Donchian x WMA Crossover (2025 Only, Adjustable TP, Real OHLC)Short Description:

Long-only breakout system that goes long when the Donchian Low crosses up through a Weighted Moving Average, and closes when it crosses back down (with an optional take-profit), restricted to calendar year 2025. All signals use the instrument’s true OHLC data (even on Heikin-Ashi charts), start with 1 000 AUD of capital, and deploy 100 % equity per trade.

Ideal parameters configured for Temple & Webster on ASX 30 minute candles. Adjust parameter to suit however best to download candle interval data and have GPT test the pine script for optimum parameters for your trading symbol.

Detailed Description

1. Strategy Concept

This strategy captures trend-driven breakouts off the bottom of a Donchian channel. By combining the Donchian Low with a WMA filter, it aims to:

Enter when volatility compresses and price breaks above the recent Donchian Low while the longer‐term WMA confirms upward momentum.

Exit when price falls back below that same WMA (i.e. when the Donchian Low crosses back down through WMA), but only if the WMA itself has stopped rising.

Optional Take-Profit: you can specify a profit target in decimal form (e.g. 0.01 = 1 %).

2. Timeframe & Universe

In-sample period: only bars stamped between Jan 1 2025 00:00 UTC and Dec 31 2025 23:59 UTC are considered.

Any resolution (e.g. 30 m, 1 h, D, etc.) is supported—just set your preferred timeframe in the TradingView UI.

3. True-Price Execution

All indicator calculations (Donchian Low, WMA, crossover checks, take-profit) are sourced from the chart’s underlying OHLC via request.security(). This guarantees that:

You can view Heikin-Ashi or other styled candles, but your strategy will execute on the real OHLC bars.

Chart styling never suppresses or distorts your backtest results.

4. Position Sizing & Equity

Initial capital: 1 000 AUD

Size per trade: 100 % of available equity

No pyramiding: one open position at a time

5. Inputs (all exposed in the “Inputs” tab):

Input Default Description

Donchian Length 7 Number of bars to calculate the Donchian channel low

WMA Length 62 Period of the Weighted Moving Average filter

Take Profit (decimal) 0.01 Exit when price ≥ entry × (1 + take_profit_perc)

6. How It Works

Donchian Low: ta.lowest(low, DonchianLength) over the specified look-back.

WMA: ta.wma(close, WMALength) applied to true closes.

Entry: ta.crossover(DonchianLow, WMA) AND barTime ∈ 2025.

Exit:

Cross-down exit: ta.crossunder(DonchianLow, WMA) and WMA is not rising (i.e. momentum has stalled).

Take-profit exit: price ≥ entry × (1 + take_profit_perc).

Calendar exit: barTime falls outside 2025.

7. Usage Notes

After adding to your chart, open the Strategy Tester tab to review performance metrics, list of trades, equity curve, etc.

You can toggle your chart to Heikin-Ashi for visual clarity without affecting execution, thanks to the real-OHLC calls.

"entry" için komut dosyalarını ara

Momentum Trend Bands (MTB)📌 What Is the Momentum Trend Bands (MTB) Indicator?

The Momentum Trend Bands (MTB) is a custom-built trend detection indicator that blends momentum and volatility into a dynamic, visual system. Its core goal is to help traders identify the beginning and strength of a trend earlier than traditional tools like moving averages, while filtering out market noise.

🧠 What Is It Built On?

The indicator is built on two foundational concepts:

1. Rate of Change (ROC): This measures the speed at which the price is moving. We use a fast and a slow version of ROC and then calculate their difference. This difference gives us a momentum signal — it shows whether the price is gaining upward or downward strength.

2. Standard Deviation (Volatility): This shows how much the price fluctuates. By calculating it over a certain period, we can measure market noise and filter out weak, insignificant moves that might otherwise cause false signals.

Together, momentum shows direction, and volatility shows confidence.

🛠️ How Does It Work?

• The core of the indicator is a smoothed momentum signal, representing the net difference between fast and slow momentum.

• Around this signal, we build upper and lower bands — these are dynamic boundaries that expand or contract based on volatility.

• When the momentum breaks above or below these bands, it signals a strong directional move — suggesting the start or continuation of a trend.

The bands also serve a visual filter:

• If momentum stays within the bands, it implies the market is consolidating or ranging.

• When it exits the bands decisively, it implies strength in that direction.

📈 How to Use It?

1. Trend Entry:

o When the momentum signal rises above the upper band, it suggests a strong bullish trend may be starting.

o When the signal drops below the lower band, it indicates a bearish trend.

2. Stay Out of Chop:

o If the signal moves sideways within the bands, it’s best to avoid trading — the market is likely consolidating or ranging.

3. Visual Confirmation:

o The background color changes with the trend: green for bullish, red for bearish, gray for neutral. This makes it quick to read visually.

4. Signal Arrows:

o Small up or down arrows appear when trends begin, serving as early entry points.

⚙️ What Kind of Market Does It Work Best In?

• Trending Markets: MTB shines in markets with strong directional movement — whether up or down. It's designed to pick up momentum early and hold through trend continuation.

• Volatile Instruments: The built-in volatility filter helps in markets like crypto or commodities where price action is fast and erratic.

• Avoid Flat or Low-Volume Conditions: In sideways markets, MTB may stay gray or flip often — these are not ideal times to trade using this indicator alone.

💎 Why Is It Unique?

Unlike many indicators that react slowly (like moving averages) or trigger too often (like raw momentum), MTB balances early detection with reliability. Its unique combination of:

• ROC difference for directional intent,

• Smoothing for signal clarity,

• Bands scaled by volatility for robustness,

…makes it stand apart from commonly available indicators on platforms like TradingView.

Three Candle Bullish Engulfing StrategyThe Three Candle Bullish Engulfing Strategy is a versatile, multi-mode trading system designed for TradingView, combining classic candlestick patterns with momentum confirmation and dynamic risk management. This script supports both swing trading and intraday approaches, as well as an optional RSI-based breakout mode for additional signal filtering.

Key Features:

Three Candle Pattern Detection:

The strategy identifies potential trend reversal points using a three-candle pattern:

The first candle is a strong bullish (or bearish) move.

The second candle is a doji or small-bodied candle, indicating indecision.

The third candle is a bullish (or bearish) engulfing candle that closes above (or below) the previous high (or low), confirming the reversal.

Flexible Trading Modes:

Swing Long Only: Enter long trades on bullish three-candle setups.

Intraday Long & Short: Trade both long and short based on bullish and bearish three-candle patterns, with automatic session-end exits.

RSI Breakout Mode: Enter long trades when the 1-hour RSI exceeds a user-defined threshold (default 80) and a bullish candle forms, with breakout confirmation and a fixed-percentage stop loss.

Visual Aids:

Plots the RSI breakout trigger price and stop loss on the chart for easy monitoring.

