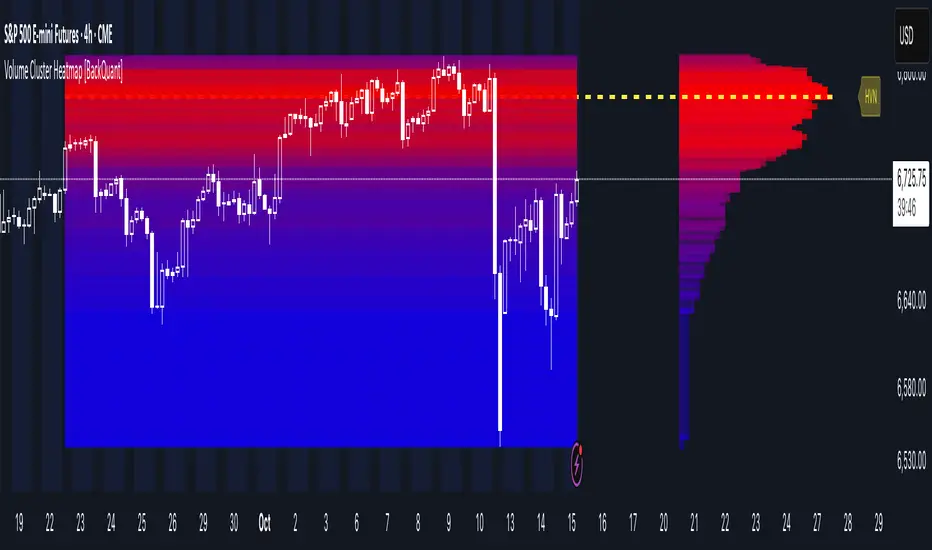

Volume Cluster Heatmap [BackQuant]Volume Cluster Heatmap

A visualization tool that maps traded volume across price levels over a chosen lookback period. It highlights where the market builds balance through heavy participation and where it moves efficiently through low-volume zones. By combining a heatmap, volume profile, and high/low volume node detection, this indicator reveals structural areas of support, resistance, and liquidity that drive price behavior.

What Are Volume Clusters?

A volume cluster is a horizontal aggregation of traded volume at specific price levels, showing where market participants concentrated their buying and selling.

High Volume Nodes (HVN) : Price levels with significant trading activity; often act as support or resistance.

Low Volume Nodes (LVN) : Price levels with little trading activity; price moves quickly through these areas, reflecting low liquidity.

Volume clusters help identify key structural zones, reveal potential reversals, and gauge market efficiency by highlighting where the market is balanced versus areas of thin liquidity.

By creating heatmaps, profiles, and highlighting high and low volume nodes (HVNs and LVNs), it allows traders to see where the market builds balance and where it moves efficiently through thin liquidity zones.

Example: Bitcoin breaking away from the high-volume zone near 118k and moving cleanly through the low-volume pocket around 113k–115k, illustrating how markets seek efficiency:

Core Features

Visual Analysis Components:

Heatmap Display : Displays volume intensity as colored boxes, lines, or a combination for a dynamic view of market participation.

Volume Profile Overlay : Shows cumulative volume per price level along the right-hand side of the chart.

HVN & LVN Labels : Marks high and low volume nodes with color-coded lines and labels.

Customizable Colors & Transparency : Adjust high and low volume colors and minimum transparency for clear differentiation.

Session Reset & Timeframe Control : Dynamically resets clusters at the start of new sessions or chosen timeframes (intraday, daily, weekly).

Alerts

HVN / LVN Alerts : Notify when price reaches a significant high or low volume node.

High Volume Zone Alerts : Trigger when price enters the top X% of cumulative volume, signaling key areas of market interest.

How It Works

Each bar’s volume is distributed proportionally across the horizontal price levels it touches. Over the lookback period, this builds a cumulative volume profile, identifying price levels with the most and least trading activity. The highest cumulative volume levels become HVNs, while the lowest are LVNs. A side volume profile shows aggregated volume per level, and a heatmap overlay visually reinforces market structure.

Applications for Traders

Identify strong support and resistance at HVNs.

Detect areas of low liquidity where price may move quickly (LVNs).

Determine market balance zones where price may consolidate.

Filter noise: because volume clusters aggregate activity into levels, minor fluctuations and irrelevant micro-moves are removed, simplifying analysis and improving strategy development.

Combine with other indicators such as VWAP, Supertrend, or CVD for higher-probability entries and exits.

Use volume clusters to anticipate price reactions to breaking points in thin liquidity zones.

Advanced Display Options

Heatmap Styles : Boxes, lines, or both. Boxes provide a traditional heatmap, lines are better for high granularity data.

Line Mode Example : Simplified line visualization for easier reading at high level counts:

Profile Width & Offset : Adjust spacing and placement of the volume profile for clarity alongside price.

Transparency Control : Lower transparency for more opaque visualization of high-volume zones.

Best Practices for Usage

Reduce the number of levels when using line mode to avoid clutter.

Use HVN and LVN markers in conjunction with volume profiles to plan entries and exits.

Apply session resets to monitor intraday vs. multi-day volume accumulation.

Combine with other technical indicators to confirm high-probability trading signals.

Watch price interactions with LVNs for potential rapid movements and with HVNs for possible support/resistance or reversals.

Technical Notes

Each bar contributes volume proportionally to the price levels it spans, creating a dynamic and accurate representation of traded interest.

Volume profiles are scaled and offset for visual clarity alongside live price.

Alerts are fully integrated for HVN/LVN interaction and high-volume zone entries.

Optimized to handle large lookback windows and numerous price levels efficiently without performance degradation.

This indicator is ideal for understanding market structure, detecting key liquidity areas, and filtering out noise to model price more accurately in high-frequency or algorithmic strategies.

"liquidity" için komut dosyalarını ara

Opening Range Gaps [TakingProphets]What is an Opening Range Gap (ORG)?

In ICT, the Opening Range Gap is defined as the price difference between the previous session’s close (e.g., 4:00 PM EST in U.S. indices) and the current day’s open (9:30 AM EST).

That gap is a liquidity void—an area where no trading occurred during regular hours.

Why ICT Traders Care About ORG

Liquidity Void (Gap Fill Logic)

-Because the gap is an untraded area, it naturally acts as a draw on liquidity.

-Price often seeks to rebalance by retracing into or fully filling this void.

Premium/Discount Sensitivity

-Once the ORG is defined, ICT treats it as a mini dealing range.

-Above EQ (Consequent Encroachment) = algorithmic premium (sell-sensitive).

-Below EQ = algorithmic discount (buy-sensitive).

-Price reaction at these levels gives a precise read on institutional intent intraday.

Support/Resistance from ORG

-If the session opens above prior close, the gap often acts as support until violated.

-If the session opens below prior close, the gap often acts as resistance until reclaimed.

Key ICT Concepts Anchored to ORG

Consequent Encroachment (CE): The midpoint of the gap. The algo is highly sensitive to CE as a decision point: reject → continuation; reclaim → reversal.

Draw on Liquidity (DoL): Price is algorithmically “pulled” toward gap fills, CE, or the opposite side of the ORG.

Order Flow Confirmation: If price ignores the gap and runs away from it, this signals strong institutional order flow in that direction.

Confluence with Other Tools: FVGs, OBs, and HTF PD arrays often overlap with ORG levels, strengthening setups.

Practical Application for Traders

Bias Formation:

Use ORG EQ as a line in the sand for intraday bias.

If price trades below ORG EQ after the open → look for short setups into the prior day’s low or external liquidity.

If price trades above ORG EQ → favor longs into highs/liquidity pools.

Execution Framework:

Wait for liquidity raids or market structure shifts at ORG edges (.00, .25, .50, .75).

Target: EQ, opposite quarter, or full gap fill.

Precision Reads:

ORG lines let traders anticipate where algorithms are likely to respond, providing mechanical invalidation and clear targets without clutter.

Marubozu Detector with Dynamic SL/TP

Strategy Overview:

This indicator detects a "Marubozu" bullish pattern or a “Marubozu” bearish pattern to suggest potential buy and sell opportunities. It uses dynamic Stop Loss (SL) and Take Profit (TP) management, based on either market volatility (ATR) or liquidity zones.

This tool is intended for educational and informational purposes only.

Key Features:

Entry: Based on detecting Marubozu bullish or bearish candle pattern.

Exit: Targets are managed through ATR multiples or previous liquidity levels (swing highs or swing lows).

Smart Liquidity: Optionally identify deeper liquidity targets.

Full Alerts: Buy and Sell signals supported with customizable alerts.

Visualized Trades: Entry, SL, and TP levels are plotted on the chart.

