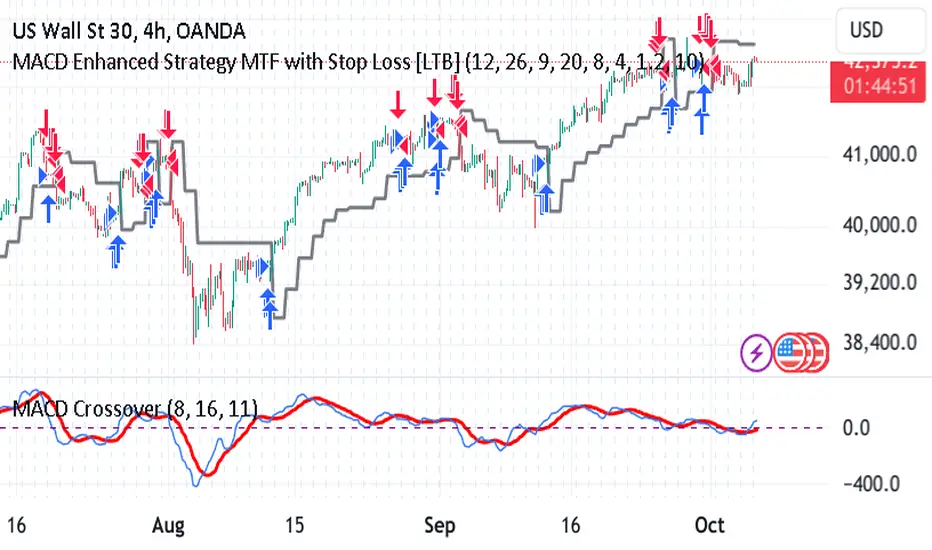

Trailing Take Profit - Close Based📝 Description

This script demonstrates a new approach to the trailing take profit.

Trailing Take Profit is a price-following technique. When used, instead of setting a limit order for the take profit target exiting from your position at the specified price, a stop order is conditionally set when the take profit target is reached. Then, the stop price (a.k.a trailing price), is placed below the take profit target at a distance defined by the user percentagewise. On regular time intervals, the stop price gets updated by following the "Trail Barrier" price (high by default) upwards. When the current price hits the stop price you exit the trade. Check the chart for more details.

This script demonstrates how to implement the close-based Trailing Take Profit logic for long positions, but it can also be applied for short positions if the logic is "reversed".

📢 NOTE

To generate some entries and showcase the "Trailing Take Profit" technique, this script uses the crossing of two moving averages. Please keep in mind that you should not relate the Backtesting results you see in the "Strategy Tester" tab with the success of the technique itself.

This is not a complete strategy per se, and the backtest results are affected by many parameters that are outside of the scope of this publication. If you choose to use this new approach of the "Trailing Take Profit" in your logic you have to make sure that you are backtesting the whole strategy.

⚔️ Comparison

In contrast to my older "Trailing Take Profit" publication where the trailing take profit implementation was tick-based, this new approach is close-based, meaning that the update of the stop price occurs at the bar close instead of every tick.

While comparing the real-time results of the two implementations is like comparing apples to oranges, because they have different dynamic behavior, the new approach offers better consistency between the backtesting results and the real-time results.

By updating the stop price on every bar close, you do not rely on the backtester assumptions anymore (check the Reasoning section below for more info).

The new approach resembles the conditional "Trailing Exit" technique, where the condition is true when the current price crosses over the take profit target. Then, the stop order is placed at the trailing price and it gets updated on every bar close to "follow" the barrier price (high). On the other hand, the older tick-based approach had more "tight" dynamics since the trailing price gets updated on every tick leaving less room for price fluctuations by making it more probable to reach the trailing price.

🤔 Reasoning

This new close-based approach addresses several practical issues the older tick-based approach had. Those issues arise mainly from the technicalities of the TV Backtester. More specifically, due to the assumptions the Broker Emulator makes for the price action of the history bars, the backtesting results in the TV Backtester are exaggerated, and depending on the timeframe, the backtesting results look way better than they are in reality.

The effect above, and the inability to reason about the performance of a strategy separated people into two groups. Those who never use this feature, because they couldn't know for sure the actual effect it might have in their strategy, (even if it turned out to be more profitable) and those who abused this type of "repainting" behavior to show off, and hijack some boosts from the community by boasting about the "fake" results of their strategies.

Even if there are ways to evaluate the effectiveness of the tick-based approach that is applied in an existing strategy (this is out of the topic of this publication), it requires extra effort to do the analysis. Using this closed-based approach we can have more predictable results, without surprises.

⚠️ Caveats

Since this approach updates the trailing price on bar close, you must wait for at least one bar to close after the price crosses over the take profit target.

"backtest" için komut dosyalarını ara

Liquidity Maxing [JOAT]Liquidity Maxing - Institutional Liquidity Matrix

Introduction

Liquidity Maxing is an open-source strategy for TradingView built around institutional market structure concepts. It identifies structural shifts, evaluates trades through multi-factor confluence, and implements layered risk controls.

The strategy is designed for swing trading on 4-hour timeframes, focusing on how institutional order flow manifests in price action through structure breaks, inducements, and liquidity sweeps.

Core Functionality

Liquidity Maxing performs three primary functions:

Tracks market structure to identify when control shifts between buyers and sellers

Scores potential trades using an eight-factor confluence system

Manages position sizing and risk exposure dynamically based on volatility and user-defined limits

The goal is selective trading when multiple conditions align, rather than frequent entries.

Market Structure Engine

The structure engine tracks three key events:

Break of Structure (BOS): Price pushes beyond a prior pivot in the direction of trend

Change of Character (CHoCH): Control flips from bullish to bearish or vice versa

Inducement Sweeps (IDM): Market briefly runs stops against trend before moving in the real direction

The structure module continuously updates strong highs and lows, labeling structural shifts visually. IDM markers are optional and disabled by default to maintain chart clarity.

The trade engine requires valid structure alignment before considering entries. No structure, no trade.

Eight-Factor Confluence System

Instead of relying on a single indicator, Liquidity Maxing uses an eight-factor scoring system:

Structure alignment with current trend

RSI within healthy bands (different ranges for up and down trends)

MACD momentum agreement with direction

Volume above adaptive baseline

Price relative to main trend EMA

Session and weekend filter (configurable)

Volatility expansion/contraction via ATR shifts

Higher-timeframe EMA confirmation

Each factor contributes one point to the confluence score. The default minimum confluence threshold is 6 out of 8, but you can adjust this from 1-8 based on your preference for trade frequency versus selectivity.

Only when structure and confluence agree does the strategy proceed to risk evaluation.

Dynamic Risk Management

Risk controls are implemented in multiple layers:

ATR-based stops and targets with configurable risk-to-reward ratio (default 2:1)

Volatility-adjusted position sizing to maintain consistent risk per trade as ranges expand or compress

Daily and weekly risk budgets that halt new entries once thresholds are reached

Correlation cooldown to prevent clustered trades in the same direction

Global circuit breaker with maximum drawdown limit and emergency kill switch

If any guardrail is breached, the strategy will not open new positions. The dashboard clearly displays risk state for transparency.

Market Presets

The strategy includes configuration presets optimized for different market types:

Crypto (BTC/ETH): RSI bands 70/30, volume multiplier 1.2, enhanced ATR scaling

Forex Majors: RSI bands 75/25, volume multiplier 1.5

Indices (SPY/QQQ): RSI bands 70/30, volume multiplier 1.3

Custom: Default values for user customization

For crypto assets, the strategy automatically applies ATR volatility scaling to account for higher volatility characteristics.

Monitoring and Dashboards

The strategy includes optional monitoring layers:

Risk Operations Dashboard (top-right):

Trend state

Confluence score

ATR value

Current position size percentage

Global drawdown

Daily and weekly risk consumption

Correlation guard state

Alert mode status

Performance Console (top-left):

Net profit

Current equity

Win rate percentage

Average trade value

Sharpe-style ratio (rolling 50-bar window)

Profit factor

Open trade count

Optional risk tint on chart background provides visual indication of "safe to trade" versus "halted" state.

All visualization elements can be toggled on/off from the inputs for clean chart viewing or full telemetry during parameter tuning.

Alerts and Automation

The strategy supports alert integration with two formats:

Standard alerts: Human-readable messages for long, short, and risk-halt conditions

Webhook format: JSON-formatted payloads ready for external execution systems (optional)

Alert messages are predictable and unambiguous, suitable for manual review or automated forwarding to execution engines.

Built-in Validation Suite

The strategy includes an optional validation layer that can be enabled from inputs. It checks:

Internal consistency of structure and confluence metrics

Sanity and ordering of risk parameters

Position sizing compliance with user-defined floors and caps

This validation is optional and not required for trading, but provides transparency into system operation during development or troubleshooting.

