Volume Cluster Profile [VCP] (Zeiierman)█ Overview

Volume Cluster Profile (Zeiierman) is a volume profile tool that builds cluster-enhanced volume-by-price maps for both the current market window and prior swing segments.

Instead of treating the profile as a raw histogram only, VCP detects the dominant volume peaks (clusters) inside the profile, then uses a Gaussian spread model to “radiate” those peaks into surrounding price bins. This produces a smoother, more context-aware profile that highlights where volume is most meaningfully concentrated, not just where it happened to print.

On top of the live profile, VCP automatically records historical swing profiles between pivots, wraps each segment for clarity, and can project the most recent segment’s High/Low Value extensions (VA/LV) forward to the current bar to keep key structure visible as price evolves.

█ How It Works

⚪ 1) Profile Construction (Volume-by-Price)

VCP builds a volume profile histogram over a chosen window (current lookback, or a swing segment):

Range Scan

The script finds the full min → max price range inside the window.

Bin the Range

That range is divided into a user-defined number of Price Bins (rows). More bins = finer detail, but heavier computation.

Accumulate Volume into Bins

For each bar inside the window, the script takes the bar’s close price, determines which price bin it belongs to, and adds the bar’s volume to that bin.

float step = (maxPrice - minPrice) / binsCount

for i = 0 to barsToUse - 1

int b = f_clamp(int(math.floor((close - minPrice) / step)), 0, binsCount - 1)

volBins += volume

Result: volBins becomes a standard volume-by-price histogram (close-based binning).

⚪ 2) Cluster Detection (Finding Dominant Peaks)

Once the raw histogram is built, VCP identifies cluster centers as the most meaningful volume “hills”:

Local Peak Test

A bin becomes a cluster candidate if its volume is greater than or equal to its immediate neighbors (left/right).

Filter Weak Peaks

Peaks must also be above a basic activity threshold (relative to the average bin volume) to avoid noise.

bool isPeak = v >= left and v >= right

if isPeak and v > avgVol

array.push(clusterIdxs, b)

Keep the Best Peaks Only

If too many peaks exist, the script keeps only the strongest ones, capped by: Max Cluster Centers

Result: clusterIdxs = the set of dominant profile peaks (cluster centers).

⚪ 3) Cluster Enhancement (Gaussian Spread Model)

This is what makes VCP different from a raw profile.

Instead of using volBins directly, the script builds an enhanced profile where each cluster center influences nearby price bins using a Gaussian curve:

Distance from each bin to each cluster center is computed in “bin units”

A Gaussian weight is applied so that bins near the center receive stronger influence, while bins farther away decay smoothly.

Cluster Spread (sigma) controls how wide this influence reaches: low sigma produces tight, sharp clusters, while high sigma results in wider, smoother structure zones.

enhanced += centerV * math.exp(-(dist*dist) / (2.0 * clusterSigma * clusterSigma))

volBinsAI := enhanced / szClFinal

Result: volBinsAI = the cluster-enhanced volume value for each bin.

In practice, VCP turns the profile into a structure map of dominant volume concentrations, rather than a simple “where volume printed” histogram.

⚪ 4) POC from the Enhanced Profile

After enhancement:

The bin with the highest volBinsAI becomes the POC (Point of Control)

POC is plotted at the midpoint price of that bin

if volBinsAI > maxVol

maxVol := volBinsAI , pocBin := b

So the POC reflects the cluster-enhanced profile rather than the raw histogram.

█ How to Use

⚪ Read Cluster Structure (Default = 2 Clusters)

By default, the Volume Cluster Profile (VCP) is configured to detect up to 2 dominant volume clusters within the profile. These clusters represent price zones where the market accepted trading activity, not just where volume printed randomly.

⚪ When TWO Clusters Appear

When VCP detects two distinct clusters, it usually indicates:

Two competing areas of value

Ongoing auction between higher and lower acceptance zones

Treat each cluster as an acceptance zone

Expect slower price action and rotation inside clusters

Expect faster movement in the low-volume space between clusters

Use cluster-to-cluster movement as:

rotation targets

range boundaries

acceptance vs rejection tests

Typical behavior:

Price enters a cluster → stalls, consolidates, rotates

Price rejects at cluster edge → moves toward the opposite cluster

⚪ When ONLY ONE Cluster Appears

If VCP detects only one cluster, or if two clusters visually merge into one:

Volume is no longer split

The market has formed a single dominant value area

Price consensus is strong

Treat the cluster as the primary value anchor

Expect pullbacks and reactions around this zone

Bias becomes directional:

Above the cluster → bullish context

Below the cluster → bearish context

Inside the cluster → balance/chop

This structure often appears during clean trends or stable equilibria.

⚪ VA/LV Extensions

VCP projects two zones from the end of the most recent swing segment:

VA extension = the segment’s highest enhanced-volume bin (dominant zone)

LV extension = the segment’s lowest enhanced-volume bin (thin/weak zone)

A breakout of the VA extension signals acceptance and potential continuation. A retest of the VA or LV extension is used to confirm acceptance or rejection, while rejection from either zone often leads to rotation back toward value.

█ Settings

Cluster Volume Profile

Lookback Bars – how many recent bars build the current profile

Price Bins – profile resolution (more bins = more detail, heavier CPU)

Cluster Spread – Gaussian sigma; higher values widen/smooth cluster influence

Max Cluster Centers – cap on detected peaks used in enhancement

Historical Swing Cluster Volume Profile

Pivot Length – swing sensitivity (larger = fewer, broader segments)

Max Profiles – how many historical segments to retain

Profile Width – thickness of each historical profile

High & Low Value Area

Profile VA/LV – extend the last segment’s top-bin and low-bin zones forward

-----------------

Disclaimer

The content provided in my scripts, indicators, ideas, algorithms, and systems is for educational and informational purposes only. It does not constitute financial advice, investment recommendations, or a solicitation to buy or sell any financial instruments. I will not accept liability for any loss or damage, including without limitation any loss of profit, which may arise directly or indirectly from the use of or reliance on such information.

All investments involve risk, and the past performance of a security, industry, sector, market, financial product, trading strategy, backtest, or individual's trading does not guarantee future results or returns. Investors are fully responsible for any investment decisions they make. Such decisions should be based solely on an evaluation of their financial circumstances, investment objectives, risk tolerance, and liquidity needs.

"curve" için komut dosyalarını ara

Kalman Hull Kijun [BackQuant]Kalman Hull Kijun

A trend baseline that merges three ideas into one clean overlay, Kalman filtering for noise control, Hull-style responsiveness, and a Kijun-like Donchian midline for structure and bias.

Context and lineage

This indicator sits in the same family as two related scripts:

Kalman Price Filter

This is the foundational building block. It introduces the Kalman filter concept, a state-estimation algorithm designed to infer an underlying “true” signal from noisy measurements, originally used in aerospace guidance and later adopted across robotics, economics, and markets.

Kalman Hull Supertrend

This is the original script made, which people loved. So it inspired me to create this one.

Kalman Hull Kijun uses the same core philosophy as the Supertrend variant, but instead of building a Supertrend band system, it produces a single structural baseline that behaves like a Kijun-style reference line.

What this indicator is trying to solve

Most trend baselines sit on a bad trade-off curve:

If you smooth hard, the line reacts late and misses turns.

If you react fast, the line whipsaws and tracks noise.

Kalman Hull Kijun is designed to land closer to the middle:

Cleaner than typical fast moving averages in chop.

More responsive than slow averages in directional phases.

More “structure aware” than pure averages because the baseline is range-derived (Kijun-like) after filtering.

Core idea in plain language

The plotted line is a Kijun-like baseline, but it is not built from raw candles directly.

High level flow:

Start with a chosen price stream (source input).

Reduce measurement noise using Kalman-style state estimation.

Add Hull-style responsiveness so the filtered stream stays usable for trend work.

Build a Kijun-like baseline by taking a Donchian midpoint of that filtered stream over the base period.

So the output is a single baseline that is intended to be:

Less jittery than a simple fast MA.

Less laggy than a slow MA.

More “range anchored” than standard smoothing lines.

How to read it

1) Trend and bias (the primary use)

Price above the baseline, bullish bias.

Price below the baseline, bearish bias.

Clean flips across the baseline are regime changes, especially when followed by a hold or retest.

2) Retests and dynamic structure

Treat the baseline like dynamic S/R rather than a signal generator:

In uptrends, pullbacks that respect the baseline can act as continuation context.

In downtrends, reclaim failures around the baseline can act as continuation context.

Repeated back-and-forth around the line usually means compression or chop, not clean trend.