How It Works:

Three Candle Pattern Entries:

Long Entry: Triggered when a bullish candle is followed by a doji, then a bullish engulfing candle closes above the previous high.

Short Entry (Intraday only): Triggered by the inverse pattern—bearish candle, doji, then bearish engulfing candle closing below the previous low.

RSI Breakout Entries:

When the RSI on a higher timeframe (default 1 hour) exceeds the set threshold and a bullish candle forms, the script records a trigger price.

A long trade is entered if the price breaks above this trigger, with a stop loss set a fixed percentage below.

Exits:

Positions are closed if the trailing stop is hit, the session ends (for intraday mode), or the stop loss is triggered in RSI breakout mode.

In RSI breakout mode, positions are also closed if a new breakout trigger forms while in position.

Zero Lag Multi Timeframe MACDCommon parts of the Multi Time Frame MACD

Why This MACD is Special

Traditional MACD (Moving Average Convergence Divergence) is a powerful trend-following indicator, but it has a key limitation: it only reflects price action on a single timeframe. Traders who rely on top-down analysis—analyzing higher timeframes first before moving to lower ones—often face a frustrating delay.

The Problem with Traditional Multi-Timeframe MACD with top down analysis:

If you’re on a 5-minute chart and want to see the 1-hour MACD, you must wait for 12 candles (1 hour) to close before the MACD updates.

This lag means you miss real-time signals and react too late to trend changes.

The Zero Lag Multi-Timeframe MACD solves this by using a custom time-adjusted formula (developed by CoffeeShopCrypto) that projects higher timeframe MACD values onto lower timeframe charts in real time.

How Traders Normally Use MACD

Single-Timeframe MACD (Traditional Approach)

Used for trend identification (bullish/bearish).

Crossovers (MACD line crossing signal line) signal potential entries.

Divergences (price vs. MACD direction) warn of trend exhaustion.

Top-Down Analysis with Standard MACD (Manual Switching)

1. Check higher timeframe (e.g., 1-hour) for trend direction.

2. Switch to lower timeframe (e.g., 5-minute) for entries.

Problem: You must constantly switch charts and wait for higher timeframe candles to close.

This MACD Eliminates the Need for Switching

Higher timeframe MACD is plotted in real time on your lower timeframe chart.

No waiting for candle closes—instant trend confirmation.

Single-chart top-down analysis without switching timeframes.

How to Use This MACD for Trading

Since the MACD is an averaging indicator, it works best when trading with the trend. This version enhances that by showing two trends at once:

Lower Timeframe (LTF) MACD – Your current chart’s trend.

Higher Timeframe (HTF) MACD – The dominant trend.

Key Trading Rules

1. Strong Uptrend Setup (Best for Long Entries)

HTF MACD line is rising & above zero (strong bullish momentum).

LTF MACD line is also rising (confirms alignment).

Entry: Look for LTF MACD to cross above signal line.

Long Entry Confirmation:

When both the High Timeframe and Low Timeframe MACD Lines are moving in the same direction, this is a confirmation that both the HTF is matching the direction of the LTF.

In this example both MACD Lines are moving long so we are only looking to take long entries at this point forward.

Short Entry Confirmation:

When both the High Timeframe and Low Timeframe MACD Lines are moving in the same direction, this is a confirmation that both the HTF is matching the direction of the LTF.

In this example both MACD Lines are moving short so we are only looking to take long entries at this point forward.

2. Potential Reversal or Weak Uptrend

Trend Divergence Confirmation

This example shows you a confirmation of divergence between the trends. Its best to watch for a continuation of the previous major trend. In this example, we just came off a downtrend with a GAP DOWN.

How to see it: (Trend Divergence)

Two things will help you confirm this divergence

1.Notice the LTF and HTF MACD are moving away from each other.

2. Both the HTF and LTF Histogram are shrinking.

This is an expression of lack of trend.

What to do:

High Timeframe Trends are always the lead so wait for the Low Timeframe to catch up to the High Timeframe trend.

Limitations:

The Exponential Moving Average calculation can only be applied to the Low Timeframe MACD because of the way its weighted against more recent price action and closing values.

This same EMA calculation can not be applied to the High Timeframe MACD as its being recalculated and the result means you can not weigh values against its current plot point.

Low Timeframe MACD can use EMA / SMA

High Timeframe MACD can only use SMA

ORB 5M + VWAP + Braid Filter + TP 2R o Niveles PreviosORB 5-Minute Breakout Strategy Summary

Strategy Name:

ORB 5M + VWAP + Braid Filter + TP 2R or Previous Levels

Timeframe:

5-minute chart

Trading Window:

9:35 AM to 11:00 AM (New York time)

✅ Entry Conditions:

Opening Range: Defined from 9:30 to 9:35 AM (first 5-minute candle).

Breakout Entry:

Long trade: Price breaks above the opening range high.

Short trade: Price breaks below the opening range low.

Confirmation Filters (All must be met):

Strong candle (green for long, red for short).

VWAP in the direction of the trade.

Braid Filter by Mango2Juice supports the breakout direction (green for long, red for short).

📉 Stop Loss:

Placed at the opposite side of the opening range.

🎯 Take Profit (TP):

+2R (Risk-to-Reward Ratio of 2:1),

or

Closest of the following: previous day’s high/low or premarket levels.

⚙️ Additional Rules:

Only valid signals between 9:35 and 11:00 AM.

Only one trade per breakout direction per day.

Filter out "trap candles" (very small or indecisive candles).

Avoid trading after 11:00 AM.

📊 Performance Goals:

Maintain a high Profit Factor (above 3 ideally).

Focus on tickers with good historical performance under this strategy (e.g., AMZN, PLTR, CVNA).

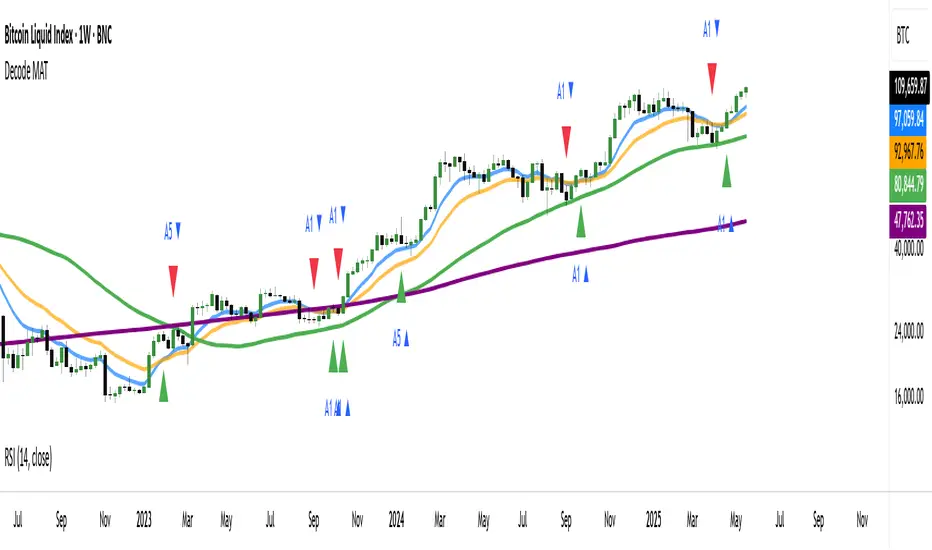

DECODE Moving Average ToolkitDECODE Moving Average Toolkit: Your All-in-One MA Analysis Powerhouse!

