Per Volume Price ImpactLiquidity, Information and Market Timing

* Market Liquidity

The term liquidity can refer to many things in finance. In this article, we will limit the scope of discussion to the market’s ability to transact without incurring a significant increase in volatility.

As we know, liquidity and volatility have an inversed relationship — the more ample the liquidity, the lower the volatility (attributed to transaction cost, price movement and, so on). With this understanding, we can say large movements in the market are driven by low liquidity. This does not seem to make sense because the markets are huge, how can it possibly be illiquid? Now, this has to do with how the market operates and how exchanges occur (This topic concerns the area of market microstructure).

* Order Book & the Trading Process

So how does a transaction actually occur in the market? Let’s assume we open a position with a market order. In this case, you will get the price on your quote board if there are enough units of assets people are willing to sell at that price. If there are not enough units, you will buy from the second-best price and so on until your order is filled. Now in the second case, as the order is being filled, the change in price is recorded. Therefore, if someone wishes to move the market, theoretically, they just need to buy up or sell up but it is problematic to do so.

Here is why:

while dry up the liquidity can make huge moves, it is inefficient to do so.

it takes a lot of money to do that

your position will be exposed, someone more resourceful than you may go against you and that is a huge risk

market manipulation charges

when you open a position, the entry price of the position is essentially a VWAP (volume-weighted average price). If you attempt to move the market and open a buy position at the same time, you will have a higher VWAP, eating into your own profit.

I think these reasons are sufficient in establishing why opening a position and drying up liquidity to profit is a dumb idea. But of course, the institutions are not stupid, the alternative is to enter your position first then move the market.

To measure liquidity one of the tools people use is the order book. It can offer an overview of the sentiment (by looking at the orders and changes in volume) and how people are positioned (if the broker offers such data). In my opinion, open interest is a much better tool than order as it records the transactions that have occurred, hence less prone to manipulations (google: “Navinder Singh Sarao”, the trader who used fake orders to manipulate algorithms to crash the market).

But to quantify the order book is so much work as well (there are ways, just difficult), what we can do is to make things simpler.

* Quantify Market Impact

We know price and volume reflect information, while the past technical information has no predictive power per semi-strong form of EMH, empirical studies have often tested this theory over a longer time horizon. In our case, precisely due to the mechanism of exchange and human behavior (The lack of incentive to move the market right away) we can, in the very short term (often intraday), foresee if the market is going to move or not. Back to the very definition of liquidity being the ability to transact without moving the market significantly, we can take this definition and quantify it with this formula:

Market Impact = (High — Low) / Volume

Why specifically “high — low”, because that’s the complete information in that moment and it is corresponding to the volume. A little crude but it is the simplest form.

A few things to take note of here:

We can only know the complete picture once the candle is complete. This is fine in most markets because it takes time to gather money and orders.

We often see high liquidity during certain time of the day, for example, when the market opens and so on. As a result, we need to take some scientific approaches to transform the data.

Now, this looks much better. To interpret this graph, the lower the value, the lower the market impact, the deeper the liquidity.

* Generate Tradable Insights

To generate trade ideas isn’t a difficult task, we all know the RSI, MOM, STOC, etc. all the indicators attempt to draw boundaries, and we can do the same but we need to be a little more advanced and critical.

step 1: we first need to normalize the data. To do that we will take the log of the values to make the skewed distribution normal. The result isn’t ideal if you zoom out but I think this is decent enough to work with. Here is

This is still not a stationary time series, but it looks stable enough and it mean-reverts. So we turn to our lovely standard deviation bands for help.

Step 2: Because this is not a stationary process (visually, you can test it statistically if you wish), we cannot just take sample mean and SD and also because we want to show off our data skills, so we turn to move averages and regressions. I’m going to use moving regression here because I think it is better (mean can be distorted by large values by a larger margin and it lags)

I’m using the moving regression band on TradingView and 1.5 SD here for convenience, you can try to optimize the parameters with codes or other regression models if you wish. But I think it is more important to understand the rationale here.

This step is essentially trying to figure out the anomalies in liquidity so that we can see when there is deep liquidity. This is also why choosing the parameter is crucial because you are essentially approximating how much informed trading is taking place (This is a concept in market microstructure for brokerages to set their spreads but it is not a good tool in a liquid market). By setting the level at 1.5 we are assuming about 86% of the time the market is in what we consider a normal liquid state. (again it is arbitrary, but based on the 68–95–99.7 rule of normal distribution). The rest of the time will be either low or high liquidity, When liquidity is deep, it perhaps, signals institutional money is pouring into the market and big moves may follow.

* Conclusion

There you have it, how to enter the market with the big bucks. But do take note there are plenty of assumptions and a lot to improve on here.

"liquidity" için komut dosyalarını ara

Smart Volume S/R Pro [The_lurker]مؤشر "Smart Volume S/R Pro " هو أداة تحليل فني متقدمة مصممة لمساعدة المتداولين في تحديد مستويات الدعم والمقاومة القوية بناءً على حجم التداول، مع إضافة ميزات تحليلية متطورة مثل تصفية الاتجاه ، مناطق الثقة ، تقييم القوة ، حساب احتمالية الاختراق ، قياس السيولة ، تحديد الأهداف السعرية ، ومستويات فيبوناتشي . وايضا تقديم تسميات (Labels) بجانب كل مستوى دعم ومقاومة، تحتوي على أرقام ومعلومات دقيقة تعكس حالة السوق. هذه التسميات ليست مجرد زينة، بل أدوات تحليلية تساعد المتداولين على اتخاذ قرارات مستنيرة بناءً على بيانات السوقيهدف هذا المؤشر إلى توفير رؤية شاملة للسوق .

الوظائف الرئيسية للمؤشر

1- تحديد مستويات الدعم والمقاومة بناءً على حجم التداول العالي

يقوم المؤشر بتحليل الأشرطة (Bars) السابقة (حتى 300 شريط افتراضيًا) لتحديد النقاط التي شهدت أعلى مستويات حجم التداول.

يرسم خطوط أفقية تمثل مستويات المقاومة (عند أعلى سعر في تلك الأشرطة) والدعم (عند أدنى سعر)، ويمكن للمستخدم اختيار عدد الخطوط المعروضة (من 1 إلى 6).

2- تصفية الاتجاه باستخدام مؤشر ADX

يستخدم المؤشر مؤشر الاتجاه المتوسط (ADX) لتقييم قوة الاتجاه في السوق.

عندما تكون قوة الاتجاه عالية (تتجاوز عتبة محددة، 25 افتراضيًا)، يقلل المؤشر عدد مستويات الدعم والمقاومة المعروضة للتركيز فقط على المستويات الأكثر أهمية.

3- مناطق الثقة الديناميكية

يضيف المؤشر مناطق حول مستويات الدعم والمقاومة بناءً على متوسط المدى الحقيقي (ATR)، مما يساعد المتداولين على تصور النطاقات التي قد يتفاعل فيها السعر مع هذه المستويات.

يمكن تعديل عرض هذه المناطق باستخدام مضاعف ATR.

4- تقييم قوة المستويات

يحسب المؤشر قوة كل مستوى بناءً على حجم التداول، عدد المرات التي تم اختبار المستوى فيها (Touch Count)، وقرب السعر الحالي من المستوى.

يتم عرض درجة القوة (من 0 إلى 100) بجانب كل مستوى إذا تم تفعيل هذه الخاصية.

5- احتمالية الاختراق

يقدّر المؤشر احتمالية اختراق كل مستوى بناءً على الزخم (ROC)، قوة المستوى، والمسافة بين السعر الحالي والمستوى.

يظهر الاحتمال كنسبة مئوية إذا تم تفعيل الخيار، مما يساعد المتداولين على توقع الحركات المحتملة.

6- تحليل السيولة التاريخية

يقيس المؤشر السيولة حول كل مستوى بناءً على حجم التداول في النطاقات القريبة منه.

يمكن عرض قيم السيولة في التسميات أو استخدامها لتعديل عرض الخطوط (الخطوط الأكثر سيولة تظهر أعرض).

7- الأهداف السعرية

عند تفعيل هذه الخاصية، يحسب المؤشر أهداف سعرية للاختراق (Breakout) والارتداد (Reversal) بناءً على الزخم وقوة المستوى وATR.

يمكن عرض هذه الأهداف كنصوص في التسميات أو كخطوط أفقية على الرسم البياني.

8- مستويات فيبوناتشي

يرسم المؤشر مستويات فيبوناتشي (0.0، 0.236، 0.382، 0.5، 0.618، 0.786، 1.0) بناءً على أعلى وأدنى سعر في فترة النظرة الخلفية.

يمكن للمستخدم اختيار أي من هذه المستويات لعرضها أو إخفائها.

9- تنبيه شامل للاختراق

يوفر المؤشر تنبيهًا واحدًا يشمل جميع المستويات، حيث يُطلق التنبيه عندما يخترق السعر أي مستوى دعم أو مقاومة مع رسالة توضح نوع الاختراق والمستوى المخترق.

كيفية عمل المؤشر

الخطوة الأولى: يحدد المؤشر الأشرطة ذات الحجم العالي خلال فترة النظرة الخلفية المحددة (Lookback Period).

الخطوة الثانية: يرسم مستويات الدعم والمقاومة بناءً على أعلى وأدنى الأسعار في تلك الأشرطة، مع مراعاة عدد الخطوط المختارة من المستخدم.