User Inputs:

ATR Length, ATR Multipliers

Take Profit Mode (Liquidity/ATR)

Swing Lookback and Strength

Toggleable Buy/Sell alerts

All Time Frames

📖 How to Use:

Add the Indicator:

Apply the script to your chart from the TradingView indicators panel.

Look for Buy Signals:

A buy signal is triggered when the script detects a "Marubozu" bullish pattern.

Entry, Stop Loss, and Take Profit levels are plotted automatically.

Look for Sell Signals:

A Sell signal is triggered when the script detects a "Marubozu" bearish pattern.

Entry, Stop Loss, and Take Profit levels are plotted automatically.

Choose Take Profit Mode:

ATR Mode: TP is based on a volatility target.

Liquidity Mode: TP is based on past swing highs.

Set Alerts (Optional):

Enable Buy/Sell alerts in the settings to receive real-time notifications.

Practice First:

Always backtest and paper trade before live use.

📜 Disclaimer:

This script does not offer financial advice.

No guarantees of profit or performance are made.

Use in demo accounts or backtesting first.

Always practice proper risk management and seek advice from licensed professionals if needed.

✅ Script Compliance:

This script is designed in full accordance with TradingView’s House Rules for educational tools.

No financial advice is provided, no performance is guaranteed, and users are encouraged to backtest thoroughly.

Ultra VolumeVisualizes volume intensity using dynamic color gradients and percentile thresholds. Includes optional SMA, bar coloring, and adaptive liquidity boxes to highlight high- and low-volume zones in real time.

Introduction

The Ultra Volume indicator enhances volume analysis by categorizing volume bars into percentile-based intensity levels. It uses color-coded gradients to quickly identify periods of unusually high or low activity. The script also includes an optional simple moving average (SMA), bar coloring, and visual box overlays to highlight zones of significant liquidity shifts.

Detailed Description

.........

Volume Classification

Volume is segmented into five tiers: Extra High, High, Medium, Normal, and Low, using percentile ranks calculated over a dynamically adjusted historical window. This segmentation adapts based on the chart's timeframe – using 100 bars for daily and 1440/minutes for intraday – allowing for consistent behavior across resolutions.

.....

Color Gradients

Each volume bar is colored based on its percentile category, smoothly transitioning between thresholds for visual clarity. This makes it easy to spot volume spikes or droughts relative to recent history.

.....

Simple Moving Average (SMA)

An optional SMA can be plotted on top of the volume bars for trend comparison and baseline reference. Its length and color are fully customizable.

.....

Bar Coloring

You can optionally color the chart's candlesticks to reflect the same volume intensity as the histogram bars, reinforcing visual cues across the chart.

.....

Liquidity Boxes

Two adaptive box systems highlight zones of increased or decreased liquidity:

High Liquidity Boxes expand upward when price exceeds the previous box’s top.

Low Liquidity Boxes expand downward when price breaks the previous box’s bottom.

These boxes persist and auto-adjust over time unless reset, helping traders spot key zones of volume-driven price action.

.....

Box Indexing

A configurable index shift determines how far back in the chart the boxes originate. Setting this to 501 makes them "stick" to the candle where they were first created.

.....

Data Handling

A safety check ensures the script throws an error if volume data is unavailable (e.g., for some crypto or CFD symbols).

.........

Summary

Ultra Volume is a practical tool for traders who want more than just raw volume bars. With intelligent percentile-based classification, real-time adaptive liquidity zones, and fully customizable visual elements, it turns volume into a highly readable, actionable signal.

ICT Setup 03 [TradingFinder] Judas Swing NY 9:30am + CHoCH/FVG🔵 Introduction

Judas Swing is an advanced trading setup designed to identify false price movements early in the trading day. This advanced trading strategy operates on the principle that major market players, or "smart money," drive price in a certain direction during the early hours to mislead smaller traders.

This deceptive movement attracts liquidity at specific levels, allowing larger players to execute primary trades in the opposite direction, ultimately causing the price to return to its true path.

The Judas Swing setup functions within two primary time frames, tailored separately for Forex and Stock markets. In the Forex market, the setup uses the 8:15 to 8:30 AM window to identify the high and low points, followed by the 8:30 to 8:45 AM frame to execute the Judas move and identify the CISD Level break, where Order Block and Fair Value Gap (FVG) zones are subsequently detected.

In the Stock market, these time frames shift to 9:15 to 9:30 AM for identifying highs and lows and 9:30 to 9:45 AM for executing the Judas move and CISD Level break.

Concepts such as Order Block and Fair Value Gap (FVG) are crucial in this setup. An Order Block represents a chart region with a high volume of buy or sell orders placed by major financial institutions, marking significant levels where price reacts.

Fair Value Gap (FVG) refers to areas where price has moved rapidly without balance between supply and demand, highlighting zones of potential price action and future liquidity.

Bullish Setup :

Bearish Setup :

🔵 How to Use

The Judas Swing setup enables traders to pinpoint entry and exit points by utilizing Order Block and FVG concepts, helping them align with liquidity-driven moves orchestrated by smart money. This setup applies two distinct time frames for Forex and Stocks to capture early deceptive movements, offering traders optimized entry or exit moments.

🟣 Bullish Setup

In the Bullish Judas Swing setup, the first step is to identify High and Low points within the initial time frame. These levels serve as key points where price may react, forming the basis for analyzing the setup and assisting traders in anticipating future market shifts.

In the second time frame, a critical stage of the bullish setup begins. During this phase, the price may create a false break or Fake Break below the low level, a deceptive move by major players to absorb liquidity. This false move often causes smaller traders to enter positions incorrectly. After this fake-out, the price reverses upward, breaking the CISD Level, a critical point in the market structure, signaling a potential bullish trend.

Upon breaking the CISD Level and reversing upward, the indicator identifies both the Order Block and Fair Value Gap (FVG). The Order Block is an area where major players typically place large buy orders, signaling potential price support. Meanwhile, the FVG marks a region of supply-demand imbalance, signaling areas where price might react.

Ultimately, after these key zones are identified, a trader may open a buy position if the price reaches one of these critical areas—Order Block or FVG—and reacts positively. Trading at these levels enhances the chance of success due to liquidity absorption and support from smart money, marking an opportune time for entering a long position.

🟣 Bearish Setup

In the Bearish Judas Swing setup, analysis begins with marking the High and Low levels in the initial time frame. These levels serve as key zones where price could react, helping to signal possible trend reversals. Identifying these levels is essential for locating significant bearish zones and positioning traders to capitalize on downward movements.

In the second time frame, the primary bearish setup unfolds. During this stage, price may exhibit a Fake Break above the high, causing a brief move upward and misleading smaller traders into incorrect positions. After this false move, the price typically returns downward, breaking the CISD Level—a crucial bearish trend indicator.

With the CISD Level broken and a bearish trend confirmed, the indicator identifies the Order Block and Fair Value Gap (FVG). The Bearish Order Block is a region where smart money places significant sell orders, prompting a negative price reaction. The FVG denotes an area of supply-demand imbalance, signifying potential selling pressure.

When the price reaches one of these critical areas—the Bearish Order Block or FVG—and reacts downward, a trader may initiate a sell position. Entering trades at these levels, due to increased selling pressure and liquidity absorption, offers traders an advantage in profiting from price declines.

🔵 Settings

Market : The indicator allows users to choose between Forex and Stocks, automatically adjusting the time frames for the "Opening Range" and "Trading Permit" accordingly: Forex: 8:15–8:30 AM for identifying High and Low points, and 8:30–8:45 AM for capturing the Judas move and CISD Level break. Stocks: 9:15–9:30 AM for identifying High and Low points, and 9:30–9:45 AM for executing the Judas move and CISD Level break.

Refine Order Block : Enables finer adjustments to Order Block levels for more accurate price responses.

Mitigation Level OB : Allows users to set specific reaction points within an Order Block, including: Proximal: Closest level to the current price. 50% OB: Midpoint of the Order Block. Distal: Farthest level from the current price.

FVG Filter : The Judas Swing indicator includes a filter for Fair Value Gap (FVG), allowing different filtering based on FVG width: FVG Filter Type: Can be set to "Very Aggressive," "Aggressive," "Defensive," or "Very Defensive." Higher defensiveness narrows the FVG width, focusing on narrower gaps.

Mitigation Level FVG : Like the Order Block, you can set price reaction levels for FVG with options such as Proximal, 50% OB, and Distal.

CISD : The Bar Back Check option enables traders to specify the number of past candles checked for identifying the CISD Level, enhancing CISD Level accuracy on the chart.

🔵 Conclusion

The Judas Swing indicator helps traders spot reliable trading opportunities by detecting false price movements and key levels such as Order Block and FVG. With a focus on early market movements, this tool allows traders to align with major market participants, selecting entry and exit points with greater precision, thereby reducing trading risks.

