Range Trading StrategyOVERVIEW

The Range Trading Strategy is a systematic trading approach that identifies price ranges

from higher timeframe candles or trading sessions, tracks pivot points, and generates

trading signals when range extremes are mitigated and confirmed by pivot levels.

CORE CONCEPT

The strategy is based on the principle that when a candle (or session) closes within the

range of the previous candle (or session), that previous candle becomes a "range" with

identifiable high and low extremes. When price breaks through these extremes, it creates

trading opportunities that are confirmed by pivot levels.

RANGE DETECTION MODES

1. HTF (Higher Timeframe) Mode:

Automatically selects a higher timeframe based on the current chart timeframe

Uses request.security() to fetch HTF candle data

Range is created when an HTF candle closes within the previous HTF candle's range

The previous HTF candle's high and low become the range extremes

2. Sessions Mode:

- Divides the trading day into 4 sessions (UTC):

* Session 1: 00:00 - 06:00 (6 hours)

* Session 2: 06:00 - 12:00 (6 hours)

* Session 3: 12:00 - 20:00 (8 hours)

* Session 4: 20:00 - 00:00 (4 hours, spans midnight)

- Tracks high, low, and close for each session

- Range is created when a session closes within the previous session's range

- The previous session's high and low become the range extremes

PIVOT DETECTION

Pivots are detected based on candle color changes (bullish/bearish transitions):

1. Pivot Low:

Created when a bullish candle appears after a bearish candle

Pivot low = minimum of the current candle's low and previous candle's low

The pivot bar is the actual bar where the low was formed (current or previous bar)

2. Pivot High:

Created when a bearish candle appears after a bullish candle

Pivot high = maximum of the current candle's high and previous candle's high

The pivot bar is the actual bar where the high was formed (current or previous bar)

IMPORTANT: There is always only ONE active pivot high and ONE active pivot low at any

given time. When a new pivot is created, it replaces the previous one.

RANGE CREATION

A range is created when:

(HTF Mode) An HTF candle closes within the previous HTF candle's range AND a new HTF

candle has just started

(Sessions Mode) A session closes within the previous session's range AND a new session

has just started

Or Range Can Be Created when the Extreme of Another Range Gets Mitigated and We Have a Pivot low Just Above the Range Low or Pivot High just Below the Range High

Range Properties:

rangeHigh: The high extreme of the range

rangeLow: The low extreme of the range

highStartTime: The timestamp when the range high was actually formed (found by looping

backwards through bars)

lowStartTime: The timestamp when the range low was actually formed (found by looping

backwards through bars)

highMitigated / lowMitigated: Flags tracking whether each extreme has been broken

isSpecial: Flag indicating if this is a "special range" (see Special Ranges section)

RANGE MITIGATION

A range extreme is considered "mitigated" when price interacts with it:

High is mitigated when: high >= rangeHigh (any interaction at or above the level)

Low is mitigated when: low <= rangeLow (any interaction at or below the level)

Mitigation can happen:

At the moment of range creation (if price is already beyond the extreme)

At any point after range creation when price touches the extreme

SIGNAL GENERATION

1. Pending Signals:

When a range extreme is mitigated, a pending signal is created:

a) BEARISH Pending Signal:

- Triggered when: rangeHigh is mitigated

- Confirmation Level: Current pivotLow

- Signal is confirmed when: close < pivotLow

- Stop Loss: Current pivotHigh (at time of confirmation)

- Entry: Short position

Signal Confirmation

b) BULLISH Pending Signal:

- Triggered when: rangeLow is mitigated

- Confirmation Level: Current pivotHigh

- Signal is confirmed when: close > pivotHigh

- Stop Loss: Current pivotLow (at time of confirmation)

- Entry: Long position

IMPORTANT: There is only ever ONE pending bearish signal and ONE pending bullish signal

at any given time. When a new pending signal is created, it replaces the previous one

of the same type.

2. Signal Confirmation:

- Bearish: Confirmed when price closes below the pivot low (confirmation level)

- Bullish: Confirmed when price closes above the pivot high (confirmation level)

- Upon confirmation, a trade is entered immediately

- The confirmation line is drawn from the pivot bar to the confirmation bar

TRADE EXECUTION

When a signal is confirmed:

1. Position Management:

- Any existing position in the opposite direction is closed first

- Then the new position is entered

2. Stop Loss:

- Bearish (Short): Stop at pivotHigh

- Bullish (Long): Stop at pivotLow

3. Take Profit:

- Calculated using Risk:Reward Ratio (default 2:1)

- Risk = Distance from entry to stop loss

- Target = Entry ± (Risk × R:R Ratio)

- Can be disabled with "Stop Loss Only" toggle

4. Trade Comments:

- "Range Bear" for short trades

- "Range Bull" for long trades

SPECIAL RANGES

Special ranges are created when:

- A range high is mitigated AND the current pivotHigh is below the range high

- A range low is mitigated AND the current pivotLow is above the range low

In these cases:

- The pivot value is stored in an array (storedPivotHighs or storedPivotLows)

- A "special range" is created with only ONE extreme:

* If pivotHigh < rangeHigh: Creates a range with rangeHigh = pivotLow, rangeLow = na

* If pivotLow > rangeLow: Creates a range with rangeLow = pivotHigh, rangeHigh = na

- Special ranges can generate signals just like normal ranges

- If a special range is mitigated on the creation bar or the next bar, it is removed

entirely without generating signals (prevents false signals)

Special Ranges

REVERSE ON STOP LOSS

When enabled, if a stop loss is hit, the strategy automatically opens a trade in the

opposite direction:

1. Long Stop Loss Hit:

- Detects when: position_size > 0 AND position_size <= 0 AND low <= longStopLoss

- Action: Opens a SHORT position

- Stop Loss: Current pivotHigh

- Trade Comment: "Reverse on Stop"

2. Short Stop Loss Hit:

- Detects when: position_size < 0 AND position_size >= 0 AND high >= shortStopLoss

- Action: Opens a LONG position

- Stop Loss: Current pivotLow

- Trade Comment: "Reverse on Stop"

The reverse trade uses the same R:R ratio and respects the "Stop Loss Only" setting.

VISUAL ELEMENTS

1. Range Lines:

- Drawn from the time when the extreme was formed to the mitigation point (or current

time if not mitigated)

- High lines: Blue (or mitigated color if mitigated)

- Low lines: Red (or mitigated color if mitigated)

- Style: SOLID

- Width: 1

2. Confirmation Lines:

- Drawn when a signal is confirmed

- Extends from the pivot bar to the confirmation bar

- Bearish: Red, solid line

- Bullish: Green, solid line

- Width: 1

- Can be toggled on/off

STRATEGY SETTINGS

1. Range Detection Mode:

- HTF: Uses higher timeframe candles

- Sessions: Uses trading session boundaries

2. Auto HTF:

- Automatically selects HTF based on current chart timeframe

- Can be disabled to use manual HTF selection

3. Risk:Reward Ratio:

- Default: 2.0 (2:1)

- Minimum: 0.5

- Step: 0.5

4. Stop Loss Only:

- When enabled: Trades only have stop loss (no take profit)

- Trades close on stop loss or when opposite signal confirms

5. Reverse on Stop Loss:

- When enabled: Hitting a stop loss opens opposite trade with stop at opposing pivot

6. Max Ranges to Display:

- Limits the number of ranges kept in memory

- Oldest ranges are purged when limit is exceeded

KEY FEATURES

1. Dynamic Pivot Tracking:

- Pivots update on every candle color change

- Always maintains one high and one low pivot

2. Range Lifecycle:

- Ranges are created when price closes within previous range

- Ranges are tracked until mitigated

- Mitigation creates pending signals

- Signals are confirmed by pivot levels

3. Signal Priority:

- Only one pending signal of each type at a time

- New signals replace old ones

- Confirmation happens on close of bar

4. Position Management:

- Closes opposite positions before entering new trades

- Tracks stop loss levels for reverse functionality

- Respects pyramiding = 1 (only one position per direction)

5. Time-Based Drawing:

- Uses time coordinates instead of bar indices for line drawing

- Prevents "too far from current bar" errors

- Lines can extend to any historical point

USAGE NOTES

- Best suited for trending and ranging markets

- Works on any timeframe, but HTF mode adapts automatically

- Sessions mode is ideal for intraday trading

- Pivot detection requires clear candle color changes

- Range detection requires price to close within previous range

- Signals are generated on bar close, not intra-bar

The strategy combines range identification, pivot tracking, and signal confirmation to

create a systematic approach to trading breakouts and reversals based on price structure, past performance does not in any way predict future performance

"bar" için komut dosyalarını ara

D Money – EMA/TEMA Touch Strategy (Distance) What it’s trying to capture

You want mean-reversion “tags” back to a moving average after price has stretched away and momentum flips:

Bearish setup (short): price has been above EMA(9) for a few bars, then MACD turns bearish, and price is far enough above the EMA (by an adaptive threshold). Exit when price tags the EMA.