3) Extension vs compression (using the fill)

The fill is meant to communicate “distance” and “pressure” visually:

Large separation between price and baseline suggests expansion.

Price compressing into the baseline suggests rebalancing and decision points.

Inputs and what they change

Kijun Base Period

Controls the structural memory of the baseline.

Higher values track broader swings and reduce flips.

Lower values track tighter swings and react faster.

Kalman Price Source

Defines what data the filter is estimating.

Close is usually the cleanest default.

HL2 often “feels” smoother as an average price.

High/Low sources can become more reactive and less stable depending on the market.

Measurement Noise

Think of this as the main smoothness knob:

Higher values generally produce a calmer filtered stream.

Lower values generally produce a faster, more reactive stream.

Process Noise

Think of this as adaptability:

Higher values adapt faster to changing conditions but can get twitchy.

Lower values adapt slower but stay stable.

Plotting and UI (what you see on chart)

1) Adaptive line coloring

Baseline turns bullish color when price is above it.

Baseline turns bearish color when price is below it.

This makes the state readable without extra panels.

2) Gradient “energy” fill

Bull fill appears between price and baseline when above.

Bear fill appears between price and baseline when below.

The goal is clarity on separation and control, not decoration.

3) Rim effect

A subtle band around price that only appears on the active side.

Helps highlight directional control without hiding candles.

4) Candle painting (optional)

Candles can be colored to match the current bias.

Useful for scanning many charts quickly.

Disable if you prefer raw candles.

Alerts

Long state alert when price is above the baseline.

Short state alert when price is below the baseline.

Best used as a bias or regime notification, not a standalone entry trigger.

Where it fits in a workflow

This is a context layer, it pairs well with:

Market structure tools, BOS/MSB, OBs, FVGs.

Momentum triggers that need a regime filter.

Mean reversion tools that need “do not fade trends” context.

Limitations

No baseline eliminates chop whipsaws, tuning only manages the trade-off.

Settings should not be copy pasted across assets without checking behavior.

This does not forecast, it estimates and smooths state, then expresses it as a structural baseline.

Disclaimer

Educational and informational only, not financial advice.

Not a complete trading system.

If you use it in any trading workflow, do proper backtesting, forward testing, and risk management before any live execution.

Punjis Dynamic Daily EMA/SMA 5,9,21,50,100 LevelsPunjis Dynamic Daily EMA/SMA 5,9,21,50,100 Levels

Overview:

This indicator displays daily timeframe moving averages as horizontal lines extending to the right of your chart, regardless of what timeframe you're currently viewing. It includes six key moving averages: EMA 5, EMA 9, EMA 21, SMA 50, SMA 100, and SMA 200.

Key Features:

Clean Chart Design: Unlike traditional moving average lines that clutter your chart with curves across all candles, this indicator uses horizontal lines that extend only from the current price level to the right edge of your screen

Multi-Timeframe Analysis: View daily moving averages on any intraday timeframe (1min, 5min, 15min, etc.) without switching charts

Fully Customizable:

Toggle each moving average on/off independently

Adjust the period length for each MA

Customize colors for each line

Master toggle to show/hide all lines at once

Reduced Visual Noise: Horizontal lines keep your price action clean and easy to read while still providing critical support/resistance levels

Professional Layout: Perfect for traders who need to monitor multiple key levels without obscuring candlestick patterns and chart analysis

Benefits of Horizontal Lines:

Cleaner Charts: Traditional MAs draw lines through every candle, creating visual clutter. Horizontal lines only show current values, keeping your chart clean

Focus on Current Levels: What matters most is where the MAs are NOW relative to price - horizontal lines highlight this instantly

Better Price Action Visibility: See candlestick patterns, volume, and support/resistance levels clearly without MA lines crossing through them

Quick Reference: Instantly identify if price is above or below key moving averages without following curved lines across the chart

Professional Appearance: Clean, minimalist design preferred by institutional traders and technical analysts

Use Cases:

Day traders monitoring higher timeframe levels on intraday charts

Swing traders tracking daily moving averages as dynamic support/resistance

Multi-timeframe analysis without chart switching

Identifying trend direction and potential reversal zones

Clean workspace for pattern recognition and price action trading

chanlun缠论 - 笔与中枢Overview

The Chanlun (缠论) Strokes & Central Zones indicator is an advanced technical analysis tool based on Chinese Chan Theory (Chanlun Theory). It automatically identifies market structure through "strokes" (笔) and "central hubs" (中枢), providing traders with a systematic framework for understanding price movements, trend structure, and potential reversal zones.

Theoretical Foundation

Chan Theory is a sophisticated price action methodology that breaks down market movements into hierarchical structures:

Local Extremes: Swing highs and lows identified through lookback periods

Strokes (笔): Valid price movements between opposite extremes that meet specific criteria

Central Hubs (中枢): Consolidation zones formed by overlapping strokes, representing key support/resistance areas

Key Components

1. Local Extreme Detection

Identifies swing highs and lows using a configurable lookback period (default: 5 bars)

Only considers extremes within the specified calculation range

Forms the foundation for stroke construction

2. Stroke (笔) Identification

The indicator applies a multi-stage filtering process to identify valid strokes:

Stage 1 - Extreme Consolidation:

Merges consecutive extremes of the same type (high or low)

Keeps only the most extreme value (highest high or lowest low)

Stage 2 - Stroke Validation:

Ensures minimum bar gap between strokes (default: 4 bars)

Alternative validation: 2+ bars with >1% price change

Eliminates noise and insignificant price movements

Color Coding:

White Lines: Regular up/down strokes

Yellow Lines: Strokes that form part of a central hub

Customizable width and colors for different stroke types

3. Central Hub (中枢) Formation

A central hub forms when at least 3 consecutive strokes have overlapping price ranges:

Formation Rules:

Stroke 1:

Stroke 2:

Stroke 3:

Hub Upper = MIN(High1, High2, High3)

Hub Lower = MAX(Low1, Low2, Low3)

Valid if: Hub Upper > Hub Lower

Hub Extension:

Subsequent strokes that overlap with the hub extend it

Hub ends when a stroke no longer overlaps

Creates rectangular zones on the chart

Visual Representation:

Green rectangular boxes: Mark the time and price range of each central hub

Dashed extension lines: Show the latest hub boundaries extending to the right

Price labels on axis: Display exact hub upper and lower boundary values

4. Extreme Point Markers (Optional)

Red markers for tops (▼)

Green markers for bottoms (▲)

Marks every validated stroke extreme point

Useful for detailed structure analysis

5. Information Table (Optional)

Displays real-time statistics:

Symbol name

Current timeframe

Lookback period setting

Minimum gap setting

Total stroke count

Parameter Settings

Performance Settings

Max Bars to Calculate (3600): Limits historical calculation to improve performance

Local Extreme Lookback Period (5): Bars used to identify swing highs/lows

Min Gap Bars (4): Minimum bars required between valid strokes

Display Settings

Show Strokes: Toggle stroke line visibility

Show Central Hub: Toggle hub box visibility

Show Hub Extension Lines: Toggle dashed boundary lines

Show Extreme Point Marks: Toggle top/bottom markers

Show Info Table: Toggle statistics table

Color Settings

Full customization of:

Up/down stroke colors and widths

Hub stroke colors and widths

Hub border and background colors

Extension line colors

Trading Applications

Trend Structure Analysis

Uptrend: Series of higher highs and higher lows connected by strokes

Downtrend: Series of lower highs and lower lows connected by strokes

Consolidation: Formation of central hubs indicating range-bound movement

Support and Resistance Identification

Central Hub Zones: Act as strong support/resistance areas

Hub Upper Boundary: Resistance level in consolidation, support after breakout

Hub Lower Boundary: Support level in consolidation, resistance after breakdown

Price tends to react at these levels due to market structure memory

Breakout Trading

Bullish Breakout: Price closes above hub upper boundary

Previous resistance becomes support

Entry on retest of upper boundary

Stop loss below hub zone

Bearish Breakdown: Price closes below hub lower boundary

Previous support becomes resistance

Entry on retest of lower boundary

Stop loss above hub zone

Reversal Detection

Hub Formation After Trend: Signals potential trend exhaustion

Multiple Hub Levels: Create probability zones for reversals

Stroke Count: Excessive strokes within hub suggest weakening momentum

Position Management

Use hub boundaries for stop loss placement

Scale out positions at hub edges

Re-enter on retests of broken hub levels

Interpretation Guide

Strong Trending Market

Long, clear strokes with minimal overlap

Few or no central hubs forming

Strokes consistently in same direction

Wide spacing between extremes

Consolidating Market

Multiple central hubs forming

Short, overlapping strokes

Yellow hub strokes dominate the chart

Narrow price range

Trend Transition

Hub formation after extended trend

Stroke direction changes frequently

Hub boundaries being tested repeatedly

Potential reversal zone

Advanced Usage Techniques

Multi-Timeframe Analysis

Higher Timeframe: Identify major hub zones for overall market structure

Lower Timeframe: Find precise entry points within larger structure

Alignment: Trade when lower timeframe strokes align with higher timeframe hub breaks

