Uptrick: Volatility Adjusted TrailIntroduction

The "Uptrick: Volatility Adjusted Trail" is a dynamic trailing band indicator. It adapts in real time to changing market conditions by adjusting both to volatility and trend consistency. Inspired by Supertrend-style logic, it enhances traditional approaches by introducing adaptive mechanisms for more context-sensitive behavior in both trending and consolidating environments.

Overview

This indicator combines an exponential moving average (EMA) as its basis with an Average True Range (ATR)-derived multiplier that adjusts dynamically. Unlike fixed-multiplier tools, this indicator modifies its band distances in real time according to volatility expansion and trend persistence. The result is a trailing system that adapts to the prevailing market regime, providing traders with clearer signals for trend bias, stop placement, and potential momentum shifts.

Originality

The script’s originality lies in its multi-layered approach to trail calculation. It introduces a real-time ATR multiplier adjustment driven by two factors: a volatility expansion ratio and a trend persistence model. The expansion ratio compares the current ATR to its moving average, making the indicator more sensitive during volatile conditions and less sensitive during quieter periods. The trend persistence model assesses directional consistency to widen the bands during sustained trends. This dual adjustment method creates a system that evolves with market behavior, making it more responsive and adaptive than static-band or fixed-multiplier alternatives.

Components & Inspiration

This indicator was designed with specific components that work together:

Exponential Moving Average (EMA): Chosen as the central baseline because it responds faster to recent price changes than a simple moving average, providing a more current reference for trailing bands.

Average True Range (ATR): Used as the volatility measure because it accounts for both intraday and gap movement, making it a robust and widely accepted standard for market volatility.

Dynamic Multiplier: The multiplier is adjusted by both volatility expansion and trend persistence to produce bands that tighten during low volatility and widen during consistent trends. This combination was chosen to give the indicator the ability to self-regulate across different market regimes.

Trend Persistence Model: Integrated to assess directional consistency, ensuring the bands expand during strong trends, which can prevent premature stop-outs.

Flip Confirmation Logic: Added to filter out noise by requiring multiple bar closes beyond a band before confirming a state change, reducing false reversals.

For inspiration, the indicator draws on the core idea behind Supertrend—using a baseline and volatility-derived bands to define trailing stop levels. However, while Supertrend uses a fixed ATR multiplier, this indicator introduces a dynamic multiplier system and persistence weighting, making it more adaptive and suited for varying conditions.

Inputs and Parameters

Basis EMA Length

Defines the period for the EMA that serves as the core price reference.

ATR Length

Sets the lookback period for the Average True Range calculation used in band spacing.

Base ATR Mult

The base multiplier applied to ATR before adjustments. Forms the starting scale of the band offset.

Volatility Expansion Sensitivity

Controls how strongly the band spacing reacts to short-term volatility bursts. Higher values create more pronounced band expansions or contractions.

Trend Persistence Window

Determines how many bars are used to calculate directional trend consistency using a smoothed step function.

Persistence Impact

Scales how much influence the trend persistence has on band widening. Values range from 0 (no effect) to 1 (maximum effect).

Min Effective Mult

Sets the minimum value that the adjusted multiplier can reach. Prevents the bands from becoming too narrow.

Max Effective Mult

Sets the maximum value the adjusted multiplier can reach. Prevents the bands from over-expanding during high volatility.

Bars Above/Below to Confirm Flip

Number of consecutive bars required to close above or below the opposing trail before confirming a bullish or bearish flip. Helps reduce noise and false signals.

Show Flip Labels

Enables or disables the display of flip markers on the chart.

Label Size

Allows users to adjust the size of flip labels from Tiny to Huge.

Label ATR Offset

Adjusts the vertical placement of flip labels in relation to the trail using an ATR-based offset.

Features and Logic

EMA Basis: All calculations stem from an EMA that tracks the centerline of price action.

Dynamic ATR Multiplier: The ATR multiplier adjusts in real time based on volatility expansion and trend persistence.

Clamped Multiplier: The adjusted multiplier is limited between user-defined minimum and maximum values to keep the band scale practical.

Upper and Lower Bands: Bands are plotted above and below the EMA using the dynamic multiplier and ATR values.

Trailing Logic: The script uses Supertrend-style trailing logic, updating the active band in the current trend direction and resetting the opposite band.

Trend State Detection: A state variable tracks the current market regime (bullish, bearish, or neutral). Transitions are confirmed only after a user-specified number of bars close beyond the respective bands.

Visual Elements: Trail lines and fill zones are color-coded (bullish cyan, bearish magenta). Candlestick and bar colors match the trend state. Optional flip labels mark confirmed transitions.

Alerts: Built-in alert conditions allow users to receive real-time notifications for bullish or bearish flips.

Usage Guidelines

This indicator can be used for:

Defining context-aware dynamic stop levels that adjust with market behavior.

Identifying trend direction and reversal points based on adaptive logic.

Filtering entry or exit signals during trending vs. consolidating conditions.

Supplementing trade management strategies with responsive visual markers.

Entering long or short positions based on the appearance of flip labels and managing stop losses by following the adaptive trail.

Traders may tune the parameters to suit different trading styles or timeframes. For example, lower ATR and EMA values may suit intraday setups, while longer settings may benefit swing or positional trading.

Summary

The "Uptrick: Volatility Adjusted Trail" provides a flexible, adaptive trailing band system that accounts for both volatility and directional consistency. By combining an EMA baseline with a dynamic ATR multiplier influenced by volatility expansion and trend persistence, it creates a context-sensitive trailing system that aligns with changing market conditions. Customizable confirmation, flip labels, alerts, and dynamic visual cues make it a versatile tool for trend-following, breakout filtering, and trailing stop logic.

Disclaimer

This indicator is provided for educational and research purposes only. It does not constitute financial advice. Trading involves risk, and past performance does not guarantee future results. Always conduct your own analysis and risk management before making trading decisions.

"Volatility" için komut dosyalarını ara

Historical Volatility with HV Average & High/Low Trendlines

### 📊 **Indicator Title**: Historical Volatility with HV Average & High/Low Trendlines

**Version**: Pine Script v5

**Purpose**:

This script visualizes market volatility using **Historical Volatility (HV)** and enhances analysis by:

* Showing a **moving average** of HV to identify volatility trends.

* Marking **high and low trendlines** to highlight extremes in volatility over a selected period.

---

### 🔧 **Inputs**:

1. **HV Length (`length`)**:

Controls how many bars are used to calculate Historical Volatility.

*(Default: 10)*

2. **Average Length (`avgLength`)**:

Number of bars used for calculating the moving average of HV.

*(Default: 20)*

3. **Trendline Lookback Period (`trendLookback`)**:

Number of bars to look back for calculating the highest and lowest values of HV.

*(Default: 100)*

---

### 📈 **Core Calculations**:

1. **Historical Volatility (`hv`)**:

$$

HV = 100 \times \text{stdev}\left(\ln\left(\frac{\text{close}}{\text{close} }\right), \text{length}\right) \times \sqrt{\frac{365}{\text{period}}}

$$

* Measures how much the stock price fluctuates.

* Adjusts annualization factor depending on whether it's intraday or daily.

2. **HV Moving Average (`hvAvg`)**:

A simple moving average (SMA) of HV over the selected `avgLength`.

3. **HV High & Low Trendlines**:

* `hvHigh`: Highest HV value over the last `trendLookback` bars.

* `hvLow`: Lowest HV value over the last `trendLookback` bars.

---

### 🖍️ **Visual Plots**:

* 🔵 **HV**: Blue line showing raw Historical Volatility.

