Jurik Price Bands and Range Box [BigBeluga]Jurik Price Bands and Range Box

The Jurik Price Bands and Range Box - BigBeluga indicator is an advanced technical analysis tool that combines Jurik Moving Average (JMA) based price bands with a dynamic range box. This versatile indicator is designed to help traders identify trends, potential reversal points, and price ranges over a specified period.

🔵 KEY FEATURES

● Jurik Price Bands

Utilizes Jurik Moving Average for smoother, more responsive bands

//@function Calculates Jurik Moving Average

//@param src (float) Source series

//@param len (int) Length parameter

//@param ph (int) Phase parameter

//@returns (float) Jurik Moving Average value

jma(src, len, ph) =>

var float jma = na

var float e0 = 0.0

var float e1 = 0.0

var float e2 = 0.0

phaseRatio = ph < -100 ? 0.5 : ph > 100 ? 2.5 : ph / 100 + 1.5

beta = 0.45 * (len - 1) / (0.45 * (len - 1) + 2)

alpha = math.pow(beta, phaseRatio)

e0 := (1 - alpha) * src + alpha * nz(e0 )

e1 := (src - e0) * (1 - beta) + beta * nz(e1 )

e2 := (e0 + phaseRatio * e1 - nz(jma )) * math.pow(1 - alpha, 2) + math.pow(alpha, 2) * nz(e2 )

jma := e2 + nz(jma )

jma

Consists of an upper band, lower band, and a smooth price line

Bands adapt to market volatility using Jurik MA on ATR

Helps identify potential trend reversal points and overextended market conditions

● Dynamic Range Box

Displays a box representing the price range over a specified period

Calculates high, low, and mid-range prices

Option for adaptive mid-range calculation based on average price

Provides visual representation of recent price action and volatility

● Price Position Indicator

Shows current price position relative to the mid-range

Displays percentage difference from mid-range

Color-coded for quick trend identification

● Dashboard

Displays key information including current price, range high, mid, and low

Shows trend direction based on price position relative to mid-range

Provides at-a-glance market context

🔵 HOW TO USE

● Trend Identification

Use the middle of the Range Box as the primary trend reference point

Price above the middle of the Range Box indicates an uptrend

Price below the middle of the Range Box indicates a downtrend

The bar on the right shows the percentage distance of the close from the middle of the box

This percentage indicates both trend direction and strength

Refer to the dashboard for quick trend direction confirmation

● Potential Reversal Points

Upper and lower Jurik Bands can indicate potential trend reversal points

Price reaching or exceeding these bands may suggest overextended conditions

Watch for price reaction at these levels for possible trend shifts or pullbacks

Range Box high and low can serve as additional reference points for price action

● Range Analysis

Use Range Box to gauge recent price volatility and trading range

Mid-range line can act as a pivot point for short-term price movements

Percentage difference from mid-range helps quantify price position strength

🔵 CUSTOMIZATION

The Jurik Price Bands and Range Box indicator offers several customization options:

Adjust Range Box length for different timeframe analysis

Toggle between standard and adaptive mid-range calculation

Standard:

Adaptive:

Modify Jurik MA length and deviation for band calculation

Toggle visibility of Jurik Bands

By fine-tuning these settings, traders can adapt the indicator to various market conditions and personal trading strategies.

The Jurik Price Bands and Range Box indicator provides a multi-faceted approach to market analysis, combining trend identification, potential reversal point detection, and range analysis in one comprehensive tool. The use of Jurik Moving Average offers a smoother, more responsive alternative to traditional moving averages, potentially providing more accurate signals.

This indicator can be particularly useful for traders looking to understand market context quickly, identify potential reversal points, and assess current market volatility. The combination of dynamic bands, range analysis, and the informative dashboard provides traders with a rich set of data points to inform their trading decisions.

As with all technical indicators, it's recommended to use the Jurik Price Bands and Range Box in conjunction with other forms of analysis and within the context of a well-defined trading strategy. While this indicator provides valuable insights, it should be considered alongside other factors such as overall market conditions, volume, and fundamental analysis when making trading decisions.

Komut dosyalarını "VAR+计量模型+黄金期货" için ara

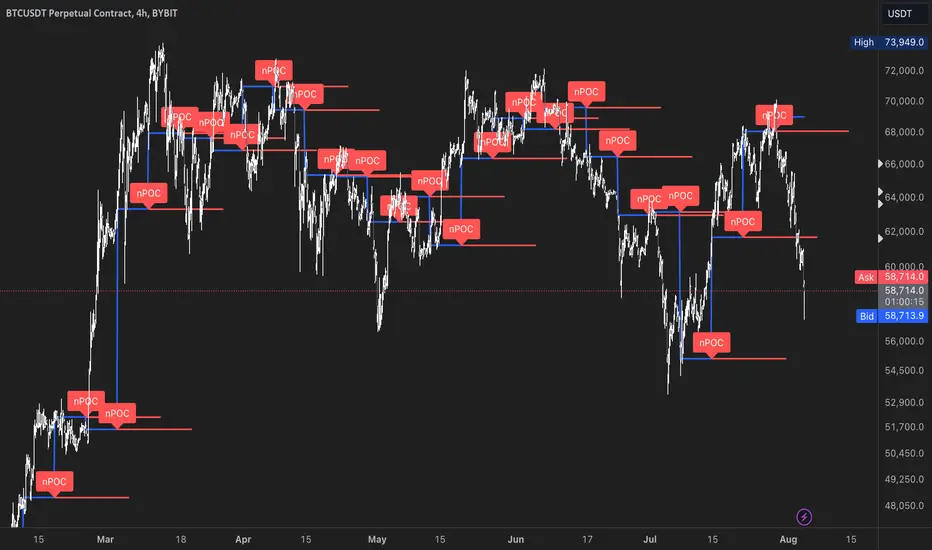

nPOC Levels by Tyler### Explanation of the Pine Script

This Pine Script identifies and displays weekly naked Points of Control (nPOCs) on a TradingView chart. An nPOC represents a Point of Control (POC) from a previous week that has not been revisited by price action in subsequent weeks. These nPOCs are extended to the right as horizontal lines, indicating potential support or resistance levels.

#### Script Overview

1. **Indicator Declaration:**

```pinescript

//@version=5

indicator("Weekly nPOCs", overlay=true)

```

- The script is defined as a version 5 Pine Script.

- The `indicator` function sets the script's name ("Weekly nPOCs") and specifies that the indicator should be overlaid on the price chart (`overlay=true`).

2. **Function to Calculate POC:**

```pinescript

f_poc(_hl2, _vol) =>

var float vol_profile = na

if (na(vol_profile))

vol_profile := array.new_float(100, 0.0)

_bin_size = (high - low) / 100

for i = 0 to 99

if _hl2 >= low + i * _bin_size and _hl2 < low + (i + 1) * _bin_size

array.set(vol_profile, i, array.get(vol_profile, i) + _vol)

max_volume = array.max(vol_profile)

poc_index = array.indexof(vol_profile, max_volume)

poc_price = low + poc_index * _bin_size + _bin_size / 2

poc_price

```

- The function `f_poc` calculates the Point of Control (POC) for a given period.

- It takes two parameters: `_hl2` (the average of the high and low prices) and `_vol` (volume).

- A volume profile array (`vol_profile`) is initialized to store volume data across different price bins.

- The price range between the high and low is divided into 100 bins (`_bin_size`).

- The function iterates over each bin, accumulating the volumes for prices within each bin.

- The bin with the maximum volume is identified as the POC (`poc_price`).

3. **Variables to Store Weekly Data:**

```pinescript

var float poc = na

var float prev_poc = na

var line poc_lines = na

if na(poc_lines)

poc_lines := array.new_line(0)

```

- `poc` stores the current week's POC.

- `prev_poc` stores the previous week's POC.

- `poc_lines` is an array to store lines representing nPOCs. The array is initialized if it is `na` (not initialized).

4. **Calculate Weekly POC:**

```pinescript

is_new_week = ta.change(time('W')) != 0

if (is_new_week)

prev_poc := poc

poc := f_poc(hl2, volume)

if not na(prev_poc)

line new_poc_line = line.new(x1=bar_index, y1=prev_poc, x2=bar_index + 100, y2=prev_poc, color=color.red, width=2)

label.new(x=bar_index, y=prev_poc, text="nPOC", style=label.style_label_down, color=color.red, textcolor=color.white)

array.push(poc_lines, new_poc_line)

```

- `is_new_week` checks if the current bar is the start of a new week using the `ta.change(time('W'))` function.

