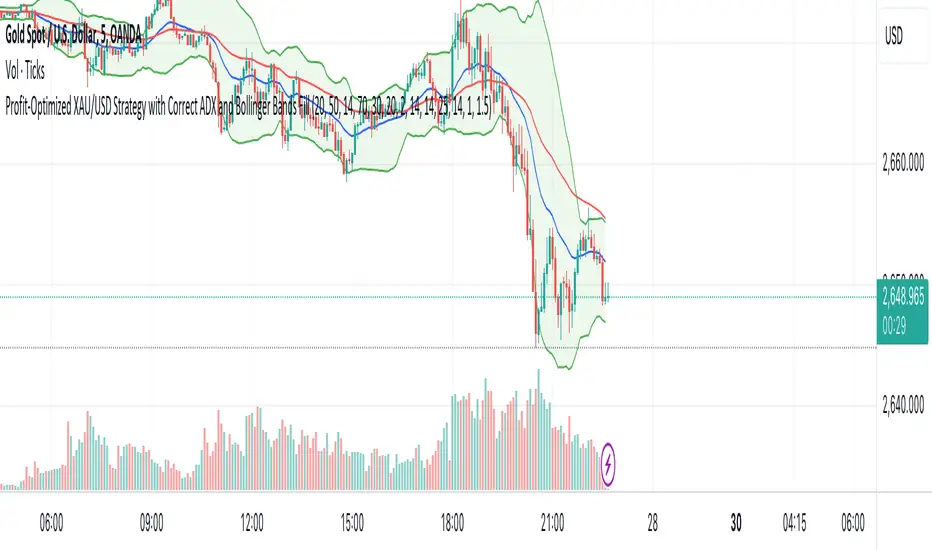

XAU/USD Strategy with Correct ADX and Bollinger Bands Fill1. *Indicators Used*:

- *Exponential Moving Averages (EMAs)*: Two EMAs (20-period and 50-period) are used to identify the trend direction and potential entry points based on crossovers.

- *Relative Strength Index (RSI)*: A momentum oscillator that measures the speed and change of price movements. It identifies overbought and oversold conditions.

- *Bollinger Bands*: These consist of a middle line (simple moving average) and two outer bands (standard deviations away from the middle). They help to identify price volatility and potential reversal points.

- *Average Directional Index (ADX)*: This indicator quantifies trend strength. It's derived from the Directional Movement Index (DMI) and helps confirm the presence of a strong trend.

- *Average True Range (ATR)*: Used to calculate position size based on volatility, ensuring that trades align with the trader's risk tolerance.

2. *Entry Conditions*:

- *Long Entry*:

- The 20 EMA crosses above the 50 EMA (indicating a potential bullish trend).

- The RSI is below the oversold level (30), suggesting the asset may be undervalued.

- The price is below the lower Bollinger Band, indicating potential price reversal.

- The ADX is above a specified threshold (25), confirming that there is sufficient trend strength.

- *Short Entry*:

- The 20 EMA crosses below the 50 EMA (indicating a potential bearish trend).

- The RSI is above the overbought level (70), suggesting the asset may be overvalued.

- The price is above the upper Bollinger Band, indicating potential price reversal.

- The ADX is above the specified threshold (25), confirming trend strength.

3. *Position Sizing*:

- The script calculates the position size dynamically based on the trader's risk per trade (expressed as a percentage of the total capital) and the ATR. This ensures that the trader does not risk more than the specified percentage on any single trade, adjusting the position size according to market volatility.

4. *Exit Conditions*:

- The strategy uses a trailing stop-loss mechanism to secure profits as the price moves in the trader's favor. The trailing stop is set at a percentage (1.5% by default) below the highest price reached since entry for long positions and above the lowest price for short positions.

- Additionally, if the RSI crosses back above the overbought level while in a long position or below the oversold level while in a short position, the position is closed to prevent losses.

5. *Alerts*:

- Alerts are set to notify the trader when a buy or sell condition is met based on the strategy's rules. This allows for timely execution of trades.

### Summary

This strategy aims to capture significant price movements in the XAU/USD market by combining trend-following (EMAs, ADX) and momentum indicators (RSI, Bollinger Bands). The dynamic position sizing based on ATR helps manage risk effectively. By implementing trailing stops and alert mechanisms, the strategy enhances the trader's ability to act quickly on opportunities while mitigating potential losses.

"rsi" için komut dosyalarını ara

Post-Open Long Strategy with ATR-based Stop Loss and Take ProfitThe "Post-Open Long Strategy with ATR-Based Stop Loss and Take Profit" is designed to identify buying opportunities after the German and US markets open. It combines various technical indicators to filter entry signals, focusing on breakout moments following price lateralization periods.

Key Components and Their Interaction:

Bollinger Bands (BB):

Description: Uses BB with a 14-period length and standard deviation multiplier of 1.5, creating narrower bands for lower timeframes.

Role in the Strategy: Identifies low volatility phases (lateralization). The lateralization condition is met when the price is near the simple moving average of the BB, suggesting an imminent increase in volatility.

Exponential Moving Averages (EMA):

10-period EMA: Quickly detects short-term trend direction.

200-period EMA: Filters long-term trends, ensuring entries occur in a bullish market.

Interaction: Positions are entered only if the price is above both EMAs, indicating a consolidated positive trend.

Relative Strength Index (RSI):

Description: 7-period RSI with a threshold above 30.

Role in the Strategy: Confirms the market is not oversold, supporting the validity of the buy signal.

Average Directional Index (ADX):

Description: 7-period ADX with 7-period smoothing and a threshold above 10.

Role in the Strategy: Assesses trend strength. An ADX above 10 indicates sufficient momentum to justify entry.

Average True Range (ATR) for Dynamic Stop Loss and Take Profit:

Description: 14-period ATR with multipliers of 2.0 for Stop Loss and 4.0 for Take Profit.

Role in the Strategy: Adjusts exit levels based on current volatility, enhancing risk management.

Resistance Identification and Breakout:

Description: Analyzes the highs of the last 20 candles to identify resistance levels with at least two touches.

Role in the Strategy: A breakout above this level signals a potential continuation of the bullish trend.

Time Filters and Market Conditions:

Trading Hours: Operates only during the opening of the German market (8:00 - 12:00) and US market (15:30 - 19:00).

Panic Candle: The current candle must close negative, leveraging potential emotional reactions in the market.

Avoiding Entry During Pullbacks:

Description: Checks that the two previous candles are not both bearish.

Role in the Strategy: Avoids entering during a potential pullback, improving trade success probability.

Post-Open Long Strategy with ATR-Based Stop Loss and Take Profit

The "Post-Open Long Strategy with ATR-Based Stop Loss and Take Profit" is designed to identify buying opportunities after the German and US markets open. It combines various technical indicators to filter entry signals, focusing on breakout moments following price lateralization periods.

Key Components and Their Interaction:

Bollinger Bands (BB):

Description: Uses BB with a 14-period length and standard deviation multiplier of 1.5, creating narrower bands for lower timeframes.

Role in the Strategy: Identifies low volatility phases (lateralization). The lateralization condition is met when the price is near the simple moving average of the BB, suggesting an imminent increase in volatility.

Exponential Moving Averages (EMA):

10-period EMA: Quickly detects short-term trend direction.

200-period EMA: Filters long-term trends, ensuring entries occur in a bullish market.

Interaction: Positions are entered only if the price is above both EMAs, indicating a consolidated positive trend.

Relative Strength Index (RSI):

Description: 7-period RSI with a threshold above 30.

Role in the Strategy: Confirms the market is not oversold, supporting the validity of the buy signal.

Average Directional Index (ADX):

Description: 7-period ADX with 7-period smoothing and a threshold above 10.

Role in the Strategy: Assesses trend strength. An ADX above 10 indicates sufficient momentum to justify entry.

Average True Range (ATR) for Dynamic Stop Loss and Take Profit:

Description: 14-period ATR with multipliers of 2.0 for Stop Loss and 4.0 for Take Profit.

Role in the Strategy: Adjusts exit levels based on current volatility, enhancing risk management.

Resistance Identification and Breakout:

Description: Analyzes the highs of the last 20 candles to identify resistance levels with at least two touches.

Role in the Strategy: A breakout above this level signals a potential continuation of the bullish trend.

Time Filters and Market Conditions:

Trading Hours: Operates only during the opening of the German market (8:00 - 12:00) and US market (15:30 - 19:00).

Panic Candle: The current candle must close negative, leveraging potential emotional reactions in the market.

Avoiding Entry During Pullbacks:

Description: Checks that the two previous candles are not both bearish.

Role in the Strategy: Avoids entering during a potential pullback, improving trade success probability.

Entry and Exit Conditions:

Long Entry:

The price breaks above the identified resistance.

