formed from swing pivots (configurable Left/Right bars + optional smoothing). Their gap is the Midpoint Cloud = structural “fair value” zone.

🔸Rolling 50% + ATR Bands

A rolling highest/lowest window computes an always-current 50% rolling midpoint plot; ±ATR × length envelopes define a soft value area and over-stretch boundaries.

🔸Actionable Visuals

Optional fill between Fib1/Fib2, labels, and candle-overlay modes to instantly read regime (above both / below both / between).

🔸Smart Defaults

Timeframe-aware presets for L/R pivots & smoothing; full manual overrides available.

➖➖➖

⚙️ Calculations (plain-English)

🔸Pivot midpoints (Fib1 & Fib2):

1) Detect a swing using `Left/Right` bars

2) Take the swing’s high/low → compute 50%

3) (Optional) Smooth the line (SMA) to stabilize on noisy TFs

4) Repeat with a different sensitivity to get two distinct midpoints

🔸Rolling midpoint:

Highest High / Lowest Low over the last *N* bars → (HH + LL) / 2

🔸ATR levels:

`Upper = Rolling50 + ATR × Mult`, `Lower = Rolling50 − ATR × Mult`

(Typical: ATR length 14–21; Multipliers 2.236 for L1, 5.382 for L2)

➖➖➖

🤖 Auto-Configured Presets (with Manual Override)

💡Goal: make the midpoints “just work” on common timeframes while still letting you dial them in.

💡How Auto Presets work

When Auto Presets = ON, the script picks sensible L/R/S (Left bars / Right bars / Smoothing) for Fib Trend 1 and Fib Trend 2 based on chart timeframe.

🔸Fib 1 (fast) emphasizes *micro-structure* for quicker bias shifts.

🔸Fib 2 (slow) emphasizes *macro-structure* for anchor/bias context.

These defaults keep Fib 1 responsive without jitter and Fib 2 stable without lag.

➡️ Turn Auto Presets = OFF to take full control with the manual inputs described below.

➖➖➖

🛠 Manual Fib Midpoint Settings (when Auto = OFF)

💡Each midpoint uses three knobs:

🔸Pivot Left (L): bars to the left that must be lower/higher to qualify a swing

🔸Pivot Right (R): bars to the right that must be lower/higher to confirm the swing

🔸Smoothing (S): SMA period applied to the raw 50% midpoint (stabilizes noise)

5-Minute optimized defaults

🔸Fib Trend 1: `L21 / R5 / S55` → responsive local structure (entries/exits, re-balancing zones)

🔸Fib Trend 2: `L55 / R13 / S89` → broader structure (trend context, anchors/stops)

Timeframe guidance

🔸1m–3m: may feel a touch laggy → consider ~`L13 / R3 / S34`

🔸15m–1h: defaults remain strong → optionally ~`L34 / R8 / S89`

🔸4h+ : increase span for stability → `L89–144 / R13–21 / S144–233`

➡️ Rule of thumb: shorter L/R = faster detection, longer S = smoother line. Tune until Fib 1 captures the “active swing” and Fib 2 captures the “dominant swing” without whipsaw.

➖➖➖

🎛 Inputs (quick reference)

🔸Fib Trend 1/2: Source (High/Low/Close), Left/Right bars, Smoothing length, Show/Hide, Cloud fill toggle

🔸Rolling 50%: Lookback length, Price basis (Wicks/Close/HLC3/OHLC4), Plot scope (Full / Last N / None)

🔸ATR Bands: ATR length, Multipliers (L1/L2), Plot scope, Line width/colors

🔸Overlay & Labels: Candle overlay mode, Label padding/size, 50% centerline toggle, Plot widths

➖➖➖

🖍️ Candle Coloring & Overlay Modes

💡Purpose: make trend instantly visible on the candles and ATR levels.

1) Color Logic (dropdown)

🔸 Fib Midpoints — Colors by position of price vs. Fib 1 & Fib 2

🔸ATR Zones — Colors by which ATR zone price is in relative to the Rolling 50%

➡️ Price Reference: Choose the input used for the decision (Close, HL2, OHLC3, OHLC4).

➡️Tip: Close is crisp; HL2/OHLC variants are smoother.

2) Overlay Style (dropdown)

🔸 None — No visual change to candles

🔸 Bar Color — Uses `barcolor()` to tint built-in candles (this takes into account your Trading View settings, for instance if you have wicks set to white, they will show up as white with this setting)

🔸 PlotCandles — Draws unified custom candles (body, wick, border) with the same color for maximum clarity

💡Practical use

🔸 Pick Fib Midpoints to read structural bias at a glance (above/below/between the cloud).

🔸 Pick ATR Zones to read value vs. stretch around the Rolling 50% (mean-reversion vs. trend extension).

➖➖➖

📘 How to use

A) Trend confirmation

- Strong bullish bias when price holds above both structural mids; strong bearish when below both.

- Use the Rolling 50% + ATR as a dynamic re-entry zone: pullbacks that respect ATR(L1) often continue the prevailing trend.

B) Transition / mean reversion

- Inside the Cloud (between Fib1 & Fib2) treat behavior as neutralization/re-balancing; range tactics tend to outperform momentum plays.

- In ranges, fades near ±ATR around the rolling 50% can mark short-term edges.

C) Breakout context

- When price leaves the Cloud, the Rolling 50% keeps you anchored so price never feels “floating.” A clean hold outside ATR(L1/L2) suggests regime strength; quick re-entries hint at traps.

➖➖➖

🖼 Chart examples

➡️ Each snapshot shows how the Cloud (structure) and the Rolling 50% + ATR (flow) work together.

1) 1-Minute Downtrend – Cloud as Dynamic Ceiling

- The Cloud slopes down; pullbacks repeatedly fail under the Cloud’s underside.

- Rolling 50% (dashed mid) + ATR(L1) act as a reversion band: rallies stall near upper ATR and rotate lower.

2) 15-Minute Persistent Drift – Structure Guides, Flow Times Entries

- Long drift lower with Cloud overhead.

- Consolidations near the rolling mid resolve in the trend direction; ATR bands frame risk on each attempt.

3) 15-Minute Uptrend (BTC) – From Cloud Escape to Value Stair-Step

- After escaping the prior Cloud, rolling 50% + ATR establish a new higher value area.

- Pullbacks into ATR(L1) produce orderly stair-steps; Cloud remains supportive on deeper dips

4) 5-Minute BTC – Pullback to Value then Rotate

- Strong leg up; retrace tags lower ATR band and rotates back toward the rolling mid.

- Labels (Fib1/Fib2) make the structural context explicit for decision-making.

➖➖➖

🧪 Starter presets

- Intraday (5–15m): Fib1 ~ L21/R5 (smooth 5), Fib2 ~ L55/R13 (smooth 9) • Rolling = 55 • ATR = 14 • L1 = 2.5x, L2 = 5.0x

- Scalping: Shorten lookbacks & smoothing; keep ATR multipliers similar, or tighten L1.

- Swing: Lengthen all lookbacks; consider ATR length 21–28.

➖➖➖

🏁Final Word

This script is not just a visual tool, it’s a complete trend and structure framework. Whether you're looking for clean trend alignment, dynamic support/resistance, or early warning signs of a reversal, this system is tuned to help you react with confidence — not hindsight.

