Trend Hunter Scalping [Daddin Algo]Trend Hunter Scalping Strategy Description

This strategy is a comprehensive scalping system designed to capture high-frequency trading opportunities within short timeframes. It combines multiple technical indicators to assess trend direction, momentum, volatility, and volume dynamics. Importantly, all parameters are user-adjustable, allowing the strategy to be optimized for various market conditions and individual preferences.

Technical Indicators and Settings

EMA (Exponential Moving Average):

The EMA is calculated based on a user-defined period. Rather than being fixed (e.g., a 200-period EMA), the period is adjustable to suit different market conditions. The position of the price relative to the EMA helps confirm the overall trend.

RSI & RSIOver:

The Relative Strength Index (RSI) measures momentum and the speed of price changes. Entry signals are generated when the RSI crosses its moving average. Additionally, overbought and oversold thresholds (set by the user) add an extra layer of confirmation for the signals.

ADX:

The Average Directional Index (ADX) assesses the strength of the current trend. When the ADX is above a user-specified threshold, the signals are considered more reliable. This helps in filtering out signals during weak trending periods.

Bollinger Bands:

Bollinger Bands gauge market volatility. The settings—including the length and the multiplier—are adjustable, providing flexibility to accommodate tightening or expanding volatility conditions.

Parabolic SAR:

This indicator identifies dynamic support and resistance levels, confirming the trend direction and helping pinpoint potential entry and exit points.

Pivot Levels (Fibonacci):

Calculated from the previous period's high, low, and close, pivot points and Fibonacci levels indicate potential reversal points and serve as support and resistance levels. These levels provide context for setting trailing stops and managing risk.

Volume Filter:

A volume condition ensures that trading signals are only considered valid when the current volume exceeds a multiple of its short-term moving average. This filter is adjustable, helping to confirm the strength of the market move.

Daddin Line:

Derived from a short-term moving average of the closing prices with a user-defined offset, the Daddin Line acts as an additional confirmation tool. Its parameters can be customized to better align with specific trading environments.

Trading Logic and Management

Signal Direction and Entry:

The strategy can generate both long (buy) and short (sell) signals, or be limited to one direction based on user preference. Entry orders are executed when all the selected indicator conditions are met. Additionally, maximum consecutive trade limits are implemented to help control risk.

Exit & Take Profit:

Trades are exited automatically when a user-defined profit percentage is reached. This take-profit percentage is flexible, enabling adjustments to match different market conditions or trading goals.

Trailing Stop (Dynamic Stop Loss):

A trailing stop mechanism is implemented using Fibonacci pivot levels. Once a position is open, the stop loss is dynamically updated as the price moves favorably. This ensures that profits are protected while minimizing losses in case of a sudden reversal.

Additional Features and Backtesting

Time Filtering (Backtesting):

The strategy includes a date range filter for backtesting. Users can define the start and end dates to evaluate the strategy’s performance during specific market periods, making it easier to assess its historical effectiveness.

Customizable Parameters:

Every indicator and risk management setting is fully customizable. This adaptability allows traders to tailor the strategy to different assets, timeframes, and market environments, ensuring optimal performance across diverse trading scenarios.

Conclusion

The Trend Hunter Scalping strategy effectively integrates multiple technical indicators to validate trends and manage risks efficiently. Its highly flexible, user-adjustable parameters make it adaptable to varying market conditions, providing traders with a robust framework for capturing quick trading opportunities.This strategy is designed to optimize both entry and exit points while offering comprehensive risk management controls.

"profit" için komut dosyalarını ara

IU BBB(Big Body Bar) StrategyDESCRIPTION

The IU BBB (Big Body Bar) Strategy is a price action-based trading strategy that identifies high-momentum candles with significantly larger body sizes compared to the average. It enters trades when a strong bullish or bearish move occurs and manages risk using an ATR-based trailing stop-loss system.

USER INPUTS:

- Big Body Threshold – Defines how many times larger the candle body should be compared to the average body ( default is 4 ).

- ATR Length – The period for the Average True Range (ATR) used in the trailing stop-loss calculation ( default is 14 ).

- ATR Factor – Multiplier for ATR to determine the trailing stop distance ( default is 2 ).

LONG CONDITION:

- The current candle’s body is greater than the average body size multiplied by the Big Body Threshold.

- The closing price is higher than the opening price (bullish candle).

SHORT CONDITION:

- The current candle’s body is greater than the average body size multiplied by the Big Body Threshold.

- The closing price is lower than the opening price (bearish candle).

LONG EXIT:

- ATR-based trailing stop-loss dynamically adjusts, locking in profits as the price moves higher.

SHORT EXIT:

- ATR-based trailing stop-loss dynamically adjusts, securing profits as the price moves lower.

WHY IT IS UNIQUE:

- Unlike traditional momentum strategies, this system adapts to volatility by filtering trades based on relative candle size.

- It incorporates an ATR-based trailing stop-loss, ensuring risk management and profit protection.

- The strategy avoids choppy market conditions by only trading when significant momentum is present.

HOW USERS CAN BENEFIT FROM IT:

- Catch Strong Price Moves – The strategy helps traders enter trades when the market shows decisive momentum.

- Effective Risk Management – The ATR-based trailing stop ensures that winning trades remain profitable.

- Works Across Markets – Can be applied to stocks, forex, crypto, and indices with proper optimization.

- Fully Customizable – Users can adjust sensitivity settings to match their trading style and time frame.

Simple APF Strategy Backtesting [The Quant Science]Simple backtesting strategy for the quantitative indicator Autocorrelation Price Forecasting. This is a Buy & Sell strategy that operates exclusively with long orders. It opens long positions and generates profit based on the future price forecast provided by the indicator. It's particularly suitable for trend-following trading strategies or directional markets with an established trend.

Main functions

1. Cycle Detection: Utilize autocorrelation to identify repetitive market behaviors and cycles.

2. Forecasting for Backtesting: Simulate trades and assess the profitability of various strategies based on future price predictions.

Logic

The strategy works as follow:

Entry Condition: Go long if the hypothetical gain exceeds the threshold gain (configurable by user interface).

Position Management: Sets a take-profit level based on the future price.

Position Sizing: Automatically calculates the order size as a percentage of the equity.

No Stop-Loss: this strategy doesn't includes any stop loss.

Example Use Case

A trader analyzes a dayli period using 7 historical bars for autocorrelation.

Sets a threshold gain of 20 points using a 5% of the equity for each trade.

Evaluates the effectiveness of a long-only strategy in this period to assess its profitability and risk-adjusted performance.

User Interface

Length: Set the length of the data used in the autocorrelation price forecasting model.

Thresold Gain: Minimum value to be considered for opening trades based on future price forecast.

Order Size: percentage size of the equity used for each single trade.

Strategy Limit

This strategy does not use a stop loss. If the price continues to drop and the future price forecast is incorrect, the trader may incur a loss or have their capital locked in the losing trade.

Disclaimer!

This is a simple template. Use the code as a starting point rather than a finished solution. The script does not include important parameters, so use it solely for educational purposes or as a boilerplate.

3Commas Multicoin Scalper LITE [SwissAlgo]

Introduction

Are you tired of tracking cryptocurrency charts and placing orders manually on your Exchange?

The 3Commas Multicoin Scalper LITE is an automated trading system designed to identify and execute potential trading setups on multiple cryptocurrencies ( simultaneously ) on your preferred Exchange (Binance, Bybit, OKX, Gate.io, Bitget) via 3Commas integration.

It analyzes price action, volume, momentum, volatility, and trend patterns across two categories of USDT Perpetual coins: the 'Top Major Coins' category (11 established cryptocurrencies) and your Custom Category (up to 10 coins of your choice).

The indicator sends real-time trading signals directly to your 3Commas bots for automated execution, identifying both trend-following and contrarian trading opportunities in all market conditions.

Trade automatically all coins of one or more selected categories:

----------------------------------------------

What it Does

The 3Commas Multicoin Scalper LITE is a technical analysis tool that monitors multiple cryptocurrency pairs simultaneously and connects with 3Commas for signal delivery and execution.

Here's how the strategy works:

🔶 Technical Analysis : Analyzes price action, volume, momentum, volatility, and trend patterns across USDT Perpetual Futures contracts simultaneously.

🔶 Pattern Detection : Identifies specific candle patterns and technical confluences that suggest potential trading setups across USDT.P contracts of the selected category.

🔶 Signal Generation : When technical criteria are met at bar close, the indicator creates deal-start signals for the relevant pairs.

🔶 3Commas Integration : Packages these signals and delivers them to 3Commas through TradingView alerts, allowing 3Commas bots to receive specific pair information ('Deal-Start' signals).

🔶 Category Management : Each TradingView alert monitors an entire category, allowing selective activation of different crypto categories.

🔶 Visual Feedback : Provides color-coded candles and backgrounds to visualize technical conditions, with optional pivot points and trend visualization.

Candle types

Signals

----------------------------------------------

Quick Start Guide

1. Setup 3Commas Bots : Configure two DCA bots in 3Commas (All USDT pairs) - one for LONG positions and one for SHORT positions.

2. Define Trading Parameters : Set your budget for each trade and adjust your preferred sensitivity within the indicator settings.

3. Create Category Alerts : Set up one TradingView alert for each crypto category you want to trade.

That's it! Once configured, the system automatically sends signals to your 3Commas bots when predefined trading setups are detected across coins in your selected/activated categories. The indicator scans all coins at bar close (for example, every hour on the 1H timeframe) and triggers trade execution only for those showing technical confluences.