The market is in a lateralization phase with low volatility.

The price is above the 10 and 200-period EMAs.

RSI is above 30, and ADX is above 10.

No short-term downtrend is detected.

The last two candles are not both bearish.

The current candle is a "panic candle" (negative close).

Order Execution: The order is executed at the close of the candle that meets all conditions.

Exit from Position:

Dynamic Stop Loss: Set at 2 times the ATR below the entry price.

Dynamic Take Profit: Set at 4 times the ATR above the entry price.

The position is automatically closed upon reaching the Stop Loss or Take Profit.

How to Use the Strategy:

Application on Volatile Instruments:

Ideal for financial instruments that show significant volatility during the target market opening hours, such as indices or major forex pairs.

Recommended Timeframes:

Intraday timeframes, such as 5 or 15 minutes, to capture significant post-open moves.

Parameter Customization:

The default parameters are optimized but can be adjusted based on individual preferences and the instrument analyzed.

Backtesting and Optimization:

Backtesting is recommended to evaluate performance and make adjustments if necessary.

Risk Management:

Ensure position sizing respects risk management rules, avoiding risking more than 1-2% of capital per trade.

Originality and Benefits of the Strategy:

Unique Combination of Indicators: Integrates various technical metrics to filter signals, reducing false positives.

Volatility Adaptability: The use of ATR for Stop Loss and Take Profit allows the strategy to adapt to real-time market conditions.

Focus on Post-Lateralization Breakout: Aims to capitalize on significant moves following consolidation periods, often associated with strong directional trends.

Important Notes:

Commissions and Slippage: Include commissions and slippage in settings for more realistic simulations.

Capital Size: Use a realistic trading capital for the average user.

Number of Trades: Ensure backtesting covers a sufficient number of trades to validate the strategy (ideally more than 100 trades).

Warning: Past results do not guarantee future performance. The strategy should be used as part of a comprehensive trading approach.

With this strategy, traders can identify and exploit specific market opportunities supported by a robust set of technical indicators and filters, potentially enhancing their trading decisions during key times of the day.

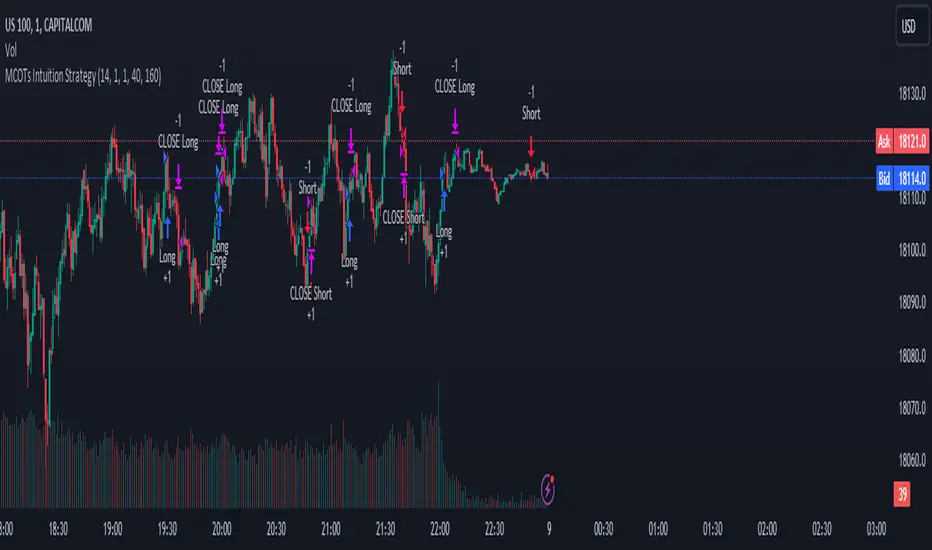

MCOTs Intuition StrategyInitial Capital: The strategy starts with an initial capital of $50,000.

Execution: Trades are executed on every price tick to capture all potential movements.

Contract Size: The default position size is one contract per trade.

Timeframe: Although not explicitly mentioned, this strategy is intended for a one-minute timeframe.

RSI Calculation: The Relative Strength Index (RSI) is calculated over a user-defined period (default is 14 periods).

Standard Deviation: The script calculates the standard deviation of the change in RSI values to determine the threshold for entering trades.

Exhaustion Detection: Before entering a long or short position, the script checks for exhaustion in the RSI’s momentum. This is to avoid entering trades during extreme conditions where a reversal is likely.

Entry Conditions: A long position is entered when the current RSI momentum exceeds the standard deviation threshold and is less than the previous momentum multiplied by an exhaustion factor. A short position is entered under the opposite conditions.

Limit Orders for Exit: Instead of traditional stop loss and take profit orders, the strategy uses limit orders to exit positions. This means the strategy sets a desired price level to close the position and waits for the market to reach this price.

Profit Target and Stop Loss: The script allows setting a profit target and stop loss in terms of ticks, which are the smallest measurable increments in price movement for the traded asset.

blah blah whatever

TrippleMACDCryptocurrency Scalping Strategy for 1m Timeframe

Introduction:

Welcome to our cutting-edge cryptocurrency scalping strategy tailored specifically for the 1-minute timeframe. By combining three MACD indicators with different parameters and averaging them, along with applying RSI, we've developed a highly effective strategy for maximizing profits in the cryptocurrency market. This strategy is designed for automated trading through our bot, which executes trades using hooks. All trades are calculated for long positions only, ensuring optimal performance in a fast-paced market.

Key Components:

MACD (Moving Average Convergence Divergence):

We've utilized three MACD indicators with varying parameters to capture different aspects of market momentum.

Averaging these MACD indicators helps smooth out noise and provides a more reliable signal for trading decisions.

RSI (Relative Strength Index):

RSI serves as a complementary indicator, providing insights into the strength of bullish trends.

By incorporating RSI, we enhance the accuracy of our entry and exit points, ensuring timely execution of trades.

Strategy Overview:

Long Position Entries:

Initiate long positions when all three MACD indicators signal bullish momentum and the RSI confirms bullish strength.

This combination of indicators increases the probability of successful trades, allowing us to capitalize on uptrends effectively.

Utilizing Linear Regression:

Linear regression is employed to identify consolidation phases in the market.

Recognizing consolidation periods helps us avoid trading during choppy price action, ensuring optimal performance.

Suitability for Grid Trading Bots:

Our strategy is well-suited for grid trading bots due to frequent price fluctuations and opportunities for grid activation.

The strategy's design accounts for price breakthroughs, which are advantageous for grid trading strategies.

Benefits of the Strategy:

Consistent Performance Across Cryptocurrencies:

Through rigorous testing on various cryptocurrency futures contracts, our strategy has demonstrated favorable results across different coins.

Its adaptability makes it a versatile tool for traders seeking consistent profits in the cryptocurrency market.

Integration of Advanced Techniques:

By integrating multiple indicators and employing linear regression, our strategy leverages advanced techniques to enhance trading performance.

This strategic approach ensures a comprehensive analysis of market conditions, leading to well-informed trading decisions.

Conclusion:

Our cryptocurrency scalping strategy offers a sophisticated yet user-friendly approach to trading in the fast-paced environment of the 1-minute timeframe. With its emphasis on automation, accuracy, and adaptability, our strategy empowers traders to navigate the complexities of the cryptocurrency market with confidence. Whether you're a seasoned trader or a novice investor, our strategy provides a reliable framework for achieving consistent profits and maximizing returns on your investment.

Strategy / Connectable [Azullian]The connectable strategy serves as a foundational component in our indicator system on TradingView, designed for intuitive testing, visualization, and construction of trading strategies. In concert with the connectable signal filter , it forms a cohesive unit that allows for efficient signal processing and strategy implementation. This integration enables the strategy to receive and act on weighted signals from various connectable indicators, making it a versatile tool for both novice and experienced traders.

Let's review the separate parts of this indicator.

█ STRATEGY INPUTS

We've provided an input to connect a signal filter or indicators or chains (→) which is set to 'Close' by default.

An input has several controls:

• Input: Connect indicators or signal filter here, choose indicators with a compatible : Signal connector.

• SM - Signal Mode: Choose a trading direction compatible with the settings in your signal filter

█ POSITION INVESTMENT

Determine the percentage of your trading budget you would like to use in each position based on the strategy's profit or loss.

• LINVB - Loss Investment Base: Choose which base to use to determine the investment percentage when the strategy is in a loss.

○ Equity: Use the equity as the base for percentage calculation.

○ Initial capital: Use the initial capital as the base for percentage calculation.

• LINV% - Loss Investment Percentage: Set a percentage of the chosen investment base as the investment for a new position.

○ For example, when 10% in loss, and a initial capital of $100, and the investment base is set to equity with a percentage of 50%, your investment will be 50% of $90, $45.

