SMT Divergence x outofoptions🔍 SMT Divergence — Advanced Market Correlation Analysis

This was created with and approved by @outofoptions to bring you smaller SMTs based on his original SMT Divergence indicator

SMT Divergence is a sophisticated technical analysis indicator designed to identify high-probability reversal and continuation signals through intelligent correlation analysis between related markets. This powerful tool reveals hidden market dynamics by comparing price action divergences across correlated instruments, providing traders with institutional-level market insight.

🎯 Core Capabilities:

Multi-Market Analysis : Automatically compares your chart with a correlated instrument to identify divergence patterns and market inefficiencies

Smart Liquidity Detection : Advanced algorithms identify key liquidity levels and sweep patterns for enhanced signal accuracy

Dynamic Divergence Mapping : Real-time visualization of bullish and bearish divergences with customizable line styles and colors

Intelligent Signal Validation : Optional candle-based confirmation system to filter high-probability setups from noise

Automated Line Management : Smart removal of invalidated divergences to maintain clean, actionable chart analysis

📊 Professional Features:

The SMT Divergence indicator excels at revealing market structure imbalances that often precede significant price movements. By analyzing the relationship between correlated markets, it identifies when institutional money may be positioned differently than retail sentiment suggests, providing early warning signals for potential reversals.

⚙️ Advanced Customization:

Flexible correlation pair selection for any market combination

Customizable visual styling with multiple line types and color schemes

Adjustable validation criteria for different trading styles

Professional alert system with detailed message customization

Automatic cleanup of broken or invalidated divergences

🎨 Visual Excellence:

Clean, professional line drawing with customizable styling

Dynamic labeling system with size and color options

Real-time divergence tracking and management

Institutional-grade chart presentation

Optimized performance for extended analysis periods

📈 Ideal For:

Swing traders seeking high-probability reversal signals

Multi-market analysts comparing correlated instruments

Institutional-style traders using correlation analysis

Advanced technical analysts studying market structure

Those seeking early warning signals for trend changes

🔔 Smart Alerts:

Comprehensive alert system with customizable messaging allows you to stay informed of new divergences across multiple timeframes and market sessions, ensuring you never miss critical market developments.

💡 Market Intelligence:

SMT Divergence transforms complex inter-market relationships into clear, actionable signals, giving you the same analytical edge used by professional trading institutions to identify market turning points before they become obvious to retail traders.

Educational Tool: This indicator is designed for educational and analytical purposes. Divergence analysis requires understanding of market correlation principles. Always combine with proper risk management and additional analysis methods.

"liquidity" için komut dosyalarını ara

ICT Concepts Toolkit [TWS]

ICT Concepts Toolkit – by Trade With Stevie

Unlock the full power of Inner Circle Trader (ICT) concepts with this all-in-one indicator built for serious traders.

The ICT Concepts Toolkit combines the most powerful price action tools into one clean, efficient, and highly customizable interface — perfect for mastering market structure and timing precision entries.

✅ Features Included:

🟩 Order Blocks – Automatically detect key institutional levels for potential reversals and entries.

📉 Fair Value Gaps (FVGs) – Visualize imbalances in price action to spot high-probability targets and mitigation zones.

📊 Support & Resistance – Dynamically plotted levels to track market structure and trend shifts in real-time.

📅 Previous Daily Highs/Lows – Key liquidity zones marked for precision scalping and swing setups.

🕒 Session Zones – Clearly defined Asian, London, and New York sessions with customizable times and colors.

📌 Extension Lines – Extends each session’s high and low to the current candle for ongoing bias and liquidity mapping.

🚦ICT Morning Signal – Your personal directional bias assistant: smart signals showing when to Buy or Sell based on ICT’s powerful Morning Model logic.

Whether you're trading Forex, Futures, or Crypto — this toolkit gives you a cleaner chart, clearer bias, and more confidence in your setups.

💡 Created by Trade With Stevie — follow for more smart tools and signal insights.

Ultimate Market Structure [Alpha Extract]Ultimate Market Structure

A comprehensive market structure analysis tool that combines advanced swing point detection, imbalance zone identification, and intelligent break analysis to identify high-probability trading opportunities.Utilizing a sophisticated trend scoring system, this indicator classifies market conditions and provides clear signals for structure breaks, directional changes, and fair value gap detection with institutional-grade precision.

🔶 Advanced Swing Point Detection

Identifies pivot highs and lows using configurable lookback periods with optional close-based analysis for cleaner signals. The system automatically labels swing points as Higher Highs (HH), Lower Highs (LH), Higher Lows (HL), and Lower Lows (LL) while providing advanced classifications including "rising_high", "falling_high", "rising_low", "falling_low", "peak_high", and "valley_low" for nuanced market analysis.

swingHighPrice = useClosesForStructure ? ta.pivothigh(close, swingLength, swingLength) : ta.pivothigh(high, swingLength, swingLength)

swingLowPrice = useClosesForStructure ? ta.pivotlow(close, swingLength, swingLength) : ta.pivotlow(low, swingLength, swingLength)

classification = classifyStructurePoint(structureHighPrice, upperStructure, true)

significance = calculateSignificance(structureHighPrice, upperStructure, true)

🔶 Significance Scoring System

Each structure point receives a significance level on a 1-5 scale based on its distance from previous points, helping prioritize the most important levels. This intelligent scoring system ensures traders focus on the most meaningful structure breaks while filtering out minor noise.

🔶 Comprehensive Trend Analysis

Calculates momentum, strength, direction, and confidence levels using volatility-normalized price changes and multi-timeframe correlation. The system provides real-time trend state tracking with bullish (+1), bearish (-1), or neutral (0) direction assessment and 0-100 confidence scoring.

