IU Indicators DashboardDESCRIPTION

The IU Indicators Dashboard is a comprehensive multi-stock monitoring tool that provides real-time technical analysis for up to 10 different stocks simultaneously. This powerful indicator creates a customizable table overlay that displays the trend status of multiple technical indicators across your selected stocks, giving you an instant overview of market conditions without switching between charts.

Perfect for portfolio monitoring, sector analysis, and quick market screening, this dashboard consolidates critical technical data into one easy-to-read interface with color-coded trend signals.

USER INPUTS

Stock Selection (10 Configurable Stocks):

- Stock 1-10: Customize any symbols (Default: NSE:CDSL, NSE:RELIANCE, NSE:VEDL, NSE:TCS, NSE:BEL, NSE:BHEL, NSE:TATAPOWER, NSE:TATASTEEL, NSE:ITC, NSE:LT)

Technical Indicator Parameters:

- EMA 1 Length: First Exponential Moving Average period (Default: 20)

- EMA 2 Length: Second Exponential Moving Average period (Default: 50)

- EMA 3 Length: Third Exponential Moving Average period (Default: 200)

- RSI Length: Relative Strength Index calculation period (Default: 14)

- SuperTrend Length: SuperTrend indicator period (Default: 10)

- SuperTrend Factor: SuperTrend multiplier factor (Default: 3.0)

Visual Customization:

- Table Size: Choose from Normal, Tiny, Small, or Large

- Table Background Color: Customize dashboard background

- Table Frame Color: Set frame border color

- Table Border Color: Configure border styling

- Text Color: Set text display color

- Bullish Color: Color for positive/bullish signals (Default: Green)

- Bearish Color: Color for negative/bearish signals (Default: Red)

LOGIC OF THE INDICATOR

The dashboard employs a multi-timeframe analysis approach using five key technical indicators:

1. Triple EMA Analysis

- Compares current price against three different EMA periods (20, 50, 200)

- Bullish Signal: Price above EMA level

- Bearish Signal: Price below EMA level

- Provides short-term, medium-term, and long-term trend perspective

2. RSI Momentum Analysis

- Uses 14-period RSI with 50-level threshold

- Bullish Signal: RSI > 50 (upward momentum)

- Bearish Signal: RSI < 50 (downward momentum)

- Identifies momentum strength and potential reversals

3. SuperTrend Direction

- Utilizes SuperTrend with configurable length and factor

- Bullish Signal: SuperTrend direction = -1 (uptrend)

- Bearish Signal: SuperTrend direction = 1 (downtrend)

- Provides clear trend direction with volatility-adjusted signals

4. MACD Histogram Analysis

- Uses standard MACD (12, 26, 9) histogram values

- Bullish Signal: Histogram > 0 (bullish momentum)

- Bearish Signal: Histogram < 0 (bearish momentum)

- Identifies momentum shifts and trend confirmations

5. Real-time Data Processing

- Implements request.security() for multi-symbol data retrieval

- Uses barstate.isrealtime logic for accurate live data

- Processes data only on the last bar for optimal performance

WHY IT IS UNIQUE

Multi-Stock Monitoring

- Monitor up to 10 different stocks simultaneously on a single chart

- No need to switch between multiple charts or timeframes

Highly Customizable Interface

- Full color customization for personalized visual experience

- Adjustable table size and positioning

- Clean, professional dashboard design

Real-time Analysis

- Live data processing with proper real-time handling

- Instant visual feedback through color-coded signals

- Optimized performance with smart data retrieval

Comprehensive Technical Coverage

- Combines trend-following, momentum, and volatility indicators

- Multiple timeframe perspective through different EMA periods

- Balanced approach using both lagging and leading indicators

Flexible Configuration

- Easy symbol switching for different markets (NSE, BSE, NYSE, NASDAQ)

- Adjustable indicator parameters for different trading styles

- Suitable for both swing trading and position trading

HOW USERS CAN BENEFIT FROM IT

Portfolio Management

- Quick Portfolio Health Check: Instantly assess the technical status of your entire stock portfolio

- Diversification Analysis: Monitor stocks across different sectors to ensure balanced exposure

- Risk Management: Identify which positions are showing bearish signals for potential exit strategies

- Rebalancing Decisions: Spot strongest performers for potential position increases

Market Screening and Analysis

- Sector Rotation: Compare different sector stocks to identify rotation opportunities

- Relative Strength Analysis: Quickly identify which stocks are outperforming or underperforming

- Market Breadth Assessment: Gauge overall market sentiment by monitoring diverse stock selections

- Trend Confirmation: Validate market trends by observing multiple stock behaviors

Time-Efficient Trading

- Single-Glance Analysis: Get complete technical overview without chart-hopping

- Pre-Market Preparation: Quickly assess overnight changes across multiple positions

- Intraday Monitoring: Track multiple opportunities simultaneously during trading hours

- End-of-Day Review: Efficiently review all watched stocks for next-day planning

Strategic Decision Making

- Entry Point Identification: Spot stocks showing bullish alignment across multiple indicators

- Exit Signal Recognition: Identify positions showing deteriorating technical conditions

- Swing Trading Opportunities: Find stocks with favorable technical setups for swing trades

- Long-term Investment Guidance: Use 200 EMA signals for long-term position decisions

Educational Benefits

- Pattern Recognition: Learn how different indicators behave across various market conditions

- Correlation Analysis: Understand how stocks move relative to each other

- Technical Analysis Learning: Observe multiple indicator interactions in real-time

- Market Sentiment Understanding: Develop better market timing skills through multi-stock observation

Workflow Optimization

- Reduced Chart Clutter: Keep your main chart clean while monitoring multiple stocks

- Faster Analysis: Complete technical analysis of 10 stocks in seconds instead of minutes

- Consistent Methodology: Apply the same technical criteria across all monitored stocks

- Alert Integration: Easy visual identification of stocks requiring immediate attention

This indicator is designed for traders and investors who want to maximize their market awareness while minimizing analysis time. Whether you're managing a portfolio, screening for opportunities, or learning technical analysis, the IU Indicators Dashboard provides the comprehensive overview you need for better trading decisions.

DISCLAIMER :

This indicator is not financial advice, it's for educational purposes only highlighting the power of coding( pine script) in TradingView, I am not a SEBI-registered advisor. Trading and investing involve risk, and you should consult with a qualified financial advisor before making any trading decisions. I do not guarantee profits or take responsibility for any losses you may incur.

"relative strength" için komut dosyalarını ara

EMA Crossover Visual Setup (RS Clásico Confirmado)Overview

This script is designed to visually highlight classic swing trading setups based on the crossover of exponential moving averages (EMAs), with additional confirmation using Relative Strength (RS) compared to a benchmark asset (e.g., SPY).

The goal is to identify bullish momentum shifts that align both with technical structure (EMA crossover) and relative outperformance, helping traders focus on strong stocks in strong markets.

Logic

A signal is triggered when the following conditions are met:

The fast EMA (e.g., 10) crosses above the slow EMA (e.g., 20).

The closing price is above a third EMA (e.g., 50) to confirm bullish structure.

The asset's Relative Strength (RS) versus a benchmark is confirmed manually, based on an RSI comparison (not calculated inside the script).

The script is meant to be used alongside manual RS confirmation, using a secondary chart or overlay of the RS ratio.

Features

Visual labels and markers for clean charting of valid entry setups

Fully customizable EMA lengths

Optional highlighting of candle patterns near entry

Ideal for use with top-down analysis and watchlist filtering

Suggested Use

Works best on daily and 4H charts for swing trading setups

Combine with volume and price action analysis for higher probability trades

Use manual RS validation: confirm that the RSI of the selected stock is stronger than the RSI of SPY (or any benchmark of your choice)

Notes

This script does not execute trades or include stop loss/take profit logic, as it is intended for discretionary traders who want to visually scan for opportunities.

It also does not calculate RS internally, allowing flexibility in how you define strength (RS line, RSI comparison, or price ratio).

Liqudation HeatMap [BigBeluga]🔵 OVERVIEW

An advanced liquidity visualization tool that plots horizontal heat zones to highlight where potential liquidations and volume clusters are most likely hiding beneath price action.

Liqudation HeatMap scans historical price movements for local highs and lows with elevated volume or candle range. It then draws dynamic heatmap boxes—shaded from lime (low interest) to yellow (high interest)—revealing potential zones of trapped positions or stop clusters. A vertical scale on the right shows you the relative strength of volume behind each level, from 0 to the highest detected.

