5-Year Returns Chart BTCvsSPXvsGOLDvsNVDACompare between thes 4 assets:

BTC

NVDA

SPX

GOLD

With an initial 1000$ investment in the last 5 years each return

"btc期权交割时间" için komut dosyalarını ara

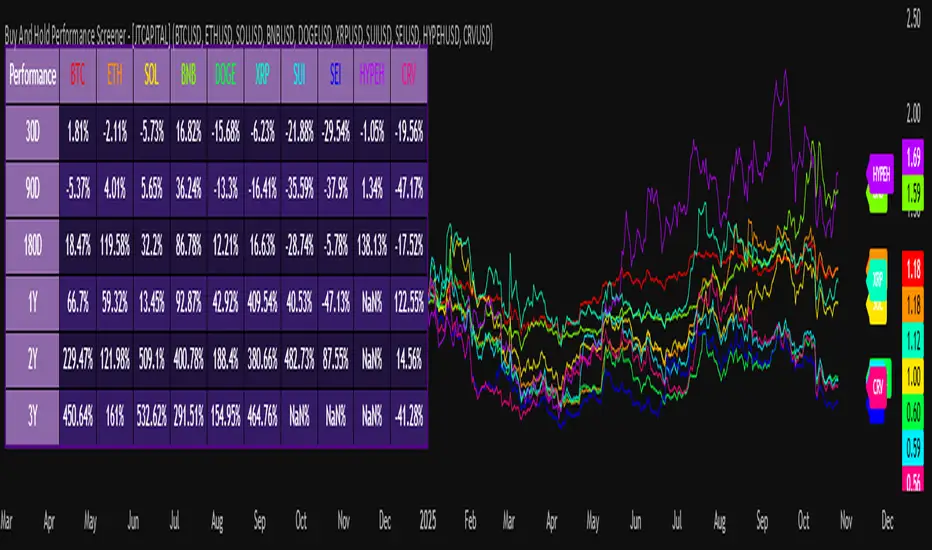

Buy And Hold Performance Screener - [JTCAPITAL]Buy And Hold Performance Screener – is a script designed to track and display multi-asset “buy and hold” performance curves and performance statistics over defined timeframes for selected symbols. It doesn’t attempt to time entries or exits; rather, it shows what would happen if one simply bought the asset at the defined start date and held it.

The indicator works by calculating in the following steps:

Start Date Definition

The script begins by reading an input for the start date. This defines the bar from which the equity curves begin.

Symbol Definitions & Close Price Retrieval

The script allows the user to specify up to ten tickers. For each ticker it uses request.security() on the “1D” timeframe to retrieve the daily close price of that symbol.

Plot Enable Inputs

For each ticker there is an input boolean controlling whether the equity curve for that ticker should be plotted.

Asset Name Cleaning

The helper function clean_name(string asset) => … takes the asset string (e.g., “CRYPTO:SOLUSD”) and manipulates it (via string splitting and replacements) to derive a cleaned short name (e.g., “SOL”). This name is used for visuals (labels, table headers).

Equity Curve Calculation (“HODL”)

The helper function f_HODL(closez) defines a variable equity that assumes a starting equity of 1 unit at the start date and then multiplies by the ratio of each bar’s close to the prior bar’s close: i.e. daily compounding of returns.

Performance Metrics Calculation

The helper function f_performance(closez) calculates, for each symbol’s close series, the percentage change of the current close relative to its close 30 days ago, 90 days ago, 180 days ago, 1 year ago (365 days), 2 years ago (730 days) and 3 years ago (1095 days).

Equity Curve Plots

For each ticker, if the corresponding plot input is true, the script assigns a plotted variable equal to the equity curve value. Its then drawing each selected equity curve on the chart, each in a distinct color.

Table Construction

If the plottable input is true, the script constructs a table and populates it with rows and column corresponding to the assigned tickers and the set 6 timeframes used for display.

Buy and Sell Conditions:

Since this is strictly a “buy-and-hold” performance screener, there are no explicit buy or sell signals generated or plotted. The script assumes: buy at the defined start_date, hold continuously to present. There are no filters, no exit logic, no take-profit or stop-loss. The benefit of this approach is to provide a clean benchmark of how selected assets would have performed if one simply adopted a passive “buy & hold” approach from a given start date.

Features and Parameters:

start_date (input.time) : Defines the date from which performance and equity curves begin.

ticker1 … ticker10 (input.symbol) : User-selectable asset symbols to include in the screener.

plot1 … plot10 (input.bool) : Boolean flags to enable/disable plotting of each asset’s equity curve.

plottable (input.bool) : Flag to enable/disable drawing the performance table.

Colored plotting + Labels for identifying each asset curve on the chart.

Specifications:

Here is a detailed breakdown of every calculation/variable/function used in the script and what each part means:

start_date

This is defined via input.time(timestamp("1 Jan 2025"), title = "Start Date"). It allows the user to pick a specific calendar date from which the equity curves and performance calculations will start.

ticker1 … ticker10

These inputs allow the user to select up to ten different assets (symbols) to monitor. The script uses each of these to fetch daily close prices.

plot1 … plot10

Boolean inputs controlling which of the ten asset equity curves are plotted. If plotX is true, the equity curve for ticker X will be visible; otherwise it will be not plotted. This gives the user flexibility to include or exclude specific assets on the chart.

Returns the cleaned asset short name.

This provides friendly text labels like “BTC”, “ETH”, “SOL”, etc., instead of full symbol codes.

The choice of distinct colours for each asset helps differentiate curves visually when multiple assets are overlaid.

Colour definitions

Variables color1…color10 are explicitly defined via color.rgb(r,g,b) to give each asset a unique colour (e.g., red, orange, yellow, green, cyan, blue, purple, pink, etc.).

What are the benefits of combining these calculations?

By computing equity curves for multiple assets from the same start date and overlaying them, you can visualise comparative performance of different assets under a uniform “buy & hold” assumption.

The performance table adds multi-horizon returns (30 D, 90 D, 180 D, 1 Y, 2 Y, 3 Y) which helps the user see both short-term and longer-term performance without having to manually compute returns.

The use of daily close data via request.security(..., "1D") removes dependency on the chart’s timeframe, thereby standardising the comparison across assets.

The equity curve and table together provide both visual (curve) and numerical (table) summaries of performance, making it easier to spot trends, divergences, and cross-asset comparisons at a glance.

Because it uses compounding (equity := equity * (closez / closez )), the curves reflect the real growth of a 1-unit investment held over time, rather than only simple returns.