// Calculate trend momentum using rate of change and volatility

calculateTrendMomentum(lookback) =>

priceChange = (close - close ) / close * 100

avgVolatility = ta.atr(lookback) / close * 100

momentum = priceChange / (avgVolatility + 0.0001)

momentum

// Calculate trend strength using multiple timeframe correlation

calculateTrendStrength(shortPeriod, longPeriod) =>

shortMA = ta.sma(close, shortPeriod)

longMA = ta.sma(close, longPeriod)

separation = math.abs(shortMA - longMA) / longMA * 100

strength = separation * slopeAlignment

❓How It Works

🔶 Imbalance Zone Detection

Identifies Fair Value Gaps (FVGs) between consecutive candles where price gaps create unfilled areas. These zones are displayed as semi-transparent boxes with optional center line mitigation tracking, highlighting potential support and resistance levels where institutional players often react.

// Detect Fair Value Gaps

detectPriceImbalance() =>

currentHigh = high

currentLow = low

refHigh = high

refLow = low

if currentOpen > currentClose

if currentHigh - refLow < 0

upperBound = currentClose - (currentClose - refLow)

lowerBound = currentClose - (currentClose - currentHigh)

centerPoint = (upperBound + lowerBound) / 2

newZone = ImbalanceZone.new(

zoneBox = box.new(bar_index, upperBound, rightEdge, lowerBound,

bgcolor=bullishImbalanceColor, border_color=hiddenColor)

)

🔶 Structure Break Analysis

Determines Break of Structure (BOS) for trend continuation and Directional Change (DC) for trend reversals with advanced classification as "continuation", "reversal", or "neutral". The system compares pre-trend and post-trend states for each break, providing comprehensive trend change momentum analysis.

🔶 Intelligent Zone Management

Features partial mitigation tracking when price enters but doesn't fully fill zones, with automatic zone boundary adjustment during partial fills. Smart array management keeps only recent structure points for optimal performance while preventing duplicate signals from the same level.

🔶 Liquidity Zone Detection

Automatically identifies potential liquidity zones at key structure points for institutional trading analysis. The system tracks broken structure points and provides adaptive zone extension with configurable time-based limits for imbalance areas.

🔶 Visual Structure Mapping

Provides clear visual indicators including swing labels with color-coded significance levels, dashed lines connecting break points with BOS/DC labels, and break signals for continuation and reversal patterns. The adaptive zones feature smart management with automatic mitigation tracking.

🔶 Market Structure Interpretation

HH/HL patterns indicate bullish market structure with trend continuation likelihood, while LH/LL patterns signal bearish structure with downtrend continuation expected. BOS signals represent structure breaks in trend direction for continuation opportunities, while DC signals warn of potential reversals.

🔶 Performance Optimization

Automatic cleanup of old structure points (keeps last 8 points), recent break tracking (keeps last 5 break events), and efficient array management ensure smooth performance across all timeframes and market conditions.

Why Choose Ultimate Market Structure ?

This indicator provides traders with institutional-grade market structure analysis, combining multiple analytical approaches into one comprehensive tool. By identifying key structure levels, imbalance zones, and break patterns with advanced significance scoring, it helps traders understand market dynamics and position themselves for high-probability trade setups in alignment with smart money concepts. The sophisticated trend scoring system and intelligent zone management make it an essential tool for any serious trader looking to decode market structure with precision and confidence.

Apex Edge - VantageApex Edge – Vantage

Quarter-Wick Reversal System | Price Action Based | Non-Repainting | Visual Confirmation Tool

Overview:

Apex Edge – Vantage is a precision price action indicator built to assist traders in identifying high-probability reversal entries — not based on indicators, but on how candles behave at their extremes.

This tool implements a clean, repeatable framework that reflects how I personally trade:

Spot a candle that closes with strong directional intent,

Then wait for a controlled pullback into the outer quarter,

And strike — only if price respects that line.

There’s no magic here — just raw, tactical logic visualized clearly on your chart. It's not designed to predict the market — it's built to respond when price offers you Vantage.

Core Logic:

Dot Detection – Final Quarter Close Candles

A green dot prints below a bullish candle if it closes within the top 25% of its wick-to-wick range.

A red dot prints above a bearish candle if it closes within the bottom 25% of its range.

These dots signify candles that made a strong, deliberate move in one direction — where price was pushed to an extreme and held that extreme into the close. These candles often signal institutional intent or momentum imbalance.

Entry Confirmation – Controlled Wick Rebalance

On the very next candle only, price must wick into the prior dot candle's outer quarter — but must not pass beyond it.

For buy entries, the wick must enter the bottom 25% of the previous green dot candle, but not dip below it.

For sell entries, the wick must reach into the top 25% of the red dot candle, but not exceed it.

This wick into the quarter is seen as a controlled rebalancing — a tactical reaction back into the origin zone before potential continuation.

Arrow Printing – Visual Entry Signal

Once the entry criteria are confirmed, an arrow is printed after the candle closes.

This arrow continues to print on each new candle as long as price does not violate the original entry zone — giving visual confirmation that the trade thesis is still valid.

If price breaks above/below the quarter range, the arrow disappears.

This ongoing confirmation is useful for staying in trades, managing risk, or spotting failed setups early.

Automatic Stop Loss Level

A horizontal Stop Loss line is drawn from the extreme wick of the original dot candle.

For buy entries, SL is placed below the green dot candle's low.

For sell entries, SL is placed above the red dot candle's high.

This provides immediate risk context — perfect for traders using limit orders or looking to scale in.

Coding Logic:

This script uses plotshape() and plot() functions for all visual elements.

Dot candles are identified using quarter-range logic via:

pinescript

Copy

Edit

close >= high - (high - low) * 0.25 // for bullish

close <= low + (high - low) * 0.25 // for bearish

Entry validation logic triggers only on the next candle, using:

pinescript

Copy

Edit

low >= quarterLine and low <= high // for buy entries

high <= quarterLine and high >= low // for sell entries

Arrows and SL lines are plotted only on closed candles, ensuring non-repainting behavior.

alertcondition() is used for real-time alerts on valid buy/sell triggers.

