TSI HMA CCIHi!

This strategy has TSI and CCI indicators with the CCI being based on a HMA instead of the Price.

There is a number of conditions that must combine to create buy or sell signals, but it is basically a couple of MA crossovers.

The strategy opens new orders on each candle if the conditions are met, Either direction, so it is hedging.

It wont open new orders if there is a floating loss, and so is constantly attempting to hold a floating profit (drawup instead of drawdown)

But It has a StopLoss (set by user) for closing of losing orders, and it closes all orders in basket style when account is in profit to users set amount target profit.

Low commission set to simulate swap but Forex pairs generally dont have commission like the crypto exchanges do. So if you use this on cryptos, remember to increase the commission to your brokers amount.

Crypto users will likely find that because this opens so many orders the commission could erase its profits.

So i recommend this for Forex only, and perhaps, only NZDUSD 4H chart. other pairs, change settings for.

The strategy has settings for testing on target time spans, so you could test it on just Jan-Feb 2020 for example, if you want, or from Jan 2020 to present day.

Have Fun! Open Script for copy/paste/edit/publish your own version :)

"profit" için komut dosyalarını ara

Heikin Ashi+RSI+EMA Strategy 2.0 v4 [Cryptocurrency] by GodtrixHi,

I know a lot of people are looking for a more sophisticated and customizable strategy tool, I'm facing the same problem too, so I created one for myself and decided to share it for free trials and if you think this tool do what you wanted, you can contact me for the subscription "Premium" version.

I'll keep it simple with point forms, if you have any further inquiries or questions, please feel free to message me. Thank you.

Best profit plan with this strategy is you trade on Future leverage while you hold on to your coin, so that when price goes up, your coin value goes up, and at the same time, you trade with your leverage to earn even more, easily doubling up your total profit.

Benefits:

Fully customizable and you can easily personalized it and FINE TUNE it according to the market or coin you trading on.

The strategy is based on REAL PRACTICAL trading skills, so it works in real-world.

I fixed the "repainting" issue so the backtest it shows you IS ACCURATE when you run for real-time.

We all know one indicator is not going to help you win your trades, so this strategy combines ALL three: EMA for long+short term trend, HA for short term trend, RSI for entry/exit

This strategy is designed for LONG trade (Buy low, Sell high), not for SHORT trade.

This is not day trading, it is more to mid-term trading, where there's only few trades per month

Mainly is coded to work with 3Commas bot auto trading, so you only need to key in your Bot ID & Email Token.

Bot trading NOTE:

You need to replace the Alert Message with this: {{strategy.order.alert_message}}

One Alert will work for both Buy and Sell Order

If you using other Bot service, you can enter Custom Command too, so it works on any bot service.

Lastly,

regarding the setting advice, I would say you try playing with different settings and your objective is to achieve a backtest result that has:

1) Profitable is > 80%

2) Losing trades is nearly 0 or below 25% of your winning trades. Trick is using far stop loss %

3) Net Profit be almost same or more than "Buy & Hold Profit"

If you interested in our subscription version, message me for price.

Best Luck & a million dollar profit to you,

Godtrix BITSTAMP:BTCUSD BINANCE:DOTUSDT

I SAHAM AK BUY LOW ____ Multi TimeFrame OversoldThis strategy is built to confirm the profitability of buying oversold using RSI indicator.

Buy & Sell point will appear on price chart.

Entry Point : RSI3, RSI10, AND RSI14 below 26.

Cut Loss : Entry Price - 5%.

Take Profit : Entry Price + 10%.

5 entries allowed in same direction eventhough open trade not yet closed. In layman words, you keep buying new low closing price for 5 times.

Commission fee fixed at 0.08%.

Decent fundamental counter is preferable.

Even at win rate of 50%, it is profitable due to Risk Reward Ratio of 1 to 2.

EMA Crossover StrategyMoving average crossover systems measure drift in the market. They are great strategies for time-limited people.

So, why don't more people use them?

I think it's due to poor choice in choosing EMA lengths: Market Wizard Ed Seykota has a guideline for moving average crossovers: the slow line should be at least 3x the fast line. This removes a lot of the whipsaws inherent in moving average systems, which means greater profitability. His other piece of advice: long-only strategies are best in stock markets where there's a lot more upside potential.

Using these simple rules, we can reduce a lot of the whipsaws and low profitability trades! This strategy was made so you can see for yourself before trading.

=== HOW TO USE THIS INDICATOR ===

1) Choose your market and timeframe.

2) Choose the length.

3) Choose the multiplier.

4) Choose if the strategy is long-only or bidirectional.

Don't overthink the above! We don't know the best answers, that's why this strategy exists! We're going to test and find out.

After you find a good combination, set up an alert system with the default Exponential Moving Average indicators provided by TradingView.

=== TIPS ===

Increase the multiplier to reduce whipsaws (back and forth trades).

Increase the length to take fewer trades, decrease the length to take more trades.

Try a Long-Only strategy to see if that performs better.

ETH/USD 15m [iTradebot]1. General

2. Additional information

3. Access

1. This is a script for crypto trading strategies, based on following trends with moving averages.

A fast moving average and a slower getting crosschecked with MACD for buying/selling signals, those signals get crosschecked by 5 different factors, like the MACD or controlling average.

Only if all requirements will be met, the script expects the trend to change and sends an according signal.

This strategy is not made for multiple entries and keeps a position open until an opposite signal gets triggered.

It was built with ETH/USD 15min chart in mind, but can be used on any other chart, though you will have to find a different combination in inputs, to make it work with other pairs or timeframes.

Fast average: The faster of the two signal moving averages.

Slow average: The slower of the two signal moving averages.

Trend strength: Determines the crosscheck with the MACD.

Control length: Sets the period length for the control average (1=1bar, 300=300bars)

Inputs used here are:

Fast average: 5

Slow average: 19

Trend strength: 4

Control length: 306

Start capital: 1000

Trade equity: 100%

Commission: 0.036% (Binance)

Result 2020-06-11 until 2021-01-07

Net Profit: 717.56%

Percent Profitable: 54.17%

Max Drawdown: 8.79%

Profit Factor: 6.523

2. There are many combinations with good net profit outcomes, but make sure to also keep a low "Max Drawdown", to lower the risk substantially.

The combination we used, gives slightly less profit than other combinations, but also lowers the max drawdown from 20% to 9%.

In general in trading with crypto we advice to only use this strategy with Bitcoin or Ethereum , due to their high value and "stable" movements, compared to other cryptocurrencies.

The strategy is using 100% equity each trade, so make sure to have your capital management in place on the account.

To be specific, DONT put all your capital into this one strategy, but only part of it, according to your capital management.

Control lengths around 150 or 300 tend to give good combinations with the other 3 inputs. (on the 15min chart)

3. You can test this strategy 14 days for free and get access for up to 1 year on our website.

14 day free trial only requires Tradingview user name and e-mail.

Click on the link in our signature below.

5 min scalper for indian marketHi friends....publishing 5 min scalper for indian market... which shows the movement of price over time and how strong those movements are/will be, regardless of the direction the price moves, up, or down. Indicator specifically useful, as it helps traders and analysts spot points where the market can and will reverse by providing signals long (buy) and short (sell). Show the relative strength of price movements but leave out the directionality of the price movements, best utilized in combination with other technical indicators – such as trend lines and moving averages – which show price trends and directions. Having an alert feature to make aware market players from signals provided by strategy.

It analyz underlying volume and shows buy and sell signal...

U also can modify algo length ..

some tips for new traders to become successful trader

1: always follow risk management...

2: every stock/ forex / crypto has it own cycle.. So pls dont jump from one stock / forex pair to another when u hear some stock / crypto has

made new high or low... Bcs after that consolidation period starts.. During consolidation we can not make more profit as in trending market.. So be patient when u had made some position or tarde in one stock/ pair...