The labelling of curves and the color-coding make the multi-asset overlay easier to interpret.

Using a clean start date ensures that all curves begin at the same point (1 unit at start_date), making relative performance intuitive.

Because of this, the script is useful as a benchmarking tool: rather than trying to pick entries or exit points, you can simply compare “what if I had held these assets since Jan 1 2025” (or your chosen date), and see which assets out-/under-performed in that period. It helps an investor or trader evaluate the long-term benefits of passive vs. active management, or of allocation decisions.

Please note:

The script assumes continuous daily data and does not account for dividends, fees, slippage, or tax implications.

It does not attempt to optimise timing or provide trading signals.

Returns prior to the start date are ignored (equity only begins once time >= start_date).

For newly listed assets with fewer than 365 or 730 or 1095 days of history, the longer-horizon returns may return na or misleading values.

Because it uses request.security() without specifying lookahead, and on “1D” timeframe, it complies with standard usage but you should verify there is no look-ahead bias in your particular setup.

ENJOY!

Crypto Index Price# Crypto Index Price - Indicator Description

## 📊 What is this indicator?

**Crypto Index Price** is an indicator for creating your own cryptocurrency index based on an equal-weighted portfolio. It allows you to track the overall dynamics of the cryptocurrency market through a composite index of selected assets.

## 🎯 Key Features

- **Up to 20 assets in the index** — create an index from any trading pairs

- **Equal-weighted methodology** — each asset has the same weight in the index

- **Moving average** — optional trend filter for the index

- **Flexible visualization settings** — customizable colors and line thickness

## 📈 How to Use

The indicator is displayed in a separate pane below the chart and shows:

1. **Blue line** — crypto index value

2. **Orange line** (optional) — moving average of the index

### Trading Applications:

- **Identify overall market trend** — if the index is rising, most coins are in an uptrend

- **Divergences** — divergence between your asset and the index may signal local opportunities

- **Signal confirmation** — use the index to confirm trading decisions on individual coins

- **Market condition filter** — trade longs when index is above MA, shorts when below

## ⚙️ Settings

### Assets (Symbols)

- **Asset 1-10** — main cryptocurrencies (default: BTC, ETH, BNB, SOL, XRP, ADA, AVAX, LINK, DOGE, TRX)

- **Asset 11-20** — additional slots for index expansion

### Visual Parameters

- **Index line color** — main line color (default: blue)

- **Line width** — from 1 to 5 pixels

- **Show moving average** — enable/disable MA

- **MA period** — moving average calculation period (default: 20)

- **MA color** — moving average line color (default: orange)

## 💡 Recommendations

- For a top coins index, use 5-10 largest cryptocurrencies by market cap

- For an altcoin index, add medium and small coins from your sector

- Use MA to filter false signals and identify the global trend

- Compare individual asset behavior with the index to find anomalies

## ⚠️ Important

The indicator uses equal-weighted methodology — each coin contributes equally regardless of price or market cap. This differs from cap-weighted indices and may provide a different market perspective.

---

*This indicator is intended for analysis and is not trading advice. Always conduct your own analysis before making trading decisions.*

---

Fib OscillatorWhat is Fib Oscillator and How to Use it?

🔶 1. Conceptual Overview

The Fib Oscillator is a Fibonacci-based relative position oscillator.

Instead of measuring momentum (like RSI or MACD), it measures where price currently sits between the recent swing high and swing low, expressed as a percentage within the Fibonacci range.

In other words:

It answers: “Where is price right now within its most recent dynamic range?”

It visualizes retracement and extension zones numerically, providing continuous feedback between 0% and 100% (and beyond if extended).

🔶 2. What the Script Does

The indicator:

Automatically detects recent high and low levels using an adaptive lookback window, which depends on ATR volatility.

Calculates the current price’s position between those levels as a percentage (0–100).

Plots that percentage as an oscillator — showing visually whether price is near the top, middle, or bottom of its recent range.

Overlays Fibonacci retracement levels (23.6%, 38.2%, 50%, 61.8%, 78.6%) as reference zones.

Generates alerts when the oscillator crosses key Fib thresholds — which can signal retracement completion, breakout potential, or pullback exhaustion.

🔶 3. Technical Flow Breakdown

(a) Inputs

Input Description Default Notes

atrLength ATR period used for volatility estimation 14 Used to dynamically tune lookback sensitivity

minLookback Minimum lookback window (candles) 20 Ensures stability even in low volatility

maxLookback Maximum lookback window 100 Limits over-expansion during high volatility

isInverse Inverts chart orientation false Useful for inverse markets (e.g. shorts or inverse BTC view)

(b) Volatility-Adaptive Lookback

Instead of using a fixed lookback, it calculates:

lookback

=

SMA(ATR,10)

/

SMA(Close,10)

×

500

lookback=SMA(ATR,10)/SMA(Close,10)×500

Then it clamps this between minLookback and maxLookback.

This makes the oscillator:

More reactive during high volatility (shorter lookback)

More stable during calm markets (longer lookback)

Essentially, it self-adjusts to market rhythm — you don’t have to constantly tweak lookback manually.

(c) High-Low Reference Points

It takes the highest and lowest points within the dynamic lookback window.

If isInverse = true, it flips the candle logic (useful if viewing inverse instruments like stablecoin pairs or when analyzing bearish setups invertedly).

(d) Oscillator Core

The main oscillator line:

osc

=

(

close

−

low

)

(

high

−

low

)

×

100

osc=

(high−low)

(close−low)

×100

0% = Price is at the lookback low.

100% = Price is at the lookback high.

50% = Midpoint (balanced).

Between Fibonacci percentages (23.6%, 38.2%, 61.8%, etc.), the oscillator indicates retracement stages.

(e) Fibonacci Levels as Reference

It overlays horizontal reference lines at:

0%, 23.6%, 38.2%, 50%, 61.8%, 78.6%, 100%

These act as support/resistance bands in oscillator space.

You can read it similar to how traders use Fibonacci retracements on charts, but compressed into a single line oscillator.

(f) Alerts

The script includes built-in alert conditions for crossovers at each major Fibonacci level.

You can set TradingView alerts such as:

“Oscillator crossed above 61.8%” → possible bullish continuation or breakout.

“Oscillator crossed below 38.2%” → possible pullback or correction starting.

This allows automated monitoring of fib retracement completions without manually drawing fib levels.