Bullish setup (long): price has been below your chosen TEMA rail (actually an EMA of 50/100/200 you pick) for a few bars, then MACD turns bullish, and price is far enough below that TEMA. Exit when price tags that TEMA.

The moving averages it uses

EMA(9) — your fast “tag” for short take-profits.

“TEMA line” input = one of EMA(50) / EMA(100) / EMA(200). (Labelled “Chosen TEMA” in the plot; it’s an EMA rail you pick.)

When it will enter trades

It requires four things per side:

Short (EMA-Touch Short)

MACD bearish cross on the signal bar

If “Require NO MA touch on cross bar” = true, the bar’s low must be above EMA(9), so it didn’t touch EMA on the cross bar (fake-out guard).

Extension/Context: you’ve had at least barsAbove consecutive closes above EMA(9) (default 3), so it’s truly stretched.

Distance test: absolute % distance from price to EMA(9) must be ≥ minDistEMA_eff (an adaptive threshold; details below).

Bounce filter: there was no bullish bounce off the EMA in the last bounceLookback bars (excluding the current one).

If all pass and you’re inside the backtest window → strategy.entry short.

Long (TEMA-Touch Long)

MACD bullish cross on the signal bar

With the same fake-out guard: the bar’s high must be below the chosen TEMA if the guard is on.

Extension/Context: at least barsAbove consecutive closes below the chosen TEMA.

Distance test: absolute % distance from price to TEMA must be ≥ minDistTEMA_eff (adaptive).

Bounce filter: there was no bearish bounce off the TEMA in the last bounceLookback bars.

If all pass and you’re in the window → strategy.entry long.

MACD timing option:

If Pure MACD Timing = ON, it only checks for the cross.

If OFF (default), it also enforces “no touch on the cross bar” if that checkbox is true. That’s your “fake-out” filter.

The adaptive distance threshold (the “secret sauce”)

You can choose how “far enough away” is determined—per side:

Fixed %

Short uses Fixed: Min distance ABOVE EMA (%)

Long uses Fixed: Min distance BELOW TEMA (%)

Auto (ATR%) (default)

Short threshold = max(floorEMA, kAtrShort × ATR%)

Long threshold = max(floorTEMA, kAtrLong × ATR%)

This scales distance by recent volatility, with a floor.

Auto (AvgDist%)

Short threshold = max(floorEMA, kAvgShort × average(|Dist to EMA|) over avgLen)

Long threshold = max(floorTEMA, kAvgLong × average(|Dist to TEMA|) over avgLen)

This adapts to the instrument’s typical stretch away from the rails.

These become minDistEMA_eff and minDistTEMA_eff and are re-computed each bar.

Fake-out / bounce logic (the “don’t get tricked” part)

A touch means the bar’s high/low overlapped the MA ± a small buffer % (touchBufPct).

A bounce is a touch plus a close on the “wrong” side (e.g., touch EMA and close above it on shorts = bullish bounce).

The script blocks entries if a bounce happened within bounceLookback bars (excluding the current signal bar).

Exits & risk

Take profit: when price touches the target MA:

Short TP = touch EMA(9)

Long TP = touch chosen TEMA

Stop loss: either

ATR stop: entry ± (atrMultStop × ATR) (default ON), or

Percent stop: entry × (1±stopPct%)

Time stop: if timeExitBars > 0, close after that many bars if still open.

Quality-of-life features

Backtest window (btFrom, btTo) so you can limit evaluation.

Labels on signal bars that show:

MACD bucket (Small/Moderate/HUGE/Violent — based on % separation on the bar),

the current absolute distance to the target MA,

and the effective minimum the engine used (plus which engine mode).

Data Window fields so you can audit:

abs distance to EMA/TEMA,

the effective min distance used on each side,

ATR%,

average absolute distances (for the AvgDist mode).

Alerts fire when a short/long signal is confirmed.

Optional debug panel to see the exact booleans & thresholds the bar had.

Quick mental model

Are we properly stretched away from the rail (by an adaptive threshold) and held on that side for a few bars?

Did MACD flip the way we want without price already tagging the rail that bar?

Have we avoided recent bounces off that rail (no fake-out)?

→ If yes, enter and aim for a tag back to the rail, with ATR/% stop and optional time stop.

If you want, I can add a simple on-chart “rating” (0–100) similar to your Python scorer (distance beyond min, MACD bucket, extension streak) so you can visually rank signals in TradingView too.

TrinityBar**TrinityBar Strategy Description**

The TrinityBar strategy is a price‐action based trading model that leverages Bill Williams’ bar thirds concept to generate entry signals and execute market orders automatically. Here’s how it works:

1. **Bar Thirds Calculation:**

The strategy calculates the range of both the current fully formed bar and the previous fully formed bar. It then divides each bar’s range into three equal parts (thirds).

- For the current bar, the lower third and upper third levels are computed.

- The same is done for the previous bar.

2. **Bar Type Classification:**

Each bar is classified into one of several types based on where its open and close fall relative to its thirds:

- **Bullish Patterns:**

- *1‑3 Bar:* Opens in the lower third and closes in the upper third.

- *2‑3 Bar:* Opens in the middle third and closes in the upper third.

- *3‑3 Bar:* Both open and close are in the upper third.

- **Bearish Patterns:**

- *3‑1 Bar:* Opens in the upper third and closes in the lower third.

- *2‑1 Bar:* Opens in the middle third and closes in the lower third.

- *1‑1 Bar:* Both open and close are in the lower third.

3. **Signal Generation:**

- **Bullish Signal:** A valid buy is generated when the previous bar exhibits any bullish pattern (1‑3, 2‑3, or 3‑3) and the current bar is either a 1‑3 or a 3‑3 bar.

- **Bearish Signal:** A valid sell is generated when the previous bar shows any bearish pattern (1‑1, 2‑1, or 3‑1) and the current bar is either a 1‑1 or a 3‑1 bar.

4. **Visual Alerts:**

When a valid signal is identified, the strategy plots a small triangle below the bar for a buy signal (labeled “B” in green) and a triangle above the bar for a sell signal (labeled “S” in red).

5. **Trade Execution:**

Once a signal is confirmed:

- If a bullish signal is generated, any short positions are closed, and if there is no existing long position, a market long order is entered.

- Conversely, if a bearish signal occurs, any long positions are closed, and a market short order is entered if not already in a short position.

This strategy is designed to capture significant price expansions by relying solely on price action and bar structure, without relying on lagging indicators. It provides a mechanical, systematic approach that removes emotional bias from trading decisions.

EXODUS EXODUS by (DAFE) Trading Systems

EXODUS is a sophisticated trading algorithm built by Dskyz (DAFE) Trading Systems for competitive and competition purposes, designed to identify high-probability trades with robust risk management. this strategy leverages a multi-signal voting system, combining three core components—SPR, VWMO, and VEI—alongside ADX, choppiness filters, and ATR-based volatility gates to ensure trades are taken only in favorable market conditions. the algo uses a take-profit to stop-loss ratio, dynamic position sizing, and a strict voting mechanism requiring all signals to align before entering a trade.

EXODUS was not overfitted for any specific symbol. instead, it uses a generic tuned setting, making it versatile across various markets. while it can trade futures, it’s not currently set up for it but has the potential to do more with further development. visuals are intentionally minimal due to its competition focus, prioritizing performance over aesthetics. a more visually stunning version may be released in the future with enhanced graphics.

The Unique Core Components Developed for EXODUS

SPR (Session Price Recalibration)

SPR measures momentum during regular trading hours (RTH, 0930-1600, America/New_York) to catch session-specific trends.

spr_lookback = input.int(15, "SPR Lookback") this sets how many bars back SPR looks to calculate momentum (default 15 bars). it compares the current session’s price-volume score to the score 15 bars ago to gauge momentum strength.

how it works: a longer lookback smooths out the signal, focusing on bigger trends. a shorter one makes SPR more sensitive to recent moves.

how to adjust: on a 1-hour chart, 15 bars is 15 hours (about 2 trading days). if you’re on a shorter timeframe like 5 minutes, 15 bars is just 75 minutes, so you might want to increase it to 50 or 100 to capture more meaningful trends. if you’re trading a choppy stock, a shorter lookback (like 5) can help catch quick moves, but it might give more false signals.

spr_threshold = input.float (0.7, "SPR Threshold")

this is the cutoff for SPR to vote for a trade (default 0.7). if SPR’s normalized value is above 0.7, it votes for a long; below -0.7, it votes for a short.

how it works: SPR normalizes its momentum score by ATR, so this threshold ensures only strong moves count. a higher threshold means fewer trades but higher conviction.

how to adjust: if you’re getting too few trades, lower it to 0.5 to let more signals through. if you’re seeing too many false entries, raise it to 1.0 for stricter filtering. test on your chart to find a balance.

spr_atr_length = input.int(21, "SPR ATR Length") this sets the ATR period (default 21 bars) used to normalize SPR’s momentum score. ATR measures volatility, so this makes SPR’s signal relative to market conditions.

how it works: a longer ATR period (like 21) smooths out volatility, making SPR less jumpy. a shorter one makes it more reactive.

how to adjust: if you’re trading a volatile stock like TSLA, a longer period (30 or 50) can help avoid noise. for a calmer stock, try 10 to make SPR more responsive. match this to your timeframe—shorter timeframes might need a shorter ATR.

rth_session = input.session("0930-1600","SPR: RTH Sess.") rth_timezone = "America/New_York" this defines the session SPR uses (0930-1600, New York time). SPR only calculates momentum during these hours to focus on RTH activity.

how it works: it ignores pre-market or after-hours noise, ensuring SPR captures the main market action.

how to adjust: if you trade a different session (like London hours, 0300-1200 EST), change the session to match. you can also adjust the timezone if you’re in a different region, like "Europe/London". just make sure your chart’s timezone aligns with this setting.