• PINVB - Profit Investment Base: Choose which base to use to determine the investment percentage when the strategy is in profit.

○ Equity: Use the equity as the base for percentage calculation.

○ Initial capital: Use the initial capital as the base for percentage calculation.

• PINV% - Profit Investment Percentage: Set a percentage of the chosen investment base as the investment for a new position.

○ For example, when 10% in profit, and an initial capital of $100, and the investment base is set to equity with a percentage of 100%, your investment will be 100% of $110, $110.

• RISK% - Risk Percentage:

○ Determine how much of the calculated position investment is at risk when the stop-loss is hit.

- For example, 1% of $45 represents a maximum loss of $0.45.

○ Risk percentage works together with the stop loss and the max leverage.

• MXLVG - Maximum Leverage:

○ Investigate the trading rules for your trading pair and use the maximum allowed amount of leverage.

○ To determine the number of contracts to be bought or sold, considering the stop loss and the specified risk percentage, the maximum leverage available will constrain the amount of leverage utilized to ensure that the maximum risk threshold is not exceeded. For instance, suppose the stop loss is set at 1%, and the risk percentage is defined as 10%. Initially, the calculated leverage to be used would be 10. However, if there is a maximum leverage cap set at 5, it would constrain the calculated leverage of 10 to adhere to the maximum limit of 5.

█ EXIT STOP LOSS

Determine the Stop Loss price based on your selected configuration.

As the stop loss is an integral part of the ordered contracts calculation used in conjunction with the Risk and Max leverage, you'll always need to provide a stop loss price.

• SLB - Stop Loss Base: Choose a stop loss mode for calculating stop loss prices.

○ Risk: Determines the price using the Risk parameter (RISK%) and maximum leverage (MXLVG). In this case, SLB% will not have any impact.

○ Price Entry + Offset: Calculates the stop loss price based on a offset percentage (SLB%) from the entry price of the position.

• SLB% - Stop Loss Base Percentage: Define an offset percentage that will be applied in the price entry + offset stop loss mode.

• SLT - Stop Loss Trailing:

○ Fixed: The initial stop loss will be kept and no trailing stop loss will be applied.

○ Trail Price: Computes the trailing stop loss price based on an offset percentage (SLT%) from the closing price of the current candle.

- If a better stop loss price is calculated, it will be set as the new stop loss price.

○ Trail Incr: Adapts the trailing stop loss price based on the offset percentage (SLT%).

- Each price change in favor of your position will incrementally adapt the trailing stop loss with SLT%.

• SLT% - Stop Loss Trailing Percentage: This percentage serves as an offset or increment depending on your chosen trailing mode.

█ EXIT TAKE PROFIT

Determine the Take Profit price based on your selected configuration.

• TPB - Take Profit Base: Choose a take profit mode for calculating take profit prices.

○ Reward: Determines the take profit price using the Risk parameter (RISK%) and the calculated Stop Loss price and the set reward percentage (TPB%).

- For example: Risk 1%, Calculated Stop loss price: $90, Entry price: $100, Reward (TPB%): 2%, will result in a take profit price on $120.

○ Price Entry + Offset: Calculates the take profit price based on a offset percentage (TPB%) from the entry price of the position.

- For example: Entry price: $100, Offset (TPB%): 2%, will result in a take profit price on $102.

• TPB% - Take Profit Base Percentage: Define an offset percentage that will be applied in the price entry + offset take profit mode.

• TPT - Take Profit Trailing:

○ Fixed: The initial take profit will be kept and no trailing take profit will be applied.

○ Trail Price: Computes the trailing take profit price based on an offset percentage (TPT%) from the closing price of the current candle.

- If an applicable take profit price is calculated, it will be set as the new take profit price.

○ Trail Incr: Adapts the trailing take profit price based on the offset percentage (TPT%). Each price change against your position will incrementally adapt the trailing take profit with TPT%.

• TPT% - Take Profit Trailing Percentage: This percentage serves as an offset or increment depending on your chosen trailing mode.

█ STRATEGY CONDITIONS

Specify when the strategy is permitted to execute trades.

• DATE: Enable the Date Range filter to restrict entries to a specific date range.

○ START: Set a start date and hour to commence trading.

○ END: Set an end date and hour to conclude trading within the defined range.

■ VISUALS

• LINE: Activate a colored dashed diagonal line to visually connect the entry and exit points of positions.

• SLTP: Enable visualization of stop loss, take profit, and break-even levels.

• PNL: Enable Break-Even and Close Lines along with a colored area in between to visualize profit and loss.

• ☼: Brightness % : Adjust the opacity of the plotted trading visuals.

• P - Profit Color : Choose the color for profit-related elements.

• L - Loss Color: Choose the color for loss-related elements.

• B - Breakeven Color : Select the color for break-even points.

• EL - Long Color: Specify the color for long positions.

• ES - Short Color: Specify the color for short positions.

• TRADE LABELING: For better analysis we've labeled all entries and exits conform with the type of order your strategy has executed, some examples:

○ XL-TP-150: Exit Long - Take Profit - Position 150

○ XS-TP-154: Exit Short - Take Profit - Position 154

○ XL-SL-160: Exit Long - Stop Loss - Position 160

○ XS-SL-164: Exit Short - Stop Loss - Position 164

█ USAGE OF CONNECTABLE INDICATORS

■ Connectable chaining mechanism

Connectable indicators can be connected directly to the signal monitor, signal filter or strategy , or they can be daisy chained to each other while the last indicator in the chain connects to the signal monitor, signal filter or strategy. When using a signal filter you can chain the filter to the strategy input to make your chain complete.

• Direct chaining: Connect an indicator directly to the signal monitor, signal filter or strategy through the provided inputs (→).

• Daisy chaining: Connect indicators using the indicator input (→). The first in a daisy chain should have a flow (⌥) set to 'Indicator only'. Subsequent indicators use 'Both' to pass the previous weight. The final indicator connects to the signal monitor, signal filter, or strategy.

■ Set up the strategy with a signal filter and an RSI indicator

Let's connect the Strategy to a connectable signal filter and a connectable RSI indicator :

1. Load all relevant indicators

• Load RSI / Connectable

• Load Signal filter / Connectable

• Load Strategy / Connectable

2. Signal Filter: Connect the RSI to the Signal Filter

• Open the signal filter settings

• Choose one of the three input dropdowns (1→, 2→, 3→) and choose : RSI / Connectable: Signal Connector

• Toggle the enable box before the connected input to enable the incoming signal

3. Signal Filter: Update the filter signals settings if needed

• The default settings of the filter enable EL (Enter Long), XL (Exit Long), ES (Enter Short) and XS (Exit Short).

4. Signal Filter: Update the weight threshold settings if needed

• All connectable indicators load by default with a score of 6 for each direction (EL, XL, ES, XS)

• By default, weight threshold (TH) is set at 5. This allows each occurrence to score, as the default score in each connectable indicator is 1 point above the threshold. Adjust to your liking.

5. Strategy: Connect the strategy to the signal filter in the strategy settings

• Select the strategy input → and select the Signal filter: Signal connector

6. Strategy: Enable filter compatible directions

• Set the signal mode of the strategy to a compatible direction with the signal filter.

Now that everything is connected, you'll notice green spikes in the signal filter representing long signals, and red spikes indicating short signals. Trades will also appear on the chart, complemented by a performance overview. Your journey is just beginning: delve into different scoring mechanisms, merge diverse connectable indicators, and craft unique chains. Instantly test your results and discover the potential of your configurations. Dive deep and enjoy the process!

█ BENEFITS

• Adaptable Modular Design: Arrange indicators in diverse structures via direct or daisy chaining, allowing tailored configurations to align with your analysis approach.

• Streamlined Backtesting: Simplify the iterative process of testing and adjusting combinations, facilitating a smoother exploration of potential setups.

• Intuitive Interface: Navigate TradingView with added ease. Integrate desired indicators, adjust settings, and establish alerts without delving into complex code.

• Signal Weight Precision: Leverage granular weight allocation among signals, offering a deeper layer of customization in strategy formulation.

• Advanced Signal Filtering: Define entry and exit conditions with more clarity, granting an added layer of strategy precision.

• Clear Visual Feedback: Distinct visual signals and cues enhance the readability of charts, promoting informed decision-making.

• Standardized Defaults: Indicators are equipped with universally recognized preset settings, ensuring consistency in initial setups across different types like momentum or volatility.

• Reliability: Our indicators are meticulously developed to prevent repainting. We strictly adhere to TradingView's coding conventions, ensuring our code is both performant and clean.

█ COMPATIBLE INDICATORS

Each indicator that incorporates our open-source 'azLibConnector' library and adheres to our conventions can be effortlessly integrated and used as detailed above.

For clarity and recognition within the TradingView platform, we append the suffix ' / Connectable' to every compatible indicator.