الخطوة الثالثة: يطبق مرشح الاتجاه (إذا كان مفعلاً) لتقليل عدد المستويات في حالة الاتجاه القوي.

الخطوة الرابعة: يضيف التحليلات الإضافية مثل القوة، السيولة، احتمالية الاختراق، والأهداف السعرية، ويرسم مناطق الثقة ومستويات فيبوناتشي حسب الإعدادات.

الخطوة الخامسة: يراقب السعر ويطلق تنبيهًا عند الاختراق.

الإعدادات القابلة للتخصيص

1- فترة النظرة الخلفية (Lookback Period): عدد الأشرطة التي يتم تحليلها (افتراضيًا 300).

2- عدد الخطوط (Number of Lines): من 1 إلى 6 مستويات دعم ومقاومة.

3- الألوان والأنماط: يمكن تغيير ألوان الخطوط وأنماطها (ممتلئة، متقطعة، منقطة).

4- التسميات: تفعيل/تعطيل التسميات، وحجمها، وموقعها، ولون النص.

5- مرشح الاتجاه: تفعيل/تعطيل ADX، وتعديل طوله وعتبته.

6- مناطق الثقة: تفعيل/تعطيل، وتعديل طول ATR ومضاعفه.

7- القوة واحتمالية الاختراق: تفعيل/تعطيل العرض، وتعديل طول ROC.

8- السيولة: تفعيل/تعطيل تأثير السيولة على عرض الخطوط وقيمها في التسميات.

9- الأهداف السعرية: تفعيل/تعطيل الأهداف وعرضها كخطوط.

10- فيبوناتشي: اختيار المستويات المعروضة ولون الخطوط.

فوائد المؤشر

دقة عالية: يعتمد على حجم التداول لتحديد المستويات، مما يجعله أكثر موثوقية من المستويات العشوائية.

مرونة: يوفر خيارات تخصيص واسعة تتيح للمتداولين تكييفه حسب استراتيجياتهم.

تحليل شامل: يجمع بين الدعم والمقاومة، الاتجاه، السيولة، والأهداف في أداة واحدة.

سهولة الاستخدام: التسميات والتنبيهات تجعل من السهل متابعة السوق دون تعقيد.

==================================================================================تسميات (Labels) بجانب كل مستوى دعم ومقاومة، تحتوي على أرقام ومعلومات دقيقة تعكس حالة السوق. هذه التسميات ليست مجرد زينة، بل أدوات تحليلية تساعد المتداولين على اتخاذ قرارات مستنيرة بناءً على بيانات السوق. في هذا الشرح، سنستعرض كل رقم أو قيمة تظهر في التسميات ومعناها العملي.

مكونات التسميات

التسميات تظهر بجانب كل مستوى دعم (Support) ومقاومة (Resistance) وتبدأ بحرف "S" للدعم أو "R" للمقاومة، تليها مجموعة من الأرقام والقيم التي يمكن تفعيلها أو تعطيلها حسب إعدادات المستخدم. إليك تفصيل كل عنصر:

1- عدد اللمسات (Touch Count)

الرمز: يظهر مباشرة بعد "S" أو "R" (مثال: "R: 5" أو "S: 3").

المعنى: يشير إلى عدد المرات التي اختبر فيها السعر هذا المستوى دون اختراقه.

الفائدة: كلما زاد عدد اللمسات، كلما كان المستوى أقوى وأكثر أهمية. على سبيل المثال، إذا كان "R: 5"، فهذا يعني أن السعر ارتد من هذا المستوى 5 مرات، مما يجعله مقاومة قوية محتملة.

2- قوة المستوى (Strength Rating)

الرمز: يظهر بين قوسين مربعين (مثال: " ").

المعنى: قيمة من 0 إلى 100 تعكس قوة المستوى بناءً على عوامل مثل حجم التداول، عدد اللمسات، وقرب السعر الحالي من المستوى.

الفائدة: القيم العالية (مثل 75 أو أكثر) تشير إلى مستوى قوي يصعب اختراقه، بينما القيم المنخفضة (مثل 30 أو أقل) تدل على ضعف المستوى وسهولة اختراقه. يمكن للمتداول استخدام هذا لتحديد المستويات الأكثر موثوقية.

3- احتمالية الاختراق (Breakout Probability)

الرمز: يبدأ بحرف "B" متبوعًا بنسبة مئوية (مثال: "B: 60%").

المعنى: نسبة من 0% إلى 100% تُظهر احتمالية اختراق السعر للمستوى بناءً على الزخم الحالي، قوة المستوى، والمسافة بين السعر والمستوى.

الفائدة: نسبة مرتفعة (مثل 60% أو أكثر) تعني أن السعر قد يخترق المستوى قريبًا، بينما النسب المنخفضة (مثل 20%) تشير إلى احتمال ارتداد السعر. هذا مفيد لتوقع الحركة التالية.

4- قيمة السيولة (Liquidity Value)

الرمز: يبدأ بحرف "L" متبوعًا برقم (مثال: "L: 1200").

المعنى: يمثل متوسط حجم التداول في النطاق القريب من المستوى، مما يعكس السيولة التاريخية حوله.

الفائدة: القيم العالية تدل على وجود سيولة كبيرة، مما يعني أن السعر قد يتفاعل بقوة مع هذا المستوى (إما بالارتداد أو الاختراق). القيم المنخفضة تشير إلى سيولة ضعيفة، مما قد يجعل المستوى أقل تأثيرًا.

5- الأهداف السعرية (Price Targets)

الرمز: يبدأ بـ "BT" (هدف الاختراق) و"RT" (هدف الارتداد) متبوعين بأرقام (مثال: "BT: 150.50 RT: 148.20").

المعنى:

BT (Breakout Target): السعر المحتمل الذي قد يصل إليه السعر بعد اختراق المستوى.

RT (Reversal Target): السعر المحتمل الذي قد يصل إليه السعر إذا ارتد من المستوى.

الفائدة: تساعد المتداولين في تحديد نقاط الخروج المحتملة بعد الاختراق أو الارتداد، مما يسهل وضع خطة تداول دقيقة.

أمثلة عملية

تسمية مقاومة: "R: 4 B: 25% L: 1500 BT: 155.00 RT: 152.00"

المستوى اختُبر 4 مرات، قوته 80 (قوي جدًا)، احتمالية الاختراق 25% (منخفضة، أي احتمال ارتداد أعلى)، السيولة 1500 (مرتفعة)، هدف الاختراق 155.00، هدف الارتداد 152.00.

الاستنتاج: المستوى قوي ومن المرجح أن يرتد السعر منه، لكن إذا اخترق، فقد يصل إلى 155.00.

تسمية دعم: "S: 2 B: 70% L: 800 BT: 145.00 RT: 147.50"

المستوى اختُبر مرتين، قوته 40 (متوسطة إلى ضعيفة)، احتمالية الاختراق 70% (مرتفعة)، السيولة 800 (متوسطة)، هدف الاختراق 145.00، هدف الارتداد 147.50.

الاستنتاج: المستوى ضعيف ومن المحتمل أن يخترقه السعر ليهبط إلى 145.00.

كيفية الاستفادة من التسميات

تحديد القوة والضعف: استخدم قوة المستوى (Strength) لمعرفة ما إذا كان المستوى موثوقًا للارتداد أو عرضة للاختراق.

توقع الحركة: انظر إلى احتمالية الاختراق (Breakout Probability) لتحديد ما إذا كنت ستنتظر اختراقًا أو ترتدًا.

إدارة المخاطر: استخدم الأهداف السعرية (BT وRT) لتحديد نقاط جني الأرباح أو وقف الخسارة.

تقييم السيولة: ركز على المستويات ذات السيولة العالية لأنها غالبًا تكون نقاط تحول رئيسية في السوق.

تأكيد التحليل: ادمج عدد اللمسات مع القوة والسيولة للحصول على صورة كاملة عن أهمية المستوى.

تخصيص التسميات

يمكن للمستخدم تفعيل أو تعطيل أي من هذه القيم (القوة، الاحتمالية، السيولة، الأهداف) من إعدادات المؤشر.

يمكن أيضًا تغيير حجم التسميات (صغير، عادي، كبير)، موقعها (يمين، يسار، أعلى، أسفل)، ولون النص لتناسب احتياجاتك.

التسميات في هذا المؤشر هي بمثابة لوحة تحكم صغيرة بجانب كل مستوى دعم ومقاومة، تقدم لك معلومات فورية عن قوته، احتمالية اختراقه، سيولته، وأهدافه السعرية. بفهم هذه الأرقام، يمكنك تحسين قراراتك في التداول، سواء كنت تبحث عن نقاط دخول، خروج، أو إدارة مخاطر. إذا كنت تريد أداة تجمع بين البساطة والعمق التحليلي .

تنويه:

المؤشر هو أداة مساعدة فقط ويجب استخدامه مع التحليل الفني والأساسي لتحقيق أفضل النتائج.

إخلاء المسؤولية

لا يُقصد بالمعلومات والمنشورات أن تكون، أو تشكل، أي نصيحة مالية أو استثمارية أو تجارية أو أنواع أخرى من النصائح أو التوصيات المقدمة أو المعتمدة من TradingView.