This versatile indicator is designed to be your go-to solution for analysing trends, identifying potential entry/exit points, and staying ahead of market movements using the power of Moving Averages (MAs).

Whether you're a seasoned trader or just starting out, the Decode MAT offers a comprehensive suite of features in a user-friendly package.

Key Features:

Multiple Moving Averages: Visualize up to 10 Moving Averages simultaneously on your chart.

Includes 5 Exponential Moving Averages (EMAs) and 5 Simple Moving Averages (SMAs).

Easily toggle the visibility of each MA and customize its length to suit your trading style and the asset you're analyzing.

Dynamic MA Ribbons: Gain a clearer perspective on trend direction and strength with 5 configurable MA Ribbons.

Each ribbon is formed between a corresponding EMA and SMA (e.g., EMA 20 / SMA 20).

The ribbon color changes to indicate bullish (e.g., green) or bearish (e.g., red) sentiment, providing an intuitive visual cue.

Toggle ribbon visibility with a single click.

Powerful Crossover Alerts: Never miss a potential trading opportunity with up to 5 customizable MA Crossover Alerts.

Define your own fast and slow MAs for each alert from any of the 10 available MAs.

Receive notifications directly through TradingView when your specified MAs cross over or cross under.

Optionally display visual symbols (e.g., triangles ▲▼) directly on your chart at the exact crossover points for quick identification.

Highly Customizable:

Adjust the source price (close, open, etc.) for all MA calculations.

Fine-tune the appearance (colors, line thickness) of every MA line, ribbon, and alert symbol to match your charting preferences.

User-Friendly Interface: All settings are neatly organized in the indicator's input menu, making configuration straightforward and intuitive.

How Can You Use the Decode MAT in Your Trading?

This toolkit is incredibly versatile and can be adapted to various trading strategies:

Trend Identification:

Use longer-term MAs (e.g., 50, 100, 200 period) to identify the prevailing market trend. When prices are consistently above these MAs, it suggests an uptrend, and vice-versa.

Observe the MA ribbons: A consistently green ribbon can indicate a strong uptrend, while a red ribbon can signal a downtrend. The widening or narrowing of the ribbon can also suggest changes in trend momentum.

Dynamic Support & Resistance:

Shorter-term MAs (e.g., 10, 20 period EMAs) can act as dynamic levels of support in an uptrend or resistance in a downtrend. Look for price pullbacks to these MAs as potential entry opportunities.

Crossover Signals (Entries & Exits):

Golden Cross / Death Cross: Configure alerts for classic crossover signals. For example, a 50-period MA crossing above a 200-period MA (Golden Cross) is often seen as a long-term bullish signal. Conversely, a 50-period MA crossing below a 200-period MA (Death Cross) can be a bearish signal.

Shorter-Term Signals: Use crossovers of shorter-term MAs (e.g., EMA 10 crossing EMA 20) for more frequent, shorter-term trading signals. A fast MA crossing above a slow MA can signal a buy, while a cross below can signal a sell.

Use the on-chart symbols for quick visual confirmation of these crossover events.

Confirmation Tool:

Combine the Decode MAT with other indicators (like RSI, MACD, or volume analysis) to confirm signals and increase the probability of successful trades. For instance, a bullish MA crossover combined with an oversold RSI reading could strengthen a buy signal.

Multi-Timeframe Analysis:

Apply the toolkit across different timeframes to get a broader market perspective. A long-term uptrend on the daily chart, confirmed by a short-term bullish crossover on the 1-hour chart, can provide a higher-confidence entry.

The DECODE Moving Average Toolkit empowers you to tailor your MA analysis precisely to your needs.

Risk Calculator PRO — manual lot size + auto lot-suggestionWhy risk management?

90 % of traders blow up because they size positions emotionally. This tool forces Risk-First Thinking: choose the amount you’re willing to lose, and the script reverse-engineers everything else.

Key features

1. Manual or Market Entry – click “Use current price” or type a custom entry.

2. Setup-based ₹-Risk – four presets (A/B/C/D). Edit to your workflow.

3. Lot-Size Input + Auto Lot Suggestion – you tell the contract size ⇒ script tells you how many lots.

4. Auto-SL (optional) – tick to push stop-loss to exactly 1-lot risk.

5. Instant Targets – 1 : 2, 1 : 3, 1 : 4, 1 : 5 plotted and alert-ready.

6. P&L Preview – table shows potential profit at each R-multiple plus real ₹ at SL.

7. Margin Column – enter per-lot margin once; script totals it for any size.

8. Clean Table UI – dark/light friendly; updates every 5 bars.

9. Alert Pack – SL, each target, plus copy-paste journal line on the chart.

How to use

1. Add to chart > “Format”.

2. Type the lot size for the symbol (e.g., 1250 for Natural Gas, 1 for cash equity).

3. Pick Side (Buy / Sell) & Setup grade.

4. ✅ If you want the script to place SL for you, tick Auto-SL (risk = 1 lot).

5. Otherwise type your own Stop-loss.

6. Read the table:

• Suggested lots = how many to trade so risk ≤ setup ₹.

• Risk (currency) = real money lost if SL hits.

7. Set TradingView alerts on the built-in conditions (T1_2, SL_hit, etc.) if you’d like push / email.

8. Copy the orange CSV label to Excel / Sheets for journalling.

Best practices

• Never raise risk to “fit” a trade. Lower size instead.

• Review win-rate vs. R multiple monthly; adjust setups A–D accordingly.

• Test Auto-SL in replay before going live.

Disclaimer

This script is educational. Past performance ≠ future results. The author isn’t responsible for trading losses.

CYCLE BY RiotWolftradingDescription of the "CYCLE" Indicator

The "CYCLE" indicator is a custom Pine Script v5 script for TradingView that visualizes cyclic patterns in price action, dividing the trading day into specific sessions and 90-minute quarters (Q1-Q4). It is designed to identify and display market phases (Accumulation, Manipulation, Distribution, and Continuation/Reversal) along with key support and resistance levels within those sessions. Additionally, it allows customization of boxes, lines, labels, and colors to suit user preferences.

Main Features

Cycle Phases:

Accumulation (1900-0100): Represents the phase where large operators accumulate positions.

Manipulation (0100-0700): Identifies potential manipulative moves to mislead retail traders.

Distribution (0700-1300): The phase where large operators distribute their positions.

Continuation/Reversal (1300-1900): Indicates whether the price continues the trend or reverses.

