MTOBVR_CheckOverview.

This indicator checks to see if the OBV follows a specific pattern and visually displays the trend of the OBV on different time legs. It also has the ability to set alerts when certain conditions are met.

How to use

Setting up the indicator

Add a new indicator on a chart in TradingView.

Copy the code into the “Pine Script™ Editor” and save it as a new script.

Apply the script to your chart.

Indicator Functions

OBV Calculation

Calculates OBV for each time frame (5-minute, 15-minute, 30-minute, 1-hour, 4-hour, daily, and weekly) and displays it on the chart OBV is an indicator that combines price changes and trading volume.

Pattern Detection

Detects whether a particular pattern, such as a double or triple bottom, appears in the OBV. This allows us to identify buy or sell signals.

When these patterns are detected, the background color changes.

Background Color Change

When an OBV forms a particular pattern, the background color of the chart changes. This provides visual confirmation that a pattern has appeared.

Minimum pattern (min_bool): when the 5-, 15-, and 30-minute conditions for OBV are met.

High hourly pattern (h_bool): when the condition is met for the 1-hour, 4-hour, and daily legs of the OBV.

One-week pattern (range_obv_1w_bool): when the condition is met for the 1-week OBV pattern.

When all conditions are met: when the minimum pattern, high hourly pattern, and one-week pattern are all met.

Alert Settings

You can set alerts when certain conditions are met. This allows you to receive signals in real time.

Minimum conditions (min_bool): conditions at 5, 15, and 30 minutes of OBV.

High timeframe condition (h_bool): condition on the 1-hour, 4-hour, and daily legs of the OBV.

When all conditions are met: When all of the above conditions are met.

One-week condition (range_obv_1w_bool): Condition for the one-week leg of the OBV.

When all conditions are met: when the minimum, high time leg, and one week conditions are all met.

Arrows

OBV_ALL_UP: A green triangle arrow is displayed when the OBV is rising on all time legs.

OBV_ALL_DOWN: A red triangle arrow appears when the OBV is falling on all time legs.

Usage Notes

Time Leg Settings: This script uses OBVs of different time legs to detect patterns. Depending on the time leg used, appropriate settings and interpretation are required.

Alert settings: In order to activate the alert function, the alert conditions and notification method must be configured using TradingView's alert system.

This indicator allows you to visually see trends and patterns in the OBV across multiple time frames, allowing you to make more informed trading decisions.

"one一季度财报" için komut dosyalarını ara

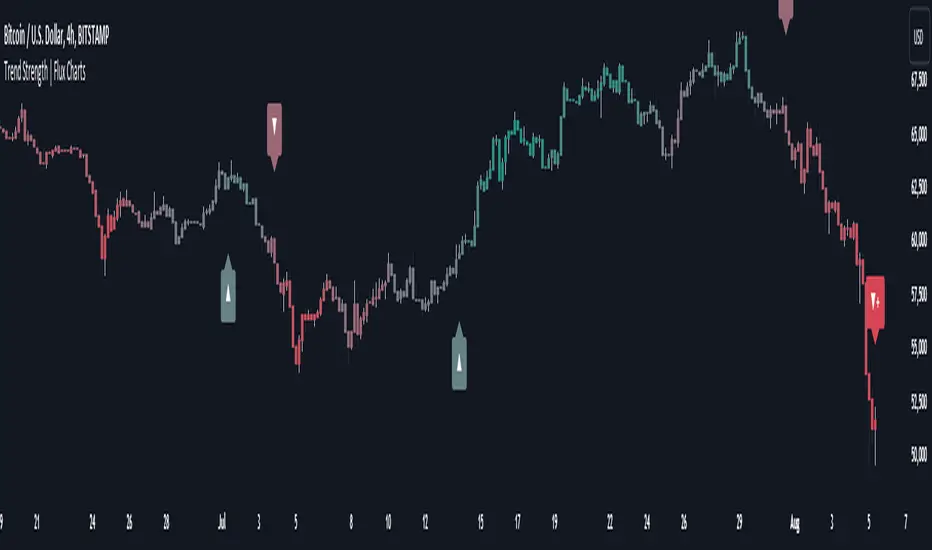

Trend Strength | Flux Charts💎 GENERAL OVERVIEW

Introducing the new Trend Strength indicator! Latest trends and their strengths play an important role for traders. This indicator aims to make trend and strength detection much easier by coloring candlesticks based on the current strength of trend. More info about the process in the "How Does It Work" section.

Features of the new Trend Strength Indicator :

3 Trend Detection Algorithms Combined (RSI, Supertrend & EMA Cross)

Fully Customizable Algorithm

Strength Labels

Customizable Colors For Bullish, Neutral & Bearish Trends

📌 HOW DOES IT WORK ?

This indicator uses three different methods of trend detection and combines them all into one value. First, the RSI is calculated. The RSI outputs a value between 0 & 100, which this indicator maps into -100 <-> 100. Let this value be named RSI. Then, the Supertrend is calculated. Let SPR be -1 if the calculated Supertrend is bearish, and 1 if it's bullish. After that, latest EMA Cross is calculated. This is done by checking the distance between the two EMA's adjusted by the user. Let EMADiff = EMA1 - EMA2. Then EMADiff is mapped from -ATR * 2 <-> ATR * 2 to -100 <-> 100.

Then a Total Strength (TS) is calculated by given formula : RSI * 0.5 + SPR * 0.2 + EMADiff * 0.3

The TS value is between -100 <-> 100, -100 being fully bearish, 0 being true neutral and 100 being fully bullish.

Then the Total Strength is converted into a color adjusted by the user. The candlesticks in the chart will be presented with the calculated color.

If the Labels setting is enabled, each time the trend changes direction a label will appear indicating the new direction. The latest candlestick will always show the current trend with a label.

EMA = Exponential Moving Average

RSI = Relative Strength Index

ATR = Average True Range

🚩 UNIQUENESS

The main point that differentiates this indicator from others is it's simplicity and customization options. The indicator interprets trend and strength detection in it's own way, combining 3 different well-known trend detection methods: RSI, Supertrend & EMA Cross into one simple method. The algorithm is fully customizable and all styling options are adjustable for the user's liking.

⚙️ SETTINGS

1. General Configuration

Detection Length -> This setting determines the amount of candlesticks the indicator will look for trend detection. Higher settings may help the indicator find longer trends, while lower settings will help with finding smaller trends.

Smoothing -> Higher settings will result in longer periods of time required for trend to change direction from bullish to bearish and vice versa.

EMA Lengths -> You can enter two EMA Lengths here, the second one must be longer than the first one. When the shorter one crosses under the longer one, this will be a bearish sign, and if it crosses above it will be a bullish sign for the indicator.

Labels -> Enables / Disables trend strength labels.

Multiple Naked LevelsPURPOSE OF THE INDICATOR

This indicator autogenerates and displays naked levels and gaps of multiple types collected into one simple and easy to use indicator.

VALUE PROPOSITION OF THE INDICATOR AND HOW IT IS ORIGINAL AND USEFUL

1) CONVENIENCE : The purpose of this indicator is to offer traders with one coherent and robust indicator providing useful, valuable, and often used levels - in one place.

2) CLUSTERS OF CONFLUENCES : With this indicator it is easy to identify levels and zones on the chart with multiple confluences increasing the likelihood of a potential reversal zone.

THE TYPES OF LEVELS AND GAPS INCLUDED IN THE INDICATOR

The types of levels include the following:

1) PIVOT levels (Daily/Weekly/Monthly) depicted in the chart as: dnPIV, wnPIV, mnPIV.

2) POC (Point of Control) levels (Daily/Weekly/Monthly) depicted in the chart as: dnPoC, wnPoC, mnPoC.

3) VAH/VAL STD 1 levels (Value Area High/Low with 1 std) (Daily/Weekly/Monthly) depicted in the chart as: dnVAH1/dnVAL1, wnVAH1/wnVAL1, mnVAH1/mnVAL1

4) VAH/VAL STD 2 levels (Value Area High/Low with 2 std) (Daily/Weekly/Monthly) depicted in the chart as: dnVAH2/dnVAL2, wnVAH2/wnVAL2, mnVAH1/mnVAL2

5) FAIR VALUE GAPS (Daily/Weekly/Monthly) depicted in the chart as: dnFVG, wnFVG, mnFVG.

6) CME GAPS (Daily) depicted in the chart as: dnCME.

7) EQUILIBRIUM levels (Daily/Weekly/Monthly) depicted in the chart as dnEQ, wnEQ, mnEQ.

HOW-TO ACTIVATE LEVEL TYPES AND TIMEFRAMES AND HOW-TO USE THE INDICATOR

You can simply choose which of the levels to be activated and displayed by clicking on the desired radio button in the settings menu.

You can locate the settings menu by clicking into the Object Tree window, left-click on the Multiple Naked Levels and select Settings.