The Smart Volume S/R Pro indicator is an advanced technical analysis tool designed to help traders identify strong support and resistance levels based on trading volume, with the addition of advanced analytical features such as trend filtering, confidence zones, strength assessment, breakout probability calculation, liquidity measurement, price target identification, and Fibonacci levels. It also provides labels next to each support and resistance level, containing accurate numbers and information that reflect the market condition. These labels are not just decorations, but analytical tools that help traders make informed decisions based on market data. This indicator aims to provide a comprehensive view of the market.

Main functions of the indicator

1- Identifying support and resistance levels based on high trading volume

The indicator analyzes previous bars (up to 300 bars by default) to identify the points that witnessed the highest levels of trading volume.

It draws horizontal lines representing resistance levels (at the highest price in those bars) and support (at the lowest price), and the user can choose the number of lines displayed (from 1 to 6).

2- Filtering the trend using the ADX indicator

The indicator uses the Average Directional Index (ADX) to assess the strength of a trend in the market.

When the strength of the trend is high (exceeding a specified threshold, 25 by default), the indicator reduces the number of support and resistance levels displayed to focus only on the most important levels.

3- Dynamic Confidence Zones

The indicator adds zones around support and resistance levels based on the Average True Range (ATR), helping traders visualize the ranges in which the price may interact with these levels.

The width of these zones can be adjusted using the ATR multiplier.

4- Assessing the Strength of Levels

The indicator calculates the strength of each level based on trading volume, the number of times the level has been tested (Touch Count), and the proximity of the current price to the level.

A strength score (from 0 to 100) is displayed next to each level if this feature is enabled.

5- Breakout Probability

The indicator estimates the probability of breaking each level based on momentum (ROC), the strength of the level, and the distance between the current price and the level.

The probability is displayed as a percentage if the option is enabled, helping traders anticipate potential moves.

6- Historical Liquidity Analysis

The indicator measures liquidity around each level based on the trading volume in the ranges near it.

The liquidity values can be displayed in the labels or used to adjust the width of the lines (the most liquid lines appear wider).

7- Price Targets

When this feature is enabled, the indicator calculates price targets for breakout and reversal based on momentum, level strength and ATR.

These targets can be displayed as text in the labels or as horizontal lines on the chart.

8- Fibonacci Levels

The indicator plots Fibonacci levels (0.0, 0.236, 0.382, 0.5, 0.618, 0.786, 1.0) based on the highest and lowest price in the lookback period.

The user can choose which of these levels to display or hide.

9- Comprehensive Breakout Alert

The indicator provides a single alert that includes all levels, where the alert is triggered when the price breaks any support or resistance level with a message explaining the type of breakout and the level broken.

How the indicator works

Step 1: The indicator identifies the bars with high volume during the specified Lookback Period.

Step 2: Draws support and resistance levels based on the highest and lowest prices in those bars, taking into account the number of lines selected by the user.

Step 3: Apply the trend filter (if enabled) to reduce the number of levels in case of a strong trend.

Step 4: Adds additional analyses such as strength, liquidity, breakout probability, and price targets, and draws confidence zones and Fibonacci levels according to the settings.

Step 5: Monitors the price and triggers an alert when the breakout occurs.

Customizable Settings

1- Lookback Period: Number of bars to analyze (default 300).

2- Number of Lines: From 1 to 6 support and resistance levels.

3- Colors and Styles: Line colors and styles can be changed (filled, dashed, dotted).

4- Labels: Enable/disable labels, their size, location, and text color.

5- Trend Filter: Enable/disable ADX, and modify its length and threshold.

6- Confidence Zones: Enable/disable, and modify the ATR length and multiplier.

7- Strength and Breakout Probability: Enable/disable the display, and modify the ROC length.

8- Liquidity: Enable/disable the effect of liquidity on the display of the lines and their values in the labels.

9- Price Targets: Enable/disable the targets and display them as lines.

10- Fibonacci: Choose the displayed levels and the color of the lines.

Indicator Benefits

High Accuracy: It relies on trading volume to determine the levels, which makes it more reliable than random levels.

Flexibility: It provides extensive customization options that allow traders to adapt it to their strategies.

Comprehensive Analysis: Combines support and resistance, trend, liquidity, and targets in one tool. Ease of Use: Labels and alerts make it easy to follow the market without complexity.

Labels next to each support and resistance level contain accurate numbers and information that reflect the market situation. These labels are not just decorations, but analytical tools that help traders make informed decisions based on market data. In this explanation, we will review each number or value that appears in the labels and their practical meaning.

Label Components

Labels appear next to each support and resistance level and begin with the letter "S" for support or "R" for resistance, followed by a set of numbers and values that can be enabled or disabled according to the user's settings. Here is a breakdown of each element:

1- Touch Count

Symbol: Appears immediately after "S" or "R" (example: "R: 5" or "S: 3").

Meaning: Indicates the number of times the price has tested this level without breaking it.

Benefit: The more touches, the stronger and more important the level. For example, if it is "R: 5", it means that the price has bounced off this level 5 times, making it a potentially strong resistance.

2- Strength Rating

Symbol: Appears between square brackets (example: " ").

Meaning: A value from 0 to 100 that reflects the strength of the level based on factors such as trading volume, number of touches, and proximity of the current price to the level.

Benefit: High values (such as 75 or more) indicate a strong level that is difficult to break, while low values (such as 30 or less) indicate a weak level that is easy to break. A trader can use this to determine the most reliable levels.

3- Breakout Probability

Symbol: Starts with the letter "B" followed by a percentage (example: "B: 60%").

Meaning: A percentage from 0% to 100% that shows the probability of the price breaking the level based on the current momentum, the strength of the level, and the distance between the price and the level.

Interest: A high percentage (such as 60% or more) means that the price may soon break through the level, while low percentages (such as 20%) indicate that the price may bounce. This is useful for anticipating the next move.

4- Liquidity Value

Symbol: Starts with the letter "L" followed by a number (example: "L: 1200").

Meaning: Represents the average trading volume in the range near the level, reflecting historical liquidity around it.

Interest: High values indicate high liquidity, meaning that the price may react strongly to this level (either by bouncing or breaking through). Low values indicate low liquidity, which may make the level less influential.

5- Price Targets

Symbol: Starts with "BT" (breakout target) and "RT" (rebound target) followed by numbers (example: "BT: 150.50 RT: 148.20").

Meaning:

BT (Breakout Target): The potential price that the price may reach after breaking the level.

RT (Reversal Target): The potential price that the price may reach if it rebounds from the level.

Utility: Helps traders identify potential exit points after a breakout or rebound, making it easier to develop an accurate trading plan.

Working examples

Resistance label: "R: 4 B: 25% L: 1500 BT: 155.00 RT: 152.00"

Level tested 4 times, strength 80 (very strong), probability of breakout 25% (low, i.e. higher probability of rebound), liquidity 1500 (high), breakout target 155.00, rebound target 152.00.

Conclusion: The level is strong and the price is likely to rebound from it, but if it breaks, it may reach 155.00.

Support Label: "S: 2 B: 70% L: 800 BT: 145.00 RT: 147.50"

Level tested twice, Strength 40 (medium to weak), Breakout Probability 70% (high), Liquidity 800 (medium), Breakout Target 145.00, Rebound Target 147.50.

Conclusion: The level is weak and the price is likely to break it to drop to 145.00.

How to use labels

Determine strength and weakness: Use the level's strength to see if the level is reliable for a bounce or vulnerable to a breakout.

Predict the move: Look at the Breakout Probability to determine whether to wait for a breakout or a bounce.

Risk Management: Use price targets (BT and RT) to set take profit or stop loss points.

Liquidity Evaluation: Focus on levels with high liquidity as they are often key turning points in the market.

Analysis Confirmation: Combine the number of touches with strength and liquidity to get a complete picture of the level’s importance.

Customize Labels

The user can enable or disable any of these values (strength, probability, liquidity, targets) from the indicator settings.

The size of the labels (small, normal, large), their position (right, left, top, bottom), and the color of the text can also be changed to suit your needs.

The labels in this indicator act as a small dashboard next to each support and resistance level, providing you with instant information about its strength, probability of breakout, liquidity, and price targets. By understanding these numbers, you can improve your trading decisions, whether you are looking for entry points, exit points, or risk management. If you want a tool that combines simplicity with analytical depth.

Disclaimer:

The indicator is an auxiliary tool only and should be used in conjunction with technical and fundamental analysis for best results.

Disclaimer

The information and posts are not intended to be, or constitute, any financial, investment, trading or other types of advice or recommendations provided or endorsed by TradingView.

Smart Money Decoded [GOLD]Title: Smart Money Decoded

Description:

Introduction

Smart Money Decoded is a comprehensive, institutional-grade visualization suite designed to simplify the complex world of Smart Money Concepts (SMC). While many indicators flood the chart with noise, this tool focuses on clarity, precision, and high-probability structure.

This script is built for traders who follow the "Inner Circle Trader" (ICT) methodologies but struggle to identify valid Zones, Displacement, and Liquidity Sweeps in real-time.

💎 Key Features & Logic

1. Refined Market Structure (BOS & CHoCH)

Instead of marking every minor pivot, this script uses a filtered Swing High/Low detection system.

HH/LL/LH/HL Labels: Only significant structure points are mapped.

BOS (Break of Structure): Marks trend continuations in the direction of the bias.

CHoCH (Change of Character): Marks potential trend reversals.

2. Advanced Order Blocks (with "Strict Mode")

Not all down-candles before an up-move are Order Blocks. This script separates the weak from the strong.

