RunRox - Backtesting System (ASMC)Introducing RunRox - Backtesting System (ASMC), a specially designed backtesting system built on the robust structure of our Advanced SMC indicator. This innovative tool evaluates various Smart Money Concept (SMC) trading setups and serves as an automatic optimizer, displaying which entry and exit points have historically shown the best results. With cutting-edge technology, RunRox - Backtesting System (ASMC) provides you with effective strategies, maximizing your trading potential and taking your trading to the next level

🟠 HOW OUR BACKTESTING SYSTEM WORKS

Our backtesting system for the Advanced SMC (ASMC) indicator is meticulously designed to provide traders with a thorough analysis of their Smart Money Concept (SMC) strategies. Here’s an overview of how it works:

🔸 Advanced SMC Structure

Our ASMC indicator is built upon an enhanced SMC structure that integrates the Institutional Distribution Model (IDM), precise retracements, and five types of order blocks (CHoCH OB, IDM OB, Local OB, BOS OB, Extreme OB). These components allow for a detailed understanding of market dynamics and the identification of key trading opportunities.

🔸 Data Integration and Analysis

1. Historical Data Testing:

Our system tests various entry and exit points using historical market data.

The ASMC indicator is used to simulate trades based on predefined SMC setups, evaluating their effectiveness over a specified time period.

Traders can select different parameters such as entry points, stop-loss, and take-profit levels to see how these setups would have performed historically.

2. Entry and Exit Events:

The backtester can simulate trades based on 12 different entry events, 14 target events, and 14 stop-loss events, providing a comprehensive testing framework.

It allows for testing with multiple combinations of entry and exit strategies, ensuring a robust evaluation of trading setups.

3. Order Block Sensitivity:

The system uses the sensitivity settings from the ASMC indicator to determine the most relevant order blocks and fair value gaps (FVGs) for entry and exit points.

It distinguishes between different types of order blocks, helping traders identify strong institutional zones versus local zones.

🔸 Optimization Capabilities

1. Auto-Optimizer:

The backtester includes an auto-optimizer feature that evaluates various setups to find those with the best historical performance.

It automatically adjusts parameters to identify the most effective strategies for both trend-following and counter-trend trading.

2. Stop Loss and Take Profit Optimization:

It optimizes stop-loss and take-profit levels by testing different settings and identifying those that provided the best historical results.

This helps traders refine their risk management and maximize potential returns.

3. Trailing Stop Optimization:

The system also optimizes trailing stops, ensuring that traders can maximize their profits by adjusting their stops dynamically as the market moves.

🔸 Comprehensive Reporting

1. Performance Metrics:

The backtesting system provides detailed reports, including key performance metrics such as Net Profit, Win Rate, Profit Factor, and Max Drawdown.

These metrics help traders understand the historical performance of their strategies and make data-driven decisions.

2. Flexible Settings:

Traders can adjust initial balance, commission rates, and risk per trade settings to simulate real-world trading conditions.

The system supports testing with different leverage settings, allowing for realistic assessments even with tight stop-loss levels.

🔸 Conclusion

The RunRox Backtesting System (ASMC) is a powerful tool for traders seeking to validate and optimize their SMC strategies. By leveraging historical data and sophisticated optimization algorithms, it provides insights into the most effective setups, enhancing trading performance and decision-making.

🟠 HERE ARE THE AVAILABLE FEATURES

Historical backtesting for any setup – Select any entry point, exit point, and various stop-loss options to see the results of your setup on historical data.

Auto-optimizer for finding the best setups – The indicator displays settings that have shown the best results historically, providing valuable insights.

Auto-optimizer for counter-trend setups – Discover entry and exit points for counter-trend trading based on historical performance.

Auto-optimizer for stop-loss – The indicator shows stop-loss points that have been most effective historically.

Auto-optimizer for take-profit – The indicator identifies take-profit points that have performed well in historical trading data.

Auto-optimizer for trailing stop – The indicator presents trailing stop settings that have shown the best historical results.

And much more within our indicator, all of which we will cover in this post. Next, we will showcase the possible entry points, targets, and stop-loss options available for testing your strategies

🟠 ENTRY SETTINGS

12 Event Triggers for Trade Entry

Extr. ChoCh OB

Extr. ChoCh FVG

ChoCh

ChoCh OB

ChoCh FVG

IDM OB

IDM FVG

BoS FVG

BoS OB

BoS

Extr. BoS FVG

Extr. BoS OB

3 Trade Direction Options

Long Only: Enter long positions only

Short Only: Enter short positions only

Long and Short: Enter both long and short positions based on trend

3 Levels for Order Block/FVG Entries

Beginning: Enter the trade at the first touch of the Order Block/FVG

Middle: Enter the trade when the middle of the Order Block/FVG is reached

End: Enter the trade upon full filling of the Order Block/FVG

*Three levels work only for Order Blocks and FVG. For trade entries based on BOS or CHoCH, these settings do not apply as these parameters are not available for these types of entries

You can choose any combination of trade entries imaginable.

🟠 TARGET SETTINGS

14 Target Events, Including Fixed % and Fixed RR (Risk/Reward):

Fixed - % change in price

Fixed RR - Risk Reward per trade

Extr. ChoCh OB

Extr. ChoCh FVG

ChoCh

ChoCh OB

ChoCh FVG

IDM OB

IDM FVG

BoS FVG

BoS OB

BoS

Extr. BoS FVG

Extr. BoS OB

3 Levels of Order Block/FVG for Target

Beginning: Close the trade at the first touch of your target.

Middle: Close the trade at the midpoint of your chosen target.

End: Close the trade when your target is fully filled.

Customizable Parameters

Easily set your Fixed % and Fixed RR targets with a user-friendly input field. This field works only for the Fixed and Fixed RR entry parameters. When selecting a different entry point, this field is ignored

Choose any combination of target events to suit your trading strategy.

🟠 STOPLOSS SETTINGS

14 Possible StopLoss Events Including Entry Orderblock/FVG

Fixed - Fix the loss on the trade when the price moves by N%

Entry Block

Extr. ChoCh OB

Extr. ChoCh FVG

ChoCh

ChoCh OB

ChoCh FVG

IDM OB

IDM FVG

BoS FVG

BoS OB

BoS

Extr. BoS FVG

Extr. BoS OB

3 Levels for Order Blocks/FVG Exits

Beginning: Exit the trade at the first touch of the order block/FVG.

Middle: Exit the trade at the middle of the order block/FVG.

End: Exit the trade at the full completion of the order block/FVG.

Dedicated Field for Setting Fixed % Value

Set a fixed % value in a dedicated field for the Fixed parameter. This field works only for the Fixed parameter. When selecting other exit parameters, this field is ignored.

🟠 ADDITIONAL SETTINGS

Trailing Stop, %

Set a Trailing Stop as a percentage of your trade to potentially increase profit based on historical data.

Move SL to Breakeven, bars

Move your StopLoss to breakeven after exiting the entry zone for a specified number of bars. This can enhance your potential WinRate based on historical performance.

Skip trade if RR less than

This feature allows you to skip trades where the potential Risk-to-Reward ratio is less than the number set in this field.

🟠 EXAMPLE OF MANUAL SETUP

For example, let me show you how it works on the chart. You select entry parameters, stop loss parameters, and take profit parameters for your trades, and the strategy automatically tests this setup on historical data, allowing you to see the results of this strategy.

In the screenshot above, the parameters were as follows:

Trade Entry: CHoCH OB (Beginning)

Stop Loss: Entry Block

Take Profit: Break of BOS

The indicator will automatically test all possible trades on the chart and display the results for this setup.

🟠 AUTO OPTIMIZATION SETTINGS

In the screenshot above, you can see the optimization table displaying various entry points, exits, and stop-loss settings, along with their historical performance results and other parameters. This feature allows you to identify trading setups that have shown the best historical outcomes.

This functionality will enhance your trading approach, providing you with valuable insights based on historical data. You’ll be aware of the Smart Money Concept settings that have historically worked best for any specific chart and timeframe.

Our indicator includes various optimization options designed to help you find the most effective settings based on historical data. There are 5 optimization modes, each offering unique benefits for every trader

Trend Entry - Optimization of the best settings for trend-following trades. The strategy will enter trades only in the direction of the trend. If the trend is upward, it will look for long entry points and vice versa.

Counter Trend Entry - Finding setups against the trend. If the trend is upward, the script will search for short entry points. This is the opposite of trend entry optimization.

Stop Loss - Identifying stop-loss points that showed the best historical performance for the specific setup you have configured. This helps in finding effective exit points to minimize losses.