* 🔴 **HV Average**: Red line (thicker) indicating smoothed HV trend.

* 🟢 **HV High**: Green horizontal line marking volatility peaks.

* 🟠 **HV Low**: Orange horizontal line marking volatility lows.

---

### ✅ **Usage**:

* **High HV**: Indicates increased risk or potential breakout conditions.

* **Low HV**: Suggests consolidation or calm markets.

* **Cross of HV above Average**: May signal rising volatility (e.g., before breakout).

* **Touching High/Low Levels**: Helps identify volatility extremes and possible reversal zones.

Volatility-Enhanced Williams %R [AIBitcoinTrend]👽 Volatility-Enhanced Williams %R (AIBitcoinTrend)

The Volatility-Enhanced Williams %R takes the classic Williams %R oscillator to the next level by incorporating volatility-adaptive smoothing, making it significantly more responsive to market dynamics. Unlike the traditional version, which uses a fixed calculation method, this indicator dynamically adjusts its smoothing factor based on market volatility, helping traders capture trends more effectively while filtering out noise.

Additionally, the indicator includes real-time divergence detection and an ATR-based trailing stop system, providing traders with enhanced risk management tools and early reversal signals.

👽 What Makes the Volatility-Enhanced Williams %R Unique?

Unlike the standard Williams %R, which applies a simple lookback-based formula, this version integrates adaptive smoothing and volatility-based filtering to refine its signals and reduce false breakouts.

✅ Volatility-Adaptive Smoothing – Adjusts dynamically based on standard deviation, enhancing signal accuracy.

✅ Real-Time Divergence Detection – Identifies bullish and bearish divergences for early trend reversal signals.

✅ Crossovers & Trailing Stops – Implements Williams %R crossovers with ATR-based trailing stops for intelligent trade management.

👽 The Math Behind the Indicator

👾 Volatility-Adaptive Smoothing

The indicator smooths the Williams %R calculation by applying an adaptive filtering mechanism, which adjusts its responsiveness based on market conditions. This helps to eliminate whipsaws and makes trend-following strategies more reliable.

The smoothing function is defined as:

clamp(x, lo, hi) => math.min(math.max(x, lo), hi)

adaptive(src, prev, len, divisor, minAlpha, maxAlpha) =>

vol = ta.stdev(src, len)

alpha = clamp(vol / divisor, minAlpha, maxAlpha)

prev + alpha * (src - prev)

Where:

Volatility Factor (vol) measures price dispersion using standard deviation.

Adaptive Alpha (alpha) dynamically adjusts smoothing strength.

Clamped Output ensures that the smoothing factor remains within a stable range.

👽 How Traders Can Use This Indicator

👾 Divergence Trading Strategy

Bullish Divergence Setup:

Price makes a lower low, while Williams %R forms a higher low.

Buy signal is confirmed when Williams %R reverses upward.

Bearish Divergence Setup:

Price makes a higher high, while Williams %R forms a lower high.

Sell signal is confirmed when Williams %R reverses downward.

👾 Trailing Stop & Signal-Based Trading

Bullish Setup:

✅ Williams %R crosses above trigger level → Buy signal.

✅ A bullish trailing stop is placed at Low - (ATR × Multiplier).

✅ Exit if price crosses below the stop.

Bearish Setup:

✅ Williams %R crosses below trigger level → Sell signal.

✅ A bearish trailing stop is placed at High + (ATR × Multiplier).

✅ Exit if price crosses above the stop.

👽 Why It’s Useful for Traders

Adaptive Filtering Mechanism – Avoids excessive noise while maintaining responsiveness.

Real-Time Divergence Alerts – Helps traders anticipate market reversals before they occur.

ATR-Based Risk Management – Stops dynamically adjust based on market volatility.

Multi-Market Compatibility – Works effectively across stocks, forex, crypto, and futures.

👽 Indicator Settings

Smoothing Factor – Controls how aggressively the indicator adapts to volatility.

Enable Divergence Analysis – Activates real-time divergence detection.

Lookback Period – Defines the number of bars for detecting pivot points.

Enable Crosses Signals – Turns on Williams %R crossover-based trade signals.

ATR Multiplier – Adjusts trailing stop sensitivity.

Disclaimer: This indicator is designed for educational purposes and does not constitute financial advice. Please consult a qualified financial advisor before making investment decisions.

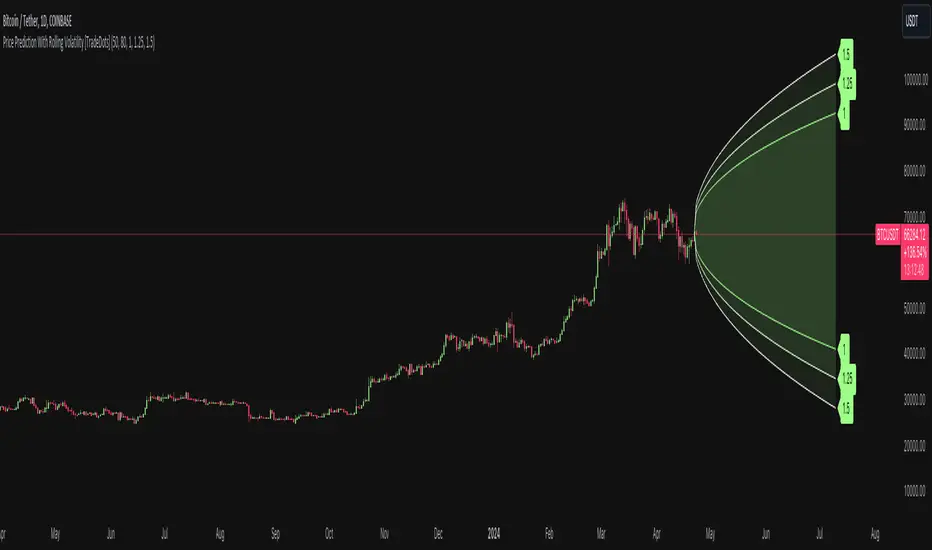

Price Prediction With Rolling Volatility [TradeDots]The "Price Prediction With Rolling Volatility" is a trading indicator that estimates future price ranges based on the volatility of price movements within a user-defined rolling window.

HOW DOES IT WORK

This indicator utilizes 3 types of user-provided data to conduct its calculations: the length of the rolling window, the number of bars projecting into the future, and a maximum of three sets of standard deviations.

Firstly, the rolling window. The algorithm amasses close prices from the number of bars determined by the value in the rolling window, aggregating them into an array. It then calculates their standard deviations in order to forecast the prospective minimum and maximum price values.

Subsequently, a loop is initiated running into the number of bars into the future, as dictated by the second parameter, to calculate the maximum price change in both the positive and negative direction.

The third parameter introduces a series of standard deviation values into the forecasting model, enabling users to dictate the volatility or confidence level of the results. A larger standard deviation correlates with a wider predicted range, thereby enhancing the probability factor.

APPLICATION

The purpose of the indicator is to provide traders with an understanding of the potential future movement of the price, demarcating maximum and minimum expected outcomes. For instance, if an asset demonstrates a substantial spike beyond the forecasted range, there's a significantly high probability of that price being rejected and reversed.

However, this indicator should not be the sole basis for your trading decisions. The range merely reflects the volatility within the rolling window and may overlook significant historical price movements. As with any trading strategies, synergize this with other indicators for a more comprehensive and reliable analysis.

Note: In instances where the number of predicted bars is exceedingly high, the lines may become scattered, presumably due to inherent limitations on the TradingView platform. Consequently, when applying three SD in your indicator, it is advised to limit the predicted bars to fewer than 80.