- If it's a new week, the previous week's POC is stored in `prev_poc`, and the current week's POC is calculated using `f_poc`.

- If `prev_poc` is not `na`, a new line (`new_poc_line`) representing the nPOC is created, extending it to the right (for 100 bars).

- A label is created at the `prev_poc` level, marking it as "nPOC".

- The new line is added to the `poc_lines` array.

5. **Remove Old Lines:**

```pinescript

if array.size(poc_lines) > 52

line.delete(array.shift(poc_lines))

```

- This section ensures that only the last 52 weeks of nPOCs are kept to avoid cluttering the chart.

- If the `poc_lines` array contains more than 52 lines, the oldest line is deleted using `array.shift`.

6. **Plot the Current Week's POC as a Reference:**

```pinescript

plot(poc, title="Current Weekly POC", color=color.blue, linewidth=2, style=plot.style_line)

```

- The current week's POC is plotted as a blue line on the chart for reference.

#### Summary

This script calculates and identifies weekly Points of Control (POCs) and marks them as nPOCs if they remain untouched by subsequent price action. These nPOCs are displayed as horizontal lines extending to the right, providing traders with potential support or resistance levels. The script also manages the number of lines plotted to maintain a clear and uncluttered chart.

Zero Lag Exponential Moving Average ForLoop [InvestorUnknown]Overview

The Zero Lag Exponential Moving Average (ZLEMA) ForLoop indicator is designed for traders seeking a responsive and adaptive tool to identify trend changes. By leveraging a range of lengths and different moving average (MA) types, this indicator helps smooth out price data and provides timely signals for market entry and exit.

User Inputs

Start and End Lengths: Define the range of lengths over which the IIRF values are calculated.

Moving Average Type: Choose from EMA, SMA, WMA, VWMA, or TMA for trend smoothing.

Moving Average Length: Specify the length for the chosen MA type.

Calculation Source: Select the price data used for calculations.

Signal Calculation

Signal Mode (sigmode): Determines the type of signal generated by the indicator. Options are "Fast", "Slow", "Thresholds Crossing", and "Fast Threshold".

1. Slow: is a simple crossing of the midline (0).

2. Fast: positive signal depends if the current MA > MA or MA is above 0.99, negative signals comes if MA < MA or MA is below -0.99.

3. Thresholds Crossing: simple ta.crossover and ta.crossunder of the user defined threshold for Long and Short.

4. Fast Threshold: signal changes if the value of MA changes by more than user defined threshold against the current signal

col1 = MA > 0 ? colup : coldn

var color col2 = na

if MA > MA or MA > 0.99

col2 := colup

if MA < MA or MA < -0.99

col2 := coldn

var color col3 = na

if ta.crossover(MA,longth)

col3 := colup

if ta.crossunder(MA,shortth)

col3 := coldn

var color col4 = na

if (MA > MA + fastth)

col4 := colup

if (MA < MA - fastth)

col4 := coldn

color col = switch sigmode

"Slow" => col1

"Fast" => col2

"Thresholds Crossing" => col3

"Fast Threshold" => col4

Visualization Settings

Bull Color (colup): The color used to indicate bullish signals.

Bear Color (coldn): The color used to indicate bearish signals.

Color Bars (barcol): Option to color the bars based on the signal.

Custom function

// Function to calculate an array of ZLEMA values over a range of lengths

ZLEMAForLoop(a, b, c, s) =>

// Initialize an array to hold ZLEMA trend values

var Array = array.new_float(b - a + 1, 0.0)

// Loop through the range from 'a' to 'b'

for x = 0 to (b - a)

// Calculate the current length

len = a + x

// Calculate the lag based on the length

lag = math.floor((len - 1) / 2)

// Calculate the smoothing factor alpha

alpha = 2 / (len + 1)

// Initialize the ZLEMA variable

zlema = 0.0

// Compute the ZLEMA value

zlema := na(zlema ) ? (s + s - s ) : alpha * (s + s - s ) + (1 - alpha) * nz(zlema )

// Determine the trend based on ZLEMA value

trend = zlema > zlema ? 1 : -1

// Store the trend in the array

array.set(Array, x, trend)

// Calculate the average of the trend values

Avg = array.avg(Array)

// Apply the selected moving average type to the average trend value

float MA = switch maType

"EMA" => ta.ema(Avg, c) // Exponential Moving Average

"SMA" => ta.sma(Avg, c) // Simple Moving Average

"WMA" => ta.wma(Avg, c) // Weighted Moving Average

"VWMA" => ta.vwma(Avg, c) // Volume-Weighted Moving Average

"TMA" => ta.trima(Avg, c) // Triangular Moving Average

=>

runtime.error("No matching MA type found.") // Error handling for unsupported MA type

float(na)

// Return the array of trends, the average trend, and the moving average

Important Considerations

Speed vs. Stability: The ZLEMA ForLoop is designed for fast response times, making it ideal for short-term trading strategies. However, its sensitivity also means it may generate more signals, some of which could be false positives.

Use with Other Indicators: To improve the reliability of the signals, it is recommended to use the ZLEMA ForLoop in conjunction with other technical indicators.

Customization: Tailor the settings to match your trading style and risk tolerance. Adjusting the lengths, MA type, and thresholds can significantly impact the indicator's performance.

Conclusion

The ZLEMA ForLoop indicator offers a flexible tool for traders looking to capture trend changes quickly. By providing multiple modes and customization options, it allows traders to fine-tune their analysis and make informed decisions. For best results, use this indicator alongside other analytical tools to confirm signals and avoid potential false entries.

Infinite Impulse Response Filter ForLoop [InvestorUnknown]Overview

The Infinite Impulse Response Filter ForLoop indicator is designed for seeking quick and accurate trend identification. Leveraging the Infinite Impulse Response (IIR) filter technique, this indicator provides fast and responsive signals to aid in market timing and trend following.

User Inputs

Start and End Lengths: Define the range of lengths over which the IIRF values are calculated.

Moving Average Type: Choose from EMA, SMA, WMA, VWMA, or TMA for trend smoothing.

Moving Average Length: Specify the length for the chosen MA type.

Calculation Source: Select the price data used for calculations (default is close price).

Signal Calculation

Signal Mode (sigmode): Determines the type of signal generated by the indicator. Options are "Fast", "Slow", "Thresholds Crossing", and "Fast Threshold".

1. Slow: is a simple crossing of the midline (0).

2. Fast: positive signal depends if the current MA > MA or MA is above 0.99, negative signals comes if MA < MA or MA is below -0.99.

3. Thresholds Crossing: simple ta.crossover and ta.crossunder of the user defined threshold for Long and Short.

4. Fast Threshold: signal changes if the value of MA changes by more than user defined threshold against the current signal

col1 = MA > 0 ? colup : coldn

var color col2 = na

if MA > MA or MA > 0.99

col2 := colup

if MA < MA or MA < -0.99

col2 := coldn

var color col3 = na

if ta.crossover(MA,longth)

col3 := colup

if ta.crossunder(MA,shortth)

col3 := coldn

var color col4 = na

if (MA > MA + fastth)

col4 := colup

if (MA < MA - fastth)

col4 := coldn

color col = switch sigmode

"Slow" => col1

"Fast" => col2

"Thresholds Crossing" => col3

"Fast Threshold" => col4

Visualization Settings

Bull Color (colup): The color used to indicate bullish signals.

Bear Color (coldn): The color used to indicate bearish signals.

Color Bars (barcol): Option to color the bars based on the signal.

Custom function

// Function to calculate an array of IIRF values over a range of lengths

IIRFforLoop(a, b, c, s) =>

// Initialize an array to store IIRF values

var Array = array.new_float(b - a + 1, 0.0)

// Loop over the range from 'a' to 'b'

for x = 0 to (b - a)

// Calculate the length for the current iteration

len = a + x

// Calculate the IIRF alpha parameter

iirfAlpha = 2 / (len + 1)

// Calculate the lag for the IIRF calculation

iirfLag = math.round(1 / iirfAlpha - 1)

// Initialize the IIRF value

iirf = 0.0

// Update the IIRF value using the IIR filter formula

iirf := iirfAlpha * (s + ta.change(s, iirfLag)) + (1 - iirfAlpha) * nz(iirf )

// Determine the trend based on the current and previous IIRF values

trend = iirf > iirf ? 1 : -1

// Store the trend value in the array

array.set(Array, x, trend)

// Calculate the average of the IIRF values in the array

Avg = array.avg(Array)

// Calculate the moving average of the average IIRF values based on the selected MA type

float MA = switch maType

"EMA" => ta.ema(Avg, c) // Exponential Moving Average

"SMA" => ta.sma(Avg, c) // Simple Moving Average

"WMA" => ta.wma(Avg, c) // Weighted Moving Average

"VWMA" => ta.vwma(Avg, c) // Volume Weighted Moving Average

"TMA" => ta.trima(Avg, c) // Triangular Moving Average

=>

runtime.error("No matching MA type found.") // Error handling for invalid MA type

float(na)

// Return the array of IIRF values, their average, and the moving average

Important Considerations

Rapid Signal Response: The IIRF ForLoop is designed to provide very fast trend signals, making it suitable for short-term trading and quick decision-making.