Standard OBs: Visualized with standard transparency.

⚡ SWEEP OBs (High Probability): Order Blocks that explicitly swept liquidity (Stop Hunt) before the reversal are highlighted with a thicker border, brighter color, and a ⚡ symbol. These are your high-probability "Turtle Soup" entries.

Strict Mode Toggle: In the settings, you can choose to hide all weak OBs and only see the ones that swept liquidity.

3. Dynamic Breaker Blocks

A true ICT Breaker is a failed Order Block that trapped liquidity.

This script automatically detects when a valid OB is mitigated (broken through) and projects it forward as a Breaker Block.

This ensures you are trading off valid flipped zones (Support becomes Resistance, Resistance becomes Support).

4. Fair Value Gaps (FVG)

Automatically detects Imbalances (Imbalance/Inefficiency).

Includes an ATR Filter to ignore tiny, insignificant gaps, keeping your chart clean.

Option to show the Consequent Encroachment (50% CE) level for precision entries.

5. Liquidity Zones (BSL / SSL)

Automatically plots Buy Side Liquidity (BSL) and Sell Side Liquidity (SSL) at key swing points.

Once price sweeps these levels, the zone is removed or marked as "Swept," helping you identify when the draw on liquidity has been met.

6. Institutional Data Panel

A dashboard in the top right corner displays:

Market Bias: Bullish/Bearish/Neutral based on structure.

Premium/Discount: Tells you if price is in the expensive (Premium) or cheap (Discount) part of the current dealing range.

Active Zones: Counts of current open arrays.

⚙️ How To Use This Indicator

Identify Bias: Look at the Structure Labels (HH/LL) and the Panel. Are we making Higher Highs?

Wait for the Trap: Look for a Liquidity Sweep (BSL/SSL taken) or a ⚡ Sweep OB.

Entry Confirmation: Watch for a return to a Fair Value Gap (FVG) or a retest of a Breaker Block (BRK).

Manage Risk: Use the visuals to place stops above/below invalidation points.

Customization:

Go to the settings to toggle "Strict Mode" for Order Blocks, change colors to match your theme, or adjust the lookback periods to fit your specific asset (Forex, Crypto, or Indices).

📚 Credits & Acknowledgments

This script is an educational tool based on the public teachings of Michael J. Huddleston (The Inner Circle Trader - ICT).

Concepts used: Order Blocks, Breakers, FVGs, Market Structure, Liquidity Pools.

Credit is fully given to ICT for originating these concepts and sharing them with the world.

⚠️ Disclaimer

This script is NOT affiliated with, endorsed by, or connected to Michael J. Huddleston (ICT) in any way. It is an independent coding project intended for educational purposes and visual assistance.

Trading involves substantial risk. This indicator does not guarantee profits. Always use proper risk management. Trust your analysis first, and use indicators as confluence.

#Smart Money Concepts, #SMC, #ICT,#Liquidity, #Market Structure, #Trend, #Price Action.

CandelaCharts - Buyside & Sellside 📝 Overview

The Buyside & Sellside Liquidity Indicator is designed to identify and emphasize one of the foundational concepts within the ICT (Inner Circle Trader) trading methodology: liquidity levels.

This tool focuses on pinpointing key areas in the market where buy-side and sell-side liquidity is concentrated, providing traders with insights into potential price targets, reversal zones, and institutional order flow behavior.

By highlighting these liquidity zones, the indicator serves as a strategic aid in understanding market dynamics and enhancing decision-making in alignment with ICT principles.

📦 Features

Buyside & Sellside Liquidity

Invalidated Liquidity

Threshold

Styling

⚙️ Settings

Liquidity: Controls visibility of Bullish/Bearish Liquidity levels.

Invalidated: Displays the invalidated liquidity levels.

Levels: Controls the number of Liquidity levels that will be displayed.

Line Style: Customize the line style and width.

Threshold: Filter by swing points the Liquidity levels.

Labels: Control the Labels visibility.

⚡️ Showcase

Buyside & Sellside

Invalidated

🚨 Alerts

This script offers alert options for all signal types.

Bearish Signal

A bearish signal is generated when the price reaches a Buyside Liquidity level.

Bullish Signal

A bullish signal is generated when the price reaches a Sellside Liquidity level.

⚠️ Disclaimer

Trading involves significant risk, and many participants may incur losses. The content on this site is not intended as financial advice and should not be interpreted as such. Decisions to buy, sell, hold, or trade securities, commodities, or other financial instruments carry inherent risks and are best made with guidance from qualified financial professionals. Past performance is not indicative of future results.

RSI Analysis with Statistical Summary Scientific Analysis of the Script "RSI Analysis with Statistical Summary"

Introduction

I observed that there are outliers in the price movement liquidity, and I wanted to understand the RSI value at those points and whether there are any notable patterns. I aimed to analyze this statistically, and this script is the result.

Explanation of Key Terms

1. Outliers in Price Movement Liquidity: An outlier is a data point that significantly deviates from other values. In this context, an outlier refers to an unusually high or low liquidity of price movement, which is the ratio of trading volume to the price difference between the open and close prices. These outliers can signal important market changes or unusual trading activities.

2. RSI (Relative Strength Index): The RSI is a technical indicator that measures the speed and change of price movements. It ranges from 0 to 100 and helps identify overbought or oversold conditions of a trading instrument. An RSI value above 70 indicates an overbought condition, while a value below 30 suggests an oversold condition.

3. Mean: The mean is a measure of the average of a dataset. It is calculated by dividing the sum of all values by the number of values. In this script, the mean of the RSI values is calculated to provide a central tendency of the RSI distribution.

4. Standard Deviation (stdev): The standard deviation is a measure of the dispersion or variation of a dataset. It shows how much the values deviate from the mean. A high standard deviation indicates that the values are widely spread, while a low standard deviation indicates that the values are close to the mean.

5. 68% Confidence Interval: A confidence interval indicates the range within which a certain percentage of values of a dataset lies. The 68% confidence interval corresponds to a range of plus/minus one standard deviation around the mean. It indicates that about 68% of the data points lie within this range, providing insight into the distribution of values.

Overview

This Pine Script™, written in Pine version 5, is designed to analyze the Relative Strength Index (RSI) of a stock or other trading instrument and create statistical summaries of the distribution of RSI values. The script identifies outliers in price movement liquidity and uses this information to calculate the frequency of RSI values. At the end, it displays a statistical summary in the form of a table.

Structure and Functionality of the Script

1. Input Parameters

- `rsi_len`: An integer input parameter that defines the length of the RSI (default: 14).

- `outlierThreshold`: An integer input parameter that defines the length of the outlier threshold (default: 10).

2. Calculating Price Movement Liquidity

- `priceMovementLiquidity`: The volume is divided by the absolute difference between the close and open prices to calculate the liquidity of the price movement.

3. Determining the Boundary for Liquidity and Identifying Outliers

- `liquidityBoundary`: The boundary is calculated using the Exponential Moving Average (EMA) of the price movement liquidity and its standard deviation.

- `outlier`: A boolean value that indicates whether the price movement liquidity exceeds the set boundary.

4. Calculating the RSI

- `rsi`: The RSI is calculated with a period length of 14, using various moving averages (e.g., SMA, EMA) depending on the settings.

5. Storing and Limiting RSI Values

- An array `rsiFrequency` stores the frequency of RSI values from 0 to 100.

- The function `f_limit_rsi` limits the RSI values between 0 and 100.

6. Updating RSI Frequency on Outlier Occurrence

- On an outlier occurrence, the limited and rounded RSI value is updated in the `rsiFrequency` array.

7. Statistical Summary

- Various variables (`mostFrequentRsi`, `leastFrequentRsi`, `maxCount`, `minCount`, `sum`, `sumSq`, `count`, `upper_interval`, `lower_interval`) are initialized to perform statistical analysis.

- At the last bar (`bar_index == last_bar_index`), a loop is run to determine the most and least frequent RSI values and their frequencies. Sum and sum of squares of RSI values are also updated for calculating mean and standard deviation.

- The mean (`mean`) and standard deviation (`stddev`) are calculated. Additionally, a 68% confidence interval is determined.

8. Creating a Table for Result Display

- A table `resultsTable` is created and filled with the results of the statistical analysis. The table includes the most and least frequent RSI values, the standard deviation, and the 68% confidence interval.

9. Graphical Representation

- The script draws horizontal lines and fills to indicate overbought and oversold regions of the RSI.

Interpretation of the Results

The script provides a detailed analysis of RSI values based on specific liquidity outliers. By calculating the most and least frequent RSI values, standard deviation, and confidence interval, it offers a comprehensive statistical summary that can help traders identify patterns and anomalies in the RSI. This can be particularly useful for identifying overbought or oversold conditions of a trading instrument and making informed trading decisions.

Critical Evaluation

1. Robustness of Outlier Identification: The method of identifying outliers is solely based on the liquidity of price movement. It would be interesting to examine whether other methods or additional criteria for outlier identification would lead to similar or improved results.

2. Flexibility of RSI Settings: The ability to select various moving averages and period lengths for the RSI enhances the adaptability of the script, allowing users to tailor it to their specific trading strategies.

3. Visualization of Results: While the tabular representation is useful, additional graphical visualizations, such as histograms of RSI distribution, could further facilitate the interpretation of the results.

