FvgCalculations█ OVERVIEW

This library provides the core calculation engine for identifying Fair Value Gaps (FVGs) across different timeframes and for processing their interaction with price. It includes functions to detect FVGs on both the current chart and higher timeframes, as well as to check for their full or partial mitigation.

█ CONCEPTS

The library's primary functions revolve around the concept of Fair Value Gaps and their lifecycle.

Fair Value Gap (FVG) Identification

An FVG, or imbalance, represents a price range where buying or selling pressure was significant enough to cause a rapid price movement, leaving an "inefficiency" in the market. This library identifies FVGs based on three-bar patterns:

Bullish FVG: Forms when the low of the current bar (bar 3) is higher than the high of the bar two periods prior (bar 1). The FVG is the space between the high of bar 1 and the low of bar 3.

Bearish FVG: Forms when the high of the current bar (bar 3) is lower than the low of the bar two periods prior (bar 1). The FVG is the space between the low of bar 1 and the high of bar 3.

The library provides distinct functions for detecting FVGs on the current (Low Timeframe - LTF) and specified higher timeframes (Medium Timeframe - MTF / High Timeframe - HTF).

FVG Mitigation

Mitigation refers to price revisiting an FVG.

Full Mitigation: An FVG is considered fully mitigated when price completely closes the gap. For a bullish FVG, this occurs if the current low price moves below or touches the FVG's bottom. For a bearish FVG, it occurs if the current high price moves above or touches the FVG's top.

Partial Mitigation (Entry/Fill): An FVG is partially mitigated when price enters the FVG's range but does not fully close it. The library tracks the extent of this fill. For a bullish FVG, if the current low price enters the FVG from above, that low becomes the new effective top of the remaining FVG. For a bearish FVG, if the current high price enters the FVG from below, that high becomes the new effective bottom of the remaining FVG.

FVG Interaction

This refers to any instance where the current bar's price range (high to low) touches or crosses into the currently unfilled portion of an active (visible and not fully mitigated) FVG.

Multi-Timeframe Data Acquisition

To detect FVGs on higher timeframes, specific historical bar data (high, low, and time of bars at indices and relative to the higher timeframe's last completed bar) is required. The requestMultiTFBarData function is designed to fetch this data efficiently.

█ CALCULATIONS AND USE

The functions in this library are typically used in a sequence to manage FVGs:

1. Data Retrieval (for MTF/HTF FVGs):

Call requestMultiTFBarData() with the desired higher timeframe string (e.g., "60", "D").

This returns a tuple of htfHigh1, htfLow1, htfTime1, htfHigh3, htfLow3, htfTime3.

2. FVG Detection:

For LTF FVGs: Call detectFvg() on each confirmed bar. It uses high , low, low , and high along with barstate.isconfirmed.

For MTF/HTF FVGs: Call detectMultiTFFvg() using the data obtained from requestMultiTFBarData().

Both detection functions return an fvgObject (defined in FvgTypes) if an FVG is found, otherwise na. They also can classify FVGs as "Large Volume" (LV) if classifyLV is true and the FVG size (top - bottom) relative to the tfAtr (Average True Range of the respective timeframe) meets the lvAtrMultiplier.

3. FVG State Updates (on each new bar for existing FVGs):

First, check for overall price interaction using fvgInteractionCheck(). This function determines if the current bar's high/low has touched or entered the FVG's currentTop or currentBottom.

If interaction occurs and the FVG is not already mitigated:

Call checkMitigation() to determine if the FVG has been fully mitigated by the current bar's currentHigh and currentLow. If true, the FVG's isMitigated status is updated.

If not fully mitigated, call checkPartialMitigation() to see if the price has further entered the FVG. This function returns the newLevel to which the FVG has been filled (e.g., currentLow for a bullish FVG, currentHigh for bearish). This newLevel is then used to update the FVG's currentTop or currentBottom.

The calling script (e.g., fvgMain.c) is responsible for storing and managing the array of fvgObject instances and passing them to these update functions.

█ NOTES

Bar State for LTF Detection: The detectFvg() function relies on barstate.isconfirmed to ensure FVG detection is based on closed bars, preventing FVGs from being detected prematurely on the currently forming bar.

Higher Timeframe Data (lookahead): The requestMultiTFBarData() function uses lookahead = barmerge.lookahead_on. This means it can access historical data from the higher timeframe that corresponds to the current bar on the chart, even if the higher timeframe bar has not officially closed. This is standard for multi-timeframe analysis aiming to plot historical HTF data accurately on a lower timeframe chart.

Parameter Typing: Functions like detectMultiTFFvg and detectFvg infer the type for boolean (classifyLV) and numeric (lvAtrMultiplier) parameters passed from the main script, while explicitly typed series parameters (like htfHigh1, currentAtr) expect series data.

fvgObject Dependency: The FVG detection functions return fvgObject instances, and fvgInteractionCheck takes an fvgObject as a parameter. This UDT is defined in the FvgTypes library, making it a dependency for using FvgCalculations.

ATR for LV Classification: The tfAtr (for MTF/HTF) and currentAtr (for LTF) parameters are expected to be the Average True Range values for the respective timeframes. These are used, if classifyLV is enabled, to determine if an FVG's size qualifies it as a "Large Volume" FVG based on the lvAtrMultiplier.

MTF/HTF FVG Appearance Timing: When displaying FVGs from a higher timeframe (MTF/HTF) on a lower timeframe (LTF) chart, users might observe that the most recent MTF/HTF FVG appears one LTF bar later compared to its appearance on a native MTF/HTF chart. This is an expected behavior due to the detection mechanism in `detectMultiTFFvg`. This function uses historical bar data from the MTF/HTF (specifically, data equivalent to `HTF_bar ` and `HTF_bar `) to identify an FVG. Therefore, all three bars forming the FVG on the MTF/HTF must be fully closed and have shifted into these historical index positions relative to the `request.security` call from the LTF chart before the FVG can be detected and displayed on the LTF. This ensures that the MTF/HTF FVG is identified based on confirmed, closed bars from the higher timeframe.

█ EXPORTED FUNCTIONS

requestMultiTFBarData(timeframe)

Requests historical bar data for specific previous bars from a specified higher timeframe.

It fetches H , L , T (for the bar before last) and H , L , T (for the bar three periods prior)

from the requested timeframe.

This is typically used to identify FVG patterns on MTF/HTF.

Parameters:

timeframe (simple string) : The higher timeframe to request data from (e.g., "60" for 1-hour, "D" for Daily).

Returns: A tuple containing: .

- htfHigh1 (series float): High of the bar at index 1 (one bar before the last completed bar on timeframe).

- htfLow1 (series float): Low of the bar at index 1.

- htfTime1 (series int) : Time of the bar at index 1.

- htfHigh3 (series float): High of the bar at index 3 (three bars before the last completed bar on timeframe).

- htfLow3 (series float): Low of the bar at index 3.

- htfTime3 (series int) : Time of the bar at index 3.

detectMultiTFFvg(htfHigh1, htfLow1, htfTime1, htfHigh3, htfLow3, htfTime3, tfAtr, classifyLV, lvAtrMultiplier, tfType)

Detects a Fair Value Gap (FVG) on a higher timeframe (MTF/HTF) using pre-fetched bar data.

Parameters:

htfHigh1 (float) : High of the first relevant bar (typically high ) from the higher timeframe.

htfLow1 (float) : Low of the first relevant bar (typically low ) from the higher timeframe.

htfTime1 (int) : Time of the first relevant bar (typically time ) from the higher timeframe.

htfHigh3 (float) : High of the third relevant bar (typically high ) from the higher timeframe.

htfLow3 (float) : Low of the third relevant bar (typically low ) from the higher timeframe.

htfTime3 (int) : Time of the third relevant bar (typically time ) from the higher timeframe.

tfAtr (float) : ATR value for the higher timeframe, used for Large Volume (LV) FVG classification.

classifyLV (bool) : If true, FVGs will be assessed to see if they qualify as Large Volume.

lvAtrMultiplier (float) : The ATR multiplier used to define if an FVG is Large Volume.

tfType (series tfType enum from no1x/FvgTypes/1) : The timeframe type (e.g., types.tfType.MTF, types.tfType.HTF) of the FVG being detected.

Returns: An fvgObject instance if an FVG is detected, otherwise na.

detectFvg(classifyLV, lvAtrMultiplier, currentAtr)

Detects a Fair Value Gap (FVG) on the current (LTF - Low Timeframe) chart.

Parameters:

classifyLV (bool) : If true, FVGs will be assessed to see if they qualify as Large Volume.

lvAtrMultiplier (float) : The ATR multiplier used to define if an FVG is Large Volume.

currentAtr (float) : ATR value for the current timeframe, used for LV FVG classification.