🔶 4. How to Use It

🔸 Visual Interpretation

Oscillator Value Zone Market Context

0–23.6% Deep Retracement Potential exhaustion of a down-move / early reversal

23.6–38.2% Shallow retracement zone Possible continuation phase

38.2–50% Mid retracement Neutral or indecisive structure

50–61.8% Key pivot region Common trend resumption zone

61.8–78.6% Late retracement Often “last pullback” area

78.6–100% Near high range Possible overextension / profit-taking

>100% Range breakout New leg formation / expansion

🔸 Practical Application Steps

Load the indicator on your chart (set overlay = false, so it’s below the main price chart).

Observe oscillator position relative to fib bands:

Use it to determine retracement depth.

Combine with structure tools:

Trend lines, swing points, or HTF market structure.

Use crossovers for timing:

Crossing above 61.8% in an uptrend often confirms breakout continuation.

Crossing below 38.2% in a downtrend signals renewed downside momentum.

For range markets, oscillator swings between 23.6% and 78.6% can define accumulation/distribution boundaries.

🔶 5. When to Use It

During Retracements: To gauge how deep the pullback has gone.

During Range Markets: To identify relative overbought/oversold positions.

Before Breakouts: Crossovers of 61.8% or 78.6% often precede impulsive moves.

In Multi-Timeframe Contexts:

LTF (15M–1H): Detect intraday retracement exhaustion.

HTF (4H–1D): Confirm major range expansions or key reversal zones.

🔶 6. Ideal Companion Indicators

The Fib Oscillator works best when contextualized with structure, volatility, and trend bias indicators.

Below are optimal pairings:

Companion Indicator Purpose Integration Insight

Market Structure MTF Tool Identify active trend direction Use Fib Oscillator only in trend direction for cleaner signals

EMA Ribbon / Supertrend Trend confirmation Align oscillator crossovers with EMA bias

ATR Bands / Volatility Envelope Validate breakout strength If oscillator >78.6% & ATR rising → valid breakout

Volume Oscillator Confirm retracement strength Volume contraction + oscillator under 38.2% → potential reversal

HTF Fib Retracement Tool Combine LTF oscillator with HTF fib confluence Powerful multi-timeframe setups

RSI or Stochastic Measure momentum relative to position RSI divergence while oscillator near 78.6% → exhaustion clue

🔶 7. Understanding the Settings

Setting Function Practical Impact

ATR Period (14) Controls volatility sampling Higher = smoother lookback adaptation

Min Lookback (20) Smallest window allowed Lower = more reactive but noisier

Max Lookback (100) Largest window allowed Higher = smoother but slower to react

Inverse Candle Chart Flips oscillator vertically Useful when analyzing bearish or inverse scenarios (e.g. short-side fib mapping)

Recommended Configs:

For scalping/intraday: ATR 10–14, lookback 20–50

For swing/position trading: ATR 14–21, lookback 50–100

🔶 8. Example Trade Logic (Practical Use)

Scenario: Uptrend on 4H chart

Oscillator drops to below 38.2% → retracement zone

Price consolidates → oscillator stabilizes

Oscillator crosses above 50% → pullback ending

Entry: Long when oscillator crosses above 61.8%

Exit: Near 78.6–100% zone or upon divergence with RSI

For Short Bias (Inverse Setup):

Enable isInverse = true to visually flip the oscillator (so lows become highs).

Use the same thresholds inversely.

🔶 9. Strengths & Limitations

✅ Strengths

Dynamic, self-adapting to volatility

Quantifies Fib retracement as a continuous function

Compact oscillator view (no clutter on chart)

Works well across all timeframes

Compatible with both trending and ranging markets

⚠️ Limitations

Doesn’t define trend direction — must be used with structure filters

Can whipsaw during choppy consolidations

The “lookback auto-adjust” may lag in sudden volatility shifts

Shouldn’t be used standalone for entries without structural confluence

🔶 10. Summary

The “Fib Oscillator” is a dynamic Fibonacci-relative positioning tool that merges retracement theory with adaptive volatility logic.

It gives traders an intuitive, quantified view of where price sits within its recent fib range, allowing anticipation of pullbacks, reversals, or breakout momentum.

Think of it as a "Fibonacci RSI", but instead of momentum strength, it shows positional depth — the vibrational location of price within its natural swing cycle.

Relative Valuation OscillatorRelative Valuation Oscillator (RVO) Description

The Valuation_OTC.pine script is a Relative Valuation Oscillator for TradingView that compares the current asset against a reference asset (like Bitcoin, S&P 500, or Gold) to determine if it's relatively overvalued or undervalued.

Key Features:

1. Multiple Calculation Methods:

Simple Ratio - Compares price ratio deviation from average

Percentage Difference - Direct percentage comparison between assets

Ratio Z-Score - Statistical measure (standard deviations from mean)

Rate of Change Comparison - Compares momentum/performance

Normalized Ratio - 0-100 scale centered at zero

2. Customizable Settings:

Reference asset selection (default: BTC/USDT)

Adjustable lookback period (10-500 bars)

Optional smoothing with configurable period

Overbought/oversold level thresholds (default: ±1.5)

3. Trading Signals:

Overvalued - Oscillator above overbought level (red zone)

Undervalued - Oscillator below oversold level (green zone)

Neutral - Between thresholds

Crossover alerts for key levels

Divergence detection (bullish/bearish)

4. Visual Components:

Color-coded oscillator line (green when positive, red when negative)

Optional signal line for additional smoothing

Background shading for valuation zones

Information table showing current metrics and status

Shape markers for crossovers and divergences

5. Alert Conditions:

Overvalued/undervalued alerts

Zero-line crossovers

Divergence signals

This indicator is useful for pairs trading, relative strength analysis, and identifying when an asset is trading at extremes relative to a benchmark asset.

Dot traderInterpret Signals: Green triangles indicate buy (e.g., if BTC holds $109k with bullish crossover); red triangles indicate sell (e.g., if it breaks $108k with bearish divergence).

Candle Colors: Green/bullish, red/bearish, orange/overbought (>70 RSI), blue/oversold (<30 RSI).

Alerts: Enable in TradingView for real-time notifications.

CHOCH + FVG Signals [30m Optimized]CHOCH + FVG Signals

🎯 What It Does:

This script automatically scans your chart for high-probability Smart Money Concepts (SMC) setups based on two key institutional trading principles:

Change of Character (CHOCH) – A shift in market structure signaling potential reversal

Fair Value Gap (FVG) – An imbalance zone where price moved too fast, often acting as support/resistance

When both conditions align, the script plots clear Buy (▲) and Sell (▼) signals directly on your chart — ideal for intraday trading on the 30-minute timeframe (but works on any timeframe).