█ COMMON MISTAKES AND CLARIFICATIONS

• Removing an indicator from a chain: Deleting a linked indicator and confirming the "remove study tree" alert will also remove all underlying indicators in the object tree. Before removing one, disconnect the adjacent indicators and move it to the object stack's bottom.

• Point systems: The azLibConnector provides 500 points for each direction (EL: Enter long, XL: Exit long, ES: Enter short, XS: Exit short) Remember this cap when devising a point structure.

• Flow misconfiguration: In daisy chains the first indicator should always have a flow (⌥) setting of 'indicator only' while other indicator should have a flow (⌥) setting of 'both'.

• Recalculate: While this strategy has undergone extensive testing, enabling recalculation options like 'After order is filled' or 'On every tick' may lead to unexpected behavior.

• Fill orders: The strategy is thoroughly tested, yet enabling fill order options such as 'Using bar magnifier', 'On bar close', or 'Using standard OHLC' might result in unexpected outcomes.

• Layout and abbreviations: To maintain a consistent structure, we use abbreviations for each input. While this may initially seem complex, you'll quickly become familiar with them. Each abbreviation is also explained in the inline tooltips.

• Optimized for crypto trading: While many principles are common across markets, this strategy is specifically optimized and tested for crypto trading.

• Inputs: Connecting a connectable indicator directly to the strategy delivers the raw signal without a weight threshold, meaning every signal will trigger a trade.

█ A NOTE OF GRATITUDE

Through years of exploring TradingView and Pine Script, we've drawn immense inspiration from the community's knowledge and innovation. Thank you for being a constant source of motivation and insight.

█ RISK DISCLAIMER

Azullian's content, tools, scripts, articles, and educational offerings are presented purely for educational and informational uses. Please be aware that past performance should not be considered a predictor of future results.

Crypto Punk [Bot] (Zeiierman)█ Overview

The Crypto Punk (Zeiierman) is a trading strategy designed for the dynamic and volatile cryptocurrency market. It utilizes algorithms that incorporate price action analysis and principles inspired by Geometric Brownian Motion (GBM). The bot's core functionality revolves around analyzing differences in high and low prices over various timeframes, estimating drift (trend) and volatility, and applying this information to generate trading signals.

█ How to use the Crypto Punk Bot

Utilize the Crypto Punk Bot as a technical analysis tool to enhance your trading strategy. The signals generated by the bot can serve as a confirmation of your existing approach to entering and exiting the market. Additionally, the backtest report provided by the bot is a valuable resource for identifying the optimal settings for the specific market and timeframe you are trading in.

One method is to use the bot's signals to confirm entry points around key support and resistance levels.

█ Key Features

Let's explain how the core features work in the strategy.

⚪ Strategy Filter

The strategy filter plays a vital role in the entries and exits. By setting this filter, the bot can identify higher or lower price points at which to execute trades. Opting for higher values will make the bot target more long-term extreme points, resulting in fewer but potentially more significant signals. Conversely, lower values focus on short-term extreme points, offering more frequent signals focusing on immediate market movements.

How is it calculated?

This filter identifies significant price points within a specified dynamic range by applying linear regression to the absolute deviation of the range, smoothing out fluctuations, and determining the trend direction. The algorithm then normalizes the data and searches for extreme points.

⚪ External AI filter

The external AI filter allows traders to incorporate two external sources as signal filters. This feature is particularly useful for refining their signal accuracy with additional data inputs.

External sources can include any indicator applied to your TradingView chart that produces a plot as an output, such as a moving average, RSI, supertrend, MACD, etc. Traders can use these indicators of their choice to set filters for screening signals within the strategy.

This approach offers traders increased flexibility to select filters that align with their trading style. For instance, one trader might prefer to take trades when the price is above a moving average, while another might opt for trades when the MACD is below the MACD signal line. These external filters enable traders to choose options that best fit their trading strategies. See the example below. Note that the input sources for the External AI filter can be any indicator applied to the chart, and the input source per se does not make this strategy unique. The AI filter takes the selected input source and applies our function to it. So, if a trader selects RSI as an input filter, RSI is not unique, but how the source is computed within the AI functions is.

How is it calculated?

Once the external filters are selected and enabled within the settings panel, our AI function is applied to enhance the filter's ability to execute trades, even when the set conditions of the filter are not met. For instance, if a trader wants to take trades only when the price is above a moving average, the AI filter can actually execute trades even if the price is below the moving average.

The filter works by combining k-nearest Neighbors (KNN) with Geometric Brownian Motion (GBM) involves first using GBM to model the historical price trends of an asset, identifying patterns of drift and volatility. KNN is then applied to compare the current market conditions with historical instances, identifying the closest matches based on similar market behaviors. By examining the drift values of these nearest historical neighbors, KNN predicts the current trend's direction.

The AI adaptability value is a setting that determines how flexible the AI algorithm is when applying the external AI filter. Setting the adaptability to 10 indicates minimal adaptability, suggesting that the bot will strictly adhere to the set filter criteria. On the other hand, a higher adaptability value grants the algorithm more leeway to "think outside the box," allowing it to consider signals that may not strictly meet the filter criteria but are deemed viable trading opportunities by the AI.

█ Examples

In this example, the RSI is used to filter out signals when the RSI is below the smoothing line, indicating that prices are declining.

Note that the external filter is specifically designed to work with either 'LONG ONLY' or 'SHORT ONLY' modes; it does not apply when the bot is set to trade on 'BOTH' modes. For 'LONG ONLY' positions, the filter criteria are met when source 1 is greater than source 2 (source 1 >= source 2). Conversely, for 'SHORT ONLY' positions, the filter criteria require source 1 to be less than source 2 (source 1 <= source 2).

Examples of Filter Usage:

Long Signals: To receive long signals when the closing price is higher than a moving average, set Source 1 to the 'close' price and Source 2 to a moving average value. This setup ensures that signals are generated only when the closing price exceeds the moving average, indicating a potential upward trend.

█ Settings

⚪ Set Timeframe

Choosing the correct entry and exit timeframes is crucial for the bot's performance. The general guideline is to select a timeframe that is higher than the one currently displayed on the trading chart but still relatively close in duration. For instance, if trading on a 1-minute chart, setting the bot's Timeframe to 5 minutes is advisable.

⚪ Entry

Traders have the flexibility to configure the bot according to their trading strategy, allowing them to choose whether the bot should engage in long positions only, short positions only or both. This customization ensures that the bot aligns with the trader's market outlook and risk tolerance.

⚪ Pyramiding

Pyramiding functionality is available to enhance the bot's trading strategy. If the current position experiences a drawdown by a specified number of points, the bot is programmed to add new positions to the existing one, potentially capitalizing on lower prices to average down the entry cost. To utilize this feature, access the settings panel, navigate to 'Properties,' and look for 'Pyramiding' to specify the number of times the bot can re-enter the market (e.g., setting it to 2 allows for two additional entries).

⚪ Risk Management

The bot incorporates several risk management methods, including a regular stop loss, trailing stop, and risk-reward-based stop loss and exit strategies. These features assist traders in managing their risk.

Stop Loss

Trailing Stop

⚪ Trading on specific days

This feature allows trading on specific days by setting which days of the week the bot can execute trades on. It enables traders to tailor their strategies according to market behavior on particular days.

⚪ Alerts

Alerts can be set for entry, exit, and risk management. This feature allows traders to automate their trading strategy, ensuring timely actions are taken according to predefined criteria.

█ How is Crypto Punk calculated?

The Crypto Punk Bot is a trading bot that utilizes a combination of price action analysis and elements inspired by Geometric Brownian Motion (GBM) to generate buy and sell signals for cryptocurrencies. The bot focuses on analyzing the difference between high and low prices over various timeframes, alongside estimates of drift (trend) and volatility derived from GBM principles.

Timeframe Analysis for Price Action

The bot examines multiple timeframes (e.g., daily, weekly) to identify the range between the highest and lowest prices within each period. This range analysis helps in understanding market volatility and the potential for significant price movements. The algorithm calculates the trading range by applying maximum and minimum functions to the set of prices over your selected timeframe. It then subtracts these values to determine the range's width. This method offers a quantitative measure of the asset's price volatility for the specified period.

Estimating Drift (Trend)

The bot estimates the drift component, which reflects the underlying trend or expected return of the cryptocurrency. The algorithm does this by estimating the drift (trend) using Geometric Brownian Motion (GBM), which involves determining an asset's average rate of return over time, reflecting the asset's expected direction of movement.

Estimating Volatility

Volatility is estimated by calculating the standard deviation of the logarithmic returns of the cryptocurrency's price over the same timeframe used for the drift calculation. Geometric Brownian Motion (GBM) involves measuring the extent of variation or dispersion in the returns of an asset over time. In the context of GBM, volatility quantifies the degree to which the price of an asset is expected to fluctuate around its drift.