In conclusion, this script provides a solid foundation for analyzing RSI values by considering liquidity outliers and enables detailed statistical evaluation that can be beneficial for various trading strategies.

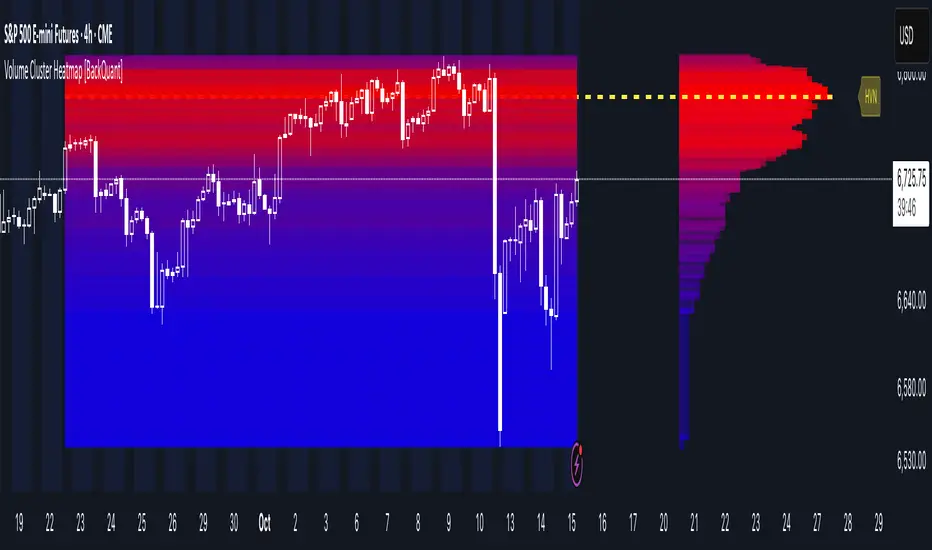

Volume Cluster Heatmap [BackQuant]Volume Cluster Heatmap

A visualization tool that maps traded volume across price levels over a chosen lookback period. It highlights where the market builds balance through heavy participation and where it moves efficiently through low-volume zones. By combining a heatmap, volume profile, and high/low volume node detection, this indicator reveals structural areas of support, resistance, and liquidity that drive price behavior.

What Are Volume Clusters?

A volume cluster is a horizontal aggregation of traded volume at specific price levels, showing where market participants concentrated their buying and selling.

High Volume Nodes (HVN) : Price levels with significant trading activity; often act as support or resistance.

Low Volume Nodes (LVN) : Price levels with little trading activity; price moves quickly through these areas, reflecting low liquidity.

Volume clusters help identify key structural zones, reveal potential reversals, and gauge market efficiency by highlighting where the market is balanced versus areas of thin liquidity.

By creating heatmaps, profiles, and highlighting high and low volume nodes (HVNs and LVNs), it allows traders to see where the market builds balance and where it moves efficiently through thin liquidity zones.

Example: Bitcoin breaking away from the high-volume zone near 118k and moving cleanly through the low-volume pocket around 113k–115k, illustrating how markets seek efficiency:

Core Features

Visual Analysis Components:

Heatmap Display : Displays volume intensity as colored boxes, lines, or a combination for a dynamic view of market participation.

Volume Profile Overlay : Shows cumulative volume per price level along the right-hand side of the chart.

HVN & LVN Labels : Marks high and low volume nodes with color-coded lines and labels.

Customizable Colors & Transparency : Adjust high and low volume colors and minimum transparency for clear differentiation.

Session Reset & Timeframe Control : Dynamically resets clusters at the start of new sessions or chosen timeframes (intraday, daily, weekly).

Alerts

HVN / LVN Alerts : Notify when price reaches a significant high or low volume node.

High Volume Zone Alerts : Trigger when price enters the top X% of cumulative volume, signaling key areas of market interest.

How It Works

Each bar’s volume is distributed proportionally across the horizontal price levels it touches. Over the lookback period, this builds a cumulative volume profile, identifying price levels with the most and least trading activity. The highest cumulative volume levels become HVNs, while the lowest are LVNs. A side volume profile shows aggregated volume per level, and a heatmap overlay visually reinforces market structure.

Applications for Traders

Identify strong support and resistance at HVNs.

Detect areas of low liquidity where price may move quickly (LVNs).

Determine market balance zones where price may consolidate.

Filter noise: because volume clusters aggregate activity into levels, minor fluctuations and irrelevant micro-moves are removed, simplifying analysis and improving strategy development.

Combine with other indicators such as VWAP, Supertrend, or CVD for higher-probability entries and exits.

Use volume clusters to anticipate price reactions to breaking points in thin liquidity zones.

Advanced Display Options

Heatmap Styles : Boxes, lines, or both. Boxes provide a traditional heatmap, lines are better for high granularity data.

Line Mode Example : Simplified line visualization for easier reading at high level counts:

Profile Width & Offset : Adjust spacing and placement of the volume profile for clarity alongside price.

Transparency Control : Lower transparency for more opaque visualization of high-volume zones.

Best Practices for Usage

Reduce the number of levels when using line mode to avoid clutter.

Use HVN and LVN markers in conjunction with volume profiles to plan entries and exits.

Apply session resets to monitor intraday vs. multi-day volume accumulation.

Combine with other technical indicators to confirm high-probability trading signals.

Watch price interactions with LVNs for potential rapid movements and with HVNs for possible support/resistance or reversals.

Technical Notes

Each bar contributes volume proportionally to the price levels it spans, creating a dynamic and accurate representation of traded interest.

Volume profiles are scaled and offset for visual clarity alongside live price.

Alerts are fully integrated for HVN/LVN interaction and high-volume zone entries.

Optimized to handle large lookback windows and numerous price levels efficiently without performance degradation.

This indicator is ideal for understanding market structure, detecting key liquidity areas, and filtering out noise to model price more accurately in high-frequency or algorithmic strategies.

Opening Range Gaps [TakingProphets]What is an Opening Range Gap (ORG)?

In ICT, the Opening Range Gap is defined as the price difference between the previous session’s close (e.g., 4:00 PM EST in U.S. indices) and the current day’s open (9:30 AM EST).

That gap is a liquidity void—an area where no trading occurred during regular hours.

Why ICT Traders Care About ORG

Liquidity Void (Gap Fill Logic)

-Because the gap is an untraded area, it naturally acts as a draw on liquidity.

-Price often seeks to rebalance by retracing into or fully filling this void.

Premium/Discount Sensitivity

-Once the ORG is defined, ICT treats it as a mini dealing range.

-Above EQ (Consequent Encroachment) = algorithmic premium (sell-sensitive).

-Below EQ = algorithmic discount (buy-sensitive).

-Price reaction at these levels gives a precise read on institutional intent intraday.

Support/Resistance from ORG

-If the session opens above prior close, the gap often acts as support until violated.

-If the session opens below prior close, the gap often acts as resistance until reclaimed.

Key ICT Concepts Anchored to ORG

Consequent Encroachment (CE): The midpoint of the gap. The algo is highly sensitive to CE as a decision point: reject → continuation; reclaim → reversal.

Draw on Liquidity (DoL): Price is algorithmically “pulled” toward gap fills, CE, or the opposite side of the ORG.

Order Flow Confirmation: If price ignores the gap and runs away from it, this signals strong institutional order flow in that direction.

Confluence with Other Tools: FVGs, OBs, and HTF PD arrays often overlap with ORG levels, strengthening setups.

Practical Application for Traders

Bias Formation:

Use ORG EQ as a line in the sand for intraday bias.

If price trades below ORG EQ after the open → look for short setups into the prior day’s low or external liquidity.

If price trades above ORG EQ → favor longs into highs/liquidity pools.

Execution Framework:

Wait for liquidity raids or market structure shifts at ORG edges (.00, .25, .50, .75).

Target: EQ, opposite quarter, or full gap fill.

Precision Reads:

ORG lines let traders anticipate where algorithms are likely to respond, providing mechanical invalidation and clear targets without clutter.

Ultra VolumeVisualizes volume intensity using dynamic color gradients and percentile thresholds. Includes optional SMA, bar coloring, and adaptive liquidity boxes to highlight high- and low-volume zones in real time.

Introduction

The Ultra Volume indicator enhances volume analysis by categorizing volume bars into percentile-based intensity levels. It uses color-coded gradients to quickly identify periods of unusually high or low activity. The script also includes an optional simple moving average (SMA), bar coloring, and visual box overlays to highlight zones of significant liquidity shifts.

Detailed Description

.........

Volume Classification

Volume is segmented into five tiers: Extra High, High, Medium, Normal, and Low, using percentile ranks calculated over a dynamically adjusted historical window. This segmentation adapts based on the chart's timeframe – using 100 bars for daily and 1440/minutes for intraday – allowing for consistent behavior across resolutions.

.....

Color Gradients

Each volume bar is colored based on its percentile category, smoothly transitioning between thresholds for visual clarity. This makes it easy to spot volume spikes or droughts relative to recent history.

.....

Simple Moving Average (SMA)

An optional SMA can be plotted on top of the volume bars for trend comparison and baseline reference. Its length and color are fully customizable.

.....

Bar Coloring

You can optionally color the chart's candlesticks to reflect the same volume intensity as the histogram bars, reinforcing visual cues across the chart.

.....

Liquidity Boxes

Two adaptive box systems highlight zones of increased or decreased liquidity:

High Liquidity Boxes expand upward when price exceeds the previous box’s top.

