Hodrick-Prescott Structural CycleThis script is about solving one specific problem: Decomposition.

In any market, you have two things happening at once: the underlying "Trend" (the structural value) and the "Cycle" (the noise or volatility around that value). The Hodrick-Prescott (HP) filter is the standard econometric tool to separate them.

1. The Separation Logic (HP Filter)

Most moving averages lag. The HP filter attempts to find a smooth curve that represents the long-term path of the asset, minimizing the variance of the cycle.

In the code, the "stiffness" of this curve is controlled by Lambda ().

get_auto_lambda() =>

timeframe.isintraday ? 6250000 :

timeframe.isdaily ? 129600 :

1600

1600 is the standard used by economists for quarterly data. If the timeframe changes (daily or intraday), it automatically scales Lambda up to maintain that same "quarterly" smoothness on a faster chart.

2. The Mechanics (2-Pole Recursion)

The classic HP filter looks at future data, which is impossible for live trading. We uses a 2-Pole Super Smoother to approximate that curve using only past data.

hp_filter_2pole(src, period) =>

// ... coefficients calculated ...

var float filt = 0.0

filt := c1 * (src + nz(src )) / 2 + c2 * nz(filt ) + c3 * nz(filt )

See the filt and filt -> that's recursion. The filter references its own previous output. This creates memory, allowing the line to resist sudden spikes in price (noise) while slowly adapting to the true direction.

3. The Four Market Regimes

This script splits the market into four distinct quadrants based on where the Z-Score is and where it is going.

bool is_expansion = z_score > 0 and z_score > z_score

bool is_downturn = z_score > 0 and z_score < z_score

bool is_recovery = z_score < 0 and z_score > z_score

bool is_recession = z_score < 0 and z_score < z_score

1. Expansion (Green): We are above the trend, and momentum is accelerating.

2. Downturn (Orange): We are above the trend, but momentum is slowing (topping out).

3. Recession (Red): We are below the trend, and price is collapsing.

4. Recovery (Blue): We are below the trend, but price has stopped falling and is turning up.

The Background Zones: Statistical Extremes

This script monitors the Z-Score (the normalized cycle). When this score moves beyond 1.0 standard deviation from the mean (zero), the background lights up.

Red Background (Recession Zone): The Z-Score is < -1.0. Price is significantly below its structural trend. This is where fear is highest, and the asset is statistically "underwater."

Green Background (Overheating Zone): The Z-Score is > 1.0. Price is stretching far above the trend.

Why it matters: Markets rarely stay beyond 2.0 standard deviations for long. When you see the background colored, you are in an outlier event. (The rubber band is stretched)

Divergences: The "Check Engine" Light

It also scans for discrepancies between Price Action and the Cycle Momentum (Z-Score).

Bullish Divergence: Price makes a Lower Low, but the Cycle makes a Higher Low. The sellers are pushing price down, but with less conviction than before.

Bearish Divergence: Price makes a Higher High, but the Cycle makes a Lower High. Buyers are exhausted.

How to use this:

Do not treat a divergence tag as an entry signal.

A divergence is a state of discrepancy, not a timing trigger. It tells you that the prevailing trend is running out of steam.

"curve" için komut dosyalarını ara

4H HOD/LOD Checkpoint Analysis4H HOD/LOD Checkpoint Analysis - Detailed User Guide

OVERVIEW

This indicator is a data-driven probability framework for NQ Futures traders that predicts High-of-Day (HOD) and Low-of-Day (LOD) placement based on statistical analysis of 3,136+ trading days (2013-2025). Unlike traditional indicators that rely on technical signals, this tool uses checkpoint-based state analysis with zero forward-looking bias to provide real-time probabilities of whether the daily range is complete.

⚠️ IMPORTANT: This indicator is specifically designed for NQ FUTURES ONLY. All probabilities, patterns, and statistics were derived from a 10+ year historical dataset of NQ 1-minute bars. Using this on other instruments will produce inaccurate results.

CORE CONCEPT: CHECKPOINT METHODOLOGY

What is a Checkpoint?

A checkpoint occurs when a 4-hour candle closes. At this moment, the indicator "locks" the current market state and calculates probabilities for the remainder of the trading day. The key innovation is that state never changes after locking - probabilities remain constant throughout the session until the next checkpoint.

The Six 4-Hour Candles (EST):

6PM (18:00-22:00) - Evening/Globex open

10PM (22:00-02:00) - Asia session

2AM (02:00-06:00) - Early London

6AM (06:00-10:00) - Late London + NY Open

10AM (10:00-14:00) - NY Morning

2PM (14:00-17:00) - NY Afternoon (3 hours only)

Five Checkpoints:

10PM Checkpoint - After 6PM closes

2AM Checkpoint - After 10PM closes

6AM Checkpoint - After 2AM closes

10AM Checkpoint - After 6AM closes (most critical)

2PM Checkpoint - After 10AM closes (highest conviction fade signals)

HOW IT WORKS: THE THREE-FACTOR STATE SYSTEM

At each checkpoint, the indicator evaluates three critical factors to determine probability:

1. ELIMINATIONS (Quantity)

An "elimination" occurs when a candle trades beyond a previous candle's high or low, effectively removing that candle from contention for HOD/LOD.

Example at 10AM Checkpoint:

6PM high = 18,000

10PM high = 18,050 (eliminates 6PM high)

2AM high = 18,100 (eliminates 10PM high)

6AM high = 18,075 (does NOT eliminate 2AM high)

Result: 2 eliminations

The number of eliminations indicates trend strength:

0 eliminations = Range-bound, high probability extremes already set

1-2 eliminations = Moderate trend

3-4 eliminations = Strong trend day, range likely to extend

2. STRUCTURE (Pattern Type)

The indicator distinguishes between two elimination patterns:

Sequential: Eliminations occur in order (6pm → 10pm → 2am → 6am → 10am)

Indicates smooth, consistent trend

Example: 10pm eliminates 6pm, then 2am eliminates 10pm (sequential)

Skip: Eliminations skip candles

Indicates choppy/reversal behavior

Example: 2am eliminates 6pm but NOT 10pm (skip pattern)

Why it matters: Skip patterns show 2X probability differences compared to sequential patterns. At 10AM checkpoint with 2 eliminations, skip pattern shows 64% participation rate vs 36% for sequential pattern with previous survived.

3. PREVIOUS CANDLE STATUS

Did the immediately prior candle get eliminated?

Eliminated: Previous candle's high/low was taken out

Indicates relentless trend

Higher probability of continuation

Survived: Previous candle's high/low still intact

Indicates trend pause

Higher probability of mean reversion or range completion

Critical insight: High and low are tracked separately. At 2AM checkpoint, 10PM might have eliminated 6PM high (relentless uptrend) but NOT eliminated 6PM low (low survived). This creates different probabilities for HOD vs LOD.

VISUAL ELEMENTS

4-Hour Candle Boxes

Each 4H candle is displayed as a colored box showing its range:

Gray = 6PM (evening)

Blue = 10PM (Asia)

Purple = 2AM (early London)

Orange = 6AM (London + NY Open) - THE CURVE SESSION

Teal = 10AM (NY morning) - THE MONEY SESSION

Red = 2PM (NY afternoon) - THE FADE SESSION

HOD/LOD Lines

Black horizontal lines extend from current HOD/LOD with labels showing:

Which candle set the extreme

Current price level

THE CHECKPOINT TABLE EXPLAINED

Table Header:

Shows current checkpoint (e.g., "🎯 10AM CHECKPOINT") or "⏳ PRE-CHECKPOINT" if between checkpoints.

Main Metrics (Side-by-Side Comparison):

The table displays HOD and LOD separately in two columns because they can have different patterns:

METRIC

HODLOD Eliminations

Number of candles eliminated so far for highs

Number of candles eliminated so far for lows

Structure

Sequential or Skip pattern for highs

Sequential or Skip pattern for lows

Prev Candle

Was previous candle's high eliminated or did it survive?

Was previous candle's low eliminated or did it survive?

Pattern

Combined interpretation: Relentless/Paused/Skip/Early

Combined interpretation: Relentless/Paused/Skip/Early

Color Coding:

Structure Row:

White = Sequential (smooth trend)

Orange = Skip (choppy/reversal)

Previous Candle Row:

Red = Eliminated (relentless trend continuing)

Blue = Survived (trend paused)

Pattern Row:

Red = Relentless (previous eliminated + sequential = strong trend)

Blue = Paused (previous survived + sequential = trend pause)

Orange = Skip/Chop (skip pattern = reversal likely)

Gray = Early (0-1 eliminations, too early to tell)

Probability Section:

Prob Already In: Percentage chance that HOD/LOD has already been set

Color coding:

Green (>75%) = High confidence extreme is in, FADE

Yellow (45-75%) = Moderate confidence

Red (<45%) = Low confidence extreme is in, CONTINUATION likely

Sample Size: Shows how many historical occurrences match this exact state (n=XXX)

Larger samples = higher confidence

Most common states have n=500-2,000+

Current: Which candle currently holds HOD/LOD

Pattern Guide Section:

Appears when you have 2+ eliminations. Provides interpretation:

📈 Paused: Trend has paused, 2pm more likely to set extreme

📈 Relentless: Breaking higher/lower, continuation expected

📈 Skip/Chop: Choppy pattern, next session likely

Same for lows with 📉 symbol.