Its extensive customization options enable adjustments for various market types and trading conditions, giving traders the flexibility to optimize their strategies. Based on ICT techniques and liquidity analysis, this indicator can be highly effective for those seeking precision in their entry points.

Overall, Judas Swing empowers traders to capitalize on significant market movements by leveraging price volatility. Offering precise and dependable signals, this tool presents an excellent opportunity for enhancing trading accuracy and improving performance

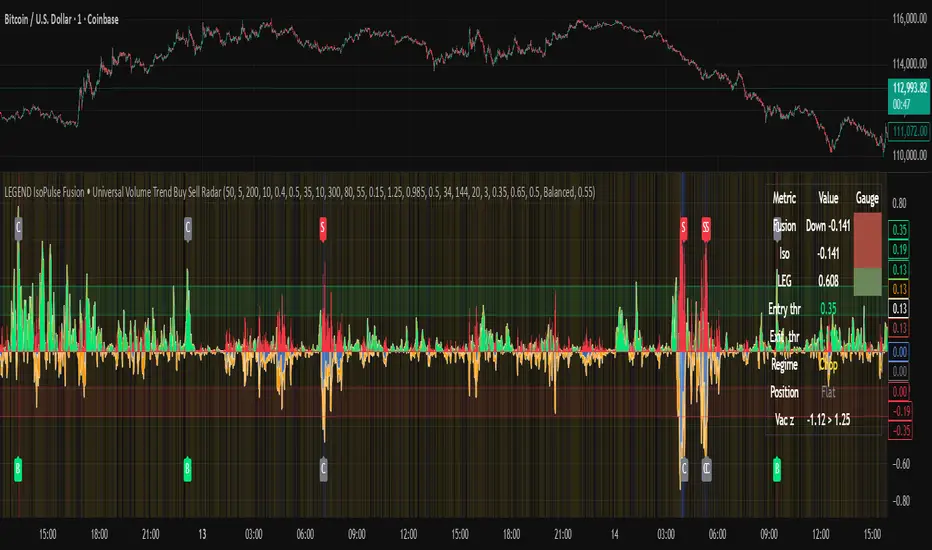

LEGEND IsoPulse Fusion Universal Volume Trend Buy Sell RadarLEGEND IsoPulse Fusion • Universal Volume Trend Buy Sell Radar

One line summary

LEGEND IsoPulse Fusion reads intent from price and volume together, learns which features matter most on your symbol, blends them into a single signed Fusion line in a stable unit range, and emits clear Buy Sell Close events with a structure gate and a liquidity safety gate so you act only when the tape is favorable.

What this script is and why it exists

Many traders keep separate windows for trend, volume, volatility, and regime filters. The result can feel fragmented. This script merges two complementary engines into one consistent view that is easy to read and simple to act on.

LEGEND Tensor estimates directional quality from five causally computed features that are normalized for stationarity. The features are Flow, Tail Pressure with Volume Mix, Path Curvature, Streak Persistence, and Entropy Order.

IsoPulse transforms raw volume into two decaying reservoirs for buy effort and sell effort using body location and wick geometry, then measures price travel per unit volume for efficiency, and detects volume bursts with a recency memory.

Both engines are mapped into the same unit range and fused by a regime aware mixer. When the tape is orderly the mixer leans toward trend features. When the tape is messy but a true push appears in volume efficiency with bursts the mixer allows IsoPulse to speak louder. The outcome is a single Fusion line that lives in a familiar range with calm behavior in quiet periods and expressive pushes when energy concentrates.

What makes it original and useful

Two reservoir volume split . The script assigns a portion of the bar volume to up effort and down effort using body location and wick geometry together. Effort decays through time using a forgetting factor so memory is present without becoming sticky.

Efficiency of move . Price travel per unit volume is often more informative than raw volume or raw range. The script normalizes both sides and centers the efficiency so it becomes signed fuel when multiplied by flow skew.

Burst detection with recency memory . Percent rank of volume highlights bursts. An exponential memory of how recently bursts clustered converts isolated blips into useful context.

Causal adaptive weighting . The LEGEND features do not receive static weights. The script learns, causally, which features have correlated with future returns on your symbol over a rolling window. Only positive contributions are allowed and weights are normalized for interpretability.

Regime aware fusion . Entropy based order and persistence create a mixer that blends IsoPulse with LEGEND. You see a single line rather than two competing panels, which reduces decision conflict.

How to read the screen in seconds

Fusion area . The pane fills above and below zero with a soft gradient. Deeper fill means stronger conviction. The white Fusion line sits on top for precise crossings.

Entry guides and exit guides . Two entry guides draw symmetrically at the active fused entry level. Two exit guides sit inside at a fraction of the entry. Think of them as an adaptive envelope.

Letters . B prints once when the script flips from flat to long. S prints once when the script flips from flat to short. C prints when a held position ends on the appropriate side. T prints when the structure gate first opens. A prints when the liquidity safety flag first appears.

Price bar paint . Bars tint green while long and red while short on the chart to mirror your virtual position.

HUD . A compact dashboard in the corner shows Fusion, IsoPulse, LEGEND, active entry and exit levels, regime status, current virtual position, and the vacuum z value with its avoid threshold.

What signals actually mean

Buy . A Buy prints when the Fusion line crosses above the active entry level while gates are open and the previous state was flat.

Sell . A Sell prints when the Fusion line crosses below the negative entry level while gates are open and the previous state was flat.

Close . A Close prints when Fusion cools back inside the exit envelope or when an opposite cross would occur or when a gate forces a stop, and the previous state was a hold.

Gates . The Trend gate requires sufficient entropy order or significant persistence. The Avoid gate uses a liquidity vacuum z score. Gates exist to protect you from weak tape and poor liquidity.

Inputs and practical tuning

Every input has a tooltip in the script. This section provides a concise reference that you can keep in mind while you work.

Setup

Core window . Controls statistics across features. Scalping often prefers the thirties or low fifties. Intraday often prefers the fifties to eighties. Swing often prefers the eighties to low hundreds. Smaller responds faster with more noise. Larger is calmer.

Smoothing . Short EMA on noisy features. A small value catches micro shifts. A larger value reduces whipsaw.

Fusion and thresholds

Weight lookback . Sample size for weight learning. Use at least five times the horizon. Larger is slower and more confident. Smaller is nimble and more reactive.

Weight horizon . How far ahead return is measured to assess feature value. Smaller favors quick reversion impulses. Larger favors continuation.

Adaptive thresholds . Entry and exit levels from rolling percentiles of the absolute LEGEND score. This self scales across assets and timeframes.

Entry percentile . Eighty selects the top quintile of pushes. Lower to seventy five for more signals. Raise for cleanliness.

Exit percentile . Mid fifties keeps trades honest without overstaying. Sixty holds longer with wider give back.

Order threshold . Minimum structure to trade. Zero point fifteen is a reasonable start. Lower to trade more. Raise to filter chop.

Avoid if Vac z . Liquidity safety level. One point two five is a good default on liquid markets. Thin markets may prefer a slightly higher setting to avoid permanent avoid mode.

IsoPulse

Iso forgetting per bar . Memory for the two reservoirs. Values near zero point nine eight to zero point nine nine five work across many symbols.

Wick weight in effort split . Balance between body location and wick geometry. Values near zero point three to zero point six capture useful behavior.

Efficiency window . Travel per volume window. Lower for snappy symbols. Higher for stability.

Burst percent rank window . Window for percent rank of volume. Around one hundred to three hundred covers most use cases.

Burst recency half life . How long burst clusters matter. Lower for quick fades. Higher for cluster memory.

IsoPulse gain . Pre compression gain before the atan mapping. Tune until the Fusion line lives inside a calm band most of the time with expressive spikes on true pushes.

Continuation and Reversal guides . Visual rails for IsoPulse that help you sense continuation or exhaustion zones. They do not force events.

Entry sensitivity and exit fraction

Entry sensitivity . Loose multiplies the fused entry level by a smaller factor which prints more trades. Strict multiplies by a larger factor which selects fewer and cleaner trades. Balanced is neutral.

Exit fraction . Exit level relative to the entry level in fused unit space. Values around one half to two thirds fit most symbols.

Visuals and UX

Columns and line . Use both to see context and precise crossings. If you present a very clean chart you can turn columns off and keep the line.

HUD . Keep it on while you learn the script. It teaches you how the gates and thresholds respond to your market.

Letters . B S C T A are informative and compact. For screenshots you can toggle them off.

Debug triggers . Show raw crosses even when gates block entries. This is useful when you tune the gates. Turn them off for normal use.

Quick start recipes

Scalping one to five minutes

Core window in the thirties to low fifties.

Horizon around five to eight.

Entry percentile around seventy five.

Exit fraction around zero point five five.