Strategy Parameters

Market Presets:

Configuration Preset: Choose between Crypto (BTC/ETH), Forex Majors, Indices (SPY/QQQ), or Custom

Market Structure Architecture:

Pivot Length: Default 5 bars

Filter by Inducement (IDM): Default enabled

Visualize Structure: Default enabled

Structure Lookback: Default 50 bars

Risk & Capital Preservation:

Risk:Reward Ratio: Default 2.0

ATR Period: Default 14

ATR Multiplier (Stop): Default 2.0

Max Drawdown Circuit Breaker: Default 10%

Risk per Trade (% Equity): Default 1.5%

Daily Risk Limit: Default 6%

Weekly Risk Limit: Default 12%

Min Position Size (% Equity): Default 0.25%

Max Position Size (% Equity): Default 5%

Correlation Cooldown (bars): Default 3

Emergency Kill Switch: Default disabled

Signal Confluence:

RSI Length: Default 14

Trend EMA: Default 200

HTF Confirmation TF: Default Daily

Allow Weekend Trading: Default enabled

Minimum Confluence Score (0-8): Default 6

Backtesting Considerations

When backtesting this strategy, consider the following:

Commission: Default 0.05% (adjustable in strategy settings)

Initial Capital: Default $100,000 (adjustable)

Position Sizing: Uses percentage of equity (default 2% per trade)

Timeframe: Optimized for 4-hour charts, though can be tested on other timeframes

Results will vary significantly based on:

Market conditions and volatility regimes

Parameter settings, especially confluence threshold

Risk limit configuration

Symbol characteristics (crypto vs forex vs equities)

Past performance does not guarantee future results. Win rate, profit factor, and other metrics should be evaluated in context of drawdown periods, trade frequency, and market conditions.

How to Use This Strategy

This is a framework that requires understanding and parameter tuning, not a one-size-fits-all solution.

Recommended workflow:

Start on 4-hour timeframe with default parameters and appropriate market preset

Run backtests and study performance console metrics: focus on drawdown behavior, win rate, profit factor, and trade frequency

Adjust confluence threshold to match your risk appetite—higher thresholds mean fewer but more selective trades

Set realistic daily and weekly risk budgets appropriate for your account size and risk tolerance

Consider ATR multiplier adjustments based on market volatility characteristics

Only connect alerts or automation after thorough testing and parameter validation

Treat this as a risk framework with an integrated entry engine, not merely an entry signal generator. The risk controls are as important as the trade signals.

Strategy Limitations

Designed for swing trading timeframes; may not perform optimally on very short timeframes

Requires sufficient market structure to identify pivots; may struggle in choppy or low-volatility environments

Crypto markets require different parameter tuning than traditional markets

Risk limits may prevent entries during favorable setups if daily/weekly budgets are exhausted

Correlation cooldown may delay entries that would otherwise be valid

Backtesting results depend on data quality and may not reflect live trading with slippage

Design Philosophy

Many indicators tell you when price crossed a moving average or RSI left oversold. This strategy addresses questions institutional traders ask:

Who is in control of the market right now?

Is this move structurally significant or just noise?

Do I want to add more risk given what I've already done today/week?

If I'm wrong, exactly how painful can this be?

The strategy provides disciplined, repeatable answers to these questions through systematic structure analysis, confluence filtering, and multi-layer risk management.

Technical Implementation

The strategy uses Pine Script v6 with:

Custom types for structure, confluence, and risk state management

Functional programming approach for reusable calculations

State management through persistent variables

Optional visual elements that can be toggled independently

The code is open-source and can be modified to suit individual needs. All important logic is visible in the source code.

Disclaimer

This script is provided for educational and informational purposes only. It is not intended as financial, investment, trading, or any other type of advice or recommendation. Trading involves substantial risk of loss and is not suitable for all investors. Past performance, whether real or indicated by historical tests of strategies, is not indicative of future results.

No representation is being made that any account will or is likely to achieve profits or losses similar to those shown. In fact, there are frequently sharp differences between backtested results and actual results subsequently achieved by any particular trading strategy.

The user should be aware of the risks involved in trading and should trade only with risk capital. The authors and publishers of this script are not responsible for any losses or damages, including without limitation, any loss of profit, which may arise directly or indirectly from use of or reliance on this script.

This strategy uses technical analysis methods and indicators that are not guaranteed to be accurate or profitable. Market conditions change, and strategies that worked in the past may not work in the future. Users should thoroughly test any strategy in a paper trading environment before risking real capital.

Commission and slippage settings in backtests may not accurately reflect live trading conditions. Real trading results will vary based on execution quality, market liquidity, and other factors not captured in backtesting.

The user assumes full responsibility for all trading decisions made using this script. Always consult with a qualified financial advisor before making investment decisions.

Enjoy - officialjackofalltrades

Alert(), alertcondition() or strategy alerts?Variety of possibilities offered by PineScript, especially thanks to recent additions, created some confusion. Especially one question repeats quite often - which method to use to trigger alerts?

I'm posting this to clarify and give some syntax examples. I'll discuss these 3 methods in chronological order, meaning - in the order they were introduced to PineScript.

ALERTCONDITION() - it is a function call, which can be used only in study-type script. Since years ago, you could create 2 types of a script: strategy and study. First one enables creating a backtest of a strategy. Second was to develop scripts which didn't require backtesting and could trigger alerts. alertcondition() calls in strategy-type scripts were rejected by Pine compiler. On the other hand compiling study-type scripts rejected all strategy...() calls. That created difficulties, because once you had a nice and backtested strategy, you had to rip it off from all strategy...() function calls to convert your script to study-type so you could produce alerts. Maintenance of two versions of each script was necessary and it was painful.

"STRATEGY ALERTS" were introduced because of alertcondition() pains. To create strategy alert, you need to click "Add alert" button inside Strategy Tester (backtester) and only there. Alerts set-up this way are bound with the backtester - whenever backtester triggers an order, which is visible on the chart, alert is also fired. And you can customize alert message using some placeholders like {{strategy.order.contracts}} or {{ticker}}.

ALERT() was added last. This is an alerts-triggering function call, which can be run from strategy-type script. Finally it is doable! You can connect it to any event coded in PineScript and generate any alert message you want, thanks to concatenation of strings and wrapping variables into tostring() function.

Out of these three alertcondition() is obviously archaic and probably will be discontinued. There is a chance this makes strategy/study distinction not making sense anymore, so I wouldn't be surprised if "studies" are deprecated at some point.

But what are the differences between "Strategy alerts" and alert()? "Strategy alerts" seem easier to set-up with just a few clicks and probably easier to understand and verify, because they go in sync with the backtester and on-chart trade markers. It is especially important to understand how they work if you're building strategy based on pending orders (stop and limit) - events in your code might trigger placing pending order, but alert will be triggered only (and when) such order is executed.

But "Strategy Alerts" have some limitations - not every variable you'd like to include in alert message is available from PineScript. And maybe you don't need the alert fired when the trade hit a stop-loss or take-profit, because you have already forwarded info about closing conditions in entry alert to your broker/exchange.

Alert() was added to PineScript to fill all these gaps. Is allows concatenating any alert message you want, with any variable you want inside it and you can attach alert() function at any event in your PineScript code. For example - when placing orders, crossing variables, exiting trades, but not explicitly at pending orders execution.

The Verdict

"Strategy Alerts" might seem a better fit - easier to set-up and verify, flexible and they fire only when a trade really happens, not producing unnecessary mess when each pending order is placed. But these advantages are illusionary, because they don't give you the full-control which is needed when trading with real money. Especially when using pending orders. If an alert is fired when price actually hit a stop-order or limit-order level, and even if you are executing such alert within 1 second thanks to a tool like TradingConnector, you might already be late and you are making entry at a market price. Slippage will play a great role here. You need to send ordering alert when logical conditions are met - then it will be executed at the price you want. Even if you need to cancel all the pending orders which were not executed. Because of that I strongly recommend sticking to ALERT() when building your alerts system.

Below is an example strategy, showing syntax to manage placing the orders and cancelling them. Yes, this is another spin-off from my TradingView Alerts to MT4 MT5 . As usual, please don't pay attention to backtest results, as this is educational script only.

P.S. For the last time - farewell alertcondition(). You served us well.

Zero Lag Trend Signals (MTF) [Quant Trading] V7Overview

The Zero Lag Trend Signals (MTF) V7 is a comprehensive trend-following strategy that combines Zero Lag Exponential Moving Average (ZLEMA) with volatility-based bands to identify high-probability trade entries and exits. This strategy is designed to reduce lag inherent in traditional moving averages while incorporating dynamic risk management through ATR-based stops and multiple exit mechanisms.

This is a longer term horizon strategy that takes limited trades. It is not a high frequency trading and therefore will also have limited data and not > 100 trades.

How It Works

Core Signal Generation:

The strategy uses a Zero Lag EMA (ZLEMA) calculated by applying an EMA to price data that has been adjusted for lag:

Calculate lag period: floor((length - 1) / 2)

Apply lag correction: src + (src - src )

Calculate ZLEMA: EMA of lag-corrected price

Volatility bands are created using the highest ATR over a lookback period multiplied by a band multiplier. These bands are added to and subtracted from the ZLEMA line to create upper and lower boundaries.