VWMO (Volume-Weighted Momentum Oscillator)

VWMO measures momentum weighted by volume to spot sustained, high-conviction moves.

vwmo_momlen = input.int(21, "VWMO Momentum Length") this sets how many bars back VWMO looks to calculate price momentum (default 21 bars). it takes the price change (close minus close 21 bars ago).

how it works: a longer period captures bigger trends, while a shorter one reacts to recent swings.

how to adjust: on a daily chart, 21 bars is about a month—good for trend trading. on a 5-minute chart, it’s just 105 minutes, so you might bump it to 50 or 100 for more meaningful moves. if you want faster signals, drop it to 10, but expect more noise.

vwmo_volback = input.int(30, "VWMO Volume Lookback") this sets the period for calculating average volume (default 30 bars). VWMO weights momentum by volume divided by this average.

how it works: it compares current volume to the average to see if a move has strong participation. a longer lookback smooths the average, while a shorter one makes it more sensitive.

how to adjust: for stocks with spiky volume (like NVDA on earnings), a longer lookback (50 or 100) avoids overreacting to one-off spikes. for steady volume stocks, try 20. match this to your timeframe—shorter timeframes might need a shorter lookback.

vwmo_smooth = input.int(9, "VWMO Smoothing")

this sets the SMA period to smooth VWMO’s raw momentum (default 9 bars).

how it works: smoothing reduces noise in the signal, making VWMO more reliable for voting. a longer smoothing period cuts more noise but adds lag.

how to adjust: if VWMO is too jumpy (lots of false votes), increase to 15. if it’s too slow and missing trades, drop to 5. test on your chart to see what keeps the signal clean but responsive.

vwmo_threshold = input.float(10, "VWMO Threshold") this is the cutoff for VWMO to vote for a trade (default 10). above 10, it votes for a long; below -10, a short.

how it works: it ensures only strong momentum signals count. a higher threshold means fewer but stronger trades.

how to adjust: if you want more trades, lower it to 5. if you’re getting too many weak signals, raise it to 15. this depends on your market—volatile stocks might need a higher threshold to filter noise.

VEI (Velocity Efficiency Index)

VEI measures market efficiency and velocity to filter out choppy moves and focus on strong trends.

vei_eflen = input.int(14, "VEI Efficiency Smoothing") this sets the EMA period for smoothing VEI’s efficiency calc (bar range / volume, default 14 bars).

how it works: efficiency is how much price moves per unit of volume. smoothing it with an EMA reduces noise, focusing on consistent efficiency. a longer period smooths more but adds lag.

how to adjust: for choppy markets, increase to 20 to filter out noise. for faster markets, drop to 10 for quicker signals. this should match your timeframe—shorter timeframes might need a shorter period.

vei_momlen = input.int(8, "VEI Momentum Length") this sets how many bars back VEI looks to calculate momentum in efficiency (default 8 bars).

how it works: it measures the change in smoothed efficiency over 8 bars, then adjusts for inertia (volume-to-range). a longer period captures bigger shifts, while a shorter one reacts faster.

how to adjust: if VEI is missing quick reversals, drop to 5. if it’s too noisy, raise to 12. test on your chart to see what catches the right moves without too many false signals.

vei_threshold = input.float(4.5, "VEI Threshold") this is the cutoff for VEI to vote for a trade (default 4.5). above 4.5, it votes for a long; below -4.5, a short.

how it works: it ensures only strong, efficient moves count. a higher threshold means fewer trades but higher quality.

how to adjust: if you’re not getting enough trades, lower to 3. if you’re seeing too many false entries, raise to 6. this depends on your market—fast stocks like NQ1 might need a lower threshold.

Features

Multi-Signal Voting: requires all three signals (SPR, VWMO, VEI) to align for a trade, ensuring high-probability setups.

Risk Management: uses ATR-based stops (2.1x) and take-profits (4.1x), with dynamic position sizing based on a risk percentage (default 0.4%).

Market Filters: ADX (default 27) ensures trending conditions, choppiness index (default 54.5) avoids sideways markets, and ATR expansion (default 1.12) confirms volatility.

Dashboard: provides real-time stats like SPR, VWMO, VEI values, net P/L, win rate, and streak, with a clean, functional design.

Visuals

EXODUS prioritizes performance over visuals, as it was built for competitive and competition purposes. entry/exit signals are marked with simple labels and shapes, and a basic heatmap highlights market regimes. a more visually stunning update may be released later, with enhanced graphics and overlays.

Usage

EXODUS is designed for stocks and ETFs but can be adapted for futures with adjustments. it performs best in trending markets with sufficient volatility, as confirmed by its generic tuning across symbols like TSLA, AMD, NVDA, and NQ1. adjust inputs like SPR threshold, VWMO smoothing, or VEI momentum length to suit specific assets or timeframes.

Setting I used: (Again, these are a generic setting, each security needs to be fine tuned)

SPR LB = 19 SPR TH = 0.5 SPR ATR L= 21 SPR RTH Sess: 9:30 – 16:00

VWMO L = 21 VWMO LB = 18 VWMO S = 6 VWMO T = 8

VEI ES = 14 VEI ML = 21 VEI T = 4

R % = 0.4

ATR L = 21 ATR M (S) =1.1 TP Multi = 2.1 ATR min mult = 0.8 ATR Expansion = 1.02

ADX L = 21 Min ADX = 25

Choppiness Index = 14 Chop. Max T = 55.5

Backtesting: TSLA

Frame: Jan 02, 2018, 08:00 — May 01, 2025, 09:00

Slippage: 3

Commission .01

Disclaimer

this strategy is for educational purposes. past performance is not indicative of future results. trading involves significant risk, and you should only trade with capital you can afford to lose. always backtest and validate any strategy before using it in live markets.

(This publishing will most likely be taken down do to some miscellaneous rule about properly displaying charting symbols, or whatever. Once I've identified what part of the publishing they want to pick on, I'll adjust and repost.)

About the Author

Dskyz (DAFE) Trading Systems is dedicated to building high-performance trading algorithms. EXODUS is a product of rigorous research and development, aimed at delivering consistent, and data-driven trading solutions.

Use it with discipline. Use it with clarity. Trade smarter.

**I will continue to release incredible strategies and indicators until I turn this into a brand or until someone offers me a contract.

2025 Created by Dskyz, powered by DAFE Trading Systems. Trade smart, trade bold.

Reversal Point Dynamics - Machine Learning⇋ Reversal Point Dynamics - Machine Learning

RPD Machine Learning: Self-Adaptive Multi-Armed Bandit Trading System

RPD Machine Learning is an advanced algorithmic trading system that implements genuine machine learning through contextual multi-armed bandits, reinforcement learning, and online adaptation. Unlike traditional indicators that use fixed rules, RPD learns from every trade outcome , automatically discovers which strategies work in current market conditions, and continuously adapts without manual intervention .

Core Innovation: The system deploys six distinct trading policies (ranging from aggressive trend-following to conservative range-bound strategies) and uses LinUCB contextual bandit algorithms with Random Fourier Features to learn which policy performs best in each market regime. After the initial learning phase (50-100 trades), the system achieves autonomous adaptation , automatically shifting between policies as market conditions evolve.

Target Users: Quantitative traders, algorithmic trading developers, systematic traders, and data-driven investors who want a system that adapts over time . Suitable for stocks, futures, forex, and cryptocurrency on any liquid instrument with >100k daily volume.

The Problem This System Solves

Traditional Technical Analysis Limitations

Most trading systems suffer from three fundamental challenges :

Fixed Parameters: Static settings (like "buy when RSI < 30") work well in backtests but may struggle when markets change character. What worked in low-volatility environments may not work in high-volatility regimes.

Strategy Degradation: Manual optimization (curve-fitting) produces systems that perform well on historical data but may underperform in live trading. The system never adapts to new market conditions.

Cognitive Overload: Running multiple strategies simultaneously forces traders to manually decide which one to trust. This leads to hesitation, late entries, and inconsistent execution.

How RPD Machine Learning Addresses These Challenges

Automated Strategy Selection: Instead of requiring you to choose between trend-following and mean-reversion strategies, RPD runs all six policies simultaneously and uses machine learning to automatically select the best one for current conditions. The decision happens algorithmically, removing human hesitation.

Continuous Learning: After every trade, the system updates its understanding of which policies are working. If the market shifts from trending to ranging, RPD automatically detects this through changing performance patterns and adjusts selection accordingly.