Order threshold around zero point one zero.

Avoid level around one point three zero.

Tune IsoPulse gain until normal Fusion sits inside a calm band and true squeezes push outside.

Intraday five to thirty minutes

Core window around fifty to eighty.

Horizon around ten to twelve.

Entry percentile around eighty.

Exit fraction around zero point five five to zero point six zero.

Order threshold around zero point one five.

Avoid level around one point two five.

Swing one hour to daily

Core window around eighty to one hundred twenty.

Horizon around twelve to twenty.

Entry percentile around eighty to eighty five.

Exit fraction around zero point six zero to zero point seven zero.

Order threshold around zero point two zero.

Avoid level around one point two zero.

How to connect signals to your risk plan

This is an indicator. You remain in control of orders and risk.

Stops . A simple choice is an ATR multiple measured on your chart timeframe. Intraday often prefers one point two five to one point five ATR. Swing often prefers one point five to two ATR. Adjust to symbol behavior and personal risk tolerance.

Exits . The script already prints a Close when Fusion cools inside the exit envelope. If you prefer targets you can mirror the entry envelope distance and convert that to points or percent in your own plan.

Position size . Fixed fractional or fixed risk per trade remains a sound baseline. One percent or less per trade is a common starting point for testing.

Sessions and news . Even with self scaling, some traders prefer to skip the first minutes after an open or scheduled news. Gate with your own session logic if needed.

Limitations and honest notes

No look ahead . The script is causal. The adaptive learner uses a shifted correlation, crosses are evaluated without peeking into the future, and no lookahead security calls are used. If you enable intrabar calculations a letter may appear then disappear before the close if the condition fails. This is normal for any cross based logic in real time.

No performance promises . Markets change. This is a decision aid, not a prediction machine. It will not win every sequence and it cannot guarantee statistical outcomes.

No dependence on other indicators . The chart should remain clean. You can add personal tools in private use but publications should keep the example chart readable.

Standard candles only for public signals . Non standard chart types can change event timing and produce unrealistic sequences. Use regular candles for demonstrations and publications.

Internal logic walkthrough

LEGEND feature block

Flow . Current return normalized by ATR then smoothed by a short EMA. This gives directional intent scaled to recent volatility.

Tail pressure with volume mix . The relative sizes of upper and lower wicks inside the high to low range produce a tail asymmetry. A volume based mix can emphasize wick information when volume is meaningful.

Path curvature . Second difference of close normalized by ATR and smoothed. This captures changes in impulse shape that can precede pushes or fades.

Streak persistence . Up and down close streaks are counted and netted. The result is normalized for the window length to keep behavior stable across symbols.

Entropy order . Shannon entropy of the probability of an up close. Lower entropy means more order. The value is oriented by Flow to preserve sign.

Causal weights . Each feature becomes a z score. A shifted correlation against future returns over the horizon produces a positive weight per feature. Weights are normalized so they sum to one for clarity. The result is angle mapped into a compact unit.

IsoPulse block

Effort split . The script estimates up effort and down effort per bar using both body location and wick geometry. Effort is integrated through time into two reservoirs using a forgetting factor.

Skew . The reservoir difference over the sum yields a stable skew in a known range. A short EMA smooths it.

Efficiency . Move size divided by average volume produces travel per unit volume. Normalization and centering around zero produce a symmetric measure.

Bursts and recency . Percent rank of volume highlights bursts. An exponential function of bars since last burst adds the notion of cluster memory.

IsoPulse unit . Skew multiplied by centered efficiency then scaled by the burst factor produces the raw IsoPulse that is angle mapped into the unit range.

Fusion and events

Regime factor . Entropy order and streak persistence form a mixer. Low structure favors IsoPulse. Higher structure favors LEGEND. The blend is convex so it remains interpretable.

Blended guides . Entry and exit guides are blended in the same way as the line so they stay consistent when regimes change. The envelope does not jump unexpectedly.

Virtual position . The script maintains state. Buy and Sell require a cross while flat and gates open. Close requires an exit or force condition while holding. Letters print once at the state change.

Disclosures

This script and description are educational. They do not constitute investment advice. Markets involve risk. You are responsible for your own decisions and for compliance with local rules. The logic is causal and does not look ahead. Signals on non standard chart types can be misleading and are not recommended for publication. When you test a strategy wrapper, use realistic commission and slippage, moderate risk per trade, and enough trades to form a meaningful sample, then document those assumptions if you share results.

Closing thoughts

Clarity builds confidence. The Fusion line gives a single view of intent. The letters communicate action without clutter. The HUD confirms context at a glance. The gates protect you from weak tape and poor liquidity. Tune it to your instrument, observe it across regimes, and use it as a consistent lens rather than a prediction oracle. The goal is not to trade every wiggle. The goal is to pick your spots with a calm process and to stand aside when the tape is not inviting.

LIT - ConfirmationsOverview

The LIT - Confirmations Indicator is a dynamic checklist tool designed for traders who uses LIT Strategy (Liquidity Inducement Theory) following liquidity and smart money concepts as benefit. This tool allows users to document and track essential trading confirmations directly on their TradingView charts, offering a structured and visual approach to market analysis.

What Makes This Unique?

Unlike other open-source tools, the LIT - Confirmations Indicator introduces a fully interactive and customizable table directly on the chart. This table provides real-time feedback with clear ✅ (checked) and ❌ (unchecked) visual indicators for each confirmation. The user can position the table on the chart according to their preference, ensuring it integrates seamlessly into their trading workflow without obscuring critical chart data.

How It Works

1. Predefined Confirmations

The indicator includes a set of commonly used trading confirmations:

Identify Liquidity: Mark areas where liquidity might pool.

Inducement: Confirm the presence of inducements before market reversals.

Relevant Break of Structure (BOS): Validate critical structural changes.

Mitigation after RBoS: Check for mitigation following a BOS.

Smart Money Trap (SMT): Identify traps often utilized by smart money.

Timing: Ensure trades are entered during high-probability time windows.

Mitigation to the Leftside: Confirm whether price action aligns with prior mitigations.

Set Targets: Define and document logical take-profit or stop-loss levels.

2.Interactive Table Display

A table is dynamically created on the chart, showing all confirmations with their current state (checked or unchecked).

Users can choose the position of the table (top, middle, or bottom and left, center, or right) and customize its background color for better visibility.

3. Customization

All confirmations are toggled through the input settings, allowing traders to adapt the indicator to their unique strategies.

The display can be easily adjusted to match the trader’s preferences without cluttering the chart.

How to Use

1. Add the indicator to your chart.

2. Open the settings panel to activate the relevant confirmations for your analysis.

3. Use the Display Settings section to adjust the table's position and background color.

4. View the table on your chart to track selected confirmations in real-time.

Who Is This For?

This indicator is ideal for traders who:

Use Liquidity Inducent Theory strategy in their analysis.

Prefer a structured and systematic trading approach.

Need an on-chart tool to document confirmations without relying on external notes or tools.

Why Closed Source?

The logic behind the interactive table and confirmation system is specifically tailored to LIT practitioners and is not publicly available in existing open-source scripts. The closed-source nature of this script protects its unique implementation, ensuring the integrity and exclusivity of the tool.

Disclaimer

This indicator does not provide trading signals or strategies. It is a tool to document user-defined confirmations and should be used in conjunction with a thorough understanding of market behavior and risk management practices.

Stablecoin Supply Ratio [Alpha Extract]Stablecoin Supply Ratio Indicator

The Stablecoin Supply Ratio (SSR) indicator compares Bitcoin's market capitalization to the aggregate supply of major stablecoins, offering insights into relative purchasing power and liquidity. This tool helps traders:

✔ Assess Bitcoin's buying power relative to the available stablecoin liquidity.

✔ Detect periods of capital inflow or outflow from stablecoins.

✔ Identify market sentiment shifts based on stablecoin reserves.

🔶 CALCULATION

The indicator aggregates the supply of key stablecoins and compares it to Bitcoin's market cap:

Stablecoin Aggregation

• Inputs:

USDT, USDC, DAI, USDD (daily closing values).

BUSD Market Cap (Glassnode data).

• Total Stablecoin Supply:

Sum of the listed stablecoins' market caps.

Stablecoin Supply Ratio (SSR)

• Formula:

SSR = Bitcoin Market Cap / Total Stablecoin Supply

• Normalized SSR:

Normalized by dividing SSR by its 200-day SMA.

Bollinger Bands

• Bands are applied to the normalized SSR using a configurable moving average type and 2 standard deviations.

Example Calculation:

ssr = btcmc / stablecoin_liq

ratio = ssr / ta.sma(ssr, 200)

basis = ta.sma(ratio, 200)

dev = 2 * ta.stdev(ratio, 200)

upper = basis + dev

lower = basis - dev

🔶 DETAILS

Visual Features:

• Normalized SSR:

Plotted as a light green line.