3 : we dont require to trade in every stocks / forex/crypto.. Just one stock and pair trading daily make u profitable beyond ur expection.. Bcs

trading in one stock / forex pair.. make u very comfortable and u may always know its movement... And u also trade in every cycle of this

stock/ pair.. So u also trdae its trend days which made highest profit. We dont know when is trend of any stock... Compare with it

business... Trading is business not one day rich game... Its business... It takes time and u have to do same thing agian and again to become

sucessfull trader for this u can use tradingview alerts. .for that u dont need to seat infrot of ur terminal screen.. u can also do algo trading

by using tradingview alerts

4 : By following risk management and incerase lot size as profit increased... This is the key 🔑 of sucess in stocks / forex / crypto market.

I thinks this tips may help new trader. U can modified according to ur trading style..

You can personal message me if u want to use this strategy

******************if u want to use this indicator u can personal message me********************************************************

intraday scalper with stopHi friends....publishing intraday scalper which shows the movement of price over time and how strong those movements are/will be, regardless of the direction the price moves, up, or down. Indicator specifically useful, as it helps traders and analysts spot points where the market can and will reverse by providing signals long (buy) and short (sell). Show the relative strength of price movements but leave out the directionality of the price movements, best utilized in combination with other technical indicators – such as trend lines and moving averages – which show price trends and directions. Having an alert feature to make aware market players from signals provided by the indicator.

u can start and close your trades at your define period. Use full for stockmarkets, mcx and forex because all movement occur in new York session....u can set your time to start trading and also for closing. you can also hold position if u want...by changing just close hours at 24..this way u can hold your trade untill next buy/sell signal come..

hope it will help intraday traders

and best of luck to all..

****you can use it any stocks ,forex and crypto**********

some tips for new traders to become sucessful trader

1: always follow risk management...

2: every stock/ forex / crypto has it own cycle.. So pls dont jump from one stock / forex pair to another when u hear some stock / crypto has

made new high or low... Bcs after that consolidation period starts.. During consolidation we can not make more profit as in trending market.. So be patient when u had made some position or tarde in one stock/ pair...

3 : we dont require to trade in every stocks / forex/crypto.. Just one stock and pair trading daily make u profitable beyond ur expection.. Bcs

trading in one stock / forex pair.. make u very comfortable and u may always know its movement... And u also trade in every cycle of this

stock/ pair.. So u also trdae its trend days which made highest profit. We dont know when is trend of any stock... Compare with it

business... Trading is business not one day rich game... Its business... It takes time and u have to do same thing agian and again to become

sucessfull trader for this u can use tradingview alerts. .for that u dont need to seat infrot of ur terminal screen.. u can also do algo trading

by using tradingview alerts

4 : By following risk management and incerase lot size as profit increased... This is the key 🔑 of sucess in stocks / forex / crypto market.

I thinks this tips may help new trader. U can modified according to ur trading style..

You can personal message me if u want to use this strategy

Swing Algo For Allhi friends....publishing Swing Algo For All .. which shows the movement of price over time and how strong those movements are/will be, regardless of the direction the price moves, up, or down. Indicator specifically useful, as it helps traders and analysts spot points where the market can and will reverse by providing signals long (buy) and short (sell). Show the relative strength of price movements but leave out the directionality of the price movements, best utilized in combination with other technical indicators – such as trend lines and moving averages – which show price trends and directions. Having an alert feature to make aware market players from signals provided by the strategy.

There are mainly 3 tyes of swing traders

1 intraday swing trader

2 weekly positional swing trader

3 monthly/yearly positional swing trader

This strategy solves problem of all the type of swing trader. you have to just select type of swing which u want to trade suppose u chose intraday swing it automatically calculate intraday swing high and low and shows buy and sell sign according to it...if it shows buy signal than in lower part it shows plotted line when this line break it automatically generate sell signal and vice versa for sell signal.

same for weekly , monthly and yearly

u can use it in any time frame bcs swing structure are same in any time frame

*********************************************************************************************************

*************** And also use for any stocks, forex and crypto*****************

screenshot on Banknifty weekly swing

some tips for new traders to become successful trader

1: always follow risk management...

2: every stock/ forex / crypto has it own cycle.. So pls dont jump from one stock / forex pair to another when u hear some stock / crypto has

made new high or low... Bcs after that consolidation period starts.. During consolidation we can not make more profit as in trending market.. So be patient when u had made some position or tarde in one stock/ pair...

3 : we dont require to trade in every stocks / forex/crypto.. Just one stock and pair trading daily make u profitable beyond ur expection.. Bcs

trading in one stock / forex pair.. make u very comfortable and u may always know its movement... And u also trade in every cycle of this

stock/ pair.. So u also trdae its trend days which made highest profit. We dont know when is trend of any stock... Compare with it

business... Trading is business not one day rich game... Its business... It takes time and u have to do same thing agian and again to become

sucessfull trader for this u can use tradingview alerts. .for that u dont need to seat infrot of ur terminal screen.. u can also do algo trading

by using tradingview alerts

4 : By following risk management and incerase lot size as profit increased... This is the key 🔑 of sucess in stocks / forex / crypto market.

I thinks this tips may help new trader. U can modified according to ur trading style..

You can personal message me if u want to use this strategy

u can personal message me if u want to use it..

DoubleTrendCloud(DTC) StrategyHello, everyone.

We try to publish a strategy for Bitcoin named 'DoubleTrendCloud(DTC) Strategy'.

It is largely based on the 'Supertrend strategy' and 'Supertrend Cloud Strategy' published by 'jhanson107'.

What we did here is just some modification for the current Bitcoin trend. It is based on a 4 hour time period.

In short, it utilizes two pairs of trend lines: short period trend and long period trend.

When the long period trend was broken upward, we do not have short position, but only long position according to the short period trend.

On the other hand, the long period trend was broken downward, we do not have long position, but only short position according to the short period trend.

The messages for the position:

long : open your long position

short : open your short position

Close entry(s) order long : close your long position

Close entry(s) order short : close your short position

As a result, this DTC Strategy guarantees higher profit and lower risk than the original supertrend strategy.

(Total profit and the maximum risk from Jan. 1. 2018 ->

(a) Supertrend (Multiplier= 2/period= 7): Total profit: 843%, the maximum risk: 39.38%

(b) Supertrend (Multiplier= 7/period= 4): Total profit: 370%, the maximum risk: 37.18%

(c) DoubleTrendCloud: Total profit: 1487%, the maximum risk: 24.25%)

Zignaly TutorialThis strategy serves as a beginner's guide to connect TradingView signals to Zignaly Crypto Trading Platform.

It was originally tested at BTCUSDT pair and 1D timeframe.

Before using this documentation it's recommended that you:

Use default TradingView strategy script or another script and setup its associated alert manually. Just make the alert pop-up in the screen.

Create a 'Copy-Trader provider' (or Signal Provider) in Zignaly and send signals to it either thanks to your browser or with some basic programming.

SETTINGS

__ SETTINGS - Capital

(CAPITAL) Capital quote invested per order in USDT units {100.0}. This setting is only used when '(ZIG) Provider type' is set to 'Signal Provider'.

(CAPITAL) Capital percentage invested per order (%) {25.0}. This setting is only used when '(ZIG) Provider type' is set to 'Copy Trader Provider'.

__ SETTINGS - Misc

(ZIG) Enable Alert message {True}: Whether to enable alert message or not.

(DEBUG) Enable debug on order comments {True}: Whether to show alerts on order comments or not.

Number of decimal digits for Prices {2}.

(DECIMAL) Maximum number of decimal for contracts {3}.

__ SETTINGS - Zignaly

(ZIG) Integration type {TradingView only}: Hybrid : Both TradingView and Zignaly handle take profit, trailing stops and stop losses. Useful if you are scared about TradingView not firing an alert. It might arise problems if TradingView and Zignaly get out of sync. TradingView only : TradingView sends entry and exit orders to Zignaly so that Zignaly only buys or sells. Zignaly won't handle stop loss or other settings on its own.

(ZIG) Zignaly Alert Type {WebHook}: 'Email' or 'WebHook'.

(ZIG) Provider type {Copy Trader Provider}: 'Copy Trader Provider' or 'Signal Provider'. 'Copy Trader Provider' sends a percentage to manage. 'Signal Provider' sends a quote to manage.

(ZIG) Exchange: 'Binance' or 'Kucoin'.

