Crypto Spot Market Bot | BacktestHello Friends.

This script is only for long positions.

How does the algorithm work ?

The Relative Momentum Index

Relative Strength İndex

Average Directional Movement İndex

Momentum

When rsi and adx produce signals in the same direction, the rmi indicator confirms the signal. After the Confirmed Signal, the buy-side transaction is entered , the closed according to the % of profit taking and stoploss specified on the algorithm in the entered transaction.

In the spot market, it is possible to make money even in a down trend

All shared charts run within a 1-hour time frame.

Note : The shared backtest results have been shared as of 9/9/2021 by calculating 50% balance and 2 pyramiding methods in an account of 1000 dollars. Keep in mind that this algorithm will want to try to average down in possible worst-case scenarios. 2% - %3take profit levels will provide consecutive gains in the spot market.

How should the adjustments be made?

Value variables should be made according to formula a and formula b values and backtest results. You can increase the frequency of transactions by lowering the adx and rsi values.

Overview :

"algo" için komut dosyalarını ara

v1 Automatic Trading Bot | BacktestHello Friends.

We have been working on this script for a long time. Briefly, our scenario works as follows.

This test data includes results as of January 1, 2022 using a balance of $1000 and 10%.

WORKİNG LOGİC :

Relative Strength Index

Directional Movement Index

Relative Momentum Index

Indicators are Blended.

1 conditions are met in the overbought and oversold zone.

If the Directional Movement Index Signal is in the same direction, If all signals are in the same decision, it will be position.

We can set the take profit and stop loss levels on the algorithm as % over the entry price.

HOW TO ADJUST :

Formula a and formula b values are adjusted by increments or decrements of 1 each. these adjustments should be changed according to the time frame and chart layout.

You do not need to intervene in overbought and oversold zones. The Best Values were thus deemed appropriate.

If you still want to intervene, you need to know; When you change the overbought and oversold values, the entry time and risk will increase.

Together with the backtest script we are able to adjust the algorithm to all timeframes.

For example, while these settings are ideal for 5 minutes, it is necessary to change the strenght and formul values for a 15-minute period. This provides a user-specific adjustable strategy.

There are 6 different triggers in total on the alarm version.

Enter a long position.

Long position take profit

Long position stop loss

Enter a Short position.

Short position take profit

Short position stop loss

Currently, one platform is also connected to the binance exchange via an API .

The maximum leverage is set to 5 and a maximum of 5 trades are ordered to enter.

I will post the alarm version soon.

Good Luck Everyone !

Cava Signals Backtesting/VisualizerPLEASE READ THE DESCRIPTION CAREFULLY

Trying this again, as it seems I keep violating the rules unintentionally. Moderator, please forgive me as I try to make this right.

This backtesting/visualizer script was created for me to get a visual idea of the Cava Signals indicator throughout its development time and continuous optimization.

This script is to be used on the 30-minute timeframe on supported markets, and whether I can only publish strategies on regular candles, the indicator is meant to trigger on heikin ashi candles.I understand backtesting on non-regular candles produces unrealistic results, but I emphasize that this script is more for visualization purposes rather than accurate $ amounts from the trades. The signals are used along with a dedicated bot configuration, so part of the strategy is not managed by the script, but by the bot's config.

Some behind the scenes on what we are looking at:

a combination of ema and sma crosses on different time frames (5m, 15m, 30m, 60m and 90m) - we call this the wave trend

a combination of stochastic rsi on different time frames (10m, 30m)

a combination of schaff trend cycles on different time frames (5m, 20m and 30m)

a combination of money flow index on different time frames (10m and 30m)

volume information for each supported market/pair

and a couple of other info particular to each pair

With the above combination of data points, we try to optimize our strategy for an entry, for dca'ing down in case the coin goes down as well as dca'ing up to maximize profit when a coin is going up, take profit levels when we recognize a good time to do so, and of course, a closing level. I would like to emphasize the *visualization* purpose of this script in recognizing lows, highs, and market structure to identify the important levels to signal - this script is NOT to be used for accurate backtesting, but for an idea of the overall performance of when signals are triggered.

Let me try to explain the workflow and icons you see on the chart:

The colored circles on the bottom of the chart are all buy signals; each color corresponds to a particular buy signal, we have a combination of 9 possible situations that would trigger a buy signal. Some would trigger a buy signal only in combination with other buy signals or other indicators within the script. we also display a green upwards arrow below bars when a buy signal is triggered.

The colored arrows pointing down on the top of the chart are close signals. We have a combination of 5 closing criteria each color corresponds to one, just like the buy signals do. We only close a trade in profit. If not in profit, we will look to DCA down.