Returns: An fvgObject instance if an FVG is detected, otherwise na.

checkMitigation(isBullish, fvgTop, fvgBottom, currentHigh, currentLow)

Checks if an FVG has been fully mitigated by the current bar's price action.

Parameters:

isBullish (bool) : True if the FVG being checked is bullish, false if bearish.

fvgTop (float) : The top price level of the FVG.

fvgBottom (float) : The bottom price level of the FVG.

currentHigh (float) : The high price of the current bar.

currentLow (float) : The low price of the current bar.

Returns: True if the FVG is considered fully mitigated, false otherwise.

checkPartialMitigation(isBullish, currentBoxTop, currentBoxBottom, currentHigh, currentLow)

Checks for partial mitigation of an FVG by the current bar's price action.

It determines if the price has entered the FVG and returns the new fill level.

Parameters:

isBullish (bool) : True if the FVG being checked is bullish, false if bearish.

currentBoxTop (float) : The current top of the FVG box (this might have been adjusted by previous partial fills).

currentBoxBottom (float) : The current bottom of the FVG box (similarly, might be adjusted).

currentHigh (float) : The high price of the current bar.

currentLow (float) : The low price of the current bar.

Returns: The new price level to which the FVG has been filled (e.g., currentLow for a bullish FVG).

Returns na if no new partial fill occurred on this bar.

fvgInteractionCheck(fvg, highVal, lowVal)

Checks if the current bar's price interacts with the given FVG.

Interaction means the price touches or crosses into the FVG's

current (possibly partially filled) range.

Parameters:

fvg (fvgObject type from no1x/FvgTypes/1) : The FVG object to check.

Its isMitigated, isVisible, isBullish, currentTop, and currentBottom fields are used.

highVal (float) : The high price of the current bar.

lowVal (float) : The low price of the current bar.

Returns: True if price interacts with the FVG, false otherwise.

"bear" için komut dosyalarını ara

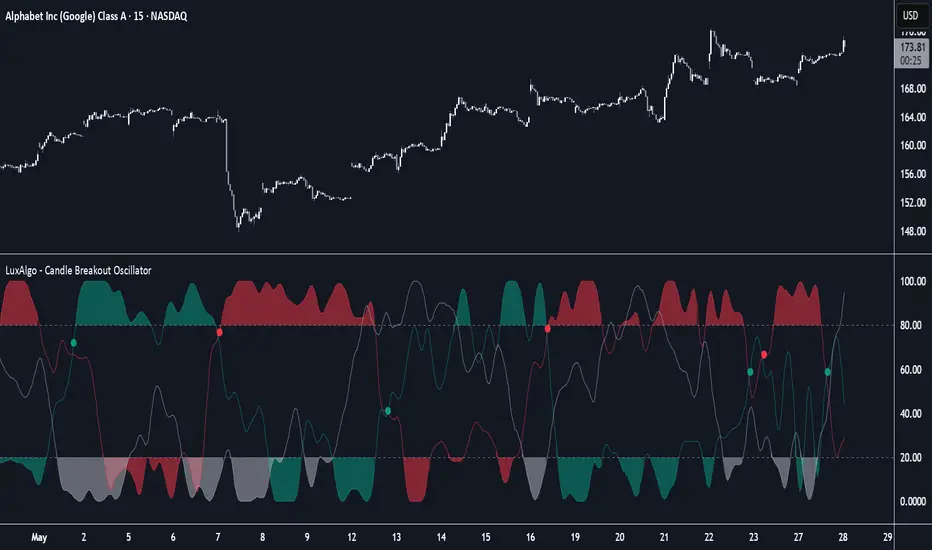

Candle Breakout Oscillator [LuxAlgo]The Candle Breakout Oscillator tool allows traders to identify the strength and weakness of the three main market states: bullish, bearish, and choppy.

Know who controls the market at any given moment with an oscillator display with values ranging from 0 to 100 for the three main plots and upper and lower thresholds of 80 and 20 by default.

🔶 USAGE

The Candle Breakout Oscillator represents the three main market states, with values ranging from 0 to 100. By default, the upper and lower thresholds are set at 80 and 20, and when a value exceeds these thresholds, a colored area is displayed for the trader's convenience.

This tool is based on pure price action breakouts. In this context, we understand a breakout as a close above the last candle's high or low, which is representative of market strength. All other close positions in relation to the last candle's limits are considered weakness.

So, when the bullish plot (in green) is at the top of the oscillator (values above 80), it means that the bullish breakouts (close below the last candle low) are at their maximum value over the calculation window, indicating an uptrend. The same interpretation can be made for the bearish plot (in red), indicating a downtrend when high.

On the other hand, weakness is indicated when values are below the lower threshold (20), indicating that breakouts are at their minimum over the last 100 candles. Below are some examples of the possible main interpretations:

There are three main things to look for in this oscillator:

Value reaches extreme

Value leaves extreme

Bullish/Bearish crossovers

As we can see on the chart, before the first crossover happens the bears come out of strength (top) and the bulls come out of weakness (bottom), then after the crossover the bulls reach strength (top) and the bears weakness (bottom), this process is repeated in reverse for the second crossover.

The other main feature of the oscillator is its ability to identify periods of sideways trends when the sideways values have upper readings above 80, and trending behavior when the sideways values have lower readings below 20. As we just saw in the case of bullish vs. bearish, sideways values signal a change in behavior when reaching or leaving the extremes of the oscillator.

🔶 DETAILS

🔹 Data Smoothing

The tool offers up to 10 different smoothing methods. In the chart above, we can see the raw data (smoothing: None) and the RMA, TEMA, or Hull moving averages.

🔹 Data Weighting

Users can add different weighting methods to the data. As we can see in the image above, users can choose between None, Volume, or Price (as in Price Delta for each breakout).

🔶 SETTINGS

Window: Execution window, 100 candles by default

🔹 Data

Smoothing Method: Choose between none or ten moving averages

Smoothing Length: Length for the moving average

Weighting Method: Choose between None, Volume, or Price

🔹 Thresholds

Top: 80 by default

Bottom: 20 by default

$ADD LevelsThis Pine Script is designed to track and visualize the NYSE Advance-Decline Line (ADD). The Advance-Decline Line is a popular market breadth indicator, showing the difference between advancing and declining stocks on the NYSE. It’s often used to gauge overall market sentiment and strength.

1. //@version=5

This line tells TradingView to use Pine Script v5, the latest and most powerful version of Pine.

2. indicator(" USI:ADD Levels", overlay=false)

• This creates a new indicator called ” USI:ADD Levels”.

• overlay=false means it will appear in a separate pane, not on the main price chart.

3. add = request.security(...)

This fetches real-time data from the symbol USI:ADD (Advance-Decline Line) using a 1-minute timeframe. You can change the timeframe if needed.

add_symbol = input.symbol(" USI:ADD ", "Market Breadth Symbol")

add = request.security(add_symbol, "1", close)

4. Key Thresholds

These define the market sentiment zones:

Zone. Value. Meaning

Overbought +1500 Extremely bullish

Bullish +1000 Generally bullish trend

Neutral ±500 Choppy, unclear market

Bearish -1000 Generally bearish trend

Oversold -1500 Extremely bearish

5. Plot the ADD Line hline(...)

Draws static lines at +1500, +1000, +500, -500, -1000, -1500 for reference so you can visually assess where ADD stands.

6. Horizontal Threshold Lines bgcolor(...)

• Green background if ADD > +1500 → extremely bullish.

• Red background if ADD < -1500 → extremely bearish.

7. Background Highlights alertcondition(...)

• Green background if ADD > +1500 → extremely bullish.

• Red background if ADD < -1500 → extremely bearish.

8. Alert Conditions. alertcondition(...)

Lets you create automatic alerts for:

• USI:ADD being very high or low.

• Crosses above +1000 (bullish trigger).

• Crosses below -1000 (bearish trigger).

You can use these to trigger trades or monitor sentiment shifts.

Summary: When to Use It

• Use this script in a market breadth dashboard.

• Combine it with price action and volume analysis.

• Monitor for ADD crosses to signal potential market reversals or momentum.

MestreDoFOMO MACD VisualMasterDoFOMO MACD Visual

Description

MasterDoFOMO MACD Visual is a custom indicator that combines a unique approach to MACD with stochastic logic and simulated Renko-based direction signals. It is designed to help traders identify entry and exit opportunities based on market momentum and trend changes, with a clear and intuitive visualization.

How It Works

Stylized MACD with Stochastic: The indicator calculates the MACD using EMAs (exponential moving averages) normalized by stochastic logic. This is done by subtracting the lowest price (lowest low) from a defined period and dividing by the range between the highest and lowest price (highest high - lowest low). The result is a MACD that is more sensitive to market conditions, magnified by a factor of 10 for better visualization.

Signal Line: An EMA of the MACD is plotted as a signal line, allowing you to identify crossovers that indicate potential trend reversals or continuations.