Important : Consider your total capital when enabling categories. More details about the setup process are provided below (see paragraph "Detailed Setup & Configuration").

----------------------------------------------

Built-in Backtesting

The 3Commas Multicoin Scalper LITE includes backtesting visualization for each coin. When viewing any USDT Perpetual pair on your chart, you can visualize how the strategy would have performed historically on that specific asset.

Color-coded candles and signal markers show past trading setups, helping you evaluate which coins responded best to the strategy. This built-in backtesting capability can support your selection of assets/categories to trade before deploying real capital.

As backtesting results are hypothetical and do not guarantee future performance, your research and analysis are essential for selecting the crypto categories/coins to trade.

The default strategy settings are: Start Capital 1,000$, leverage 10X, Commissions 0.1% (average Taker Fee on Exchanges for average users), Order Amount 200$ for Longs/Shorts, Slippage 4

Example of backtesting view

----------------------------------------------

Key Features

🔶 Multi-Exchange Support : Compatible with BINANCE, BYBIT, BITGET, GATEIO, and OKX USDT Perpetual markets (USDT.P)

🔶 Category Options : Analyze cryptocurrencies in the Top Major Coins category or create your custom watchlist

🔶 Custom Category Option : Create your watchlist with up to 10 custom USDT Perpetual pairs

🔶 3Commas Integration : Seamlessly connects with 3Commas bots to automate trade entries and exits

🔶 Dual Strategy Approach : Identifies both "trend following" and "contrarian" potential setups

🔶 Confluence-Based Signals : Uses a combination of multiple technical factors - price spikes, price momentum, volume spikes, volume momentum, trend analysis, and volatility spikes - to generate potential trading setups

🔶 Risk Management : Adjustable sensitivity/risk levels, leverage settings, and budget allocation for each trade

🔶 Visual Indicators : Color-coded candles and trading signals provide visual feedback on market conditions

🔶 Trend Indication : Background colors showing ongoing uptrends/downtrends

🔶 Pivot Points & Daily Open : Optional display of pivot points and daily open price for additional context

🔶 Liquidity Analysis : Optional display of high/low liquidity timeframes throughout the trading week

🔶 Trade Control : Configurable limit for the maximum number of signals sent to 3Commas for execution (per bar close and category)

5 Available Exchanges

Pick coins/tokens and defined your Custom Category

----------------------------------------------

Methodology

The 3Commas Multicoin Scalper LITE utilizes a multi-faceted approach to identify potential trading setups:

1. Price Action Analysis : Detects abnormal price movements by comparing the current candle's range to historical averages and standard deviations, helping identify potential "pump and dump" scenarios or new-trends start

2. Price Momentum : Evaluates the relative strength of bullish vs. bearish price movements over time, indicating the build-up of buying or selling pressure.

3. Volume Analysis: Identifies unusual volume spikes by comparing current volume to historical averages, signaling strong market interest in a particular direction.

4. Volume Momentum : Measures the ratio of bullish to bearish volume, revealing the dominance of buyers or sellers over time.

5. Trend Analysis : Combines EMA slopes, RSI, and Stochastic RSI to determine overall trend direction and strength.

6. Volatility : Monitors the ATR (Average True Range) to detect periods of increased market volatility, which may indicate potential breakouts or reversals

7. Candle Wick Analysis : Evaluates upper and lower wick percentages to detect potential rejection patterns and reversals.

8. Pivot Point Analysis : Uses pivot points (PP, R1-R3, S1-S3) for identifying key support/resistance areas and potential breakout/breakdown levels.

9. Daily Open Reference: Analyzes price action relative to the daily open for potential setups related to price movement vs. the opening price

10. Market Timing/Liquidity : Evaluates high/low liquidity periods, specific days/times of heightened risk, and potential market manipulation timeframes.

11. Boost Factors : Applies additional weight to certain confluence patterns to adjust global scores

These factors are combined into a "Global Score" ranging from -1 to +1 , applied at bar close to the newly formed candles.

Scores above predefined thresholds (configurable via the Sensitivity Settings) indicate strong bullish or bearish conditions and trigger signals based on predefined patterns. The indicator then applies additional filters to generate specific "Trend Following" and "Contrarian" trading signals. The identified signals are packaged and sent to 3Commas for execution.

Pivot Points

Trend Background

----------------------------------------------

Who This Strategy Is For

The 3Commas Multicoin Scalper LITE may benefit:

Crypto Traders seeking to automate their trading across multiple coins simultaneously

3Commas Users looking to enhance their bot performance with technical signals

Busy Traders who want to monitor market opportunities without constant chart-watching

Multi-strategy traders interested in both trend-following and reversal trading approaches

Traders of Various Experience Levels from intermediate traders wanting to save time to advanced traders seeking to optimize their operations

Perpetual Futures Traders on major exchanges (Binance, Bybit, OKX, Gate.io, Bitget)

Swing and Scalp Traders seeking to identify short to medium-term profit opportunities

----------------------------------------------

Visual Indicators

The indicator provides visual feedback through:

1. Candlestick Colors :

* Lime: Strong bullish candle (High positive score)

* Blue: Moderate bullish candle (Medium positive score)

* Red: Strong bearish candle (High negative score)

* Purple: Moderate bearish candle (Medium negative score)

* Pale Green/Red: Mild bullish/bearish candle

2. Signal Markers :

* ↗: Trend following Long signal

* ↘: Trend following Short signal

* ⤴: Contrarian Long signal

* ⤵: Contrarian Short signal

3. Optional Elements :

* Pivot Points: Daily support/resistance levels (R1-R3, S1-S3, PP)

* Daily Open: Reference price level for the current trading day

* Trend Background: Color-coded background suggesting potential ongoing uptrend/downtrend

* Liquidity Highlighting: Background colors indicating typical high/low market liquidity periods

4. TradingView Strategy Plots and Backtesting Data : Standard performance metrics showing entry/exit points, equity curves, and trade statistics, based on the signals generated by the script.

----------------------------------------------

Detailed Setup & Configuration

The indicator features a user-friendly input panel organized in sequential steps to guide you through the complete setup process. Tooltips for each step provide additional information to help you understand the actions required to get the strategy running.

Informative tables provide additional details and instructions for critical setup steps such as 3Commas bot configuration and TradingView alert creation (to activate trading on specific categories).

1. Choose Exchange, Crypto Category & Sensitivity

* Select your USDT Perpetual Exchange (BINANCE, BYBIT, BITGET, GATEIO, or OKX) - i.e. the same Exchange connected in your 3Commas account

* Choose your preferred crypto category, or define your watchlist

* Choose from three sensitivity levels: Default, Aggressive, or Test Mode (test mode is designed to generate more signals, a potentially helpful feature when you are testing the indicator and alerts)

2. Setup 3Commas Bots and integrate them with the algo

* Create both LONG and SHORT DCA Bots in 3Commas

* Configure bots to accept signals for 'All USDT Pairs' with "TradingView Custom Signal" as deal start condition

* Enter your Bot IDs and Email Token in the indicator settings

* Set a maximum budget for LONG and SHORT trades

* Choose whether to allow LONG trades, SHORT trades, or both, according to your preference and market analysis

* Set maximum trades per bar/category (i.e. the max. number of simultaneous signals that the algo may send to your 3Commas bots for execution at every bar close - every hour if you set the 1H timeframe)

* Access the detailed setup guide table for step-by-step 3Commas configuration instructions

3Commas integration

3. Choose Visuals

* Toggle various optional visual elements to add to the chart: category metrics, fired alerts, coin metrics, daily open, pivot points

* Select a color theme: Dark or Light

4. Activate Trading via Alerts

* Create TradingView alerts for each category you want to trade

* Set alert condition to "3Commas Multicoin Scalper" with "Any alert() function call"

* Set the content of the message field to: {{Message}}, deleting the default content shown in this text field, to enable proper 3Commas integration (any other text than {{Message}}, would break the delivery trading signals from Tradingview to 3Commas)

* View the alerts setup instruction table for visual guidance on this critical step

Alerts

Fired Alerts (example at a single bar)

Fired Alerts (frequency)

Important Configuration Notes

Ensure that the TradingView chart's exchange matches your selected exchange in the indicator settings and your 3Commas bot settings.

You must configure the same leverage in both the script and your 3Commas bots

Your 3Commas bots must be configured for All USDT pairs

You must enter the exact Bot IDs and Email Token from 3Commas (these remain confidential - no one, including us, has access to them)

If you activate multiple categories without sufficient capital, 3Commas will display " insufficient funds " errors - align your available capital with the number of categories you activate (each deal will use the budget amount specified in user inputs)

You are free to set your Take Profit % / trailing on 3Commas

We recommend not to use DCA orders (i.e. set the number of DCA orders at zero)

Legend of symbols and plots on the chart

----------------------------------------------

FAQs

General Questions

❓ Q: What features are included in this indicator? A: This indicator provides access to the "Top Major Coins" category and a custom category option where you can define up to 10 pairs of your choice. It includes multi-exchange support, 3Commas integration, a dual strategy approach, visual indicators, trade controls, and comprehensive backtesting capabilities. The indicator is optimized to manage up to 2 trades per hour/category with leverage up to 10x and trade sizes up to 500 USDT - everything needed for traders looking to automate their crypto trading across multiple pairs simultaneously.