DCA signals are shown by the green flag above bars. they are signals to DCA up or down depending on the trade being negative or positive. DCA'ing up or down is also managed by the bot's configuration for limits on when to accept the signal.

Take Profit levels are shown by the green diamond above bars and work in conjunction with the bot's config on when to take the signal if at all and other take profit levels. Usually, when we hit the first take profit level we move our stop loss to entry via the bot's take profit safety feature. You can see this call with the close entry named TPS .

The black bars you may see on the chart is to illustrate when the market is extended based on a particular strategy. During this period we will not trigger a buy signal unless there is a huge spike in positive volume .

The green number below the bars is the total positive delta volume on the buy candles.

On the table on the right upper corner, we show some information on the market and performance of the backtesting - for visualization purposes only!

Currently, the script is tailored to work with the following markets/pairs:

Binance Spot: ADA, ALGO, ATOM, AVAX, BNB, BTC , DOT, ETH, LINK, LUNA, MATIC, SOL, VET, XRP, XTZ

Binance Futures: BTC , ETH, ADA, ALGO, ATOM, BNB, COMP, DOT, ENJ , LINK, OCEAN, OMG, SOL, VET, XMR, XRP, XTZ, AVAX, AAVE, DOGE, LTC, LUNA, MKR , NEAR, ONT, RUNE, SUSHI, LTC, XLM , COMP, ONT, THETA, FTM , EGLD , WAVES, ONE, HTN , CHZ , HOT, MANA, CRV , RVN, BAT, ANKR, 1INCH, ALICE, ATA , AXS , CHR , COTI, NKN , RAY, REN, SRM , SXP , TLM

ByBit Inverse Perpetual: BTCUSD , ETHUSD

ByBit Futures: AAVE, ADA, ALGO, AVAX, AXS , BNB, BTC , DOT, ETH, LINK, LTC, MATIC, SOL, SUSHI, UNI , XEM, XRP, XTZ

The chosen pairs are subject to change based on the best-performing assets we are constantly analyzing.

I hope this helps to understand the script, its purpose and ideas. I hope this satisfies the community rules - it was not my intention to break them - if there's anything on the above or the script that still violates the guidelines, please let me know and accept my apologies in advance.

If anyone would like to know more, let me know in the comment section.

Thank you!

alGROWithm Premium - Strategy TesterThe alGROWithm Strategy Tester is a supplement to the original alGROWithm indicator.

Use this strategy to do your own back testing and find the best settings that work for your asset of choice.

█ WHY THIS IS IMPORTANT

Different assets require different settings for optimal results. This strategy script will allow you back test different settings for alGROWithm in order to analyze key metrics such as win rate and P/L. TradingView functionality also enables you to view a high level performance summary and even see every single individual trade made by the algo.

█ BEST PRACTICES

Depending on the asset you are testing, it is very important to update the settings as needed. For example, if you are back testing on US30, you will likely need to increase the starting capital. For other assets, you may also need to change the order size to use the Contracts option.

It is important to decide for yourself which back testing parameter you will weigh more heavily in terms of importance. For example, a day trader may want to use a setting that maximizes win rate rather than profit % since we are humans and not computers. Further, it is highly recommended to utilize all of the rich features that TradingView provides with regards to back testing. For example, using the List of Trades tab, go back to find a failed trade and analyze the trade to see if you actually would have taken it in the moment.

After finding the best sensitivity for your asset, it is important to set that sensitivity value on the non-strategy version of alGROWithm for usage. Changing settings on this version will not carry over to the non-strategy version.

█ DEFAULT SETTINGS

We have set the following default settings on the strategy:

Starting capital: $100k

Order size: 30% of equity

Sell 1/5 of position every Take Profit level

Algonize Pivot Strategy (APS)This study is based on several Price Action parameters of :-

• Pivot Points,

• Higher High and Lower Lows,

• High Low Index ,

• Support and Resistance.

► How To Use This Strategy?

This is a pure scalping strategy and it is advised to use this only with algo trading systems. Due to high trade frequency.

► This Strategy has inbuilt custom time frame backtester, which enables you to test for performance between any date or check for a single day.

► To Create Alerts for algo trading in this strategy simply Check "Activate Algo" from Settings then Create new alert , select your strategy in condition box, and now scroll down to message box and write

{{strategy.order.comment}}

That's it , Just Click on Create Alert Button

Backtest Values Used:-

Initial Capital : 1000000

Order Size (Lots) : 1 (Contract) Lots

Pyramiding : 0 orders

Commission : 0.003%

Sharpe Ratio : 1.741

Profit Factor : 1.174

Test Yourself and give feedback.