Complementary Tool: While powerful, the IIRF ForLoop should be used in conjunction with other indicators and market analysis techniques to confirm signals and improve trading accuracy.

Conclusion

The Infinite Impulse Response Filter ForLoop indicator is a highly responsive and flexible tool that can significantly enhance your trading strategy. Its ability to quickly identify trends and generate signals based on various moving average types and customizable thresholds makes it invaluable for active traders. For the best results, use this indicator alongside other technical analysis tools to confirm signals and ensure robust trading decisions.

Aroon ForLoop [InvestorUnknown]Overview

The Aroon ForLoop indicator is designed to calculate an array of Aroon values over a range of lengths, providing trend signals based on various moving averages. It offers flexibility with different signal modes and visual customizations.

User Input

Start Length (a) and End Length (b): Defines the range for calculating Aroon values.

MA Type (maType) and MA Length (c): Selects the moving average type (EMA, SMA, WMA, VWMA, TMA) and its length.

Calculation Source (s): Specifies the data source for calculations.

Signal Mode (sigmode): Offers options like Fast, Slow, Thresholds Crossing, and Fast Threshold to generate signals.

Thresholds: Configures long and short thresholds for signal generation.

Visualization Options: Customizes bull and bear colors, and enables/disables bar coloring.

Alert Settings: Chooses whether to wait for bar close for alert confirmation.

Signal Calculation

Signal Mode (sigmode): Determines the type of signal generated by the indicator. Options are "Fast", "Slow", "Thresholds Crossing", and "Fast Threshold".

1. Slow: is a simple crossing of the midline (0).

2. Fast: positive signal depends if the current MA > MA or MA is above 0.99, negative signals comes if MA < MA or MA is below -0.99.

3. Thresholds Crossing: simple ta.crossover and ta.crossunder of the user defined threshold for Long and Short.

4. Fast Threshold: signal changes if the value of Aroon MA changes by more than user defined threshold against the current signal

col1 = MA > 0 ? colup : coldn

var color col2 = na

if MA > MA or MA > 0.99

col2 := colup

if MA < MA or MA < -0.99

col2 := coldn

var color col3 = na

if ta.crossover(MA,longth)

col3 := colup

if ta.crossunder(MA,shortth)

col3 := coldn

var color col4 = na

if (MA > MA + fastth)

col4 := colup

if (MA < MA - fastth)

col4 := coldn

color col = na

if sigmode == "Slow"

col := col1

if sigmode == "Fast"

col := col2

if sigmode == "Thresholds Crossing"

col := col3

if sigmode == "Fast Threshold"

col := col4

else

na

Visualization Settings

Bull Color (colup): The color used to indicate bullish signals.

Bear Color (coldn): The color used to indicate bearish signals.

Color Bars (barcol): Option to color the bars based on the signal.

Custom Function

AroonForLoop: Calculates Aroon values over the specified range, determines the trend, and averages the results using the chosen moving average type.

AroonForLoop(a, b, c) =>

var SignalArray = array.new_float(b - a + 1, 0.0)

for x = 0 to (b - a)

len = a + x

upper = 100 * (ta.highestbars(high, len + 1) + len)/len

lower = 100 * (ta.lowestbars(low, len + 1) + len)/len

trend = upper > lower ? 1 : -1

array.set(SignalArray, x, trend)

Avg = array.avg(SignalArray)

float MA = switch maType

"EMA" => ta.ema(Avg, c)

"SMA" => ta.sma(Avg, c)

"WMA" => ta.wma(Avg, c)

"VWMA" => ta.vwma(Avg, c)

"TMA" => ta.trima(Avg, c)

=>

runtime.error("No matching MA type found.")

float(na)

Important Considerations

Fast Responses: The Aroon ForLoop indicator is designed for quick identification of trend changes, making it ideal for fast-paced trading environments.

Moving Average Types: Supports various MA types (EMA, SMA, WMA, VWMA, TMA) for adaptable smoothing of trend signals.

Combination with Other Indicators: For more reliable signals, use this indicator in conjunction with other technical indicators.

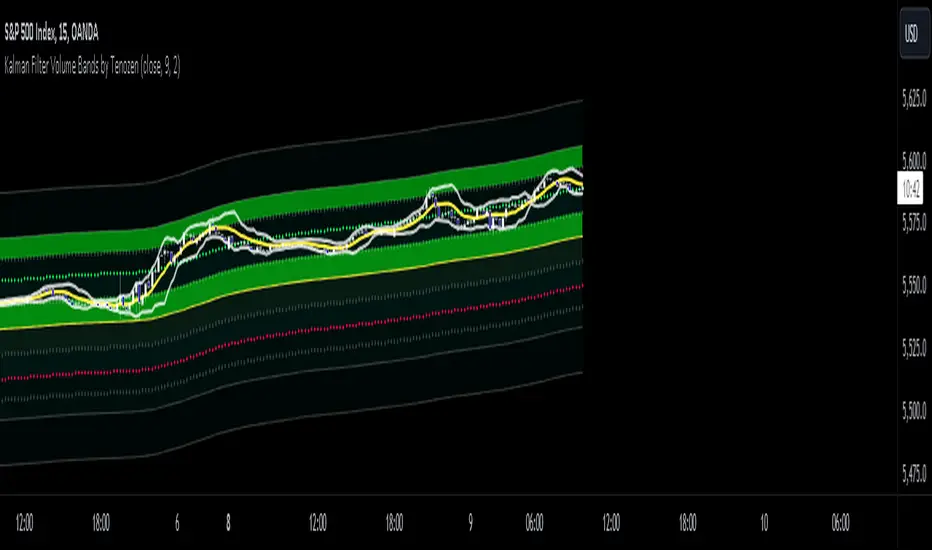

Kalman Filter Volume Bands by TenozenHello there! I am excited to introduce a new original indicator, the Kalman Filter Volume Bands. This indicator is calculated using the Kalman Filter, which is an adaptive-based smoothing quantitative tool. The Kalman Filter Volume Bands have two components that support the calculation, namely VWAP and VaR.

VWAP is used to determine the weight of the Kalman Filter Returns, but it doesn't have a significant impact on the calculation. On the other hand, VaR or Value at risk is calculated using the 99th percentile, which means that there is a 1% chance for the returns to exceed the 99th percentile level. After getting the VaR value, I manually adjust the bands based on the current market I'm trading on. I take the highest point (VaR*2) and the lowest point (-(VaR*2)) from the Kalman Filter, and then divide them into segments manually based on my preference.

This process results in 8 segments, where 2 segments near the Kalman Filter are further divided, making a total of 12 segments. These segments classify the current state of the price based on code-based coloring. The five states are very bullish, bullish, very bearish, bearish, and neutral.

I created this indicator to have an adaptive band that is not biased toward the volatility of the market. Most band-based indicators don't capture reversals that well, but the Kalman Filter Volume Bands can capture both trends and reversals. This makes it suitable for both trend-following and reversal trading approaches.

That's all for the explanation! Ciao!

Additional Reminder:

- Please use hourly timeframes or higher as lower timeframes are too noisy for reliable readings of this indicator.

ConditionalAverages█ OVERVIEW

This library is a Pine Script™ programmer’s tool containing functions that average values selectively.

█ CONCEPTS

Averaging can be useful to smooth out unstable readings in the data set, provide a benchmark to see the underlying trend of the data, or to provide a general expectancy of values in establishing a central tendency. Conventional averaging techniques tend to apply indiscriminately to all values in a fixed window, but it can sometimes be useful to average values only when a specific condition is met. As conditional averaging works on specific elements of a dataset, it can help us derive more context-specific conclusions. This library offers a collection of averaging methods that not only accomplish these tasks, but also exploit the efficiencies of the Pine Script™ runtime by foregoing unnecessary and resource-intensive for loops.