Take Profit - Determining targets for the configured setup based on historical performance, helping to identify potentially profitable take profit levels.

Trailing Stop - Finding optimal percentages for the trailing stop function based on historical data, which can potentially increase the profit of your trades.

Ability to set parameters for auto-optimization within a specified range. For example, if you choose FixRR TP from 1 to 10, the indicator will automatically test all possible Risk Reward Take Profit variations from 1 to 10 and display the results for each parameter individually.

Ability to set initial deposit parameters, position commissions, and risk per trade as a fixed percentage or fixed amount. Additionally, you can set the maximum leverage for a trade.

There are times when the stop loss is very close to the entry point, and adhering to the risk per trade values set in the settings may not allow for such a loss in any situation. That’s why we added the ability to set the maximum possible leverage, allowing you to test your trading strategy even with very tight stop losses.

Duplicated Smart Money Structure settings from our Advanced SMC indicator that you can adjust to match your trading style flexibly. All these settings will be taken into account during the optimization process or when manually calculating settings.

Additionally, you can test your strategy based on higher timeframe order blocks. For example, you can test a strategy on a 1-minute chart while displaying order blocks from a 15-minute timeframe. The auto-optimizer will consider all these parameters, including higher timeframe order blocks, and will enter trades based on these order blocks.

Highly flexible dashboard and results optimization settings allow you to display the tables you need and sort results by six different criteria: Profit Factor, Profit, Winrate, Max Drawdown, Wins, and Trades. This enables you to find the exact setup you desire, based on these comprehensive data points.

🟠 ALERT CUSTOMIZATION

With this indicator, you can set up buy and sell alerts based on the test results, allowing you to create a comprehensive trading strategy. This feature enables you to receive real-time signals, making it a powerful tool for implementing your trading strategies.

🟠 STRATEGY PROPERTIES

For backtesting, we used realistic initial data for entering trades, such as:

Starting balance: $1000

Commission: 0.01%

Risk per trade: 1%

To ensure realistic data, we used the above settings. We offer two methods for calculating your order size, and in our case, we used a 1% risk per trade. Here’s what it means:

Risk per trade: This is the maximum loss from your deposit if the trade goes against you. The trade volume can change depending on your stop-loss distance from the entry point. Here’s the formula we use to calculate the possible volume for a single trade:

1. quantity = percentage_risk * balance / loss_per_1_contract (incl. fee)

Then, we calculate the maximum allowed volume based on the specified maximum leverage:

2. max_quantity = maxLeverage * balance / entry_price

3. If quantity < max_quantity, meaning the leverage is less than the maximum allowed, we keep quantity. If quantity > max_quantity, we use max_quantity (the maximum allowed volume according to the set leverage).

This way, depending on the stop-loss distance, the position size can vary and be up to 100% of your deposit, but the loss in each trade will not exceed the set percentage, which in our case is 1% for this backtest. This is a standard risk calculation method based on your stop-loss distance.

🔸 Statistical Significance of Trade Data

In our strategy, you may notice there weren’t enough trades to form statistically significant data. This is inherent to the Smart Money Concept (SMC) strategy, where the focus is not on the number of trades but rather on the risk-to-reward ratio per trade. In SMC strategies, it’s crucial to avoid taking numerous uncertain setups and instead perform a comprehensive analysis of the market situation.

Therefore, our strategy results show fewer than 100 trades. It’s important to understand that this small sample size isn’t statistically significant and shouldn’t be relied upon for strategy analysis. Backtesting with a small number of trades should not be used to draw conclusions about the effectiveness of a strategy.

🔸 Versatile Use Cases

The methods of using this indicator are numerous, ranging from identifying potentially the best-performing order blocks on the chart to creating a comprehensive trading strategy based on the data provided by our indicator. We believe that every trader will find a valuable application for this tool, enhancing their entry and exit points in trades.

Disclaimer

Past performance is not indicative of future results. The results shown by this indicator do not guarantee similar outcomes in the future. Use this tool as part of a comprehensive trading strategy, considering all market conditions and risks.

How to access

For access to this indicator, please read the author’s instructions below this post

"profit" için komut dosyalarını ara

Strategy - Plus / Connectable [Azullian]Discover the advanced capabilities of Strategy Plus, an essential component of the connectable indicator system designed for fast-paced strategy testing, visualization, and building within TradingView. This enhanced version of our foundational connectable strategy indicator seamlessly integrates with all connectable indicators . By utilizing the TradingView input source as a signal connector , it facilitates the linking of indicators to form a cohesive strategy. Each connectable indicator within the system sends signal weight to the next node, culminating in a comprehensive strategy that incorporates advanced customization options, sophisticated signal interpretation, and elaborate backtest labeling. Strategy Plus stands out by offering improved position management and extensive alert messaging capabilities, ensuring effective strategy refinement and backend integration.

█ DISTINCTIVE FEATURES

The Connectable Strategy Plus enhances risk mitigation within the connectable system through its advanced features and capabilities:

• Refined Signal Input Management: Tailor and precisely connect up to two signal filters with enhanced input flexibility, gain control, and strategic direction settings.

• Strategic Position Investment Control: Optimize positioning with versatile investment bases, custom investment percentages, and direction-specific investments for effective risk management.

• Advanced Exit Stop Loss Configuration: Implement custom stop loss tactics with diverse base modes and trailing options for tailored risk management.

• Strategic Exit Take Profit Settings: Apply precision-driven take profit strategies with various calculation modes and dynamic trailing functionality.

• Calibrated Entry Position Allocation: Optimize investment distribution for entry positions, including DCA and BRO trades, for strategic market response.

• Refined Order Setting Customization: Ensure exchange compliance with adjustable order settings, enhancing backtest accuracy and strategy reliability.

• Comprehensive Condition Settings: Define precise conditions for strategy execution, including date range filtering and order/loss limitations.

• Intuitive Visualization: Enhance strategy clarity with customizable visual elements and trade visualization features.

• Advanced Alert Configurations: Stay informed with comprehensive and customizable alerts for effective backend integration.

• Backend Integration With JSON Format: Leverage elaborate and structured data in JSON format for advanced analytics, enhancing decision-making and strategy optimization outside TradingView.

Let's review the separate parts of this indicator.

█ STRATEGY INPUTS

We've provided 2 inputs for connecting a signal filter or indicators or chains (1→, 2→) which are all set to 'Close' by default.

An input has several controls:

• Enable disable: Toggle the entire input on or off

• Input: Connect indicators or signal filter here, choose indicators with a compatible : Signal connector.

• G - Gain: Increase or reduce the strength of the incoming signal by a factor.

• SM - Signal Mode: Choose a trading direction compatible with the settings in your signal filter

• XM - Exit Mode: Determine when to allow to exit your open trade

○ Always: Doesn't take the restrictions into account, this ignores all the settings chosen in ML or MP

○ Restricted: Use both ML and MP conditions

○ Loss: Use the ML condition only, for example: Position will be exited and the exit signal will be allowed only when the loss exceeds the ML parameter

○ Profit: Use the MP condition only for example: Exits will only be allowed when the profit of the position exceeds the condition of the MP parameter

█ POSITION INVESTMENT

Determine the percentage of your trading budget you would like to use in each position based on the strategy's profit or loss.

• LINVB - Loss Investment Base: Choose which base to use to determine the investment percentage when the strategy is in a loss.

○ Equity: Use the equity as the base for percentage calculation.

○ Initial capital: Use the initial capital as the base for percentage calculation.

• LINV% - Loss Investment Percentage: Set a percentage of the chosen investment base as the investment for a new position.

○ For example, when 10% in loss, and a initial capital of $100, and the investment base is set to equity with a percentage of 50%, your investment will be 50% of $90, $45.

• PINVB - Profit Investment Base: Choose which base to use to determine the investment percentage when the strategy is in profit.

○ Equity: Use the equity as the base for percentage calculation.

○ Initial capital: Use the initial capital as the base for percentage calculation.

• PINV% - Profit Investment Percentage: Set a percentage of the chosen investment base as the investment for a new position.

○ For example, when 10% in profit, and an initial capital of $100, and the investment base is set to equity with a percentage of 100%, your investment will be 100% of $110, $110.

• XINVB - Custom Profit Investment Base: Choose which base to use to determine the investment percentage when the strategy is above a custom profit threshold (XT).

○ Equity: Use the equity as the base for percentage calculation.

○ Initial capital: Use the initial capital as the base for percentage calculation.

• XINV% - Custom Profit Investment Percentage: Set a percentage of the chosen investment base as the investment for a new position.