PM us to obtain access.

Best strategy for TradingView (fake)Hello everyone! I want to show you this strategy so you don't fall for the tricks of scammers. On TradingView, you can write an algorithm (probably more than one) that will show any profit you want: from 1% to 100,000% in one year (maybe more)! This can be done, for example, using the built-in linebreak () function and several conditions for opening long and short.

I am sure that sometimes scammers show up on TradingView showing their incredible strategies. Will a smart person sell a profitable quick strategy? When a lot of people start using the quick strategy, it stops working. Therefore, no smart person would sell you a quick strategy. It is acceptable to sell slow strategies: several transactions per month - this does not greatly affect the market.

So, don't fall for the tricks of scammers, write quick strategies yourself.

About this strategy, I can say that the linebreak () function does not work correctly in it. Accordingly, the lines are not drawn correctly on the chart. They are drawn in such a way as to show the maximum profit. I watched this algorithm on a 1m timeframe - no lines are drawn in real time. This is a fake!

T3 ICL MACD STRATEGY

Backtested manually and received approx 60% winrate. Tradingview strategy tester is skewed because this program does not specify when to sell at profit target or at a stop loss.

Uses 1 min for entry and a longer time frame for confirmation (5,10,15, etc..) (Not sure what the yellow arrows are in the picture but they can be ignored)

Ideal Long Entry - The algo uses T3 moving average (T3) and the Ichimoku Conversion Line (ICL) to determine when to enter a long or short position. In this case we are going to showcase what causes the algo to alert long. It first checks to see if the the ICL is greater than T3. Once that condition is met T3 must be green in order to enter long and finally the last closing price has to be greater than the ICL. You can use the MACD to further verify a long trend as well!

Ideal Short Entry - The algo uses T3 moving average (T3) and the Ichimoku Conversion Line (ICL) to determine when to enter a long or short position. In this case we are going to showcase what causes the algo to alert short. It first checks to see if the the ICL is less than T3. Once that condition is met T3 must be red in order to enter short and finally the last closing price has to be less than the ICL. You can use the MACD to further verify a long trend as well!

KundaliniThe Kundalini is a technical indicator. Based on algorithm calculations, this indicator extrapolates the previous price for the next bar. Plus addition Multi time frame ATR volatility Reading environment for higher conditions

Here is how Dominator is calculated:

1. The study estimates the price projected for the next bar. The estimated price is based on the algorithm method.

2. The study extrapolates this value to find a projected price change for the next bar.

The resulting extrapolated value is shown as a histogram on a lower subgraph. By default, sections of the histogram where the extrapolated value is increasing are shown in green; sections corresponding to the decreasing value are shown in red.

Note: Value projection is purely mathematical as all calculations are based on algorithm averaging of previous values.

Overlay True

The strategy includes 3 different adjustable levels for the ladder , plus automatic adjustable stop loss and takes profit calculated from your average entry price after each ladder adds.

Adjustable BAcktest Window.

1 long signals

3 ladder long add signals

1 short signals

3 ladder short add signals

1 dynamic stop calculated from your average entry price

1 dynamic take profit calculated from your average entry price

Please Private Msg me if you like more info about the script Full pdf available or if you need access to it

thx for your time and support

Dominator Ladder StrategyThe Dominator is a technical indicator. Based on algorithm calculations, this indicator extrapolates the previous price for the next bar.

Here is how Dominator is calculated:

1. The study estimates the price projected for the next bar. The estimated price is based on the algorithm method.

2. The study extrapolates this value to find a projected price change for the next bar.

The resulting extrapolated value is shown as a histogram on a lower subgraph. By default, sections of the histogram where the extrapolated value is increasing are shown in green; sections corresponding to the decreasing value are shown in red.

Note: Value projection is purely mathematical as all calculations are based on algorithm averaging of previous values.

Note: lower subgraph it's just for you to understand and view the waves during the Strategy process Study it's not included in this strategy.

Overlay True

The strategy includes 3 different adjustable levels for the ladder , plus automatic adjustable stop loss and takes profit calculated from your average entry price after each ladder adds.

Adjustable BAcktest Window.

1 long signals

3 ladder long add signals

1 short signals

3 ladder short add signals

1 dynamic stop calculated from your average entry price

1 dynamic take profit calculated from your average entry price

Detrended Price Oscillator StrategyTHIS IS THE STRATEGY VERSION

What is DPO?