90-Minute Quarters (Q1-Q4):

Divides each 6-hour cycle (360 minutes) into four 90-minute quarters (Q1: 00:00-01:30, Q2: 01:30-03:00, Q3: 03:00-04:30, Q4: 04:30-06:00 UTC).

Each quarter is displayed with a colored box (Q1: light purple, Q2: light blue, Q3: light gray, Q4: light pink) and labels (defaulted to black).

Support and Resistance Visualization:

Draws boxes or lines (based on settings) showing the high and low levels of each session.

Optionally displays accumulated volume at the highs and lows within the boxes.

Daily Lines and Last 3 Boxes:

How to Use the Indicator

Step 1: Add the Indicator to TradingView

Open TradingView and select the chart where you want to apply the indicator (e.g., UMG9OOR on a 5-minute timeframe, as shown in the screenshot).

Go to the Pine Editor (at the bottom of the TradingView interface).

Copy and paste the provided code.

Click Compile and then Add to Chart.

Step 2: Configure the Indicator

Click on the indicator name on the chart ("CYCLE") and select Settings (or double-click the name).

Adjust the options based on your needs:

Cycle Phases: Enable/disable phases (Accumulation, Manipulation, Distribution, Continuation/Reversal) and adjust their time slots if needed.

90-Minute Quarters: Enable/disable quarters (Q1-Q4).

Step 3: Interpret the Indicator

Identify Cycle Phases:

Observe the red boxes indicating the phases (Accumulation, Manipulation, etc.).

The high and low levels within each phase are potential support/resistance zones.

If volume is enabled, pay attention to the accumulated volume at highs and lows, as it may indicate the strength of those levels.

Use the 90-Minute Quarters (Q1-Q4):

The colored boxes (Q1-Q4) divide the day into 90-minute segments.

Each quarter shows the price range (high and low) during that period.

Use these boxes to identify price patterns within each quarter, such as breakouts or consolidations.

The labels (Q1, Q2, etc.) help you track time and anticipate potential moves in the next quarter.

Analyze Support and Resistance:

The high and low levels of each phase/quarter act as support and resistance.

Daily lines (if enabled) show key levels from the previous day, useful for planning entries/exits.

The "last 3 boxes below price" (if enabled) highlight potential support levels the price might target.

Avoid Manipulation:

During the Manipulation phase (0100-0700), be cautious of sharp moves or false breakouts.

Use the high/low levels of this phase to identify potential traps (as explained in your first question about manipulation candles).

Step 4: Trading Strategy

Entries and Exits:

Support/Resistance: Use the high/low levels of phases and quarters to set entry or exit points.

For example, if the price bounces off a Q1 support level, consider a buy.

Breakouts: If the price breaks a high/low of a quarter (e.g., Q2), wait for confirmation to enter in the direction of the breakout.

Volume: If accumulated volume is high near a key level, that level may be more significant.

Risk Management:

Place stop-loss orders below lows (for buys) or above highs (for sells) identified by the indicator.

Avoid trading during the Manipulation phase unless you have a specific strategy to handle false breakouts.

Time Context:

Use the quarters (Q1-Q4) to plan your trades based on time. For example, if Q3 is typically volatile in your market, prepare for larger moves between 03:00-04:30 UTC.

Step 5: Adjustments and Testing

Test on Different Timeframes: The indicator is set for a 5-minute timeframe (as in the screenshot), but you can test it on other timeframes (e.g., 1-minute, 15-minute) by adjusting the time slots if needed.

Adjust Colors and Styles: If the default colors are not visible on your chart, change them for better clarity.

---

📌 1. **Accumulation: Strong Institutional Activity**

- During the **accumulation phase, we see **high volume: 82.773K, which suggests strong buying interest**, likely from institutional players.

- This sets the base for the following upward move in price.

---

📌 2. **Manipulation: False Breakout with Lower Volume**

- Later, there's a manipulation phase where price breaks above previous highs, but the volume (71.814K) is **lower than during accumulation**.

- This implies that buyers are not as aggressive as before—no real demandbehind the breakout.

- It’s likely a bull trap, where smart money is selling into the breakout to exit their positions.

---

### 📌 3. Distribution: Weakness and Lack of Demand

- The market enters a distribution phase, and volume drops even further (only 7.914K).

- Price struggles to go higher, and you start seeing rejections at the top.

- This shows that demand is drying up, and smart money is offloading positions**—not accumulating anymore.

---

### 💡 Why Take the Short Here?

- Volume is not increasing with new highs—showing weak demand**.

- The manipulation volume is weaker than the accumulation volume, confirming the breakout was likely false.

- Structure starts to break down (Q levels falling), which confirms weakness.

- This creates a high-probability short setup:

- **Entry:** after confirmation of distribution and structural breakdown.

- **Stop loss:** above the manipulation high.

- **Target:** down toward previous lows or value zones.

---

### ✅ Conclusion

Since the manipulation volume failed to exceed the accumulation volume, the breakout lacked real strength. Combined with decreasing volume in the distribution phase, this indicates fading demand and supply taking control—which justifies entering a short position.

RSI Divergence Strategy - AliferCryptoStrategy Overview

The RSI Divergence Strategy is designed to identify potential reversals by detecting regular bullish and bearish divergences between price action and the Relative Strength Index (RSI). It automatically enters positions when a divergence is confirmed and manages risk with configurable stop-loss and take-profit levels.

Key Features

Automatic Divergence Detection: Scans for RSI pivot lows/highs vs. price pivots using user-defined lookback windows and bar ranges.

Dual SL/TP Methods:

- Swing-based: Stops placed a configurable percentage beyond the most recent swing high/low.

- ATR-based: Stops placed at a multiple of Average True Range, with a separate risk/reward multiplier.

Long and Short Entries: Buys on bullish divergences; sells short on bearish divergences.

Fully Customizable: Input groups for RSI, divergence, swing, ATR, and general SL/TP settings.

Visual Plotting: Marks divergences on chart and plots stop-loss (red) and take-profit (green) lines for active trades.

Alerts: Built-in alert conditions for both bullish and bearish RSI divergences.

Detailed Logic

RSI Calculation: Computes RSI of chosen source over a specified period.

Pivot Detection:

- Identifies RSI pivot lows/highs by scanning a lookback window to the left and right.

- Uses ta.barssince to ensure pivots are separated by a minimum/maximum number of bars.

Divergence Confirmation:

- Bullish: Price makes a lower low while RSI makes a higher low.

- Bearish: Price makes a higher high while RSI makes a lower high.

Entry:

- Opens a Long position when bullish divergence is true.

- Opens a Short position when bearish divergence is true.

Stop-Loss & Take-Profit:

- Swing Method: Computes the recent swing high/low then adjusts by a percentage margin.

- ATR Method: Uses the current ATR × multiplier applied to the entry price.

- Take-Profit: Calculated as entry price ± (risk × R/R ratio).