Rembember, no single indicator should be used in isolation. For best results, combine it with price action analysis, higher-timeframe context, and complementary tools like trendlines, moving averages etc Use it as part of a well-rounded trading approach to confirm setups — not to define them alone.

---

💡Turn logic into clarity. Structure into trades. And uncertainty into confidence.

Trend Fib Zone Bounce (TFZB) [KedArc Quant]Description:

Trend Fib Zone Bounce (TFZB) trades with the latest confirmed Supply/Demand zone using a single, configurable Fib pullback (0.3/0.5/0.6). Trade only in the direction of the most recent zone and use a single, configurable fib level for pullback entries.

• Detects market structure via confirmed swing highs/lows using a rolling window.

• Draws Supply/Demand zones (bearish/bullish rectangles) from the latest MSS (CHOCH or BOS) event.

• Computes intra zone Fib guide rails and keeps them extended in real time.

• Triggers BUY only inside bullish zones and SELL only inside bearish zones when price touches the selected fib and closes back beyond it (bounce confirmation).

• Optional labels print BULL/BEAR + fib next to the triangle markers.

What it does

Finds structure using confirmed swing highs/lows (you choose the confirmation length).

Builds the latest zone (bullish = demand, bearish = supply) after a CHOCH/BOS event.

Draws intra-zone “guide rails” (Fib lines) and extends them live.

Signals only with the trend of that zone:

BUY inside a bullish zone when price tags the selected Fib and closes back above it.

SELL inside a bearish zone when price tags the selected Fib and closes back below it.

Optional labels print BULL/BEAR + Fib next to triangles for quick context

Why this is different

Most “zone + fib + signal” tools bolt together several indicators, or fire counter-trend signals because they don’t fully respect structure. TFZB is intentionally minimal:

Single bias source: the latest confirmed zone defines direction; nothing else overrides it.

Single entry rule: one Fib bounce (0.3/0.5/0.6 selectable) inside that zone—no counter-trend trades by design.

Clean visuals: you can show only the most recent zone, clamp overlap, and keep just the rails that matter.

Deterministic & transparent: every plot/label comes from the code you see—no external series or hidden smoothing

How it helps traders

Cuts decision noise: you always know the bias and the only entry that matters right now.

Forces discipline: if price isn’t inside the active zone, you don’t trade.

Adapts to volatility: pick 0.3 in strong trends, 0.5 as the default, 0.6 in chop.

Non-repainting zones: swings are confirmed after Structure Length bars, then used to build zones that extend forward (they don’t “teleport” later)

How it works (details)

*Structure confirmation

A swing high/low is only confirmed after Structure Length bars have elapsed; the dot is plotted back on the original bar using offset. Expect a confirmation delay of about Structure Length × timeframe.

*Zone creation

After a CHOCH/BOS (momentum shift / break of prior swing), TFZB draws the new Supply/Demand zone from the swing anchors and sets it active.

*Fib guide rails

Inside the active zone TFZB projects up to five Fib lines (defaults: 0.3 / 0.5 / 0.7) and extends them as time passes.

*Entry logic (with-trend only)

BUY: bar’s low ≤ fib and close > fib inside a bullish zone.

SELL: bar’s high ≥ fib and close < fib inside a bearish zone.

*Optionally restrict to one signal per zone to avoid over-trading.

(Optional) Aggressive confirm-bar entry

When do the swing dots print?

* The code confirms a swing only after `structureLen` bars have elapsed since that candidate high/low.

* On a 5-min chart with `structureLen = 10`, that’s about 50 minutes later.

* When the swing confirms, the script plots the dot back on the original bar (via `offset = -structureLen`). So you *see* the dot on the old bar, but it only appears on the chart once the confirming bar arrives.

> Practical takeaway: expect swing markers to appear roughly `structureLen × timeframe` later. Zones and signals are built from those confirmed swings.

Best timeframe for this Indicator

Use the timeframe that matches your holding period and the noise level of the instrument:

* Intraday :

* 5m or 15m are the sweet spots.

* Suggested `structureLen`:

* 5m: 10–14 (confirmation delay \~50–70 min)

* 15m: 8–10 (confirmation delay \~2–2.5 hours)

* Keep Entry Fib at 0.5 to start; try 0.3 in strong trends, 0.6 in chop.

* Tip: avoid the first 10–15 minutes after the open; let the initial volatility set the early structure.

* Swing/overnight:

* 1h or 4h.

* `structureLen`:

* 1h: 6–10 (6–10 hours confirmation)

* 4h: 5–8 (20–32 hours confirmation)

* 1m scalping: not recommended here—the confirmation lag relative to the noise makes zones less reliable.

Inputs (all groups)

Structure

• Show Swing Points (structureTog)

o Plots small dots on the bar where a swing point is confirmed (offset back by Structure Length).

• Structure Length (structureLen)

o Lookback used to confirm swing highs/lows and determine local structure. Higher = fewer, stronger swings; lower = more reactive.

Zones

• Show Last (zoneDispNum)

o Maximum number of zones kept on the chart when Display All Zones is off.

• Display All Zones (dispAll)

o If on, ignores Show Last and keeps all zones/levels.

• Zone Display (zoneFilter): Bullish Only / Bearish Only / Both

o Filters which zone types are drawn and eligible for signals.

• Clean Up Level Overlap (noOverlap)

o Prevents fib lines from overlapping when a new zone starts near the previous one (clamps line start/end times for readability).

Fib Levels

Each row controls whether a fib is drawn and how it looks:

• Toggle (f1Tog…f5Tog): Show/hide a given fib line.

• Level (f1Lvl…f5Lvl): Numeric ratio in . Defaults active: 0.3, 0.5, 0.7 (0 and 1 off by default).

• Line Style (f1Style…f5Style): Solid / Dashed / Dotted.

• Bull/Bear Colors (f#BullColor, f#BearColor): Per-fib color in bullish vs bearish zones.

Style

• Structure Color: Dot color for confirmed swing points.

• Bullish Zone Color / Bearish Zone Color: Rectangle fills (transparent by default).

Signals

• Entry Fib for Signals (entryFibSel): Choose 0.3, 0.5 (default), or 0.6 as the trigger line.

• Show Buy/Sell Signals (showSignals): Toggles triangle markers on/off.

• One Signal Per Zone (oneSignalPerZone): If on, suppresses additional entries within the same zone after the first trigger.

• Show Signal Text Labels (Bull/Bear + Fib) (showSignalLabels): Adds a small label next to each triangle showing zone bias and the fib used (e.g., BULL 0.5 or BEAR 0.3).

How TFZB decides signals

With trend only:

• BUY

1. Latest active zone is bullish.

2. Current bar’s close is inside the zone (between top and bottom).

3. The bar’s low ≤ selected fib and it closes > selected fib (bounce).

• SELL

1. Latest active zone is bearish.

2. Current bar’s close is inside the zone.

3. The bar’s high ≥ selected fib and it closes < selected fib.

Markers & labels

• BUY: triangle up below the bar; optional label “BULL 0.x” above it.

• SELL: triangle down above the bar; optional label “BEAR 0.x” below it.

Right-Panel Swing Log (Table)

What it is

A compact, auto-updating log of the most recent Swing High/Low events, printed in the top-right of the chart.

It helps you see when a pivot formed, when it was confirmed, and at what price—so you know the earliest bar a zone-based signal could have appeared.

Columns

Type – Swing High or Swing Low.