A detrended price oscillator is an oscillator that strips out price trends in an effort to estimate the length of price cycles from peak to peak or trough to trough. Unlike other oscillators, such as the stochastic or moving average convergence divergence (MACD), the DPO is not a momentum indicator. It highlights peaks and troughs in price, which are used to estimate buy and sell points in line with the historical cycle.

(From Investopedia )

Indicator features:

Responds faster than the original code.

Added alternative smoothing algorithms. Defaults to Ehler's Optimum Elliptic filter instead of the orginal SMA

IPOCS - can start printing out data at day 1 instead of waiting for 14 or 20 bars

Dynamic colors

Auto timeframe detection to adjust period/length

How to use:

Buy above zero

Sell below zero

Who is it for?

Long term investors - this is the perfect indicator for those who buy and hold

CLI : micro variations strategyDisclaimer :

This script is exclusively reserved to business customers.

There's no free trial.

For any request, drop us a private message.

_____________________________________________________________

Hello TV community,

Let us present our internal script strategy :

The core algorithm focuses on micro-variations (μ.var feature) calculations.

It has been developed in order to be timeframe independent : as a consequence, μ.var feature will keep a similar value scale amongst timeframes.

Preventing from any lags, the core algorithm detects any minimal and to be considered trend change (signal feature).

It's definitely a great tool for scalpers due to its core feature (micro-variations focused).

Sincerely,

SECURIX

________________________

Risk Warning : The value of your investments can go down as well as up, so you could get back less than you invested. Past performance is no guarantee of future returns.

Trend SR based strategyIt is a logical continuation of my Trend SR based indicator

Algo of strategy is next

1)Detect SR levels

2)Calculate separate channels for SR made by highs and lows

3)it takes position if the current SR is breaking and close price is not in opposite channel zone

4)It closes position if prise leave current channel zone or as an option (stoploss) if SR is breaking in an opposite direction

-uses //@version=4

-no volume needed for detecting SR breaking and entering a long position

-volume confirmation of SR breaking may be used in the option section

-volume has an option to use smoothing with MA: SMA, AHMA, VIDYA

-volume has option to use volume pump as confirmation of SR breaking (simple dev function)

-stoploss as option

-uses barstate.isconfirmed (returns true if the script is calculating the last (closing) update of the current bar) for entering position on current bar close

-as an option, all or only current SR levels detected by algo can be plotted

-option to plot SR as a channel - as FILTERED whole SR history, in a long or short position it plots only stoploss level and entering opposite position level, in no position it plots long and short entering levels

It works well on 1D

For using on 4h or lower timeframes - Volume confirmation with VIDYA or AHMA may give better results

For better work especially on LTF algo needs better detection of highs and lows, now it uses fractal filter of last bars

Dompeet Pompeet (Breakout bot)Dompeet Pompeet is my first attempt at a viable swingtrading algo.

It uses volatility and some trend analysis to enter trade when the market is about to breakout or break down. Having a trailing stop locks in profits and prevents runaway losses for low drawdown and 2:1 profit factor.

Settings to use:

BTCUSD or XBTUSD

4hr Timeframe or 2hr or 1hr (not shorter)

Bars window: 13, 16 or 20 bars

Moving average settings: 100/10 EMA to confirm trend

Trade the Trend - check on to only take trades long in a confirmed uptrend (vice versa short), otherwise it will attempt to buy and sell counter trend, which increases profits but also increases loss rate.

Trailing stop, values from 2-5% give the best results.

Take with a pinch of salt, there are some bugs in pine script which are difficult to track down but overall I'm pleased with the idea.

Trend tracking strategy of proprietary traders-RabbitThis is my latest strategy integration. It is a combination of trend tracking strategy and visualization trend. I believe it will bring you a clear trend discrimination and relatively reliable trading signal hints.

(Note: This strategy parameter has special parameter debugging and Optimization for BTC1h/BIANACE Heikin-ashi chart. It works best here. Other trade pairs or parameter versions of investment targets will be published specially if necessary.)

Statement of strategy concept:

The concept of strategy is trend tracking. The formation and continuation of trend is the product of speculation market for thousands of years. There are various strategies including CTA trend strategy, shock regression strategy, grid strategy, Martin strategy, Alpha strategy and so on. These strategies have their own merits just like different schools of Chinese knight-errant. Choose one, a master is not able to do hundreds of tricks, but to practice one trick thousands of times.

Every strategy has its own right and wrong. Trading is not violence, but a process of advancing, retreating, and making profits steadily. Therefore, the use of trend tracking strategy must overcome greed in human nature, profit and loss homology, dare to bear the shock of withdrawal in order to make a big profit when the real trend arrives. (Of course, this strategy has largely avoided filtering shocks, which will be explained later.)