PRACTICAL TRADING EXAMPLES

Example 1: High Conviction Fade Setup

State at 10AM Checkpoint:

Eliminations: 0 (both HOD/LOD)

Structure: None (no eliminations yet)

Prev Candle: Survived

Table shows:

HOD Prob Already In: 68.9% (n=582)

LOD Prob Already In: 73.6% (n=785)

Interpretation: Range is likely complete. Fade extremes. With 0 eliminations and 70%+ probability, this is a high-conviction mean reversion signal.

Example 2: Strong Continuation Signal

State at 10AM Checkpoint:

Eliminations: 3 (both HOD/LOD)

Structure: Sequential

Prev Candle: Eliminated (relentless)

Table shows:

HOD Prob Already In: 29.8% (n=1,758)

LOD Prob Already In: 34.6% (n=1,451)

Pattern: 📈 Relentless / 📉 Relentless

Interpretation: Strong trend day. Only 30-35% chance range is complete. Look for breakouts in direction of trend. 10AM and 2PM likely to extend range.

Example 3: Pattern Structure Edge

State at 10AM Checkpoint:

Eliminations: 2 (HOD)

Structure: Skip (orange background)

Prev Candle: Eliminated vs Alternative State:

Eliminations: 2 (HOD)

Structure: Sequential

Prev Candle: Survived

Result: Skip pattern shows 64% chance 10AM participates vs 36% for sequential+survived. Skip pattern = 2X more likely to see 10AM high. This structural edge is unique to this indicator.

Example 4: Different HOD vs LOD Patterns

State at 10AM Checkpoint:

HOD: 2 eliminations, Sequential, Previous Eliminated (Relentless) = 46.7% in

LOD: 2 eliminations, Skip, Previous Eliminated (Choppy) = 48.4% in

Interpretation: Highs show relentless uptrend but lows show choppy behavior. This divergence suggests potential for upside continuation but with volatility. Not a clean trend day.

KEY CHECKPOINT STATISTICS (DERIVED FROM 10-YEAR DATASET)

10PM Checkpoint (After 6PM):

Very early in day

13.5% HOD in, 21.3% LOD in

Most likely outcome: Range extends into 6AM/10AM

2AM Checkpoint (After 10PM):

Still early

With 0 elims: 22-31% in (balanced)

With 1 elim: 8-12% in (strong trend signal)

6AM Checkpoint (After 2AM) - Critical Decision Point:

With 0 elims: 40-47% in (balanced, could go either way)

With 2 elims: 18-22% in (strong trend into 6AM/10AM)

Most likely outcome: 10AM sets extremes (~38-40%)

10AM Checkpoint (After 6AM) - Highest Conviction:

With 0 elims: 69-74% in → FADE (high confidence)

With 3 elims: 30-35% in → BUY/SELL continuation

This is THE money checkpoint for high-probability setups

2PM Checkpoint (After 10AM) - Maximum Fade Conviction:

With 0-3 elims: 67-95% in → FADE strongly

With 4 elims: 49-61% in (monster trend, weaker fade)

2PM is primarily a mean reversion session

UNDERSTANDING THE UNDERLYING DATA

All probabilities are derived from analysis of:

Instrument: NQ Futures (E-mini NASDAQ-100)

Timeframe: 1-minute bars

Period: January 2013 - December 2025

Sample: 3,136+ complete trading days

Methodology: Real-time checkpoint analysis with zero forward-looking bias

Why NQ-Specific?

Each futures contract has unique:

Session characteristics (6AM in NQ shows 60-64% curve behavior, other sessions differ)

Timing patterns (NQ's 10AM session has 67-74% immediate takeouts)

Volatility profiles (NQ 2PM shows 56% bullish bias vs ES shows different bias)

Using this indicator on ES, RTY, or other instruments will produce inaccurate results because the probability tables are NQ-specific.

ORIGINALITY & INNOVATION

What Makes This Indicator Unique:

Zero Forward-Looking Bias: State locks at checkpoint moments. Traditional indicators recalculate continuously, introducing bias. This indicator freezes probabilities at the exact moment a 4H candle closes.

Three-Factor State System: Combines elimination count, structure pattern, and previous candle status. Most indicators only track one dimension. This multi-factor approach provides 2X+ probability differentials.

Separate HOD/LOD Tracking: Highs and lows can have different patterns simultaneously (relentless high with choppy low). This indicator tracks them separately for precision.

Pattern Structure Analysis: Distinguishes between sequential and skip patterns, a concept not found in standard indicators. Skip patterns show mean reversion while sequential shows continuation.

10+ Year Statistical Foundation: Every probability is backed by hundreds to thousands of historical occurrences (sample sizes shown in table). Not based on theories or assumptions.

Checkpoint-Specific Probabilities: Different checkpoints have different probability profiles. 10AM checkpoint with 0 eliminations = 70%+ fade. 6AM checkpoint with same state = 40%+ fade. Context matters.

HOW TO USE THIS INDICATOR

Step 1: Wait for Checkpoint

The table will show "⏳ PRE-CHECKPOINT" until a 4H candle closes. Probabilities are only valid at checkpoint moments.

Step 2: Read the State

Check the three factors:

How many eliminations?

Sequential or skip?

Previous candle eliminated or survived?

Step 3: Check Probability

Look at "Prob Already In" percentage:

>75% (Green) = High confidence extreme is set, fade

45-75% (Yellow) = Moderate confidence, use other confirmation

<45% (Red) = Low confidence extreme is set, continuation likely

Step 4: Check Sample Size

Larger sample (n=1,000+) = higher confidence

Smaller sample (n=50-200) = use caution, edge is real but less robust

Step 5: Consider Pattern

Read the pattern guide:

Relentless = trend continuing

Paused = trend stalled, mean reversion

Skip/Chop = reversal/range likely

Step 6: Compare HOD vs LOD

If both show similar patterns = cleaner signal

If divergent patterns = complex day, be cautious

BEST PRACTICES

Focus on 10AM and 2PM checkpoints - These have the highest conviction signals

Combine with price action - Don't fade blindly at 90% probability if price is breaking out strongly

Larger samples = better edges - Prioritize setups with n=500+

Watch for pattern divergence - When HOD and LOD show different patterns, expect complexity

Remember session characteristics:

6AM = THE CURVE SESSION (60-64% mean reversion when Q2 breaks Q1)

10AM = THE MONEY SESSION (67-74% immediate takeouts, highest conviction)

2PM = THE FADE SESSION (67-95% extremes already in)

SETTINGS

Show 4H Candle Boxes - Display colored boxes for each 4H candle

Show HOD/LOD Lines - Display horizontal lines at current extremes

Show Checkpoint Analysis - Display probability table

Table Position - Choose where to place the checkpoint table

Table Size - Tiny/Small/Normal

Colors - Customize box colors for each session

LIMITATIONS & DISCLAIMERS

NQ FUTURES ONLY - Do not use on other instruments

Not a standalone system - Use as confluence with your strategy

Historical data - Past performance doesn't guarantee future results

Sample size variance - Some states have smaller samples, use judgment

Requires understanding - Read this guide fully before trading with this tool

FINAL NOTES

This indicator represents 10+ years of NQ futures data distilled into actionable, real-time probabilities. The checkpoint methodology ensures zero forward-looking bias, while the three-factor state system provides granular edge that traditional indicators miss.

Remember: This tool provides probabilities, not certainties. Trade with proper risk management, and use this as one input in your decision-making process.

Hyper Insight MA Strategy [Universal]Hyper Insight MA Strategy ** is a comprehensive trend-following engine designed for traders who require precision and flexibility. Unlike standard indicators that lock you into a single calculation method, this strategy serves as a "Universal Adapter," allowing you to **Mix & Match 13 different Moving Average types** for both the Fast and Slow trend lines independently.

Whether you need the smoothness of T3, the responsiveness of HMA, or the classic reliability of SMA, this script enables you to backtest thousands of combinations to find the perfect edge for your specific asset class.

---

🔬 Deep Dive: Calculation Logic of Included MAs

This strategy includes 13 distinct calculation methods. Understanding the math behind them will help you choose the right tool for your specific market conditions.

#### 1. Standard Averages

* **SMA (Simple Moving Average):** The unweighted mean of the previous $n$ data points.

* *Logic:* Treats every price point in the period with equal importance. Good for identifying long-term macro trends but reacts slowly to recent volatility.

* **WMA (Weighted Moving Average):** A linear weighted average.