Histogram: The difference between the MACD and the signal line is displayed as a histogram, with distinct colors (fuchsia for positive, purple for negative) to make momentum easier to read.

Simulated Renko Direction: Uses ATR (Average True Range) to calculate the size of Renko "bricks", generating signals of change in direction (bullish or bearish). These signals are displayed as arrows on the chart, helping to identify trend reversals.

Purpose

The indicator combines the sensitivity of the Stochastic MACD with the robustness of Renko signals to provide a versatile tool. It is ideal for traders looking to capture momentum-based market movements (using the MACD and histogram) while confirming trend changes with Renko signals. This combination reduces false signals and improves accuracy in volatile markets.

Settings

Stochastic Period (45): Sets the period for calculating the Stochastic range (highest high - lowest low).

Fast EMA Period (12): Period of the fast EMA used in the MACD.

Slow EMA Period (26): Period of the slow EMA used in the MACD.

Signal Line Period (9): Period of the EMA of the signal line.

Overbought/Oversold Levels (1.0/-1.0): Thresholds for identifying extreme conditions in the MACD.

ATR Period (14): Period for calculating the Renko brick size.

ATR Multiplier (1.0): Adjusts the Renko brick size.

Show Histogram: Enables/disables the histogram.

Show Renko Markers: Enables/disables the Renko direction arrows.

How to Use

MACD Crossovers: A MACD crossover above the signal line indicates potential bullishness, while below suggests bearishness.

Histogram: Fuchsia bars indicate bullish momentum; purple bars indicate bearish momentum.

Renko Arrows: Green arrows (upward triangle) signal a change to an uptrend; red arrows (downward triangle) signal a downtrend.

Overbought/Oversold Levels: Use the levels to identify potential reversals when the MACD reaches extreme values.

Notes

The chart should be set up with this indicator in isolation for better clarity.

Adjust the periods and ATR multiplier according to the asset and timeframe used.

Use the built-in alerts ("Renko Up Signal" and "Renko Down Signal") to set up notifications of direction changes.

This indicator is ideal for day traders and swing traders who want a visually clear and functional tool for trading based on momentum and trends.

Delta Volume Profile [BigBeluga]🔵Delta Volume Profile

A dynamic volume analysis tool that builds two separate horizontal profiles: one for bullish candles and one for bearish candles. This indicator helps traders identify the true balance of buying vs. selling volume across price levels, highlighting points of control (POCs), delta dominance, and hidden volume clusters with remarkable precision.

🔵 KEY FEATURES

Split Volume Profiles (Bull vs. Bear):

The indicator separates volume based on candle direction:

If close > open , the candle’s volume is added to the bullish profile (positive volume).

If close < open , it contributes to the bearish profile (negative volume).

ATR-Based Binning:

The price range over the selected lookback is split into bins using ATR(200) as the bin height.

Each bin accumulates both bull and bear volumes to form the dual-sided profile.

Bull and Bear Volume Bars:

Bullish volumes are shown as right-facing bars on the right side, colored with a bullish gradient.

Bearish volumes appear as left-facing bars on the left side, shaded with a bearish gradient.

Each bar includes a volume label (e.g., +12.45K or -9.33K) to show exact volume at that price level.

Points of Control (POC) Highlighting:

The bin with the highest bullish volume is marked with a border in POC+ color (default: blue).

The bin with the highest bearish volume is marked with a POC− color (default: orange).

Total Volume Density Map:

A neutral gray background box is plotted behind candles showing the total volume (bull + bear) per bin.

This reveals high-interest price zones regardless of direction.

Delta and Total Volume Summary:

A Delta label appears at the top, showing net % difference between bull and bear volume.

A Total label at the bottom shows total accumulated volume across all bins.

🔵 HOW IT WORKS

The indicator captures all candles within the lookback period .

It calculates the price range and splits it into bins using ATR for adaptive resolution.

For each candle:

If price intersects a bin and close > open , volume is added to the positive profile .

If close < open , volume is added to the negative profile .

The result is two side-by-side histograms at each price level—one for buyers, one for sellers.

The bin with the highest value on each side is visually emphasized using POC highlight colors.

At the end, the script calculates:

Delta: Total % difference between bull and bear volumes.

Total: Sum of all volumes in the lookback window.

🔵 USAGE

Volume Imbalance Zones: Identify price levels where buyers or sellers were clearly dominant.

Fade or Follow Volume Clusters: Use POC+ or POC− levels for reaction trades or breakouts.

Delta Strength Filtering: Strong delta values (> ±20%) suggest momentum or exhaustion setups.

Volume-Based Anchoring: Use profile levels to mark hidden support/resistance and execution zones.

🔵 CONCLUSION

Delta Volume Profile offers a unique advantage in market reading by separating buyer and seller activity into two visual layers. This allows traders to not only spot where volume was high, but also who was more aggressive. Whether you’re analyzing trend continuations, reversals, or absorption levels, this indicator gives you the transparency needed to trade with confidence.

Lyapunov Market Instability (LMI)Lyapunov Market Instability (LMI)

What is Lyapunov Market Instability?

Lyapunov Market Instability (LMI) is a revolutionary indicator that brings chaos theory from theoretical physics into practical trading. By calculating Lyapunov exponents—a measure of how rapidly nearby trajectories diverge in phase space—LMI quantifies market sensitivity to initial conditions. This isn't another oscillator or trend indicator; it's a mathematical lens that reveals whether markets are in chaotic (trending) or stable (ranging) regimes.

Inspired by the meditative color field paintings of Mark Rothko, this indicator transforms complex chaos mathematics into an intuitive visual experience. The elegant simplicity of the visualization belies the sophisticated theory underneath—just as Rothko's seemingly simple color blocks contain profound depth.

Theoretical Foundation (Chaos Theory & Lyapunov Exponents)

In dynamical systems, the Lyapunov exponent (λ) measures the rate of separation of infinitesimally close trajectories:

λ > 0: System is chaotic—small changes lead to dramatically different outcomes (butterfly effect)

λ < 0: System is stable—trajectories converge, perturbations die out

λ ≈ 0: Edge of chaos—transition between regimes

Phase Space Reconstruction

Using Takens' embedding theorem , we reconstruct market dynamics in higher dimensions:

Time-delay embedding: Create vectors from price at different lags

Nearest neighbor search: Find historically similar market states

Trajectory evolution: Track how these similar states diverged over time

Divergence rate: Calculate average exponential separation

Market Application

Chaotic markets (λ > threshold): Strong trends emerge, momentum dominates, use breakout strategies

Stable markets (λ < threshold): Mean reversion dominates, fade extremes, range-bound strategies work

Transition zones: Market regime about to change, reduce position size, wait for confirmation

How LMI Works

1. Phase Space Construction

Each point in time is embedded as a vector using historical prices at specific delays (τ). This reveals the market's hidden attractor structure.

2. Lyapunov Calculation

For each current state, we:

- Find similar historical states within epsilon (ε) distance

- Track how these initially similar states evolved

- Measure exponential divergence rate

- Average across multiple trajectories for robustness

3. Signal Generation

Chaos signals: When λ crosses above threshold, market enters trending regime

Stability signals: When λ crosses below threshold, market enters ranging regime

Divergence detection: Price/Lyapunov divergences signal potential reversals

4. Rothko Visualization

Color fields: Background zones represent market states with Rothko-inspired palettes

Glowing line: Lyapunov exponent with intensity reflecting market state

Minimalist design: Focus on essential information without clutter

Inputs:

📐 Lyapunov Parameters

Embedding Dimension (default: 3)

Dimensions for phase space reconstruction

2-3: Simple dynamics (crypto/forex) - captures basic momentum patterns

4-5: Complex dynamics (stocks/indices) - captures intricate market structures

Higher dimensions need exponentially more data but reveal deeper patterns

Time Delay τ (default: 1)

Lag between phase space coordinates

1: High-frequency (1m-15m charts) - captures rapid market shifts

2-3: Medium frequency (1H-4H) - balances noise and signal

4-5: Low frequency (Daily+) - focuses on major regime changes

Match to your timeframe's natural cycle

Initial Separation ε (default: 0.001)

Neighborhood size for finding similar states

0.0001-0.0005: Highly liquid markets (major forex pairs)

0.0005-0.002: Normal markets (large-cap stocks)

0.002-0.01: Volatile markets (crypto, small-caps)

Smaller = more sensitive to chaos onset

Evolution Steps (default: 10)

How far to track trajectory divergence

5-10: Fast signals for scalping - quick regime detection

10-20: Balanced for day trading - reliable signals

20-30: Slow signals for swing trading - major regime shifts only

Nearest Neighbors (default: 5)

Phase space points for averaging

3-4: Noisy/fast markets - adapts quickly

5-6: Balanced (recommended) - smooth yet responsive

7-10: Smooth/slow markets - very stable signals

📊 Signal Parameters

Chaos Threshold (default: 0.05)