Context-Aware Decisions: Unlike simple voting systems that treat all conditions equally, RPD analyzes market context (ADX regime, entropy levels, volatility state, volume patterns, time of day, historical performance) and learns which combinations of context features correlate with policy success.

Machine Learning Architecture: What Makes This "Real" ML

Component 1: Contextual Multi-Armed Bandits (LinUCB)

What Is a Multi-Armed Bandit Problem?

Imagine facing six slot machines, each with unknown payout rates. The exploration-exploitation dilemma asks: Should you keep pulling the machine that's worked well (exploitation) or try others that might be better (exploration)? RPD solves this for trading policies.

Academic Foundation:

RPD implements Linear Upper Confidence Bound (LinUCB) from the research paper "A Contextual-Bandit Approach to Personalized News Article Recommendation" (Li et al., 2010, WWW Conference). This algorithm is used in content recommendation and ad placement systems.

How It Works:

Each policy (AggressiveTrend, ConservativeRange, VolatilityBreakout, etc.) is treated as an "arm." The system maintains:

Reward History: Tracks wins/losses for each policy

Contextual Features: Current market state (8-10 features including ADX, entropy, volatility, volume)

Uncertainty Estimates: Confidence in each policy's performance

UCB Formula: predicted_reward + α × uncertainty

The system selects the policy with highest UCB score , balancing proven performance (predicted_reward) with potential for discovery (uncertainty bonus). Initially, all policies have high uncertainty, so the system explores broadly. After 50-100 trades, uncertainty decreases, and the system focuses on known-performing policies.

Why This Matters:

Traditional systems pick strategies based on historical backtests or user preference. RPD learns from actual outcomes in your specific market, on your timeframe, with your execution characteristics.

Component 2: Random Fourier Features (RFF)

The Non-Linearity Challenge:

Market relationships are often non-linear. High ADX may indicate favorable conditions when volatility is normal, but unfavorable when volatility spikes. Simple linear models struggle to capture these interactions.

Academic Foundation:

RPD implements Random Fourier Features from "Random Features for Large-Scale Kernel Machines" (Rahimi & Recht, 2007, NIPS). This technique approximates kernel methods (like Support Vector Machines) while maintaining computational efficiency for real-time trading.

How It Works:

The system transforms base features (ADX, entropy, volatility, etc.) into a higher-dimensional space using random projections and cosine transformations:

Input: 8 base features

Projection: Through random Gaussian weights

Transformation: cos(W×features + b)

Output: 16 RFF dimensions

This allows the bandit to learn non-linear relationships between market context and policy success. For example: "AggressiveTrend performs well when ADX >25 AND entropy <0.6 AND hour >9" becomes naturally encoded in the RFF space.

Why This Matters:

Without RFF, the system could only learn "this policy has X% historical performance." With RFF, it learns "this policy performs differently in these specific contexts" - enabling more nuanced selection.

Component 3: Reinforcement Learning Stack

Beyond bandits, RPD implements a complete RL framework :

Q-Learning: Value-based RL that learns state-action values. Maps 54 discrete market states (trend×volatility×RSI×volume combinations) to 5 actions (4 policies + no-trade). Updates via Bellman equation after each trade. Converges toward optimal policy after 100-200 trades.

TD(λ) with Eligibility Traces: Extension of Q-Learning that propagates credit backwards through time . When a trade produces an outcome, TD(λ) updates not just the final state-action but all states visited during the trade, weighted by eligibility decay (λ=0.90). This accelerates learning from multi-bar trades.

Policy Gradient (REINFORCE): Learns a stochastic policy directly from 12 continuous market features without discretization. Uses gradient ascent to increase probability of actions that led to positive outcomes. Includes baseline (average reward) for variance reduction.

Meta-Learning: The system learns how to learn by adapting its own learning rates based on feature stability and correlation with outcomes. If a feature (like volume ratio) consistently correlates with success, its learning rate increases. If unstable, rate decreases.

Why This Matters:

Q-Learning provides fast discrete decisions. Policy Gradient handles continuous features. TD(λ) accelerates learning. Meta-learning optimizes the optimization. Together, they create a robust, multi-approach learning system that adapts more quickly than any single algorithm.

Component 4: Policy Momentum Tracking (v2 Feature)

The Recency Challenge:

Standard bandits treat all historical data equally. If a policy performed well historically but struggles in current conditions due to regime shift, the system may be slow to adapt because historical success outweighs recent underperformance.

RPD's Solution:

Each policy maintains a ring buffer of the last 10 outcomes. The system calculates:

Momentum: recent_win_rate - global_win_rate (range: -1 to +1)

Confidence: consistency of recent results (1 - variance)

Policies with positive momentum (recent outperformance) get an exploration bonus. Policies with negative momentum and high confidence (consistent recent underperformance) receive a selection penalty.

Effect: When markets shift, the system detects the shift more quickly through momentum tracking, enabling faster adaptation than standard bandits.

Signal Generation: The Core Algorithm

Multi-Timeframe Fractal Detection

RPD identifies reversal points using three complementary methods :

1. Quantum State Analysis:

Divides price range into discrete states (default: 6 levels)

Peak signals require price in top states (≥ state 5)

Valley signals require price in bottom states (≤ state 1)

Prevents mid-range signals that may struggle in strong trends

2. Fractal Geometry:

Identifies swing highs/lows using configurable fractal strength

Confirms local extremum with neighboring bars

Validates reversal only if price crosses prior extreme

3. Multi-Timeframe Confirmation:

Analyzes higher timeframe (4× default) for alignment

MTF confirmation adds probability bonus

Designed to reduce false signals while preserving valid setups

Probability Scoring System

Each signal receives a dynamic probability score (40-99%) based on:

Base Components:

Trend Strength: EMA(velocity) / ATR × 30 points

Entropy Quality: (1 - entropy) × 10 points

Starting baseline: 40 points

Enhancement Bonuses:

Divergence Detection: +20 points (price/momentum divergence)

RSI Extremes: +8 points (RSI >65 for peaks, <40 for valleys)

Volume Confirmation: +5 points (volume >1.2× average)

Adaptive Momentum: +10 points (strong directional velocity)

MTF Alignment: +12 points (higher timeframe confirms)

Range Factor: (high-low)/ATR × 3 - 1.5 points (volatility adjustment)

Regime Bonus: +8 points (trending ADX >25 with directional agreement)

Penalties:

High Entropy: -5 points (entropy >0.85, chaotic price action)

Consolidation Regime: -10 points (ADX <20, no directional conviction)

Final Score: Clamped to 40-99% range, classified as ELITE (>85%), STRONG (75-85%), GOOD (65-75%), or FAIR (<65%)

Entropy-Based Quality Filter

What Is Entropy?

Entropy measures randomness in price changes . Low entropy indicates orderly, directional moves. High entropy indicates chaotic, unpredictable conditions.

Calculation:

Count up/down price changes over adaptive period

Calculate probability: p = ups / total_changes

Shannon entropy: -p×log(p) - (1-p)×log(1-p)

Normalized to 0-1 range

Application:

Entropy <0.5: Highly ordered (ELITE signals possible)

Entropy 0.5-0.75: Mixed (GOOD signals)

Entropy >0.85: Chaotic (signals blocked or heavily penalized)

Why This Matters:

Prevents trading during choppy, news-driven conditions where technical patterns may be less reliable. Automatically raises quality bar when market is unpredictable.

Regime Detection & Market Microstructure - ADX-Based Regime Classification

RPD uses Wilder's Average Directional Index to classify markets:

Bull Trend: ADX >25, +DI > -DI (directional conviction bullish)

Bear Trend: ADX >25, +DI < -DI (directional conviction bearish)

Consolidation: ADX <20 (no directional conviction)

Transitional: ADX 20-25 (forming direction, ambiguous)

Filter Logic:

Blocks all signals during Transitional regime (avoids trading during uncertain conditions)

Blocks Consolidation signals unless ADX ≥ Min Trend Strength

Adds probability bonus during strong trends (ADX >30)

Effect: Designed to reduce signal frequency while focusing on higher-quality setups.

Divergence Detection

Bearish Divergence:

Price makes higher high

Velocity (price momentum) makes lower high

Indicates weakening upward pressure → SHORT signal quality boost

Bullish Divergence:

Price makes lower low

Velocity makes higher low

Indicates weakening downward pressure → LONG signal quality boost

Bonus: Adds probability points and additional acceleration factor. Divergence signals have historically shown higher success rates in testing.