You will then get a menu of different level types and timeframes. Click the checkboxes for the level types and timeframes that you want to display on the chart.

You can then go into the chart and check out which naked levels that have appeared. You can then use those levels as part of your technical analysis.

The levels displayed on the chart can serve as additional confluences or as part of your overall technical analysis and indicators.

In order to back-test the impact of the different naked levels you can also enable tapped levels to be depicted on the chart. Do this by toggling the 'Show tapped levels' checkbox.

Keep in mind however that Trading View can not shom more than 500 lines and text boxes so the indocator will not be able to give you the complete history back to the start for long duration assets.

In order to clean up the charts a little bit there are two additional settings that can be used in the Settings menu:

- Selecting the price range (%) from the current price to be included in the chart. The default is 25%. That means that all levels below or above 20% will not be displayed. You can set this level yourself from 0 up to 100%.

- Selecting the minimum gap size to include on the chart. The default is 1%. That means that all gaps/ranges below 1% in price difference will not be displayed on the chart. You can set the minimum gap size yourself.

BASIC DESCRIPTION OF THE INNER WORKINGS OF THE INDICTATOR

The way the indicator works is that it calculates and identifies all levels from the list of levels type and timeframes above. The indicator then adds this level to a list of untapped levels.

Then for each bar after, it checks if the level has been tapped. If the level has been tapped or a gap/range completely filled, this level is removed from the list so that the levels displayed in the end are only naked/untapped levels.

Below is a descrition of each of the level types and how it is caluclated (algorithm):

PIVOT

Daily, Weekly and Monthly levels in trading refer to significant price points that traders monitor within the context of a single trading day. These levels can provide insights into market behavior and help traders make informed decisions regarding entry and exit points.

Traders often use D/W/M levels to set entry and exit points for trades. For example, entering long positions near support (daily close) or selling near resistance (daily close).

Daily levels are used to set stop-loss orders. Placing stops just below the daily close for long positions or above the daily close for short positions can help manage risk.

The relationship between price movement and daily levels provides insights into market sentiment. For instance, if the price fails to break above the daily high, it may signify bearish sentiment, while a strong breakout can indicate bullish sentiment.

The way these levels are calculated in this indicator is based on finding pivots in the chart on D/W/M timeframe. The level is then set to previous D/W/M close = current D/W/M open.

In addition, when price is going up previous D/W/M open must be smaller than previous D/W/M close and current D/W/M close must be smaller than the current D/W/M open. When price is going down the opposite.

POINT OF CONTROL

The Point of Control (POC) is a key concept in volume profile analysis, which is commonly used in trading.

It represents the price level at which the highest volume of trading occurred during a specific period.

The POC is derived from the volume traded at various price levels over a defined time frame. In this indicator the timeframes are Daily, Weekly, and Montly.

It identifies the price level where the most trades took place, indicating strong interest and activity from traders at that price.

The POC often acts as a significant support or resistance level. If the price approaches the POC from above, it may act as a support level, while if approached from below, it can serve as a resistance level. Traders monitor the POC to gauge potential reversals or breakouts.

The way the POC is calculated in this indicator is by an approximation by analysing intrabars for the respective timeperiod (D/W/M), assigning the volume for each intrabar into the price-bins that the intrabar covers and finally identifying the bin with the highest aggregated volume.

The POC is the price in the middle of this bin.

The indicator uses a sample space for intrabars on the Daily timeframe of 15 minutes, 35 minutes for the Weekly timeframe, and 140 minutes for the Monthly timeframe.

The indicator has predefined the size of the bins to 0.2% of the price at the range low. That implies that the precision of the calulated POC og VAH/VAL is within 0.2%.

This reduction of precision is a tradeoff for performance and speed of the indicator.

This also implies that the bigger the difference from range high prices to range low prices the more bins the algorithm will iterate over. This is typically the case when calculating the monthly volume profile levels and especially high volatility assets such as alt coins.

Sometimes the number of iterations becomes too big for Trading View to handle. In these cases the bin size will be increased even more to reduce the number of iterations.

In such cases the bin size might increase by a factor of 2-3 decreasing the accuracy of the Volume Profile levels.

Anyway, since these Volume Profile levels are approximations and since precision is traded for performance the user should consider the Volume profile levels(POC, VAH, VAL) as zones rather than pin point accurate levels.

VALUE AREA HIGH/LOW STD1/STD2

The Value Area High (VAH) and Value Area Low (VAL) are important concepts in volume profile analysis, helping traders understand price levels where the majority of trading activity occurs for a given period.

The Value Area High/Low is the upper/lower boundary of the value area, representing the highest price level at which a certain percentage of the total trading volume occurred within a specified period.

The VAH/VAL indicates the price point above/below which the majority of trading activity is considered less valuable. It can serve as a potential resistance/support level, as prices above/below this level may experience selling/buying pressure from traders who view the price as overvalued/undervalued

In this indicator the timeframes are Daily, Weekly, and Monthly. This indicator provides two boundaries that can be selected in the menu.

The first boundary is 70% of the total volume (=1 standard deviation from mean). The second boundary is 95% of the total volume (=2 standard deviation from mean).

The way VAH/VAL is calculated is based on the same algorithm as for the POC.

However instead of identifying the bin with the highest volume, we start from range low and sum up the volume for each bin until the aggregated volume = 30%/70% for VAL1/VAH1 and aggregated volume = 5%/95% for VAL2/VAH2.

Then we simply set the VAL/VAH equal to the low of the respective bin.

FAIR VALUE GAPS

Fair Value Gaps (FVG) is a concept primarily used in technical analysis and price action trading, particularly within the context of futures and forex markets. They refer to areas on a price chart where there is a noticeable lack of trading activity, often highlighted by a significant price movement away from a previous level without trading occurring in between.

FVGs represent price levels where the market has moved significantly without any meaningful trading occurring. This can be seen as a "gap" on the price chart, where the price jumps from one level to another, often due to a rapid market reaction to news, events, or other factors.

These gaps typically appear when prices rise or fall quickly, creating a space on the chart where no transactions have taken place. For example, if a stock opens sharply higher and there are no trades at the prices in between the two levels, it creates a gap. The areas within these gaps can be areas of liquidity that the market may return to “fill” later on.

FVGs highlight inefficiencies in pricing and can indicate areas where the market may correct itself. When the market moves rapidly, it may leave behind price levels that traders eventually revisit to establish fair value.

Traders often watch for these gaps as potential reversal or continuation points. Many traders believe that price will eventually “fill” the gap, meaning it will return to those price levels, providing potential entry or exit points.

This indicator calculate FVGs on three different timeframes, Daily, Weekly and Montly.

In this indicator the FVGs are identified by looking for a three-candle pattern on a chart, signalling a discrete imbalance in order volume that prompts a quick price adjustment. These gaps reflect moments where the market sentiment strongly leans towards buying or selling yet lacks the opposite orders to maintain price stability.

The indicator sets the gap to the difference from the high of the first bar to the low of the third bar when price is moving up or from the low of the first bar to the high of the third bar when price is moving down.

CME GAPS (BTC only)

CME gaps refer to price discrepancies that can occur in charts for futures contracts traded on the Chicago Mercantile Exchange (CME). These gaps typically arise from the fact that many futures markets, including those on the CME, operate nearly 24 hours a day but may have significant price movements during periods when the market is closed.

CME gaps occur when there is a difference between the closing price of a futures contract on one trading day and the opening price on the following trading day. This difference can create a "gap" on the price chart.

Opening Gaps: These usually happen when the market opens significantly higher or lower than the previous day's close, often influenced by news, economic data releases, or other market events occurring during non-trading hours.

Gaps can result from reactions to major announcements or developments, such as earnings reports, geopolitical events, or changes in economic indicators, leading to rapid price movements.

The importance of CME Gaps in Trading is the potential for Filling Gaps: Many traders believe that prices often "fill" gaps, meaning that prices may return to the gap area to establish fair value.

This can create potential trading opportunities based on the expectation of gap filling. Gaps can act as significant support or resistance levels. Traders monitor these levels to identify potential reversal points in price action.

The way the gap is identified in this indicator is by checking if current open is higher than previous bar close when price is moving up or if current open is lower than previous day close when price is moving down.

EQUILIBRIUM

Equilibrium in finance and trading refers to a state where supply and demand in a market balance each other, resulting in stable prices. It is a key concept in various economic and trading contexts. Here’s a concise description:

Market Equilibrium occurs when the quantity of a good or service supplied equals the quantity demanded at a specific price level. At this point, there is no inherent pressure for the price to change, as buyers and sellers are in agreement.

Equilibrium Price is the price at which the market is in equilibrium. It reflects the point where the supply curve intersects the demand curve on a graph. At the equilibrium price, the market clears, meaning there are no surplus goods or shortages.

