CE - Market Performance TableThe 𝓜𝓪𝓻𝓴𝓮𝓽 𝓟𝓮𝓻𝓯𝓸𝓻𝓶𝓪𝓷𝓬𝓮 𝓣𝓪𝓫𝓵𝓮 is a sophisticated market tool designed to provide valuable insights into the current market trends and the approximate current position in the Macroeconomic Regime.

Furthermore the 𝓜𝓪𝓻𝓴𝓮𝓽 𝓟𝓮𝓻𝓯𝓸𝓻𝓶𝓪𝓷𝓬𝓮 𝓣𝓪𝓫𝓵𝓮 provides the Correlation Implied Trend for the Asset on the Chart. Lastly it provides information about current "RISK ON" or "RISK OFF" periods.

Methodology:

𝓜𝓪𝓻𝓴𝓮𝓽 𝓟𝓮𝓻𝓯𝓸𝓻𝓶𝓪𝓷𝓬𝓮 𝓣𝓪𝓫𝓵𝓮 tracks the 15 underlying Stock ETF's to identify their performance and puts the combined performances together to visualize 42MACRO's GRID Equity Model.

For this it uses the below ETF's:

Dividends (SPHD)

Low Beta (SPLV)

Quality (QUAL)

Defensives (DEF)

Growth (IWF)

High Beta (SPHB)

Cyclicals (IYT, IWN)

Value (IWD)

Small Caps (IWM)

Mid Caps (IWR)

Mega Cap Growth (MGK)

Size (OEF)

Momentum (MTUM)

Large Caps (IWB)

Overall Settings:

The main time values you want to change are:

Correlation Length

- Defines the time horizon for the Correlation Table

ROC Period

- Defines the time horizon for the Performance Table

Normalization lookback

- Defines the time horizon for the Trend calculation of the ETF's

- For longer term Trends over weeks or months a length of 50 is usually pretty accurate

Visuals:

There is a variety of options to change the visual settings of what is being plotted and the two table positions and additional considerations.

Everything that is relevant in the underlying logic that can help comprehension can be visualized with these options.

Market Correlation:

The Market Correlation Table takes the Correlation of the above ETF's to the Asset on the Chart, it furthermore uses the Normalized KAMA Oscillator by IkkeOmar to analyse the current trend of every single ETF.

It then Implies a Correlation based on the Trend and the Correlation to give a probabilistically adjusted expectation for the future Chart Asset Movement. This is strengthened by taking the average of all Implied Trends.

With this the Correlation Table provides valuable insights about probabilistically likely Movement of the Asset, for Traders and Investors alike, over the defined time duration.

Market Performance:

𝓜𝓪𝓻𝓴𝓮𝓽 𝓟𝓮𝓻𝓯𝓸𝓻𝓶𝓪𝓷𝓬𝓮 𝓣𝓪𝓫𝓵𝓮 is the actual valuable part of this Indicator.

It provides valuable information about the current market environment (whether it's risk on or risk off), the rough GRID models from 42MACRO and the actual market performance.

This allows you to obtain a deeper understanding of how the market works and makes it simple to identify the actual market direction.

Utility:

The 𝓜𝓪𝓻𝓴𝓮𝓽 𝓟𝓮𝓻𝓯𝓸𝓻𝓶𝓪𝓷𝓬𝓮 𝓣𝓪𝓫𝓵𝓮 is divided in 4 Sections which are the GRID regimes:

Economic Growth:

Goldilocks

Reflation

Economic Contraction:

Inflation

Deflation

Top 5 Equity Style Factors:

Are the values green for a specific Column? If so then the market reflects the corresponding GRID behavior.

Bottom 5 Equity Style Factors:

Are the values red for a specific Column? If so then the market reflects the corresponding GRID behavior.

So if we have Goldilocks as current regime we would see green values in the Top 5 Goldilocks Cells and red values in the Bottom 5 Goldilocks Cells.

You will find that Reflation will look similar, as it is also a sign of Economic Growth.

Same is the case for the two Contraction regimes.

"implied" için komut dosyalarını ara

VIX HeatmapVIX HeatMap

Instructions:

- To be used with the S&P500 index (ES, SPX, SPY, any S&P ETF) as that's the input from where the CBOE calculates and measures the VIX. Can also be used with the Dow Jones, Nasdaq, & Nasdaq100.

Description:

- Expected Implied Volatility regime simplified & visualized. Know if we are in a high, medium, or low volatility regime, instantly.

- Ranges from Hot to Cold: The hotter the heat-map, the higher the implied volatility and fear & vice versa.

- The VIX HeatMap, color-maps important VIX levels (7 in this case) in measuring volatility for day trading & swing trading.

Using the VIX HeatMap:

- A LOW level volatility environment: Represented by "cooler" colors (Blue & White) depicts that the level of volatility and fear is low. Percentage moves on the index level are going to be tame and less volatile more often than not. Low fear = low perceived risk.

- A MEDIUM level volatility environment: Represented by "warmer" colors (Green & Yellow) depicts that the markets are transitioning from a calmer period or from a more fearful period. Market volatility here will be higher and provide more volatile swings in price.

- A HIGH level volatility environment: Represented by "hotter" colors (Orange, Red, & Purple) depicts that the markets are very fearful at the moment and will have big swings in both directions. Historically, extreme VIX levels tend to coincide with bottoms but are in no way predictive of the exact timing as the volatile moves can continue for an extended period of time.

- Transitioning between the 7 VIX Zones: Each and every one of these specific VIX zone levels is important.

1. Extreme low: <16

2. Low: 16 to 20

3. Normal: 20 to 24

4. Medium: 24 to 28

5. Med-High: 28 to 32

6. High: 32 to 36

7. Extreme high: >36

- These VIX levels in particular measure volatility changes that have a major impact on switching between smaller time frames and measuring depths of a sell move and vice versa. Each level also behaves as its own support & resistance level in terms of taking a bit of effort to switch regimes, and aids in identifying and measuring the potential depth of pullbacks in bull markets and bounces in bear markets to reveal reversal points.

- Examples of VIX level supports depicted on the chart marked with arrows. From left to right:

1. March 10th: Markets jumped 2 volatility levels in 2 days. The fluctuations from blue to yellow to green where a sign that price action would reverse from the selloff.

2. March 28th: As soon as we move from green to the blue VIX level (<20), markets began to rally and only ended when the volatility level moved sub VIX 16 (white).

3. May 4th & 24th: Next we see the 2 dips where volatility levels went from blue to green (VIX > 20), marked bottoms and reversed higher.

4. June 1st: We see a change in VIX regime yet again into lower VIX level and markets rocket higher.

Knowing the current VIX regime is a very important tool and aid in trading, now easily visualized.

SPX Expected MoveThis indicator plots the "expected move" of SPX for today's trading session. Expected move is the amount that SPX is predicted to increase or decrease from its current price, based on the current level of implied volatility. The implied volatility in this indicator is computed from the current value of the VIX (or one of several volatility symbols available on Trading view). The computation is done using standard formula. The resulting plots are labeled as 1 and 2 standard deviations. The default values are to use VIX as well as 252 trading days in the years.

Use the square root of (days to expiration, or in this case a fraction of the day remaining) divided but the square root of (252, or number of trading days in a year).

timeRemaining = math.sqrt(DTE) / math.sqrt(252)

Standard deviation move = SPX bar closing price * (VIX/100) * timeRemaining

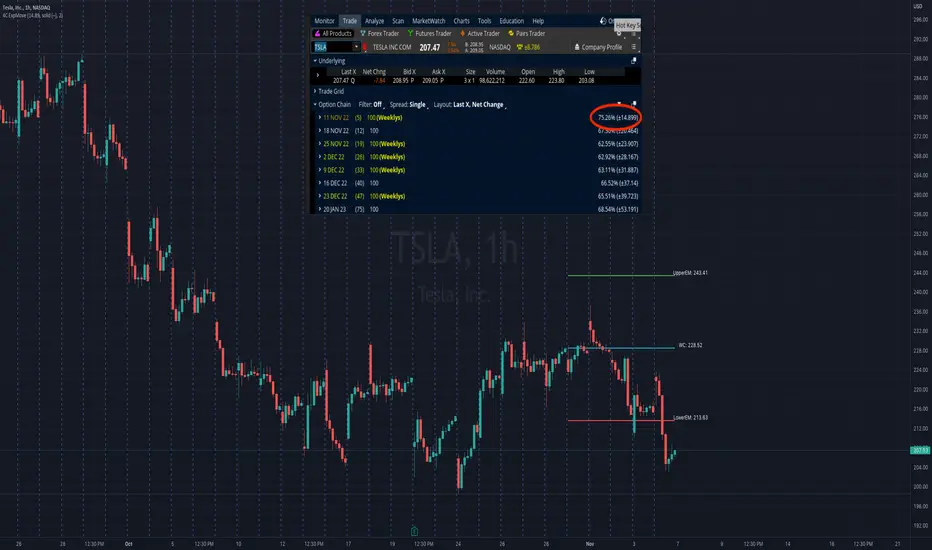

4C Expected Move (Weekly Options)This indicator plots the Expected Move (EM) calculated from weekly options pricing, for a quick visual reference.

The EM is the amount that a stock is predicted to increase or decrease from its current price, based on the current level of implied volatility.

This range can be viewed as support and resistance, or once price gets outside of the range, institutional hedging actions can accelerate the move in that direction.

The EM range is based on the Weekly close of the prior week.

It can be useful to know what the weekly EM range is for a stock to understand the probabilities of the overall distance, direction and volatility for the week.

To use this indicator you must have access to a broker with options data (not available on Tradingview).

Look at the stock's option chain and find the weekly expected move. You will have to do your own research to find where this information is displayed depending on your broker.

See screenshot example on the chart. This is the Thinkorswim platform's option chain, and the Implied Volatility % and the calculated EM is circled in red. Use the +- number in parentheses, NOT the % value.

