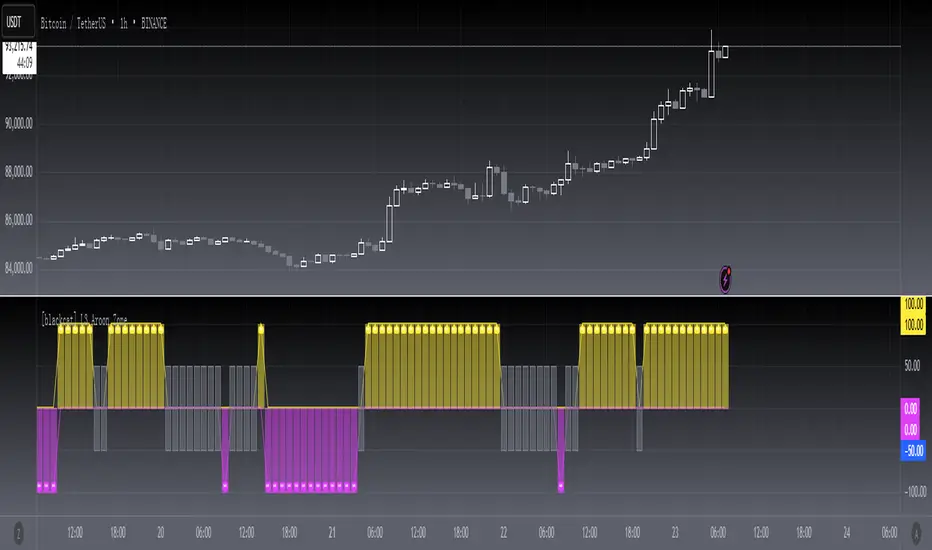

[blackcat] L3 Aroon ZoneLevel 3

Background

The Aroon indicator developed by Tushar Chanand indicates whether there is a trend price or is located in a trading area.

Function

Classical Aroon can also show the beginning of a new trend, its strength and expectation of changes from trade areas to trends. However, it produces too much noise when is bull or bear during sideways. In this improved version, I use bars without "blur cross" to classify bull, bear and sideways, which could look better to know the status of current market.

Since Chinese uses red for bull, green for bear, while others use green for bull and red for bear, i try to avoid to use red or green, which may be confusing. I use my style of color for bull and bear:

Yellow --> Bull

Fuchsia --> Bear

Gray --> Sideways

Remarks

Feedbacks are appreciated.

"aroon" için komut dosyalarını ara

Harmonic Trend Fusion [kikfraben]📈 Harmonic Trend Fusion - Your Personal Trading Assistant

This versatile tool combines multiple indicators to provide a holistic view of market trends and potential signals.

🚀 Key Features:

Multi-Indicator Synergy: Benefit from the combined insights of Aroon, DMI, MACD, Parabolic SAR, RSI, Supertrend, and SMI Ergodic Oscillator, all in one powerful indicator.

Customizable Plot Options: Tailor your chart by choosing which signals to visualize. Whether you're interested in trendlines, histograms, or specific indicators, the choice is yours.

Color-Coded Trends: Quickly identify bullish and bearish trends with the color-coded visualizations. Stay ahead of market movements with clear and intuitive signals.

Table Display: Stay informed at a glance with the interactive table. It dynamically updates to reflect the current market sentiment, providing you with key information and trend direction.

Precision Control: Fine-tune your analysis with precision control over indicator parameters. Adjust lengths, colors, and other settings to align with your unique trading strategy.

🛠️ How to Use:

Customize Your View: Select which indicators to display and adjust plot options to suit your preferences.

Table Insights: Monitor the dynamic table for real-time updates on market sentiment and trend direction.

Indicator Parameters: Experiment with different lengths and settings to find the combination that aligns with your trading style.

Whether you're a seasoned trader or just starting, Harmonic Trend Fusion equips you with the tools you need to navigate the markets confidently. Take control of your trading journey and enhance your decision-making process with this comprehensive trading assistant.

5 in 1 (rsi,aroon,stoch,macd,adx di)5 indicators in 1.

You can choose wich one you want to see (rsi ,aroon,macd,stoch or adx di)

Usefull to save space for other indicators

Aroon+Williams+MA2+ADX+Aroon Str.Inspired by the Watchbot strategy which makes about +60% profit in two months.

cafe.naver.com

This is customized to "EOSUSDT, 15 min, Binance" as a default.

I want to add the function for avoiding the recurrence of the trading for 24 ticks(period), but don't know how to yet.

SExI - Super Exhaustion Indicator [Da_Prof]As we know, the RSI can remain at "overbought" or "oversold" levels for long periods of time while the price continues in that direction. The SExI (Super Exhaustion Indicator) is an indicator designed to help detect exhaustion of strong moves.

The SExI is a combination of the RSI and "upper" Aroon. For the indicator to trigger, the RSI has to be above or below a top/bottom trigger line when the Aroon has had a set number of drives up or down correspondingly. An Aroon top drive is defined as the Aroon hitting 100% on the current candle when the previous candle was below 100%. An Aroon bottom drive is defined as the Aroon hitting 0% on the current candle when the previous candle was above 0%. Consecutive top or bottom drives are counted and exhaustion triggers when these drives hit a setpoint (default is 5 drives = the Aroon exhaustion trigger). When Aroon exhaustion is triggered and the RSI is correspondingly above/below a trigger line, the overall indicator signals exhaustion. There are two lines for bottoms and tops, one each for a "normal" trigger and and an "extreme" trigger.

The Aroon drives are visualized at the top and bottom of the indicator. The RSI is plotted as a line that crosses top and bottom trigger lines. There are extreme trigger values for both the bottom and top exhaustion triggers.

--Da_Prof

Indicators Combination Framework v3 IND [DTU]Hello All,

This script is a framework to analyze and see the results by combine selected indicators for (long, short, longexit, shortexit) conditions.

I was designed this for beginners and users to facilitate to see effects of the technical indicators combinations on the chart WITH NO CODE

You can improve your strategies according the results of this system by connecting the framework to a strategy framework/template such as Pinecoder, Benson, daveatt or custom.

This is enhanced version of my previous indicator "Indicators & Conditions Test Framework "

Currently there are 93 indicators (23 newly added) connected over library. You can also import an External Indicator or add Custom indicator (In the source)

It is possible to change it from Indicator to strategy (simple one) by just remarking strategy parts in the source code and see real time profit of your combinations

Feel free to change or use it in your source

Special thanks goes to Pine wizards: Trading view (built-in Indicators), @Rodrigo, @midtownsk8rguy, @Lazybear, @Daveatt and others for their open source codes and contributions

SIMPLE USAGE

1. SETTING: Show Alerts= True (To see your entries and Exists)

2. Define your Indicators (ex: INDICATOR1: ema(close,14), INDICATOR2: ema(close,21), INDICATOR3: ema(close,200)

3. Define Your Combinations for long & Short Conditions

a. For Long: (INDICATOR1 crossover INDICATOR2) AND (INDICATOR3 < close)

b. For Short: (INDICATOR1 crossunder INDICATOR2) AND (INDICATOR3 > close)

4. Select Strategy/template (Import strategy to chart) that you export your signals from the list

5. Analyze the best profit by changing Indicators values

SOME INDICATORS DETAILS

Each Indicator includes:

- Factorization : Converting the selected indicator to Double, triple Quadruple such as EMA to DEMA, TEMA QEMA

- Log : Simple or log10 can be used for calculation on function entries

- Plot Type : You can overlay the indicator on the chart (such ema) or you can use stochastic/Percentrank approach to display in the variable hlines range

- Extended Parametes : You can use default parameters or you can use extended (P1,P2) parameters regarding to indicator type and your choice

- Color : You can define indicator color and line properties

- Smooth : you can enable swma smooth

- indicators : you can select one of the 93 function like ema(),rsi().. to define your indicator

- Source : you can select from already defined indicators (IND1-4), External Indicator (EXT), Custom Indicator (CUST), and other sources (close, open...)

CONDITION DETAILS

- There are are 4 type of conditions, long entry, short entry, long exit, short exit.

- Each condition are built up from 4 combinations that joined with "AND" & "OR" operators

- You can see the results by enabling show alerts check box

- If you only wants to enter long entry and long exit, just fill these conditions

- If "close on opposite" checkbox selected on settings, long entry will be closed on short entry and vice versa

COMBINATIONS DETAILS

- There are 4 combinations that joined with "AND" & "OR" operators for each condition

- combinations are built up from compare 1st entry with 2nd one by using operator

- 1st and 2nd entries includes already defined indicators (IND1-5), External Indicator (EXT), Custom Indicator (CUST), and other sources (close, open...)

- Operators are comparison values such as >,<, crossover,...

- 2nd entry include "VALUE" parameter that will use to compare 1st indicator with value area

- If 2nd indicator selected different than "VALUE", value are will mean previous value of the selection. (ex: value area= 2, 2nd entry=close, means close )

- Selecting "NONE" for the 1st entry will disable calculation of current and following combinations

JOINS DETAILS

- Each combination will join wiht the following one with the JOIN (AND, OR) operator (if the following one is not equal "NONE")

CUSTOM INDICATOR

- Custom Indicator defines harcoded in the source code.