In this indicator the equilibrium level is calculated simply by finding the midpoint of the Daily, Weekly, and Montly candles respectively.

NOTES

1) Performance. The algorithms are quite resource intensive and the time it takes the indicator to calculate all the levels could be 5 seconds or more, depending on the number of bars in the chart and especially if Montly Volume Profile levels are selected (POC, VAH or VAL).

2) Levels displayed vs the selected chart timeframe. On a timeframe smaller than the daily TF - both Daily, Weekly, and Monthly levels will be displayed. On a timeframe bigger than the daily TF but smaller than the weekly TF - the Weekly and Monthly levels will be display but not the Daily levels. On a timeframe bigger than the weekly TF but smaller than the monthly TF - only the Monthly levels will be displayed. Not Daily and Weekly.

CREDITS

The core algorithm for calculating the POC levels is based on the indicator "Naked Intrabar POC" developed by rumpypumpydumpy (https:www.tradingview.com/u/rumpypumpydumpy/).

The "Naked intrabar POC" indicator calculates the POC on the current chart timeframe.

This indicator (Multiple Naked Levels) adds two new features:

1) It calculates the POC on three specific timeframes, the Daily, Weekly, and Monthly timeframes - not only the current chart timeframe.

2) It adds functionaly by calculating the VAL and VAH of the volume profile on the Daily, Weekly, Monthly timeframes .

MarkdownUtilsLibrary "MarkdownUtils"

This library shows all of CommonMark's formatting elements that are currently (2024-03-30)

available in Pine Script® and gives some hints on how to use them.

The documentation will be in the tooltip of each of the following functions. It is also

logged into Pine Logs by default if it is called. We can disable the logging by setting `pLog = false`.

mediumMathematicalSpace()

Medium mathematical space that can be used in e.g. the library names like `Markdown Utils`.

Returns: The medium mathematical space character U+205F between those double quotes " ".

zeroWidthSpace()

Zero-width space.

Returns: The zero-width character U+200B between those double quotes "".

stableSpace(pCount)

Consecutive space characters in Pine Script® are replaced by a single space character on output.

Therefore we require a "stable" space to properly indent text e.g. in Pine Logs. To use it in code blocks

of a description like this one, we have to copy the 2(!) characters between the following reverse brackets instead:

# > <

Those are the zero-width character U+200B and a space.

Of course, this can also be used within a text to add some extra spaces.

Parameters:

pCount (simple int)

Returns: A zero-width space combined with a space character.

headers(pLog)

Headers

```

# H1

## H2

### H3

#### H4

##### H5

###### H6

```

*results in*

# H1

## H2

### H3

#### H4

##### H5

###### H6

*Best practices*: Add blank line before and after each header.

Parameters:

pLog (bool)

paragrahps(pLog)

Paragraphs

```

First paragraph

Second paragraph

```

*results in*

First paragraph

Second paragraph

Parameters:

pLog (bool)

lineBreaks(pLog)

Line breaks

```

First row

Second row

```

*results in*

First row\

Second row

Parameters:

pLog (bool)

emphasis(pLog)

Emphasis

With surrounding `*` and `~` we can emphasize text as follows. All emphasis can be arbitrarily combined.

```

*Italics*, **Bold**, ***Bold italics***, ~~Scratch~~

```

*results in*

*Italics*, **Bold**, ***Bold italics***, ~~Scratch~~

Parameters:

pLog (bool)

blockquotes(pLog)

Blockquotes

Lines starting with at least one `>` followed by a space and text build block quotes.

```

Text before blockquotes.

> 1st main blockquote

>

> 1st main blockquote

>

>> 1st 1-nested blockquote

>

>>> 1st 2-nested blockquote

>

>>>> 1st 3-nested blockquote

>

>>>>> 1st 4-nested blockquote

>

>>>>>> 1st 5-nested blockquote

>

>>>>>>> 1st 6-nested blockquote

>

>>>>>>>> 1st 7-nested blockquote

>

> 2nd main blockquote, 1st paragraph, 1st row\

> 2nd main blockquote, 1st paragraph, 2nd row

>

> 2nd main blockquote, 2nd paragraph, 1st row\

> 2nd main blockquote, 2nd paragraph, 2nd row

>

>> 2nd nested blockquote, 1st paragraph, 1st row\

>> 2nd nested blockquote, 1st paragraph, 2nd row

>

>> 2nd nested blockquote, 2nd paragraph, 1st row\

>> 2nd nested blockquote, 2nd paragraph, 2nd row

Text after blockquotes.

```

*results in*

Text before blockquotes.

> 1st main blockquote

>

>> 1st 1-nested blockquote

>

>>> 1st 2-nested blockquote

>

>>>> 1st 3-nested blockquote

>

>>>>> 1st 4-nested blockquote

>

>>>>>> 1st 5-nested blockquote

>

>>>>>>> 1st 6-nested blockquote

>

>>>>>>>> 1st 7-nested blockquote

>

> 2nd main blockquote, 1st paragraph, 1st row\

> 2nd main blockquote, 1st paragraph, 2nd row

>

> 2nd main blockquote, 2nd paragraph, 1st row\

> 2nd main blockquote, 2nd paragraph, 2nd row

>

>> 2nd nested blockquote, 1st paragraph, 1st row\

>> 2nd nested blockquote, 1st paragraph, 2nd row

>

>> 2nd nested blockquote, 2nd paragraph, 1st row\

>> 2nd nested blockquote, 2nd paragraph, 2nd row

Text after blockquotes.

*Best practices*: Add blank line before and after each (nested) blockquote.

Parameters:

pLog (bool)

lists(pLog)

Paragraphs

#### Ordered lists

The first line starting with a number combined with a delimiter `.` or `)` starts an ordered

list. The list's numbering starts with the given number. All following lines that also start

with whatever number and the same delimiter add items to the list.

#### Unordered lists

A line starting with a `-`, `*` or `+` becomes an unordered list item. All consecutive items with

the same start symbol build a separate list. Therefore every list can only have a single symbol.

#### General information

To start a new list either use the other delimiter or add some non-list text between.

List items in Pine Script® allow line breaks but cannot have paragraphs or blockquotes.

Lists Pine Script® cannot be nested.

```

1) 1st list, 1st item, 1st row\

1st list, 1st item, 2nd row

1) 1st list, 2nd item, 1st row\

1st list, 2nd item, 2nd row

1) 1st list, 2nd item, 1st row\

1st list, 2nd item, 2nd row

1. 2nd list, 1st item, 1st row\

2nd list, 1st item, 2nd row

Intermediary text.

1. 3rd list

Intermediary text (sorry, unfortunately without proper spacing).

8. 4th list, 8th item

8. 4th list, 9th item

Intermediary text.

- 1st list, 1st item

- 1st list, 2nd item

* 2nd list, 1st item

* 2nd list, 2nd item

Intermediary text.

+ 3rd list, 1st item

+ 3rd list, 2nd item

```

*results in*

1) 1st list, 1st item, 1st row\

1st list, 1st item, 2nd row

1) 1st list, 2nd item, 1st row\

1st list, 2nd item, 2nd row

1) 1st list, 2nd item, 1st row\

1st list, 2nd item, 2nd row

1. 2nd list, 1st item, 1st row\

2nd list, 1st item, 2nd row

Intermediary text.

1. 3rd list

Intermediary text (sorry, unfortunately without proper spacing).

8. 4th list, 8th item

8. 4th list, 9th item

Intermediary text.

- 1st list, 1st item

- 1st list, 2nd item

* 2nd list, 1st item

* 2nd list, 2nd item

Intermediary text.

+ 3rd list, 1st item

+ 3rd list, 2nd item

Parameters:

pLog (bool)

code(pLog)

### Code

`` `Inline code` `` is formatted like this.

To write above line we wrote `` `` `Inline code` `` ``.

And to write that line we added another pair of `` `` `` around that code and

a zero-width space of function between the inner `` `` ``.

### Code blocks

can be formatted like that:

~~~

```

export method codeBlock() =>

"code block"

```

~~~

Or like that:

```

~~~

export method codeBlock() =>

"code block"

~~~

```

To write ````` within a code block we can either surround it with `~~~`.

Or we "escape" those ````` by only the zero-width space of function (stableSpace) in between.

To escape \` within a text we use `` \` ``.

Parameters:

pLog (bool)

horizontalRules(pLog)

Horizontal rules

At least three connected `*`, `-` or `_` in a separate line build a horizontal rule.

```

Intermediary text.

---

Intermediary text.

***

Intermediary text.

___

Intermediary text.

```

*results in*

Intermediary text.

---

Intermediary text.

***

Intermediary text.

___

Intermediary text.

*Best practices*: Add blank line before and after each horizontal rule.