Lyapunov value above which market is chaotic

0.01-0.03: Sensitive - more chaos signals, earlier detection

0.05: Balanced - optimal for most markets

0.1-0.2: Conservative - only strong trends trigger

Stability Threshold (default: -0.05)

Lyapunov value below which market is stable

-0.01 to -0.03: Sensitive - quick stability detection

-0.05: Balanced - reliable ranging signals

-0.1 to -0.2: Conservative - only deep stability

Signal Smoothing (default: 3)

EMA period for noise reduction

1-2: Raw signals for experienced traders

3-5: Balanced - recommended for most

6-10: Very smooth for position traders

🎨 Rothko Visualization

Rothko Classic: Deep reds for chaos, midnight blues for stability

Orange/Red: Warm sunset tones throughout

Blue/Black: Cool, meditative ocean depths

Purple/Grey: Subtle, sophisticated palette

Visual Options:

Market Zones : Background fields showing regime areas

Transitions: Arrows marking regime changes

Divergences: Labels for price/Lyapunov divergences

Dashboard: Real-time state and trading signals

Guide: Educational panel explaining the theory

Visual Logic & Interpretation

Main Elements

Lyapunov Line: The heart of the indicator

Above chaos threshold: Market is trending, follow momentum

Below stability threshold: Market is ranging, fade extremes

Between thresholds: Transition zone, reduce risk

Background Zones: Rothko-inspired color fields

Red zone: Chaotic regime (trending)

Gray zone: Transition (uncertain)

Blue zone: Stable regime (ranging)

Transition Markers:

Up triangle: Entering chaos - start trend following

Down triangle: Entering stability - start mean reversion

Divergence Signals:

Bullish: Price makes low but Lyapunov rising (stability breaking down)

Bearish: Price makes high but Lyapunov falling (chaos dissipating)

Dashboard Information

Market State: Current regime (Chaotic/Stable/Transitioning)

Trading Bias: Specific strategy recommendation

Lyapunov λ: Raw value for precision

Signal Strength: Confidence in current regime

Last Change: Bars since last regime shift

Action: Clear trading directive

Trading Strategies

In Chaotic Regime (λ > threshold)

Follow trends aggressively: Breakouts have high success rate

Use momentum strategies: Moving average crossovers work well

Wider stops: Expect larger swings

Pyramid into winners: Trends tend to persist

In Stable Regime (λ < threshold)

Fade extremes: Mean reversion dominates

Use oscillators: RSI, Stochastic work well

Tighter stops: Smaller expected moves

Scale out at targets: Trends don't persist

In Transition Zone

Reduce position size: Uncertainty is high

Wait for confirmation: Let regime establish

Use options: Volatility strategies may work

Monitor closely: Quick changes possible

Advanced Techniques

- Multi-Timeframe Analysis

- Higher timeframe LMI for regime context

- Lower timeframe for entry timing

- Alignment = highest probability trades

- Divergence Trading

- Most powerful at regime boundaries

- Combine with support/resistance

- Use for early reversal detection

- Volatility Correlation

- Chaos often precedes volatility expansion

- Stability often precedes volatility contraction

- Use for options strategies

Originality & Innovation

LMI represents a genuine breakthrough in applying chaos theory to markets:

True Lyapunov Calculation: Not a simplified proxy but actual phase space reconstruction and divergence measurement

Rothko Aesthetic: Transforms complex math into meditative visual experience

Regime Detection: Identifies market state changes before price makes them obvious

Practical Application: Clear, actionable signals from theoretical physics

This is not a combination of existing indicators or a visual makeover of standard tools. It's a fundamental rethinking of how we measure and visualize market dynamics.

Best Practices

Start with defaults: Parameters are optimized for broad market conditions

Match to your timeframe: Adjust tau and evolution steps

Confirm with price action: LMI shows regime, not direction

Use appropriate strategies: Chaos = trend, Stability = reversion

Respect transitions: Reduce risk during regime changes

Alerts Available

Chaos Entry: Market entering chaotic regime - prepare for trends

Stability Entry: Market entering stable regime - prepare for ranges

Bullish Divergence: Potential bottom forming

Bearish Divergence: Potential top forming

Chart Information

Script Name: Lyapunov Market Instability (LMI) Recommended Use: All markets, all timeframes Best Performance: Liquid markets with clear regimes

Academic References

Takens, F. (1981). "Detecting strange attractors in turbulence"

Wolf, A. et al. (1985). "Determining Lyapunov exponents from a time series"

Rosenstein, M. et al. (1993). "A practical method for calculating largest Lyapunov exponents"

Note: After completing this indicator, I discovered @loxx's 2022 "Lyapunov Hodrick-Prescott Oscillator w/ DSL". While both explore Lyapunov exponents, they represent independent implementations with different methodologies and applications. This indicator uses phase space reconstruction for regime detection, while his combines Lyapunov concepts with HP filtering.

Disclaimer

This indicator is for research and educational purposes only. It does not constitute financial advice or provide direct buy/sell signals. Chaos theory reveals market character, not future prices. Always use proper risk management and combine with your own analysis. Past performance does not guarantee future results.

See markets through the lens of chaos. Trade the regime, not the noise.

Bringing theoretical physics to practical trading through the meditative aesthetics of Mark Rothko

Trade with insight. Trade with anticipation.

— Dskyz , for DAFE Trading Systems

Full Day Midpoint Line with Dynamic StdDev Bands (ETH & RTH)A Pine Script indicator designed to plot a midpoint line based on the high and low prices of a user-defined trading session (typically Extended Trading Hours, ETH) and to add dynamic standard deviation (StdDev) bands around this midpoint.

Session Midpoint Line:

The midpoint is calculated as the average of the session's highest high and lowest low during the defined ETH period (e.g., 4:00 AM to 8:00 PM).

This line represents a central tendency or "fair value" for the session, similar to a pivot point or volume-weighted average price (VWAP) anchor.

Interpretation:

Prices above the midpoint suggest bullish sentiment, while prices below indicate bearish sentiment.

The midpoint can act as a dynamic support/resistance level, where price may revert to or react at this level during the session.

Dynamic StdDev Bands:

The bands are calculated by adding/subtracting a multiple of the standard deviation of the midpoint values (tracked in an array) from the midpoint.

The standard deviation is dynamically computed based on the historical midpoint values within the session, making the bands adaptive to volatility.

Interpretation:

The upper and lower bands represent potential overbought (upper) and oversold (lower) zones.

Prices approaching or crossing the bands may indicate stretched conditions, potentially signaling reversals or breakouts.

Trend Identification:

Use the midpoint as a reference for the session’s trend. Persistent price action above the midpoint suggests bullishness, while below indicates bearishness.

Combine with other indicators (e.g., moving averages, RSI) to confirm trend direction.

Support/Resistance Trading:

Treat the midpoint as a dynamic pivot point. Price rejections or consolidations near the midpoint can be entry points for mean-reversion trades.

The StdDev bands can act as secondary support/resistance levels. For example, price reaching the upper band may signal a potential short entry if accompanied by reversal signals.

Breakout/Breakdown Strategies:

A strong move beyond the upper or lower band may indicate a breakout (bullish above upper, bearish below lower). Confirm with volume or momentum indicators to avoid false breakouts.

The dynamic nature of the bands makes them useful for identifying significant price extensions.

Volatility Assessment:

Wider bands indicate higher volatility, suggesting larger price swings and potentially riskier trades.

Narrow bands suggest consolidation, which may precede a breakout. Traders can prepare for volatility expansions in such scenarios.

The "Full Day Midpoint Line with Dynamic StdDev Bands" is a versatile and visually intuitive indicator well-suited for day traders focusing on session-specific price action. Its dynamic midpoint and volatility-adjusted bands provide valuable insights into support, resistance, and potential reversals or breakouts.

Enhanced BTC Order Block IndicatorThe script you provided is an "Enhanced BTC Order Block Indicator" written in Pine Script v5 for TradingView. It is designed to identify and visually mark Order Blocks (OBs) on a Bitcoin (BTC) price chart, specifically tailored for a high-frequency scalping strategy on the 5-minute (M5) timeframe. Order Blocks are key price zones where institutional traders are likely to have placed significant buy or sell orders, making them high-probability areas for reversals or continuations. The script incorporates customizable filters, visual indicators, and alert functionality to assist traders in executing the strategy outlined earlier.

Key Features and Functionality

Purpose:

The indicator detects bullish Order Blocks (buy zones) and bearish Order Blocks (sell zones) based on a predefined percentage price movement (default 0.5–1%) and volume confirmation.

It marks these zones on the chart with colored boxes and provides alerts when an OB is detected.

User-Configurable Inputs:

Price Move Range: minMovePercent (default 0.5%) and maxMovePercent (default 1.0%) define the acceptable price movement range for identifying OBs.