• Upper Band:

Red line indicating SSR overbought zone.

• Lower Band:

Green line signaling SSR oversold zone.

Interpretation:

• High SSR: Indicates stablecoin reserves are low relative to Bitcoin's market cap, reducing stablecoin buying power.

• Low SSR: Suggests high stablecoin liquidity relative to Bitcoin's market cap, increasing potential buying pressure.

• Band Crosses: Movements beyond the upper or lower bands may signal sentiment extremes.

🔶 EXAMPLES

Market insights include:

• Capital Outflows: SSR rising into the upper band may reflect decreasing stablecoin reserves, potentially signaling a liquidity drain.

• Capital Inflows: SSR dropping near the lower band could indicate growing stablecoin reserves, potentially fueling Bitcoin demand.

🔶 SETTINGS

Customization Options:

• MA Type: Choose between SMA, EMA, WMA, SMMA, and VWMA for band calculation.

• Period: Adjust the 200-day smoothing period.

• Deviation Multiplier: Modify the standard deviation multiplier (default: 2).

The Stablecoin Supply Ratio indicator is a valuable tool for traders monitoring liquidity dynamics and stablecoin trends to anticipate Bitcoin market moves and capital flows.

Classic Nacked Z-Score ArbitrageThe “Classic Naked Z-Score Arbitrage” strategy employs a statistical arbitrage model based on the Z-score of the price spread between two assets. This strategy follows the premise of pair trading, where two correlated assets, typically from the same market sector, are traded against each other to profit from relative price movements (Gatev, Goetzmann, & Rouwenhorst, 2006). The approach involves calculating the Z-score of the price spread between two assets to determine market inefficiencies and capitalize on short-term mispricing.

Methodology

Price Spread Calculation:

The strategy calculates the spread between the two selected assets (Asset A and Asset B), typically from different sectors or asset classes, on a daily timeframe.

Statistical Basis – Z-Score:

The Z-score is used as a measure of how far the current price spread deviates from its historical mean, using the standard deviation for normalization.

Trading Logic:

• Long Position:

A long position is initiated when the Z-score exceeds the predefined threshold (e.g., 2.0), indicating that Asset A is undervalued relative to Asset B. This signals an arbitrage opportunity where the trader buys Asset B and sells Asset A.

• Short Position:

A short position is entered when the Z-score falls below the negative threshold, indicating that Asset A is overvalued relative to Asset B. The strategy involves selling Asset B and buying Asset A.

Theoretical Foundation

This strategy is rooted in mean reversion theory, which posits that asset prices tend to return to their long-term average after temporary deviations. This form of arbitrage is widely used in statistical arbitrage and pair trading techniques, where investors seek to exploit short-term price inefficiencies between two assets that historically maintain a stable price relationship (Avery & Sibley, 2020).

Further, the Z-score is an effective tool for identifying significant deviations from the mean, which can be seen as a signal for the potential reversion of the price spread (Braucher, 2015). By capturing these inefficiencies, traders aim to profit from convergence or divergence between correlated assets.

Practical Application

The strategy aligns with the Financial Algorithmic Trading and Market Liquidity analysis, emphasizing the importance of statistical models and efficient execution (Harris, 2024). By utilizing a simple yet effective risk-reward mechanism based on the Z-score, the strategy contributes to the growing body of research on market liquidity, asset correlation, and algorithmic trading.

The integration of transaction costs and slippage ensures that the strategy accounts for practical trading limitations, helping to refine execution in real market conditions. These factors are vital in modern quantitative finance, where liquidity and execution risk can erode profits (Harris, 2024).

References

• Gatev, E., Goetzmann, W. N., & Rouwenhorst, K. G. (2006). Pairs Trading: Performance of a Relative-Value Arbitrage Rule. The Review of Financial Studies, 19(3), 1317-1343.

• Avery, C., & Sibley, D. (2020). Statistical Arbitrage: The Evolution and Practices of Quantitative Trading. Journal of Quantitative Finance, 18(5), 501-523.

• Braucher, J. (2015). Understanding the Z-Score in Trading. Journal of Financial Markets, 12(4), 225-239.

• Harris, L. (2024). Financial Algorithmic Trading and Market Liquidity: A Comprehensive Analysis. Journal of Financial Engineering, 7(1), 18-34.

Macros ICT KillZones [TradingFinder] Times & Price Trading Setup🔵 Introduction

ICT Macros, developed by Michael Huddleston, also known as ICT (Inner Circle Trader), is a powerful trading tool designed to help traders identify the best trading opportunities during key time intervals like the London and New York trading sessions.

For traders aiming to capitalize on market volatility, liquidity shifts, and Fair Value Gaps (FVG), understanding and using these critical time zones can significantly improve trading outcomes.

In today’s highly competitive financial markets, identifying the moments when the market is seeking buy-side or sell-side liquidity, or filling price imbalances, is essential for maximizing profitability.

The ICT Macros indicator is built on the renowned ICT time and price theory, which enables traders to track and leverage key market dynamics such as breaks of highs and lows, imbalances, and liquidity hunts.

This indicator automatically detects crucial market times and optimizes strategies for traders by highlighting the specific moments when price movements are most likely to occur. A standout feature of ICT Macros is its automatic adjustment for Daylight Saving Time (DST), ensuring that traders remain synced with the correct session times.

This means you can rely on accurate market timing without the need for manual updates, allowing you to focus on capturing profitable trades during critical timeframes.

🔵 How to Use

The ICT Macros indicator helps you capitalize on trading opportunities during key market moments, particularly when the market is breaking highs or lows, filling Fair Value Gaps (FVG), or addressing imbalances. This indicator is particularly beneficial for traders who seek to identify liquidity, market volatility, and price imbalances.

🟣 Sessions

London Sessions

London Macro 1 :

UTC Time : 06:33 to 07:00

New York Time : 02:33 to 03:00

London Macro 2 :

UTC Time : 08:03 to 08:30

New York Time : 04:03 to 04:30

New York Sessions

New York Macro AM 1 :

UTC Time : 12:50 to 13:10

New York Time : 08:50 to 09:10

New York Macro AM 2 :

UTC Time : 13:50 to 14:10

New York Time : 09:50 to 10:10

New York Macro AM 3 :

UTC Time : 14:50 to 15:10

New York Time : 10:50 to 11:10

New York Lunch Macro :

UTC Time : 15:50 to 16:10

New York Time : 11:50 to 12:10

New York PM Macro :

UTC Time : 17:10 to 17:40

New York Time : 13:10 to 13:40

New York Last Hour Macro :

UTC Time : 19:15 to 19:45

New York Time : 15:15 to 15:45

These time intervals adjust automatically based on Daylight Saving Time (DST), helping traders to enter or exit trades during key market moments when price volatility is high.

Below are the main applications of this tool and how to incorporate it into your trading strategies :

🟣 Combining ICT Macros with Trading Strategies

The ICT Macros indicator can easily be used in conjunction with various trading strategies. Two well-known strategies that can be combined with this indicator include:

ICT 2022 Trading Model : This model is designed based on identifying market liquidity, structural price changes, and Fair Value Gaps (FVG). By using ICT Macros, you can identify the key time intervals when the market is seeking liquidity, filling imbalances, or breaking through important highs and lows, allowing you to enter or exit trades at the right moment.

Silver Bullet Strategy : This strategy, which is built around liquidity hunting and rapid price movements, can work more accurately with the help of ICT Macros. The indicator pinpoints precise liquidity times, helping traders take advantage of market shifts caused by filling Fair Value Gaps or correcting imbalances.

🟣 Capitalizing on Price Volatility During Key Times

Large market algorithms often seek liquidity or fill Fair Value Gaps (FVG) during the intervals marked by ICT Macros. These periods are when price volatility increases, and traders can use these moments to enter or exit trades.

For example, if sell-side liquidity is drained and the market fills an imbalance, the price might move toward buy-side liquidity. By identifying these moments, which may also involve breaking a previous high or low, you can leverage rapid market fluctuations to your advantage.

🟣 Identifying Liquidity and Price Imbalances

One of the important uses of ICT Macros is identifying points where the market is seeking liquidity and correcting imbalances. You can determine high or low liquidity levels in the market before each ICT Macro, as well as Fair Value Gaps (FVG) and price imbalances that need to be filled, using them to adjust your trading strategy. This capability allows you to manage trades based on liquidity shifts or imbalance corrections without needing a bias toward a specific direction.

🔵 Settings

The ICT Macros indicator offers various customization options, allowing users to tailor it to their specific needs. Below are the main settings:

Time Zone Mode : You can select one of the following options to define how time is displayed:

UTC : For traders who need to work with Universal Time.