* *Logic:* Assigns heavier weight to current data linearly (e.g., $1, 2, 3... n$). It reacts faster than SMA but is still relatively smooth.

* **SWMA (Symmetrically Weighted Moving Average):**

* *Logic:* Uses a fixed-length window (usually 4 bars) with symmetrical weights $ $. It prioritizes the center of the recent data window.

#### 2. Exponential & Lag-Reducing Averages

* **EMA (Exponential Moving Average):**

* *Logic:* Applies an exponential decay weighting factor. Recent prices have significantly more impact on the average than older prices, reducing lag compared to SMA.

* **RMA (Running Moving Average):** Also known as Wilder's Smoothing (used in RSI).

* *Logic:* It is essentially an EMA but with a slower alpha weight of $1/length$. It provides a very smooth, stable line that filters out noise effectively.

* **DEMA (Double Exponential Moving Average):**

* *Logic:* Calculated as $2 \times EMA - EMA(EMA)$. By subtracting the "lag" (the smoothed EMA) from the original EMA, DEMA provides a much faster reaction to price changes with less noise than a standard EMA.

* **TEMA (Triple Exponential Moving Average):**

* *Logic:* Calculated as $3 \times EMA - 3 \times EMA(EMA) + EMA(EMA(EMA))$. This effectively eliminates the lag inherent in single and double EMAs, making it an extremely fast-tracking indicator for scalping.

#### 3. Advanced & Adaptive Averages

* **HMA (Hull Moving Average):**

* *Logic:* A composite formula involving Weighted Moving Averages: ASX:WMA (2 \times Integer(n/2)) - WMA(n)$. The result is then smoothed by a $\sqrt{n}$ WMA.

* *Effect:* It eliminates lag almost entirely while managing to improve curve smoothness, solving the traditional trade-off between speed and noise.

* **ZLEMA (Zero Lag Exponential Moving Average):**

* *Logic:* This calculation attempts to remove lag by modifying the data source before smoothing. It calculates a "lag" value $(length-1)/2$ and applies an EMA to the data: $Source + (Source - Source )$. This creates a projection effect that tracks price tightly.

* **T3 (Tillson T3 Moving Average):**

* *Logic:* A complex smoothing technique that runs an EMA through a filter multiple times using a "Volume Factor" (set to 0.7 in this script).

* *Effect:* It produces a curve that is incredibly smooth and free of "overshoot," making it excellent for filtering out market chop.

* **ALMA (Arnaud Legoux Moving Average):**

* *Logic:* Uses a Gaussian distribution (bell curve) to assign weights. It allows the user to offset the moving average (moving the peak of the weight) to align it perfectly with the price, balancing smoothness and responsiveness.

* **LSMA (Least Squares Moving Average):**

* *Logic:* Calculates the endpoint of a Linear Regression line for the lookback period. It essentially guesses where the price "should" be based on the best-fit line of the recent trend.

* **VWMA (Volume Weighted Moving Average):**

* *Logic:* Weights the closing price by the volume of that bar.

* *Effect:* Prices on high volume days pull the MA harder than prices on low volume days. This is excellent for validating true trend strength (i.e., a breakout on high volume will move the VWMA significantly).

---

### 🛠 Features & Settings

* **Universal Switching:** Change the `Fast MA` and `Slow MA` types instantly via the settings menu.

* **Trend Cloud:** A dynamic background fill (Green/Red) highlights the crossover zone for immediate visual trend identification.

* **Strategy Mode:** Built-in Backtesting logic triggers `LONG` entries when Fast MA crosses over Slow MA, and `EXIT` when Fast MA crosses under.

### ⚠️ Disclaimer

This script is intended for educational and research purposes. The wide variety of MA combinations can produce vastly different results. Past performance is not indicative of future results. Please use proper risk management.

UM VIX30/VIX Regime & Volatility Roll Yield

SUMMARY

A front-of-the-curve volatility indicator that compares spot VIX to a synthetic 30-day VIX (VIX30) built from VX1/VX2 futures, revealing early volatility pressure, regime shifts, and roll-yield transitions. Ideal for timing long/short volatility trades in VXX, UVXY, SVIX, and VIX futures.

DESCRIPTION

This indicator compares spot VIX to a synthetic 30-day constant-maturity volatility estimate (“VIX30”) built from VX1 and VX2 futures. The VIX30/VIX Ratio reveals short-term volatility pressure and regime shifts that traditional VX1/VX2 roll-yield alone often misses.

VIX30 is constructed using true calendar-day interpolation between VX1 and VX2, with VX1% and VX2% showing the real-time weights behind the 30-day volatility anchor. The table displays the volatility regime, the VX1/VX2 weights, spot-term roll yield (VIX30/VIX), and futures-term roll yield (VX2/VX1), giving a complete, front-of-the-curve perspective on volatility dynamics.

Use this to spot early volatility expansions, collapsing contango, and regime transitions that influence VXX, UVXY, SVIX, VX options, and VIX futures.

HOW IT WORKS

The script calculates the exact calendar days to expiration for the front two VIX futures. It then applies linear interpolation to blend VX1 and VX2 into a 30-day constant-maturity synthetic volatility measure (“VIX30”). Comparing VIX30 to spot VIX produces the VIX30/VIX Ratio, which highlights short-term volatility pressure and regime direction. A full term-structure table summarizes regime, VX1%/VX2% weights, and both spot-term and futures-term roll yields.

DEFAULT SETTINGS

VX1! and VX2! are used by default for front-month and second-month futures. These may be manually overridden if TradingView rolls contracts early. The default timeframe is 30 minutes, and the VIX30/VIX Ratio uses a 21-period EMA for regime smoothing. The historical threshold is set to 1.08, reflecting the long-run average relationship between VIX30 and VIX.

SUGGESTED USES

• Identify early volatility expansions before they appear in VX1/VX2 roll yield.

• Confirm contango/backwardation shifts with front-of-curve context.

• Time long/short volatility trades in VXX, UVXY, SVIX, and VX options.

• Monitor regime transitions (Low → Cautionary → High) to anticipate trend inflections.

• Combine with price action, Nadaraya-Watson trends, or MA color-flip systems for higher-confidence entries.

• MA red → green flips may signal opportunities to short volatility or increase equity exposure.

• MA green → red flips may signal opportunities to go long volatility, reduce equity exposure, or take short-equity positions.

ALERTS

Alerts trigger when the ratio crosses above or below the historical threshold or when the moving-average slope flips direction. A green flip signals rising volatility pressure; a red flip signals fading or collapsing volatility. These alert conditions can be used to automate long/short volatility bias shifts or trade-entry notifications.

FURTHER HINTS

• Increasing orange/red in the table suggests an emerging higher-volatility environment.

• SVIX (inverse volatility ETF) can trend strongly when volatility decays; on a 6-hour chart, MA green flips often align with attractive short-volatility opportunities.

• For long-volatility trades, consider shrinking to a 30-minute chart and watching for MA green → red flips as early entry cues.

• Experiment with different timeframes and smoothing lengths to match your trading style.

• Higher VIX30/VIX and VX2/VX1 roll yields generally imply faster decay in VXX, UVXY, and UVIX — or stronger upside momentum in SVIX.

• The author likes the 6-hour chart for short vol, and the 30-minute chart for long vol. Long vol trades are fast and furious so you want to be quick.

NEURAL FLOW INDEX — Core Energy • Momentum Stream • Pulse SyncNeural Flow Index (NFI) — Advanced Triple-Layer Reversal Framework

The Neural Flow Index (NFI) is a next-generation market oscillator designed to reveal the hidden synchronization between trend energy, cyclical momentum, and internal pulse dynamics.

It merges three powerful analytical layers into a single, normalized view:

Core Energy Curve (based on RSO logic) — captures structural trend bias and volatility expansion.

Momentum Stream (WaveTrend algorithm) — visualizes cyclical motion of price waves.

Pulse Sync (Stochastic RSI adaptation) — measures short-term momentum rhythm and overextension.

Each layer feeds into a unified flow model that adapts to both trend-following and reversal conditions. The goal is not to chase every fluctuation, but to sense where momentum, direction, and volatility converge into true inflection points.

Conceptual Mechanics

The oscillator translates complex market behavior into an elegant, multi-phase signal system:

Core Energy Curve (RSO foundation):

A smoothed dynamic field representing the overall strength and direction of market pressure.

Green energy indicates expansion (bullish dominance); red energy reflects contraction (bearish decay).

Momentum Stream (WaveTrend):

The teal line functions like an electro-wave, oscillating through phases of expansion and exhaustion.

It provides the heartbeat of the market — smooth, rhythmic, and beautifully cyclic.

Pulse Sync (Stochastic RSI):

The purple line acts as the market’s nervous pulse, reacting to micro-momentum changes before the larger trend adjusts.

It identifies micro-tops and micro-bottoms that precede major trend shifts.

When these three forces align, they create high-probability reversal zones known as Neural Nodes — regions where energy, momentum, and rhythm converge.