✅ Key Features:

🔹 Visual Fair Value Gaps

Green shaded zones = Bullish FVGs (potential support)

Red shaded zones = Bearish FVGs (potential resistance)

Toggle on/off in settings

🔹 Smart CHOCH Detection

Detects breaks of recent swing highs/lows with proper context

Avoids false signals by confirming prior price structure

🔹 Clear Trade Signals

Green ▲ below bar = Buy signal (Bullish CHOCH + FVG confluence)

Red ▼ above bar = Sell signal (Bearish CHOCH + FVG confluence)

🔹 Customizable Filters

Option to require FVG for a signal (recommended for higher accuracy)

Adjust sensitivity via swing detection settings (default optimized for 30m)

🔹 Alert-Ready

Built-in alert conditions for instant notifications on TradingView mobile/desktop

⚙️ How to Use:

Apply to a 30-minute chart (e.g., EURUSD, Gold, NAS100, BTC)

Wait for at least 50–100 bars to load (so swing points appear)

Look for:

A green triangle (▲) → consider long entry near FVG support

A red triangle (▼) → consider short entry near FVG resistance

Confirm with price action: Wait for a strong candle close or rejection at the FVG zone

Use stop-loss below/above the FVG and target recent liquidity pools

💡 Pro Tip: Best used during high-volume sessions (e.g., London Open 7–10 AM UTC, NY Open 12:30–3:30 PM UTC).

🛠️ Settings (Inputs):

Show Fair Value Gaps

✅ Enabled

Visualize FVG zones

Max FVG History

100 bars

Prevent chart clutter

Require FVG for Signal?

✅ Enabled

Higher-quality setups (disable to test CHOCH-only)

⚠️ Important Notes:

This is a signal generator, not financial advice. Always manage risk.

Works best in trending or breaking markets — avoid during low-volatility ranges.

FVGs may get filled (tested) before price continues — patience improves results.

Backtest on historical data before live trading.

📣 Ideal For:

Retail traders learning Smart Money Concepts (SMC)

Price action traders seeking institutional-level confluence

Intraday scalpers & swing traders on 30m–1H timeframes

Risk-On / Risk-Off CompositeReal-time Risk-On / Risk-Off Composite from your four ratios:

SPY / TLT (equities vs long bonds)

HYG / LQD (high-yield vs IG credit)

HG / GOLD (copper vs gold)

BTC / GOLD (speculative vs defensive)

It:

normalizes each ratio with a z-score (so they’re comparable),

lets you weight them,

plots a composite line + histogram (up = risk-on, down = risk-off),

shows a small heat-table for each sub-signal,

and includes alert conditions for Risk-On / Risk-Off flips.

Puell Multiple Variants [OperationHeadLessChicken]Overview

This script contains three different, but related indicators to visualise Bitcoin miner revenue.

The classical Puell Multiple : historically, it has been good at signaling Bitcoin cycle tops and bottoms, but due to the diminishing rewards miners get after each halving, it is not clear how you determine overvalued and undervalued territories on it. Here is how the other two modified versions come into play:

Halving-Corrected Puell Multiple : The idea is to multiply the miner revenue after each halving with a correction factor, so overvalued levels are made comparable by a horizontal line across cycles. After experimentation, this correction factor turned out to be around 1.63. This brings cycle tops close to each other, but we lose the ability to see undervalued territories as a horizontal region. The third variant aims to fix this:

Miner Revenue Relative Strength Index (Miner Revenue RSI) : It uses RSI to map miner revenue into the 0-100 range, making it easy to visualise over/undervalued territories. With correct parameter settings, it eliminates the diminishing nature of the original Puell Multiple, and shows both over- and undervalued revenues correctly.

Example usage

The goal is to determine cycle tops and bottoms. I recommend using it on high timeframes, like monthly or weekly . Lower than that, you will see a lot of noise, but it could still be used. Here I use monthly as the example.

The classical Puell Multiple is included for reference. It is calculated as Miner Revenue divided by the 365-day Moving Average of the Miner Revenue . As you can see in the picture below, it has been good at signaling tops at 1,3,5,7.

The problems:

- I have to switch the Puell Multiple to a logarithmic scale

- Still, I cannot use a horizontal oversold territory

- 5 didn't touch the trendline, despite being a cycle top

- 9 touched the trendline despite not being a cycle top

Halving-Corrected Puell Multiple (yellow): Multiplies the Puell Multiple by 1.63 (a number determined via experimentation) after each halving. In the picture below, you can see how the Classical (white) and Corrected (yellow) Puell Multiples compare:

Advantages:

- Now you can set a constant overvalued level (12.49 in my case)

- 1,3,7 are signaled correctly as cycle tops

- 9 is correctly not signaled as a cycle top

Caveats:

- Now you don't have bottom signals anymore

- 5 is still not signaled as cycle top

Let's see if we can further improve this:

Miner Revenue RSI (blue):

On the monthly, you can see that an RSI period of 6, an overvalued threshold of 90, and an undervalued threshold of 35 have given historically pretty good signals.

Advantages:

- Uses two simple and clear horizontal levels for undervalued and overvalued levels

- Signaling 1,3,5,7 correctly as cycle tops

- Correctly does not signal 9 as a cycle top

- Signaling 4,6,8 correctly as cycle bottoms

Caveats:

- Misses two as a cycle bottom, although it was a long time ago when the Bitcoin market was much less mature

- In the past, gave some early overvalued signals

Usage

Using the example above, you can apply these indicators to any timeframe you like and tweak their parameters to obtain signals for overvalued/undervalued BTC prices

You can show or hide any of the three indicators individually

Set overvalued/undervalued thresholds for each => the background will highlight in green (undervalued) or red (overvalued)

Set special parameters for the given indicators: correction factor for the Corrected Puell and RSI period for Revenue RSI

Show or hide halving events on the indicator panel

All parameters and colours are adjustable

Gold–Bitcoin Correlation (Offset Model) by KManus88This indicator analyzes the correlation between Gold (XAU/USD) and Bitcoin (BTC/USD) using a time-offset model adjustable by the user.

The goal is to detect cyclical leads or lags between both assets, highlighting how capital flows into Gold may precede or follow movements in the crypto market.

Key Features:

Dynamic correlation calculation between Gold and Bitcoin.

Adjustable offset in days (default: 107) to fine-tune the temporal shift.

Automatic labels and on-chart visualization.

Compatible with multiple timeframes and logarithmic scales.