Input that number into the indicator on a weekly basis, ideally on the weekend sometime after the cash market close on Friday, and before the Market open at the beginning of the trading week.

The indicator must be manually updated each week.

It will automatically start over at the beginning of the week.

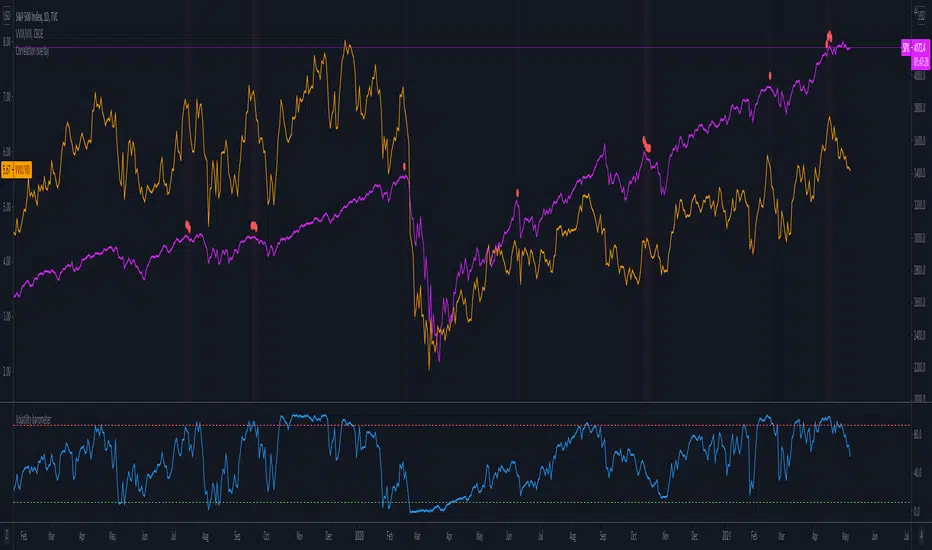

Volatility barometerIt is the indicator that analyzes the behaviour of VIX against CBOE volaility indices (VIX3M, VIX6M and VIX1Y) and VIX futures (next contract to the front one - VX!2). Because VIX is a derivate of SPX, the indicator shall be used on the SPX chart (or equivalent like SPY).

When the readings get above 90 / below 10, it means the market is overbought / oversold in terms of implied volatility. However, it does not mean it will reverse - if the price go higher along with the indicator readings then everything is fine. There is an alarming situation when the SPX is diverging - e.g. the price go higher, the readings lower. It means the SPX does not play in the same team as IVOL anymore and might reverse.

You can use it in conjunction with other implied volatility indicators for stronger signals: the Correlation overlay ( - the indicator that measures the correlation between VVIX and VIX) and VVIX/VIX ratio (it generates a signal the ratio makes 50wk high).

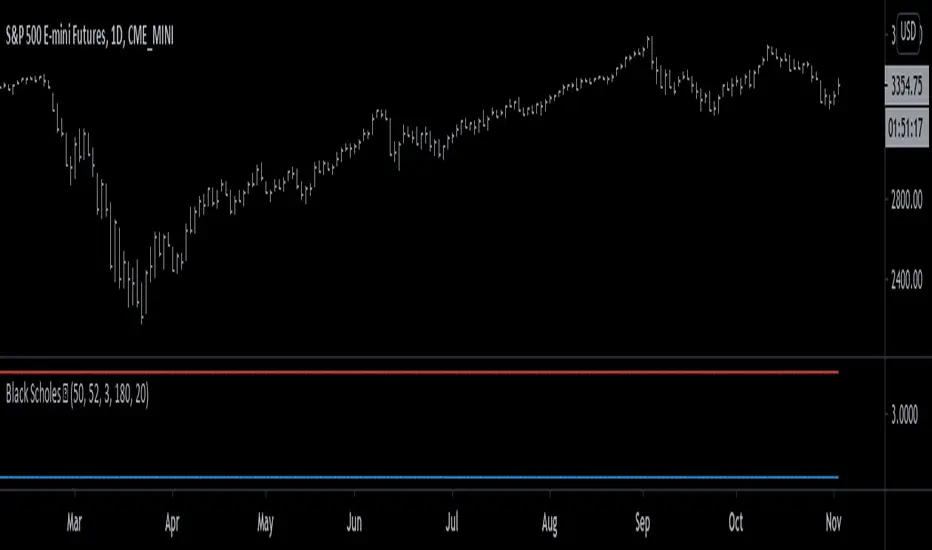

Black Scholes Model [racer8]This is the Black Scholes Model. This indicator tells you the prices of both a call option & a put option.

Input variables are spot price, strike price, risk free rate %, days to maturity, and implied volatility %.

This indicator was made generally for educational purposes.

By using this indicator, you will develop a better understanding of how options are priced.

This indicator was made to be as simple as possible so that the user can easily understand it.

I recreated the Black Scholes Model because there is very little scripts on TV that are based on the Black Scholes Model.

I am aware that are Black Scholes Model (BSM) scripts already on TV, but mine is not the same. Correct me if I'm wrong, but I don't think there is a BSM script out there yet that relies on the exact same inputs that mine does.

Why use this indicator?

If you don't already have your own IV indicator...

You can use this indicator to approximate the value of implied volatility %.

You already know every input variable except IV%, and you know the call & put option prices.

So put in the numbers for each input and put a random number between 0 to 100 into the IV% input to get the options prices.

Adjust that random number for IV% until the output (options prices) matches correctly with what you already know they are to be.

This is called the trial and error method.

On the other hand, if you already know all input variables including IV%. Then you can use this indicator to find the call & put options prices directly.

Hope this helps. Enjoy 🙂

ABCD Harmonic Pattern Strategy (Bull + Bear) This script is a strategy implementation of the classic ABCD Harmonic Pattern, designed for market structure analysis, backtesting, and educational research.

The ABCD pattern is one of the foundational harmonic price patterns in technical analysis. Its Fibonacci ratio relationships were formalized and standardized within harmonic trading theory by Scott M. Carney, whose work helped define modern harmonic pattern rules.

This strategy is conceptually inspired by educational ABCD pattern logic shared by the TradingView author theEccentricTrader.

The code, structure, execution logic, filters, and risk management have been independently developed, reconstructed, and extended into a complete TradingView strategy.

What this strategy does

Detects bullish and bearish ABCD harmonic patterns based on price structure and Fibonacci ratios.

Reconstructs ABCD market structure logic for both directions instead of using a simple visual inversion.

Draws the ABCD legs, structure labels (A, B, C, D), and projection levels directly on the chart.

Generates long and short trade entries using confirmed ABCD structures.

Includes optional confluence filters, such as:

Higher-timeframe EMA trend filter

RSI strength filter

ATR volatility filter

Volume confirmation

Candle body confirmation

Minimum bounce distance from point D

Provides built-in risk management, including:

Configurable Stop Loss

Configurable Take Profit

Optional trailing stop

Designed for backtesting, parameter optimization, and analytical research.

Why this strategy is different

This script is not a simple indicator conversion nor a basic bullish/bearish mirror.

The ABCD pattern logic has been recreated at the structural level to better reflect how bullish and bearish market formations behave in real price action.

Key differences

Reconstructed bullish and bearish structures

Bullish and bearish ABCD patterns are independently defined using market structure logic, not just inverted visually.

Each direction has its own pivot relationships and validation rules to produce a more faithful representation of the ABCD pattern.

Structure-aware pattern validation

Pattern confirmation is based on price swings, structure continuity, and Fibonacci alignment, helping reduce distorted or forced patterns.

Strategy-based execution

Unlike indicator-only ABCD tools that only visualize patterns, this script uses strategy.entry and strategy.exit, enabling full backtesting and performance analysis.

Confluence-driven entries

Trade entries can require multiple confirmation layers beyond the pattern itself, helping reduce low-quality signals and overtrading.

Integrated risk management

Stop Loss, Take Profit, and optional trailing logic are applied consistently for both long and short positions.

Non-repainting design

Pattern detection and entries rely on confirmed bars (barstate.isconfirmed) and higher-timeframe data with lookahead_off, ensuring signals do not repaint historically.

Improved and controlled visualization

Pattern drawings, projections, and entry markers are managed with strict object limits to comply with TradingView performance and publishing requirements.

How to use

Add the strategy to a chart and select a symbol and timeframe.

Enable or disable filters under “Entry Filters (Confluence)”.

Configure Stop Loss, Take Profit, and trailing behavior under “TP/SL”.

Use pattern drawings and entry markers as visual and analytical confirmation, not as standalone trade signals.

Important notes

This script is provided for educational and research purposes only.

It does not provide financial or investment advice.

No profitability or performance is implied or guaranteed.

Past performance does not indicate future results.

Always test across multiple markets and timeframes and apply proper risk management.

Credits

ABCD Harmonic Pattern: Harmonic trading principles as formalized by Scott M. Carney.

Conceptual inspiration: Educational ABCD pattern logic shared by @theEccentricTrader on TradingView.

Pattern reconstruction, strategy logic, and risk management: Independent development.

Log Trend Channel Enhanced**Log Trend Channel Enhanced (LTC+)**

A logarithmic regression channel with 11 deviation bands and comprehensive statistical metrics.

**Features:**

- Logarithmic regression trendline from customizable start date

- 11 parallel bands at ±0.5σ, ±1σ, ±1.5σ, ±2σ, ±2.5σ standard deviations

- Color-coded zones (green = undervalued, red = overvalued)

**Metrics displayed:**

- R² (goodness of fit)

- Pearson correlation

- Implied CAGR (annualized return from trendline)

- Distance from trend (%)

- Current σ position

- Channel position (%)

- Historical percentile rank

**Usage:**

Ideal for long-term trend analysis on assets with exponential growth patterns. Use on log-scale charts for best visualization. Green zones near -2σ historically indicate accumulation opportunities; red zones near +2σ suggest distribution phases.