Parameters:

pLog (bool)

tables(pLog)

Tables

A table consists of a single header line with columns separated by `|`

and followed by a row of alignment indicators for either left (`---`, `:---`), centered (`:---:`) and right (`---:`)

A table can contain several rows of data.

The table can be written as follows but hasn't to be formatte like that. By adding (stableSpace)

on the correct side of the header we could even adjust the spacing if we don't like it as it is. Only around

the column separator we should only use a usual space on each side.

```

Header 1 | Header 1 | Header 2 | Header 3

--- | :--- | :----: | ---:

Left (Default) | Left | Centered | Right

Left (Default) | Left | Centered | Right

```

*results in*

Header 1 | Header 1 | Header 2 | Header 3

--- | :--- | :----: | ---:

Left (Default) | Left | Centered | Right

Left (Default) | Left | Centered | Right

Parameters:

pLog (bool)

links(pLog)

## Links.

### Inline-style

` (Here should be the link to the TradingView homepage)`\

results in (Here should be the link to the TradingView homepage)

` (Here should be the link to the TradingView homepage "Trading View tooltip")`\

results in (Here should be the link to the TradingView homepage "Trading View tooltip")

### Reference-style

One can also collect all links e.g. at the end of a description and use a reference to that as follows.

` `\

results in .

` `\

results in .

` `\

results in .

` (../tradingview/scripts/readme)`\

results in (../tradingview/scripts/readme).

### URLs and email

URLs are also identified by the protocol identifier, email addresses by `@`. They can also be surrounded by `<` and `>`.

Input | Result

--- | ---

`Here should be the link to the TradingView homepage` | Here should be the link to the TradingView homepage

`` |

`support@tradingview.com` | support@tradingview.com

`` |

## Images

We can display gif, jp(e)g and png files in our documentation, if we add `!` before a link.

### Inline-style:

`! (Here should be the link to the favicon of the TradingView homepage "Trading View icon")`

results in

! (Here should be the link to the favicon of the TradingView homepage "Trading View icon")\

### Reference-style:

`! `

results in

!

## References for reference-style links

Even though only the formatted references are visible here in the output, this text is also followed

by the following references with links in the style

` : Referenced link`

```

: Here should be the link to the TradingView homepage "Trading view text-reference tooltip"

: Here should be the link to the TradingView homepage "Trading view number-reference tooltip"

: Here should be the link to the TradingView homepage "Trading view self-reference tooltip"

: Here should be the link to the favicon of the TradingView homepage "Trading View icon (reference)"

```

: Here should be the link to the TradingView homepage "Trading view text-reference tooltip"

: Here should be the link to the TradingView homepage "Trading view number-reference tooltip"

: Here should be the link to the TradingView homepage "Trading view self-reference tooltip"

: Here should be the link to the favicon of the TradingView homepage "Trading View icon (reference)"

Parameters:

pLog (bool)

taskLists(pLog)

Task lists.

Other Markdown implementations can also display task lists for list items like `- ` respective `- `.

This can only be simulated by inline code `` ´ ` ``.

Make sure to either add a line-break `\` at the end of the line or a new paragraph by a blank line.

### Task lists

` ` Finish library

` ` Finish library

Parameters:

pLog (bool)

escapeMd(pLog)

Escaping Markdown syntax

To write and display Markdown syntax in regular text, we have to escape it. This can be done

by adding `\` before the Markdown syntax. If the Markdown syntax consists of more than one character

in some cases also the character of function can be helpful if a command consists of

more than one character if it is placed between the separate characters of the command.

Parameters:

pLog (bool)

test()

Calls all functions of above script.

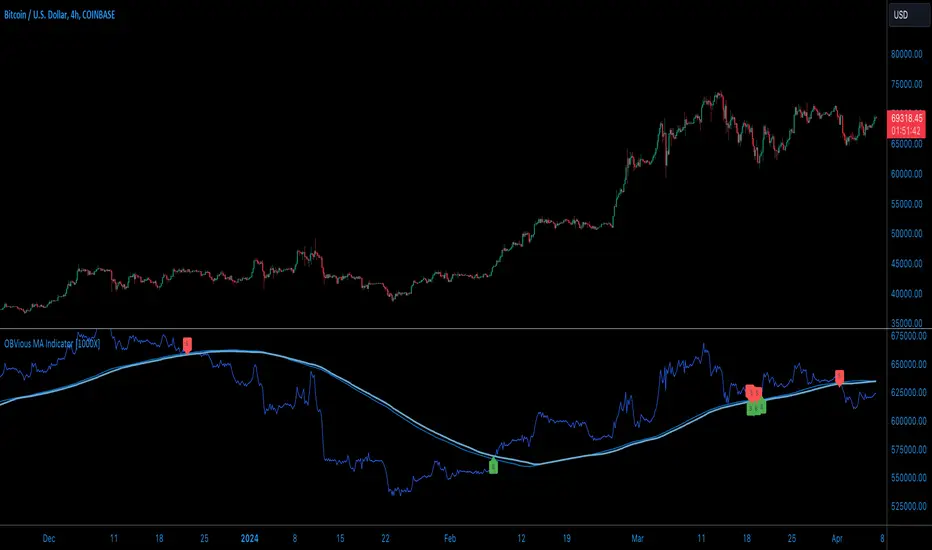

OBVious MA Indicator [1000X] On Balance Volume (OBV) is a gift to traders. OBV often provides a leading signal at the outset of a trend, when compression in the markets produces a surge in OBV prior to increased volatility.

This indicator demonstrates one method of utilizing OBV to your advantage. I call it the "OBVious MA Indicator ” only because it is simple in its mechanics. The primary utility of the OBVious MA indicator is as a volume confirmation filter that complements other components of a strategy.

Indicator Features:

• The Indicator revolves around the On Balance Volume indicator. OBV is a straightforward indicator: it registers a value by adding total volume traded on up candles, and subtracts total volume on down candles, generating a line by connecting those values. OBV was described in 1963 by Joe Granville in his book "Granville's New Key to Stock Market Profits” in which the author argues that OBV is the most vital key to success as a trader, with volume changes are a major predictor of price changes.

• Dual Moving Averages: here we use separate moving averages for entries and exits. This allows for more granular trade management; for example, one can either extend the length of the exit MA to hold positions longer, or shorten the MA for swifter exits, independently of the entry signals.

Execution: long trades are signalled when the OBV line crosses above the Long Entry Moving Average of the OBV. Long exits signals occur when the OBV line crosses under the Long Exit MA of the OBV. Shorts signal occur on a cross below the Short Entry MA, and exit signals come on a cross above the Short Exit MA.

Application:

While this indicator outlines entry and exit conditions based on OBV crossovers with designated moving averages, is is, as stated, best used in conjunction with a supporting cast of confirmatory indicators (feel free to drop me a note and tell me how you've used it). It can be used to confirm entries, or you might try using it as a sole exit indicator in a strategy.

Visualization:

The indicator includes conditional plotting of the OBV MAs, which plot based on the selected trading direction. This visualization aids in understanding how OBV interacts with the set moving averages.

Further Discussion:

We all know the importance of volume; this indicator demonstrates one simple yet effective method of incorporating the OBV for volume analysis. The OBV indicator can be used in many ways - for example, we can monitor OBV trend line breaks, look for divergences, or as we do here, watch for breaks of the moving average.

Despite its simplicity, I'm unaware of any previously published cases of this method. But the concept of applying MAs or EMAs to volume-based indicators like OBV is not uncommon in technical analysisIf, so I expect work like this has been done before. If you know of other similar indicators or strategies, please mention in the comments.

One comparable method uses EMAs of the OBV is QuantNomad’s "On Balance Volume Oscillator Strategy ”. That strategy uses a pair of EMAs on a normalized-range OBV-based oscillator. In that strategy, however, entry and exit signals occur on one EMA crossing the other, which places trades at distinctly different times than crossings of the OBV itself. Both are valid approaches with strength in simplicity.

Note: This is the indicator version of the Strategy found here .