How I Personally Use It:

I wait for a dot to print — this shows directional conviction.

On the next candle, I watch for a tap into the outer quarter.

If the wick meets the criteria and the candle closes, I’ll execute manually at the close of that candle.

As long as the arrow remains on the chart, I know the setup hasn’t been invalidated.

I combine this with market structure, session timing, and liquidity context to build confluence around each trade.

Alerts Included:

Buy Entry Alert: When a green arrow prints (entry confirmed)

Sell Entry Alert: When a red arrow prints (entry confirmed)

These fire once per confirmed signal, allowing you to react in real-time or automate if desired.

Who This Is For:

Manual traders who want clean price-based entries

Anyone who uses market structure, SMC, or liquidity concepts

Traders looking to replace indicators with pure candle logic

Discretionary or semi-systematic traders who want visual tools to guide their decisions

Final Word

Apex Edge – Vantage doesn’t predict price — it shows you where price is offering you control.

This is a surgical tool designed to help you act only when the market gives you a measurable edge — and to stay in the trade as long as that edge holds.

If you're ready to stop chasing trades and start striking from a position of Vantage, then this tool belongs on your chart.

Supply/Demand Market Structure (SMA Multi-Timeframe)Supply/Demand Based Market Structure

Structure + Order Blocks from Synthetic SMA Candles

Overview:

The SMA Supply/Demand Market Structure indicator combines market structure analysis with supply/demand logic, powered by SMA-based synthetic candles . Instead of relying on raw candle data, this tool generates smoothed higher-timeframe candles using simple moving averages to identify more stable zones and cleaner structure shifts.

It detects bullish and bearish breaks of structure (BoS) , highlights swing points like HH, HL, LH, LL , and plots institutional-style supply and demand zones formed from aggressive rallies or drops. The result is a precise and noise-filtered view of market intent, perfect for trend-following or smart money strategies.

How It Works:

- Synthetic candles are created using SMA of OHLC values on your selected timeframe (HTF).

- A bullish break occurs when price closes above the high of the last bearish synthetic candle.

- A bearish break occurs when price closes below the low of the last bullish synthetic candle.

- Upon break confirmation:

- A demand zone is drawn using the last bearish candle.

- A supply zone is drawn using the last bullish candle.

- Each zone is extended forward for a user-defined number of bars and optionally deleted upon mitigation.

- Zigzag-based internal structure connects valid swing points and classifies them as HH, HL, LH, LL , including Liquidity Sweeps (LS) .

- BoS levels are highlighted with lines that automatically reset when new structure forms.

Key Features:

- Synthetic SMA Candles : Smooth and reliable structure from average-based HTF candles

- Break Modes : Choose between raw HTF closes or SMA closes for break logic

- Custom Timeframe Selection : Analyze structure across any HTF you choose

- Dynamic Supply/Demand Zones : Auto-plot boxes from valid rallies/drops

- Mitigation Detection : Optionally fade or delete zones when price trades through

- Zigzag Structure Mapping : Automatically connect structural highs/lows

- BoS Detection : Real-time breakout of swing points with visual confirmation

- Smart Labels : Marks HH, HL, LH, LL, and LS directly on the chart

- Multi-timeframe Alert System : Notify for all structural changes, BoS, and new zones

How to Use:

- Set your desired HTF and SMA Length for synthetic candle smoothing.

- Use SMA=1 for raw candles

- Select a Break Mode :

- Raw Close : Uses standard HTF close values

- SMA Close : Uses smoothed closes from SMA

- Watch for bullish or bearish breaks — zones are plotted when price confirms breakout structure.

- Use demand zones as long entry areas and supply zones as short setups on retests.

- Rely on internal shifts and zigzag swings to monitor structure continuity.

- Enable alerts for swing formations, BoS, and liquidity sweeps to trade hands-free.

Recommended Strategies:

- Smart Money & ICT Models : Use synthetic demand/supply + BoS for mitigation or continuation plays

- Swing Trading : Align with higher timeframe structure and use zones for entry triggers

- Trend Trading : Confirm structure alignment and wait for pullbacks into zones

- Reversal Entries : Trade structure breaks when zones fail and a BoS confirms the shift

Customization Options:

- Timeframe input for custom HTF control

- SMA Length to adjust candle smoothing

- Zone Style : Control zone color, transparency, and duration

- Structure Display : Toggle swing labels and zigzag visuals

- Alert Mode : Choose between LTF, MTF, or HTF alerts

Summary:

SMA Supply/Demand Market Structure provides a clean, flexible view of price structure and institutional intent by fusing market structure with SMA-based synthetic candles. It’s ideal for anyone seeking reduced noise, visually guided entries, and rule-based trading based on structural shifts and real-time demand/supply dynamics.

Ralph Indicator - ZaraTrust Smart MoneyThe Ralph Indicator – ZaraTrust Smart Money is a powerful yet simple Smart Money Concepts (SMC) based tool designed for traders who want to trade like institutions. It auto-detects high-probability Buy/Sell zones, Support/Resistance levels, and Demand/Supply areas on the chart — giving you clear, visual, and actionable signals without the clutter.