Policy-building instructions:

Any trend tracking strategy can produce good results when there is a trend, so judging whether a trend strategy is good or bad depends on its withdrawal performance when it is shaking. This CTA trend tracking strategy uses Kauffman adaptive algorithm, fractal adaptive dimension, self-research algorithm and other tools, and has largely avoided filtering the signal in the shock without delay to follow the trend.

New version of the note:

The latest version adds the trend drawing of negativity, which can clearly distinguish the rising or falling or oscillating trend. However, the algorithm of strategy signal has no direct relationship with trend color. Trend color helps you to distinguish trend, and point signal helps you to refer to trade. This strategy is only a simple trading signal, risk control, warehouse management also need manual operation.

(Note: This strategy parameter has special parameter debugging and Optimization for BTC1h/BIANACE Heikin-ashi chart. It works best here. Other trade pairs or parameter versions of investment targets will be published specially if necessary.)

Good luck to all of you and a smooth deal.~

Trend tracking strategy of proprietary traders-RabbitThis is my latest strategy integration. It is a combination of trend tracking strategy and visualization trend. I believe it will bring you a clear trend discrimination and relatively reliable trading signal hints.

(Note: This strategy parameter has special parameter debugging and Optimization for BTC1h/BIANACE Heikin-ashi chart. It works best here. Other trade pairs or parameter versions of investment targets will be published specially if necessary.)

Statement of strategy concept:

The concept of strategy is trend tracking. The formation and continuation of trend is the product of speculation market for thousands of years. There are various strategies including CTA trend strategy, shock regression strategy, grid strategy, Martin strategy, Alpha strategy and so on. These strategies have their own merits just like different schools of Chinese knight-errant. Choose one, a master is not able to do hundreds of tricks, but to practice one trick thousands of times.

Every strategy has its own right and wrong. Trading is not violence, but a process of advancing, retreating, and making profits steadily. Therefore, the use of trend tracking strategy must overcome greed in human nature, profit and loss homology, dare to bear the shock of withdrawal in order to make a big profit when the real trend arrives. (Of course, this strategy has largely avoided filtering shocks, which will be explained later.)

Policy-building instructions:

Any trend tracking strategy can produce good results when there is a trend, so judging whether a trend strategy is good or bad depends on its withdrawal performance when it is shaking. This CTA trend tracking strategy uses Kauffman adaptive algorithm, fractal adaptive dimension, self-research algorithm and other tools, and has largely avoided filtering the signal in the shock without delay to follow the trend.

Additional notes for the new version:

The latest integrated version has increased the visualization of trends. It can clearly distinguish the trend of ups and downs or consolidation shocks based on chart color. However, trading signals are not calculated according to color changes, but the visualization helps you identify trends and signals help you to refer to sales.

This is only a simple trading signal strategy, and the other warehouse management and risk control need manual completion operation.

(Note: This strategy parameter has special parameter debugging and Optimization for BTC1h/BIANACE Heikin-ashi chart. It works best here. Other trade pairs or parameter versions of investment targets will be published specially if necessary.)

Good luck to all of you and a smooth deal.~

Readjusting Alpha (RA-1)The basis for this algorithm is an EMA 50/200 crossover protocol with one significant difference: it readjusts (or "learns") whether the original EMA crossover strategy is profitable based on its past performance and flips the conditions accordingly. The result is improved performance on relatively all timeframes in all statistical categories. There are options for long- and short-only trigger conditions. This algorithm is by invite only. If you have any questions about the algorithm, feel free to contact me.

Happy trades,

Sim

Matrix Trend Reverse EngineeringSelling algorithms.

Contact me to code your own indicators or strategy.

Enhanced MA Crossover Pro📝 Strategy Summary: Enhanced MA Crossover Pro

This strategy is an advanced, highly configurable moving average (MA) crossover system designed for algorithmic trading. It uses the crossover of two customizable MAs (a "Fast" MA 1 and a "Slow" MA 2) as its core entry signal, but aggressively integrates multiple technical filters, time controls, and dynamic position management to create a robust and comprehensive trading system.

💡 Core Logic

Entry Signal: A bullish crossover (MA1 > MA2) generates a Long signal, and a bearish crossover (MA1 < MA2) generates a Short signal. Users can opt to use MA crossovers from a Higher Timeframe (HTF) for the entry signal.

Confirmation/Filters: The basic MA cross signal is filtered by several optional indicators (see Filters section below) to ensure trades align with a broader trend or momentum context.