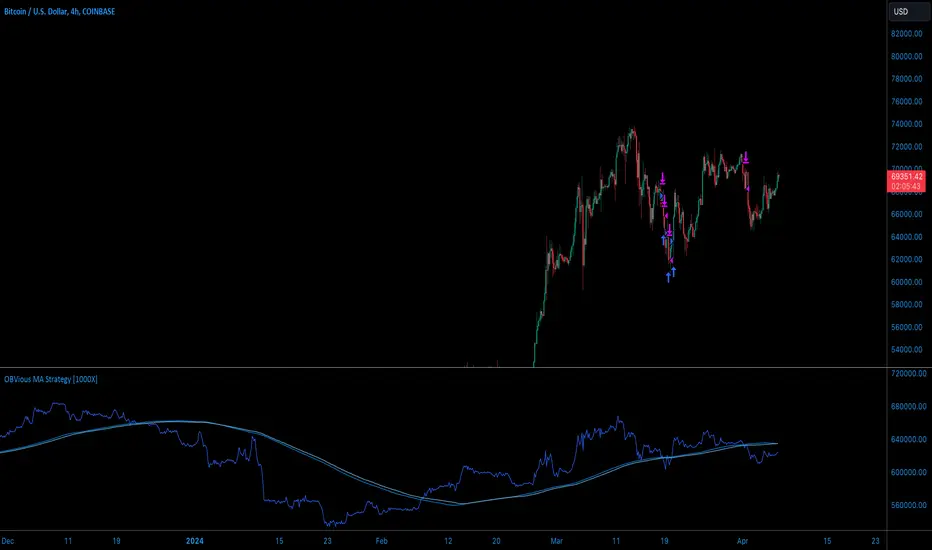

OBVious MA Strategy [1000X Trader]Exploring OBV: The OBVious MA Strategy

Are you using On Balance Volume (OBV) effectively? OBV is a gift to traders. OBV often provides a leading signal at the outset of a trend, when compression in the markets produces a surge in OBV prior to increased volatility.

This strategy demonstrates one method of utilizing OBV to your advantage. I call it the "OBVious MA Strategy ” only because it is so simple in its mechanics. This is meant to be a demonstration, not a strategy to utilize in live trading, as the primary utility of the OBVious MA indicator is as a volume confirmation filter that complements other components of a strategy. That said, I felt useful to present this indicator in isolation in this strategy to demonstrate the power it holds.

Strategy Features:

• OBV is the core signal: this strategy revolves around the On Balance Volume indicator. OBV is a straightforward indicator: it registers a value by adding total volume traded on up candles, and subtracts total volume on down candles, generating a line by connecting those values. OBV was described in 1963 by Joe Granville in his book "Granville's New Key to Stock Market Profits” in which the author argues that OBV is the most vital key to success as a trader, as volume changes are a major predictor of price changes.

• Dual Moving Averages: here we use separate moving averages for entries and exits. This allows for more granular trade management; for example, one can either extend the length of the exit MA to hold positions longer, or shorten the MA for swifter exits, independently of the entry signals.

Execution: long trades are taken when the OBV line crosses above the Long Entry Moving Average of the OBV. Long exits occur when the OBV line crosses under the Long Exit MA of the OBV. Shorts enter on a cross below the Short Entry MA, and exit on a cross above the Short Exit MA.

• Directional Trading: a direction filter can be set to "long" or "short," but not “both”, given that there is no trend filter in this strategy. When used in a bi-directional strategy with a trend filter, we add “both” to the script as a third option.

Application:

While this strategy outlines entry and exit conditions based on OBV crossovers with designated moving averages, is is, as stated, best used in conjunction with a supporting cast of confirmatory indicators (feel free to drop me a note and tell me how you've used it). It can be used to confirm entries, or you might try using it as a sole exit indicator in a strategy.

Visualization:

The strategy includes conditional plotting of the OBV MAs, which plot based on the selected trading direction. This visualization aids in understanding how OBV interacts with the set moving averages.

Further Discussion:

We all know the importance of volume; this strategy demonstrates one simple yet effective method of incorporating the OBV for volume analysis. The OBV indicator can be used in many ways - for example, we can monitor OBV trend line breaks, look for divergences, or as we do here, watch for breaks of the moving average.

Despite its simplicity, I'm unaware of any previously published cases of this method. The concept of applying MAs or EMAs to volume-based indicators like OBV is not uncommon in technical analysis, so I expect that work like this has been done before. If you know of other similar indicators or strategies, please mention in the comments.

One comparable strategy that uses EMAs of the OBV is QuantNomad’s "On Balance Volume Oscillator Strategy ", which uses a pair of EMAs on a normalized-range OBV-based oscillator. In that strategy, however, entries and exits occur on one EMA crossing the other, which places trades at distinctly different times than crossings of the OBV itself. Both are valid approaches with strength in simplicity.

Bearish Cassiopeia C Harmonic Patterns [theEccentricTrader]█ OVERVIEW

This indicator automatically detects and draws bearish Cassiopeia C harmonic patterns and price projections derived from the ranges that constitute the patterns.

Cassiopeia A, B and C harmonic patterns are patterns that I created/discovered myself. They are all inspired by the Cassiopeia constellation and each one is based on different rotations of the constellation as it moves through the sky. The range ratios are also based on the constellation's right ascension and declination listed on Wikipedia:

Right ascension 22h 57m 04.5897s–03h 41m 14.0997s

Declination 77.6923447°–48.6632690°

en.wikipedia.org

I actually developed this idea quite a while ago now but have not felt audacious enough to introduce a new harmonic pattern, let alone 3 at the same time! But I have since been able to run backtests on tick data going back to 2002 across a variety of market and timeframe combinations and have learned that the Cassiopeia patterns can certainly hold their own against the currently known harmonic patterns.

I would also point out that the Cassiopeia constellation does actually look like a harmonic pattern and the Cassiopeia A star is literally the 'strongest source of radio emission in the sky beyond the solar system', so its arguably more of a real harmonic phenomenon than the current patterns.

www.britannica.com

chandra.si.edu

█ CONCEPTS

Green and Red Candles

• A green candle is one that closes with a close price equal to or above the price it opened.

• A red candle is one that closes with a close price that is lower than the price it opened.

Swing Highs and Swing Lows

• A swing high is a green candle or series of consecutive green candles followed by a single red candle to complete the swing and form the peak.

• A swing low is a red candle or series of consecutive red candles followed by a single green candle to complete the swing and form the trough.

Peak and Trough Prices (Basic)

• The peak price of a complete swing high is the high price of either the red candle that completes the swing high or the high price of the preceding green candle, depending on which is higher.

• The trough price of a complete swing low is the low price of either the green candle that completes the swing low or the low price of the preceding red candle, depending on which is lower.

Historic Peaks and Troughs

The current, or most recent, peak and trough occurrences are referred to as occurrence zero. Previous peak and trough occurrences are referred to as historic and ordered numerically from right to left, with the most recent historic peak and trough occurrences being occurrence one.

Range

The range is simply the difference between the current peak and current trough prices, generally expressed in terms of points or pips.

Upper Trends

• A return line uptrend is formed when the current peak price is higher than the preceding peak price.

• A downtrend is formed when the current peak price is lower than the preceding peak price.

• A double-top is formed when the current peak price is equal to the preceding peak price.

Lower Trends

• An uptrend is formed when the current trough price is higher than the preceding trough price.

• A return line downtrend is formed when the current trough price is lower than the preceding trough price.

• A double-bottom is formed when the current trough price is equal to the preceding trough price.

Muti-Part Upper and Lower Trends

• A multi-part return line uptrend begins with the formation of a new return line uptrend and continues until a new downtrend ends the trend.

• A multi-part downtrend begins with the formation of a new downtrend and continues until a new return line uptrend ends the trend.

• A multi-part uptrend begins with the formation of a new uptrend and continues until a new return line downtrend ends the trend.

• A multi-part return line downtrend begins with the formation of a new return line downtrend and continues until a new uptrend ends the trend.

Double Trends

• A double uptrend is formed when the current trough price is higher than the preceding trough price and the current peak price is higher than the preceding peak price.

• A double downtrend is formed when the current peak price is lower than the preceding peak price and the current trough price is lower than the preceding trough price.

Muti-Part Double Trends

• A multi-part double uptrend begins with the formation of a new uptrend that proceeds a new return line uptrend, and continues until a new downtrend or return line downtrend ends the trend.

• A multi-part double downtrend begins with the formation of a new downtrend that proceeds a new return line downtrend, and continues until a new uptrend or return line uptrend ends the trend.

Wave Cycles

A wave cycle is here defined as a complete two-part move between a swing high and a swing low, or a swing low and a swing high. The first swing high or swing low will set the course for the sequence of wave cycles that follow; for example a chart that begins with a swing low will form its first complete wave cycle upon the formation of the first complete swing high and vice versa.

Figure 1.

Retracement and Extension Ratios

Retracement and extension ratios are calculated by dividing the current range by the preceding range and multiplying the answer by 100. Retracement ratios are those that are equal to or below 100% of the preceding range and extension ratios are those that are above 100% of the preceding range.

Fibonacci Retracement and Extension Ratios

The Fibonacci sequence is a series of numbers in which each number is the sum of the two preceding numbers, starting with 0 and 1. For example 0 + 1 = 1, 1 + 1 = 2, 1 + 2 = 3, and so on. Ultimately, we could go on forever but the first few numbers in the sequence are as follows: 0 , 1, 1, 2, 3, 5, 8, 13, 21, 34, 55, 89, 144.