⸻

🔍 Key Features:

✅ Smart Money Structure

• Uses pivot-based logic to identify potential structure points

• Helps you understand market flow (e.g., BOS, CHoCH simplified logic)

✅ Automatic Support & Resistance

• Plots major levels based on significant highs and lows

• Helps catch key reversal or breakout zones

✅ Demand & Supply Zones

• Visually shows areas where price may react strongly

• Based on smart pivot detection from recent swings

✅ Buy/Sell Trade Signals

• Highlights buy when price breaks resistance (possible bullish shift)

• Highlights sell when price breaks support (possible bearish shift)

✅ Clean & Easy UI

• Toggle features on/off from settings panel

• Labels and shapes are plotted clearly on the chart for instant reading

⸻

🛠️ Recommended Use:

• Use on 15min to 4H timeframe for intraday or swing trading

• Combine with price action (e.g., confirmation candles, liquidity grab)

• Works best when paired with institutional logic (OBs, FVG, liquidity)

⸻

⚠️ Disclaimer:

This indicator is a tool, not a signal service.

It does not guarantee 98% accuracy, but it’s designed to highlight smart money zones and high-probability areas. Always do your own risk management and backtest before using on a live account.

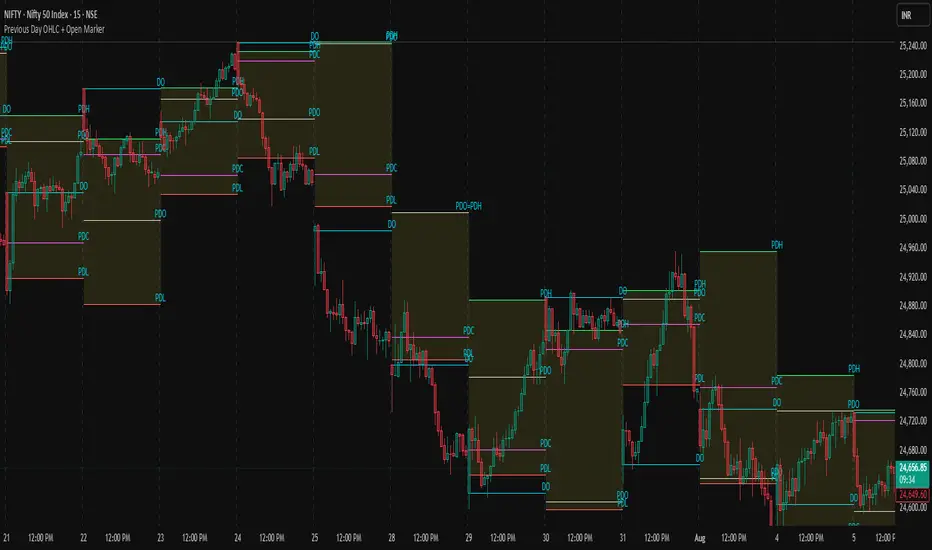

Previous Day OHLC + Open MarkerPrevious Day OHLC + Open Marker

This indicator is designed to help traders quickly identify the most important price levels from the previous trading session and today’s open. It provides a clean and configurable overlay of the previous day’s OHLC (Open, High, Low, Close) along with the current day's opening price, making it easy to spot price reactions, liquidity sweeps, and confluence zones.

📌 Key Features

✅ Previous Day OHLC Lines

Plots horizontal lines for High (H), Low (L), Open (O), and Close (C) from the previous session

Each line is independently toggleable

Fully customizable in color, transparency, and thickness

✅ Today's Session Open (DO)

Marks the current day's opening price

Helps identify directional bias, trend/momentum shifts, or mean-reversion points

✅ Minimalist Labels for Clarity

Text-only labels like H, L, O, C, and DO — no bulky label boxes

Color-matched to each line for visual simplicity

Optional display to keep charts clean

✅ Session-Based Highlight Zone

Optionally highlights the area between the previous day’s High and Low with a shaded box

Useful for identifying the day’s value area or range breakouts

✅ Smart Alerts

Receive alerts when price crosses any of the levels: PDH, PDL, PDO, PDC, or Today’s Open

Helps you catch key interactions without watching the chart constantly

🧠 Ideal For

Intraday traders using VWAP, order blocks, or liquidity concepts

Swing traders who want to see how current price relates to prior structure

Scalpers looking for clean levels to enter fades, reversals, or breakouts

Anyone applying institutional trading concepts (PDH/PDL sweeps, FVGs, BPRs, etc.)

⚙️ Customization Options

Toggle each level (H/L/O/C/DO) individually

Show or hide labels and highlight zone

Customize color, line thickness, and transparency

Clean layout — no line extensions across the entire chart

🧼 Design Philosophy

This script was created for clarity, speed, and minimalism. It avoids clutter while preserving all the crucial context price action traders need. Labels are informative but unobtrusive, and alerts help automate level tracking.

🛠 Built with Pine Script v5

🔔 Alerts Included

📊 Optimized for both intraday and swing trading

📦 Lightweight and modular by design

Alt Szn Oracle - Institutional GradeThe Alt Szn Oracle is a macro-level indicator built to help traders front-run altseason by tracking liquidity, dominance rotation, sentiment, and capital flows—all in one signal. It’s designed for those who don’t just chase pumps, but want to understand when the tide is turning and why. This tool doesn't predict specific coin breakouts—it tells you when the market as a whole is gearing up to rotate into higher beta assets like altcoins, including memes and microcaps.

The index consolidates ten macro inputs into a normalized, smoothed score from 0–100. These include Bitcoin and Ethereum dominance, ETH/BTC, altcoin market cap (Total3), relative volume flows, and stablecoin supply (USDT, USDC, DAI)—which act as proxies for risk-on appetite and dry powder entering the system. It also incorporates manually updated sentiment metrics from Google Trends and the Fear & Greed Index, giving it a behavioral edge that most indicators lack.

The logic is simple but powerful: when BTC dominance is falling, ETH/BTC is rising, altcoin volume increases relative to BTC/ETH, and stablecoins start moving—you're likely in the early innings of rotation. The index is also filtered through a volatility threshold and smoothed with an EMA to eliminate chop and fakeouts.