RISK DISCLAIMER

Trading entails substantial risk, and most day traders incur losses. All content, tools, scripts, articles, and education provided by TradeDots serve purely informational and educational purposes. Past performances are not definitive predictors of future results.

EWMA Implied Volatility based on Historical VolatilityVolatility is the most common measure of risk.

Volatility in this sense can either be historical volatility (one observed from past data), or it could implied volatility (observed from market prices of financial instruments.)

The main objective of EWMA is to estimate the next-day (or period) volatility of a time series and closely track the volatility as it changes.

The EWMA model allows one to calculate a value for a given time on the basis of the previous day's value.

The EWMA model has an advantage in comparison with SMA, because the EWMA has a memory.

The EWMA remembers a fraction of its past by a factor A, that makes the EWMA a good indicator of the history of the price movement if a wise choice of the term is made.

Full details regarding the formula :

www.investopedia.com

In this scenario, we are looking at the historical volatility using the anual length of 252 trading days and a monthly length of 21.

Once we apply all of that we are going to get the yearly volatility.

After that we just have to divide that by the square root of number of days in a year, or weeks in a year or months in a year in order to get the daily/weekly/monthly expected volatility.

Once we have the expected volatility, we can estimate with a high chance where the market top and bottom is going to be and continue our analysis on that premise.

If you have any questions, please let me know !

Relative Normalized VolatilityThere are plenty of indicators that aim to measure the volatility (degree of variation) in the price of an instrument, the most well known being the average true range and the rolling standard deviation. Volatility indicators form the key components of most bands and trailing stops indicators, but can also be used to normalize oscillators, they are therefore extremely versatile.

Today proposed indicator aim to compare the estimated volatility of two instruments in order to provide various informations to the user, especially about risk and profitability.

CALCULATION

The relative normalized volatility (RNV) indicator is the ratio between the moving average of the absolute normalized price changes value of two securities, that is:

SMA(|Δ(a)/σ(a)|)

―――――――――――

SMA(|Δ(b)/σ(b)|)

Where a and b are two different securities (note that notation "Δ(x)" refer to the 1st difference of x, and the "||" notation is used to indicate absolute value, for example "|x|" means absolute value of x) .

INTERPRETATION

The indicator aim tell us which security is more volatile between a and b , with a value of the indicator greater than 1 indicating that a is on average more volatile than b over the last length period, while a value lower than 1 indicating that the security b is more on average volatile than a .

The indicator use the current symbol as a , while the second security b must be defined in the setting window (by default the S&P500). Risk and profitability are closely related to volatility, as larger price variations could potentially mean larger losses (but also larger gains), therefore a value of the indicator greater than 1 can indicate that it could be more risked (and profitable) to trade security a .

RNV using AMD (top) volatility against Intel (bottom) volatility.

RNV using EURUSD (top) volatility against USDJPY (bottom) volatility.

Larger values of length will make the indicator fluctuate less often around 1. You can also plot the logarithm of the ratio instead in order to have the indicator centered around 0, it will also help make values originally below 1 have more importance in the scale.

POSSIBLE ERRORS

If you compare different types of markets the indicator might return NaN values, this is because one market might be closed, for example if you compare AMD against BTCUSD with the indicator you will get NaN values. If you really need to compare two markets then increase your time frame, else use an histogram or area plot in order to have a cleaner plot.

CONCLUSION

An original indicator comparing the volatility between two securities has been presented. The choice of posting a volatility indicator has been made by my twitter followers, so if you want to decide which type of indicator i should do next make sure to check my twitter to see if there are polls available (i should do one after every posted indicator).

Scott’s ATR volatility histogram with smoothingATR shows volatility. The sma of the ATR (default=14 period) shows the average volatility over the look-back period, (default=200 period.)

When volatility is higher than average, the histogram turns green. When volatility is less than average, the histogram turns red. This shows volatility expansion and contraction. Volatility expansion is a good confirmation for entering a trade position. Volatility contraction is a sign that a trend is not developing.

Now I have added an sma which acts as a smoothing of expanding or contracting volatility. When the histogram is higher than this smoothing (default=21) then volatility expansion momentum is creasing. WWhen the histogram is lower than the smoothing sma, volatility contraction momentum is increasing.

I introduce an idea that volatility momentum can be used as a substitute for volatility expansion and contraction.

Now we have volatility expansion momentum and volatility contraction momentum.

Dynamic Volatility Channel (DVC) - Smooth

The indicator's adaptability comes from a unique blend of well-known concepts:

The Adaptive Engine (ADX): The indicator uses the Average Directional Index (ADX) in the background to analyze the strength of the trend. This acts as the "brain", telling the channel whether the market is trending strongly or moving sideways.

Hybrid Volatility: This is the core of the indicator. The width of the channel is determined by a weighted mix of two volatility measures:

In trending markets (high ADX), the channel gives more weight to the Average True Range (ATR).

In ranging markets (low ADX), the channel gives more weight to Standard Deviation.

Smooth Centerline (HMA): The channel is centered around a Hull Moving Average (HMA), which is known for its smoothness and reduced lag compared to other moving averages.

Advanced Smoothing Layers: This version includes dedicated smoothing for both the volatility components (ATR and StDev) and the logic that switches between regimes. This ensures the channel expands, contracts, and adapts in a very fluid manner, eliminating sudden jumps and reducing market noise.

Mean Reversion: In ranging markets (indicated by a flatter channel), the outer bands can act as dynamic support and resistance levels. Look for opportunities to sell near the upper band and buy near the lower band, always waiting for price action confirmation like reversal candles.

Trend Following: In strong trends (indicated by a steeply sloped channel), the centerline (HMA) often serves as a dynamic level of support (in an uptrend) or resistance (in a downtrend). Pullbacks to the centerline can present opportunities to join the trend. A "band ride," where price action consistently pushes against the upper or lower band, signals a very strong trend.

Volatility Analysis: A "squeeze," where the bands come very close together, indicates low volatility and can foreshadow a significant price breakout. A sudden expansion of the bands signals an increase in volatility and the potential start of a new, powerful move.

All core parameters are fully customizable to suit your trading style and preferred assets:

You can adjust the lengths for the HMA, ATR, StDev, and the ADX filter.

You can change the multipliers for the ATR and Standard Deviation components.

Crucially, you can control the Volatility Smoothing Length and Logic Smoothing Length to find the perfect balance between responsiveness and smoothness.

Disclaimer: This indicator is provided for educational and analytical purposes only. It is not financial advice, and past performance is not indicative of future results. Always conduct your own research and backtesting before risking capital in a live market.