Volume Threshold: volumeThreshold (default 1.5x average volume) ensures OB detection is backed by significant trading activity.

Lookback Period: lookback (default 10 candles) determines how many previous candles are analyzed to find the last candle before a strong move.

Wick/Body Option: useWick (default false) allows users to choose whether the OB zone is based on the candle’s wick or body.

Colors: bullishOBColor (default green) and bearishOBColor (default red) set the visual appearance of OB boxes.

Box Extension: boxExtension (default 100 bars) controls how far the OB box extends to the right on the chart.

RSI Filter: useRSI (default true) enables an RSI filter, with rsiLength (default 14), rsiBullishThreshold (default 50), and rsiBearishThreshold (default 50) for trend confirmation.

M15 Support/Resistance: useSR (default true) and srLookback (default 20) integrate M15 timeframe swing highs and lows for additional OB validation.

Core Logic:

Bullish OB Detection: Identifies a strong upward move (0.5–1%) with volume above the threshold. It then looks back to the last bearish candle before the move to define the OB zone. RSI > 50 and proximity to M15 support/resistance (optional) enhance confirmation.

Bearish OB Detection: Identifies a strong downward move (0.5–1%) with volume confirmation, tracing back to the last bullish candle. RSI < 50 and M15 resistance proximity (optional) add validation.

The OB zone is drawn as a rectangle from the high to low of the identified candle, extended rightward.

Visual Output:

Boxes: Uses box.new to draw OB zones, with left set to the previous bar (bar_index ), right extended by boxExtension, top and bottom defined by the OB’s high and low prices. Each box includes a text label ("Bullish OB" or "Bearish OB") and is semi-transparent.

Colors distinguish between bullish (green) and bearish (red) OBs.

Alerts:

Global alertcondition definitions trigger notifications for "Bullish OB Detected" and "Bearish OB Detected" when the respective conditions are met, displaying the current close price in the message.

Helper Functions:

f_priceChangePercent: Calculates the percentage price change between open and close prices.

isNearSR: Checks if the price is within 0.2% of M15 swing highs or lows for support/resistance confluence.

How It Works

The script runs on each candle, evaluating the current price action against the user-defined criteria.

When a bullish or bearish move is detected (meeting the percentage, volume, RSI, and S/R conditions), it identifies the preceding candle to define the OB zone.

The OB is then visualized on the chart, and an alert is triggered if configured in TradingView.

Use Case

This indicator is tailored for your BTC scalping strategy, where trades last 1–15 minutes targeting 0.3–0.5% gains. It helps traders spot institutional order zones on the M5 chart, confirmed by secondary M1 analysis, and integrates with your use of EMAs, RSI, and volume. The customizable settings allow adaptation to varying market conditions or personal preferences.

Limitations

The M15 S/R detection is simplified (using swing highs/lows), which may not always align perfectly with manual support/resistance levels.

Alerts depend on TradingView’s alert system and require manual setup.

Performance may vary with high volatility or low-volume periods, necessitating parameter adjustments.

Ultimate Scalping Tool[BullByte]Overview

The Ultimate Scalping Tool is an open-source TradingView indicator built for scalpers and short-term traders released under the Mozilla Public License 2.0. It uses a custom Quantum Flux Candle (QFC) oscillator to combine multiple market forces into one visual signal. In plain terms, the script reads momentum, trend strength, volatility, and volume together and plots a special “candlestick” each bar (the QFC) that reflects the overall market bias. This unified view makes it easier to spot entries and exits: the tool labels signals as Strong Buy/Sell, Pullback (a brief retracement in a trend), Early Entry, or Exit Warning . It also provides color-coded alerts and a small dashboard of metrics. In practice, traders see green/red oscillator bars and symbols on the chart when conditions align, helping them scalp or trend-follow without reading multiple separate indicators.

Core Components

Quantum Flux Candle (QFC) Construction

The QFC is the heart of the indicator. Rather than using raw price, it creates a candlestick-like bar from the underlying oscillator values. Each QFC bar has an “open,” “high/low,” and “close” derived from calculated momentum and volatility inputs for that period . In effect, this turns the oscillator into intuitive candle patterns so traders can recognize momentum shifts visually. (For comparison, note that Heikin-Ashi candles “have a smoother look because take an average of the movement”. The QFC instead represents exact oscillator readings, so it reflects true momentum changes without hiding price action.) Colors of QFC bars change dynamically (e.g. green for bullish momentum, red for bearish) to highlight shifts. This is the first open-source QFC oscillator that dynamically weights four non-correlated indicators with moving thresholds, which makes it a unique indicator on its own.

Oscillator Normalization & Adaptive Weights

The script normalizes its oscillator to a fixed scale (for example, a 0–100 range much like the RSI) so that various inputs can be compared fairly. It then applies adaptive weighting: the relative influence of trend, momentum, volatility or volume signals is automatically adjusted based on current market conditions. For instance, in very volatile markets the script might weight volatility more heavily, or in a strong trend it might give extra weight to trend direction. Normalizing data and adjusting weights helps keep the QFC sensitive but stable (normalization ensures all inputs fit a common scale).

Trend/Momentum/Volume/Volatility Fusion

Unlike a typical single-factor oscillator, the QFC oscillator fuses four aspects at once. It may compute, for example, a trend indicator (such as an ADX or moving average slope), a momentum measure (like RSI or Rate-of-Change), a volume-based pressure (similar to MFI/OBV), and a volatility measure (like ATR) . These different values are combined into one composite oscillator. This “multi-dimensional” approach follows best practices of using non-correlated indicators (trend, momentum, volume, volatility) for confirmation. By encoding all these signals in one line, a high QFC reading means that trend, momentum, and volume are all aligned, whereas a neutral reading might mean mixed conditions. This gives traders a comprehensive picture of market strength.

Signal Classification

The script interprets the QFC oscillator to label trades. For example:

• Strong Buy/Sell : Triggered when the oscillator crosses a high-confidence threshold (e.g. breaks clearly above zero with strong slope), indicating a well-confirmed move. This is like seeing a big green/red QFC candle aligned with the trend.

• Pullbacks : Identified when the trend is up but momentum dips briefly. A Pullback Buy appears if the overall trend is bullish but the oscillator has a short retracement – a typical buying opportunity in an uptrend. (A pullback is “a brief decline or pause in a generally upward price trend”.)

• Early Buy/Sell : Marks an initial swing in the oscillator suggesting a possible new trend, before it is fully confirmed. It’s a hint of momentum building (an early-warning signal), not as strong as the confirmed “Strong” signal.

• Exit Warnings : Issued when momentum peaks or reverses. For instance, if the QFC bars reach a high and start turning red/green opposite, the indicator warns that the move may be ending. In other words, a Momentum Peak is the point of maximum strength after which weakness may follow.

These categories correspond to typical trading concepts: Pullback (temporary reversal in an uptrend), Early Buy (an initial bullish cross), Strong Buy (confirmed bullish momentum), and Momentum Peak (peak oscillator value suggesting exhaustion).

Filters (DI Reversal, Dynamic Thresholds, HTF EMA/ADX)

Extra filters help avoid bad trades. A DI Reversal filter uses the +DI/–DI lines (from the ADX system) to require that the trend direction confirms the signal . For example, it might ignore a buy signal if the +DI is still below –DI. Dynamic Thresholds adjust signal levels on-the-fly: rather than fixed “overbought” lines, they move with volatility so signals happen under appropriate market stress. An optional High-Timeframe EMA or ADX filter adds a check against a larger timeframe trend: for instance, only taking a trade if price is above the weekly EMA or if weekly ADX shows a strong trend. (Notably, the ADX is “a technical indicator used by traders to determine the strength of a price trend”, so requiring a high-timeframe ADX avoids trading against the bigger trend.)

Dashboard Metrics & Color Logic

The Dashboard in the Ultimate Scalping Tool (UST) serves as a centralized information hub, providing traders with real-time insights into market conditions, trend strength, momentum, volume pressure, and trade signals. It is highly customizable, allowing users to adjust its appearance and content based on their preferences.

1. Dashboard Layout & Customization

Short vs. Extended Mode : Users can toggle between a compact view (9 rows) and an extended view (13 rows) via the `Short Dashboard` input.

Text Size Options : The dashboard supports three text sizes— Tiny, Small, and Normal —adjustable via the `Dashboard Text Size` input.

Positioning : The dashboard is positioned in the top-right corner by default but can be moved if modified in the script.

2. Key Metrics Displayed

The dashboard presents critical trading metrics in a structured table format:

Trend (TF) : Indicates the current trend direction (Strong Bullish, Moderate Bullish, Sideways, Moderate Bearish, Strong Bearish) based on normalized trend strength (normTrend) .

Momentum (TF) : Displays momentum status (Strong Bullish/Bearish or Neutral) derived from the oscillator's position relative to dynamic thresholds.