❓ Q: What is Global Score? A: The Global Score serves as a foundation for signal generation. When a candle's score exceeds certain thresholds (defined by your Risk Level setting), it becomes a candidate for signal generation. However, not all high-scoring candles generate trading signals - the indicator applies additional pattern recognition and contextual filters. For example, a strongly positive score (lime candle) in an established uptrend may trigger a "Trend Following" signal, while a strongly negative score (red candle) in a downtrend might generate a "Trend following Short" signal. Similarly, contrarian signals are generated when specific reversal patterns occur alongside appropriate Global Score values, often involving wick analysis and pivot point interactions. This multi-layer approach helps filter out false positives and identify higher-probability trading setups.

❓ Q: What's the difference between "Trend following" and "Contrarian" signals in the script? A: "Trend Following" signals follow the identified trends while "Contrarian" signals anticipate potential trend reversals.

❓ Q: Why don't I see any signals on my chart? A: Make sure you're viewing a USDT Perpetual pair from your selected exchange that belongs to the crypto category you've chosen to analyze. For example, if you've selected the "Top Major Coins" category with Binance as your exchange, you need to view a chart of one of those specific pairs (like BINANCE:BTCUSDT.P) to see signals. If you switch exchanges, for example from Binance to Bybit, you need to pull a Bybit pair on the chart to see backtesting data and signals.

❓ Q: Does this indicator guarantee profits? A: No. Trading cryptocurrencies involves significant risk, and past performance is not indicative of future results. This indicator is a tool to help you identify potential trading setups, but it does not and cannot guarantee profits.

❓ Q: Does this indicator repaint or use lookahead bias? A: No. All trading signals generated by this indicator are based only on completed price data and do not repaint. The system is designed to ensure that backtesting results reflect as closely as possible what you should experience in live trading.

While reference levels like pivot points are kept stable throughout the day using lookahead on, the actual buy and sell signals are calculated using only historical data (lookahead off) that would have been available at that moment in time. This ensures reliability and consistency between backtesting and real-time trading performance.

Technical Setup

❓ Q: What exchanges are supported? A: The strategy supports BINANCE, BYBIT, BITGET, GATEIO, and OKX USDT Perpetual markets (i.e. all the Exchanges you can connect to your 3Commas account for USDT Perpetual trading, excluding Coinbase Perpetual that offers USDC pairs, instead of USDT).

❓ Q: What timeframe should I use? A: The indicator is optimized for the 1-hour (1H) timeframe but may run on any timeframe.

❓ Q: How many coins can I trade at once? A: You can trade all coins within the selected category. You can activate categories by setting up alerts.

❓ Q: How many alerts do I need to set up? A: You need to set up one alert for each crypto category you want to trade. We recommend starting with one category, testing the results carefully, monitoring performance daily, and perhaps activating additional categories in a second stage.

❓ Q: Are there any specific risk management features built into the indicator? A: Yes, the indicator includes risk management features: adjustable maximum trades per hour/category, the ability to enable/disable long or short signals depending on market conditions, customizable trade size for both long and short positions, and different sensitivity/risk level settings.

❓ Q: What happens if 3Commas can't execute a signal? A: If 3Commas cannot execute a signal (due to insufficient funds, bot offline, etc.), the trade will be skipped. The indicator will continue sending signals for other valid setups, but it doesn't retry failed signals.

❓ Q: Can I run this indicator on multiple charts at once? A: Yes, but it's not necessary. The indicator analyzes all coins in your selected categories regardless of which chart you apply it to. For optimal resource usage, apply it to a single chart of a USDT Perpetual pair from your selected exchange. To stop trading a category, simply delete the alert created for that category.

❓ Q: How frequently does the indicator scan for new signals? A: The indicator scans all coins in your selected categories at the close of each bar (every hour if you selected the 1H timeframe).

----------------------------------------------

⚠️

Disclaimer

This indicator is for informational and educational purposes only and does not constitute financial advice. Trading cryptocurrencies involves significant risk, including the potential loss of all invested capital, and past performance is not indicative of future results.

Always conduct your own thorough research (DYOR) and understand the risks involved before making any trading decisions. Trading with leverage significantly amplifies both potential profits and losses - exercise extreme caution when using leverage and never risk more than you can afford to lose.

The Bot ID and Email Token information are transmitted directly from TradingView to 3Commas via secure connections. No third party or entity will ever have access to this data (including the Author). Do not share your 3Commas credentials with anyone.

This indicator is not affiliated with, endorsed by, or sponsored by TradingView or 3Commas.

FVG Breakout Lite by tradingbauhausExplanation of "FVG Breakout Lite by tradingbauhaus"

This script is a trading strategy built for TradingView that helps you spot and trade "Fair Value Gaps" (FVGs)—price areas where the market moved quickly, leaving a gap that might act as support or resistance later. It’s designed to catch breakout opportunities when the price moves strongly in one direction, with extra filters to make trades more reliable. Here’s how it works and how you can use it:

What It Does

1. Finds Fair Value Gaps (FVGs):

A "Bullish FVG" happens when the price jumps up quickly, leaving a gap below where it didn’t trade much (e.g., today’s low is higher than the high from two bars ago).

A "Bearish FVG" is the opposite: the price drops fast, leaving a gap above (e.g., today’s high is lower than the low from two bars ago).

The script draws colored boxes on your chart to show these gaps: green for bullish, red for bearish.

2. Spots Breakouts:

It looks for "strong" FVGs by comparing them to a trend (based on the highest highs and lowest lows over a set period).

If a bullish gap forms above the recent highs, or a bearish gap below the recent lows, it’s marked as a breakout opportunity.

3. Adds a Volume Check:

Trades only happen if the market’s volume is higher than usual (e.g., 1.2x the average volume over the last 20 bars). This helps ensure the breakout has real momentum behind it.

4. Trades Automatically:

Long Trades (Buy): If a bullish breakout FVG forms and volume is high, it buys at the current price.

Short Trades (Sell): If a bearish breakout FVG forms with high volume, it sells short.

Each trade comes with a stop loss (to limit losses) and a take profit (to lock in gains), both adjustable by you.

5. Shows Mitigation Lines (Optional):

If you turn on "Display Mitigation Zones," it draws lines at the edge of each breakout FVG. These lines show where the price might return to "fill" the gap later, helping you see key levels.

6. Includes Webull Costs:

The script factors in real trading fees from Webull, like tiny SEC and FINRA fees for selling, and a daily margin cost if you’re borrowing money to trade. These don’t show up on the chart but affect the strategy’s performance in backtesting.

How to Use It

1. Add to Your Chart:

Copy the script into TradingView’s Pine Editor, click "Add to Chart," and it’ll start drawing FVGs and running the strategy.

2. Customize Settings:

Trend Period (Default: 25): How many bars it looks back to define the trend. Longer periods mean fewer but stronger signals.

Volume Lookback (Default: 20) & Volume Threshold (Default: 1.2): Adjust how it measures "high volume." Increase the threshold for stricter trades.

Stop Loss % (Default: 1.5%) & Take Profit % (Default: 3%): Set how much you’re willing to lose or aim to gain per trade.

Margin Rate % (Default: 8.74%): Webull’s rate for borrowing money—lower it if your account qualifies for a better rate.

Display Mitigation Zones (Default: On): Toggle this to see or hide the gap lines.

Colors: Change the green (bullish) and red (bearish) shades to suit your chart.

3. Backtest It:

Go to the "Strategy Tester" tab in TradingView to see how it performs on past data. It’ll show trades, profits, losses, and Webull fees included.

4. Watch It Work:

Green boxes mean bullish FVGs; red boxes mean bearish FVGs. If volume spikes and the price breaks out, you’ll see trades happen automatically.

What to Expect

Visuals: You’ll see colored boxes for FVGs and optional lines showing where they start. These help you spot key price zones even if you’re not trading.

Trades: It’s selective—only trades when FVGs align with a breakout and volume confirms it. Expect fewer trades but with higher potential.

Risk: The stop loss keeps losses in check, while the take profit aims for a 2:1 reward-to-risk ratio by default (3% gain vs. 1.5% loss).

Costs: Webull’s fees are small but baked into the results, so you’re seeing a realistic picture of profits.

Tips for Users

Test it on a small timeframe (like 5-minute charts) for day trading or a larger one (like daily) for swing trading.

Play with the volume threshold—if you get too few trades, lower it (e.g., 1.1); if too many, raise it (e.g., 1.5).

Watch how price reacts to the mitigation lines—they’re often support or resistance zones traders target.

This strategy is lightweight, focused, and built for traders who like breakouts with a bit of confirmation. It’s not foolproof (no strategy is!), but it gives you a clear way to trade FVGs with some smart filters.