Date – Calendar date of the swing bar (follows the chart’s timezone).

Swing @ – Time of the original swing bar (where the dot is drawn).

Confirm @ – Time of the bar that confirmed that swing (≈ Structure Length × timeframe after the swing). This is also the earliest moment a new zone/entry can be considered.

Price – The swing price (high for SH, low for SL).

Why it’s useful

Clarity on repaint/confirmation: shows the natural delay between a swing forming and being usable—no guessing.

Planning & journaling: quick reference of today’s pivots and prices for notes/backtesting.

Scanning intraday: glance to see if you already have a confirmed zone (and therefore valid fib-bounce entries), or if you’re still waiting.

Context for signals: if a fib-bounce triangle appears before the time listed in Confirm @, it’s not a valid trade (you were too early).

Settings (Inputs → Logging)

Log swing times / Show table – turn the table on/off.

Rows to keep – how many recent entries to display.

Show labels on swing bar – optional tags on the chart (“Swing High 11:45”, “Confirm SH 14:15”) that match the table.

Recommended defaults

• Structure Length: 10–20 for intraday; 20–40 for swing.

• Entry Fib for Signals: 0.5 to start; try 0.3 in stronger trends and 0.6 in choppier markets.

• One Signal Per Zone: ON (prevents over trading).

• Zone Display: Both.

• Fib Lines: Keep 0.3/0.5/0.7 on; turn on 0 and 1 only if you need anchors.

Alerts

Two alert conditions are available:

• BUY signal – fires when a with trend bullish bounce at the selected fib occurs inside a bullish zone.

• SELL signal – fires when a with trend bearish bounce at the selected fib occurs inside a bearish zone.

Create alerts from the chart’s Alerts panel and select the desired condition. Use Once Per Bar Close to avoid intrabar flicker.

Notes & tips

• Swing dots are confirmed only after Structure Length bars, so they plot back in time; zones built from these confirmed swings do not repaint (though they extend as new bars form).

• If you don’t see a BUY where you expect one, check: (1) Is the active zone bullish? (2) Did the candle’s low actually pierce the selected fib and close above it? (3) Is One Signal Per Zone suppressing a second entry?

• You can hide visual clutter by reducing Show Last to 1–3 while keeping Display All Zones off.

Glossary

• CHOCH (Change of Character): A shift where price breaks beyond the last opposite swing while local momentum flips.

• BOS (Break of Structure): A cleaner break beyond the prior swing level in the current momentum direction.

• MSS: Either CHOCH or BOS – any event that spawns a new zone.

Extension ideas (optional)

• Add fib extensions (1.272 / 1.618) for target lines.

• Zone quality score using ATR normalization to filter weak impulses.

• HTF filter to only accept zones aligned with a higher timeframe trend.

⚠️ Disclaimer This script is provided for educational purposes only.

Past performance does not guarantee future results.

Trading involves risk, and users should exercise caution and use proper risk management when applying this strategy.

VWAP Momentum Oscillator How It Works

Core Calculation Method

The oscillator combines four key market measurements into a single, normalized reading:

1. Price-VWAP Deviation: `(Close - VWAP) / VWAP × 100`

2. VWAP-MA Momentum: `(VWAP - MovingAverage) / MovingAverage × 100`

3. Anchored VWAP Strength: Average of high/low anchor deviations from rolling VWAP

4. Range Position: `(Close - PeriodLow) / (PeriodHigh - PeriodLow) × 100 - 50`

Dynamic Signal Line

The signal line uses an EMA that automatically adjusts its length based on your chart timeframe:

- Futures: Always covers 23 hours of trading (1,380 minutes)

- Stocks: Always covers 6.5 hours of trading (390 minutes)

- Examples: 276 periods on 5-min futures chart, 1,380 periods on 1-min futures chart

Trading Signals

🟢 Buy Signals

- Condition: Main oscillator crosses above signal line while below zero

- Logic: Momentum turning bullish from oversold conditions

- Visual: Green "BUY" label below price action

🔴 Sell Signals

- Condition: Main oscillator crosses below signal line while above zero

- Logic: Momentum turning bearish from overbought conditions

- Visual: Red "SELL" label above price action

⚠️ Extreme Warnings

- Extreme Overbought: Red triangle when oscillator crosses above +4.0

- Extreme Oversold: Green triangle when oscillator crosses below -4.0

- Purpose: Risk management alerts, not entry/exit signals

Oscillator Zones

Interpretation Guide

- Above +2.0: Strong bullish momentum zone (green background)

- 0 to +2.0: Mild bullish territory

- 0 to -2.0: Mild bearish territory

- Below -2.0: Strong bearish momentum zone (red background)

- Above +4.0: Extreme overbought (caution advised)

- Below -4.0: Extreme oversold (potential reversal zone)

Customization Options

Moving Average Settings

- EMA/SMA Toggle: Choose between exponential or simple moving average

- Color Customization: Adjust MA line color and width

Visual Controls

- Bullish/Bearish Colors: Customize momentum zone colors

- Signal Line: Toggle visibility and adjust color

- Line Widths: Control thickness of all plot lines

Anchor Modes

- NY Session Only: Anchors reset at NY market open (9:30 AM ET)

- 24H NY Day: Anchors reset at NY calendar day change (midnight ET)

Best Practices

Timeframe Selection

- Scalping: 1-5 minute charts for quick momentum changes

- Day Trading: 5-15 minute charts for clearer trend signals

- Swing Trading: 1-4 hour charts for major momentum shifts

Signal Confirmation

- Wait for crossovers: Don't trade on oscillator position alone

- Respect extreme levels: Exercise caution above +4 or below -4

- Use with price action: Combine with support/resistance levels

Risk Management

- Extreme zones: Reduce position size when oscillator is extended

- Failed signals: Exit quickly if momentum doesn't follow through

- Market context: Consider overall trend direction and market volatility

Technical Specifications

Calculation Components

- Base Length: 1,380 periods (futures) / 390 periods (stocks)

- Signal Line: Dynamic EMA covering one full trading day

- Smoothing: 3-period SMA on raw oscillator (adjustable)

- Update Frequency: Real-time on every price tick

Performance Notes

- Resource Efficient: Optimized calculations minimize CPU usage

- Memory Friendly: Uses incremental VWAP calculations

- Fast Loading: Minimal historical data requirements

Version History & Development

This oscillator evolved from advanced VWAP overlay strategies, transforming complex multi-line analysis into a single, actionable momentum gauge. The indicator maintains the sophistication of institutional VWAP analysis while providing the clarity needed for retail trading decisions.

Core Philosophy

Traditional VWAP indicators show where price is relative to volume-weighted averages, but they don't quantify momentum or provide clear entry/exit signals. This oscillator solves that problem by normalizing all VWAP relationships into a single, bounded indicator that works consistently across all timeframes and asset classes.

---

Open Source License: This indicator is provided free for the TradingView community. Feel free to modify and enhance according to your trading needs.

Enhanced Chande Momentum OscillatorEnhanced Chande Momentum Oscillator (Enh CMO)

📊 Description

The Enhanced Chande Momentum Oscillator is an advanced version of the classic Chande Momentum Oscillator with dynamic envelope boundaries that automatically adapt to market volatility. This indicator provides clear visual signals for potential price reversals and momentum shifts.

