ZigZag█ OVERVIEW

This library is a Pine Script™ programmer’s tool containing custom user-defined types and functions to calculate Zig Zag indicators within their scripts. It is not a stand-alone indicator.

Pine Script™ libraries are publications that contain reusable code for importing into Pine Script™ indicators, strategies, and other libraries. For more information on libraries and incorporating them into your scripts, see the Libraries section of the Pine Script™ User Manual .

█ CONCEPTS

Zig Zag

Zig Zag is a popular indicator that filters out minor price fluctuations to denoise data and emphasize trends. Traders commonly use Zig Zag for trend confirmation, identifying potential support and resistance, and pattern detection. It is formed by identifying significant local high and low points in alternating order and connecting them with straight lines, omitting all other data points from their output. There are several ways to calculate the Zig Zag's data points and the conditions by which its direction changes. This script uses pivots as the data points, which are the highest or lowest values over a defined number of bars before and after them. The direction only reverses when a newly formed pivot deviates from the last Zig Zag point in the opposite direction by an amount greater than or equal to a specified percentage.

To learn more about Zig Zag and how to calculate it, see this entry from the Help Center.

█ FOR Pine Script™ CODERS

Notes

This script's architecture utilizes user-defined types (UDTs) to create custom objects which are the equivalent of variables containing multiple parts, each able to hold independent values of different types . UDTs are the newest addition to Pine Script™ and the most advanced feature the language has seen to date. The feature's introduction creates a new runway for experienced coders to push the boundaries of Pine. We recommend that newcomers to the language explore the basics first before diving into UDTs and objects.

Demonstration Code

Our example code shows a simple use case by displaying a Zig Zag with user-defined settings. A new ZigZag object is instantiated on the first bar using a Settings object to control its attributes. The fields for the Settings object are declared using variables assigned to input.* functions, allowing control of the field values from the script's settings. The `update()` function is invoked on each bar to update the ZigZag object's fields and create new lines and labels when required.

Look first. Then leap.

█ TYPES

This library contains the following types:

Settings

Provides calculation and display attributes to ZigZag objects.

Fields:

devThreshold : The minimum percentage deviation from a point before the ZigZag will change direction.

depth : The number of bars required for pivot detection.

lineColor : Line color.

extendLast : Condition allowing a line to connect the most recent pivot with the current close.

displayReversalPrice : Condition to display the pivot price in the pivot label.

displayCumulativeVolume : Condition to display the cumulative volume for the pivot segment in the pivot label.

displayReversalPriceChange : Condition to display the change in price or percent from the previous pivot in the pivot label.

differencePriceMode : Reversal change display mode. Options are "Absolute" or "Percent".

draw : Condition to display lines and labels.

Point

A coordinate containing time and price information.

Fields:

tm : A value in UNIX time.

price : A value on the Y axis (price).

Pivot

A level of significance used to determine directional movement or potential support and resistance.

Fields:

ln : A line object connecting the `start` and `end` Point objects.

lb : A label object to display pivot values.

isHigh : A condition to determine if the pivot is a pivot high.

vol : Volume for the pivot segment.

start : The coordinate of the previous Point.

end : The coordinate of the current Point.

ZigZag

An object to maintain Zig Zag settings, pivots, and volume.

Fields:

settings : Settings object to provide calculation and display attributes.

pivots : An array of Pivot objects.

sumVol : The volume sum for the pivot segment.

extend : Pivot object used to project a line from the last pivot to the last bar.

█ FUNCTIONS

This library contains the following functions:

lastPivot(this)

Returns the last Pivot of `this` ZigZag if there is at least one Pivot to return, and `na` otherwise.

Parameters:

this : (series ZigZag) A ZigZag object.

Returns: (Pivot) The last Pivot in the ZigZag.

update(this)

Updates `this` ZigZag object with new pivots, volume, lines, labels.

Parameters:

this : (series ZigZag) a ZigZag object.

Returns: (bool) true if a new Zig Zag line is found or the last Zig Zag line has changed.

newInstance(settings)

Instantiates a new ZigZag object with `settings`. If no settings are provided, a default ZigZag object is created.