Trading Logic

Potential Entry Zones:

When the purple Pulse Sync line crosses the green Momentum Stream near the lower or upper bounds of the oscillator, a potential turning point forms.

Yet, these crossovers are only validated when the Core Energy histogram (RSO) simultaneously supports the same direction — confirming that energy and rhythm are synchronized.

Histogram Confirmation:

The histogram is the “voice” of the oscillator.

Rising green volume within the histogram during a Pulse-Momentum crossover suggests a legitimate upward reversal.

Conversely, expanding red energy during an upper-band cross indicates momentum exhaustion and an early short-side opportunity.

Neutral Zones:

When all three layers flatten near the zero line, the market enters an equilibrium phase — no clear trend dominance, ideal for patience and re-entry planning.

| Layer | Representation | Color | Function |

| --------------------- | ------------------- | ----------------- | ------------------------------ |

| **Core Energy Curve** | Area / Histogram | Lime-Red gradient | Trend bias & volatility energy |

| **Momentum Stream** | WaveTrend line | Teal | Cyclical flow of price |

| **Pulse Sync** | Stochastic RSI line | Purple | Short-term momentum rhythm |

Interpretation Summary

Converging Waves: Trend, momentum, and pulse move together → strong continuation.

Diverging Waves: Pulse or Momentum decouple from Core Energy → early reversal warnings.

Histogram Expansion: Confirms direction and strength of the new wave.

Crossovers at Extremes: Potential entries, especially when confirmed by energy alignment.

🪶 Philosophy Behind NFI

The Neural Flow Index is not just a technical indicator — it’s a behavioral visualization system.

Instead of focusing on lagging confirmations, it captures the neural pattern of price motion:

how liquidity flows, contracts, and expands through time.

It bridges the gap between pure mathematics and market intuition — giving traders a cinematic, harmonic view of energy transition inside price structure.

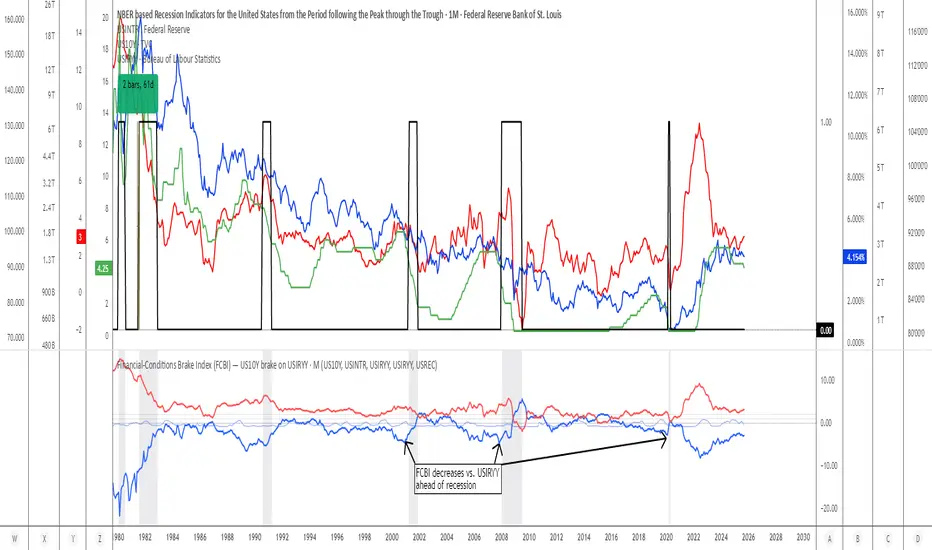

Financial-Conditions Brake Index (FCBI) — US10Y brake on USIRYYFinancial-Conditions Brake Index (FCBI) – US10Y Brake on USIRYY

Concept

The Financial-Conditions Brake Index (FCBI) measures how U.S. long-term yields (US10Y) interact with the Federal Funds Rate (USINTR) and inflation (CPI YoY) to shape real-rate conditions (USIRYY).

It visualizes whether the bond market is tightening or loosening overall financial conditions relative to the Federal Reserve’s policy stance.

Formula

FCBI = (US10Y) − (USINTR) − (CPI YoY)

How It Works

The FCBI expresses the difference between the long-term yield curve and short-term policy rates, adjusted for inflation. It shows whether the long end of the curve is amplifying or counteracting the Fed’s stance.

FCBI > +2 → Strong brake → Long yields remain elevated despite easing → tight conditions → recession delayed.

FCBI +1 to +2 → Mild brake → Financial transmission slower; lag ≈ 12–18 months.

FCBI 0 to +1 → Neutral → Typical early post-cut environment.

FCBI < 0 → Accelerator → Long yields and inflation expectations falling → liquidity flows freely → recession often follows within 6–14 months.

How to Read the Chart

Blue line (FCBI) shows the strength of the financial brake.

Red line (USIRYY) represents the real yield baseline.

Recession shading (gray) marks NBER recessions for comparison.

FCBI < USIRYY → Brake engaged → financial conditions tighter than real-rate baseline.

FCBI > USIRYY → Brake released → long end easing faster than policy → liquidity surge → late-cycle setup.

Historically, U.S. recessions begin on average about 14 months after the first Fed rate cut, and a decline of the FCBI below zero often precedes that window.

Practical Use

Use the FCBI to identify when policy transmission is blocked (brake engaged) or flowing (brake released).

Cross-check with yield-curve inversions, Fed policy shifts, and inflation expectations to estimate macro timing windows.

Current Example (Oct 2025)

FCBI ≈ −3.1, USIRYY ≈ +3.0 → Brake still engaged.

Once FCBI rises above USIRYY and crosses positive, it signals the “brake released” phase — historically the final liquidity surge before a U.S. recession.

Summary

FCBI shows how tight the brake is.

USIRYY shows how fast the car is moving.

When FCBI rises above USIRYY, the brake is released — liquidity accelerates and the historical recession countdown begins.

Chart Fusion Line SND Detection by TitikSona🧭 Overview

Fusion Line Momentum Analyzer is a momentum visualization tool that introduces a unified model of oscillator fusion.

It blends Fast and Slow Stochastics with RSI into one adaptive curve, designed to eliminate conflicting signals between different momentum sources.

Instead of reading three separate oscillators, the Fusion Line provides a consolidated view of strength and exhaustion zones in a single framework.

This approach helps analysts detect aligned momentum shifts with greater clarity and less noise, without repainting or lagging methods.

⚙️ Core Concept

Traditional oscillators often provide conflicting readings when volatility changes.

To solve this, the Fusion Line averages three normalized components:

Fast Stochastic (12,3,3) — reacts quickly to short-term momentum spikes.

Slow Stochastic (100,8,8) — filters long-term momentum context.

RSI (26) — measures internal strength between buying and selling pressure.

Each is rescaled to a 0–100 range, then averaged into a single curve called the Fusion Line.

A secondary Signal Line (SMA 9) is added to visualize directional confirmation.

This combination aims to preserve responsiveness from the fast components while maintaining structural stability from the slow and RSI layers.

🌈 Features

Unified momentum curve combining stochastic and RSI dynamics.

Automatic bias shading to highlight dominant trend direction.

Real-time percentage strength meter (visual intensity).

Configurable alert triggers on key momentum zones (20/80).

Clean chart display without unnecessary elements or overlays.

📘 Interpretation

Rising Fusion Line → indicates strengthening bullish momentum.

Falling Fusion Line → indicates strengthening bearish pressure.

Fusion values below 20 → potential oversold recovery.

Fusion values above 80 → possible exhaustion or reversal zone.

Mid-zone movement → reflects equilibrium or sideways momentum.

These readings should always be combined with higher timeframe structure or volume confirmation for context.

⚙️ Default Parameters

Fast Stochastic (12,3,3)

Slow Stochastic (100,8,8)

RSI Length (26)

Signal Line Smoothing (9)

All values can be adjusted to adapt to asset volatility or timeframe conditions.

⚠️ Disclaimer

This indicator is a research and visualization tool, not a signal generator.

It does not predict price movement or guarantee performance.

Use for analytical purposes only and combine with your own trading framework.

👨💻 Developer

Created by TitikSona — Research & Fusion Concept Designer

Built using Pine Script v6

Type: Open-source educational script

💬 Short Description

Fusion-based momentum visualization combining Double Stochastic and RSI into one adaptive line for clearer, noise-free momentum analysis.

Keltner Channel Enhanced [DCAUT]█ Keltner Channel Enhanced

📊 ORIGINALITY & INNOVATION

The Keltner Channel Enhanced represents an important advancement over standard Keltner Channel implementations by introducing dual flexibility in moving average selection for both the middle band and ATR calculation. While traditional Keltner Channels typically use EMA for the middle band and RMA (Wilder's smoothing) for ATR, this enhanced version provides access to 25+ moving average algorithms for both components, enabling traders to fine-tune the indicator's behavior to match specific market characteristics and trading approaches.

Key Advancements:

Dual MA Algorithm Flexibility: Independent selection of moving average types for middle band (25+ options) and ATR smoothing (25+ options), allowing optimization of both trend identification and volatility measurement separately

Enhanced Trend Sensitivity: Ability to use faster algorithms (HMA, T3) for middle band while maintaining stable volatility measurement with traditional ATR smoothing, or vice versa for different trading strategies

Adaptive Volatility Measurement: Choice of ATR smoothing algorithm affects channel responsiveness to volatility changes, from highly reactive (SMA, EMA) to smoothly adaptive (RMA, TEMA)

Comprehensive Alert System: Five distinct alert conditions covering breakouts, trend changes, and volatility expansion, enabling automated monitoring without constant chart observation

Multi-Timeframe Compatibility: Works effectively across all timeframes from intraday scalping to long-term position trading, with independent optimization of trend and volatility components

This implementation addresses key limitations of standard Keltner Channels: fixed EMA/RMA combination may not suit all market conditions or trading styles. By decoupling the trend component from volatility measurement and allowing independent algorithm selection, traders can create highly customized configurations for specific instruments and market phases.

📐 MATHEMATICAL FOUNDATION

Keltner Channel Enhanced uses a three-component calculation system that combines a flexible moving average middle band with ATR-based (Average True Range) upper and lower channels, creating volatility-adjusted trend-following bands.

Core Calculation Process:

1. Middle Band (Basis) Calculation:

The basis line is calculated using the selected moving average algorithm applied to the price source over the specified period:

basis = ma(source, length, maType)

Supported algorithms include EMA (standard choice, trend-biased), SMA (balanced and symmetric), HMA (reduced lag), WMA, VWMA, TEMA, T3, KAMA, and 17+ others.

2. Average True Range (ATR) Calculation:

ATR measures market volatility by calculating the average of true ranges over the specified period:

trueRange = max(high - low, abs(high - close ), abs(low - close ))

atrValue = ma(trueRange, atrLength, atrMaType)

ATR smoothing algorithm significantly affects channel behavior, with options including RMA (standard, very smooth), SMA (moderate smoothness), EMA (fast adaptation), TEMA (smooth yet responsive), and others.

3. Channel Calculation:

Upper and lower channels are positioned at specified multiples of ATR from the basis:

upperChannel = basis + (multiplier × atrValue)

lowerChannel = basis - (multiplier × atrValue)

Standard multiplier is 2.0, providing channels that dynamically adjust width based on market volatility.

Keltner Channel vs. Bollinger Bands - Key Differences:

While both indicators create volatility-based channels, they use fundamentally different volatility measures:

Keltner Channel (ATR-based):

Uses Average True Range to measure actual price movement volatility

Incorporates gaps and limit moves through true range calculation

More stable in trending markets, less prone to extreme compression

Better reflects intraday volatility and trading range

Typically fewer band touches, making touches more significant

More suitable for trend-following strategies

Bollinger Bands (Standard Deviation-based):

Uses statistical standard deviation to measure price dispersion

Based on closing prices only, doesn't account for intraday range

Can compress significantly during consolidation (squeeze patterns)

More touches in ranging markets

Better suited for mean-reversion strategies

Provides statistical probability framework (95% within 2 standard deviations)

Algorithm Combination Effects:

The interaction between middle band MA type and ATR MA type creates different indicator characteristics:

Trend-Focused Configuration (Fast MA + Slow ATR): Middle band uses HMA/EMA/T3, ATR uses RMA/TEMA, quick trend changes with stable channel width, suitable for trend-following

Volatility-Focused Configuration (Slow MA + Fast ATR): Middle band uses SMA/WMA, ATR uses EMA/SMA, stable trend with dynamic channel width, suitable for volatility trading

Balanced Configuration (Standard EMA/RMA): Classic Keltner Channel behavior, time-tested combination, suitable for general-purpose trend following

Adaptive Configuration (KAMA + KAMA): Self-adjusting indicator responding to efficiency ratio, suitable for markets with varying trend strength and volatility regimes

📊 COMPREHENSIVE SIGNAL ANALYSIS

Keltner Channel Enhanced provides multiple signal categories optimized for trend-following and breakout strategies.

Channel Position Signals:

Upper Channel Interaction:

Price Touching Upper Channel: Strong bullish momentum, price moving more than typical volatility range suggests, potential continuation signal in established uptrends

Price Breaking Above Upper Channel: Exceptional strength, price exceeding normal volatility expectations, consider adding to long positions or tightening trailing stops

Price Riding Upper Channel: Sustained strong uptrend, characteristic of powerful bull moves, stay with trend and avoid premature profit-taking

Price Rejection at Upper Channel: Momentum exhaustion signal, consider profit-taking on longs or waiting for pullback to middle band for reentry

Lower Channel Interaction:

Price Touching Lower Channel: Strong bearish momentum, price moving more than typical volatility range suggests, potential continuation signal in established downtrends

Price Breaking Below Lower Channel: Exceptional weakness, price exceeding normal volatility expectations, consider adding to short positions or protecting against further downside

Price Riding Lower Channel: Sustained strong downtrend, characteristic of powerful bear moves, stay with trend and avoid premature covering

Price Rejection at Lower Channel: Momentum exhaustion signal, consider covering shorts or waiting for bounce to middle band for reentry

Middle Band (Basis) Signals:

Trend Direction Confirmation:

Price Above Basis: Bullish trend bias, middle band acts as dynamic support in uptrends, consider long positions or holding existing longs

Price Below Basis: Bearish trend bias, middle band acts as dynamic resistance in downtrends, consider short positions or avoiding longs

Price Crossing Above Basis: Potential trend change from bearish to bullish, early signal to establish long positions

Price Crossing Below Basis: Potential trend change from bullish to bearish, early signal to establish short positions or exit longs

Pullback Trading Strategy:

Uptrend Pullback: Price pulls back from upper channel to middle band, finds support, and resumes upward, ideal long entry point

Downtrend Bounce: Price bounces from lower channel to middle band, meets resistance, and resumes downward, ideal short entry point

Basis Test: Strong trends often show price respecting the middle band as support/resistance on pullbacks

Failed Test: Price breaking through middle band against trend direction signals potential reversal

Volatility-Based Signals:

Narrow Channels (Low Volatility):

Consolidation Phase: Channels contract during periods of reduced volatility and directionless price action

Breakout Preparation: Narrow channels often precede significant directional moves as volatility cycles

Trading Approach: Reduce position sizes, wait for breakout confirmation, avoid range-bound strategies within channels

Breakout Direction: Monitor for price breaking decisively outside channel range with expanding width

Wide Channels (High Volatility):

Trending Phase: Channels expand during strong directional moves and increased volatility

Momentum Confirmation: Wide channels confirm genuine trend with substantial volatility backing

Trading Approach: Trend-following strategies excel, wider stops necessary, mean-reversion strategies risky

Exhaustion Signs: Extreme channel width (historical highs) may signal approaching consolidation or reversal

Advanced Pattern Recognition:

Channel Walking Pattern:

Upper Channel Walk: Price consistently touches or exceeds upper channel while staying above basis, very strong uptrend signal, hold longs aggressively

Lower Channel Walk: Price consistently touches or exceeds lower channel while staying below basis, very strong downtrend signal, hold shorts aggressively

Basis Support/Resistance: During channel walks, price typically uses middle band as support/resistance on minor pullbacks

Pattern Break: Price crossing basis during channel walk signals potential trend exhaustion

Squeeze and Release Pattern:

Squeeze Phase: Channels narrow significantly, price consolidates near middle band, volatility contracts

Direction Clues: Watch for price positioning relative to basis during squeeze (above = bullish bias, below = bearish bias)

Release Trigger: Price breaking outside narrow channel range with expanding width confirms breakout

Follow-Through: Measure squeeze height and project from breakout point for initial profit targets

Channel Expansion Pattern:

Breakout Confirmation: Rapid channel widening confirms volatility increase and genuine trend establishment

Entry Timing: Enter positions early in expansion phase before trend becomes overextended

Risk Management: Use channel width to size stops appropriately, wider channels require wider stops

Basis Bounce Pattern:

Clean Bounce: Price touches middle band and immediately reverses, confirms trend strength and entry opportunity

Multiple Bounces: Repeated basis bounces indicate strong, sustainable trend

Bounce Failure: Price penetrating basis signals weakening trend and potential reversal

Divergence Analysis:

Price/Channel Divergence: Price makes new high/low while staying within channel (not reaching outer band), suggests momentum weakening

Width/Price Divergence: Price breaks to new extremes but channel width contracts, suggests move lacks conviction

Reversal Signal: Divergences often precede trend reversals or significant consolidation periods

Multi-Timeframe Analysis:

Keltner Channels work particularly well in multi-timeframe trend-following approaches:

Three-Timeframe Alignment:

Higher Timeframe (Weekly/Daily): Identify major trend direction, note price position relative to basis and channels

Intermediate Timeframe (Daily/4H): Identify pullback opportunities within higher timeframe trend

Lower Timeframe (4H/1H): Time precise entries when price touches middle band or lower channel (in uptrends) with rejection

Optimal Entry Conditions:

Best Long Entries: Higher timeframe in uptrend (price above basis), intermediate timeframe pulls back to basis, lower timeframe shows rejection at middle band or lower channel

Best Short Entries: Higher timeframe in downtrend (price below basis), intermediate timeframe bounces to basis, lower timeframe shows rejection at middle band or upper channel

Risk Management: Use higher timeframe channel width to set position sizing, stops below/above higher timeframe channels

🎯 STRATEGIC APPLICATIONS

Keltner Channel Enhanced excels in trend-following and breakout strategies across different market conditions.

Trend Following Strategy:

Setup Requirements:

Identify established trend with price consistently on one side of basis line

Wait for pullback to middle band (basis) or brief penetration through it

Confirm trend resumption with price rejection at basis and move back toward outer channel

Enter in trend direction with stop beyond basis line

Entry Rules:

Uptrend Entry:

Price pulls back from upper channel to middle band, shows support at basis (bullish candlestick, momentum divergence)

Enter long on rejection/bounce from basis with stop 1-2 ATR below basis

Aggressive: Enter on first touch; Conservative: Wait for confirmation candle

Downtrend Entry:

Price bounces from lower channel to middle band, shows resistance at basis (bearish candlestick, momentum divergence)

Enter short on rejection/reversal from basis with stop 1-2 ATR above basis

Aggressive: Enter on first touch; Conservative: Wait for confirmation candle

Trend Management:

Trailing Stop: Use basis line as dynamic trailing stop, exit if price closes beyond basis against position

Profit Taking: Take partial profits at opposite channel, move stops to basis

Position Additions: Add to winners on subsequent basis bounces if trend intact

Breakout Strategy:

Setup Requirements:

Identify consolidation period with contracting channel width

Monitor price action near middle band with reduced volatility

Wait for decisive breakout beyond channel range with expanding width

Enter in breakout direction after confirmation

Breakout Confirmation:

Price breaks clearly outside channel (upper for longs, lower for shorts), channel width begins expanding from contracted state

Volume increases significantly on breakout (if using volume analysis)

Price sustains outside channel for multiple bars without immediate reversal

Entry Approaches:

Aggressive: Enter on initial break with stop at opposite channel or basis, use smaller position size

Conservative: Wait for pullback to broken channel level, enter on rejection and resumption, tighter stop

Volatility-Based Position Sizing:

Adjust position sizing based on channel width (ATR-based volatility):

Wide Channels (High ATR): Reduce position size as stops must be wider, calculate position size using ATR-based risk calculation: Risk / (Stop Distance in ATR × ATR Value)

Narrow Channels (Low ATR): Increase position size as stops can be tighter, be cautious of impending volatility expansion

ATR-Based Risk Management: Use ATR-based risk calculations, position size = 0.01 × Capital / (2 × ATR), use multiples of ATR (1-2 ATR) for adaptive stops

Algorithm Selection Guidelines:

Different market conditions benefit from different algorithm combinations:

Strong Trending Markets: Middle band use EMA or HMA, ATR use RMA, capture trends quickly while maintaining stable channel width

Choppy/Ranging Markets: Middle band use SMA or WMA, ATR use SMA or WMA, avoid false trend signals while identifying genuine reversals

Volatile Markets: Middle band and ATR both use KAMA or FRAMA, self-adjusting to changing market conditions reduces manual optimization

Breakout Trading: Middle band use SMA, ATR use EMA or SMA, stable trend with dynamic channels highlights volatility expansion early

Scalping/Day Trading: Middle band use HMA or T3, ATR use EMA or TEMA, both components respond quickly

Position Trading: Middle band use EMA/TEMA/T3, ATR use RMA or TEMA, filter out noise for long-term trend-following

📋 DETAILED PARAMETER CONFIGURATION

Understanding and optimizing parameters is essential for adapting Keltner Channel Enhanced to specific trading approaches.

Source Parameter:

Close (Most Common): Uses closing price, reflects daily settlement, best for end-of-day analysis and position trading, standard choice

HL2 (Median Price): Smooths out closing bias, better represents full daily range in volatile markets, good for swing trading

HLC3 (Typical Price): Gives more weight to close while including full range, popular for intraday applications, slightly more responsive than HL2

OHLC4 (Average Price): Most comprehensive price representation, smoothest option, good for gap-prone markets or highly volatile instruments

Length Parameter:

Controls the lookback period for middle band (basis) calculation:

Short Periods (10-15): Very responsive to price changes, suitable for day trading and scalping, higher false signal rate

Standard Period (20 - Default): Represents approximately one month of trading, good balance between responsiveness and stability, suitable for swing and position trading

Medium Periods (30-50): Smoother trend identification, fewer false signals, better for position trading and longer holding periods

Long Periods (50+): Very smooth, identifies major trends only, minimal false signals but significant lag, suitable for long-term investment

Optimization by Timeframe: 1-15 minute charts use 10-20 period, 30-60 minute charts use 20-30 period, 4-hour to daily charts use 20-40 period, weekly charts use 20-30 weeks.

ATR Length Parameter:

Controls the lookback period for Average True Range calculation, affecting channel width:

Short ATR Periods (5-10): Very responsive to recent volatility changes, standard is 10 (Keltner's original specification), may be too reactive in whipsaw conditions

Standard ATR Period (10 - Default): Chester Keltner's original specification, good balance between responsiveness and stability, most widely used

Medium ATR Periods (14-20): Smoother channel width, ATR 14 aligns with Wilder's original ATR specification, good for position trading

Long ATR Periods (20+): Very smooth channel width, suitable for long-term trend-following

Length vs. ATR Length Relationship: Equal values (20/20) provide balanced responsiveness, longer ATR (20/14) gives more stable channel width, shorter ATR (20/10) is standard configuration, much shorter ATR (20/5) creates very dynamic channels.

Multiplier Parameter:

Controls channel width by setting ATR multiples:

Lower Values (1.0-1.5): Tighter channels with frequent price touches, more trading signals, higher false signal rate, better for range-bound and mean-reversion strategies

Standard Value (2.0 - Default): Chester Keltner's recommended setting, good balance between signal frequency and reliability, suitable for both trending and ranging strategies

Higher Values (2.5-3.0): Wider channels with less frequent touches, fewer but potentially higher-quality signals, better for strong trending markets

Market-Specific Optimization: High volatility markets (crypto, small-caps) use 2.5-3.0 multiplier, medium volatility markets (major forex, large-caps) use 2.0 multiplier, low volatility markets (bonds, utilities) use 1.5-2.0 multiplier.

MA Type Parameter (Middle Band):

Critical selection that determines trend identification characteristics:

EMA (Exponential Moving Average - Default): Standard Keltner Channel choice, Chester Keltner's original specification, emphasizes recent prices, faster response to trend changes, suitable for all timeframes

SMA (Simple Moving Average): Equal weighting of all data points, no directional bias, slower than EMA, better for ranging markets and mean-reversion

HMA (Hull Moving Average): Minimal lag with smooth output, excellent for fast trend identification, best for day trading and scalping

TEMA (Triple Exponential Moving Average): Advanced smoothing with reduced lag, responsive to trends while filtering noise, suitable for volatile markets

T3 (Tillson T3): Very smooth with minimal lag, excellent for established trend identification, suitable for position trading

KAMA (Kaufman Adaptive Moving Average): Automatically adjusts speed based on market efficiency, slow in ranging markets, fast in trends, suitable for markets with varying conditions

ATR MA Type Parameter:

Determines how Average True Range is smoothed, affecting channel width stability:

RMA (Wilder's Smoothing - Default): J. Welles Wilder's original ATR smoothing method, very smooth, slow to adapt to volatility changes, provides stable channel width

SMA (Simple Moving Average): Equal weighting, moderate smoothness, faster response to volatility changes than RMA, more dynamic channel width

EMA (Exponential Moving Average): Emphasizes recent volatility, quick adaptation to new volatility regimes, very responsive channel width changes

TEMA (Triple Exponential Moving Average): Smooth yet responsive, good balance for varying volatility, suitable for most trading styles

Parameter Combination Strategies:

Conservative Trend-Following: Length 30/ATR Length 20/Multiplier 2.5, MA Type EMA or TEMA/ATR MA Type RMA, smooth trend with stable wide channels, suitable for position trading

Standard Balanced Approach: Length 20/ATR Length 10/Multiplier 2.0, MA Type EMA/ATR MA Type RMA, classic Keltner Channel configuration, suitable for general purpose swing trading

Aggressive Day Trading: Length 10-15/ATR Length 5-7/Multiplier 1.5-2.0, MA Type HMA or EMA/ATR MA Type EMA or SMA, fast trend with dynamic channels, suitable for scalping and day trading

Breakout Specialist: Length 20-30/ATR Length 5-10/Multiplier 2.0, MA Type SMA or WMA/ATR MA Type EMA or SMA, stable trend with responsive channel width

Adaptive All-Conditions: Length 20/ATR Length 10/Multiplier 2.0, MA Type KAMA or FRAMA/ATR MA Type KAMA or TEMA, self-adjusting to market conditions

Offset Parameter:

Controls horizontal positioning of channels on chart. Positive values shift channels to the right (future) for visual projection, negative values shift left (past) for historical analysis, zero (default) aligns with current price bars for real-time signal analysis. Offset affects only visual display, not alert conditions or actual calculations.