Use this indicator on macro charts like TOTAL3, TOTAL2, or ETHBTC to gauge market health, or overlay it on specific coins like PEPE, DOGE, or SOL to confirm if the tide is in your favor. Interpreting the score is straightforward: readings above 80 suggest euphoria and signal it’s time to de-risk, 60–80 indicates expansion and confirms altseason is underway, 40–60 is neutral, and 20–40 is a capitulation zone where smart money accumulates.

What sets this apart is that it doesn’t just track price—it reflects the flow of capital, the positioning of liquidity, and the sentiment of the crowd. Most altseason indicators are lagging, overfitted, or too simplistic. This one is modular, forward-looking, and grounded in real capital rotation theory.

If you're a trader who wants to time the cycle, not guess it, this is your tool. Refine it, fork it, or expand it to your niche—DeFi, NFTs, meme coins, or L1s. It’s a framework for reading the macro winds, not a signal service. Use it with discipline, and you’ll catch the wave while others drown in noise.

Fair Value Gap Profiles [AlgoAlpha]🟠 OVERVIEW

This script draws and manages Fair Value Gap (FVG) zones by detecting unfilled gaps in price action and then augmenting them with intra-gap volume profiles from a lower timeframe. It is designed to help traders find potential areas where price may return to fill liquidity voids, and to provide extra detail about volume distribution inside each gap to assess strength and likely mitigation. The script automatically tracks each gap, updates its state over time, and can show which gaps are still unfilled or have been mitigated.

🟠 CONCEPTS

A Fair Value Gap is a zone between candles where no trades occurred, often seen as an inefficiency that price later revisits. The script checks each bar to see if a bullish (low above 2-bars-ago high) or bearish (high below 2-bars-ago low) gap has formed, and measures whether the gap’s size exceeds a threshold defined by a volatility-adjusted multiplier of past gap widths (to only detect significantly large gaps). Once a qualified gap is found, it gets recorded and visualized with a box that can stretch forward in time until filled. To add more context, a mini volume profile is built from a lower timeframe’s price and volume data, showing how volume is distributed inside the gap. The lowest-volume subzone is also highlighted using a sliding window scan method to visualise the true gap (area with least trading activity)

🟠 FEATURES

Visual gap boxes that appear automatically when bullish or bearish fair value gaps are detected on the chart.

Color-coded zones showing bullish gaps in one color and bearish gaps in another so you can easily see which side the gap favors.

Volume profile histograms plotted inside each gap using data from a lower timeframe, helping you see where volume concentrated inside the gap area.

Highlight of the lowest-volume subzone within each gap so you can spot areas price may target when filling the gap.

Dynamic extension of the gap boxes across the chart until price comes back and fills them, marking them as mitigated.

Customizable colors and transparency settings for gap boxes, profiles, and low-volume highlights to match your chart style.

Alerts that notify you when a new gap is created or when price fills an existing gap.

🟠 USAGE

This indicator helps you find and track unfilled price gaps that often act as magnets for price to revisit. You can use it to spot areas where liquidity may rest and plan entries or exits around these zones.

The colored gap boxes show you exactly where a fair value gap starts and ends, so you can anticipate potential pullbacks or continuations when price approaches them.

The intra-gap volume profile lets you gauge whether the gap was created on strong or thin participation, which can help judge how likely it is to be filled. The highlighted lowest-volume subzone shows where price might accelerate once inside the gap.

Traders often look for entries when price returns to a gap, aiming for a reaction or reversal in that area. You can also combine the mitigation alerts with your trade management to track when gaps have been closed and adjust your bias accordingly. Overall, the tool gives a clear visual reference for imbalance zones that can help structure trades around supply and demand dynamics.

First FVG📘 Indicator Description (English)

First FVG – NY Open is a TradingView indicator designed to automatically identify the first Fair Value Gap (FVG) that appears during the New York session, following the ICT (Inner Circle Trader) methodology.

It highlights institutional inefficiencies in price caused by imbalanced price action and helps traders spot high-probability entry zones, especially after the 9:30 AM EST (New York Open).

⚙️ How It Works

Session time: The indicator scans for FVGs starting at 9:32 AM (allowing 3 candles after the NY Open to form).

FVG Conditions:

Bullish FVG: When the high of 2 candles ago is lower than the low of the current candle and the middle candle is bullish.

Bearish FVG: When the low of 2 candles ago is higher than the high of the current candle and the middle candle is bearish.

Only the first FVG per session is drawn, as taught by ICT for setups like Judas Swing or NY Reversal models.

A colored box is drawn to represent the FVG zone.

A dotted horizontal line (CE) is drawn at the midpoint of the FVG box (Consequent Encroachment), a key level watched by smart money traders.

A dashed vertical line is drawn at 9:30 NY time to mark the open.

🧠 How to Use It

Wait for the NY Open (9:30 AM EST) – the indicator becomes active at 9:32 AM.

Watch for the first FVG box of the day. This is often a high-probability reaction zone.

Use the CE line (center of the FVG) as a reference for entries, rejections, or liquidity grabs.

Combine with market structure, PD Arrays, and liquidity concepts as taught by ICT for confluence.

The FVG box and CE line will extend forward for several candles for visual clarity.

🎛️ Customizable Settings

Session time (default: 09:32–16:00 NY)

FVG box color (up/down)

Text color

Max number of days to keep boxes on chart

Option to show or hide the 9:30 NY Open vertical line

Position Size Calculator with Fees# Position Size Calculator with Portfolio Management - Manual

## Overview

The Position Size Calculator with Portfolio Management is an advanced Pine Script indicator designed to help traders calculate optimal position sizes based on their total portfolio value and risk management strategy. This tool automatically calculates your risk amount based on portfolio allocation percentages and determines the exact position size needed while accounting for trading fees.