Parameters:

settings : (series Settings) A Settings object.

Returns: (ZigZag) A new ZigZag instance.

"TradingView+手机版" için komut dosyalarını ara

Intrabar Efficiency Ratio█ OVERVIEW

This indicator displays a directional variant of Perry Kaufman's Efficiency Ratio, designed to gauge the "efficiency" of intrabar price movement by comparing the sum of movements of the lower timeframe bars composing a chart bar with the respective bar's movement on an average basis.

█ CONCEPTS

Efficiency Ratio (ER)

Efficiency Ratio was first introduced by Perry Kaufman in his 1995 book, titled "Smarter Trading". It is the ratio of absolute price change to the sum of absolute changes on each bar over a period. This tells us how strong the period's trend is relative to the underlying noise. Simply put, it's a measure of price movement efficiency. This ratio is the modulator utilized in Kaufman's Adaptive Moving Average (KAMA), which is essentially an Exponential Moving Average (EMA) that adapts its responsiveness to movement efficiency.

ER's output is bounded between 0 and 1. A value of 0 indicates that the starting price equals the ending price for the period, which suggests that price movement was maximally inefficient. A value of 1 indicates that price had travelled no more than the distance between the starting price and the ending price for the period, which suggests that price movement was maximally efficient. A value between 0 and 1 indicates that price had travelled a distance greater than the distance between the starting price and the ending price for the period. In other words, some degree of noise was present which resulted in reduced efficiency over the period.

As an example, let's say that the price of an asset had moved from $15 to $14 by the end of a period, but the sum of absolute changes for each bar of data was $4. ER would be calculated like so:

ER = abs(14 - 15)/4 = 0.25

This suggests that the trend was only 25% efficient over the period, as the total distanced travelled by price was four times what was required to achieve the change over the period.

Intrabars

Intrabars are chart bars at a lower timeframe than the chart's. Each 1H chart bar of a 24x7 market will, for example, usually contain 60 intrabars at the LTF of 1min, provided there was market activity during each minute of the hour. Mining information from intrabars can be useful in that it offers traders visibility on the activity inside a chart bar.

Lower timeframes (LTFs)

A lower timeframe is a timeframe that is smaller than the chart's timeframe. This script determines which LTF to use by examining the chart's timeframe. The LTF determines how many intrabars are examined for each chart bar; the lower the timeframe, the more intrabars are analyzed, but fewer chart bars can display indicator information because there is a limit to the total number of intrabars that can be analyzed.

Intrabar precision

The precision of calculations increases with the number of intrabars analyzed for each chart bar. As there is a 100K limit to the number of intrabars that can be analyzed by a script, a trade-off occurs between the number of intrabars analyzed per chart bar and the chart bars for which calculations are possible.

Intrabar Efficiency Ratio (IER)

Intrabar Efficiency Ratio applies the concept of ER on an intrabar level. Rather than comparing the overall change to the sum of bar changes for the current chart's timeframe over a period, IER compares single bar changes for the current chart's timeframe to the sum of absolute intrabar changes, then applies smoothing to the result. This gives an indication of how efficient changes are on the current chart's timeframe for each bar of data relative to LTF bar changes on an average basis. Unlike the standard ER calculation, we've opted to preserve directional information by not taking the absolute value of overall change, thus allowing it to be utilized as a momentum oscillator. However, by taking the absolute value of this oscillator, it could potentially serve as a replacement for ER in the design of adaptive moving averages.

Since this indicator preserves directional information, IER can be regarded as similar to the Chande Momentum Oscillator (CMO) , which was presented in 1994 by Tushar Chande in "The New Technical Trader". Both CMO and ER essentially measure the same relationship between trend and noise. CMO simply differs in scale, and considers the direction of overall changes.

█ FEATURES

Display

Three different display types are included within the script:

• Line : Displays the middle length MA of the IER as a line .

Color for this display can be customized via the "Line" portion of the "Visuals" section in the script settings.

• Candles : Displays the non-smooth IER and two moving averages of different lengths as candles .

The `open` and `close` of the candle are the longest and shortest length MAs of the IER respectively.