Key Features:

Original Chande Momentum Oscillator calculation

Dynamic upper and lower boundaries based on statistical analysis

Adaptive envelope that adjusts to market volatility

Visual fill area between boundaries for easy interpretation

Real-time values table with current readings

Built-in alert conditions for boundary touches

Customizable moving average types (SMA, EMA, WMA)

⚙️ Settings

CMO Settings:

CMO Length (9): Period for calculating the base Chande Momentum Oscillator

Source (close): Price source for calculations

Envelope Settings:

Envelope Length (20): Lookback period for calculating the moving average and standard deviation

Envelope Multiplier (1.5): Multiplier for standard deviation to create upper/lower bounds

Moving Average Type (EMA): Type of moving average for envelope calculation

📈 How to Use

Visual Elements

Lines:

White Line: Main Chande Momentum Oscillator

Red Line: Upper boundary (resistance level)

Green Line: Lower boundary (support level)

Yellow Line: Moving average of CMO (trend direction)

Purple Fill: Visual envelope between boundaries

Reference Lines:

Zero Line: Neutral momentum level

+50/-50 Lines: Traditional overbought/oversold levels

Trading Signals

🔴 Sell/Short Signals

CMO touches or crosses above upper boundary → Potential bearish reversal

CMO is above +50 and declining → Weakening bullish momentum

CMO crosses below yellow MA line while above zero → Momentum shift

🟢 Buy/Long Signals

CMO touches or crosses below lower boundary → Potential bullish reversal

CMO is below -50 and rising → Weakening bearish momentum

CMO crosses above yellow MA line while below zero → Momentum shift

⚡ Advanced Signals

Boundary contraction → Decreasing volatility, potential breakout coming

Boundary expansion → High volatility period, use wider stops

CMO hugging upper boundary → Strong uptrend continuation

CMO hugging lower boundary → Strong downtrend continuation

🎯 Trading Strategies

Strategy 1: Reversal Trading

Wait for CMO to touch extreme boundaries (red or green lines)

Look for divergence with price action

Enter counter-trend position when CMO starts moving back toward center

Set stop beyond the boundary breach point

Take profit near zero line or opposite boundary

Strategy 2: Momentum Confirmation

Use CMO direction to confirm trend

Enter positions when CMO crosses above/below yellow MA line

Hold positions while CMO remains on the correct side of MA

Exit when CMO crosses back through MA line

Strategy 3: Volatility Breakout

Monitor boundary width (envelope expansion/contraction)

When boundaries contract significantly, prepare for breakout

Enter in direction of CMO breakout from narrow range

Use boundary expansion as confirmation signal

⚠️ Important Notes

Best Timeframes

Scalping: 1m, 5m charts

Day Trading: 15m, 30m, 1H charts

Swing Trading: 4H, Daily charts

Market Conditions

Trending Markets: Focus on momentum confirmation signals

Ranging Markets: Focus on boundary reversal signals

High Volatility: Increase envelope multiplier (1.8-2.5)

Low Volatility: Decrease envelope multiplier (1.0-1.3)

Risk Management

Always use stop losses beyond boundary levels

Reduce position size during boundary expansion periods

Combine with price action and support/resistance levels

Monitor the real-time table for precise entry/exit levels

🔔 Alerts

The indicator includes built-in alert conditions:

"CMO Above Upper Bound": Potential reversal down signal

"CMO Below Lower Bound": Potential reversal up signal

Set these alerts to catch opportunities without constantly monitoring charts.

💡 Tips for Success

Combine with other indicators: Use with RSI, MACD, or volume indicators for confirmation

Watch for divergences: CMO making new highs/lows while price doesn't follow

Use multiple timeframes: Check higher timeframe CMO for overall trend context

Adjust settings for different assets: Crypto may need different settings than forex

Paper trade first: Test the indicator with your trading style before using real money

🎨 Customization Tips

Change colors in the Pine Script to match your chart theme

Adjust envelope length for faster (shorter) or slower (longer) signals

Modify envelope multiplier based on asset volatility

Hide the table if it obstructs your view by commenting out the table section

Complete trading solution: Pair with the Optimus Indicator (paid indicator) for multi-timeframe trend analysis and trend signals.

Together they create a powerful confluence system for professional trading setups.

Advanced Grid Trading System - [WOLONG X DBG]Overview

This sophisticated grid trading system combines Bollinger Bands breakout analysis with RSI filtering to create a comprehensive automated trading approach. The system implements advanced grid management with dynamic lot sizing, intelligent ATR-based spacing, and comprehensive risk management features including drawdown protection, time-based trading controls, and multi-level position management.

Methodology

The indicator employs a multi-layered analytical approach based on established technical analysis principles:

Core Signal Generation

Bollinger Bands Breakout Engine: Utilizes customizable period Bollinger Bands (default 35) with highest/lowest price detection over the calculation period to identify potential reversal points when price breaks below recent lows or above recent highs

RSI Confirmation Filter: Implements RSI-based signal filtering with customizable maximum RSI values to avoid entries during overbought/oversold conditions, requiring RSI below (50 - max_rsi_value) for buy signals and above (50 + max_rsi_value) for sell signals

Grid Management System: Advanced progressive grid system with configurable pip-based spacing, intelligent ATR-based distance calculation, and cumulative lot sizing with customizable multipliers

Advanced Features

Dynamic Lot Sizing: Eight calculation methods including Fixed Lot, Dynamic by Balance/Equity, and risk-based percentage approaches (Low Risk 20%, Medium Risk 40%, High Risk 80%, Extreme Risk 120%, Margin Loading)

Comprehensive Risk Management: Multi-layered drawdown protection with percentage and absolute value limits, automatic position closure options, and trading suspension features with time-based recovery

Time-Based Controls: Configurable GMT-based trading hours with start/stop times for session-specific trading and market condition adaptation

Key Components

Signal Types

Primary Entry Signals: Buy signals when price breaks below recent lowest values within Bollinger period with RSI confirmation; Sell signals when price breaks above recent highest values with RSI confirmation

Grid Expansion Logic: Automatic additional entries based on configurable pip distances from base price, triggered when price moves against initial position by specified intervals

Take Profit Systems: Dual-mode TP calculation using either weighted average across all positions or individual level TP with customizable pip values

Stop Loss Protection: Grid-wide SL with customizable pip distances or default 1000-pip protection

Visual Elements

Bollinger Bands Display: Three-line Bollinger Bands system with upper, middle (SMA), and lower bands for trend and volatility analysis

Grid Base Line: Yellow dashed line showing initial grid entry level with right extension for reference

Comprehensive TP/SL Lines: Dual-line system showing both first order reference levels (dotted, light colors) and official Martingale weighted average levels (solid, bold colors)

Entry Point Labels: Detailed entry markers showing BUY/SELL direction, grid level, and lot size information

Dual Dashboard System: Main control panel (top-right) and dark theme entry log (bottom-right) with real-time status updates

Usage Instructions

Basic Configuration

Capital Management: Select lot calculation method from dropdown (recommended: "Low Risk 20%" for conservative approach)

Grid Parameters: Configure trading distance (default 35 pips) and enable smart distance for ATR-based dynamic adjustments

Strategy Settings: Set Bollinger period (35), RSI period (20), and maximum RSI value (15) for signal filtering

Risk Controls: Configure maximum drawdown percentage and action when limits are exceeded

Signal Interpretation

Buy Entry Conditions: Generated when current close price breaks below the lowest price in the Bollinger calculation period, with RSI below (50 - max_rsi_value)