Hierarchical Policy System - The Six Trading Policies

1. AggressiveTrend (Policy 0):

Probability Threshold: 60% (trades more frequently)

Entropy Threshold: 0.70 (tolerates moderate chaos)

Stop Multiplier: 2.5× ATR (wider stops for trends)

Target Multiplier: 5.0R (larger targets)

Entry Mode: Pyramid (scales into winners)

Best For: Strong trending markets, breakouts, momentum continuation

2. ConservativeRange (Policy 1):

Probability Threshold: 75% (more selective)

Entropy Threshold: 0.60 (requires order)

Stop Multiplier: 1.8× ATR (tighter stops)

Target Multiplier: 3.0R (modest targets)

Entry Mode: Single (one-shot entries)

Best For: Range-bound markets, low volatility, mean reversion

3. VolatilityBreakout (Policy 2):

Probability Threshold: 65% (moderate)

Entropy Threshold: 0.80 (accepts high entropy)

Stop Multiplier: 3.0× ATR (wider stops)

Target Multiplier: 6.0R (larger targets)

Entry Mode: Tiered (splits entry)

Best For: Compression breakouts, post-consolidation moves, gap opens

4. EntropyScalp (Policy 3):

Probability Threshold: 80% (very selective)

Entropy Threshold: 0.40 (requires extreme order)

Stop Multiplier: 1.5× ATR (tightest stops)

Target Multiplier: 2.5R (quick targets)

Entry Mode: Single

Best For: Low-volatility grinding moves, tight ranges, highly predictable patterns

5. DivergenceHunter (Policy 4):

Probability Threshold: 70% (quality-focused)

Entropy Threshold: 0.65 (balanced)

Stop Multiplier: 2.2× ATR (moderate stops)

Target Multiplier: 4.5R (balanced targets)

Entry Mode: Tiered

Best For: Divergence-confirmed reversals, exhaustion moves, trend climax

6. AdaptiveBlend (Policy 5):

Probability Threshold: 68% (balanced)

Entropy Threshold: 0.75 (balanced)

Stop Multiplier: 2.0× ATR (standard)

Target Multiplier: 4.0R (standard)

Entry Mode: Single

Best For: Mixed conditions, general trading, fallback when no clear regime

Policy Clustering (Advanced/Extreme Modes)

Policies are grouped into three clusters based on regime affinity:

Cluster 1 (Trending): AggressiveTrend, DivergenceHunter

High regime affinity (0.8): Performs well when ADX >25

Moderate vol affinity (0.6): Works in various volatility

Cluster 2 (Ranging): ConservativeRange, AdaptiveBlend

Low regime affinity (0.3): Better suited for ADX <20

Low vol affinity (0.4): Optimized for calm markets

Cluster 3 (Breakout): VolatilityBreakout

Moderate regime affinity (0.6): Works in multiple regimes

High vol affinity (0.9): Requires high volatility for optimal characteristics

Hierarchical Selection Process:

Calculate cluster scores based on current regime and volatility

Select best-matching cluster

Run UCB selection within chosen cluster

Apply momentum boost/penalty

This two-stage process reduces learning time - instead of choosing among 6 policies from scratch, system first narrows to 1-2 policies per cluster, then optimizes within cluster.

Risk Management & Position Sizing

Dynamic Kelly Criterion Sizing (Optional)

Traditional Fixed Sizing Challenge:

Using the same position size for all signal probabilities may be suboptimal. Higher-probability signals could justify larger positions, lower-probability signals smaller positions.

Kelly Formula:

f = (p × b - q) / b

Where:

p = win probability (from signal score)

q = loss probability (1 - p)

b = win/loss ratio (average_win / average_loss)

f = fraction of capital to risk

RPD Implementation:

Uses Fractional Kelly (1/4 Kelly default) for safety. Full Kelly is theoretically optimal but can recommend large position sizes. Fractional Kelly reduces volatility while maintaining adaptive sizing benefits.

Enhancements:

Probability Bonus: Normalize(prob, 65, 95) × 0.5 multiplier

Divergence Bonus: Additional sizing on divergence signals

Regime Bonus: Additional sizing during strong trends (ADX >30)

Momentum Adjustment: Hot policies receive sizing boost, cold policies receive reduction

Safety Rails:

Minimum: 1 contract (floor)

Maximum: User-defined cap (default 10 contracts)

Portfolio Heat: Max total risk across all positions (default 4% equity)

Multi-Mode Stop Loss System

ATR Mode (Default):

Stop = entry ± (ATR × base_mult × policy_mult)

Consistent risk sizing

Ignores market structure

Best for: Futures, forex, algorithmic trading

Structural Mode:

Finds swing low (long) or high (short) over last 20 bars

Identifies fractal pivots within lookback

Places stop below/above structure + buffer (0.1× ATR)

Best for: Stocks, instruments that respect structure

Hybrid Mode (Intelligent):

Attempts structural stop first

Falls back to ATR if:

Structural level is invalid (beyond entry)

Structural stop >2× ATR away (too wide)

Best for: Mixed instruments, adaptability

Dynamic Adjustments:

Breakeven: Move stop to entry + 1 tick after 1.0R profit

Trailing: Trail stop 0.8R behind price after 1.5R profit

Timeout: Force close after 30 bars (optional)

Tiered Entry System

Challenge: Equal sizing on all signals may not optimize capital allocation relative to signal quality.

Solution:

Tier 1 (40% of size): Enters immediately on all signals

Tier 2 (60% of size): Enters only if probability ≥ Tier 2 trigger (default 75%)

Example:

Calculated optimal size: 10 contracts

Signal probability: 72%

Tier 2 trigger: 75%

Result: Enter 4 contracts only (Tier 1)

Same signal at 80% probability

Result: Enter 10 contracts (4 Tier 1 + 6 Tier 2)

Effect: Automatically scales size to signal quality, optimizing capital allocation.

Performance Optimization & Learning Curve

Warmup Phase (First 50 Trades)

Purpose: Ensure all policies get tested before system focuses on preferred strategies.

Modifications During Warmup:

Probability thresholds reduced 20% (65% becomes 52%)

Entropy thresholds increased 20% (more permissive)

Exploration rate stays high (30%)

Confidence width (α) doubled (more exploration)

Why This Matters:

Without warmup, system might commit to early-performing policy without testing alternatives. Warmup forces thorough exploration before focusing on best-performing strategies.

Curriculum Learning

Phase 1 (Trades 1-50): Exploration

Warmup active

All policies tested

High exploration (30%)

Learning fundamental patterns

Phase 2 (Trades 50-100): Refinement

Warmup ended, thresholds normalize

Exploration decaying (30% → 15%)

Policy preferences emerging

Meta-learning optimizing

Phase 3 (Trades 100-200): Specialization

Exploration low (15% → 8%)

Clear policy preferences established

Momentum tracking fully active

System focusing on learned patterns

Phase 4 (Trades 200+): Maturity

Exploration minimal (8% → 5%)

Regime-policy relationships learned

Auto-adaptation to market shifts

Stable performance expected

Convergence Indicators

System is learning well when:

Policy switch rate decreasing over time (initially ~50%, should drop to <20%)

Exploration rate decaying smoothly (30% → 5%)

One or two policies emerge with >50% selection frequency

Performance metrics stabilizing over time

Consistent behavior in similar market conditions

System may need adjustment when:

Policy switch rate >40% after 100 trades (excessive exploration)

Exploration rate not decaying (parameter issue)

All policies showing similar selection (not differentiating)

Performance declining despite relaxed thresholds (underlying signal issue)

Highly erratic behavior after learning phase

Advanced Features

Attention Mechanism (Extreme Mode)

Challenge: Not all features are equally important. Trading hour might matter more than price-volume correlation, but standard approaches treat them equally.

Solution:

Each RFF dimension has an importance weight . After each trade:

Calculate correlation: sign(feature - 0.5) × sign(reward)

Update importance: importance += correlation × 0.01

Clamp to range

Effect: Important features get amplified in RFF transformation, less important features get suppressed. System learns which features correlate with successful outcomes.

Temporal Context (Extreme Mode)

Challenge: Current market state alone may be incomplete. Historical context (was volatility rising or falling?) provides additional information.

Solution:

Includes 3-period historical context with exponential decay (0.85):

Current features (weight 1.0)

1 bar ago (weight 0.85)

2 bars ago (weight 0.72)

Effect: Captures momentum and acceleration of market features. System learns patterns like "rising volatility with falling entropy" that may precede significant moves.

Transfer Learning via Episodic Memory

Short-Term Memory (STM):

Last 20 trades

Fast adaptation to immediate regime

High learning rate

Long-Term Memory (LTM):

Condensed historical patterns

Preserved knowledge from past regimes

Low learning rate

Transfer Mechanism:

When STM fills (20 trades), patterns consolidated into LTM . When similar regime recurs later, LTM provides faster adaptation than starting from scratch.