**Settings:**

- Adjustable start date (default: 1 year ago)

- Customizable colors and line widths

- Optional deviation labels

- Configurable future projection

Adaptive Bull Ratio Strategy█ Overview: Why This Strategy

Most option strategies fall into two traps:

They are too rigid: A "Call Ratio Spread" works great in slow markets but gets destroyed if the market rallies hard.

They are too simple: A simple "Buy Call" suffers from time decay (Theta) if the market chops sideways.

The Adaptive Bull Ratio Strategy solves both . It is a living strategy that "shifts gears" based on price action.

It is called "Adaptive" because it morphs its structure three times during a trade. It starts conservative to harvest Time Decay, but if the market explodes upwards, it "uncaps" itself to ride the trend aggressively.

█ The Entry Philosophy: Why Supertrend?

The default setting uses the Supertrend indicator as the trigger. This is intentional:

Volatility Awareness: Supertrend adapts to market noise using ATR. In high volatility, bands widen to prevent false entries.

Trend Confirmation: Since Phase 1 involves selling options, entering "too early" against a falling market is dangerous. Supertrend forces patience, waiting for a confirmed reversal (Close > Trend Line), ensuring the momentum is actually in your favor before you commit capital.

The "Drift" Benefit: This strategy excels in markets that "drift" upwards. Supertrend identifies these trends while filtering out short-term chop.

Flexibility with External Sources:

While Supertrend is the default, the strategy is designed to be flexible. You can enable the 'Enable External Source' option in the settings to plug in any custom indicator (e.g., Moving Averages, Parabolic SAR, or a proprietary trendline).

The Golden Rule for External Sources: The script interprets a Bullish Signal whenever your External Source line is below the Close price (Ext Source < Close).

Compatibility: As long as your custom indicator behaves like a support line in an uptrend (plotting below the candles), it will work seamlessly with this strategy's logic.

█ The "Long Only" Rationale: Avoiding the Volatility Trap

Why not trade this on the short side (Puts) during crashes?

The Volatility Trap (Vega Risk): In Bull markets, Implied Volatility (IV) usually drops, helping your sold options decay faster. In Bear markets, IV explodes (panic). Selling OTM Puts during a crash is dangerous as their value skyrockets, neutralizing gains.

Velocity Risk: Bear markets crash fast ("Elevator Down"). Prices can blow through adjustment levels faster than the strategy can safely roll down, causing slippage.

Structural Skew: OTM Puts are inherently more expensive. Buying expensive ITM Puts and selling expensive OTM Puts shifts the breakeven further away, making V-shape recoveries painful.

█ How It Works & Stands Out

This strategy actively transforms risk profiles based on market movement:

Phase 1: The "Safe" Start (Entry)

Setup: Initiates a Call Ratio Spread (Buy 2 ITM, Sell 4 OTM) + Protective Puts.

Logic: Profits from sideways drift or slow rallies via Time Decay (Theta). The sold options finance the trade.

Phase 2: The "Shift" (Adjustment Level 1)

Trigger: Market moves above Leg 2 (3 OTM Call).

Action: Rolls Up the position. Exits initial legs, enters new higher legs, and adds a Short Put to finance the roll.

Impact: Aggressive. You bet the trend is strong enough to support the added downside risk of the short put.

Phase 3: The "Uncap" (Adjustment Level 2)

Trigger: Market moves above Leg 3 (4 OTM Call).

Action: Exits all Sold Calls.

Impact: Uncaps profit potential. The trade becomes a Net Long position (Long Calls + Short Puts), allowing you to ride a massive rally without a ceiling.

Phase 4: The "Lock-In" (Optional Trail Adjustment)

Trigger: The market goes parabolic (price rises X levels above Leg 3, configurable in settings).

Action (If Enabled):

Call Adj: Exits the Phase 3 calls and buys fresh 1-OTM calls (Rolling Up to lock profits).

Put Adj: Exits all Put legs (Removing downside risk completely).

Impact: Maximum Safety. This phase is about "banking" the windfall from a massive rally and leaving a smaller, risk-free runner to capture any final extension.

█ How to Start: A Quick Setup Guide

Step 1: Map Expiry Dates

Manually input your trading expiry dates in Settings -> Expiry Management.

Format: YYYY-MM-DD (e.g., 2025-12-25). Strict adherence required for DhanHQ.

Step 2: Configure Symbol & Size

Exchange/Symbol: Enter NSE and NIFTY (or your ticker).

Lot Multiplier: Default is 1. Set to 2 to double all quantities (e.g., Buy 2 becomes Buy 4).

Step 3: Understand Visuals

Entry Window (Light Blue): Strategy is scanning for new trades.

Non-Entry Window (Dark Blue): Trading blocked (Day before Expiry & Expiry Day). Only management allowed.

Green Box: Valid Late Entry Zone.

Red Dashed Line: Invalidation Level (if price touches this, no late entry).

Fuchsia Line: Trigger level for Special Trail Adjustments (Phase 4).

IMPORTANT: Broker & Technology Heads-Up:

The alerts generated by this script ({"secret": "...", "alertType": "multi_leg_order"...}) are specifically formatted for the DhanHQ webhook structure.

Dhan Users: Plug-and-play.

Other Brokers: You need middleware (NextLevelBot, Quantiply) to parse the JSON.

█ Risk Disclaimer & Advice

Trading options involves substantial risk.

The Whipsaw Risk: In Phase 2, you are Long Calls and Short Puts. A sharp reversal causes losses on both sides.

Margin: Selling options requires significant margin. Keep a 15-20% cash buffer to handle adjustments instantly.

Testing: This strategy is optimized for NIFTY Weekly Options. Effectiveness on BankNifty or Stocks is untested and may require parameter tuning.

Advice:

Backtest: Use TradingView Replay.

Paper Trade: Run for at least one expiry cycle before live deployment.

Consult: Seek professional financial advice before trading.

Practical Tips for Smooth Execution

For a new trader deploying this system, these operational tips are vital:

Capital Buffer: Do not trade at your limit. Always keep 10-15% free cash in your broker account. Adjustments (specifically Phase 2, where you sell an extra Put) require additional margin instantly. If margin is short, the order fails, and your hedge breaks.

Liquidity Awareness : The script trades "Far Deep OTM" options (Leg 4) to reduce margin. On indices like Nifty/BankNifty, this is fine. On individual stocks, these deep strikes might be illiquid. Check the option chain volume before deploying on stocks.

Trust the Process (but Verify) : While the algo drives, you are the pilot.

Check your API connection every morning.

Ensure the "Entry Window" background color on the chart matches your real-world date.

Verify that your broker executed all legs of a multi-leg order (partial fills are rare but possible).

The "Human" Stop: If major news breaks (e.g., unexpected election results, war announcements), volatility can expand faster than any algo can react. It is acceptable—and smart—to pause the strategy during known "Black Swan" events or earnings releases.

█ Timeframe Selection: The 30-Minute Standard

Critical Requirement: This indicator must be applied to a 30-minute chart.

Why?

Noise Filtering: The Supertrend logic is tuned to capture multi-day trends. Lower timeframes (5m, 15m) are full of "noise"—random fluctuations that look like trend changes but aren't.

Execution Logic (The Hybrid Engine): The script has a built-in "Dual Timeframe" architecture.

Decision Layer (30m): Uses the chart timeframe to decide when to be Bullish or Bearish.

Execution Layer (5m): Internally fetches 5-minute data to manage the how (Adjustments, Late Entries, and precise invalidation).

The Risk of Lower Timeframes: If you run the main chart on 5-minutes, you destroy this hierarchy. You will get too many signals, pay too much brokerage, and the internal logic may behave erratically.

Recommendation: Always keep your TradingView chart interval at 30m. Do not switch to lower timeframes expecting "faster" signals; you will likely just get "false" signals.

█ Testing Scope, Feedback

⚠️ Important Note on Asset Classes:

This strategy logic and the associated strike step calculations have been rigorously tested ONLY on NIFTY Index Options with Weekly Expiry.

BankNifty / Sensex / FinNifty: The volatility characteristics (ATR) and strike intervals of these instruments differ significantly from NIFTY. The effectiveness of this strategy on these other scripts has not been verified and may require different parameter tuning (e.g., strike_step or ATR Length).

Stocks: Individual stock options often lack the liquidity required for the "Deep OTM" legs, leading to potential execution failures.

We encourage traders to backtest this logic on other indices and share their findings! If you find a robust parameter set for BankNifty or observe unique behaviors on other scripts, please let us know in the comments below so we can improve the algorithm for everyone. Your feedback is appriciated.

Gold Macro Projection ModelGOLD MACRO PROJECTION MODEL

Multi-Factor Fair Value Estimation for Gold

OVERVIEW

The Gold Macro Projection Model estimates gold's fair value based on its historical relationships with key macroeconomic drivers. By synthesizing data from silver , M2 money supply , the US Dollar Index , TIPS (real rates proxy) , and major equity indices , this indicator projects where gold should theoretically be trading—helping traders identify potential overvaluation and undervaluation conditions.

HOW IT WORKS

This indicator employs three complementary projection methodologies :

Correlation-Weighted Z-Score Composite (50% weight)

Calculates rolling correlations between gold and each input factor. Factors with stronger correlations receive more influence. Each factor is normalized to a z-score, combined into a composite, then converted back to gold's price scale.

Silver/Gold Ratio Mean Reversion (35% weight)

The silver/gold ratio historically exhibits mean-reverting behavior. This component projects gold's implied price based on current silver prices and the historical average ratio.

M2 Money Supply Relationship (15% weight)

Gold tracks monetary expansion over long time horizons. This anchors the projection to the fundamental relationship between gold and the monetary base.