(ZIG) Exchange Type {Spot}: 'Spot' or 'Futures'.

(ZIG) Leverage {1}. Set it to '1' when '(ZIG) Exchange Type' is set to 'Spot'.

__ SETTINGS - Strategy

(STRAT) Strategy Type: 'Long and Short', 'Long Only' or 'Short Only'.

(STOPTAKE) Take Profit? {false}: Whether to enable Take Profit.

(STOPTAKE) Stop Loss? {True}: Whether to enable Stop Loss.

(TRAILING) Enable Trailing Take Profit (%) {True}: Whether to enable Trailing Take Profit.

(STOPTAKE) Take Profit % {3.0}: Take profit percentage. This setting is only used when '(STOPTAKE) Take Profit?' setting is set to true.

(STOPTAKE) Stop Loss % {2.0}: Stop loss percentage. This setting is only used when '(STOPTAKE) Stop Loss?' setting is set to true.

(TRAILING) Trailing Take Profit Trigger (%) {2.5}: Trailing Stop Trigger Percentage. This setting is only used when '(TRAILING) Enable Trailing Take Profit (%)' setting is set to true.

(TRAILING) Trailing Take Profit as a percentage of Trailing Take Profit Trigger (%) {25.0}: Trailing Stop Distance Percentage. This setting is only used when '(TRAILING) Enable Trailing Take Profit (%)' setting is set to true.

(RECENT) Number of minutes to wait to open a new order after the previous one has been opened {6}.

DEFAULT SETTINGS

By default this strategy has been setup with these beginner settings:

'(ZIG) Integration type' : TradingView only

'(ZIG) Provider type' : 'Copy Trader Provider'

'(ZIG) Exchange' : 'Binance'

'(ZIG) Exchange Type' : 'Spot'

'(STRAT) Strategy Type' : 'Long Only'

'(ZIG) Leverage' : '1' (Or no leverage)

but you can change those settings if needed.

FIRST STEP

For both future of spot markets you should make sure to change '(ZIG) Zignaly Alert Type' to match either WebHook or Email. If you have a non paid account in TradingView as in October 2020 you would have to use Email which it's free to use.

RECOMMENDED SETTINGS

__ RECOMMENDED SETTINGS - Spot markets

'(ZIG) Exchange Type' setting should be set to 'Spot'

'(STRAT) Strategy Type' setting should be set to 'Long Only'

'(ZIG) Leverage' setting should be set to '1'

__ RECOMMENDED SETTINGS - Future markets

'(ZIG) Exchange Type' setting should be set to 'Futures'

'(STRAT) Strategy Type' setting should be set to 'Long and Short'

'(ZIG) Leverage' setting might be changed if desired.

__ RECOMMENDED SETTINGS - Signal Providers

'(ZIG) Provider type' setting should be set to 'Signal Provider'

'(CAPITAL) Capital quote invested per order in USDT units' setting might be changed if desired.

__ RECOMMENDED SETTINGS - Copy Trader Providers

'(ZIG) Provider type' setting should be set to 'Copy Trader Provider'

'(CAPITAL) Capital percentage invested per order (%)' setting might be changed if desired.

Strategy Properties setting: 'Initial Capital' might be changed if desired.

INTEGRATION TYPE EXPLANATION

'Hybrid': Both TradingView and Zignaly handle take profit, trailing stops and stop losses. Useful if you are scared about TradingView not firing an alert. It might arise problems if TradingView and Zignaly get out of sync.

'TradingView only': TradingView sends entry and exit orders to Zignaly so that Zignaly only buys or sells. Zignaly won't handle stop loss or other settings on its own.

HOW TO USE THIS STRATEGY

Beginner: Copy and paste the strategy and change it to your needs. Turn off '(DEBUG) Enable debug on order comments' setting.

Medium: Reuse functions and inputs from this strategy into your own as if it was a library.

Advanced: Check Strategy Tester. List of trades. Copy and paste the different suggested 'alert_message' variable contents to your script.

Expert: I needed a way to pass data from TradingView script to the alert. Now I know it's the 'alert_message' variable. I can do this own my own.

ALERTS SETUP

This is the important piece of information that allows you to connect TradingView to Zignaly in a semi-automatic manner.

__ ALERTS SETUP - WebHook

Webhook URL: https : // zignaly . com / api / signals.php?key=MYSECRETKEY

Message: { {{strategy.order.alert_message}} , "key" : "MYSECRETKEY" }

__ ALERTS SETUP - Email

Setup a new Hotmail account

Add it as an 'SMS email' in TradingView Profile settings page.

Confirm your own the email address

Create a rule in your Hotmail account that 'Redirects' (not forwards) emails to 'signals @ zignaly . email' when (1): 'Subject' includes 'Alert', (2): 'Email body' contains string 'MYZIGNALYREDIRECTTRIGGER' and (3): 'From' contains 'noreply @ tradingview . com'.

In 'More Actions' check: Send Email-to-SMS

Message: ||{{strategy.order.alert_message}}||key=MYSECRETKEY||

MYZIGNALYREDIRECTTRIGGER

'(DEBUG) Enable debug on order comments' is turned on by default so that you can see in the Strategy Tester. List of Trades. The different orders alert_message that would have been sent to your alert. You might want to turn it off it some many letters in the screen is problem.

STRATEGY ADVICE

If you turn on 'Take Profit' then turn off 'Trailing Take Profit'.

ZIGNALY SIDE ADVICE

If you are a 'Signal Provider' make sure that 'Allow reusing the same signalId if there isn't any open position using it?' setting in the profile tab is set to true.

You can find your 'MYSECRETKEY' in your 'Copy Trader/Signal' provider Edit tab at 'Signal URL'.

ADDITIONAL ZIGNALY DOCUMENTATION

docs . zignaly . com / signals / how-to -- How to send signals to Zignaly

3 Ways to send signals to Zignaly

SIGNALS

FINAL REMARKS

This strategy tries to match the Pine Script Coding Conventions as best as possible.

Hammer Long strategy with filtered and enforced alertsA Hammer Long strategy is a price pattern in candlestick charting that occurs when a security trades significantly lower than its opening, but rallies within the period to close near opening price. This pattern forms a hammer-shaped candlestick , in which the lower shadow is at least twice the size of the real body. The body of the candlestick represents the difference between the open and closing prices, while the shadow shows the high and low prices for the period.

Key takeaways:

Hammers have a small real body and a long lower shadow.

Hammers occur after a price decline.

The hammer candlestick shows sellers came into the market during the period but by the close the selling had been absorbed and buyers had pushed the price back to near the open.

The close can be above or below the open, although the close should be near the open in order for the real body to remain small.

The lower shadow should be at least two times the height of the real body.

Hammer candlesticks indicate a potential price reversal to the upside.

The strategy enhances standard Hammer pattern accuracy by clearing out market noises and manipulations from the indicator's triggers. Combination of Volume oscillator filter and Directional Movement Index (DMI) components values adjustments allows to detect only strong signals. The strategy is developed to forecast Long positions entries and exits. The strategy supports spot, futures, options and marginal trading exchanges. It works accurately with BTC, USD, USDT, ETH and BNB quote currencies. Best to use with 30 and 60 minutes timeframe charts. The strategy can be and should be configured for each particular asset. You can change filters and risk management settings to receive the most advanced accurate alerts

Advantages of this script:

1. Weak signals and market noises are filtered. This allows to receive only strong and confirmed alerts

2. Strategy can be easily configured in user interface for each particular asset

3. High performance. At the chart you can see examples of strategy entries and exits, you also can check strategy backtest for RENUSDT position:

Net profit: 26.95%

Percent profitable: 90%

Profit factor: 7.418

Duration of trade: 16 hours

How to use?

1. Apply indicator to the trading pair your are interested in at 30m or 60m timeframe chart

2. Configure the strategy: change filters values and risk management settings until Strategy tester shows good results according to mathematical expectation

3. Set up a TradingView alert to trigger when Hammer strategy conditions are met

4. Strategy will send alerts when to enter and when to exit positions

If you want to obtain access to the indicator please send us a personal message

[NLX-L3] Backtest- Introduction -

This backtest module is part of my new modular trading framework - however it can be used with any indicator that has a signal plot output (1 = long / -1 = short)

I chose to release this one first, I've got all the modules for the framework ready and they going to be released in the coming days. Got to start somewhere... ;)

This trading framework is the result of many years experience building indicators and trading strategies.