Trend Detection:

The strategy maintains a trend variable that switches between bullish (1) and bearish (-1):

Long Signal: Triggers when price crosses above ZLEMA + volatility band

Short Signal: Triggers when price crosses below ZLEMA - volatility band

Optional ZLEMA Trend Confirmation:

When enabled, this filter requires ZLEMA to show directional momentum before entry:

Bullish Confirmation: ZLEMA must increase for 4 consecutive bars

Bearish Confirmation: ZLEMA must decrease for 4 consecutive bars

This additional filter helps avoid false signals in choppy or ranging markets.

Risk Management Features:

The strategy includes multiple stop-loss and take-profit mechanisms:

Volatility-Based Stops: Default stop-loss is placed at ZLEMA ± volatility band

ATR-Based Stops: Dynamic stop-loss calculated as entry price ± (ATR × multiplier)

ATR Trailing Stop: Ratcheting stop-loss that follows price but never moves against position

Risk-Reward Profit Target: Take-profit level set as a multiple of stop distance

Break-Even Stop: Moves stop to entry price after reaching specified R:R ratio

Trend-Based Exit: Closes position when price crosses EMA in opposite direction

Performance Tracking:

The strategy includes optional features for monitoring and analyzing trades:

Floating Statistics Table: Displays key metrics including win rate, GOA (Gain on Account), net P&L, and max drawdown

Trade Log Labels: Shows entry/exit prices, P&L, bars held, and exit reason for each closed trade

CSV Export Fields: Outputs trade data for external analysis

Default Strategy Settings

Commission & Slippage:

Commission: 0.1% per trade

Slippage: 3 ticks

Initial Capital: $1,000

Position Size: 100% of equity per trade

Main Calculation Parameters:

Length: 70 (range: 70-7000) - Controls ZLEMA calculation period

Band Multiplier: 1.2 - Adjusts width of volatility bands

Entry Conditions (All Disabled by Default):

Use ZLEMA Trend Confirmation: OFF - Requires ZLEMA directional momentum

Re-Enter on Long Trend: OFF - Allows multiple entries during sustained trends

Short Trades:

Allow Short Trades: OFF - Strategy is long-only by default

Performance Settings (All Disabled by Default):

Use Profit Target: OFF

Profit Target Risk-Reward Ratio: 2.0 (when enabled)

Dynamic TP/SL (All Disabled by Default):

Use ATR-Based Stop-Loss & Take-Profit: OFF

ATR Length: 14

Stop-Loss ATR Multiplier: 1.5

Profit Target ATR Multiplier: 2.5

Use ATR Trailing Stop: OFF

Trailing Stop ATR Multiplier: 1.5

Use Break-Even Stop-Loss: OFF

Move SL to Break-Even After RR: 1.5

Use Trend-Based Take Profit: OFF

EMA Exit Length: 9

Trade Data Display (All Disabled by Default):

Show Floating Stats Table: OFF

Show Trade Log Labels: OFF

Enable CSV Export: OFF

Trade Label Vertical Offset: 0.5

Backtesting Date Range:

Start Date: January 1, 2018

End Date: December 31, 2069

Important Usage Notes

Default Configuration: The strategy operates in its most basic form with default settings - using only ZLEMA crossovers with volatility bands and volatility-based stop-losses. All advanced features must be manually enabled.

Stop-Loss Priority: If multiple stop-loss methods are enabled simultaneously, the strategy will use whichever condition is hit first. ATR-based stops override volatility-based stops when enabled.

Long-Only by Default: Short trading is disabled by default. Enable "Allow Short Trades" to trade both directions.

Performance Monitoring: Enable the floating stats table and trade log labels to visualize strategy performance during backtesting.

Exit Mechanisms: The strategy can exit trades through multiple methods: stop-loss hit, take-profit reached, trend reversal, or trailing stop activation. The trade log identifies which exit method was used.

Re-Entry Logic: When "Re-Enter on Long Trend" is enabled with ZLEMA trend confirmation, the strategy can take multiple long positions during extended uptrends as long as all entry conditions remain valid.

Capital Efficiency: Default setting uses 100% of equity per trade. Adjust "default_qty_value" to manage position sizing based on risk tolerance.

Realistic Backtesting: Strategy includes commission (0.1%) and slippage (3 ticks) to provide realistic performance expectations. These values should be adjusted based on your broker and market conditions.

Recommended Use Cases

Trending Markets: Best suited for markets with clear directional moves where trend-following strategies excel

Medium to Long-Term Trading: The default length of 70 makes this strategy more appropriate for swing trading rather than scalping

Risk-Conscious Traders: Multiple stop-loss options allow traders to customize risk management to their comfort level

Backtesting & Optimization: Comprehensive performance tracking features make this strategy ideal for testing different parameter combinations

Limitations & Considerations

Like all trend-following strategies, performance may suffer in choppy or ranging markets

Default 100% position sizing means full capital exposure per trade - consider reducing for conservative risk management

Higher length values (70+) reduce signal frequency but may improve signal quality

Multiple simultaneous risk management features may create conflicting exit signals

Past performance shown in backtests does not guarantee future results

Customization Tips

For more aggressive trading:

Reduce length parameter (minimum 70)

Decrease band multiplier for tighter bands

Enable short trades

Use lower profit target R:R ratios

For more conservative trading:

Increase length parameter

Enable ZLEMA trend confirmation

Use wider ATR stop-loss multipliers

Enable break-even stop-loss

Reduce position size from 100% default

For optimal choppy market performance:

Enable ZLEMA trend confirmation

Increase band multiplier

Use tighter profit targets

Avoid re-entry on trend continuation

Visual Elements

The strategy plots several elements on the chart:

ZLEMA line (color-coded by trend direction)

Upper and lower volatility bands

Long entry markers (green triangles)

Short entry markers (red triangles, when enabled)

Stop-loss levels (when positions are open)

Take-profit levels (when enabled and positions are open)

Trailing stop lines (when enabled and positions are open)

Optional ZLEMA trend markers (triangles at highs/lows)

Optional trade log labels showing complete trade information

Exit Reason Codes (for CSV Export)

When CSV export is enabled, exit reasons are coded as:

0 = Manual/Other

1 = Trailing Stop-Loss

2 = Profit Target

3 = ATR Stop-Loss

4 = Trend Change

Conclusion

Zero Lag Trend Signals V7 provides a robust framework for trend-following with extensive customization options. The strategy balances simplicity in its core logic with sophisticated risk management features, making it suitable for both beginner and advanced traders. By reducing moving average lag while incorporating volatility-based signals, it aims to capture trends earlier while managing risk through multiple configurable exit mechanisms.

The modular design allows traders to start with basic trend-following and progressively add complexity through ZLEMA confirmation, multiple stop-loss methods, and advanced exit strategies. Comprehensive performance tracking and export capabilities make this strategy an excellent tool for systematic testing and optimization.

Note: This strategy is provided for educational and backtesting purposes. All trading involves risk. Past performance does not guarantee future results. Always test thoroughly with paper trading before risking real capital, and adjust position sizing and risk parameters according to your risk tolerance and account size.

================================================================================

TAGS:

================================================================================

trend following, ZLEMA, zero lag, volatility bands, ATR stops, risk management, swing trading, momentum, trend confirmation, backtesting

================================================================================

CATEGORY:

================================================================================

Strategies

================================================================================

CHART SETUP RECOMMENDATIONS:

================================================================================

For optimal visualization when publishing:

Use a clean chart with no other indicators overlaid

Select a timeframe that shows multiple trade signals (4H or Daily recommended)

Choose a trending asset (crypto, forex major pairs, or trending stocks work well)

Show at least 6-12 months of data to demonstrate strategy across different market conditions

Enable the floating stats table to display key performance metrics

Ensure all indicator lines (ZLEMA, bands, stops) are clearly visible

Use the default chart type (candlesticks) - avoid Heikin Ashi, Renko, etc.

Make sure symbol information and timeframe are clearly visible

================================================================================

COMPLIANCE NOTES:

================================================================================

✅ Open-source publication with complete code visibility

✅ English-only title and description

✅ Detailed explanation of methodology and calculations

✅ Realistic commission (0.1%) and slippage (3 ticks) included

✅ All default parameters clearly documented

✅ Performance limitations and risks disclosed

✅ No unrealistic claims about performance

✅ No guaranteed results promised

✅ Appropriate for public library (original trend-following implementation with ZLEMA)

✅ Educational disclaimers included

✅ All features explained in detail

================================================================================

Markov Chain [3D] | FractalystWhat exactly is a Markov Chain?

This indicator uses a Markov Chain model to analyze, quantify, and visualize the transitions between market regimes (Bull, Bear, Neutral) on your chart. It dynamically detects these regimes in real-time, calculates transition probabilities, and displays them as animated 3D spheres and arrows, giving traders intuitive insight into current and future market conditions.

How does a Markov Chain work, and how should I read this spheres-and-arrows diagram?

Think of three weather modes: Sunny, Rainy, Cloudy.

Each sphere is one mode. The loop on a sphere means “stay the same next step” (e.g., Sunny again tomorrow).

The arrows leaving a sphere show where things usually go next if they change (e.g., Sunny moving to Cloudy).