🔵 CONCEPTS

Maps areas of potential liquidity using volume or candle range (if volume is unavailable).

Identifies swing highs/lows (pivots) and extends heatmap boxes outward from these levels. Colors each zone based on the relative strength of volume concentration.

Fades or removes zones once price crosses their midpoints, simulating the idea of liquidity being “consumed.”

Displays a live vertical scale that shows the volume range for quick reference.

🔵 FEATURES

Dynamic Heatmap Zones:

Draws few boxes above and after pivot highs and below pivot lows, each shaded based on volume concentration.

Smart Coloring System:

Uses a gradient from lime (low) to yellow (high) to visually distinguish between weak and strong liquidity zones.

Adaptive ATR Widths:

Automatically adjusts zone thickness based on volatility (ATR), scaling intelligently across timeframes.

Liquidity Consumption Logic:

Zones are stope extending once price interacts with them—mimicking the behavior of real liquidation sweeps.

Volume Scale Legend:

A real-time scale is plotted on the right side, showing the min-max range of volume used for heat calculations.

🔵 HOW TO USE

Look for thick yellow zones to identify areas of concentrated stop losses or liquidation triggers.

Use these levels to anticipate mean reversion points or high-volatility zones.

Combine with your trend or structure tools to trade into or fade these liquidity pools.

On lower timeframes, use this tool to confirm entries around sweeps or deviations.

Use the right-side scale to compare relative zone strength instantly.

🔵 CONCLUSION

Liqudation HeatMap is a powerful visualization tool that uncovers where liquidity likely resides on the chart. By highlighting hidden traps and reactive levels in real-time, it gives traders a significant edge when it comes to spotting stop hunts, mean reversions, and areas of institutional interest. Whether you’re scalping or swing trading, this heatmap provides unmatched context on the market’s hidden intent.

FX Majors (+CN) Currency Basket ComparisonDescription:

This indicator shows how individual FX major currencies (including CNY) have performed relative to each other. It calculates each currency's performance against a "Trade Weighted" basket of other major currencies.

I created this because I couldn't find it, and I wanted an easy way to see currency behaviour and flows.

Purpose:

It lets you see the relative strength and weakness of each currency, similar to how the DXY measures USD strength, but for all the major currencies. Each basket and currency weights are based on Trade Weighted values from literature/economics.

This way you can maybe decide which crosses / pairs to trade.

Can helps you visualise how events (economic, news or otherwise) affect currency flows.

Features:

Relative Performance: Focuses on how a currency's value has changed over time, rather than its absolute level.

Normalization: Adjusts currency values to a starting date, making it easy to compare their performance.

Adjustable Start Date: You can set the anchor date to choose the starting point for calculating relative performance.

Customizable Weights: The indicator allows you to use custom weights for each currency basket should you wish.

ETI IndicatorThe Ensemble Technical Indicator (ETI) is a script that combines multiple established indicators into one single powerful indicator. Specifically, it takes a number of technical indicators and then converts them into +1 to represent a bullish trend, or a -1 to represent a bearish trend. It then adds these values together and takes the running sum over the past 20 days.

The ETI is composed of the following indicators and converted to +1 or -1 using the following criteria:

Simple Moving Average (10 days) : When the price is above the 10-day simple moving averaging, +1, when below -1

Weighted Moving Average (10 days) : Similar to the SMA 10, when the the price is above the 10-day weighted moving average, +1, when below -1

Stochastic K% : If the current Stochastic K% is greater than the previous value, then +1, else -1.

Stochastic D% : Similar to the Stochastic K%, when the current Stochastic D% is greater than the previous value, +1, else -1.

MACD Difference : First subtract the MACD signal (i.e. the moving average) from the MACD value and if the current value is higher than the previous value, then +1, else -1.

William's R% : If the current William's R% is greater than the previous one, then +1, else -1.

William's Accumulation/Distribution : If the current William's AD value is greater than the previous value, then +1, else -1.

Commodity Channel Index : If the Commodity Channel Index is greater than 200 (overbought), then -1, if it is less than -200 (oversold) then +1. When it is between those values, if the current value is greater than the previous value then +1, else -1.

Relative Strength Index : If the Relative Strength Index is over 70 (overbought) then -1 and if under 30 (oversold) then +1. If the Relative Strength Indicator is between those values then if the current value is higher than the previous value +1, else -1.

Momentum (9 days) : If the momentum value is greater than 0, then +1, else -1.

Again, once these values have been calculated and converted, they are added up to produce a single value. This single value is then summed across the previous 20 candles to produce a running sum.

By coalescing multiple technical indicators into a single value across time, traders can better understand how multiple inter-related indicators are behaving at once; high scores indicate that numerous indicators are showing bullish signals indicating a potential or ongoing uptrend (and vice-versa with low scores).

Additional Features

Numerous smoothing transformations have also been added (e.g. gaussian smoothing) to remove some of the noise might exist.

Suggested Use

It is recommended that stocks are shorted when the cross below 0, and are bought when the ETI crosses above -40. Arrows can be shown on the indicator to show these points. However feel free to use levels that work best for you.

Traditionally, I have treated values above +50 as overbought and below -40 as undersold (with -80 indicating extremely oversold); however these levels could also indicate either upwards and downwards momentum so taking a position based on where the ETI is (rather than crossing levels) should be done with caution.

Multi Scanner Plot & Table V1Here's how to interpret each column in the table:

Price vs MAs:

What it shows: Where the current price is relative to the short-term (e.g., 20-period) and long-term (e.g., 50-period) Simple Moving Averages (SMAs) calculated on your current chart's timeframe.

Interpretation:

Above Both (Green background): Price is above both the short and long MAs. Generally considered a bullish sign for the current trend.

Below Both (Red background): Price is below both MAs. Generally considered a bearish sign.

Mixed (Gray background): Price is between the two MAs (e.g., above the short but below the long, or vice-versa). Indicates indecision or a potential trend change.

RSI Value:

What it shows: The actual numerical value of the Relative Strength Index (RSI) calculated on your current chart's timeframe.

Interpretation: Just the raw RSI number (e.g., 65.32). The background is always gray. You compare this value to standard overbought/oversold levels (like 70/30) or the levels defined in the script's inputs.

RSI Status:

What it shows: Interprets the RSI Value based on the Overbought/Oversold levels set in the script's inputs (default 70/30). Calculated on your current chart's timeframe.

Interpretation:

Overbought (Red background): RSI is above the overbought level (e.g., > 70). Suggests the asset might be due for a pullback or reversal downwards. Red indicates a potentially bearish condition.

Oversold (Green background): RSI is below the oversold level (e.g., < 30). Suggests the asset might be due for a bounce or reversal upwards. Green indicates a potentially bullish condition.

Neutral (Gray background): RSI is between the oversold and overbought levels.

Last Sig Price:

What it shows: The price level where the last "SIG NOW" Buy or Sell signal occurred on your current chart's timeframe.

Interpretation: Helps you see the entry price of the most recent short-term signal generated by this script. The background color matches the signal type: Green for the last Buy signal, Red for the last Sell signal. N/A if no signal has occurred yet.

SIG NOW:

What it shows: This is the main short-term signal generated by the script based on conditions on your current chart's timeframe. It combines the "Price vs MAs" status and specific RSI conditions (price must be above/below both MAs and RSI must be within a certain range defined in the inputs).

Interpretation:

BUY (Green background): The specific buy conditions are met right now. (Price above both MAs AND RSI is strong but not necessarily overbought).

SELL (Red background): The specific sell conditions are met right now. (Price below both MAs AND RSI is weak but not necessarily oversold).

NEUTRAL (Gray background): Neither the Buy nor the Sell conditions are currently met.

ALERT:

What it shows: Flags unusual volume activity on the current bar compared to the recent average volume (calculated on your current chart's timeframe).

Interpretation:

SPIKE (Yellow background, black text): Current volume is significantly higher than the recent average (defined by the Volume Spike Multiplier). Can indicate strong interest or a potential climax.

DUMP (Purple background): Current volume is significantly lower than the recent average (defined by the Volume Dump Multiplier). Can indicate fading interest.

NONE (Gray background): Volume is within the normal range for the lookback period.

SD$:

What it shows: The price level where the last Volume Spike or Dump occurred on your current chart's timeframe.