The extension ratios are calculated by dividing each number in the sequence by the number preceding it. For example 0/1 = 0, 1/1 = 1, 2/1 = 2, 3/2 = 1.5, 5/3 = 1.6666..., 8/5 = 1.6, 13/8 = 1.625, 21/13 = 1.6153..., 34/21 = 1.6190..., 55/34 = 1.6176..., 89/55 = 1.6181..., 144/89 = 1.6179..., and so on. The retracement ratios are calculated by inverting this process and dividing each number in the sequence by the number proceeding it. For example 0/1 = 0, 1/1 = 1, 1/2 = 0.5, 2/3 = 0.666..., 3/5 = 0.6, 5/8 = 0.625, 8/13 = 0.6153..., 13/21 = 0.6190..., 21/34 = 0.6176..., 34/55 = 0.6181..., 55/89 = 0.6179..., 89/144 = 0.6180..., and so on.

1.618 is considered to be the 'golden ratio', found in many natural phenomena such as the growth of seashells and the branching of trees. Some now speculate the universe oscillates at a frequency of 0,618 Hz, which could help to explain such phenomena, but this theory has yet to be proven.

Traders and analysts use Fibonacci retracement and extension indicators, consisting of horizontal lines representing different Fibonacci ratios, for identifying potential levels of support and resistance. Fibonacci ranges are typically drawn from left to right, with retracement levels representing ratios inside of the current range and extension levels representing ratios extended outside of the current range. If the current wave cycle ends on a swing low, the Fibonacci range is drawn from peak to trough. If the current wave cycle ends on a swing high the Fibonacci range is drawn from trough to peak.

Harmonic Patterns

The concept of harmonic patterns in trading was first introduced by H.M. Gartley in his book "Profits in the Stock Market", published in 1935. Gartley observed that markets have a tendency to move in repetitive patterns, and he identified several specific patterns that he believed could be used to predict future price movements.

Since then, many other traders and analysts have built upon Gartley's work and developed their own variations of harmonic patterns. One such contributor is Larry Pesavento, who developed his own methods for measuring harmonic patterns using Fibonacci ratios. Pesavento has written several books on the subject of harmonic patterns and Fibonacci ratios in trading. Another notable contributor to harmonic patterns is Scott Carney, who developed his own approach to harmonic trading in the late 1990s and also popularised the use of Fibonacci ratios to measure harmonic patterns. Carney expanded on Gartley's work and also introduced several new harmonic patterns, such as the Shark pattern and the 5-0 pattern.

The bullish and bearish Gartley patterns are the oldest recognized harmonic patterns in trading and all the other harmonic patterns are ultimately modifications of the original Gartley patterns. Gartley patterns are fundamentally composed of 5 points, or 4 waves.

Bullish and Bearish Cassiopeia C Harmonic Patterns

• Bullish Cassiopeia C patterns are fundamentally composed of three troughs and two peaks. The second peak being higher than the first peak. And the third trough being lower than both the first and second troughs, while the second trough is higher than the first.

• Bearish Cassiopeia C patterns are fundamentally composed of three peaks and two troughs. The second trough being lower than the first trough. And the third peak being higher than both the first and second peaks, while the second peak is lower than the first.

The ratio measurements I use to detect the patterns are as follows:

• Wave 1 of the pattern, generally referred to as XA, has no specific ratio requirements.

• Wave 2 of the pattern, generally referred to as AB, should retrace by at least 11.34%, but no further than 22.31% of the range set by wave 1.

• Wave 3 of the pattern, generally referred to as BC, should extend by at least 225.7%, but no further than 341% of the range set by wave 2.

• Wave 4 of the pattern, generally referred to as CD, should retrace by at least 77.69%, but no further than 88.66% of the range set by wave 3.

Measurement Tolerances

In general, tolerance in measurements refers to the allowable variation or deviation from a specific value or dimension. It is the range within which a particular measurement is considered to be acceptable or accurate. In this script I have applied this concept to the measurement of harmonic pattern ratios to increase to the frequency of pattern occurrences.

For example, the AB measurement of Gartley patterns is generally set at around 61.8%, but with such specificity in the measuring requirements the patterns are very rare. We can increase the frequency of pattern occurrences by setting a tolerance. A tolerance of 10% to both downside and upside, which is the default setting for all tolerances, means we would have a tolerable measurement range between 51.8-71.8%, thus increasing the frequency of occurrence.

█ FEATURES

Inputs

• AB Lower Tolerance

• AB Upper Tolerance

• BC Lower Tolerance

• BC Upper Tolerance

• CD Lower Tolerance

• CD Upper Tolerance

• Pattern Color

• Label Color

• Show Projections

• Extend Current Projection Lines

Alerts

Users can set alerts for when the patterns occur.

█ LIMITATIONS

All green and red candle calculations are based on differences between open and close prices, as such I have made no attempt to account for green candles that gap lower and close below the close price of the preceding candle, or red candles that gap higher and close above the close price of the preceding candle. This may cause some unexpected behaviour on some markets and timeframes. I can only recommend using 24-hour markets, if and where possible, as there are far fewer gaps and, generally, more data to work with.

█ NOTES

I know a few people have been requesting a single indicator that contains all my patterns and I definitely hear you on that one. However, I have been very busy working on other projects while trying to trade and be a human at the same time. For now I am going to maintain my original approach of releasing each pattern individually so as to maintain consistency. But I am now also working on getting my some of my libraries ready for public release and in doing so I will finally be able to fit all patterns into one script. I will also be giving my scripts some TLC by making them cleaner once I have the libraries up and running. Please bear with me in the meantime, this may take a while. Cheers!

Bullish Cassiopeia C Harmonic Patterns [theEccentricTrader]█ OVERVIEW

This indicator automatically detects and draws bullish Cassiopeia C harmonic patterns and price projections derived from the ranges that constitute the patterns.

Cassiopeia A, B and C harmonic patterns are patterns that I created/discovered myself. They are all inspired by the Cassiopeia constellation and each one is based on different rotations of the constellation as it moves through the sky. The range ratios are also based on the constellation's right ascension and declination listed on Wikipedia:

Right ascension 22h 57m 04.5897s–03h 41m 14.0997s

Declination 77.6923447°–48.6632690°

en.wikipedia.org

I actually developed this idea quite a while ago now but have not felt audacious enough to introduce a new harmonic pattern, let alone 3 at the same time! But I have since been able to run backtests on tick data going back to 2002 across a variety of market and timeframe combinations and have learned that the Cassiopeia patterns can certainly hold their own against the currently known harmonic patterns.

I would also point out that the Cassiopeia constellation does actually look like a harmonic pattern and the Cassiopeia A star is literally the 'strongest source of radio emission in the sky beyond the solar system', so its arguably more of a real harmonic phenomenon than the current patterns.

www.britannica.com

chandra.si.edu

█ CONCEPTS

Green and Red Candles

• A green candle is one that closes with a close price equal to or above the price it opened.

• A red candle is one that closes with a close price that is lower than the price it opened.

Swing Highs and Swing Lows

• A swing high is a green candle or series of consecutive green candles followed by a single red candle to complete the swing and form the peak.

• A swing low is a red candle or series of consecutive red candles followed by a single green candle to complete the swing and form the trough.

Peak and Trough Prices (Basic)

• The peak price of a complete swing high is the high price of either the red candle that completes the swing high or the high price of the preceding green candle, depending on which is higher.

• The trough price of a complete swing low is the low price of either the green candle that completes the swing low or the low price of the preceding red candle, depending on which is lower.

Historic Peaks and Troughs

The current, or most recent, peak and trough occurrences are referred to as occurrence zero. Previous peak and trough occurrences are referred to as historic and ordered numerically from right to left, with the most recent historic peak and trough occurrences being occurrence one.

Range

The range is simply the difference between the current peak and current trough prices, generally expressed in terms of points or pips.

Upper Trends

• A return line uptrend is formed when the current peak price is higher than the preceding peak price.

• A downtrend is formed when the current peak price is lower than the preceding peak price.

• A double-top is formed when the current peak price is equal to the preceding peak price.

Lower Trends

• An uptrend is formed when the current trough price is higher than the preceding trough price.

• A return line downtrend is formed when the current trough price is lower than the preceding trough price.

• A double-bottom is formed when the current trough price is equal to the preceding trough price.

Muti-Part Upper and Lower Trends

• A multi-part return line uptrend begins with the formation of a new return line uptrend and continues until a new downtrend ends the trend.

• A multi-part downtrend begins with the formation of a new downtrend and continues until a new return line uptrend ends the trend.

• A multi-part uptrend begins with the formation of a new uptrend and continues until a new return line downtrend ends the trend.

• A multi-part return line downtrend begins with the formation of a new return line downtrend and continues until a new uptrend ends the trend.

Double Trends

• A double uptrend is formed when the current trough price is higher than the preceding trough price and the current peak price is higher than the preceding peak price.