Hub Quality Assessment

Wide Hubs: Strong consolidation, higher probability support/resistance

Narrow Hubs: Weak consolidation, may break easily

Extended Hubs: More strokes = stronger zone

Isolated Hubs: Single hub = potential pivot point

Stroke Analysis

Stroke Length: Longer strokes = stronger momentum

Stroke Speed: Fewer bars per stroke = explosive moves

Stroke Clustering: Many short strokes = indecision

Best Practices

Parameter Optimization

Adjust lookback period based on timeframe and volatility

Lower periods (3-4): More strokes, more noise, faster signals

Higher periods (7-10): Fewer strokes, cleaner structure, slower signals

Confirmation Strategy

Don't trade on strokes alone

Combine with volume analysis

Use candlestick patterns at hub boundaries

Wait for breakout confirmation

Risk Management

Always place stops outside hub zones

Use hub width to size positions (wider hub = smaller position)

Exit if price re-enters broken hub from wrong direction

Avoid Common Pitfalls

Don't trade within central hubs (range-bound, unpredictable)

Don't ignore higher timeframe hub structures

Don't chase strokes after they've extended far from hub

Don't trust single-stroke hubs (need 3+ strokes for validity)

Performance Considerations

Max Bars Limit: Set to 3600 to balance detail with performance

Safe Distance Calculation: Only draws objects within 2000 bars of current price

Object Cleanup: Automatically removes old drawing objects to prevent memory issues

Efficient Arrays: Uses indexed arrays for fast lookup and processing

Ideal Market Conditions

Best Performance:

Liquid markets with clear structure (major forex pairs, indices, large-cap stocks)

Trending markets with periodic consolidations

Medium to high volatility for clear stroke formation

Less Effective:

Extremely choppy, directionless markets

Very low timeframes (< 5 minutes) with excessive noise

Illiquid instruments with erratic price action

Integration with Other Indicators

Complementary Tools:

Volume Profile: Confirm hub significance with volume nodes

Moving Averages: Use for trend bias within stroke structure

RSI/MACD: Momentum confirmation at hub boundaries

Fibonacci Retracements: Hub levels often align with Fib levels

Advantages

✓ Objective Structure: Removes subjectivity from market structure analysis

✓ Visual Clarity: Color-coded strokes and clear hub zones

✓ Multi-Timeframe Applicable: Works on all timeframes from minutes to months

✓ Complete Framework: Provides entry, exit, and risk management levels

✓ Theoretical Foundation: Based on proven Chan Theory methodology

✓ Customizable: Extensive parameter and visual customization options

Limitations

⚠ Learning Curve: Requires understanding of Chan Theory principles

⚠ Lag Factor: Strokes confirm after price movements complete

⚠ Parameter Sensitivity: Different settings produce significantly different results

⚠ Choppy Market Struggles: Can generate excessive hubs in range-bound conditions

⚠ Computation Intensive: May slow down on lower-end systems with max bars setting

Optimization Tips

Timeframe Selection

Scalping: 5-15 minute charts, lookback period 3-4

Day Trading: 15-60 minute charts, lookback period 4-5

Swing Trading: 4-hour to daily charts, lookback period 5-7

Position Trading: Daily to weekly charts, lookback period 7-10

Volatility Adjustment

High volatility: Increase minimum gap bars to reduce noise

Low volatility: Decrease lookback period to capture smaller moves

Visual Optimization

Use contrasting colors for different market conditions

Adjust line widths based on chart resolution

Toggle markers off for cleaner appearance once familiar with structure

Quick Start Guide

For Beginners:

Start with default settings (5 lookback, 4 min gap)

Enable "Show Info Table" to track stroke count

Focus on identifying clear hub formations

Practice waiting for price to break hub boundaries before trading

For Advanced Users:

Optimize lookback and gap parameters for your instrument

Use hub strokes (yellow) to identify key consolidation zones

Combine with multiple timeframes for confirmation

Develop entry rules based on hub breakout/retest patterns

This indicator provides a complete structural framework for understanding market behavior through the lens of Chan Theory, offering traders a systematic approach to identifying high-probability trading opportunities.

ZenAlgo - ADXThis open-source indicator builds upon the official Average Directional Index (ADX) implementation by TradingView. It preserves the core logic of the original ADX while introducing additional visualization features, configurability, and analytical overlays to assist with directional strength analysis.

Core Calculation

The script computes the ADX, +DI, and -DI based on smoothed directional movement and true range over a user-defined length. The smoothing is performed using Wilder’s method, as in the original implementation.

True Range is calculated from the current high, low, and previous close.

Directional Movement components (+DM, -DM) are derived by comparing the change in highs and lows between consecutive bars.

These values are then smoothed, and the +DI and -DI are expressed as percentages of the smoothed True Range.

The difference between +DI and -DI is normalized to derive DX, which is further smoothed to yield the ADX value.

The indicator includes a selectable signal line (SMA or EMA) applied to the ADX for crossover-based visualization.

Visualization Enhancements

Several plots and conditions have been added to improve interpretability:

Color-coded histograms and lines visualize DI relative to a configurable threshold (default: 25). Colors follow the ZenAlgo color scheme.

Dynamic opacity and gradient coloring are used for both ADX and DI components, allowing users to distinguish weak/moderate/strong directional trends visually.

Mirrored ADX is internally calculated for certain overlays but not directly plotted.

The script also provides small circles and diamonds to highlight:

Crossovers between ADX and its signal line.

DI crossing above or below the 25 threshold.

Rising ADX confirmed by rising DI values, with point size reflecting ADX strength.

Divergence Detection

The indicator includes optional detection of fractal-based divergences on the DI curve:

Regular and hidden bullish and bearish divergences are identified based on relative fractal highs/lows in both price and DI.

Detected divergences are optionally labeled with 'R' (Regular) or 'H' (Hidden), and color-coded accordingly.

Fractal points are defined using 5-bar patterns to ensure consistency and reduce false positives.

ADX/DI Table

When enabled, a floating table displays live values and summaries:

ADX value , trend direction (rising/falling), and qualitative strength.

DI composite , trend direction, and relative strength.

Contextual power dynamics , describing whether bulls or bears are gaining or losing strength.

The background colors of the table reflect current trend strength and direction.

Interpretation Guidelines

ADX indicates the strength of a trend, regardless of its direction. Values below 20 are often considered weak, while those above 40 suggest strong trending conditions.

+DI and -DI represent bullish and bearish directional movements, respectively. Crossovers between them are used to infer trend direction.

When ADX is rising and either +DI or -DI is dominant and increasing, the trend is likely strengthening.

Divergences between DI and price may suggest potential reversals but should be interpreted cautiously and not in isolation.

The threshold line (default 25) provides a basic filter for ignoring low-strength conditions. This can be adjusted depending on the market or timeframe.

Added Value over Existing Indicators

Fully color-graded ADX and DI display for better visual clarity.

Optional signal MA over ADX with crossover markers.

Rich contextual labeling for both divergence and threshold events.

Power dynamics commentary and live table help users contextualize current momentum.

Customizable options for smoothing type, divergence display, table position, and visual offsets.

These additions aim to improve situational awareness without altering the fundamental meaning of ADX/DI values.

Limitations and Disclaimers

As with any ADX-based tool, this indicator does not indicate market direction alone —it measures strength, not trend bias.

Divergence detection relies on fractal patterns and may lag or produce false positives in sideways markets.

Signal MA crossovers and DI threshold breaks are not entry signals , but contextual markers that may assist with timing or filtering other systems.

The table text and labels are for visual assistance and do not replace proper technical analysis or market context.

RMSD Trend [InvestorUnknown]RMSD Trend is a trend-following indicator that utilizes Root Mean Square Deviation (RMSD) to dynamically construct a volatility-weighted trend channel around a selected moving average. This indicator is designed to enhance signal clarity, minimize noise, and offer quantitative insights into market momentum, ideal for both discretionary and systematic traders.