Interpretation:

Positive correlation suggests synchronized trends between both assets.

Negative correlation signals divergence or rotation of liquidity.

The time-offset parameter helps estimate when a shift in Gold could later reflect in Bitcoin.

Recommended use:

For macro-financial and global liquidity cycle analysis.

As a complementary tool in cross-asset momentum strategies.

© 2025 – Developed by KManus88 | Inspired by monetary correlation studies and global liquidity cycles.

This script is for educational purposes only and does not constitute financial advice.

Fair Value Lead-Lag Model [BackQuant]Fair Value Lead-Lag Model

A cross-asset model that estimates where price "should" be relative to a chosen reference series, then tracks the deviation as a normalized oscillator. It helps you answer two questions: 1) is the asset rich or cheap vs its driver, and 2) is the driver leading or lagging price over the next N bars.

Concept in one paragraph

Many assets co-move with a macro or sector driver. Think BTC vs DXY, gold vs real yields, a stock vs its sector ETF. This tool builds a rolling fair value of the charted asset from a reference series and shows how far price is above or below that fair value in standard deviation units. You can shift the reference forward or backward to test who leads whom, then use the deviation and its bands to structure mean-reversion or trend-following ideas.

What the model does

Reference mapping : Pulls a reference symbol at a chosen timeframe, with an optional lead or lag in bars to test causality.

Fair value engine : Converts the reference into a synthetic fair value of the chart using one of four methods:

Ratio : price/ref with a rolling average ratio. Good when the relationship is proportional.

Spread : price minus ref with a rolling average spread. Good when the relationship is additive.

Z-Score : normalizes both series, aligns on standardized units, then re-projects to price space. Good when scale drifts.

Beta-Adjusted : rolling regression style. Uses covariance and variance to compute beta, then builds a fair value = mean(price) + beta * (ref − mean(ref)).

Deviation and bands : Computes a z-scored deviation of price vs fair value and plots sigma bands (±1, ±2, ±3) around the fair value line on the chart.

Correlation context : Shows rolling correlation so you can judge if deviations are meaningful or just noise when co-movement is weak.

Visuals :

Fair value line on price chart with sigma envelopes.

Deviation as a column oscillator and optional line.

Threshold shading beyond user-set upper and lower levels.

Summary table with reference, deviation, status, correlation, and method.

Why this is useful

Mean reversion framework : When correlation is healthy and deviation stretches beyond your sigma threshold, probability favors reversion toward fair value. This is classic pairs logic adapted to a driver and a target.

Trend confirmation : If price rides the fair value line and deviation stays modest while correlation is positive, it supports trend persistence. Pullbacks to negative deviation in an uptrend can be buyable.

Lead-lag discovery : Shift the reference forward by +N bars. If correlation improves, the reference tends to lead. Shift backward for the reverse. Use the best setting for planning early entries or hedges.

Regime detection : Large persistent deviations with falling correlation hint at regime change. The relationship you relied on may be breaking down, so reduce confidence or switch methods.

How to use it step by step

Pick a sensible reference : Choose a macro, index, currency, or sector driver that logically explains the asset’s moves. Example: gold with DXY, a semiconductor stock with SOXX.

Test lead-lag : Nudge Lead/Lag Periods to small positive values like +1 to +5 to see if the reference leads. If correlation improves, keep that offset. If correlation worsens, try a small negative value or zero.

Select a method :

Start with Beta-Adjusted when the relationship is approximately linear with drift.

Use Ratio if the assets usually move in proportional terms.

Use Spread when they trade around a level difference.

Use Z-Score when scales wander or volatility regimes shift.

Tune windows :

Rolling Window controls how quickly fair value adapts. Shorter equals faster but noisier.

Normalization Period controls how deviations are standardized. Longer equals stabler sigma sizing.

Correlation Length controls how co-movement is measured. Keep it near the fair value window.

Trade the edges :

Mean reversion idea : Wait for deviation beyond your Upper or Lower Threshold with positive correlation. Fade back toward fair value. Exit at the fair value line or the next inner sigma band.

Trend idea : In an uptrend, buy pullbacks when deviation dips negative but correlation remains healthy. In a downtrend, sell bounces when deviation spikes positive.

Read the table : Deviation shows how many sigmas you are from fair value. Status tells you overvalued or undervalued. Correlation color hints confidence. Method tells you the projection style used.

Reading the display

Fair value line on price chart: the model’s estimate of where price should trade given the reference, updated each bar.

Sigma bands around fair value: a quick sense of residual volatility. Reversions often target inner bands first.

Deviation oscillator : above zero means rich vs fair value, below zero means cheap. Color bins intensify with distance.

Correlation line (optional): scale is folded to match thresholds. Higher values increase trust in deviations.

Parameter tips

Start with Rolling Window 20 to 30, Normalization Period 100, Correlation Length 50.

Upper and Lower Threshold at ±2.0 are classic. Tighten to ±1.5 for more signals or widen to ±2.5 to focus on outliers.

When correlation drifts below about 0.3, treat deviations with caution. Consider switching method or reference.

If the fair value line whipsaws, increase Rolling Window or move to Beta-Adjusted which tends to be smoother.

Playbook examples

Pairs-style reversion : Asset is +2.3 sigma rich vs reference, correlation 0.65, trend flat. Short the deviation back toward fair value. Cover near the fair value line or +1 sigma.

Pro-trend pullback : Uptrend with correlation 0.7. Deviation dips to −1.2 sigma while price sits near the −1 sigma band. Buy the dip, target the fair value line, trail if the line is rising.

Lead-lag timing : Reference leads by +3 bars with improved correlation. Use reference swings as early cues to anticipate deviation turns on the target.

Caveats

The model assumes a stable relationship over the chosen windows. Structural breaks, policy shocks, and index rebalances can invalidate recent history.

Correlation is descriptive, not causal. A strong correlation does not guarantee future convergence.

Do not force trades when the reference has low liquidity or mismatched hours. Use a reference timeframe that captures real overlap.

Bottom line

This tool turns a loose cross-asset intuition into a quantified, visual fair value map. It gives you a consistent way to find rich or cheap conditions, time mean-reversion toward a statistically grounded target, and confirm or fade trends when the driver agrees.

Luxy Adaptive MA Cloud - Trend Strength & Signal Tracker V2Luxy Adaptive MA Cloud - Professional Trend Strength & Signal Tracker

Next-generation moving average cloud indicator combining ultra-smooth gradient visualization with intelligent momentum detection. Built for traders who demand clarity, precision, and actionable insights.