## Key Features

- **Portfolio-Based Risk Management**: Calculates risk based on total portfolio value

- **Tiered Risk Allocation**: Separates trading allocation from total portfolio

- **Automatic Trade Direction Detection**: Determines long/short based on entry vs stop loss

- **Fee Integration**: Accounts for trading fees in position size calculations

- **Risk Factor Adjustment**: Allows scaling of position size up or down

- **Visual Display**: Shows all calculations in a clear, color-coded table

- **Automatic Risk Calculation**: No need to manually input risk amount

## Input Parameters

### Total Portfolio ($)

- **Purpose**: The total value of your investment portfolio

- **Default**: 0.0

- **Range**: Any positive value

- **Step**: 0.01

- **Example**: If your total portfolio is worth $100,000, enter 100000

### Trading Portfolio Allocation (%)

- **Purpose**: The percentage of your total portfolio allocated to active trading

- **Default**: 20.0%

- **Range**: 0.0% to 100.0%

- **Step**: 0.01

- **Example**: If you allocate 20% of your portfolio to trading, enter 20

### Risk from Trading (%)

- **Purpose**: The percentage of your trading allocation you're willing to risk per trade

- **Default**: 0.1%

- **Range**: Any positive value

- **Step**: 0.01

- **Example**: If you risk 0.1% of your trading allocation per trade, enter 0.1

### Entry Price ($)

- **Purpose**: The price at which you plan to enter the trade

- **Default**: 0.0

- **Range**: Any positive value

- **Step**: 0.01

### Stop Loss ($)

- **Purpose**: The price at which you will exit if the trade goes against you

- **Default**: 0.0

- **Range**: Any positive value

- **Step**: 0.01

### Risk Factor

- **Purpose**: A multiplier to scale your position size up or down

- **Default**: 1.0 (no scaling)

- **Range**: 0.0 to 10.0

- **Step**: 0.1

- **Examples**:

- 1.0 = Normal position size

- 2.0 = Double the position size

- 0.5 = Half the position size

### Fee (%)

- **Purpose**: The percentage fee charged per transaction

- **Default**: 0.01% (0.01)

- **Range**: 0.0% to 1.0%

- **Step**: 0.001

## How Risk Amount is Calculated

The script automatically calculates your risk amount using this formula:

```

Risk Amount = Total Portfolio × Trading Allocation (%) × Risk % ÷ 10,000

```

### Example Calculation:

- Total Portfolio: $100,000

- Trading Allocation: 20%

- Risk per Trade: 0.1%

**Risk Amount = $100,000 × 20 × 0.1 ÷ 10,000 = $20**

This means you would risk $20 per trade, which is 0.1% of your $20,000 trading allocation.

## Portfolio Structure Example

Let's say you have a $100,000 portfolio:

### Allocation Structure:

- **Total Portfolio**: $100,000

- **Trading Allocation (20%)**: $20,000

- **Long-term Investments (80%)**: $80,000

### Risk Management:

- **Risk per Trade (0.1% of trading)**: $20

- **Maximum trades at risk**: Could theoretically have 1,000 trades before risking entire trading allocation

## How Position Size is Calculated

### Trade Direction Detection

- **Long Trade**: Entry price > Stop loss price

- **Short Trade**: Entry price < Stop loss price

### Position Size Formulas

#### For Long Trades:

```

Position Size = -Risk Factor × Risk Amount / (Stop Loss × (1 - Fee) - Entry Price × (1 + Fee))

```

#### For Short Trades:

```

Position Size = -Risk Factor × Risk Amount / (Entry Price × (1 - Fee) - Stop Loss × (1 + Fee))

```

## Output Display

The indicator displays a comprehensive table with color-coded sections:

### Portfolio Information (Light Blue Background)

- **Portfolio (USD)**: Your total portfolio value

- **Trading Portfolio Allocation (%)**: Percentage allocated to trading

- **Risk as % of Trading**: Risk percentage per trade

### Trade Setup (Gray Background)

- **Entry Price**: Your specified entry price

- **Stop Loss**: Your specified stop loss price

- **Fee (%)**: Trading fee percentage

- **Risk Factor**: Position size multiplier

### Risk Analysis (Red Background)

- **Risk Amount**: Automatically calculated dollar risk

- **Effective Entry**: Actual entry cost including fees

- **Effective Exit**: Actual exit value including fees

- **Expected Loss**: Calculated loss if stop loss is hit

- **Deviation from Risk %**: Accuracy of risk calculation

### Final Result (Blue Background)

- **Position Size**: Number of shares/units to trade

## Usage Examples

### Example 1: Conservative Long Trade

- **Total Portfolio**: $50,000

- **Trading Allocation**: 15%

- **Risk per Trade**: 0.05%

- **Entry Price**: $25.00

- **Stop Loss**: $24.00

- **Risk Factor**: 1.0

- **Fee**: 0.01%

**Calculated Risk Amount**: $50,000 × 15% × 0.05% ÷ 100 = $3.75

### Example 2: Aggressive Short Trade

- **Total Portfolio**: $200,000

- **Trading Allocation**: 30%

- **Risk per Trade**: 0.2%

- **Entry Price**: $150.00

- **Stop Loss**: $155.00

- **Risk Factor**: 2.0

- **Fee**: 0.01%

**Calculated Risk Amount**: $200,000 × 30% × 0.2% ÷ 100 = $120

**Actual Risk**: $120 × 2.0 = $240 (due to risk factor)

## Color Coding System

- **Green/Red Header**: Trade direction (Long/Short)

- **Light Blue**: Portfolio management parameters

- **Gray**: Trade setup parameters

- **Red**: Risk-related calculations and results

- **Blue**: Final position size result

## Best Practices

### Portfolio Management

1. **Keep trading allocation reasonable** (typically 10-30% of total portfolio)

2. **Use conservative risk percentages** (0.05-0.2% per trade)