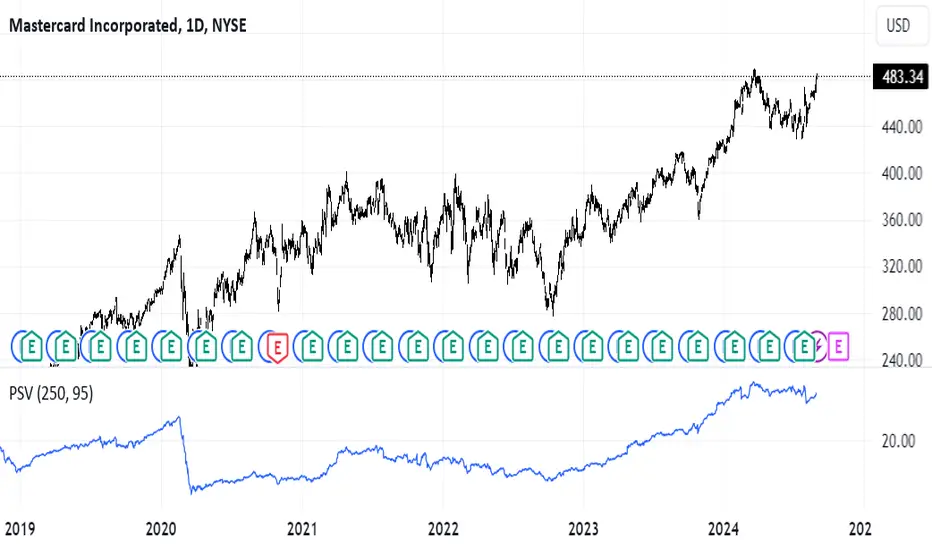

Position Sizer by VolatilityDescription :

The **Position Sizer by Volatility (PSV)** is an indicator that helps traders determine what percentage of their deposit a position will occupy, taking into account the current market volatility. PSV calculates the range of price movements over recent periods and shows how large this movement is compared to historical data. The lower the value, the lower the volatility, and the smaller the stop-loss required relative to the current price.

Explanation of PSV Parameters:

- ` len ` (Period Length):** This parameter sets the number of candles (bars) on the chart that will be used to calculate volatility. For example, if `len` is set to 250, the indicator will analyze price movements over the last 250 bars. The larger the value, the longer the period used for volatility assessment.

- ` percent ` (Percentile):** This parameter determines how strong price fluctuations you want to account for. For instance, if you set `percent` to 95, the indicator will focus on the 5% of instances where the price range was the largest over the specified period. This helps evaluate volatility during periods of sharp price movements, which may require a larger stop-loss. A higher percentile accounts for rarer but stronger movements, and vice versa.

Advanced Volatility Oscillator with SignalsTitle: Advanced Volatility Oscillator with Signals (AVO-S)

In-Depth Description:

Introduction:

The Advanced Volatility Oscillator with Signals (AVO-S) is designed to offer traders a nuanced understanding of market volatility, combining traditional concepts with innovative visual aids and signal interpretation. This indicator is tailored for diverse financial markets, helping to identify potential trend reversals and momentum shifts.

Calculation and Methodology:

Spike Calculation: The core of AVO-S is the 'spike', calculated as the difference between the closing and opening prices (spike = close - open). This measure provides a straightforward gauge of intra-period volatility.

Standard Deviation: The indicator employs standard deviation to assess the variability of the 'spike', offering a dynamic threshold for understanding market extremities (stdDev = stdev(spike, length)).

Colored Columns: These columns visually represent the 'spike'. Their color changes based on the spike’s value relative to the zero line and the standard deviation threshold, providing an immediate visual cue of market state.

Blue Columns: Indicate moderate positive movement when the spike is above zero but below the standard deviation.

Green and Red Columns: Suggest stronger bullish (above standard deviation) and bearish (below negative standard deviation) movements, respectively.

Bullish and Bearish Signals:

The indicator generates signals based on the relationship between the 'spike' and its standard deviation.

Bullish Signals: Shown as upward triangles, these are formed when the 'spike' crosses above the standard deviation, indicating potential upward momentum.

Bearish Signals: Represented by downward triangles, these signals are generated when the 'spike' falls below the negative standard deviation, hinting at potential downward trends.

Usage and Application:

Traders can use the colored columns to quickly assess market sentiment and volatility.

The bullish and bearish signals serve as potential indicators for market entry or exit points, or for further analysis in conjunction with other technical tools.

Inspiration and Credits:

Inspired by Veryfid's original Volatility Oscillator, the AVO-S refines and builds upon these ideas to provide a comprehensive and user-friendly tool for market analysis. This indicator is a testament to the continuous evolution of technical analysis tools in the trading community.

Natenberg's VolatilityThis indicator is historical volatility indicator created by Sheldon Natenberg , as the standard deviation of the logarithmic price changes measured at regular intervals of time.

In Mr. Natenberg's book, Option Volatility & Pricing, he covers volatility in detail and gives the formula for computing historical volatility.

My changes :

I didn't changed formula, i just added smooth version of volatility it can be used as trigger when cross(over/under) non-smoothed volatility.

Note:

There is two formulas for daily and weekly. Indicator showing only daily formula !

Who wants to display the weekly formula change line 17, namely remove "//"

Enjoy!

Volatility/Volume ImpactWe often hear statements such as follow the big volume to project possible price movements. Or low volatility is good for trend. How much of it is statistically right for different markets. I wrote this small script to study the impact of Volatility and Volume on price movements.

Concept is as below:

Compare volume with a reference median value. You can also use moving average or other types for this comparison.

If volume is higher than median, increment positive value impact with change in close price. If volume is less than median, then increment negative value impact with change in close price.

With this we derive pvd and nvd which are measure of price change when volume is higher and lower respectively. pvd measures the price change when volume is higher than median whereas nvd measures price change when volume is lower than median.

Calculate correlation of pvd and nvd with close price to see what is impacting the price by higher extent.

Colors are applied to plots which have higher correlation to price movement. For example, if pvd has higher correlation to price movement, then pvd is coloured green whereas nvd is coloured silver. Similarly if nvd has higher correlation to price then nvd is coloured in red whereas pvd is coloured in silver.

Similar calculation also applied for volatility.

With this, you can observe how price change is correlated to high/low volume and volatility.

Let us see some examples on different markets.

Example 1: AMEX:SPY

From the chart snapshot below, it looks evident that SPY always thrive when there is low volatility and LOW VOLUME!!

Example 2: NASDAQ:TSLA

The picture will be different if you look at individual stocks. For Tesla, the price movement is more correlated to high volume (unlike SPY where low volume days define the trend)

Example 3: KUCOIN:BTCUSDT

Unlike stocks and indices, high volatility defined the trend for BTC for long time. It thrived when volatility is more. We can see that high volume is still major influencer in BTC price movements.

Settings are very simple and self explanatory.

Hint: You can also move the indicator to chart overlay for better visualisation of comparison with close price.

Wilder's Volatility Trailing Stop Strategy with various MA'sFor Educational Purposes. Results can differ on different markets and can fail at any time. Profit is not guaranteed.

This only works in a few markets and in certain situations. Changing the settings can give better or worse results for other markets. This strategy is based on Wilder's Volatility System. It is an ATR trailing stop that is used for long term trends. This strategy focuses on the trailing stop alone and goes long and short only when it goes above or below the trailing line. It is similar to Donchian channels except it does not include the certain period channel breakout, only the trailing signal. This is only the trailing stop and an attempt to show how well it works standalone as Wilder described.

In his book, Wilder recommends a multiplier of 2.8-3.1 and an ATR lookback of 7 periods along with a running moving average or otherwise known as Wilder's moving average. The calculation and programming part for the trailing stop varies everywhere. I opted to keep it as simple and accurate as I could think of and interpret from the book. The variations to these types of indicators are numerous unfortunately, but Wilder seems to be the original author of ATR and this ATR-based trailing stop. In his book he says to use the significant closing price or highest/lowest closing price for the calculation part but I also included the option of choosing the highest high and lowest low, and the option to choose various moving averages in case anyone wants to experiment.

Comparing this and Donchian channels, it seems that a 2.5 multiplier is somewhat similar to the middle band of DCs and a 3.0 multiplier is somewhat similar to a double length middle band of DCs. It's hard to say which is the better trailing stop for a long term strategy. It's hard to beat the simplicity of DCs but maybe some might find a need for more inputs in a trailing stop or maybe an ATR based one like Wilder's can work better depending on what setting or strategy it's used in.