█ NOTES

To Loop or Not to Loop

Though for and while loops are essential programming tools, they are often unnecessary in Pine Script™. This is because the Pine Script™ runtime already runs your scripts in a loop where it executes your code on each bar of the dataset. Pine Script™ programmers who understand how their code executes on charts can use this to their advantage by designing loop-less code that will run orders of magnitude faster than functionally identical code using loops. Most of this library's function illustrate how you can achieve loop-less code to process past values. See the User Manual page on loops for more information. If you are looking for ways to measure execution time for you scripts, have a look at our LibraryStopwatch library .

Our `avgForTimeWhen()` and `totalForTimeWhen()` are exceptions in the library, as they use a while structure. Only a few iterations of the loop are executed on each bar, however, as its only job is to remove the few elements in the array that are outside the moving window defined by a time boundary.

Cumulating and Summing Conditionally

The ta.cum() or math.sum() built-in functions can be used with ternaries that select only certain values. In our `avgWhen(src, cond)` function, for example, we use this technique to cumulate only the occurrences of `src` when `cond` is true:

float cumTotal = ta.cum(cond ? src : 0) We then use:

float cumCount = ta.cum(cond ? 1 : 0) to calculate the number of occurrences where `cond` is true, which corresponds to the quantity of values cumulated in `cumTotal`.

Building Custom Series With Arrays

The advent of arrays in Pine has enabled us to build our custom data series. Many of this library's functions use arrays for this purpose, saving newer values that come in when a condition is met, and discarding the older ones, implementing a queue .

`avgForTimeWhen()` and `totalForTimeWhen()`

These two functions warrant a few explanations. They operate on a number of values included in a moving window defined by a timeframe expressed in milliseconds. We use a 1D timeframe in our example code. The number of bars included in the moving window is unknown to the programmer, who only specifies the period of time defining the moving window. You can thus use `avgForTimeWhen()` to calculate a rolling moving average for the last 24 hours, for example, that will work whether the chart is using a 1min or 1H timeframe. A 24-hour moving window will typically contain many more values on a 1min chart that on a 1H chart, but their calculated average will be very close.

Problems will arise on non-24x7 markets when large time gaps occur between chart bars, as will be the case across holidays or trading sessions. For example, if you were using a 24H timeframe and there is a two-day gap between two bars, then no chart bars would fit in the moving window after the gap. The `minBars` parameter mitigates this by guaranteeing that a minimum number of bars are always included in the calculation, even if including those bars requires reaching outside the prescribed timeframe. We use a minimum value of 10 bars in the example code.

Using var in Constant Declarations

In the past, we have been using var when initializing so-called constants in our scripts, which as per the Style Guide 's recommendations, we identify using UPPER_SNAKE_CASE. It turns out that var variables incur slightly superior maintenance overhead in the Pine Script™ runtime, when compared to variables initialized on each bar. We thus no longer use var to declare our "int/float/bool" constants, but still use it when an initialization on each bar would require too much time, such as when initializing a string or with a heavy function call.

Look first. Then leap.

█ FUNCTIONS

avgWhen(src, cond)

Gathers values of the source when a condition is true and averages them over the total number of occurrences of the condition.

Parameters:

src : (series int/float) The source of the values to be averaged.

cond : (series bool) The condition determining when a value will be included in the set of values to be averaged.

Returns: (float) A cumulative average of values when a condition is met.

avgWhenLast(src, cond, cnt)

Gathers values of the source when a condition is true and averages them over a defined number of occurrences of the condition.

Parameters:

src : (series int/float) The source of the values to be averaged.

cond : (series bool) The condition determining when a value will be included in the set of values to be averaged.

cnt : (simple int) The quantity of last occurrences of the condition for which to average values.

Returns: (float) The average of `src` for the last `x` occurrences where `cond` is true.

avgWhenInLast(src, cond, cnt)

Gathers values of the source when a condition is true and averages them over the total number of occurrences during a defined number of bars back.

Parameters:

src : (series int/float) The source of the values to be averaged.

cond : (series bool) The condition determining when a value will be included in the set of values to be averaged.

cnt : (simple int) The quantity of bars back to evaluate.

Returns: (float) The average of `src` in last `cnt` bars, but only when `cond` is true.

avgSince(src, cond)

Averages values of the source since a condition was true.

Parameters:

src : (series int/float) The source of the values to be averaged.

cond : (series bool) The condition determining when the average is reset.

Returns: (float) The average of `src` since `cond` was true.

avgForTimeWhen(src, ms, cond, minBars)

Averages values of `src` when `cond` is true, over a moving window of length `ms` milliseconds.

Parameters:

src : (series int/float) The source of the values to be averaged.

ms : (simple int) The time duration in milliseconds defining the size of the moving window.

cond : (series bool) The condition determining which values are included. Optional.

minBars : (simple int) The minimum number of values to keep in the moving window. Optional.

Returns: (float) The average of `src` when `cond` is true in the moving window.

totalForTimeWhen(src, ms, cond, minBars)

Sums values of `src` when `cond` is true, over a moving window of length `ms` milliseconds.

Parameters:

src : (series int/float) The source of the values to be summed.

ms : (simple int) The time duration in milliseconds defining the size of the moving window.

cond : (series bool) The condition determining which values are included. Optional.

minBars : (simple int) The minimum number of values to keep in the moving window. Optional.

Returns: (float) The sum of `src` when `cond` is true in the moving window.

Logger Library For Pinescript (Logging and Debugging)Library "LoggerLib"

This is a logging library for Pinescript. It is aimed to help developers testing and debugging scripts with a simple to use logger function.

Pinescript lacks a native logging implementation. This library would be helpful to mitigate this insufficiency.

This library uses table to print outputs into its view. It is simple, customizable and robust.

You can start using it's .log() method just like any other logging method in other languages.

//////////////////

USAGE

//////////////////

-- Recommended: Please Read The Documentation From Source Code Below. It Is Much More Readable There And Will Be Updated Along With Newer Versions. --

Importing the Library

---------------------

import paragjyoti2012/LoggerLib/ as Logger

.init() : Initializes the library and returns the logger pointer. (Later will be used as a function parameter)

.initTable: Initializes the Table View for the Logger and returns the table id. (Later will be used as a function parameter)

parameters:

logger: The logger pointer got from .init()

max_rows_count: Number of Rows to display in the Logger Table (default is 10)

offset: The offset value for the rows (Used for scrolling the view)

position: Position of the Table View

Values could be:

left

right

top-right

(default is left)

size: Font Size of content

Values could be:

small

normal

large

(default is small)

hide_date: Whether to hide the Date/Time column in the Logger (default is false)

returns: Table

example usage of .initTable()

import paragjyoti2012/LoggerLib/1 as Logger

var logger=Logger.init()

var logTable=Logger.initTable(logger, max_rows_count=20, offset=0, position="top-right")

-------------------

LOGGING

-------------------

.log() : Logging Method

params: (string message, |string| logger, table table_id, string type="message")

logger: pass the logger pointer from .init()

table_id: pass the table pointer from .initTable()

message: The message to log

type: Type of the log message

Values could be:

message

warning

error

info

success

(default is message)

returns: void

///////////////////////////////////////

Full Boilerplate For Using In Indicator

///////////////////////////////////////

P.S: Change the | (pipe) character into square brackets while using in script (or copy it from the source code instead)

offset=input.int(0,"Offset",minval=0)

size=input.string("small","Font Size",options=|"normal","small","large"|)

rows=input.int(15,"No Of Rows")

position=input.string("left","Position",options=|"left","right","top-right"|)

hide_date=input.bool(false,"Hide Time")

import paragjyoti2012/LoggerLib/1 as Logger

var logger=Logger.init()

var logTable=Logger.initTable(logger,rows,offset,position,size,hide_date)

rsi=ta.rsi(close,14)

|macd,signal,hist|=ta.macd(close,12,26,9)

if(ta.crossunder(close,34000))

Logger.log("Dropped Below 34000",logger,logTable,"warning")

if(ta.crossunder(close,35000))

Logger.log("Dropped Below 35000",logger,logTable)

if(ta.crossover(close,38000))

Logger.log("Crossed 38000",logger,logTable,"info")

if(ta.crossunder(rsi,20))

Logger.log("RSI Below 20",logger,logTable,"error")

if(ta.crossover(macd,signal))

Logger.log("Macd Crossed Over Signal",logger,logTable)

if(ta.crossover(rsi,80))

Logger.log("RSI Above 80",logger,logTable,"success")

////////////////////////////

// For Scrolling the Table View

////////////////////////////

There is a subtle way of achieving nice scrolling behaviour for the Table view. Open the input properties panel for the table/indicator. Focus on the input field for "Offset", once it's focused, you could use your mouse scroll wheel to increment/decrement the offset values; It will smoothly scroll the Logger Table Rows as well.