• A double downtrend is formed when the current peak price is lower than the preceding peak price and the current trough price is lower than the preceding trough price.

Muti-Part Double Trends

• A multi-part double uptrend begins with the formation of a new uptrend that proceeds a new return line uptrend, and continues until a new downtrend or return line downtrend ends the trend.

• A multi-part double downtrend begins with the formation of a new downtrend that proceeds a new return line downtrend, and continues until a new uptrend or return line uptrend ends the trend.

Wave Cycles

A wave cycle is here defined as a complete two-part move between a swing high and a swing low, or a swing low and a swing high. The first swing high or swing low will set the course for the sequence of wave cycles that follow; for example a chart that begins with a swing low will form its first complete wave cycle upon the formation of the first complete swing high and vice versa.

Figure 1.

Retracement and Extension Ratios

Retracement and extension ratios are calculated by dividing the current range by the preceding range and multiplying the answer by 100. Retracement ratios are those that are equal to or below 100% of the preceding range and extension ratios are those that are above 100% of the preceding range.

Fibonacci Retracement and Extension Ratios

The Fibonacci sequence is a series of numbers in which each number is the sum of the two preceding numbers, starting with 0 and 1. For example 0 + 1 = 1, 1 + 1 = 2, 1 + 2 = 3, and so on. Ultimately, we could go on forever but the first few numbers in the sequence are as follows: 0 , 1, 1, 2, 3, 5, 8, 13, 21, 34, 55, 89, 144.

The extension ratios are calculated by dividing each number in the sequence by the number preceding it. For example 0/1 = 0, 1/1 = 1, 2/1 = 2, 3/2 = 1.5, 5/3 = 1.6666..., 8/5 = 1.6, 13/8 = 1.625, 21/13 = 1.6153..., 34/21 = 1.6190..., 55/34 = 1.6176..., 89/55 = 1.6181..., 144/89 = 1.6179..., and so on. The retracement ratios are calculated by inverting this process and dividing each number in the sequence by the number proceeding it. For example 0/1 = 0, 1/1 = 1, 1/2 = 0.5, 2/3 = 0.666..., 3/5 = 0.6, 5/8 = 0.625, 8/13 = 0.6153..., 13/21 = 0.6190..., 21/34 = 0.6176..., 34/55 = 0.6181..., 55/89 = 0.6179..., 89/144 = 0.6180..., and so on.

1.618 is considered to be the 'golden ratio', found in many natural phenomena such as the growth of seashells and the branching of trees. Some now speculate the universe oscillates at a frequency of 0,618 Hz, which could help to explain such phenomena, but this theory has yet to be proven.

Traders and analysts use Fibonacci retracement and extension indicators, consisting of horizontal lines representing different Fibonacci ratios, for identifying potential levels of support and resistance. Fibonacci ranges are typically drawn from left to right, with retracement levels representing ratios inside of the current range and extension levels representing ratios extended outside of the current range. If the current wave cycle ends on a swing low, the Fibonacci range is drawn from peak to trough. If the current wave cycle ends on a swing high the Fibonacci range is drawn from trough to peak.

Harmonic Patterns

The concept of harmonic patterns in trading was first introduced by H.M. Gartley in his book "Profits in the Stock Market", published in 1935. Gartley observed that markets have a tendency to move in repetitive patterns, and he identified several specific patterns that he believed could be used to predict future price movements.

Since then, many other traders and analysts have built upon Gartley's work and developed their own variations of harmonic patterns. One such contributor is Larry Pesavento, who developed his own methods for measuring harmonic patterns using Fibonacci ratios. Pesavento has written several books on the subject of harmonic patterns and Fibonacci ratios in trading. Another notable contributor to harmonic patterns is Scott Carney, who developed his own approach to harmonic trading in the late 1990s and also popularised the use of Fibonacci ratios to measure harmonic patterns. Carney expanded on Gartley's work and also introduced several new harmonic patterns, such as the Shark pattern and the 5-0 pattern.

The bullish and bearish Gartley patterns are the oldest recognized harmonic patterns in trading and all the other harmonic patterns are ultimately modifications of the original Gartley patterns. Gartley patterns are fundamentally composed of 5 points, or 4 waves.

Bullish and Bearish Cassiopeia C Harmonic Patterns

• Bullish Cassiopeia C patterns are fundamentally composed of three troughs and two peaks. The second peak being higher than the first peak. And the third trough being lower than both the first and second troughs, while the second trough is higher than the first.

• Bearish Cassiopeia C patterns are fundamentally composed of three peaks and two troughs. The second trough being lower than the first trough. And the third peak being higher than both the first and second peaks, while the second peak is lower than the first.

The ratio measurements I use to detect the patterns are as follows:

• Wave 1 of the pattern, generally referred to as XA, has no specific ratio requirements.

• Wave 2 of the pattern, generally referred to as AB, should retrace by at least 11.34%, but no further than 22.31% of the range set by wave 1.

• Wave 3 of the pattern, generally referred to as BC, should extend by at least 225.7%, but no further than 341% of the range set by wave 2.

• Wave 4 of the pattern, generally referred to as CD, should retrace by at least 77.69%, but no further than 88.66% of the range set by wave 3.

Measurement Tolerances

In general, tolerance in measurements refers to the allowable variation or deviation from a specific value or dimension. It is the range within which a particular measurement is considered to be acceptable or accurate. In this script I have applied this concept to the measurement of harmonic pattern ratios to increase to the frequency of pattern occurrences.

For example, the AB measurement of Gartley patterns is generally set at around 61.8%, but with such specificity in the measuring requirements the patterns are very rare. We can increase the frequency of pattern occurrences by setting a tolerance. A tolerance of 10% to both downside and upside, which is the default setting for all tolerances, means we would have a tolerable measurement range between 51.8-71.8%, thus increasing the frequency of occurrence.

█ FEATURES

Inputs

• AB Lower Tolerance

• AB Upper Tolerance

• BC Lower Tolerance

• BC Upper Tolerance

• CD Lower Tolerance

• CD Upper Tolerance

• Pattern Color

• Label Color

• Show Projections

• Extend Current Projection Lines

Alerts

Users can set alerts for when the patterns occur.

█ LIMITATIONS

All green and red candle calculations are based on differences between open and close prices, as such I have made no attempt to account for green candles that gap lower and close below the close price of the preceding candle, or red candles that gap higher and close above the close price of the preceding candle. This may cause some unexpected behaviour on some markets and timeframes. I can only recommend using 24-hour markets, if and where possible, as there are far fewer gaps and, generally, more data to work with.

█ NOTES

I know a few people have been requesting a single indicator that contains all my patterns and I definitely hear you on that one. However, I have been very busy working on other projects while trying to trade and be a human at the same time. For now I am going to maintain my original approach of releasing each pattern individually so as to maintain consistency. But I am now also working on getting my some of my libraries ready for public release and in doing so I will finally be able to fit all patterns into one script. I will also be giving my scripts some TLC by making them cleaner once I have the libraries up and running. Please bear with me in the meantime, this may take a while. Cheers!

Bearish Cassiopeia B Harmonic Patterns [theEccentricTrader]█ OVERVIEW

This indicator automatically detects and draws bearish Cassiopeia B harmonic patterns and price projections derived from the ranges that constitute the patterns.

Cassiopeia A, B and C harmonic patterns are patterns that I created/discovered myself. They are all inspired by the Cassiopeia constellation and each one is based on different rotations of the constellation as it moves through the sky. The range ratios are also based on the constellation's right ascension and declination listed on Wikipedia:

Right ascension 22h 57m 04.5897s–03h 41m 14.0997s

Declination 77.6923447°–48.6632690°

en.wikipedia.org

I actually developed this idea quite a while ago now but have not felt audacious enough to introduce a new harmonic pattern, let alone 3 at the same time! But I have since been able to run backtests on tick data going back to 2002 across a variety of market and timeframe combinations and have learned that the Cassiopeia patterns can certainly hold their own against the currently known harmonic patterns.

I would also point out that the Cassiopeia constellation does actually look like a harmonic pattern and the Cassiopeia A star is literally the 'strongest source of radio emission in the sky beyond the solar system', so its arguably more of a real harmonic phenomenon than the current patterns.

www.britannica.com

chandra.si.edu

█ CONCEPTS

Green and Red Candles

• A green candle is one that closes with a close price equal to or above the price it opened.

• A red candle is one that closes with a close price that is lower than the price it opened.

Swing Highs and Swing Lows

• A swing high is a green candle or series of consecutive green candles followed by a single red candle to complete the swing and form the peak.

• A swing low is a red candle or series of consecutive red candles followed by a single green candle to complete the swing and form the trough.

Peak and Trough Prices (Basic)

• The peak price of a complete swing high is the high price of either the red candle that completes the swing high or the high price of the preceding green candle, depending on which is higher.