Volatility Stop Flow [AR]The indicator is designed to scan cross multiple timeframes and display the Volatility Stop Value.

Realized Volatility IIR Filters with BandsDISCLAIMER:

The Following indicator/code IS NOT intended to be a formal investment advice or recommendation by the author, nor should be construed as such. Users will be fully responsible by their use regarding their own trading vehicles/assets.

The following indicator was made for NON LUCRATIVE ACTIVITIES and must remain as is following TradingView's regulations. Use of indicator and their code are published by Invitation Only for work and knowledge sharing. All access granted over it, their use, copy or re-use should mention authorship(s) and origin(s).

WARNING NOTICE!

THE INCLUDED FUNCTION MUST BE CONSIDERED AS TESTING. The models included in the indicator have been taken from open sources on the web and some of them has been modified by the author, problems could occur at diverse data sceneries.

WHAT'S THIS...?

Work derived by previous own research for study:

This is mainly an INFINITE IMPULSE RESPONSE FILTERING INDICATOR , it's purpose is to catch trend given by the nature of lag given by a VOLATILITY ESTIMATION ALGORITHM as it's coefficient. It provides as well an INFINITE IMPULSE RESPONSE DEVIATION FILTER that uses the same coefficients of the main filter to plot deviation bands as an auxiliary tool.

The given Filter based indicator provides my own Multi Volatility-Estimators Function with only 3 models:

ELASTIC VOLUME WEIGHTED VOLATILITY : This is a Modified Daigler & Padungsaksawasdi "Volume Weighted Volatility" as on DOI: 10.1504/IJBAAF.2018.089423 but with Elastic Volume Weighted Moving Average instead of VWAP (intraday) for faster (but inaccurate) calculation. A future version is planned on the way using intra-bar inspection for intraday timeframe as described in original paper.

GARMAN & KLASS / YANG-ZANG EXTENSION : As one of the best range based (OHLC) with open gaps inclusion in a single bar.

PETER MARTIN'S ULCER INDEX : This is a better approach to measure realized volatility than standard deviation of log returns given it's proven convex risk metric for DrawDowns as shown in Chekhlov et al. (2005) . Regarding this particular model, I take a different approach to use it as coefficient feed: Given that the UI only takes in consideration DrawDawns, I code myself the inverse of this to compute Draw-Ups as well and use both of them to filter minimums volatility levels in order to create a SLOW version of the IIR filter, and maximums of both to calculate as FAST variation. This approach can be used as a better proxy instead of any other common moving average given that with NO COMPOUND IN TIME AT ALL (N=1) or only using as long as N=3 bars of compund, the filter can catch a trend easily, making the indicator nearly a NON PARAMETRIC FILTER.

NOTES:

This version DO NOT INCLUDE ALERTS.

This version DO NOT INCLUDE STRATEGY: ALL Feedback welcome.

DERIVED WORK:

Incremental calculation of weighted mean and variance by Tony Finch (fanf2@cam. ac .uk) (dot@dotat.at), 2009.

Volume weighted volatility: empirical evidence for a new realised volatility measure by Chaiyuth Padungsaksawasdi & Robert T. Daigler, 2018.

Basic DSP Tips & Trics by TradingView user @alexgrover

CHEERS!

@XeL_Arjona 2020.

JPMorgan G7 Volatility IndexThe JPMorgan G7 Volatility Index: Scientific Analysis and Professional Applications

Introduction

The JPMorgan G7 Volatility Index (G7VOL) represents a sophisticated metric for monitoring currency market volatility across major developed economies. This indicator functions as an approximation of JPMorgan's proprietary volatility indices, providing traders and investors with a normalized measurement of cross-currency volatility conditions (Clark, 2019).

Theoretical Foundation

Currency volatility is fundamentally defined as "the statistical measure of the dispersion of returns for a given security or market index" (Hull, 2018, p.127). In the context of G7 currencies, this volatility measurement becomes particularly significant due to the economic importance of these nations, which collectively represent more than 50% of global nominal GDP (IMF, 2022).

According to Menkhoff et al. (2012, p.685), "currency volatility serves as a global risk factor that affects expected returns across different asset classes." This finding underscores the importance of monitoring G7 currency volatility as a proxy for global financial conditions.

Methodology

The G7VOL indicator employs a multi-step calculation process:

Individual volatility calculation for seven major currency pairs using standard deviation normalized by price (Lo, 2002)

- Weighted-average combination of these volatilities to form a composite index

- Normalization against historical bands to create a standardized scale

- Visual representation through dynamic coloring that reflects current market conditions

The mathematical foundation follows the volatility calculation methodology proposed by Bollerslev et al. (2018):

Volatility = σ(returns) / price × 100

Where σ represents standard deviation calculated over a specified timeframe, typically 20 periods as recommended by the Bank for International Settlements (BIS, 2020).

Professional Applications

Professional traders and institutional investors employ the G7VOL indicator in several key ways:

1. Risk Management Signaling

According to research by Adrian and Brunnermeier (2016), elevated currency volatility often precedes broader market stress. When the G7VOL breaches its high volatility threshold (typically 1.5 times the 100-period average), portfolio managers frequently reduce risk exposure across asset classes. As noted by Borio (2019, p.17), "currency volatility spikes have historically preceded equity market corrections by 2-7 trading days."

2. Counter-Cyclical Investment Strategy

Low G7 volatility periods (readings below the lower band) tend to coincide with what Shin (2017) describes as "risk-on" environments. Professional investors often use these signals to increase allocations to higher-beta assets and emerging markets. Campbell et al. (2021) found that G7 volatility in the lowest quintile historically preceded emerging market outperformance by an average of 3.7% over subsequent quarters.

3. Regime Identification

The normalized volatility framework enables identification of distinct market regimes:

- Readings above 1.0: Crisis/high volatility regime

- Readings between -0.5 and 0.5: Normal volatility regime

- Readings below -1.0: Unusually calm markets

According to Rey (2015), these regimes have significant implications for global monetary policy transmission mechanisms and cross-border capital flows.

Interpretation and Trading Applications

G7 currency volatility serves as a barometer for global financial conditions due to these currencies' centrality in international trade and reserve status. As noted by Gagnon and Ihrig (2021, p.423), "G7 currency volatility captures both trade-related uncertainty and broader financial market risk appetites."

Professional traders apply this indicator in multiple contexts:

- Leading indicator: Research from the Federal Reserve Board (Powell, 2020) suggests G7 volatility often leads VIX movements by 1-3 days, providing advance warning of broader market volatility.

- Correlation shifts: During periods of elevated G7 volatility, cross-asset correlations typically increase what Brunnermeier and Pedersen (2009) term "correlation breakdown during stress periods." This phenomenon informs portfolio diversification strategies.

- Carry trade timing: Currency carry strategies perform best during low volatility regimes as documented by Lustig et al. (2011). The G7VOL indicator provides objective thresholds for initiating or exiting such positions.

References

Adrian, T. and Brunnermeier, M.K. (2016) 'CoVaR', American Economic Review, 106(7), pp.1705-1741.

Bank for International Settlements (2020) Monitoring Volatility in Foreign Exchange Markets. BIS Quarterly Review, December 2020.

Bollerslev, T., Patton, A.J. and Quaedvlieg, R. (2018) 'Modeling and forecasting (un)reliable realized volatilities', Journal of Econometrics, 204(1), pp.112-130.

Borio, C. (2019) 'Monetary policy in the grip of a pincer movement', BIS Working Papers, No. 706.

Brunnermeier, M.K. and Pedersen, L.H. (2009) 'Market liquidity and funding liquidity', Review of Financial Studies, 22(6), pp.2201-2238.