/////////////////////

For any assistance using this library or reporting issues, please write in the comment section below.

I will try my best to guide you and update the library. Thanks :)

/////////////////////

[BCT] Can BTC be predicted or is it purely random?Variance Ratio**This indicator can be applied to the ticker of your choice (not just BTC)**

Markets are said to be "efficient". An efficient market is by definition unpredictable - no matter the amount of ML, computation, or indicators thrown at it. In particular, in an efficient market, TA will not be of help.

An illustration of efficient markets is the WSJ's longstanding monkey vs. human contest:Blindfolded Monkey Beats Humans With Stock Picks, granted there are several flaws to it.

BTC is a relatively new market. New markets are typically highly inefficient (easier to make money) and become more and more efficient over time (harder to make money). How much more efficient is BTC becoming?

We apply the Variance Ratio method and apply it to BTC.

BACKGROUND ON THE VARIANCE RATIO METHOD

Based on 1988 MacKinlay's seminal paper "Stock Market Prices do not Follow a Random Walk", the idea is to exploit a phenomenon called "variance scaling".

For those keen on looking into the math, the short version of it is under the assumption of iid (random walk) we have the following:

H0: Var(Sum(returns over K bars))=Sum(Var(returns over 1 bar))=k*Var(return over 1 bar)

We look to reject or not H0 depending on the observations.

In this script, we compare the variance of the (log) returns for the chart selected between:

(1) The (average) variance over k bars (call this Vk)

(2) The (average) variance over 1 bar (call this V1)

H0 simply says that Vk=k*V1 if the stock follows a random walk.

We compute the Variance Ratio VR(k)=Variance(returns over k bar)/(Sum(Var(returns over 1 bar)))-1

We then compute the associated Z-score which we chart out for a configurable k number of bars.

HOW TO INTERPRET THE CHART

The line drawn is the Z-Score for VR(k). It represents the number of standard deviations of VR(k) from 0 - the further out, the less random.

- If the line is close / hovers around 0, the ticker appears to follow a random walk (i.e. may not be predictable)

- If the line is consistently > 2 or <-2, the ticker likely does not follow a random walk (i.e. may have predictable features)

- If the line is positive, it means that the Variance on the k bars is larger than the variance on 1 bar (more variance on longer timeframes)

- If the line is negative, it means that the Variance on the k bars is smaller than the variance on 1 bar (more variance on smaller timeframes)

USE CASES

- Identify timeframes where you won't be able to make money

- Identify whether a stock cannot be predicted (forget about TA, indicators etc. -- a random walk is not predictable)

- Identify whether a stock is becoming less and less predictable (Z-score amplitude will decrease over time)

FEATURES

- select the number of K bar to compare vs. 1 bar (default = 16) - ideally a power of 2 but any other number will work. The chart is based off this selection

- select the lookback period for the analysis (500 bars by default)

- select the source to analyze (default = close, but you may select other inputs to calculate the returns from)

- results form the statistical tests on different K's in the table on the right/bottom side of the chart (H0 rejected = not random walk; H0 not rejected = it essentially looks rather random and we can't conclude that it's not a random walk)

COMMENTARY ON BTC

- It appears BTC's absolute value of the ZScore on the Variance Ratio is declining year after year - corroborating an increasingly efficient market as new participants join.

- However, we can still detect a fair amount of potential inefficiency using this simple test.

As usual, this is not investment advice. DYOR.

With love,

🐵BCT🐵

Two Poles Trend Finder MTF [BigBeluga]🔵 OVERVIEW

Two Poles Trend Finder MTF is a refined trend-following overlay that blends a two-pole Gaussian filter with a multi-timeframe dashboard. It provides a smooth view of price dynamics along with a clear summary of trend directions across multiple timeframes—perfect for traders seeking alignment between short and long-term momentum.

🔵 CONCEPTS

Two-Pole Filter: A smoothing algorithm that responds faster than traditional moving averages but avoids the noise of short-term fluctuations.

var float f = na

var float f_prev1 = na

var float f_prev2 = na

// Apply two-pole Gaussian filter

if bar_index >= 2

f := math.pow(alpha, 2) * source + 2 * (1 - alpha) * f_prev1 - math.pow(1 - alpha, 2) * f_prev2

else

f := source // Warm-up for first bars

// Shift state

f_prev2 := f_prev1

f_prev1 := f

Trend Detection Logic: Trend direction is determined by comparing the current filtered value with its value n bars ago (shifted comparison).

MTF Alignment Dashboard: Trends from 5 configurable timeframes are monitored and visualized as colored boxes:

• Green = Uptrend

• Magenta = Downtrend

Summary Arrow: An average trend score from all timeframes is used to plot an overall arrow next to the asset name.

🔵 FEATURES

Two-Pole Gaussian Filter offers ultra-smooth trend curves while maintaining responsiveness.

Multi-Timeframe Trend Detection:

• Default: 1H, 2H, 4H, 12H, 1D (fully customizable)

• Each timeframe is assessed independently using the same trend logic.

Visual Trend Dashboard positioned at the bottom-right of the chart with color-coded trend blocks.

Dynamic Summary Arrow shows overall market bias (🢁 / 🢃) based on majority of uptrends/downtrends.

Bold + wide trail plot for the filter value with gradient coloring based on directional bias.

🔵 HOW TO USE

Use the multi-timeframe dashboard to identify aligned trends across your preferred trading horizons.

Confirm trend strength or weakness by observing filter slope direction .

Look for dashboard consensus (e.g., 4 or more timeframes green] ) as confirmation for breakout, continuation, or trend reentry strategies.

Combine with volume or price structure to enhance entry timing.

🔵 CONCLUSION

Two Poles Trend Finder MTF delivers a clean and intuitive trend-following solution with built-in multi-timeframe awareness. Whether you’re trading intra-day or positioning for swing setups, this tool helps filter out market noise and keeps you focused on directional consensus.

light_logLight Log - A Defensive Programming Library for Pine Script

Overview

The Light Log library transforms Pine Script development by introducing structured logging and defensive programming patterns typically found in enterprise languages like C#. This library addresses a fundamental challenge in Pine Script: the lack of sophisticated error handling and debugging tools that developers expect when building complex trading systems.

At its core, Light Log provides three transformative capabilities that work together to create more reliable and maintainable code. First, it wraps all native Pine Script types in error-aware containers, allowing values to carry validation state alongside their data. Second, it offers a comprehensive logging system with severity levels and conditional rendering. Third, it includes defensive programming utilities that catch errors early and make code self-documenting.

The Philosophy of Errors as Values

Traditional Pine Script error handling relies on runtime errors that halt execution, making it difficult to build resilient systems that can gracefully handle edge cases. Light Log introduces a paradigm shift by treating errors as first-class values that flow through your program alongside regular data.

When you wrap a value using Light Log's type system, you're not just storing data – you're creating a container that can carry both the value and its validation state. For example, when you call myNumber.INT() , you receive an INT object that contains both the integer value and a Log object that can describe any issues with that value. This approach, inspired by functional programming languages, allows errors to propagate through calculations without causing immediate failures.

Consider how this changes error handling in practice. Instead of a calculation failing catastrophically when it encounters invalid input, it can produce a result object that contains both the computed value (which might be na) and a detailed log explaining what went wrong. Subsequent operations can check has_error() to decide whether to proceed or handle the error condition gracefully.

The Typed Wrapper System

Light Log provides typed wrappers for every native Pine Script type: INT, FLOAT, BOOL, STRING, COLOR, LINE, LABEL, BOX, TABLE, CHART_POINT, POLYLINE, and LINEFILL. These wrappers serve multiple purposes beyond simple value storage.

Each wrapper type contains two fields: the value field v holds the actual data, while the error field e contains a Log object that tracks the value's validation state. This dual nature enables powerful programming patterns. You can perform operations on wrapped values and accumulate error information along the way, creating an audit trail of how values were processed.

The wrapper system includes convenient methods for converting between wrapped and unwrapped values. The extension methods like INT() , FLOAT() , etc., make it easy to wrap existing values, while the from_INT() , from_FLOAT() methods extract the underlying values when needed. The has_error() method provides a consistent interface for checking whether any wrapped value has encountered issues during processing.

The Log Object: Your Debugging Companion

The Log object represents the heart of Light Log's debugging capabilities. Unlike simple string concatenation for error messages, the Log object provides a structured approach to building, modifying, and rendering diagnostic information.