I couldn’t find a trading framework in Pine Script that would suit my needs and so I started to design my own from scratch. I’m trading with this framework myself so I’ve made sure that it’s flexible and absolutely reliable in a live-trading environment.

- Architecture -

What makes this framework so flexible is the modular architecture, different layers that all serve a very specific purpose.

You will notice that the module names include either L1 - L2 or L3:

- Layer 1 (L1) is the base layer and the foundation. L1 indicators are used to determine the trend, volume profile and filter noise. You would use L1 to see if it’s a good time to trade, what is the direction - or if it's better to trade at all in unfavourable conditions

- Layer 2 (L2) receives the result of L1 and if the market conditions are good the L2 indicator looks for an optimal entry point to go long or short. It is possible to combine several L2 indicators and trigger a long/short signal only if all L2 indicators agree.

- Layer 3 (L3) receives the final signal from L2 and it’s where we can now backtest the result of our trading strategy and trigger trade alerts with help of the alert module.

- Features -

External Input Source (any indicator with signal plot can be used)

Safe Entries Option: Enter a trade only if the position is profitable ad the momentum allows

Pyramid Entries

Partial Take-Profit: %-Step Interval and Quantity per Step

Stop Methods: Trailing Stop, TP/SL with ATR Option, several type of stop bands...

Profit/Loss Label with Fee, Slippage and Leverage Calculation

- Upcoming Modules -

I'll release a couple of great indicators and filter in the coming days...

Trend Score (includes 10 different Trend and Filter algorithms)

Breakouts & Pullbacks

QQE++

True Range Filter

Support / Resistance

Consolidation Range Breakouts

- Alerts & Trading Automation -

Will be released shortly. Check my signature below.

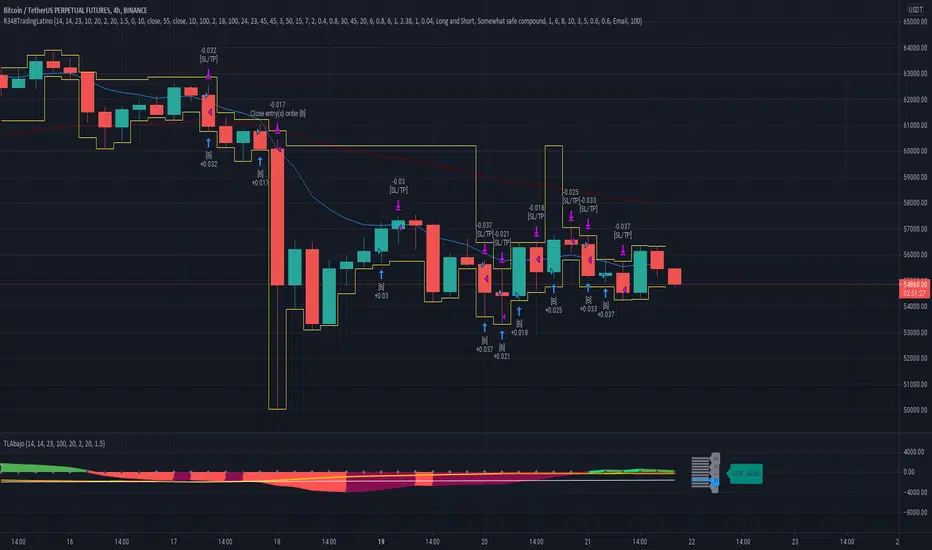

Ruckard TradingLatinoThis strategy tries to mimic TradingLatino strategy.

The current implementation is beta.

Si hablas castellano o espanyol por favor consulta MENSAJE EN CASTELLANO más abajo.

It's aimed at BTCUSDT pair and 4h timeframe.

STRATEGY DEFAULT SETTINGS EXPLANATION

max_bars_back=5000 : This is a random number of bars so that the strategy test lasts for one or two years

calc_on_order_fills=false : To wait for the 4h closing is too much. Try to check if it's worth entering a position after closing one. I finally decided not to recheck if it's worth entering after an order is closed. So it is false.

calc_on_every_tick=false

pyramiding=0 : We only want one entry allowed in the same direction. And we don't want the order to scale by error.

initial_capital=1000 : These are 1000 USDT. By using 1% maximum loss per trade and 7% as a default stop loss by using 1000 USDT at 12000 USDT per BTC price you would entry with around 142 USDT which are converted into: 0.010 BTC . The maximum number of decimal for contracts on this BTCUSDT market is 3 decimals. E.g. the minimum might be: 0.001 BTC . So, this minimal 1000 amount ensures us not to entry with less than 0.001 entries which might have happened when using 100 USDT as an initial capital.

slippage=1 : Binance BTCUSDT mintick is: 0.01. Binance slippage: 0.1 % (Let's assume). TV has an integer slippage. It does not have a percentage based slippage. If we assume a 1000 initial capital, the recommended equity is 142 which at 11996 USDT per BTC price means: 0.011 BTC. The 0.1% slippage of: 0.011 BTC would be: 0.000011 . This is way smaller than the mintick. So our slippage is going to be 1. E.g. 1 (slippage) * 0.01 (mintick)

commission_type=strategy.commission.percent and commission_value=0.1 : According to: binance . com / en / fee / schedule in VIP 0 level both maker and taker fees are: 0.1 %.

BACKGROUND

Jaime Merino is a well known Youtuber focused on crypto trading

His channel TradingLatino

features monday to friday videos where he explains his strategy.

JAIME MERINO STANCE ON BOTS

Jaime Merino stance on bots (taken from memory out of a 2020 June video from him):

'~

You know. They can program you a bot and it might work.

But, there are some special situations that the bot would not be able to handle.

And, I, as a human, I would handle it. And the bot wouldn't do it.

~'

My long term target with this strategy script is add as many

special situations as I can to the script

so that it can match Jaime Merino behaviour even in non normal circumstances.

My alternate target is learn Pine script

and enjoy programming with it.

WARNING

This script might be bigger than other TradingView scripts.

However, please, do not be confused because the current status is beta.

This script has not been tested with real money.

This is NOT an official strategy from Jaime Merino.

This is NOT an official strategy from TradingLatino . net .

HOW IT WORKS

It basically uses ADX slope and LazyBear's Squeeze Momentum Indicator

to make its buy and sell decisions.

Fast paced EMA being bigger than slow paced EMA

(on higher timeframe) advices going long.

Fast paced EMA being smaller than slow paced EMA

(on higher timeframe) advices going short.

It finally add many substrats that TradingLatino uses.

SETTINGS

__ SETTINGS - Basics

____ SETTINGS - Basics - ADX

(ADX) Smoothing {14}

(ADX) DI Length {14}

(ADX) key level {23}

____ SETTINGS - Basics - LazyBear Squeeze Momentum

(SQZMOM) BB Length {20}

(SQZMOM) BB MultFactor {2.0}

(SQZMOM) KC Length {20}

(SQZMOM) KC MultFactor {1.5}

(SQZMOM) Use TrueRange (KC) {True}

____ SETTINGS - Basics - EMAs

(EMAS) EMA10 - Length {10}

(EMAS) EMA10 - Source {close}

(EMAS) EMA55 - Length {55}

(EMAS) EMA55 - Source {close}

____ SETTINGS - Volume Profile

Lowest and highest VPoC from last three days

is used to know if an entry has a support

VPVR of last 100 4h bars

is also taken into account

(VP) Use number of bars (not VP timeframe): Uses 'Number of bars {100}' setting instead of 'Volume Profile timeframe' setting for calculating session VPoC

(VP) Show tick difference from current price {False}: BETA . Might be useful for actions some day.

(VP) Number of bars {100}: If 'Use number of bars (not VP timeframe)' is turned on this setting is used to calculate session VPoC.