Interpretation: Shows the price associated with the most recent significant volume event. The background color indicates the type of the last event: Green if the last event was a Spike, Red if the last event was a Dump. N/A if no Spike/Dump has occurred yet.

BB Value (%B):

What it shows: This relates to Bollinger Bands, but specifically calculated on a Higher Timeframe (HTF) that you can set in the inputs (e.g., Daily BBs while viewing an Hourly chart). It shows the Bollinger Band Percent B (%B) value for that HTF. %B measures where the HTF closing price is relative to the HTF upper and lower bands.

Interpretation:

Value > 1: HTF price closed above the HTF upper Bollinger Band.

Value < 0: HTF price closed below the HTF lower Bollinger Band.

Value between 0 and 1: HTF price closed within the HTF Bollinger Bands (e.g., 0.5 is exactly on the middle band).

The background is always gray.

LTS (Long Term Signal):

What it shows: A signal derived only from the Higher Timeframe (HTF) Bollinger Bands.

Interpretation:

BUY (Green background): The HTF price closed above the HTF upper Bollinger Band (see BB Value > 1). Considered a strong bullish signal from the higher timeframe perspective.

SELL (Red background): The HTF price closed below the HTF lower Bollinger Band (see BB Value < 0). Considered a strong bearish signal from the higher timeframe perspective.

NEUTRAL (Gray background): The HTF price closed within the HTF Bollinger Bands.

How to Understand Bollinger Bands and Signals in this Context:

Bollinger Bands are primarily used for the Long Term Signal (LTS) column. This script calculates BBs on a higher timeframe (you choose which one, or it defaults to the chart's timeframe if left blank).

The "LTS" signal triggers:

A BUY when the price on that higher timeframe closes above its upper Bollinger Band. This often indicates strong momentum or a potential breakout.

A SELL when the price on that higher timeframe closes below its lower Bollinger Band. This often indicates strong negative momentum or a potential breakdown.

The "BB Value" column gives you the raw %B number from that same higher timeframe, showing you exactly where the price is relative to the bands (is it just barely above/below, or way outside?).

The script does not directly use Bollinger Bands from the current chart timeframe for the "SIG NOW" or other table signals. The main short-term signals ("SIG NOW") rely on Moving Averages and RSI on the current timeframe. The LTS provides a longer-term perspective using HTF Bollinger Bands.

In summary: Look at the table to quickly gauge:

Short-term trend (Price vs MAs).

Short-term momentum (RSI Status, SIG NOW).

Recent short-term entry points (Last Sig Price).

Current volume anomalies (ALERT).

Long-term strength/weakness based on HTF Bollinger Bands (LTS, BB Value).

Combine these pieces of information to get a more rounded view of the current market conditions according to this specific script's logic.

Volume Flow RatioVolume Flow Ratio (VFR) Indicator

Overview

The Volume Flow Ratio (VFR) is a sophisticated volume analysis tool that measures current trading volume relative to the maximum volume of the previous period. Unlike traditional volume indicators that show raw volume or simple moving averages, VFR provides context by comparing current activity to recent maximum activity levels.

Core Features

1. Split Period Analysis

- Multiple Timeframe Options:

- Daily: Compares to previous day's maximum

- Weekly: Week-to-week comparison

- NYSE Weekly: Specialized for stock market trading (Monday-Friday only)

- Monthly: Month-to-month analysis

- Quarterly: Quarter-to-quarter perspective

- Yearly: Year-over-year volume comparison

2. Ratio-Based Measurement

- Displays volume as a ratio (0 to 1+) rather than raw numbers

- 1.0 represents volume equal to previous period's maximum

- Example: If previous max was 50,000 contracts:

- Current volume of 25,000 shows as 0.5

- Current volume of 75,000 shows as 1.5

3. Triple Coloring Modes

- Moving Average Based:

- Compares current ratio to its moving average

- Customizable MA period

- Green: Above MA (higher than average activity)

- Red: Below MA (lower than average activity)

- Previous Candle Comparison:

- Simple increase/decrease from previous bar

- Green: Higher than previous bar

- Red: Lower than previous bar

- Candle Color Based:

- Syncs with price action

- Green: Bullish candles (close > open)

- Red: Bearish candles (close < open)

Primary Use Cases

1. Volume Profile Analysis

- Perfect for traders who need to understand when markets are most active

- Helps identify unusual volume spikes relative to recent history

- Useful for timing entries and exits based on market participation

2. Market Activity Traders

Ideal for traders who:

- Need to identify high-liquidity periods

- Want to avoid low-volume periods

- Look for volume breakouts or divergences

- Trade based on institutional participation levels

3. Mean Reversion Traders

Helps identify:

- Overextended volume conditions (potential reversals)

- Volume exhaustion points

- Return to normal volume levels after spikes

4. Momentum Traders

Useful for:

- Confirming trend strength through volume

- Identifying potential trend exhaustion

- Validating breakouts with volume confirmation

Advantages Over Traditional Volume Indicators

1. Contextual Analysis

- Shows relative strength rather than raw numbers

- Easier to compare across different time periods

- Automatically adjusts to changing market conditions

2. Period-Specific Insights

- Respects natural market cycles (daily, weekly, monthly)

- Special handling for NYSE trading days

- Eliminates weekend noise in stock market analysis

3. Flexible Visualization

- Three distinct coloring methods for different trading styles

- Clear reference line at 1.0 for quick analysis

- Histogram style for easy pattern recognition

Best Practices

For Day Traders

- Use Daily split for intraday volume patterns

- MA coloring mode with shorter periods (5-10)

- Focus on ratios during market hours

For Swing Traders

- Weekly or NYSE Weekly splits

- Longer MA periods (15-20)

- Look for sustained volume patterns

For Position Traders

- Monthly or Quarterly splits

- Candle color mode for trend confirmation

- Focus on major volume shifts

Limitations

- Requires one full period to establish baseline

- May be less effective in extremely low volume conditions

- NYSE Weekly mode specific to stock market hours

This indicator is particularly valuable for traders who understand that volume is a crucial component of price action but need a more sophisticated way to analyze it than simple volume bars. It's especially useful for those who trade based on market participation levels and need to quickly identify whether current volume is significant relative to recent history.

Adaptable Relative Momentum Index [ParadoxAlgo]The Adaptable Relative Momentum Index (RMI) by ParadoxAlgo is an advanced momentum-based indicator that builds upon the well-known RSI (Relative Strength Index) concept by introducing a customizable momentum length. This indicator measures price momentum over a specified number of periods and applies a Rolling Moving Average (RMA) to both the positive and negative price changes. The result is a versatile tool that can help traders gauge the strength of a trend, pinpoint overbought/oversold levels, and potentially identify breakout opportunities.

⸻

Smart Configuration Feature

What sets this version of the RMI apart is ParadoxAlgo’s exclusive “Smart Configuration” functionality. Instead of manually adjusting parameters, traders can simply select their Asset Class (e.g., Stocks, Forex, Futures/Indices, Crypto, Commodities) and Trading Style (e.g., Scalping, Day Trading, Swing Trading, Short-Term Investing, Long-Term Investing). Based on these selections, the indicator automatically optimizes its core parameters:

• Length – The period over which the price changes are smoothed.

• Momentum Length – The number of bars used to calculate the price change.

By automating this process, users save time on tedious trial-and-error adjustments, ensuring that the RMI’s settings are tailored to the characteristics of specific markets and personal trading horizons.

⸻

Key Features & Benefits

1. Momentum-Based Insights

• Uses RMA to smooth price movements, helping identify shifts in market momentum more clearly than a basic RSI.

• Enhanced adaptability for a wide range of asset classes and time horizons.

2. Simple Yet Powerful Configuration

• Smart Configuration automatically sets optimal parameter values for each combination of asset class and trading style.

• Eliminates guesswork and manual recalibration when switching between markets or timeframes.

3. Overbought & Oversold Visualization

• Integrated highlight zones mark potential overbought and oversold extremes (default at 80 and 20).

• Optional breakout highlighting draws attention to times when the indicator crosses these key thresholds, helping spot possible entry or exit signals.

4. Intuitive Design & Ease of Use

• Clean plotting and color-coded signal lines make it easy to interpret bullish or bearish shifts in momentum.

• Straightforward dropdown menus keep the interface user-friendly, even for novice traders.