○ For example, when 100% in profit, exceeding the XT threshold of 50%, and an initial capital of $100, and the investment base is set to equity with a percentage of 50%, your investment will be 50% of $200, $100.

• XT% - Custom Profit Threshold: Determine how much profit triggers these custom profit investment settings.

• ELIB% - Entry Long Investment Base: Following previous settings, you can further restrict the investment according to the long trading direction.

○ For instance, if the previous calculation resulted in $45 to be used as an investment, and you've set the ELIB% to 50%, your long position will use 50% of $45, which is $22.5.

• ESIB% - Entry Short Investment Base: Following previous settings, you can further restrict the investment according to the short trading direction.

○ For example, if the previous calculation resulted in $45 to be used as an investment, and you've set the ESIB% to 50%, your short position will use 50% of $45, which is $22.5.

• RISK% - Risk Percentage:

○ Determine how much of the calculated position investment is at risk when the stop-loss is hit.

- For example, 1% of $45 represents a maximum loss of $0.45.

○ Risk percentage works together with the stop loss and the max leverage.

• MXLVG - Maximum Leverage:

○ Investigate the trading rules for your trading pair and use the maximum allowed amount of leverage.

○ To determine the number of contracts to be bought or sold, considering the stop loss and the specified risk percentage, the maximum leverage available will constrain the amount of leverage utilized to ensure that the maximum risk threshold is not exceeded. For instance, suppose the stop loss is set at 1%, and the risk percentage is defined as 10%. Initially, the calculated leverage to be used would be 10. However, if there is a maximum leverage cap set at 5, it would constrain the calculated leverage of 10 to adhere to the maximum limit of 5.

█ EXIT STOP LOSS

Determine the Stop Loss price based on your selected configuration.

As the stop loss is an integral part of the ordered contracts calculation used in conjunction with the Risk and Max leverage, you'll always need to provide a stop loss price.

• SLLB - Stop Loss Long Base: Choose a stop loss mode for calculating stop loss prices in long positions.

○ Risk: Determines the price using the Risk parameter (RISK%) and maximum leverage (MXLVG). In this case, SLLB% will not have any impact.

○ Price Entry + Offset: Calculates the stop loss price based on a offset percentage (SLLB%) from the entry price of the position.

○ Source: Computes the stop loss price based on an external indicator defined in SLLSRC.

- If this results in an invalid price, the calculation will revert to using the price entry + offset.

○ Source + Offset: Determines the stop loss price based on a positive or negative offset percentage (SLLB%) from an external indicator defined in SLLSRC.

- If this results in an invalid price, the calculation will fall back to using the price entry + offset.

• SLLB% - Stop Loss Long Base Percentage: Define an offset percentage that will be applied in the price entry + offset and source + offset stop loss modes.

• SLLSRC - Stop Loss Long Source: Connect an external indicator as the source for stop loss (only those providing price values eg: bollinger bands, moving averages...).

• SLLT - Stop Loss Long Trailing:

○ Fixed: The initial stop loss will be kept and no trailing stop loss will be applied.

○ Trail Stop: Takes into account all settings defined in SLLB and SLLB% and recalculates them with each candle.

- If a better stop loss is computed, it replaces the existing stop loss. In this mode SLLT% will be disregarded.

○ Trail Stop till BE: Similar to trailing stop mode, but it stops trailing when the stop loss reaches the break-even point.

○ Trail Stop from BE: Similar to trailing stop mode, but it starts trailing when the stop loss reaches the break-even point.

○ Trail Price: Computes the trailing stop loss price based on an offset percentage (SLLT%) from the closing price of the current candle.

- If a better stop loss price is calculated, it will be set as the new stop loss price.

○ Trail Price till BE: Similar to the Trail Price mode, but it stops trailing when the stop loss reaches the break-even point.

○ Trail Price from BE: Similar to Trail Price mode, but it starts trailing when the stop loss reaches the break-even point.

○ Trail Incr: Adapts the trailing stop loss price based on the offset percentage (SLLT%).

- Each price change in favor of your position will incrementally adapt the trailing stop loss with SLLT%.

○ Trail Incr till BE: Similar to the Trail Incr mode, but it stops trailing when the stop loss reaches the break-even point.

• SLLT% - Stop Loss Long Trailing Percentage: This percentage serves as an offset or increment depending on your chosen trailing mode.

• SLSB - Stop Loss Short Base: Functions similarly to SLLB but for short positions.

• SLSB% - Stop Loss Short Base Percentage: Functions similarly to SLLB% but for short positions.

• SLSSRC - Stop Loss Short Source: Functions similarly to SLLSRC but for short positions.

• SLST - Stop Loss Short Trailing: Functions similarly to SLLT but for short positions.

• SLST% - Stop Loss Short Trailing Percentage: Functions similarly to SLLT% but for short positions.

█ EXIT TAKE PROFIT

Determine the Take Profit price based on your selected configuration.

• TPLB - Take Profit Long Base: Choose a take profit mode for calculating take profit prices in long positions.

○ Reward: Determines the take profit price using the Risk parameter (RISK%) and the calculated Stop Loss price and the set reward percentage (TPLB%).

- For example: Risk 1%, Calculated Stop loss price: $90, Entry price: $100, Reward (TPLB%): 2%, will result in a take profit price on $120.

○ Price Entry + Offset: Calculates the take profit price based on a offset percentage (TPLB%) from the entry price of the position.

- For example: Entry price: $100, Offset (TPLB%): 2%, will result in a take profit price on $102.

○ Source: Computes the take profit price based on an external input from another indicator defined in TPLSRC.

- If this results in an invalid price, the calculation will revert to using the price entry + offset.

○ Source + Offset: Determines the take profit price based on a positive or negative offset percentage (TPLB%) from an external indicator inpuy defined in TPLSRC.

- If this results in an invalid price, the calculation will fall back to using the price entry + offset.

• TPLB% - Take Profit Long Base Percentage: Define an offset percentage that will be applied in the price entry + offset and source + offset take profit modes.

• TPLSRC - Take Profit Long Source: Choose to connect an external indicator as the source for take profit (of course only those which provide price values eg: bollinger bands, moving averages... but not oscillators).

• TPLT - Take Profit Long Trailing:

○ Fixed: The initial take profit will be kept and no trailing take profit will be applied.

○ Trail Profit: Takes into account all settings defined in TPLB and TPLB% and recalculates them with each candle.

- If an applicable take profit is computed, it replaces the existing take profit. In this mode TPLT% will be disregarded.

○ Trail Profit till BE: Similar to trailing profit mode, but it stops trailing when the take profit reaches the break-even point.

○ Trail Profit from BE: Similar to trailing profit mode, but it starts trailing when the take profit reaches the break-even point.

○ Trail Price: Computes the trailing take profit price based on an offset percentage (TPLT%) from the closing price of the current candle.

- If an applicable take profit price is calculated, it will be set as the new take profit price.

○ Trail Price till BE: Similar to the Trail Price mode, but it stops trailing when the take profit reaches the break-even point.

○ Trail Price from BE: Similar to Trail Price mode, but it starts trailing when the take profit reaches the break-even point.

○ Trail Incr: Adapts the trailing take profit price based on the offset percentage (TPLT%). Each price change against your position will incrementally adapt the trailing take profit with TPLT%.

○ Trail Incr till BE: Similar to the Trail Incr mode, but it stops trailing when the take profit reaches the break-even point.

• TPLT% - Take Profit Long Trailing Percentage: This percentage serves as an offset or increment depending on your chosen trailing mode.

• TPSB - Take Profit Short Base: Functions similarly to TPLB but for short positions.

• TPSB% - Take Profit Short Base Percentage: Functions similarly to TPLB% but for short positions.

• TPSSRC - Take Profit Short Source: Functions similarly to TPLSRC but for short positions.

• TPST - Take Profit Short Trailing: Functions similarly to TPLT but for short positions.

• TPST% - Take Profit Short Trailing Percentage: Functions similarly to TPLT% but for short positions.

█ ENTRY INVESTMENT DISTRIBUTION

Based on your position investment calculation you can distribute the position investment accross the initial opening trade of the position (SIG%) or the follow up Dollar Cost Averaging (DCA%) or Break Out (BRO%) trades.

For example: SIG%: 10%, DCA%: 45%, BRO%: 45% and the calculated Position Investment is $100, then the initial trade will receive $10, DCA will receive $45, and BRO will receive $45 to work with. Disable BRO and or DCA by setting them to 0%. Keep in mind that the sum of SIG, BRO and DCA may not exceed 100%.

• SIG% - Initial order investment percentage based on the signal: The percentage of the position investment distributed over normal trades.