- You can call it with "CUST" in the Indicator definition source or combination entries source

- You can change or implement your custom indicator by updating the source code

EXTERNAL INDICATOR

- You can import an external indicator by selecting it from the ext source.

- External Indicator should be already imported to the chart and it have an plot function to output its signal

EXPORTING SIGNAL

- You can export your result to an already defined strategy template such as Pine coders, Benson, Daveatt Strategy templates

- Or you can define your custom export for other future strategy templates

ALERTS

- By enabling show alerts checkbox, you can see long entry exits on the bottom, and short entry exits aon the top of the chart

ADDITIONAL INFO

- You can see all off the inputs descriptions in the tooltips. (You can also see the previous version for details)

- Availability to set start, end dates

- Minimize repainting by using security function options (Secure, Semi Secure, Repaint)

- Availability of use timeframes

-

Version 3 INDICATORS LIST (More to be added):

▼▼▼ OVERLAY INDICATORS ▼▼▼

alma(src,len,offset=0.85,sigma=6).-------Arnaud Legoux Moving Average

ama(src,len,fast=14,slow=100).-----------Adjusted Moving Average

accdist().-------------------------------Accumulation/distribution index.

cma(src,len).----------------------------Corrective Moving average

dema(src,len).---------------------------Double EMA (Same as EMA with 2 factor)

ema(src,len).----------------------------Exponential Moving Average

gmma(src,len).---------------------------Geometric Mean Moving Average

highest(src,len).------------------------Highest value for a given number of bars back.

hl2ma(src,len).--------------------------higest lowest moving average

hma(src,len).----------------------------Hull Moving Average.

lagAdapt(src,len,perclen=5,fperc=50).----Ehlers Adaptive Laguerre filter

lagAdaptV(src,len,perclen=5,fperc=50).---Ehlers Adaptive Laguerre filter variation

laguerre(src,len).-----------------------Ehlers Laguerre filter

lesrcp(src,len).-------------------------lowest exponential esrcpanding moving line

lexp(src,len).---------------------------lowest exponential expanding moving line

linreg(src,len,loffset=1).---------------Linear regression

lowest(src,len).-------------------------Lovest value for a given number of bars back.

mcginley(src, len.-----------------------McGinley Dynamic adjusts for market speed shifts, which sets it apart from other moving averages, in addition to providing clear moving average lines

percntl(src,len).------------------------percentile nearest rank. Calculates percentile using method of Nearest Rank.

percntli(src,len).-----------------------percentile linear interpolation. Calculates percentile using method of linear interpolation between the two nearest ranks.

previous(src,len).-----------------------Previous n (len) value of the source

pivothigh(src,BarsLeft=len,BarsRight=2).-Previous pivot high. src=src, BarsLeft=len, BarsRight=p1=2

pivotlow(src,BarsLeft=len,BarsRight=2).--Previous pivot low. src=src, BarsLeft=len, BarsRight=p1=2

rema(src,len).---------------------------Range EMA (REMA)

rma(src,len).----------------------------Moving average used in RSI. It is the exponentially weighted moving average with alpha = 1 / length.

sar(start=len, inc=0.02, max=0.02).------Parabolic SAR (parabolic stop and reverse) is a method to find potential reversals in the market price direction of traded goods.start=len, inc=p1, max=p2. ex: sar(0.02, 0.02, 0.02)

sma(src,len).----------------------------Smoothed Moving Average

smma(src,len).---------------------------Smoothed Moving Average

super2(src,len).-------------------------Ehlers super smoother, 2 pole

super3(src,len).-------------------------Ehlers super smoother, 3 pole

supertrend(src,len,period=3).------------Supertrend indicator

swma(src,len).---------------------------Sine-Weighted Moving Average

tema(src,len).---------------------------Triple EMA (Same as EMA with 3 factor)

tma(src,len).----------------------------Triangular Moving Average

vida(src,len).---------------------------Variable Index Dynamic Average

vwma(src,len).---------------------------Volume Weigted Moving Average

volstop(src,len,atrfactor=2).------------Volatility Stop is a technical indicator that is used by traders to help place effective stop-losses. atrfactor=p1

wma(src,len).----------------------------Weigted Moving Average

vwap(src_).------------------------------Volume Weighted Average Price (VWAP) is used to measure the average price weighted by volume

▼▼▼ NON OVERLAY INDICATORS ▼▼

adx(dilen=len, adxlen=14, adxtype=0).----adx. The Average Directional Index (ADX) is a used to determine the strength of a trend. len=>dilen, p1=adxlen (default=14), p2=adxtype 0:ADX, 1:+DI, 2:-DI (def:0)

angle(src,len).--------------------------angle of the series (Use its Input as another indicator output)

aroon(len,dir=0).------------------------aroon indicator. Aroons major function is to identify new trends as they happen.p1 = dir: 0=mid (default), 1=upper, 2=lower

atr(src,len).----------------------------average true range. RMA of true range.

awesome(fast=len=5,slow=34,type=0).------Awesome Oscilator is an indicator used to measure market momentum. defaults : fast=len= 5, p1=slow=34, p2=type: 0=Awesome, 1=difference

bbr(src,len,mult=1).---------------------bollinger %%

bbw(src,len,mult=2).---------------------Bollinger Bands Width. The Bollinger Band Width is the difference between the upper and the lower Bollinger Bands divided by the middle band.

cci(src,len).----------------------------commodity channel index

cctbbo(src,len).-------------------------CCT Bollinger Band Oscilator

change(src,len).-------------------------A.K.A. Momentum. Difference between current value and previous, source - source . is most commonly referred to as a rate and measures the acceleration of the price and/or volume of a security

cmf(len=20).-----------------------------Chaikin Money Flow Indicator used to measure Money Flow Volume over a set period of time. Default use is len=20

cmo(src,len).----------------------------Chande Momentum Oscillator. Calculates the difference between the sum of recent gains and the sum of recent losses and then divides the result by the sum of all price movement over the same period.

cog(src,len).----------------------------The cog (center of gravity) is an indicator based on statistics and the Fibonacci golden ratio.

copcurve(src,len).-----------------------Coppock Curve. was originally developed by Edwin Sedge Coppock (Barrons Magazine, October 1962).

correl(src,len).-------------------------Correlation coefficient. Describes the degree to which two series tend to deviate from their ta.sma values.

count(src,len).--------------------------green avg - red avg

cti(src,len).----------------------------Ehler s Correlation Trend Indicator by

dev(src,len).----------------------------ta.dev() Measure of difference between the series and its ta.sma

dpo(len).--------------------------------Detrended Price OScilator is used to remove trend from price.

efi(len).--------------------------------Elders Force Index (EFI) measures the power behind a price movement using price and volume.

eom(len=14,div=10000).-------------------Ease of Movement.It is designed to measure the relationship between price and volume.p1 = div: 10000= (default)

falling(src,len).------------------------ta.falling() Test if the `source` series is now falling for `length` bars long. (Use its Input as another indicator output)

fisher(len).-----------------------------Fisher Transform is a technical indicator that converts price to Gaussian normal distribution and signals when prices move significantly by referencing recent price data

histvol(len).----------------------------Historical volatility is a statistical measure used to analyze the general dispersion of security or market index returns for a specified period of time.

kcr(src,len,mult=2).---------------------Keltner Channels Range

kcw(src,len,mult=2).---------------------ta.kcw(). Keltner Channels Width. The Keltner Channels Width is the difference between the upper and the lower Keltner Channels divided by the middle channel.

klinger(type=len).-----------------------Klinger oscillator aims to identify money flow’s long-term trend. type=len: 0:Oscilator 1:signal

macd(src,len).---------------------------MACD (Moving Average Convergence/Divergence)

mfi(src,len).----------------------------Money Flow Index s a tool used for measuring buying and selling pressure

msi(len=10).-----------------------------Mass Index (def=10) is used to examine the differences between high and low stock prices over a specific period of time

nvi().-----------------------------------Negative Volume Index

obv().-----------------------------------On Balance Volume

pvi().-----------------------------------Positive Volume Index

pvt().-----------------------------------Price Volume Trend

ranges(src,upper=len, lower=-5).---------ranges of the source. src=src, upper=len, v1:lower=upper . returns: -1 source=upper otherwise 0

rising(src,len).-------------------------ta.rising() Test if the `source` series is now rising for `length` bars long. (Use its Input as another indicator output)

roc(src,len).----------------------------Rate of Change

rsi(src,len).----------------------------Relative strength Index

rvi(src,len).----------------------------The Relative Volatility Index (RVI) is calculated much like the RSI, although it uses high and low price standard deviation instead of the RSI’s method of absolute change in price.

smi_osc(src,len,fast=5, slow=34).--------smi Oscillator

smi_sig(src,len,fast=5, slow=34).--------smi Signal

stc(src,len,fast=23,slow=50).------------Schaff Trend Cycle (STC) detects up and down trends long before the MACD. Code imported from

stdev(src,len).--------------------------Standart deviation

trix(src,len) .--------------------------the rate of change of a triple exponentially smoothed moving average.

tsi(src,len).----------------------------The True Strength Index indicator is a momentum oscillator designed to detect, confirm or visualize the strength of a trend.

ultimateOsc(len.-------------------------Ultimate Oscillator indicator (UO) indicator is a technical analysis tool used to measure momentum across three varying timeframes

variance(src,len).-----------------------ta.variance(). Variance is the expectation of the squared deviation of a series from its mean (ta.sma), and it informally measures how far a set of numbers are spread out from their mean.

willprc(src,len).------------------------Williams %R

wad().-----------------------------------Williams Accumulation/Distribution.

wvad().----------------------------------Williams Variable Accumulation/Distribution.