(VP) Volume Profile timeframe {1 day}: If 'Use number of bars (not VP timeframe)' is turned off this setting is used to calculate session VPoC.

(VP) Row width multiplier {0.6}: Adjust how the extra Volume Profile bars are shown in the chart.

(VP) Resistances prices number of decimal digits : Round Volume Profile bars label numbers so that they don't have so many decimals.

(VP) Number of bars for bottom VPOC {18}: 18 bars equals 3 days in suggested timeframe of 4 hours. It's used to calculate lowest session VPoC from previous three days. It's also used as a top VPOC for sells.

(VP) Ignore VPOC bottom advice on long {False}: If turned on it ignores bottom VPOC (or top VPOC on sells) when evaluating if a buy entry is worth it.

(VP) Number of bars for VPVR VPOC {100}: Number of bars to calculate the VPVR VPoC. We use 100 as Jaime once used. When the price bounces back to the EMA55 it might just bounce to this VPVR VPoC if its price it's lower than the EMA55 (Sells have inverse algorithm).

____ SETTINGS - ADX Slope

ADX Slope

help us to understand if ADX

has a positive slope, negative slope

or it is rather still.

(ADXSLOPE) ADX cut {23}: If ADX value is greater than this cut (23) then ADX has strength

(ADXSLOPE) ADX minimum steepness entry {45}: ADX slope needs to be 45 degrees to be considered as a positive one.

(ADXSLOPE) ADX minimum steepness exit {45}: ADX slope needs to be -45 degrees to be considered as a negative one.

(ADXSLOPE) ADX steepness periods {3}: In order to avoid false detection the slope is calculated along 3 periods.

____ SETTINGS - Next to EMA55

(NEXTEMA55) EMA10 to EMA55 bounce back percentage {80}: EMA10 might bounce back to EMA55 or maybe to 80% of its complete way to EMA55

(NEXTEMA55) Next to EMA55 percentage {15}: How much next to the EMA55 you need to be to consider it's going to bounce back upwards again.

____ SETTINGS - Stop Loss and Take Profit

You can set a default stop loss or a default take profit.

(STOPTAKE) Stop Loss % {7.0}

(STOPTAKE) Take Profit % {2.0}

____ SETTINGS - Trailing Take Profit

You can customize the default trailing take profit values

(TRAILING) Trailing Take Profit (%) {1.0}: Trailing take profit offset in percentage

(TRAILING) Trailing Take Profit Trigger (%) {2.0}: When 2.0% of benefit is reached then activate the trailing take profit.

____ SETTINGS - MAIN TURN ON/OFF OPTIONS

(EMAS) Ignore advice based on emas {false}.

(EMAS) Ignore advice based on emas (On closing long signal) {False}: Ignore advice based on emas but only when deciding to close a buy entry.

(SQZMOM) Ignore advice based on SQZMOM {false}: Ignores advice based on SQZMOM indicator.

(ADXSLOPE) Ignore advice based on ADX positive slope {false}

(ADXSLOPE) Ignore advice based on ADX cut (23) {true}

(STOPTAKE) Take Profit? {false}: Enables simple Take Profit.

(STOPTAKE) Stop Loss? {True}: Enables simple Stop Loss.

(TRAILING) Enable Trailing Take Profit (%) {True}: Enables Trailing Take Profit.

____ SETTINGS - Strategy mode

(STRAT) Type Strategy: 'Long and Short', 'Long Only' or 'Short Only'. Default: 'Long and Short'.

____ SETTINGS - Risk Management

(RISKM) Risk Management Type: 'Safe', 'Somewhat safe compound' or 'Unsafe compound'. ' Safe ': Calculations are always done with the initial capital (1000) in mind. The maximum losses per trade/day/week/month are taken into account. ' Somewhat safe compound ': Calculations are done with initial capital (1000) or a higher capital if it increases. The maximum losses per trade/day/week/month are taken into account. ' Unsafe compound ': In each order all the current capital is gambled and only the default stop loss per order is taken into account. That means that the maximum losses per trade/day/week/month are not taken into account. Default : 'Somewhat safe compound'.

(RISKM) Maximum loss per trade % {1.0}.

(RISKM) Maximum loss per day % {6.0}.

(RISKM) Maximum loss per week % {8.0}.

(RISKM) Maximum loss per month % {10.0}.

____ SETTINGS - Decimals

(DECIMAL) Maximum number of decimal for contracts {3}: How small (3 decimals means 0.001) an entry position might be in your exchange.

EXTRA 1 - PRICE IS IN RANGE indicator

(PRANGE) Print price is in range {False}: Enable a bottom label that indicates if the price is in range or not.

(PRANGE) Price range periods {5}: How many previous periods are used to calculate the medians

(PRANGE) Price range maximum desviation (%) {0.6} ( > 0 ): Maximum positive desviation for range detection

(PRANGE) Price range minimum desviation (%) {0.6} ( > 0 ): Mininum negative desviation for range detection

EXTRA 2 - SQUEEZE MOMENTUM Desviation indicator

(SQZDIVER) Show degrees {False}: Show degrees of each Squeeze Momentum Divergence lines to the x-axis.

(SQZDIVER) Show desviation labels {False}: Whether to show or not desviation labels for the Squeeze Momentum Divergences.

(SQZDIVER) Show desviation lines {False}: Whether to show or not desviation lines for the Squeeze Momentum Divergences.

EXTRA 3 - VOLUME PROFILE indicator

WARNING: This indicator works not on current bar but on previous bar. So in the worst case it might be VP from 4 hours ago. Don't worry, inside the strategy calculus the correct values are used. It's just that I cannot show the most recent one in the chart.

(VP) Print recent profile {False}: Show Volume Profile indicator

(VP) Avoid label price overlaps {False}: Avoid label prices to overlap on the chart.

EXTRA 4 - ZIGNALY SUPPORT

(ZIG) Zignaly Alert Type {Email}: 'Email', 'Webhook'. ' Email ': Prepare alert_message variable content to be compatible with zignaly expected email content format. ' Webhook ': Prepare alert_message variable content to be compatible with zignaly expected json content format.

EXTRA 5 - DEBUG

(DEBUG) Enable debug on order comments {False}: If set to true it prepares the order message to match the alert_message variable. It makes easier to debug what would have been sent by email or webhook on each of the times an order is triggered.

HOW TO USE THIS STRATEGY

BOT MODE: This is the default setting.

PROPER VOLUME PROFILE VIEWING: Click on this strategy settings. Properties tab. Make sure Recalculate 'each time the order was run' is turned off.

NEWBIE USER: (Check PROPER VOLUME PROFILE VIEWING above!) You might want to turn on the 'Print recent profile {False}' setting. Alternatively you can use my alternate realtime study: 'Resistances and supports based on simplified Volume Profile' but, be aware, it might consume one indicator.

ADVANCED USER 1: Turn on the 'Print price is in range {False}' setting and help us to debug this subindicator. Also help us to figure out how to include this value in the strategy.

ADVANCED USER 2: Turn on the all the (SQZDIVER) settings and help us to figure out how to include this value in the strategy.

ADVANCED USER 3: (Check PROPER VOLUME PROFILE VIEWING above!) Turn on the 'Print recent profile {False}' setting and report any problem with it.

JAIME MERINO: Just use the indicator as it comes by default. It should only show BUY signals, SELL signals and their associated closing signals. From time to time you might want to check 'ADVANCED USER 2' instructions to check that there's actually a divergence. Check also 'ADVANCED USER 1' instructions for your amusement.

EXTRA ADVICE

It's advised that you use this strategy in addition to these two other indicators:

* Squeeze Momentum Indicator

* ADX

so that your chart matches as close as possible to TradingLatino chart.

ZIGNALY INTEGRATION

This strategy supports Zignaly email integration by default. It also supports Zignaly Webhook integration.

ZIGNALY INTEGRATION - Email integration example

What you would write in your alert message:

||{{strategy.order.alert_message}}||key=MYSECRETKEY||

ZIGNALY INTEGRATION - Webhook integration example

What you would write in your alert message:

{ {{strategy.order.alert_message}} , "key" : "MYSECRETKEY" }

CREDITS

I have reused and adapted some code from

'Directional Movement Index + ADX & Keylevel Support' study

which it's from TradingView console user.