Volume (CMF) : Shows buying/selling pressure levels (Very High Buying, High Selling, Neutral, etc.) based on the Chaikin Money Flow (CMF) indicator.

Basic & Advanced Signals:

Basic Signal : Provides simple trade signals (Strong Buy, Strong Sell, Pullback Buy, Pullback Sell, No Trade).

Advanced Signal : Offers nuanced signals (Early Buy/Sell, Momentum Peak, Weakening Momentum, etc.) with color-coded alerts.

RSI : Displays the Relative Strength Index (RSI) value, colored based on overbought (>70), oversold (<30), or neutral conditions.

HTF Filter : Indicates the higher timeframe trend status (Bullish, Bearish, Neutral) when using the Leading HTF Filter.

VWAP : Shows the V olume-Weighted Average Price and whether the current price is above (bullish) or below (bearish) it.

ADX : Displays the Average Directional Index (ADX) value, with color highlighting whether it is rising (green) or falling (red).

Market Mode : Shows the selected market type (Crypto, Stocks, Options, Forex, Custom).

Regime : Indicates volatility conditions (High, Low, Moderate) based on the **ATR ratio**.

3. Filters Status Panel

A secondary panel displays the status of active filters, helping traders quickly assess which conditions are influencing signals:

- DI Reversal Filter: On/Off (confirms reversals before generating signals).

- Dynamic Thresholds: On/Off (adjusts buy/sell thresholds based on volatility).

- Adaptive Weighting: On/Off (auto-adjusts oscillator weights for trend/momentum/volatility).

- Early Signal: On/Off (enables early momentum-based signals).

- Leading HTF Filter: On/Off (applies higher timeframe trend confirmation).

4. Visual Enhancements

Color-Coded Cells : Each metric is color-coded (green for bullish, red for bearish, gray for neutral) for quick interpretation.

Dynamic Background : The dashboard background adapts to market conditions (bullish/bearish/neutral) based on ADX and DI trends.

Customizable Reference Lines : Users can enable/disable fixed reference lines for the oscillator.

How It(QFC) Differs from Traditional Indicators

Quantum Flux Candle (QFC) Versus Heikin-Ashi

Heikin-Ashi candles smooth price by averaging (HA’s open/close use averages) so they show trend clearly but hide true price (the current HA bar’s close is not the real price). QFC candles are different: they are oscillator values, not price averages . A Heikin-Ashi chart “has a smoother look because it is essentially taking an average of the movement”, which can cause lag. The QFC instead shows the raw combined momentum each bar, allowing faster recognition of shifts. In short, HA is a smoothed price chart; QFC is a momentum-based chart.

Versus Standard Oscillators

Common oscillators like RSI or MACD use fixed formulas on price (or price+volume). For example, RSI “compares gains and losses and normalizes this value on a scale from 0 to 100”, reflecting pure price momentum. MFI is similar but adds volume. These indicators each show one dimension: momentum or volume. The Ultimate Scalping Tool’s QFC goes further by integrating trend strength and volatility too. In practice, this means a move that looks strong on RSI might be downplayed by low volume or weak trend in QFC. As one source notes, using multiple non-correlated indicators (trend, momentum, volume, volatility) provides a more complete market picture. The QFC’s multi-factor fusion is unique – it is effectively a multi-dimensional oscillator rather than a traditional single-input one.

Signal Style

Traditional oscillators often use crossovers (RSI crossing 50) or fixed zones (MACD above zero) for signals. The Ultimate Scalping Tool’s signals are custom-classified: it explicitly labels pullbacks, early entries, and strong moves. These terms go beyond a typical indicator’s generic “buy”/“sell.” In other words, it packages a strategy around the oscillator, which traders can backtest or observe without reading code.

Key Term Definitions

• Pullback : A short-term dip or consolidation in an uptrend. In this script, a Pullback Buy appears when price is generally rising but shows a brief retracement. (As defined by Investopedia, a pullback is “a brief decline or pause in a generally upward price trend”.)

• Early Buy/Sell : An initial or tentative entry signal. It means the oscillator first starts turning positive (or negative) before a full trend has developed. It’s an early indication that a trend might be starting.

• Strong Buy/Sell : A confident entry signal when multiple conditions align. This label is used when momentum is already strong and confirmed by trend/volume filters, offering a higher-probability trade.

• Momentum Peak : The point where bullish (or bearish) momentum reaches its maximum before weakening. When the oscillator value stops rising (or falling) and begins to reverse, the script flags it as a peak – signaling that the current move could be overextended.

What is the Flux MA?

The Flux MA (Moving Average) is an Exponential Moving Average (EMA) applied to a normalized oscillator, referred to as FM . Its purpose is to smooth out the fluctuations of the oscillator, providing a clearer picture of the underlying trend direction and strength. Think of it as a dynamic baseline that the oscillator moves above or below, helping you determine whether the market is trending bullish or bearish.

How it’s calculated (Flux MA):

1.The oscillator is normalized (scaled to a range, typically between 0 and 1, using a default scale factor of 100.0).

2.An EMA is applied to this normalized value (FM) over a user-defined period (default is 10 periods).

3.The result is rescaled back to the oscillator’s original range for plotting.

Why it matters : The Flux MA acts like a support or resistance level for the oscillator, making it easier to spot trend shifts.

Color of the Flux Candle

The Quantum Flux Candle visualizes the normalized oscillator (FM) as candlesticks, with colors that indicate specific market conditions based on the relationship between the FM and the Flux MA. Here’s what each color means:

• Green : The FM is above the Flux MA, signaling bullish momentum. This suggests the market is trending upward.

• Red : The FM is below the Flux MA, signaling bearish momentum. This suggests the market is trending downward.

• Yellow : Indicates strong buy conditions (e.g., a "Strong Buy" signal combined with a positive trend). This is a high-confidence signal to go long.

• Purple : Indicates strong sell conditions (e.g., a "Strong Sell" signal combined with a negative trend). This is a high-confidence signal to go short.

The candle mode shows the oscillator’s open, high, low, and close values for each period, similar to price candlesticks, but it’s the color that provides the quick visual cue for trading decisions.

How to Trade the Flux MA with Respect to the Candle

Trading with the Flux MA and Quantum Flux Candle involves using the MA as a trend indicator and the candle colors as entry and exit signals. Here’s a step-by-step guide:

1. Identify the Trend Direction

• Bullish Trend : The Flux Candle is green and positioned above the Flux MA. This indicates upward momentum.

• Bearish Trend : The Flux Candle is red and positioned below the Flux MA. This indicates downward momentum.

The Flux MA serves as the reference line—candles above it suggest buying pressure, while candles below it suggest selling pressure.

2. Interpret Candle Colors for Trade Signals

• Green Candle : General bullish momentum. Consider entering or holding a long position.

• Red Candle : General bearish momentum. Consider entering or holding a short position.

• Yellow Candle : A strong buy signal. This is an ideal time to enter a long trade.

• Purple Candle : A strong sell signal. This is an ideal time to enter a short trade.

3. Enter Trades Based on Crossovers and Colors

• Long Entry : Enter a buy position when the Flux Candle turns green and crosses above the Flux MA. If it turns yellow, this is an even stronger signal to go long.

• Short Entry : Enter a sell position when the Flux Candle turns red and crosses below the Flux MA. If it turns purple, this is an even stronger signal to go short.

4. Exit Trades

• Exit Long : Close your buy position when the Flux Candle turns red or crosses below the Flux MA, indicating the bullish trend may be reversing.

• Exit Short : Close your sell position when the Flux Candle turns green or crosses above the Flux MA, indicating the bearish trend may be reversing.

•You might also exit a long trade if the candle changes from yellow to green (weakening strong buy signal) or a short trade from purple to red (weakening strong sell signal).

5. Use Additional Confirmation

To avoid false signals, combine the Flux MA and candle signals with other indicators or dashboard metrics (e.g., trend strength, momentum, or volume pressure). For example:

•A yellow candle with a " Strong Bullish " trend and high buying volume is a robust long signal.

•A red candle with a " Moderate Bearish " trend and neutral momentum might need more confirmation before shorting.

Practical Example

Imagine you’re scalping a cryptocurrency:

• Long Trade : The Flux Candle turns yellow and is above the Flux MA, with the dashboard showing "Strong Buy" and high buying volume. You enter a long position. You exit when the candle turns red and dips below the Flux MA.

• Short Trade : The Flux Candle turns purple and crosses below the Flux MA, with a "Strong Sell" signal on the dashboard. You enter a short position. You exit when the candle turns green and crosses above the Flux MA.