Sell Entry Conditions: Generated when current close price breaks above the highest price in the Bollinger calculation period, with RSI above (50 + max_rsi_value)

Grid Expansion: Automatic additional entries when price moves against position by configured pip distances, with progressive lot sizing using multipliers

Exit Conditions: Weighted average TP achievement, breakeven after specified grid levels, or manual cycle completion

Dashboard Analysis

Main Control Panel: Displays current grid level, trading direction, open orders count, total volume, next lot size, grid P&L, current balance, floating drawdown, RSI status, trading hours, and system locks

Dark Theme Entry Log: Shows recent entry history with timestamps, entry types (BUY/SELL), prices, lot sizes, and grid levels for trade tracking

Risk Monitoring: Real-time drawdown tracking with color-coded warnings and automatic protection activation

Risk Management Features

Automatic Protections

Drawdown Limits: Configurable percentage (default 100%) and absolute USD drawdown limits with four response options: Close Orders and Stop 24h/Until Restart, or Prevent New Grid/Until Restart

Position Sizing: Eight dynamic lot calculation methods based on account equity, balance, or risk tolerance with maximum lot size limits

Grid Limitations: Maximum number of grid levels (default 9) to prevent excessive exposure accumulation

Time Controls: GMT-based trading hour restrictions to avoid high-volatility periods or specific market sessions

Confirmation Requirements

Multi-Indicator Alignment: Requires both Bollinger Bands breakout and RSI confirmation before signal generation

Intelligent Spacing: ATR-based grid spacing adjustment using short-term (96-period) vs long-term (672-period) ATR ratio for market volatility adaptation

Progressive Sizing: Configurable lot multipliers for different grid levels (Order 2: 1.0x, Orders 3-5: 2.0x, Orders 6+: 1.5x default)

Optimal Settings

Timeframe Recommendations

Scalping: 1M-5M charts with reduced grid spacing (20-25 pips) and tighter RSI filters

Day Trading: 15M-1H charts with standard settings (35 pips) and default RSI parameters

Swing Trading: 4H-Daily charts with increased spacing (50+ pips) and relaxed RSI filters

Market Conditions

Trending Markets: Reduce RSI maximum value to 10-12, increase grid spacing to 40-50 pips, enable breakeven functionality

Ranging Markets: Standard settings with weighted TP enabled and moderate grid spacing

High Volatility: Enable smart distance, reduce maximum grid levels to 6-7, increase drawdown limits

Advanced Features

Customization Options

Lot Calculation Methods: Eight different approaches from fixed lot (0.01) to risk-based percentage calculations with margin loading options

Grid Multipliers: Separate multiplier settings for different grid levels (2nd order, 3rd-5th orders, 6th+ orders) with decimal precision

TP/SL Configuration: Individual or weighted average TP calculation with positive/negative pip values, breakeven after specified levels

Visual Controls: Toggle options for dashboard display, entry labels, TP/SL lines, lot information, and dark theme components

Technical Specifications

Grid Management: Up to 50 configurable grid levels with progressive lot sizing and cumulative position tracking

Risk Controls: Dual drawdown limits (percentage and absolute) with four different response actions and time-based recovery

Time Management: GMT-based trading hours with flexible start/end times supporting overnight sessions

Alert System: Five comprehensive alert conditions for new signals, drawdown warnings, maximum levels, and cycle completion

Important Limitations

Lagging Nature: Signals may appear after optimal entry points due to confirmation requirements and breakout validation

Grid Risk: Progressive lot sizing can lead to significant exposure accumulation during extended adverse price movements

Market Dependency: Performance varies significantly between trending and ranging market conditions, requiring parameter adjustments

Computational Load: Complex multi-array calculations and real-time dashboard updates may impact performance on slower devices

No Guarantee: All signals are suggestions based on technical analysis calculations and may be incorrect

Educational Disclaimers

This indicator is designed for educational and analytical purposes only. It represents a technical analysis tool based on mathematical calculations of historical price data and should not be considered as financial advice or trading recommendations.

Risk Warning: Grid trading involves substantial risk of loss and is not suitable for all investors. The progressive lot sizing methodology can lead to significant exposure accumulation during adverse market movements. Past performance of any trading system or methodology is not necessarily indicative of future results.

Important Notes:

Always conduct your own analysis before making trading decisions

Use appropriate position sizing and risk management strategies

Never risk more than you can afford to lose

Consider your investment objectives, experience level, and risk tolerance

Seek advice from qualified financial professionals when needed

Grid trading can result in multiple simultaneous positions with compounding risk exposure

Performance Disclaimer: Backtesting results do not guarantee future performance. Market conditions change constantly, and what worked in the past may not work in the future. The indicator's mathematical calculations are based on historical data patterns that may not repeat. Always paper trade new strategies before risking real capital.

System Limitations: The indicator relies on technical analysis principles and may produce false signals during unusual market conditions, news events, or periods of extreme volatility. Users should implement additional confirmation methods and maintain strict risk management protocols.

Advanced Trading System - [WOLONG X DBG]Advanced Multi-Timeframe Trading System

Overview

This technical analysis indicator combines multiple established methodologies to provide traders with market insights across various timeframes. The system integrates SuperTrend analysis, moving average clouds, MACD-based candle coloring, RSI analysis, and multi-timeframe trend detection to suggest potential entry and exit opportunities for both swing and day trading approaches.

Methodology

The indicator employs a multi-layered analytical approach based on established technical analysis principles:

Core Signal Generation

SuperTrend Engine: Utilizes adaptive SuperTrend calculations with customizable sensitivity (1-20) combined with SMA confirmation filters to identify potential trend changes and continuations

Braid Filter System: Implements moving average filtering using multiple MA types (McGinley Dynamic, EMA, DEMA, TEMA, Hull, Jurik, FRAMA) with percentage-based strength filtering to help reduce false signals

Multi-Timeframe Analysis: Analyzes trend conditions across 10 different timeframes (1-minute to Daily) using EMA-based trend detection for broader market context

Advanced Features

MACD Candle Coloring: Applies dynamic 4-level candle coloring system based on MACD histogram momentum and signal line relationships for visual trend strength assessment

RSI Analysis: Identifies potential reversal areas using RSI oversold/overbought conditions with SuperTrend confirmation

Take Profit Analysis: Features dual-mode TP detection using statistical slope analysis and Parabolic SAR integration for exit timing analysis

Key Components

Signal Types

Primary Signals: Green ▲ for potential long entries, Red ▼ for potential short entries with trend and SMA alignment

Reversal Signals: Small circular indicators for RSI-based counter-trend possibilities

Take Profit Markers: X-cross symbols indicating statistical TP analysis zones

Pullback Signals: Purple arrows for potential trend continuation entries using Parabolic SAR

Visual Elements

8-Layer MA Cloud: Customizable moving average cloud system with 3 color themes for trend visualization

Real-Time Dashboard: Multi-timeframe trend analysis table showing bullish/bearish status across all timeframes

Dynamic Candle Colors: 4-intensity MACD-based coloring system (ranging from light to strong trend colors)

Entry/SL/TP Labels: Automatic calculation and display of suggested entry points, stop losses, and multiple take profit levels