Low Liquidity Boxes expand downward when price breaks the previous box’s bottom.

These boxes persist and auto-adjust over time unless reset, helping traders spot key zones of volume-driven price action.

.....

Box Indexing

A configurable index shift determines how far back in the chart the boxes originate. Setting this to 501 makes them "stick" to the candle where they were first created.

.....

Data Handling

A safety check ensures the script throws an error if volume data is unavailable (e.g., for some crypto or CFD symbols).

.........

Summary

Ultra Volume is a practical tool for traders who want more than just raw volume bars. With intelligent percentile-based classification, real-time adaptive liquidity zones, and fully customizable visual elements, it turns volume into a highly readable, actionable signal.

ICT Setup 03 [TradingFinder] Judas Swing NY 9:30am + CHoCH/FVG🔵 Introduction

Judas Swing is an advanced trading setup designed to identify false price movements early in the trading day. This advanced trading strategy operates on the principle that major market players, or "smart money," drive price in a certain direction during the early hours to mislead smaller traders.

This deceptive movement attracts liquidity at specific levels, allowing larger players to execute primary trades in the opposite direction, ultimately causing the price to return to its true path.

The Judas Swing setup functions within two primary time frames, tailored separately for Forex and Stock markets. In the Forex market, the setup uses the 8:15 to 8:30 AM window to identify the high and low points, followed by the 8:30 to 8:45 AM frame to execute the Judas move and identify the CISD Level break, where Order Block and Fair Value Gap (FVG) zones are subsequently detected.

In the Stock market, these time frames shift to 9:15 to 9:30 AM for identifying highs and lows and 9:30 to 9:45 AM for executing the Judas move and CISD Level break.

Concepts such as Order Block and Fair Value Gap (FVG) are crucial in this setup. An Order Block represents a chart region with a high volume of buy or sell orders placed by major financial institutions, marking significant levels where price reacts.

Fair Value Gap (FVG) refers to areas where price has moved rapidly without balance between supply and demand, highlighting zones of potential price action and future liquidity.

Bullish Setup :

Bearish Setup :

🔵 How to Use

The Judas Swing setup enables traders to pinpoint entry and exit points by utilizing Order Block and FVG concepts, helping them align with liquidity-driven moves orchestrated by smart money. This setup applies two distinct time frames for Forex and Stocks to capture early deceptive movements, offering traders optimized entry or exit moments.

🟣 Bullish Setup

In the Bullish Judas Swing setup, the first step is to identify High and Low points within the initial time frame. These levels serve as key points where price may react, forming the basis for analyzing the setup and assisting traders in anticipating future market shifts.

In the second time frame, a critical stage of the bullish setup begins. During this phase, the price may create a false break or Fake Break below the low level, a deceptive move by major players to absorb liquidity. This false move often causes smaller traders to enter positions incorrectly. After this fake-out, the price reverses upward, breaking the CISD Level, a critical point in the market structure, signaling a potential bullish trend.

Upon breaking the CISD Level and reversing upward, the indicator identifies both the Order Block and Fair Value Gap (FVG). The Order Block is an area where major players typically place large buy orders, signaling potential price support. Meanwhile, the FVG marks a region of supply-demand imbalance, signaling areas where price might react.

Ultimately, after these key zones are identified, a trader may open a buy position if the price reaches one of these critical areas—Order Block or FVG—and reacts positively. Trading at these levels enhances the chance of success due to liquidity absorption and support from smart money, marking an opportune time for entering a long position.

🟣 Bearish Setup

In the Bearish Judas Swing setup, analysis begins with marking the High and Low levels in the initial time frame. These levels serve as key zones where price could react, helping to signal possible trend reversals. Identifying these levels is essential for locating significant bearish zones and positioning traders to capitalize on downward movements.

In the second time frame, the primary bearish setup unfolds. During this stage, price may exhibit a Fake Break above the high, causing a brief move upward and misleading smaller traders into incorrect positions. After this false move, the price typically returns downward, breaking the CISD Level—a crucial bearish trend indicator.

With the CISD Level broken and a bearish trend confirmed, the indicator identifies the Order Block and Fair Value Gap (FVG). The Bearish Order Block is a region where smart money places significant sell orders, prompting a negative price reaction. The FVG denotes an area of supply-demand imbalance, signifying potential selling pressure.

When the price reaches one of these critical areas—the Bearish Order Block or FVG—and reacts downward, a trader may initiate a sell position. Entering trades at these levels, due to increased selling pressure and liquidity absorption, offers traders an advantage in profiting from price declines.

🔵 Settings

Market : The indicator allows users to choose between Forex and Stocks, automatically adjusting the time frames for the "Opening Range" and "Trading Permit" accordingly: Forex: 8:15–8:30 AM for identifying High and Low points, and 8:30–8:45 AM for capturing the Judas move and CISD Level break. Stocks: 9:15–9:30 AM for identifying High and Low points, and 9:30–9:45 AM for executing the Judas move and CISD Level break.

Refine Order Block : Enables finer adjustments to Order Block levels for more accurate price responses.

Mitigation Level OB : Allows users to set specific reaction points within an Order Block, including: Proximal: Closest level to the current price. 50% OB: Midpoint of the Order Block. Distal: Farthest level from the current price.

FVG Filter : The Judas Swing indicator includes a filter for Fair Value Gap (FVG), allowing different filtering based on FVG width: FVG Filter Type: Can be set to "Very Aggressive," "Aggressive," "Defensive," or "Very Defensive." Higher defensiveness narrows the FVG width, focusing on narrower gaps.

Mitigation Level FVG : Like the Order Block, you can set price reaction levels for FVG with options such as Proximal, 50% OB, and Distal.

CISD : The Bar Back Check option enables traders to specify the number of past candles checked for identifying the CISD Level, enhancing CISD Level accuracy on the chart.

🔵 Conclusion

The Judas Swing indicator helps traders spot reliable trading opportunities by detecting false price movements and key levels such as Order Block and FVG. With a focus on early market movements, this tool allows traders to align with major market participants, selecting entry and exit points with greater precision, thereby reducing trading risks.

Its extensive customization options enable adjustments for various market types and trading conditions, giving traders the flexibility to optimize their strategies. Based on ICT techniques and liquidity analysis, this indicator can be highly effective for those seeking precision in their entry points.

Overall, Judas Swing empowers traders to capitalize on significant market movements by leveraging price volatility. Offering precise and dependable signals, this tool presents an excellent opportunity for enhancing trading accuracy and improving performance

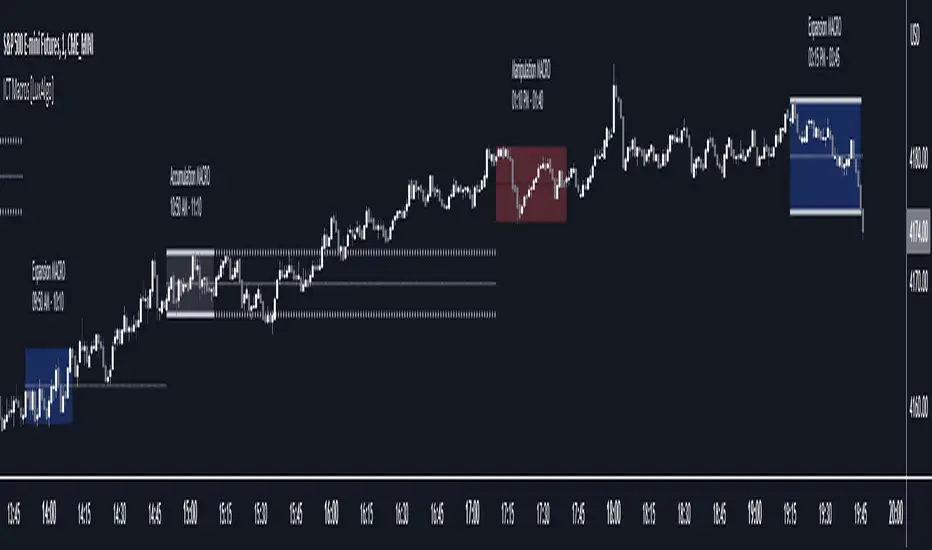

ICT Macros [LuxAlgo]The ICT Macros indicator aims to highlight & classify ICT Macros, which are time intervals where algorithmic trading takes place to interact with existing liquidity or to create new liquidity.

🔶 SETTINGS

🔹 Macros

Macro Time options (such as '09:50 AM 10:10'): Enable specific macro display.

Top Line , Mid Line , Bottom Line and Extending Lines options: Controls the lines for the specific macro.

🔹 Macro Classification

Length : A length to detect Market Structure Brakes and classify macro type based on detection.

Swing Area : Swing or Liquidity Area selection, highest/lowest of the wick or the candle bodies.

Accumulation , Manipulation and Expansion color options for the classified macros.

🔹 Others

Macro Texts : Controls both the size and the visibility of the macro text.

Alert Macro Times in Advance (Minutes) : This option will plot a vertical line presenting the start of the next macro time. The line will not appear all the time, but it will be there based on remaining minutes specified in the option.

Daylight Saving Time (DST) : Adjust time appropriate to Daylight Saving Time of the specific region.

🔶 USAGE

A macro is a way to automate a task or procedure which you perform on a regular basis.