3. **Don't risk more than you can afford to lose**

### Risk Management

1. **Start with small risk factors** (1.0 or less) until comfortable

2. **Monitor your total exposure** across all open positions

3. **Adjust risk based on market conditions**

### Trade Execution

1. **Always validate calculations** before placing trades

2. **Account for slippage** in volatile markets

3. **Consider position size relative to liquidity**

## Risk Management Guidelines

### Conservative Approach

- Trading Allocation: 10-20%

- Risk per Trade: 0.05-0.1%

- Risk Factor: 0.5-1.0

### Moderate Approach

- Trading Allocation: 20-30%

- Risk per Trade: 0.1-0.15%

- Risk Factor: 1.0-1.5

### Aggressive Approach

- Trading Allocation: 30-40%

- Risk per Trade: 0.15-0.25%

- Risk Factor: 1.5-2.0

## Troubleshooting

### Common Issues

1. **Position Size shows 0**

- Verify all portfolio inputs are greater than 0

- Check that entry price differs from stop loss

- Ensure calculated risk amount is positive

2. **Very small position sizes**

- Increase risk percentage or risk factor

- Check if your risk amount is too small for the price difference

3. **Large risk deviation**

- Normal for very small positions

- Consider adjusting entry/stop loss levels

### Validation Checklist

- Total portfolio value is realistic

- Trading allocation percentage makes sense

- Risk percentage is conservative

- Entry and stop loss prices are valid

- Trade direction matches your intention

## Advanced Features

### Risk Factor Usage

- **Scaling up**: Use risk factors > 1.0 for high-confidence trades

- **Scaling down**: Use risk factors < 1.0 for uncertain trades

- **Never exceed**: Risk factors that would risk more than your comfort level

### Multiple Timeframe Analysis

- Use different risk factors for different timeframes

- Consider correlation between positions

- Adjust trading allocation based on market conditions

## Disclaimer

This tool is for educational and planning purposes only. Always verify calculations manually and consider market conditions, liquidity, and correlation between positions. The automated risk calculation assumes you're comfortable with the mathematical relationship between portfolio allocation and individual trade risk. Past performance doesn't guarantee future results, and all trading involves risk of loss.

Fair Value Gap [Custom]📌 FVG Indicator – Smart Money Concepts Tool

This script is based on Smart Money Concepts (SMC) and automatically detects and marks Fair Value Gaps (FVG) on the chart, helping traders identify unbalanced price areas left behind by institutional moves.

🧠 What is an FVG?

An FVG (Fair Value Gap) is the price gap formed when the market moves rapidly, leaving behind a candle range where no trading occurred — typically between Candle 1’s high and Candle 3’s low (in a three-candle pattern). These gaps often signal imbalance, created during structural breaks or liquidity grabs, and may act as retrace zones or entry points.

🛠 Features:

✅ Automatically detects and highlights FVG zones (high-low range)

✅ Differentiates between open (unfilled) and closed (filled) FVGs

✅ Adjustable timeframe settings (works best on 1H–4H charts)

✅ Option to toggle display of filled FVGs

✅ Great for identifying pullback entries, continuation zones, or reversal setups

💡 Recommended Use:

After BOS/CHoCH, watch for price to return to the FVG for entry

Combine with Order Blocks and liquidity zones for higher accuracy

Best used as part of an ICT or SMC-based trading system

Sweep + BOS (Lines + First Confirmed Only)🔍 Indicator: Sweep + BOS (Break of Structure with Visual Lines)

🧠 Overview

This indicator combines Swing detection, Liquidity Sweeps, and Break of Structure (BOS) logic, with:

Customizable swing length,

BOS signals only after confirmed sweeps,

BOS shown only once per sweep,

Visual labels and connecting lines to highlight structure breaks clearly.

⚙️ Inputs

Swing Length:

Defines how many candles to use to identify a swing high/low. Must be an odd number (e.g., 3, 5, 7...).

Sweep Lookback Window:

Sets how far back the script checks for a sweep (false breakout over a swing).

BOS Validity After Sweep:

Number of bars within which a BOS can be considered valid after a sweep.

Toggle Options:

Show/hide:

Swing Labels

Sweep Labels

BOS Labels

BOS Connecting Lines

📌 Logic Breakdown

✅ Swings

Swing High: A candle’s high is greater than the highs of all N candles on both sides.

Swing Low: A candle’s low is lower than the lows of all N candles on both sides.

💧 Liquidity Sweeps

Sweep High:

Price spikes above a previous Swing High,

Then closes back below it (false breakout).

Sweep Low:

Price drops below a previous Swing Low,

Then closes back above it.

🔁 Break of Structure (BOS)

A BOS is only shown if:

It occurs after a valid sweep (within X bars),

It hasn’t been already plotted for that sweep,

BOS ↑ is only possible after Sweep Low,

BOS ↓ is only possible after Sweep High,

Opposite BOS type resets the last BOS state.

BOS ↑ (Bullish):

Confirmed when price closes above previous Swing High after Sweep Low.

Label appears at the candle low.

A line is drawn from the Swing Low to the BOS candle.

BOS ↓ (Bearish):

Confirmed when price closes below previous Swing Low after Sweep High.

Label appears at the candle high.

A line is drawn from the Swing High to the BOS candle.

Simple Market Kill-Zones + Open (UTC)What it does

This Pine v6 indicator highlights the “kill-zones” around the big session opens—Asian (23:00–03:00 UTC), London (07:00–09:00 UTC) and New York (13:30–15:30 UTC)—by reading each bar’s actual UTC timestamp. It also draws dashed vertical lines at exactly 23:00, 07:00 and 13:30 UTC, so you never miss the liquidity ramps. Because it uses raw UTC hours/minutes, it stays accurate even when exchanges pause (e.g. Nano-BTC’s daily halt) or your chart’s display timezone changes.