Campbell, J.Y., Sunderam, A. and Viceira, L.M. (2021) 'Inflation Bets or Deflation Hedges? The Changing Risks of Nominal Bonds', Critical Finance Review, 10(2), pp.303-336.

Clark, J. (2019) 'Currency Volatility and Macro Fundamentals', JPMorgan Global FX Research Quarterly, Fall 2019.

Gagnon, J.E. and Ihrig, J. (2021) 'What drives foreign exchange markets?', International Finance, 24(3), pp.414-428.

Hull, J.C. (2018) Options, Futures, and Other Derivatives. 10th edn. London: Pearson.

International Monetary Fund (2022) World Economic Outlook Database. Washington, DC: IMF.

Lo, A.W. (2002) 'The statistics of Sharpe ratios', Financial Analysts Journal, 58(4), pp.36-52.

Lustig, H., Roussanov, N. and Verdelhan, A. (2011) 'Common risk factors in currency markets', Review of Financial Studies, 24(11), pp.3731-3777.

Menkhoff, L., Sarno, L., Schmeling, M. and Schrimpf, A. (2012) 'Carry trades and global foreign exchange volatility', Journal of Finance, 67(2), pp.681-718.

Powell, J. (2020) Monetary Policy and Price Stability. Speech at Jackson Hole Economic Symposium, August 27, 2020.

Rey, H. (2015) 'Dilemma not trilemma: The global financial cycle and monetary policy independence', NBER Working Paper No. 21162.

Shin, H.S. (2017) 'The bank/capital markets nexus goes global', Bank for International Settlements Speech, January 15, 2017.

Volatility Adjusted Profit Target

In my 'Volatility Adjusted Profit Target' indicator, I've crafted a dynamic tool for calculating target profit percentages suitable for both long and short trading strategies. It evaluates the highest and lowest prices over the anticipated duration of your trade, establishing a profit target that shifts with market volatility. As volatility increases, the potential for profit follows, with the target percentage rising accordingly; conversely, it declines with decreasing volatility. As a trader, setting an optimal Take Profit level has always been a challenge. This indicator not only helps in determining that level but also dynamically adjusts it throughout the trade's duration, providing a strategic edge in volatile markets.

Implied Volatility PercentileThis script calculates the Implied Volatility (IV) based on the daily returns of price using a standard deviation. It then annualizes the 30 day average to create the historical Implied Volatility. This indicator is intended to measure the IV for options traders but could also provide information for equities traders to show how price is extended in the expected price range based on the historical volatility.

The IV Rank (Green line) is then calculated by looking at the high and low volatility over the number of days back specified in the input parameter, default is 252 (trading days in 1 year) and then calculating the rank of the current IV compared to the High and Low. This is not as reliable as the IV Percentile as the and extreme high or low could have a side effect on the ranking but it is included for those that want to use.

The IV Percentile is calculated by counting the number of days below the current IV, then returns this as a % of the days back in the input

You can adjust the number of days back to check the IV Rank & IV Percentile if you are not wanting to look back a whole year.

This will only work on Daily or higher timeframe charts.

Volatility-Targeted Momentum Portfolio [BackQuant]Volatility-Targeted Momentum Portfolio

A complete momentum portfolio engine that ranks assets, targets a user-defined volatility, builds long, short, or delta-neutral books, and reports performance with metrics, attribution, Monte Carlo scenarios, allocation pie, and efficiency scatter plots. This description explains the theory and the mechanics so you can configure, validate, and deploy it with intent.

Table of contents

What the script does at a glance

Momentum, what it is, how to know if it is present

Volatility targeting, why and how it is done here

Portfolio construction modes: Long Only, Short Only, Delta Neutral

Regime filter and when the strategy goes to cash

Transaction cost modelling in this script

Backtest metrics and definitions

Performance attribution chart

Monte Carlo simulation

Scatter plot analysis modes

Asset allocation pie chart

Inputs, presets, and deployment checklist

Suggested workflow

1) What the script does at a glance

Pulls a list of up to 15 tickers, computes a simple momentum score on each over a configurable lookback, then volatility-scales their bar-to-bar return stream to a target annualized volatility.

Ranks assets by raw momentum, selects the top 3 and bottom 3, builds positions according to the chosen mode, and gates exposure with a fast regime filter.

Accumulates a portfolio equity curve with risk and performance metrics, optional benchmark buy-and-hold for comparison, and a full alert suite.

Adds visual diagnostics: performance attribution bars, Monte Carlo forward paths, an allocation pie, and scatter plots for risk-return and factor views.

2) Momentum: definition, detection, and validation

Momentum is the tendency of assets that have performed well to continue to perform well, and of underperformers to continue underperforming, over a specific horizon. You operationalize it by selecting a horizon, defining a signal, ranking assets, and trading the leaders versus laggards subject to risk constraints.

Signal choices . Common signals include cumulative return over a lookback window, regression slope on log-price, or normalized rate-of-change. This script uses cumulative return over lookback bars for ranking (variable cr = price/price - 1). It keeps the ranking simple and lets volatility targeting handle risk normalization.

How to know momentum is present .

Leaders and laggards persist across adjacent windows rather than flipping every bar.

Spread between average momentum of leaders and laggards is materially positive in sample.

Cross-sectional dispersion is non-trivial. If everything is flat or highly correlated with no separation, momentum selection will be weak.

Your validation should include a diagnostic that measures whether returns are explained by a momentum regression on the timeseries.

Recommended diagnostic tool . Before running any momentum portfolio, verify that a timeseries exhibits stable directional drift. Use this indicator as a pre-check: It fits a regression to price, exposes slope and goodness-of-fit style context, and helps confirm if there is usable momentum before you force a ranking into a flat regime.

3) Volatility targeting: purpose and implementation here

Purpose . Volatility targeting seeks a more stable risk footprint. High-vol assets get sized down, low-vol assets get sized up, so each contributes more evenly to total risk.

Computation in this script (per asset, rolling):

Return series ret = log(price/price ).

Annualized volatility estimate vol = stdev(ret, lookback) * sqrt(tradingdays).

Leverage multiplier volMult = clamp(targetVol / vol, 0.1, 5.0).

This caps sizing so extremely low-vol assets don’t explode weight and extremely high-vol assets don’t go to zero.

Scaled return stream sr = ret * volMult. This is the per-bar, risk-adjusted building block used in the portfolio combinations.

Interpretation . You are not levering your account on the exchange, you are rescaling the contribution each asset’s daily move has on the modeled equity. In live trading you would reflect this with position sizing or notional exposure.

4) Portfolio construction modes

Cross-sectional ranking . Assets are sorted by cr over the chosen lookback. Top and bottom indices are extracted without ties.

Long Only . Averages the volatility-scaled returns of the top 3 assets: avgRet = mean(sr_top1, sr_top2, sr_top3). Position table shows per-asset leverages and weights proportional to their current volMult.

Short Only . Averages the negative of the volatility-scaled returns of the bottom 3: avgRet = mean(-sr_bot1, -sr_bot2, -sr_bot3). Position table shows short legs.

Delta Neutral . Long the top 3 and short the bottom 3 in equal book sizes. Each side is sized to 50 percent notional internally, with weights within each side proportional to volMult. The return stream mixes the two sides: avgRet = mean(sr_top1,sr_top2,sr_top3, -sr_bot1,-sr_bot2,-sr_bot3).

Notes .

The selection metric is raw momentum, the execution stream is volatility-scaled returns. This separation is deliberate. It avoids letting volatility dominate ranking while still enforcing risk parity at the return contribution stage.