Session Local Time : The local time corresponding to the London or New York markets.

Your Time Zone : You can specify your own time zone (e.g., "UTC-4:00").

Your Time Zone : If you choose "Your Time Zone," you can set your specific time zone. By default, this is set to UTC-4:00.

Show Range Time : This option allows you to display the time range of each session on the chart. If enabled, the exact start and end times of each interval are shown.

Show or Hide Time Ranges : Toggle on/off for visual clarity depending on user preference.

Custom Colors : Set distinct colors for each session, allowing users to personalize their chart based on their trading style.These settings allow you to adjust the key time intervals of each trading session to your preference and customize the time format according to your own needs.

🔵 Conclusion

The ICT Macros indicator is a powerful tool for traders, helping them to identify key time intervals where the market seeks liquidity or fills Fair Value Gaps (FVG), corrects imbalances, and breaks highs or lows. This tool is especially valuable for traders using liquidity-based strategies such as ICT 2022 or Silver Bullet.

One of the key features of this indicator is its support for Daylight Saving Time (DST), ensuring you are always in sync with the correct trading session timings without manual adjustments. This is particularly beneficial for traders operating across different time zones.

With ICT Macros, you can capitalize on crucial market opportunities during sensitive times, take advantage of imbalances, and enhance your trading strategies based on market volatility, liquidity shifts, and Fair Value Gaps.

Engulfing Candles with Sweep by AydmaxxEngulfing Candles with Sweep Indicator

The "Engulfing Candles with Sweep" indicator identifies bullish and bearish engulfing candles that exhibit liquidity sweeps. It marks these significant candlestick patterns and draws a 50% Fibonacci retracement line from the high to low of the engulfing candle. The indicator helps traders spot potential reversal points where large market players might be accumulating or distributing positions.

Key Features:

Bullish Engulfing Candle with Sweep:

Identifies when a bullish candle (closing higher than it opened) engulfs the previous bearish candle (closing lower than it opened).

Ensures that the bullish candle’s low is lower than the previous candle’s low, indicating a sweep of liquidity.

Marks the identified bullish candle with a symbol below the candlestick.

Draws a 50% Fibonacci retracement line from the high to the low of the bullish engulfing candle.

Bearish Engulfing Candle with Sweep:

Identifies when a bearish candle (closing lower than it opened) engulfs the previous bullish candle (closing higher than it opened).

Ensures that the bearish candle’s high is higher than the previous candle’s high, indicating a sweep of liquidity.

Marks the identified bearish candle with a symbol above the candlestick.

Draws a 50% Fibonacci retracement line from the high to the low of the bearish engulfing candle.

Customizable Settings:

Fibonacci Line Color: Allows customization of the Fibonacci retracement line color for both bullish and bearish engulfing candles.

Fibonacci Line Style: Provides options to choose the line style (solid, dotted, dashed).

Fibonacci Line Width: Enables adjustment of the line width for better visibility.

Toggle Fibonacci Lines: Option to enable or disable the display of Fibonacci retracement lines.

How to Use:

Apply the indicator to your chart.

Look for symbols below or above the candlesticks, indicating bullish or bearish engulfing candles with liquidity sweeps.

Utilize the 50% Fibonacci retracement lines to identify potential support or resistance levels.

Benefits:

Helps in identifying key reversal patterns in the market.

Provides visual aids with Fibonacci retracement levels for potential entry and exit points.

Enhances trading decisions by confirming engulfing patterns with liquidity sweeps.

ICT Power Of Three | Flux Charts💎 GENERAL OVERVIEW

Introducing our new ICT Power Of Three Indicator! This indicator is built around the ICT's "Power Of Three" strategy. This strategy makes use of these 3 key smart money concepts : Accumulation, Manipulation and Distribution. Each step is explained in detail within this write-up. For more information about the process, check the "HOW DOES IT WORK" section.

Features of the new ICT Power Of Three Indicator :

Implementation of ICT's Power Of Three Strategy

Different Algorithm Modes

Customizable Execution Settings

Customizable Backtesting Dashboard

Alerts for Buy, Sell, TP & SL Signals

📌 HOW DOES IT WORK ?

The "Power Of Three" comes from these three keywords "Accumulation, Manipulation and Distribution". Here is a brief explanation of each keyword :

Accumulation -> Accumulation phase is when the smart money accumulate their positions in a fixed range. This phase indicates price stability, generally meaning that the price constantly switches between up & down trend between a low and a high pivot point. When the indicator detects an accumulation zone, the Power Of Three strategy begins.

Manipulation -> When the smart money needs to increase their position sizes, they need retail traders' positions for liquidity. So, they manipulate the market into the opposite direction of their intended direction. This will result in retail traders opening positions the way that the smart money intended them to do, creating liquidity. After this step, the real move that the smart money intended begins.

Distribution -> This is when the real intention of the smart money comes into action. With the new liquidity thanks to the manipulation phase, the smart money add their positions towards the opposite direction of the retail mindset. The purpose of this indicator is to detect the accumulation and manipulation phases, and help the trader move towards the same direction as the smart money for their trades.

Detection Methods Of The Indicator :

Accumulation -> The indicator detects accumulation zones as explained step-by-step :

1. Draw two lines from the lowest point and the highest point of the latest X bars.

2. If the (high line - low line) is lower than Average True Range (ATR) * accumulationConstant

3. After the condition is validated, an accumulation zone is detected. The accumulation zone will be invalidated and manipulation phase will begin when the range is broken.

Manipulation -> If the accumulation range is broken, check if the current bar closes / wicks above the (high line + ATR * manipulationConstant) or below the (low line - ATR * manipulationConstant). If the condition is met, the indicator detects a manipulation zone.

Distribution -> The purpose of this indicator is to try to foresee the distribution zone, so instead of a detection, after the manipulation zone is detected the indicator automatically create a "shadow" distribution zone towards the opposite direction of the freshly detected manipulation zone. This shadow distribution zone comes with a take-profit and stop-loss layout, customizable by the trader in the settings.

The X bars, accumulationConstant and manipulationConstant are subject to change with the "Algorithm Mode" setting. Read the "Settings" section for more information.

This indicator follows these steps and inform you step by step by plotting them in your chart.

🚩UNIQUENESS

This indicator is an all-in-one suite for the ICT's Power Of Three concept. It's capable of plotting the strategy, giving signals, a backtesting dashboard and alerts feature. Different and customizable algorithm modes will help the trader fine-tune the indicator for the asset they are currently trading. The backtesting dashboard allows you to see how your settings perform in the current ticker. You can also set up alerts to get informed when the strategy is executable for different tickers.

⚙️SETTINGS

1. General Configuration

Algorithm Mode -> The indicator offers 3 different detection algorithm modes according to your needs. Here is the explanation of each mode.

a) Small Manipulation

This mode has the default bar length for the accumulation detection, but a lower manipulation constant, meaning that slighter imbalances in the price action can be detected as manipulation. This setting can be useful on tickers that have lower liquidity, thus can be manipulated easier.

b) Big Manipulation

This mode has the default bar length for the accumulation detection, but a higher manipulation constant, meaning that heavier imbalances on the price action are required in order to detect manipulation zones. This setting can be useful on tickers that have higher liquidity, thus can be manipulated harder.

c) Short Accumulation

This mode has a ~70% lower bar length requirement for accumulation zone detection, and the default manipulation constant. This setting can be useful on tickers that are highly volatile and do not enter accumulation phases too often.

Breakout Method -> If "Close" is selected, bar close price will be taken into calculation when Accumulation & Manipulation zone invalidation. If "Wick" is selected, a wick will be enough to validate the corresponding zone.

2. TP / SL

TP / SL Method -> If "Fixed" is selected, you can adjust the TP / SL ratios from the settings below. If "Dynamic" is selected, the TP / SL zones will be auto-determined by the algorithm.

Risk -> The risk you're willing to take if "Dynamic" TP / SL Method is selected. Higher risk usually means a better winrate at the cost of losing more if the strategy fails. This setting is has a crucial effect on the performance of the indicator, as different tickers may have different volatility so the indicator may have increased performance when this setting is correctly adjusted.

3. Visuals

Show Zones -> Enables / Disables rendering of Accumulation (yellow) and Manipulation (red) zones.

Dark Energy Divergence OscillatorThe Dark Energy Divergence Oscillator (DEDO)

What makes The Universe grow at an accelerating pace?

Dark Energy.

What makes The Economy grow at an accelerating pace?

Debt.

Debt is the Dark Energy of The Economy.

I pronounce DEDO "Deed-oh", but variations are fine with me.