Practical Implementation Guide - Recommended Settings by Instrument

Futures (ES, NQ, CL):

Adaptive Period: 20-25

ML Mode: Advanced

RFF Dimensions: 16

Policies: 6

Base Risk: 1.5%

Stop Mode: ATR or Hybrid

Timeframe: 5-15 min

Forex Majors (EURUSD, GBPUSD):

Adaptive Period: 25-30

ML Mode: Advanced

RFF Dimensions: 16

Policies: 6

Base Risk: 1.0-1.5%

Stop Mode: ATR

Timeframe: 5-30 min

Cryptocurrency (BTC, ETH):

Adaptive Period: 20-25

ML Mode: Extreme (handles non-stationarity)

RFF Dimensions: 32 (captures complexity)

Policies: 6

Base Risk: 1.0% (volatility consideration)

Stop Mode: Hybrid

Timeframe: 15 min - 4 hr

Stocks (Large Cap):

Adaptive Period: 25-30

ML Mode: Advanced

RFF Dimensions: 16

Policies: 5-6

Base Risk: 1.5-2.0%

Stop Mode: Structural or Hybrid

Timeframe: 15 min - Daily

Scaling Strategy

Phase 1 (Testing - First 50 Trades):

Max Contracts: 1-2

Goal: Validate system on your instrument

Monitor: Performance stabilization, learning progress

Phase 2 (Validation - Trades 50-100):

Max Contracts: 2-3

Goal: Confirm learning convergence

Monitor: Policy stability, exploration decay

Phase 3 (Scaling - Trades 100-200):

Max Contracts: 3-5

Enable: Kelly sizing (1/4 Kelly)

Goal: Optimize capital efficiency

Monitor: Risk-adjusted returns

Phase 4 (Full Deployment - Trades 200+):

Max Contracts: 5-10

Enable: Full momentum tracking

Goal: Sustained consistent performance

Monitor: Ongoing adaptation quality

Limitations & Disclaimers

Statistical Limitations

Learning Sample Size: System requires minimum 50-100 trades for basic convergence, 200+ trades for robust learning. Early performance (first 50 trades) may not reflect mature system behavior.

Non-Stationarity Risk: Markets change over time. A system trained on one market regime may need time to adapt when conditions shift (typically 30-50 trades for adjustment).

Overfitting Possibility: With 16-32 RFF dimensions and 6 policies, system has substantial parameter space. Small sample sizes (<200 trades) increase overfitting risk. Mitigated by regularization (λ) and fractional Kelly sizing.

Technical Limitations

Computational Complexity: Extreme mode with 32 RFF dimensions, 6 policies, and full RL stack requires significant computation. May perform slowly on lower-end systems or with many other indicators loaded.

Pine Script Constraints:

No true matrix inversion (uses diagonal approximation for LinUCB)

No cryptographic RNG (uses market data as entropy)

No proper random number generation for RFF (uses deterministic pseudo-random)

These approximations reduce mathematical precision compared to academic implementations but remain functional for trading applications.

Data Requirements: Needs clean OHLCV data. Missing bars, gaps, or low liquidity (<100k daily volume) can degrade signal quality.

Forward-Looking Bias Disclaimer

Reward Calculation Uses Future Data: The RL system evaluates trades using an 8-bar forward-looking window. This means when a position enters at bar 100, the reward calculation considers price movement through bar 108.

Why This is Disclosed:

Entry signals do NOT look ahead - decisions use only data up to entry bar

Forward data used for learning only, not signal generation

In live trading, system learns identically as bars unfold in real-time

Simulates natural learning process (outcomes are only known after trades complete)

Implication: Backtested metrics reflect this 8-bar evaluation window. Live performance may vary if:

- Positions held longer than 8 bars

- Slippage/commissions differ from backtest settings

- Market microstructure changes (wider spreads, different execution quality)

Risk Warnings

No Guarantee of Profit: All trading involves substantial risk of loss. Machine learning systems can fail if market structure fundamentally changes or during unprecedented events.

Maximum Drawdown: With 1.5% base risk and 4% max total risk, expect potential drawdowns. Historical drawdowns do not predict future drawdowns. Extreme market conditions can exceed expectations.

Black Swan Events: System has not been tested under: flash crashes, trading halts, circuit breakers, major geopolitical shocks, or other extreme events. Such events can exceed stop losses and cause significant losses.

Leverage Risk: Futures and forex involve leverage. Adverse moves combined with leverage can result in losses exceeding initial investment. Use appropriate position sizing for your risk tolerance.

System Failures: Code bugs, broker API failures, internet outages, or exchange issues can prevent proper execution. Always monitor automated systems and maintain appropriate safeguards.

Appropriate Use

This System Is:

✅ A machine learning framework for adaptive strategy selection

✅ A signal generation system with probabilistic scoring

✅ A risk management system with dynamic sizing

✅ A learning system designed to adapt over time

This System Is NOT:

❌ A price prediction system (does not forecast exact prices)

❌ A guarantee of profits (can and will experience losses)

❌ A replacement for due diligence (requires monitoring and understanding)

❌ Suitable for complete beginners (requires understanding of ML concepts, risk management, and trading fundamentals)

Recommended Use:

Paper trade for 100 signals before risking capital

Start with minimal position sizing (1-2 contracts) regardless of calculated size

Monitor learning progress via dashboard

Scale gradually over several months only after consistent results

Combine with fundamental analysis and broader market context

Set account-level risk limits (e.g., maximum drawdown threshold)

Never risk more than you can afford to lose

What Makes This System Different

RPD implements academically-derived machine learning algorithms rather than simple mathematical calculations or optimization:

✅ LinUCB Contextual Bandits - Algorithm from WWW 2010 conference (Li et al.)

✅ Random Fourier Features - Kernel approximation from NIPS 2007 (Rahimi & Recht)

✅ Q-Learning, TD(λ), REINFORCE - Standard RL algorithms from Sutton & Barto textbook

✅ Meta-Learning - Learning rate adaptation based on feature correlation

✅ Online Learning - Real-time updates from streaming data

✅ Hierarchical Policies - Two-stage selection with clustering

✅ Momentum Tracking - Recent performance analysis for faster adaptation

✅ Attention Mechanism - Feature importance weighting

✅ Transfer Learning - Episodic memory consolidation

Key Differentiators:

Actually learns from trade outcomes (not just parameter optimization)

Updates model parameters in real-time (true online learning)

Adapts to changing market regimes (not static rules)

Improves over time through reinforcement learning

Implements published ML algorithms with proper citations

Conclusion

RPD Machine Learning represents a different approach from traditional technical analysis to adaptive, self-learning systems . Instead of manually optimizing parameters (which can overfit to historical data), RPD learns behavior patterns from actual trading outcomes in your specific market.

The combination of contextual bandits, reinforcement learning, random fourier features, hierarchical policy selection, and momentum tracking creates a multi-algorithm learning system designed to handle non-stationary markets better than static approaches.

After the initial learning phase (50-100 trades), the system achieves autonomous adaptation - automatically discovering which strategies work in current conditions and shifting allocation without human intervention. This represents an approach where systems adapt over time rather than remaining static.

Use responsibly. Paper trade extensively. Scale gradually. Understand that past performance does not guarantee future results and all trading involves risk of loss.

Taking you to school. — Dskyz, Trade with insight. Trade with anticipation.

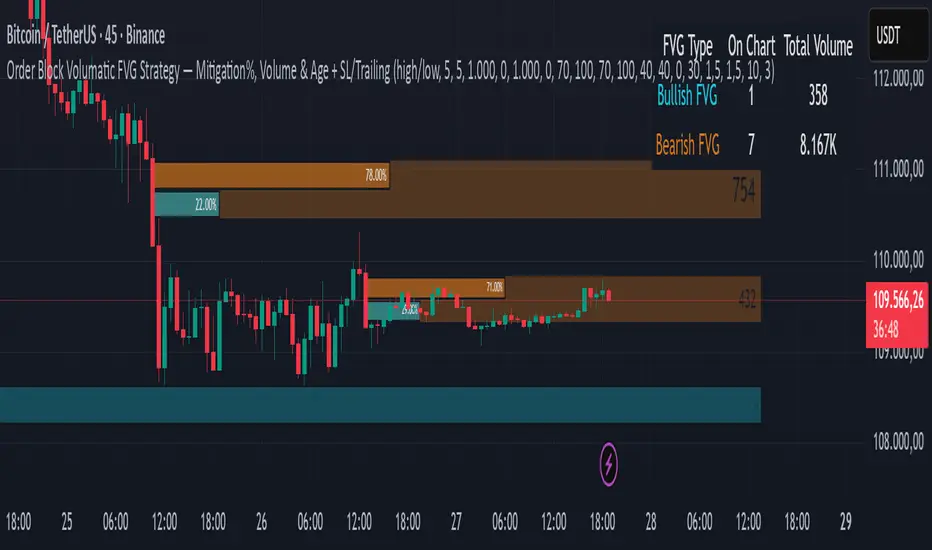

Order Block Volumatic FVG StrategyInspired by: Volumatic Fair Value Gaps —

License: CC BY-NC-SA 4.0 (Creative Commons Attribution–NonCommercial–ShareAlike).

This script is a non-commercial derivative work that credits the original author and keeps the same license.

What this strategy does

This turns BigBeluga’s visual FVG concept into an entry/exit strategy. It scans bullish and bearish FVG boxes, measures how deep price has mitigated into a box (as a percentage), and opens a long/short when your mitigation threshold and filters are satisfied. Risk is managed with a fixed Stop Loss % and a Trailing Stop that activates only after a user-defined profit trigger.

Additions vs. the original indicator

✅ Strategy entries based on % mitigation into FVGs (long/short).

✅ Lower-TF volume split using upticks/downticks; fallback if LTF data is missing (distributes prior bar volume by close’s position in its H–L range) to avoid NaN/0.