Market Presets and Adaptation

This indicator is designed to work on any market with candlestick price data (stocks, crypto, forex, indices, etc.). To handle different behavior, it provides presets for major asset classes. Selecting a “Stocks,” “Crypto,” “Forex,” or “Options” preset automatically loads a set of parameter values optimized for that market . For example, a crypto preset might use a shorter lookback or higher sensitivity to account for crypto’s high volatility, while a stocks preset might use slightly longer smoothing since stocks often trend more slowly. In practice, this means the same core QFC logic applies across markets, but the thresholds and smoothing adjust so signals remain relevant for each asset type.

Usage Guidelines

• Recommended Timeframes : Optimized for 1 minute to 15 minute intraday charts. Can also be used on higher timeframes for short term swings.

• Market Types : Select “Crypto,” “Stocks,” “Forex,” or “Options” to auto tune periods, thresholds and weights. Use “Custom” to manually adjust all inputs.

• Interpreting Signals : Always confirm a signal by checking that trend, volume, and VWAP agree on the dashboard. A green “Strong Buy” arrow with green trend, green volume, and price > VWAP is highest probability.

• Adjusting Sensitivity : To reduce false signals in fast markets, enable DI Reversal Confirmation and Dynamic Thresholds. For more frequent entries in trending environments, enable Early Entry Trigger.

• Risk Management : This tool does not plot stop loss or take profit levels. Users should define their own risk parameters based on support/resistance or volatility bands.

Background Shading

To give you an at-a-glance sense of market regime without reading numbers, the indicator automatically tints the chart background in three modes—neutral, bullish and bearish—with two levels of intensity (light vs. dark):

Neutral (Gray)

When ADX is below 20 the market is considered “no trend” or too weak to trade. The background fills with a light gray (high transparency) so you know to sit on your hands.

Bullish (Green)

As soon as ADX rises above 20 and +DI exceeds –DI, the background turns a semi-transparent green, signaling an emerging uptrend. When ADX climbs above 30 (strong trend), the green becomes more opaque—reminding you that trend-following signals (Strong Buy, Pullback) carry extra weight.

Bearish (Red)

Similarly, if –DI exceeds +DI with ADX >20, you get a light red tint for a developing downtrend, and a darker, more solid red once ADX surpasses 30.

By dynamically varying both hue (green vs. red vs. gray) and opacity (light vs. dark), the background instantly communicates trend strength and direction—so you always know whether to favor breakout-style entries (in a strong trend) or stay flat during choppy, low-ADX conditions.

The setup shown in the above chart snapshot is BTCUSD 15 min chart : Binance for reference.

Disclaimer

No indicator guarantees profits. Backtest or paper trade this tool to understand its behavior in your market. Always use proper position sizing and stop loss orders.

Good luck!

- BullByte

Volume-Weighted Price MovementThe Volume-Weighted Price Movement (VWPM) indicator is an easy to read technical analysis tool that analyses how volume and price movement work together to drive market momentum.

How It Works

The VWPM indicator tracks two primary components:

Bullish Movement (green line): Measures the upward price movement weighted by volume. When price closes above the open, this component calculates how much buying pressure exists by multiplying the price change (close - open) by the volume of that period.

Bearish Movement (red line): Measures the downward price movement weighted by volume. When price closes below the open, this component calculates how much selling pressure exists by multiplying the price change (open - close) by the volume of that period.

Bull-Bear Difference (lime/orange line): Shows the net momentum by subtracting bearish movement from bullish movement, providing an at-a-glance view of which force is dominant.

The VWPM integrates volume data to identify whether price movements are backed by significant participation. A large price move with low volume carries less weight than the same move with high volume, providing a more accurate reflection of market strength.

A shorter lookback period makes the indicator more responsive to recent price action, while a longer period smooths out market noise for trend identification.

Interpretation

Bullish Signals

When the green line (bull movement) rises and stays above the red line

When the Bull-Bear Difference line crosses above zero and maintains positive momentum

Divergence between price making lower lows but the bull line making higher lows (hidden strength)

Bearish Signals

When the red line (bear movement) rises and stays above the green line

When the Bull-Bear Difference line crosses below zero and maintains negative momentum

Divergence between price making higher highs but the bull line making lower highs (hidden weakness)

open source, if anyone makes the script better please let me know :)

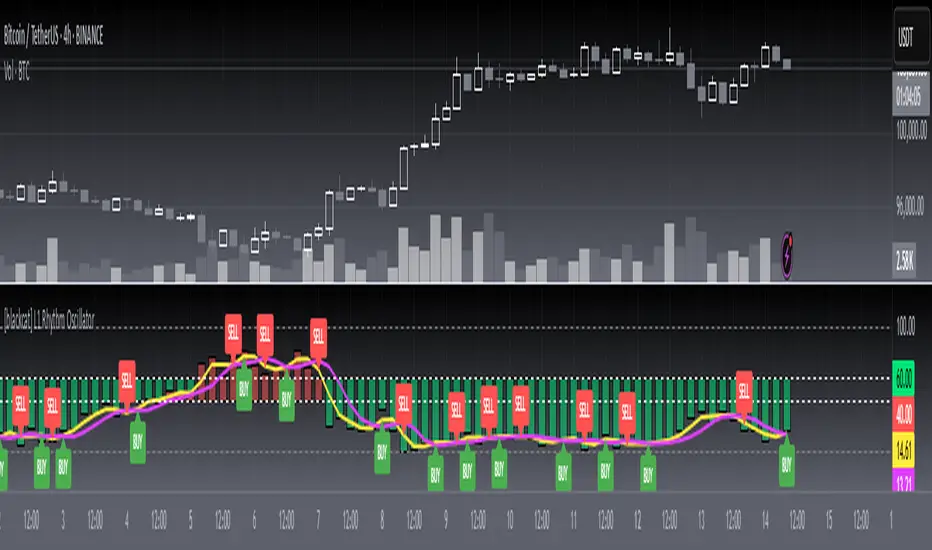

[blackcat] L1 Rhythm OscillatorOVERVIEW 📊💡

The L1 Rhythm Oscillator is an advanced oscillator designed to identify potential entry points in financial markets using a combination of Williams %R indicators and Time-Varying Moving Averages (TVMAs). This script provides traders with clear buy and sell signals that help them capitalize on trends while minimizing risk.

FEATURES 💡🌟

Williams %R Analysis:

Base Indicator (WR0): Measures overbought/oversold conditions within a specified period.

Smoothed Indicators (WR1 & WR2): Further refined versions of WR0 to filter out noise and highlight significant trends.

Dynamic Bands:

Bull Band: Shaded area between WR0 and the bullish threshold when WR0 falls below the defined level.

Bear Band: Shaded area between WR0 and the bearish threshold when WR0 exceeds the defined level.

Trading Signals:

Buy Signal: Generated when WR1 crosses above WR2, indicating a potential upward trend reversal.

Sell Signal: Triggered when WR1 crosses below WR2, suggesting a downward trend shift.

Thresholds:

Bull Threshold (default 60%): Marks levels where the asset is considered relatively undervalued.

Bear Threshold (default 40%): Indicates regions where the asset might be overvalued.

Visual Enhancements:

Colored Bands: Clearly distinguish between bullish and bearish areas.

Horizontal Lines: Provide quick reference points for overbought/oversold levels.

Labels: Display "BUY" and "SELL" markers at key signal locations.

HOW TO USE ⚙️📈

Add the Indicator to Your Chart:

Open your preferred asset's chart on TradingView.

Click on “Indicators” and search for “ L1 Rhythm Oscillator.”

Add the indicator to your chart.

Customize Parameters:

Adjust these inputs according to your trading strategy:

WR Period: Sets the lookback window for calculating Williams %R.

Bull Threshold: Defines the upper limit for bullish territory.

Bear Threshold: Establishes the lower boundary for bearish territory.

TVMA Length: Controls the sensitivity of the moving average used in calculations.

Interpret Visual Elements:

Yellow Line (WR1): The first smoothed version of the base Williams %R.

Fuchsia Line (WR2): The second smoothed line derived from WR1 via TVMA.

Lime-Shaded Area: Represents Bull Band where prices are potentially undervalued.

Red-Shaded Area: Symbolizes Bear Band indicating possible overvaluation.

Horizontal Lines:

Value 0% represents perfect overbought condition.

Value 100% indicates extreme oversold state.

Bull/Bear thresholds provide additional context for interpreting market sentiment.

Act on Crossovers:

Look for instances where WR1 crosses through WR2:

When WR1 moves above WR2 → Potential BUY opportunity.

When WR1 dips below WR2 → Likely SELL scenario.

Consider Contextual Factors:

Combine the oscillator signals with other technical indicators like MACD, RSI, or volume analysis for more robust decision-making.

Be aware of broader market trends and news events that could impact price movements.

Manage Risk:

Always use proper stop-loss orders to protect against adverse price movements.

Consider position sizing based on available capital and risk tolerance.

LIMITATIONS ⚠️🔍

Historical Data Dependency: Like most oscillators, this tool relies on past data patterns which may not always predict future behavior accurately.