The `high` and `low` of the candle are the max and min of the IER, longest length MA of the IER, and shortest length MA of the IER respectively.

Colors for this display can be customized via the "Candles" portion of the "Visuals" section in the script settings.

• Circles : Displays three MAs of the IER as circles .

The color of each plot depends on the percent rank of the respective MA over the previous 100 bars.

Different colors are triggered when ranks are below 10%, between 10% and 50%, between 50% and 90%, and above 90%.

Colors for this display can be customized via the "Circles" portion of the "Visuals" section in the script settings.

With either display type, an optional information box can be displayed. This box shows the LTF that the script is using, the average number of lower timeframe bars per chart bar, and the number of chart bars that contain LTF data.

Specifying intrabar precision

Ten options are included in the script to control the number of intrabars used per chart bar for calculations. The greater the number of intrabars per chart bar, the fewer chart bars can be analyzed.

The first five options allow users to specify the approximate amount of chart bars to be covered:

• Least Precise (Most chart bars) : Covers all chart bars by dividing the current timeframe by four.

This ensures the highest level of intrabar precision while achieving complete coverage for the dataset.

• Less Precise (Some chart bars) & More Precise (Less chart bars) : These options calculate a stepped LTF in relation to the current chart's timeframe.

• Very precise (2min intrabars) : Uses the second highest quantity of intrabars possible with the 2min LTF.

• Most precise (1min intrabars) : Uses the maximum quantity of intrabars possible with the 1min LTF.

The stepped lower timeframe for "Less Precise" and "More Precise" options is calculated from the current chart's timeframe as follows:

Chart Timeframe Lower Timeframe

Less Precise More Precise

< 1hr 1min 1min

< 1D 15min 1min

< 1W 2hr 30min

> 1W 1D 60min

The last five options allow users to specify an approximate fixed number of intrabars to analyze per chart bar. The available choices are 12, 24, 50, 100, and 250. The script will calculate the LTF which most closely approximates the specified number of intrabars per chart bar. Keep in mind that due to factors such as the length of a ticker's sessions and rounding of the LTF, it is not always possible to produce the exact number specified. However, the script will do its best to get as close to the value as possible.

Specifying MA type

Seven MA types are included in the script for different averaging effects:

• Simple

• Exponential

• Wilder (RMA)

• Weighted

• Volume-Weighted

• Arnaud Legoux with `offset` and `sigma` set to 0.85 and 6 respectively.

• Hull

Weighting

This script includes the option to weight IER values based on the percent rank of absolute price changes on the current chart's timeframe over a specified period, which can be enabled by checking the "Weigh using relative close changes" option in the script settings. This places reduced emphasis on IER values from smaller changes, which may help to reduce noise in the output.

█ FOR Pine Script™ CODERS

• This script imports the recently published lower_ltf library for calculating intrabar statistics and the optimal lower timeframe in relation to the current chart's timeframe.

• This script uses the recently released request.security_lower_tf() Pine Script™ function discussed in this blog post .

It works differently from the usual request.security() in that it can only be used on LTFs, and it returns an array containing one value per intrabar.

This makes it much easier for programmers to access intrabar information.

• This script implements a new recommended best practice for tables which works faster and reduces memory consumption.

Using this new method, tables are declared only once with var , as usual. Then, on the first bar only, we use table.cell() to populate the table.

Finally, table.set_*() functions are used to update attributes of table cells on the last bar of the dataset.

This greatly reduces the resources required to render tables.

Look first. Then leap.