HISTORY

v3.01

ADD: 23 new indicators added to indicators list from the library. Current Total number of Indicators are 93. (to be continued to adding)

ADD: 2 more Parameters (P1,P2) for indicator calculation added. Par:(Use Defaults) uses only indicator(Source, Length) with library's default parameters. Par:(Use Extra Parameters P1,P2) use indicator(Source,Length,p1,p2) with additional parameters if indicator needs.

ADD: log calculation (simple, log10) option added on indicator function entries

ADD: New Output Signals added for compatibility on exporting condition signals to different Strategy templates.

ADD: Alerts Added according to conditions results

UPD: Indicator source inputs now display with indicators descriptions

UPD: Most off the source code rearranged and some functions moved to the new library. Now system work like a little bit frontend/backend

UPD: Performance improvement made on factorization and other source code

UPD: Input GUI rearranged

UPD: Tooltips corrected

REM: Extended indicators removed

UPD: IND1-IND4 added to indicator data source. Now it is possible to create new indicators with the previously defined indicators value. ex: IND1=ema(close,14) and IND2=rsi(IND1,20) means IND2=rsi(ema(close,14),20)

UPD: Custom Indicator (CUST) added to indicator data source and Combination Indicator source.

UPD: Volume added to indicator data source and Combination Indicator source.

REM: Custom indicators removed and only one custom indicator left

REM: Plot Type "Org. Range (-1,1)" removed

UPD: angle, rising, falling type operators moved to indicator library

pandas_taLibrary "pandas_ta"

Level: 3

Background

Today is the first day of 2022 and happy new year every tradingviewers! May health and wealth go along with you all the time. I use this chance to publish my 1st PINE v5 lib : pandas_ta

This is not a piece of cake like thing, which cost me a lot of time and efforts to build this lib. Beyond 300 versions of this script was iterated in draft.

Function

Library "pandas_ta"

PINE v5 Counterpart of Pandas TA - A Technical Analysis Library in Python 3 at github.com

The Original Pandas Technical Analysis (Pandas TA) is an easy to use library that leverages the Pandas package with more than 130 Indicators and Utility functions and more than 60 TA Lib Candlestick Patterns.

I realized most of indicators except Candlestick Patterns because tradingview built-in Candlestick Patterns are even more powerful!

I use this to verify pandas_ta python version indicators for myself, but I realize that maybe many may need similar lib for pine v5 as well.

Function Brief Descriptions (Pls find details in script comments)

bton --> Binary to number

wcp --> Weighted Closing Price (WCP)

counter --> Condition counter

xbt --> Between

ebsw --> Even Better SineWave (EBSW)

ao --> Awesome Oscillator (AO)

apo --> Absolute Price Oscillator (APO)

xrf --> Dynamic shifted values

bias --> Bias (BIAS)

bop --> Balance of Power (BOP)

brar --> BRAR (BRAR)

cci --> Commodity Channel Index (CCI)

cfo --> Chande Forcast Oscillator (CFO)

cg --> Center of Gravity (CG)

cmo --> Chande Momentum Oscillator (CMO)

coppock --> Coppock Curve (COPC)

cti --> Correlation Trend Indicator (CTI)

dmi --> Directional Movement Index(DMI)

er --> Efficiency Ratio (ER)

eri --> Elder Ray Index (ERI)

fisher --> Fisher Transform (FISHT)

inertia --> Inertia (INERTIA)

kdj --> KDJ (KDJ)

kst --> 'Know Sure Thing' (KST)

macd --> Moving Average Convergence Divergence (MACD)

mom --> Momentum (MOM)

pgo --> Pretty Good Oscillator (PGO)

ppo --> Percentage Price Oscillator (PPO)

psl --> Psychological Line (PSL)

pvo --> Percentage Volume Oscillator (PVO)

qqe --> Quantitative Qualitative Estimation (QQE)

roc --> Rate of Change (ROC)

rsi --> Relative Strength Index (RSI)

rsx --> Relative Strength Xtra (rsx)

rvgi --> Relative Vigor Index (RVGI)

slope --> Slope

smi --> SMI Ergodic Indicator (SMI)

sqz* --> Squeeze (SQZ) * NOTE: code sufferred from very strange error, code was commented.

sqz_pro --> Squeeze PRO(SQZPRO)

xfl --> Condition filter

stc --> Schaff Trend Cycle (STC)

stoch --> Stochastic (STOCH)

stochrsi --> Stochastic RSI (STOCH RSI)

trix --> Trix (TRIX)

tsi --> True Strength Index (TSI)

uo --> Ultimate Oscillator (UO)

willr --> William's Percent R (WILLR)

alma --> Arnaud Legoux Moving Average (ALMA)

xll --> Dynamic rolling lowest values

dema --> Double Exponential Moving Average (DEMA)

ema --> Exponential Moving Average (EMA)

fwma --> Fibonacci's Weighted Moving Average (FWMA)

hilo --> Gann HiLo Activator(HiLo)

hma --> Hull Moving Average (HMA)

hwma --> HWMA (Holt-Winter Moving Average)

ichimoku --> Ichimoku Kinkō Hyō (ichimoku)

jma --> Jurik Moving Average Average (JMA)

kama --> Kaufman's Adaptive Moving Average (KAMA)

linreg --> Linear Regression Moving Average (linreg)

mgcd --> McGinley Dynamic Indicator

rma --> wildeR's Moving Average (RMA)

sinwma --> Sine Weighted Moving Average (SWMA)

ssf --> Ehler's Super Smoother Filter (SSF) © 2013

supertrend --> Supertrend (supertrend)

xsa --> X simple moving average

swma --> Symmetric Weighted Moving Average (SWMA)

t3 --> Tim Tillson's T3 Moving Average (T3)

tema --> Triple Exponential Moving Average (TEMA)

trima --> Triangular Moving Average (TRIMA)

vidya --> Variable Index Dynamic Average (VIDYA)

vwap --> Volume Weighted Average Price (VWAP)

vwma --> Volume Weighted Moving Average (VWMA)

wma --> Weighted Moving Average (WMA)

zlma --> Zero Lag Moving Average (ZLMA)

entropy --> Entropy (ENTP)

kurtosis --> Rolling Kurtosis

skew --> Rolling Skew

xev --> Condition all

zscore --> Rolling Z Score

adx --> Average Directional Movement (ADX)

aroon --> Aroon & Aroon Oscillator (AROON)

chop --> Choppiness Index (CHOP)

xex --> Condition any

cksp --> Chande Kroll Stop (CKSP)

dpo --> Detrend Price Oscillator (DPO)

long_run --> Long Run

psar --> Parabolic Stop and Reverse (psar)

short_run --> Short Run

vhf --> Vertical Horizontal Filter (VHF)

vortex --> Vortex

accbands --> Acceleration Bands (ACCBANDS)

atr --> Average True Range (ATR)

bbands --> Bollinger Bands (BBANDS)

donchian --> Donchian Channels (DC)

kc --> Keltner Channels (KC)

massi --> Mass Index (MASSI)

natr --> Normalized Average True Range (NATR)

pdist --> Price Distance (PDIST)

rvi --> Relative Volatility Index (RVI)

thermo --> Elders Thermometer (THERMO)

ui --> Ulcer Index (UI)

ad --> Accumulation/Distribution (AD)

cmf --> Chaikin Money Flow (CMF)

efi --> Elder's Force Index (EFI)

ecm --> Ease of Movement (EOM)

kvo --> Klinger Volume Oscillator (KVO)

mfi --> Money Flow Index (MFI)

nvi --> Negative Volume Index (NVI)

obv --> On Balance Volume (OBV)

pvi --> Positive Volume Index (PVI)

dvdi --> Dual Volume Divergence Index (DVDI)

xhh --> Dynamic rolling highest values

pvt --> Price-Volume Trend (PVT)

Remarks

I also incorporated func descriptions and func test script in commented mode, you can test the functino with the embedded test script and modify them as you wish.

This is a Level 3 free and open source indicator library.

Feedbacks are appreciated.

This is not the end of pandas_ta lib publication, but it is start point with pine v5 lib function and I will add more and more funcs into this lib for my own indicators.