Combining Drift and Volatility for Signal Generation

The bot uses the calculated drift and volatility to understand the current market conditions. A higher drift coupled with manageable volatility may indicate a strong upward trend, suggesting a potential buy signal. Conversely, a low or negative drift with increasing volatility might suggest a weakening market, triggering a sell signal.

█ Strategy Properties

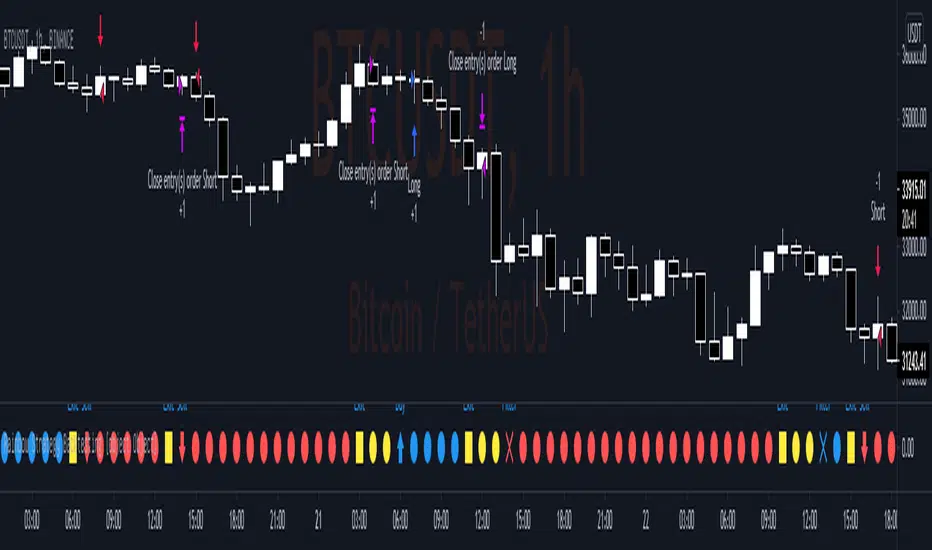

This script backtest is done on the 1 hour chart Bitcoin, using the following backtesting properties:

Balance (default): 10 000 (default base currency)

Order Size: 10% of the equity

Commission: 0.05 %

Slippage: 500 ticks

Stop Loss: Risk Reward set to 1

These parameters are set to provide an accurate representation of the backtesting environment. It's important to recognize that default settings may vary for several reasons outlined below:

Order Size: The standard is set at one contract to facilitate compatibility with a wide range of instruments, including futures.

Commission: This fee is subject to fluctuation based on the specific market and financial instrument, and as such, there isn't a standard rate that will consistently yield accurate outcomes.

We advise users to customize the Script Properties in the strategy settings to match their personal trading accounts and preferred platforms. This adjustment is crucial for obtaining practical insights from the deployed strategies.

-----------------

Disclaimer

The information contained in my Scripts/Indicators/Ideas/Algos/Systems does not constitute financial advice or a solicitation to buy or sell any securities of any type. I will not accept liability for any loss or damage, including without limitation any loss of profit, which may arise directly or indirectly from the use of or reliance on such information.

All investments involve risk, and the past performance of a security, industry, sector, market, financial product, trading strategy, backtest, or individual's trading does not guarantee future results or returns. Investors are fully responsible for any investment decisions they make. Such decisions should be based solely on an evaluation of their financial circumstances, investment objectives, risk tolerance, and liquidity needs.

My Scripts/Indicators/Ideas/Algos/Systems are only for educational purposes!

Ücretli komut dosyası

JS-TechTrading: Supertrend-Strategy_Basic versionAre you looking for a reliable and profitable algorithmic trading strategy for TradingView? If so, you might be interested in our Supertrend basic strategy, which is based on three powerful indicators: Supertrend (ATR), RSI and EMA.

Supertrend is a trend-following indicator that helps you identify the direction and strength of the market. It also gives you clear signals for entry and exit points based on price movements.

RSI is a momentum indicator that measures the speed and change of price movements. It helps you filter out false signals and avoid overbought or oversold conditions.

EMA is a moving average indicator that smooths out price fluctuations and shows you the long-term trend of the market. It helps you confirm the validity of your trades and avoid trading against the trend.

Our Supertrend basic strategy combines these three indicators to give you a simple yet effective way to trade any market. Here's how it works:

- For long trades, you enter when the price is above Supertrend and pulls back below it (the low of the candle crosses Supertrend) and then rebounds above it (the high of the next candle goes above the pullback candle). You exit when the price closes below Supertrend or when you reach your target profit or stop loss.

- For short trades, you enter when the price is below Supertrend and pulls back above it (the high of the candle crosses Supertrend) and then drops below it (the low of the next candle goes below the pullback candle). You exit when the price closes above Supertrend or when you reach your target profit or stop loss.

- You can also use RSI and EMA filters to improve your results. For long trades, you only enter if RSI is above 50 and price is above 200 EMA. For short trades, you only enter if RSI is below 50 and price is below 200 EMA.

- You can set your stop loss and target profit as a percentage of your entry price or based on other criteria. You can also adjust the parameters of each indicator according to your preferences and risk tolerance.

Our Supertrend basic strategy is easy to use and has been tested on various markets and time frames. It can help you capture consistent profits while minimizing your losses.

Mean Reversion and TrendfollowingTitle: Mean Reversion and Trendfollowing

Introduction:

This script presents a hybrid trading strategy that combines mean reversion and trend following techniques. The strategy aims to capitalize on short-term price corrections during a downtrend (mean reversion) as well as ride the momentum of a trending market (trend following). It uses a 200-period Simple Moving Average (SMA) and a 2-period Relative Strength Index (RSI) to generate buy and sell signals.

Key Features:

Combines mean reversion and trend following techniques

Utilizes 200-period SMA and 2-period RSI

Customizable starting date

Allows for enabling/disabling mean reversion or trend following modes

Adjustable position sizing for trend following and mean reversion

Script Description:

The script implements a trading strategy that combines mean reversion and trend following techniques. Users can enable or disable either of these techniques through the input options. The strategy uses a 200-period Simple Moving Average (SMA) and a 2-period Relative Strength Index (RSI) to generate buy and sell signals.

The mean reversion mode is active when the price is below the SMA200, while the trend following mode is active when the price is above the SMA200. The script generates buy signals when the RSI is below 20 (oversold) in mean reversion mode or when the price is above the SMA200 in trend following mode. The script generates sell signals when the RSI is above 80 (overbought) in mean reversion mode or when the price falls below 95% of the SMA200 in trend following mode.

Users can adjust the position sizing for both trend following and mean reversion modes using the input options.

To use this script on TradingView, follow these steps:

Open TradingView and load your preferred chart.

Click on the 'Pine Editor' tab located at the bottom of the screen.

Paste the provided script into the Pine Editor.

Click 'Add to Chart' to apply the strategy to your chart.

Please note that the past performance of any trading system or methodology is not necessarily indicative of future results. Always use proper risk management and consult a financial advisor before making any investment decisions.

------

The following is a summary of the underlying whitepaper (onlinelibrary.wiley.com) for this strategy:

This paper proposes a theory of securities market under- and overreactions based on two psychological biases: investor overconfidence about the precision of private information and biased self-attribution, which causes asymmetric shifts in investors' confidence as a function of their investment outcomes. The authors show that overconfidence implies negative long-lag autocorrelations, excess volatility, and public-event-based return predictability. Biased self-attribution adds positive short-lag autocorrelations (momentum), short-run earnings "drift," and negative correlation between future returns and long-term past stock market and accounting performance.

The paper explains that there is empirical evidence challenging the traditional view that securities are rationally priced to reflect all publicly available information. Some of these anomalies include event-based return predictability, short-term momentum, long-term reversal, high volatility of asset prices relative to fundamentals, and short-run post-earnings announcement stock price "drift."

The authors argue that investor overconfidence can lead to stock prices overreacting to private information signals and underreacting to public signals. This overreaction-correction pattern is consistent with long-run negative autocorrelation in stock returns, excess volatility, and further implications for volatility conditional on the type of signal. The market's tendency to over- or underreact to different types of information allows the authors to address the pattern that average announcement date returns in virtually all event studies are of the same sign as the average post-event abnormal returns.

Biased self-attribution implies short-run momentum and long-term reversals in security prices. The dynamic analysis based on biased self-attribution can also lead to a lag-dependent response to corporate events. Cash flow or earnings surprises at first tend to reinforce confidence, causing a same-direction average stock price trend. Later reversal of overreaction can lead to an opposing stock price trend.