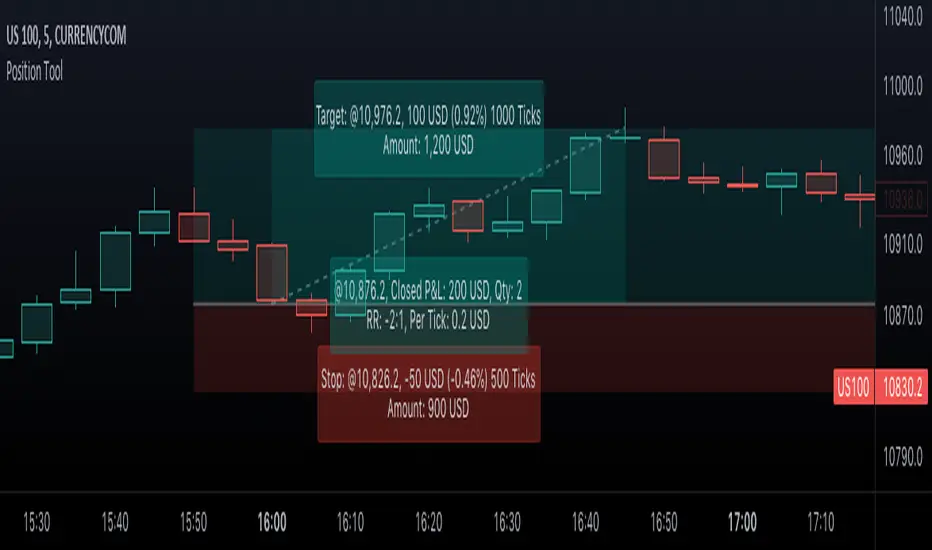

Position Tool█ OVERVIEW

This script is an interactive measurement tool that can be used to evaluate or keep track of trades. Like the long and short position drawing tools, it calculates a risk reward ratio and a risk-adjusted position size from the entry, stop and take profit levels, but it also does much more:

• It can be used to configure long or short trades.

• All monetary values can be expressed in any number of currencies.

• The value of tick/pip movement (which varies with the position's size) is displayed in the currency you have selected.

• The CAGR ( Compound Annual Growth Rate ) for the trade can be displayed.

• It does live tracking of the position.

• You can configure alerts on entries and exits.

█ HOW TO USE IT

Load the indicator on an active chart (see here if you don't know how).

When you first load this script on a chart, you will enter an interactive selection mode where the script asks you to pick three points in price and time on your chart by clicking on the chart. Directions will appear in a blue box at the bottom of the screen with each click of the mouse. The first selection is the entry point for the trade you are considering, which takes into account both the time and level you choose, the next are the take profit and stop levels. Once you have selected all three points, the script will draw trade zones and labels containing the trade metrics. The script determines if the trade is a long or short from the position of the take profit and stop loss levels in relation to the entry price. If the take profit level is above the entry price, the stop must be below and vice versa, otherwise an error occurs.

You can change levels by dragging the handles that appear when you select the indicator, or by entering new values in the script's settings. The only way to re-enter interactive mode is to re-add the indicator to your chart.

Once you place the position tool on a chart, it will appear at the same levels on all symbols you use. If your scale is not set to "Scale price chart only", the position tool's levels will be taken into account when scaling the chart, which can cause the symbol's bars to be compressed. If your scale is set to "Scale price chart only", the position tool will still be there, but it will not impact the scale of the chart's bars, so you won't see it if it sits outside the symbol's price scale.

If you select the position tool on your chart and delete it, this will also delete the indicator from the chart. You will need to re-add it if you want to draw another position tool. You can add multiple instances of the indicator if you need a position tool on more than one of your charts.

█ FEATURES

Display

The position tool displays the following information for entries:

• The entry's price level with an '@' sign before it.

• Open or Closed P&L : For an open trade, the "Open P&L" displays the difference in money value between the entry level and the chart's current price.

For a closed trade, the "Closed P&L" displays the realized P&L on the trade.

• Quantity : The trade size, which takes into account the risk tolerance you set in the script's settings.

• RR : The reward to risk ratio expresses the relationship of the distance between the entry and the take profit level vs the entry and the stop level.

Example: A $100 stop with a $100 target will have a ratio of 1:1, whereas a $200 target with the same stop will have a 2:1 ratio.

• Per tick/pip : Represents the money value of a tick or pip movement.

• CAGR : The Compound Annual Growth Rate will be displayed on the main order label on trades that exceed one day in duration.

This value is calculated the same way as in our CAGR Custom Range indicator.

If the trade duration is less than one day, the metric will not be present in the display.

The stop and take profit levels display:

• Their price level with an '@' sign before it.