Function Name List:

bton()

wcp()

count()

xbt()

ebsw()

ao()

apo()

xrf()

bias()

bop()

brar()

cci()

cfo()

cg()

cmo()

coppock()

cti()

dmi()

er()

eri()

fisher()

inertia()

kdj()

kst()

macd()

mom()

pgo()

ppo()

psl()

pvo()

qqe()

roc()

rsi()

rsx()

rvgi()

slope()

smi()

sqz_pro()

xfl()

stc()

stoch()

stochrsi()

trix()

tsi()

uo()

willr()

alma()

wcx()

xll()

dema()

ema()

fwma()

hilo()

hma()

hwma()

ichimoku()

jma()

kama()

linreg()

mgcd()

rma()

sinwma()

ssf()

supertrend()

xsa()

swma()

t3()

tema()

trima()

vidya()

vwap()

vwma()

wma()

zlma()

entropy()

kurtosis()

skew()

xev()

zscore()

adx()

aroon()

chop()

xex()

cksp()

dpo()

long_run()

psar()

short_run()

vhf()

vortex()

accbands()

atr()

bbands()

donchian()

kc()

massi()

natr()

pdist()

rvi()

thermo()

ui()

ad()

cmf()

efi()

ecm()

kvo()

mfi()

nvi()

obv()

pvi()

dvdi()

xhh()

pvt()

Multiple Symbol Trend Screener [Pineify]Multiple Symbol Trend Screener Pineify – Ultimate Multi-Indicator Scanner for TradingView

Empower your trading with deep market insights across multiple symbols using this feature-rich Pine Script screener. The Multiple Symbol Trend Screener Pineify enables traders to monitor and compare trends, reversals, and consolidations in real-time across the biggest equity symbols on TradingView, through a synergistic blend of popular technical indicators.

Key Features

Monitor up to 15 symbols and their trends simultaneously

Integrates 7 professional-grade indicators: MA Distance, Aroon, Parabolic SAR (PSAR), ADX, Supertrend, Keltner Channel, and BBTrend

Color-coded table display for instant visual assessment

Customizable lookback periods, indicator types, and calculation methods

SEO optimized for multi-symbol trend detection, screener, and advanced TradingView indicator

How It Works

This indicator leverages TradingView’s Pine Script v6 and request.security() to process multiple symbols across selected timeframes. Data populates a dynamic table, updating each cell based on the calculated value of every underlying indicator. MA Distance highlights deviation from moving averages; Aroon flags emerging trend strength; PSAR marks potential trend reversals; ADX assesses trend momentum; Supertrend detects bullish/bearish phases; Keltner Channel and BBTrend offer volatility and power insights.

Set up your preferred symbols and timeframes

Each indicator runs its calculation per symbol using its parameter group

All results are displayed in a table for a comprehensive dashboard view

Trading Ideas and Insights

Traders can use this screener for cross-market comparison, directional bias, entry/exit filtering, and comprehensive trend evaluation. The screener is excellent for swing trading, day trading, and portfolio tracking. It enables confirmation across multiple frameworks — for example, spotting momentum with ADX before confirming direction with Supertrend and PSAR.

Identify correlated movements or divergences across selected assets

Spot synchronized trend changes for basket trading ideas

Filter symbols by volatility, strength, or trend status for precise trade selection

How Multiple Indicators Work Together

The screener’s edge lies in its intelligent correlation of popular indicators. MA Distance measures the proximity to chosen moving averages, ideal for spotting overbought/oversold conditions. Aroon reveals the strength of new price trends, PSAR indicates reversal signals, and ADX quantifies the momentum of these trends. Supertrend provides a directional phase, while Keltner Channel & BBTrend analyze volatility shifts and band compressions. This amalgamation allows for a robust, multi-dimensional market snapshot, capturing details missed by single-indicator tools.

By displaying all key metrics side-by-side, the screener enables holistic decision-making, revealing confluence zones and contradiction areas across multiple tickers and timeframes.

Unique Aspects

Original implementation combining seven independent trend and momentum indicators for each symbol

Rich customization for symbols, timeframes, and all indicator parameters

Intuitive color-coding for quick reading of bullish/bearish/neutral signals

Comprehensive dashboard for instant actionable insights

How to Use

Load the indicator onto your TradingView chart

Go to the script’s settings and input your preferred symbols and relevant timeframes

Set your desired parameters for each indicator group: Moving Average type, Aroon length, PSAR values, ADX smoothing, etc.

Observe the results in the top-right table, then use it to filter candidates and validate trade setups

The screener is suitable for all timeframes and asset classes available on TradingView. Make sure your chart’s timeframe matches the one used in the scanner for optimal accuracy.

Customization

Choose up to 15 symbols to monitor in a single dashboard

Customize lookback periods, indicator types, colors, and display settings

Configure alerting options and thresholds for advanced trade automation

Conclusion

The Multiple Symbol Trend Screener Pineify sets a new standard for multi-asset screening on TradingView. By elegantly merging seven proven technical indicators, the screener delivers powerful trend detection, reversal analysis, and volatility monitoring — all in one dashboard. Take your trading to new heights with in-depth, customizable market surveillance.

taLibrary "ta"

█ OVERVIEW

This library holds technical analysis functions calculating values for which no Pine built-in exists.

Look first. Then leap.

█ FUNCTIONS

cagr(entryTime, entryPrice, exitTime, exitPrice)

It calculates the "Compound Annual Growth Rate" between two points in time. The CAGR is a notional, annualized growth rate that assumes all profits are reinvested. It only takes into account the prices of the two end points — not drawdowns, so it does not calculate risk. It can be used as a yardstick to compare the performance of two instruments. Because it annualizes values, the function requires a minimum of one day between the two end points (annualizing returns over smaller periods of times doesn't produce very meaningful figures).

Parameters:

entryTime : The starting timestamp.

entryPrice : The starting point's price.

exitTime : The ending timestamp.

exitPrice : The ending point's price.

Returns: CAGR in % (50 is 50%). Returns `na` if there is not >=1D between `entryTime` and `exitTime`, or until the two time points have not been reached by the script.

█ v2, Mar. 8, 2022

Added functions `allTimeHigh()` and `allTimeLow()` to find the highest or lowest value of a source from the first historical bar to the current bar. These functions will not look ahead; they will only return new highs/lows on the bar where they occur.

allTimeHigh(src)

Tracks the highest value of `src` from the first historical bar to the current bar.

Parameters:

src : (series int/float) Series to track. Optional. The default is `high`.

Returns: (float) The highest value tracked.

allTimeLow(src)

Tracks the lowest value of `src` from the first historical bar to the current bar.

Parameters:

src : (series int/float) Series to track. Optional. The default is `low`.

Returns: (float) The lowest value tracked.

█ v3, Sept. 27, 2022

This version includes the following new functions:

aroon(length)

Calculates the values of the Aroon indicator.

Parameters:

length (simple int) : (simple int) Number of bars (length).

Returns: ( [float, float ]) A tuple of the Aroon-Up and Aroon-Down values.

coppock(source, longLength, shortLength, smoothLength)

Calculates the value of the Coppock Curve indicator.

Parameters:

source (float) : (series int/float) Series of values to process.

longLength (simple int) : (simple int) Number of bars for the fast ROC value (length).

shortLength (simple int) : (simple int) Number of bars for the slow ROC value (length).

smoothLength (simple int) : (simple int) Number of bars for the weigted moving average value (length).

Returns: (float) The oscillator value.

dema(source, length)

Calculates the value of the Double Exponential Moving Average (DEMA).

Parameters:

source (float) : (series int/float) Series of values to process.

length (simple int) : (simple int) Length for the smoothing parameter calculation.

Returns: (float) The double exponentially weighted moving average of the `source`.

dema2(src, length)

An alternate Double Exponential Moving Average (Dema) function to `dema()`, which allows a "series float" length argument.

Parameters:

src : (series int/float) Series of values to process.

length : (series int/float) Length for the smoothing parameter calculation.

Returns: (float) The double exponentially weighted moving average of the `src`.

dm(length)

Calculates the value of the "Demarker" indicator.

Parameters:

length (simple int) : (simple int) Number of bars (length).

Returns: (float) The oscillator value.

donchian(length)

Calculates the values of a Donchian Channel using `high` and `low` over a given `length`.

Parameters:

length (int) : (series int) Number of bars (length).

Returns: ( [float, float, float ]) A tuple containing the channel high, low, and median, respectively.

ema2(src, length)

An alternate ema function to the `ta.ema()` built-in, which allows a "series float" length argument.

Parameters:

src : (series int/float) Series of values to process.

length : (series int/float) Number of bars (length).

Returns: (float) The exponentially weighted moving average of the `src`.

eom(length, div)

Calculates the value of the Ease of Movement indicator.

Parameters:

length (simple int) : (simple int) Number of bars (length).

div (simple int) : (simple int) Divisor used for normalzing values. Optional. The default is 10000.