The paper concludes by summarizing the findings, relating the analysis to the literature on exogenous noise trading, and discussing issues related to the survival of overconfident traders in financial markets.

[SPOILED]SuperTrench - ETH Super ScalperHi Traders,

I'm republishing this script as I finally polished it to perfection IMO. The script uses 5 coding sections: entry, trend filter, pivot filter, take profit, and stop loss. The script mainly uses trailing as take profit; this is probably the easiest way to make a profitable scalper strategy.

Backtest capital is set to 1000 USDT, 35% equity, 0.04% commission, limited backtest date from Jan 2022 to now, backtested on ETH/USDT prep contracts 15m timeframe, result as shown below.

It looks unreal right? Hell no, I actually tested this strategy on Binance from Dec 06 to Dec 10. I got 8.29% return with 4x leverage, 50% equity setup; 75% win rate,1.58 profit factor, with 4.3% max drawdown, it is amazingly close to the backtest result.

User Manual

Entry >>> Stoch RSI:

I added 5 MA types to the Stoch RSI which is HMA/VWMA/WMA/EMA/SMA, HMA with Length setting of 5, 8 seems to be most efficient, VWMA and WMA with 8, 13 will generate less entry signals but with less entry risks.

Entry >>> R Style:

It based on price action, with candlestick makes a U turn, after 2nd candlestick confirmed, it generates entry signal, this will give you some extra entries, better leave it enabled.

Entry >>> Price Step:

This probably is the core feature of this strategy; also my secret ingredient to making this strategy this efficient. It is recommended to enable step 1-5, more steps basically means more entries, but they are not necessarily profitable.

Trend Filter >>> Price Step:

I couldn't tell you much details about how this indicator works, but it is a reliable indicator, based on price action, and I got some ideas from Demark9 indicator. The bigger the level, the stronger the filter is, please note that if 'Price Step Entries' less than Price Step Trend, entries will be ignored.

Pivot Filter >>> RSI Pivot & Pinbar Pivot:

RSI Pivot detects if the RSI signal line making U turn in certain condition, Pinbar detection combines R Style entry when price action U turn took place, these 2 pivot filter will close the trade once it is counter trend, so it better enable and leave it as is.

Trend Filter >>> Trend Magic:

Trend Magic uses CCI and ATR to calculate trend status, green means uptrend, red means downtrend, pretty straight forward, the best value for this indicator would be, 21, 34, 55, 89.

Trend Filter >>> Alpha:

This filter combines R style pivot, price step, EMA all together to detects consolidation area, because EMA was involved, so the best look back period would be around 15-35, it is best to use default value IMO, in another hands, if you need stronger filter, feel free to use 10, 18, 20, 25, 30, 35, make sure look back period should increase or decrease by 5 every time.

Take Profit and Stop Loss:

The default value for tp is set to 0.4%, but I also give you option to switch to ATR TP; you can adjust in the ATR multiplier, default ATR trailing stop loss uses 1 ATR, but you can adjust it for better drawdown tolerance. Fixed ATR SL is also given when fixed ATR is enabled. There will be a failsafe SL default set to 1% if price moves counter direction of opened position, it will close trade no matter what happens.

Enjoy :)

Buy/Sell Signal Template/Boilerplate Strategy [MyTradingCoder]This script allows the user to connect an external indicator output/plot value to allow for a no-code solution to setup a simple buy/sell signal strategy. For those of you who do not know how to program, do not be intimidated as this is a very easy setup process.

Maybe you want to buy when the 'RSI' value drops below '30' and then sell when the 'RSI' value climbs above '70', but you don't want to code it. You can do that with this indicator along with thousands of others found on the free TradingView indicator library.

Step #1:

Put the strategy on the chart.

Step #2:

Apply a secondary indicator onto the chart, such as an RSI .

Step #3:

Open the strategy settings and change the source to the RSI

Step #4:

Change the 'Signal Settings' to match when you want a buy, or a sell. For example, if you want to get a buy signal when the RSI crosses above 50, and get a sell when it crosses below 50, set the 'buy value' to 50, and the 'buy type' to greater than, then set the 'sell value' to 50 and the 'sell type' to less than. BOOM! It works :)

RSITrendStrategyI don't know if there is any strategy based on RSI cross over. The strategy is designed based on RSI crossover, considering RSI(5) and RSI(11), with RSI(6) to identify highs & lows.

I used this strategy to trade in Nifty 50 & Nifty bank indices. Whenever there is long mentioned on chart, I go for buying call option with premium near to 300, and placing stoploss of 50 on candle closing basis, vice versa.

Target is open until short is mentioned on the chart. Sometimes, i used standard pivot points as well to mark my targets and also to trail my trades.

Customizable Non-Repainting HTF MACD MFI Scalper Bot Strategy v2Customizable Non-Repainting HTF MACD MFI Scalper Bot Strategy v2

This script was originally shared by Wunderbit as a free open source script for the community to work with. This is my second published iteration of this idea.

WHAT THIS SCRIPT DOES:

It is intended for use on an algorithmic bot trading platform but can be used for scalping and manual trading.

This strategy is based on the trend-following momentum indicator . It includes the Money Flow index as an additional point for entry.

This is a new and improved version geared for lower timeframes (15-5 minutes), but can be run on larger ones as well. I am testing it live as my high frequency trader.

HOW IT DOES IT:

It uses a combination of MACD and MFI indicators to create entry signals. Parameters for each indicator have been surfaced for user configurability.

Take profits are now trailing profits, and the stop loss is now fixed. Why? I found that the trailing stop loss with ATR in the previous version yields very good results for back tests but becomes very difficult to deploy live due to transaction fees. As you can see the average trade is a higher profit percentage than the previous version.

HOW IS MY VERSION ORIGINAL:

Now instead of using ATR stop loss, we have a fixed stop loss - counter intuitively to what some may believe this performs better in live trading scenarios since it gives the strategy room to move. I noticed that the ATR trailing stop was stopping out too fast and was eating away balance due to transaction fees.

The take profit on the other hand is now a trailing profit with a customizable deviation. This ensures that you can have a minimum profit you want to take in order to exit.

I have depracated the old ATR trailing stop as it became too confusing to have those as different options. I kept the old version for others that want to experiment with it. The source code still requires some cleanup, but its fully functional.

I added in a way to show RSI values and ATR values with a checkbox so that you can use the new an improved ATR Filter (and grab the right RSI values for the RSI filter). This will help to filter out times of very low volatility where we are unlikely to find a profitable trade. Use the "Show Data" checkbox to see what the values are on the indicator pane, then use those values to gauge what you want to filter out.

Both versions

Delayed Signals : The script has been refactored to use a time frame drop down. The higher time frame can be run on a faster chart (recommended on one minute chart for fastest signal confirmation and relay to algotrading platform.)

Repainting Issues : All indicators have been recoded to use the security function that checks to see if the current calculation is in realtime, if it is, then it uses the previous bar for calculation. If you are still experiencing repainting issues based on intended (or non intended use), please provide a report with screenshot and explanation so I can try to address.

Filtering : I have added to additional filters an ABOVE EMA Filter and a BELOW RSI Filter (both can be turned on and off)

Customizable Long and Close Messages : This allows someone to use the script for algorithmic trading without having to alter code. It also means you can use one indicator for all of your different alterts required for your bots.

HOW TO USE IT:

It is intended to be used in the 5-30 minute time frames, but you might be able to get a good configuration for higher time frames. I welcome feedback from other users on what they have found.

Find a pair with high volatility (example KUCOIN:ETH3LUSDT ) - I have found it works particularly well with 3L and 3S tokens for crypto. although it the limitation is that confrigurations I have found to work typically have low R/R ratio, but very high win rate and profit factor.

Ideally set one minute chart for bots, but you can use other charts for manual trading. The signal will be delayed by one bar but I have found configurations that still test well.

Select a time frame in configuration for your indicator calculations.

Select the strategy config for time frame (resolution). I like to use 5 and 15 minutes for scalping scenarios, but I am interested in hearing back from other community memebers.

Optimize your indicator without filters : customize your settings for MACD and MFI that are profitable with your chart and selected time frame calculation. Try different Take Profits (try about 2-5%) and stop loss (try about 5-8%). See if your back test is profitable and continue to optimize.

Use the Trend, RSI, ATR Filter to further refine your signals for entry. You will get less entries but you can increase your win ratio.

You can use the open and close messages for a platform integration, but I choose to set mine up on the destination platform and let the platform close it. With certain platforms you cannot be sure what your entry point actually was compared to Trading View due to slippage and timing, so I let the platform decide when it is actually profitable.

Limitations: this works rather well for short term, and does some good forward testing but back testing large data sets is a problem when switching from very small time frame to large time frame. For instance, finding a configuration that works on a one minute chart but then changing to a 1 hour chart means you lose some of your intra bar calclulations. There are some new features in pine script which might be able to address, this, but I have not had a chance to work on that issue.