If everything rallies together and dispersion collapses, Long Only may behave like a single beta. Delta Neutral is designed to extract cross-sectional momentum with low net beta.

5) Regime filter

A fast EMA(12) vs EMA(21) filter gates exposure.

Long Only active when EMA12 > EMA21. Otherwise the book is set to cash.

Short Only active when EMA12 < EMA21. Otherwise cash.

Delta Neutral is always active.

This prevents taking long momentum entries during obvious local downtrends and vice versa for shorts. When the filter is false, equity is held flat for that bar.

6) Transaction cost modelling

There are two cost touchpoints in the script.

Per-bar drag . When the regime filter is active, the per-bar return is reduced by fee_rate * avgRet inside netRet = avgRet - (fee_rate * avgRet). This models proportional friction relative to traded impact on that bar.

Turnover-linked fee . The script tracks changes in membership of the top and bottom baskets (top1..top3, bot1..bot3). The intent is to charge fees when composition changes. The template counts changes and scales a fee by change count divided by 6 for the six slots.

Use case: increase fee_rate to reflect taker fees and slippage if you rebalance every bar or trade illiquid assets. Reduce it if you rebalance less often or use maker orders.

Practical advice .

If you rebalance daily, start with 5–20 bps round-trip per switch on liquid futures and adjust per venue.

For crypto perp microcaps, stress higher cost assumptions and add slippage buffers.

If you only rotate on lookback boundaries or at signals, use alert-driven rebalances and lower per-bar drag.

7) Backtest metrics and definitions

The script computes a standard set of portfolio statistics once the start date is reached.

Net Profit percent over the full test.

Max Drawdown percent, tracked from running peaks.

Annualized Mean and Stdev using the chosen trading day count.

Variance is the square of annualized stdev.

Sharpe uses daily mean adjusted by risk-free rate and annualized.

Sortino uses downside stdev only.

Omega ratio of sum of gains to sum of losses.

Gain-to-Pain total gains divided by total losses absolute.

CAGR compounded annual growth from start date to now.

Alpha, Beta versus a user-selected benchmark. Beta from covariance of daily returns, Alpha from CAPM.

Skewness of daily returns.

VaR 95 linear-interpolated 5th percentile of daily returns.

CVaR average of the worst 5 percent of daily returns.

Benchmark Buy-and-Hold equity path for comparison.

8) Performance attribution

Cumulative contribution per asset, adjusted for whether it was held long or short and for its volatility multiplier, aggregated across the backtest. You can filter to winners only or show both sides. The panel is sorted by contribution and includes percent labels.

9) Monte Carlo simulation

The panel draws forward equity paths from either a Normal model parameterized by recent mean and stdev, or non-parametric bootstrap of recent daily returns. You control the sample length, number of simulations, forecast horizon, visibility of individual paths, confidence bands, and a reproducible seed.

Normal uses Box-Muller with your seed. Good for quick, smooth envelopes.

Bootstrap resamples realized returns, preserving fat tails and volatility clustering better than a Gaussian assumption.

Bands show 10th, 25th, 75th, 90th percentiles and the path mean.

10) Scatter plot analysis

Four point-cloud modes, each plotting all assets and a star for the current portfolio position, with quadrant guides and labels.

Risk-Return Efficiency . X is risk proxy from leverage, Y is expected return from annualized momentum. The star shows the current book’s composite.

Momentum vs Volatility . Visualizes whether leaders are also high vol, a cue for turnover and cost expectations.

Beta vs Alpha . X is a beta proxy, Y is risk-adjusted excess return proxy. Useful to see if leaders are just beta.

Leverage vs Momentum . X is volMult, Y is momentum. Shows how volatility targeting is redistributing risk.

11) Asset allocation pie chart

Builds a wheel of current allocations.

Long Only, weights are proportional to each long asset’s current volMult and sum to 100 percent.

Short Only, weights show the short book as positive slices that sum to 100 percent.

Delta Neutral, 50 percent long and 50 percent short books, each side leverage-proportional.

Labels can show asset, percent, and current leverage.

12) Inputs and quick presets

Core

Portfolio Strategy . Long Only, Short Only, Delta Neutral.

Initial Capital . For equity scaling in the panel.

Trading Days/Year . 252 for stocks, 365 for crypto.

Target Volatility . Annualized, drives volMult.

Transaction Fees . Per-bar drag and composition change penalty, see the modelling notes above.

Momentum Lookback . Ranking horizon. Shorter is more reactive, longer is steadier.

Start Date . Ensure every symbol has data back to this date to avoid bias.

Benchmark . Used for alpha, beta, and B&H line.

Diagnostics

Metrics, Equity, B&H, Curve labels, Daily return line, Rolling drawdown fill.

Attribution panel. Toggle winners only to focus on what matters.

Monte Carlo mode with Normal or Bootstrap and confidence bands.

Scatter plot type and styling, labels, and portfolio star.

Pie chart and labels for current allocation.

Presets

Crypto Daily, Long Only . Lookback 25, Target Vol 50 percent, Fees 10 bps, Regime filter on, Metrics and Drawdown on. Monte Carlo Bootstrap with Recent 200 bars for bands.

Crypto Daily, Delta Neutral . Lookback 25, Target Vol 50 percent, Fees 15–25 bps, Regime filter always active for this mode. Use Scatter Risk-Return to monitor efficiency and keep the star near upper left quadrants without drifting rightward.

Equities Daily, Long Only . Lookback 60–120, Target Vol 15–20 percent, Fees 5–10 bps, Regime filter on. Use Benchmark SPX and watch Alpha and Beta to keep the book from becoming index beta.

13) Suggested workflow

Universe sanity check . Pick liquid tickers with stable data. Thin assets distort vol estimates and fees.

Check momentum existence . Run on your timeframe. If slope and fit are weak, widen lookback or avoid that asset or timeframe.

Set risk budget . Choose a target volatility that matches your drawdown tolerance. Higher target increases turnover and cost sensitivity.

Pick mode . Long Only for bull regimes, Short Only for sustained downtrends, Delta Neutral for cross-sectional harvesting when index direction is unclear.

Tune lookback . If leaders rotate too often, lengthen it. If entries lag, shorten it.

Validate cost assumptions . Increase fee_rate and stress Monte Carlo. If the edge vanishes with modest friction, refine selection or lengthen rebalance cadence.

Run attribution . Confirm the strategy’s winners align with intuition and not one unstable outlier.

Use alerts . Enable position change, drawdown, volatility breach, regime, momentum shift, and crash alerts to supervise live runs.

Important implementation details mapped to code

Momentum measure . cr = price / price - 1 per symbol for ranking. Simplicity helps avoid overfitting.

Volatility targeting . vol = stdev(log returns, lookback) * sqrt(tradingdays), volMult = clamp(targetVol / vol, 0.1, 5), sr = ret * volMult.

Selection . Extract indices for top1..top3 and bot1..bot3. The arrays rets, scRets, lev_vals, and ticks_arr track momentum, scaled returns, leverage multipliers, and display tickers respectively.

Regime filter . EMA12 vs EMA21 switch determines if the strategy takes risk for Long or Short modes. Delta Neutral ignores the gate.

Equity update . Equity multiplies by 1 + netRet only when the regime was active in the prior bar. Buy-and-hold benchmark is computed separately for comparison.

Tables . Position tables show current top or bottom assets with leverage and weights. Metric table prints all risk and performance figures.

Visualization panels . Attribution, Monte Carlo, scatter, and pie use the last bars to draw overlays that update as the backtest proceeds.