INPUT FACTORS

Silver — Strong positive correlation; precious metals move together

M2 Money Supply — Positive correlation; gold as inflation hedge

US Dollar Index (DXY) — Typically negative correlation; inverse relationship

TIPS ETF — Real interest rate proxy; gold responds to real yields

Equity Indices — Variable correlation; risk-on/risk-off dynamics

VISUAL ELEMENTS

Yellow Line — Actual gold price

Aqua Line — Projected fair value

Green Fill — Gold trading below projection (potentially undervalued)

Red Fill — Gold trading above projection (potentially overvalued)

Aqua Bands — Standard deviation envelope around projection

INFO TABLE

The indicator displays a real-time information panel showing:

Current actual vs. projected price

Divergence percentage and Z-score

Rolling correlations for each factor

Dynamic weight allocation

Buy/Sell signal based on divergence extremes

SIGNAL INTERPRETATION

STRONG BUY — Z-score below -2 (extremely undervalued)

BUY — Z-score between -2 and -1 (moderately undervalued)

NEUTRAL — Z-score between -1 and +1 (fairly valued)

SELL — Z-score between +1 and +2 (moderately overvalued)

STRONG SELL — Z-score above +2 (extremely overvalued)

SETTINGS

Correlation Period — Lookback for correlation calculations (default: 60)

Regression Period — Lookback for mean/standard deviation (default: 120)

Smoothing Period — EMA smoothing for projection line (default: 10)

Auto Weights — Toggle between correlation-based or manual weights

Band Multiplier — Standard deviation multiplier for bands (default: 1.5)

ALERTS

Gold Extremely Undervalued — Z crosses below -2

Gold Extremely Overvalued — Z crosses above +2

Gold Crossed Above Projection

Gold Crossed Below Projection

BEST PRACTICES

Use on daily timeframe for most reliable signals

Combine with the companion Gold Divergence Oscillator for timing

Disclaimer: This indicator is for educational purposes only. Past correlations do not guarantee future relationships. Always use proper risk management.

Silver Macro Projection ModelSILVER MACRO PROJECTION MODEL

Multi-Factor Fair Value Estimation for Silver

OVERVIEW

The Silver Macro Projection Model estimates silver's fair value based on its historical relationships with key macroeconomic drivers. By synthesizing data from gold, M2 money supply, the US Dollar Index, and major equity indices, this indicator projects where silver should theoretically be trading, helping traders identify potential overvaluation and undervaluation conditions.

HOW IT WORKS

This indicator employs three complementary projection methodologies:

Correlation-Weighted Z-Score Composite (50% weight) - Calculates rolling correlations between silver and each input factor. Factors with stronger correlations receive more influence. Each factor is normalized to a z-score, combined into a composite, then converted back to silver's price scale.

Gold/Silver Ratio Mean Reversion (35% weight) - The gold/silver ratio historically exhibits mean-reverting behavior. This component projects silver's implied price based on current gold prices and the historical average ratio.

M2 Money Supply Relationship (15% weight) - Silver tracks monetary expansion over long time horizons. This anchors the projection to the fundamental relationship between silver and the monetary base.

INPUT FACTORS

Gold - Strong Positive - Precious metals move together; silver amplifies gold

M2 Supply - Positive - Inflation hedge; expands with monetary base

DXY - Negative - Dollar strength pressures commodity prices

S&P 500 - Variable - Risk sentiment indicator

Dow Jones - Variable - Industrial/economic health proxy

Nasdaq 100 - Variable - Growth/risk appetite indicator

Russell 2000 - Variable - Small-cap risk sentiment

VISUAL ELEMENTS

Silver Line (Gray) - Actual silver price

Yellow Line - Model's projected fair value

Green Fill - Silver trading BELOW projection (potentially undervalued)

Red Fill - Silver trading ABOVE projection (potentially overvalued)

INFORMATION TABLE

The indicator displays a real-time panel showing:

Current correlation coefficients for each factor

Dynamic weight allocation based on correlation strength

Z-scores for each input factor

Actual vs. projected silver price

Percentage divergence from fair value

Signal classification (Strong Buy to Strong Sell)

SETTINGS

Lookback Settings

Correlation Period (default: 60) - Bars used for rolling correlations

Regression Period (default: 120) - Bars for z-score normalization

Smoothing Period (default: 10) - EMA smoothing on projection

Weight Settings

Use Auto Correlation Weights - Weights adjust dynamically based on correlation strength

Manual Weights - Override with custom factor weights

ALERTS

Silver Extremely Undervalued (Z < -2)

Silver Extremely Overvalued (Z > +2)

Price crossed above projection

Price crossed below projection

BEST PRACTICES

Use on daily timeframe for most reliable signals

Combine with the companion Divergence Oscillator for timing

Extreme divergences (>2 sigma) historically precede mean reversion

Consider macro environment as correlations shift during different regimes

Longer regression periods (150-250) for investing; shorter (60-90) for trading

Disclaimer: This indicator is for educational purposes only. Past correlations do not guarantee future relationships. Always use proper risk management.

Q# ML Logistic Regression Indicator [Lite]

Q TechLabs MLLR Lite — Machine Learning Logistic Regression Trading Indicator

© Q# Tech Labs 2025 Developed by Team Q TechLabs

Overview

Q# MLLR Lite is an open-source, lightweight TradingView indicator implementing a logistic regression model to generate buy/sell signals based on engineered price features. This “lite” version is designed for broad community access and serves as a foundation for the upcoming Pro version with advanced features and integration.

Features

Logistic Regression-based buy/sell signal generation

Customizable price source input (Open, High, Low, Close, HL2, HLC3, OHLC4)

Adjustable signal threshold and smoothing parameters

Signal confidence plotted in a separate pane

Alert conditions for buy and sell signals

Fully documented, clean Pine Script (v6) code for easy customization

Installation

Open TradingView and navigate to the Pine Script editor

Create a new script and paste the full content of the Q# MLLR Lite Pine Script

Save and add to chart

Configure inputs as needed for your trading style

Licensing

Q# MLLR Lite is provided under the MIT License, promoting open use, modification, and community collaboration with attributi

Q# MLLR Lite — Machine Learning Logistic Regression Trading Indicator

© Q# Tech Labs 2025 — Developed by Team Q#

Overview

Q# MLLR Lite is an open-source, lightweight TradingView indicator implementing a logistic regression model to generate buy/sell signals based on engineered price features. This “lite” version is designed for broad community access and serves as a foundation for the upcoming Pro version with advanced features and integration.

Features

Logistic Regression-based buy/sell signal generation

Customizable price source input (Open, High, Low, Close, HL2, HLC3, OHLC4)

Adjustable signal threshold and smoothing parameters

Signal confidence plotted in a separate pane

Alert conditions for buy and sell signals

Fully documented, clean Pine Script (v6) code for easy customization

Installation

Open TradingView and navigate to the Pine Script editor

Create a new script and paste the full content of the Q# MLLR Lite Pine Script

Save and add to chart

Configure inputs as needed for your trading style

Licensing

Q# MLLR Lite is provided under the MIT License, promoting open use, modification, and community collaboration with attribution.

Copyright (c) 2025 Q# Tech Labs

Permission is hereby granted, free of charge, to any person obtaining a copy

of this software and associated documentation files (the "Software"), to deal

in the Software without restriction, including without limitation the rights

to use, copy, modify, merge, publish, distribute, sublicense, and/or sell

copies of the Software, and to permit persons to whom the Software is

furnished to do so, subject to the following conditions:

The above copyright notice and this permission notice shall be included in all

copies or substantial portions of the Software.

THE SOFTWARE IS PROVIDED "AS IS", WITHOUT WARRANTY OF ANY KIND, EXPRESS OR

IMPLIED, INCLUDING BUT NOT LIMITED TO THE WARRANTIES OF MERCHANTABILITY,

FITNESS FOR A PARTICULAR PURPOSE AND NONINFRINGEMENT. IN NO EVENT SHALL THE

AUTHORS OR COPYRIGHT HOLDERS BE LIABLE FOR ANY CLAIM, DAMAGES OR OTHER

LIABILITY, WHETHER IN AN ACTION OF CONTRACT, TORT OR OTHERWISE, ARISING FROM,

OUT OF OR IN CONNECTION WITH THE SOFTWARE OR THE USE OR OTHER DEALINGS IN THE

SOFTWARE.

Buying Opportunity Score V2.2Buying Opportunity Indicator V2.2

What This Indicator Does

This indicator identifies potential buying opportunities during market fear and pullbacks by combining multiple technical signals into a single composite score (0-100). Higher scores indicate more fear/oversold conditions are present simultaneously.

Why These Components?

Market bottoms typically occur when multiple fear signals align. This indicator combines five complementary measurements that each capture different aspects of market stress:

1. VIX Level (30 points) - Measures implied volatility/fear. VIX spikes during selloffs as traders buy protection. Thresholds based on historical percentiles (VIX 25+ is ~85th percentile historically).

2. Price Drawdown (30 points) - Distance from 52-week high. Larger drawdowns create better risk/reward for mean reversion entries. A 10%+ drawdown from highs historically presents better entry points than buying at all-time highs.

3. RSI 14 (12 points) - Classic momentum oscillator measuring oversold conditions. RSI below 30 indicates short-term selling exhaustion.

4. Bollinger Band Position (13 points) - Statistical measure of price extension. Price below the lower band (2 standard deviations) indicates statistically unusual weakness.

5. VIX Timing (15 points) - Bonus points when VIX is declining from a recent peak. This helps avoid catching falling knives by waiting for fear to subside.

How The Score Works

- Each component contributes points based on severity

- Components are weighted by predictive value from historical analysis

- Score of 70+ means multiple fear signals are present

- Score of 80+ means extreme fear across most components

How To Use

1. Apply to SPY, QQQ, or IWM on daily timeframe

2. Monitor the Current Score in the statistics table

3. Scores below 50 = normal conditions, no action needed

4. Scores 60-69 = elevated fear, monitor closely

5. Scores 70+ = consider entering long positions

6. Scores 80+ = strongest historical entry points

Important Limitations

- This is a research tool, not financial advice

- Past patterns may not repeat in the future

- Signals are infrequent (typically 2-4 per year reaching 70+)

- Works best on broad market ETFs; not validated for individual stocks

- Always use proper position sizing and risk management

- The indicator identifies conditions that have historically been favorable, but cannot predict future returns

Statistics Table

The table shows:

- Current Score with context message

- Chart Results: Rolling 1Y/3Y/5Y statistics from your loaded chart data

Alerts

Multiple alert options available for different score thresholds.