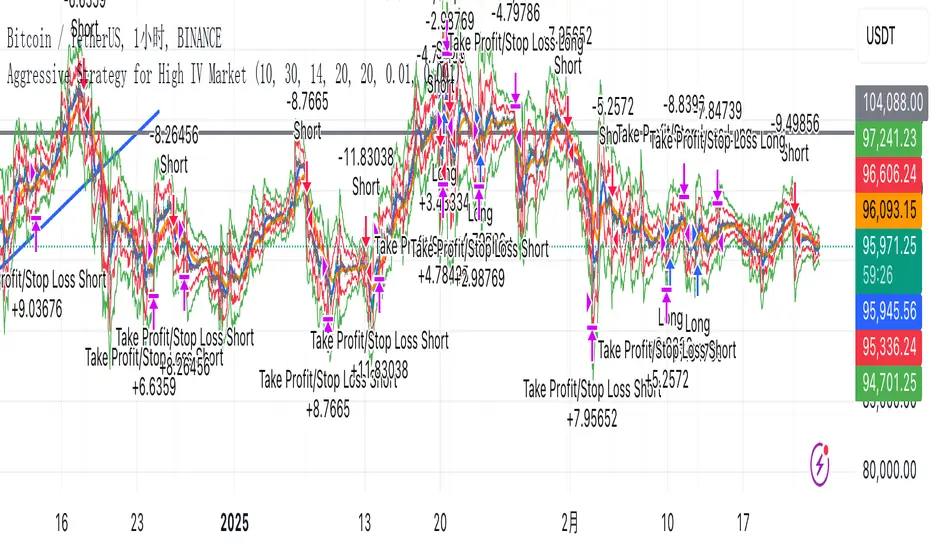

Aggressive Strategy for High IV Market### Strategic background

In a volatile high IV market, prices are volatile and market expectations of future uncertainty are high. This environment provides opportunities for aggressive trading strategies, but also comes with a high level of risk. In pursuit of a high Sharpe ratio (i.e., risk-adjusted return), we need to design a strategy that captures the benefits of market volatility while effectively controlling risk. Based on daily line cycles, I choose a combination of trend tracking and volatility filtering for highly volatile assets such as stocks, futures or cryptocurrencies.

---

### Strategy framework

#### Data

- Use daily data, including opening, closing, high and low prices.

- Suitable for highly volatile markets such as technology stocks, cryptocurrencies or volatile index futures.

#### Core indicators

1. ** Trend Indicators ** :

Fast Exponential Moving Average (EMA_fast) : 10-day EMA, used to capture short-term trends.

- Slow Exponential Moving Average (EMA_slow) : 30-day EMA, used to determine the long-term trend.

2. ** Volatility Indicators ** :

Average true Volatility (ATR) : 14-day ATR, used to measure market volatility.

- ATR mean (ATR_mean) : A simple moving average of the 20-day ATR that serves as a volatility benchmark.

- ATR standard deviation (ATR_std) : The standard deviation of the 20-day ATR, which is used to judge extreme changes in volatility.

#### Trading logic

The strategy is based on a trend following approach of double moving averages and filters volatility through ATR indicators, ensuring that trading only in a high-volatility environment is in line with aggressive and high sharpe ratio goals.

---

### Entry and exit conditions

#### Admission conditions

- ** Multiple entry ** :

- EMA_fast Crosses EMA_slow (gold cross), indicating that the short-term trend is turning upward.

-ATR > ATR_mean + 1 * ATR_std indicates that the current volatility is above average and the market is in a state of high volatility.

- ** Short Entry ** :

- EMA_fast Crosses EMA_slow (dead cross) downward, indicating that the short-term trend turns downward.

-ATR > ATR_mean + 1 * ATR_std, confirming high volatility.

#### Appearance conditions

- ** Long show ** :

- EMA_fast Enters the EMA_slow (dead cross) downward, and the trend reverses.

- or ATR < ATR_mean-1 * ATR_std, volatility decreases significantly and the market calms down.

- ** Bear out ** :

- EMA_fast Crosses the EMA_slow (gold cross) on the top, and the trend reverses.

- or ATR < ATR_mean-1 * ATR_std, the volatility is reduced.

---

### Risk management

To control the high risk associated with aggressive strategies, set up the following mechanisms:

1. ** Stop loss ** :

- Long: Entry price - 2 * ATR.

- Short: Entry price + 2 * ATR.

- Dynamic stop loss based on ATR can adapt to market volatility changes.

2. ** Stop profit ** :

- Fixed profit target can be selected (e.g. entry price ± 4 * ATR).

- Or use trailing stop losses to lock in profits following price movements.

3. ** Location Management ** :

- Reduce positions appropriately in times of high volatility, such as dynamically adjusting position size according to ATR, ensuring that the risk of a single trade does not exceed 1%-2% of the account capital.

---

### Strategy features

- ** Aggressiveness ** : By trading only in a high ATR environment, the strategy takes full advantage of market volatility and pursues greater returns.

- ** High Sharpe ratio potential ** : Trend tracking combined with volatility filtering to avoid ineffective trades during periods of low volatility and improve the ratio of return to risk.

- ** Daily line Cycle ** : Based on daily line data, suitable for traders who operate frequently but are not too complex.

---

### Implementation steps

1. ** Data Preparation ** :

- Get the daily data of the target asset.

- Calculate EMA_fast (10 days), EMA_slow (30 days), ATR (14 days), ATR_mean (20 days), and ATR_std (20 days).

2. ** Signal generation ** :

- Check EMA cross signals and ATR conditions daily to generate long/short signals.

3. ** Execute trades ** :

- Enter according to the signal, set stop loss and profit.

- Monitor exit conditions and close positions in time.

4. ** Backtest and Optimization ** :

- Use historical data to backtest strategies to evaluate Sharpe ratios, maximum retracements, and win rates.

- Optimize parameters such as EMA period and ATR threshold to improve policy performance.

---

### Precautions

- ** Trading costs ** : Highly volatile markets may result in frequent trading, and the impact of fees and slippage on earnings needs to be considered.

- ** Risk Control ** : Aggressive strategies may face large retracements and need to strictly implement stop losses.

- ** Scalability ** : Additional metrics (such as volume or VIX) can be added to enhance strategy robustness, or combined with machine learning to predict trends and volatility.

---

### Summary

This is a trend following strategy based on dual moving averages and ATR, designed for volatile high IV markets. By entering into high volatility and exiting into low volatility, the strategy combines aggressive and risk-adjusted returns for traders seeking a high sharpe ratio. It is recommended to fully backtest before implementation and adjust the parameters according to the specific market.

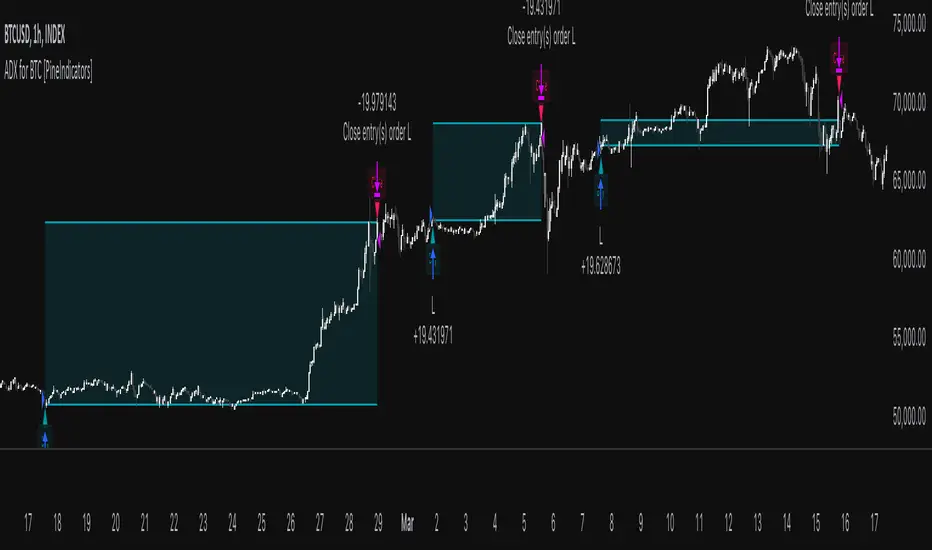

ADX for BTC [PineIndicators]The ADX Strategy for BTC is a trend-following system that uses the Average Directional Index (ADX) to determine market strength and momentum shifts. Designed for Bitcoin trading, this strategy applies a customizable ADX threshold to confirm trend signals and optionally filters entries using a Simple Moving Average (SMA). The system features automated entry and exit conditions, dynamic trade visualization, and built-in trade tracking for historical performance analysis.

⚙️ Core Strategy Components

1️⃣ Average Directional Index (ADX) Calculation

The ADX indicator measures trend strength without indicating direction. It is derived from the Positive Directional Movement (+DI) and Negative Directional Movement (-DI):

+DI (Positive Directional Index): Measures upward price movement.

-DI (Negative Directional Index): Measures downward price movement.

ADX Value: Higher values indicate stronger trends, regardless of direction.

This strategy uses a default ADX length of 14 to smooth out short-term fluctuations while detecting sustainable trends.

2️⃣ SMA Filter (Optional Trend Confirmation)

The strategy includes a 200-period SMA filter to validate trend direction before entering trades. If enabled:

✅ Long Entry is only allowed when price is above a long-term SMA multiplier (5x the standard SMA length).

✅ If disabled, the strategy only considers the ADX crossover threshold for trade entries.

This filter helps reduce entries in sideways or weak-trend conditions, improving signal reliability.

📌 Trade Logic & Conditions

🔹 Long Entry Conditions

A buy signal is triggered when:

✅ ADX crosses above the threshold (default = 14), indicating a strengthening trend.

✅ (If SMA filter is enabled) Price is above the long-term SMA multiplier.

🔻 Exit Conditions

A position is closed when:

✅ ADX crosses below the stop threshold (default = 45), signaling trend weakening.

By adjusting the entry and exit ADX levels, traders can fine-tune sensitivity to trend changes.

📏 Trade Visualization & Tracking

Trade Markers

"Buy" label (▲) appears when a long position is opened.

"Close" label (▼) appears when a position is exited.