Returns: (float) The oscillator value.

frama(source, length)

The Fractal Adaptive Moving Average (FRAMA), developed by John Ehlers, is an adaptive moving average that dynamically adjusts its lookback period based on fractal geometry.

Parameters:

source (float) : (series int/float) Series of values to process.

length (int) : (series int) Number of bars (length).

Returns: (float) The fractal adaptive moving average of the `source`.

ft(source, length)

Calculates the value of the Fisher Transform indicator.

Parameters:

source (float) : (series int/float) Series of values to process.

length (simple int) : (simple int) Number of bars (length).

Returns: (float) The oscillator value.

ht(source)

Calculates the value of the Hilbert Transform indicator.

Parameters:

source (float) : (series int/float) Series of values to process.

Returns: (float) The oscillator value.

ichimoku(conLength, baseLength, senkouLength)

Calculates values of the Ichimoku Cloud indicator, including tenkan, kijun, senkouSpan1, senkouSpan2, and chikou. NOTE: offsets forward or backward can be done using the `offset` argument in `plot()`.

Parameters:

conLength (int) : (series int) Length for the Conversion Line (Tenkan). The default is 9 periods, which returns the mid-point of the 9 period Donchian Channel.

baseLength (int) : (series int) Length for the Base Line (Kijun-sen). The default is 26 periods, which returns the mid-point of the 26 period Donchian Channel.

senkouLength (int) : (series int) Length for the Senkou Span 2 (Leading Span B). The default is 52 periods, which returns the mid-point of the 52 period Donchian Channel.

Returns: ( [float, float, float, float, float ]) A tuple of the Tenkan, Kijun, Senkou Span 1, Senkou Span 2, and Chikou Span values. NOTE: by default, the senkouSpan1 and senkouSpan2 should be plotted 26 periods in the future, and the Chikou Span plotted 26 days in the past.

ift(source)

Calculates the value of the Inverse Fisher Transform indicator.

Parameters:

source (float) : (series int/float) Series of values to process.

Returns: (float) The oscillator value.

kvo(fastLen, slowLen, trigLen)

Calculates the values of the Klinger Volume Oscillator.

Parameters:

fastLen (simple int) : (simple int) Length for the fast moving average smoothing parameter calculation.

slowLen (simple int) : (simple int) Length for the slow moving average smoothing parameter calculation.

trigLen (simple int) : (simple int) Length for the trigger moving average smoothing parameter calculation.

Returns: ( [float, float ]) A tuple of the KVO value, and the trigger value.

pzo(length)

Calculates the value of the Price Zone Oscillator.

Parameters:

length (simple int) : (simple int) Length for the smoothing parameter calculation.

Returns: (float) The oscillator value.

rms(source, length)

Calculates the Root Mean Square of the `source` over the `length`.

Parameters:

source (float) : (series int/float) Series of values to process.

length (int) : (series int) Number of bars (length).

Returns: (float) The RMS value.

rwi(length)

Calculates the values of the Random Walk Index.

Parameters:

length (simple int) : (simple int) Lookback and ATR smoothing parameter length.

Returns: ( [float, float ]) A tuple of the `rwiHigh` and `rwiLow` values.

stc(source, fast, slow, cycle, d1, d2)

Calculates the value of the Schaff Trend Cycle indicator.

Parameters:

source (float) : (series int/float) Series of values to process.

fast (simple int) : (simple int) Length for the MACD fast smoothing parameter calculation.

slow (simple int) : (simple int) Length for the MACD slow smoothing parameter calculation.

cycle (simple int) : (simple int) Number of bars for the Stochastic values (length).

d1 (simple int) : (simple int) Length for the initial %D smoothing parameter calculation.

d2 (simple int) : (simple int) Length for the final %D smoothing parameter calculation.

Returns: (float) The oscillator value.

stochFull(periodK, smoothK, periodD)

Calculates the %K and %D values of the Full Stochastic indicator.

Parameters:

periodK (simple int) : (simple int) Number of bars for Stochastic calculation. (length).

smoothK (simple int) : (simple int) Number of bars for smoothing of the %K value (length).

periodD (simple int) : (simple int) Number of bars for smoothing of the %D value (length).

Returns: ( [float, float ]) A tuple of the slow %K and the %D moving average values.

stochRsi(lengthRsi, periodK, smoothK, periodD, source)

Calculates the %K and %D values of the Stochastic RSI indicator.

Parameters:

lengthRsi (simple int) : (simple int) Length for the RSI smoothing parameter calculation.

periodK (simple int) : (simple int) Number of bars for Stochastic calculation. (length).

smoothK (simple int) : (simple int) Number of bars for smoothing of the %K value (length).

periodD (simple int) : (simple int) Number of bars for smoothing of the %D value (length).

source (float) : (series int/float) Series of values to process. Optional. The default is `close`.

Returns: ( [float, float ]) A tuple of the slow %K and the %D moving average values.

supertrend(factor, atrLength, wicks)

Calculates the values of the SuperTrend indicator with the ability to take candle wicks into account, rather than only the closing price.

Parameters:

factor (float) : (series int/float) Multiplier for the ATR value.

atrLength (simple int) : (simple int) Length for the ATR smoothing parameter calculation.

wicks (simple bool) : (simple bool) Condition to determine whether to take candle wicks into account when reversing trend, or to use the close price. Optional. Default is false.

Returns: ( [float, int ]) A tuple of the superTrend value and trend direction.

szo(source, length)

Calculates the value of the Sentiment Zone Oscillator.

Parameters:

source (float) : (series int/float) Series of values to process.

length (simple int) : (simple int) Length for the smoothing parameter calculation.

Returns: (float) The oscillator value.

t3(source, length, vf)

Calculates the value of the Tilson Moving Average (T3).

Parameters:

source (float) : (series int/float) Series of values to process.

length (simple int) : (simple int) Length for the smoothing parameter calculation.

vf (simple float) : (simple float) Volume factor. Affects the responsiveness.

Returns: (float) The Tilson moving average of the `source`.

t3Alt(source, length, vf)

An alternate Tilson Moving Average (T3) function to `t3()`, which allows a "series float" `length` argument.

Parameters:

source (float) : (series int/float) Series of values to process.

length (float) : (series int/float) Length for the smoothing parameter calculation.

vf (simple float) : (simple float) Volume factor. Affects the responsiveness.

Returns: (float) The Tilson moving average of the `source`.

tema(source, length)

Calculates the value of the Triple Exponential Moving Average (TEMA).

Parameters:

source (float) : (series int/float) Series of values to process.

length (simple int) : (simple int) Length for the smoothing parameter calculation.

Returns: (float) The triple exponentially weighted moving average of the `source`.

tema2(source, length)

An alternate Triple Exponential Moving Average (TEMA) function to `tema()`, which allows a "series float" `length` argument.

Parameters:

source (float) : (series int/float) Series of values to process.

length (float) : (series int/float) Length for the smoothing parameter calculation.

Returns: (float) The triple exponentially weighted moving average of the `source`.

trima(source, length)

Calculates the value of the Triangular Moving Average (TRIMA).

Parameters:

source (float) : (series int/float) Series of values to process.

length (int) : (series int) Number of bars (length).

Returns: (float) The triangular moving average of the `source`.

trima2(src, length)

An alternate Triangular Moving Average (TRIMA) function to `trima()`, which allows a "series int" length argument.

Parameters:

src : (series int/float) Series of values to process.

length : (series int) Number of bars (length).

Returns: (float) The triangular moving average of the `src`.

trix(source, length, signalLength, exponential)

Calculates the values of the TRIX indicator.

Parameters:

source (float) : (series int/float) Series of values to process.

length (simple int) : (simple int) Length for the smoothing parameter calculation.

signalLength (simple int) : (simple int) Length for smoothing the signal line.

exponential (simple bool) : (simple bool) Condition to determine whether exponential or simple smoothing is used. Optional. The default is `true` (exponential smoothing).

Returns: ( [float, float, float ]) A tuple of the TRIX value, the signal value, and the histogram.

uo(fastLen, midLen, slowLen)

Calculates the value of the Ultimate Oscillator.

Parameters:

fastLen (simple int) : (series int) Number of bars for the fast smoothing average (length).

midLen (simple int) : (series int) Number of bars for the middle smoothing average (length).

slowLen (simple int) : (series int) Number of bars for the slow smoothing average (length).

Returns: (float) The oscillator value.

vhf(source, length)

Calculates the value of the Vertical Horizontal Filter.

Parameters:

source (float) : (series int/float) Series of values to process.

length (simple int) : (simple int) Number of bars (length).

Returns: (float) The oscillator value.

vi(length)

Calculates the values of the Vortex Indicator.

Parameters:

length (simple int) : (simple int) Number of bars (length).

Returns: ( [float, float ]) A tuple of the viPlus and viMinus values.

vzo(length)

Calculates the value of the Volume Zone Oscillator.

Parameters:

length (simple int) : (simple int) Length for the smoothing parameter calculation.

Returns: (float) The oscillator value.

williamsFractal(period)

Detects Williams Fractals.