📈 PERFORMANCE ANALYSIS & COMPETITIVE ADVANTAGES

Keltner Channel Enhanced provides improvements over standard implementations while maintaining proven effectiveness.

Response Characteristics:

Standard EMA/RMA Configuration: Moderate trend lag (approximately 0.4 × length periods), smooth and stable channel width from RMA smoothing, good balance for most market conditions

Fast HMA/EMA Configuration: Approximately 60% reduction in trend lag compared to EMA, responsive channel width from EMA ATR smoothing, suitable for quick trend changes and breakouts

Adaptive KAMA/KAMA Configuration: Variable lag based on market efficiency, automatic adjustment to trending vs. ranging conditions, self-optimizing behavior reduces manual intervention

Comparison with Traditional Keltner Channels:

Enhanced Version Advantages:

Dual Algorithm Flexibility: Independent MA selection for trend and volatility vs. fixed EMA/RMA, separate tuning of trend responsiveness and channel stability

Market Adaptation: Choose configurations optimized for specific instruments and conditions, customize for scalping, swing, or position trading preferences

Comprehensive Alerts: Enhanced alert system including channel expansion detection

Traditional Version Advantages:

Simplicity: Fewer parameters, easier to understand and implement

Standardization: Fixed EMA/RMA combination ensures consistency across users

Research Base: Decades of backtesting and research on standard configuration

When to Use Enhanced Version: Trading multiple instruments with different characteristics, switching between trending and ranging markets, employing different strategies, algorithm-based trading systems requiring customization, seeking optimization for specific trading style and timeframe.

When to Use Standard Version: Beginning traders learning Keltner Channel concepts, following published research or trading systems, preferring simplicity and standardization, wanting to avoid optimization and curve-fitting risks.

Performance Across Market Conditions:

Strong Trending Markets: EMA or HMA basis with RMA or TEMA ATR smoothing provides quicker trend identification, pullbacks to basis offer excellent entry opportunities

Choppy/Ranging Markets: SMA or WMA basis with RMA ATR smoothing and lower multipliers, channel bounce strategies work well, avoid false breakouts

Volatile Markets: KAMA or FRAMA with EMA or TEMA, adaptive algorithms excel by automatic adjustment, wider multipliers (2.5-3.0) accommodate large price swings

Low Volatility/Consolidation: Channels narrow significantly indicating consolidation, algorithm choice less impactful, focus on detecting channel width contraction for breakout preparation

Keltner Channel vs. Bollinger Bands - Usage Comparison:

Favor Keltner Channels When: Trend-following is primary strategy, trading volatile instruments with gaps, want ATR-based volatility measurement, prefer fewer higher-quality channel touches, seeking stable channel width during trends.

Favor Bollinger Bands When: Mean-reversion is primary strategy, trading instruments with limited gaps, want statistical framework based on standard deviation, need squeeze patterns for breakout identification, prefer more frequent trading opportunities.

Use Both Together: Bollinger Band squeeze + Keltner Channel breakout is powerful combination, price outside Bollinger Bands but inside Keltner Channels indicates moderate signal, price outside both indicates very strong signal, Bollinger Bands for entries and Keltner Channels for trend confirmation.

Limitations and Considerations:

General Limitations:

Lagging Indicator: All moving averages lag price, even with reduced-lag algorithms

Trend-Dependent: Works best in trending markets, less effective in choppy conditions

No Direction Prediction: Indicates volatility and deviation, not future direction, requires confirmation

Enhanced Version Specific Considerations:

Optimization Risk: More parameters increase risk of curve-fitting historical data

Complexity: Additional choices may overwhelm beginning traders

Backtesting Challenges: Different algorithms produce different historical results

Mitigation Strategies:

Use Confirmation: Combine with momentum indicators (RSI, MACD), volume, or price action

Test Parameter Robustness: Ensure parameters work across range of values, not just optimized ones

Multi-Timeframe Analysis: Confirm signals across different timeframes

Proper Risk Management: Use appropriate position sizing and stops

Start Simple: Begin with standard EMA/RMA before exploring alternatives

Optimal Usage Recommendations:

For Maximum Effectiveness:

Start with standard EMA/RMA configuration to understand classic behavior

Experiment with alternatives on demo account or paper trading

Match algorithm combination to market condition and trading style

Use channel width analysis to identify market phases

Combine with complementary indicators for confirmation

Implement strict risk management using ATR-based position sizing

Focus on high-quality setups rather than trading every signal

Respect the trend: trade with basis direction for higher probability

Complementary Indicators:

RSI or Stochastic: Confirm momentum at channel extremes

MACD: Confirm trend direction and momentum shifts

Volume: Validate breakouts and trend strength

ADX: Measure trend strength, avoid Keltner signals in weak trends

Support/Resistance: Combine with traditional levels for high-probability setups

Bollinger Bands: Use together for enhanced breakout and volatility analysis

USAGE NOTES

This indicator is designed for technical analysis and educational purposes. Keltner Channel Enhanced has limitations and should not be used as the sole basis for trading decisions. While the flexible moving average selection for both trend and volatility components provides valuable adaptability across different market conditions, algorithm performance varies with market conditions, and past characteristics do not guarantee future results.

Key considerations:

Always use multiple forms of analysis and confirmation before entering trades

Backtest any parameter combination thoroughly before live trading

Be aware that optimization can lead to curve-fitting if not done carefully

Start with standard EMA/RMA settings and adjust only when specific conditions warrant

Understand that no moving average algorithm can eliminate lag entirely

Consider market regime (trending, ranging, volatile) when selecting parameters

Use ATR-based position sizing and risk management on every trade

Keltner Channels work best in trending markets, less effective in choppy conditions

Respect the trend direction indicated by price position relative to basis line

The enhanced flexibility of dual algorithm selection provides powerful tools for adaptation but requires responsible use, thorough understanding of how different algorithms behave under various market conditions, and disciplined risk management.

Auto-Fit Growth Trendline# **Theoretical Algorithmic Principles of the Auto-Fit Growth Trendline (AFGT)**

## **🎯 What Does This Algorithm Do?**

The Auto-Fit Growth Trendline is an advanced technical analysis system that **automates the identification of long-term growth trends** and **projects future price levels** based on historical cyclical patterns.

### **Primary Functionality:**

- **Automatically detects** the most significant lows in regular periods (monthly, quarterly, semi-annually, annually)

- **Constructs a dynamic trendline** that connects these historical lows

- **Projects the trend into the future** with high mathematical precision

- **Generates Fibonacci bands** that act as dynamic support and resistance levels

- **Automatically adapts** to different timeframes and market conditions

### **Strategic Purpose:**

The algorithm is designed to identify **fundamental value zones** where price has historically found support, enabling traders to:

- Identify optimal entry points for long positions

- Establish realistic price targets based on mathematical projections

- Recognize dynamic support and resistance levels

- Anticipate long-term price movements

---

## **🧮 Core Mathematical Foundations**

### **Adaptive Temporal Segmentation Theory**

The algorithm is based on **dynamic temporal partition theory**, where time is divided into mathematically coherent uniform intervals. It uses modular transformations to create bijective mappings between continuous timestamps and discrete periods, ensuring each temporal point belongs uniquely to a specific period.

**What does this achieve?** It allows the algorithm to automatically identify natural market cycles (annual, quarterly, etc.) without manual intervention, adapting to the inherent periodicity of each asset.

The temporal mapping function implements a **discrete affine transformation** that normalizes different frequencies (monthly, quarterly, semi-annual, annual) to a space of unique identifiers, enabling consistent cross-temporal comparative analysis.

---

## **📊 Local Extrema Detection Theory**

### **Multi-Point Retrospective Validation Principle**

Local minima detection is founded on **relative extrema theory with sliding window**. Instead of using a simple minimum finder, it implements a cross-validation system that examines the persistence of the extremum across multiple historical periods.

**What problem does this solve?** It eliminates false minima caused by temporal volatility, identifying only those points that represent true historical support levels with statistical significance.

This approach is based on the **statistical confirmation principle**, where a minimum is only considered valid if it maintains its extremum condition during a defined observation period, significantly reducing false positives caused by transitory volatility.

---

## **🔬 Robust Interpolation Theory with Outlier Control**

### **Contextual Adaptive Interpolation Model**

The mathematical core uses **piecewise linear interpolation with adaptive outlier correction**. The key innovation lies in implementing a **contextual anomaly detector** that identifies not only absolute extreme values, but relative deviations to the local context.