How It Works

At its core, RMSD Trend calculates a deviation band around a selected moving average using the Root Mean Square Deviation (similar to standard deviation but with squared errors), capturing the magnitude of price dispersion over a user-defined period. The logic is simple:

When price crosses above the upper deviation band, the market is considered bullish (Risk-ON Long).

When price crosses below the lower deviation band, the market is considered bearish (Risk-ON Short).

If price stays within the band, the market is interpreted as neutral or ranging, offering low-risk decision zones.

The indicator also generates trend flips (Long/Short) based on crossovers and crossunders of the price and the RMSD bands, and colors candles accordingly for enhanced visual feedback.

Features

7 Moving Average Types: Choose between SMA, EMA, HMA, DEMA, TEMA, RMA, and FRAMA for flexibility.

Customizable Source Input: Use price types like close, hl2, ohlc4, etc.

Volatility-Aware Channel: Adjustable RMSD multiplier determines band width based on volatility.

Smart Coloring: Candles and bands adapt their colors to reflect trend direction (green for bullish, red for bearish).

Intra-bar Repainting Toggle: Option to allow more responsive but repaintable signals.

Speculation Fill Zones: When price exceeds the deviation channel, a semi-transparent fill highlights potential momentum surges.

Backtest Mode

Switching to Backtest Mode unlocks a robust suite of simulation features:

Built-in Equity Curve: Visualizes both strategy equity and Buy & Hold performance.

Trade Metrics Table: Displays the number of trades, win rates, gross profits/losses, and long/short breakdowns.

Performance Metrics Table: Includes key stats like CAGR, drawdown, Sharpe ratio, and more.

Custom Date Range: Set a custom start date for your backtest.

Trade Sizing: Simulate results using position sizing and initial capital settings.

Signal Filters: Choose between Long & Short, Long Only, or Short Only strategies.

Alerts

The RMSD Trend includes six built-in alert conditions:

LONG (RMSD Trend) - Trend flips from Short to Long

SHORT (RMSD Trend) - Trend flips from Long to Short

RISK-ON LONG (RMSD Trend) - Price crosses above upper RMSD band

RISK-OFF LONG (RMSD Trend) - Price falls back below upper RMSD band

RISK-ON SHORT (RMSD Trend) - Price crosses below lower RMSD band

RISK-OFF SHORT (RMSD Trend) - Price rises back above lower RMSD band

Use Cases

Trend Confirmation: Confirms directional bias with RMSD-weighted confidence zones.

Breakout Detection: Highlights moments when price breaks free from historical volatility norms.

Mean Reversion Filtering: Avoids false signals by incorporating RMSD’s volatility sensitivity.

Strategy Development: Backtest your signals or integrate with a broader system for alpha generation.

Settings Summary

Display Mode: Overlay (default) or Backtest Mode

Average Type: Choose from SMA, EMA, HMA, DEMA, etc.

Average Length: Lookback window for moving average

RMSD Multiplier: Band width control based on RMS deviation

Source: Input price source (close, hl2, ohlc4, etc.)

Intra-bar Updating: Real-time updates (may repaint)

Color Bars: Toggle bar coloring by trend direction

Disclaimer

This indicator is provided for educational and informational purposes only. It is not financial advice. Past performance, including backtest results, is not indicative of future results. Use with caution and always test thoroughly before live deployment.

Dskyz (DAFE) AI Adaptive Regime - Beginners VersionDskyz (DAFE) AI Adaptive Regime - Pro: Revolutionizing Trading for All

Introduction

In the fast-paced world of financial markets, traders need tools that can keep up with ever-changing conditions while remaining accessible. The Dskyz (DAFE) AI Adaptive Regime - Pro is a groundbreaking TradingView strategy that delivers advanced, AI-driven trading capabilities to everyday traders. Available on TradingView (TradingView Scripts), this Pine Script strategy combines sophisticated market analysis with user-friendly features, making it a standout choice for both novice and experienced traders.

Core Functionality

The strategy is built to adapt to different market regimes—trending, ranging, volatile, or quiet—using a robust set of technical indicators, including:

Moving Averages (MA): Fast and slow EMAs to detect trend direction.

Average True Range (ATR): For dynamic stop-loss and volatility assessment.

Relative Strength Index (RSI) and MACD: Multi-timeframe confirmation of momentum and trend.

Average Directional Index (ADX): To identify trending markets.

Bollinger Bands: For assessing volatility and range conditions.

Candlestick Patterns: Recognizes patterns like bullish engulfing, hammer, and double bottoms, confirmed by volume spikes.

It generates buy and sell signals based on a scoring system that weighs these indicators, ensuring trades align with the current market environment. The strategy also includes dynamic risk management with ATR-based stops and trailing stops, as well as performance tracking to optimize future trades.

What Sets It Apart

The Dskyz (DAFE) AI Adaptive Regime - Pro distinguishes itself from other TradingView strategies through several unique features, which we compare to common alternatives below:

| Feature | Dskyz (DAFE) | Typical TradingView Strategies|

|---------|-------------|------------------------------------------------------------|

| Regime Detection | Automatically identifies and adapts to **four** market regimes | Often static or limited to trend/range detection |

| Multi‑Timeframe Analysis | Uses higher‑timeframe RSI/MACD for confirmation | Rarely incorporates multi‑timeframe data |

| Pattern Recognition | Detects candlestick patterns **with volume confirmation** | Limited or no pattern recognition |

| Dynamic Risk Management | ATR‑based stops and trailing stops | Often uses fixed stops or basic risk rules |

| Performance Tracking | Adjusts thresholds based on past performance | Typically static parameters |

| Beginner‑Friendly Presets | Aggressive, Conservative, Optimized profiles | Requires manual parameter tuning |

| Visual Cues | Color‑coded backgrounds for regimes | Basic or no visual aids |

The Dskyz strategy’s ability to integrate regime detection, multi-timeframe analysis, and user-friendly presets makes it uniquely versatile and accessible, addressing the needs of everyday traders who want professional-grade tools without the complexity.

-Key Features and Benefits

[Why It’s Ideal for Everyday Traders

⚡The Dskyz (DAFE) AI Adaptive Regime - Pro democratizes advanced trading by offering professional-grade tools in an accessible package. Unlike many TradingView strategies that require deep technical knowledge or fail in changing market conditions, this strategy simplifies complex analysis while maintaining robustness. Its presets and visual aids make it easy for beginners to start, while its adaptive features and performance tracking appeal to advanced traders seeking an edge.

🔄Limitations and Considerations

Market Dependency: Performance varies by market and timeframe. Backtesting is essential to ensure compatibility with your trading style.

Learning Curve: While presets simplify use, understanding regimes and indicators enhances effectiveness.

No Guaranteed Profits: Like all strategies, success depends on market conditions and proper execution. The Reddit discussion highlights skepticism about TradingView strategies’ universal success (Reddit Discussion).

Instrument Specificity: Optimized for futures (e.g., ES, NQ) due to fixed tick values. Test on other instruments like stocks or forex to verify compatibility.

📌Conclusion

The Dskyz (DAFE) AI Adaptive Regime - Pro is a revolutionary TradingView strategy that empowers everyday traders with advanced, AI-driven tools. Its ability to adapt to market regimes, confirm signals across timeframes, and manage risk dynamically. sets it apart from typical strategies. By offering beginner-friendly presets and visual cues, it makes sophisticated trading accessible without sacrificing power. Whether you’re a novice looking to trade smarter or a pro seeking a competitive edge, this strategy is your ticket to mastering the markets. Add it to your chart, backtest it, and join the elite traders leveraging AI to dominate. Trade like a boss today! 🚀

Use it with discipline. Use it with clarity. Trade smarter.

**I will continue to release incredible strategies and indicators until I turn this into a brand or until someone offers me a contract.

-Dskyz

Standard Deviation (fadi)The Standard Deviation indicator uses standard deviation to map out price movements. Standard deviation measures how much prices stray from their average—small values mean steady trends, large ones mean wild swings. Drawing from up to 20 years of data, it plots key levels using customizable Fibonacci lines tied to that standard deviation, giving traders a snapshot of typical price behavior.

These levels align with a bell curve: about 68% of price moves stay within 1 standard deviation, 95% within roughly 2, and 99.7% within roughly 3. When prices break past the 1 StDev line, they’re outliers—only 32% of moves go that far. Prices often snap back to these lines or the average, though the reversal might not happen the same day.

How Traders Use It

If prices surge past the 1 StDev line, traders might wait for momentum to fade, then trade the pullback to that line or the average, setting a target and stop.