• Their distance from the entry in money value, percentage and ticks/pips.

• The projected end money value of the position if the level is reached. These values are calculated based on the trade size and the currency.

Currency adjustments

This indicator modifies the trade label's colors and values based on the final Profit and Loss (P&L), which considers the dynamic exchange rate between base and conversion currencies in its calculations when the conversion currency is a specified value other than the default. Depending on the cross rate between the base and account currencies, this process can yield a negative P&L on an otherwise successful simulated trade.

For instance, if your account is in currency XYZ, you might buy 10 Apple shares at $150 each, with the XYZ to USD exchange rate being 2:1. This purchase would cost you 3000 units of XYZ. Suppose that later on, the shares appreciate to $170 each, and you decide to sell. One might expect this trade to result in profit. However, if the exchange rate has now equalized to 1:1, the return on selling the shares, calculated in XYZ, would only be 1700 units, resulting in a loss of 1300 units XYZ.

The indicator will mark the P&L and the target labels in red in such cases, regardless of whether the market price reached the profit target, as the trade produced a net loss due to reduced funds after currency conversion. Conversely, an otherwise unsuccessful position can result in a net profit in the account currency due to conversion rate fluctuations. The final losses or gains appear in the label metrics, and the corresponding color coding reflects the trade's success or failure.

Settings

The settings in the "Trade sizing" section are used to calculate the position size and the monetary value of trades. Two types of risk can be chosen from the menu; a percentage based risk calculation, or a fixed money value. The risk is used to calculate the quantity of units to purchase to achieve that level of risk exposure. Example: An account size of $1000 and 10% risk will have a projected end amount of $900 if the stop loss is hit. The quantity is a product of this relationship; a projected number of units to allow for the equivalent of $100 of risk exposure over the change in price from the entry to the stop value.

The "Trade levels" allow you to manually set the entry, take profit and stop levels of an existing position tool on your chart.

You can control the appearance of the tool and the values it displays in the settings following these first two sections.

Alerts

Three alerts that will trigger when you configure an alert on this indicator. The first will send an alert when the entry price is breached by price action if that price has not already been breached in the previous price history. This is dependant on the entry location you select when placing the indicator on the chart. The other two alerts will trigger when either the stop loss or the take profit level is breached to signal that a trade exit has occurred.

█ NOTES FOR Pine Script™ CODERS

• Interactive inputs are implemented for input.time() and input.price() . These specialized input functions allow users to interact with a script.

You can create one interactive input for both time and price values by using the same `inline` argument in a pair of input.time() and input.price() function calls.

• We use the `cagr()` function from our ta library.

• The script uses the runtime.error() function to throw an error if the stop and limit prices are not placed on opposing sides of the entry price.

• We use the `currency` parameter in a request.security() call to convert currencies.

Look first. Then leap.

Chart CAGR█ OVERVIEW

This simple script displays in the lower-right corner of the chart the Growth Rate and the Compound Annual Growth Rate (CAGR) between the open of the chart's first visible bar and the close of its last bar. As you zoom/scroll the chart, calculations will adjust to the chart's bars. You can change the location and colors of the displayed text in the script's settings.

If you need to calculate the CAGR between any two points on the chart, see our CAGR Custom Range indicator.

█ FOR Pine Script™ CODERS

Like our Chart VWAP publication, this script calculates on the range of visible bars utilizing the new Pine Script™ functions announced here and the VisibleChart library by PineCoders . It also uses the `cagr()` function from our ta library, which was recently augmented with many new functions.

Look first. Then leap.

Chart VWAP█ OVERVIEW

This indicator displays a Volume-Weighted Average Price anchored to the leftmost visible bar of the chart. It dynamically recalculates when the chart's visible bars change because you scroll or zoom your chart.

If you are not already familiar with VWAP, our Help Center will get you started. The typical VWAP is designed to be used on intraday charts, as it resets at the beginning of the day. Our Rolling VWAP , instead, resets on a rolling time window. You may also find the VWAP Auto Anchored built-in indicator worth a try.