Position Management: Trades are managed with a sophisticated system of Stop Loss, Take Profit, Trailing Stops, and Breakeven stops that can be fixed, ATR-based, or dynamically adjusted.

Risk Management: Daily limits are enforced for maximum profit/loss and maximum trades per day.

⚙️ Key Features and Customization

1. Moving Averages

Primary MAs (MA1 & MA2): Highly configurable lengths (default 8 & 20) and types: EMA, WMA, SMA, or SMMA/RMA.

Higher Timeframe (HTF) MAs: Optional MAs calculated on a user-defined resolution (e.g., "60" for 1-hour) for use as an entry signal or as a trend confirmation filter.

2. Multi-Filter System

The entry signal can be filtered by the following optional conditions:

SMA Filter: Price must be above a 200-period SMA for long trades, and below it for short trades.

VWAP Filter: Price must be above VWAP for long trades, and below it for short trades.

RSI Filter: Long trades are blocked if RSI is overbought (default 70); short trades are blocked if RSI is oversold (default 30).

MACD Filter: Requires the MACD Line to be above the Signal Line for long trades (and vice versa for short trades).

HTF Confirmation: Requires the HTF MA1 to be above HTF MA2 for long entries (and vice versa).

3. Dynamic Stop and Target Management (S/L & T/P)

The strategy provides extensive control over exits:

Stop Loss Methods:

Fixed: Fixed tick amount.

ATR: Based on a multiple of the Average True Range (ATR).

Capped ATR: ATR stop limited by a maximum fixed tick amount.

Exit on Close Cross MA: Position is closed if the price crosses back over the chosen MA (MA1 or MA2).

Breakeven Stop: A stop can be moved to the entry price once a trigger distance (fixed ticks or Adaptive Breakeven based on ATR%) is reached.

Trailing Stop: Can be fixed or ATR-based, with an optional feature to auto-tighten the trailing multiplier after the breakeven condition is met.

Profit Target: Can be a fixed tick amount or a dynamic target based on an ATR multiplier.

4. Time and Session Control

Trading Session: Trades are only taken between defined Start/End Hours and Minutes (e.g., 9:30 to 16:00).

Forced Close: All open positions are closed near the end of the session (e.g., 15:45).

Trading Days: Allows specific days of the week to be enabled or disabled for trading.

5. Risk and Position Limits

Daily Profit/Loss Limits: The strategy tracks daily realized and unrealized PnL in ticks and will close all positions and block new entries if the user-defined maximum profit or maximum loss is hit.

Max Trades Per Day: Limits the number of executed trades in a single day.

🎨 Outputs and Alerts

Plots: Plots the MA1, MA2, SMA, VWAP, and HTF MAs (if enabled) on the chart.

Shapes: Plots visual markers (BUY/SELL labels) on the bar where the MA crossover occurs.

Trailing Stop: Plots the dynamic trailing stop level when a position is open.

Alerts: Generates JSON-formatted alerts for entry ({"action":"buy", "price":...}) and exit ({"action":"exit", "position":"long", "price":...}).

Vandan V2Vandan V2 is an automated trend-following strategy for NASDAQ E-mini Futures (NQ1!).

It uses multi-timeframe momentum and volatility filters to identify high-probability entries.

Includes dynamic risk management and trailing logic optimized for intraday trading.

Empire OS Trading Fully Automated Prop Firm Ready💎 Prop-Firm-Ready Momentum System v3 — The Gold-Mine Algorithm 💎

Engineered for the same standards that top prop firms demand — minimal drawdown, consistent equity growth, and precision-based execution. This isn’t a basic indicator; it’s a refined momentum engine built for traders who scale capital and manage risk like professionals.

Performance Snapshot

• Profit Factor 2.26 • Win Rate 33 % • Max Drawdown 0.9 % • Total P/L + $447 • W/L Ratio 4.6 : 1

Stress-tested on Gold (XAUUSD) across live-market conditions, it stays composed under volatility and delivers structured, data-driven consistency.

⚡ See it. Test it. Scale it.

Built for prop-firm precision — from $10 K to $300 K and beyond.