⸻

Practical Applications

• Early Trend Detection: Spot emerging trends when the RMI transitions from oversold to higher levels or vice versa.

• Breakout Confirmation: Confirm potential breakout trades by tracking overbought/oversold breakouts alongside other technical signals.

• Support/Resistance Confluence: Combine RMI signals with horizontal support/resistance levels to reinforce trade decisions.

• Trade Timing: Quickly gauge when momentum could be shifting, helping you time entries and exits more effectively.

⸻

Disclaimer

As with any technical indicator, the Adaptable Relative Momentum Index should be used as part of a broader trading strategy that includes risk management, fundamental analysis, and other forms of technical confirmation. Past performance does not guarantee future results.

⸻

Enjoy using the Adaptable RMI and experience a more streamlined, flexible approach to momentum analysis. Feel free to explore different asset classes and trading styles to discover which configurations resonate best with your unique trading preferences.

Johnny's Machine Learning Moving Average (MLMA) w/ Trend Alerts📖 Overview

Johnny's Machine Learning Moving Average (MLMA) w/ Trend Alerts is a powerful adaptive moving average indicator designed to capture market trends dynamically. Unlike traditional moving averages (e.g., SMA, EMA, WMA), this indicator incorporates volatility-based trend detection, Bollinger Bands, ADX, and RSI, offering a comprehensive view of market conditions.

The MLMA is "machine learning-inspired" because it adapts dynamically to market conditions using ATR-based windowing and integrates multiple trend strength indicators (ADX, RSI, and volatility bands) to provide an intelligent moving average calculation that learns from recent price action rather than being static.

🛠 How It Works

1️⃣ Adaptive Moving Average Selection

The MLMA automatically selects one of four different moving averages:

📊 EMA (Exponential Moving Average) – Reacts quickly to price changes.

🔵 HMA (Hull Moving Average) – Smooth and fast, reducing lag.

🟡 WMA (Weighted Moving Average) – Gives recent prices more importance.

🔴 VWAP (Volume Weighted Average Price) – Accounts for volume impact.

The user can select which moving average type to use, making the indicator customizable based on their strategy.

2️⃣ Dynamic Trend Detection

ATR-Based Adaptive Window 📏

The Average True Range (ATR) determines the window size dynamically.

When volatility is high, the moving average window expands, making the MLMA more stable.

When volatility is low, the window shrinks, making the MLMA more responsive.

Trend Strength Filters 📊

ADX (Average Directional Index) > 25 → Indicates a strong trend.

RSI (Relative Strength Index) > 70 or < 30 → Identifies overbought/oversold conditions.

Price Position Relative to Upper/Lower Bands → Determines bullish vs. bearish momentum.

3️⃣ Volatility Bands & Dynamic Support/Resistance

Bollinger Bands (BB) 📉

Uses standard deviation-based bands around the MLMA to detect overbought and oversold zones.

Upper Band = Resistance, Lower Band = Support.

Helps traders identify breakout potential.

Adaptive Trend Bands 🔵🔴

The MLMA has built-in trend envelopes.

When price breaks the upper band, bullish momentum is confirmed.

When price breaks the lower band, bearish momentum is confirmed.

4️⃣ Visual Enhancements

Dynamic Gradient Fills 🌈

The trend strength (ADX-based) determines the gradient intensity.

Stronger trends = More vivid colors.

Weaker trends = Lighter colors.

Trend Reversal Arrows 🔄

🔼 Green Up Arrow: Bullish reversal signal.

🔽 Red Down Arrow: Bearish reversal signal.

Trend Table Overlay 🖥

Displays ADX, RSI, and Trend State dynamically on the chart.

📢 Trading Signals & How to Use It

1️⃣ Bullish Signals 📈

✅ Conditions for a Long (Buy) Trade:

The MLMA crosses above the lower band.

The ADX is above 25 (confirming trend strength).

RSI is above 55, indicating positive momentum.

Green trend reversal arrow appears (confirmation of a bullish reversal).

🔹 How to Trade It:

Enter a long trade when the MLMA turns bullish.

Set stop-loss below the lower Bollinger Band.

Target previous resistance levels or use the upper band as take-profit.

2️⃣ Bearish Signals 📉

✅ Conditions for a Short (Sell) Trade:

The MLMA crosses below the upper band.

The ADX is above 25 (confirming trend strength).

RSI is below 45, indicating bearish pressure.

Red trend reversal arrow appears (confirmation of a bearish reversal).

🔹 How to Trade It:

Enter a short trade when the MLMA turns bearish.

Set stop-loss above the upper Bollinger Band.

Target the lower band as take-profit.

💡 What Makes This a Machine Learning Moving Average?

📍 1️⃣ Adaptive & Self-Tuning

Unlike static moving averages that rely on fixed parameters, this MLMA automatically adjusts its sensitivity to market conditions using:

ATR-based dynamic windowing 📏 (Expands/contracts based on volatility).

Adaptive smoothing using EMA, HMA, WMA, or VWAP 📊.

Multi-indicator confirmation (ADX, RSI, Volatility Bands) 🏆.

📍 2️⃣ Intelligent Trend Confirmation

The MLMA "learns" from recent price movements instead of blindly following a fixed-length average.

It incorporates ADX & RSI trend filtering to reduce noise & false signals.

📍 3️⃣ Dynamic Color-Coding for Trend Strength

Strong trends trigger more vivid colors, mimicking confidence levels in machine learning models.

Weaker trends appear faded, suggesting uncertainty.

🎯 Why Use the MLMA?

✅ Pros

✔ Combines multiple trend indicators (MA, ADX, RSI, BB).

✔ Automatically adjusts to market conditions.

✔ Filters out weak trends, making it more reliable.

✔ Visually intuitive (gradient colors & reversal arrows).

✔ Works across all timeframes and assets.

⚠️ Cons

❌ Not a standalone strategy → Best used with volume confirmation or candlestick analysis.

❌ Can lag slightly in fast-moving markets (due to smoothing).

Comprehensive Volume and Metrics with Pre-Market Volume Data

This script is designed for traders who want a detailed view of market activity, including regular market and pre-market volume, dollar volume, relative volume (RVOL), average daily range (ADR), average true range (ATR), relative strength index (RSI), and the QQQ’s percentage change.

The script includes customizable metrics displayed in tables on the chart for easy analysis, with the option to toggle the visibility of each metric.

Key Features:

Volume and Dollar Volume:

Displays the volume of shares traded during the current day (or pre-market, if enabled).

Includes a calculation of dollar volume, representing the total dollar amount of trades (Volume × Close Price).

Relative Volume (RVOL):

Displays RVOL Day, which is the relative volume of the current day compared to the 2-day moving average.

Shows RVOL 90D, indicating relative volume over the past 90 days.

Both RVOL metrics are calculated as percentages and display the percentage change compared to the standard (100%).

Pre-Market Data:

Includes pre-market volume (PVOL) and pre-market dollar volume (P$ VOL) which are displayed only if pre-market data is enabled.

Tracks volume and dollar volume during pre-market hours (4:00 AM to 9:30 AM Eastern Time) for more in-depth analysis.

Optionally, shows pre-market RSI based on volume-weighted close prices.

Average Daily Range (ADR):

Displays the percentage change between the highest and lowest prices over the defined ADR period (default is 20 days).

Average True Range (ATR):

Shows the ATR, a popular volatility indicator, for a given period (default is 14 bars).

RSI (Relative Strength Index):

Displays RSI for the given period (default is 14).

RSI is calculated using pre-market data when available.

QQQ:

Shows the percentage change of the QQQ ETF from the previous day’s close.

The QQQ percentage change is color-coded: green for positive, red for negative, and gray for no change.

Customizable Inputs:

Visibility Options: Toggle the visibility of each metric, such as volume, dollar volume, RVOL, ADR, ATR, RSI, and QQQ.

Pre-Market Data: Enable or disable the display of pre-market data for volume and dollar volume.

Table Positioning: Adjust the position of tables displaying the metrics either at the bottom-left or bottom-right of the chart.

Text Color and Table Background: Choose between white or black text for the tables and customize the background color.

Tables:

The script utilizes tables to display multiple metrics in an organized and easy-to-read format.

The values are updated dynamically, reflecting real-time data as the market moves.

Pre-Market Data:

The script calculates pre-market volume and dollar volume, along with other key metrics like RSI and RVOL, to help assess market sentiment before the market officially opens.

The pre-market data is accumulated from 4:00 AM to 9:30 AM ET, allowing for pre-market analysis and comparison to regular market hours.

User-Friendly and Flexible:

This script is designed to be highly customizable, giving you the ability to toggle which metrics to display and where they appear on the chart. You can easily focus on the data that matters most to your trading strategy.

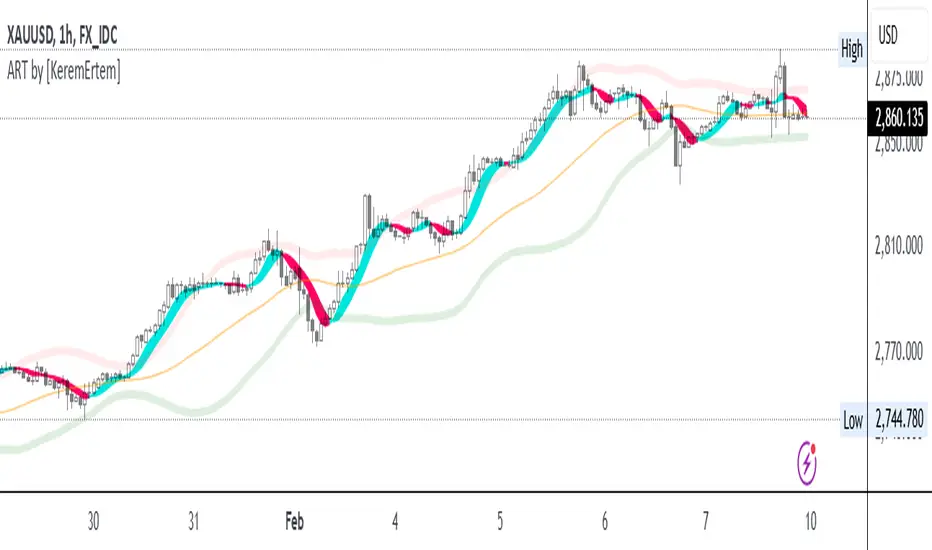

ADX, RSI, & TSI utilized as ART [by KeremErtem]The "ADX, RSI, & TSI utilized as ART" script is an advanced technical analysis tool designed by Kerem Ertem to help traders identify trend direction, strength, and potential reversals. It integrates the Average Directional Index (ADX), Relative Strength Index (RSI), and True Strength Index (TSI) into a cohesive, user-friendly indicator known as ART (Adaptive Relative Trend) .

What it does:

Trend Detection: Utilizes ADX to identify the strength and direction of trends.

Momentum Analysis: Uses RSI to gauge the speed and change of price movements.

Signal Smoothing: Incorporates TSI to reduce noise and provide clearer signals.

How it works:

Input Settings: Customize the source (hlc3), signal period (l1), and lookback range (l2) to tailor the indicator to your trading strategy.

Angle Calculation (ACI): The script calculates the angle of price movements using a custom function, which combines the lowest and highest prices with moving averages to create a smoother representation of trend angles.

Weighted Average: The ACI function is applied to the source price to derive a weighted average, which serves as the foundation for further calculations.

RSI Integration: The script calculates the RSI based on the weighted average price and further refines it using the ACI function to enhance signal accuracy.

ADX Calculation: ADX values are computed and adjusted using the ACI function to provide a clearer indication of trend strength and direction.

ART Indicator: The combined results of the RSI and ADX calculations form the ART indicator, which is plotted alongside trend lines and bands for comprehensive trend analysis.

Bands and Trend Lines: The script plots upper, lower, and center bands based on standard deviation and moving averages, providing visual cues for potential support and resistance levels.

How to use it:

Customization: Adjust the signal period, lookback range, RSI length, and ADX settings to fit your trading preferences.

Interpretation: Green ART signal lines indicate bullish trends, while red lines indicate bearish trends. The trend line color changes from cyan to magenta based on the trend direction.

Bands: Use the upper and lower bands as potential entry and exit points, with the center line acting as a trend confirmation.

This script offers a comprehensive approach to trend and momentum analysis, making it a valuable tool for traders seeking to enhance their trading strategies with advanced technical indicators.

[blackcat] L2 BullBear OscillatorOVERVIEW

The " L2 BullBear Oscillator" is a custom trading indicator for TradingView that helps traders identify market trends, potential tops and bottoms, and the strength of trends using various moving averages and price relationships.

FEATURES

Calculates a base oscillator based on the close price relative to the highest and lowest prices over the past 60 periods.

Smoothes the oscillator using exponential moving averages (EMAs).

Determines market strength through relative strength indicators and moving averages.

Identifies potential tops and strong support levels based on specific conditions involving oscillators and price actions.

Plots several signals to help traders make informed decisions.

HOW TO USE

Install the script on your TradingView chart.

Customize the settings in the "Inputs" section:

Set the periods for the short-term and long-term EMAs.

Set the periods for the three SMAs used in calculations.

Interpret the plots:

BullBear Signal (Fuchsia Line): Indicates the overall market trend. Uptrends suggest buying opportunities, while downtrends suggest selling.

Decreasing BullBear Signal (Aqua Line): Highlights periods when the trend is weakening or turning bearish, signaling possible selling opportunities.

Potential Top Condition (Yellow Plot): Signals possible trend reversals from bullish to bearish, indicating times to consider taking profits or preparing for a downtrend.

High Price Condition (Yellow Plot): Indicates strong bullish momentum but also potentially overbought conditions, which might precede a correction.

Earning Condition (Red Line): Possibly signifies strong bullish signals, indicating good times to enter long positions.

Strong Support Condition (White Arrows): Signals potential bottoms or support levels, indicating buying opportunities.

Start Hiding Condition (Fuchsia Plot): Might indicate times to exit positions or reduce exposure due to unfavorable market conditions.

ALGORITHMS

Moving Averages:

Simple Moving Averages (SMAs): Used to calculate averages of price data over specified periods.

Exponential Moving Averages (EMAs): Used to give more weight to recent prices, making the moving averages more responsive to new data.

Oscillator Calculation:

The base oscillator is calculated based on the close price's position within the highest and lowest prices over 60 periods, normalized to a 0-100 scale.

This oscillator is then smoothed using EMAs to reduce noise and make trends more visible.

Relative Strength Indicator:

Calculated based on the close price's position within the highest and lowest prices over 20 periods, also normalized to a 0-100 scale.

This is smoothed using SMAs to get a more stable signal.

Condition Checks:

Various conditions are checked to identify potential tops, strong support, and other market states based on the relationships between these indicators and price actions.

LIMITATIONS

The script is based on historical data and does not guarantee future performance.

It is recommended to use the script in conjunction with other analysis tools.

The effectiveness of the strategy may vary depending on the market conditions and asset being traded.

NOTES

The script is designed for educational purposes and should not be considered financial advice.

Users are encouraged to backtest the strategy on a demo account before applying it to live trades.

THANKS

Special thanks to the TradingView community for their support and feedback.

Uptrick: Smart BoundariesThis script is an indicator that combines the RSI (Relative Strength Index) and Bollinger Bands to highlight potential points where price momentum and volatility may both be at extreme levels. Below is a detailed explanation of its components, how it calculates signals, and why these two indicators have been merged into one tool. This script is intended solely for educational purposes and for traders who want to explore the combined use of momentum and volatility measures. Please remember that no single indicator guarantees profitable results.

Purpose of This Script

This script is designed to serve as a concise, all-in-one tool for traders seeking to track both momentum and volatility extremes in real time. By overlaying RSI signals with Bollinger Band boundaries, it helps users quickly identify points on a chart where price movement may be highly stretched. The goal is to offer a clearer snapshot of potential overbought or oversold conditions without requiring two separate indicators. Additionally, its optional pyramiding feature enables users to manage how many times they initiate trades when signals repeat in the same direction. Through these combined functions, the script aims to streamline technical analysis by consolidating two popular measures—momentum via RSI and volatility via Bollinger Bands—into a single, manageable interface.

1. Why Combine RSI and Bollinger Bands

• RSI (Relative Strength Index): This is a momentum oscillator that measures the speed and magnitude of recent price changes. It typically ranges between 0 and 100. Traders often watch for RSI crossing into “overbought” or “oversold” levels because it may indicate a potential shift in momentum.

• Bollinger Bands: These bands are plotted around a moving average, using a standard deviation multiplier to create an upper and lower boundary. They help illustrate how volatile the price has been relative to its recent average. When price moves outside these boundaries, some traders see it as a sign the price may be overstretched and could revert closer to the average.

Combining these two can be useful because it blends two different perspectives on market movement. RSI attempts to identify momentum extremes, while Bollinger Bands track volatility extremes. By looking for moments when both conditions agree, the script tries to highlight points where price might be unusually stretched in terms of both momentum and volatility.

2. How Signals Are Generated

• Buy Condition:

- RSI dips below a specified “oversold” level (for example, 30 by default).

- Price closes below the lower Bollinger Band.

When these occur together, the script draws a label indicating a potential bullish opportunity. The underlying reasoning is that momentum (RSI) suggests a stronger-than-usual sell-off, and price is also stretched below the lower Bollinger Band.

• Sell Condition:

- RSI rises above a specified “overbought” level (for example, 70 by default).

- Price closes above the upper Bollinger Band.

When these occur together, a label is plotted for a potential bearish opportunity. The rationale is that momentum (RSI) may be overheated, and the price is trading outside the top of its volatility range.

3. Pyramiding Logic and Trade Count Management

• Pyramiding refers to taking multiple positions in the same direction when signals keep firing. While some traders prefer just one position per signal, others like to scale into a trade if the market keeps pushing in their favor.

• This script uses variables that keep track of how many recent buy or sell signals have fired. If the count reaches a user-defined maximum, no more signals of that type will trigger additional labels. This protects traders from over-committing to one direction if the market conditions remain “extreme” for a prolonged period.

• If you disable the pyramiding feature, the script will only plot one label per side until the condition resets (i.e., until RSI and price conditions are no longer met).

4. Labels and Visual Feedback

• Whenever a buy or sell condition appears, the script plots a label directly on the chart:

- Buy labels under the price bar.

- Sell labels above the price bar.

These labels make it easier to review where both RSI and Bollinger Band conditions align. It can be helpful for visually scanning the chart to see if the signals show any patterns related to market reversals or trend continuations.

• The Bollinger Bands themselves are plotted so traders can see when the price is approaching or exceeding the upper or lower band. Watching the RSI and Bollinger Band plots simultaneously can give traders more context for each signal.

5. Originality and Usefulness

This script provides a distinct approach by merging two well-established concepts—RSI and Bollinger Bands—within a single framework, complemented by optional pyramiding controls. Rather than using each indicator separately, it attempts to uncover moments when momentum signals from RSI align with volatility extremes highlighted by Bollinger Bands. This combined perspective can aid in spotting areas of possible overextension in price. Additionally, the built-in pyramiding mechanism offers a method to manage multiple signals in the same direction, allowing users to adjust how aggressively they scale into trades. By integrating these elements together, the script aims to deliver a tool that caters to diverse trading styles while remaining straightforward to configure and interpret.

6. How to Use the Indicator

• Configure the Inputs:

- RSI Length (the lookback period used for the RSI calculation).

- RSI Overbought and Oversold Levels.

- Bollinger Bands Length and Multiplier (defines the moving average period and the degree of deviation).

- Option to reduce pyramiding.

• Set Alerts (Optional):

- You can create TradingView alerts for when these conditions occur, so you do not have to monitor the chart constantly. Choose the buy or sell alert conditions in your alert settings.

• Integration in a Trading Plan:

- This script alone is not a complete trading system. Consider combining it with other forms of analysis, such as support and resistance, volume profiles, or candlestick patterns. Thorough research, testing on historical data, and risk management are always recommended.

7. No Performance Guarantees

• This script does not promise any specific trading results. It is crucial to remember that no single indicator can accurately predict future market movements all the time. The script simply tries to highlight moments when two well-known indicators both point to an extreme condition.

• Actual trading decisions should factor in a range of market information, including personal risk tolerance and broader market conditions.

8. Purpose and Limitations

• Purpose:

- Provide a combined view of momentum (RSI) and volatility (Bollinger Bands) in a single script.

- Assist in spotting times when price may be at an extreme.

- Offer a configurable system for labeling potential buy or sell points based on these extremes.

• Limitations:

- Overbought and oversold conditions can persist for an extended period in trending markets.

- Bollinger Band breakouts do not always result in immediate reversals. Sometimes price keeps moving in the same direction.

- The script does not include a built-in exit strategy or risk management rules. Traders must handle these themselves.

Additional Disclosures

This script is published open-source and does not rely on any external or private libraries. It does not use lookahead methods or repaint signals; all calculations are performed on the current bar without referencing future data. Furthermore, the script is designed for standard candlestick or bar charts rather than non-standard chart types (e.g., Heikin Ashi, Renko). Traders should keep in mind that while the script can help locate potential momentum and volatility extremes, it does not include an exit strategy or account for factors like slippage or commission. All code comes from built-in Pine Script functions and standard formulas for RSI and Bollinger Bands. Anyone reviewing or modifying this script should exercise caution and incorporate proper risk management when applying it to their own trading.

Calculation Details

The script computes RSI by examining a user-defined number of prior bars (the RSI Length) and determining the average of up-moves relative to the average of down-moves over that period. This ratio is then scaled to a 0–100 range, so lower values typically indicate stronger downward momentum, while higher values suggest stronger upward momentum. In parallel, Bollinger Bands are generated by first calculating a simple moving average (SMA) of the closing price for the user-specified length. The script then measures the standard deviation of closing prices over the same period and multiplies it by the chosen factor (the Bollinger Bands Multiplier) to form the upper and lower boundaries around the SMA. These two measures are checked in tandem: if the RSI dips below a certain oversold threshold and price trades below the lower Bollinger Band, a condition is met that may imply a strong short-term sell-off; similarly, if the RSI surpasses the overbought threshold and price rises above the upper Band, it may indicate an overextended move to the upside. The pyramiding counters track how many of these signals occur in sequence, preventing excessive stacking of labels on the chart if conditions remain extreme for multiple bars.

Conclusion

This indicator aims to provide a more complete view of potential market extremes by overlaying the RSI’s momentum readings on top of Bollinger Band volatility signals. By doing so, it attempts to help traders see when both indicators suggest that the market might be oversold or overbought. The optional reduced pyramiding logic further refines how many signals appear, giving users the choice of a single entry or multiple scaling entries. It does not claim any guaranteed success or predictive power, but rather serves as a tool for those wanting to explore this combined approach. Always be cautious and consider multiple factors before placing any trades.

Support/Resistance

Custom Moving Average Indicator with MACD, RSI, and Support/Resistance

This indicator is designed to help traders make informed trading decisions by integrating several technical indicators, including moving averages, the Relative Strength Index (RSI), and the Moving Average Convergence Divergence (MACD).

Key Features:

Moving Averages:

This indicator uses simple moving averages (SMAs) for several periods (4, 18, 66, 89, 632, 1000, 1500, 2000, and 3000 bars). This helps to identify the overall trend of the price and potential support and resistance levels.

The color of each moving average line is dynamically changed based on the closing price's position relative to the average; it turns red if the price is above the average and green if the price is below.

Relative Strength Index (RSI):

The RSI is calculated for a 14-bar period, which is a measure of overbought or oversold conditions.

An RSI value above 70 indicates an overbought condition, while a value below 30 indicates an oversold condition.

MACD:

The MACD is calculated using a fast length of 12, a slow length of 26, and a signal length of 9. Crossovers between the MACD line and the signal line indicate momentum shifts.

A crossover of the MACD line above the signal line suggests a potential buy signal, while a crossover below indicates a potential sell signal.

Buy and Sell Signals:

Buy Signal: Triggered when the MACD line crosses above the signal line, the RSI is below 30, the MACD is above 0, and there is high volume.

Sell Signal: Triggered when the MACD line crosses below the signal line, the RSI is above 70, the MACD is below 0, and there is high volume.

Alerts:

The indicator includes alerts that are triggered when buy and sell signals occur, helping traders respond quickly to market opportunities.

How to Trade Using the Indicator (continued):

Trading on Buy Signals:

Look for buy signals when the MACD line crosses above the signal line. Ensure that the RSI is below 30, indicating there is a potential for price recovery from an oversold condition.

Confirm that the volume is above the average, which indicates strong market participation and adds validity to the trade.

Trading on Sell Signals:

Search for sell signals when the MACD line crosses below the signal line. Check that the RSI is above 70 to confirm an overbought condition, implying the price may decline.

As with buy signals, ensure that volume is high to validate the strength of the sell signal.

Risk Management:

Use stop-loss orders to protect your capital. Establish an initial loss threshold based on your risk management strategy.

Continuously monitor the market and new signals and adjust your approach according to your market analysis.

Conclusion:

This combined indicator helps traders make informed decisions by relying on a set of technical tools. To achieve the best results, ensure you integrate the analysis from these indicators with your trading strategies and other techniques.

Feel free to use this explanation as an introduction or guide to inform traders on how to effectively use the indicator. If you have any more questions or need further details, don't hesitate to ask!

Crypto Sectors Performance [Daveatt]IMPORTANT

⚠️ This script must be used on the Daily timeframe only.

OVERVIEW

This indicator brings the powerful sector analysis capabilities from velo.xyz/market's

Sector Performance chart to TradingView.

It enables traders to track and compare performance across the crypto market's major sectors, providing essential insights for sector rotation strategies and market analysis.

CALCULATION METHOD

The indicator calculates performance across six key crypto sectors: DeFi, Gaming, Layer 1s, Layer 2s, AI, and Memecoins.

For each sector, it computes a rolling percentage performance by averaging the performance of multiple representative tokens.

All sector performances are rebased to 0% at the start of each period, making relative comparisons clear and intuitive.

VISUALIZATION MODES

The script features two distinct visualization methods:

Plots Mode:

Displays continuous performance lines for each sector over time, ideal for tracking relative strength trends and sector momentum. Each sector has its own color-coded line with performance values clearly marked.

Bars Mode:

Presents current sector performance as vertical bars, offering an immediate visual comparison of sector gains and losses.

The bars are color-coded and labeled with exact percentage values for precise analysis.

For the "Bars Mode", I used the box.new() function

SECTOR COMPOSITION

Each sector comprises carefully selected representative tokens:

- DeFi: AAVE, 1INCH, JUP, MKR, UNI

- Gaming: GALA, AXS, RONIN, SAND

- Layer 1: BTC, ETH, AVAX, APT, SOL, BNB, SUI

- Layer 2: ARB, OP, ZK, POL, STRK, MNT

- AI: FET, NEAR, RENDER, TAO

- Memecoins: PEPE, BONK, SHIB, DOGE, WIFU, POPCAT

PERFORMANCE TRACKING

The indicator implements a rolling window approach for performance calculations.

Starting from 0% at the beginning of each period, it tracks relative performance with positive values indicating outperformance and negative values showing underperformance.

Multiple timeframe options (1W, 1M, 3M, 6M, and 1Y) allow for both short-term and long-term analysis.

APPLICATIONS

This tool proves invaluable for:

- Sector rotation analysis

- Identifying trending sectors

- Comparing relative strength

- Gauging market sentiment

- Understanding market structure through sector performance

Thanks for reading and for the support

Daveatt

Adapted RSI w/ Multi-Asset Regime Detection v1.1The relative strength index (RSI) is a momentum indicator used in technical analysis. RSI measures the speed and magnitude of an asset's recent price changes to detect overbought or oversold conditions in the price of said asset.

In addition to identifying overbought and oversold assets, the RSI can also indicate whether your desired asset may be primed for a trend reversal or a corrective pullback in price. It can signal when to buy and sell.

The RSI will oscillate between 0 and 100. Traditionally, an RSI reading of 70 or above indicates an overbought condition. A reading of 30 or below indicates an oversold condition.

The RSI is one of the most popular technical indicators. I intend to offer a fresh spin.

Adapted RSI w/ Multi-Asset Regime Detection

Our Adapted RSI makes necessary improvements to the original Relative Strength Index (RSI) by combining multi-timeframe analysis with multi-asset monitoring and providing traders with an efficient way to analyse market-wide conditions across different timeframes and assets simultaneously. The indicator automatically detects market regimes and generates clear signals based on RSI levels, presenting this data in an organised, easy-to-read format through two dynamic tables. Simplicity is key, and having access to more RSI data at any given time, allows traders to prepare more effectively, especially when trading markets that "move" together.

How we calculate the RSI

First, the RSI identifies price changes between periods, calculating gains and losses from one look-back period to the next. This look-back period averages gains and losses over 14 periods, which in this case would be 14 days, and those gains/losses are calculated based on the daily closing price. For example:

Average Gain = Sum of Gains over the past 14 days / 14

Average Loss = Sum of Losses over the past 14 days / 14

Then we calculate the Relative Strength (RS):

RS = Average Gain / Average Loss

Finally, this is converted to the RSI value:

RSI = 100 - (100 / (1 + RS))

Key Features

Our multi-timeframe RSI indicator enhances traditional technical analysis by offering synchronised Daily, Weekly, and Monthly RSI readings with automatic regime detection. The multi-asset monitoring system allows tracking of up to 10 different assets simultaneously, with pre-configured major pairs that can be customised to any asset selection. The signal generation system provides clear market guidance through automatic regime detection and a five-level signal system, all presented through a sophisticated visual interface with dynamic RSI line colouring and customisable display options.

Quick Guide to Use it

Begin by adding the indicator to your chart and configuring your preferred assets in the "Asset Comparison" settings.

Position the two information tables according to your preference.

The main table displays RSI analysis across three timeframes for your current asset, while the asset table shows a comparative analysis of all monitored assets.

Signals are colour-coded for instant recognition, with green indicating bullish conditions and red for bearish conditions. Pay special attention to regime changes and signal transitions, using multi-timeframe confluence to identify stronger signals.

How it Works (Regime Detection & Signals)

When we say 'Regime', a regime is determined by a persistent trend or in this case momentum and by leveraging this for RSI, which is a momentum oscillator, our indicator employs a relatively simple regime detection system that classifies market conditions as either Bullish (RSI > 50) or Bearish (RSI < 50). Our benchmark between a trending bullish or bearish market is equal to 50. By leveraging a simple classification system helps determine the probability of trend continuation and the weight given to various signals. Whilst we could determine a Neutral regime for consolidating markets, we have employed a 'neutral' signal generation which will be further discussed below...

Signal generation occurs across five distinct levels:

Strong Buy (RSI < 15)

Buy (RSI < 30)

Neutral (RSI 30-70)

Sell (RSI > 70)

Strong Sell (RSI > 85)

Each level represents different market conditions and probability scenarios. For instance, extreme readings (Strong Buy/Sell) indicate the highest probability of mean reversion, while neutral readings suggest equilibrium conditions where traders should focus on the overall regime bias (Bullish/Bearish momentum).

This approach offers traders a new and fresh spin on a popular and well-known tool in technical analysis, allowing traders to make better and more informed decisions from the well presented information across multiple assets and timeframes. Experienced and beginner traders alike, I hope you enjoy this adaptation.

[3Commas] Signal BuilderSignal Builder is a tool designed to help traders create custom buy and sell signals by combining multiple technical indicators. Its flexibility allows traders to set conditions based on their specific strategy, whether they’re into scalping, swing trading, or long-term investing. Additionally, its integration with 3Commas bots makes it a powerful choice for those looking to automate their trades, though it’s also ideal for traders who prefer receiving alerts and making manual decisions.

🔵 How does Signal Builder work?

Signal Builder allows users to define custom conditions using popular technical indicators, which, when met, generate clear buy or sell signals. These signals can be used to trigger TradingView alerts, ensuring that you never miss a market opportunity. Additionally, all conditions are evaluated using "AND" logic, meaning signals are only activated when all user-defined conditions are met. This increases precision and helps avoid false signals.

🔵 Available indicators and recommended settings:

Signal Builder provides access to a wide range of technical indicators, each customizable to popular settings that maximize effectiveness:

RSI (Relative Strength Index): An oscillator that measures the relative strength of price over a specific period. Traders typically configure it with 14 periods, using levels of 30 (oversold) and 70 (overbought) to identify potential reversals.

MACD (Moving Average Convergence Divergence): A key indicator tracking the crossover between two moving averages. Common settings include 12 and 26 periods for the moving averages, with a 9-period signal line to detect trend changes.

Ultimate Oscillator: Combines three different time frames to offer a comprehensive view of buying and selling pressure. Popular settings are 7, 14, and 28 periods.

Bollinger Bands %B: Provides insight into where the price is relative to its upper and lower bands. Standard settings include a 20-period moving average and a standard deviation of 2.

ADX (Average Directional Index): Measures the strength of a trend. Values above 25 typically indicate a strong trend, while values below suggest weak or sideways movement.