Parameters:

period (int) : (series int) Number of bars (length).

Returns: ( [bool, bool ]) A tuple of an up fractal and down fractal. Variables are true when detected.

wpo(length)

Calculates the value of the Wave Period Oscillator.

Parameters:

length (simple int) : (simple int) Length for the smoothing parameter calculation.

Returns: (float) The oscillator value.

█ v7, Nov. 2, 2023

This version includes the following new and updated functions:

atr2(length)

An alternate ATR function to the `ta.atr()` built-in, which allows a "series float" `length` argument.

Parameters:

length (float) : (series int/float) Length for the smoothing parameter calculation.

Returns: (float) The ATR value.

changePercent(newValue, oldValue)

Calculates the percentage difference between two distinct values.

Parameters:

newValue (float) : (series int/float) The current value.

oldValue (float) : (series int/float) The previous value.

Returns: (float) The percentage change from the `oldValue` to the `newValue`.

donchian(length)

Calculates the values of a Donchian Channel using `high` and `low` over a given `length`.

Parameters:

length (int) : (series int) Number of bars (length).

Returns: ( [float, float, float ]) A tuple containing the channel high, low, and median, respectively.

highestSince(cond, source)

Tracks the highest value of a series since the last occurrence of a condition.

Parameters:

cond (bool) : (series bool) A condition which, when `true`, resets the tracking of the highest `source`.

source (float) : (series int/float) Series of values to process. Optional. The default is `high`.

Returns: (float) The highest `source` value since the last time the `cond` was `true`.

lowestSince(cond, source)

Tracks the lowest value of a series since the last occurrence of a condition.

Parameters:

cond (bool) : (series bool) A condition which, when `true`, resets the tracking of the lowest `source`.

source (float) : (series int/float) Series of values to process. Optional. The default is `low`.

Returns: (float) The lowest `source` value since the last time the `cond` was `true`.

relativeVolume(length, anchorTimeframe, isCumulative, adjustRealtime)

Calculates the volume since the last change in the time value from the `anchorTimeframe`, the historical average volume using bars from past periods that have the same relative time offset as the current bar from the start of its period, and the ratio of these volumes. The volume values are cumulative by default, but can be adjusted to non-accumulated with the `isCumulative` parameter.

Parameters:

length (simple int) : (simple int) The number of periods to use for the historical average calculation.

anchorTimeframe (simple string) : (simple string) The anchor timeframe used in the calculation. Optional. Default is "D".

isCumulative (simple bool) : (simple bool) If `true`, the volume values will be accumulated since the start of the last `anchorTimeframe`. If `false`, values will be used without accumulation. Optional. The default is `true`.

adjustRealtime (simple bool) : (simple bool) If `true`, estimates the cumulative value on unclosed bars based on the data since the last `anchor` condition. Optional. The default is `false`.

Returns: ( [float, float, float ]) A tuple of three float values. The first element is the current volume. The second is the average of volumes at equivalent time offsets from past anchors over the specified number of periods. The third is the ratio of the current volume to the historical average volume.

rma2(source, length)

An alternate RMA function to the `ta.rma()` built-in, which allows a "series float" `length` argument.

Parameters:

source (float) : (series int/float) Series of values to process.

length (float) : (series int/float) Length for the smoothing parameter calculation.

Returns: (float) The rolling moving average of the `source`.

supertrend2(factor, atrLength, wicks)

An alternate SuperTrend function to `supertrend()`, which allows a "series float" `atrLength` argument.

Parameters:

factor (float) : (series int/float) Multiplier for the ATR value.

atrLength (float) : (series int/float) Length for the ATR smoothing parameter calculation.

wicks (simple bool) : (simple bool) Condition to determine whether to take candle wicks into account when reversing trend, or to use the close price. Optional. Default is `false`.

Returns: ( [float, int ]) A tuple of the superTrend value and trend direction.

vStop(source, atrLength, atrFactor)

Calculates an ATR-based stop value that trails behind the `source`. Can serve as a possible stop-loss guide and trend identifier.

Parameters:

source (float) : (series int/float) Series of values that the stop trails behind.

atrLength (simple int) : (simple int) Length for the ATR smoothing parameter calculation.

atrFactor (float) : (series int/float) The multiplier of the ATR value. Affects the maximum distance between the stop and the `source` value. A value of 1 means the maximum distance is 100% of the ATR value. Optional. The default is 1.

Returns: ( [float, bool ]) A tuple of the volatility stop value and the trend direction as a "bool".

vStop2(source, atrLength, atrFactor)

An alternate Volatility Stop function to `vStop()`, which allows a "series float" `atrLength` argument.

Parameters:

source (float) : (series int/float) Series of values that the stop trails behind.

atrLength (float) : (series int/float) Length for the ATR smoothing parameter calculation.

atrFactor (float) : (series int/float) The multiplier of the ATR value. Affects the maximum distance between the stop and the `source` value. A value of 1 means the maximum distance is 100% of the ATR value. Optional. The default is 1.

Returns: ( [float, bool ]) A tuple of the volatility stop value and the trend direction as a "bool".

Removed Functions:

allTimeHigh(src)

Tracks the highest value of `src` from the first historical bar to the current bar.

allTimeLow(src)

Tracks the lowest value of `src` from the first historical bar to the current bar.

trima2(src, length)

An alternate Triangular Moving Average (TRIMA) function to `trima()`, which allows a

"series int" length argument.

Trend Background by Alejandro PThis indicator is a comprehensive trend indicator designed to help traders filter market conditions for their trading.

The indicator has the option to use a classic Simple Moving Average as a trend filer or a more advanced Simple Moving Average Slope.

The indicator can also use the Aroon indicator as the trend filter and both the SMA and Aroon can be used together to only trade in strong trends.

The Simple Moving Average Slope and the Aroon filters can allow you to filter our 3 market conditions. 1- Upwards Trend, 2- Downwards Trend, 3- Ranging

By tuning these filters to your strategy you can make sure you are only taking trades when the trend is on your side and you can even filter out ranging market conditions to trade the best strategies depending on the market conditions.

Technical details:

If the Simple Moving Average filter is on and the Slope filter if off the indicator will determine the trend by where the price is relative to the moving average. If the price is higher than the SMA then the trend will be bullish, if the price is below the SMA the trend will be bearish.

If SMA filter and Slope FIlter are both on then the trend es defined by the slope of the SMA, this means that if the SMA slope is increasing then the trend will be bullish, if the slow is negative then it will be bearish, but if the slope is within a certain percentile that is classified as neutral then there will be no trend or a neutral market.

If the Aroon filter is enabled this will calculate the trend by the percent of candles with new highs or lows in a similar way as the SMA slope filter works

If both filters are enabled then both filters will have to coincide for a bull or bear trend to be determined.

FS Scorpion TailKey Features & Components:

1. Custom Date & Chart-Based Controls

The software allows users to define whether they want signals to start on a specific date (useSpecificDate) or base calculations on the visible chart’s range (useRelativeScreenSumLeft and useRelativeScreenSumRight).

Users can input the number of stocks to buy/sell per signal and decide whether to sell only for profit.

2. Technical Indicators Used

EMA (Exponential Moving Average): Users can define the length of the EMA and specify if buy/sell signals should occur when the EMA is rising or falling.

MACD (Moving Average Convergence Divergence): MACD crossovers, slopes of the MACD line, signal line, and histogram are used for generating buy/sell signals.

ATR (Average True Range): Signals are generated based on rising or falling ATR.

Aroon Indicator: Buy and sell signals are based on the behavior of the Aroon upper and lower lines.

RSI (Relative Strength Index): Tracks whether the RSI and its moving average are rising or falling to generate signals.

Bollinger Bands: Buy/sell signals depend on the basis, upper, and lower band behavior (rising or falling).

3. Signal Detection

The software creates arrays for each indicator to store conditions for buy/sell signals.

The allTrue() function checks whether all conditions for buy/sell signals are true, ensuring that only valid signals are plotted.

Signals are differentiated between buy-only, sell-only, and both buy and sell (dual signal).

4. Visual Indicators

Vertical Lines: When buy, sell, or dual signals are detected, vertical lines are drawn at the corresponding bar with configurable colors (green for buy, red for sell, silver for dual).

Buy/Sell Labels: Visual labels are plotted directly on the chart to denote buy or sell signals, allowing for clear interpretation of the strategy.

5. Cash Flow & Metrics Display

The software maintains an internal ledger of how many stocks are bought/sold, their prices, and whether a profit is being made.

A table is displayed at the bottom right of the chart, showing:

Initial investment

Current stocks owned

Last buy price

Market stake

Net profit

The table background turns green for profit and red for loss.

6. Dynamic Decision Making

Buy Condition: If a valid buy signal is generated, the software decrements the cash balance and adds stocks to the inventory.

Sell Condition: If the sell signal is valid (and meets the profit requirement), stocks are sold, and cash is incremented.

A fallback check ensures the sell logic prevents selling more stocks than are available and adjusts stock holding appropriately (e.g., sell half).