Some paths matter more than others. A more prominent loop means the current mode tends to persist. A more prominent outgoing arrow means a change to that destination is the usual next step.

Direction isn’t symmetric: moving Sunny→Cloudy can behave differently than Cloudy→Sunny.

Now relabel the spheres to markets: Bull, Bear, Neutral.

Spheres: market regimes (uptrend, downtrend, range).

Self‑loop: tendency for the current regime to continue on the next bar.

Arrows: the most common next regime if a switch happens.

How to read: Start at the sphere that matches current bar state. If the loop stands out, expect continuation. If one outgoing path stands out, that switch is the typical next step. Opposite directions can differ (Bear→Neutral doesn’t have to match Neutral→Bear).

What states and transitions are shown?

The three market states visualized are:

Bullish (Bull): Upward or strong-market regime.

Bearish (Bear): Downward or weak-market regime.

Neutral: Sideways or range-bound regime.

Bidirectional animated arrows and probability labels show how likely the market is to move from one regime to another (e.g., Bull → Bear or Neutral → Bull).

How does the regime detection system work?

You can use either built-in price returns (based on adaptive Z-score normalization) or supply three custom indicators (such as volume, oscillators, etc.).

Values are statistically normalized (Z-scored) over a configurable lookback period.

The normalized outputs are classified into Bull, Bear, or Neutral zones.

If using three indicators, their regime signals are averaged and smoothed for robustness.

How are transition probabilities calculated?

On every confirmed bar, the algorithm tracks the sequence of detected market states, then builds a rolling window of transitions.

The code maintains a transition count matrix for all regime pairs (e.g., Bull → Bear).

Transition probabilities are extracted for each possible state change using Laplace smoothing for numerical stability, and frequently updated in real-time.

What is unique about the visualization?

3D animated spheres represent each regime and change visually when active.

Animated, bidirectional arrows reveal transition probabilities and allow you to see both dominant and less likely regime flows.

Particles (moving dots) animate along the arrows, enhancing the perception of regime flow direction and speed.

All elements dynamically update with each new price bar, providing a live market map in an intuitive, engaging format.

Can I use custom indicators for regime classification?

Yes! Enable the "Custom Indicators" switch and select any three chart series as inputs. These will be normalized and combined (each with equal weight), broadening the regime classification beyond just price-based movement.

What does the “Lookback Period” control?

Lookback Period (default: 100) sets how much historical data builds the probability matrix. Shorter periods adapt faster to regime changes but may be noisier. Longer periods are more stable but slower to adapt.

How is this different from a Hidden Markov Model (HMM)?

It sets the window for both regime detection and probability calculations. Lower values make the system more reactive, but potentially noisier. Higher values smooth estimates and make the system more robust.

How is this Markov Chain different from a Hidden Markov Model (HMM)?

Markov Chain (as here): All market regimes (Bull, Bear, Neutral) are directly observable on the chart. The transition matrix is built from actual detected regimes, keeping the model simple and interpretable.

Hidden Markov Model: The actual regimes are unobservable ("hidden") and must be inferred from market output or indicator "emissions" using statistical learning algorithms. HMMs are more complex, can capture more subtle structure, but are harder to visualize and require additional machine learning steps for training.

A standard Markov Chain models transitions between observable states using a simple transition matrix, while a Hidden Markov Model assumes the true states are hidden (latent) and must be inferred from observable “emissions” like price or volume data. In practical terms, a Markov Chain is transparent and easier to implement and interpret; an HMM is more expressive but requires statistical inference to estimate hidden states from data.

Markov Chain: states are observable; you directly count or estimate transition probabilities between visible states. This makes it simpler, faster, and easier to validate and tune.

HMM: states are hidden; you only observe emissions generated by those latent states. Learning involves machine learning/statistical algorithms (commonly Baum–Welch/EM for training and Viterbi for decoding) to infer both the transition dynamics and the most likely hidden state sequence from data.

How does the indicator avoid “repainting” or look-ahead bias?

All regime changes and matrix updates happen only on confirmed (closed) bars, so no future data is leaked, ensuring reliable real-time operation.

Are there practical tuning tips?

Tune the Lookback Period for your asset/timeframe: shorter for fast markets, longer for stability.

Use custom indicators if your asset has unique regime drivers.

Watch for rapid changes in transition probabilities as early warning of a possible regime shift.

Who is this indicator for?

Quants and quantitative researchers exploring probabilistic market modeling, especially those interested in regime-switching dynamics and Markov models.

Programmers and system developers who need a probabilistic regime filter for systematic and algorithmic backtesting:

The Markov Chain indicator is ideally suited for programmatic integration via its bias output (1 = Bull, 0 = Neutral, -1 = Bear).

Although the visualization is engaging, the core output is designed for automated, rules-based workflows—not for discretionary/manual trading decisions.

Developers can connect the indicator’s output directly to their Pine Script logic (using input.source()), allowing rapid and robust backtesting of regime-based strategies.

It acts as a plug-and-play regime filter: simply plug the bias output into your entry/exit logic, and you have a scientifically robust, probabilistically-derived signal for filtering, timing, position sizing, or risk regimes.

The MC's output is intentionally "trinary" (1/0/-1), focusing on clear regime states for unambiguous decision-making in code. If you require nuanced, multi-probability or soft-label state vectors, consider expanding the indicator or stacking it with a probability-weighted logic layer in your scripting.

Because it avoids subjectivity, this approach is optimal for systematic quants, algo developers building backtested, repeatable strategies based on probabilistic regime analysis.

What's the mathematical foundation behind this?

The mathematical foundation behind this Markov Chain indicator—and probabilistic regime detection in finance—draws from two principal models: the (standard) Markov Chain and the Hidden Markov Model (HMM).

How to use this indicator programmatically?

The Markov Chain indicator automatically exports a bias value (+1 for Bullish, -1 for Bearish, 0 for Neutral) as a plot visible in the Data Window. This allows you to integrate its regime signal into your own scripts and strategies for backtesting, automation, or live trading.

Step-by-Step Integration with Pine Script (input.source)

Add the Markov Chain indicator to your chart.

This must be done first, since your custom script will "pull" the bias signal from the indicator's plot.

In your strategy, create an input using input.source()

Example:

//@version=5

strategy("MC Bias Strategy Example")

mcBias = input.source(close, "MC Bias Source")

After saving, go to your script’s settings. For the “MC Bias Source” input, select the plot/output of the Markov Chain indicator (typically its bias plot).

Use the bias in your trading logic

Example (long only on Bull, flat otherwise):

if mcBias == 1

strategy.entry("Long", strategy.long)

else

strategy.close("Long")

For more advanced workflows, combine mcBias with additional filters or trailing stops.

How does this work behind-the-scenes?

TradingView’s input.source() lets you use any plot from another indicator as a real-time, “live” data feed in your own script (source).

The selected bias signal is available to your Pine code as a variable, enabling logical decisions based on regime (trend-following, mean-reversion, etc.).

This enables powerful strategy modularity : decouple regime detection from entry/exit logic, allowing fast experimentation without rewriting core signal code.

Integrating 45+ Indicators with Your Markov Chain — How & Why

The Enhanced Custom Indicators Export script exports a massive suite of over 45 technical indicators—ranging from classic momentum (RSI, MACD, Stochastic, etc.) to trend, volume, volatility, and oscillator tools—all pre-calculated, centered/scaled, and available as plots.

// Enhanced Custom Indicators Export - 45 Technical Indicators

// Comprehensive technical analysis suite for advanced market regime detection

//@version=6

indicator('Enhanced Custom Indicators Export | Fractalyst', shorttitle='Enhanced CI Export', overlay=false, scale=scale.right, max_labels_count=500, max_lines_count=500)

// |----- Input Parameters -----| //

momentum_group = "Momentum Indicators"

trend_group = "Trend Indicators"

volume_group = "Volume Indicators"

volatility_group = "Volatility Indicators"

oscillator_group = "Oscillator Indicators"

display_group = "Display Settings"

// Common lengths

length_14 = input.int(14, "Standard Length (14)", minval=1, maxval=100, group=momentum_group)

length_20 = input.int(20, "Medium Length (20)", minval=1, maxval=200, group=trend_group)

length_50 = input.int(50, "Long Length (50)", minval=1, maxval=200, group=trend_group)

// Display options

show_table = input.bool(true, "Show Values Table", group=display_group)

table_size = input.string("Small", "Table Size", options= , group=display_group)

// |----- MOMENTUM INDICATORS (15 indicators) -----| //

// 1. RSI (Relative Strength Index)

rsi_14 = ta.rsi(close, length_14)

rsi_centered = rsi_14 - 50

// 2. Stochastic Oscillator

stoch_k = ta.stoch(close, high, low, length_14)

stoch_d = ta.sma(stoch_k, 3)

stoch_centered = stoch_k - 50

// 3. Williams %R

williams_r = ta.stoch(close, high, low, length_14) - 100

// 4. MACD (Moving Average Convergence Divergence)

= ta.macd(close, 12, 26, 9)

// 5. Momentum (Rate of Change)

momentum = ta.mom(close, length_14)

momentum_pct = (momentum / close ) * 100

// 6. Rate of Change (ROC)

roc = ta.roc(close, length_14)