✅ Per-FVG total volume filter (min/max) so you can skip weak boxes.

✅ Age filter (min bars since the FVG was created) to avoid fresh/immature boxes.

✅ Bull% / Bear% share filter (the 46%/53% numbers you see inside each FVG).

✅ Optional candle confirmation and cooldown between trades.

✅ Risk management: fixed SL % + Trailing Stop with a profit trigger (doesn’t trail until your trigger is reached).

✅ Pine v6 safety: no unsupported args, no indexof/clamp/when, reverse-index deletes, guards against zero/NaN.

How a trade is decided (logic overview)

Detect FVGs (same rules as the original visual logic).

For each FVG currently intersected by the bar, compute:

Mitigation % (how deep price has entered the box).

Bull%/Bear% split (internal volume share).

Total volume (printed on the box) from LTF aggregation or fallback.

Age (bars) since the box was created.

Apply your filters:

Mitigation ≥ Long/Short threshold.

Volume between your min and max (if enabled).

Age ≥ min bars (if enabled).

Bull% / Bear% within your limits (if enabled).

(Optional) the current candle must be in trade direction (confirm).

If multiple FVGs qualify on the same bar, the strategy uses the most recent one.

Enter long/short (no pyramiding).

Exit with:

Fixed Stop Loss %, and

Trailing Stop that only starts after price reaches your profit trigger %.

Input settings (quick guide)

Mitigation source: close or high/low. Use high/low for intrabar touches; close is stricter.

Mitigation % thresholds: minimal mitigation for Long and Short.

TOTAL Volume filter: skip FVGs with too little/too much total volume (per box).

Bull/Bear share filter: require, e.g., Long only if Bull% ≥ 50; avoid Short when Bull% is high (Short Bull% max).

Age filter (bars): e.g., ≥ 20–30 bars to avoid fresh boxes.

Confirm candle: require candle direction to match the trade.

Cooldown (bars): minimum bars between entries.

Risk:

Stop Loss % (fixed from entry price).

Activate trailing at +% profit (the trigger).

Trailing distance % (the trailing gap once active).

Lower-TF aggregation:

Auto: TF/Divisor → picks 1/3/5m automatically.

Fixed: choose 1/3/5/15m explicitly.

If LTF can’t be fetched, fallback allocates prior bar’s volume by its close position in the bar’s H–L.

Suggested starting presets (you should optimize per market)

Mitigation: 60–80% for both Long/Short.

Bull/Bear share:

Long: Bull% ≥ 50–70, Bear% ≤ 100.

Short: Bull% ≤ 60 (avoid shorting into strong support), Bear% ≥ 0–70 as you prefer.

Age: ≥ 20–30 bars.

Volume: pick a min that filters noise for your symbol/timeframe.

Risk: SL 4–6%, trailing trigger 1–2%, distance 1–2% (crypto example).

Set slippage/fees in Strategy Properties.

Notes, limitations & best practices

Data differences: The LTF split uses request.security_lower_tf. If the exchange/data feed has sparse LTF data, the fallback kicks in (it’s deliberate to avoid NaNs but is a heuristic).

Real-time vs backtest: The current bar can update until close; results on historical bars use closed data. Use “Bar Replay” to understand intrabar effects.

No pyramiding: Only one position at a time. Modify pyramiding in the header if you need scaling.

Assets: For spot/crypto, TradingView “volume” is exchange volume; in some markets it may be tick volume—interpret filters accordingly.

Risk disclosure: Past performance ≠ future results. Use appropriate position sizing and risk controls; this is not financial advice.

Credits

Visual FVG concept and original implementation: BigBeluga.

This derivative strategy adds entry/exit logic, volume/age/share filters, robust LTF handling, and risk management while preserving the original spirit.

License remains CC BY-NC-SA 4.0 (non-commercial, attribution required, share-alike).

Dskyz (DAFE) Aurora Divergence – Quant Master Dskyz (DAFE) Aurora Divergence – Quant Master

Introducing the Dskyz (DAFE) Aurora Divergence – Quant Master , a strategy that’s your secret weapon for mastering futures markets like MNQ, NQ, MES, and ES. Born from the legendary Aurora Divergence indicator, this fully automated system transforms raw divergence signals into a quant-grade trading machine, blending precision, risk management, and cyberpunk DAFE visuals that make your charts glow like a neon skyline. Crafted with care and driven by community passion, this strategy stands out in a sea of generic scripts, offering traders a unique edge to outsmart institutional traps and navigate volatile markets.

The Aurora Divergence indicator was a cult favorite for spotting price-OBV divergences with its aqua and fuchsia orbs, but traders craved a system to act on those signals with discipline and automation. This strategy delivers, layering advanced filters (z-score, ATR, multi-timeframe, session), dynamic risk controls (kill switches, adaptive stops/TPs), and a real-time dashboard to turn insights into profits. Whether you’re a newbie dipping into futures or a pro hunting reversals, this strat’s got your back with a beginner guide, alerts, and visuals that make trading feel like a sci-fi mission. Let’s dive into every detail and see why this original DAFE creation is a must-have.

Why Traders Need This Strategy

Futures markets are a battlefield—fast-paced, volatile, and riddled with institutional games that can wipe out undisciplined traders. From the April 28, 2025 NQ 1k-point drop to sneaky ES slippage, the stakes are high. Meanwhile, platforms are flooded with unoriginal, low-effort scripts that promise the moon but deliver noise. The Aurora Divergence – Quant Master rises above, offering:

Unmatched Originality: A bespoke system built from the ground up, with custom divergence logic, DAFE visuals, and quant filters that set it apart from copycat clutter.

Automation with Precision: Executes trades on divergence signals, eliminating emotional slip-ups and ensuring consistency, even in chaotic sessions.

Quant-Grade Filters: Z-score, ATR, multi-timeframe, and session checks filter out noise, targeting high-probability reversals.

Robust Risk Management: Daily loss and rolling drawdown kill switches, plus ATR-based stops/TPs, protect your capital like a fortress.

Stunning DAFE Visuals: Aqua/fuchsia orbs, aurora bands, and a glowing dashboard make signals intuitive and charts a work of art.

Community-Driven: Evolved from trader feedback, this strat’s a labor of love, not a recycled knockoff.

Traders need this because it’s a complete, original system that blends accessibility, sophistication, and style. It’s your edge to trade smarter, not harder, in a market full of traps and imitators.

1. Divergence Detection (Core Signal Logic)

The strategy’s core is its ability to detect bullish and bearish divergences between price and On-Balance Volume (OBV), pinpointing reversals with surgical accuracy.

How It Works:

Price Slope: Uses linear regression over a lookback (default: 9 bars) to measure price momentum (priceSlope).

OBV Slope: OBV tracks volume flow (+volume if price rises, -volume if falls), with its slope calculated similarly (obvSlope).

Bullish Divergence: Price slope negative (falling), OBV slope positive (rising), and price above 50-bar SMA (trend_ma).

Bearish Divergence: Price slope positive (rising), OBV slope negative (falling), and price below 50-bar SMA.

Smoothing: Requires two consecutive divergence bars (bullDiv2, bearDiv2) to confirm signals, reducing false positives.

Strength: Divergence intensity (divStrength = |priceSlope * obvSlope| * sensitivity) is normalized (0–1, divStrengthNorm) for visuals.

Why It’s Brilliant:

- Divergences catch hidden momentum shifts, often exploited by institutions, giving you an edge on reversals.

- The 50-bar SMA filter aligns signals with the broader trend, avoiding choppy markets.

- Adjustable lookback (min: 3) and sensitivity (default: 1.0) let you tune for different instruments or timeframes.

2. Filters for Precision

Four advanced filters ensure signals are high-probability and market-aligned, cutting through the noise of volatile futures.

Z-Score Filter:

Logic: Calculates z-score ((close - SMA) / stdev) over a lookback (default: 50 bars). Blocks entries if |z-score| > threshold (default: 1.5) unless disabled (useZFilter = false).

Impact: Avoids trades during extreme price moves (e.g., blow-off tops), keeping you in statistically safe zones.

ATR Percentile Volatility Filter:

Logic: Tracks 14-bar ATR in a 100-bar window (default). Requires current ATR > 80th percentile (percATR) to trade (tradeOk).

Impact: Ensures sufficient volatility for meaningful moves, filtering out low-volume chop.

Multi-Timeframe (HTF) Trend Filter:

Logic: Uses a 50-bar SMA on a higher timeframe (default: 60min). Longs require price > HTF MA (bullTrendOK), shorts < HTF MA (bearTrendOK).

Impact: Aligns trades with the bigger trend, reducing counter-trend losses.

US Session Filter:

Logic: Restricts trading to 9:30am–4:00pm ET (default: enabled, useSession = true) using America/New_York timezone.

Impact: Focuses on high-liquidity hours, avoiding overnight spreads and erratic moves.

Evolution:

- These filters create a robust signal pipeline, ensuring trades are timed for optimal conditions.

- Customizable inputs (e.g., zThreshold, atrPercentile) let traders adapt to their style without compromising quality.