Usage Instructions

Basic Configuration

Sensitivity Setting: Start with default value 6

Increase (7-15) for more frequent signals in volatile markets

Decrease (3-5) for higher quality signals in trending markets

MA Filter Type: McGinley Dynamic recommended for smoother signals

Filter Strength: Set to 80% for balanced filtering, adjust based on market conditions

Signal Interpretation

Long Entry: Green ▲ suggests when price crosses above SuperTrend with bullish SMA alignment

Short Entry: Red ▼ suggests when price crosses below SuperTrend with bearish SMA alignment

Reversal Opportunities: Small circles indicate RSI-based counter-trend analysis

Take Profit Zones: X-crosses mark statistical TP areas based on slope analysis

Dashboard Analysis

Green Cells: Bullish trend detected on that timeframe

Red Cells: Bearish trend detected on that timeframe

Multi-Timeframe Confluence: Look for alignment across multiple timeframes for stronger signal confirmation

Risk Management Features

Automatic Calculations

ATR-Based Stop Loss: Dynamic stop loss calculation using ATR multiplier (default 1.9x)

Multiple Take Profit Levels: Three TP targets with 1:1, 1:2, and 1:3 risk-reward ratios

Position Sizing Guidance: Entry labels display suggested price levels for order placement

Confirmation Requirements

Trend Alignment: Requires SuperTrend and SMA confirmation before signal generation

Filter Validation: Braid filter must show sufficient strength before signals activate

Multi-Timeframe Context: Dashboard provides broader market context for decision making

Optimal Settings

Timeframe Recommendations

Scalping: 1M-5M charts with sensitivity 8-12

Day Trading: 15M-1H charts with sensitivity 6-8

Swing Trading: 4H-Daily charts with sensitivity 4-6

Market Conditions

Trending Markets: Reduce sensitivity, increase filter strength

Ranging Markets: Increase sensitivity, enable reversal signals

High Volatility: Adjust ATR risk factor to 2.0-2.5

Advanced Features

Customization Options

MA Cloud Periods: 8 customizable periods for cloud layers (default: 2,6,11,18,21,24,28,34)

Color Themes: Three professional color schemes plus transparent option

Dashboard Position: 9 positioning options with 4 size settings

Signal Filtering: Individual toggle controls for each signal type

Technical Specifications

Moving Average Types: 21 different MA calculations including advanced types (Jurik, FRAMA, VIDA, CMA)

Pullback Detection: Parabolic SAR with customizable start, increment, and maximum values

Statistical Analysis: Linear regression slope calculation for trend-based TP analysis

Important Limitations

Lagging Nature: Some signals may appear after potential entry points due to confirmation requirements

Ranging Markets: May produce false signals during extended sideways price action

High Volatility: Requires parameter adjustment during news events or unusual market conditions

Computational Load: Multiple timeframe analysis may impact performance on slower devices

No Guarantee: All signals are suggestions based on technical analysis and may be incorrect

Educational Disclaimers

This indicator is designed for educational and analytical purposes only. It represents a technical analysis tool based on mathematical calculations of historical price data and should not be considered as financial advice or trading recommendations.

Risk Warning: Trading involves substantial risk of loss and is not suitable for all investors. Past performance of any trading system or methodology is not necessarily indicative of future results. The high degree of leverage can work against you as well as for you.

Important Notes:

Always conduct your own analysis before making trading decisions

Use appropriate position sizing and risk management strategies

Never risk more than you can afford to lose

Consider your investment objectives, experience level, and risk tolerance

Seek advice from qualified financial professionals when needed

Performance Disclaimer: Backtesting results do not guarantee future performance. Market conditions change constantly, and what worked in the past may not work in the future. Always paper trade new strategies before risking real capital.

5 Adaptable SMA bandsProfessional-grade technical indicator designed for elite traders who demand precision, visual clarity, and adaptive market analysis.

This sophisticated tool revolutionizes traditional Simple Moving Average analysis by transforming thin lines into dynamic, adaptive bands that provide superior trend identification and market structure visualization across all timeframes and asset classes.

🎯 Key Professional Features

5 Fully Configurable SMAs with independent period, color, and width controls

3 Advanced Adaptation Methods: Price Percentage, ATR Adaptive, Dynamic Volatility

Institutional-Grade Visual Design with thick, clearly visible bands

Real-Time Information Dashboard displaying all active parameters

Professional Default Setup: SMA 8 (Green), SMA 20 (Blue), SMA 200 (Red)

Precision Band Width Control from 0.05% to 2.0% with 0.05% increments

Individual Toggle Control for each moving average

Optional Center Lines for exact price level identification

📈 Advanced Adaptation Technology

Price Percentage Method: Band width as percentage of SMA value

ATR Adaptive Method (Recommended): Automatically adjusts to market volatility using Average True Range

Dynamic Volatility Method: Uses standard deviation for high-volatility instruments

💼 Professional Trading Applications

Multi-Timeframe Trend Analysis: Identify short, medium, and long-term trends simultaneously

Dynamic Support/Resistance Levels: Adaptive bands act as dynamic S/R zones

Market Structure Analysis: Visualize trend strength and momentum shifts

Entry/Exit Signal Enhancement: Clear visual confirmation of trend changes

Risk Management: Better position sizing based on volatility-adjusted bands

🏆 Competitive Advantages

Superior Visual Clarity: Thick bands are easier to identify than traditional thin lines

Automatic Volatility Adjustment: Adapts to any instrument's characteristics

Zoom-Independent Scaling: Maintains visual proportions at any chart zoom level

Universal Compatibility: Works flawlessly on Forex, Stocks, Crypto, Commodities, Indices

⚙️ Recommended Professional Setups

Scalping: SMAs 8, 20, 50 with ATR Adaptive method

Day Trading: SMAs 20, 50, 100 with 0.3-0.5% band width

Swing Trading: SMAs 50, 100, 200 with Dynamic Volatility method

Position Trading: SMAs 100, 200 with 0.5-0.8% band width

[blackcat] L2 Trend LinearityOVERVIEW

The L2 Trend Linearity indicator is a sophisticated market analysis tool designed to help traders identify and visualize market trend linearity by analyzing price action relative to dynamic support and resistance zones. This powerful Pine Script indicator utilizes the Arnaud Legoux Moving Average (ALMA) algorithm to calculate weighted price calculations and generate dynamic support/resistance zones that adapt to changing market conditions. By visualizing market zones through colored candles and histograms, the indicator provides clear visual cues about market momentum and potential trading opportunities. The script generates buy/sell signals based on zone crossovers, making it an invaluable tool for both technical analysis and automated trading strategies. Whether you're a day trader, swing trader, or algorithmic trader, this indicator can help you identify market regimes, support/resistance levels, and potential entry/exit points with greater precision.