Trade History Boxes

Green if a trade is profitable.

Red if a trade closes at a loss.

Trend Tracking Lines

Horizontal lines mark entry and exit prices.

A filled trade box visually represents trade duration and profitability.

These elements provide clear visual insights into trade execution and performance.

⚡ How to Use This Strategy

1️⃣ Apply the script to a BTC chart in TradingView.

2️⃣ Adjust ADX entry/exit levels based on trend sensitivity.

3️⃣ Enable or disable the SMA filter for trend confirmation.

4️⃣ Backtest performance to analyze historical trade execution.

5️⃣ Monitor trade markers and history boxes for real-time trend insights.

This strategy is designed for trend traders looking to capture high-momentum market conditions while filtering out weak trends.

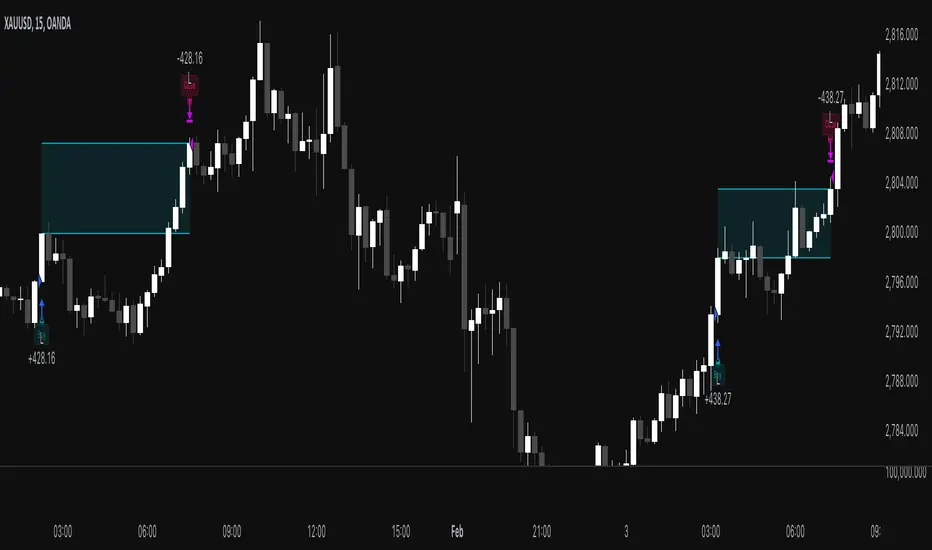

MACD Volume Strategy for XAUUSD (15m) [PineIndicators]The MACD Volume Strategy is a momentum-based trading system designed for XAUUSD on the 15-minute timeframe. It integrates two key market indicators: the Moving Average Convergence Divergence (MACD) and a volume-based oscillator to identify strong trend shifts and confirm trade opportunities. This strategy uses dynamic position sizing, incorporates leverage customization, and applies structured entry and exit conditions to improve risk management.

⚙️ Core Strategy Components

1️⃣ Volume-Based Momentum Calculation

The strategy includes a custom volume oscillator to filter trade signals based on market activity. The oscillator is derived from the difference between short-term and long-term volume trends using Exponential Moving Averages (EMAs)

Short EMA (default = 5) represents recent volume activity.

Long EMA (default = 8) captures broader volume trends.

Positive values indicate rising volume, supporting momentum-based trades.

Negative values suggest weak market activity, reducing signal reliability.

By requiring positive oscillator values, the strategy ensures momentum confirmation before entering trades.

2️⃣ MACD Trend Confirmation

The strategy uses the MACD indicator as a trend filter. The MACD is calculated as:

Fast EMA (16-period) detects short-term price trends.

Slow EMA (26-period) smooths out price fluctuations to define the overall trend.

Signal Line (9-period EMA) helps identify crossovers, signaling potential trend shifts.

Histogram (MACD – Signal) visualizes trend strength.

The system generates trade signals based on MACD crossovers around the zero line, confirming bullish or bearish trend shifts.

📌 Trade Logic & Conditions

🔹 Long Entry Conditions

A buy signal is triggered when all the following conditions are met:

✅ MACD crosses above 0, signaling bullish momentum.

✅ Volume oscillator is positive, confirming increased trading activity.

✅ Current volume is at least 50% of the previous candle’s volume, ensuring market participation.

🔻 Short Entry Conditions

A sell signal is generated when:

✅ MACD crosses below 0, indicating bearish momentum.

✅ Volume oscillator is positive, ensuring market activity is sufficient.

✅ Current volume is less than 50% of the previous candle’s volume, showing decreasing participation.

This multi-factor approach filters out weak or false signals, ensuring that trades align with both momentum and volume dynamics.

📏 Position Sizing & Leverage

Dynamic Position Calculation:

Qty = strategy.equity × leverage / close price

Leverage: Customizable (default = 1x), allowing traders to adjust risk exposure.

Adaptive Sizing: The strategy scales position sizes based on account equity and market price.

Slippage & Commission: Built-in slippage (2 points) and commission (0.01%) settings provide realistic backtesting results.

This ensures efficient capital allocation, preventing overexposure in volatile conditions.

🎯 Trade Management & Exits

Take Profit & Stop Loss Mechanism

Each position includes predefined profit and loss targets:

Take Profit: +10% of risk amount.

Stop Loss: Fixed at 10,100 points.

The risk-reward ratio remains balanced, aiming for controlled drawdowns while maximizing trade potential.

Visual Trade Tracking

To improve trade analysis, the strategy includes:

📌 Trade Markers:

"Buy" label when a long position opens.

"Close" label when a position exits.

📌 Trade History Boxes:

Green for profitable trades.

Red for losing trades.

📌 Horizontal Trade Lines:

Shows entry and exit prices.

Helps identify trend movements over multiple trades.

This structured visualization allows traders to analyze past performance directly on the chart.

⚡ How to Use This Strategy

1️⃣ Apply the script to a XAUUSD (Gold) 15m chart in TradingView.

2️⃣ Adjust leverage settings as needed.

3️⃣ Enable backtesting to assess past performance.

4️⃣ Monitor volume and MACD conditions to understand trade triggers.

5️⃣ Use the visual trade markers to review historical performance.

The MACD Volume Strategy is designed for short-term trading, aiming to capture momentum-driven opportunities while filtering out weak signals using volume confirmation.

2xSPYTIPS Strategy by Fra public versionThis is a test strategy with S&P500, open source so everyone can suggest everything, I'm open to any advice.

Rules of the "2xSPYTIPS" Strategy :

This trading strategy is designed to operate on the S&P 500 index and the TIPS ETF. Here’s how it works:

1. Buy Conditions ("BUY"):

- The S&P 500 must be above its **200-day simple moving average (SMA 200)**.

- This condition is checked at the **end of each month**.

2. Position Management:

- If leverage is enabled (**2x leverage**), the purchase quantity is increased based on a configurable percentage.

3. Take Profit:

- A **Take Profit** is set at a fixed percentage above the entry price.

4. Visualization & Alerts:

- The **SMA 200** for both S&P 500 and TIPS is plotted on the chart.

- A **BUY signal** appears visually and an alert is triggered.

What This Strategy Does NOT Do

- It does not use a **Stop Loss** or **Trailing Stop**.

- It does not directly manage position exits except through Take Profit.

FRAMA-LRO📌 FRAMA × LRO Auto-Trading Strategy - Adaptive Trend & Momentum System

Overview

This Pine Script provides an automated trading strategy that combines FRAMA (Fractal Adaptive Moving Average) and LRO (Linear Regression Oscillator) to enhance trend detection and momentum analysis. Unlike traditional moving averages, FRAMA dynamically adjusts to price volatility, while LRO effectively measures momentum for high-precision entries.

📌 Key Features

1. Dynamic Trend & Momentum Synergy

FRAMA: Detects price trends by adjusting to market conditions using fractal dimensions.

LRO: Filters trades based on linear regression slope momentum.

Breakout Confirmation: Entry is validated when price breaks FRAMA bands with LRO support.

2. Realistic Backtesting Settings

Initial Capital: $5,000 (more in line with retail traders).

Risk Management: 5% equity per trade.

Slippage & Commission: Adjusted to realistic values (1 pip slippage, 94 pips spread per trade).

Backtest Data: Covers at least 100 trades for statistical significance.

3. Clear Trade Logic

Long Entry: Price breaks above FRAMA upper band & LRO > 0.

Short Entry: Price breaks below FRAMA lower band & LRO < 0.

Stop-Loss: Dynamic ATR-based calculation.

Take-Profit: Fixed risk-reward ratio (1:2).

📌 How It Works

The system identifies trend strength with FRAMA, then confirms momentum shifts with LRO before executing trades. This ensures higher accuracy and filters false breakouts.

📌 Visual Aids for Clarity

Color-Coded Candles:

🟢 Uptrend (LRO > 0)

🔵 Downtrend (LRO < 0)

⚪ Neutral (LRO ≈ 0)

Chart Annotations: Clearly marked trade signals for easy reference.

📌 Risk Management & Automation

Fully automated execution of entries, stop-loss, and take-profit.

ATR-based volatility adaptation for dynamic SL adjustments.

Customizable parameters (period, volatility settings, risk percentage).

📌 Originality & Enhancements

This script is not just a combination of FRAMA & LRO, but an optimized system designed to:

Improve signal accuracy using adaptive trend detection.

Eliminate noise with LRO-based momentum filtering.

Implement dynamic risk management via ATR-based SL.