Exit Orders: Uses strategy.exit to place bracket orders (stop + limit) for both long and short positions.

Inputs and Configuration

RSI Settings: Length & price source for the RSI.

Divergence Settings: Pivot lookback parameters and valid bar ranges.

SL/TP Settings: Choice between Swing or ATR method.

Swing Settings: Swing lookback length, margin (%), and risk/reward ratio.

ATR Settings: ATR length, stop multiplier, and risk/reward ratio.

Usage Notes

Adjust the Pivot Lookback and Range values to suit the volatility and timeframe of your market.

Use higher ATR multipliers for wider stops in choppy conditions, or tighten swing margins in trending markets.

Backtest different R/R ratios to find the balance between win rate and reward.

Disclaimer

This script is for educational purposes only and does not constitute financial advice. Trading carries significant risk and you may lose more than your initial investment. Always conduct your own research and consider consulting a professional before making any trading decisions.

Head Hunter HHHead Hunter HH - Advanced Market Structure & Volume Analysis Indicator

This indicator combines volume analysis, price action, and VWAP to identify high-probability trading opportunities across multiple timeframes.

Key Features:

• Smart Volume Analysis: Detects institutional volume patterns using dynamic thresholds

• VWAP-Based Market Structure: Multiple standard deviation bands for precision entry/exit

• Daily Level Integration: Previous day's high, low, close, and current day's open

• Advanced Signal Classification: Regular, Super Strong, and Scalp signals

Signal Types:

1. Regular Signals (White/Purple Triangles)

• Volume-confirmed reversals

• Institutional price levels

• Technical momentum alignment

2. Super Strong Signals (Green/Red Diamonds)

• High-volume breakouts

• Strong momentum confirmation

• Multiple timeframe alignment

3. Scalp Signals (Green/Magenta Circles)

• Quick reversal opportunities

• VWAP deviation analysis

• Volume surge confirmation

Visual Components:

• VWAP with Standard Deviation Bands

• 50 MA (optional)

• Daily Reference Levels

• Color-coded signals based on strength

• Bar color changes on confirmed signals

Best Practices:

• Most effective on higher timeframes (1H+)

• Use with major pairs/instruments

• Combine signals with support/resistance

• Monitor volume confirmation

• Wait for candle close confirmation

This indicator helps identify institutional order flow and high-probability reversal zones by analyzing volume patterns, price action, and market structure, providing traders with multiple confirmation layers before entry.

Note: Results may vary based on market conditions and timeframe selection. Always use proper risk management.

Trend Indicator with ArrowsTrend Indicator with arrows is a NoBrainer indicator to see the trend clearly.

UpTrend is defined as a candle closing above previous high. I

DownTrend is defined as a candle closing below previous low

A consolidation is defined as a candle closing inside previous candle high low.

UpTrend - Indicated with a green arrow below the candle with the current indicator.

DownTrend - ndicated with a red arrow above the candle with the current indicator.

So How to use this Indicator?

Identify zones of consolidation where the indicator doesn't show any arrows. Upon shift from consolidation to UpTrend or DownTrend take a entry. This is one way.

Second and most useful way is wait for Support or resistant hit.

If it's a support. Upon support hit wait for Consolidation, DownTrend and then UpTrend/(Consolidation again with uptrend) for long entry.

If its a resistance. Upon resistance hit wait for Consolidation, Uptrend and then DownTrend/(Consolidation again with DownTrend) for short Entry.

LUX CLARA - EMA + VWAP (No ATR Filter) - v6EMA STRAT SHOUT OUTOUTLIERSSSSS

Overview:

an intraday strategy built around two core principles:

Trend Confirmation using the 50 EMA (Exponential Moving Average) in relation to the VWAP (Volume-Weighted Average Price).

Entry Signals triggered by the 8 EMA crossing the 50 EMA in the direction of that confirmed trend.

Key Logic:

Bullish Trend if the 50 EMA is above VWAP. Only long entries are allowed when the 8 EMA crosses above the 50 EMA during that bullish phase.

Bearish Trend if the 50 EMA is below VWAP. Only short entries are allowed when the 8 EMA crosses below the 50 EMA during that bearish phase.

Intraday Focus: Trades are restricted to a user-defined session window (default 7:30 AM–11:30 AM), aligning entries/exits with peak intraday liquidity.

Exit Rule: Positions close automatically when the 8 EMA crosses back in the opposite direction of the entry.

Why It Works:

EMA + VWAP helps detect both immediate momentum (EMAs) and overall institutional bias (VWAP).

By confining trades to a set intraday window, the strategy aims to capture morning volatility while avoiding choppy afternoon or overnight sessions.

Customization:

Users can adjust EMA lengths, session times, or incorporate stops/targets for additional risk management.

It can be tested on various symbols and intraday timeframes to gauge performance and robustness.

Smart Money Pivot Strategy [Jason Kasei]This strategy is designed to identify key pivot points (Pivot High and Pivot Low) in the market and leverage the "Smart Money" concept to capture price breakout opportunities. It supports both long and short trades, offering customizable stop-loss (SL) and take-profit (TP) settings, while visually plotting pivot points and breakout signals on the chart.

Core Features

Pivot Point Detection:

Utilizes ta.pivothigh and ta.pivotlow functions to detect the highest (Pivot High) and lowest (Pivot Low) points within a specified period (default: 20 bars).

Trading Signals:

Long Signal: Triggered when the price breaks above a previous Pivot High, indicating a potential uptrend.

Short Signal: Triggered when the price breaks below a previous Pivot Low, indicating a potential downtrend.

How It Works

Detects Pivot High (PH) and Pivot Low (PL) over the specified period and records their price and time.

Triggers a long entry when the price breaks above a Pivot High and a short entry when it falls below a Pivot Low.

Sets exit conditions automatically based on predefined SL and TP percentages after entry.

Plots breakout points and levels on the chart for analysis.

Considerations

The strategy relies on accurate pivot point detection; adjust the period parameter based on market volatility.

In highly volatile markets, consider widening the stop loss to avoid frequent triggering.

Combine with other indicators or analysis methods to validate signals and avoid blind trading.

Long Term Profitable Swing | AbbasA Story of a Profitable Swing Trading Strategy

Imagine you're sailing across the ocean, looking for the perfect wave to ride. Swing trading is quite similar—you're navigating the stock market, searching for the ideal moments to enter and exit trades. This strategy, created by Abbas, helps you find those waves and ride them effectively to profitable outcomes.

🌊 Finding the Perfect Wave (Entry)

Our journey begins with two simple signs that tell us a great trading opportunity is forming:

- Moving Averages: We use two lines that follow price trends—the faster one (EMA 16) reacts quickly to recent price moves, and the slower one (EMA 30) gives us a longer-term perspective. When the faster line crosses above the slower line, it's like a clear signal saying, "Hey! The wave is rising, and prices might move higher!"