// 7. Commodity Channel Index (CCI)

cci = ta.cci(close, length_20)

// 8. Money Flow Index (MFI)

mfi = ta.mfi(close, length_14)

mfi_centered = mfi - 50

// 9. Awesome Oscillator (AO)

ao = ta.sma(hl2, 5) - ta.sma(hl2, 34)

// 10. Accelerator Oscillator (AC)

ac = ao - ta.sma(ao, 5)

// 11. Chande Momentum Oscillator (CMO)

cmo = ta.cmo(close, length_14)

// 12. Detrended Price Oscillator (DPO)

dpo = close - ta.sma(close, length_20)

// 13. Price Oscillator (PPO)

ppo = ta.sma(close, 12) - ta.sma(close, 26)

ppo_pct = (ppo / ta.sma(close, 26)) * 100

// 14. TRIX

trix_ema1 = ta.ema(close, length_14)

trix_ema2 = ta.ema(trix_ema1, length_14)

trix_ema3 = ta.ema(trix_ema2, length_14)

trix = ta.roc(trix_ema3, 1) * 10000

// 15. Klinger Oscillator

klinger = ta.ema(volume * (high + low + close) / 3, 34) - ta.ema(volume * (high + low + close) / 3, 55)

// 16. Fisher Transform

fisher_hl2 = 0.5 * (hl2 - ta.lowest(hl2, 10)) / (ta.highest(hl2, 10) - ta.lowest(hl2, 10)) - 0.25

fisher = 0.5 * math.log((1 + fisher_hl2) / (1 - fisher_hl2))

// 17. Stochastic RSI

stoch_rsi = ta.stoch(rsi_14, rsi_14, rsi_14, length_14)

stoch_rsi_centered = stoch_rsi - 50

// 18. Relative Vigor Index (RVI)

rvi_num = ta.swma(close - open)

rvi_den = ta.swma(high - low)

rvi = rvi_den != 0 ? rvi_num / rvi_den : 0

// 19. Balance of Power (BOP)

bop = (close - open) / (high - low)

// |----- TREND INDICATORS (10 indicators) -----| //

// 20. Simple Moving Average Momentum

sma_20 = ta.sma(close, length_20)

sma_momentum = ((close - sma_20) / sma_20) * 100

// 21. Exponential Moving Average Momentum

ema_20 = ta.ema(close, length_20)

ema_momentum = ((close - ema_20) / ema_20) * 100

// 22. Parabolic SAR

sar = ta.sar(0.02, 0.02, 0.2)

sar_trend = close > sar ? 1 : -1

// 23. Linear Regression Slope

lr_slope = ta.linreg(close, length_20, 0) - ta.linreg(close, length_20, 1)

// 24. Moving Average Convergence (MAC)

mac = ta.sma(close, 10) - ta.sma(close, 30)

// 25. Trend Intensity Index (TII)

tii_sum = 0.0

for i = 1 to length_20

tii_sum += close > close ? 1 : 0

tii = (tii_sum / length_20) * 100

// 26. Ichimoku Cloud Components

ichimoku_tenkan = (ta.highest(high, 9) + ta.lowest(low, 9)) / 2

ichimoku_kijun = (ta.highest(high, 26) + ta.lowest(low, 26)) / 2

ichimoku_signal = ichimoku_tenkan > ichimoku_kijun ? 1 : -1

// 27. MESA Adaptive Moving Average (MAMA)

mama_alpha = 2.0 / (length_20 + 1)

mama = ta.ema(close, length_20)

mama_momentum = ((close - mama) / mama) * 100

// 28. Zero Lag Exponential Moving Average (ZLEMA)

zlema_lag = math.round((length_20 - 1) / 2)

zlema_data = close + (close - close )

zlema = ta.ema(zlema_data, length_20)

zlema_momentum = ((close - zlema) / zlema) * 100

// |----- VOLUME INDICATORS (6 indicators) -----| //

// 29. On-Balance Volume (OBV)

obv = ta.obv

// 30. Volume Rate of Change (VROC)

vroc = ta.roc(volume, length_14)

// 31. Price Volume Trend (PVT)

pvt = ta.pvt

// 32. Negative Volume Index (NVI)

nvi = 0.0

nvi := volume < volume ? nvi + ((close - close ) / close ) * nvi : nvi

// 33. Positive Volume Index (PVI)

pvi = 0.0

pvi := volume > volume ? pvi + ((close - close ) / close ) * pvi : pvi

// 34. Volume Oscillator

vol_osc = ta.sma(volume, 5) - ta.sma(volume, 10)

// 35. Ease of Movement (EOM)

eom_distance = high - low

eom_box_height = volume / 1000000

eom = eom_box_height != 0 ? eom_distance / eom_box_height : 0

eom_sma = ta.sma(eom, length_14)

// 36. Force Index

force_index = volume * (close - close )

force_index_sma = ta.sma(force_index, length_14)

// |----- VOLATILITY INDICATORS (10 indicators) -----| //

// 37. Average True Range (ATR)

atr = ta.atr(length_14)

atr_pct = (atr / close) * 100

// 38. Bollinger Bands Position

bb_basis = ta.sma(close, length_20)

bb_dev = 2.0 * ta.stdev(close, length_20)

bb_upper = bb_basis + bb_dev

bb_lower = bb_basis - bb_dev

bb_position = bb_dev != 0 ? (close - bb_basis) / bb_dev : 0

bb_width = bb_dev != 0 ? (bb_upper - bb_lower) / bb_basis * 100 : 0

// 39. Keltner Channels Position

kc_basis = ta.ema(close, length_20)

kc_range = ta.ema(ta.tr, length_20)

kc_upper = kc_basis + (2.0 * kc_range)

kc_lower = kc_basis - (2.0 * kc_range)

kc_position = kc_range != 0 ? (close - kc_basis) / kc_range : 0

// 40. Donchian Channels Position

dc_upper = ta.highest(high, length_20)

dc_lower = ta.lowest(low, length_20)

dc_basis = (dc_upper + dc_lower) / 2

dc_position = (dc_upper - dc_lower) != 0 ? (close - dc_basis) / (dc_upper - dc_lower) : 0

// 41. Standard Deviation

std_dev = ta.stdev(close, length_20)

std_dev_pct = (std_dev / close) * 100

// 42. Relative Volatility Index (RVI)

rvi_up = ta.stdev(close > close ? close : 0, length_14)

rvi_down = ta.stdev(close < close ? close : 0, length_14)

rvi_total = rvi_up + rvi_down

rvi_volatility = rvi_total != 0 ? (rvi_up / rvi_total) * 100 : 50

// 43. Historical Volatility

hv_returns = math.log(close / close )

hv = ta.stdev(hv_returns, length_20) * math.sqrt(252) * 100

// 44. Garman-Klass Volatility

gk_vol = math.log(high/low) * math.log(high/low) - (2*math.log(2)-1) * math.log(close/open) * math.log(close/open)

gk_volatility = math.sqrt(ta.sma(gk_vol, length_20)) * 100

// 45. Parkinson Volatility

park_vol = math.log(high/low) * math.log(high/low)

parkinson = math.sqrt(ta.sma(park_vol, length_20) / (4 * math.log(2))) * 100

// 46. Rogers-Satchell Volatility

rs_vol = math.log(high/close) * math.log(high/open) + math.log(low/close) * math.log(low/open)

rogers_satchell = math.sqrt(ta.sma(rs_vol, length_20)) * 100

// |----- OSCILLATOR INDICATORS (5 indicators) -----| //

// 47. Elder Ray Index

elder_bull = high - ta.ema(close, 13)

elder_bear = low - ta.ema(close, 13)

elder_power = elder_bull + elder_bear

// 48. Schaff Trend Cycle (STC)

stc_macd = ta.ema(close, 23) - ta.ema(close, 50)

stc_k = ta.stoch(stc_macd, stc_macd, stc_macd, 10)

stc_d = ta.ema(stc_k, 3)

stc = ta.stoch(stc_d, stc_d, stc_d, 10)

// 49. Coppock Curve

coppock_roc1 = ta.roc(close, 14)

coppock_roc2 = ta.roc(close, 11)

coppock = ta.wma(coppock_roc1 + coppock_roc2, 10)

// 50. Know Sure Thing (KST)

kst_roc1 = ta.roc(close, 10)

kst_roc2 = ta.roc(close, 15)

kst_roc3 = ta.roc(close, 20)

kst_roc4 = ta.roc(close, 30)

kst = ta.sma(kst_roc1, 10) + 2*ta.sma(kst_roc2, 10) + 3*ta.sma(kst_roc3, 10) + 4*ta.sma(kst_roc4, 15)