If prices dip below, they might buy, anticipating a bounce—sometimes a day or two later. It’s a tool to spot overstretched prices likely to revert and/or measure the odds of continuation.

Settings

Higher Timeframe: Sets the Higher Timeframe to calculate the Standard Deviation for

Show Levels for the Last X Days: Displays levels for the specified number of days.

Based on X Period: Number of days to calculate standard deviation (e.g., 20 years ≈ 5,040 days). Larger periods smooth out daily level changes.

Mirror Levels on the Other Side: Plots symmetric positive and negative levels around the average.

Fibonacci Levels Settings: Defines which levels and line styles to show. With mirroring, negative values aren’t needed.

Background Transparency: Turn on Background color derived from the level colors with the specified transparency

Overrides: Lets advanced users input custom standard deviations for specific tickers (e.g., NQ1! at 0.01296).

Daily Standard Deviation (fadi)The Daily Standard Deviation indicator uses standard deviation to map out daily price movements. Standard deviation measures how much prices stray from their average—small values mean steady trends, large ones mean wild swings. Drawing from up to 20 years of data, it plots key levels using customizable Fibonacci lines tied to that standard deviation, giving traders a snapshot of typical price behavior.

These levels align with a bell curve: about 68% of price moves stay within 1 standard deviation, 95% within roughly 2, and 99.7% within roughly 3. When prices break past the 1 StDev line, they’re outliers—only 32% of moves go that far. Prices often snap back to these lines or the average, though the reversal might not happen the same day.

How Traders Use It

If prices surge past the 1 StDev line, traders might wait for momentum to fade, then trade the pullback to that line or the average, setting a target and stop.

If prices dip below, they might buy, anticipating a bounce—sometimes a day or two later. It’s a tool to spot overstretched prices likely to revert and/or measure the odds of continuation.

Settings

Open Hour: Sets the trading day’s start (default: 18:00 EST).

Show Levels for the Last X Days: Displays levels for the specified number of days.

Based on X Period: Number of days to calculate standard deviation (e.g., 20 years ≈ 5,040 days). Larger periods smooth out daily level changes.

Mirror Levels on the Other Side: Plots symmetric positive and negative levels around the average.

Fibonacci Levels Settings: Defines which levels and line styles to show. With mirroring, negative values aren’t needed.

Overrides: Lets advanced users input custom standard deviations for specific tickers (e.g., NQ1! at 0.01296).

MA Multi-Timeframe [ChartPrime]The MA Multi-Timeframe indicator is designed to provide multi-timeframe moving averages (MAs) for better trend analysis across different periods. This tool allows traders to monitor up to four different MAs on a single chart, each coming from a selectable timeframe and type (SMA, EMA, SMMA, WMA, VWMA). The indicator helps traders gauge both short-term and long-term price trends, allowing for a clearer understanding of market dynamics.

⯁ KEY FEATURES AND HOW TO USE

⯌ Multi-Timeframe Moving Averages :

The indicator allows traders to select up to four MAs, each from different timeframes. These timeframes can be set in the input settings (e.g., Daily, Weekly, Monthly), and each moving average can be displayed with its corresponding timeframe label directly on the chart.

Example of different timeframes for MAs:

⯌ Moving Average Types :

Users can choose from several types of moving averages, including SMA, EMA, SMMA, WMA, and VWMA, making the indicator adaptable to different strategies and market conditions. This flexibility allows traders to tailor the MAs to their preference.

Example of different types of MAs:

⯌ Dashboard Display :

The indicator includes a built-in dashboard that shows each MA, its timeframe, and whether the price is currently above or below that MA. This dashboard provides a quick overview of the trend across different timeframes, allowing traders to determine whether the overall trend is up or down.

Example of trend overview via the dashboard:

⯌ Polyline Representation :

Each MA is plotted using polylines to avoid plot functions and create a curves across up to 4000 bars back, ensuring that historical data is visualized clearly for a deeper analysis of how the price interacts with these levels over time.

if barstate.islast

for i = 0 to 4000

cp.push(chart.point.from_index(bar_index , ma ))

polyline.delete(polyline.new(cp, curved = false, line_color = color, line_style = style) )

Example of polylines for moving averages:

⯌ Customization Options :

Traders can customize the length of the MAs for all timeframes using a single input. The color, style (solid, dashed, dotted) of each moving average are also customizable, giving users full control over the visual appearance of the indicator on their chart.

Example of custom MA styles:

⯁ USER INPUTS

MA Type : Select the type of moving average for each timeframe (SMA, EMA, SMMA, WMA, VWMA).

Timeframe : Choose the timeframe for each moving average (e.g., Daily, Weekly, Monthly).

MA Length : Set the length for the moving averages, which will be applied to all four MAs.

Line Style : Customize the style of each MA line (solid, dashed, or dotted).

Colors : Set the color for each MA for better visual distinction.

⯁ CONCLUSION

The MA Multi-Timeframe indicator is a versatile and powerful tool for traders looking to monitor price trends across multiple timeframes with different types of moving averages. The dashboard simplifies trend identification, while the customizable options make it easy to adapt to individual trading strategies. Whether you're analyzing short-term price movements or long-term trends, this indicator offers a comprehensive solution for tracking market direction.

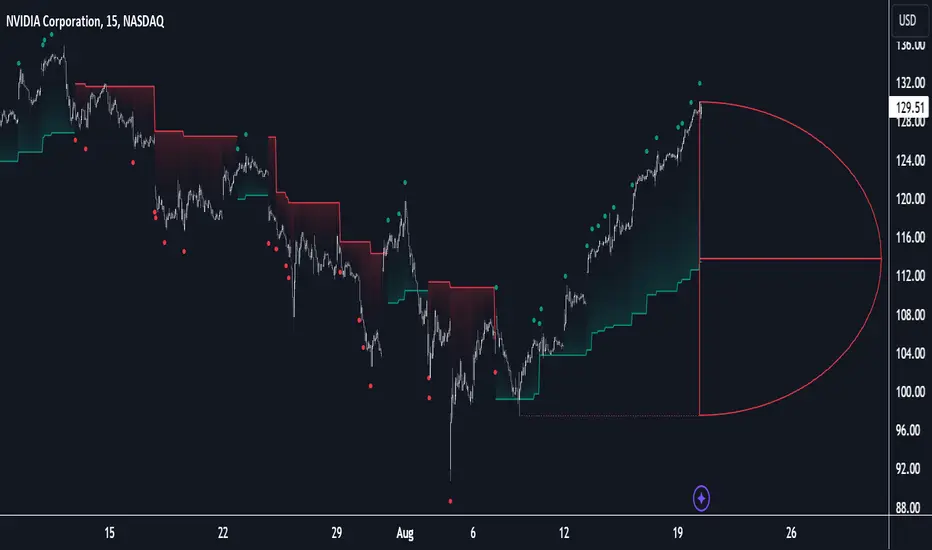

D-Shape Breakout Signals [LuxAlgo]The D-Shape Breakout Signals indicator uses a unique and novel technique to provide support/resistance curves, a trailing stop loss line, and visual breakout signals from semi-circular shapes.

🔶 USAGE

D-shape is a new concept where the distance between two Swing points is used to create a semi-circle/arc, where the width is expressed as a user-defined percentage of the radius. The resulting arc can be used as a potential support/resistance as well as a source of breakouts.

Users can adjust this percentage (width of the D-shape) in the settings ( "D-Width" ), which will influence breakouts and the Stop-Loss line.

🔹 Breakouts of D-Shape

The arc of this D-shape is used for detecting breakout signals between the price and the curve. Only one breakout per D-shape can occur.

A breakout is highlighted with a colored dot, signifying its location, with a green dot being used when the top part of the arc is exceeded, and red when the bottom part of the arc is surpassed.

When the price reaches the right side of the arc without breaking the arc top/bottom, a blue-colored dot is highlighted, signaling a "Neutral Breakout".

🔹 Trailing Stop-Loss Line

The script includes a Trailing Stop-Loss line (TSL), which is only updated when a breakout of the D-Shape occurs. The TSL will return the midline of the D-Shape subject to a breakout.

The TSL can be used as a stop-loss or entry-level but can also act as a potential support/resistance level or trend visualization.

🔶 DETAILS

A D-shape will initially be colored green when a Swing Low is followed by a Swing High, and red when a Swing Low is followed by a Swing High.

A breakout of the upper side of the D-shape will always update the color to green or to red when the breakout occurs in the lower part. A Neutral Breakout will result in a blue-colored D-shape. The transparency is lowered in the event of a breakout.