I have reused and adapted some code from

'3ema' study

which it's from TradingView hunganhnguyen1193 user.

I have reused and adapted some code from

'Squeeze Momentum Indicator ' study

which it's from TradingView LazyBear user.

I have reused and adapted some code from

'Strategy Tester EMA-SMA-RSI-MACD' study

which it's from TradingView fikira user.

I have reused and adapted some code from

'Support Resistance MTF' study

which it's from TradingView LonesomeTheBlue user.

I have reused and adapted some code from

'TF Segmented Linear Regression' study

which it's from TradingView alexgrover user.

I have reused and adapted some code from

"Poor man's volume profile" study

which it's from TradingView IldarAkhmetgaleev user.

FEEDBACK

Please check the strategy source code for more detailed information

where, among others, I explain all of the substrats

and if they are implemented or not.

Q1. Did I understand wrong any of the Jaime substrats (which I have implemented)?

Q2. The strategy yields quite profit when we should long (EMA10 from 1d timeframe is higher than EMA55 from 1d timeframe.

Why the strategy yields much less profit when we should short (EMA10 from 1d timeframe is lower than EMA55 from 1d timeframe)?

Any idea if you need to do something else rather than just reverse what Jaime does when longing?

FREQUENTLY ASKED QUESTIONS

FAQ1. Why are you giving this strategy for free?

TradingLatino and his fellow enthusiasts taught me this strategy. Now I'm giving back to them.

FAQ2. Seriously! Why are you giving this strategy for free?

I'm confident his strategy might be improved a lot. By keeping it to myself I would avoid other people contributions to improve it.

Now that everyone can contribute this is a win-win.

FAQ3. How can I connect this strategy to my Exchange account?

It seems that you can attach alerts to strategies.

You might want to combine it with a paying account which enable Webhook URLs to work.

I don't know how all of this works right now so I cannot give you advice on it.

You will have to do your own research on this subject. But, be careful. Automating trades, if not done properly,

might end on you automating losses.

FAQ4. I have just found that this strategy by default gives more than 3.97% of 'maximum series of losses'. That's unacceptable according to my risk management policy.

You might want to reduce default stop loss setting from 7% to something like 5% till you are ok with the 'maximum series of losses'.

FAQ5. Where can I learn more about your work on this strategy?

Check the source code. You might find unused strategies. Either because there's not a substantial increases on earnings. Or maybe because they have not been implemented yet.

FAQ6. How much leverage is applied in this strategy?

No leverage.

FAQ7. Any difference with original Jaime Merino strategy?

Most of the times Jaime defines an stop loss at the price entry. That's not the case here. The default stop loss is 7% (but, don't be confused it only means losing 1% of your investment thanks to risk management). There's also a trailing take profit that triggers at 2% profit with a 1% trailing.

FAQ8. Why this strategy return is so small?

The strategy should be improved a lot. And, well, backtesting in this platform is not guaranteed to return theoric results comparable to real-life returns. That's why I'm personally forward testing this strategy to verify it.

MENSAJE EN CASTELLANO

En primer lugar se agradece feedback para mejorar la estrategia.

Si eres un usuario avanzado y quieres colaborar en mejorar el script no dudes en comentar abajo.

Ten en cuenta que aunque toda esta descripción tenga que estar en inglés no es obligatorio que el comentario esté en inglés.

CHISTE - CASTELLANO

¡Pero Jaime!

¡400.000!

¡Tu da mun!

Random entry pointsIt is profitable strategy with random entry points.

A simple strategy involving random opening of trades. But such a strategy on large samples will demonstrate profit. Because the strategy adheres to the golden rule of trading: "Let profits rise and quickly stop losses."

Remember, exit points are very important. Many traders make the mistake of focusing all their attention on entry points.

HFT Divergence Hunter BacktesterDefault Settings are meant to be used in BTC /USDT chart on 5 min time frame on Binance Futures . If you want to use for another asset on another time frame YOU MUST CHANGE THE SETTINGS

This is a divergence finding strategy developed by HFT Research. It is a highly customizable strategy and provides endless opportunities to find profitable trades in the market.

Default Settings are meant to be used in BTC /USDT chart on 5 min time frame on Binance Futures . If you want to use for another asset on another time frame YOU MUST CHANGE THE SETTINGS

This is a divergence finding indicator developed by HFT Research. It is a highly customizable indicator and provides endless opportunities to find profitable trades in the market.

Use Envelope , this is the main decision maker in this strategy. The idea behind is that you choose the length of the moving average and set an offset % to create an upper and lower band. If you click on “display envelope” you will be able to visually see the band you have created. This way, you get to scalp the market as the price is diverging and moving away from the moving average. As the famous saying goes, moving averages act like magnets and prices always visits them back. Using this ideology, we aim to capitilize on the price swings that move away from the chosen moving average by x%.

STARC Bands ;

These are two bands that are applied above and below a simple moving average of an asset’s price. The upper band is created by adding the value of the average true range (ATR) or a multiple of i. The lower band is created by subtracting the value of the ATR from the SMA . The channel can provide traders with ideas on when to buy or sell. During an overall uptrend, buying near the lower band and selling near the top band is favorable. However, from our testing results it does fairly poorly in crypto markets while it does pretty well in traditional markets.

Use RSI ;

One of the most commonly used indicators in the trading world. The idea is simple, buy when its oversold and sell when its overbought. You can use RSI as a secondary confirmation of the dips. It can be turned on and off.

Use MFI

MFI stands for Money Flow Index and it is an oscillator like RSI . However, it does track the price in a different fashion than RSI providing a reliable option. It uses the price and volume data for identifying overbought and oversold signals in an asset.

Use Fisher Transform

Even though, it has a funny name, Fisher is actually a very decent and reliable indicator. It converts the prices into a Gaussian normal distribution channel. Therefore, the indicator detects when the prices have moved to an extreme, based on recent price action.

Use VWAP

VWAP stands for volume weighted average price . It is an extremely useful indicator when trading intra-day. It does reset every trading session which is at 00:00 UTC . Instead of looking at x number of candles and providing an average price, it will take into consideration the volume that’s traded at a certain price and weigh it accordingly. It will NOT give entry signals but act as a filter. If the price is above VWAP will filter out the shorts and other way around for longs.

Use ADX

Average directional index is a powerful indicator when one is assessing the strength of a trend as well as measuring the volatility in the market. Unfortunately, the worst market condition for this strategy is sideways market. ADX becomes a useful tool since it can detect trend. If the volatility is low and there is no real price movement, ADX will pick that up and will not let you get in trades during a sideways market. It will allow you to enter trades only when the market is trending.

Use Super trend Filter

The indicator works well in a trending market but can give false signals when a market is trading in a range.

It uses the ATR ( average true range ) as part of its calculation which takes into account the volatility of the market. The ATR is adjusted using the multiplier setting which determines how sensitive the indicator is.

Use MA Filter

Lookback: It is an option to look back x number of candles to validate the price crossing. If the market is choppy and the price keeps crossing up and down the moving average you have chosen, it will generate a lot of “noisy” signals. This option allows you to confirm the cross by selecting how many candles the price needs to stay above or below the moving average. Setting it 0 will turn it off.

MA Filter Type: There is a selection of moving averages that is available on TradingView currently. You can choose from 14 different moving average types to detect the trend as accurate as possible.

Filter Length: You can select the length of your moving average. Most commonly used length being 50,100 and 200.

Filter Type: This is our propriety smoothing method in order to make the moving averages lag less and influence the way they are calculated slightly. Type 1 being the normal calculation and type 2 being the secret sauce .

Reverse MA Filter: This option allows you to use the moving average in reverse. For example, the strategy will go long when the price is above the moving average. However, if you use the reserve MA Filter, you will go short when the price is above the moving average. This method works best in sideways market where price usually retraces back to the moving average. So, in an anticipation of price reverting back to the moving average, it is a useful piece of option to use during sideway markets.