False Signals: No single indicator can guarantee correct predictions; false positives/negatives can arise during volatile periods.

Overfitting Risks: Customized settings might work well historically but fail under different market conditions without careful validation.

Complexity: Multiple layers of smoothing and crossover logic require understanding to interpret correctly.

NOTES 🔍📝

Parameter Optimization: Experiment with various combinations of WR Period, Bull/Bear Thresholds, and TVMA Length to find what works best for specific assets and timeframes.

Regular Review: Continuously monitor the performance of the indicator versus actual outcomes, adjusting parameters as needed.

Educational Resources: Deepen your knowledge about oscillator strategies, particularly focusing on how they detect reversals and momentum shifts.

Consistency Key: For successful implementation, maintain consistent rules regarding trade entries/exits regardless of short-term fluctuations.

Support BandsSupport Bands – Discount Zones for Bitcoin

⚡Overview:

-The Support Bands indicator identifies one of the most tested and respected support zones for Bitcoin using moving averages from higher timeframes.

-These zones are visualized through colored bands (blue, white, and violet), simplifying the decision making process especially for less experienced traders who seek high-probability areas to accumulate Bitcoin during retracements.

-Band levels are based on manual backtesting and real-world price behavior throughout Bitcoin’s history.

-Each zone reflects a different degree of support strength, from temporary pullback zones to historical bottoms.

⚡️ Key Characteristics:

-Highlights discount zones where Bitcoin has historically shown strong reactions.

-Uses 3 different levels of supports based on EMA/SMA combinations.

-Offers a clean, non-intrusive overlay that reduces chart clutter.

⚡ How to Use:

-Open your chart on the 1W timeframe and select the BTC Bitstamp or BLX symbol, as they provide the most complete historical data, ensuring optimal performance of the indicator.

-Use the bands as reference zones for support and potential pullbacks.

- Level 3 (violet band) historically marks the bottom of Bitcoin bear markets and is ideal for long-term entries during deep corrections.

- Level 2 (white band) often signals macro reaccumulation zones but usually requires 1–3 months of consolidation before a breakout. If the price closes below and then retests this level as resistance for 1–2 weekly candles, it often marks the start of a macro downtrend.

-Level 1 (blue band) acts as short-term support during strong bullish moves, typically after a successful rebound from Level 2.

⚡ What Makes It Unique:

- This script merges moving averages per level into three simplified bands for clearer analysis.

-Reduces chart noise by avoiding multiple overlapping lines, helping you make faster and cleaner decisions.

- Built from manual market study based on recurring Bitcoin behavior, not just random code.

-Historically backtested:

-Level 3 (violet band) until today has always marked the bitcoin bearmarket bottom.

- Level 2 (white band) is the strongest support during bull markets; losing it often signals a macro trend reversal.

- Level 1 is frequently retested during impulsive rallies and can act as short-term support or resistance.

⚡ Disclaimer:

-This script is a visual tool to assist with market analysis.

-It does not generate buy or sell signals, nor does it predict future movements.

-Historical performance is not indicative of future results.

-Always use independent judgment and proper risk management.

⚡ Why Use Support Bands:

-Ideal for traders who want clarity without dozens of lines on their charts.

- Helps identify logical zones for entry or reaccumulation.

- Based on actual market behavior rather than hypothetical setups.

-If the blue band (Level 1) doesn't hold as support, the price often moves to the white band (Level 2), and if that fails too, the violet band (Level 3) is typically the last strong support. By dividing your capital into three planned entries, one at each level,you can manage risk more effectively compared to entering blindly without this structure.

Multi-Timeframe Continuity Custom Candle ConfirmationMulti-Timeframe Continuity Custom Candle Confirmation

Overview

The Timeframe Continuity Indicator is a versatile tool designed to help traders identify alignment between their current chart’s candlestick direction and higher timeframes of their choice. By coloring bars on the current chart (e.g., 1-minute) based on the directional alignment with selected higher timeframes (e.g., 10-minute, daily), this indicator provides a visual cue for confirming trends across multiple timeframes—a concept known as Timeframe Continuity. This approach is particularly useful for day traders, swing traders, and scalpers looking to ensure their trades align with broader market trends, reducing the risk of trading against the prevailing momentum.

Originality and Usefulness

This indicator is an original creation, built from scratch to address a common challenge in trading: ensuring that price action on a lower timeframe aligns with the trend on higher timeframes. Unlike many trend-following indicators that rely on moving averages, oscillators, or other lagging metrics, this script directly compares the bullish or bearish direction of candlesticks across timeframes. It introduces the following unique features:

Customizable Timeframes: Users can select from a range of higher timeframes (5m, 10m, 15m, 30m, 1h, 2h, 4h, 1d, 1w, 1M) to check for alignment, making it adaptable to various trading styles.

Neutral Candle Handling: The script accounts for neutral candles (where close == open) on the current timeframe by allowing them to inherit the direction of the higher timeframe, ensuring continuity in trend visualization.

Table: A table displays the direction of each selected timeframe and the current timeframe, helping identify direction in the event you don't want to color bars.

Toggles for Flexibility: Options to disable bar coloring and the debug table allow users to customize the indicator’s visual output for cleaner charts or focused analysis.

This indicator is not a mashup of existing scripts but a purpose-built tool to visualize timeframe alignment directly through candlestick direction, offering traders a straightforward way to confirm trend consistency.

What It Does

The Timeframe Continuity Indicator colors bars on your chart when the direction of the current timeframe’s candlestick (bullish, bearish, or neutral) aligns with the direction of the selected higher timeframes:

Lime: The current bar (e.g., 1m) is bullish or neutral, and all selected higher timeframes (e.g., 10m) are bullish.

Pink: The current bar is bearish or neutral, and all selected higher timeframes are bearish.

Default Color: If the directions don’t align (e.g., 1m bar is bearish but 10m is bullish), the bar remains the default chart color.

The indicator also includes a debug table (toggleable) that shows the direction of each selected timeframe and the current timeframe, helping traders diagnose alignment issues.

How It Works

The script uses the following methodology:

1. Direction Calculation: For each timeframe (current and selected higher timeframes), the script determines the candlestick’s direction:

Bullish (1): close > open / Bearish (-1): close < open / Neutral (0): close == open

Higher timeframe directions are fetched using Pine Script’s request.security function, ensuring accurate data retrieval.

2. Alignment Check: The script checks if all selected higher timeframes are uniformly bullish (full_bullish) or bearish (full_bearish).

o A higher timeframe must have a clear direction (bullish or bearish) to trigger coloring. If any selected timeframe is neutral, alignment fails, and no coloring occurs.

3. Coloring Logic: The current bar is colored only if its direction aligns with the higher timeframes:

Lime if the higher timeframes are bullish and the current bar is bullish or neutral.

Maroon if the higher timeframes are bearish and the current bar is bearish or neutral.

If the current bar’s direction opposes the higher timeframe (e.g., 1m bearish, 10m bullish), the bar remains uncolored.

Users can disable bar coloring entirely via the settings, leaving bars in their default chart color.

4. Direction Table:

A table in the top-right corner (toggleable) displays the direction of each selected timeframe and the current timeframe, using color-coded labels (green for bullish, red for bearish, gray for neutral).

This feature helps traders understand why a bar is or isn’t colored, making the indicator accessible to users unfamiliar with Pine Script.

How to Use

1. Add the Indicator: Add the "Timeframe Continuity Indicator" to your chart in TradingView (e.g., a 1m chart of SPY).

2. Configure Settings:

Timeframe Selection: Check the boxes for the higher timeframes you want to compare against (default: 10m). Options include 5m, 10m, 15m, 30m, 1h, 2h, 4h, 1D, 1W, and 1M. Select multiple timeframes if you want to ensure alignment across all of them (e.g., 10m and 1d).

Enable Bar Coloring: Default: true (bars are colored lime or maroon when aligned). Set to false to disable coloring and keep the default chart colors.

Show Table: Default: true (table is displayed in the top-right corner). Set to false to hide the table for a cleaner chart.

3. Interpret the Output:

Colored Bars: Lime bars indicate the current bar (e.g., 1m) is bullish or neutral, and all selected higher timeframes are bullish. Maroon bars indicate the current bar is bearish or neutral, and all selected higher timeframes are bearish. Uncolored bars (default chart color) indicate a mismatch (e.g., 1m bar is bearish while 10m is bullish) or no coloring if disabled.

Direction Table: Check the table to see the direction of each selected timeframe and the current timeframe.

4. Example Use Case:

On a 1m chart of SPY, select the 10m timeframe.

If the 10m timeframe is bearish, 1m bars that are bearish or neutral will color maroon, confirming you’re trading with the higher timeframe’s trend.

If a 1m bar is bullish while the 10m is bearish, it remains uncolored, signaling a potential misalignment to avoid trading.

Underlying Concepts