CryptoAlgo DCA / AccumulationThis is a Dollar Cost Average (DCA) / Accumulation strategy. Every time there is a long signal it will buy a fixed USD amount that you have specified in the settings and keep buying at the dips and corrections in the market. This strategy is low-risk, however it assumes you have a long time horizon of at least 2+ years. The longer your holding-period, the better your returns.

There is 3 different entry conditions you can choose from:

The first entry condition is bollinger bands. Bollinger bands is a set of trendlines plotted two standard deviations (positively and negatively) away from a simple moving average (SMA) of an assets price. Every time a candle closes below the lower trendline the strategy will buy.

The second entry condition is the Relative Strength Index (RSI). The RSI is a momentum indicator used in technical analysis that measures the magnitude of recent price changes to evaluate overbought or oversold conditions in the price of a stock or other asset. Every time the RSI is meaning oversold and goes below a point of your choosing the strategy will buy.

The third entry condition is based on pivot points and moving averages that will determine small term trend changes in the market and low price points. Every time there is a bullish trend reversal the strategy will buy.

All three of these entry conditions can be controlled by a higher timeframe RSI that will stop entries when the RSI is above a certain point where the market is overbought and not ideal for accumulation.

The take profits in this strategy is dynamic and will signal trend changes like the third entry condition by using pivot points and moving averages. Since this is a DCA/ Accumulation strategy and will accumulate for the long term it will only exit a small percentage of the accumulated position. This will ensure that you take profit as the asset is appreciating in price while keeping the majority of the position for greater profit in the future.

At the bottom right corner of the chart you will be able to see the key results of the DCA

The first reading is the Average amount USD that the strategy is investing on average every month. This value will help you identify the best settings for you and what USD amount the strategy should enter at the signals so that it stays below the amount you are willing to invest every month. Keep in mind that this is an average and that there will be a lot of deviation up or down based on where the market is going. If the market is having a correction the strategy will signal a lot more entries than when it is going up.

The second reading is the average profit per month. This is also an average and the result will go up exponentially from the starting point as the strategy accumulates and the market appreciates in price.

The third reading is the position average price. This is the average price all the accumulated USD in the asset.

The fourth reading is the total profit. This is the result of both the realised profit from taking profit and the accumulated usd amount left in the position.

The last reading is the performance score. This is a scoring system that i created that looks at the data from the readings and weighs it based on importance and then spits out a number that will help identify the best settings. The higher the number the better the performance, meaning more profit and better DCA.

When you have found the right settings you can insert the messages from your automatic trading platform at the bottom of the inputs and then create an alert with your unique webhook address along with the alert message below:

{{strategy.order.alert_message}}

You will be able to adjust all parameters in the settings.

Enjoy!

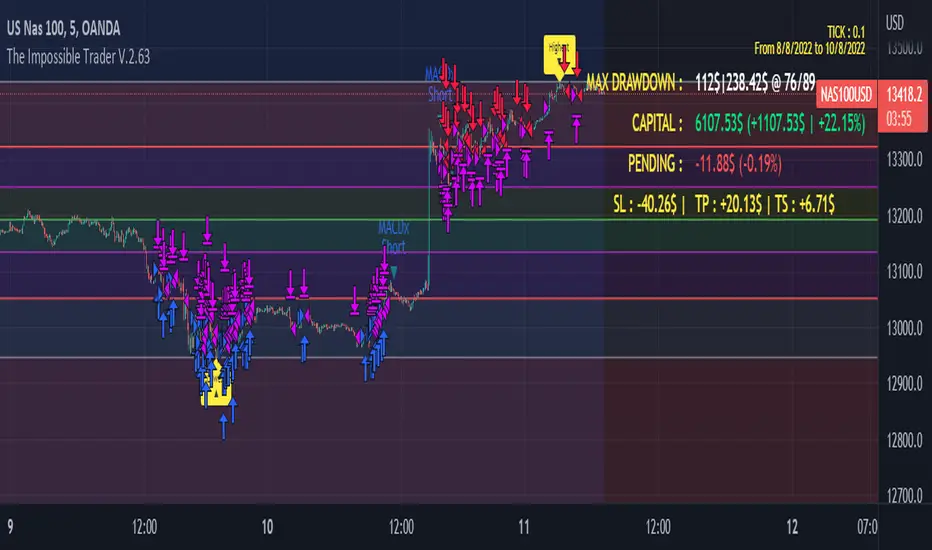

The Impossible TraderTHE IMPOSSIBLE TRADER

A simple, but effective High Freq Strategy script based on MACD or RSI trend, with extra customizable Alert Messages for Bots.

WHAT IT DOES

This script (works best at lower TimeFrames) just follow the trend of MACD or RSI on your asset.

Why it should work? Because in an upper trend, there are more chance of green candles than reds. And in dump trend there are more chance of red candles than greens.

While trend is positive, it will try to open Long orders as fast as possible at market price.

While trend is negative, it will try to open Short orders as fast as possible at market price.

HOW TO SETUP YOUR PREFERENCES

Capital : Insert a % of Margin you want to use for your positions (usually 30% is quite good)

Leverage : Choose leverage based on your plans

Trail Tick @ : This value (in Tick) tell the script "when" the "Trail Stop" order must be activated (from the Entry price)

Offset Tick @ : This is the price (in Tick) from the Trail Stop Price activated. Basically it is a Stop Loss that follow the price at a fixed distance.

SL Tick @ : Set a Stop Loss at amount Tick distance from the Entry Price. (Let's call it a Safety Stop Loss for bad decisions...)

TP Tick @ : Set a Take Profit at amount Tick distance from the Entry Price. Sometimes is better to exit in full Gain than keep positions.

Strategy : You can choose a Only Long, Only Short or Long+Short sametime strategy.

with MACD or RSI : You can try the strategy applied on MACD or applied on customizable RSI EMA

EMA : If you choosed RSI EMA, you can set any value for your testing (usually 80-120 works very nice)

Exit order after bars : Some Exchanges / Brokers apply fixed cost, and a strategy too fast could not be productive. This set will let you to delay the Exit Order on already Opened positions.

Keep Stop Loss active : If you are planning a delay for Exit Orders, sometime could be useful to keep activated Stop Loss.

Strategy Preset : Some preset I've found interesting, with good results.

BackTest Days : If there are too many results and script doesn't work, you can choose a closer range to show results.

EXTRA FEATURES

On Screen Display : OSD will show you some realtime stats about your strategy, like Asset Tick, Trading Period Range, Drawdown, Gains and not closed trade.

Alert Message : You can enter custom Long Entry/Exit and Short Entry/Exit message for your Bots (like AutoView, WunderBit, etc...). When alert is triggered, you can send custom message with {{strategy.order.comment}} in the text field

AutoView Alert Message : If you are user of AutoView, you can generate your calls. Those are tested only on Oanda with index like Sp500, US100, Us30.

TIPS ON USE

Some asset on TradingView require an higher initial capital. Go to this Script Settings -> Properties and rise Initial Capital.

Be aware of commissions and spread when evalutating a strategy. Go to this Script Settings -> Properties and set Commission and Slippage

Trail Stop and Ticks could be difficult to understand, but very profitable. Please take your time and study how it works.

Consider Tick like the minimum movement your asset can do. Ticks occurs "intra-bar", so some of your positions could be closed almost instantly.

Consider Trail Stop like a Stop Loss that keep always the same distance from your positions, but never came back . If you are in gain, say of 10 Ticks, and your Trail have 5 Ticks, this means for sure a close at minimum 5 Ticks from Entry Price.

On Screen Display will show you Ticks for your asset. This will help you on strategy settings, because not all asset responds on the same way.

ONLY LONG EXAMPLE

ONLY SHORT EXAMPLE

Pro Divergence [regular + hidden] by TradingClue█ Pro Divergence is my new divergence-based toolkit that will help you to spot lucrative opportunities in all kinds of markets.

I've developed toolkits and strategies that use divergences for many years, e.g. AutoDivergence and CCIDivergence . Pro Divergence is my latest development and benefits from those yearlong experiences.

The main algorithm to detect divergences has changed from using linear regressions and moving averages to algorithmic trendline detection like I've been using in TD Lines .

This new approach supports the detection of regular divergences but also hidden divergences can be identified.

Before going more into the details of the mechanics of Pro Divergence, let's recap, what divergences are all about when it comes to trading.

█ Regular Divergence

The basic idea is pretty simple: If price goes in the opposite direction than some other technical indicator - in most cases an oscillator - we speak of a divergence. A regular divergence might be a signal for a trend reversal. That's it.

For example, if the price is currently rising, while at the same time Momentum is falling - it might be time for a reversal and the price of an asset is about to fall soon. If there are additional indications to confirm the signal, e.g. if RSI is in the overbought area, it might be a good idea to go short on that specific asset.