Influences & Acknowledgments

This strategy builds on methodologies inspired by ChartPrime and BigBeluga, refining their concepts for a systematic approach.

📌 Disclaimer

This script is for educational purposes only. Past performance does not guarantee future results. Always manage risk appropriately.

SMA + RSI + Volume + ATR StrategySMA + RSI + Volume + ATR Strategy

1. Indicators Used:

SMA (Simple Moving Average): This is a trend-following indicator that calculates the average price of a security over a specified period (50 periods in this case). It's used to identify the overall trend of the market.

RSI (Relative Strength Index): This measures the speed and change of price movements. It tells us if the market is overbought (too high) or oversold (too low). Overbought is above 70 and oversold is below 30.

Volume: This is the amount of trading activity. A higher volume often indicates strong interest in a particular price move.

ATR (Average True Range): This measures volatility, or how much the price is moving in a given period. It helps us adjust stop losses and take profits based on market volatility.

2. Conditions for Entering Trades:

Buy Signal (Green Up Arrow):

Price is above the 50-period SMA (indicating an uptrend).

RSI is below 30 (indicating the market might be oversold or undervalued, signaling a potential reversal).

Current volume is higher than average volume (indicating strong interest in the move).

ATR is increasing (indicating higher volatility, suggesting that the market might be ready for a move).

Sell Signal (Red Down Arrow):

Price is below the 50-period SMA (indicating a downtrend).

RSI is above 70 (indicating the market might be overbought or overvalued, signaling a potential reversal).

Current volume is higher than average volume (indicating strong interest in the move).

ATR is increasing (indicating higher volatility, suggesting that the market might be ready for a move).

3. Take Profit & Stop Loss:

Take Profit: When a trade is made, the strategy will set a target price at a certain percentage above or below the entry price (1.5% in this case) to automatically exit the trade once that target is hit.

Stop Loss: If the price goes against the position, a stop loss is set at a percentage below or above the entry price (0.5% in this case) to limit losses.

4. Execution of Trades:

When the buy condition is met, the strategy will enter a long position (buying).

When the sell condition is met, the strategy will enter a short position (selling).

5. Visual Representation:

Green Up Arrow: Appears on the chart when the buy condition is met.

Red Down Arrow: Appears on the chart when the sell condition is met.

These arrows help you see at a glance when the strategy suggests you should buy or sell.

In Summary:

This strategy uses a combination of trend-following (SMA), momentum (RSI), volume, and volatility (ATR) to decide when to buy or sell a stock. It looks for opportunities when the market is either oversold (buy signal) or overbought (sell signal) and makes sure there’s enough volume and volatility to back up the move. It also includes take-profit and stop-loss levels to manage risk.

Smart DCA Invest LiteEnglish description:

📊 Smart DCA Invest – Features Overview

✅ Automated DCA strategy with dynamic profit targets, optimized risk management.

⚙️ Functionality:

🕒 Time Interval Settings

• 📅 Start Date and Time: The strategy activates only after the specified start time.

• 🔄 Auto Restart: Automatically restarts the strategy after a position is closed.

💵 Investment Amounts

• 🟢 Initial Investment Amount: The amount invested when the first position is opened.

• 🔄 Recurring Investment Amount: The amount invested periodically for subsequent purchases.

📊 Purchase Frequency

• ⏱ Interval Between Purchases: Specifies the minimum number of candles between two purchases to avoid overly frequent position expansions.

🛡️ Risk Management

• 📉 Loss Limit: The strategy halts additional purchases if the price does not drop below a predefined loss level, optimizing the average cost reduction.

• 🎯 Take Profit: A predefined profit target percentage, triggering position closure upon reaching it.

📈 Dynamic Take Profit (TP) Settings

• ⏳ TP Increase Frequency: The interval in days for dynamic TP growth.

• 📊 TP Growth Rate: The percentage by which the TP level increases at the end of each interval.

• ⚙️ Enable Dynamic TP: Allows the TP level to increase dynamically over time based on holding duration.

• 🧠 Smart Invest: Accumulates skipped purchases above the average entry or loss limit price and invests them when the price drops below the loss limit.

🎨 Visual Representation

• 📏 Average Price Line: Displays the average entry price in yellow.

• 🛑 Stop Limit Line: Displays the loss limit in red.

• ✅ Take Profit Line: Displays the dynamically updated profit target in green.

🎨 Visual Elements

• 📏 Average Price Line: Visualizes the average cost on the chart.

• 🛑 Stop Limit Line: Visualizes the loss limit level.

• ✅ Take Profit Line: Displays the TP level graphically.

• 📊 Statistics Table: Detailed data summary presented in a table at the end of the strategy.

📊 Statistics Table

• 📈 Average Price: The average entry price of the current position.

• 🛑 Stop Limit: The loss limit value.

• ✅ Take Profit: The profit target value.

• 📦 Position Size: The size of the current position.

• 💵 Max Invested Amount: The highest amount invested.

• ⏳ Longest DCA Period: The longest duration a DCA position was open.

• 💼 Current Investment: The amount currently invested.

• 🔄 Multiplier: Purchase multiplier value.

• 📊 Dynamically Adjusted TP %: The current dynamic Take Profit percentage.

- Recommended for retesting

Hungarian description:

📊 Smart DCA Invest – Funkciók Leírása

✅ Automatizált DCA stratégia dinamikus profitcélokkal, optimalizált kockázatkezeléssel.

⚙️ Működés:

🕒 Időintervallum Beállítások

• 📅 Kezdési dátum és idő: A stratégia csak a meghatározott kezdési időpont után aktiválódik.

• ⏳ Befejezési dátum és idő: A stratégia a meghatározott időpontig működik.

• 🔄 Automatikus újraindítás: Pozíciózárás után a stratégia automatikusan újraindulhat.

💵 Befektetési Összegek

• 🟢 Első befektetési összeg: Az első pozíció nyitásakor befektetett összeg.

• 🔄 Napi vásárlási összeg: Ismételt periódusonkénti vásárlások összege.

📊 Vásárlási Gyakoriság

• ⏱ Intervallum két vásárlás között: Meghatározza a minimális gyertya intervallumot két vásárlás között, elkerülve a túl gyakori pozícióbővítéseket.

🛡️ Kockázatkezelés

• 📉 Loss Limit: Ha az ár nem csökken egy meghatározott veszteségi szint alá, a stratégia nem vásárol tovább, hogy hatékonyabban csökkentse az átlagárat.

• 🎯 Take Profit: Előre meghatározott profitcél százalékos értéke, amely elérésekor a pozíció lezárul.

📈 Dinamikus Take Profit (TP) Beállítások

• ⏳ TP növelési gyakoriság: A dinamikus TP növekedésének időszaka napokban.

• 📊 TP növekedés mértéke: A TP szint százalékos növekedése az intervallum végén.

• ⚙️ Dinamikus TP engedélyezése: A TP szint dinamikusan növekszik a tartási idő függvényében.

• 🧠 Smart Invest: Kihagyott vásárlások felhalmozása (átlagos bekerülési vagy „Loss limit” feletti árfolyamnál), amelyek a „Loss limit” árszint alatt befektetésre kerülnek.

🎨 Vizuális Megjelenítés

• 📏 Átlagár vonal: Sárga színnel jelzi az átlagárat.

• 🛑 Stop Limit vonal: Piros színnel jelzi a veszteségi korlátot.

• ✅ Take Profit vonal: Zöld színnel jelzi a dinamikusan frissülő profitcélt.

🎨 Vizuális Elemek

• 📏 Átlagár vonal: Az átlagár megjelenítése a grafikonon.

• 🛑 Stop Limit vonal: A veszteségkorlátozási szint megjelenítése.

• ✅ Take Profit vonal: A Take Profit szint grafikai megjelenítése.

• 📊 Statisztikai táblázat megjelenítése: A stratégia végén részletes adatok jelennek meg egy táblázatban.

📊 Statisztikai Táblázat

• 📈 Átlagár: Az aktuális pozíció átlagos bekerülési ára.

• 🛑 Stop Limit: A veszteségkorlátozási szint értéke.

• ✅ Take Profit: A profitcél értéke.

• 📦 Pozícióméret: Az aktuális pozíció nagysága.

• 💵 Maximális befektetett összeg: A legnagyobb befektetett érték.

• ⏳ Leghosszabb DCA időszak: A leghosszabb időtartam, amíg egy DCA pozíció nyitva maradt.

• 💼 Aktuális befektetés: Az aktuálisan befektetett összeg.

• 🔄 Multiplikátor: Vásárlási szorzó érték.

• 📊 Dinamikusan beállított TP %: Az aktuálisan érvényes Take Profit százalékos értéke.