Each Log object carries three essential pieces of information: an error type (info, warning, error, or runtime_error), a message string that can be built incrementally, and an active flag that controls conditional rendering. This structure enables sophisticated logging patterns where you can build up detailed diagnostic information throughout your script's execution and decide later whether and how to display it.

The Log object's methods support fluent chaining, allowing you to build complex messages in a readable way. The write() and write_line() methods append text to the log, while new_line() adds formatting. The clear() method resets the log for reuse, and the rendering methods ( render_now() , render_condition() , and the general render() ) control when and how messages appear.

Defensive Programming Made Easy

Light Log's argument validation functions transform how you write defensive code. Instead of cluttering your functions with verbose validation logic, you can use concise, self-documenting calls that make your intentions clear.

The argument_error() function provides strict validation that halts execution when conditions aren't met – perfect for catching programming errors early. For less critical issues, argument_log_warning() and argument_log_error() record problems without stopping execution, while argument_log_info() provides debug visibility into your function's behavior.

These functions follow a consistent pattern: they take a condition to check, the function name, the argument name, and a descriptive message. This consistency makes error messages predictable and helpful, automatically formatting them to show exactly where problems occurred.

Building Modular, Reusable Code

Light Log encourages a modular approach to Pine Script development by providing tools that make functions more self-contained and reliable. When functions validate their inputs and return wrapped values with error information, they become true black boxes that can be safely composed into larger systems.

The void_return() function addresses Pine Script's requirement that all code paths return a value, even in error handling branches. This utility function provides a clean way to satisfy the compiler while making it clear that a particular code path should never execute.

The static log pattern, initialized with init_static_log() , enables module-wide error tracking. You can create a persistent Log object that accumulates information across multiple function calls, building a comprehensive diagnostic report that helps you understand complex behaviors in your indicators and strategies.

Real-World Applications

In practice, Light Log shines when building sophisticated trading systems. Imagine developing a complex indicator that processes multiple data streams, performs statistical calculations, and generates trading signals. With Light Log, each processing stage can validate its inputs, perform calculations, and pass along both results and diagnostic information.

For example, a moving average calculation might check that the period is positive, that sufficient data exists, and that the input series contains valid values. Instead of failing silently or throwing runtime errors, it can return a FLOAT object that contains either the calculated average or a detailed explanation of why the calculation couldn't be performed.

Strategy developers benefit even more from Light Log's capabilities. Complex entry and exit logic often involves multiple conditions that must all be satisfied. With Light Log, each condition check can contribute to a comprehensive log that explains exactly why a trade was or wasn't taken, making strategy debugging and optimization much more straightforward.

Performance Considerations

While Light Log adds a layer of abstraction over raw Pine Script values, its design minimizes performance impact. The wrapper objects are lightweight, containing only two fields. The logging operations only consume resources when actually rendered, and the conditional rendering system ensures that production code can run with logging disabled for maximum performance.

The library follows Pine Script best practices for performance, using appropriate data structures and avoiding unnecessary operations. The var keyword in init_static_log() ensures that persistent logs don't create new objects on every bar, maintaining efficiency even in real-time calculations.

Getting Started

Adopting Light Log in your Pine Script projects is straightforward. Import the library, wrap your critical values, add validation to your functions, and use Log objects to track important events. Start small by adding logging to a single function, then expand as you see the benefits of better error visibility and code organization.

Remember that Light Log is designed to grow with your needs. You can use as much or as little of its functionality as makes sense for your project. Even simple uses, like adding argument validation to key functions, can significantly improve code reliability and debugging ease.

Transform your Pine Script development experience with Light Log – because professional trading systems deserve professional development tools.

Light Log Technical Deep Dive: Advanced Patterns and Architecture

Understanding Errors as Values

The concept of "errors as values" represents a fundamental shift in how we think about error handling in Pine Script. In traditional Pine Script development, errors are events – they happen at a specific moment in time and immediately interrupt program flow. Light Log transforms errors into data – they become information that flows through your program just like any other value.

This transformation has profound implications. When errors are values, they can be stored, passed between functions, accumulated, transformed, and inspected. They become part of your program's data flow rather than exceptions to it. This approach, popularized by languages like Rust with its Result type and Haskell with its Either monad, brings functional programming's elegance to Pine Script.

Consider a practical example. Traditional Pine Script might calculate a momentum indicator like this:

momentum = close - close

If period is invalid or if there isn't enough historical data, this calculation might produce na or cause subtle bugs. With Light Log's approach:

calculate_momentum(src, period)=>

result = src.FLOAT()

if period <= 0

result.e.write("Invalid period: must be positive", true, ErrorType.error)

result.v := na

else if bar_index < period

result.e.write("Insufficient data: need " + str.tostring(period) + " bars", true, ErrorType.warning)

result.v := na

else

result.v := src - src

result.e.write("Momentum calculated successfully", false, ErrorType.info)

result

Now the function returns not just a value but a complete computational result that includes diagnostic information. Calling code can make intelligent decisions based on both the value and its associated metadata.

The Monad Pattern in Pine Script

While Pine Script lacks the type system features to implement true monads, Light Log brings monadic thinking to Pine Script development. The wrapped types (INT, FLOAT, etc.) act as computational contexts that carry both values and metadata through a series of transformations.

The key insight of monadic programming is that you can chain operations while automatically propagating context. In Light Log, this context is the error state. When you have a FLOAT that contains an error, operations on that FLOAT can check the error state and decide whether to proceed or propagate the error.

This pattern enables what functional programmers call "railway-oriented programming" – your code follows a success track when all is well but can switch to an error track when problems occur. Both tracks lead to the same destination (a result with error information), but they take different paths based on the validity of intermediate values.

Composable Error Handling

Light Log's design encourages composition – building complex functionality from simpler, well-tested components. Each component can validate its inputs, perform its calculation, and return a result with appropriate error information. Higher-level functions can then combine these results intelligently.

Consider building a complex trading signal from multiple indicators:

generate_signal(src, fast_period, slow_period, signal_period) =>

log = init_static_log(ErrorType.info)

// Calculate components with error tracking

fast_ma = calculate_ma(src, fast_period)

slow_ma = calculate_ma(src, slow_period)

// Check for errors in components

if fast_ma.has_error()

log.write_line("Fast MA error: " + fast_ma.e.message, true)

if slow_ma.has_error()

log.write_line("Slow MA error: " + slow_ma.e.message, true)

// Proceed with calculation if no errors

signal = 0.0.FLOAT()

if not (fast_ma.has_error() or slow_ma.has_error())

macd_line = fast_ma.v - slow_ma.v

signal_line = calculate_ma(macd_line, signal_period)

if signal_line.has_error()

log.write_line("Signal line error: " + signal_line.e.message, true)

signal.e := log

else

signal.v := macd_line - signal_line.v

log.write("Signal generated successfully")

else

signal.e := log

signal.v := na

signal

This composable approach makes complex calculations more reliable and easier to debug. Each component is responsible for its own validation and error reporting, and the composite function orchestrates these components while maintaining comprehensive error tracking.

The Static Log Pattern

The init_static_log() function introduces a powerful pattern for maintaining state across function calls. In Pine Script, the var keyword creates variables that persist across bars but are initialized only once. Light Log leverages this to create logging objects that can accumulate information throughout a script's execution.

This pattern is particularly valuable for debugging complex strategies where you need to understand behavior across multiple bars. You can create module-level logs that track important events:

// Module-level diagnostic log

diagnostics = init_static_log(ErrorType.info)

// Track strategy decisions across bars

check_entry_conditions() =>

diagnostics.clear() // Start fresh each bar

diagnostics.write_line("Bar " + str.tostring(bar_index) + " analysis:")

if close > sma(close, 20)

diagnostics.write_line("Price above SMA20", false)

else

diagnostics.write_line("Price below SMA20 - no entry", true, ErrorType.warning)

if volume > sma(volume, 20) * 1.5

diagnostics.write_line("Volume surge detected", false)

else

diagnostics.write_line("Normal volume", false)

// Render diagnostics based on verbosity setting

if debug_mode

diagnostics.render_now()

Advanced Validation Patterns

Light Log's argument validation functions enable sophisticated precondition checking that goes beyond simple null checks. You can implement complex validation logic while keeping your code readable:

validate_price_data(open_val, high_val, low_val, close_val) =>

argument_error(na(open_val) or na(high_val) or na(low_val) or na(close_val),

"validate_price_data", "OHLC values", "contain na values")

argument_error(high_val < low_val,

"validate_price_data", "high/low", "high is less than low")

argument_error(close_val > high_val or close_val < low_val,

"validate_price_data", "close", "is outside high/low range")

argument_log_warning(high_val == low_val,

"validate_price_data", "high/low", "are equal (no range)")

This validation function documents its requirements clearly and fails fast with helpful error messages when assumptions are violated. The mix of errors (which halt execution) and warnings (which allow continuation) provides fine-grained control over how strict your validation should be.