In the event of a D-shape breakout, the shape will be removed when the total number of visible D-Shapes exceeds the user set "Minimum Patterns" setting. Any D-shape whose boundaries have not been exceeded (and therefore still active) will remain visible.

🔹 Trailing Stop-Loss Line

Only when a breakout occurs will the midline of the D-shape closest to the closing price potentially become the new Trailing Stop value.

The script will only consider middle lines below the closing price on an upward breakout or middle lines above the closing price when it concerns a downward breakout.

In an uptrend, with an already available green TSL, the potential new Stop-Loss value must be higher than the previous TSL value; while in a downtrend, the new TSL value must be lower.

The Stop-Loss line won't be updated when a "Neutral Breakout" occurs.

🔶 SETTINGS

Swing Length: Period used for the swing detection, with higher values returning longer-term Swing Levels.

🔹 D-Patterns

Minimum Patterns: Minimum amount of visible D-Shape patterns.

D-Width: Width of the D-Shape as a percentage of the distance between both Swing Points.

Included Swings: Include "Swing High" (followed by a Swing Low), "Swing Low" (followed by a Swing High), or "Both"

Style Historical Patterns: Show the "Arc", "Midline" or "Both" of historical patterns.

🔹 Style

Label Size/Colors

Connecting Swing Level: Shows a line connecting the first Swing Point.

Color Fill: colorfill of Trailing Stop-Loss

Correlation AnalysisAs the name suggests, this indicator is a market correlation analysis tool.

It contains two main features:

- The Curve: represents the historic correlation coefficient between the current chart and the “Reference Market” input from the settings menu. It aims to give more depth to the current correlation values found in the second feature.

- The Screener: this second feature displays all correlation coefficient values between the (max) 20 markets inputs. You can use it to create several screeners for several market types (crypto, forex, metals, etc.) or even replicate your current portfolio of investments and gauge the correlation of its components.

Aside from these two previous features, you can visually plot the variation rate from one bar to another along with the covariance coefficient (both used in the correlation calculation). Finally, a simple “signal” moving average can be applied to the correlation coefficient .

I might add alerts to this script or even turn it into a strategy to do some backtesting. Do not hesitate to contact me or comment below if this is something you would be interested in or if you have any suggestions for improvement.

Enjoy!!

VHF Adaptive Linear Regression KAMAIntroduction

Heyo, in this indicator I decided to add VHF adaptivness, linear regression and smoothing to a KAMA in order to squeeze all out of it.

KAMA:

Developed by Perry Kaufman, Kaufman's Adaptive Moving Average (KAMA) is a moving average designed to account for market noise or volatility. KAMA will closely follow prices when the price swings are relatively small and the noise is low. KAMA will adjust when the price swings widen and follow prices from a greater distance. This trend-following indicator can be used to identify the overall trend, time turning points and filter price movements.

VHF:

Vertical Horizontal Filter (VHF) was created by Adam White to identify trending and ranging markets. VHF measures the level of trend activity, similar to ADX DI. Vertical Horizontal Filter does not, itself, generate trading signals, but determines whether signals are taken from trend or momentum indicators. Using this trend information, one is then able to derive an average cycle length.

Linear Regression Curve:

A line that best fits the prices specified over a user-defined time period.

This is very good to eliminate bad crosses of KAMA and the pric.

Usage

You can use this indicator on every timeframe I think. I mostly tested it on 1 min, 5 min and 15 min.

Signals

Enter Long -> crossover(close, kama) and crossover(kama, kama )

Enter Short -> crossunder(close, kama) and crossunder(kama, kama )

Thanks for checking this out!

--

Credits to

▪️@cheatcountry – Hann Window Smoohing

▪️@loxx – VHF and T3

▪️@LucF – Gradient

Power Law S/RBerger's article on the Power Law Model for Bitcoin is a compelling read and gives the best evidence so far of the diminishing case for retracing below $3000, of a slowing market on a log-log plot, and reducing but continued volatility.

After seeing it acts as support routinely in the last 10 years, I put together a quick little script that plots his midline curve for Bitcoin. You can change the intercept and slope but will need to do your own calculations for other curves.

I hope you all like it.

Savitzky-Golay Smoothing FilterThe Savitzky-Golay Filter is a polynomial smoothing filter.

This version implements 3rd degree polynomials using coefficients from Savitzky and Golay's table, specifically the coefficients for a 5-, 7-, 9-, 15- and 25-point window moving averages.

The filters are offset to the left by the number of coefficients (n-1)/2 so it smooths on top of the actual curve.

You can turn off some of the smoothing curves, as it can get cluttered displaying all at once.

Any feedback is very welcome.

Multi-Timeframe Recursive Zigzag [Trendoscope®]🎲 Welcome to the Advanced World of Zigzag Analysis

Embark on a journey through the most comprehensive and feature-rich Zigzag implementation you’ll ever encounter. Our Multi-Timeframe Recursive Zigzag Indicator is not just another tool; it's a groundbreaking advancement in technical analysis.

🎯 Key Features

Multi Time-Frame Support - One of the rare open-source Zigzag indicators with robust multi-timeframe capabilities, this feature sets our tool apart, enabling a broader and more dynamic market analysis.

Innovative Recursive Zigzag Algorithm - At its core is our unique Recursive Zigzag Algorithm, a pioneering development that powers multiple Zigzag levels, offering an intricate view of market movements. This proprietary algorithm is the backbone of our advanced pattern recognition indicators.

Sub-Waves and Micro-Waves Analysis - Dive deeper into market trends with our Sub-Waves and Micro-Waves feature. Sub-Waves reveal the interconnectedness of various Zigzag levels, while Micro-Waves offer insight into the fundamental waves at the base level.

Enhanced Indicator Tracking - Integrate and track your custom indicators or oscillators with the zigzag, capturing their values at each Zigzag level, complete with retracement ratios. This offers a comprehensive view of market dynamics.

Curved Zigzag Visualization - Experience a new way of visualizing market movements with our Curved Zigzag Display, employing Pine Script’s polyline feature for a more intuitive and visually appealing representation.

Built-in Customizable Alerts - Stay ahead with built-in alerts that can be customized via user input settings.

🎯 Practical Applications

Our Zigzag Indicator is designed with an understanding of its inherent nature - the last unconfirmed pivot that consistently repaints. This characteristic, while by design, directs its usage more towards pattern recognition rather than direct identification of market tops and bottoms. Here's how you can leverage the Zigzag Indicator:

Harmonic Patterns - Ideal for those familiar with harmonic patterns, this tool simplifies the manual spotting of complex XABCD, ABC, and ABCD patterns on charts.

Chart Patterns - Effortlessly identify patterns like Double/Triple Taps, Head and Shoulders, Inverse Head and Shoulders, and Cup and Handle patterns with enhanced clarity. Navigate through challenging patterns such as Triangles, Wedges, Flags, and Price Channels, where the Zigzag Indicator adds a layer of precision to your breakout strategy.

Elliott Wave Components - The indicator's detailed pivot highlighting aids in identifying key Elliott Wave components, enhancing your wave analysis and decision-making process.

🎲 Deep Dive into Indicator Features

Join us as we explore the intricate features of our indicator in more detail.

🎯 Multi-Timeframe Capability

Our indicator comes equipped with an input option for selecting the desired resolution. This unique feature allows users to view higher timeframe Zigzag patterns directly on their lower timeframe charts.

🎯 Recursive Multi Level Zigzag

Our advanced recursive approach creates multi-level Zigzags from lower-level data. For instance, the level 0 Zigzag forms the base, calculated from specified length and depth parameters, while level 1 Zigzag is derived using level 0 as its foundation, and so forth.

The indicator not only displays multiple Zigzag levels but also offers settings to emphasize specific levels for more detailed analysis.

🎯 Sub-Components and Micro-Components of Zigzag Wave

Sub-components within a Zigzag wave consist of the previous level's Zigzag pivots. Meanwhile, the micro-components are composed of the base level (Level 0) Zigzag pivots encapsulated within the wave.

🎯 Curved Zigzag

Experience a new perspective with our curved Zigzag display. This innovative feature utilizes the polyline curved option to automatically generate sinusoidal waves based on multiple points.

🎯 Indicator Tracking

Default indicators such as RSI, MFI, and OBV are included, alongside the ability to track one external indicator at each Zigzag pivot.

🎯 Customizable Alerts

Our indicator employs the `alert()` function for alert creation. While this means the absence of a customization text box in the alert settings, we've included a custom text area for users to create their own alert templates.

Template placeholders include:

{alertType} - type of alert. Either Confirmed Pivot Update or Last Pivot Update. Depends on the alert type selected in the inputs.