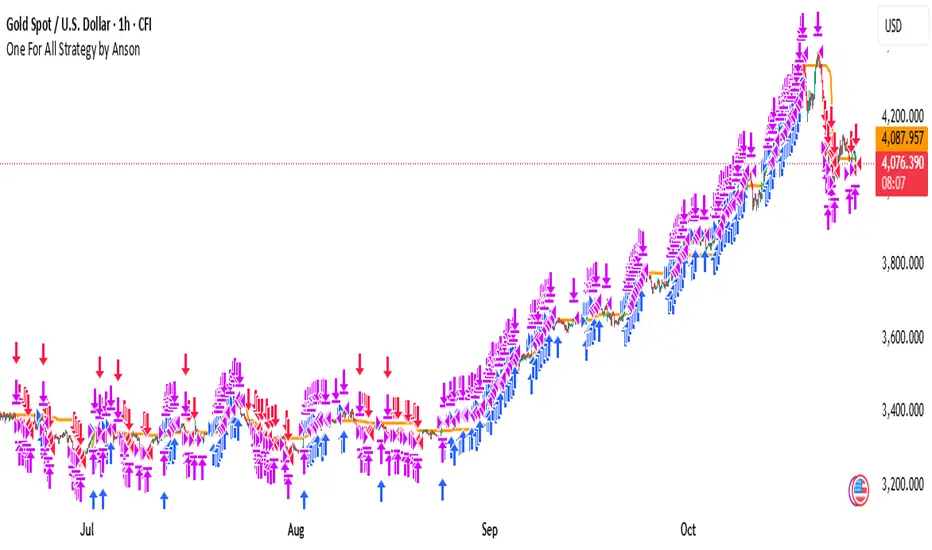

One For All Strategy by Anson🏆 Exclusive Indicator: One For All Strategy

.

📈 Works for stocks, forex, crypto, indices

📈 Easy to use, real-time alerts, no repaint

📈 No grid, no martingale, no hedging

📈 One position at a time

.

One For All Strategy by Anson

A multi-indicator TradingView strategy designed to identify long and short trading opportunities by combining trend-following and momentum signals, paired with risk management rules to guide entries and exits.

.

Core Logic & Key Indicator:

X Moving Average: A proprietary adaptive moving average that adjusts its responsiveness to price changes based on market volatility. It uses an efficiency ratio to modify its smoothing behavior—adapting to whether the market is trending or ranging. Users can toggle a setting to let this ratio dynamically adjust the indicator’s sensitivity or use a fixed smoothing factor.

.

Entry Conditions:

.

Long Entry: Triggered when momentum signals strength, price action aligns with a broader upward trend, the X MA indicates short-term upward momentum, and a minimum number of bars have passed since the last trade (to prevent overtrading).

.

Short Entry: Triggered when momentum signals weakness, price action aligns with a broader downward trend, the X MA indicates short-term downward momentum, and a minimum number of bars have passed since the last trade.

.

Exit Conditions:

.

Trailing Stop: Activates after a position has been open for a set number of bars (to avoid premature exits). A trailing stop—based on a percentage of the entry price—locks in profits as the trade moves favorably, adjusting dynamically to protect gains.

.

Additional Features:

Visualisation: Overlays the X MA (orange line) and price (semi-transparent blue) on the chart for clear signal tracking.

.

See the author's instructions on the right to learn how to get access to the strategy.

🚀 DocBrown PRO Edition V14++🚀 DocBrown PRO Edition V14++ | Advanced 10-Minute Scalping System

A sophisticated algorithmic trading bot designed for high-frequency scalping on 10-minute timeframes, delivering exceptional results with 91%+ win rate and controlled 6.5% maximum drawdown.

Key Features:

Multi-Layer EMA System with dynamic support/resistance detection

Adaptive Volatility Stop Loss (VATS) - automatically adjusts to market conditions

Smart Entry Filters - ADX-based trend detection prevents range-bound losses

Dynamic Take Profit - targets key S&R levels for optimal exits

Anti-Liquidation Protection - multiple safety mechanisms including ATR trailing stops

Momentum Derivative Logic - closes positions before reversals hit your stop loss

Breakeven Protection - locks in profits automatically after minimal gains

Risk Management Excellence:

✅ Automatic stop-loss at breakeven + commission buffer

✅ Counter-trend detection with multi-confirmation system

✅ Volume spike protection against adverse moves

✅ Stagnation exit to avoid dead positions

✅ Consecutive bar monitoring for early exit signals

Optimized for: BTC, ETH, and high-volume altcoin pairs on leverage (20x recommended)

Performance: 17.76% net profit with 34.4 profit factor - wins $34 for every $1 risked.

Perfect for traders seeking consistent scalping profits with institutional-grade risk management.

[Aegis]Original Turtle System for CryptoAs Richard Dennis once said, "Even if I published all the Turtle rules in the newspaper right now, no one would be able to 'execute' them," and 40 years later, even in modern financial markets (like the crypto market) where all the conditions have been disclosed, this strategy continues to deliver amazing performance. The following outlines the original Turtle rules as disclosed by Curtis Faith in his book *Way of the Turtle*, and a TradingView algorithm that translates these rules for application in the crypto market.