// 51. Percentage Price Oscillator (PPO)

ppo_line = ((ta.ema(close, 12) - ta.ema(close, 26)) / ta.ema(close, 26)) * 100

ppo_signal = ta.ema(ppo_line, 9)

ppo_histogram = ppo_line - ppo_signal

// |----- PLOT MAIN INDICATORS -----| //

// Plot key momentum indicators

plot(rsi_centered, title="01_RSI_Centered", color=color.purple, linewidth=1)

plot(stoch_centered, title="02_Stoch_Centered", color=color.blue, linewidth=1)

plot(williams_r, title="03_Williams_R", color=color.red, linewidth=1)

plot(macd_histogram, title="04_MACD_Histogram", color=color.orange, linewidth=1)

plot(cci, title="05_CCI", color=color.green, linewidth=1)

// Plot trend indicators

plot(sma_momentum, title="06_SMA_Momentum", color=color.navy, linewidth=1)

plot(ema_momentum, title="07_EMA_Momentum", color=color.maroon, linewidth=1)

plot(sar_trend, title="08_SAR_Trend", color=color.teal, linewidth=1)

plot(lr_slope, title="09_LR_Slope", color=color.lime, linewidth=1)

plot(mac, title="10_MAC", color=color.fuchsia, linewidth=1)

// Plot volatility indicators

plot(atr_pct, title="11_ATR_Pct", color=color.yellow, linewidth=1)

plot(bb_position, title="12_BB_Position", color=color.aqua, linewidth=1)

plot(kc_position, title="13_KC_Position", color=color.olive, linewidth=1)

plot(std_dev_pct, title="14_StdDev_Pct", color=color.silver, linewidth=1)

plot(bb_width, title="15_BB_Width", color=color.gray, linewidth=1)

// Plot volume indicators

plot(vroc, title="16_VROC", color=color.blue, linewidth=1)

plot(eom_sma, title="17_EOM", color=color.red, linewidth=1)

plot(vol_osc, title="18_Vol_Osc", color=color.green, linewidth=1)

plot(force_index_sma, title="19_Force_Index", color=color.orange, linewidth=1)

plot(obv, title="20_OBV", color=color.purple, linewidth=1)

// Plot additional oscillators

plot(ao, title="21_Awesome_Osc", color=color.navy, linewidth=1)

plot(cmo, title="22_CMO", color=color.maroon, linewidth=1)

plot(dpo, title="23_DPO", color=color.teal, linewidth=1)

plot(trix, title="24_TRIX", color=color.lime, linewidth=1)

plot(fisher, title="25_Fisher", color=color.fuchsia, linewidth=1)

// Plot more momentum indicators

plot(mfi_centered, title="26_MFI_Centered", color=color.yellow, linewidth=1)

plot(ac, title="27_AC", color=color.aqua, linewidth=1)

plot(ppo_pct, title="28_PPO_Pct", color=color.olive, linewidth=1)

plot(stoch_rsi_centered, title="29_StochRSI_Centered", color=color.silver, linewidth=1)

plot(klinger, title="30_Klinger", color=color.gray, linewidth=1)

// Plot trend continuation

plot(tii, title="31_TII", color=color.blue, linewidth=1)

plot(ichimoku_signal, title="32_Ichimoku_Signal", color=color.red, linewidth=1)

plot(mama_momentum, title="33_MAMA_Momentum", color=color.green, linewidth=1)

plot(zlema_momentum, title="34_ZLEMA_Momentum", color=color.orange, linewidth=1)

plot(bop, title="35_BOP", color=color.purple, linewidth=1)

// Plot volume continuation

plot(nvi, title="36_NVI", color=color.navy, linewidth=1)

plot(pvi, title="37_PVI", color=color.maroon, linewidth=1)

plot(momentum_pct, title="38_Momentum_Pct", color=color.teal, linewidth=1)

plot(roc, title="39_ROC", color=color.lime, linewidth=1)

plot(rvi, title="40_RVI", color=color.fuchsia, linewidth=1)

// Plot volatility continuation

plot(dc_position, title="41_DC_Position", color=color.yellow, linewidth=1)

plot(rvi_volatility, title="42_RVI_Volatility", color=color.aqua, linewidth=1)

plot(hv, title="43_Historical_Vol", color=color.olive, linewidth=1)

plot(gk_volatility, title="44_GK_Volatility", color=color.silver, linewidth=1)

plot(parkinson, title="45_Parkinson_Vol", color=color.gray, linewidth=1)

// Plot final oscillators

plot(rogers_satchell, title="46_RS_Volatility", color=color.blue, linewidth=1)

plot(elder_power, title="47_Elder_Power", color=color.red, linewidth=1)

plot(stc, title="48_STC", color=color.green, linewidth=1)

plot(coppock, title="49_Coppock", color=color.orange, linewidth=1)

plot(kst, title="50_KST", color=color.purple, linewidth=1)

// Plot final indicators

plot(ppo_histogram, title="51_PPO_Histogram", color=color.navy, linewidth=1)

plot(pvt, title="52_PVT", color=color.maroon, linewidth=1)

// |----- Reference Lines -----| //

hline(0, "Zero Line", color=color.gray, linestyle=hline.style_dashed, linewidth=1)

hline(50, "Midline", color=color.gray, linestyle=hline.style_dotted, linewidth=1)

hline(-50, "Lower Midline", color=color.gray, linestyle=hline.style_dotted, linewidth=1)

hline(25, "Upper Threshold", color=color.gray, linestyle=hline.style_dotted, linewidth=1)

hline(-25, "Lower Threshold", color=color.gray, linestyle=hline.style_dotted, linewidth=1)

// |----- Enhanced Information Table -----| //

if show_table and barstate.islast

table_position = position.top_right

table_text_size = table_size == "Tiny" ? size.tiny : table_size == "Small" ? size.small : size.normal

var table info_table = table.new(table_position, 3, 18, bgcolor=color.new(color.white, 85), border_width=1, border_color=color.gray)

// Headers

table.cell(info_table, 0, 0, 'Category', text_color=color.black, text_size=table_text_size, bgcolor=color.new(color.blue, 70))

table.cell(info_table, 1, 0, 'Indicator', text_color=color.black, text_size=table_text_size, bgcolor=color.new(color.blue, 70))

table.cell(info_table, 2, 0, 'Value', text_color=color.black, text_size=table_text_size, bgcolor=color.new(color.blue, 70))

// Key Momentum Indicators

table.cell(info_table, 0, 1, 'MOMENTUM', text_color=color.purple, text_size=table_text_size, bgcolor=color.new(color.purple, 90))

table.cell(info_table, 1, 1, 'RSI Centered', text_color=color.purple, text_size=table_text_size)

table.cell(info_table, 2, 1, str.tostring(rsi_centered, '0.00'), text_color=color.purple, text_size=table_text_size)

table.cell(info_table, 0, 2, '', text_color=color.blue, text_size=table_text_size)

table.cell(info_table, 1, 2, 'Stoch Centered', text_color=color.blue, text_size=table_text_size)

table.cell(info_table, 2, 2, str.tostring(stoch_centered, '0.00'), text_color=color.blue, text_size=table_text_size)

table.cell(info_table, 0, 3, '', text_color=color.red, text_size=table_text_size)

table.cell(info_table, 1, 3, 'Williams %R', text_color=color.red, text_size=table_text_size)

table.cell(info_table, 2, 3, str.tostring(williams_r, '0.00'), text_color=color.red, text_size=table_text_size)

table.cell(info_table, 0, 4, '', text_color=color.orange, text_size=table_text_size)

table.cell(info_table, 1, 4, 'MACD Histogram', text_color=color.orange, text_size=table_text_size)

table.cell(info_table, 2, 4, str.tostring(macd_histogram, '0.000'), text_color=color.orange, text_size=table_text_size)

table.cell(info_table, 0, 5, '', text_color=color.green, text_size=table_text_size)

table.cell(info_table, 1, 5, 'CCI', text_color=color.green, text_size=table_text_size)

table.cell(info_table, 2, 5, str.tostring(cci, '0.00'), text_color=color.green, text_size=table_text_size)

// Key Trend Indicators

table.cell(info_table, 0, 6, 'TREND', text_color=color.navy, text_size=table_text_size, bgcolor=color.new(color.navy, 90))

table.cell(info_table, 1, 6, 'SMA Momentum %', text_color=color.navy, text_size=table_text_size)

table.cell(info_table, 2, 6, str.tostring(sma_momentum, '0.00'), text_color=color.navy, text_size=table_text_size)

table.cell(info_table, 0, 7, '', text_color=color.maroon, text_size=table_text_size)

table.cell(info_table, 1, 7, 'EMA Momentum %', text_color=color.maroon, text_size=table_text_size)

table.cell(info_table, 2, 7, str.tostring(ema_momentum, '0.00'), text_color=color.maroon, text_size=table_text_size)

table.cell(info_table, 0, 8, '', text_color=color.teal, text_size=table_text_size)

table.cell(info_table, 1, 8, 'SAR Trend', text_color=color.teal, text_size=table_text_size)

table.cell(info_table, 2, 8, str.tostring(sar_trend, '0'), text_color=color.teal, text_size=table_text_size)

table.cell(info_table, 0, 9, '', text_color=color.lime, text_size=table_text_size)

table.cell(info_table, 1, 9, 'Linear Regression', text_color=color.lime, text_size=table_text_size)

table.cell(info_table, 2, 9, str.tostring(lr_slope, '0.000'), text_color=color.lime, text_size=table_text_size)