• DCA% - Dollar Cost Averaging investment percentage: The percentage of the position investment distributed to DCA trades.

• BRO% - Break Out investment percentage: The percentage of the position investment distributed to BRO trades.

█ ENTRY DCA

DCA (Dollar-Cost Averaging) is a risk mitigation strategy where the allocated DCA% budget from the Entry Investment Distribution is distributed among x levels (DCA#) based on calculated prices (DPLM) and order sizes (DOSM), when prices move against your position.

• DCA# - Maximum DCA levels: Set the maximum number of DCA levels.

• DPLM - DCA Price Level Mode: Choose a price level mode that determines at which prices the additional purchases are distributed:

○ Linear: Entry prices are evenly spaced at regular intervals.

○ QuadIn: Entry prices are front-loaded, with more at the beginning and fewer later.

○ QuadOut: Entry prices are back-loaded, with fewer at the beginning and more later.

○ QuadInOut: Entry prices start front-loaded, then become back-loaded.

○ CubicIn: Similar to QuadIn but with a smoother front-loaded distribution.

○ CubicOut: Similar to QuadOut but with a smoother back-loaded distribution.

○ ExpoIn: Entry prices are exponentially increasing, starting small and growing.

○ ExpoOut: Entry prices are exponentially decreasing, starting large and reducing.

○ ExpoInOut: Entry prices start exponentially increasing, then decrease exponentially.

• DOSM - DCA Order Size Mode: Choose a DCA budget distribution mode for order sizes:

○ Linear: Order sizes are evenly spaced at regular intervals.

○ QuadIn: Order sizes are front-loaded, with larger orders at the beginning and smaller ones later.

○ QuadOut: Order sizes are back-loaded, with smaller orders at the beginning and larger ones later.

○ QuadInOut: Order sizes start front-loaded and transition to back-loaded.

○ CubicIn: Similar to QuadIn but with a smoother front-loaded distribution of order sizes.

○ CubicOut: Similar to QuadOut but with a smoother back-loaded distribution of order sizes.

○ ExpoIn: Order sizes exponentially increase, starting small and growing.

○ ExpoOut: Order sizes exponentially decrease, starting large and reducing.

○ ExpoInOut: Order sizes start exponentially increasing, then decrease exponentially.

For a visual representation of the price or order size distribution modes, refer to online easing curves.

█ ENTRY BRO

BRO (Break Out) is a risk mitigation strategy where the allocated BRO% budget from the Entry Investment Distribution is distributed among x levels (BRO#) based on calculated prices (BPLM) and order sizes (BOSM), when prices move in favor of your position.

• BRO# - Maximum BRO levels: Set the maximum number of BRO levels.

• BPLM - BRO Price Level Mode: Choose a price level mode that determines at which prices the additional purchases are distributed:

○ Distribution easing modes work similar as the DCA easing modes.

• BOSM - BRO Order Size Mode: Choose a BRO budget distribution mode for order sizes:

○ Distribution easing modes work similar as the DCA easing modes.

█ ORDER SETTINGS

Fine-tune accuracy to match your exchange's trading constraints, enhancing backtest precision with these settings, default settings are least restrictive for crypto trading pairs.

• MINP - Mininmum Position Notional Value: Exchange-defined minimum notional value for positions:

○ Calculated based on your exchange's rules and is the minimum total value your position must hold to meet their requirements It is calculated by multiplying Quantity with price and leverage.

○ It helps ensure your trades align with your exchange's standards.

• MAXP - Maximum Position Notional Value: Exchange-defined maximum notional value for positions:

○ Similar to MINP, this value is calculated based on your exchange's rules and represents the maximum total value allowed for your position.

• MINQ - Mininmum Order Quantity: Least permissible order quantity based on exchange rules:

○ This is the smallest quantity of an asset that your exchange allows you to trade in a single order.

• MAXQ - Maximum Order Quantity: Highest permissible order quantity according to exchange rules:

○ Opposite of MINQ, this is the largest quantity of an asset you can trade in a single order as defined by your exchange.

• DECP - Decimals in Order Price: Allowed decimal places in order prices as per exchange specifications:

○ This value specifies the number of decimal places you can use when specifying the price of an order.

• DECQ - Decimals in Order Quantity: Permitted decimal places in order quantities according to exchange specifications:

○ Similar to DECP, this value indicates the number of decimal places you can use when specifying the quantity of an asset in an order.

█ STRATEGY CONDITIONS

Specify when the strategy is permitted to execute trades.

• DATE: Enable the Date Range filter to restrict entries to a specific date range.

○ START: Set a start date and hour to commence trading.

○ END: Set an end date and hour to conclude trading within the defined range.

• IDO - Maximum Intraday Orders: Limit the number of orders the strategy can place within a single trading day. Upon reaching this limit, the strategy temporarily halts further entries for the day.

• DL% - Maximum Intraday Loss%: Set a threshold for the maximum allowable intraday loss as a percentage of equity. When exceeded, the strategy temporarily suspends trading for the day.

• CLD - Maximum Consecutive Loss Days: Define the maximum number of consecutive days the strategy can incur losses. Upon reaching this limit, the strategy halts trading and avoids new entries.

• DD% - Maximum Drawdown: Specify the maximum permissible drawdown as a percentage of equity. If this limit is met, the strategy halts trading and refrains from placing additional entries.

• TP% - Total Profit %: Establish a target for the total profit percentage the strategy aims to achieve. Once this target is attained, the strategy halts trading and refrains from initiating new entries.

• TL% - Total Loss %: Define a limit for the total loss percentage relative to the initial capital. If this limit is exceeded, the strategy discontinues trading and refrains from placing further entries.

■ VISUALS

• LINE: Activate a colored dashed diagonal line to visually connect the entry and exit points of positions.

• SLTP: Enable visualization of stop loss, take profit, and break-even levels.

• PNL: Enable Break-Even and Close Lines along with a colored area in between to visualize profit and loss.

• ☼: Brightness % : Adjust the opacity of the plotted trading visuals.

• P - Profit Color : Choose the color for profit-related elements.

• L - Loss Color: Choose the color for loss-related elements.

• B - Breakeven Color : Select the color for break-even points.

• EL - Long Color: Specify the color for long positions.

• ES - Short Color: Specify the color for short positions.

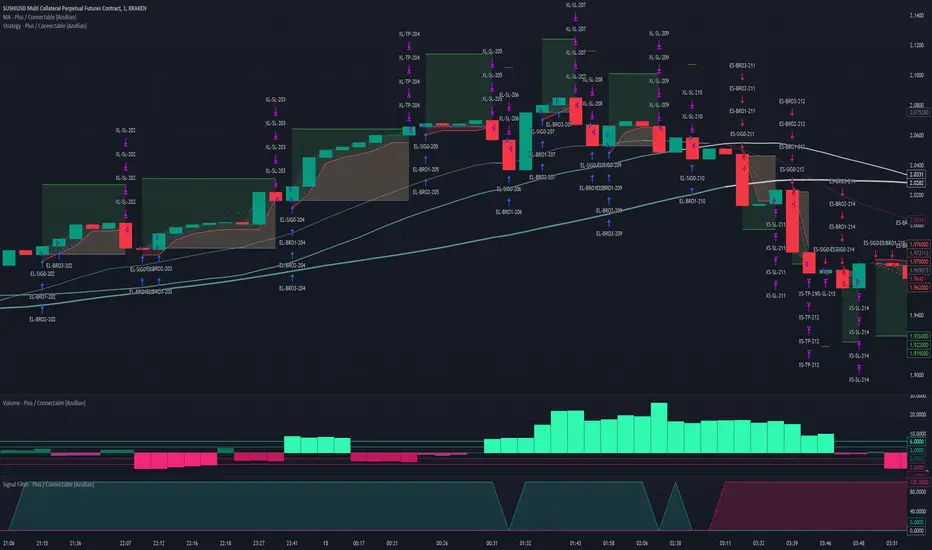

• TRADE LABELING: For better analysis we've labeled all entries and exits conform with the type of order your strategy has executed, some examples:

○ EL-SIG0-124: Enter Long - Signal 0 - Position 124

○ EL-BRO1-130: Enter Long - BRO1 - Position 130

○ EL-BRO2-130: Enter Long - BRO2 - Position 130

○ ES-DCA1-140: Enter Short - DCA1 - Position 140

○ XS-DCA2-140: Exit Short - DCA2 - Position 140

○ XL-TP-150: Exit Long - Take Profit - Position 150

○ XS-TP-154: Exit Short - Take Profit - Position 154

○ XL-SL-160: Exit Long - Stop Loss - Position 160

○ XS-SL-164: Exit Short - Stop Loss - Position 164

○ XS-CND-165: Exit Short - Strategy Condition - Max intraday loss - Position 165

■ ALERT SETTINGS

For developers and those who wish to integrate TradingView alerts into their backend systems, we offer comprehensive labeling options.