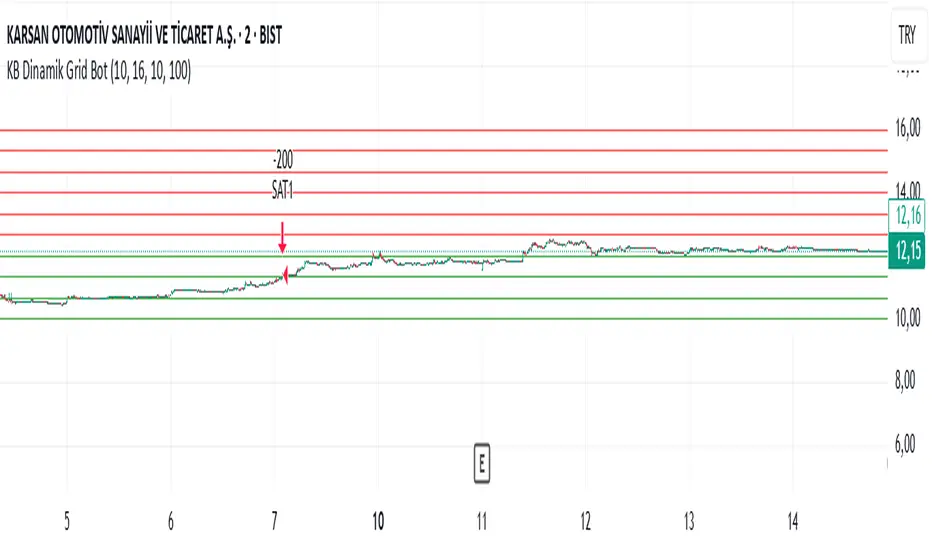

KB Dinamik Grid Bot V8 TrailingThis Pine Script code aims to create a "Dynamic Grid Trading Bot" and perform automatic trading between price ranges. Let's break it down into sections to better understand its functions:

1. Settings and User Inputs

The user can specify the following parameters for the bot:

Lower and Upper Price Limit: Determines the price range where the grid levels are defined.

Number of Grid Lines: Defines how many levels the grid will consist of.

Transaction Amount: Specifies the trading volume for each trading transaction.

Start Date: The date when the bot will start trading.

Price Step (priceStep): Specifies specific steps after the comma to adjust the grid levels more precisely.

Trailing: A feature that activates dynamic selling by following price movements.

2. Calculating Grid Levels

Grid levels: Divides the specified price range into user-defined levels and rounds each level with priceStep.

Lines and labels: Lines and labels are created to visually represent grid levels.

3. Buying and Selling Logic

Buying Transaction: When the price approaches a lower grid level (as much as the offset) and the position is empty, a purchase is made.

Trailing Selling: If Trailing is active, a sale is made when the price passes the specified "trailing step" level.

Normal Selling: If Trailing is not active, a sale is made when the price approaches an upper grid level.

4. Profit and Statistics Tracking

The bot tracks the profit-loss status per transaction and in total.

The number of purchases and sales and net profit information are calculated from the start date.

5. Table Display

The bot places statistical data in a table:

Number of purchases and sales.

Starting date.

Total number of transactions.

Net profit.

Amount of open positions.

6. Drawing and Tracking

Each price movement is updated and the color of the grid lines (green or red) is changed depending on the price's status relative to the level.

This code is a strategy that aims to make a profit by continuously buying and selling in the event of price fluctuations within a range. The "Trailing" feature allows you to keep your profits when the price moves upwards. Net profit, open positions and other statistics are displayed in the table.

Bullish Reversal Bar Strategy [Skyrexio]Overview

Bullish Reversal Bar Strategy leverages the combination of candlestick pattern Bullish Reversal Bar (description in Methodology and Justification of Methodology), Williams Alligator indicator and Williams Fractals to create the high probability setups. Candlestick pattern is used for the entering into trade, while the combination of Williams Alligator and Fractals is used for the trend approximation as close condition. Strategy uses only long trades.

Unique Features

No fixed stop-loss and take profit: Instead of fixed stop-loss level strategy utilizes technical condition obtained by Fractals and Alligator or the candlestick pattern invalidation to identify when current uptrend is likely to be over (more information in "Methodology" and "Justification of Methodology" paragraphs)

Configurable Trading Periods: Users can tailor the strategy to specific market windows, adapting to different market conditions.

Trend Trade Filter: strategy uses Alligator and Fractal combination as high probability trend filter.

Methodology

The strategy opens long trade when the following price met the conditions:

1.Current candle's high shall be below the Williams Alligator's lines (Jaw, Lips, Teeth)(all details in "Justification of Methodology" paragraph)

2.Price shall create the candlestick pattern "Bullish Reversal Bar". Optionally if MFI and AO filters are enabled current candle shall have the decreasing AO and at least one of three recent bars shall have the squat state on the MFI (all details in "Justification of Methodology" paragraph)

3.If price breaks through the high of the candle marked as the "Bullish Reversal Bar" the long trade is open at the price one tick above the candle's high

4.Initial stop loss is placed at the Bullish Reversal Bar's candle's low

5.If price hit the Bullish Reversal Bar's low before hitting the entry price potential trade is cancelled

6.If trade is active and initial stop loss has not been hit, trade is closed when the combination of Alligator and Williams Fractals shall consider current trend change from upward to downward.

Strategy settings

In the inputs window user can setup strategy setting:

Enable MFI (if true trades are filtered using Market Facilitation Index (MFI) condition all details in "Justification of Methodology" paragraph), by default = false)

Enable AO (if true trades are filtered using Awesome Oscillator (AO) condition all details in "Justification of Methodology" paragraph), by default = false)

Justification of Methodology

Let's explore the key concepts of this strategy and understand how they work together. The first and key concept is the Bullish Reversal Bar candlestick pattern. This is just the single bar pattern. The rules are simple:

Candle shall be closed in it's upper half

High of this candle shall be below all three Alligator's lines (Jaw, Lips, Teeth)

Next, let’s discuss the short-term trend filter, which combines the Williams Alligator and Williams Fractals. Williams Alligator

Developed by Bill Williams, the Alligator is a technical indicator that identifies trends and potential market reversals. It consists of three smoothed moving averages:

Jaw (Blue Line): The slowest of the three, based on a 13-period smoothed moving average shifted 8 bars ahead.

Teeth (Red Line): The medium-speed line, derived from an 8-period smoothed moving average shifted 5 bars forward.

Lips (Green Line): The fastest line, calculated using a 5-period smoothed moving average shifted 3 bars forward.

When the lines diverge and align in order, the "Alligator" is "awake," signaling a strong trend. When the lines overlap or intertwine, the "Alligator" is "asleep," indicating a range-bound or sideways market. This indicator helps traders determine when to enter or avoid trades.

Fractals, another tool by Bill Williams, help identify potential reversal points on a price chart. A fractal forms over at least five consecutive bars, with the middle bar showing either:

Up Fractal: Occurs when the middle bar has a higher high than the two preceding and two following bars, suggesting a potential downward reversal.

Down Fractal: Happens when the middle bar shows a lower low than the surrounding two bars, hinting at a possible upward reversal.

Traders often use fractals alongside other indicators to confirm trends or reversals, enhancing decision-making accuracy.

How do these tools work together in this strategy? Let’s consider an example of an uptrend.

When the price breaks above an up fractal, it signals a potential bullish trend. This occurs because the up fractal represents a shift in market behavior, where a temporary high was formed due to selling pressure. If the price revisits this level and breaks through, it suggests the market sentiment has turned bullish.

The breakout must occur above the Alligator’s teeth line to confirm the trend. A breakout below the teeth is considered invalid, and the downtrend might still persist. Conversely, in a downtrend, the same logic applies with down fractals.

How we can use all these indicators in this strategy? This strategy is a counter trend one. Candle's high shall be below all Alligator's lines. During this market stage the bullish reversal bar candlestick pattern shall be printed. This bar during the downtrend is a high probability setup for the potential reversal to the upside: bulls were able to close the price in the upper half of a candle. The breaking of its high is a high probability signal that trend change is confirmed and script opens long trade. If market continues going down and break down the bullish reversal bar's low potential trend change has been invalidated and strategy close long trade.

If market really reversed and started moving to the upside strategy waits for the trend change form the downtrend to the uptrend according to approximation of Alligator and Fractals combination. If this change happens strategy close the trade. This approach helps to stay in the long trade while the uptrend continuation is likely and close it if there is a high probability of the uptrend finish.

Optionally users can enable MFI and AO filters. First of all, let's briefly explain what are these two indicators. The Awesome Oscillator (AO), created by Bill Williams, is a momentum-based indicator that evaluates market momentum by comparing recent price activity to a broader historical context. It assists traders in identifying potential trend reversals and gauging trend strength.

AO = SMA5(Median Price) − SMA34(Median Price)

where:

Median Price = (High + Low) / 2

SMA5 = 5-period Simple Moving Average of the Median Price

SMA 34 = 34-period Simple Moving Average of the Median Price

This indicator is filtering signals in the following way: if current AO bar is decreasing this candle can be interpreted as a bullish reversal bar. This logic is applicable because initially this strategy is a trend reversal, it is searching for the high probability setup against the current trend. Decreasing AO is the additional high probability filter of a downtrend.

Let's briefly look what is MFI. The Market Facilitation Index (MFI) is a technical indicator that measures the price movement per unit of volume, helping traders gauge the efficiency of price movement in relation to trading volume. Here's how you can calculate it:

MFI = (High−Low)/Volume

MFI can be used in combination with volume, so we can divide 4 states. Bill Williams introduced these to help traders interpret the interaction between volume and price movement. Here’s a quick summary:

Green Window (Increased MFI & Increased Volume): Indicates strong momentum with both price and volume increasing. Often a sign of trend continuation, as both buying and selling interest are rising.

Fake Window (Increased MFI & Decreased Volume): Shows that price is moving but with lower volume, suggesting weak support for the trend. This can signal a potential end of the current trend.

Squat Window (Decreased MFI & Increased Volume): Shows high volume but little price movement, indicating a tug-of-war between buyers and sellers. This often precedes a breakout as the pressure builds.