// Key Volatility Indicators

table.cell(info_table, 0, 10, 'VOLATILITY', text_color=color.yellow, text_size=table_text_size, bgcolor=color.new(color.yellow, 90))

table.cell(info_table, 1, 10, 'ATR %', text_color=color.yellow, text_size=table_text_size)

table.cell(info_table, 2, 10, str.tostring(atr_pct, '0.00'), text_color=color.yellow, text_size=table_text_size)

table.cell(info_table, 0, 11, '', text_color=color.aqua, text_size=table_text_size)

table.cell(info_table, 1, 11, 'BB Position', text_color=color.aqua, text_size=table_text_size)

table.cell(info_table, 2, 11, str.tostring(bb_position, '0.00'), text_color=color.aqua, text_size=table_text_size)

table.cell(info_table, 0, 12, '', text_color=color.olive, text_size=table_text_size)

table.cell(info_table, 1, 12, 'KC Position', text_color=color.olive, text_size=table_text_size)

table.cell(info_table, 2, 12, str.tostring(kc_position, '0.00'), text_color=color.olive, text_size=table_text_size)

// Key Volume Indicators

table.cell(info_table, 0, 13, 'VOLUME', text_color=color.blue, text_size=table_text_size, bgcolor=color.new(color.blue, 90))

table.cell(info_table, 1, 13, 'Volume ROC', text_color=color.blue, text_size=table_text_size)

table.cell(info_table, 2, 13, str.tostring(vroc, '0.00'), text_color=color.blue, text_size=table_text_size)

table.cell(info_table, 0, 14, '', text_color=color.red, text_size=table_text_size)

table.cell(info_table, 1, 14, 'EOM', text_color=color.red, text_size=table_text_size)

table.cell(info_table, 2, 14, str.tostring(eom_sma, '0.000'), text_color=color.red, text_size=table_text_size)

// Key Oscillators

table.cell(info_table, 0, 15, 'OSCILLATORS', text_color=color.purple, text_size=table_text_size, bgcolor=color.new(color.purple, 90))

table.cell(info_table, 1, 15, 'Awesome Osc', text_color=color.blue, text_size=table_text_size)

table.cell(info_table, 2, 15, str.tostring(ao, '0.000'), text_color=color.blue, text_size=table_text_size)

table.cell(info_table, 0, 16, '', text_color=color.red, text_size=table_text_size)

table.cell(info_table, 1, 16, 'Fisher Transform', text_color=color.red, text_size=table_text_size)

table.cell(info_table, 2, 16, str.tostring(fisher, '0.000'), text_color=color.red, text_size=table_text_size)

// Summary Statistics

table.cell(info_table, 0, 17, 'SUMMARY', text_color=color.black, text_size=table_text_size, bgcolor=color.new(color.gray, 70))

table.cell(info_table, 1, 17, 'Total Indicators: 52', text_color=color.black, text_size=table_text_size)

regime_color = rsi_centered > 10 ? color.green : rsi_centered < -10 ? color.red : color.gray

regime_text = rsi_centered > 10 ? "BULLISH" : rsi_centered < -10 ? "BEARISH" : "NEUTRAL"

table.cell(info_table, 2, 17, regime_text, text_color=regime_color, text_size=table_text_size)

This makes it the perfect “indicator backbone” for quantitative and systematic traders who want to prototype, combine, and test new regime detection models—especially in combination with the Markov Chain indicator.

How to use this script with the Markov Chain for research and backtesting:

Add the Enhanced Indicator Export to your chart.

Every calculated indicator is available as an individual data stream.

Connect the indicator(s) you want as custom input(s) to the Markov Chain’s “Custom Indicators” option.

In the Markov Chain indicator’s settings, turn ON the custom indicator mode.

For each of the three custom indicator inputs, select the exported plot from the Enhanced Export script—the menu lists all 45+ signals by name.

This creates a powerful, modular regime-detection engine where you can mix-and-match momentum, trend, volume, or custom combinations for advanced filtering.

Backtest regime logic directly.

Once you’ve connected your chosen indicators, the Markov Chain script performs regime detection (Bull/Neutral/Bear) based on your selected features—not just price returns.

The regime detection is robust, automatically normalized (using Z-score), and outputs bias (1, -1, 0) for plug-and-play integration.

Export the regime bias for programmatic use.

As described above, use input.source() in your Pine Script strategy or system and link the bias output.

You can now filter signals, control trade direction/size, or design pairs-trading that respect true, indicator-driven market regimes.

With this framework, you’re not limited to static or simplistic regime filters. You can rigorously define, test, and refine what “market regime” means for your strategies—using the technical features that matter most to you.

Optimize your signal generation by backtesting across a universe of meaningful indicator blends.

Enhance risk management with objective, real-time regime boundaries.

Accelerate your research: iterate quickly, swap indicator components, and see results with minimal code changes.

Automate multi-asset or pairs-trading by integrating regime context directly into strategy logic.

Add both scripts to your chart, connect your preferred features, and start investigating your best regime-based trades—entirely within the TradingView ecosystem.

References & Further Reading

Ang, A., & Bekaert, G. (2002). “Regime Switches in Interest Rates.” Journal of Business & Economic Statistics, 20(2), 163–182.

Hamilton, J. D. (1989). “A New Approach to the Economic Analysis of Nonstationary Time Series and the Business Cycle.” Econometrica, 57(2), 357–384.

Markov, A. A. (1906). "Extension of the Limit Theorems of Probability Theory to a Sum of Variables Connected in a Chain." The Notes of the Imperial Academy of Sciences of St. Petersburg.

Guidolin, M., & Timmermann, A. (2007). “Asset Allocation under Multivariate Regime Switching.” Journal of Economic Dynamics and Control, 31(11), 3503–3544.

Murphy, J. J. (1999). Technical Analysis of the Financial Markets. New York Institute of Finance.

Brock, W., Lakonishok, J., & LeBaron, B. (1992). “Simple Technical Trading Rules and the Stochastic Properties of Stock Returns.” Journal of Finance, 47(5), 1731–1764.

Zucchini, W., MacDonald, I. L., & Langrock, R. (2017). Hidden Markov Models for Time Series: An Introduction Using R (2nd ed.). Chapman and Hall/CRC.

On Quantitative Finance and Markov Models:

Lo, A. W., & Hasanhodzic, J. (2009). The Heretics of Finance: Conversations with Leading Practitioners of Technical Analysis. Bloomberg Press.

Patterson, S. (2016). The Man Who Solved the Market: How Jim Simons Launched the Quant Revolution. Penguin Press.

TradingView Pine Script Documentation: www.tradingview.com

TradingView Blog: “Use an Input From Another Indicator With Your Strategy” www.tradingview.com

GeeksforGeeks: “What is the Difference Between Markov Chains and Hidden Markov Models?” www.geeksforgeeks.org

What makes this indicator original and unique?

- On‑chart, real‑time Markov. The chain is drawn directly on your chart. You see the current regime, its tendency to stay (self‑loop), and the usual next step (arrows) as bars confirm.

- Source‑agnostic by design. The engine runs on any series you select via input.source() — price, your own oscillator, a composite score, anything you compute in the script.

- Automatic normalization + regime mapping. Different inputs live on different scales. The script standardizes your chosen source and maps it into clear regimes (e.g., Bull / Bear / Neutral) without you micromanaging thresholds each time.

- Rolling, bar‑by‑bar learning. Transition tendencies are computed from a rolling window of confirmed bars. What you see is exactly what the market did in that window.

- Fast experimentation. Switch the source, adjust the window, and the Markov view updates instantly. It’s a rapid way to test ideas and feel regime persistence/switch behavior.

Integrate your own signals (using input.source())

- In settings, choose the Source . This is powered by input.source() .

- Feed it price, an indicator you compute inside the script, or a custom composite series.

- The script will automatically normalize that series and process it through the Markov engine, mapping it to regimes and updating the on‑chart spheres/arrows in real time.

Credits:

Deep gratitude to @RicardoSantos for both the foundational Markov chain processing engine and inspiring open-source contributions, which made advanced probabilistic market modeling accessible to the TradingView community.

Special thanks to @Alien_Algorithms for the innovative and visually stunning 3D sphere logic that powers the indicator’s animated, regime-based visualization.

Disclaimer

This tool summarizes recent behavior. It is not financial advice and not a guarantee of future results.

Rifle UnifiedThis script is designed for use on 30-second charts of Dow Jones-related symbols (YM, MYM, US30). It provides automated buy and sell signals using a combination of price action, RSI (Relative Strength Index), and volume analysis. The script is intended for both live trading signals and backtesting, with configurable risk management and debugging features.

Core Functionality

1. Signal Generation Logic

Trigger: The algorithm looks for a sharp price move (drop or rise) of a user-defined threshold (default: 80 points) within a specified lookback window (default: 20 minutes).

Levels: It monitors for price drops below specific numerical levels ending in 23, 43, or 73 (e.g., 42223, 42273).

RSI Condition: When price falls below one of these levels and the RSI is below 30, the setup is considered active.