Note: The Pine Script version of DEDO is improved from the original formula, which used a constant all-time high calculation in the normalization factor. This was technically not as accurate for calculating liquidity pressure in historical data because it meant that historical prices were being tested against future liquidity factors. Now using Pine, the functions can be normalized for the bar at the time of calculation, so the liquidity factors are normalized per candle, not across the entire series, which feels like an improvement to me.

Thought Process:

It's all about the liquidity. What I started with is a correlation between major stock indices such as SPX and WRESBAL , a balance sheet metric on FRED

After September 2008, when QE was initiated, many asset valuations started to follow more closely with liquidity factors. This led me to create a function that could combine asset prices and liquidity in WRESBAL , in order to calculate their divergence and chart the signal in TradingView.

The original formula:

First, we don't want "non-QE" data. we only want data for the market affected by QE .

So, find SPX on the day of pre-QE: 1255.08 and subtract that from the 2022 top 4818.62 = 3563.54

With this post-QE SPX range, now you can normalize the price level simply by dividing by the range = ( SPX -1255.08)/3563.54)

Normalization produces values from 0 to 1 so that they can be compared with other normalized figures.

In order to test the 0 to 1 normalized SPX range measure against the liquidity number, WRESBAL , it's the same idea: normalize it using the max as the denominator and you get a 0 to 1 liquidity index:

( WRESBAL /4276000000000)

Subtract one from the other to get the divergence:

(( WRESBAL /4276000000000)-(( SPX -1255.08)/3563.54))*10

x10 to reduce decimal places, but this option is configurable in DEDO's input settings tab.

Positive values indicate there's ample liquidity to hold up price or even create bullish momentum in some cases. Negative values mean price levels are potentially extended beyond what liquidity levels can support.

Note: many viewers of the charts on social media wanted the values to go down in alignment with price moving down, so inverting the chart is what I do with Option + I. I like the fact that negative values represent a deficit in liquidity to hold up price but that's just me.

Now with Pine Script and some help from other liquidity focused accounts on TradingView , I was able to derive a script that includes central bank liquidity and Reverse Repo liquidity drain, all in one algorithm, with adjustable settings.

Central bank assets included in this version:

-JPY (Japan)

-CNY (China)

-UK (British Pound)

-SNB (Swiss National Bank)

-ECB (European Central Bank )

Central Bank assets can be adjusted to an allocation % so that the formula is adjusted for the market cap of the asset.

A handy table in the lower right corner displays useful information about the asset market cap, and percentage it represents in the liquidity pool.

Reverse repo soak is also an optional addition in the Input settings using the RRPONTSYD value from FRED. This value is subtracted from global liquidity used to determine divergence since it is swept away from markets when residing in the Fed's reverse repo facility.

There is an option to draw a line at the Zero bound. This provides a convenience so that the line doesn't keep having to be redrawn on every chart. The normalized equation produces a value that should oscillate around zero, as price/valuation grows past liquidity support, falls under it, and repeats in cycles.

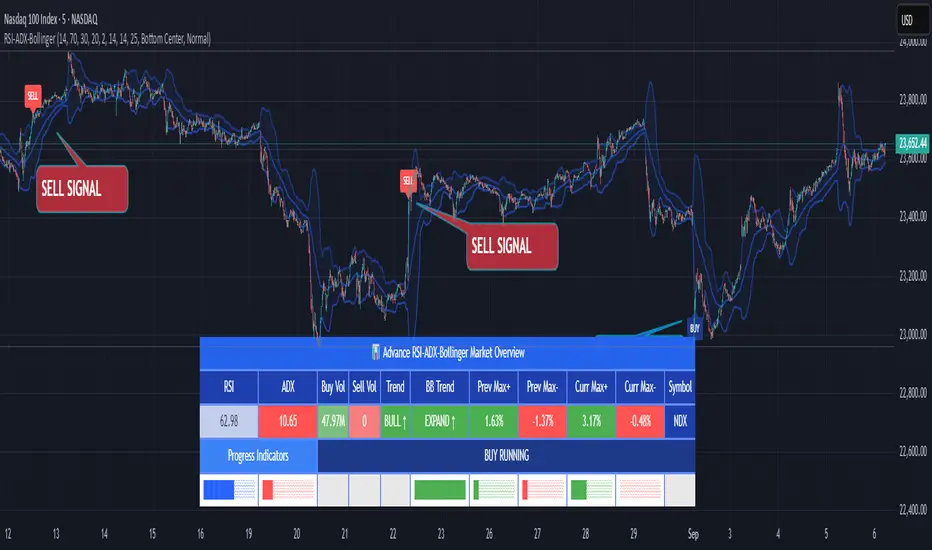

RSI ADX Bollinger Analysis High-level purpose and design philosophy

This indicator — RSI-ADX-Bollinger Analysis — is a compact, educational market-analysis toolkit that blends momentum (RSI), trend strength (ADX), volatility structure (Bollinger Bands) and simple volumetrics to provide traders a snapshot of market condition and trade idea quality. The design philosophy is explicit and layered: use each component to answer a different question about price action (momentum, conviction, volatility, participation), then combine answers to form a more robust, explainable signal. The mashup is intended for analysis and learning, not automatic execution: it surfaces the why behind signals so traders can test, learn and apply rules with risk management.

________________________________________

What each indicator contributes (component-by-component)

RSI (Relative Strength Index) — role and behavior: RSI measures short-term momentum by comparing recent gains to recent losses. A high RSI (near or above the overbought threshold) indicates strong recent buying pressure and potential exhaustion if price is extended. A low RSI (near or below the oversold threshold) indicates strong recent selling pressure and potential exhaustion or a value area for mean-reversion. In this dashboard RSI is used as the primary momentum trigger: it helps identify whether price is locally over-extended on the buy or sell side.

ADX (Average Directional Index) — role and behavior: ADX measures trend strength independently of direction. When ADX rises above a chosen threshold (e.g., 25), it signals that the market is trending with conviction; ADX below the threshold suggests range or weak trend. Because patterns and momentum signals perform differently in trending vs. ranging markets, ADX is used here as a filter: only when ADX indicates sufficient directional strength does the system treat RSI+BB breakouts as meaningful trade candidates.

Bollinger Bands — role and behavior: Bollinger Bands (20-period basis ± N standard deviations) show volatility envelope and relative price position vs. a volatility-adjusted mean. Price outside the upper band suggests pronounced extension relative to recent volatility; price outside the lower band suggests extended weakness. A band expansion (increasing width) signals volatility breakout potential; contraction signals range-bound conditions and potential squeeze. In this dashboard, Bollinger Bands provide the volatility/structural context: RSI extremes plus price beyond the band imply a stronger, volatility-backed move.

Volume split & basic MA trend — role and behavior: Buy-like and sell-like volume (simple heuristic using close>open or closeopen) or sell-like (close1.2 for validation and compare win rate and expectancy.

4. TF alignment: Accept signals only when higher timeframe (e.g., 4h) trend agrees — compare results.

5. Parameter sensitivity: Vary RSI threshold (70/30 vs 80/20), Bollinger stddev (2 vs 2.5), and ADX threshold (25 vs 30) and measure stability of results.

These exercises teach both statistical thinking and the specific failure modes of the mashup.

________________________________________

Limitations, failure modes and caveats (explicit & teachable)

• ADX and Bollinger measures lag during fast-moving news events — signals can be late or wrong during earnings, macro shocks, or illiquid sessions.

• Volume classification by open/close is a heuristic; it does not equal TAPEDATA, footprint or signed volume. Use it as supportive evidence, not definitive proof.

• RSI can remain overbought or oversold for extended stretches in persistent trends — relying solely on RSI extremes without ADX or BB context invites large drawdowns.

• Small-cap or low-liquidity instruments yield noisy band behavior and unreliable volume ratios.

Being explicit about these limitations is a strong point in a TradingView description — it demonstrates transparency and educational intent.

________________________________________

Originality & mashup justification (text you can paste)

This script intentionally combines classical momentum (RSI), volatility envelope (Bollinger Bands) and trend-strength (ADX) because each indicator answers a different and complementary question: RSI answers is price locally extreme?, Bollinger answers is price outside normal volatility?, and ADX answers is the market moving with conviction?. Volume participation then acts as a practical check for real market involvement. This combination is not a simple “indicator mashup”; it is a designed ensemble where each element reduces the others’ failure modes and together produce a teachable, testable signal framework. The script’s purpose is educational and analytical — to show traders how to interpret the interplay of momentum, volatility, and trend strength.

________________________________________

TradingView publication guidance & compliance checklist

To satisfy TradingView rules about mashups and descriptions, include the following items in your script description (without exposing source code):

1. Purpose statement: One or two lines describing the script’s objective (educational multi-indicator market overview and idea filter).

2. Component list: Name the major modules (RSI, Bollinger Bands, ADX, volume heuristic, SMA trend checks, signal tracking) and one-sentence reason for each.