═══════════════════════════════════════════════

WHAT MAKES THIS INDICATOR SPECIAL?

═══════════════════════════════════════════════

Unlike traditional MA indicators that show static lines, Luxy Adaptive MA Cloud creates a living, breathing visualization of market momentum. Here's what sets it apart:

Exponential Gradient Technology

This isn't just a simple fill between two lines. It's a professionally engineered gradient system with 26 precision layers using exponential density distribution. The result? An organic, cloud-like appearance where the center is dramatically darker (15% transparency - where crossovers and price action occur), while edges fade gracefully (75% transparency). Think of it as a visual "heat map" of trend strength.

Dynamic Momentum Intelligence

Most MA clouds only show structure (which MA is on top). This indicator shows momentum strength in real-time through four intelligent states:

- 🟢 Bright Green = Explosive bullish momentum (both MAs rising strongly)

- 🔵 Blue = Weakening bullish (structure intact, but momentum fading)

- 🟠 Orange = Caution zone (bearish structure forming, weak momentum)

- 🔴 Deep Red = Strong bearish momentum (both MAs falling)

The cloud literally tells you when trends are accelerating or losing steam.

Conditional Performance Architecture

Every calculation is optimized for speed. Disable a feature? It stops calculating entirely—not just hidden, but not computed . The 26-layer gradient only renders when enabled. Toggle signals off? Those crossover checks don't run. This makes it one of the most efficient cloud indicators available, even with its advanced visual system.

Zero Repaint Guarantee

All signals and momentum states are based on confirmed bar data only . What you see in historical data is exactly what you would have seen trading live. No lookahead bias. No repainting tricks. No signals that "magically" appear perfect in hindsight. If a signal shows in history, it would have triggered in real-time at that exact moment.

Educational by Design

Every single input includes comprehensive tooltips with:

- Clear explanations of what each parameter does

- Practical examples of when to use different settings

- Recommended configurations for scalping, day trading, and swing trading

- Real-world trading impact ("This affects entry timing" vs "This is visual only")

You're not just getting an indicator—you're learning how to use it effectively .

═══════════════════════════════════════════════

THE GRADIENT CLOUD - TECHNICAL DETAILS

═══════════════════════════════════════════════

Architecture:

26 precision layers for silk-smooth transitions

Exponential density curve - layers packed tightly near center (where crossovers happen), spread wider at edges

75%-15% transparency range - center is highly opaque (15%), edges fade gracefully (75%)

V-Gradient design - emphasizes the action zone between Fast and Medium MAs

The Four Momentum States:

🟢 GREEN - Strong Bullish

Fast MA above Medium MA

Both MAs rising with momentum > 0.02%

Action: Enter/hold LONG positions, strong uptrend confirmed

🔵 BLUE - Weak Bullish

Fast MA above Medium MA

Weak or flat momentum

Action: Caution - bullish structure but losing strength, consider trailing stops

🟠 ORANGE - Weak Bearish

Medium MA above Fast MA

Weak or flat momentum

Action: Warning - bearish structure developing, consider exits

🔴 RED - Strong Bearish

Medium MA above Fast MA

Both MAs falling with momentum < -0.02%

Action: Enter/hold SHORT positions, strong downtrend confirmed

Smooth Transitions: The momentum score is smoothed using an 8-bar EMA to eliminate noise and prevent whipsaws. You see the true trend , not every minor fluctuation.

═══════════════════════════════════════════════

FLEXIBLE MOVING AVERAGE SYSTEM

═══════════════════════════════════════════════

Three Customizable MAs:

Fast MA (default: EMA 10) - Reacts quickly to price changes, defines short-term momentum

Medium MA (default: EMA 20) - Balances responsiveness with stability, core trend reference

Slow MA (default: SMA 200, optional) - Long-term trend filter, major support/resistance

Six MA Types Available:

EMA - Exponential; faster response, ideal for momentum and day trading

SMA - Simple; smooth and stable, best for swing trading and trend following

WMA - Weighted; middle ground between EMA and SMA

VWMA - Volume-weighted; reflects market participation, useful for liquid markets

RMA - Wilder's smoothing; used in RSI/ADX, excellent for trend filters

HMA - Hull; extremely responsive with minimal lag, aggressive option

Recommended Settings by Trading Style:

Scalping (1m-5m):

Fast: EMA(5-8)

Medium: EMA(10-15)

Slow: Not needed or EMA(50)

Day Trading (5m-1h):

Fast: EMA(10-12)

Medium: EMA(20-21)

Slow: SMA(200) for bias

Swing Trading (4h-1D):

Fast: EMA(10-20)

Medium: EMA(34-50)

Slow: SMA(200)

Pro Tip: Start with Fast < Medium < Slow lengths. The gradient works best when there's clear separation between Fast and Medium MAs.

═══════════════════════════════════════════════

CROSSOVER SIGNALS - CLEAN & RELIABLE

═══════════════════════════════════════════════

Golden Cross ⬆ LONG Signal

Fast MA crosses above Medium MA

Classic bullish reversal or trend continuation signal

Most reliable when accompanied by GREEN cloud (strong momentum)

Death Cross ⬇ SHORT Signal

Fast MA crosses below Medium MA

Classic bearish reversal or trend continuation signal

Most reliable when accompanied by RED cloud (strong momentum)

Signal Intelligence:

Anti-spam filter - Minimum 5 bars between signals prevents noise

Clean labels - Placed precisely at crossover points

Alert-ready - Built-in ALERTS for automated trading systems

No repainting - Signals based on confirmed bars only

Signal Quality Assessment:

High-Quality Entry:

Golden Cross + GREEN cloud + Price above both MAs

= Strong bullish setup ✓

Low-Quality Entry (skip or wait):

Golden Cross + ORANGE cloud + Choppy price action

= Weak bullish setup, likely whipsaw ✗

═══════════════════════════════════════════════

REAL-TIME INFO PANEL

═══════════════════════════════════════════════

An at-a-glance dashboard showing:

Trend Strength Indicator:

Visual display of current momentum state

Color-coded header matching cloud color

Instant recognition of market bias

MA Distance Table:

Shows percentage distance of price from each enabled MA:

Green rows : Price ABOVE MA (bullish)

Red rows : Price BELOW MA (bearish)

Gray rows : Price AT MA (rare, decision point)

Distance Interpretation:

+2% to +5%: Healthy uptrend

+5% to +10%: Getting extended, caution

+10%+: Overextended, expect pullback

-2% to -5%: Testing support

-5% to -10%: Oversold zone

-10%+: Deep correction or downtrend

Customization:

4 corner positions

5 font sizes (Tiny to Huge)

Toggle visibility on/off

═══════════════════════════════════════════════

HOW TO USE - PRACTICAL TRADING GUIDE

═══════════════════════════════════════════════

STRATEGY 1: Trend Following

Identify trend : Wait for GREEN (bullish) or RED (bearish) cloud

Enter on signal : Golden Cross in GREEN cloud = LONG, Death Cross in RED cloud = SHORT

Hold position : While cloud maintains color

Exit signals :

• Cloud turns ORANGE/BLUE = momentum weakening, tighten stops

• Opposite crossover = close position

• Cloud turns opposite color = full reversal

STRATEGY 2: Pullback Entries

Confirm trend : GREEN cloud established (bullish bias)

Wait for pullback : Price touches or crosses below Fast MA

Enter when : Price rebounds back above Fast MA with cloud still GREEN

Stop loss : Below Medium MA or recent swing low

Target : Previous high or when cloud weakens

STRATEGY 3: Momentum Confirmation

Your setup triggers : (e.g., chart pattern, support/resistance)

Check cloud color :

• GREEN = proceed with LONG

• RED = proceed with SHORT

• BLUE/ORANGE = skip or reduce size

Use gradient as confluence : Not as primary signal, but as momentum filter

Risk Management Tips:

Never enter against the cloud color (don't LONG in RED cloud)

Reduce position size during BLUE/ORANGE (transition periods)

Place stops beyond Medium MA for swing trades

Use Slow MA (200) as final trend filter - don't SHORT above it in uptrends

═══════════════════════════════════════════════

PERFORMANCE & OPTIMIZATION

═══════════════════════════════════════════════

Tested On:

Crypto: BTC, ETH, major altcoins

Stocks: SPY, AAPL, TSLA, QQQ

Forex: EUR/USD, GBP/USD, USD/JPY

Indices: S&P 500, NASDAQ, DJI

═══════════════════════════════════════════════

TRANSPARENCY & RELIABILITY

═══════════════════════════════════════════════

Educational Focus:

Detailed tooltips on every input

Clear documentation of methodology

Practical examples in descriptions

Teaches you why , not just what

Open Logic:

Momentum calculation: (Fast slope + Medium slope) / 2

Smoothing: 8-bar EMA to reduce noise

Thresholds: ±0.02% for strong momentum classification

Everything is transparent and explainable

═══════════════════════════════════════════════

COMPLETE FEATURE LIST

═══════════════════════════════════════════════

Visual Components:

26-layer exponential gradient cloud

3 customizable moving average lines

Golden Cross / Death Cross labels

Real-time info panel with trend strength

MA distance table

Calculation Features:

6 MA types (EMA, SMA, WMA, VWMA, RMA, HMA)

Momentum-based cloud coloring

Smoothed trend strength scoring

Conditional performance optimization

Customization Options:

All MA lengths adjustable

All colors customizable (when gradient disabled)

Panel position (4 corners)

Font sizes (5 options)

Toggle any feature on/off

Signal Features:

Anti-spam filter (configurable gap)

Clean, non-overlapping labels

Built-in alert conditions

No repainting guarantee

═══════════════════════════════════════════════

IMPORTANT DISCLAIMERS

═══════════════════════════════════════════════

This indicator is for educational and informational purposes only

Not financial advice - always do your own research

Past performance does not guarantee future results

Use proper risk management - never risk more than you can afford to lose

Test on paper/demo accounts before using with real money

Combine with other analysis methods - no single indicator is perfect

Works best in trending markets; less effective in choppy/sideways conditions

Signals may perform differently in different timeframes and market conditions

The indicator uses historical data for MA calculations - allow sufficient lookback period

═══════════════════════════════════════════════

CREDITS & TECHNICAL INFO

═══════════════════════════════════════════════

Version: 2.0

Release: October 2025

Special Thanks:

TradingView community for feedback and testing

Pine Script documentation for technical reference

═══════════════════════════════════════════════

SUPPORT & UPDATES

═══════════════════════════════════════════════

Found a bug? Comment below with:

Ticker symbol

Timeframe

Screenshot if possible

Steps to reproduce

Feature requests? I'm always looking to improve! Share your ideas in the comments.

Questions? Check the tooltips first (hover over any input) - most answers are there. If still stuck, ask in comments.

═══════════════════════════════════════════════

Happy Trading!

Remember: The best indicator is the one you understand and use consistently. Take time to learn how the cloud behaves in different market conditions. Practice on paper before going live. Trade smart, manage risk, and may the trends be with you! 🚀

Friday’s Close – Futures Weekend AnchorPurpose:

This indicator highlights the US futures weekend close price — the exact level where CME markets end trading on Friday at 4:00 PM CT / 5:00 PM ET.

It’s designed primarily for crypto traders who want to compare weekend market behavior to the traditional finance (TradFi) close.

Why it matters:

Crypto trades 24/7, but global liquidity and sentiment still pivot around the Friday futures close. During the weekend, crypto can “drift” relative to traditional markets — this line shows exactly where the week ended for Wall Street, giving you a clean reference point until futures reopen on Sunday evening.

Features

Precise Friday close capture (CME weekend close minute, not just daily bar)

Works on any ticker — especially useful for BTC, ETH, or other crypto assets

Adjustable for time zone (New York / Chicago / custom)

Option to select prior weeks with weekOffset

Draws a single clean line from Friday’s close forward — no clutter, no vertical stitches

Optional right-edge label with the close value and timestamp

Usage Tips

Keep the chart’s timezone in sync with your anchor (America/New_York = 5 PM ET, America/Chicago = 4 PM CT).

Use weekOffset = 1 to view last week’s Friday close.

Combine with volume, funding, or open interest indicators to see how weekend moves relate to the TradFi close.

Ideal for weekend analysis — shows whether crypto is trading rich or cheap vs. the Friday benchmark before futures reopen.

Recommended For

Crypto traders, analysts, and quant enthusiasts who monitor TradFi–crypto decoupling or weekend premium behavior.

Liquidity Index with Advanced Statistical NormalizationLiquidity Index with Advanced Statistical Normalization

An open-source TradingView indicator for analyzing global liquidity cycles using robust statistical methods

Overview

This Pine Script indicator combines multiple macroeconomic data sources to construct a composite liquidity index that tracks global financial conditions. It employs advanced statistical techniques typically found in quantitative finance research, adapted for real-time charting.