FEATURES

Dynamic Support/Resistance Zones: Calculates dynamic support (bear market zone) and resistance (bull market zone) using weighted price calculations and ALMA smoothing

Visual Market Representation: Color-coded candles and histograms provide immediate visual feedback about market conditions

Smart Signal Generation: Automatic buy/sell signals generated from zone crossovers with clear visual indicators

Customizable Parameters: Four different ALMA smoothing parameters for various timeframes and trading styles

Multi-Timeframe Compatibility: Works across different timeframes from 1-minute to weekly charts

Real-time Analysis: Provides instant feedback on market momentum and trend direction

Clear Visual Cues: Green candles indicate bullish momentum, red candles indicate bearish momentum, and white candles indicate neutral conditions

Histogram Visualization: Blue histogram shows bear market zone (below support), aqua histogram shows bull market zone (above resistance)

Signal Labels: "B" labels mark buy signals (price crosses above resistance), "S" labels mark sell signals (price crosses below support)

Overlay Functionality: Works as an overlay indicator without cluttering the chart with unnecessary elements

Highly Customizable: All parameters can be adjusted to suit different trading strategies and market conditions

HOW TO USE

Add the Indicator to Your Chart

Open TradingView and navigate to your desired trading instrument

Click on "Indicators" in the top menu and select "New"

Search for "L2 Trend Linearity" or paste the Pine Script code

Click "Add to Chart" to apply the indicator

Configure the Parameters

ALMA Length Short: Set the short-term smoothing parameter (default: 3). Lower values provide more responsive signals but may generate more false signals

ALMA Length Medium: Set the medium-term smoothing parameter (default: 5). This provides a balance between responsiveness and stability

ALMA Length Long: Set the long-term smoothing parameter (default: 13). Higher values provide more stable signals but with less responsiveness

ALMA Length Very Long: Set the very long-term smoothing parameter (default: 21). This provides the most stable support/resistance levels

Understand the Visual Elements

Green Candles: Indicate bullish momentum when price is above the bear market zone (support)

Red Candles: Indicate bearish momentum when price is below the bull market zone (resistance)

White Candles: Indicate neutral market conditions when price is between support and resistance zones

Blue Histogram: Shows bear market zone when price is below support level

Aqua Histogram: Shows bull market zone when price is above resistance level

"B" Labels: Mark buy signals when price crosses above resistance

"S" Labels: Mark sell signals when price crosses below support

Identify Market Regimes

Bullish Regime: Price consistently above resistance zone with green candles and aqua histogram

Bearish Regime: Price consistently below support zone with red candles and blue histogram

Neutral Regime: Price oscillating between support and resistance zones with white candles

Generate Trading Signals

Buy Signals: Look for price crossing above the bull market zone (resistance) with confirmation from green candles

Sell Signals: Look for price crossing below the bear market zone (support) with confirmation from red candles

Confirmation: Always wait for confirmation from candle color changes before entering trades

Optimize for Different Timeframes

Scalping: Use shorter ALMA lengths (3-5) for 1-5 minute charts

Day Trading: Use medium ALMA lengths (5-13) for 15-60 minute charts

Swing Trading: Use longer ALMA lengths (13-21) for 1-4 hour charts

Position Trading: Use very long ALMA lengths (21+) for daily and weekly charts

LIMITATIONS

Whipsaw Markets: The indicator may generate false signals in choppy, sideways markets where price oscillates rapidly between support and resistance

Lagging Nature: Like all moving average-based indicators, there is inherent lag in the calculations, which may result in delayed signals

Not a Standalone Tool: This indicator should be used in conjunction with other technical analysis tools and risk management strategies

Market Structure Dependency: Performance may vary depending on market structure and volatility conditions

Parameter Sensitivity: Different markets may require different parameter settings for optimal performance

No Volume Integration: The indicator does not incorporate volume data, which could provide additional confirmation signals

Limited Backtesting: Pine Script limitations may restrict comprehensive backtesting capabilities

Not Suitable for All Instruments: May perform differently on stocks, forex, crypto, and futures markets

Requires Confirmation: Signals should always be confirmed with other indicators or price action analysis

Not Predictive: The indicator identifies current market conditions but does not predict future price movements

NOTES

ALMA Algorithm: The indicator uses the Arnaud Legoux Moving Average (ALMA) algorithm, which is known for its excellent smoothing capabilities and reduced lag compared to traditional moving averages

Weighted Price Calculations: The bear market zone uses (2low + close) / 3, while the bull market zone uses (high + 2close) / 3, providing more weight to recent price action

Dynamic Zones: The support and resistance zones are dynamic and adapt to changing market conditions, making them more responsive than static levels

Color Psychology: The color scheme follows traditional trading psychology - green for bullish, red for bearish, and white for neutral

Signal Timing: The signals are generated on the close of each bar, ensuring they are based on complete price action

Label Positioning: Buy signals appear below the bar (red "B" label), while sell signals appear above the bar (green "S" label)

Multiple Timeframes: The indicator can be applied to multiple timeframes simultaneously for comprehensive analysis

Risk Management: Always use proper risk management techniques when trading based on indicator signals

Market Context: Consider the overall market context and trend direction when interpreting signals

Confirmation: Look for confirmation from other indicators or price action patterns before entering trades

Practice: Test the indicator on historical data before using it in live trading

Customization: Feel free to experiment with different parameter combinations to find what works best for your trading style

THANKS

Special thanks to the TradingView community and the Pine Script developers for creating such a powerful and flexible platform for technical analysis. This indicator builds upon the foundation of the ALMA algorithm and various moving average techniques developed by technical analysis pioneers. The concept of dynamic support and resistance zones has been refined over decades of market analysis, and this script represents a modern implementation of these timeless principles. We acknowledge the contributions of all traders and developers who have contributed to the evolution of technical analysis and continue to push the boundaries of what's possible with algorithmic trading tools.

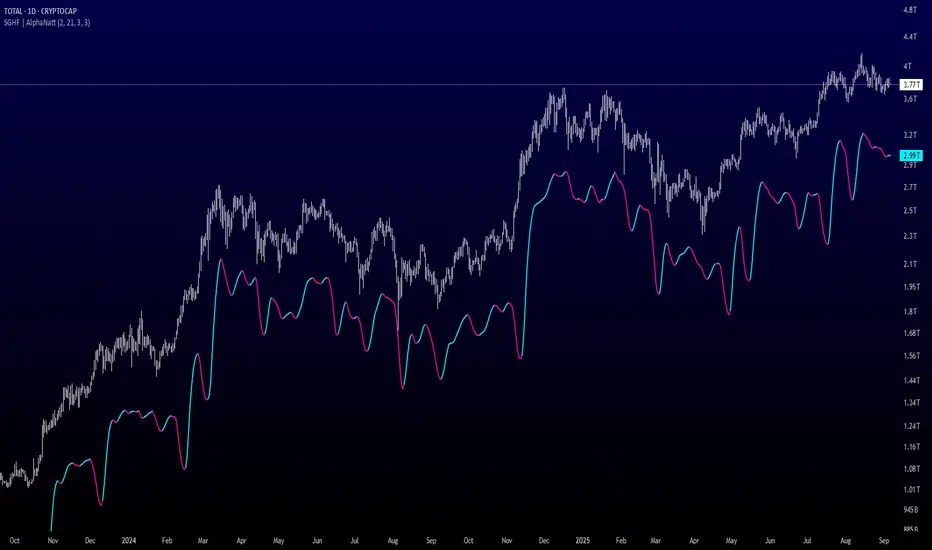

Savitzky-Golay Hampel Filter | AlphaNattSavitzky-Golay Hampel Filter | AlphaNatt

A revolutionary indicator combining NASA's satellite data processing algorithms with robust statistical outlier detection to create the most scientifically advanced trend filter available on TradingView.

"This is the same mathematics that processes signals from the Hubble Space Telescope and analyzes data from the Large Hadron Collider - now applied to financial markets."