Key Inputs

Show Asia/London/NY Kill Zone – toggle each shaded band on/off

Zone Colors – pick your own semi-transparent hues

Show Session-Open Lines – enable dashed verticals at the exact open times

Line Colors – customize the line opacity and style

How to use

Apply on your favorite timeframe (15 min–1 h is a sweet spot).

Toggle the zones you care about and pick readable colors.

Use the dashed lines as entry triggers or as visual bookmarks.

In your own Pine strategies, wrap order logic with the zone booleans to only trade when liquidity’s alive.

Thursday High & Friday Low Breakout (Safe)This TradingView Pine Script indicator is designed to help traders visually track two key situational breakout patterns that occur across the Thursday–Monday trading window. Specifically, it detects:

Whether the high of Thursday has been taken out on Friday, and

Whether the low of Friday has been breached on Monday.

These conditions are based on commonly observed market behaviors where key highs and lows from the previous days often act as liquidity targets or decision points. By identifying these events, traders can better understand the unfolding market structure and anticipate potential follow-through or reversals.

The script stores Thursday's high and Friday's low at the close of each respective day and evaluates the breakout conditions in real-time as new bars are printed. When Friday’s price action exceeds Thursday’s high, an upward-pointing green triangle is plotted above the bar. Conversely, when Monday’s price breaks below Friday’s low, a red downward triangle is plotted below the bar.

Unlike scripts that rely on label.new (which can create compatibility issues on certain platforms or versions), this version uses plotshape() to ensure wide compatibility and reliable visual cues, even on older Pine Script environments. This makes it lightweight, robust, and ideal for traders who want a quick-glance tool without cluttering their charts.

The indicator is best used on 1H, 4H, or daily timeframes to clearly observe the Thursday–Friday–Monday structure. It works well in both trending and consolidating markets as a tool to mark potential liquidity sweeps or break-of-structure setups.

OI Bahavior MapThis indicator visualizes Open Interest (OI) changes for Binance Futures and highlights the behavior of market participants — whether takers or makers are opening or closing positions.

📊 Supported display modes:

• Taker or Maker

• Longs or Shorts

• Cumulative or Per-Bar

• Displayed in USD or Coins

💡 Each candle color reflects the dominant trade direction (delta):

🟢 Green = Aggressive buying (Delta Buy)

🔴 Red = Aggressive selling (Delta Sell)

OI direction (↑/↓) determines whether positions are being opened or closed.

🛠️ Optional metrics:

• Moving average of OI (SMA, EMA, WMA, VWMA, LSMA)

• Volatility channels (Bollinger Bands or Extremums)

⚙️ How it works:

• Fetches OI data from the SYMBOL_OI ticker (e.g., BTCUSDT_OI)

• Compares current OI with the previous bar

• Uses signed volume delta (close - open) to infer intent

• Classifies bar as open/close, long/short, taker/maker

• Displays the net effect as a colored candle on a secondary chart

🤔 How to interpret Taker and Maker?

• Taker: The aggressive participant who removes liquidity (initiates the trade)

• Maker: The passive participant who provides liquidity (places resting orders)

You can choose to display the same event from either the Taker or Maker perspective — the chart will look the same, but the interpretation changes.

🧠 Core Logic Mapping

```

🟢 Green: Taker Longs (Buy, OI↑) | Maker Shorts (Buy, OI↓)

🔴 Red: Taker Shorts (Sell, OI↑) | Maker Longs (Sell, OI↓)

```

⚠️ Limitations:

• Works only for Binance Futures

• Requires existence of SYMBOL_OI ticker on TradingView

• Represents approximate intent based on OI + volume behavior

💬 Open Source

The script is open for the community. Suggestions and feedback are welcome in the comments!

__________________________________________________________________________________

Этот индикатор визуализирует изменения открытого интереса (OI) для Binance Futures и показывает поведение участников рынка — открывают или закрывают позиции тейкеры или мейкеры.

📊 Доступные режимы отображения:

• Taker или Maker

• Longs или Shorts

• Кумулятивный или по бару

• В USD или в монетах

💡 Каждый цвет свечи отражает преобладающее направление сделок (дельта):

🟢 Зеленый = Агрессивные покупки (Delta Buy)

🔴 Красный = Агрессивные продажи (Delta Sell)

Направление OI (↑/↓) показывает, открываются или закрываются позиции.

🛠️ Дополнительные метрики:

• Скользящая средняя OI (SMA, EMA, WMA, VWMA, LSMA)

• Волатильностные каналы (Bollinger Bands или экстремумы)

⚙️ Как работает:

• Получает данные OI из тикера SYMBOL_OI (например, BTCUSDT_OI)

• Сравнивает текущий OI с предыдущим баром

• Использует направленную дельту объема (close - open) для определения намерения

• Классифицирует бар как открытие/закрытие, лонг/шорт, тейкер/мейкер

• Отображает итог в виде цветной свечи на дополнительном графике

🤔 Как интерпретировать Taker и Maker?

• Taker: Агрессивный участник, который изымает ликвидность (инициирует сделку)

• Maker: Пассивный участник, который создает ликвидность (выставляет лимитные заявки)

Вы можете выбрать отображение события с позиции тейкера или мейкера — график будет одинаковым, но смысл меняется.

🧠 Схема логики

```

🟢 Зеленый: Taker Longs (Покупка, OI↑) | Maker Shorts (Покупка, OI↓)

🔴 Красный: Taker Shorts (Продажа, OI↑) | Maker Longs (Продажа, OI↓)

```

⚠️ Ограничения:

• Работает только для Binance Futures

• Требуется наличие тикера SYMBOL_OI на TradingView

• Показывает приблизительное намерение на основе OI и дельты объема

💬 Open Source

Скрипт открыт для сообщества. Предложения и обратная связь приветствуются в комментариях!