Open Source

Code is fully visible for review and educational purposes.

MarketMind LITEM🜁rketMind LITE ────────────────────

Essential Market Awareness, Reduced to Its Core

M🜁rketMind LITE is a lightweight market awareness tool designed to display essential situational context .

It provides basic orientation and movement awareness without interpretation, risk framing, diagnostics, or decision guidance.

This script is designed as a standalone awareness layer. It does not evaluate trade quality, issue signals, or influence decision-making.

WHAT IT DOES ────────────────────

M🜁rketMind LITE presents a minimal, static view of current market conditions focused entirely on awareness rather than analysis.

The system displays only essential context, allowing traders to stay oriented without introducing judgment, noise, or implied direction.

The script provides visibility into:

Time-of-day session context

Basic market regime classification (trending, range-bound, mixed)

Short-term momentum direction only (up, down, neutral)

A clean, static HUD display

M🜁rketMind LITE also includes a minimal visual state indicator that reflects recent price responsiveness, intended to be observed over time alongside the trader’s own experience.

The goal is to support awareness without influence .

HOW TO USE IT ────────────────────

M🜁rketMind LITE is not a signal generator.

It is designed to remain visible in the background of any chart, offering quiet orientation while traders rely entirely on their own process for analysis and execution.

Common use cases include:

Maintaining session awareness

Preserving context during focused trading periods

Reducing cognitive load while monitoring markets

M🜁rketMind LITE does not evaluate risk, alignment, or opportunity.

It simply shows what is happening.

DESIGN PHILOSOPHY ────────────────────

M🜁rketMind LITE is intentionally minimal.

It includes only essential awareness elements and excludes all interpretive or evaluative logic:

Situational context only

Directional momentum (up / down / neutral)

No diagnostics, confidence, or conviction framing

No process, risk, or quality assessment

Presentation controls only (HUD on/off, size, position)

Nothing is inferred.

Nothing is suggested.

This script shows market state without interpretation.

WHO IT IS FOR ────────────────────

M🜁rketMind LITE is suited for traders who:

Want passive situational awareness

Prefer minimal on-chart information

Already operate with a defined decision process

It is not designed for:

Analytical or diagnostic use

Risk evaluation or context synthesis

Traders seeking guidance or confirmation

IMPORTANT NOTES ────────────────────

M🜁rketMind LITE does not provide financial advice

No system can predict future price behavior

This tool is designed for awareness only

Used appropriately, M🜁rketMind LITE helps traders stay oriented without interference.

Density Zones (GM Crossing Clusters) + QHO Spin FlipsINDICATOR NAME

Density Zones (GM Crossing Clusters) + QHO Spin Flips

OVERVIEW

This indicator combines two complementary ideas into a single overlay: *this combines my earlier Geometric Mean Indicator with the Quantum Harmonic Oscillator (Overlay) with additional enhancements*

1) Density Zones (GM Crossing Clusters)

A “Density Zone” is detected when price repeatedly crosses a Geometric Mean equilibrium line (GM) within a rolling lookback window. Conceptually, this identifies regions where the market is repeatedly “snapping” across an equilibrium boundary—high churn, high decision pressure, and repeated re-selection of direction.

2) QHO Spin Flips (Regression-Residual σ Breaches)

A “Spin Flip” is detected when price deviates beyond a configurable σ-threshold (κ) from a regression-based equilibrium, using normalized residuals. Conceptually, this marks excursions into extreme states (decoherence / expansion), which often precede a reversion toward equilibrium and/or a regime re-scaling.

These two systems are related but not identical:

- Density Zones identify where equilibrium crossings cluster (a “singularity”/anchor behavior around GM).

- Spin Flips identify when price exceeds statistically extreme displacement from the regression equilibrium (LSR), indicating expansion beyond typical variance.

CORE CONCEPTS AND FORMULAS

SECTION A — GEOMETRIC MEAN EQUILIBRIUM (GM)

We define two moving averages:

(1) MA1_t = SMA(close_t, L1)

(2) MA2_t = SMA(close_t, L2)

We define the equilibrium anchor as the geometric mean of MA1 and MA2:

(3) GM_t = sqrt( MA1_t * MA2_t )

This GM line acts as an equilibrium boundary. Repeated crossings are interpreted as high “equilibrium churn.”

SECTION B — CROSS EVENTS (UP/DOWN)

A “cross event” is registered when the sign of (close - GM) changes:

Define a sign function s_t:

(4) s_t =

+1 if close_t > GM_t

-1 if close_t < GM_t

s_{t-1} if close_t == GM_t (tie-breaker to avoid false flips)

Then define the crossing event indicator:

(5) crossEvent_t = 1 if s_t != s_{t-1}

0 otherwise

Additionally, the indicator plots explicit cross markers:

- Cross Above GM: crossover(close, GM)

- Cross Below GM: crossunder(close, GM)

These provide directional visual cues and match the original Geometric Mean Indicator behavior.

SECTION C — DENSITY MEASURE (CROSSING CLUSTER COUNT)

A Density Zone is based on the number of cross events occurring in the last W bars:

(6) D_t = Σ_{i=0..W-1} crossEvent_{t-i}

This is a “crossing density” score: how many times price has toggled across GM recently.

The script implements this efficiently using a cumulative sum identity:

Let x_t = crossEvent_t.

(7) cumX_t = Σ_{j=0..t} x_j

Then:

(8) D_t = cumX_t - cumX_{t-W} (for t >= W)

cumX_t (for t < W)

SECTION D — DENSITY ZONE TRIGGER

We define a Density Zone state:

(9) isDZ_t = ( D_t >= θ )

where:

- θ (theta) is the user-selected crossing threshold.

Zone edges:

(10) dzStart_t = isDZ_t AND NOT isDZ_{t-1}

(11) dzEnd_t = NOT isDZ_t AND isDZ_{t-1}

SECTION E — DENSITY ZONE BOUNDS

While inside a Density Zone, we track the running high/low to display zone bounds:

(12) dzHi_t = max(dzHi_{t-1}, high_t) if isDZ_t

(13) dzLo_t = min(dzLo_{t-1}, low_t) if isDZ_t

On dzStart:

(14) dzHi_t := high_t

(15) dzLo_t := low_t

Outside zones, bounds are reset to NA.

These bounds visually bracket the “singularity span” (the churn envelope) during each density episode.

SECTION F — QHO EQUILIBRIUM (REGRESSION CENTERLINE)

Define the regression equilibrium (LSR):

(16) m_t = linreg(close_t, L, 0)

This is the “centerline” the QHO system uses as equilibrium.

SECTION G — RESIDUAL AND σ (FIELD WIDTH)

Residual:

(17) r_t = close_t - m_t

Rolling standard deviation of residuals:

(18) σ_t = stdev(r_t, L)

This σ_t is the local volatility/width of the residual field around the regression equilibrium.

SECTION H — NORMALIZED DISPLACEMENT AND SPIN FLIP

Define the standardized displacement:

(19) Y_t = (close_t - m_t) / σ_t

(If σ_t = 0, the script safely treats Y_t = 0.)

Spin Flip trigger uses a user threshold κ:

(20) spinFlip_t = ( |Y_t| > κ )

Directional spin flips:

(21) spinUp_t = ( Y_t > +κ )

(22) spinDn_t = ( Y_t < -κ )

The default κ=3.0 corresponds to “3σ excursions,” which are statistically extreme under a normal residual assumption (even though real markets are not perfectly normal).

SECTION I — QHO BANDS (OPTIONAL VISUALIZATION)

The indicator optionally draws the standard σ-bands around the regression equilibrium:

(23) 1σ bands: m_t ± 1·σ_t

(24) 2σ bands: m_t ± 2·σ_t

(25) 3σ bands: m_t ± 3·σ_t

These provide immediate context for the Spin Flip events.

WHAT YOU SEE ON THE CHART

1) MA1 / MA2 / GM lines (optional)

- MA1 (blue), MA2 (red), GM (green).

- GM is the equilibrium anchor for Density Zones and cross markers.

2) GM Cross Markers (optional)

- “GM↑” label markers appear on bars where close crosses above GM.

- “GM↓” label markers appear on bars where close crosses below GM.

3) Density Zone Shading (optional)

- Background shading appears while isDZ_t = true.

- This is the period where the crossing density D_t is above θ.

4) Density Zone High/Low Bounds (optional)

- Two lines (dzHi / dzLo) are drawn only while in-zone.

- These bounds bracket the full churn envelope during the density episode.

5) QHO Bands (optional)

- 1σ, 2σ, 3σ shaded zones around regression equilibrium.

- These visualize the current variance field.

6) Regression Equilibrium (LSR Centerline)

- The white centerline is the regression equilibrium m_t.

7) Spin Flip Markers

- A circle is plotted when |Y_t| > κ (beyond your chosen σ-threshold).

- Marker size is user-controlled (tiny → huge).

HOW TO USE IT

Step 1 — Pick the equilibrium anchor (GM)

- L1 and L2 define MA1 and MA2.

- GM = sqrt(MA1 * MA2) becomes your equilibrium boundary.

Typical choices:

- Faster equilibrium: L1=20, L2=50 (default-like).

- Slower equilibrium: L1=50, L2=200 (macro anchor).

Interpretation:

- GM acts like a “center of mass” between two moving averages.

- Crosses show when price flips from one side of equilibrium to the other.

Step 2 — Tune Density Zones (W and θ)

- W controls the time window measured (how far back you count crossings).

- θ controls how many crossings qualify as a “density/singularity episode.”

Guideline:

- Larger W = slower, broader density detection.

- Higher θ = only the most intense churn is labeled as a Density Zone.

Interpretation:

- A Density Zone is not “bullish” or “bearish” by itself.

- It is a condition: repeated equilibrium toggling (high churn / high compression).

- These often precede expansions, but direction is not implied by the zone alone.

Step 3 — Tune the QHO spin flip sensitivity (L and κ)

- L controls regression memory and σ estimation length.

- κ controls how extreme the displacement must be to trigger a spin flip.

Guideline:

- Smaller L = more reactive centerline and σ.

- Larger L = smoother, slower “field” definition.

- κ=3.0 = strong extreme filter.

- κ=2.0 = more frequent flips.

Interpretation:

- Spin flips mark when price exits the “normal” residual field.

- In your model language: a moment of decoherence/expansion that is statistically extreme relative to recent equilibrium.

Step 4 — Read the combined behavior (your key thesis)

A) Density Zone forms (GM churn clusters):

- Market repeatedly crosses equilibrium (GM), compressing into a bounded churn envelope.

- dzHi/dzLo show the envelope range.

B) Expansion occurs:

- Price can release away from the density envelope (up or down).

- If it expands far enough relative to regression equilibrium, a Spin Flip triggers (|Y| > κ).

C) Re-coherence:

- After a spin flip, price often returns toward equilibrium structures:

- toward the regression centerline m_t

- and/or back toward the density envelope (dzHi/dzLo) depending on regime behavior.

- The indicator does not guarantee return, but it highlights the condition where return-to-field is statistically likely in many regimes.

IMPORTANT NOTES / DISCLAIMERS

- This indicator is an analytical overlay. It does not provide financial advice.

- Density Zones are condition states derived from GM crossing frequency; they do not predict direction.

- Spin Flips are statistical excursions based on regression residuals and rolling σ; markets have fat tails and non-stationarity, so σ-based thresholds are contextual, not absolute.

- All parameters (L1, L2, W, θ, L, κ) should be tuned per asset, timeframe, and volatility regime.

PARAMETER SUMMARY

Geometric Mean / Density Zones:

- L1: MA1 length

- L2: MA2 length

- GM_t = sqrt(SMA(L1)*SMA(L2))

- W: crossing-count lookback window

- θ: crossing density threshold

- D_t = Σ crossEvent_{t-i} over W

- isDZ_t = (D_t >= θ)

- dzHi/dzLo track envelope bounds while isDZ is true

QHO / Spin Flips:

- L: regression + residual σ length

- m_t = linreg(close, L, 0)

- r_t = close_t - m_t

- σ_t = stdev(r_t, L)

- Y_t = r_t / σ_t

- spinFlip_t = (|Y_t| > κ)

Visual Controls:

- toggles for GM lines, cross markers, zone shading, bounds, QHO bands

- marker size options for GM crosses and spin flips

ALERTS INCLUDED

- Density Zone START / END

- Spin Flip UP / DOWN

- Cross Above GM / Cross Below GM

SUMMARY

This indicator treats the Geometric Mean as an equilibrium boundary and identifies “Density Zones” when price repeatedly crosses that equilibrium within a rolling window, forming a bounded churn envelope (dzHi/dzLo). It also models a regression-based equilibrium field and triggers “Spin Flips” when price makes statistically extreme σ-excursions from that field. Used together, Density Zones highlight compression/decision regions (equilibrium churn), while Spin Flips highlight extreme expansion states (σ-breaches), allowing the user to visualize how price compresses around equilibrium, releases outward, and often re-stabilizes around equilibrium structures over time.

Shiori TFGI Lite Technical Fear and Greed Index (Open Source)Shiori’s TFGI Lite

Technical Fear & Greed Index (Open Source)

---

English — Official Description

Shiori’s TFGI Lite is an open-source Technical Fear & Greed Index designed to help traders and investors understand market emotion, not predict price.

Instead of generating buy or sell signals, this indicator focuses on answering a calmer, more important question:

> Is the market emotionally stretched away from its own historical balance?

TFGI Lite combines three well-known technical dimensions — volatility, price deviation, and momentum — and normalizes them into a single, intuitive 0–100 sentiment scale.

What This Indicator Is

* A market context tool, not a trading signal

* A way to observe emotional extremes and misalignment

* Designed for any asset, any timeframe

* Fully open source, transparent and adjustable

Core Components

* Fear Factor: Short-term vs long-term ATR ratio with logarithmic compression

* Greed Factor: Price Z-score with tanh-based normalization

* Momentum Factor: Classic RSI as emotional momentum

These factors are blended and gently smoothed to form the current sentiment level.

Historical Baseline & Deviation

TFGI Lite introduces a historical baseline concept:

* The baseline represents the market’s own emotional equilibrium

* Deviation measures how far current sentiment has drifted from that equilibrium

This allows the indicator to highlight conditions such as:

* 🔥 Overheated: High sentiment + strong positive deviation

* 💎 Undervalued: Low sentiment + strong negative deviation

* ⚠️ Misaligned: Emotionally extreme, but inconsistent with historical behavior

How to Use (Lite Philosophy)

* Use TFGI Lite as a background compass, not a trigger

* Combine it with price structure, risk management, and your own strategy

* Extreme readings suggest emotional tension, not immediate reversal

> Think of TFGI Lite as market weather — it tells you the climate, not when to open or close the door.

About Parameters & Customization

All parameters in TFGI Lite are fully adjustable. Markets have different personalities — volatility, sentiment range, and emotional extremes vary by asset and timeframe.

You are encouraged to:

* Adjust fear/greed thresholds based on the asset you trade

* Tune smoothing and baseline lengths to match your timeframe

* Treat sentiment levels as relative, not universal absolutes

There is no single “correct” setting — TFGI Lite is designed to adapt to your market, not force the market into a fixed model.

Important Notes

* This is a technical sentiment indicator, not financial advice

* No future performance is implied

* Designed to reduce emotional decision-making, not replace it

---

🇹🇼 繁體中文 — 指標說明

Shiori’s TFGI Lite(技術型恐懼與貪婪指數) 是一款開源的市場情緒指標,目的不是預測價格,而是幫助你理解市場當下的「情緒狀態」。

與其問「現在該不該買或賣」,TFGI Lite 更關心的是:

> 市場情緒是否已經偏離了它自己的歷史平衡?

本指標整合三個常見但關鍵的技術面向,並統一轉換為 0–100 的情緒刻度,讓市場狀態一眼可讀。

這個指標是什麼

* 市場情緒與狀態觀察工具(非買賣訊號)

* 用來辨識情緒極端與錯位狀態

* 適用於任何商品與任何週期

* 完全開源,可學習、可調整

核心構成

* 恐懼因子:短期 / 長期 ATR 比例(對數壓縮)

* 貪婪因子:價格 Z-Score(tanh 正規化)

* 動能因子:RSI 作為情緒動量

歷史基準與偏離

TFGI Lite 引入「歷史情緒基準」的概念:

* 基準代表市場長期的情緒平衡

* 偏離值顯示當前情緒與自身歷史的距離

因此可以辨識:

* 🔥 過熱(高情緒 + 正向偏離)

* 💎 低估(低情緒 + 負向偏離)

* ⚠️ 錯位(情緒極端,但不符合歷史行為)

使用建議(Lite 精神)

* 將 TFGI Lite 作為「背景雷達」,而非進出場依據

* 搭配價格結構、風險控管與個人策略

* 情緒極端不等於立刻反轉

> 你可以把它想像成市場的天氣預報,而不是交易指令。

參數調整與個人化說明

本指標中的所有參數皆可調整。不同市場、不同商品,其波動特性與情緒區間並不相同。

建議你:

* 依標的特性自行調整恐懼 / 貪婪門檻

* 依交易週期調整平滑與基準長度

* 將情緒數值視為「相對狀態」,而非固定答案

TFGI Lite 的設計初衷,是讓你定義市場,而不是被單一參數綁住。

溫馨提示

如果你在調整指標參數時遇到不熟悉的項目,請點擊參數旁邊的 「!」圖示,每個設定都有清楚的說明。

本指標設計為可慢慢探索,請依自己的節奏理解市場狀態。

---

🇯🇵 日本語 — インジケーター説明

Shiori’s TFGI Lite は、価格を予測するための指標ではなく、

市場の「感情状態」を可視化するためのオープンソース指標です。

この指標が問いかけるのは、

> 現在の市場感情は、過去のバランスからどれだけ乖離しているのか?

という一点です。

特徴

* 売買シグナルではありません

* 市場心理の極端さやズレを観察するためのツールです

* すべての銘柄・時間軸に対応

* 学習・調整可能なオープンソース

構成要素

* 恐怖要素:ATR 比率(対数圧縮)

* 強欲要素:価格 Z スコア(tanh 正規化)

* モメンタム:RSI

ベースラインと乖離

市場自身の感情的な基準点と、

現在の感情との距離を測定します。

過熱・割安・感情のズレを視覚的に把握できます。

パラメータ調整について

TFGI Lite のすべてのパラメータは調整可能です。市場ごとにボラティリティや感情の振れ幅は異なります。

* 恐怖・強欲の閾値は銘柄に応じて調整してください

* 時間軸に合わせて平滑化やベースライン期間を変更できます

* 数値は絶対値ではなく、相対的な感情状態として捉えてください

この指標は、市場に合わせて柔軟に使うことを前提に設計されています。

フレンドリーヒント

入力項目で分からない設定がある場合は、横に表示されている 「!」アイコン をクリックしてください。各パラメータには分かりやすい説明が用意されています。

このインジケーターは、落ち着いて市場の状態を理解するためのものです。

---

🇰🇷 한국어 — 지표 설명

Shiori’s TFGI Lite는 매수·매도 신호를 제공하는 지표가 아니라,

시장 감정의 상태를 이해하기 위한 기술적 심리 지표입니다.

이 지표의 핵심 질문은 다음과 같습니다.

> 현재 시장 감정은 과거의 균형 상태에서 얼마나 벗어나 있는가?

특징

* 거래 신호 아님

* 시장 심리의 과열·저평가·불일치를 관찰

* 모든 자산, 모든 타임프레임 지원

* 오픈소스 기반

구성 요소

* 공포 요인: ATR 비율 (로그 압축)

* 탐욕 요인: Z-Score (tanh 정규화)

* 모멘텀: RSI

활용 방법

TFGI Lite는 배경 지표로 사용하세요.

가격 구조와 리스크 관리와 함께 사용할 때 가장 효과적입니다.

파라미터 조정 안내

TFGI Lite의 모든 설정 값은 사용자가 직접 조정할 수 있습니다. 자산마다 변동성과 감정 범위는 서로 다릅니다.

* 공포 / 탐욕 기준값은 종목 특성에 맞게 조정하세요

* 타임프레임에 따라 스무딩 및 기준 기간을 변경할 수 있습니다

* 감정 수치는 절대적인 값이 아닌 상대적 상태로 해석하세요

이 지표는 하나의 정답을 강요하지 않고, 시장에 맞춰 적응하도록 설계되었습니다.

친절한 안내

설정 값이 익숙하지 않다면, 항목 옆에 있는 "!" 아이콘을 클릭해 보세요. 각 입력값마다 설명이 제공됩니다.

이 지표는 천천히 시장의 맥락을 이해하도록 설계되었습니다.

---

Educational purpose only. Not financial advice.

---

#FearAndGreed #MarketSentiment #TradingPsychology #TechnicalAnalysis #OpenSourceIndicator #Volatility #RSI #ATR #ZScore #MultiAsset #TradingView #Shiori

FF calculation Saptarshi ChatterjeeForward factor (in options contexts) measures implied volatility (IV) for a future period between two expirations, like from 30 DTE (days to expiry) front-month to 60 DTE back-month options.

This indicator calculates the FORWARD FACTOR(FF) using 2 IVs of 2 DTEs.

+ve value means front DTE is rich in premium and back expiry is cheap.

-ve value means front DTE IV is cheap and 2nd DTE is expensive

we can use this term structure disbalance to trade calendar spreads with edge.

FAIR VALUE CEDEARSFair Value CEDEARS y ETFs

Important: load together with the CEDEARdata library.

Returns the “Fair Value” of CEDEAR and CEDEAR-based ETF prices traded on ByMA, using as a reference the price of the underlying ordinary share or ETF traded on the NYSE or NASDAQ. It multiplies the NYSE/NASDAQ price by the CEDEAR or ETF conversion ratio and converts the currency to ARS or Dólar MEP using the exchange rate implied by the AL30/AL30C ratio for tickers quoted in ARS (e.g., AAPL) and AL30D/AL30C for tickers quoted in Dólar MEP (e.g., AAPLD).

If the CEDEAR or ETF quote is higher than Fair Value, it highlights the difference in red; if it is lower, it highlights it in green. If any of the markets is closed or in an auction period, it notifies the user and changes the background color.

By default, the CEDEAR or ETF quote used is the last price, but the user may choose to use the BID or OFFER instead. This allows CEDEAR and ETF buyers to compare Fair Value against the OFFER, while sellers may prefer to measure Fair Value against the BID of the local instrument.

BCBA:AAPL

BCBA:AAPLD

NASDAQ:AAPL

BCBA:SPY

BCBA:TSLA

BCBA:TSLAD

CEDEARS

ETFs

ByMA

CISD**CISD – Continuous Implied Structure Displacement (Body-Based Version)**

CISD displays structure levels derived from a simple sequence:

1. A valid pullback (based on body closes only)

2. Followed by a displacement (a body-based break in the opposite direction)

When these two conditions occur, the script prints a CISD level at the pullback’s reference price.

Each CISD level extends forward until price closes through it using body logic only.

---

### How this version works

**1. Pullback Detection (Body-Only)**

A pullback is recognized when a candle’s body meaningfully retraces the previous candle’s body.

Tiny candles are filtered out, reducing noise and improving level quality.

**2. CISD Formation**

After a valid pullback, if price breaks structure in the opposite direction using body highs/lows only:

- A **Bullish CISD** level is created from a bearish pullback

- A **Bearish CISD** level is created from a bullish pullback

**3. CISD Completion**

When a CISD level is violated by a full body close beyond the level, the CISD is marked completed and a new opposite CISD becomes eligible.

**4. Visual Output**

- Clean horizontal CISD levels

- Single active level per direction (unless extended manually)

- Labels marked “CISD” for clarity

---

### What this indicator is *not*

This tool does **not** generate trade signals or provide financial advice.

It is a visual mechanism for observing how price reacts to pullback-based structural shifts using body logic only.

---

### Intended Use

CISD can help users:

- Track transitions in short-term structure

- Identify when pullbacks lead to meaningful displacement

- Observe reaction points derived strictly from body behavior (ignoring wicks)

The logic is minimalistic and designed for clean, uncluttered structure observation.

Volatility Regime NavigatorA guide to understanding VIX, VVIX, VIX9D, VVIX/VIX, and the Composite Risk Score

1. Purpose of the Indicator

This dashboard summarizes short-term market volatility conditions using four core volatility metrics.

It produces:

• Individual readings

• A combined Regime classification

• A Composite Risk Score (0–100)

• A simplified Risk Bucket (Bullish → Stress)

Use this to evaluate market fragility, drift potential, tail-risk, and overall risk-on/off conditions.

This is especially useful for intraday ES/NQ trading, expected-move context, and understanding when breakouts or fades have edge.

2. The Four Core Volatility Inputs

(1) VIX — Baseline Equity Volatility

• < 16: Complacent (easy drift-up, but watch for fragility)

• 16–22: Healthy, normal volatility → ideal trading conditions

• > 22: Stress rising

• > 26: Tail-risk / risk-off environment

(2) VIX9D — Short-Term Event Vol

Measures 9-day implied volatility. Reacts to immediate news/events.

• < 14: Strongly bullish (drift regime)

• 14–17: Bullish to neutral

• 17–20: Event risk building

• > 20: Short-term stress / caution

(3) VVIX — Volatility of VIX (fragility index)

Tracks volatility of volatility.

• < 100: “Bullish, Bullish” — very low fragility

• 100–120: Normal

• 120–140: Fragile

• > 140: Stress, hedging pressure

(4) VVIX/VIX Ratio — Microstructure Risk-On/Risk-Off

One of the most sensitive indicators of market confidence.

• 5.0–6.5: Strongest “normal/bullish” zone

• < 5.0: Bottom-stalking / fear regime

• > 6.5: Complacency → vulnerable to reversals

• > 7.5: Fragile / top-risk

3. Composite Risk Score (0–100)

The dashboard converts all four inputs into a single score.

Score Interpretation

• 80–100 → Bullish - Drift regime. Shallow pullbacks. Upside favored.

• 60–79 → Normal - Healthy tape. Balanced two-way trading.

• 40–59 → Fragile - Choppy, failed breakouts, thinner liquidity.

• 20–39 → Risk-Off - Downside tails active. Favor fades and defensive behavior.

• < 20 → Stress - Crisis or event-driven tape. Avoid longs.

Score updates every bar.

4. Regime Label

Independent of the composite score, the script provides a Regime classification based on combinations of VIX + VVIX/VIX:

• Bullish+ → Buying is easy, tape lifts passively

• Normal → Cleanest and most tradable conditions

• Complacent → Top-risk; be careful chasing upside

• Mixed → Signals conflict; chop potential

• Bottom Stalk → High VIX, low VVIX/VIX (capitulation signatures)

A trailing “+” or “*” indicates additional bullish or caution overlays from VIX9D/VVIX.

5. How to Use the Dashboard in Trading

When Bullish (Score ≥ 80):

• Expect drift-up behavior

• Downside limited unless catalyst hits

• Structure favors breakouts and trend continuation

• Mean reversion trades have lower expectancy

When Normal (Score 60–79):

• The “playbook regime”

• Breakouts and mean reversion both valid

• Best overall trading environment

When Fragile (Score 40–59):

• Expect chop

• Breakouts fail

• Take quicker profits

• Avoid overleveraged directional bets

When Risk-Off (20–39):

• Favor fades of strength

• Downside tails activate

• Trend-following short setups gain edge

• Respect volatility bands

When Stress (<20):

• Avoid long exposure

• Do not chase dips

• Expect violent, news-sensitive behavior

• Position sizing becomes critical

6. Quick Summary

• VIX = weather

• VIX9D = short-term storm radar

• VVIX = foundation stability

• VVIX/VIX = confidence vs fragility

• Composite Score = overall regime health

• Risk Bucket = simple “what do I do?” label

This dashboard gives traders a high-confidence, low-noise view of equity volatility conditions in real time.

NIFTY Weekly Option Seller DirectionalHere’s a straight description you can paste into the TradingView “Description” box and tweak if needed:

---

### NIFTY Weekly Option Seller – Regime + Score + Management (Single TF)

This indicator is built for **weekly option sellers** (primarily NIFTY) who want a **structured regime + scoring framework** to decide:

* Whether to trade **Iron Condor (IC)**, **Put Credit Spread (PCS)** or **Call Credit Spread (CCS)**

* How strong that regime is on the current timeframe (score 0–5)

* When to **DEFEND** existing positions and when to **HARVEST** profits

> **Note:** This is a **single timeframe** tool. The original system uses it on **4H and 1D separately**, then combines scores manually (e.g., using `min(4H, 1D)` for conviction and lot sizing).

---

## Core logic

The script classifies the market into 3 regimes:

* **IC (Iron Condor)** – range/mean-reversion conditions

* **PCS (Put Credit Spread)** – bullish/trend-up conditions

* **CCS (Call Credit Spread)** – bearish/trend-down conditions

For each regime, it builds a **0–5 score** using:

* **EMA stack (8/13/34)** – trend structure

* **ADX (custom DMI-based)** – trend strength vs range

* **Previous-day CPR** – in CPR vs break above/below

* **VWAP (session)** – near/far value

* **Camarilla H3/L3** – for IC context

* **RSI (14)** – used as a **brake**, not a primary signal

* **Daily trend / Daily ADX** – used as **hard gates**, not double-counted as extra points

Then:

* Scores for PCS / CCS / IC are **cross-penalised** (they pull each other down if conflicting)

* Final scores are **smoothed** (current + previous bar) to avoid jumpy signals

The **background colour** shows the current regime and conviction:

* Blue = IC

* Green = PCS

* Red = CCS

* Stronger tint = higher regime score

---

## Scoring details (per timeframe)

**PCS (uptrend, bullish credit spreads)**

* +2 if EMA(8) > EMA(13) > EMA(34)

* +1 if ADX > ADX_TREND

* +1 if close > CPR High

* +1 if close > VWAP

* RSI brake:

* If RSI < 50 → PCS capped at 2

* If RSI > 75 → PCS capped at 3

* Daily gating:

* If daily EMA stack is **not** uptrend → PCS capped at 2

**CCS (downtrend, bearish credit spreads)**

* +2 if EMA(8) < EMA(13) < EMA(34)

* +1 if ADX > ADX_TREND

* +1 if close < CPR Low

* +1 if close < VWAP

* RSI brake:

* If RSI > 50 → CCS capped at 2

* If RSI < 25 → CCS capped at 3

* Daily gating:

* If daily EMA stack is **not** downtrend → CCS capped at 2

**IC (range / mean-reversion)**

* +2 if ADX < ADX_RANGE (low trend)

* +1 if close inside CPR

* +1 if near VWAP

* +0.5 if inside Camarilla H3–L3

* +1 if daily ADX < ADX_RANGE (daily also range-like)

* +0.5 if RSI between 45 and 55 (classic balance zone)

* Daily gating:

* If daily ADX ≥ ADX_TREND → IC capped at 2 (no “strong IC” in strong trends)

**Cross-penalty & smoothing**

* Each regime’s raw score is reduced by **0.5 × max(other two scores)**

* Final IC / PCS / CCS scores are then **smoothed** with previous bar

* Scores are always clipped to ** **

---

## Regime selection

* If one regime has the highest score → that regime is selected.

* If there is a tie or close scores:

* When ADX is high, trend regimes (PCS/CCS) are preferred in the direction of the EMA stack.

* When ADX is low, IC is preferred.

The selected regime’s score is used for:

* Background colour intensity

* Minimum score gate for alerts

* Display in the info panel

---

## DEFEND / HARVEST / REGIME alerts

The script also defines **management signals** using ATR-based buffers and Camarilla breaks:

* **DEFEND**

* Price moving too close to short strikes (PCS/CCS/IC) relative to ATR, or

* Trend breaks through Camarilla with ADX strong

→ Suggests rolling away / widening / converting to reduce risk.

* **HARVEST**

* Price has moved far enough from your short strikes (in ATR multiples) and market is still range-compatible

→ Suggests booking profits / rolling closer / reducing risk.

* **REGIME CHANGED**

* Regime flips (IC ↔ PCS/CCS) with cooldown and minimum score gate

→ Suggests switching playbook (range vs trend) for new entries.

Each of these has a plotshape label plus an `alertcondition()` for TradingView alerts.

---

## UI / Panel

The **top-right panel** (optional) shows:

* Strategy + final regime score (IC / PCS / CCS, x/5)

* ADX / RSI values

* CPR status (Narrow / Normal / Wide + %)

* EMA Stack (Up / Down / Mixed) and EMA tightness

* VWAP proximity (Near / Away)

* Final **IC / PCS / CCS** scores (for this timeframe)

* H3/L3, H4/L4, CPR Low/High and VWAP levels (rounded)

These values are meant to be **read quickly at the decision time** (e.g. near the close of the 4H bar or daily bar).

---

## Intended workflow

1. Run the script on **4H** and **1D** charts separately.

2. For each timeframe, read the panel’s **IC / PCS / CCS scores** and regime.

3. Decide:

* Final regime (IC vs PCS vs CCS)

* Combined score (e.g. `AlignScore = min(Score_4H, Score_1D)`)

4. Map that combined score to **your own lot-size buckets** and trade rules.

5. During the life of the position, use **DEFEND / HARVEST / REGIME** alerts to adjust.

The script does **not** auto-calculate lot size or P&L. It focuses on giving a structured, consistent **market regime + strength + levels + management** layer for weekly option selling.

---

## Disclaimer

This is a discretionary **decision-support tool**, not a guarantee of profit or a replacement for risk management.

No performance is implied or promised. Always size positions and manage risk according to your own capital, rules, and regulations.

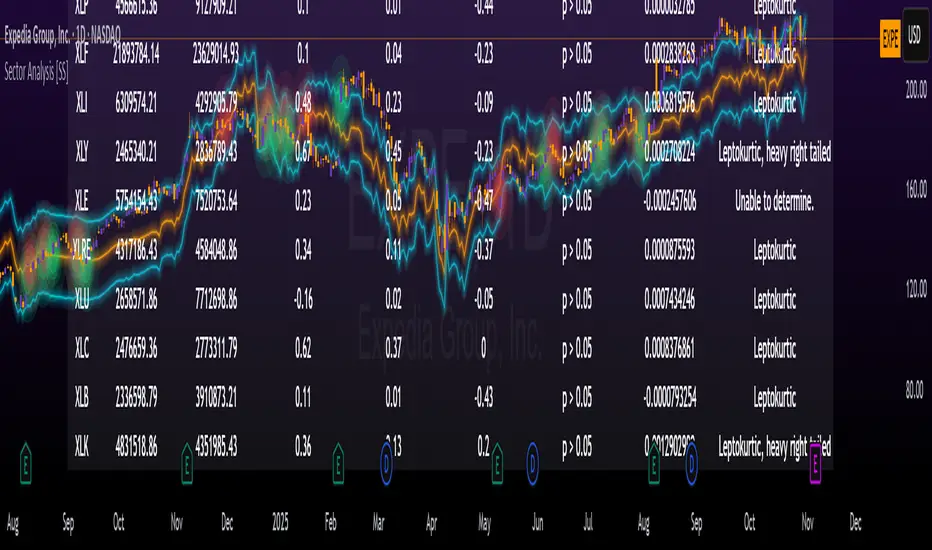

Sector Analysis [SS]Introducing the most powerful sector analysis tool/indicator available, to date, in Pine!

This is a whopper indicator, so be sure to read carefully to ensure you understand its applications and uses!

First of all, because this is a whopper, let's go over the key functional points of the indicator.

The indicator compares the 11 main sector ETFs against whichever ticker you are looking at.

The functions include the following:

Ability to pull technicals from the sectors, such as RSI, Stochastic and Z-Score;

Ability to look at the correlation of the sector ETF to the current ticker you are looking at.

Ability to calculate the R2 value between the ticker you are looking at and each sector.

The ability to run a Two Tailed T-Test against the log returns of the Ticker of interest and the Sector (to analyze statistically significant returns between sectors/tickers).

The ability to analyze the distribution of returns across all sector ETFs.

The ability to pull buying and selling volume across all sector ETFs.

The ability to create an integrated moving average using a sector ETF to predict the expected close range of a ticker of interest.

These are the highlight functions. Below, I will go more into them, what they mean and how to use them.

Pulling Technicals

This is pretty straight forward. You can pull technicals, such as RSI, Stochastic and Z-Score from all the sector ETFs and view them in a table.

See below for the example:

Pulling Correlation

In order to see which sector your ticker of interest follows more closely, we need to look first at correlation and then at R2.

The correlation will look at the immediate relationship over a specified time. A highly positive value, indicates a strong, symbiotic relationship, which the sector and the ticker follow each other. This would be represented by a correlation of 0.8 or higher.

A strong negative correlation, such as -0.8 or lower, indicates that the sector and the ticker are completely opposite. When one goes up, the other goes down and vice versa.

You can adjust your correlation assessment length directly in the settings menu:

If you want to use a sector ETF to find the expected range for a ticker of interest, it is important to locate the highest, POSITIVE, correlation value. Here are the results for MSFT at a correlation lookback of 200:

In this example, we can see the best relationship is with the ETF XLK.

Analysis of R2

R2 is an important metric. It essentially measures how much of the variance between 2 tickers are explained by a simple, linear relationship.

A high R2 means that a huge degree of variance can be explained between the 2 tickers. A low R2 means that it cannot and that the 2 tickers are likely not integrated or closely related.

In general, if you want to use the sector ETF to find the mean and trading range and identify over-valuation/over-extension and under-extension statistically, you need to see both a high correlation and a high R-Squared. These 2 metrics should be analyzed together.

Let's take a look at MSFT:

Here, despite the correlation implying that XLK was the ticker we should use to analyze, when we look at the R Squared, we see actually, we should be using XLI.

XLI has a strong positive relationship with MSFT, albeit a bit less than XLK, but the R2 is solid, > 0.9, indicating the XLI explains much of MSFT's variance.

Two Tailed T-Test

A two tailed T-test analyzes whether there is a statistically significant difference between 2 different groups, or in our case, tickers.

The T-Test is conducted on the log returns of the ticker of interest and the sector. You then can see the P value results, whether it is significant or not. Let's look at MSFT again:

Looking at this, we can see there is no statistically significant difference in returns between MSFT and any of the sectors.

We can also see the SMA of the log returns for more detailed comparison.

If we were to observe a significant finding on the T-Test metrics, this would indicate that one sector either outperforms or underperforms your ticker to a statistically significant degree! If you stumble upon this, you would check the average log returns to compare against the average returns of your ticker of interest, to see whether there is better performance or worse performance from the sector ETF vs. your ticker of interest.

Analyzing the Distribution

The indicator will also analyze the distribution of returns.

This is an interesting option as it can help you ascertain risk. Normally distributed returns imply mean reverting behavviour. Deviations from that imply trending behaviour with higher risk expectancy. If we look at the distribution statistics currently over the last 200 trading days, here are the results:

Here, we can see all show signs of trending, as none of the returns are normally distributed. The highest risk sectors are XLK and XLY.

Why are they the highest risk?