When Last Pivot Update type is selected, the alerts are triggered whenever there is a new Zigzag Pivot. This may also be a repaint of last unconfirmed pivot.

When Confirmed Pivot Update type is selected, the alerts are triggered only when a pivot becomes a confirmed pivot.

{level} - Zigzag level on which the alert is triggered.

{pivot} - Details of the last pivot or confirmed pivot including price, ratio, indicator values and ratios, subcomponent and micro-component pivots.

🎲 User Settings Overview

🎯 Zigzag and Generic Settings

This involves some generic zigzag calculation settings such as length, depth, and timeframe. And few display options such as theme, Highlight Level and Curved Zigzag. By default, zigzag calculation is done based on the latest real time bar. An option is provided to disable this and use only confirmed bars for the calculation.

Indicator Settings

Allows users to track one or more oscillators or volume indicators. Option to add any indicator via external input is provided.

🎯 Alert Settings

Has input fields required to select and customize alerts.

Polynomial Regression Channel [ChartPrime]⯁ OVERVIEW

The Polynomial Regression Channel fits price action using advanced polynomial regression, extending beyond simple linear or logarithmic models. By leveraging matrix calculations, it builds a curved regression line that adapts to swings more naturally. The channel includes extrapolated forward projections, helping traders visualize where price may gravitate in the near future. Midline color shifts reflect directional bias, while prediction ranges are marked with dashed extensions, labeled prices, and a live table for clarity.

⯁ KEY FEATURES

Polynomial Regression Core:

Uses matrix algebra to calculate a polynomial fit of customizable degree, adapting to complex, non-linear market structures.

polyreg(source, length, degree, extrapolate) =>

total = length + extrapolate

X_all = matrix.new(total, degree + 1, 0.0)

for i = 0 to total - 1

for j = 0 to degree

matrix.set(X_all, i, j, math.pow(i, j))

// y (length × 1), oldest→newest over the fit window

y = matrix.new(length, 1, 0.0)

for i = 0 to length - 1

matrix.set(y, i, 0, source )

// X_train (first `length` rows of X_all)

X_tr = matrix.new(length, degree + 1, 0.0)

for i = 0 to length - 1

for j = 0 to degree

matrix.set(X_tr, i, j, matrix.get(X_all, i, j))

// OLS via normal equations: (X'X)^(-1)b = X'y ⇒ b = (X'X)^(-1) X'y

Xt = matrix.transpose(X_tr) // X'

XtX = matrix.mult(Xt, X_tr) // (X'X)

Xty = matrix.mult(Xt, y) // X'y

XtX_inv = matrix.inv(XtX) // (X'X)^(-1)

b = matrix.mult(XtX_inv, Xty) // b = (X'X)^(-1) X'y

// Predictions for all rows (fit + extrap)

preds = matrix.mult(X_all, matrix.col(b,0))

preds

Extrapolated Future Projections:

Forward-looking range (dashed lines + circular markers) shows where the fitted polynomial suggests price may move.

Dynamic Midline Coloring:

Regression midline shifts green when slope turns upward and magenta when slope turns downward, giving instant directional context.

Channel Boundaries:

Upper and lower levels expand from the midline using a volatility-based offset, framing potential overbought and oversold conditions.

Top-Right Data Table:

A live table displays Upper, Middle, and Lower Prediction values, updating in real time for quick reference without scanning the chart.

⯁ USAGE

Use the regression midline to gauge underlying market bias; green slopes suggest continuation, magenta slopes caution for weakness.

Watch dashed extrapolated ranges as potential targets or reaction zones during upcoming sessions.

Price labels and table values act as precise reference levels for planning entries, exits, or stop placement.

Increase Degree for more curve-fitting on choppy markets, or keep it low for broader trend approximation.

Adjust Period and Extrapolate length to balance stability vs. responsiveness.

⯁ CONCLUSION

The Polynomial Regression Channel offers a mathematically advanced way to visualize price trends and anticipate future paths. With matrix-driven polynomial fitting, extrapolated projections, and integrated live labels, it combines statistical rigor with practical trading visuals — a robust upgrade over standard regression channels.

KernelFunctionsLibrary "KernelFunctions"

This library provides non-repainting kernel functions for Nadaraya-Watson estimator implementations. This allows for easy substition/comparison of different kernel functions for one another in indicators. Furthermore, kernels can easily be combined with other kernels to create newer, more customized kernels.

rationalQuadratic(_src, _lookback, _relativeWeight, startAtBar)

Rational Quadratic Kernel - An infinite sum of Gaussian Kernels of different length scales.

Parameters:

_src (float) : The source series.

_lookback (simple int) : The number of bars used for the estimation. This is a sliding value that represents the most recent historical bars.

_relativeWeight (simple float) : Relative weighting of time frames. Smaller values resut in a more stretched out curve and larger values will result in a more wiggly curve. As this value approaches zero, the longer time frames will exert more influence on the estimation. As this value approaches infinity, the behavior of the Rational Quadratic Kernel will become identical to the Gaussian kernel.

startAtBar (simple int)

Returns: yhat The estimated values according to the Rational Quadratic Kernel.

gaussian(_src, _lookback, startAtBar)

Gaussian Kernel - A weighted average of the source series. The weights are determined by the Radial Basis Function (RBF).

Parameters:

_src (float) : The source series.

_lookback (simple int) : The number of bars used for the estimation. This is a sliding value that represents the most recent historical bars.

startAtBar (simple int)

Returns: yhat The estimated values according to the Gaussian Kernel.

periodic(_src, _lookback, _period, startAtBar)

Periodic Kernel - The periodic kernel (derived by David Mackay) allows one to model functions which repeat themselves exactly.

Parameters:

_src (float) : The source series.

_lookback (simple int) : The number of bars used for the estimation. This is a sliding value that represents the most recent historical bars.

_period (simple int) : The distance between repititions of the function.

startAtBar (simple int)

Returns: yhat The estimated values according to the Periodic Kernel.

locallyPeriodic(_src, _lookback, _period, startAtBar)

Locally Periodic Kernel - The locally periodic kernel is a periodic function that slowly varies with time. It is the product of the Periodic Kernel and the Gaussian Kernel.

Parameters:

_src (float) : The source series.

_lookback (simple int) : The number of bars used for the estimation. This is a sliding value that represents the most recent historical bars.

_period (simple int) : The distance between repititions of the function.

startAtBar (simple int)

Returns: yhat The estimated values according to the Locally Periodic Kernel.

Ellipse Price Action Indicator v2 (Upgraded)

This upgraded Ellipse Price Action Indicator (EPAI v2) to take high-accuracy trades.

I am explaining it as if you are looking at the chart step by step, so you will understand exactly:

-When to buy

-When to

-When to avoid

-How to read Strength Meter

-How Ellipse zones work

⭐ 1. THE BASICS — What This Indicator Actually Does

This indicator tracks:

✔ The “Elliptical Path” of price

Like a planet revolving around the Sun, price “oscillates” around a center.

The indicator detects this hidden mathematical path using:

Two Focus Points (Fast MA & Slow MA)

Curved Ellipse boundaries

Compression of price

Momentum of trend

Breakout zones

⭐ 2. UNDERSTANDING THE 3 ZONES

🔴 UPPER ZONE = Sell Zone

Price is near the upper ellipse boundary → overbought space.

🟢 LOWER ZONE = Buy Zone

Price near lower ellipse boundary → oversold space.

🔵 CENTRAL ZONE = No Trade Zone

Price swinging inside the ellipse center → noise.

Only trade in UPPER or LOWER zones.

Never in the central zone.

⭐ 3. THE MOST IMPORTANT PART — Strength Meter v2

Strength Meter v2 (0 to 100%) is the core filter.

✔ Above 70% → High winning probability (take trade)

✔ 60–70% → Medium probability (trade if confident)

❌ Below 60% → Avoid trade

Strength combines:

Ellipse compression

Momentum slope

Price position curve

Eccentricity

Trend direction

This alone removes 70% bad trades.