- RSI Momentum: Next, we check a tool called the RSI, which measures momentum (how strongly prices are moving). If the RSI number is above 50, it means there's enough strength behind this rising wave to carry us forward.

When both signals appear together, that's our green light. It's time to jump on our surfboard and start riding this promising wave.

⚓ Safely Riding the Wave (Risk Management)

While we're riding this wave, we want to ensure we're safe from sudden surprises. To do this, we use something called the Average True Range (ATR), which measures how volatile (or bumpy) the price movements are:

- Stop-Loss: To avoid falling too hard, we set a safety line (stop-loss) 8 times the ATR below our entry price. This helps ensure we exit if the wave suddenly turns against us, protecting us from heavy losses.

- Take Profit: We also set a goal to exit the trade at 11 times the ATR above our entry. This way, we capture significant profits when the wave reaches a nice high point.

🌟 Multiple Rides, Bigger Adventures

This strategy allows us to take multiple positions simultaneously—like riding several waves at once, up to 5. Each trade we make uses only 10% of our trading capital, keeping risks manageable and giving us multiple opportunities to win big.

🗺️ Easy to Follow Settings

Here are the basic settings we use:

- Fast EMA**: 16

- Slow EMA**: 30

- RSI Length**: 9

- RSI Threshold**: 50

- ATR Length**: 21

- ATR Stop-Loss Multiplier**: 8

- ATR Take-Profit Multiplier**: 11

These settings are flexible—you can adjust them to better suit different markets or your personal trading style.

🎉 Riding the Waves of Success

This simple yet powerful swing trading approach helps you confidently enter trades, clearly know when to exit, and effectively manage your risk. It’s a reliable way to ride market waves, capture profits, and minimize losses.

Happy trading, and may you find many profitable waves to ride! 🌊✨

Please test, and take into account that it depends on taking multiple longs within the swing, and you only get to invest 25/30% of your equity.

Mswing HommaThe Mswing is a momentum oscillator that calculates the rate of price change over 20 and 50 periods (days/weeks). Apart from quantifying momentum, it can be used for assessing relative strength, sectoral rotation & entry/exit signals.

Quantifying Momentum Strength

The Mswing's relationship with its EMA (e.g., 5-period or 9-period) is used for momentum analysis:

• M Swing >0 and Above EMA: Momentum is positive and accelerating (ideal for entries).

• M Swing >0 and Below EMA: Momentum is positive but decelerating (caution).

• M Swing <0 and Above EMA: Momentum is negative but improving (watch for reversals).

• M Swing <0 and Below EMA: Momentum is negative and worsening (exit or avoid).

Relative Strength Scanning (M Score)

Sort stocks by their M Swing using TradingView’s Pine scanner.

Compare the Mswing scores of indices/sectors to allocate capital to stronger groups (e.g., renewables vs. traditional energy).

Stocks with strong Mswing scores tend to outperform during bullish phases, while weak ones collapse faster in downtrends.

Entry and Exit Signals

Entry: Buy when Mswing crosses above 0 + price breaks key moving averages (50-day SMA). Use Mswing >0 to confirm valid breakouts. Buy dips when Mswing holds above EMA during retracements.

Exit: Mswing can be used for exiting a stock in 2 ways:

• Sell in Strength: Mswing >4 (overbought).

• Sell in Weakness: Mswing <0 + price below 50-day SMA.

Multi-Timeframe Analysis

• Daily: For swing trades.

• Weekly: For trend confirmation.

• Monthly: For long-term portfolio adjustments.

Fibonacci & Bollinger Bands StrategyTrading System: Fibonacci & Bollinger Bands Strategy

1. Session Timing

Trade only from 1 PM onwards.

Identify the first candle on the 1 PM vertical line to set the market direction.

If it's a bullish candle, look for buy opportunities.

If it's a bearish candle, look for sell opportunities.

2. Fibonacci Retracement as a Measuring Tool

Identify the recent swing high and swing low before the 1 PM session.

Draw Fibonacci retracement levels from low to high (for buys) or high to low (for sells).

Key retracement levels to watch: 0.0%, 50.0%, and 100.0%.

Entries can be placed at 0.0% or 50.0%, aiming for a move toward 100.0% retracement.

3. Bollinger Bands Confirmation

If the Bollinger Bands are above price, expect a downward move (sell).

If the Bollinger Bands are below price, expect an upward move (buy).

Use this as additional confirmation for your Fibonacci-based trade.

4. Entry & Exit Rules

Entry:

If the 1 PM candle confirms a bullish bias, enter long near Fibonacci 0.0% or 50.0%.

If the 1 PM candle confirms a bearish bias, enter short near Fibonacci 0.0% or 50.0%.

Stop Loss: Below (for buys) or above (for sells) the swing low/high used for Fibonacci.

Take Profit: Target 100.0% retracement level or next key resistance/support.

5. Risk Management

Risk 1-2% per trade.

Avoid trading if price is too far from Fibonacci levels.

Confirm setup with Bollinger Bands alignment.

BBr1 Candle Range Volitility Gap IndicatorModified Candle Range Volatility Gap Indicator

1. Useful to analyze bars body and wicks and volatility of security.

2. Added a Percentage Option - easier to analyze across different securities.

2. Added a Standard Deviation ("1 std dev= 68.2%, 2 std dev=95.4%, 3 std dev=99.7%, etc") based upon user defined lookback period.

3. Added the ability to include Gaps in Analysis. (Gaps are when the prior closing cost does not equal opening price)

4. Possible Uses setting up stop losses, trailing entries/exits (inside range or outside range).

5. Use it with other indicators in determining if to make an entry or close entry.

Reposted Original Description by © ka66 Kamal Advani

Visually shows the Body Range (open to close) and Candle Range (high to low).

Semi-transparent overlapping area is the full Candle Range, and fully-opaque smaller area is the Body Range. For aesthetics and visual consistency, Candle Range follows the direction of the Body Range, even though technically it's always positive (high - low).

The different plots for each range type also means the UI will allow deselecting one or the other as needed. For example, some strategies may care only about the Body Range, rather than the entire Candle Range, so the latter can be hidden to reduce noise.

Threshold horizontal lines are plotted, so the trader can modify these high and low levels as needed through the user interface. These need to be configured to match the instrument's price range levels for the timeframe. The defaults are pretty arbitrary for +/- 0.0080 (80 pips in a 4-decimal place forex pair). Where a range reaches or exceeds a threshold, it's visually marked as well with a shape at the Body or Candle peak, to assist with quicker visual potential setup scanning, for example, to anticipate a following reversal or continuation.

Opening Range BoxIndicator Name: Opening Range Box with Extensions

Author: YanivBull

Description:

The Opening Range Box with Extensions is a powerful tool designed to visualize the trading range established during the first 30 minutes of a market session, a critical period for setting the day's trend. This indicator plots a box representing the high and low prices formed within this opening range, with dashed extension lines projecting these levels forward throughout the session.