In the context of ICT's teachings, a macro is a small program or set of instructions that unfolds within an algorithm, which influences price movements in the market. These macros operate at specific times and can be related to price runs from one level to another or certain market behaviors during specific time intervals. They help traders anticipate market movements and potential setups during specific time intervals.

To trade these effectively, it is important to understand the time of day when certain macros come into play, and it is strongly advised to introduce the concept of liquidity in your analysis.

Macros can be classified into three categories where the Macro classification is calculated based on the Market Structure prior to macro and the Market Structure during the macro duration:

Manipulation Macro

Manipulation macros are characterized by liquidity being swept both on the buyside and sellside.

Expansion Macro

Expansion macros are characterized by liquidity being swept only on the buyside or sellside. Prices within these macros are highly correlated with the overall trend.

Accumulation Macro

Accumulation macros are characterized by an accumulation of liquidity. Prices within these macros tend to range.

The script returns the maximum/minimum price values reached during the macro interval alongside the average between the maximum/minimum and extends them until a new macro starts. These levels can act as supports and resistances.

🔶 DETAILS

All required data for the macro detection and classification is retrieved using 1 minute data sets, this includes candles as well as pivot/swing highs and lows. This approach guarantees the visually presented objects are same (same highs/lows) on higher timeframes as well as the macro classification remain same as it is in 1 min charts.

8 Macros can be displayed by the script (4 are enabled by default):

02:33 AM 03:00 London Macro

04:03 AM 04:30 London Macro

08:50 AM 09:10 New York Macro

09:50 AM 10:10 New York Macro

10:50 AM 11:10 New York Macro

11:50 AM 12:10 New York Launch Macro

13:10 PM 13:40 New York Macro

15:15 PM 15:45 New York Macro

🔶 ALERTS

When an alert is configured, the user will have the ability to be notified in advance of the next Macro time, where the value specified in 'Alert Macro Times in Advance (Minutes)' option indicates how early to be notified.

🔶 LIMITATIONS

The script is supported on 1 min, 3 mins and 5 mins charts.

🔶 RELATED SCRIPTS

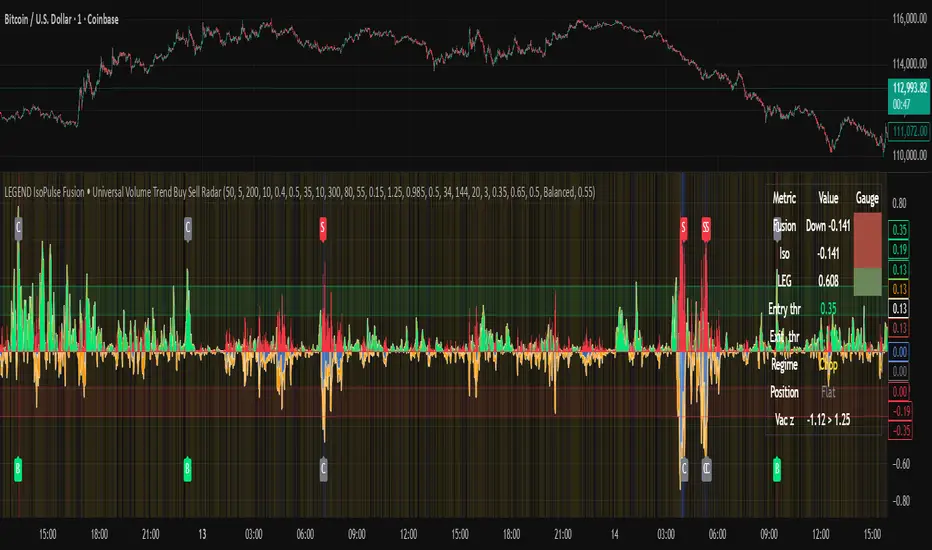

LEGEND IsoPulse Fusion Universal Volume Trend Buy Sell RadarLEGEND IsoPulse Fusion • Universal Volume Trend Buy Sell Radar

One line summary

LEGEND IsoPulse Fusion reads intent from price and volume together, learns which features matter most on your symbol, blends them into a single signed Fusion line in a stable unit range, and emits clear Buy Sell Close events with a structure gate and a liquidity safety gate so you act only when the tape is favorable.

What this script is and why it exists

Many traders keep separate windows for trend, volume, volatility, and regime filters. The result can feel fragmented. This script merges two complementary engines into one consistent view that is easy to read and simple to act on.

LEGEND Tensor estimates directional quality from five causally computed features that are normalized for stationarity. The features are Flow, Tail Pressure with Volume Mix, Path Curvature, Streak Persistence, and Entropy Order.

IsoPulse transforms raw volume into two decaying reservoirs for buy effort and sell effort using body location and wick geometry, then measures price travel per unit volume for efficiency, and detects volume bursts with a recency memory.

Both engines are mapped into the same unit range and fused by a regime aware mixer. When the tape is orderly the mixer leans toward trend features. When the tape is messy but a true push appears in volume efficiency with bursts the mixer allows IsoPulse to speak louder. The outcome is a single Fusion line that lives in a familiar range with calm behavior in quiet periods and expressive pushes when energy concentrates.

What makes it original and useful

Two reservoir volume split . The script assigns a portion of the bar volume to up effort and down effort using body location and wick geometry together. Effort decays through time using a forgetting factor so memory is present without becoming sticky.

Efficiency of move . Price travel per unit volume is often more informative than raw volume or raw range. The script normalizes both sides and centers the efficiency so it becomes signed fuel when multiplied by flow skew.

Burst detection with recency memory . Percent rank of volume highlights bursts. An exponential memory of how recently bursts clustered converts isolated blips into useful context.

Causal adaptive weighting . The LEGEND features do not receive static weights. The script learns, causally, which features have correlated with future returns on your symbol over a rolling window. Only positive contributions are allowed and weights are normalized for interpretability.

Regime aware fusion . Entropy based order and persistence create a mixer that blends IsoPulse with LEGEND. You see a single line rather than two competing panels, which reduces decision conflict.

How to read the screen in seconds

Fusion area . The pane fills above and below zero with a soft gradient. Deeper fill means stronger conviction. The white Fusion line sits on top for precise crossings.

Entry guides and exit guides . Two entry guides draw symmetrically at the active fused entry level. Two exit guides sit inside at a fraction of the entry. Think of them as an adaptive envelope.

Letters . B prints once when the script flips from flat to long. S prints once when the script flips from flat to short. C prints when a held position ends on the appropriate side. T prints when the structure gate first opens. A prints when the liquidity safety flag first appears.

Price bar paint . Bars tint green while long and red while short on the chart to mirror your virtual position.

HUD . A compact dashboard in the corner shows Fusion, IsoPulse, LEGEND, active entry and exit levels, regime status, current virtual position, and the vacuum z value with its avoid threshold.

What signals actually mean

Buy . A Buy prints when the Fusion line crosses above the active entry level while gates are open and the previous state was flat.

Sell . A Sell prints when the Fusion line crosses below the negative entry level while gates are open and the previous state was flat.

Close . A Close prints when Fusion cools back inside the exit envelope or when an opposite cross would occur or when a gate forces a stop, and the previous state was a hold.

Gates . The Trend gate requires sufficient entropy order or significant persistence. The Avoid gate uses a liquidity vacuum z score. Gates exist to protect you from weak tape and poor liquidity.

Inputs and practical tuning

Every input has a tooltip in the script. This section provides a concise reference that you can keep in mind while you work.

Setup

Core window . Controls statistics across features. Scalping often prefers the thirties or low fifties. Intraday often prefers the fifties to eighties. Swing often prefers the eighties to low hundreds. Smaller responds faster with more noise. Larger is calmer.

Smoothing . Short EMA on noisy features. A small value catches micro shifts. A larger value reduces whipsaw.

Fusion and thresholds

Weight lookback . Sample size for weight learning. Use at least five times the horizon. Larger is slower and more confident. Smaller is nimble and more reactive.

Weight horizon . How far ahead return is measured to assess feature value. Smaller favors quick reversion impulses. Larger favors continuation.

Adaptive thresholds . Entry and exit levels from rolling percentiles of the absolute LEGEND score. This self scales across assets and timeframes.

Entry percentile . Eighty selects the top quintile of pushes. Lower to seventy five for more signals. Raise for cleanliness.

Exit percentile . Mid fifties keeps trades honest without overstaying. Sixty holds longer with wider give back.

Order threshold . Minimum structure to trade. Zero point fifteen is a reasonable start. Lower to trade more. Raise to filter chop.

Avoid if Vac z . Liquidity safety level. One point two five is a good default on liquid markets. Thin markets may prefer a slightly higher setting to avoid permanent avoid mode.

IsoPulse

Iso forgetting per bar . Memory for the two reservoirs. Values near zero point nine eight to zero point nine nine five work across many symbols.

Wick weight in effort split . Balance between body location and wick geometry. Values near zero point three to zero point six capture useful behavior.

Efficiency window . Travel per volume window. Lower for snappy symbols. Higher for stability.

Burst percent rank window . Window for percent rank of volume. Around one hundred to three hundred covers most use cases.

Burst recency half life . How long burst clusters matter. Lower for quick fades. Higher for cluster memory.

IsoPulse gain . Pre compression gain before the atan mapping. Tune until the Fusion line lives inside a calm band most of the time with expressive spikes on true pushes.

Continuation and Reversal guides . Visual rails for IsoPulse that help you sense continuation or exhaustion zones. They do not force events.