---

### **The Original Turtle Trading Rules**

#### **1. Markets**

* Trade in liquid futures markets.

#### **2. Position Sizing**

The volatility measure, **N**, is used as the basis for all calculations.

**True Range (TR) Calculation:** Select the largest of the following three values:

* Current High - Current Low

* $|\text{Current High} - \text{Previous Close}|$ (Absolute Value)

* $|\text{Current Low} - \text{Previous Close}|$ (Absolute Value)

**N (Average True Range, ATR) Calculation:**

$$N = \frac{(19 \times \text{PDN} + \text{TR})}{20}$$

* **PDN:** Previous Day's N value

* **TR:** Current True Range

This is similar to a 20-day Exponential Moving Average, and is sometimes calculated using a Simple Moving Average.

**Unit Size Calculation:**

$$\text{Unit Size (Number of Contracts)} = \frac{1\% \text{ of Account Equity}}{(\text{N} \times \text{Dollars per Point})}$$

* **Dollars per Point (Tick Value):** The value of a 1-point change in price.

#### **3. Entries**

* **Entry:** Buy when the 55-day high is broken to the upside, and sell when the 55-day low is broken to the downside.

#### **5. Stops**

* The stop-loss for every unit is set at a price **2N** unfavorable from the entry price.

* For each additional unit added, the stop price for the **entire position** is adjusted favorably by **1/2 N**.

* In other words, the stop price of the last unit entered becomes the stop price for the entire position.

#### **6. Exits**

The exit rule for profitable positions (before a stop is hit) is as follows:

* **Long Positions:** Exit when the 20-day low is broken to the downside.

* **Short Positions:** Exit when the 20-day high is broken to the upside.

*Note: This exit rule is followed only if the price has moved up by a value greater than or equal to the N value multiplied by the criterion for changing the take-profit line (the original Korean text mentions a condition based on N, which is commonly interpreted as requiring a profit before applying the channel exit).*

리처드 데니스가 앞서 "내가 지금 당장 터틀의 모든 규칙을 신문에 공표한다고 해도 아무도 '실행'하지 못할 것"라고 말했듯 40년이 흘러 모든 조건이 공개된 현대 금융시장(크립토 시장)에서도 여전히 이 전략은 놀라운 퍼포먼스를 기록하고 있습니다. 아래는 커티스 페이스가 자신의 저서 '터틀의 방식'에 공개한 오리지널 터틀 규칙과 이를 알고리즘으로 변환하여 크립토마켓에 적용한 트레이딩뷰 알고리즘 입니다.

##### 1. 시장 (Markets)

• 유동성이 풍부한 선물 시장에서 거래한다.

##### 2. 포지션 크기 (Position Sizing)

변동성 측정 단위인 N을 모든 계산의 기초로 사용한다.

**True Range (TR) 계산:** 다음 세 가지 값 중 가장 큰 값을 선택한다.

- • 현재 고가 - 현재 저가

- • |현재 고가 - 전일 종가| (절대값)

- • |현재 저가 - 전일 종가| (절대값)

**N (Average True Range, ATR) 계산:**

N = (19 × PDN + TR) / 20

- • PDN: 이전 날의 N 값

- • TR: 현재 True Range

이는 20일 지수이동평균과 유사하며, 단순이동평균으로 계산하기도 한다.

**1 유닛(Unit)의 크기 계산:**

유닛 크기 (계약 수) = 계좌 자산의 1% / (N × 틱 가치)

• 틱 가치(Dollars per Point): 1포인트 변동 시의 가치

##### 3. 진입 (Entries)

- • 진입: 55일 고가를 상향 돌파하면 매수, 55일 저가를 하향 돌파하면 매도한다.

##### 5. 손절 (Stops)

- • 모든 유닛에 대한 손절 기준은 진입 가격으로부터 2N 만큼 불리한 가격에 설정한다.

- • 유닛이 추가될 때마다 전체 포지션의 손절 가격을 1/2 N 만큼 유리한 방향으로 상향 조정한다.

- • 즉, 마지막으로 진입한 유닛의 손절 가격이 전체 포지션의 손절 가격이 된다.

##### 6. 청산 (Exits)

손절에 도달하기 전 수익 중인 포지션의 청산 규칙은 다음과 같다.

- • 매수 포지션: 20일 저가를 하향 돌파할 때 청산한다.

- • 매도 포지션: 20일 고가를 상향 돌파할 때 청산한다.

단, N값에 익절선 변경 기준을 곱한 값 이상으로 가격이 상승할 경우, 위 규칙을 따른다.