Its primary purpose is to identify the boundaries of the initial trend at the start of trading. When these boundaries are breached, it serves as a trigger for potential trading opportunities: a breakout above the box high signals a possible long entry, while a breakdown below the box low indicates a potential short entry. The indicator also includes historical boxes for up to 5 previous days (configurable), allowing traders to analyze past opening ranges and their extensions for context and pattern recognition.

Key Features:

Customizable session start time (hour and minute) to adapt to various markets (e.g., NYSE, DAX, etc.).

Displays the current session's opening range box in blue and historical boxes in gray.

Plots dashed extension lines from the high and low of each box, limited to 500 bars or the end of the trading day.

Adjustable number of historical days (1-20, default 5).

Usage:

Set the Session Start Hour and Session Start Minute according to your market's opening time (relative to your chart's timezone, e.g., UTC+2). Watch for price action around the box boundaries—breakouts above the high or below the low can be used as signals for initiating long or short trades, respectively. Combine with other technical analysis tools for confirmation.

This indicator is ideal for day traders looking to capitalize on early session momentum and breakout strategies.

Consecutive Close Tracker (CCT)Consecutive Close Tracker (CCT) Indicator

The Consecutive Close Tracker (CCT) is a powerful momentum and breakout detection tool designed to identify consecutive bullish and bearish closes, potential reversals, and breakout points. By tracking consecutive candle closes and plotting key levels, this indicator provides traders with visual cues to recognize trend continuations, reversals, and breakout opportunities effectively.

🔹 Key Features of CCT

1️⃣ Consecutive Move Lines (Green/Red/Yellow Lines)

Tracks three consecutive bullish or bearish closes.

If the fourth candle confirms the trend, a green line (bullish) or red line (bearish) is drawn.

If the fourth candle fails to confirm, a yellow line is drawn, signaling potential indecision.

Helps traders spot trend continuations and exhaustion points.

2️⃣ Reversal Detection Lines (Cyan & Light Red)

Identifies bullish and bearish reversals based on three higher/lower closes followed by a reversal.

A cyan line indicates a bullish reversal, while a light red line signals a bearish reversal.

Useful for traders looking for trend reversals and key turning points.

3️⃣ Breakout Line (Dynamic Resistance/Support Level)

Automatically calculates a breakout level based on the previous timeframe’s open and close.

Can be customized to use different timeframes (e.g., hourly, daily, weekly).

Acts as a dynamic resistance or support level, helping traders determine breakout opportunities.

🔍 How to Use the Indicator?

✅ 1. Spotting Trend Continuations with Consecutive Move Lines

Green Line: Three consecutive bullish closes followed by a fourth higher close.

🚀 Indicates strong buying pressure & potential uptrend continuation.

Red Line: Three consecutive bearish closes followed by a fourth lower close.

📉 Indicates strong selling pressure & potential downtrend continuation.

Yellow Line: Three consecutive closes, but the fourth candle fails to confirm.

⚠️ Signals possible indecision or trend exhaustion.

🔥 Best Strategy:

If a green line appears near support, consider long entries.

If a red line appears near resistance, consider short entries.

If a yellow line appears, wait for further confirmation before entering a trade.

✅ 2. Identifying Trend Reversals with Reversal Lines

Cyan Line: A bearish trend with three consecutive lower closes, followed by a bullish candle → Possible uptrend reversal.

Light Red Line: A bullish trend with three consecutive higher closes, followed by a bearish candle → Possible downtrend reversal.

🔥 Best Strategy:

If a cyan line appears near a major support level, look for long entry opportunities.

If a light red line appears near resistance, prepare for a potential short entry.

Use these lines in combination with candlestick patterns (e.g., bullish engulfing, pin bars) for confirmation.

✅ 3. Using the Breakout Line for Key Entry & Exit Points

The breakout line represents a key dynamic level (midpoint of the previous timeframe’s open & close).

If price breaks above the breakout line, it suggests bullish momentum → Consider long trades.

If price breaks below the breakout line, it suggests bearish momentum → Consider short trades.

🔥 Best Strategy:

Use the breakout line in combination with support & resistance levels.

When price approaches the breakout line, watch for confirmation candles before entering a trade.

The breakout line can also act as a stop-loss or take-profit level.

🎯 How to Utilize CCT Effectively?

✅ For Intraday Traders

Use the consecutive close tracker on a 5M or 15M chart to catch short-term trends.

Watch for reversal lines near major intraday support/resistance for quick scalping opportunities.

Use the breakout line from the hourly chart to identify potential trend shifts.

✅ For Swing Traders

Apply the indicator on 1H, 4H, or daily charts to track medium-term trends.

Look for green/red lines near key Fibonacci retracement or pivot levels.

Use reversal lines to detect early trend reversals before bigger moves occur.

✅ For Breakout Traders

Focus on the breakout line on higher timeframes (e.g., 1H, 4H, Daily) to identify strong momentum shifts.

If price crosses the breakout line with strong volume, enter trades with trend confirmation.

Place stop-loss just below the breakout level for controlled risk management.

🏆 Final Thoughts

The Consecutive Close Tracker (CCT) is a powerful momentum and reversal indicator that helps traders:

✅ Identify strong trend continuations (green/red lines).

✅ Detect early reversal points (cyan/light red lines).

✅ Use a dynamic breakout line for better trade entries & exits.

Whether you’re an intraday trader, swing trader, or breakout trader, this tool can enhance your market insights and improve your trading decisions. 📈🔥

🚀 Try it out, and integrate it with your strategy to maximize its potential! 🚀

Impulse MACD enhancedThis indicator is designed to provide robust trade entry signals by combining multiple technical filters. Here’s a summary of its key components:

Impulse MACD Calculation:

Uses a Zero-Lag EMA (ZLEMA) based approach to generate a momentum indicator (with a signal line and histogram) that identifies shifts in market momentum.

Simulated Higher Timeframe (HTF) Trend Filter:

Computes an SMA over a multiplied period to simulate a higher timeframe trend. It requires the price to be in line with this broader trend before signaling an entry.

RSI Filter:

Ensures that for bullish entries the RSI is above a set threshold (indicating momentum) and for bearish entries it’s below a threshold.

ADX Filter:

Uses a manually calculated ADX to confirm that the market is in a strong trend (ADX > 30) to reduce false signals in weakly trending or sideways markets.

Volume Filter:

Compares the current volume to a 20‑bar SMA of volume, requiring volume to be significantly higher (by a user-defined percentage) to confirm the strength of the move.

VWAP Confirmation:

Uses the Volume-Weighted Average Price as an extra layer of confirmation: bullish signals require the price to be above VWAP, bearish signals below.

Optional Long-Term & Short-Term MA Filters:

These filters can be enabled to ensure the price is trading above (or below) longer-term and shorter-term moving averages, further aligning the trade with the prevailing trend.

ATR Volatility Filter:

Checks that volatility (as measured by the ATR relative to price) is below a maximum threshold, which helps avoid taking trades in overly volatile conditions.