Use MACD Filter

MACD here will act as a filter rather than an entry signal generator. There are a few different ways to use this MACD filter. You can click on the Use MACD filter and it will use filter out the shorts generated in a bullish territory and longs generated in the bearish territory. It will greatly reduce the number of trades the strategy will trade because MACD is a lagging indicator. By the time MACD turns bullish or bearish , most of the other indicators will have already generated the signals. Therefore, resulting in less trades. You can use MACD filter as MA oscillator meaning that it will only look at the MA lines in MACD to filter out trades. Alternatively, you can use it with the histogram (Signal lines) meaning that it will only look at the histogram whether its below or above the zero line in order to filter out the trades.

TP (%)

Place your desired take profit percentage here. Default is 1.5%

Move SL At Entry x% Profit

This is when the strategy will move your SL to the entry point if the position reaches x% profit. It can also generate a signal which can be automated to adjust the SL on the exchange.

SL (%)

Place your desired stop loss percentage here. Default is 1%

The backtester assumes the following;

- 1000$ capital

- 0.06% commission based on binance

- 1% risk meaning 100% equity on cross leverage

- Backtest results are starting from 2020

If you want to get access to this indicator please DM me or visit our website.

BV's MACD SIGNAL TESTERHello ladies and gentlemen,

Today, as you may have seen in the title, I have coded a strategy to determine once and for all if MACD could make you money in 2020.

So, at the end of this video, you will know which MACD strategy will bring you the most money.

Spoiler alert: we've hit the 90% WinRAte mark on the Euro New Zealand Dollar chart.

I've seen a lot of videos of people testing different MACD signals, some up to 100 times.

But In my opinion, all traders must rely on statistics to put all the odds on their side and good statistics require a lot more data.

The algorithm I'm showing you tests each signal one by one over a 3 year period and on 28 different graphs.

That way we are sure that we have encountered all possible market behavior.

From phases of congestion to major trends or even the effects of COVID-19

I use the ATR to determine my Stop Loss and Take Profits. The Stop Loss is placed at 1.5 times the ATR, the Take Profit is placed at 1 time the ATR.

If my Take Profit is hit, I take 50% of the profits and let the position run by moving my Stop Loss to Zero.

This way, the position can no longer be a losing position.

If you are not familiar with this practice, I invite you to study the "Scaling out" video from the NoNonsenseForex channel.

BV's Trading Journal.

Best strategy for TradingView (fake)Hello everyone! I want to show you this strategy so you don't fall for the tricks of scammers. On TradingView, you can write an algorithm (probably more than one) that will show any profit you want: from 1% to 100,000% in one year (maybe more)! This can be done, for example, using the built-in linebreak () function and several conditions for opening long and short.

I am sure that sometimes scammers show up on TradingView showing their incredible strategies. Will a smart person sell a profitable quick strategy? When a lot of people start using the quick strategy, it stops working. Therefore, no smart person would sell you a quick strategy. It is acceptable to sell slow strategies: several transactions per month - this does not greatly affect the market.

So, don't fall for the tricks of scammers, write quick strategies yourself.

About this strategy, I can say that the linebreak () function does not work correctly in it. Accordingly, the lines are not drawn correctly on the chart. They are drawn in such a way as to show the maximum profit. I watched this algorithm on a 1m timeframe - no lines are drawn in real time. This is a fake!

Buy The Dips - MA200 OptimisedThe strategy combines a contrarian approach (buying the dips) with a trend-following logic (only when the price is above the MA200)

The strategy seeks to find the best times when buying the dips on the asset should result to be more profitable.

The price above a long-term moving average indicates momentum that increases the possibility of profiting from buying the asset on short-term weakness.

MarketGodx for Tradingview - Strategy TestMarketGodx for Tradingview

Version = MarketGodx²

Indicator Description

MarketGodx weighs the probability of a given scenario and the outcome associated to prior events before sequentially weighing the impact of a probable move by the significance of the timeframe and its corresponding close sequence relative to other TFs, The indicator combines several components of classical technical analysis and then provides a Buy or Sell alert to traders, which is then acted upon by the user. There are modifications made to alerts to manipulate them in the alternating appearance as the visual above shows.

MarketGod can be applied to any market, with any time-frame associated to it. The signals relay the alert at the close of the period, and the painted alert is then available to users to see on the chart or even set notifications for via tradingview's alert system. We recommend that users implement marketgod on their preferred time frames for trading, which for us is the 1h, 4h, 6h, 1D and above TFs.

Indicator Components

Gann Trend Analysis

Stochastic K

Stochastic D

KDJ Calculation

MACD

SlowRSI

Bollinger Band

Keltner Channels

Ichimoku Cloud

HHLL Trend Detector

MarketGod EMA , WMA , SMA , HullMA

Accumulation + Distribution

Suggested Uses

MarketGod will inevitably produce false positives. We've taken steps to reduce this but we highly suggest you add this as a component of your strategy, not an end all be all

That said, please do not feel the need to fire a trade based solely on a marketgod signal, or to every signal it fires.

MarketGod users should backtest their strategy using OHLC candles for best results

Heikin Ashi candles were recomended in the past, and we have eliminated the need for them, meaning that traditional candlestick inputs will yield the highest results.

MarketGod will always give stronger alerts on higher TF's. If the 1-Day has fired a given signal and the 30 min or similar fire the opposite signal, know that the overall trend is still likely downward. Same concept applies to all timeframes on this tool.

Adjusting the Filter Settings

This tool has a noise filter for users to adjust.

The filter is a percentage based calculation, between significant points in time. The filter ranges between .5 and 25, with .5 increments

For lower TFs (IE Intraday), keep the filter set between .5-5

Mid-TFs (4H,6H,12H,1D), the recommended range is between 5.5-10

Higher TFs (3D and Higher), look for approx 11-20 range

Customizations

Customize the indicator by adjusting the colors in the style pane. Additionally, users can change the plots into labels with the price of close added to them, or a few other label text options, listed in the 'inputs' panel, below the filter adjustments. Users can also opt to turn the strategy orders as well, as this version will have them printed.

Strategy Performance Interpretation

Its important to understand the only metric that should be relevant is not the win %, as many may initially think. Alternatively, the only metric that matters in the end is your take home profit... meaning the profit one fees and taxes are accounted for. In our example here, the % brought back since the beginning of our window of 2018 is around 47% for $10,000 initial capital and 10% traded per position. Many are ignorant to the take home profit aspect as they focus solely on the winning %, which is ultimately incorrect approach to trading as a whole. as long as we maintain +30% (our goal minimum), the outcome being in the green, is our goal.

Access MarketGod for Tradingview

Learn more about how to access this tool by following the links in our signature below.

GOAT Signals Custom No Repaint Buy Sell Arrow Strategy Tester

WELCOME to GOAT Signals Custom No Repaint Buy Sell Moving Average (MA) Strategy Tester!

This indicator can quickly and easily identify the past trading success of signals based on moving averages.

What is a Moving Average?

According to investopedia.com a moving average (MA) is a widely used indicator in technical analysis that helps smooth out price action by filtering out the “noise” from random short-term price fluctuations.

Keeping this in mind let me give an example how this indicator could be useful in identifying trends.

Many Bitcoin traders use the 21 moving average on the weekly chart to make trading decisions.

Some of this has to do with 21 being a Fibonacci sequence number, and also because of how Bitcoin price action has reacted to it's trend line in the past.

When applying this script to the Bitcoin(BLX) weekly chart with a 21 moving average the strategy tester gives us 33.33 % Percent Profitable results with 6.31 % Net Profit.

If we test another moving average, let's try 29, and change our step input to 1, we get 85.71 % Percent Profitable with 9.22 % Net Profit.

With a bit of tweaking we may be able to find charts and settings with even better performance.

Keep in mind the strategy tester does not calculate trading fees, therefore in most cases will work better on longer time frames.

The Step input gives price action some breathing space if desired. Steps can be added or subtracted.

Personally, I use the Daily and Weekly charts except during high volatility, and use a one or two bar trail depending on price action.

Past performance does NOT guarantee future gains but keep in mind Bitcoin, Litecoin and a few others are on deflationary cycles.

For full invite only access please contact DogeyBlaze.