⭐ 4. BUY SETUP (Exact Rules)

You get a BUY only if all conditions match:

① Price goes to lower ellipse zone

② Compression is ON (ellipse is tight)

③ Momentum slope direction = UP

④ Focus Lines Cross Bullish (Fast > Slow)

⑤ Strength v2 ≥ your threshold (default 60%)

⑥ A BUY signal prints (triangle UP)

When these align →

🟢 BUY with high accuracy

Best Accuracy Buy is:

Price in lower zone

Strength ≥ 0.75

Slope UP

Ellipse compressed

⭐ 5. SELL SETUP (Exact Rules)

Same logic reversed:

① Price in upper ellipse zone

② Compression ON

③ Momentum slope DOWN

④ Focus Lines cross bearish (Fast < Slow)

⑤ Strength v2 ≥ threshold

⑥ SELL signal prints (triangle DOWN)

This means:

🔴 SELL with high accuracy

Best Accuracy Sell is:

Price in upper zone

Strength ≥ 0.75

Slope DOWN

Ellipse compressed

⭐ 6. BREAKOUT TRADES (Optional but powerful)

When price breaks above/below ellipse:

🔸 Upper Breakout → SELL (if strength strong)

🔸 Lower Breakout → BUY (if strength strong)

Breakout signals are marked by orange arrows.

Breakouts are taken only if:

Strength v2 > 50%

Slope supports breakout

Compression exists before breakout

Breakout trades catch trend continuation.

⭐ 7. HOW TO CONFIRM A STRONG TRADE

Look at the table on the chart:

✔ Strength v2 ≥ 70% (GREEN)

✔ Compression = GREEN

✔ Slope direction = UP (for buy) or DOWN (for sell)

✔ Zone = LOWER or UPPER

✔ Eccentricity = LOW (<0.5 means smooth trend)

If these line up →

⭐ High-probability entry.

⭐ 8. WHEN YOU SHOULD NOT TRADE

❌ If price is in Central Zone

❌ Strength < 60

❌ No compression detected

❌ Slope is flat or against direction

❌ Only one condition is matching

❌ Eccentricity is too large

(Big ellipse = unpredictable swings)

⭐ 9. What Is the Accuracy Level?

In trending markets → 75% to 85% accuracy

In ranging markets → 50% (use compression filter to avoid)

The indicator is designed to avoid bad market conditions automatically.

⭐ 10. BEST TIMEFRAMES

✔ 5m, 15m, 1H → Intraday

✔ 4H, 1D → Swing Trading

✔ NOT recommended below 1m timeframe

⭐ SUMMARY (EASY VERSION)

🟢 BUY:

Lower zone + compression + bullish slope + strong focus cross + strength ≥ 60

🔴 SELL:

Upper zone + compression + bearish slope + strong focus cross + strength ≥ 60

🟠 Breakout:

Upper/lower breakout + strength ≥ 50

🔵 Avoid:

Central zone or weak strength

Log Regression Channel (Dezza Fixed v2)This custom indicator builds a curved Logarithmic Regression Channel designed for long-term Bitcoin and macro asset analysis. It performs a linear regression on the logarithm of price to estimate the market’s fair-value growth curve, then converts that back into price space to form upper and lower deviation bands.

It helps identify where price sits relative to its long-term exponential trend — showing potential overvaluation (upper band) or undervaluation (lower band) zones.

Best used on weekly or monthly charts to visualise market cycles and fair-value reversion. Adjustable inputs let you control lookback length, band width, and midline visibility.

Log Regression Channel (Dezza)This custom indicator builds a curved Logarithmic Regression Channel designed for long-term Bitcoin and macro asset analysis. It performs a linear regression on the logarithm of price to estimate the market’s fair-value growth curve, then converts that back into price space to form upper and lower deviation bands.

It helps identify where price sits relative to its long-term exponential trend — showing potential overvaluation (upper band) or undervaluation (lower band) zones.

Best used on weekly or monthly charts to visualise market cycles and fair-value reversion. Adjustable inputs let you control lookback length, band width, and midline visibility.

Volume Weighted Linear Regression BandThe Volume-Weighted Linear Regression Band (VWLRBd) is a volatility channel that uses a Linear Regression line as its dynamic baseline. Its primary feature is the decomposition of total volatility into two distinct components, visualized as layered bands.

Key Features:

Volatility Decomposition: The indicator separates volatility based on the 'Estimate Bar Statistics' option.

Standard Mode (Estimate Bar Statistics = OFF): The indicator functions as a standard (Volume-Weighted) Linear Regression Channel. It plots a single set of bands based on the standard deviation of the residuals (the error between the Source price and the regression line).

Decomposition Mode (Estimate Bar Statistics = ON): The indicator uses a statistical model ('Estimator') to calculate within-bar volatility. (Assumption: In this mode, the Source input is ignored, and an estimated mean for each bar is used for the regression). This mode displays two sets of bands:

Inner Bands: Show only the contribution of the 'residual' (trend noise) volatility, calculated proportionally.

Outer Bands: Show the total volatility (the sum of residual and within-bar components).

Regression Baseline (Linear / Exponential): The central line is a (Volume-Weighted) Linear Regression curve. An optional 'Normalize' mode performs all calculations in logarithmic space, transforming the baseline into an Exponential Regression Curve and the bands into constant percentage deviations, suitable for analyzing growth assets.

Volume Weighting: An option (Volume weighted) allows for volume to be incorporated into the calculation of both the regression baseline and the volatility decomposition, giving more influence to high-participation bars.

Multi-Timeframe (MTF) Engine: The indicator includes an MTF conversion block. When a Higher Timeframe (HTF) is selected, advanced options become available: Fill Gaps handles data gaps, and Wait for timeframe to close prevents repainting by ensuring the indicator only updates when the HTF bar closes.

Integrated Alerts: Includes a full set of built-in alerts for the source price crossing over or under the central regression line and the outermost calculated volatility band.

DISCLAIM_

For Informational/Educational Use Only: This indicator is provided for informational and educational purposes only. It does not constitute financial, investment, or trading advice, nor is it a recommendation to buy or sell any asset.

Use at Your Own Risk: All trading decisions you make based on the information or signals generated by this indicator are made solely at your own risk.

No Guarantee of Performance: Past performance is not an indicator of future results. The author makes no guarantee regarding the accuracy of the signals or future profitability.

No Liability: The author shall not be held liable for any financial losses or damages incurred directly or indirectly from the use of this indicator.

Signals Are Not Recommendations: The alerts and visual signals (e.g., crossovers) generated by this tool are not direct recommendations to buy or sell. They are technical observations for your own analysis and consideration.

Quantum Flux Universal Strategy Summary in one paragraph

Quantum Flux Universal is a regime switching strategy for stocks, ETFs, index futures, major FX pairs, and liquid crypto on intraday and swing timeframes. It helps you act only when the normalized core signal and its guide agree on direction. It is original because the engine fuses three adaptive drivers into the smoothing gains itself. Directional intensity is measured with binary entropy, path efficiency shapes trend quality, and a volatility squash preserves contrast. Add it to a clean chart, watch the polarity lane and background, and trade from positive or negative alignment. For conservative workflows use on bar close in the alert settings when you add alerts in a later version.

Scope and intent

• Markets. Large cap equities and ETFs. Index futures. Major FX pairs. Liquid crypto

• Timeframes. One minute to daily

• Default demo used in the publication. QQQ on one hour

• Purpose. Provide a robust and portable way to detect when momentum and confirmation align, while dampening chop and preserving turns

• Limits. This is a strategy. Orders are simulated on standard candles only

Originality and usefulness

• Unique concept or fusion. The novelty sits in the gain map. Instead of gating separate indicators, the model mixes three drivers into the adaptive gains that power two one pole filters. Directional entropy measures how one sided recent movement has been. Kaufman style path efficiency scores how direct the path has been. A volatility squash stabilizes step size. The drivers are blended into the gains with visible inputs for strength, windows, and clamps.

• What failure mode it addresses. False starts in chop and whipsaw after fast spikes. Efficiency and the squash reduce over reaction in noise.

• Testability. Every component has an input. You can lengthen or shorten each window and change the normalization mode. The polarity plot and background provide a direct readout of state.

• Portable yardstick. The core is normalized with three options. Z score, percent rank mapped to a symmetric range, and MAD based Z score. Clamp bounds define the effective unit so context transfers across symbols.

Method overview in plain language

The strategy computes two smoothed tracks from the chart price source. The fast track and the slow track use gains that are not fixed. Each gain is modulated by three drivers. A driver for directional intensity, a driver for path efficiency, and a driver for volatility. The difference between the fast and the slow tracks forms the raw flux. A small phase assist reduces lag by subtracting a portion of the delayed value. The flux is then normalized. A guide line is an EMA of a small lead on the flux. When the flux and its guide are both above zero, the polarity is positive. When both are below zero, the polarity is negative. Polarity changes create the trade direction.

Base measures

• Return basis. The step is the change in the chosen price source. Its absolute value feeds the volatility estimate. Mean absolute step over the window gives a stable scale.