Performance Optimization Strategies

While Light Log adds abstraction, careful design minimizes overhead. Understanding Pine Script's execution model helps you use Light Log efficiently.

Pine Script executes once per bar, so operations that seem expensive in traditional programming might have negligible impact. However, when building real-time systems, every optimization matters. Light Log provides several patterns for efficient use:

Lazy Evaluation: Log messages are only built when they'll be rendered. Use conditional logging to avoid string concatenation in production:

if debug_mode

log.write_line("Calculated value: " + str.tostring(complex_calculation))

Selective Wrapping: Not every value needs error tracking. Wrap values at API boundaries and critical calculation points, but use raw values for simple operations:

// Wrap at boundaries

input_price = close.FLOAT()

validated_period = validate_period(input_period).INT()

// Use raw values internally

sum = 0.0

for i = 0 to validated_period.v - 1

sum += close

Error Propagation: When errors occur early, avoid expensive calculations:

process_data(input) =>

validated = validate_input(input)

if validated.has_error()

validated // Return early with error

else

// Expensive processing only if valid

perform_complex_calculation(validated)

Integration Patterns

Light Log integrates smoothly with existing Pine Script code. You can adopt it incrementally, starting with critical functions and expanding coverage as needed.

Boundary Validation: Add Light Log at the boundaries of your system – where user input enters and where final outputs are produced. This catches most errors while minimizing changes to existing code.

Progressive Enhancement: Start by adding argument validation to existing functions. Then wrap return values. Finally, add comprehensive logging. Each step improves reliability without requiring a complete rewrite.

Testing and Debugging: Use Light Log's conditional rendering to create debug modes for your scripts. Production users see clean output while developers get detailed diagnostics:

// User input for debug mode

debug = input.bool(false, "Enable debug logging")

// Conditional diagnostic output

if debug

diagnostics.render_now()

else

diagnostics.render_condition() // Only shows errors/warnings

Future-Proofing Your Code

Light Log's patterns prepare your code for Pine Script's evolution. As Pine Script adds more sophisticated features, code that uses structured error handling and defensive programming will adapt more easily than code that relies on implicit assumptions.

The type wrapper system, in particular, positions your code to take advantage of potential future features or more sophisticated type inference. By thinking in terms of wrapped values and error propagation today, you're building code that will remain maintainable and extensible tomorrow.

Light Log doesn't just make your Pine Script better today – it prepares it for the trading systems you'll need to build tomorrow.

Library "light_log"

A lightweight logging and defensive programming library for Pine Script.

Designed for modular and extensible scripts, this utility provides structured runtime validation,

conditional logging, and reusable `Log` objects for centralized error propagation.

It also introduces a typed wrapping system for all native Pine values (e.g., `INT`, `FLOAT`, `LABEL`),

allowing values to carry errors alongside data. This enables functional-style flows with built-in

validation tracking, error detection (`has_error()`), and fluent chaining.

Inspired by structured logging patterns found in systems like C#, it reduces boilerplate,

enforces argument safety, and encourages clean, maintainable code architecture.

method INT(self, error_type)

Wraps an `int` value into an `INT` struct with an optional log severity.

Namespace types: series int, simple int, input int, const int

Parameters:

self (int) : The raw `int` value to wrap.

error_type (series ErrorType) : Optional severity level to associate with the log. Default is `ErrorType.error`.

Returns: An `INT` object containing the value and a default Log instance.

method FLOAT(self, error_type)

Wraps a `float` value into a `FLOAT` struct with an optional log severity.

Namespace types: series float, simple float, input float, const float

Parameters:

self (float) : The raw `float` value to wrap.

error_type (series ErrorType) : Optional severity level to associate with the log. Default is `ErrorType.error`.

Returns: A `FLOAT` object containing the value and a default Log instance.

method BOOL(self, error_type)

Wraps a `bool` value into a `BOOL` struct with an optional log severity.

Namespace types: series bool, simple bool, input bool, const bool

Parameters:

self (bool) : The raw `bool` value to wrap.

error_type (series ErrorType) : Optional severity level to associate with the log. Default is `ErrorType.error`.

Returns: A `BOOL` object containing the value and a default Log instance.

method STRING(self, error_type)

Wraps a `string` value into a `STRING` struct with an optional log severity.

Namespace types: series string, simple string, input string, const string

Parameters:

self (string) : The raw `string` value to wrap.

error_type (series ErrorType) : Optional severity level to associate with the log. Default is `ErrorType.error`.

Returns: A `STRING` object containing the value and a default Log instance.

method COLOR(self, error_type)

Wraps a `color` value into a `COLOR` struct with an optional log severity.

Namespace types: series color, simple color, input color, const color

Parameters:

self (color) : The raw `color` value to wrap.

error_type (series ErrorType) : Optional severity level to associate with the log. Default is `ErrorType.error`.

Returns: A `COLOR` object containing the value and a default Log instance.

method LINE(self, error_type)

Wraps a `line` object into a `LINE` struct with an optional log severity.

Namespace types: series line

Parameters:

self (line) : The raw `line` object to wrap.

error_type (series ErrorType) : Optional severity level to associate with the log. Default is `ErrorType.error`.

Returns: A `LINE` object containing the value and a default Log instance.

method LABEL(self, error_type)

Wraps a `label` object into a `LABEL` struct with an optional log severity.

Namespace types: series label

Parameters:

self (label) : The raw `label` object to wrap.

error_type (series ErrorType) : Optional severity level to associate with the log. Default is `ErrorType.error`.

Returns: A `LABEL` object containing the value and a default Log instance.

method BOX(self, error_type)

Wraps a `box` object into a `BOX` struct with an optional log severity.

Namespace types: series box

Parameters:

self (box) : The raw `box` object to wrap.

error_type (series ErrorType) : Optional severity level to associate with the log. Default is `ErrorType.error`.

Returns: A `BOX` object containing the value and a default Log instance.

method TABLE(self, error_type)

Wraps a `table` object into a `TABLE` struct with an optional log severity.

Namespace types: series table

Parameters:

self (table) : The raw `table` object to wrap.

error_type (series ErrorType) : Optional severity level to associate with the log. Default is `ErrorType.error`.

Returns: A `TABLE` object containing the value and a default Log instance.

method CHART_POINT(self, error_type)

Wraps a `chart.point` value into a `CHART_POINT` struct with an optional log severity.

Namespace types: chart.point

Parameters:

self (chart.point) : The raw `chart.point` value to wrap.

error_type (series ErrorType) : Optional severity level to associate with the log. Default is `ErrorType.error`.

Returns: A `CHART_POINT` object containing the value and a default Log instance.

method POLYLINE(self, error_type)

Wraps a `polyline` object into a `POLYLINE` struct with an optional log severity.

Namespace types: series polyline, series polyline, series polyline, series polyline

Parameters:

self (polyline) : The raw `polyline` object to wrap.

error_type (series ErrorType) : Optional severity level to associate with the log. Default is `ErrorType.error`.

Returns: A `POLYLINE` object containing the value and a default Log instance.

method LINEFILL(self, error_type)

Wraps a `linefill` object into a `LINEFILL` struct with an optional log severity.

Namespace types: series linefill

Parameters:

self (linefill) : The raw `linefill` object to wrap.

error_type (series ErrorType) : Optional severity level to associate with the log. Default is `ErrorType.error`.

Returns: A `LINEFILL` object containing the value and a default Log instance.

method from_INT(self)

Extracts the integer value from an INT wrapper.

Namespace types: INT

Parameters:

self (INT) : The wrapped INT instance.

Returns: The underlying `int` value.

method from_FLOAT(self)

Extracts the float value from a FLOAT wrapper.

Namespace types: FLOAT

Parameters:

self (FLOAT) : The wrapped FLOAT instance.

Returns: The underlying `float` value.

method from_BOOL(self)

Extracts the boolean value from a BOOL wrapper.

Namespace types: BOOL

Parameters:

self (BOOL) : The wrapped BOOL instance.

Returns: The underlying `bool` value.

method from_STRING(self)

Extracts the string value from a STRING wrapper.

Namespace types: STRING

Parameters:

self (STRING) : The wrapped STRING instance.

Returns: The underlying `string` value.

method from_COLOR(self)

Extracts the color value from a COLOR wrapper.

Namespace types: COLOR

Parameters:

self (COLOR) : The wrapped COLOR instance.

Returns: The underlying `color` value.

method from_LINE(self)

Extracts the line object from a LINE wrapper.

Namespace types: LINE

Parameters:

self (LINE) : The wrapped LINE instance.

Returns: The underlying `line` object.

method from_LABEL(self)

Extracts the label object from a LABEL wrapper.

Namespace types: LABEL

Parameters:

self (LABEL) : The wrapped LABEL instance.

Returns: The underlying `label` object.

method from_BOX(self)

Extracts the box object from a BOX wrapper.

Namespace types: BOX

Parameters:

self (BOX) : The wrapped BOX instance.

Returns: The underlying `box` object.

method from_TABLE(self)

Extracts the table object from a TABLE wrapper.

Namespace types: TABLE

Parameters:

self (TABLE) : The wrapped TABLE instance.

Returns: The underlying `table` object.

method from_CHART_POINT(self)

Extracts the chart.point from a CHART_POINT wrapper.

Namespace types: CHART_POINT

Parameters:

self (CHART_POINT) : The wrapped CHART_POINT instance.

Returns: The underlying `chart.point` value.

method from_POLYLINE(self)

Extracts the polyline object from a POLYLINE wrapper.

Namespace types: POLYLINE

Parameters:

self (POLYLINE) : The wrapped POLYLINE instance.

Returns: The underlying `polyline` object.

method from_LINEFILL(self)

Extracts the linefill object from a LINEFILL wrapper.

Namespace types: LINEFILL

Parameters:

self (LINEFILL) : The wrapped LINEFILL instance.

Returns: The underlying `linefill` object.

method has_error(self)

Returns true if the INT wrapper has an active log entry.

Namespace types: INT

Parameters:

self (INT) : The INT instance to check.

Returns: True if an error or message is active in the log.

method has_error(self)

Returns true if the FLOAT wrapper has an active log entry.

Namespace types: FLOAT

Parameters:

self (FLOAT) : The FLOAT instance to check.

Returns: True if an error or message is active in the log.

method has_error(self)

Returns true if the BOOL wrapper has an active log entry.

Namespace types: BOOL

Parameters:

self (BOOL) : The BOOL instance to check.

Returns: True if an error or message is active in the log.

method has_error(self)

Returns true if the STRING wrapper has an active log entry.

Namespace types: STRING

Parameters:

self (STRING) : The STRING instance to check.

Returns: True if an error or message is active in the log.

method has_error(self)

Returns true if the COLOR wrapper has an active log entry.

Namespace types: COLOR

Parameters:

self (COLOR) : The COLOR instance to check.

Returns: True if an error or message is active in the log.

method has_error(self)

Returns true if the LINE wrapper has an active log entry.

Namespace types: LINE

Parameters:

self (LINE) : The LINE instance to check.

Returns: True if an error or message is active in the log.

method has_error(self)

Returns true if the LABEL wrapper has an active log entry.

Namespace types: LABEL

Parameters:

self (LABEL) : The LABEL instance to check.

Returns: True if an error or message is active in the log.

method has_error(self)

Returns true if the BOX wrapper has an active log entry.

Namespace types: BOX

Parameters:

self (BOX) : The BOX instance to check.

Returns: True if an error or message is active in the log.

method has_error(self)

Returns true if the TABLE wrapper has an active log entry.

Namespace types: TABLE

Parameters:

self (TABLE) : The TABLE instance to check.

Returns: True if an error or message is active in the log.

method has_error(self)

Returns true if the CHART_POINT wrapper has an active log entry.

Namespace types: CHART_POINT

Parameters:

self (CHART_POINT) : The CHART_POINT instance to check.

Returns: True if an error or message is active in the log.

method has_error(self)

Returns true if the POLYLINE wrapper has an active log entry.

Namespace types: POLYLINE

Parameters:

self (POLYLINE) : The POLYLINE instance to check.

Returns: True if an error or message is active in the log.

method has_error(self)

Returns true if the LINEFILL wrapper has an active log entry.

Namespace types: LINEFILL

Parameters:

self (LINEFILL) : The LINEFILL instance to check.

Returns: True if an error or message is active in the log.

void_return()

Utility function used when a return is syntactically required but functionally unnecessary.

Returns: Nothing. Function never executes its body.

argument_error(condition, function, argument, message)

Throws a runtime error when a condition is met. Used for strict argument validation.

Parameters:

condition (bool) : Boolean expression that triggers the runtime error.

function (string) : Name of the calling function (for formatting).

argument (string) : Name of the problematic argument.

message (string) : Description of the error cause.

Returns: Never returns. Halts execution if the condition is true.

argument_log_info(condition, function, argument, message)

Logs an informational message when a condition is met. Used for optional debug visibility.

Parameters:

condition (bool) : Boolean expression that triggers the log.

function (string) : Name of the calling function.

argument (string) : Argument name being referenced.

message (string) : Informational message to log.

Returns: Nothing. Logs if the condition is true.

argument_log_warning(condition, function, argument, message)

Logs a warning when a condition is met. Non-fatal but highlights potential issues.

Parameters:

condition (bool) : Boolean expression that triggers the warning.

function (string) : Name of the calling function.

argument (string) : Argument name being referenced.

message (string) : Warning message to log.

Returns: Nothing. Logs if the condition is true.

argument_log_error(condition, function, argument, message)

Logs an error message when a condition is met. Does not halt execution.

Parameters:

condition (bool) : Boolean expression that triggers the error log.

function (string) : Name of the calling function.

argument (string) : Argument name being referenced.

message (string) : Error message to log.

Returns: Nothing. Logs if the condition is true.

init_static_log(error_type, message, active)

Initializes a persistent (var) Log object. Ideal for global logging in scripts or modules.

Parameters:

error_type (series ErrorType) : Initial severity level (required).

message (string) : Optional starting message string. Default value of ("").

active (bool) : Whether the log should be flagged active on initialization. Default value of (false).

Returns: A static Log object with the given parameters.

method new_line(self)

Appends a newline character to the Log message. Useful for separating entries during chained writes.

Namespace types: Log

Parameters:

self (Log) : The Log instance to modify.

Returns: The updated Log object with a newline appended.

method write(self, message, flag_active, error_type)

Appends a message to a Log object without a newline. Updates severity and active state if specified.

Namespace types: Log

Parameters:

self (Log) : The Log instance being modified.

message (string) : The text to append to the log.

flag_active (bool) : Whether to activate the log for conditional rendering. Default value of (false).

error_type (series ErrorType) : Optional override for the severity level. Default value of (na).

Returns: The updated Log object.

method write_line(self, message, flag_active, error_type)

Appends a message to a Log object, prefixed with a newline for clarity.

Namespace types: Log

Parameters:

self (Log) : The Log instance being modified.

message (string) : The text to append to the log.

flag_active (bool) : Whether to activate the log for conditional rendering. Default value of (false).

error_type (series ErrorType) : Optional override for the severity level. Default value of (na).

Returns: The updated Log object.

method clear(self, flag_active, error_type)

Clears a Log object’s message and optionally reactivates it. Can also update the error type.

Namespace types: Log

Parameters:

self (Log) : The Log instance being cleared.

flag_active (bool) : Whether to activate the log after clearing. Default value of (false).

error_type (series ErrorType) : Optional new error type to assign. If not provided, the previous type is retained. Default value of (na).

Returns: The cleared Log object.

method render_condition(self, flag_active, error_type)

Conditionally renders the log if it is active. Allows overriding error type and controlling active state afterward.

Namespace types: Log

Parameters:

self (Log) : The Log instance to evaluate and render.

flag_active (bool) : Whether to activate the log after rendering. Default value of (false).

error_type (series ErrorType) : Optional error type override. Useful for contextual formatting just before rendering. Default value of (na).

Returns: The updated Log object.

method render_now(self, flag_active, error_type)

Immediately renders the log regardless of `active` state. Allows overriding error type and active flag.

Namespace types: Log

Parameters:

self (Log) : The Log instance to render.

flag_active (bool) : Whether to activate the log after rendering. Default value of (false).

error_type (series ErrorType) : Optional error type override. Allows dynamic severity adjustment at render time. Default value of (na).

Returns: The updated Log object.

render(self, condition, flag_active, error_type)