█ HOW TO USE IT

Load the indicator on an active chart (see the Help Center if you don't know how). By default, it displays the chart's VWAP in orange and a simple average of the chart's visible close values in gray. This average can be used as a companion to the VWAP, since both are calculated from the same set of bars. The script's settings allow you to hide it.

You may also use the script's settings to enable the display of the chart's OHLC (open, high, low, close) levels and the values of the high and low. These are also calculated from the range of visible bars. You can complement the high and low lines with their price and their distance in percent from the chart's latest visible close . You can use the levels to quickly identify the distances from extreme points in the visible price range, as well as observe the visible chart's beginning and end prices.

█ NOTES FOR Pine Script™ CODERS

This script showcases three novelties:

• Dynamic recalculation on visible bars

• The VisibleChart library by PineCoders

• The new `anchor` parameter of ta.vwap()

Dynamic recalculation on visible bars

This script behaves in a novel way made possible by the recent introduction of two new built-in variables: chart.left_visible_bar_time and chart.right_visible_bar_time , which return the opening time of the leftmost and rightmost visible bars on the chart. These are only two of many new built-ins in the `chart.*` namespace. See this blog post for more information, or look up them up by typing "chart." in the Pine Script™ Reference Manual .

Any script using chart.left_visible_bar_time or chart.right_visible_bar_time acquires a unique property, which triggers its recalculation when traders scroll or zoom their chart, causing the range of visible bars to change. This new capability is what makes it possible for this script to calculate its VWAP on the chart's visible bars only, and dynamically recalculate if the user scrolls or zooms their chart.

This script is just a start to the party; endless uses for indicators that redraw on changes to the chart will no doubt emerge through the hands of our community's Pine Script™ programmers.

The VisibleChart library by PineCoders

The newly published VisibleChart library is designed to help programmers benefit from the new capabilities made possible by the fact that Pine Script™ code can now tell when it is executing on visible bars. The library's description, functions and example code will help programmers make the most of the new feature.

This script uses three of the library's functions:

• `PCvc.vVwap()` calculates a VWAP for visible bars.

• `PCvc.avg()` calculates the average of a source value for visible bars only. We use it to calculate the average close (the default source).

• `PCvc.chartXTimePct(25)` calculates a time value corresponding to 25% of the horizontal distance between visible bars, starting from the left.

The new `anchor` parameter of ta.vwap()

Our script also uses this new `anchor` parameter to reset the VWAP at the leftmost visible bar. See how simple the code is for the VisibleChart library's `vVwap()` function.

Look first. Then leap.

Polarity Divergences█ OVERVIEW

This indicator looks at the polarity of the intrabars composing a chart bar and fills chart candles orange when a majority of intrabars does not have the same polarity as that of the chart bar.

█ CONCEPTS

Bar polarity

By bar polarity , we mean the direction of a bar, which is determined by looking at the bar's close vs its open .

Intrabars

Intrabars are chart bars at a lower timeframe than the chart's. Each 1H chart bar of a 24x7 market will, for example, usually contain 60 bars at the lower timeframe of 1min, provided there was market activity during each minute of the hour. Mining information from intrabars can be useful in that it offers traders visibility on the activity inside a chart bar.

Lower timeframes (LTFs)

A lower timeframe is a timeframe that is smaller than the chart's timeframe. This script determines which LTF to use by examining the chart's timeframe. The LTF determines how many intrabars are examined for each chart bar; the lower the timeframe, the more intrabars are analyzed. This table shows which LTF is used for each range of chart timeframes:

Chart TF LTF

< 1D 1min

< 1W 30min

>= 1W 1D

█ HOW TO USE IT

The idea underlying this indicator is that if the polarity of a chart bar is up or down, the majority of its constituent intrabars should also be up or down. If that is not the case, then we can consider the bar to be abnormal, and so worthy of our attention. You will notice that such anomalies often occur before reversals, but irregularities do not necessarily announce reversals, as they also occur on pauses in trends or in trend-less conditions.

The indicator will update in real time, as intrabars composing the realtime chart bar are gradually built. The closer the realtime bar is to being closed, the more reliable the result will be, as that is when the indicator can analyze the most intrabars.