• ALID: A unique identifier you've assigned to your alert.

• NAME: A structured name you've given to this strategy.

• LAYOUT: The layout key of the strategy, allowing direct chart linking from your backend.

• SYMBOL: The symbol on which the strategy operates.

○ ONCE: You can choose to include this information only in the first message to reduce message size and repetition in follow-up messages. (max. 4096 characters)

• TICK: The ticker for the strategy.

• CHART: The chart parameter containing the timeframe.period and timeframe.multiplier.

○ ONCE: You can choose to include this information only in the first message to reduce message size and repetition in follow-up messages. (max. 4096 characters)

• BAR: Includes bar information in the alert message.

• STRATEGY: Adds strategy inputs to the alert message.

○ ONCE: You can choose to include this information only in the first message to reduce message size and repetition in follow-up messages. (max. 4096 characters)

• PERFORMANCE: Incorporates strategy performance data into the alert message.

• SIGNAL: Appends received signal weights (EL, XL, ES, XS) to the alert message.

• ORDERS: Includes order details in the alert message.

• TAGS: Adds up to 6 tags and their corresponding values to the alert message.

○ ONCE: You can choose to include this information only in the first message to reduce message size and repetition in follow-up messages. (max. 4096 characters)

Of course we can't neglect letting you in on how this juicy JSON would look (without the // comments):

{

"id": 20726, // Message Id

"t": "2023-11-01T10:35:00Z", // Message Time

"al": { // Alert

"id": "639bfa9a-5f01-4031-8880-7ec01e972055", // Alert Id

"n": "TEST04", // Name

"l": "ABC123" // Layout

},

"sym": { // Symbol

"typ": "crypto", // Type

"r": "DOGEUSD.PM", // Root

"pre": "KRAKEN", // Prefix

"tc": "DOGEUSD.PM", // Ticker

"bc": "DOGE", // BaseCurrency

"c": "USD", // Currency

"d": "DOGEUSD Multi Collateral Perpetual Futures Contract", // Description

"mtc": 0.000001, // MinTick

"pv": 1, // PointValue

"ct": "PF_DOGEUSD" // CustomTicker

},

"ch": { // Chart

"pd": "1", // Period

"mul": 1 // Multiplier

},

"bar": { // Bar

"id": 20725, // Index

"t": "2023-11-01T10:33:00Z", // Time

"o": 0.066799, // Open

"h": 0.066799, // High

"l": 0.066799, // Low

"c": 0.066799, // Close

"v": 2924 // Vol

},

"strat": { // Strategy

"n": "Strategy - Plus / Connectable ", // Name

"sig": { // Signal

"c1e": true, // Connector1Enabled

"c1s": 500500.500501, // Connector1Source

"c1g": 1, // Connector1Gain

"c2e": false, // Connector2Enabled

"c2s": 0.067043, // Connector2Source

"c2g": 1, // Connector2Gain

"sm": "Swing (EL, ES)", // SignalMode

"xm": "Always", // ExitMode

"mlp": 0.01, // ExitModeMinPercLoss

"mpp": 0.01 // ExitModeMinPercProfit

},

"inv": { // Investment

"lb": "Equity", // LossBase

"lp": 50, // LossPerc

"pb": "Equity", // ProfitBase

"pp": 100, // ProfitPerc

"pcb": "Equity", // ProfitCustomBase

"pcp": 100, // ProfitCustomPerc

"pct": 10000, // ProfitCustomThreshold

"elp": 100, // LongPerc

"esp": 100, // ShortPerc

"rsk": 1, // MaxRisk

"lvg": 10 // MaxLeverage

},

"sl": { // StopLoss

"lb": "Price Entry + Offset", // LongBase

"lp": 0.2, // LongPerc

"lsrc": 0.067043, // LongSource

"lt": "Trail Stop", // LongTrailMode

"ltp": 0.2, // LongTrailPerc

"sb": "Price Entry + Offset", // ShortBase

"sp": 0.2, // ShortPerc

"ssrc": 0.067043, // ShortSource

"st": "Trail Stop", // ShortTrailMode

"stp": 0.2 // ShortTrailPerc

},

"tp": { // TakeProfit

"lb": "Price Entry + Offset", // LongBase

"lp": 1, // LongPerc

"lsrc": 0.067043, // LongSource

"lt": "Fixed", // LongTrailMode

"ltp": 1, // LongTrailPerc

"sb": "Price Entry + Offset", // ShortBase

"sp": 1, // ShortPerc

"ssrc": 0.067043, // ShortSource

"st": "Fixed", // ShortTrailMode

"stp": 1 // ShortTrailPerc

},

"dis": { // Distribution

"sigp": 10, // SignalPerc

"dcap": 0, // DCAPerc

"brop": 90 // BROPerc

},

"dca": { // DCA

"lvl": 3, // Levels

"pl": "linear", // ModePriceLevel

"os": "linear" // ModeOrderSize

},

"bro": { // BRO

"lvl": 3, // Levels

"pl": "expoIn", // ModePriceLevel

"os": "cubicOut" // ModeOrderSize

},

"ord": { // OrderSettings

"pmin": 5, // PNVMin

"pmax": 30000000, // PNVMax

"qmin": 0, // QtyMin

"qmax": 1000000000, // QtyMax

"dp": 6, // DecPrice

"dq": 6 // DecQty

},

"cnd": { // Conditions

"de": true, // DateRangeEnabled

"start": "2023-11-01T10:30:00Z", // StartTime

"end": "2024-12-31T23:30:00Z", // EndTime

"idoe": false, // MaxIntradayOrdersEnabled

"ido": 100, // MaxIntradayOrders

"dle": false, // MaxIntradayLossEnabled

"dl": 10, // MaxIntradayLossPerc

"clde": false, // MaxConsLossDaysEnabled

"cld": false, // MaxConsLossDays

"dde": false, // MaxDrawdownEnabled

"dd": 100, // MaxDrawdownPerc

"mpe": false, // MaxProfitEnabled

"mp": 200, // MaxProfitPerc

"mle": false, // MaxLossEnabled

"ml": -50 // MaxLossPerc

}

},

"perf": { // Performance

"ic": 1000, // InitialCapital

"eq": 1000, // Equity

"np": 0, // NetProfit

"op": 0, // OpenProfit

"ct": 0, // ClosedTrades

"ot": 0, // OpenTrades

"p": "FLAT", // MarketPosition

"ps": 0, // MarketPositionSize

"pp": "FLAT", // PreviousMarketPosition

"pps": 0 // PreviousMarketPositionSize

},

"sig": { // Signal

"el": 0, // EL

"xl": 0, // XL

"es": 6, // ES

"xs": 0 // XS

},

"ord": ,

"tag":

}

█ USAGE OF CONNECTABLE INDICATORS

■ Connectable chaining mechanism

Connectable indicators can be connected directly to the signal monitor, signal filter or strategy , or they can be daisy chained to each other while the last indicator in the chain connects to the signal monitor, signal filter or strategy. When using a signal filter you can chain the filter to the strategy input to make your chain complete.

• Direct chaining: Connect an indicator directly to the signal monitor, signal filter or strategy through the provided inputs (→).

• Daisy chaining: Connect indicators using the indicator input (→). The first in a daisy chain should have a flow (⌥) set to 'Indicator only'. Subsequent indicators use 'Both' to pass the previous weight. The final indicator connects to the signal monitor, signal filter, or strategy.

■ Set up this indicator with signals and a signal filter

The indicator provides visual cues based on signal conditions. However, its weight system is best utilized when paired with a connectable signal filter, monitor, or strategy .

Let's connect the Strategy - Plus to a connectable signal filter and connectable indicators :

1. Load all relevant indicators

• Load MA - Plus / Connectable

• Load Signal filter - Plus / Connectable

• Load Strategy - Plus / Connectable

2. Signal Filter Plus: Connect the MA - Plus to the Signal Filter

• Open the signal filter settings

• Choose one of the five input dropdowns (1→, 2→, 3→, 4→, 5→) and choose : MA - Plus / Connectable: Signal Connector

• Toggle the enable box before the connected input to enable the incoming signal

3. Signal Filter: Update the filter settings if needed

• The default filter mode for the trading direction is SWING, and is compatible with the default settings in the strategy and indicators.