Customization and Usage

Indicator Adjustments: The user can choose which indicators to activate (e.g., EMA, MACD, RSI) via input controls. Each indicator has specific customizable parameters such as lengths, slopes, and conditions.

Signal Flexibility: The user can adjust conditions for buying and selling based on various technical indicators, which adds flexibility in implementing trading strategies. For example, users may require the RSI to be higher than its moving average or trigger sales only when MACD crosses under the signal line.

Profit Sensitivity: The software allows the option to sell only when a profit is assured by checking if the current price is higher than the last buy price.

Summary of Usage:

Indicator Selection: Enable or disable technical indicators like EMA, MACD, RSI, Aroon, ATR, and Bollinger Bands to fit your trading strategy.

Custom Date/Chart Settings: Choose whether to calculate based on specific time ranges or visible portions of the chart.

Dynamic Signal Plotting: Once buy or sell conditions are met, the software will visually plot signals on your chart, giving clear entry and exit points.

Investment Tracking: Real-time tracking of stock quantities, investments, and profit ensures a clear view of your trading performance.

Backtesting: Use this software for backtesting your strategy by analyzing how buy and sell signals would have performed historically based on the chosen indicators.

Conclusion

The FS Scorpion Tail software is a robust and flexible trading tool, allowing traders to develop custom strategies based on multiple well-known technical indicators. Its visual aid, coupled with real-time investment tracking, makes it valuable for systematic traders looking to automate or refine their trading approach.

RSI Weighted Trend System I [InvestorUnknown]The RSI Weighted Trend System I is an experimental indicator designed to combine both slow-moving trend indicators for stable trend identification and fast-moving indicators to capture potential major turning points in the market. The novelty of this system lies in the dynamic weighting mechanism, where fast indicators receive weight based on the current Relative Strength Index (RSI) value, thus providing a flexible tool for traders seeking to adapt their strategies to varying market conditions.

Dynamic RSI-Based Weighting System

The core of the indicator is the dynamic weighting of fast indicators based on the value of the RSI. In essence, the higher the absolute value of the RSI (whether positive or negative), the higher the weight assigned to the fast indicators. This enables the system to capture rapid price movements around potential turning points.

Users can choose between a threshold-based or continuous weight system:

Threshold-Based Weighting: Fast indicators are activated only when the absolute RSI value exceeds a user-defined threshold. Below this threshold, fast indicators receive no weight.

Continuous Weighting: By setting the weight threshold to zero, the fast indicators always receive some weight, although this can result in more false signals in ranging markets.

// Calculate weight for Fast Indicators based on RSI (Slow Indicator weight is kept to 1 for simplicity)

f_RSI_Weight_System(series float rsi, simple float weight_thre) =>

float fast_weight = na

float slow_weight = na

if weight_thre > 0

if math.abs(rsi) <= weight_thre

fast_weight := 0

slow_weight := 1

else

fast_weight := 0 + math.sqrt(math.abs(rsi))

slow_weight := 1

else

fast_weight := 0 + math.sqrt(math.abs(rsi))

slow_weight := 1

Slow and Fast Indicators

Slow Indicators are designed to identify stable trends, remaining constant in weight. These include:

DMI (Directional Movement Index) For Loop

CCI (Commodity Channel Index) For Loop

Aroon For Loop

Fast Indicators are more responsive and designed to spot rapid trend shifts:

ZLEMA (Zero-Lag Exponential Moving Average) For Loop

IIRF (Infinite Impulse Response Filter) For Loop

Each of these indicators is calculated using a for-loop method to generate a moving average, which captures the trend of a given length range.

RSI Normalization

To facilitate the weighting system, the RSI is normalized from its usual 0-100 range to a -1 to 1 range. This allows for easy scaling when calculating weights and helps the system adjust to rapidly changing market conditions.

// Normalize RSI (1 to -1)

f_RSI(series float rsi_src, simple int rsi_len, simple string rsi_wb, simple string ma_type, simple int ma_len) =>

output = switch rsi_wb

"RAW RSI" => ta.rsi(rsi_src, rsi_len)

"RSI MA" => ma_type == "EMA" ? (ta.ema(ta.rsi(rsi_src, rsi_len), ma_len)) : (ta.sma(ta.rsi(rsi_src, rsi_len), ma_len))

Signal Calculation

The final trading signal is a weighted average of both the slow and fast indicators, depending on the calculated weights from the RSI. This ensures a balanced approach, where slow indicators maintain overall trend guidance, while fast indicators provide timely entries and exits.

// Calculate Signal (as weighted average)

sig = math.round(((DMI*slow_w) + (CCI*slow_w) + (Aroon*slow_w) + (ZLEMA*fast_w) + (IIRF*fast_w)) / (3*slow_w + 2*fast_w), 2)

Backtest Mode and Performance Metrics

This version of the RSI Weighted Trend System includes a comprehensive backtesting mode, allowing users to evaluate the performance of their selected settings against a Buy & Hold strategy. The backtesting includes:

Equity calculation based on the signals generated by the indicator.

Performance metrics table comparing Buy & Hold strategy metrics with the system’s signals, including: Mean, positive, and negative return percentages, Standard deviations (of all, positive and negative returns), Sharpe Ratio, Sortino Ratio, and Omega Ratio

f_PerformanceMetrics(series float base, int Lookback, simple float startDate, bool Annualize = true) =>

// Initialize variables for positive and negative returns

pos_sum = 0.0

neg_sum = 0.0

pos_count = 0

neg_count = 0

returns_sum = 0.0

returns_squared_sum = 0.0

pos_returns_squared_sum = 0.0

neg_returns_squared_sum = 0.0

// Loop through the past 'Lookback' bars to calculate sums and counts

if (time >= startDate)

for i = 0 to Lookback - 1

r = (base - base ) / base

returns_sum += r

returns_squared_sum += r * r

if r > 0

pos_sum += r

pos_count += 1

pos_returns_squared_sum += r * r

if r < 0

neg_sum += r

neg_count += 1

neg_returns_squared_sum += r * r

float export_array = array.new_float(12)

// Calculate means

mean_all = math.round((returns_sum / Lookback) * 100, 2)

mean_pos = math.round((pos_count != 0 ? pos_sum / pos_count : na) * 100, 2)

mean_neg = math.round((neg_count != 0 ? neg_sum / neg_count : na) * 100, 2)

// Calculate standard deviations

stddev_all = math.round((math.sqrt((returns_squared_sum - (returns_sum * returns_sum) / Lookback) / Lookback)) * 100, 2)

stddev_pos = math.round((pos_count != 0 ? math.sqrt((pos_returns_squared_sum - (pos_sum * pos_sum) / pos_count) / pos_count) : na) * 100, 2)

stddev_neg = math.round((neg_count != 0 ? math.sqrt((neg_returns_squared_sum - (neg_sum * neg_sum) / neg_count) / neg_count) : na) * 100, 2)

// Calculate probabilities

prob_pos = math.round((pos_count / Lookback) * 100, 2)

prob_neg = math.round((neg_count / Lookback) * 100, 2)

prob_neu = math.round(((Lookback - pos_count - neg_count) / Lookback) * 100, 2)

// Calculate ratios

sharpe_ratio = math.round(mean_all / stddev_all * (Annualize ? math.sqrt(Lookback) : 1), 2)

sortino_ratio = math.round(mean_all / stddev_neg * (Annualize ? math.sqrt(Lookback) : 1), 2)

omega_ratio = math.round(pos_sum / math.abs(neg_sum), 2)

// Set values in the array

array.set(export_array, 0, mean_all), array.set(export_array, 1, mean_pos), array.set(export_array, 2, mean_neg),

array.set(export_array, 3, stddev_all), array.set(export_array, 4, stddev_pos), array.set(export_array, 5, stddev_neg),

array.set(export_array, 6, prob_pos), array.set(export_array, 7, prob_neu), array.set(export_array, 8, prob_neg),

array.set(export_array, 9, sharpe_ratio), array.set(export_array, 10, sortino_ratio), array.set(export_array, 11, omega_ratio)

// Export the array

export_array

The metrics help traders assess the effectiveness of their strategy over time and can be used to optimize their settings.

Calibration Mode

A calibration mode is included to assist users in tuning the indicator to their specific needs. In this mode, traders can focus on a specific indicator (e.g., DMI, CCI, Aroon, ZLEMA, IIRF, or RSI) and fine-tune it without interference from other signals.

The calibration plot visualizes the chosen indicator's performance against a zero line, making it easy to see how changes in the indicator’s settings affect its trend detection.

Customization and Default Settings

Important Note: The default settings provided are not optimized for any particular market or asset. They serve as a starting point for experimentation. Traders are encouraged to calibrate the system to suit their own trading strategies and preferences.

The indicator allows deep customization, from selecting which indicators to use, adjusting the lengths of each indicator, smoothing parameters, and the RSI weight system.

Alerts

Traders can set alerts for both long and short signals when the indicator flips, allowing for automated monitoring of potential trading opportunities.