Entry sensitivity and exit fraction

Entry sensitivity . Loose multiplies the fused entry level by a smaller factor which prints more trades. Strict multiplies by a larger factor which selects fewer and cleaner trades. Balanced is neutral.

Exit fraction . Exit level relative to the entry level in fused unit space. Values around one half to two thirds fit most symbols.

Visuals and UX

Columns and line . Use both to see context and precise crossings. If you present a very clean chart you can turn columns off and keep the line.

HUD . Keep it on while you learn the script. It teaches you how the gates and thresholds respond to your market.

Letters . B S C T A are informative and compact. For screenshots you can toggle them off.

Debug triggers . Show raw crosses even when gates block entries. This is useful when you tune the gates. Turn them off for normal use.

Quick start recipes

Scalping one to five minutes

Core window in the thirties to low fifties.

Horizon around five to eight.

Entry percentile around seventy five.

Exit fraction around zero point five five.

Order threshold around zero point one zero.

Avoid level around one point three zero.

Tune IsoPulse gain until normal Fusion sits inside a calm band and true squeezes push outside.

Intraday five to thirty minutes

Core window around fifty to eighty.

Horizon around ten to twelve.

Entry percentile around eighty.

Exit fraction around zero point five five to zero point six zero.

Order threshold around zero point one five.

Avoid level around one point two five.

Swing one hour to daily

Core window around eighty to one hundred twenty.

Horizon around twelve to twenty.

Entry percentile around eighty to eighty five.

Exit fraction around zero point six zero to zero point seven zero.

Order threshold around zero point two zero.

Avoid level around one point two zero.

How to connect signals to your risk plan

This is an indicator. You remain in control of orders and risk.

Stops . A simple choice is an ATR multiple measured on your chart timeframe. Intraday often prefers one point two five to one point five ATR. Swing often prefers one point five to two ATR. Adjust to symbol behavior and personal risk tolerance.

Exits . The script already prints a Close when Fusion cools inside the exit envelope. If you prefer targets you can mirror the entry envelope distance and convert that to points or percent in your own plan.

Position size . Fixed fractional or fixed risk per trade remains a sound baseline. One percent or less per trade is a common starting point for testing.

Sessions and news . Even with self scaling, some traders prefer to skip the first minutes after an open or scheduled news. Gate with your own session logic if needed.

Limitations and honest notes

No look ahead . The script is causal. The adaptive learner uses a shifted correlation, crosses are evaluated without peeking into the future, and no lookahead security calls are used. If you enable intrabar calculations a letter may appear then disappear before the close if the condition fails. This is normal for any cross based logic in real time.

No performance promises . Markets change. This is a decision aid, not a prediction machine. It will not win every sequence and it cannot guarantee statistical outcomes.

No dependence on other indicators . The chart should remain clean. You can add personal tools in private use but publications should keep the example chart readable.

Standard candles only for public signals . Non standard chart types can change event timing and produce unrealistic sequences. Use regular candles for demonstrations and publications.

Internal logic walkthrough

LEGEND feature block

Flow . Current return normalized by ATR then smoothed by a short EMA. This gives directional intent scaled to recent volatility.

Tail pressure with volume mix . The relative sizes of upper and lower wicks inside the high to low range produce a tail asymmetry. A volume based mix can emphasize wick information when volume is meaningful.

Path curvature . Second difference of close normalized by ATR and smoothed. This captures changes in impulse shape that can precede pushes or fades.

Streak persistence . Up and down close streaks are counted and netted. The result is normalized for the window length to keep behavior stable across symbols.

Entropy order . Shannon entropy of the probability of an up close. Lower entropy means more order. The value is oriented by Flow to preserve sign.

Causal weights . Each feature becomes a z score. A shifted correlation against future returns over the horizon produces a positive weight per feature. Weights are normalized so they sum to one for clarity. The result is angle mapped into a compact unit.

IsoPulse block

Effort split . The script estimates up effort and down effort per bar using both body location and wick geometry. Effort is integrated through time into two reservoirs using a forgetting factor.

Skew . The reservoir difference over the sum yields a stable skew in a known range. A short EMA smooths it.

Efficiency . Move size divided by average volume produces travel per unit volume. Normalization and centering around zero produce a symmetric measure.

Bursts and recency . Percent rank of volume highlights bursts. An exponential function of bars since last burst adds the notion of cluster memory.

IsoPulse unit . Skew multiplied by centered efficiency then scaled by the burst factor produces the raw IsoPulse that is angle mapped into the unit range.

Fusion and events

Regime factor . Entropy order and streak persistence form a mixer. Low structure favors IsoPulse. Higher structure favors LEGEND. The blend is convex so it remains interpretable.

Blended guides . Entry and exit guides are blended in the same way as the line so they stay consistent when regimes change. The envelope does not jump unexpectedly.

Virtual position . The script maintains state. Buy and Sell require a cross while flat and gates open. Close requires an exit or force condition while holding. Letters print once at the state change.

Disclosures

This script and description are educational. They do not constitute investment advice. Markets involve risk. You are responsible for your own decisions and for compliance with local rules. The logic is causal and does not look ahead. Signals on non standard chart types can be misleading and are not recommended for publication. When you test a strategy wrapper, use realistic commission and slippage, moderate risk per trade, and enough trades to form a meaningful sample, then document those assumptions if you share results.

Closing thoughts

Clarity builds confidence. The Fusion line gives a single view of intent. The letters communicate action without clutter. The HUD confirms context at a glance. The gates protect you from weak tape and poor liquidity. Tune it to your instrument, observe it across regimes, and use it as a consistent lens rather than a prediction oracle. The goal is not to trade every wiggle. The goal is to pick your spots with a calm process and to stand aside when the tape is not inviting.

Marubozu Detector with Dynamic SL/TP

Strategy Overview:

This indicator detects a "Marubozu" bullish pattern or a “Marubozu” bearish pattern to suggest potential buy and sell opportunities. It uses dynamic Stop Loss (SL) and Take Profit (TP) management, based on either market volatility (ATR) or liquidity zones.

This tool is intended for educational and informational purposes only.

Key Features:

Entry: Based on detecting Marubozu bullish or bearish candle pattern.

Exit: Targets are managed through ATR multiples or previous liquidity levels (swing highs or swing lows).

Smart Liquidity: Optionally identify deeper liquidity targets.

Full Alerts: Buy and Sell signals supported with customizable alerts.

Visualized Trades: Entry, SL, and TP levels are plotted on the chart.

User Inputs:

ATR Length, ATR Multipliers

Take Profit Mode (Liquidity/ATR)

Swing Lookback and Strength

Toggleable Buy/Sell alerts

All Time Frames

📖 How to Use:

Add the Indicator:

Apply the script to your chart from the TradingView indicators panel.

Look for Buy Signals:

A buy signal is triggered when the script detects a "Marubozu" bullish pattern.

Entry, Stop Loss, and Take Profit levels are plotted automatically.

Look for Sell Signals:

A Sell signal is triggered when the script detects a "Marubozu" bearish pattern.

Entry, Stop Loss, and Take Profit levels are plotted automatically.

Choose Take Profit Mode:

ATR Mode: TP is based on a volatility target.

Liquidity Mode: TP is based on past swing highs.

Set Alerts (Optional):

Enable Buy/Sell alerts in the settings to receive real-time notifications.

Practice First:

Always backtest and paper trade before live use.

📜 Disclaimer:

This script does not offer financial advice.

No guarantees of profit or performance are made.

Use in demo accounts or backtesting first.

Always practice proper risk management and seek advice from licensed professionals if needed.

✅ Script Compliance:

This script is designed in full accordance with TradingView’s House Rules for educational tools.

No financial advice is provided, no performance is guaranteed, and users are encouraged to backtest thoroughly.

LIT - ConfirmationsOverview

The LIT - Confirmations Indicator is a dynamic checklist tool designed for traders who uses LIT Strategy (Liquidity Inducement Theory) following liquidity and smart money concepts as benefit. This tool allows users to document and track essential trading confirmations directly on their TradingView charts, offering a structured and visual approach to market analysis.

What Makes This Unique?

Unlike other open-source tools, the LIT - Confirmations Indicator introduces a fully interactive and customizable table directly on the chart. This table provides real-time feedback with clear ✅ (checked) and ❌ (unchecked) visual indicators for each confirmation. The user can position the table on the chart according to their preference, ensuring it integrates seamlessly into their trading workflow without obscuring critical chart data.

How It Works

1. Predefined Confirmations

The indicator includes a set of commonly used trading confirmations:

Identify Liquidity: Mark areas where liquidity might pool.

Inducement: Confirm the presence of inducements before market reversals.

Relevant Break of Structure (BOS): Validate critical structural changes.

Mitigation after RBoS: Check for mitigation following a BOS.

Smart Money Trap (SMT): Identify traps often utilized by smart money.

Timing: Ensure trades are entered during high-probability time windows.

Mitigation to the Leftside: Confirm whether price action aligns with prior mitigations.

Set Targets: Define and document logical take-profit or stop-loss levels.

2.Interactive Table Display

A table is dynamically created on the chart, showing all confirmations with their current state (checked or unchecked).

Users can choose the position of the table (top, middle, or bottom and left, center, or right) and customize its background color for better visibility.

3. Customization

All confirmations are toggled through the input settings, allowing traders to adapt the indicator to their unique strategies.