Fade Window (Decreased MFI & Decreased Volume): Indicates a lack of interest from both buyers and sellers, leading to lower momentum. This typically happens in range-bound markets and may signal consolidation before a new move.

For our purposes we are interested in squat bars. This is the sign that volume cannot move the price easily. This type of bar increases the probability of trend reversal. In this indicator we added to enable the MFI filter of reversal bars. If potential reversal bar or two preceding bars have squat state this bar can be interpret as a reversal one.

Backtest Results

Operating window: Date range of backtests is 2023.01.01 - 2024.12.31. It is chosen to let the strategy to close all opened positions.

Commission and Slippage: Includes a standard Binance commission of 0.1% and accounts for possible slippage over 5 ticks.

Initial capital: 10000 USDT

Percent of capital used in every trade: 50%

Maximum Single Position Loss: -5.29%

Maximum Single Profit: +29.99%

Net Profit: +5472.66 USDT (+54.73%)

Total Trades: 103 (33.98% win rate)

Profit Factor: 1.634

Maximum Accumulated Loss: 1231.15 USDT (-8.32%)

Average Profit per Trade: 53.13 USDT (+0.94%)

Average Trade Duration: 76 hours

How to Use

Add the script to favorites for easy access.

Apply to the desired timeframe and chart (optimal performance observed on 4h ETH/USDT).

Configure settings using the dropdown choice list in the built-in menu.

Set up alerts to automate strategy positions through web hook with the text: {{strategy.order.alert_message}}

Disclaimer:

Educational and informational tool reflecting Skyrex commitment to informed trading. Past performance does not guarantee future results. Test strategies in a simulated environment before live implementation

These results are obtained with realistic parameters representing trading conditions observed at major exchanges such as Binance and with realistic trading portfolio usage parameters.

Omega_galskyThe strategy uses three Exponential Moving Averages (EMAs) — EMA8, EMA21, and EMA89 — to decide when to open buy or sell trades. It also includes a mechanism to move the Stop Loss (SL) to the Break-Even (BE) point, which is the entry price, once the price reaches a Risk-to-Reward (R2R) ratio of 1:1.

Key Steps:

Calculating EMAs: The script computes the EMA values for the specified periods. These help identify market trends and potential entry points.

Buy Conditions:

EMA8 crosses above EMA21.

The candle that causes the crossover is green (closing price is higher than the opening price).

The closing price is above EMA89.

If all conditions are met, a buy order is executed.

Sell Conditions:

EMA8 crosses below EMA21.

The candle that causes the crossover is red (closing price is lower than the opening price).

The closing price is below EMA89.

If all conditions are met, a sell order is executed.

Stop Loss and Take Profit:

Initial Stop Loss and Take Profit levels are calculated based on the entry price and a percentage defined by the user.

These levels help protect against large losses and lock in profits.

Break-Even Logic:

When the price moves favorably to reach a 1:1 R2R ratio:

For a buy trade, the Stop Loss is moved to the entry price if the price increases sufficiently.

For a sell trade, the Stop Loss is moved to the entry price if the price decreases sufficiently.

This ensures the trade is risk-free after the price reaches the predefined level.

Visual Representation:

The EMAs are plotted on the chart for easy visualization of trends and crossovers.

Entry and exit points are also marked on the chart to track trades.

Purpose:

The strategy is designed to capitalize on EMA crossovers while minimizing risks using Break-Even logic and predefined Stop Loss/Take Profit levels. It automates decision-making for trend-following traders and ensures disciplined risk management.

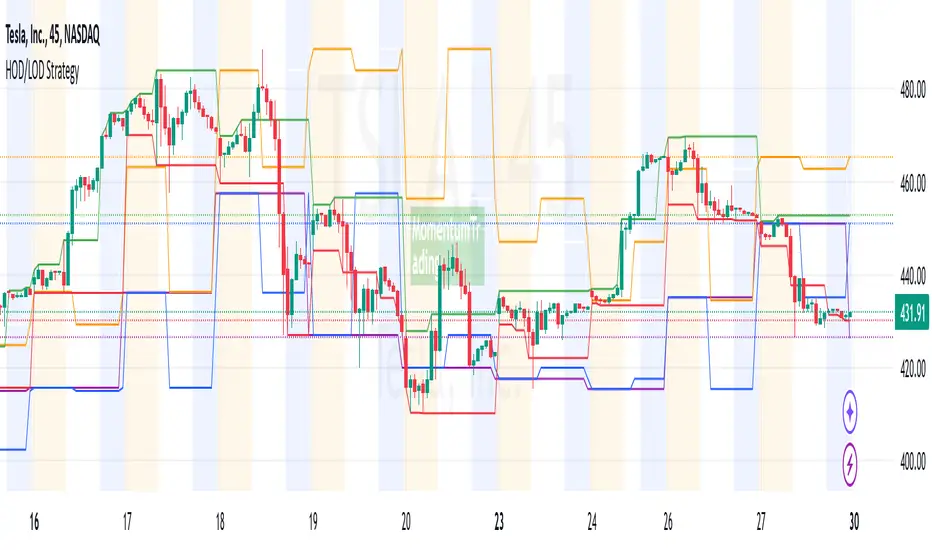

HOD/LOD/PMH/PML/PDH/PDL Strategy by @tradingbauhaus This script is a trading strategy @tradingbauhaus designed to trade based on key price levels, such as the High of Day (HOD), Low of Day (LOD), Premarket High (PMH), Premarket Low (PML), Previous Day High (PDH), and Previous Day Low (PDL). Below, I’ll explain in detail what the script does:

Core Functionality of the Script:

Calculates Key Price Levels:

HOD (High of Day): The highest price of the current day.

LOD (Low of Day): The lowest price of the current day.

PMH (Premarket High): The highest price during the premarket session (before the market opens).

PML (Premarket Low): The lowest price during the premarket session.

PDH (Previous Day High): The highest price of the previous day.

PDL (Previous Day Low): The lowest price of the previous day.

Draws Horizontal Lines on the Chart:

Plots horizontal lines on the chart for each key level (HOD, LOD, PMH, PML, PDH, PDL) with specific colors for easy visual identification.

Defines Entry and Exit Rules:

Long Entry (Buy): If the price crosses above the PMH (Premarket High) or the PDH (Previous Day High).

Short Entry (Sell): If the price crosses below the PML (Premarket Low) or the PDL (Previous Day Low).

Long Exit: If the price reaches the HOD (High of Day) during a long position.

Short Exit: If the price reaches the LOD (Low of Day) during a short position.

How the Script Works Step by Step:

Calculates Key Levels:

Uses the request.security function to fetch the HOD and LOD of the current day, as well as the highs and lows of the previous day (PDH and PDL).

Calculates the PMH and PML during the premarket session (before 9:30 AM).

Plots Levels on the Chart:

Uses the plot function to draw horizontal lines on the chart representing the key levels (HOD, LOD, PMH, PML, PDH, PDL).

Each level has a specific color for easy identification:

HOD: White.

LOD: Purple.

PDH: Orange.

PDL: Blue.

PMH: Green.

PML: Red.

Defines Trading Rules:

Uses conditions with ta.crossover and ta.crossunder to detect when the price crosses key levels.

Long Entry: If the price crosses above the PMH or PDH, a long position (buy) is opened.

Short Entry: If the price crosses below the PML or PDL, a short position (sell) is opened.

Long Exit: If the price reaches the HOD during a long position, the position is closed.

Short Exit: If the price reaches the LOD during a short position, the position is closed.

Executes Orders Automatically:

Uses the strategy.entry and strategy.close functions to open and close positions automatically based on the defined rules.

Advantages of This Strategy:

Based on Key Levels: Uses important price levels that often act as support and resistance.

Easy to Visualize: Horizontal lines on the chart make it easy to identify levels.

Automated: Entries and exits are executed automatically based on the defined rules.

Limitations of This Strategy:

Dependent on Volatility: Works best in markets with significant price movements.

False Crosses: There may be false crosses that generate incorrect signals.

No Advanced Risk Management: Does not include dynamic stop-loss or take-profit mechanisms.

How to Improve the Strategy:

Add Stop-Loss and Take-Profit: To limit losses and lock in profits.

Filter Signals with Indicators: Use RSI, MACD, or other indicators to confirm signals.

Optimize Levels: Adjust key levels based on the asset’s behavior.

In summary, this script is a trading strategy that operates based on key price levels, such as HOD, LOD, PMH, PML, PDH, and PDL. It is useful for traders who want to trade based on significant support and resistance levels.

ROBO STB GainCraft strategyPure Price Action Candlestick Strategy by ROBO STB

Overview

This strategy is built entirely on the principles of price action and candlestick analysis, designed for traders who prefer raw market data over traditional indicators. By focusing solely on candlestick patterns and their context within recent price movements, the strategy identifies high-probability entry and exit points in liquid markets.

Entry signals are generated based on these patterns appearing at significant market locations, such as after consolidations, pullbacks, or at key support/resistance levels.

Price Action Integration:

Instead of relying on oscillators or moving averages, the script leverages the inherent market structure provided by candlesticks to interpret potential trend reversals or continuations.

This approach provides a clearer view of market sentiment.

No External Indicators:

This script avoids the use of traditional indicators like RSI, MACD, or Bollinger Bands, offering a clean, uncluttered chart.

Risk Management (Optional):

Fixed-percentage risk management options can also be enabled, ensuring trades remain within acceptable risk parameters.

How the Strategy Works

Entry Conditions: