MAX1 Ord. Volatility Market ScannerScan volatility of 40 pair, print result in label ordered form higher or lower volatility

Use it in combination with MAX2 Ord. Volatility Market Scanner for have 80 coin scan

"Volatility" için komut dosyalarını ara

[A618] Historical Volatility Bands

Historical Volatility Bands

To be used over 5 mins for best results

HVB is a standard deviation measure for Historical Volatility Percentile,

It helps you figure out the next level of Support and Resistances

> If the HVB width is narrow, its an indication for a Trending market day

> Price crossing the highest green band line symbolises a nice upmove

> Price crossing the lowest red band line symbolises a nice downmove

> Green and Red lines are levels of Support and Resistances with respect to Historical Volatility

Credits

Historical Volatility Percentile calculation part : @cheatcountry

Link to cheatcountry idea

Hope this Helps!

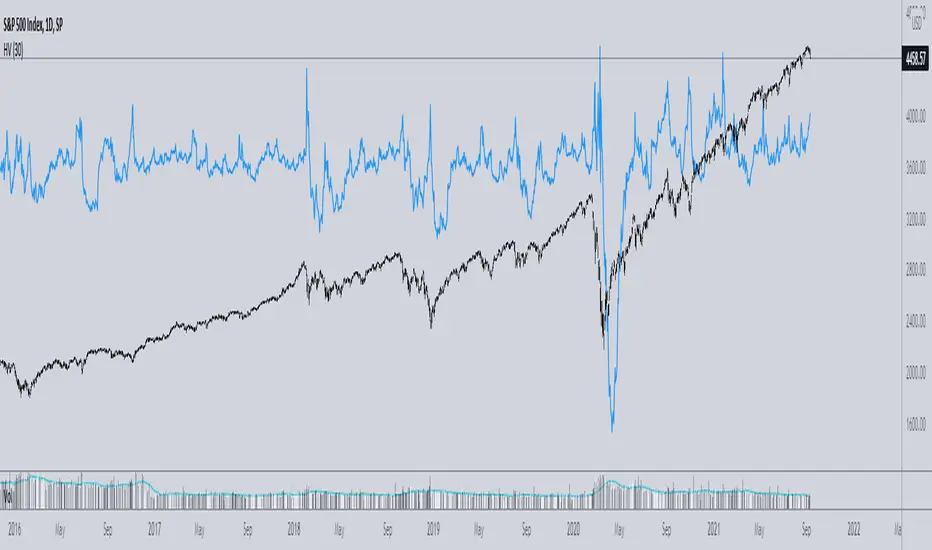

Implied minus Historical VolatilityJust a simple comparison of 30 day historical volatility versus 30 day implied volatility(VIX). In general, when VIX is way above realized or historical Vol, in general that is quite bullish. Backtest will be available soon.

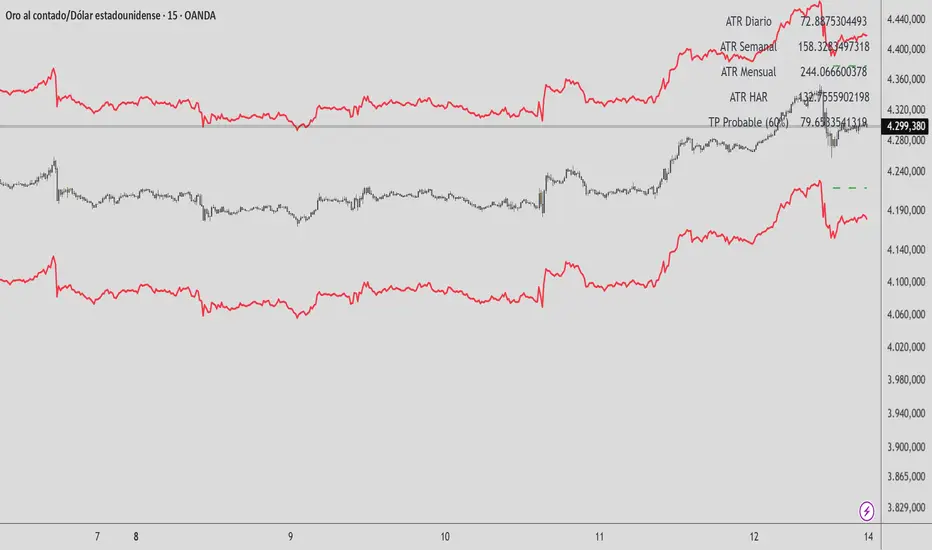

HAR Volatility ATR (Multi-Asset) - Andreus VillalobosIndicator based on the HAR (Hyper-Realized Volatility) model.

Combines daily, weekly, and monthly ATRs to project:

– Most probable price range (90%)

– Most probable take profit (60%)

Does not generate entry signals.

Designed for use in conjunction with:

market structure, liquidity, and price action.

Works on Forex, Indices, Gold, and Cryptocurrencies.

HAR Volatility ATR v1.0 (Andreus Villalobos)

Indicator based on the HAR (Hyper-Realized Volatility) model.

Combines daily, weekly, and monthly ATRs to project:

– Most probable price range (90%)

– Most probable take profit (60%)

Does not generate entry signals.

Designed for use in conjunction with:

market structure, liquidity, and price action.

Works on Forex, Indices, Gold, and Cryptocurrencies.

ATR Volatility HistogramATR Volatility Histogram showing result as coloured histogram where Rising > Greenand Fallig < Red. Input can be varied in settings.

Vince/Williams Extreme Volatility VulnerabilityDescription: This indicator implements the "Period of Extreme Vulnerability" concept developed by Ralph Vince and Larry Williams. The theory posits that a healthy market must regularly see the number of New Lows "dry up" (drop to near zero). When the percentage of New Lows fails to drop below a minimal threshold (default 0.15%) for a prolonged period (default 65 days), it indicates that internal market structure is rotting even if prices are rising, leaving the market fragile and prone to sudden volatility shocks.

I have programmed this script to track that exact condition—the extended absence of a "low" New Lows reading. It applies a 50-day Moving Average filter to contextually categorize the signal:

Red Dot (Crash Warning): Triggers when the vulnerability period begins while the price is above the 50 SMA. This is the classic warning signal, indicating that an uptrend is unsupported by market internals and a sharp correction may be imminent.

Green Dot (Contrarian Buy): Triggers when the vulnerability period begins while the price is below the 50 SMA. The script identifies this as a potential capitulation or value point where the persistent internal weakness is likely already priced in.

Note: This indicator requires exchange-wide data (New Lows, Advancers, Decliners) to function. It is best used on daily timeframes.

Relative Measured Volatility (RMV)RMV • Volume-Sensitive Consolidation Indicator

A lightweight Pine Script that highlights true low-volatility, low-volume bars in a single squeeze measure.

What it does

Calculates each bar’s raw High-Low range.

Down-weights bars where volume is below its 30-day average, emphasizing genuine quiet periods.

Normalizes the result over the prior 15 bars (excluding the current bar), scaling from 0 (tightest) to 100 (most volatile).

Draws the series as a step plot, shades true “tight” bars below the user threshold, and marks sustained squeezes with a small arrow.

Key inputs

Lookback (bars): Number of bars to use for normalization (default 15).

Tight Threshold: RMV value under which a bar is considered squeezed (default 15).

Volume SMA Period: Period for the volume moving average benchmark (default 30).

How it works

Raw range: barRange = high - low

Volume ratio: volRatio = min(volume / sma(volume,30), 1)

Weighted range: vwRange = barRange * volRatio

Rolling min/max (prior 15 bars): exclude today so a new low immediately registers a 0.

Normalize: rmv = clamp(100 * (vwRange - min) / (max - min), 0, 100)

Visualization & signals

Step line for exact bar-by-bar values.

Shaded background when RMV < threshold.

Consecutive-bar filter ensures arrows only appear when tightness lasts at least two bars, cutting noise.

Why use it

Quickly spot consolidation zones that combine narrow price action with genuine dry volume—ideal for swing entries ahead of breakouts.

Crypto Market VolatilityCross market look at different Crypto markets ans their growth from the lowest value in 6 hours.

Green = +10% growth

Orange = 0 001- 9.99% growth

red = lowest price in last 6 hours

Use 1 minutes candles.Orange lines signify less volatility for bots.

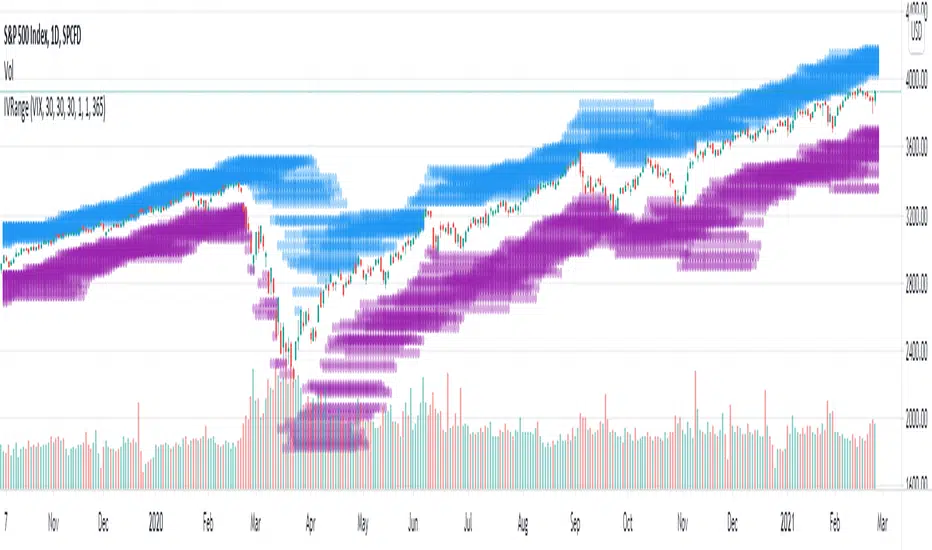

Implied Volatility Range ProjectionThis script plots an expected future range estimation based on implied volatilities, using a specified volatility index as proxy for ATM implied volatilities.

For example the S&P 500 could use the VIX.

Please help to make Larry Williams' volatility breakthrough.Hello Traders!

I'm going to backtest Larry Williams' volatility breakthrough strategy.

However, contrary to my expectation, orders at certain bars are made the next day.

Is there anything I missed at my pine script code?

Please give me any tiny tips.

Thank you!!

Historical VolatilityNothing special here, just an open source Historical Volatility, for my own practice more than anything else.

Decided to make it public just because maybe somebody can edit it (as the TV standard one's source code is locked) and put in adaptive lengths or whatever else they want to do.

Just leave me a credit if you use it somehow.

Cheers.

[WJ] - Volatility RangeA simple script to find the percentage or cash value of volatility in the specified length. Handy for setting your target profit and/or loss numbers.

Exponential weighted volatilityEstimator of current annualized volatility that works for daily, weekly, monthly timeframes.

Lambda should be choosen inside the 0 to 1 range, with a lower lambda giving more weight to the movement in the most recent candlesticks. The literature default is 0.97, I'm setting a default value of 0.94 instead.

Relative Volatility Index + EMA + HTF RVI// this Script is based on

// added EMA of RVI

// added HTF RVI

// for HTF RVI i use at least 3xcurrent TF

// if RVI goes below EMA and HTF RVI -> weakness

// if RVI goes above EMA and HTF RVI -> strength

Volatility Trend (Zeiierman)█ Overview

The Volatility Trend (Zeiierman) is an indicator designed to help traders identify and analyze market trends based on price volatility. By calculating a dynamic trend line and volatility-adjusted bands, the indicator provides visual cues to understand the current market direction, potential reversal points and volatility.

█ How It Works

The indicator uses a weighted moving average of historical prices to create a responsive trend line that is adjusted for volatility using standard deviation. The indicator sets upper and lower bands at intervals of two standard deviations, acting as markers for potential overbought or oversold conditions. Additionally, by comparing current and previous trend line values, the indicator identifies the trend direction, providing crucial insights for traders.

█ How to Use

Trend Identification

Use the trend line to identify the overall market direction. An upward-sloping line indicates an uptrend, while a downward-sloping line indicates a downtrend.

Volatility Assessment

Use the distance between the upper and lower bands to gauge market volatility. Wider bands indicate higher volatility, while narrower bands indicate lower volatility.

Overbought/Oversold

If the price reaches or exceeds the upper or lower bands, it may be in an overbought or oversold condition, respectively.

█ Settings

Trend Control: Adjusts the sensitivity and smoothness of the trend line. Lower values make the trend more responsive, while higher values make it smoother.

Trend Dynamic: Controls how quickly the trend adjusts to price changes. Higher values result in a slower adjustment.

Volatility: Consists of two parts - the scaling factor for volatility and the sensitivity for volatility adjustment. Adjusting these settings alters the distance between the trend lines and the price, as well as how sensitive the bands are to changes in volatility.

Squeeze Control: Influences the degree to which market squeeze is considered in the calculation, with higher values increasing sensitivity.

Enable Scalping Trend: A toggle that, when activated, makes the indicator focus on short-term trends, which is particularly useful for scalping strategies.

█ Related scripts with the same calculation philosophy

TrendCylinder

TrendSphere

Predictive Trend and Structure

-----------------

Disclaimer

The information contained in my Scripts/Indicators/Ideas/Algos/Systems does not constitute financial advice or a solicitation to buy or sell any securities of any type. I will not accept liability for any loss or damage, including without limitation any loss of profit, which may arise directly or indirectly from the use of or reliance on such information.

All investments involve risk, and the past performance of a security, industry, sector, market, financial product, trading strategy, backtest, or individual's trading does not guarantee future results or returns. Investors are fully responsible for any investment decisions they make. Such decisions should be based solely on an evaluation of their financial circumstances, investment objectives, risk tolerance, and liquidity needs.

My Scripts/Indicators/Ideas/Algos/Systems are only for educational purposes!

Volatility Cone Forecaster Lite [PhenLabs]📊 Volatility Cone Forecaster

Version: PineScript™v6

📌Description

The Volatility Cone Forecaster (VCF) is an advanced indicator designed to provide traders with a forward-looking perspective on market volatility. Instead of merely measuring past price fluctuations, the VCF analyzes historical volatility data to project a statistical “cone” that outlines a probable range for future price movements. Its core purpose is to contextualize the current market environment, helping traders to anticipate potential shifts from low to high volatility periods (and vice versa). By identifying whether volatility is expanding or contracting relative to historical norms, it solves the critical problem of preparing for significant market moves before they happen, offering a clear statistical edge in strategy development.

This indicator moves beyond lagging measures by employing percentile analysis to rank the current volatility state. This allows traders to understand not just what volatility is, but how significant it is compared to the recent past. The VCF is built for discretionary traders, system developers, and options strategists who need a sophisticated understanding of market dynamics to manage risk and identify high-probability opportunities.

🚀Points of Innovation

Forward-Looking Volatility Projection: Unlike standard indicators that only show historical data, the VCF projects a statistical cone of future volatility.

Percentile-Based Regime Analysis: Ranks current volatility against historical data (e.g., 90th, 75th percentiles) to provide objective context.

Automated Regime Detection: Automatically identifies and labels the market as being in a ‘High’, ‘Low’, or ‘Normal’ volatility regime.

Expansion & Contraction Signals: Clearly indicates whether volatility is currently increasing or decreasing, signaling shifts in market energy.

Integrated ATR Comparison: Plots an ATR-equivalent volatility measure to offer a familiar point of reference against the statistical model.

Dynamic Visual Modeling: The cone visualization directly on the price chart provides an intuitive guide for future expected price ranges.

🔧Core Components

Realized Volatility Engine: Calculates historical volatility using log returns over multiple user-defined lookback periods (short, medium, long) for a comprehensive view.

Percentile Analysis Module: A custom function calculates the 10th, 25th, 50th, 75th, and 90th percentiles of volatility over a long-term lookback (e.g., 252 days).

Forward Projection Calculator: Uses the calculated volatility percentiles to mathematically derive and draw the upper and lower bounds of the future volatility cone.

Volatility Regime Classifier: A logic-based system that compares current volatility to the historical percentile bands to classify the market state.

🔥Key Features

Customizable Lookback Periods: Adjust short, medium, and long-term lookbacks to fine-tune the indicator’s sensitivity to different market cycles.

Configurable Forward Projection: Set the number of days for the forward cone projection to align with your specific trading horizon.

Interactive Display Options: Toggle visibility for percentile labels, ATR levels, and regime coloring to customize the chart display.

Data-Rich Information Table: A clean, on-screen table displays all key metrics, including current volatility, percentile rank, regime, and trend.

Built-in Alert Conditions: Set alerts for critical events like volatility crossing the 90th percentile, dropping below the 10th, or switching between expansion and contraction.

🎨Visualization

Volatility Cone: Shaded bands projected onto the future price axis, representing the probable price range at different statistical confidence levels (e.g., 75th-90th percentile).

Color-Coded Volatility Line: The primary volatility plot dynamically changes color (e.g., red for high, green for low) to reflect the current volatility regime, providing instant context.

Historical Percentile Bands: Horizontal lines plotted across the indicator pane mark the key percentile levels, showing how current volatility compares to the past.

On-Chart Labels: Clear labels automatically display the current volatility reading, its percentile rank, the detected regime, and trend (Expanding/Contracting).

📖Usage Guidelines

Setting Categories

Short-term Lookback: Default: 10, Range: 5-50. Controls the most sensitive volatility calculation.

Medium-term Lookback: Default: 21, Range: 10-100. The primary input for the current volatility reading.

Long-term Lookback: Default: 63, Range: 30-252. Provides a baseline for long-term market character.

Percentile Lookback Period: Default: 252, Range: 100-1000. Defines the period for historical ranking; 252 represents one trading year.

Forward Projection Days: Default: 21, Range: 5-63. Determines how many bars into the future the cone is projected.

✅Best Use Cases

Breakout Trading: Identify periods of deep consolidation when volatility falls to low percentile ranks (e.g., below 25th) and begins to expand, signaling a potential breakout.

Mean Reversion Strategies: Target trades when volatility reaches extreme high percentile ranks (e.g., above 90th), as these periods are often unsustainable and lead to contraction.

Options Strategy: Use the cone’s projected upper and lower bounds to help select strike prices for strategies like iron condors or straddles.

Risk Management: Widen stop-losses and reduce position sizes when the indicator signals a transition into a ‘High’ volatility regime.

⚠️Limitations

Probabilistic, Not Predictive: The cone represents a statistical probability, not a guarantee of future price action. Extreme, unpredictable news events can drive prices outside the cone.

Lagging by Nature: All calculations are based on historical price data, meaning the indicator will always react to, not pre-empt, market changes.

Non-Directional: The indicator forecasts the *magnitude* of future moves, not the *direction*. It should be paired with a directional analysis tool.

💡What Makes This Unique

Forward Projection: Its primary distinction is projecting a data-driven, statistical forecast of future volatility, which standard oscillators do not do.

Contextual Analysis: It doesn’t just provide a number; it tells you what that number means through percentile ranking and automated regime classification.

🔬How It Works

1. Data Calculation:

The indicator first calculates the logarithmic returns of the asset’s price. It then computes the annualized standard deviation of these returns over short, medium, and long-term lookback periods to generate realized volatility readings.

2. Percentile Ranking:

Using a 252-day lookback, it analyzes the history of the medium-term volatility and determines the values that correspond to the 10th, 25th, 50th, 75th, and 90th percentiles. This builds a statistical map of the asset’s volatility behavior.

3. Cone Projection:

Finally, it takes these historical percentile values and projects them forward in time, calculating the potential upper and lower price bounds based on what would happen if volatility were to run at those levels over the next 21 days.

💡Note:

The Volatility Cone Forecaster is most effective on daily and weekly charts where statistical volatility models are more reliable. For lower timeframes, consider shortening the lookback periods. Always use this indicator as part of a comprehensive trading plan that includes other forms of analysis.

Adaptive Volatility-Scaled Oscillator [AVSO] (Zeiierman)█ Overview

The Adaptive Volatility-Scaled Oscillator (AVSO) is a dynamic trading indicator that measures and visualizes volatility-adjusted market behavior. By scaling various metrics (such as volume, price changes, standard deviation, ATR, and Yang-Zhang volatility) and applying adaptive smoothing, AVSO helps traders identify market conditions where volatility deviates significantly from the norm.

This indicator uses standardized scaling (Z-Score logic) to highlight periods of abnormally high or low volatility relative to recent history. With gradient coloring and clear volatility zones, AVSO provides a visually intuitive way to analyze market volatility and adapt trading strategies accordingly.

█ How It Works

⚪ Scaling Metrics: The indicator scales user-selected metrics (e.g., volume, ATR, standard deviation) relative to the market and price, providing a standardized volatility measure.

⚪ Z-Score Standardization: The scaled metric is normalized using a Z-Score to measure how far current volatility deviates from its recent mean.

Positive Z-Score: Above-average volatility.

Negative Z-Score: Below-average volatility.

⚪ Adaptive Smoothing: An Adaptive EMA smooths the Z-Score, dynamically adjusting its length based on the strength of the volatility. Stronger deviations result in shorter smoothing, increasing responsiveness.

█ Unique Feature: Yang-Zhang Volatility

The Yang-Zhang volatility estimator sets this indicator apart by providing a more robust and accurate measure of volatility compared to traditional methods like ATR or standard deviation.

⚪ What Makes Yang-Zhang Volatility Unique?

Comprehensive Calculation: It combines overnight price gaps (log returns from the previous close to the current open) and intraday price movements (high, low, and close).

Accurate for Gapped Markets: Traditional volatility measures can misrepresent price movement when significant gaps occur between sessions. Yang-Zhang accounts for these gaps, making it highly reliable for assets prone to overnight price jumps, such as stocks, cryptocurrencies, and futures.

Adaptable to Real Market Conditions : By including both close-to-open returns and intraday volatility, it provides a balanced and adaptive measure that captures the full volatility picture.

⚪ Why This Matters to Traders

Better Volatility Insights: Yang-Zhang offers a clearer view of true market volatility, especially in markets with price gaps or uneven trading sessions.

Improved Trade Timing: By identifying volatility spikes and calm periods more effectively, traders can time their entries and exits with greater confidence.

█ How to Use

Identify High and Low Volatility

A high Z-Score (>2) indicates significant market volatility. This can signal momentum-driven moves, breakouts, or areas of increased risk.

A low Z-Score (<-2) suggests low volatility or a calm market environment. This often occurs before a potential breakout or reversal.

Trade Signals

High Volatility Zones (background highlight): Monitor for potential breakouts, trend continuations, or reversals.

Low Volatility Zones: Anticipate range-bound conditions or upcoming volatility spikes.

█ Settings

Source: Select the price source for scaling calculations (close, high, low, open).

Metric Measure: Choose the volatility measure:

Volume: Scales raw volume.

Close: Uses closing price changes.

Standard Deviation: Price dispersion.

ATR: Average True Range.

Yang: Yang-Zhang volatility estimate.

Bars to Analyze: Number of historical bars used to calculate the mean and standard deviation of the scaled metric.

ATR / Standard Deviation Period: Lookback period for ATR or Standard Deviation calculation.

Yang Volatility Period: Period for the Yang-Zhang volatility estimator.

Smoothing Period: Base smoothing length for the adaptive smoothing line.

-----------------

Disclaimer

The information contained in my Scripts/Indicators/Ideas/Algos/Systems does not constitute financial advice or a solicitation to buy or sell any securities of any type. I will not accept liability for any loss or damage, including without limitation any loss of profit, which may arise directly or indirectly from the use of or reliance on such information.

All investments involve risk, and the past performance of a security, industry, sector, market, financial product, trading strategy, backtest, or individual's trading does not guarantee future results or returns. Investors are fully responsible for any investment decisions they make. Such decisions should be based solely on an evaluation of their financial circumstances, investment objectives, risk tolerance, and liquidity needs.

My Scripts/Indicators/Ideas/Algos/Systems are only for educational purposes!

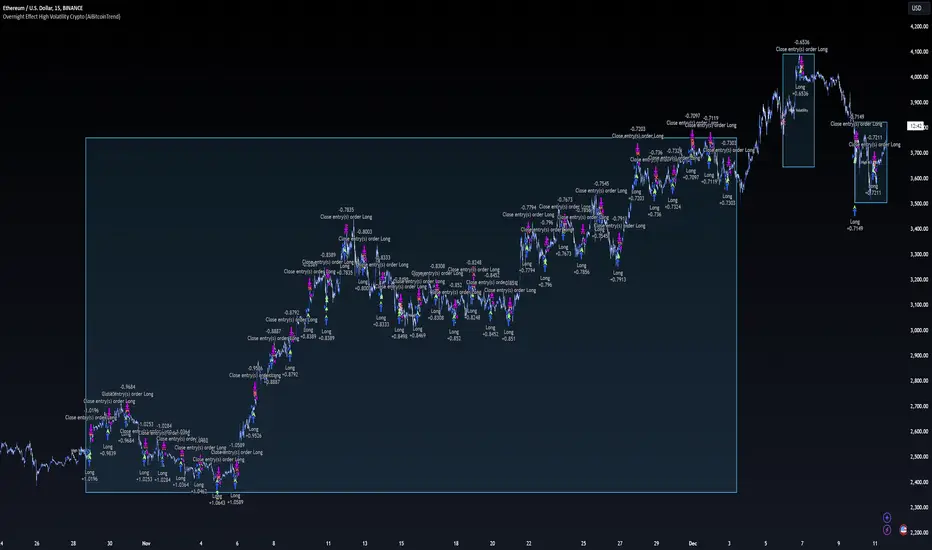

Overnight Effect High Volatility Crypto (AiBitcoinTrend)👽 Overview of the Strategy

This strategy leverages the overnight effect in the cryptocurrency market, specifically targeting the two-hour window from 21:00 UTC to 23:00 UTC. The strategy is designed to be applied only during periods of high volatility, which is determined using historical volatility data. This approach, inspired by research from Padyšák and Vojtko (2022), aims to capitalize on statistically significant return patterns observed during these hours.

Deep Backtesting with a High Volatility Filter

Deep Backtesting without a High Volatility Filter

👽 How the Strategy Works

Volatility Calculation:

Each day at 00:00 UTC, the strategy calculates the 30-day historical volatility of crypto returns (typically Bitcoin). The historical volatility is the standard deviation of the log returns over the past 30 days, representing the market's recent volatility level.

Median Volatility Benchmark:

The median of the 30-day historical volatility is calculated over a 365-day period (one year). This median acts as a benchmark to classify each day as either:

👾 High Volatility: When the current 30-day volatility exceeds the median volatility.

👾 Low Volatility: When the current 30-day volatility is below the median.

Trading Rule:

If the day is classified as a High Volatility Day, the strategy executes the following trades:

👾 Buy at 21:00 UTC.

👾 Sell at 23:00 UTC.

Trade Execution Details:

The strategy uses a 0.02% fee per trade.

Each trade is executed with 25% of the available capital. This allocation helps manage risk while allowing for compounding returns.

Rationale:

The returns during the 22:00 and 23:00 UTC hours have been found to be statistically significant during high volatility periods. The overnight effect is believed to drive this phenomenon due to the asynchronous closing hours of global financial markets. This creates unique trading opportunities in the cryptocurrency market, where exchanges remain open 24/7.

👽 Market Context and Global Time Zone Impact

👾 Why 21:00 to 23:00 UTC?

During this window, major traditional financial markets are closed:

NYSE (New York) closes at 21:00 UTC.

London and European markets are closed during these hours.

Asian markets (Tokyo, Hong Kong, etc.) open later, leaving this window largely unaffected by traditional trading flows.

This global market inactivity creates a period where significant moves can occur in the cryptocurrency market, particularly during high volatility.

👽 Strategy Parameters

Volatility Period: 30 days.

The lookback period for calculating historical volatility.

Median Period: 365 days.

The lookback period for calculating the median volatility benchmark.

Entry Time: 21:00 UTC.

Adjust this to your local time if necessary (e.g., 16:00 in New York, 22:00 in Stockholm).

Exit Time: 23:00 UTC.

Adjust this to your local time if necessary (e.g., 18:00 in New York, 00:00 midnight in Stockholm).

👽 Benefits of the Strategy

Seasonality Effect:

The strategy captures consistent patterns driven by the overnight effect and high volatility periods.

Risk Reduction:

Since trades are executed during a specific window and only on high volatility days, the strategy helps mitigate exposure to broader market risk.

Simplicity and Efficiency:

The strategy is moderately complex, making it accessible for traders while offering significant returns.

Global Applicability:

Suitable for traders worldwide, with clear guidelines on adjusting for local time zones.

👽 Considerations

Market Conditions: The strategy works best in a high-volatility environment.

Execution: Requires precise timing to enter and exit trades at the specified hours.

Time Zone Adjustments: Ensure you convert UTC times accurately based on your location to execute trades at the correct local times.

Disclaimer: This information is for entertainment purposes only and does not constitute financial advice. Please consult with a qualified financial advisor before making any investment decisions.

Volatility Trigger IndexThe script allows to assess the volatility of an asset.

It works by calculating the rate of change and the standard deviation.

The index is useful to determine the lowest volatility periods (could be useful to look strategies) and also it determine the highest volatility periods (maybe for exits or partial closes).

It has 3 iputs:

Lenght.

Low volatility value.

High volatility value.

The low and high values are set after a visual inspection. The values changes in each time frame. Usually when the timeframe is higher the value of the index is higher as well. So the low and high levels must be changed after each time frame set.

As an idea could be used in combination with any moving average to determine the market direction and the index used as a trigger.

GARCH Volume Volatility [MarkitTick]Title: GARCH Volume Volatility

Description

Overview

The GARCH Volume Volatility (GV) indicator is a sophisticated quantitative tool designed to analyze the rate of change in market participation. While the vast majority of technical indicators focus on Price Volatility (how much price moves), this script focuses on Volume Volatility (how unstable the participation is).

Market volume is rarely distributed evenly; it tends to cluster. Periods of high activity are often followed by more high activity, and periods of calm tend to persist. This behavior is known as "heteroskedasticity." This script utilizes an Exponentially Weighted Moving Average (EWMA) model—a core component of Generalized Autoregressive Conditional Heteroskedasticity (GARCH) frameworks—to model these changing variance regimes.

By isolating volume volatility from raw volume data, this tool helps traders distinguish between sustainable liquidity flows and erratic, unsustainable volume shocks that often precede market reversals or breakouts.

Methodology and Calculations

1. Logarithmic vs. Percentage Returns

The foundation of this indicator is the calculation of "Volume Returns"—the period-over-period change in volume.

- The script defaults to Logarithmic Returns. In financial statistics, log returns are preferred because they normalize data that can vary wildly in magnitude (such as cryptocurrency volume spikes), providing a more symmetric view of changes.

- Users can opt for standard percentage changes if they prefer a linear approach.

2. Variance Proxy (Squared Returns)

To measure volatility, the direction of the volume change (up or down) matters less than the magnitude. The script squares the returns to create a "Variance Proxy." This ensures that a massive drop in volume is treated with the same statistical weight as a massive spike in volume—both represent a significant change in the volatility of participation.

3. GARCH-Style Smoothing (EWMA)

Standard Moving Averages (SMA) treat all data points in the lookback period equally. However, volatility is dynamic. This script uses an EWMA model with a tunable "Lambda" (Decay Factor).

- The Recursive Formula: The current calculation relies on a weighted average of the current variance and the previous period's smoothed variance.

- Memory Effect: This allows the indicator to "remember" recent volatility shocks while gradually letting their influence fade. This mimics the GARCH process of conditional variance.

4. Dynamic Statistical Thresholds

The final output is the Volatility (square root of variance). To make this data actionable, the script calculates a dynamic upper and lower limit based on the standard deviation (Z-Score) of the volatility itself over a user-defined lookback period.

How to Use

The indicator plots a histogram that categorizes the market into four distinct volatility regimes:

1. High Volatility (Red Histogram)

Trigger: Volatility > High Band (Upper Standard Deviation).

Interpretation: This signals an extreme anomaly in volume stability. This is not just "high volume," but "erratic volume behavior." This often occurs at:

- Capitulation bottoms (panic selling).

- Euphoric tops (blow-off tops).

- Major news events or earnings releases.

2. Elevated Volatility (Maroon Histogram)

Trigger: Volatility > Mean Average.

Interpretation: The market is in an active state. Participation is changing rapidly, but within statistically normal bounds. This is common during healthy, trending moves where new participants are entering the market steadily.

3. Normal/Low Volatility (Green Histogram)

Trigger: Volatility is within the lower bands.

Interpretation: The market volume is stable. There are no sudden shocks in participation. This is typical of consolidation phases or "creeping" trends where the price drifts without significant volume conviction.

4. Extremely Low Volatility (Bright Green/Transparent)

Trigger: Volatility < Low Band.

Interpretation: The "calm before the storm." When volume volatility collapses to near-zero, it implies that the market has reached a state of equilibrium or disinterest. Historically, volatility is cyclical; periods of extreme compression often lead to violent expansion.

Settings and Configuration

Core Settings

- Use EWMA: When checked (Default), uses the recursive GARCH-style calculation. If unchecked, it reverts to a simple SMA of variance, which is less sensitive to recent shocks but more stable.

- Log Returns: Uses natural log for calculations. Highly recommended for assets with exponential growth or large volume ranges.

- Length: The baseline period for the calculation.

- Threshold Lookback: The number of bars used to calculate the Mean and Standard Deviation bands.

- EWMA Lambda: The decay factor (0.0 to 1.0). A value of 0.94 is standard for risk metrics.

-- Higher Lambda (e.g., 0.98): The indicator reacts slower and is smoother (long memory).

-- Lower Lambda (e.g., 0.80): The indicator reacts very fast to new data (short memory).

Visuals

- Show Thresholds: Toggles the visibility of the statistical bands on the chart.

- High Band (StdDev): The multiplier for the upper warning zone. Default is 1.5 deviations. Increasing this to 2.0 or 3.0 will filter for only the most extreme events.

Disclaimer This tool is for educational and technical analysis purposes only. Breakouts can fail (fake-outs), and past geometric patterns do not guarantee future price action. Always manage risk and use this tool in conjunction with other forms of analysis.

Implied Volatility and Historical VolatilityThis indicator provides a visualization of two different volatility measures, aiding in understanding market perceptions and actual price movements. Remember to combine it with other technical analysis tools and risk management strategies for informed trading decisions. The two measures of volatility:

Implied Volatility: Based on the standard deviation of recent price changes, it represents the market's expectation of future volatility.

Historical Volatility: Measured by the daily high-low range as a percentage of the closing price, it reflects the actual volatility experienced recently. It is intended to be used along side the Mean and Standard Deviation Lines indicator.

Inputs:

Period (Days): Defines the number of past bars used to calculate both types of volatility.

Calculations:

Interpretation:

Comparing the lines: Divergence between the lines can indicate potential mispricing:

If the Implied Volatility is higher than the Historical Volatility, the market might be overestimating future volatility.

Conversely, if the Implied Volatility is lower, the market might be underestimating future volatility.

Monitoring trends: Track changes in both lines over time to identify potential shifts in volatility expectations or actual market behavior.

Limitations:

Assumes normality in price distribution, which may not always hold true.

Historical Volatility only reflects past behavior, not future expectations.

Consider other factors like market sentiment and news events for comprehensive volatility analysis.