• The trough price of a complete swing low is the low price of either the green candle that completes the swing low or the low price of the preceding red candle, depending on which is lower.

Historic Peaks and Troughs

The current, or most recent, peak and trough occurrences are referred to as occurrence zero. Previous peak and trough occurrences are referred to as historic and ordered numerically from right to left, with the most recent historic peak and trough occurrences being occurrence one.

Range

The range is simply the difference between the current peak and current trough prices, generally expressed in terms of points or pips.

Upper Trends

• A return line uptrend is formed when the current peak price is higher than the preceding peak price.

• A downtrend is formed when the current peak price is lower than the preceding peak price.

• A double-top is formed when the current peak price is equal to the preceding peak price.

Lower Trends

• An uptrend is formed when the current trough price is higher than the preceding trough price.

• A return line downtrend is formed when the current trough price is lower than the preceding trough price.

• A double-bottom is formed when the current trough price is equal to the preceding trough price.

Muti-Part Upper and Lower Trends

• A multi-part return line uptrend begins with the formation of a new return line uptrend and continues until a new downtrend ends the trend.

• A multi-part downtrend begins with the formation of a new downtrend and continues until a new return line uptrend ends the trend.

• A multi-part uptrend begins with the formation of a new uptrend and continues until a new return line downtrend ends the trend.

• A multi-part return line downtrend begins with the formation of a new return line downtrend and continues until a new uptrend ends the trend.

Double Trends

• A double uptrend is formed when the current trough price is higher than the preceding trough price and the current peak price is higher than the preceding peak price.

• A double downtrend is formed when the current peak price is lower than the preceding peak price and the current trough price is lower than the preceding trough price.

Muti-Part Double Trends

• A multi-part double uptrend begins with the formation of a new uptrend that proceeds a new return line uptrend, and continues until a new downtrend or return line downtrend ends the trend.

• A multi-part double downtrend begins with the formation of a new downtrend that proceeds a new return line downtrend, and continues until a new uptrend or return line uptrend ends the trend.

Wave Cycles

A wave cycle is here defined as a complete two-part move between a swing high and a swing low, or a swing low and a swing high. The first swing high or swing low will set the course for the sequence of wave cycles that follow; for example a chart that begins with a swing low will form its first complete wave cycle upon the formation of the first complete swing high and vice versa.

Figure 1.

Retracement and Extension Ratios

Retracement and extension ratios are calculated by dividing the current range by the preceding range and multiplying the answer by 100. Retracement ratios are those that are equal to or below 100% of the preceding range and extension ratios are those that are above 100% of the preceding range.

Fibonacci Retracement and Extension Ratios

The Fibonacci sequence is a series of numbers in which each number is the sum of the two preceding numbers, starting with 0 and 1. For example 0 + 1 = 1, 1 + 1 = 2, 1 + 2 = 3, and so on. Ultimately, we could go on forever but the first few numbers in the sequence are as follows: 0 , 1, 1, 2, 3, 5, 8, 13, 21, 34, 55, 89, 144.

The extension ratios are calculated by dividing each number in the sequence by the number preceding it. For example 0/1 = 0, 1/1 = 1, 2/1 = 2, 3/2 = 1.5, 5/3 = 1.6666..., 8/5 = 1.6, 13/8 = 1.625, 21/13 = 1.6153..., 34/21 = 1.6190..., 55/34 = 1.6176..., 89/55 = 1.6181..., 144/89 = 1.6179..., and so on. The retracement ratios are calculated by inverting this process and dividing each number in the sequence by the number proceeding it. For example 0/1 = 0, 1/1 = 1, 1/2 = 0.5, 2/3 = 0.666..., 3/5 = 0.6, 5/8 = 0.625, 8/13 = 0.6153..., 13/21 = 0.6190..., 21/34 = 0.6176..., 34/55 = 0.6181..., 55/89 = 0.6179..., 89/144 = 0.6180..., and so on.

1.618 is considered to be the 'golden ratio', found in many natural phenomena such as the growth of seashells and the branching of trees. Some now speculate the universe oscillates at a frequency of 0,618 Hz, which could help to explain such phenomena, but this theory has yet to be proven.

Traders and analysts use Fibonacci retracement and extension indicators, consisting of horizontal lines representing different Fibonacci ratios, for identifying potential levels of support and resistance. Fibonacci ranges are typically drawn from left to right, with retracement levels representing ratios inside of the current range and extension levels representing ratios extended outside of the current range. If the current wave cycle ends on a swing low, the Fibonacci range is drawn from peak to trough. If the current wave cycle ends on a swing high the Fibonacci range is drawn from trough to peak.

Harmonic Patterns

The concept of harmonic patterns in trading was first introduced by H.M. Gartley in his book "Profits in the Stock Market", published in 1935. Gartley observed that markets have a tendency to move in repetitive patterns, and he identified several specific patterns that he believed could be used to predict future price movements.

Since then, many other traders and analysts have built upon Gartley's work and developed their own variations of harmonic patterns. One such contributor is Larry Pesavento, who developed his own methods for measuring harmonic patterns using Fibonacci ratios. Pesavento has written several books on the subject of harmonic patterns and Fibonacci ratios in trading. Another notable contributor to harmonic patterns is Scott Carney, who developed his own approach to harmonic trading in the late 1990s and also popularised the use of Fibonacci ratios to measure harmonic patterns. Carney expanded on Gartley's work and also introduced several new harmonic patterns, such as the Shark pattern and the 5-0 pattern.

The bullish and bearish Gartley patterns are the oldest recognized harmonic patterns in trading and all the other harmonic patterns are ultimately modifications of the original Gartley patterns. Gartley patterns are fundamentally composed of 5 points, or 4 waves.

Bullish and Bearish Cassiopeia B Harmonic Patterns

• Bullish Cassiopeia B patterns are fundamentally composed of three troughs and two peaks. The second peak being lower than the first peak. And the third trough being lower than both the first and second troughs, while the second trough is also lower than the first.

• Bearish Cassiopeia B patterns are fundamentally composed of three peaks and two troughs. The second trough being higher than the first trough. And the third peak being higher than both the first and second peaks, while the second peak is also higher than the first.

The ratio measurements I use to detect the patterns are as follows:

• Wave 1 of the pattern, generally referred to as XA, has no specific ratio requirements.

• Wave 2 of the pattern, generally referred to as AB, should retrace by at least 11.34%, but no further than 22.31% of the range set by wave 1.

• Wave 3 of the pattern, generally referred to as BC, should extend by at least 225.7%, but no further than 341% of the range set by wave 2.

• Wave 4 of the pattern, generally referred to as CD, should retrace by at least 77.69%, but no further than 88.66% of the range set by wave 3.

Measurement Tolerances

In general, tolerance in measurements refers to the allowable variation or deviation from a specific value or dimension. It is the range within which a particular measurement is considered to be acceptable or accurate. In this script I have applied this concept to the measurement of harmonic pattern ratios to increase to the frequency of pattern occurrences.

For example, the AB measurement of Gartley patterns is generally set at around 61.8%, but with such specificity in the measuring requirements the patterns are very rare. We can increase the frequency of pattern occurrences by setting a tolerance. A tolerance of 10% to both downside and upside, which is the default setting for all tolerances, means we would have a tolerable measurement range between 51.8-71.8%, thus increasing the frequency of occurrence.

█ FEATURES

Inputs

• AB Lower Tolerance

• AB Upper Tolerance

• BC Lower Tolerance

• BC Upper Tolerance

• CD Lower Tolerance

• CD Upper Tolerance

• Pattern Color

• Label Color

• Show Projections

• Extend Current Projection Lines

Alerts

Users can set alerts for when the patterns occur.

█ LIMITATIONS

All green and red candle calculations are based on differences between open and close prices, as such I have made no attempt to account for green candles that gap lower and close below the close price of the preceding candle, or red candles that gap higher and close above the close price of the preceding candle. This may cause some unexpected behaviour on some markets and timeframes. I can only recommend using 24-hour markets, if and where possible, as there are far fewer gaps and, generally, more data to work with.

█ NOTES

I know a few people have been requesting a single indicator that contains all my patterns and I definitely hear you on that one. However, I have been very busy working on other projects while trying to trade and be a human at the same time. For now I am going to maintain my original approach of releasing each pattern individually so as to maintain consistency. But I am now also working on getting my some of my libraries ready for public release and in doing so I will finally be able to fit all patterns into one script. I will also be giving my scripts some TLC by making them cleaner once I have the libraries up and running. Please bear with me in the meantime, this may take a while. Cheers!

Bullish Cassiopeia B Harmonic Patterns [theEccentricTrader]█ OVERVIEW

This indicator automatically detects and draws bullish Cassiopeia B harmonic patterns and price projections derived from the ranges that constitute the patterns.