Key Features

📊 Multi-Source Data Integration

- Federal Reserve Components: Fed Funds Rate, Reverse Repo (RRP), Treasury General Account (TGA)

- PBOC Components: China M2 Money Stock adjusted by CNY/USD exchange rate

- Volatility Index: MOVE Index (bond market volatility)

🔬 Advanced Statistical Methods

1. Theil-Sen Estimator: Robust trend detection resistant to outliers

2. Triple Normalization:

- Z-score normalization

- MAD (Median Absolute Deviation) normalization

- Quantile normalization via inverse normal CDF

3. Multi-Timeframe Analysis: Short (8-bar) and long (34-bar) windows with blended composite

📈 Signal Processing

- Log-transformation for non-linear relationships

- Smoothing via customizable SMA

- Composite signal averaging across normalization methods

Why This Approach?

Traditional liquidity indicators often suffer from:

- Sensitivity to outliers in economic data

- Assumption of normal distributions

- Single-timeframe bias

This script addresses these issues by:

- Using median-based robust statistics (Theil-Sen, MAD)

- Applying multiple normalization techniques

- Blending short and long-term perspectives

Customization Options

short_length // Short window (default: 8)

long_length // Long window (default: 34)

show_short // Display short composite

show_long // Display long composite

show_blended // Display blended signal

smoothing_length // SMA smoothing period (default: 10)

How to Use

1. Liquidity Expansion (positive values): Risk-on environment, favorable for asset prices

2. Liquidity Contraction (negative values): Risk-off environment, potential market stress

3. Divergences: Compare indicator direction vs. price action for early warnings

Potential Improvements

Community members are encouraged to enhance:

- Additional data sources (ECB balance sheet, BOJ operations, etc.)

- Alternative normalization methods (robust scaling, rank transformation)

- Machine learning integration (LSTM forecasting, regime detection)

- Alert conditions for liquidity inflection points

- Volatility-adjusted weighting schemes

Technical Notes

- Uses request.security() for multi-symbol data fetching

- All calculations handle missing data via nz() functions

- Median-based statistics computed via array operations

- Custom inverse CDF approximation (no external libraries required)

Contributing

This is a foundation for liquidity analysis. Potential extensions:

- LLM Integration: Use language models to parse Fed/PBOC meeting minutes and adjust weights dynamically

- Sentiment Layer: Incorporate crypto funding rates or options skew

- Adaptive Parameters: Auto-tune window lengths based on market regime

- Cross-Asset Validation: Backtest signals against BTC, equities, bonds

---

License: Open source - modify and redistribute freelyDisclaimer: For educational purposes only. Not financial advice.

High Volume Arrow Signals (Ajustável)The High Volume Arrow Signals (Adjustable) indicator is a professional technical analysis tool designed to clearly pinpoint moments when trading volume significantly exceeds its recent average, signaling potential institutional pressure, strong conviction, or market exhaustion.

Its primary function is to overlay confirmation signals directly onto the price bars without altering the original candle colors.

Strategic Application

This indicator is most effective when used as a confluence tool to confirm moves initiated by price action or other indicators:

Breakout Confirmation: An arrow plotted during a price range breakout suggests the move has genuine volume conviction.

Reversal Identification: A Buy arrow appearing at a key support level (or a Sell arrow at resistance) indicates strong volume rejection and a potential turning point.

The adjustable multiplier ensures users can fine-tune the indicator to the specific volatility and volume characteristics of assets like BTC and ETH across different timeframes.

Jensen Alpha RS🧠 Jensen Alpha RS (J-Alpha RS)

Jensen Alpha RS is a quantitative performance evaluation tool designed to compare multiple assets against a benchmark using Jensen’s Alpha — a classic risk-adjusted return metric from modern portfolio theory.

It helps identify which assets have outperformed their benchmark on a risk-adjusted basis and ranks them in real time, with optional gating and visual tools. 📊

✨ Key Features

• 🧩 Multi-Asset Comparison: Evaluate up to four assets simultaneously.

• 🔀 Adaptive Benchmarking: TOTALES mode uses CRYPTOCAP:TOTALES (total crypto market cap ex-stablecoins). Dynamic mode automatically selects the strongest benchmark among BTC, ETH, and TOTALES based on rolling momentum.

• 📐 Jensen’s Alpha Calculation: Uses rolling covariance, variance, and beta to estimate α, showing how much each asset outperformed its benchmark.

• 📈 Z-Score & Consistency Metrics: Z-Score highlights statistical deviations in alpha; Consistency % shows how often α has been positive over a chosen window.

• 🚦 Trend & Zero Gates: Optional filters that require assets to be above EMA (trend) and/or have α > 0 for confirmation.

• 🏆 Leaders Board Table: Displays α, Z, Rank, Consistency %, and Gate ✓/✗ for all assets in a clear visual layout.

• 🔔 Dynamic Alerts: Get notified whenever the top alpha leader changes on confirmed (non-repainting) data.

• 🎨 Visual Enhancements: Smooth α with an SMA or color bars by the current top-performing asset.

🧭 Typical Use Cases

• 🔄 Portfolio Rotation & Relative Strength: Identify which assets consistently outperform their benchmark to optimize capital allocation.

• 🧮 Alpha Persistence Analysis: Gauge whether a trend’s performance advantage is statistically sustainable.

• 🌐 Market Regime Insight: Observe how asset leadership rotates as benchmarks shift across market cycles.

⚙️ Inputs Overview

• 📝 Assets (1–4): Select up to four tickers for evaluation.

• 🧭 Benchmark Mode: Choose between static TOTALES or Dynamic auto-selection.

• 📏 Alpha Settings: Adjustable lookback, smoothing, and consistency windows.

• 🚦 Gates: Optional trend and alpha filters to refine results.

• 🖥️ Display: Enable/disable table and customize colors.

• 🔔 Alerts: Toggle notifications on leadership changes.

🔎 Formula Basis

Jensen’s Alpha (α) is estimated as:

α = E − β × E

where β = Cov(Ra, Rb) / Var(Rb), and Ra/Rb represent asset and benchmark returns, respectively.

A positive α indicates outperformance relative to the risk-adjusted benchmark expectation. ✅

⚠️ Disclaimer

This script is for educational and analytical purposes only.

It is NOT a signal. 🚫📉

It does not constitute financial advice, trading signals, or investment recommendations. 💬

The author is not responsible for any financial losses or trading decisions made based on this indicator. 🙏

Always perform your own analysis and use proper risk management. 🛡️