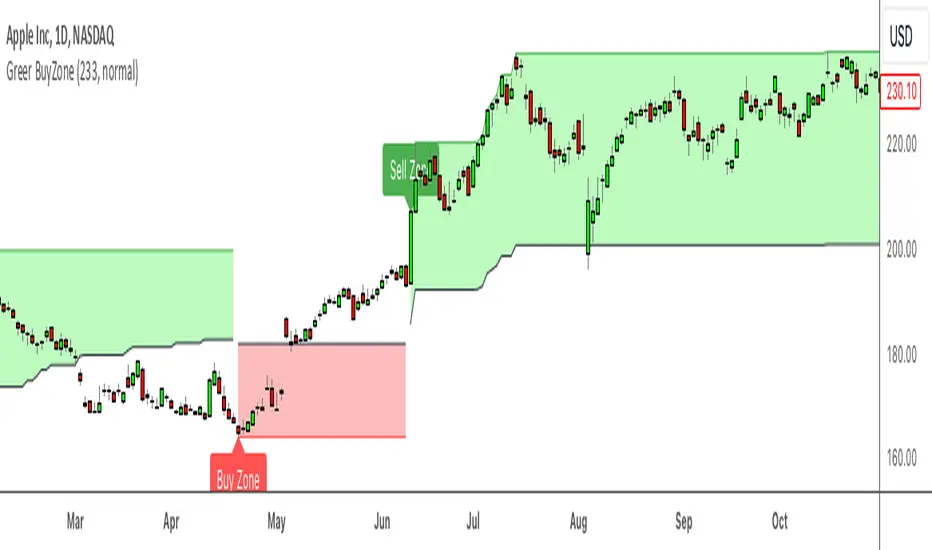

Greer BuyZone toolGreer BuyZone Tool

Description:

The Greer BuyZone Tool is a custom Pine Script indicator designed to help identify potential long-term investment opportunities by marking BuyZones on the chart. This tool utilizes the Aroon indicator in combination with Fibonacci numbers to define periods where the asset might be a good candidate for dollar-cost averaging.

Features:

BuyZone Detection: The script identifies and marks the beginning and end of a BuyZone with vertical lines and labels.

Visual Markers: A red vertical line and label indicate the start of a BuyZone, while a green vertical line and label mark the end of a BuyZone.

Aroon Indicator Calculation: Utilizes the Aroon indicator with a Fibonacci length (233) to determine key price levels.

How to Use:

Setup: Add the Greer BuyZone Tool to your TradingView chart. It will display vertical lines and labels marking the BuyZone periods.

BuyZone Identification: Use the red lines and labels ("BZ Begins ->>") to identify the start of a BuyZone, and the green lines and labels ("<<- BZ Ends") to determine when the BuyZone ends.

Long-Term Investment: This tool is intended for long-term investing and dollar-cost averaging strategies, not for day trading.

Disclaimer:

This script is provided for informational purposes only and is not intended as financial advice. The Greer BuyZone Tool is designed to assist in identifying potential long-term investment opportunities and is not suitable for day trading. The use of this tool involves risk, and there is no guarantee of profitability. Users are advised to conduct their own research and consult with a qualified financial advisor before making any investment decisions. The creator of this script assumes no liability for any losses or damages resulting from the use of this indicator.

Author: Sean Lee Greer

Date: 9/1/2024

MA Ratio Weighted Trend System I [InvestorUnknown]The MA Ratio Weighted Trend System I combines slow and fast indicators to identify stable trends and capture potential market turning points. By dynamically adjusting the weight of fast indicators based on the Moving Average Ratio (MAR), the system aims to provide timely entry and exit signals while maintaining overall trend stability through slow indicators.

Slow and Fast Indicators with Dynamic Weighting

Slow Indicators: Designed for stable trend identification, these indicators maintain a constant weight in the overall signal calculation. They include:

DMI For Loop (Directional Movement Index)

CCI For Loop (Commodity Channel Index)

Aroon For Loop

Fast Indicators: Aim to detect rapid market changes and potential turning points. Their weights are dynamically adjusted based on the absolute value of the Moving Average Ratio (MAR). Fast indicators include:

ZLEMA For Loop (Zero-Lag Exponential Moving Average)

IIRF For Loop (Infinite Impulse Response Filter)

Dynamic Weighting Mechanism:

Moving Average Ratio (MAR) is calculated as the ratio of the price to its moving average, minus one (for simplicity and visualization).

Weight Calculation

Fast indicator weights are determined based on the absolute value of MAR, possibly with an offset to avoid scenarios where MAR follows rapid price reversals too closely:

// Function to calculate weights based on MAR

f_mar_weights(series float mar, simple int offset, simple float weight_thre) =>

o_mar = math.abs(mar )

float fast_weight = 0

float slow_weight = 1

if o_mar != 0

if weight_thre > 0

if o_mar <= weight_thre

fast_weight := o_mar

else

fast_weight := o_mar

Threshold-Based vs. Continuous Weighting:

Threshold-Based: Fast indicators receive weight only when the absolute MAR exceeds a user-defined threshold (weight_thre).

Continuous: By setting weight_thre to zero, fast indicators always receive some weight, though this may increase false signals.

Offset Mechanism

The offset parameter shifts the MAR used for weighting by a certain number of bars. This helps avoid situations where the MAR follows sudden price movements too closely, preventing fast indicators from failing to provide timely exit signals.

Signal Calculation

The final signal is a weighted average of the slow and fast indicators:

// Calculate Signal (as weighted average)

float sig = math.round(((DMI*slow_w) + (CCI*slow_w) + (Aroon*slow_w) + (ZLEMA*fast_w) + (IIRF*fast_w)) / (3*slow_w + 2*fast_w), 2)

Backtesting and Performance Metrics

Enables users to test the indicator's performance over historical data, comparing it to a buy-and-hold strategy.

Alerts

Set up alerts for when the signal crosses above or below the thresholds.

alertcondition(long_alert, "LONG (MAR Weighted Trend System)", "MAR Weighted Trend System flipped ⬆LONG⬆")

alertcondition(short_alert, "SHORT (MAR Weighted Trend System)", "MAR Weighted Trend System flipped ⬇Short⬇")

Important Notes

Customization: Due to the experimental nature of this indicator, users are strongly encouraged to adjust and calibrate the settings to align with their trading strategies and market conditions.

Default Settings Disclaimer: The default settings are not optimized or recommended for any specific use and serve only as placeholders for the indicator's publication.

Backtest Results Disclaimer: Historical backtest results are not indicative of future performance. Market conditions change, and past results do not guarantee future outcomes.

FMS Suite [KFB Quant]FMS Suite

Overview

The FMS Suite is a powerful and adaptive trend and momentum analysis tool that leverages multiple technical indicators to deliver a comprehensive signal for market direction. This suite combines the strengths of the Aroon, DMI, RSI, Supertrend, and Trix indicators, offering traders a well-rounded perspective on market trends.

How It Works

The FMS Suite integrates five essential components to assess market behavior:

Aroon Indicator : Detects trend strength and direction by analyzing the frequency of recent highs and lows over multiple timeframes. Directional Movement Index (DMI) : Measures the direction and strength of trends, with an ADX component for better trend assessment. Relative Strength Index (RSI) : Evaluates market momentum by indicating overbought or oversold conditions, with signals derived from the 50-line. Supertrend : Utilizes ATR-based volatility measures to establish dynamic support and resistance levels, signaling potential trend changes. Trix : A triple-smoothed EMA oscillator that highlights trend reversals using rate-of-change dynamics.

Each component is calculated across three separate timeframes (fast, medium, and slow), which are then averaged to produce a final FMS Signal . Users can also apply signal smoothing to reduce noise and enhance clarity.

Key Features

Customizable Parameters : Adjust the lengths for each component (fast, medium, slow) to optimize the indicator's responsiveness to different markets. Signal Smoothing Options : Select from various smoothing methods, including SMA, EMA, DEMA, and WMA, to fine-tune the FMS signal. Visual Representation : The FMS Suite plots a histogram representing the raw signal and a smoother line for clearer trend visualization. The background color shifts dynamically to indicate long, short, or neutral conditions. Threshold-Based Alerts : Set your own long and short thresholds, tailoring the indicator to your trading strategy and market outlook. Informative Table Display : An integrated table provides an at-a-glance summary of the current FMS and smoothed FMS signals, along with their respective scores and market state.

How to Use

Trend Confirmation : Utilize the FMS histogram and smoothed signal to validate or challenge existing trend assumptions. Trade Entries and Exits : Identify potential buy (long) or sell (short) signals based on the relationship between the FMS signal and predefined thresholds. Strategy Customization : Fine-tune the indicator settings to align with your trading style, whether it’s short-term scalping or long-term trend following.

Important Considerations

Not Predictive : The FMS Suite does not predict future price movements and should be used in conjunction with other analysis methods. It is based on historical price data, and past performance is not indicative of future results. Settings and Backtesting : Experiment with different lengths and smoothing techniques to optimize performance for specific instruments and market conditions. Always backtest thoroughly.