4. Signal Filter: Update the weight threshold settings if needed

• All connectable indicators load by default with a score of 6 for each direction (EL, XL, ES, XS)

• By default, weight threshold is 'ABOVE' Threshold 1 (TH1) and Threshold 2 (TH2), both set at 5. This allows each occurrence to score, as the default score is 1 point above the threshold.

5. Strategy Plus: Connect one of the strategy plus inputs to the signal filters signal connector in the strategy settings

• Select a strategy input → and select the Signal filter - Plus: Signal connector

6. Strateg Plus: Enable filter compatible directions

• As the default setting of the filter is SWING, we should also set the SM (Strategy mode) to SWING.

7. Strateg Plus: You're ready to start optimizing

• Dive into all parameters and start optimizing your backtesting results.

█ BENEFITS

• Adaptable Modular Design: Arrange indicators in diverse structures via direct or daisy chaining, allowing tailored configurations to align with your analysis approach.

• Streamlined Backtesting: Simplify the iterative process of testing and adjusting combinations, facilitating a smoother exploration of potential setups.

• Intuitive Interface: Navigate TradingView with added ease. Integrate desired indicators, adjust settings, and establish alerts without delving into complex code.

• Signal Weight Precision: Leverage granular weight allocation among signals, offering a deeper layer of customization in strategy formulation.

• Advanced Signal Filtering: Define entry and exit conditions with more clarity, granting an added layer of strategy precision.

• Clear Visual Feedback: Distinct visual signals and cues enhance the readability of charts, promoting informed decision-making.

• Standardized Defaults: Indicators are equipped with universally recognized preset settings, ensuring consistency in initial setups across different types like momentum or volatility.

• Reliability: Our indicators are meticulously developed to prevent repainting. We strictly adhere to TradingView's coding conventions, ensuring our code is both performant and clean.

█ COMPATIBLE INDICATORS

Each indicator that incorporates our open-source 'azLibConnector' library and adheres to our conventions can be effortlessly integrated and used as detailed above.

For clarity and recognition within the TradingView platform, we append the suffix ' / Connectable' to every compatible indicator.

█ COMMON MISTAKES, CLARIFICATIONS AND TIPS

• Removing an indicator from a chain: Deleting a linked indicator and confirming the "remove study tree" alert will also remove all underlying indicators in the object tree. Before removing one, disconnect the adjacent indicators and move it to the object stack's bottom.

• Point systems: The azLibConnector provides 500 points for each direction (EL: Enter long, XL: Exit long, ES: Enter short, XS: Exit short) Remember this cap when devising a point structure.

• Flow misconfiguration: In daisy chains the first indicator should always have a flow (⌥) setting of 'indicator only' while other indicator should have a flow (⌥) setting of 'both'.

• Hide attributes: As connectable indicators send through quite some information you'll notice all the arguments are taking up some screenwidth and cause some visual clutter. You can disable arguments in Chart Settings / Status line.

• Layout and abbreviations: To maintain a consistent structure, we use abbreviations for each input. While this may initially seem complex, you'll quickly become familiar with them. Each abbreviation is also explained in the inline tooltips.

• Inputs: Connecting a connectable indicator directly to the strategy delivers the raw signal without a weight threshold, meaning every signal will trigger a trade.

• Layout and Abbreviations: Abbreviations streamline structure and input identification. Although they may seem complex initially, inline tooltips provide explanations, facilitating quick acclimatization.

• Total Trade Limit Error & Date-Time Filter: For deep backtesting, be mindful of the total trade limit. Utilize the date-time filter to narrow the test scope and avoid TradingView order limits.

• Calculation Timeout: Encounter a timeout? Adjust any parameter slightly to restart the calculation process.

• Message Character Limit: To stay within message character limits, consider turning off certain features or setting some to 'once'.

• Direct Indicator-to-Strategy Connection: When connecting an indicator directly to a strategy without thresholds, the strategy will default to long if weights are equally assigned.

• Pyramid Enabling with DCA and BRO: Activate pyramid orders, enabling you to optimize your strategy during Dollar Cost Averaging and Break Out trades.

• Recalculate & Fill Orders Properties: Adjusting these default settings in strategy properties tab may lead to unexpected behavior when backtesting. Approach with caution.

• Optimized for Crypto: Our indicators have been optimized and tested primarily on cryptocurrency markets. Results in other markets may vary.

• Inline Tooltips Documentation: Detailed documentation and guidance are available via inline tooltips for immediate assistance.

• Strategy Settings Margin: Set margin to 1 to be able to apply leverage.

• Styling Panel: Explore the styling panel to disable labels or any other visual cues to reduce clutter on busy charts, enhancing visual clarity and personalization.

• Applying Leverage on Spot Markets: Ensure that maximum leverage on spot markets is configured to 1.

• Unrealistic Order Sizes: Verify that the order book can accommodate your backtested order sizes.

█ A NOTE OF GRATITUDE

Through years of exploring TradingView and Pine Script, we've drawn immense inspiration from the community's knowledge and innovation. Thank you for being a constant source of motivation and insight.

█ RISK DISCLAIMER

Azullian's content, tools, scripts, articles, and educational offerings are presented purely for educational and informational uses. Please be aware that past performance should not be considered a predictor of future results.

Self Optimizing ROC [Starbots]Self Optimizing Rate of Change (ROC) Strategy. (non-repainting)

Script constantly tests 15 different ROC parameter combinations for maximum profitability and trades based on the best performing combination.

You will notice that signal lines switch after a bar close sometimes, this is when the strategy optimizes to the better combination and change plots, strategy is dynamic.

---------------------------------------------------------------------------------------------------------

The Rate-of-Change (ROC) indicator, which is also referred to as Momentum, is a pure momentum oscillator that measures the percent change in price from one period to the next. The ROC calculation compares the current price with the price “n” periods ago. The plot forms an oscillator that fluctuates above and below the zero line as the rate of change moves from positive to negative. As a momentum oscillator, ROC signals include centerline crossovers, divergences, and overbought-oversold readings.

ROC = (Close - Close n periods ago) / (Close n periods ago) * 100

-----------------------------------------------------------------------------------------------------------

The logic of self - optimizing:

This script is always backtesting 15 different combinations of ROC settings in the background and saves the net. profit gained for every single one of them, then strategy selects and use the best performing combination of settings currently available for you to trade.

It's recalculating on every bar close - if one of the parameters starts performing better than others - have a higher net profit gain (it's literally like running 15 backtests with different settings in the background) strategy switches to that parameter and continues trading like that until one of the other indicator parameters starts performing better again and switches to that settings.

We are optimizing our strategy based on 15 different 'lengths' or also called 'periods' of ROC.

Inputs (ROC period) : (you don't need to change them, you have a nice wide variety of periods)

🔴Roc (default=9) = 5

🟢Roc2 = 6

🔵Roc3 = 7

🟡Roc4 = 8

🟣Roc5 = 9

🟠Roc6 = 10

🔴Roc7 = 11

🟢Roc8 = 12

🔵Roc9 = 13

🟡Roc10 = 14

🟣Roc11 = 15

🟠Roc12 = 16

🟡Roc13 = 17

🟣Roc14 = 18

🟠Roc15 = 20

Backtester in the background works like this:

backtest ROC1 => save net. profit

backtest ROC2 => save net. profit ;

backtest ROC3 => save net. profit ;

..........

..........

backtest ROC15 => save net. profit ;

=>

It will backtest 15 different ROC parameters and save their profits.

Your strategy then trades based on the best performing (highest net.profit) ROC Setting currently available. It will check the calculations and backtest them on every new bar close - it's like running 15 strategies at time, and manually selecting the best performing one.

________________________________________________________________________

If you wish to use it as INDICATOR - turn on 'Recalculate after every tick' in Properties tab to have this script updating constantly and use it as a normal Indicator tool for manual trading.

-- Noise Filter - This will punish the tiny trades made by certain parameters and give more advantage to big average trades. It's basically normal fee calculation, it will deduct 0.xx % fee from every trade when optimizing. You usually want it to have the same number as your fees on exchange. Large number will choose big long swing trades, small number will prioritize small scalping trades.

-- Turn on ROC Combination Profits and spot the worst/best performing combination. You can change periods to get the best performance after checking this table stats.

-- Backtesting Range - backtest within your desired time window. Example: 'from 01 / 01 /2020 to 01 / 01 /2023'.

-- Optimizing range - you can decrease the amount of bars/data for optimizing script. This way you can keep it up to date to more recent market by selecting optimizing range to optimize it just from the recent 3-6months of data for example. Strategy before this selected range will normally trade (backtest) based on the first ROC period ( 'Roc(default=9)' Input) parameter in your menu if you have Optimizing Range turned on.