Buy Signal: A buy is triggered if, after setup:

Price rises back above the level,

The RSI rate of change (ROC) indicates exhaustion of the drop,

The current bar shows positive momentum.

2. Trade Management

Stop Loss & Take Profit: Configurable fixed or trailing stop loss and take profit levels are plotted and managed automatically.

Exit Signals: The script signals exit based on price action relative to these risk management levels.

3. Filters & Enhancements

Parabolic Move Filter: Prevents entries during extreme price moves.

Dead Cat Bounce Filter: Avoids false signals after sharp reversals.

Volume Filter: Optionally requires volume conditions for trade entries (especially for shorts).

Multiple Confirmation Layers : Includes checks for 5-minute RSI, momentum, and price retracement.

User Inputs & Customization

Trade Direction: Toggle between LONG and SHORT signal generation.

Trigger Settings: Adjust thresholds for price moves, lookback windows, RSI ROC, and volume requirements.

Trade Settings: Set take profit, stop loss, and trailing stop behavior.

Debug & Visualization: Enable or disable various plots, labels, and debug tables for in-depth analysis.

Backtesting: Integrated backtester with summary and detailed statistics tables.

Technical Features

Uses External Libraries: Relies on RifleShooterLib for core logic and BackTestLib for backtesting and statistics.

Multi-timeframe Analysis: Incorporates both 30-second and 5-minute RSI calculations.

Chart Annotations: Plots entry/exit points, risk levels, and debug information directly on the chart.

Alert Conditions: Built-in alert triggers for key events (initial move, stall, entry).

Intended Use

Markets: Dow Jones symbols (YM, MYM, US30, or US30 CFD).

Timeframe: 30-second chart.

Purpose: Automated signal generation for discretionary or algorithmic trading, with robust risk management and backtesting support.

Notable Customization & Extension Points

Momentum Calculation: Plans to replace the current momentum measure with "sqz momentum".

Displacement Logic: Future update to use "FVG concept" for displacement.

High-Contrast RSI: Optional visual enhancements for RSI extremes.

Time-based Stop: Consideration for adding a time-based stop mechanism.

This script is highly modular, with extensive user controls, and is suitable for both live trading and historical analysis of Dow Jones index movements

Market Regime# MARKET REGIME IDENTIFICATION & TRADING SYSTEM

## Complete User Guide

---

## 📋 TABLE OF CONTENTS

1. (#overview)

2. (#regimes)

3. (#indicator-usage)

4. (#entry-signals)

5. (#exit-signals)

6. (#regime-strategies)

7. (#confluence)

8. (#backtesting)

9. (#optimization)

10. (#examples)

---

## OVERVIEW

### What This System Does

This is a **complete market regime identification and trading system** that:

1. **Identifies 6 distinct market regimes** automatically

2. **Adapts trading tactics** to each regime

3. **Provides high-probability entry signals** with confluence scoring

4. **Shows optimal exit points** for each trade

5. **Can be backtested** to validate performance

### Two Components Provided

1. **Indicator** (`market_regime_indicator.pine`)

- Visual regime identification

- Entry/exit signals on chart

- Dynamic support/resistance

- Info tables with live data

- Use for manual trading

2. **Strategy** (`market_regime_strategy.pine`)

- Fully automated backtestable version

- Same logic as indicator

- Position sizing and risk management

- Performance metrics

- Use for backtesting and automation

---

## THE 6 MARKET REGIMES

### 1. 🟢 BULL TRENDING

**Characteristics:**

- Strong uptrend

- Price above SMA50 and SMA200

- ADX > 25 (strong trend)

- Higher highs and higher lows

- DI+ > DI- (bullish momentum)

**What It Means:**

- Market has clear upward direction

- Buyers in control

- Pullbacks are buying opportunities

- Strongest regime for long positions

**How to Trade:**

- ✅ **BUY dips to EMA20 or SMA20**

- ✅ Enter when RSI < 60 on pullback

- ✅ Hold through minor corrections

- ❌ Don't short against the trend

- ❌ Don't sell too early

**Expected Behavior:**

- Pullbacks are shallow (5-10%)

- Bounces are strong

- Support at moving averages holds

- Volume increases on rallies

---

### 2. 🔴 BEAR TRENDING

**Characteristics:**

- Strong downtrend

- Price below SMA50 and SMA200

- ADX > 25 (strong trend)

- Lower highs and lower lows

- DI- > DI+ (bearish momentum)

**What It Means:**

- Market has clear downward direction

- Sellers in control

- Rallies are selling opportunities

- Strongest regime for short positions

**How to Trade:**

- ✅ **SELL rallies to EMA20 or SMA20**

- ✅ Enter when RSI > 40 on bounce

- ✅ Hold through minor bounces

- ❌ Don't buy against the trend

- ❌ Don't cover shorts too early

**Expected Behavior:**

- Rallies are weak (5-10%)

- Selloffs are strong

- Resistance at moving averages holds

- Volume increases on declines

---

### 3. 🔵 BULL RANGING

**Characteristics:**

- Bullish bias but consolidating

- Price near or above SMA50

- ADX < 20 (weak trend)

- Trading in range

- Choppy price action

**What It Means:**

- Uptrend is pausing

- Accumulation phase

- Support and resistance zones clear

- Lower volatility

**How to Trade:**

- ✅ **BUY at support zone**

- ✅ Enter when RSI < 40

- ✅ Take profits at resistance

- ⚠️ Smaller position sizes

- ⚠️ Tighter stops

**Expected Behavior:**

- Range-bound oscillations

- Support bounces repeatedly

- Resistance rejections common

- Eventually breaks higher (usually)

---

### 4. 🟠 BEAR RANGING

**Characteristics:**

- Bearish bias but consolidating

- Price near or below SMA50

- ADX < 20 (weak trend)

- Trading in range

- Choppy price action

**What It Means:**

- Downtrend is pausing

- Distribution phase

- Support and resistance zones clear

- Lower volatility

**How to Trade:**

- ✅ **SELL at resistance zone**

- ✅ Enter when RSI > 60

- ✅ Take profits at support

- ⚠️ Smaller position sizes

- ⚠️ Tighter stops

**Expected Behavior:**

- Range-bound oscillations

- Resistance holds repeatedly

- Support bounces are weak

- Eventually breaks lower (usually)

---

### 5. ⚪ CONSOLIDATION

**Characteristics:**

- No clear direction

- Range compression

- Very low ADX (< 15 often)

- Price inside tight range

- Neutral sentiment

**What It Means:**

- Market is coiling

- Building energy for next move

- Indecision between buyers/sellers

- Calm before the storm

**How to Trade:**

- ✅ **WAIT for breakout direction**

- ✅ Enter on high-volume breakout

- ✅ Direction becomes clear

- ❌ Don't trade inside the range

- ❌ Avoid choppy scalping

**Expected Behavior:**

- Narrow range

- Low volume

- False breakouts possible

- Explosive move when it breaks

---

### 6. 🟣 CHAOS (High Volatility)

**Characteristics:**

- Extreme volatility

- No clear direction

- Erratic price swings

- ATR > 2x average

- Unpredictable

**What It Means:**

- Market panic or euphoria

- News-driven moves

- Emotion dominates logic

- Highest risk environment

**How to Trade:**

- ❌ **STAY OUT!**

- ❌ No positions

- ❌ Wait for stability

- ✅ Protect existing positions

- ✅ Reduce risk

**Expected Behavior:**

- Large intraday swings

- Gaps up/down

- Stop hunts

- Whipsaws

- Eventually calms down

---

## INDICATOR USAGE

### Visual Elements

#### 1. Background Colors

- **Light Green** = Bull Trending (go long)

- **Light Red** = Bear Trending (go short)

- **Light Teal** = Bull Ranging (buy dips)

- **Light Orange** = Bear Ranging (sell rallies)

- **Light Gray** = Consolidation (wait)

- **Purple** = Chaos (stay out!)

#### 2. Regime Labels

- Appear when regime changes

- Show new regime name

- Positioned at highs (bullish) or lows (bearish)

#### 3. Entry Signals

- **Green "LONG"** labels = Buy here

- **Red "SHORT"** labels = Sell here

- Number shows confluence score (X/5 signals)

- Hover for details (stop, target, RSI, etc.)

#### 4. Exit Signals

- **Orange "EXIT LONG"** = Close long position

- **Orange "EXIT SHORT"** = Close short position

- Shows exit reason in tooltip

#### 5. Support/Resistance Lines

- **Green line** = Dynamic support (buy zone)

- **Red line** = Dynamic resistance (sell zone)

- Adapts to regime automatically

#### 6. Moving Averages

- **Blue** = SMA 20 (short-term trend)

- **Orange** = SMA 50 (medium-term trend)

- **Purple** = SMA 200 (long-term trend)

### Information Tables

#### Top Right Table (Main Info)

Shows real-time market conditions:

- **Current Regime** - What regime we're in

- **Bias** - Long, Short, Breakout, or Stay Out

- **ADX** - Trend strength (>25 = strong)

- **Trend** - Strong, Moderate, or Weak

- **Volatility** - High or Normal