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

🚀 SCIENTIFIC PEDIGREE

Savitzky-Golay Filter Applications:

NASA: Satellite telemetry and space probe data processing

CERN: Particle physics data analysis at the LHC

Pharmaceutical: Chromatography and spectroscopy analysis

Astronomy: Processing signals from radio telescopes

Medical: ECG and EEG signal processing

Hampel Filter Usage:

Aerospace: Cleaning sensor data from aircraft and spacecraft

Manufacturing: Quality control in precision engineering

Seismology: Earthquake detection and analysis

Robotics: Sensor fusion and noise reduction

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

🧬 THE MATHEMATICS

1. Savitzky-Golay Filter

The SG filter performs local polynomial regression on data points:

Fits a polynomial of degree n to a sliding window of data

Evaluates the polynomial at the center point

Preserves higher moments (peaks, valleys) unlike moving averages

Maintains derivative information for true momentum analysis

Originally published in Analytical Chemistry (1964)

Mathematical Properties:

Optimal smoothing in the least-squares sense

Preserves statistical moments up to polynomial order

Exact derivative calculation without additional lag

Superior frequency response vs traditional filters

2. Hampel Filter

A robust outlier detector based on Median Absolute Deviation (MAD):

Identifies outliers using robust statistics

Replaces spurious values with polynomial-fitted estimates

Resistant to up to 50% contaminated data

MAD is 1.4826 times more robust than standard deviation

Outlier Detection Formula:

|x - median| > k × 1.4826 × MAD

Where k is the threshold parameter (typically 3 for 99.7% confidence)

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

💎 WHY THIS IS SUPERIOR

vs Moving Averages:

Preserves peaks and valleys (critical for catching tops/bottoms)

No lag penalty for smoothness

Maintains derivative information

Polynomial fitting > simple averaging

vs Other Filters:

Outlier immunity (Hampel component)

Scientifically optimal smoothing

Preserves higher-order features

Used in billion-dollar research projects

Unique Advantages:

Feature Preservation: Maintains market structure while smoothing

Spike Immunity: Ignores false breakouts and stop hunts

Derivative Accuracy: True momentum without additional indicators

Scientific Validation: 60+ years of academic research

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

⚙️ PARAMETER OPTIMIZATION

1. Polynomial Order (2-5)

2 (Quadratic): Maximum smoothing, gentle curves

3 (Cubic): Balanced smoothing and responsiveness (recommended)

4-5 (Higher): More responsive, preserves more features

2. Window Size (7-51)

Must be odd number

Larger = smoother but more lag

Formula: 2×(desired smoothing period) + 1

Default 21 = analyzes 10 bars each side

3. Hampel Threshold (1.0-5.0)

1.0: Aggressive outlier removal (68% confidence)

2.0: Moderate outlier removal (95% confidence)

3.0: Conservative outlier removal (99.7% confidence) (default)

4.0+: Only extreme outliers removed

4. Final Smoothing (1-7)

Additional WMA smoothing after filtering

1 = No additional smoothing

3-5 = Recommended for most timeframes

7 = Ultra-smooth for position trading

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

📊 TRADING STRATEGIES

Signal Recognition:

Cyan Line: Bullish trend with positive derivative

Pink Line: Bearish trend with negative derivative

Color Change: Trend reversal with polynomial confirmation

1. Trend Following Strategy

Enter when price crosses above cyan filter

Exit when filter turns pink

Use filter as dynamic stop loss

Best in trending markets

2. Mean Reversion Strategy

Enter long when price touches filter from below in uptrend

Enter short when price touches filter from above in downtrend

Exit at opposite band or filter color change

Excellent for range-bound markets

3. Derivative Strategy (Advanced)

The SG filter preserves derivative information

Acceleration = second derivative > 0

Enter on positive first derivative + positive acceleration

Exit on negative second derivative (momentum slowing)

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

📈 PERFORMANCE CHARACTERISTICS

Strengths:

Outlier Immunity: Ignores stop hunts and flash crashes

Feature Preservation: Catches tops/bottoms better than MAs

Smooth Output: Reduces whipsaws significantly

Scientific Basis: Not curve-fitted or optimized to markets

Considerations:

Slight lag in extreme volatility (all filters have this)

Requires odd window sizes (mathematical requirement)

More complex than simple moving averages

Best with liquid instruments

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

🔬 SCIENTIFIC BACKGROUND

Savitzky-Golay Publication:

"Smoothing and Differentiation of Data by Simplified Least Squares Procedures"

- Abraham Savitzky & Marcel Golay

- Analytical Chemistry, Vol. 36, No. 8, 1964

Hampel Filter Origin:

"Robust Statistics: The Approach Based on Influence Functions"

- Frank Hampel et al., 1986

- Princeton University Press

These techniques have been validated in thousands of scientific papers and are standard tools in:

NASA's Jet Propulsion Laboratory

European Space Agency

CERN (Large Hadron Collider)

MIT Lincoln Laboratory

Max Planck Institutes

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

💡 ADVANCED TIPS

News Trading: Lower Hampel threshold before major events to catch spikes

Scalping: Use Order=2 for maximum smoothness, Window=11 for responsiveness

Position Trading: Increase Window to 31+ for long-term trends

Combine with Volume: Strong trends need volume confirmation

Multiple Timeframes: Use daily for trend, hourly for entry

Watch the Derivative: Filter color changes when first derivative changes sign

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

⚠️ IMPORTANT NOTICES

Not financial advice - educational purposes only

Past performance does not guarantee future results

Always use proper risk management

Test settings on your specific instrument and timeframe

No indicator is perfect - part of complete trading system

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

🏆 CONCLUSION

The Savitzky-Golay Hampel Filter represents the pinnacle of scientific signal processing applied to financial markets. By combining polynomial regression with robust outlier detection, traders gain access to the same mathematical tools that:

Guide spacecraft to other planets

Detect gravitational waves from black holes

Analyze particle collisions at near light-speed

Process signals from deep space

This isn't just another indicator - it's rocket science for trading .

"When NASA needs to separate signal from noise in billion-dollar missions, they use these exact algorithms. Now you can too."

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

Developed by AlphaNatt

Version: 1.0

Release: 2025

Pine Script: v6

"Where Space Technology Meets Market Analysis"

Not financial advice. Always DYOR

Golden Duck Runner With TargetsGolden Duck Runner With Targets

Overview

The Golden Duck Runner is a comprehensive trend-following indicator designed for intraday and swing trading. It combines dual EMA analysis with pullback detection to identify high-probability entry points in trending markets.

Key Features

Core Signal Logic

Dual EMA System: Uses a fast EMA (default 18) and trend filter EMA (default 111)

Pullback Detection: Identifies when price pulls back to the fast EMA while staying above/below the trend filter

Trend Confirmation: Only generates signals in the direction of the overall trend

Visual Elements

Dynamic EMA Colors: Golden fast EMA, with trend filter changing from teal (uptrend) to orange (downtrend)

Entry Signals: Clear golden arrows marking buy/sell opportunities

Target Levels: Displays three take profit levels and stop loss with visual confirmation

Professional Dashboard: Real-time position and trend information

Risk Management

Fixed Tick-Based Targets: Consistent risk/reward ratios across all instruments

Multiple Take Profits: Three progressive profit-taking levels (30, 50, 75 ticks)

Stop Loss Protection: 36-tick stop loss with visual tracking

Position Duration Limit: Automatic closure after 20 bars if targets not reached

Alert System

Comprehensive alert notifications for:

Long and short entry signals