Regular bullish divergences are indicated when price is forming lower lows while an oscillator shows higher lows.

Regular bearish divergences are indicated when price is forming higher highs while an oscillator shows lower highs.

█ Hidden Divergence

While regular divergences indicate trend reversals, hidden divergences indicate a trend continuation.

When the price is making higher lows and the oscillator is showing lower lows, we speak of a bullish hidden divergence. When the price is making lower highs and the oscillator shows higher highs, it's a bearish hidden divergence.

These rules for identifying divergences are pretty simple and straightforward. And they are also confusing at times. But that's what Pro Divergence is helping you with: trade based on customizable signals to identify all kinds of divergences.

You could either use the strategy settings of the toolkit to optimize the properties to show winning backtesting results. Or you use the signals as an extra confirmation to some other kind of signal/ strategy you are working with.

█ Summary of all current features

• Oscillator: choose between CCI, Momentum, MACD, or RSI. All oscillators-settings are customizable.

• RSI-filter: in some cases, the quality of the signals can be improved by an RSI filter, e.g. a bullish signal would only be valid if RSI is in the oversold area. Set the RSI period and the oversold/ overbought levels to your preferred values.

• You can display all divergences on the chart to get an idea of the current price action. Or you can pick any combination of signals you would like to include in a backtest. Possible signals are: regular bullish divergence, regular bearish divergence, hidden bullish divergence, hidden bearish divergence

• Exits: there are many ways to get exit signals - combinations of the below options are possible:

• fixed profit targets/ stop losses based on ticks

• Exit when momentum reverses

• Exit when price touches the opposite Bollinger Band (e.g. a long position will be closed when price touches the upper Bollinger Band). The settings for the Bollinger Bands are customizable.

• Entry: you can choose only to enter a trade if momentum is going in the same direction as the direction of your trade (e.g. only go long if momentum is rising)

• time and date filer

• Do a backtest only in a given time range (maybe you're not interested in the whole range of historical data when trading in a higher timeframe. Or you would like to do some kind of walk forward analysis)

• Only trade during special times of a day, e.g. only trade during the first hours of a trading session

Since this strategy is making heavy use of math and technical indicators, it is not tied to a certain asset class or timeframe. It was tested successfully on a large number of financial instruments like stocks, crypto, forex, and others.

ReversionStrategyThis strategy aims to identify condition of exhaustion to trade market reversal. It uses multiple indicators to enter a position. It uses following indicator:

1. RSI

2. ATR

Functionality of the Multi-Indicator:

1. RSI:

If RSI value is more then 70(input parameter) then market is over-brought. When less than 30 (input parameter) then market is over sold. Over brought or over sold market are good to play reversal.

2. ATR:

If current bar atr is more than 20 period (input) atr then it indicates over extended move.

3. Candle structure:

If a big candle closes near (within 10%) to its high then it indicates exhaustion. Same when big candle closes near to lows.

The combination of above 3 identifies buy or sell condition. Stop loss is 1.5 times atr. These parameter are input.

Sell condition:

1. RSI is more than 70

2. Current bar ATR is more than 20 perios ATR

3. Candle closes within 10% of its high.

If above 3 conditions are met on a candle then it indicates exhaustion of up move and sell order should be opened on next candle.

Buy condition:

1. RSI is less than 30

2. Current bar ATR is more than 20 perios ATR

3. Candle closes within 10% of its lows.

If above 3 conditions are met on a candle then it indicates exhaustion of down move and buy order should be opened on next candle.

MZ SRSI Strategy V1.0Strategy Introduction

This strategy starts from selection of 1st Moving Average from one of following:

SMA

EMA

DEMA

TEMA

LRC

WMA

MF

VAMA

TMA

HMA

JMA

Kijun v2

EDSMA

McGinley

Then it calculates the RSI of selected 1st Moving Average

In the end it calculates Moving Average of previously calculated RSI and for this purpose 2nd Moving Average is also selected from above list.

Cross of RSI and its Moving Average generates Strategy Alerts

Only long trades are enabled currently

Default Settings

I've set the default selection to the perfect options for 1D and 4h timeframes. You can modify both MAs selection and their length according to your selected timeframe.

Following default settings are used:

Heiken Ashi Candles are selected by default as source

1st Moving Average selection is set to LRC (Linear Regression Curve)

Length of 1st Moving Average is set to 50

RSI length is set to 2 because it is supposed to be fast

2nd Moving Average of RSI is set to TMA (Triangular Moving Average)

Length of 1st Moving Average is set to 5

Start date is set to 2011

Backtesting can also be done selecting %age of equity

Suggestions for Usage

Mostly winning trades have no prominent drawdown so losing trades can be abolished with Stoploss. Would soon add Stoploss, MTF and Takeprofit options in next version. Also if you want an alerts version of it then just comment below and would publish it later. I’ve found this strategy useful on 1D and 4h timeframes with described default settings.

Smoothed Waddah ATR~~~All Credit to LAZY BEAR for posting the original Script which is an old MT4 indicator.~~~~

No this system does not repaint... if it does let me know. Either the code is wrong or you are using a repainting chart such as renko candles.

*PURPOSE*

This Is an "Enhanced or Smoothed" version of the script that captures the heiken-ashi closing price as its main calculation variable. While using normal bar or line charts. Enhancements integrate trade filters to reduce false signals.

*WHAT TYPE OF TRADING STRATEGY IS THIS?*

This is a Long Only, Trend Trading System. Is intended to be applied to Charts/Timeframes that produce sustainable trends for which ever asset you are trading.

*NOTE OF ADVICE REGARDING SETTINGS*

Settings can be tweaked but I have found that best results come with the given settings. If a chart is too choppy to trade this indicator successfully, it is advised not to change the settings but either find a different timeframe or different asset to apply this strategy to.

TLDR

Indicator measures the change of the MacD (difference between MAC D of given EMA's) and compares it to the difference between the Upper and Lower Bollinger bands. Green bar over trigger line= entry. Red bar over trigger line = close.

*SETTINGS AND INPUTS*

-MacD of HeikenAshi chart (will always be of the Heikenashi chart even when applied to different chart type)

sensitivity = input(150, title='Sensitivity') =range should be (125-175)multiplier so that MacD can be compared to BB

fastLength = input(20, title='MacD FastEMA Length')

slowLength = input(40, title='MacD SlowEMA Length')

-Bollinger Band of currently used price chart type

channelLength = input(20, title='BB Channel Length')

mult = input(1.5, title='BB Stdev Multiplier')

-14 Period RSI Trade Filter (set to 0 to Disable)

RSI14filter = input(40, title='RSI Value trade filter') =only gives entry when RSI is higher than given value

*ABSTRACT & CONCEPT*

TLDR - Indicator measures the change of the MacD (difference between MAC D of given EMA's) and compares it to the difference between the Upper and Lower Bollinger bands. Green bar over trigger line= entry. Red bar over trigger line = close.

Indicator plots -

Bars are the change in the MAC D and the indicator line is the difference in the BB.

When Bars are higher than the indicator line then it is considered a trend "Explosion"

Green Bars are Trend Explosion to the upside, Red Bars are Trend explosion to the downside.

GENERAL DETAIL-

the core calculation is measuring the change in MacD of current candle compared to the MacD of two previous candles.

This value is multiplied by the sensitivy so it can be compared to the change in Bollinger Band Width.

if the MACD change is positive then you get a green/lime bar for that value. If the MacDchange is negative you get a red/orange bar for that value.

and are determined by whether the actual change is increasing in that direction or decreasing. (bars getting taller or bars getting shorter)

Entry signal for long is A positive change in MACD difference (Green bar) that is greater than the change of the bollinger band (orange signal line) AND if the RSI value is above your filter.

Close signal or Trend Stop Warning Signal is given when a Negative MacD Difference (red bar) is greater than the change of the bollinger band (orange Line)

*CONSIDERATIONS AND THOUGHTS*

I have over 150 iterations of this indicator and this is the most consistent and best version of settings and filters I was able to generate. I built this indicator specifically for 3 charts. SPY monthly, QQQ monthly, BTC 3 Day. However this indicator works well on any long term bullish chart. (tech stocks are great) .

Trend trading systems are intended to be homerun hitting, plunge protecting indicators that allow for long legs and expanding volatility. This indicator does this as the trigger line is Dynamic with the expansion and contraction of the bollinger band.

I do not take every signal specifically not the close signals. Instead they more like warnings in ultra bullish environments.

If i had to pair this indicator with any other filter than the RSI, it would be a long term moving average i.e. the 50 week or equivalent for your chart. signals above rising moving averages means that you are trading with an upward trending market.

Hope this helps. Happy trades.

-SnarkyPuppy