**** I recommend 'Optimizing Range' to be turned off, use max amount of available bars in your history for optimization script.

-- Strategy is trading on the bar close without repaint. You can trade Long-Sell or Long- Short. Alerts available, insert webhook messages.

-- Turn on Profit Calendar for better overview of how your strategy performs monthly/annualy

-- Recommended ROC periods: from 5 to 24.

-- Recommended Sources : close, hlc3, hlcc4

-- Recommended Chart Timeframe : 4h +

-- Notes window : add your custom comments here or save your webhook messages inside here

-- Trading Session: in a session, you have to specify the time range for every day. It will trade only within this window and close trades when it's out. Session from 9am to 5pm will look like that: 0900-1700 or 7am to 4:30pm 0700-1630. After the colon, you can specify days of the week for your trading session. 1234567 trading all days, 23456 – Monday to Friday ('1 is Sunday here'). 0000-0000:1234567 by default will trade every day nonstop. 00.00am to 00.00pm and 1234567 every day of the week for example - Cryptocurrencies.

This script is simple to use for any trader as it saves a lot of time for searching good parameters on your own. It's self-optimizing and adjusting to the markets on the go.

INFINITY ALGO🆕Meet the updated version of our flagship indicator, now it's INFINITY ALGO!

🏃🏻 QUICK START

In very simple terms, our indicator generates complex trading signals on your chart (buy/sell), including Entry Point, Take Profit levels, Stop Loss level

To start, you need to add our indicator to your chart , choose a timeframe (we recommend 13min,15min and 4h but you can try any, these only have the best results) and set up notifications (how to do it told below) and that's it, you can work with it even without changing the settings!

Of course, to improve the accuracy of signals you will have to choose the optimal settings of the script for each trading pair and timeframe (you can find a guide below)

📊 SIGNALS

This script will generate complex trading recommendations, both Long and Short (signals); signals include:

- Entry Point:

Calculated based on pivot levels with confirmation by EMA/SMA (you can select this in the settings); also bullish/bearish cup is checked to confirm the entry.

Additionally, in the settings you can enable Heiken Ashi calculation mode (it shows much better on some trading pairs).

Why do we mashup these components and how they work together?

- The main indicator in our script is pivot levels, it is enabled by default and cannot be disabled. Auxiliary indicators (which you can switch on and off in the script settings) are EMA/SMA and Heiken Ashi. We have used pivot levels, which mark potential support and resistance zones based on previous price action. We have also used EMA/SMA that smooth out price fluctuations and show the direction of the trend. We have added an option to use Heiken Ashi that filters out noise and highlights the trend. We have also checked for bullish/bearish cup patterns, which are reversal patterns that indicate a change in momentum. By combining these indicators, we have created a more robust entry point that considers multiple factors such as price levels, trend, noise, and momentum.

- 6 Take Profit levels:

It is also possible to change in the settings (It is also possible to change the values for Short or Long positions separately), it will be fixed values in % (The default Take Profits for Long&Short are as follows: TP1-0.3%; TP2-1%; TP3-2%; TP4-3%; TP5-7.5%; TP6-16.5%)

- Stop Loss Level:

As with Take Profits, this is a fixed % value that you can customise to suit your risk management needs (It is also possible to change the values for Short or Long positions separately, by default is 4.5% for Long&Short positions)

*When trading on these signals, we strongly recommend that you exit the position in parts at each take profit or close your entire position at one particular take profit. Our script was designed specifically for exiting a position on take profits

⚙️ SETTINGS

Now let's talk about the settings of this script, which allow you to customise the signals quite a lot. In general, we recommend selecting the settings for each trading pair and timeframe separately, this will allow you to achieve better targets accuracy (the default settings are universal, you can trade with them without changing them if you want)

-> IMAGE <-

1. Period - minimum value of 2. Increasing this parameter will increase the accuracy of signals, but will reduce their number (accordingly, lowering the parameter will do the opposite). For the majority of trading pairs and timeframes the optimal period will be between 5 and 10 (the default value is 5).

2. Maximum Breakout length (in bars) - for most trading pairs you can set the value from 200 to 300 and it will be optimal. Below 200 is not recommended

3. T hreshold Rate % - this value also affects the accuracy and the number of signals - the higher this value is, the more often signals will be generated, but it can negatively affect the accuracy. The minimum value is 3, and the maximum value is 10. We recommend to try values in the range from 4 to 7 for most tickers

4. Minimum Number of tests - the number of level checks is required, we recommend to try 2, and only for some timeframes increase to 3

5. MA type & MA filter - The shorter the length of moving averages, the faster they react to trend changes, and show more local trends than global ones. If the length of MAs is longer, more global trends are shown. By default, the most optimal values are set.

By the way, you can ask us for a ready-made preset for any pair and we will be happy to help you!

📄 BACKTESTING

Now let's talk about how to properly test the settings and evaluate their effectiveness. Our script has a c ustom built-in backtester that shows statistics on the current trading pair and allows you to calculate the accuracy of each take profit target, as well as calculate values such as Gross profit/loss, net profit, and the ratio of initial deposit to profit. (you can enable/disable backtester "statistics" label in main settings)

In the main settings you can change the values for: initial deposit (Deposit $), trade size $ and leverage (by the way, it also affects the display of the label "Peak profit", which is calculated with this leverage)

-> IMAGE <-

Now let's look at the backtester - it shows detailed statistics for each Take Profit level, including: accuracy in % and number of trades; gross profit & loss; net profit in % and $ (based on selected settings); deposit to profit ratio in % and $.

Why did we choose such properties in the backtest for publication?

- Well, as the initial capital we took 5000$ and deposit 3% (150$) of the initial capital in each trade. For the fee was taken the value from the exchange Binance, which is 0.06% per trade (Taker + Maker, for a user without VIP on Binance and without taking into account additional fees such as funding, leverage fees, etc).

- Please also take a look at our inbuilt backtester ( IMAGE ) which counts the accuracy to each Take Profit. Also note that our inbuilt backtester does not take any fees into account. Pay attention to the last field "Deposit with Profit" it shows the value if you would close all positions at a certain target. For example, we can see that the most optimal is TP3 at these settings for this trading pair and timeframe, as the deposit to profit ratio will be +61.2%

- Also the script is more designed for swing and long term trading, so on most trading pairs you will be able to see statistics for 60-90 trades dataset

*disclaimer: please note that past results does not guarantee future performance! The accuracy of take profit targets in our backtester is calculated on past results, keep this in mind please

📥 NOTIFICATIONS

We have provided notifications that will deliver the latest signals to you in a convenient format in TradingView. The notification looks like this: It contains the entry point, Take Profits, Stop Loss, and a bit of advice on risk management. -> IMAGE <-

To set up notifications:

1. Select the script settings, trading pair and timeframe

2. Click "add alert on InfinityAlgo", then select "alert () function calls only" in the settings

-> IMAGE <-

3. That's it, now all that's left is to wait for a fresh alert

🔑 HOW TO GET ACCESS

We hope you will like this script :) We are always ready to help you with customisation, just let us know! To learn more about our scripts & get access - check out the “Author’s instructions” below 👇🏼

FluxFilter Trend Strategy [BITsPIP]Hello fellow traders, I'm excited to share with you the FluxFilter Trend Strategy, a trading approach I've developed for those interested in exploring trend-following strategies. My goal was to create something straightforward and accessible, so traders looking to refine their portfolios can easily integrate its features. By the end of this guide, I hope you'll have a solid grasp of how the FluxFilter Trend Strategy functions, appreciate its benefits, understand its potential drawbacks, and see how it might fit into various trading contexts.

I) Overview

The FluxFilter Trend Strategy is tailored to align with the market's long-term trend. It examines the price data from the previous year to gauge the market's overall trajectory by employing moving averages. Subsequently, within shorter timeframes, the strategy utilizes a combination of modified Supertrend, Hull Suite, and various trend-following and filtering techniques to generate buy or sell signals. Although its advanced take profit and stop loss mechanisms might initially present a learning curve, they are integral to the strategy's effectiveness. They are designed to secure gains by capturing prevailing trends and mitigating the impact of false reversal signals.

II) Deep Backtesting

Deep backtesting stands as a cornerstone in the development of trading strategies, offering a robust method for traders to assess the performance of their strategy against historical data. This process yields a retrospective view, illustrating how the strategy might have navigated through past market fluctuations, thereby shedding light on its potential robustness and areas for refinement. However, it's crucial to acknowledge that a strategy's performance can be influenced by a myriad of factors including market dynamics, the chosen timeframe, and the inherent attributes of the traded asset. Consequently, it's advisable to conduct thorough backtesting under various conditions to ascertain the strategy's reliability before applying it to actual trading scenarios.