Alert Script And Limited Time Free Trial Available.

Not Certified Financial Advice.

Crypto Scalper Pro===========

Crypto Scalper Pro Strategy

===========

Crypto Scalper Pro is a scalping strategy developed to work alongside our Crypto Tipster Strategy, now you can trade the D markets with our Tipster, and Intra-Day markets with our Scalper!

This strategy works very well on shorter time frames across multiple crypto pairs, everything from 4H all the way down to a 5m chart, our Crypto Scalper will find the best Entry and Exit points for consistent and reliable returns.

We've added a few variables for you to play with to fine tune this scalper to suit your chosen trading plan - however, these will only adjust the strategy to a certain degree, as there are many algorithms and indicators doing their thing hidden in the background that take precedence.

Check out the Crypto Scalper Pro Alert Indicator to automate this strategy!

-----------

What's Included?

Crypto Scalper Pro comes with a host of features and is being continually updated, these features include (but are not limited to):

- Date Range Settings

Setting custom Start/End dates can help hone your strategy to suit the current times, or get a general overview of the market over the years.

- Heikin Ashi Confirmation

We added HA confirmation for both Entry & Exit of trades. This started as a form of "Safe Mode", we have since adapted our safe mode far beyond Heikin Ashi; but kept this confirmation as an added extra.

- Variable Indicator Settings

As well as our Fixed Indicators and Price Action analysis going on in the background of the strategy, we've also included some Variable Indicators that you have access to edit.

Lookback Period will help establish how far back you'd want to be confirming price indications on the strategy - the higher the number the further back it will look, making the Scalping Strategy appear smoother with less trades during choppy times, the downside with a higher lookback is you might miss the start of a potentially epic trade, and only be shown an Entry after the event has already happened.

We find Lookback Lengths of between 5 and 100 could work depending on various other settings, the market being traded, and the timeframe being used.

MA Length (Length of Moving Average) - We use a few MA's to best determine various factors involved with successfully scalping a market, overall trend direction, current price movements and fake-out detection to name just a few. You've got the option of determining a good average length for a few of these variables.

Again, a short MA Length will catch every big move right at the start, but you're almost guaranteed a Negative Expected Value with that method, due to the vast quantity of losing trades in times of chop/ranging markets. A Higher MA Length will remove a lot of chop, reduce the quantity of trades, and therefore (should) result in a higher Percent of Trades Profitable; it will however add a certain lag to the strategy, meaning those highly profitable trades we're looking for may turn out to be not so highly profitable!

- Safe Mode

Enabling Safe Mode will add a couple more confirmation indicators to the strategy - the aim of Safe Mode is, in essence, to remove any trading signals that would end of being false/bad moves. Usually resulting in less Overall Trades, a higher Net Profit, higher % Profitable, higher Profit Factor AND a lower Drawdown. Use Safe Mode to help eliminate orders that would otherwise be placed in choppy markets.

- Stop Loss/Take Profit Settings

This is where Crypto Scalper Pro really proves itself, Money Management. We have an editable Fixed SL/TP, as well as Trailing Stops for Long or Short orders, all of which you can use on their own, or combined with each other. Playing with these settings can turn an un-profitable system into a very-profitable trading plan!

-----------

For more information and a FREE 7-Day Trial with the Crypto Scalper Pro Strategy visit the link in our signature.

Good Luck and Happy Trading!

Takashi Bows Autopilot | 2nd Gen | [Strategy]This is a strategy tester for Takashi Bows Autopilot indicator. Please check for more details and instructions at our website.

Takashi Bows Autopilot is the ultimate trading tool. Effortless, its signals put traders inside strong trends, locking big profits that cover all loss generated during sideways trends.

An upgrade version of Takashi Bows v1, this script is the result of some operations developed by us, it can easily adapt to different markets and time frames. Now ranging from level 1 to 20, traders can select the amount of signals to be displayed on the chart. Based on price movement, it signals entries after strong movement up or down.

Take Profit included. If a position is opened in one direction, it should be closed at take profit levels or when a position in the opposite direction is opened.

Inputs

Level

Integer input. Sets a level for signals generated up and down. The higher the level, more signals on chart, and vice-versa.

Take Profit %

Float input. Sets a percent of take profit for exiting previous open position.

Rule

Float input. Sets a ruler for more accuracy on less volatile markets. Standard value 1 for high volatile markets, higher values for low volatile markets.

Disclaimer:

Back-tests do not guarantee performance on the future. Even if a trading setup is profitable in historical data. it could be unprofitable in the future.

To get access to this and other scripts check links below.

ARKADIY V1.0This strategy is made for trading Bitcoin (BTC) using data from BITMEX exchange on 4 hour timeframe.

There is also a special indicator for the strategy to receive alerts on your tradingview platform which is very handful to enter the market as soon as there is a buy/sell signal.

Strategy is based on Pine script v.4 and it uses several indicators and oscillators (modified RSI, CCI, ADX, TRIX and EMA) to generate a buy/sell signal for BTC.

There is no repaint, which means that a signal will not disappear when price goes in wrong direction.

And this is one of the advantages of the strategy over other 90% strategies.

The strategy is a SWING strategy, which means that a signal for opening a position (buy or sell) at the same time closes previous position.

Because of its specificity the strategy doesn’t have take profit/stop loss options and doesn’t use leverage.

The strategy has a backtest statistics on TradingView. 2018 – 1197%, 2019 – 79%, until March 13, 2020 – 88% of net profit.

Max drawdown (the sum of non-profitable trades until receiving a profitable trade) during a year not more than 14%.

To get access to the strategy write in comments and in private messages.

_____________________________________________________________________________________________________________

Данная стратегия работает на инструменте биткоин ( BTC ) по котировкам биржи BITMEX на 4 часовом таймфрейме, а также имеет удобные алерты для сигналов на сделку (будильник).

Это позволит Вам заниматься своими делами, не следя за тем, что происходит на рынке, но в нужное время совершить сделку, получив предупреждение на телефон / компьютер.

Стратегия построена на последней версии Pine Script, в ее основе лежит совокупность множества индикаторов и правил (модифицированные RSI, CCI, ADX, TRIX and EMA), которые в определенный момент дают сигнал на покупку или продажу BTC . Стратегия протестирована с использованием аргумента "Recalculate After Order is Filled" и подразумевает "non-repaint" базис. Другими словами, если стратегия показала вход в сделку (по итогу закрытия свечи) - то сигнал так и остается без изменений. Это выгодно отличает данную стратегию от 90% таковых в Trading View и дает уверенность, что появившийся сигнал не исчезнет в случае, если рынок пойдет в противоположную сторону.

Данная стратегия относится к сегменту SWING стратегий, когда один сигнал является одновременно закрытием одной сделки и открытием противоположной.

В связи со спецификой стратегии она не использует стоп-ордера, поэтому предполагает торговлю без плечей.

Ваш риск ограничен временным интервалом от момента, как цена пошла в противоположную сторону, до момента пока стратегия не дала сигнал на перекладку в новую сделку.

Статистика, подтвержденная бэктестом в Trading View, за последние пару лет: 2018 - 197%, 2019 - 79%, на 13.03.20 - 88%. Это данные по Чистой прибыли на вложенный капитал.

Максимальная длящаяся просадка (совокупность минусовых сделок до момента возникновения плюсовой сделки) в течение года составляет не более 18%

Основные отличия от индикаторов наших коллег:

+ Результаты бэктеста не в excell, а в платформе Trading View – прозрачная статистика по сделкам

+ Построен на принципах non-repaint basis – сигналы не исчезают и не появляются из неоткуда

+ Работает на 4Н таймфрейме. Это значит сделки не могут быть чаще, чем в раз в 4 часа. Занимайтесь своими делами, пока стратегия стоит на страже рыночного анализа. Она сама Вам сообщит, когда нужно открыть / закрыть сделку.

+ Разберется любой! Стратегия построена по принципу one-click setup

+ Поддержка с возможностью организации телефонного звонка.

Для предоставления доступа к данной стратегии - пожалуйста пишите в комментариях запрос с копией в личные сообщения. Мы быстро с Вами свяжемся.