Final notes

Momentum is a portfolio effect. The edge comes from cross-sectional dispersion, adequate risk normalization, and disciplined turnover control, not from a single best asset call.

Volatility targeting stabilizes path but does not fix selection. Use the momentum regression link above to confirm structure exists before you size into it.

Always test higher lag costs and slippage, then recheck metrics, attribution, and Monte Carlo envelopes. If the edge persists under stress, you have something robust.

volatility-adjusted breakout envelopethis indicator is designed to help traders visually identify potential entry and exit points based on volatility-adjusted price thresholds. it works by calculating a dynamic expected price move around the previous close using historical volatility data smoothed by exponential moving averages to reduce noise and present a clear range boundary on the chart.

the indicator first computes the logarithmic returns over a user-defined lookback period and calculates the standard deviation of these returns, which represents raw volatility. it annualizes this volatility according to the chart timeframe selected, then uses it to estimate an expected price movement for the current timeframe. this expected move is smoothed to avoid sudden spikes or drops that could cause confusing signals.

using this expected move, the indicator generates two key threshold lines: an upper threshold and a lower threshold. these lines create a volatility-based range around the smoothed previous close price. the thresholds themselves are further smoothed with exponential moving averages to produce smooth, easy-to-interpret lines that adapt to changing market conditions without being choppy.

the core trading signals are generated when the price closes outside of these smoothed threshold ranges. specifically, a long entry signal is indicated when the price closes above the upper threshold for the first time, signaling potential upward momentum beyond normal volatility expectations. a short entry signal occurs when the price closes below the lower threshold for the first time, indicating potential downward momentum.

once an entry signal is triggered, the indicator waits for the price to close back inside the threshold range before signaling an exit. when this occurs, an exit marker is displayed to indicate that the price has returned within normal volatility bounds, which may suggest that the previous trend is losing strength or the breakout has ended.

these signals are visually represented on the chart using small shapes: triangles pointing upwards mark the initial long entries, triangles pointing downwards mark short entries, and x shapes mark the exits for both long and short positions. the colors of these shapes are customizable to suit user preferences.

to use this indicator effectively, traders should watch for the first close outside the smoothed volatility range to consider entering a position in the breakout direction. the exit signals help identify when price action reverts back into the expected range, which can be used to close or reduce the position. this method emphasizes trading breakouts supported by statistically significant moves relative to recent volatility while providing a clear exit discipline.

this indicator is best applied to intraday or daily charts with consistent volatility and volume characteristics. users should adjust the volatility lookback period, smoothing factor, and trading session times to match their specific market and trading style. because it relies on price volatility rather than fixed price levels, it can adapt to changing market conditions but should be combined with other analysis tools and proper risk management.

overall, this indicator provides a smoothed, dynamic volatility envelope with clear visual entry and exit cues based on first closes outside and back inside these envelopes, making it a helpful assistant for manual traders seeking to capture statistically significant breakouts while maintaining disciplined exits.

Volatility Trend Bands [UAlgo]The Volatility Trend Bands is a trend-following indicator that combines the concepts of volatility and trend detection. Built using the Average True Range (ATR) to measure volatility, this indicator dynamically adjusts upper and lower bands around price movements. The bands act as dynamic support and resistance levels, making it easier to identify trend shifts and potential entry and exit points.

With the ATR multiplier, this indicator effectively captures volatility-based shifts in the market. The use of midline values allows for accurate trend detection, which is displayed through color-coded signals on the chart. Additionally, this tool provides clear buy and sell signals, accompanied by intuitive graphical markers for ease of use.

The Volatility Trend Bands is ideal for traders seeking an adaptive trend-following method that responds to changing market conditions while maintaining robust volatility control.

🔶 Key Features

Dynamic Support and Resistance: The indicator utilizes volatility to create dynamic bands. The upper band acts as resistance, and the lower band acts as support for the price. Wider bands indicate higher volatility, while narrower bands indicate lower volatility.

Customizable Inputs

You can tailor the indicator to your strategy by adjusting the:

Price Source: Select the price data (e.g., closing price) used for calculations.

ATR Length: Define the lookback period for the Average True Range (ATR) volatility measure.

ATR Multiplier: This factor controls the width of the volatility bands relative to the ATR value.

Color Options: Choose colors for the bands and signal arrows for better visualization.

Visual Signals: Arrows ("▲" for buy, "▼" for sell) appear on the chart when the trend changes, providing clear entry point indications.

Alerts: Integrated alerts for both buy and sell conditions, allowing you to receive notifications for potential trade opportunities.

🔶 Interpreting Indicator

Upper and Lower Bands: The upper and lower bands are dynamic, adjusting based on market volatility using the ATR. These bands serve as adaptive support and resistance levels. When price breaks above the upper band, it indicates a potential bullish breakout, signaling a strong uptrend. Conversely, a break below the lower band signals a bearish breakout, indicating a downtrend.

Buy/Sell Signals: The indicator provides clear buy and sell signals at breakout points. A buy signal ("▲") is generated when the price breaks above the upper band, suggesting the start of a bullish trend. A sell signal ("▼") is triggered when the price breaks below the lower band, indicating the beginning of a bearish trend. These signals help traders identify potential entry and exit points at key breakout levels.

Color-Coded Bars: The bars on the chart change color based on the trend direction. Teal bars represent bullish momentum, while purple bars signify bearish momentum. This color coding provides a quick visual cue about the market's current direction.

🔶 Disclaimer

Use with Caution: This indicator is provided for educational and informational purposes only and should not be considered as financial advice. Users should exercise caution and perform their own analysis before making trading decisions based on the indicator's signals.

Not Financial Advice: The information provided by this indicator does not constitute financial advice, and the creator (UAlgo) shall not be held responsible for any trading losses incurred as a result of using this indicator.

Backtesting Recommended: Traders are encouraged to backtest the indicator thoroughly on historical data before using it in live trading to assess its performance and suitability for their trading strategies.

Risk Management: Trading involves inherent risks, and users should implement proper risk management strategies, including but not limited to stop-loss orders and position sizing, to mitigate potential losses.

No Guarantees: The accuracy and reliability of the indicator's signals cannot be guaranteed, as they are based on historical price data and past performance may not be indicative of future results.

Universal Volatility IndexThe Universal Volatility Index (UVI) is a robust indicator designed to gauge market volatility across various asset classes. By synthesizing multiple volatility measures, the UVI offers traders a nuanced understanding of market dynamics, aiding in the assessment of risk and the decision-making process.

How It Works:

The UVI incorporates three key components to calculate a composite volatility score:

Average True Range (ATR): This represents the average volatility over the specified period, giving a base measure of market movement.

Bollinger Bands Width: Highlights the expansion or contraction of price ranges, offering insights into market volatility relative to recent price action.

Rate of Change (ROC): Captures the momentum or the velocity of price changes, adding a temporal dimension to volatility assessment.

By combining these components, the UVI delivers a singular volatility metric that adapts to changing market conditions, providing a valuable tool for traders in any market.

Usage:

To apply the UVI to your chart, add the indicator from the Pine Script library and adjust the input parameters as desired.

The plot will display a line representing the composite volatility score, with higher values indicating increased market volatility and lower values suggesting calmer market conditions.

Benefits:

The UVI is versatile and can be applied to any market, making it a universal tool for traders.

The indicator helps in identifying periods of high risk where tighter risk management may be warranted.

It assists in pinpointing potential breakouts when volatility is expanding after a period of consolidation.

Compliance with TradingView House Rules:

This script is provided for educational purposes and does not constitute financial advice. It has been created to contribute to the TradingView community by offering a versatile tool that helps traders understand and navigate market volatility.