3. Risk Management

The strategy’s risk controls are a masterclass in balancing aggression and safety, protecting capital in volatile markets.

Daily Loss Kill Switch:

Logic: Tracks daily loss (dayStartEquity - strategy.equity). Halts trading if loss ≥ $300 (default) and enabled (killSwitch = true, killSwitchActive).

Impact: Caps daily downside, crucial during events like April 27, 2025 ES slippage.

Rolling Drawdown Kill Switch:

Logic: Monitors drawdown (rollingPeak - strategy.equity) over 100 bars (default). Stops trading if > $1000 (rollingKill).

Impact: Prevents prolonged losing streaks, preserving capital for better setups.

Dynamic Stop-Loss and Take-Profit:

Logic: Stops = entry ± ATR * multiplier (default: 1.0x, stopDist). TPs = entry ± ATR * 1.5x (profitDist). Longs: stop below, TP above; shorts: vice versa.

Impact: Adapts to volatility, keeping stops tight but realistic, with TPs targeting 1.5:1 reward/risk.

Max Bars in Trade:

Logic: Closes trades after 8 bars (default) if not already exited.

Impact: Frees capital from stagnant trades, maintaining efficiency.

Kill Switch Buffer Dashboard:

Logic: Shows smallest buffer ($300 - daily loss or $1000 - rolling DD). Displays 0 (red) if kill switch active, else buffer (green).

Impact: Real-time risk visibility, letting traders adjust dynamically.

Why It’s Brilliant:

- Kill switches and ATR-based exits create a safety net, rare in generic scripts.

- Customizable risk inputs (maxDailyLoss, dynamicStopMult) suit different account sizes.

- Buffer metric empowers disciplined trading, a DAFE signature.

4. Trade Entry and Exit Logic

The entry/exit rules are precise, filtered, and adaptive, ensuring trades are deliberate and profitable.

Entry Conditions:

Long Entry: bullDiv2, cooldown passed (canSignal), ATR filter passed (tradeOk), in US session (inSession), no kill switches (not killSwitchActive, not rollingKill), z-score OK (zOk), HTF trend bullish (bullTrendOK), no existing long (lastDirection != 1, position_size <= 0). Closes shorts first.

Short Entry: Same, but for bearDiv2, bearTrendOK, no long (lastDirection != -1, position_size >= 0). Closes longs first.

Adaptive Cooldown: Default 2 bars (cooldownBars). Doubles (up to 10) after a losing trade, resets after wins (dynamicCooldown).

Exit Conditions:

Stop-Loss/Take-Profit: Set per trade (ATR-based). Exits on stop/TP hits.

Other Exits: Closes if maxBarsInTrade reached, ATR filter fails, or kill switch activates.

Position Management: Ensures no conflicting positions, closing opposites before new entries.

Built To Be Reliable and Consistent:

- Multi-filtered entries minimize false signals, a stark contrast to basic scripts.

- Adaptive cooldown prevents overtrading, especially after losses.

- Clean position handling ensures smooth execution, even in fast markets.

5. DAFE Visuals

The visuals are a DAFE hallmark, blending function with clean flair to make signals intuitive and charts stunning.

Aurora Bands:

Display: Bands around price during divergences (bullish: below low, bearish: above high), sized by ATR * bandwidth (default: 0.5).

Colors: Aqua (bullish), fuchsia (bearish), with transparency tied to divStrengthNorm.

Purpose: Highlights divergence zones with a glowing, futuristic vibe.

Divergence Orbs:

Display: Large/small circles (aqua below for bullish, fuchsia above for bearish) when bullDiv2/bearDiv2 and canSignal. Labels show strength (0–1).

Purpose: Pinpoints entries with eye-catching clarity.

Gradient Background:

Display: Green (bullish), red (bearish), or gray (neutral), 90–95% transparent.

Purpose: Sets the market mood without clutter.

Strategy Plots:

- Stop/TP Lines: Red (stops), green (TPs) for active trades.

- HTF MA: Yellow line for trend context.

- Z-Score: Blue step-line (if enabled).

- Kill Switch Warning: Red background flash when active.

What Makes This Next-Level?:

- Visuals make complex signals (divergences, filters) instantly clear, even for beginners.

- DAFE’s unique aesthetic (orbs, bands) sets it apart from generic scripts, reinforcing originality.

- Functional plots (stops, TPs) enhance trade management.

6. Metrics Dashboard

The top-right dashboard (2x8 table) is your command center, delivering real-time insights.

Metrics:

Daily Loss ($): Current loss vs. day’s start, red if > $300.

Rolling DD ($): Drawdown vs. 100-bar peak, red if > $1000.

ATR Threshold: Current percATR, green if ATR exceeds, red if not.

Z-Score: Current value, green if within threshold, red if not.

Signal: “Bullish Div” (aqua), “Bearish Div” (fuchsia), or “None” (gray).

Action: “Consider Buying”/“Consider Selling” (signal color) or “Wait” (gray).

Kill Switch Buffer ($): Smallest buffer to kill switch, green if > 0, red if 0.

Why This Is Important?:

- Consolidates critical data, making decisions effortless.

- Color-coded metrics guide beginners (e.g., green action = go).

- Buffer metric adds transparency, rare in off-the-shelf scripts.

7. Beginner Guide

Beginner Guide: Middle-right table (shown once on chart load), explains aqua orbs (bullish, buy) and fuchsia orbs (bearish, sell).

Key Features:

Futures-Optimized: Tailored for MNQ, NQ, MES, ES with point-value adjustments.

Highly Customizable: Inputs for lookback, sensitivity, filters, and risk settings.

Real-Time Insights: Dashboard and visuals update every bar.

Backtest-Ready: Fixed qty and tick calc for accurate historical testing.

User-Friendly: Guide, visuals, and dashboard make it accessible yet powerful.

Original Design: DAFE’s unique logic and visuals stand out from generic scripts.

How to Use

Add to Chart: Load on a 5min MNQ/ES chart in TradingView.

Configure Inputs: Adjust instrument, filters, or risk (defaults optimized for MNQ).

Monitor Dashboard: Watch signals, actions, and risk metrics (top-right).

Backtest: Run in strategy tester to evaluate performance.

Live Trade: Connect to a broker (e.g., Tradovate) for automation. Watch for slippage (e.g., April 27, 2025 ES issues).

Replay Test: Use bar replay (e.g., April 28, 2025 NQ drop) to test volatility handling.

Disclaimer

Trading futures involves significant risk of loss and is not suitable for all investors. Past performance is not indicative of future results. Backtest results may not reflect live trading due to slippage, fees, or market conditions. Use this strategy at your own risk, and consult a financial advisor before trading. Dskyz (DAFE) Trading Systems is not responsible for any losses incurred.

Backtesting:

Frame: 2023-09-20 - 2025-04-29

Fee Typical Range (per side, per contract)

CME Exchange $1.14 – $1.20

Clearing $0.10 – $0.30

NFA Regulatory $0.02

Firm/Broker Commis. $0.25 – $0.80 (retail prop)

TOTAL $1.60 – $2.30 per side

Round Turn: (enter+exit) = $3.20 – $4.60 per contract

Final Notes

The Dskyz (DAFE) Aurora Divergence – Quant Master isn’t just a strategy—it’s a movement. Crafted with originality and driven by community passion, it rises above the flood of generic scripts to deliver a system that’s as powerful as it is beautiful. With its quant-grade logic, DAFE visuals, and robust risk controls, it empowers traders to tackle futures with confidence and style. Join the DAFE crew, light up your charts, and let’s outsmart the markets together!

(This publishing will most likely be taken down do to some miscellaneous rule about properly displaying charting symbols, or whatever. Once I've identified what part of the publishing they want to pick on, I'll adjust and repost.)

Use it with discipline. Use it with clarity. Trade smarter.

**I will continue to release incredible strategies and indicators until I turn this into a brand or until someone offers me a contract.

Created by Dskyz, powered by DAFE Trading Systems. Trade fast, trade bold.

Scalping with Williams %R, MACD, and SMA (1m)Overview:

This trading strategy is designed for scalping in the 1-minute timeframe. It uses a combination of the Williams %R, MACD, and SMA indicators to generate buy and sell signals. It also includes alert functionalities to notify users when trades are executed or closed.

Indicators Used:

Williams %R : A momentum indicator that measures overbought and oversold conditions. The Williams %R values range from -100 to 0.

Length: 140 bars (i.e., 140-period).

MACD (Moving Average Convergence Divergence) : A trend-following momentum indicator that shows the relationship between two moving averages of a security's price.

Fast Length: 24 bars

Slow Length: 52 bars

MACD Length: 9 bars (signal line)

SMA (Simple Moving Average) : A trend-following indicator that smooths out price data to create a trend-following indicator.

Length: 7 bars

Conditions and Logic:

Timeframe Check :

The strategy is designed specifically for the 1-minute timeframe. If the current chart is not on the 1-minute timeframe, a warning label is displayed on the chart instructing the user to switch to the 1-minute timeframe.

Williams %R Conditions :