3. How they interact: A succinct non-code explanation: “RSI finds momentum extremes; Bollinger confirms volatility expansion; ADX confirms trend strength; all three must align for a BUY/SELL.”

4. Inputs: List adjustable inputs (RSI length and thresholds, BB length & stddev, ADX threshold & smoothing, volume MA, table position/size).

5. Usage instructions: Short workflow (check TF alignment → confirm participation → define stop & R:R → backtest).

6. Limitations & assumptions: Explicitly state volume is approximated, ADX has lag, and avoid promising guaranteed profits.

7. Non-promotional language: No external contact info, ads, claims of exclusivity or guaranteed outcomes.

8. Trademark clause: If you used trademark symbols, remove or provide registration proof.

9. Risk disclaimer: Add the copy-ready disclaimer below.

This matches TradingView’s request for meaningful descriptions that explain originality and inter-component reasoning.

________________________________________

Copy-ready short publication description (paste into TradingView)

Advanced RSI-ADX-Bollinger Market Overview — educational multi-indicator dashboard. This script combines RSI (momentum extremes), Bollinger Bands (volatility envelope and band expansion), ADX (trend strength), simple SMA trend bias and a basic buy/sell volume heuristic to surface high-quality idea candidates. Signals require alignment of momentum, volatility expansion and rising ADX; volume participation is displayed to support signal confidence. Inputs are configurable (RSI length/levels, BB length/stddev, ADX length/threshold, volume MA, display options). This tool is intended for analysis and learning — not for automated execution. Users should back test and apply robust risk management. Limitations: volume classification here is a heuristic (close>open), ADX and BB measures lag in fast news events, and results vary by instrument liquidity.

________________________________________

Copy-ready risk & misuse disclaimer (paste into description or help file)

This script is provided for educational and analytical purposes only and does not constitute financial or investment advice. It does not guarantee profits. Indicators are heuristics and may give false or late signals; always back test and paper-trade before using real capital. The author is not responsible for trading losses resulting from the use or misuse of this indicator. Use proper position sizing and risk controls.

________________________________________

Risk Disclaimer: This tool is provided for education and analysis only. It is not financial advice and does not guarantee returns. Users assume all risk for trades made based on this script. Back test thoroughly and use proper risk management.

Market structure + TF Bucket Market Structure + TF Bucket

This Pine Script™ indicator, published under the Mozilla Public License 2.0, extends the "Market Structure" script by mickes (), with full credit to mickes. It integrates the enhanced MarketStructure library by Fenomentn (), also based on mickes’ library under MPL 2.0, to provide advanced market structure analysis with multi-timeframe pivot length customization.

Functionality

Market Structure Analysis: Detects internal (orderflow) and swing market structures, visualizing Break of Structure (BOS), Change of Character (CHoCH), Equal High/Low (EQH/EQL), and liquidity zones using the MarketStructure library.

Timeframe Bucket (TF Bucket): Dynamically adjusts pivot lengths for six user-defined timeframes (e.g., 3m, 5m, 10m, 15m, 4h, 12h), optimizing structure detection across different chart timeframes.

Trend Strength Visualization: Displays a trend strength metric (from the library) for internal and swing structures, indicating trend reliability based on pivot frequency and volatility.

Statistics Table: Shows yearly counts of BOS and CHoCH events for internal and swing structures, configurable by a user-defined period.

Screener Support: Outputs BOS and CHoCH signals for TradingView’s screener, with a configurable signal persistence period.

Customizable Alerts: Enables alerts for BOS and CHoCH events, separately configurable for internal and swing structures.

Methodology

Pivot Detection: Uses the library’s Pivot function, which applies a volatility filter (ATR-based) to confirm significant pivots, reducing false signals in low-volatility markets.

TF Bucket: Maps user-selected timeframes to Pine Script’s timeframe.period using f_getTimeframePeriod, applying custom pivot lengths when the chart’s timeframe matches a selected one (or base lengths in Static mode).

Trend Strength: Calculates a score as pivotCount / LeftLength * (currentATR / ATR), displayed via labels to help traders assess trend reliability.

BOS/CHoCH Detection: Identifies BOS when price breaks a pivot in the trend direction and CHoCH when price reverses against the trend, labeling events as “MSF” or “MSF+” based on pivot patterns.

EQH/EQL and Liquidity: Draws boxes for equal high/low zones within ATR-based thresholds and visualizes liquidity levels with confirmation bars.

Statistics and Screener: Tracks BOS/CHoCH events in a yearly table and outputs signals for screener use, with persistence controlled by a user-defined period.

Usage

Integration: Apply the indicator to any chart and import the library via import Fenomentn/MarketStructure/1.

Configuration: Set up to six timeframes with custom pivot lengths, enable/disable internal and swing structures, configure alerts, and adjust statistics years in the settings panel.

Alerts: Enable BOS and CHoCH alerts for real-time notifications, triggered on bar close to avoid repainting.

Screener: Use the plotted signals to monitor BOS/CHoCH events across multiple tickers in TradingView’s screener.

Best Practices: Optimal for forex and crypto charts on 1m to 12h timeframes. Adjust pivot lengths and the library’s volatility threshold for specific market conditions.

Originality

This indicator enhances mickes’ original script with:

Timeframe Bucket: Dynamic pivot length selection for multi-timeframe analysis, not present in the original.

Trend Strength Display: Visualizes the library’s TrendStrength metric for enhanced trend analysis.

Enhanced Library Integration: Leverages Fenomentn/MarketStructure/1, which adds a volatility-based pivot filter, dynamic label sizing, and customizable BOS/CHoCH visualization styles.No additional open-source code was reused beyond mickes’ script and library, fully credited under MPL 2.0.

Advanced ICT Theory - A-ICT📊 Advanced ICT Theory (A-ICT): The Institutional Manipulation Detector

Are you tired of being the liquidity? Stop chasing shadows and start tracking the architects of price movement.

This is not another lagging indicator. This is a complete framework for viewing the market through the lens of institutional traders. Advanced ICT Theory (A-ICT) is an all-in-one, military-grade analysis engine designed to decode the complex language of "Smart Money." It automates the core tenets of Inner Circle Trader (ICT) methodology, moving beyond simple patterns to build a dynamic, real-time narrative of market manipulation, liquidity engineering, and institutional order flow.

AIT provides a living blueprint of the market, identifying high-probability zones, tracking structural shifts, and scoring the quality of setups with a sophisticated, multi-factor algorithm. This is your X-ray into the market's true intentions.

🔬 THE CORE ENGINE: DECODING THE THEORY & FORMULAS

A-ICT is built upon a sophisticated, multi-layered logic system that interprets price action as a story of cause and effect. It does not guess; it confirms. Here is the foundational theory that drives the engine:

1. Market Structure: The Blueprint of Trend

The script first establishes a deep understanding of the market's skeleton through multi-level pivot analysis. It uses ta.pivothigh and ta.pivotlow to identify significant swing points.

Internal Structure (iBOS): Minor swings that show the short-term order flow. A break of internal structure is the first whisper of a potential shift.

External Structure (eBOS): Major swing points that define the primary trend. A confirmed break of external structure is a powerful statement of trend continuation. AIT validates this with optional Volume Confirmation (volume > volumeSMA * 1.2) and Candle Confirmation to ensure the break is driven by institutional force, not just a random spike.

Change of Character (CHoCH): This is the earthquake. A CHoCH occurs when a confirmed eBOS happens against the prevailing trend (e.g., a bearish eBOS in a clear uptrend). A-ICT flags this immediately, as it is the strongest signal that the primary trend is under threat of reversal.

2. Liquidity Engineering: The Fuel of the Market

Institutions don't buy into strength; they buy into weakness. They need liquidity. A-ICT maps these liquidity pools with forensic precision:

Buyside & Sellside Liquidity (BSL/SSL): Using ta.highest and ta.lowest, AIT identifies recent highs and lows where clusters of stop-loss orders (liquidity) are resting. These are institutional targets.

Liquidity Sweeps: This is the "manipulation" part of the detector. AIT has a specific formula to detect a sweep: high > bsl and close < bsl . This signifies that institutions pushed price just high enough to trigger buy-stops before aggressively selling—a classic "stop hunt." This event dramatically increases the quality score of subsequent patterns.

3. The Element Lifecycle: From Potential to Power

This is the revolutionary heart of A-ICT. Zones are not static; they have a lifecycle. AIT tracks this with its dynamic classification engine.

Phase 1: PENDING (Yellow): The script identifies a potential zone of interest based on a specific candle formation (a "displacement"). It is marked as "Pending" because its true nature is unknown. It is a question.

Phase 2: CLASSIFICATION: After the zone is created, AIT watches what happens next. The zone's identity is defined by its actions: