FVG Premium [no1x]█ OVERVIEW

This indicator provides a comprehensive toolkit for identifying, visualizing, and tracking Fair Value Gaps (FVGs) across three distinct timeframes (current chart, a user-defined Medium Timeframe - MTF, and a user-defined High Timeframe - HTF). It is designed to offer traders enhanced insight into FVG dynamics through detailed state monitoring (formation, partial fill, full mitigation, midline touch), extensive visual customization for FVG representation, and a rich alert system for timely notifications on FVG-related events.

█ CONCEPTS

This indicator is built upon the core concept of Fair Value Gaps (FVGs) and their significance in price action analysis, offering a multi-layered approach to their detection and interpretation across different timeframes.

Fair Value Gaps (FVGs)

A Fair Value Gap (FVG), also known as an imbalance, represents a range in price delivery where one side of the market (buying or selling) was more aggressive, leaving an inefficiency or an "imbalance" in the price action. This concept is prominently featured within Smart Money Concepts (SMC) and Inner Circle Trader (ICT) methodologies, where such gaps are often interpreted as footprints left by "smart money" due to rapid, forceful price movements. These methodologies suggest that price may later revisit these FVG zones to rebalance a prior inefficiency or to seek liquidity before continuing its path. These gaps are typically identified by a three-bar pattern:

Bullish FVG : This is a three-candle formation where the second candle shows a strong upward move. The FVG is the space created between the high of the first candle (bottom of FVG) and the low of the third candle (top of FVG). This indicates a strong upward impulsive move.

Bearish FVG : This is a three-candle formation where the second candle shows a strong downward move. The FVG is the space created between the low of the first candle (top of FVG) and the high of the third candle (bottom of FVG). This indicates a strong downward impulsive move.

FVGs are often watched by traders as potential areas where price might return to "rebalance" or find support/resistance.

Multi-Timeframe (MTF) Analysis

The indicator extends FVG detection beyond the current chart's timeframe (Low Timeframe - LTF) to two higher user-defined timeframes: Medium Timeframe (MTF) and High Timeframe (HTF). This allows traders to:

Identify FVGs that might be significant on a broader market structure.

Observe how FVGs from different timeframes align or interact.

Gain a more comprehensive perspective on potential support and resistance zones.

FVG State and Lifecycle Management

The indicator actively tracks the lifecycle of each detected FVG:

Formation : The initial identification of an FVG.

Partial Fill (Entry) : When price enters but does not completely pass through the FVG. The indicator updates the "current" top/bottom of the FVG to reflect the filled portion.

Midline (Equilibrium) Touch : When price touches the 50% level of the FVG.

Full Mitigation : When price completely trades through the FVG, effectively "filling" or "rebalancing" the gap. The indicator records the mitigation time.

This state tracking is crucial for understanding how price interacts with these zones.

FVG Classification (Large FVG)

FVGs can be optionally classified as "Large FVGs" (LV) if their size (top to bottom range) exceeds a user-defined multiple of the Average True Range (ATR) for that FVG's timeframe. This helps distinguish FVGs that are significantly larger relative to recent volatility.

Visual Customization and Information Delivery

A key concept is providing extensive control over how FVGs are displayed. This control is achieved through a centralized set of visual parameters within the indicator, allowing users to configure numerous aspects (colors, line styles, visibility of boxes, midlines, mitigation lines, labels, etc.) for each timeframe. Additionally, an on-chart information panel summarizes the nearest unmitigated bullish and bearish FVG levels for each active timeframe, providing a quick glance at key price points.

█ FEATURES

This indicator offers a rich set of features designed to provide a highly customizable and comprehensive Fair Value Gap (FVG) analysis experience. Users can tailor the FVG detection, visual representation, and alerting mechanisms across three distinct timeframes: the current chart (Low Timeframe - LTF), a user-defined Medium Timeframe (MTF), and a user-defined High Timeframe (HTF).

Multi-Timeframe FVG Detection and Display

The core strength of this indicator lies in its ability to identify and display FVGs from not only the current chart's timeframe (LTF) but also from two higher, user-selectable timeframes (MTF and HTF).

Timeframe Selection: Users can specify the exact MTF (e.g., "60", "240") and HTF (e.g., "D", "W") through dedicated inputs in the "MTF (Medium Timeframe)" and "HTF (High Timeframe)" settings groups. The visibility of FVGs from these higher timeframes can be toggled independently using the "Show MTF FVGs" and "Show HTF FVGs" checkboxes.

Consistent Detection Logic: The FVG detection logic, based on the classic three-bar imbalance pattern detailed in the 'Concepts' section, is applied consistently across all selected timeframes (LTF, MTF, HTF)

Timeframe-Specific Visuals: Each timeframe's FVGs (LTF, MTF, HTF) can be customized with unique colors for bullish/bearish states and their mitigated counterparts. This allows for easy visual differentiation of FVGs originating from different market perspectives.

Comprehensive FVG Visualization Options

The indicator provides extensive control over how FVGs are visually represented on the chart for each timeframe (LTF, MTF, HTF).

FVG Boxes:

Visibility: Main FVG boxes can be shown or hidden per timeframe using the "Show FVG Boxes" (for LTF), "Show Boxes" (for MTF/HTF) inputs.

Color Customization: Colors for bullish, bearish, active, and mitigated FVG boxes (including Large FVGs, if classified) are fully customizable for each timeframe.

Box Extension & Length: FVG boxes can either be extended to the right indefinitely ("Extend Boxes Right") or set to a fixed length in bars ("Short Box Length" or "Box Length" equivalent inputs).

Box Labels: Optional labels can display the FVG's timeframe and fill percentage on the box. These labels are configurable for all timeframes (LTF, MTF, and HTF). Please note: If FVGs are positioned very close to each other on the chart, their respective labels may overlap. This can potentially lead to visual clutter, and it is a known behavior in the current version of the indicator.

Box Borders: Visibility, width, style (solid, dashed, dotted), and color of FVG box borders are customizable per timeframe.

Midlines (Equilibrium/EQ):

Visibility: The 50% level (midline or EQ) of FVGs can be shown or hidden for each timeframe.

Style Customization: Width, style, and color of the midline are customizable per timeframe. The indicator tracks if this midline has been touched by price.

Mitigation Lines:

Visibility: Mitigation lines (representing the FVG's opening level that needs to be breached for full mitigation) can be shown or hidden for each timeframe. If shown, these lines are always extended to the right.

Style Customization: Width, style, and color of the mitigation line are customizable per timeframe.

Mitigation Line Labels: Optional price labels can be displayed on mitigation lines, with a customizable horizontal bar offset for positioning. For optimal label placement, the following horizontal bar offsets are recommended: 4 for LTF, 8 for MTF, and 12 for HTF.

Persistence After Mitigation: Users can choose to keep mitigation lines visible even after an FVG is fully mitigated, with a distinct color for such lines. Importantly, this option is only effective if the general setting 'Hide Fully Mitigated FVGs' is disabled, as otherwise, the entire FVG and its lines will be removed upon mitigation.

FVG State Management and Behavior

The indicator tracks and visually responds to changes in FVG states.

Hide Fully Mitigated FVGs: This option, typically found in the indicator's general settings, allows users to automatically remove all visual elements of an FVG from the chart once price has fully mitigated it. This helps maintain chart clarity by focusing on active FVGs.

Partial Fill Visualization: When price enters an FVG, the indicator offers a dynamic visual representation: the portion of the FVG that has been filled is shown as a "mitigated box" (typically with a distinct color), while the original FVG box shrinks to clearly highlight the remaining, unfilled portion. This two-part display provides an immediate visual cue about how much of the FVG's imbalance has been addressed and what potential remains within the gap.

Visual Filtering by ATR Proximity: To help users focus on the most relevant price action, FVGs can be dynamically hidden if they are located further from the current price than a user-defined multiple of the Average True Range (ATR). This behavior is controlled by the "Filter Band Width (ATR Multiple)" input; setting this to zero disables the filter entirely, ensuring all detected FVGs remain visible regardless of their proximity to price.

Alternative Usage Example: Mitigation Lines as Key Support/Resistance Levels

For traders preferring a minimalist chart focused on key Fair Value Gap (FVG) levels, the indicator's visualization settings can be customized to display only FVG mitigation lines. This approach leverages these lines as potential support and resistance zones, reflecting areas where price might revisit to address imbalances.

To configure this view:

Disable FVG Boxes: Turn off "Show FVG Boxes" (for LTF) or "Show Boxes" (for MTF/HTF) for the desired timeframes.

Hide Midlines: Disable the visibility of the 50% FVG Midlines (Equilibrium/EQ).

Ensure Mitigation Lines are Visible: Keep "Mitigation Lines" enabled.

Retain All Mitigation Lines:

Disable the "Hide Fully Mitigated FVGs" option in the general settings.

Enable the feature to "keep mitigation lines visible even after an FVG is fully mitigated". This ensures lines from all FVGs (active or fully mitigated) remain on the chart, which is only effective if "Hide Fully Mitigated FVGs" is disabled.

This setup offers:

A Decluttered Chart: Focuses solely on the FVG opening levels.

Precise S/R Zones: Treats mitigation lines as specific points for potential price reactions.

Historical Level Analysis: Includes lines from past, fully mitigated FVGs for a comprehensive view of significant price levels.

For enhanced usability with this focused view, consider these optional additions:

The on-chart Information Panel can be activated to display a quick summary of the nearest unmitigated FVG levels.

Mitigation Line Labels can also be activated for clear price level identification. A customizable horizontal bar offset is available for positioning these labels; for example, offsets of 4 for LTF, 8 for MTF, and 12 for HTF can be effective.

FVG Classification (Large FVG)

This feature allows for distinguishing FVGs based on their size relative to market volatility.

Enable Classification: Users can enable "Classify FVG (Large FVG)" to identify FVGs that are significantly larger than average.

ATR-Based Threshold: An FVG is classified as "Large" if its height (price range) is greater than or equal to the Average True Range (ATR) of its timeframe multiplied by a user-defined "Large FVG Threshold (ATR Multiple)". The ATR period for this calculation is also configurable.

Dedicated Colors: Large FVGs (both bullish/bearish and active/mitigated) can be assigned unique colors, making them easily distinguishable on the chart.

Panel Icon: Large FVGs are marked with a special icon in the Info Panel.

Information Panel

An on-chart panel provides a quick summary of the nearest unmitigated FVG levels.

Visibility and Position: The panel can be shown/hidden and positioned in any of the nine standard locations on the chart (e.g., Top Right, Middle Center).

Content: It displays the price levels of the nearest unmitigated bullish and bearish FVGs for LTF, MTF (if active), and HTF (if active). It also indicates if these nearest FVGs are Large FVGs (if classification is enabled) using a selectable icon.

Styling: Text size, border color, header background/text colors, default text color, and "N/A" cell background color are customizable.

Highlighting: Background and text colors for the cells displaying the overall nearest bullish and bearish FVG levels (across all active timeframes) can be customized to draw attention to the most proximate FVG.

Comprehensive Alert System

The indicator offers a granular alert system for various FVG-related events, configurable for each timeframe (LTF, MTF, HTF) independently. Users can enable alerts for:

New FVG Formation: Separate alerts for new bullish and new bearish FVG formations.

FVG Entry/Partial Fill: Separate alerts for price entering a bullish FVG or a bearish FVG.

FVG Full Mitigation: Separate alerts for full mitigation of bullish and bearish FVGs.

FVG Midline (EQ) Touch: Separate alerts for price touching the midline of a bullish or bearish FVG.

Alert messages are detailed, providing information such as the timeframe, FVG type (bull/bear, Large FVG), relevant price levels, and timestamps.

█ NOTES

This section provides additional information regarding the indicator's usage, performance considerations, and potential interactions with the TradingView platform. Understanding these points can help users optimize their experience and troubleshoot effectively.

Performance and Resource Management

Maximum FVGs to Track : The "Max FVGs to Track" input (defaulting to 25) limits the number of FVG objects processed for each category (e.g., LTF Bullish, MTF Bearish). Increasing this value significantly can impact performance due to more objects being iterated over and potentially drawn, especially when multiple timeframes are active.

Drawing Object Limits : To manage performance, this script sets its own internal limits on the number of drawing objects it displays. While it allows for up to approximately 500 lines (max_lines_count=500) and 500 labels (max_labels_count=500), the number of FVG boxes is deliberately restricted to a maximum of 150 (max_boxes_count=150). This specific limit for boxes is a key performance consideration: displaying too many boxes can significantly slow down the indicator, and a very high number is often not essential for analysis. Enabling all visual elements for many FVGs across all three timeframes can cause the indicator to reach these internal limits, especially the stricter box limit

Optimization Strategies : To help you manage performance, reduce visual clutter, and avoid exceeding drawing limits when using this indicator, I recommend the following strategies:

Maintain or Lower FVG Tracking Count: The "Max FVGs to Track" input defaults to 25. I find this value generally sufficient for effective analysis and balanced performance. You can keep this default or consider reducing it further if you experience performance issues or prefer a less dense FVG display.

Utilize Proximity Filtering: I suggest activating the "Filter Band Width (ATR Multiple)" option (found under "General Settings") to display only those FVGs closer to the current price. From my experience, a value of 5 for the ATR multiple often provides a good starting point for balanced performance, but you should feel free to adjust this based on market volatility and your specific trading needs.

Hide Fully Mitigated FVGs: I strongly recommend enabling the "Hide Fully Mitigated FVGs" option. This setting automatically removes all visual elements of an FVG from the chart once it has been fully mitigated by price. Doing so significantly reduces the number of active drawing objects, lessens computational load, and helps maintain chart clarity by focusing only on active, relevant FVGs.

Disable FVG Display for Unused Timeframes: If you are not actively monitoring certain higher timeframes (MTF or HTF) for FVG analysis, I advise disabling their display by unchecking "Show MTF FVGs" or "Show HTF FVGs" respectively. This can provide a significant performance boost.

Simplify Visual Elements: For active FVGs, consider hiding less critical visual elements if they are not essential for your specific analysis. This could include box labels, borders, or even entire FVG boxes if, for example, only the mitigation lines are of interest for a particular timeframe.

Settings Changes and Platform Limits : This indicator is comprehensive and involves numerous calculations and drawings. When multiple settings are changed rapidly in quick succession, it is possible, on occasion, for TradingView to issue a "Runtime error: modify_study_limit_exceeding" or similar. This can cause the indicator to temporarily stop updating or display errors.

Recommended Approach : When adjusting settings, it is advisable to wait a brief moment (a few seconds) after each significant change. This allows the indicator to reprocess and update on the chart before another change is made

Error Recovery : Should such a runtime error occur, making a minor, different adjustment in the settings (e.g., toggling a checkbox off and then on again) and waiting briefly will typically allow the indicator to recover and resume correct operation. This behavior is related to platform limitations when handling complex scripts with many inputs and drawing objects.

Multi-Timeframe (MTF/HTF) Data and Behavior

HTF FVG Confirmation is Essential: : For an FVG from a higher timeframe (MTF or HTF) to be identified and displayed on your current chart (LTF), the three-bar pattern forming the FVG on that higher timeframe must consist of fully closed bars. The indicator does not draw speculative FVGs based on incomplete/forming bars from higher timeframes.

Data Retrieval and LTF Processing: The indicator may use techniques like lookahead = barmerge.lookahead_on for timely data retrieval from higher timeframes. However, the actual detection of an FVG occurs after all its constituent bars on the HTF have closed.

Appearance Timing on LTF (1 LTF Candle Delay): As a natural consequence of this, an FVG that is confirmed on an HTF (i.e., its third bar closes) will typically become visible on your LTF chart one LTF bar after its confirmation on the HTF.

Example: Assume an FVG forms on a 30-minute chart at 15:30 (i.e., with the close of the 30-minute bar that covers the 15:00-15:30 period). If you are monitoring this FVG on a 15-minute chart, the indicator will detect this newly formed 30-minute FVG while processing the data for the 15-minute bar that starts at 15:30 and closes at 15:45. Therefore, the 30-minute FVG will become visible on your 15-minute chart at the earliest by 15:45 (i.e., with the close of that relevant 15-minute LTF candle). This means the HTF FVG is reflected on the LTF chart with a delay equivalent to one LTF candle.

FVG Detection and Display Logic

Fair Value Gaps (FVGs) on the current chart timeframe (LTF) are detected based on barstate.isconfirmed. This means the three-bar pattern must be complete with closed bars before an FVG is identified. This confirmation method prevents FVGs from being prematurely identified on the forming bar.

Alerts

Alert Setup : To receive alerts from this indicator, you must first ensure you have enabled the specific alert conditions you are interested in within the indicator's own settings (see 'Comprehensive Alert System' under the 'FEATURES' section). Once configured, open TradingView's 'Create Alert' dialog. In the 'Condition' tab, select this indicator's name, and crucially, choose the 'Any alert() function call' option from the dropdown list. This setup allows the indicator to trigger alerts based on the precise event conditions you have activated in its settings

Alert Frequency : Alerts are designed to trigger once per bar close (alert.freq_once_per_bar_close) for the specific event.

User Interface (UI) Tips

Settings Group Icons: In the indicator settings menu, timeframe-specific groups are marked with star icons for easier navigation: 🌟 for LTF (Current Chart Timeframe), 🌟🌟 for MTF (Medium Timeframe), and 🌟🌟🌟 for HTF (High Timeframe).

Dependent Inputs: Some input settings are dependent on others being enabled. These dependencies are visually indicated in the settings menu using symbols like "↳" (dependent setting on the next line), "⟷" (mutually exclusive inline options), or "➜" (directly dependent inline option).

Settings Layout Overview: The indicator settings are organized into logical groups for ease of use. Key global display controls – such as toggles for MTF FVGs, HTF FVGs (along with their respective timeframe selectors), and the Information Panel – are conveniently located at the very top within the '⚙️ General Settings' group. This placement allows for quick access to frequently adjusted settings. Other sections provide detailed customization options for each timeframe (LTF, MTF, HTF), specific FVG components, and alert configurations.

█ FOR Pine Script® CODERS

This section provides a high-level overview of the FVG Premium indicator's internal architecture, data flow, and the interaction between its various library components. It is intended for Pine Script™ programmers who wish to understand the indicator's design, potentially extend its functionality, or learn from its structure.

System Architecture and Modular Design

The indicator is architected moduarly, leveraging several custom libraries to separate concerns and enhance code organization and reusability. Each library has a distinct responsibility:

FvgTypes: Serves as the foundational data definition layer. It defines core User-Defined Types (UDTs) like fvgObject (for storing all attributes of an FVG) and drawSettings (for visual configurations), along with enumerations like tfType.

CommonUtils: Provides utility functions for common tasks like mapping user string inputs (e.g., "Dashed" for line style) to their corresponding Pine Script™ constants (e.g., line.style_dashed) and formatting timeframe strings for display.

FvgCalculations: Contains the core logic for FVG detection (both LTF and MTF/HTF via requestMultiTFBarData), FVG classification (Large FVGs based on ATR), and checking FVG interactions with price (mitigation, partial fill).

FvgObject: Implements an object-oriented approach by attaching methods to the fvgObject UDT. These methods manage the entire visual lifecycle of an FVG on the chart, including drawing, updating based on state changes (e.g., mitigation), and deleting drawing objects. It's responsible for applying the visual configurations defined in drawSettings.

FvgPanel: Manages the creation and dynamic updates of the on-chart information panel, which displays key FVG levels.

The main indicator script acts as the orchestrator, initializing these libraries, managing user inputs, processing data flow between libraries, and handling the main event loop (bar updates) for FVG state management and alerts.

Core Data Flow and FVG Lifecycle Management

The general data flow and FVG lifecycle can be summarized as follows:

Input Processing: User inputs from the "Settings" dialog are read by the main indicator script. Visual style inputs (colors, line styles, etc.) are consolidated into a types.drawSettings object (defined in FvgTypes). Other inputs (timeframes, filter settings, alert toggles) control the behavior of different modules. CommonUtils assists in mapping some string inputs to Pine constants.

FVG Detection:

For the current chart timeframe (LTF), FvgCalculations.detectFvg() identifies potential FVGs based on bar patterns.

For MTF/HTF, the main indicator script calls FvgCalculations.requestMultiTFBarData() to fetch necessary bar data from higher timeframes, then FvgCalculations.detectMultiTFFvg() identifies FVGs.

Newly detected FVGs are instantiated as types.fvgObject and stored in arrays within the main script. These objects also undergo classification (e.g., Large FVG) by FvgCalculations.

State Update & Interaction: On each bar, the main indicator script iterates through active FVG objects to manage their state based on price interaction:

Initially, the main script calls FvgCalculations.fvgInteractionCheck() to efficiently determine if the current bar's price might be interacting with a given FVG.

If a potential interaction is flagged, the main script then invokes methods directly on the fvgObject instance (e.g., updateMitigation(), updatePartialFill(), checkMidlineTouch(), which are part of FvgObject).

These fvgObject methods are responsible for the detailed condition checking and the actual modification of the FVG's state. For instance, the updateMitigation() and updatePartialFill() methods internally utilize specific helper functions from FvgCalculations (like checkMitigation() and checkPartialMitigation()) to confirm the precise nature of the interaction before updating the fvgObject’s state fields (such as isMitigated, currentTop, currentBottom, or isMidlineTouched).

Visual Rendering:

The FvgObject.updateDrawings() method is called for each fvgObject. This method is central to drawing management; it creates, updates, or deletes chart drawings (boxes, lines, labels) based on the FVG's current state, its prev_* (previous bar state) fields for optimization, and the visual settings passed via the drawSettings object.

Information Panel Update: The main indicator script determines the nearest FVG levels, populates a panelData object (defined in FvgPanelLib), and calls FvgPanel.updatePanel() to refresh the on-chart display.

Alert Generation: Based on the updated FVG states and user-enabled alert settings, the main indicator script constructs and triggers alerts using Pine Script's alert() function."

Key Design Considerations

UDT-Centric Design: The fvgObject UDT is pivotal, acting as a stateful container for all information related to a single FVG. Most operations revolve around creating, updating, or querying these objects.

State Management: To optimize drawing updates and manage FVG lifecycles, fvgObject instances store their previous bar's state (e.g., prevIsVisible, prevCurrentTop). The FvgObject.updateDrawings() method uses this to determine if a redraw is necessary, minimizing redundant drawing calls.

Settings Object: A drawSettings object is populated once (or when inputs change) and passed to drawing functions. This avoids repeatedly reading numerous input() values on every bar or within loops, improving performance.

Dynamic Arrays for FVG Storage: Arrays are used to store collections of fvgObject instances, allowing for dynamic management (adding new FVGs, iterating for updates).

"ha溢价率" için komut dosyalarını ara

FvgObject█ OVERVIEW

This library provides a suite of methods designed to manage the visual representation and lifecycle of Fair Value Gap (FVG) objects on a Pine Script™ chart. It extends the `fvgObject` User-Defined Type (UDT) by attaching object-oriented functionalities for drawing, updating, and deleting FVG-related graphical elements. The primary goal is to encapsulate complex drawing logic, making the main indicator script cleaner and more focused on FVG detection and state management.

█ CONCEPTS

This library is built around the idea of treating each Fair Value Gap as an "object" with its own visual lifecycle on the chart. This is achieved by defining methods that operate directly on instances of the `fvgObject` UDT.

Object-Oriented Approach for FVGs

Pine Script™ v6 introduced the ability to define methods for User-Defined Types (UDTs). This library leverages this feature by attaching specific drawing and state management functions (methods) directly to the `fvgObject` type. This means that instead of calling global functions with an FVG object as a parameter, you call methods *on* the FVG object itself (e.g., `myFvg.updateDrawings(...)`). This approach promotes better code organization and a more intuitive way to interact with FVG data.

FVG Visual Lifecycle Management

The core purpose of this library is to manage the complete visual journey of an FVG on the chart. This lifecycle includes:

Initial Drawing: Creating the first visual representation of a newly detected FVG, including its main box and optionally its midline and labels.

State Updates & Partial Fills: Modifying the FVG's appearance as it gets partially filled by price. This involves drawing a "mitigated" portion of the box and adjusting the `currentTop` or `currentBottom` of the remaining FVG.

Full Mitigation & Tested State: Handling how an FVG is displayed once fully mitigated. Depending on user settings, it might be hidden, or its box might change color/style to indicate it has been "tested." Mitigation lines can also be managed (kept or deleted).

Midline Interaction: Visually tracking if the price has touched the FVG's 50% equilibrium level (midline).

Visibility Control: Dynamically showing or hiding FVG drawings based on various criteria, such as user settings (e.g., hide mitigated FVGs, timeframe-specific visibility) or external filters (e.g., proximity to current price).

Deletion: Cleaning up all drawing objects associated with an FVG when it's no longer needed or when settings dictate its removal.

Centralized Drawing Logic

By encapsulating all drawing-related operations within the methods of this library, the main indicator script is significantly simplified. The main script can focus on detecting FVGs and managing their state (e.g., in arrays), while delegating the complex task of rendering and updating them on the chart to the methods herein.

Interaction with `fvgObject` and `drawSettings` UDTs

All methods within this library operate on an instance of the `fvgObject` UDT. This `fvgObject` holds not only the FVG's price/time data and state (like `isMitigated`, `currentTop`) but also the IDs of its associated drawing elements (e.g., `boxId`, `midLineId`).

The appearance of these drawings (colors, styles, visibility, etc.) is dictated by a `drawSettings` UDT instance, which is passed as a parameter to most drawing-related methods. This `drawSettings` object is typically populated from user inputs in the main script, allowing for extensive customization.

Stateful Drawing Object Management

The library's methods manage Pine Script™ drawing objects (boxes, lines, labels) by storing their IDs within the `fvgObject` itself (e.g., `fvgObject.boxId`, `fvgObject.mitigatedBoxId`, etc.). Methods like `draw()` create these objects and store their IDs, while methods like `updateDrawings()` modify them, and `deleteDrawings()` removes them using these stored IDs.

Drawing Optimization

The `updateDrawings()` method, which is the most comprehensive drawing management function, incorporates optimization logic. It uses `prev_*` fields within the `fvgObject` (e.g., `prevIsMitigated`, `prevCurrentTop`) to store the FVG's state from the previous bar. By comparing the current state with the previous state, and also considering changes in visibility or relevant drawing settings, it can avoid redundant and performance-intensive drawing operations if nothing visually significant has changed for that FVG.

█ METHOD USAGE AND WORKFLOW

The methods in this library are designed to be called in a logical sequence as an FVG progresses through its lifecycle. A crucial prerequisite for all visual methods in this library is a properly populated `drawSettings` UDT instance, which dictates every aspect of an FVG's appearance, from colors and styles to visibility and labels. This `settings` object must be carefully prepared in the main indicator script, typically based on user inputs, before being passed to these methods.

Here’s a typical workflow within a main indicator script:

1. FVG Instance Creation (External to this library)

An `fvgObject` instance is typically created by functions in another library (e.g., `FvgCalculations`) when a new FVG pattern is identified. This object will have its core properties (top, bottom, startTime, isBullish, tfType) initialized.

2. Initial Drawing (`draw` method)

Once a new `fvgObject` is created and its initial visibility is determined:

Call the `myFvg.draw(settings)` method on the new FVG object.

`settings` is an instance of the `drawSettings` UDT, containing all relevant visual configurations.

This method draws the primary FVG box, its midline (if enabled in `settings`), and any initial labels. It also initializes the `currentTop` and `currentBottom` fields of the `fvgObject` if they are `na`, and stores the IDs of the created drawing objects within the `fvgObject`.

3. Per-Bar State Updates & Interaction Checks

On each subsequent bar, for every active `fvgObject`:

Interaction Check (External Logic): It's common to first use logic (e.g., from `FvgCalculations`' `fvgInteractionCheck` function) to determine if the current bar's price interacts with the FVG.

State Field Updates (External Logic): Before calling the `FvgObjectLib` methods below, ensure that your `fvgObject`'s state fields (such as `isMitigated`, `currentTop`, `currentBottom`, `isMidlineTouched`) are updated using the current bar's price data and relevant functions from other libraries (e.g., `FvgCalculations`' `checkMitigation`, `checkPartialMitigation`, etc.). This library's methods render the FVG based on these pre-updated state fields.

If interaction occurs and the FVG is not yet fully mitigated:

Full Mitigation Update (`updateMitigation` method): Call `myFvg.updateMitigation(high, low)`. This method updates `myFvg.isMitigated` and `myFvg.mitigationTime` if full mitigation occurs, based on the interaction determined by external logic.

Partial Fill Update (`updatePartialFill` method): If not fully mitigated, call `myFvg.updatePartialFill(high, low, settings)`. This method updates `myFvg.currentTop` or `myFvg.currentBottom` and adjusts drawings to show the filled portion, again based on prior interaction checks and fill level calculations.

Midline Touch Check (`checkMidlineTouch` method): Call `myFvg.checkMidlineTouch(high, low)`. This method updates `myFvg.isMidlineTouched` if the price touches the FVG's 50% level.

4. Comprehensive Visual Update (`updateDrawings` method)

After the FVG's state fields have been potentially updated by external logic and the methods in step 3:

Call `myFvg.updateDrawings(isVisibleNow, settings)` on each FVG object.

`isVisibleNow` is a boolean indicating if the FVG should currently be visible.

`settings` is the `drawSettings` UDT instance.

This method synchronizes the FVG's visual appearance with its current state and settings, managing all drawing elements (boxes, lines, labels), their styles, and visibility. It efficiently skips redundant drawing operations if the FVG's state or visibility has not changed, thanks to its internal optimization using `prev_*` fields, which are also updated by this method.

5. Deleting Drawings (`deleteDrawings` method)

When an FVG object is no longer tracked:

Call `myFvg.deleteDrawings(deleteTestedToo)`.

This method removes all drawing objects associated with that `fvgObject`.

This workflow ensures that FVG visuals are accurately maintained throughout their existence on the chart.

█ NOTES

Dependencies: This library relies on `FvgTypes` for `fvgObject` and `drawSettings` definitions, and its methods (`updateMitigation`, `updatePartialFill`) internally call functions from `FvgCalculations`.

Drawing Object Management: Be mindful of TradingView's limits on drawing objects per script. The main script should manage the number of active FVG objects.

Performance and `updateDrawings()`: The `updateDrawings()` method is comprehensive. Its internal optimization (checking `hasStateChanged` based on `prev_*` fields) is crucial for performance. Call it judiciously.

Role of `settings.currentTime`: The `currentTime` field in `drawSettings` is key for positioning time-dependent elements like labels and the right edge of non-extended drawings.

Mutability of `fvgObject` Instances: Methods in this library directly modify the `fvgObject` instance they are called upon (e.g., its state fields and drawing IDs).

Drawing ID Checks: Methods generally check if drawing IDs are `na` before acting on them, preventing runtime errors.

█ EXPORTED FUNCTIONS

method draw(this, settings)

Draws the initial visual representation of the FVG object on the chart. This includes the main FVG box, its midline (if enabled), and a label

(if enabled for the specific timeframe). This method is typically invoked

immediately after an FVG is first detected and its initial properties are set. It uses drawing settings to customize the appearance based on the FVG's timeframe type.

Namespace types: types.fvgObject

Parameters:

this (fvgObject type from no1x/FvgTypes/1) : The FVG object instance to be drawn. Core properties (top, bottom,

startTime, isBullish, tfType) should be pre-initialized. This method will

initialize boxId, midLineId, boxLabelId (if applicable), and

currentTop/currentBottom (if currently na) on this object.

settings (drawSettings type from no1x/FvgTypes/1) : A drawSettings object providing all visual parameters. Reads display settings (colors, styles, visibility for boxes, midlines, labels,

box extension) relevant to this.tfType. settings.currentTime is used for

positioning labels and the right boundary of non-extended boxes.

method updateMitigation(this, highVal, lowVal)

Checks if the FVG has been fully mitigated by the current bar's price action.

Namespace types: types.fvgObject

Parameters:

this (fvgObject type from no1x/FvgTypes/1) : The FVG object instance. Reads this.isMitigated, this.isVisible,

this.isBullish, this.top, this.bottom. Updates this.isMitigated and

this.mitigationTime if full mitigation occurs.

highVal (float) : The high price of the current bar, used for mitigation check.

lowVal (float) : The low price of the current bar, used for mitigation check.

method updatePartialFill(this, highVal, lowVal, settings)

Checks for and processes partial fills of the FVG.

Namespace types: types.fvgObject

Parameters:

this (fvgObject type from no1x/FvgTypes/1) : The FVG object instance. Reads this.isMitigated, this.isVisible,

this.isBullish, this.currentTop, this.currentBottom, original this.top/this.bottom,

this.startTime, this.tfType, this.isLV. Updates this.currentTop or

this.currentBottom, creates/updates this.mitigatedBoxId, and may update this.boxId's

top/bottom to reflect the filled portion.

highVal (float) : The high price of the current bar, used for partial fill check.

lowVal (float) : The low price of the current bar, used for partial fill check.

settings (drawSettings type from no1x/FvgTypes/1) : The drawing settings. Reads timeframe-specific colors for mitigated

boxes (e.g., settings.mitigatedBullBoxColor, settings.mitigatedLvBullColor),

box extension settings (settings.shouldExtendBoxes, settings.shouldExtendMtfBoxes, etc.),

and settings.currentTime to style and position the mitigatedBoxId and potentially adjust the main boxId.

method checkMidlineTouch(this, highVal, lowVal)

Checks if the FVG's midline (50% level or Equilibrium) has been touched.

Namespace types: types.fvgObject

Parameters:

this (fvgObject type from no1x/FvgTypes/1) : The FVG object instance. Reads this.midLineId, this.isMidlineTouched,

this.top, this.bottom. Updates this.isMidlineTouched if a touch occurs.

highVal (float) : The high price of the current bar, used for midline touch check.

lowVal (float) : The low price of the current bar, used for midline touch check.

method deleteDrawings(this, deleteTestedToo)

Deletes all visual drawing objects associated with this FVG object.

Namespace types: types.fvgObject

Parameters:

this (fvgObject type from no1x/FvgTypes/1) : The FVG object instance. Deletes drawings referenced by boxId,

mitigatedBoxId, midLineId, mitLineId, boxLabelId, mitLineLabelId,

and potentially testedBoxId, keptMitLineId. Sets these ID fields to na.

deleteTestedToo (simple bool) : If true, also deletes drawings for "tested" FVGs

(i.e., testedBoxId and keptMitLineId).

method updateDrawings(this, isVisibleNow, settings)

Manages the comprehensive update of all visual elements of an FVG object

based on its current state (e.g., active, mitigated, partially filled) and visibility. It handles the drawing, updating, or deletion of FVG boxes (main and mitigated part),

midlines, mitigation lines, and their associated labels. Visibility is determined by the isVisibleNow parameter and relevant settings

(like settings.shouldHideMitigated or timeframe-specific show flags). This method is central to the FVG's visual lifecycle and includes optimization

to avoid redundant drawing operations if the FVG's relevant state or appearance

settings have not changed since the last bar. It also updates the FVG object's internal prev_* state fields for future optimization checks.

Namespace types: types.fvgObject

Parameters:

this (fvgObject type from no1x/FvgTypes/1) : The FVG object instance to update. Reads most state fields (e.g.,

isMitigated, currentTop, tfType, etc.) and updates all drawing ID fields

(boxId, midLineId, etc.), this.isVisible, and all this.prev_* state fields.

isVisibleNow (bool) : A flag indicating whether the FVG should be currently visible. Typically determined by external logic (e.g., visual range filter). Affects

whether active FVG drawings are created/updated or deleted by this method.

settings (drawSettings type from no1x/FvgTypes/1) : A fully populated drawSettings object. This method extensively

reads its fields (colors, styles, visibility toggles, timeframe strings, etc.)

to render FVG components according to this.tfType and current state. settings.currentTime is critical for positioning elements like labels and extending drawings.

Sector Relative StrengthDescription

This script compares sector performance relative to the S&P 500. Sector price levels or charts alone can mislead, because they tend to move with the broader market. An increase in a sector’s price does not necessarily indicate strength, as it may simply be following the index.

For more a more reliable picture, the script calculates a ratio between each sector ETF and SPY. If the ratio has increased, the sector has outperformed the index. In case it has declined, the sector has underperformed. If the value is near zero, the sector has moved in line with the index. The sectors are presented in a table and sorted on relative performance.

Calculation Method

The performance is expressed as a percentage change in the ratio over a user-defined lookback period. The default lookback is set to 21 bars, which corresponds to one month on a daily chart. This value can be adopted in the settings to match preferred time period.

Z-Score

In addition to the percentage change, the script calculates a Z-score of the ratio, which measures how far the current value deviates from its recent mean. A high positive Z-score indicates that the ratio is significantly above its average, while a negative value indicates it is below. This normalization allows for comparison between sectors with different price levels or volatility profiles.

Table Columns

- Relative %: The sector's performance relative to SPY over the selected lookback period

- Z-Score: Standardized measure of current performance ratio is relative to its average

- Trend Arrow: Indicates the direction of relative performance up down or flat

Example Interpretation

For example, if XLK shows a 3.7% change, it has outperformed SPY over the selected period. Another sector might show a -2.1% change, which indicates underperformance. While both values shows relative strength or weakness, the Z-score is optional and can provide additional context based on how unusual that performance is compared to the sector's own recent behavior.

Use Case

This approach helps evaluate overall market conditions and supports a top-down method. By starting with sector performance, it becomes easier to identify where the market is showing leadership or weakness. This allows the stock selection process to be more deliberate and can help refine or customize screeners based on certain sectors.

UTSStrategyHelperLibrary "UTSStrategyHelper"

TODO: add library description here

stopLossPrice(sig, atr, factor, isLong)

Calculates the stop loss price using a distance determined by ATR multiplied by a factor. Example for Long trade SL: PRICE - (ATR * factor).

Parameters:

sig (float)

atr (float) : (float): The value of the atr.

factor (float)

isLong (bool) : (bool): The current trade direction.

Returns: (bool): A boolean value.

takeProfitPrice(sig, atr, factor, isLong)

Calculates the take profit price using a distance determined by ATR multiplied by a factor. Example for Long trade TP: PRICE + (ATR * factor). When take profit price is reached usually 50 % of the position is closed and the other 50 % get a trailing stop assigned.

Parameters:

sig (float)

atr (float) : (float): The value of the atr.

factor (float)

isLong (bool) : (bool): The current trade direction.

Returns: (bool): A boolean value.

trailingStopPrice(initialStopPrice, atr, factor, priceSource, isLong)

Calculates a trailing stop price using a distance determined by ATR multiplied by a factor. It takes an initial price and follows the price closely if it changes in a favourable way.

Parameters:

initialStopPrice (float) : (float): The initial stop price which, for consistency also should be ATR * factor behind price: e.g. Long trade: PRICE - (ATR * factor)

atr (float) : (float): The value of the atr. Ideally the ATR value at trade open is taken and used for subsequent calculations.

factor (float)

priceSource (float) : (float): The current price.

isLong (bool) : (bool): The current trade direction.

Returns: (bool): A boolean value.

hasGreaterPositionSize(positionSize)

Determines if the strategy's position size has grown since the last bar.

Parameters:

positionSize (float) : (float): The size of the position.

Returns: (bool): A boolean value.

hasSmallerPositionSize(positionSize)

Determines if the strategy's position size has decreased since the last bar.

Parameters:

positionSize (float) : (float): The size of the position.

Returns: (bool): A boolean value.

hasUnchangedPositionSize(positionSize)

Determines if the strategy's position size has changed since the last bar.

Parameters:

positionSize (float) : (float): The size of the position.

Returns: (bool): A boolean value.

exporthasLongPosition(positionSize)

Determines if the strategy has an open long position.

Parameters:

positionSize (float) : (float): The size of the position.

Returns: (bool): A boolean value.

hasShortPosition(positionSize)

Determines if the strategy has an open short position.

Parameters:

positionSize (float) : (float): The size of the position.

Returns: (bool): A boolean value.

hasAnyPosition(positionSize)

Determines if the strategy has any open position, regardless of short or long.

Parameters:

positionSize (float) : (float): The size of the position.

Returns: (bool): A boolean value.

hasSignal(value)

Determines if the given argument contains a valid value (means not 'na').

Parameters:

value (float) : (float): The actual value.

Returns: (bool): A boolean value.

Adaptive ATR Limits█ OVERVIEW

This indicator plots adaptive ATR limits for intraday trading. A key feature of this indicator, which makes it different from other ATR limit indicators, is that the top and bottom ATR limit lines are always exactly one ATR apart from each other (in "auto" mode; there is also a "basic" mode, which plots the limits in the more traditional way—i.e., one ATR above the low and one ATR below the high at all times—and this can be used for comparison).

█ FEATURES

Provides an algorithm to plot the most reasonable intraday ATR top/bottom limits based on currently available information

Dynamically adapts limits as the price evolves during the day

Works correctly and consistently on both RTH and ETH charts

Has a user-selected ADR mode to base the limits on ADR instead of ATR

Option to include the current pre-market and previous day's post-market range in the calculation

Configurable ATR/ADR averaging length

Provides a visual smoothing option

Provides an information box showing the current numerical ATR/ADR values

Reasonable defaults that work well if the user changes nothing

Well-documented, high-quality, open-source code for those interested

█ HOW TO USE

At a minimum, there is nothing that needs to be set. The defaults work well. The ATR top line (red, configurable) gives you the most reasonable move given the currently available information. The line will move away from the price as the price approaches it; that is normal—it is reacting to new information. This happens until the ATR bottom limit hits the lower of the daily low and the previous day's close (in ATR mode). The ATR bottom line (green, configurable) works the same way, with reversed logic.

There is an option to use ADR instead of ATR. The ATR includes the previous day's RTH close in the range, whereas ADR does not. Another option allows the user to add the current day's pre-market range or the previous day's post-market into the current day's range, which has an effect if either of those went outside of today's RTH range, plus yesterday's RTH close (in the default ATR mode). Pre-market and post-market range is not typically included in the daily true range, so only change it if you really know you want it.

█ CONCEPTS

Most traditional ATR limit indicators plot the top ATR limit one ATR above the current daily low, and the bottom ATR limit one ATR below the current daily high. This indicator can also do that (in "basic" mode), but its value lies in its default "auto" mode, which uses an algorithm to dynamically adapt the ATR limits throughout the day, keeping them one ATR apart at all times. It tries to plot the most sensible ATR limits based on the current daily ATR, in order to provide a reasonable visual intraday target, given the available information at that point in time.

"Auto" mode is actually a weighted average of two methods: midpoint and relative (both of which can also be explicitly selected). The midpoint method places the midpoint of the ATR limit equal to the midpoint of the currently established daily range. The relative method measures the currently established daily range and calculates the position of the current price within it (as a ratio between 0 and 1). It then uses that value as a weight in a weighted average of extreme locations for the ATR limits, which are: the ATR top anchored to one ATR above the daily low, and the ATR bottom anchored to one ATR below the daily high.

The relative method is more advanced and better for most of the day; however, it can cause wild swings in the early market or pre-market before a reasonable range (as a percentage of ATR) has been established. "Auto" mode therefore takes another weighted average between the two methods, with the weight determined by the percentage of the ATR currently established within the day, more strongly weighting the calmer midpoint method before a good range is established. Once the full ATR has been achieved, the algorithm in "auto" mode will have fully switched to the relative method and will remain with that method for the rest of the day.

To explain the effect further, as an example, imagine that the price is approaching the full ATR range on the high side. At this point, the indicator will have almost fully transitioned to the second (relative) method. The lower ATR limit will now be anchored to the daily low as the price hits the upper ATR limit. If the price goes beyond the upper ATR, the lower ATR limit will stay anchored to the daily low, and the upper limit will stay anchored to one ATR above the lower limit. This allows you to see how far the price is going beyond the upper ATR limit. If the price then returns and backs off the upper ATR limit, the lower ATR limit will un-anchor from the daily low (it will actually rise, since the daily ATR range has been exceeded, so the lower ATR limit needs to come up because the actual daily range can’t fit into the ATR range anymore). The overall effect is to give you the best visual indication of where the price is in relation to a possible upper ATR-based target. Reverse this example for when the price low approaches the ATR range on the low side.

Care was taken so that the code uses no hard-coded time zones, exchanges, or session times. For this reason, it can in principle work globally. However, it very much depends on the information provided by the exchange, which is reflected in built-in Pine Script variables (see Limitations below).

█ LIMITATIONS

The indicator was developed for US/European equities and is tested on them only. It is also known to work on US futures; in this case, the whole 23-hour session is used, and the "Sessions to include in range" setting has no effect. It may or may not work as intended on security types and equities/futures for other countries.

[Stop!Loss] ADR Signal ADR Signal - a technical indicator located in a separate window, which displays by default the 80%-level , as well as the 100%-level of the average daily range (ADR) for the last 10 days and compares it with the current intraday range. The indicator helps not only with the use of a mathematical-statistical method to identify a potential reversal at the moment during intraday trading, but can also serves as an effective assistant in risk management.

👉 Basic mechanics of the indicator

Firstly, this indicator tracks the performance of the standard ATR indicator on the daily chart, in other words, ADR (Average Daily Range).

Important ❗️The ATR (Average True Range) indicator was created by J. Welles Wilder Jr. He first introduced ATR in his book "New Concepts in Technical Trading Systems", published in 1978. Wilder developed this indicator to measure market volatility to help traders estimate the range of price movements. This indicator is built into TradingView, more details can be found by link: www.tradingview.com

Like ATR , ADR calculates the average true range for a specified period. In this case, the distance in points from the maximum of each day to its minimum is calculated, after which the arithmetic mean is calculated - this is ADR .

👉 Visualization

ADR Signal is located in a separate window on the chart and has 3 levels:

1) "ADR level" (green line) - the same parameter, the calculations of which are briefly described above. There is 100%-level of ATR on the daily chart (ADR).

2) "Current level" (red line) - this is the current price passage within the day, calculated in points. At the start of a new day, this parameter is reset. Therefore, in the indicator window, this line has sharp drops at the start of a new trading day: "A new trading day - the instrument's power reserve is renewed again".

3) "Signal level" (blue line) - this is an individually customized value that demonstrates a certain part of the ADR parameter.

👉 Inputs

1) - is responsible for the ATR indicator period, the value of which will always be calculated on the daily chart. The default value is "10", that is, ATR is calculated for the last 10 days (not including the current one).

2) - signal level (in %). The default value is "0.8", that is, 80%-level of the ADR parameter (set earlier) is calculated.

👉 Style

1) - by default, this level is colored "blue".

2) - by default, this level is colored "red".

3) - by default, this level is colored "green".

👉 How to use this indicator

Important❗️ The two methods of the use of the ADR Signal indicator described below will be most effective when trading intraday (which is highlighted quite well below), so it is more logical to use the indicator information on time periods H1 and below.

1) Identifying potential reversals during intraday trading:

The ADR Signal indicator can be used as a potential individual reversal strategy.

Important ❗️It should be noted that using it in it without additional confirming analysis tools will be a rather aggressive trading approach. Therefore, it is best to support the entry point in particular with other methods.

In this case, the crossing of the red line (the number of points passed within the current day, that is, from the minimum of the current day to its maximum) and the blue line (color of the Signal level based on the default settings), indicates that the trading instrument has passed 80% (based on the default settings for the "Signal level") of its average distance from the maximum to the minimum over the past 10 days (based on the default settings for the "ADR Length"). Such a situation in the context of the mathematical-statistical approach indicates a probable reversal, since the "power reserve" of this instrument is mostly exhausted, so one can expect with a higher probability, at least, a price stop and possibly a reversal. In case of crossing of the red line and the green one (ADR level), it says again that based on the mathematical-statistical approach, this trading instrument has completely exhausted its intraday "power reserve". In this situation, a stop or reversal of the price will be even more likely.

Of course, using the "Signal level" parameter, one can filter out even more reliable situations for potential price reversals within a day, namely, by specifying, for example, 1.5 in the field of this parameter. Under such conditions, in the case of crossing the red and blue lines (based on the default style settings), to say that the trading instrument has passed 150% of its average distance over the last 10 days (based on the default style settings "ADR length"). In this case, the probability of a stop or reversal of the price increases even more.

2) Use in risk management:

In terms of risk management, this indicator is more applicable to open trades. For example, if one had an open Buy-position (especially if it is an intraday trade) and the price has raised significantly during the day, then the crossing of the red line with the blue line , and especially the red line with the green line , may indicate that the price will most likely stop growing, since the "power reserve" is almost or completely exhausted for this instrument within the current day. In this case, one can, at a minimum, move the trade to breakeven or even partially fix the profit.

We will continue to discuss the methods of using this indicator and strategies based on it here. And we are always waiting for your reactions and feedback on this topic 💬.

Thank you for your support 🚀

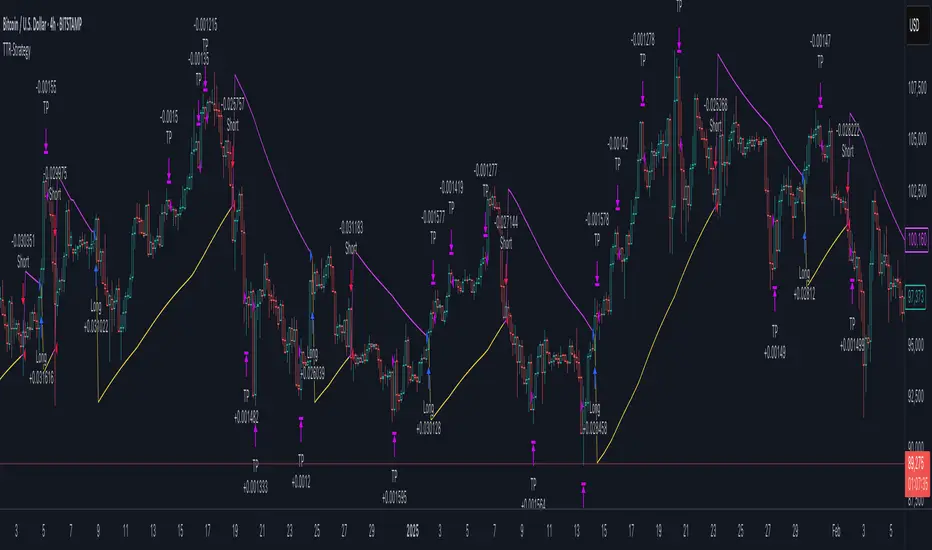

Trend Trader-Remastered StrategyOfficial Strategy for Trend Trader - Remastered

Indicator: Trend Trader-Remastered (TTR)

Overview:

The Trend Trader-Remastered is a refined and highly sophisticated implementation of the Parabolic SAR designed to create strategic buy and sell entry signals, alongside precision take profit and re-entry signals based on marked Bill Williams (BW) fractals. Built with a deep emphasis on clarity and accuracy, this indicator ensures that only relevant and meaningful signals are generated, eliminating any unnecessary entries or exits.

Please check the indicator details and updates via the link above.

Important Disclosure:

My primary objective is to provide realistic strategies and a code base for the TradingView Community. Therefore, the default settings of the strategy version of the indicator have been set to reflect realistic world trading scenarios and best practices.

Key Features:

Strategy execution date&time range.

Take Profit Reduction Rate: The percentage of progressive reduction on active position size for take profit signals.

Example:

TP Reduce: 10%

Entry Position Size: 100

TP1: 100 - 10 = 90

TP2: 90 - 9 = 81

Re-Entry When Rate: The percentage of position size on initial entry of the signal to determine re-entry.

Example:

RE When: 50%

Entry Position Size: 100

Re-Entry Condition: Active Position Size < 50

Re-Entry Fill Rate: The percentage of position size on initial entry of the signal to be completed.

Example:

RE Fill: 75%

Entry Position Size: 100

Active Position Size: 50

Re-Entry Order Size: 25

Final Active Position Size:75

Important: Even RE When condition is met, the active position size required to drop below RE Fill rate to trigger re-entry order.

Key Points:

'Process Orders on Close' is enabled as Take Profit and Re-Entry signals must be executed on candle close.

'Calculate on Every Tick' is enabled as entry signals are required to be executed within candle time.

'Initial Capital' has been set to 10,000 USD.

'Default Quantity Type' has been set to 'Percent of Equity'.

'Default Quantity' has been set to 10% as the best practice of investing 10% of the assets.

'Currency' has been set to USD.

'Commission Type' has been set to 'Commission Percent'

'Commission Value' has been set to 0.05% to reflect the most realistic results with a common taker fee value.

Fractal Breakout Trend Following StrategyOverview

The Fractal Breakout Trend Following Strategy is a trend-following system which utilizes the Willams Fractals and Alligator to execute the long trades on the fractal's breakouts which have a high probability to be the new uptrend phase beginning. This system also uses the normalized Average True Range indicator to filter trades after a large moves, because it's more likely to see the trend continuation after a consolidation period. Strategy can execute only long trades.

Unique Features

Trend and volatility filtering system: Strategy uses Williams Alligator to filter the counter-trend fractals breakouts and normalized Average True Range to avoid the trades after large moves, when volatility is high

Configurable Trading Periods: Users can tailor the strategy to specific market windows, adapting to different market conditions.

Flexible Risk Management: Users can choose the stop-loss percent (by default = 3%) for trades, but strategy also has the dynamic stop-loss level using down fractals.

Methodology

The strategy places stop order at the last valid fractal breakout level. Validity of this fractal is defined by the Williams Alligator indicator. If at the moment of time when price breaking the last fractal price is higher than Alligator's teeth line (8 period SMA shifted 5 bars in the future) this is a valid breakout. Moreover strategy has the additional volatility filtering system using normalized ATR. It calculates the average normalized ATR for last user-defined number of bars and if this value lower than the user-defined threshold value the long trade is executed.

When trade is opened, script places the stop loss at the price higher of two levels: user defined stop-loss from the position entry price or down fractal validation level. The down fractal is valid with the rule, opposite as the up fractal validation. Price shall break to the downside the last down fractal below the Willians Alligator's teeth line.

Strategy has no fixed take profit. Exit level changes with the down fractal validation level. If price is in strong uptrend trade is going to be active until last down fractal is not valid. Strategy closes trade when price hits the down fractal validation level.

Risk Management

The strategy employs a combined approach to risk management:

It allows positions to ride the trend as long as the price continues to move favorably, aiming to capture significant price movements. It features a user-defined stop-loss parameter to mitigate risks based on individual risk tolerance. By default, this stop-loss is set to a 3% drop from the entry point, but it can be adjusted according to the trader's preferences.

Justification of Methodology

This strategy leverages Williams Fractals to open long trade when price has broken the key resistance level to the upside. This resistance level is the last up fractal and is shall be broken above the Williams Alligator's teeth line to be qualified as the valid breakout according to this strategy. The Alligator filtering increases the probability to avoid the false breakouts against the current trend.

Moreover strategy has an additional filter using Average True Range(ATR) indicator. If average value of ATR for the last user-defined number of bars is lower than user-defined threshold strategy can open the long trade according to open trade condition above. The logic here is following: we want to open trades after period of price consolidation inside the range because before and after a big move price is more likely to be in sideways, but we need a trend move to have a profit.

Another one important feature is how the exit condition is defined. On the one hand, strategy has the user-defined stop-loss (3% below the entry price by default). It's made to give users the opportunity to restrict their losses according to their risk-tolerance. On the other hand, strategy utilizes the dynamic exit level which is defined by down fractal activation. If we assume the breaking up fractal is the beginning of the uptrend, breaking down fractal can be the start of downtrend phase. We don't want to be in long trade if there is a high probability of reversal to the downside. This approach helps to not keep open trade if trend is not developing and hold it if price continues going up.

Backtest Results

Operating window: Date range of backtests is 2023.01.01 - 2024.05.01. It is chosen to let the strategy to close all opened positions.

Commission and Slippage: Includes a standard Binance commission of 0.1% and accounts for possible slippage over 5 ticks.

Initial capital: 10000 USDT

Percent of capital used in every trade: 30%

Maximum Single Position Loss: -3.19%

Maximum Single Profit: +24.97%

Net Profit: +3036.90 USDT (+30.37%)

Total Trades: 83 (28.92% win rate)

Profit Factor: 1.953

Maximum Accumulated Loss: 963.98 USDT (-8.29%)

Average Profit per Trade: 36.59 USDT (+1.12%)

Average Trade Duration: 72 hours

These results are obtained with realistic parameters representing trading conditions observed at major exchanges such as Binance and with realistic trading portfolio usage parameters.

How to Use

Add the script to favorites for easy access.

Apply to the desired timeframe and chart (optimal performance observed on 4h and higher time frames and the BTC/USDT).

Configure settings using the dropdown choice list in the built-in menu.

Set up alerts to automate strategy positions through web hook with the text: {{strategy.order.alert_message}}

Disclaimer:

Educational and informational tool reflecting Skyrex commitment to informed trading. Past performance does not guarantee future results. Test strategies in a simulated environment before live implementation

time_libraryLibrary "time_library"

This library provides utilities for working with time intervals in milliseconds, seconds, minutes, hours, days, and weeks. It includes functions to handle conditions based on time rather than bars.

ms(TIME)

ms - Converts a time period in string format to milliseconds.

Parameters:

TIME (string) : (series ) - The time period ("ms", "s", "m", "h", "d", "w").

Returns: (int) - The corresponding time period in milliseconds.

true_in(timestamp, period, multiplier)

true_in - Checks if the current time has reached a specific time after the given timestamp.

Parameters:

timestamp (int) : (series ) - The starting timestamp.

period (string) : (series |series ) - The period in string format ("ms", "s", "m", "h", "d", "w"), or as an integer in milliseconds.

multiplier (float) : (series ) - Multiplier to extend the period.

Returns: (bool) - True if current time is equal or past the end date calculated from timestamp and period.

true_in(timestamp, period, multiplier)

true_in - Checks if the current time has reached a specific time after the given timestamp.

Parameters:

timestamp (int) : (series ) - The starting timestamp.

period (int) : (series |series ) - The period in string format ("ms", "s", "m", "h", "d", "w"), or as an integer in milliseconds.

multiplier (float) : (series ) - Multiplier to extend the period.

Returns: (bool) - True if current time is equal or past the end date calculated from timestamp and period.

true_after(trigger, period, multiplier)

true_after - Returns true after a specified period multiplied by a multiplier has passed since a trigger was last true.

Parameters:

trigger (bool) : (series ) - The condition that triggers the timer.

period (string) : (series |series ) - The period in string format ("ms", "s", "m", "h", "d", "w"), or as an integer in milliseconds.

multiplier (float) : (series ) - Multiplier to extend the period.

Returns: (bool) - True if the specified time has passed since the last trigger.

true_after(trigger, ms, multiplier)

true_after - Returns true after a specified period multiplied by a multiplier has passed since a trigger was last true.

Parameters:

trigger (bool) : (series ) - The condition that triggers the timer.

ms (int)

multiplier (float) : (series ) - Multiplier to extend the period.

Returns: (bool) - True if the specified time has passed since the last trigger.

MS

MS - Holds common time intervals in milliseconds.

Fields:

ms (series int) : (int) - Milliseconds.

s (series int) : (int) - Seconds converted to milliseconds.

m (series int) : (int) - Minutes converted to milliseconds.

h (series int) : (int) - Hours converted to milliseconds.

d (series int) : (int) - Days converted to milliseconds.

w (series int) : (int) - Weeks converted to milliseconds.

RiskMetrics█ OVERVIEW

This library is a tool for Pine programmers that provides functions for calculating risk-adjusted performance metrics on periodic price returns. The calculations used by this library's functions closely mirror those the Broker Emulator uses to calculate strategy performance metrics (e.g., Sharpe and Sortino ratios) without depending on strategy-specific functionality.

█ CONCEPTS

Returns, risk, and volatility

The return on an investment is the relative gain or loss over a period, often expressed as a percentage. Investment returns can originate from several sources, including capital gains, dividends, and interest income. Many investors seek the highest returns possible in the quest for profit. However, prudent investing and trading entails evaluating such returns against the associated risks (i.e., the uncertainty of returns and the potential for financial losses) for a clearer perspective on overall performance and sustainability.

One way investors and analysts assess the risk of an investment is by analyzing its volatility , i.e., the statistical dispersion of historical returns. Investors often use volatility in risk estimation because it provides a quantifiable way to gauge the expected extent of fluctuation in returns. Elevated volatility implies heightened uncertainty in the market, which suggests higher expected risk. Conversely, low volatility implies relatively stable returns with relatively minimal fluctuations, thus suggesting lower expected risk. Several risk-adjusted performance metrics utilize volatility in their calculations for this reason.

Risk-free rate

The risk-free rate represents the rate of return on a hypothetical investment carrying no risk of financial loss. This theoretical rate provides a benchmark for comparing the returns on a risky investment and evaluating whether its excess returns justify the risks. If an investment's returns are at or below the theoretical risk-free rate or the risk premium is below a desired amount, it may suggest that the returns do not compensate for the extra risk, which might be a call to reassess the investment.

Since the risk-free rate is a theoretical concept, investors often utilize proxies for the rate in practice, such as Treasury bills and other government bonds. Conventionally, analysts consider such instruments "risk-free" for a domestic holder, as they are a form of government obligation with a low perceived likelihood of default.

The average yield on short-term Treasury bills, influenced by economic conditions, monetary policies, and inflation expectations, has historically hovered around 2-3% over the long term. This range also aligns with central banks' inflation targets. As such, one may interpret a value within this range as a minimum proxy for the risk-free rate, as it may correspond to the minimum rate required to maintain purchasing power over time.

The built-in Sharpe and Sortino ratios that strategies calculate and display in the Performance Summary tab use a default risk-free rate of 2%, and the metrics in this library's example code use the same default rate. Users can adjust this value to fit their analysis needs.

Risk-adjusted performance

Risk-adjusted performance metrics gauge the effectiveness of an investment by considering its returns relative to the perceived risk. They aim to provide a more well-rounded picture of performance by factoring in the level of risk taken to achieve returns. Investors can utilize such metrics to help determine whether the returns from an investment justify the risks and make informed decisions.

The two most commonly used risk-adjusted performance metrics are the Sharpe ratio and the Sortino ratio.

1. Sharpe ratio

The Sharpe ratio , developed by Nobel laureate William F. Sharpe, measures the performance of an investment compared to a theoretically risk-free asset, adjusted for the investment risk. The ratio uses the following formula:

Sharpe Ratio = (𝑅𝑎 − 𝑅𝑓) / 𝜎𝑎

Where:

• 𝑅𝑎 = Average return of the investment

• 𝑅𝑓 = Theoretical risk-free rate of return

• 𝜎𝑎 = Standard deviation of the investment's returns (volatility)

A higher Sharpe ratio indicates a more favorable risk-adjusted return, as it signifies that the investment produced higher excess returns per unit of increase in total perceived risk.

2. Sortino ratio

The Sortino ratio is a modified form of the Sharpe ratio that only considers downside volatility , i.e., the volatility of returns below the theoretical risk-free benchmark. Although it shares close similarities with the Sharpe ratio, it can produce very different values, especially when the returns do not have a symmetrical distribution, since it does not penalize upside and downside volatility equally. The ratio uses the following formula:

Sortino Ratio = (𝑅𝑎 − 𝑅𝑓) / 𝜎𝑑

Where:

• 𝑅𝑎 = Average return of the investment

• 𝑅𝑓 = Theoretical risk-free rate of return

• 𝜎𝑑 = Downside deviation (standard deviation of negative excess returns, or downside volatility)

The Sortino ratio offers an alternative perspective on an investment's return-generating efficiency since it does not consider upside volatility in its calculation. A higher Sortino ratio signifies that the investment produced higher excess returns per unit of increase in perceived downside risk.

█ CALCULATIONS

Return period detection

Calculating risk-adjusted performance metrics requires collecting returns across several periods of a given size. Analysts may use different period sizes based on the context and their preferences. However, two widely used standards are monthly or daily periods, depending on the available data and the investment's duration. The built-in ratios displayed in the Strategy Tester utilize returns from either monthly or daily periods in their calculations based on the following logic:

• Use monthly returns if the history of closed trades spans at least two months.

• Use daily returns if the trades span at least two days but less than two months.

• Do not calculate the ratios if the trade data spans fewer than two days.

This library's `detectPeriod()` function applies related logic to available chart data rather than trade data to determine which period is appropriate:

• It returns true if the chart's data spans at least two months, indicating that it's sufficient to use monthly periods.

• It returns false if the chart's data spans at least two days but not two months, suggesting the use of daily periods.

• It returns na if the length of the chart's data covers less than two days, signifying that the data is insufficient for meaningful ratio calculations.

It's important to note that programmers should only call `detectPeriod()` from a script's global scope or within the outermost scope of a function called from the global scope, as it requires the time value from the first bar to accurately measure the amount of time covered by the chart's data.

Collecting periodic returns

This library's `getPeriodicReturns()` function tracks price return data within monthly or daily periods and stores the periodic values in an array . It uses a `detectPeriod()` call as the condition to determine whether each element in the array represents the return over a monthly or daily period.