Price Action Filter:

Ensures that for a bullish signal the current close is above the highest high over a specified lookback period (and vice versa for bearish), indicating a clear breakout.

Signal Throttling:

Signals are limited to one every 10 bars to prevent excessive trading.

When all these conditions are met, the indicator outputs an entry signal for either a bullish or bearish trade.

This multi-filter approach aims to increase win rate by reducing false signals and aligning trades with strong, confirmed trends while filtering out noise.

3 Red / 3 Green Strategy with Volatility CheckStrategy Name: 3 Red / 3 Green Strategy with Volatility Check by AlgoTradeKit

Overview

This long-only strategy is designed for daily bars on NASDAQ (or similar instruments) and combines simple price action with a volatility filter. It “tells it like it is” – enter when the market shows weakness, but only in sufficiently volatile conditions, and exit either on signs of a reversal or after a set number of days.

Entry Conditions

- Price Action :

Enter a long position when there are 3 consecutive red days (each day's close is below its open).

- Volatility Filter :

The entry is allowed only if the current ATR (Average True Range) calculated over the specified ATR Period (default 12) is greater than its 30-day simple moving average. This ensures the market has enough volatility to justify the trade.

Exit Conditions

- Reversal Signal :

Exit the long position when 3 consecutive green days occur (each day's close is above its open), signaling a potential reversal.

- Time Limit :

Regardless of market conditions, any open trade is closed if it reaches the Maximum Trade Duration (default 22 days). This helps limit exposure during stagnant or unfavorable market conditions.

- You can toggle the three-green-day exit if you want to isolate the time-based exit.

Input Parameters

- Maximum Trade Duration (days): Default is 22 days.

- ATR Period: Default is 12.

- Use 3 Green Days Exit: Toggle to enable or disable the three-green-day exit condition.

How It Works

1. Entry: The strategy monitors daily price action for 3 consecutive down days. When this occurs and if the market is volatile enough (current ATR > 30-day ATR average), it opens a long position.

2. Exit: The position is closed if the price action reverses with 3 consecutive up days or if the trade has been open for the maximum allowed duration - i.e. use it on daily chart.

Risk Management

- The built-in maximum trade duration prevents trades from lingering too long in a non-trending or consolidating market.

- The volatility filter helps ensure that trades are only taken when there is sufficient price movement, potentially increasing the odds of a meaningful move.

Disclaimer

This strategy is provided “as is” without any warranties. It is essential to backtest and validate the performance on your specific instrument and market conditions before deploying live capital. Trading involves significant risk, and you should adjust parameters to match your risk tolerance.

Test and tweak this strategy to see if it fits your trading style and market conditions. Happy trading!

Balance of Power for US30 4H [PineIndicators]The Balance of Power (BoP) Strategy is a momentum-based trading system for the US30 index on a 4-hour timeframe. It measures the strength of buyers versus sellers in each candle using the Balance of Power (BoP) indicator and executes trades based on predefined threshold crossovers. The strategy includes dynamic position sizing, adjustable leverage, and visual trade tracking.

⚙️ Core Strategy Mechanics

Positive values indicate buying strength.

Negative values indicate selling strength.

Values close to 1 suggest strong bullish momentum.

Values close to -1 indicate strong bearish pressure.

The strategy uses fixed threshold crossovers to determine trade entries and exits.

📌 Trade Logic

Entry Conditions

Long Entry: When BoP crosses above 0.8, signaling strong buying pressure.

Exit Conditions

Position Close: When BoP crosses below -0.8, indicating a shift to selling pressure.

This threshold-based system filters out low-confidence signals and focuses on high-momentum shifts.

📏 Position Sizing & Leverage

Leverage: Adjustable by the user (default = 5x).

Risk Management: Position size adapts dynamically based on equity fluctuations.

📊 Trade Visualization & History Tracking

Trade Markers:

"Buy" labels appear when a long position is opened.

"Close" labels appear when a position is exited.

Trade History Boxes:

Green for profitable trades.

Red for losing trades.

These elements provide clear visual tracking of past trade execution.

⚡ Usage & Customization

1️⃣ Apply the script to a US30 4H chart in TradingView.

2️⃣ Adjust leverage settings as needed.

3️⃣ Review trade signals and historical performance with visual markers.

4️⃣ Enable backtesting to evaluate past performance.

This strategy is designed for momentum-based trading and is best suited for volatile market conditions.

[SHORT ONLY] ATR Sell the Rip Mean Reversion Strategy█ STRATEGY DESCRIPTION

The "ATR Sell the Rip Mean Reversion Strategy" is a contrarian system that targets overextended price moves on stocks and ETFs. It calculates an ATR‐based trigger level to identify shorting opportunities. When the current close exceeds this smoothed ATR trigger, and if the close is below a 200-period EMA (if enabled), the strategy initiates a short entry, aiming to profit from an anticipated corrective pullback.

█ HOW IS THE ATR SIGNAL BAND CALCULATED?

This strategy computes an ATR-based signal trigger as follows:

Calculate the ATR

The strategy computes the Average True Range (ATR) using a configurable period provided by the user:

atrValue = ta.atr(atrPeriod)

Determine the Threshold

Multiply the ATR by a predefined multiplier and add it to the current close:

atrThreshold = close + atrValue * atrMultInput

Smooth the Threshold

Apply a Simple Moving Average over a specified period to smooth out the threshold, reducing noise:

signalTrigger = ta.sma(atrThreshold, smoothPeriodInput)

█ SIGNAL GENERATION

1. SHORT ENTRY

A Short Signal is triggered when:

The current close is above the smoothed ATR signal trigger.

The trade occurs within the specified trading window (between Start Time and End Time).

If the EMA filter is enabled, the close must also be below the 200-period EMA.

2. EXIT CONDITION

An exit Signal is generated when the current close falls below the previous bar’s low (close < low ), indicating a potential bearish reversal and prompting the strategy to close its short position.

█ ADDITIONAL SETTINGS

ATR Period: The period used to calculate the ATR, allowing for adaptability to different volatility conditions (default is 20).

ATR Multiplier: The multiplier applied to the ATR to determine the raw threshold (default is 1.0).

Smoothing Period: The period over which the raw ATR threshold is smoothed using an SMA (default is 10).

Start Time and End Time: Defines the time window during which trades are allowed.

EMA Filter (Optional): When enabled, short entries are only executed if the current close is below the 200-period EMA, confirming a bearish trend.

█ PERFORMANCE OVERVIEW

This strategy is designed for use on the Daily timeframe, targeting stocks and ETFs by capitalizing on overextended price moves.

It utilizes a dynamic, ATR-based trigger to identify when prices have potentially peaked, setting the stage for a mean reversion short entry.

The optional EMA filter helps align trades with broader market trends, potentially reducing false signals.

Backtesting is recommended to fine-tune the ATR multiplier, smoothing period, and EMA settings to match the volatility and behavior of specific markets.