**Why is this important?** Financial markets contain extreme events (crashes, bubbles) that can distort projections. This system identifies and appropriately weights them without completely eliminating them, preserving directional information while attenuating distortions.

### **Implicit Bayesian Smoothing Algorithm**

When an outlier is detected (deviation >300% of local average), the system applies a **simplified Kalman filter** that combines the current observation with a local trend estimation, using a weight factor that preserves directional information while attenuating extreme fluctuations.

---

## **📈 Stabilized Extrapolation Theory**

### **Exponential Growth Model with Dampening**

Extrapolation is based on a **modified exponential growth model with progressive dampening**. It uses multiple historical points to calculate local growth ratios, implements statistical filtering to eliminate outliers, and applies a dampening factor that increases with extrapolation distance.

**What advantage does this offer?** Long-term projections in finance tend to be exponentially unrealistic. This system maintains short-to-medium term accuracy while converging toward realistic long-term projections, avoiding the typical "exponential explosions" of other methods.

### **Asymptotic Convergence Principle**

For long-term projections, the algorithm implements **controlled asymptotic convergence**, where growth ratios gradually converge toward pre-established limits, avoiding unrealistic exponential projections while preserving short-to-medium term accuracy.

---

## **🌟 Dynamic Fibonacci Projection Theory**

### **Continuous Proportional Scaling Model**

Fibonacci bands are constructed through **uniform proportional scaling** of the base curve, where each level represents a linear transformation of the main curve by a constant factor derived from the Fibonacci sequence.

**What is its practical utility?** It provides dynamic resistance and support levels that move with the trend, offering price targets and profit-taking points that automatically adapt to market evolution.

### **Topological Preservation Principle**

The system maintains the **topological properties** of the base curve in all Fibonacci projections, ensuring that spatial and temporal relationships are consistently preserved across all resistance/support levels.

---

## **⚡ Adaptive Computational Optimization**

### **Multi-Scale Resolution Theory**

It implements **automatic multi-resolution analysis** where data granularity is dynamically adjusted according to the analysis timeframe. It uses the **adaptive Nyquist principle** to optimize the signal-to-noise ratio according to the temporal observation scale.

**Why is this necessary?** Different timeframes require different levels of detail. A 1-minute chart needs more granularity than a monthly one. This system automatically optimizes resolution for each case.

### **Adaptive Density Algorithm**

Calculation point density is optimized through **adaptive sampling theory**, where calculation frequency is adjusted according to local trend curvature and analysis timeframe, balancing visual precision with computational efficiency.

---

## **🛡️ Robustness and Fault Tolerance**

### **Graceful Degradation Theory**

The system implements **multi-level graceful degradation**, where under error conditions or insufficient data, the algorithm progressively falls back to simpler but reliable methods, maintaining basic functionality under any condition.

**What does this guarantee?** That the indicator functions consistently even with incomplete data, new symbols with limited history, or extreme market conditions.

### **State Consistency Principle**

It uses **mathematical invariants** to guarantee that the algorithm's internal state remains consistent between executions, implementing consistency checks that validate data structure integrity in each iteration.

---

## **🔍 Key Theoretical Innovations**

### **A. Contextual vs. Absolute Outlier Detection**

It revolutionizes traditional outlier detection by considering not only the absolute magnitude of deviations, but their relative significance within the local context of the time series.

**Practical impact:** It distinguishes between legitimate market movements and technical anomalies, preserving important events like breakouts while filtering noise.

### **B. Extrapolation with Weighted Historical Memory**

It implements a memory system that weights different historical periods according to their relevance for current prediction, creating projections more adaptable to market regime changes.

**Competitive advantage:** It automatically adapts to fundamental changes in asset dynamics without requiring manual recalibration.

### **C. Automatic Multi-Timeframe Adaptation**

It develops an automatic temporal resolution selection system that optimizes signal extraction according to the intrinsic characteristics of the analysis timeframe.

**Result:** A single indicator that functions optimally from 1-minute to monthly charts without manual adjustments.

### **D. Intelligent Asymptotic Convergence**

It introduces the concept of controlled asymptotic convergence in financial extrapolations, where long-term projections converge toward realistic limits based on historical fundamentals.

**Added value:** Mathematically sound long-term projections that avoid the unrealistic extremes typical of other extrapolation methods.

---

## **📊 Complexity and Scalability Theory**

### **Optimized Linear Complexity Model**

The algorithm maintains **linear computational complexity** O(n) in the number of historical data points, guaranteeing scalability for extensive time series analysis without performance degradation.

### **Temporal Locality Principle**

It implements **temporal locality**, where the most expensive operations are concentrated in the most relevant temporal regions (recent periods and near projections), optimizing computational resource usage.

---

## **🎯 Convergence and Stability**

### **Probabilistic Convergence Theory**

The system guarantees **probabilistic convergence** toward the real underlying trend, where projection accuracy increases with the amount of available historical data, following **law of large numbers** principles.

**Practical implication:** The more history an asset has, the more accurate the algorithm's projections will be.

### **Guaranteed Numerical Stability**

It implements **intrinsic numerical stability** through the use of robust floating-point arithmetic and validations that prevent overflow, underflow, and numerical error propagation.

**Result:** Reliable operation even with extreme-priced assets (from satoshis to thousand-dollar stocks).

---

## **💼 Comprehensive Practical Application**

**The algorithm functions as a "financial GPS"** that:

1. **Identifies where we've been** (significant historical lows)

2. **Determines where we are** (current position relative to the trend)

3. **Projects where we're going** (future trend with specific price levels)

4. **Provides alternative routes** (Fibonacci bands as alternative targets)

This theoretical framework represents an innovative synthesis of time series analysis, approximation theory, and computational optimization, specifically designed for long-term financial trend analysis with robust and mathematically grounded projections.

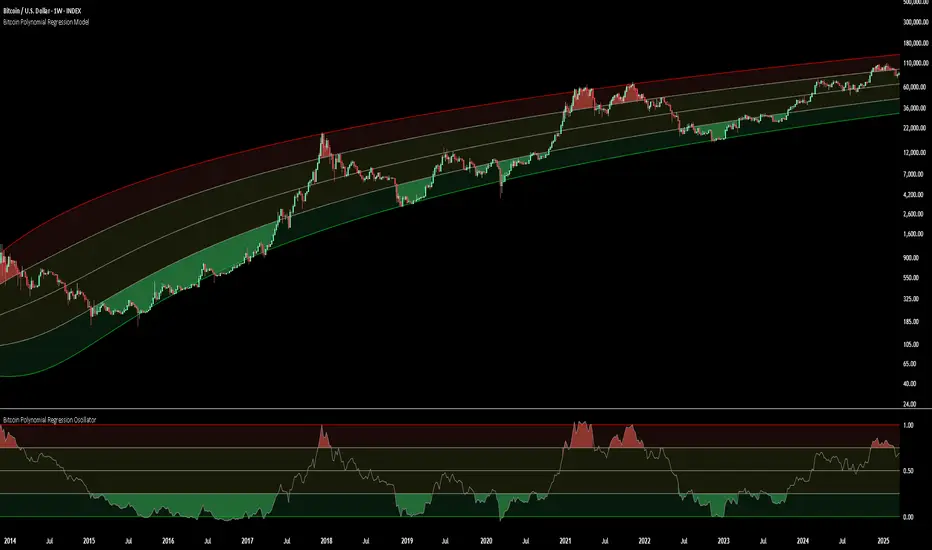

Bitcoin Polynomial Regression ModelThis is the main version of the script. Click here for the Oscillator part of the script.

💡Why this model was created:

One of the key issues with most existing models, including our own Bitcoin Log Growth Curve Model , is that they often fail to realistically account for diminishing returns. As a result, they may present overly optimistic bull cycle targets (hence, we introduced alternative settings in our previous Bitcoin Log Growth Curve Model).

This new model however, has been built from the ground up with a primary focus on incorporating the principle of diminishing returns. It directly responds to this concept, which has been briefly explored here .

📉The theory of diminishing returns:

This theory suggests that as each four-year market cycle unfolds, volatility gradually decreases, leading to more tempered price movements. It also implies that the price increase from one cycle peak to the next will decrease over time as the asset matures. The same pattern applies to cycle lows and the relationship between tops and bottoms. In essence, these price movements are interconnected and should generally follow a consistent pattern. We believe this model provides a more realistic outlook on bull and bear market cycles.

To better understand this theory, the relationships between cycle tops and bottoms are outlined below:https://www.tradingview.com/x/7Hldzsf2/

🔧Creation of the model:

For those interested in how this model was created, the process is explained here. Otherwise, feel free to skip this section.

This model is based on two separate cubic polynomial regression lines. One for the top price trend and another for the bottom. Both follow the general cubic polynomial function:

ax^3 +bx^2 + cx + d.