Stochastic Oscillator: A momentum indicator comparing the closing price to its range over a defined period. Popular configurations include 14 periods for %K and 3 for %D smoothing.

Parabolic SAR: Ideal for identifying trend reversals and entry/exit points. Commonly configured with a 0.02 step and a 0.2 maximum.

Money Flow Index (MFI): Similar to RSI but incorporates volume into the calculation. Standard settings use 14 periods, with levels of 20 and 80 as oversold and overbought thresholds.

Commodity Channel Index (CCI): Measures the deviation of price from its average. Traders often use a 20-period setting with levels of +100 and -100 to identify extreme overbought or oversold conditions.

Heikin Ashi Candles: These candles smooth out price fluctuations to show clearer trends. Commonly used in trend-following strategies to filter market noise.

🔵 How to use Signal Builder:

Configure indicators: Select the indicators that best fit your strategy and adjust their settings as needed. You can combine multiple indicators to define precise entry and exit conditions.

Define custom signals: Create buy or sell conditions that trigger when your selected indicators meet the criteria you’ve set. For example, configure a buy signal when RSI crosses above 30 and MACD confirms with a bullish crossover.

TradingView alerts: Set up alerts in TradingView to receive real-time notifications when the conditions you’ve defined are met, allowing you to react quickly to market opportunities without constantly monitoring charts.

Monitor with the panel: Signal Builder includes a visual panel that shows active conditions for each indicator in real time, helping you keep track of signals without manually checking each indicator.

🔵 3Commas integration:

In addition to being a valuable tool for any trader, Signal Builder is optimized to work seamlessly with 3Commas bots through Webhooks. This allows you to automate your trades based on the signals you’ve configured, ensuring that no opportunity is missed when your defined conditions are met. If you prefer automation, Signal Builder can send buy or sell signals to your 3Commas bots, enhancing your trading process and helping you manage multiple trades more efficiently.

🔵 Example of use:

Imagine you trade in volatile markets and want to trigger a sell signal when:

Stochastic Oscillator indicates overbought conditions with the %K value crossing below 80.

Bollinger Bands %B shows the price has surpassed the upper band, suggesting a potential reversal.

ADX is below 20, indicating that the trend is weak and could be about to change.

With Signal Builder , you can configure these conditions to trigger a sell signal only when all are met simultaneously. Then, you can set up a TradingView alert to notify you as soon as the signal is activated, giving you the opportunity to react quickly and adjust your strategy accordingly.

👨🏻💻💭 If this tool helps your trading strategy, don’t forget to give it a boost! Feel free to share in the comments how you're using it or if you have any questions.

_________________________________________________________________

The information and publications within the 3Commas TradingView account are not meant to be and do not constitute financial, investment, trading, or other types of advice or recommendations supplied or endorsed by 3Commas and any of the parties acting on behalf of 3Commas, including its employees, contractors, ambassadors, etc.

Ichimoku Crosses_RSI_AITIchimoku Crosser_RSI_AIT

Overview

The "Ichimoku Cloud Crosses_AIT" strategy is a technical trading strategy that combines the Ichimoku Cloud components with the Relative Strength Index (RSI) to generate trade signals. This strategy leverages the crossovers of the Tenkan-sen and Kijun-sen lines of the Ichimoku Cloud, along with RSI levels, to identify potential entry and exit points for long and short trades. This guide explains the strategy components, conditions, and how to use it effectively in your trading.

1. Strategy Parameters

User Inputs

Tenkan-sen Period (tenkanLength): Default value is 21. This is the period used to calculate the Tenkan-sen line (conversion line) of the Ichimoku Cloud.

Kijun-sen Period (kijunLength): Default value is 120. This is the period used to calculate the Kijun-sen line (base line) of the Ichimoku Cloud.

Senkou Span B Period (senkouBLength): Default value is 52. This is the period used to calculate the Senkou Span B line (leading span B) of the Ichimoku Cloud.

RSI Period (rsiLength): Default value is 14. This period is used to calculate the Relative Strength Index (RSI).

RSI Long Entry Level (rsiLongLevel): Default value is 60. This level indicates the minimum RSI value for a long entry signal.

RSI Short Entry Level (rsiShortLevel): Default value is 40. This level indicates the maximum RSI value for a short entry signal.

2. Strategy Components

Ichimoku Cloud

Tenkan-sen: A short-term trend indicator calculated as the simple moving average (SMA) of the highest high and the lowest low over the Tenkan-sen period.

Kijun-sen: A medium-term trend indicator calculated as the SMA of the highest high and the lowest low over the Kijun-sen period.

Senkou Span A: Calculated as the average of the Tenkan-sen and Kijun-sen, plotted 26 periods ahead.

Senkou Span B: Calculated as the SMA of the highest high and lowest low over the Senkou Span B period, plotted 26 periods ahead.

Chikou Span: The closing price plotted 26 periods behind.

Relative Strength Index (RSI)

RSI: A momentum oscillator that measures the speed and change of price movements. It ranges from 0 to 100 and is used to identify overbought or oversold conditions.

3. Entry and Exit Conditions

Entry Conditions

Long Entry:

The Tenkan-sen crosses above the Kijun-sen (bullish crossover).

The RSI value is greater than or equal to the rsiLongLevel.

Short Entry:

The Tenkan-sen crosses below the Kijun-sen (bearish crossover).

The RSI value is less than or equal to the rsiShortLevel.

Exit Conditions

Exit Long Position: The Tenkan-sen crosses below the Kijun-sen.

Exit Short Position: The Tenkan-sen crosses above the Kijun-sen.

4. Visual Representation

Tenkan-sen Line: Plotted on the chart. The color changes based on its relation to the Kijun-sen (green if above, red if below) and is displayed with a line width of 2.

Kijun-sen Line: Plotted as a white line with a line width of 1.

Entry Arrows:

Long Entry: Displayed as a yellow triangle below the bar.

Short Entry: Displayed as a fuchsia triangle above the bar.

5. How to Use

Apply the Strategy: Apply the "Ichimoku Cloud Crosses_AIT" strategy to your chart in TradingView.

Configure Parameters: Adjust the strategy parameters (Tenkan-sen, Kijun-sen, Senkou Span B, and RSI settings) according to your trading preferences.

Interpret the Signals:

Long Entry: A yellow triangle appears below the bar when a long entry signal is generated.

Short Entry: A fuchsia triangle appears above the bar when a short entry signal is generated.

Monitor Open Positions: The strategy automatically exits positions based on the defined conditions.

Backtesting and Live Trading: Use the strategy for backtesting and live trading. Adjust risk management settings in the strategy properties as needed.

Conclusion

The "Ichimoku Cloud Crosses_AIT" strategy uses Ichimoku Cloud crossovers and RSI to generate trading signals. This strategy aims to capture market trends and potential reversals, providing a structured way to enter and exit trades. Make sure to backtest and optimize the strategy parameters to suit your trading style and market conditions before using it in a live trading environment.

Inverted SD Dema RSI | viResearchInverted SD Dema RSI | viResearch

The "Inverted SD Dema RSI" developed by viResearch introduces a new approach to trend analysis by combining the Double Exponential Moving Average (DEMA), Standard Deviation (SD), and Relative Strength Index (RSI). This unique indicator provides traders with a tool to capture market trends by integrating volatility-based thresholds. By using the smoothed DEMA along with standard deviation, the indicator offers improved responsiveness to price fluctuations, while RSI thresholds offer insight into overbought and oversold market conditions.

At the core of the "Inverted SD Dema RSI" is the combination of DEMA and standard deviation for a more nuanced view of market volatility. The use of RSI further aids in detecting price extremes and potential trend reversals.

DEMA Calculation (sublen): The Double Exponential Moving Average (DEMA) smoothes out price data over a user-defined period, reducing lag compared to traditional moving averages. This provides a clearer representation of the market's overall direction.

Standard Deviation Calculation (sublen_2): The standard deviation of the DEMA is used to define the upper (u) and lower (d) bands, highlighting areas where price volatility may signal a change in trend. These dynamic bands help traders gauge price volatility and potential breakouts or breakdowns.

RSI Calculation (len): The script applies the Relative Strength Index (RSI) to the smoothed DEMA values, allowing traders to detect momentum shifts based on a modified data set. This provides a more accurate reflection of market strength when combined with the DEMA.