III) Benefits

A primary advantage of the FluxFilter Trend Strategy is its proficiency in discerning genuine market trends from mere price fluctuations, thereby avoiding premature or uncertain trades. Unlike approaches that take high risks on speculative trades, this strategy prioritizes a high degree of confidence in the direction of the trade. It meticulously waits for a clear confirmation of the market trend. Once this certainty is established, the strategy promptly generates trade signals, ensuring that traders are positioned to capitalize on optimal market entry points without delay. This approach not only enhances the potential for profit but also aligns with a disciplined and methodical trading ethos.

IV) Applications

FluxFilter Trend Strategy can be applied across various timeframes, with a particular efficacy in those under 15 minutes. Its adaptable framework means it can be customized to cater to a variety of asset classes, encompassing stocks, commodities, forex, and cryptocurrencies. Initially, the strategy was specifically calibrated for low-volatile cryptocurrencies, as reflected in the default settings for stop loss and take profit values. It's important to recognize that the unique volatility and trend patterns of your selected market necessitate careful adjustments to these parameters. This fine-tuning of profit targets and stop loss thresholds is crucial for aligning the strategy with the specific dynamics of your chosen market, which I will discuss shortly.

V) Strategy's Logic

1. Trend Identification: My conviction lies in the power of trend trading to yield long-term gains. Central to the FluxFilter Trend Strategy is the Hull Suite indicator, a tool developed by InSilico, serving as one of the confirmation indicators. This indicator acts as a compass for trend direction; a price residing above the Hull Suite line signals an uptrend, potentially marking an entry point for a buy position or confirming it. In contrast, a price positioned below this line suggests a downtrend, potentially indicating a strategic moment to sell or confirming the sell.

2. Noise Reduction: The financial markets are known for their 'noise'—short-lived price movements that can obscure the true market direction. The FluxFilter Trend Strategy is designed to sift through this noise, thereby facilitating more lucid and informed trading decisions. It employs a set of straightforward yet innovative techniques to single out significant misleading fluctuations. This is achieved by analyzing recent bars to spot bars with unusually large bodies, which often represent misleading market noise.

3. Risk Management: A key facet of the strategy is its emphasis on pragmatic risk management. Traders are empowered to establish practical stop-loss and take-profit levels, tailoring these crucial parameters to the specific market they are engaging in. This customization is instrumental in optimizing long-term profitability, ensuring that the strategy adapts fluidly to the unique characteristics and volatility patterns of different trading environments.

VI) Strategy's Input Settings and Default Values

1. Modified Supertrend

i. Factor: Serving as a multiplier in the Average True Range (ATR) calculation, this parameter adjusts the distance of the Supertrend line relative to the price chart. Elevating the factor value widens the gap between the Supertrend line and price, offering a more conservative stance. On the flip side, diminishing the factor value pulls the Supertrend line closer to the price action, heightening its sensitivity. While the preset value is 1, you have the flexibility to modify this to suit your trading approach.

ii. ATR Length: This defines the count of bars that are incorporated into the ATR computation, directly influencing the Supertrend's adaptability to market changes. With a default setting of 30 bars, it strikes a balance, smoothing over short-term fluctuations while maintaining a meaningful sensitivity to market trends. Adjusting this parameter allows you to tailor the indicator's responsiveness to suit your trading strategy, considering the volatility and behavioral patterns of the asset you are trading.

2. Hull Suite

i. Hull Suite Length: Designed for capturing long-term trends, the Hull Suite Length is configured at 1000. Functioning comparably to moving averages, the Hull Suite features upper and lower bands, though these are not employed in our current strategy.

ii. Length Multiplier: It's advisable to maintain a minimal value for the Length Multiplier, prioritizing the optimization of the Hull Suite Length. Presently, it is set to 1.

3. Filtering Indicators

i. Fluctuation Filtering Percentage: It's advisable to set this parameter to ten times the size of the average bar in your specific market, as this helps effectively mitigate the impact of market fluctuations. While the initial default is 0.4(%), based on the BTCUSDT market, it's crucial to adjust this figure to align with the characteristics of different assets or markets you're trading in.

ii. Fluctuation Filtering Bars: This parameter designates the count of preceding bars to consider when assessing market fluctuations. It's fully customizable, allowing you to tailor it based on your market insights. The preset default is 3, a balance chosen to minimize susceptibility to potentially misleading signals.

iii. Trend Confirmation Percentage: This metric is pivotal for verifying the viability of a trend post-entry. If the trade doesn't achieve this percentage in profit, it indicates a deviation from the expected trend. Under such circumstances, it may be prudent to exit the trade prematurely rather than awaiting the stop-loss trigger. It's recommended to set this parameter at half the size of the average candle body for the market you're analyzing. The initial default is set at 0.2(%).

4. StopLoss and TakeProfit

i. StopLoss and TakeProfit Settings: Two distinct approaches are available. Semi-Automatic StopLoss/TakeProfit Setting and Manual StopLoss/TakeProfit Setting. The Semi-Automatic mode streamlines the process by allowing you to input values for a 5-minute timeframe, subsequently auto-adjusting these values across various timeframes, both lower and higher. Conversely, the Manual mode offers full control, enabling you to meticulously define TakeProfit values for each individual timeframe.

ii. TakeProfit Threshold # and TakeProfit Value #: Imagine this mechanism as an ascending staircase. Each step represents a range, with the lower boundary (TakeProfit Value) designed to close the trade upon being reached, and the upper boundary (TakeProfit Threshold) upon being hit, propelling the trade to the next level, and forming a new range. This stair-stepping approach enhances risk management and has the potential to increase profitability. The pre-set configurations are tailored for volatile markets, such as BTCUSDT. It's advisable to devote time to tailoring these settings to your specific market, aiming to achieve optimal results based on backtesting.

iii. StopLoss Value: In line with its name, this value marks the limit of loss you're prepared to accept should the market trend go against your expectations. It's crucial to note that once your asset reaches the first TakeProfit range, the initial StopLoss value becomes obsolete, supplanted by the first TakeProfit Value. The default StopLoss value is pegged at 1.8(%), a figure worth considering in your trading strategy.

VII) Entry Conditions

The principal element that triggers the signal is the Modified Supertrend. Additional indicators serve as confirmatory tools. Nonetheless, to refine your strategy effectively, it's crucial to fine-tune the parameters. This involves adjusting input variables such as take profit levels, threshold parameters, and the filtering values discussed previously.

VIII) Exit Conditions

The strategy stipulates exit conditions primarily governed by stop loss and take profit parameters. On infrequent occasions, if the trend lacks confirmation post-entry, the strategy mandates an exit upon the issuance of a reverse signal (whether confirmed or unconfirmed) by the strategy itself.

Good Luck!!

Ichimoku Clouds Strategy Long and ShortOverview:

The Ichimoku Clouds Strategy leverages the Ichimoku Kinko Hyo technique to offer traders a range of innovative features, enhancing market analysis and trading efficiency. This strategy is distinct in its combination of standard methodology and advanced customization, making it suitable for both novice and experienced traders.

Unique Features:

Enhanced Interpretation: The strategy introduces weak, neutral, and strong bullish/bearish signals, enabling detailed interpretation of the Ichimoku cloud and direct chart plotting.

Configurable Trading Periods: Users can tailor the strategy to specific market windows, adapting to different market conditions.

Dual Trading Modes: Long and Short modes are available, allowing alignment with market trends.

Flexible Risk Management: Offers three styles in each mode, combining fixed risk management with dynamic indicator states for versatile trade management.

Indicator Line Plotting: Enables plotting of Ichimoku indicator lines on the chart for visual decision-making support.

Methodology:

The strategy utilizes the standard Ichimoku Kinko Hyo model, interpreting indicator values with settings adjustable through a user-friendly menu. This approach is enhanced by TradingView's built-in strategy tester for customization and market selection.

Risk Management:

Our approach to risk management is dynamic and indicator-centric. With data from the last year, we focus on dynamic indicator states interpretations to mitigate manual setting causing human factor biases. Users still have the option to set a fixed stop loss and/or take profit per position using the corresponding parameters in settings, aligning with their risk tolerance.

Backtest Results:

Operating window: Date range of backtests is 2023.01.01 - 2024.01.04. It is chosen to let the strategy to close all opened positions.

Commission and Slippage: Includes a standard Binance commission of 0.1% and accounts for possible slippage over 5 ticks.