█ NOTES FOR Pine Script™ CODERS

This script uses the recently released request.security_lower_tf() Pine Script™ function discussed in this blog post . It works differently from the usual request.security() in that it can only be used at LTFs, and it returns an array containing one value per intrabar. This makes it much easier for programmers to access intrabar information.

A script can access a maximum of 100K intrabars; that is the reason we step the LTF by taking into account the chart's timeframe. By progressively increasing the LTF as the chart's timeframe increases, we provide users with optimal coverage of the chart bars. Always using a 1min LTF would, for example, limit the chart coverage to the last 69 bars on a 1D chart of a 24x7 market because each chart bar will usually contain 1440 intrabars (100K / 1440 = 69.4). By using a 30min LTF for 1D charts, we cover 100K / 48 = 2083 bars.

Look first. Then leap.

Rolling VWAP█ OVERVIEW

This indicator displays a Rolling Volume-Weighted Average Price. Contrary to VWAP indicators which reset at the beginning of a new time segment, RVWAP calculates using a moving window defined by a time period (not a simple number of bars), so it never resets.

█ CONCEPTS

If you are not already familiar with VWAP, our Help Center will get you started.

The typical VWAP is designed to be used on intraday charts, as it resets at the beginning of the day. Such VWAPs cannot be used on daily, weekly or monthly charts. Instead, this rolling VWAP uses a time period that automatically adjusts to the chart's timeframe. You can thus use RVWAP on any chart that includes volume information in its data feed.

Because RVWAP uses a moving window, it does not exhibit the jumpiness of VWAP plots that reset. You can see the more jagged VWAP on the chart above. We think both can be useful to traders; up to you to decide which flavor works for you.

█ HOW TO USE IT

Load the indicator on an active chart (see the Help Center if you don't know how).

Time period

By default, the script uses an auto-stepping mechanism to adjust the time period of its moving window to the chart's timeframe. The following table shows chart timeframes and the corresponding time period used by the script. When the chart's timeframe is less than or equal to the timeframe in the first column, the second column's time period is used to calculate RVWAP:

Chart Time

timeframe period

1min 🠆 1H

5min 🠆 4H

1H 🠆 1D

4H 🠆 3D

12H 🠆 1W

1D 🠆 1M

1W 🠆 3M

You can use the script's inputs to specify a fixed time period, which you can express in any combination of days, hours and minutes.

By default, the time period currently used is displayed in the lower-right corner of the chart. The script's inputs allow you to hide the display or change its size and location.

Minimum Window Size

This input field determines the minimum number of values to keep in the moving window, even if these values are outside the prescribed time period. This mitigates situations where a large time gap between two bars would cause the time window to be empty, which can occur in non-24x7 markets where large time gaps may separate contiguous chart bars, namely across holidays or trading sessions. For example, if you were using a 1D time period and there is a two-day gap between two bars, then no chart bars would fit in the moving window after the gap. The default value is 10 bars.

█ NOTES

If you are interested in VWAP indicators, you may find the VWAP Auto Anchored built-in indicator worth a try.

For Pine Script™ coders

The heart of this script's calculations uses the `totalForTimeWhen()` function from the ConditionalAverages library published by PineCoders . It works by maintaining an array of values included in a time period, but without a for loop requiring a lookback from the current bar, so it is much more efficient.

We write our Pine Script™ code using the recommendations in the User Manual's Style Guide .

Look first. Then leap.

Strategy█ OVERVIEW

This library is a Pine Script™ programmer’s tool containing a variety of strategy-related functions to assist in calculations like profit and loss, stop losses and limits. It also includes several useful functions one can use to convert between units in ticks, price, currency or a percentage of the position's size.

█ CONCEPTS

The library contains three types of functions:

1 — Functions beginning with `percent` take either a portion of a price, or the current position's entry price and convert it to the value outlined in the function's documentation.

Example: Converting a percent of the current position entry price to ticks, or calculating a percent profit at a given level for the position.

2 — Functions beginning with `tick` convert a tick value to another form.

These are useful for calculating a price or currency value from a specified number of ticks.

3 — Functions containing `Level` are used to calculate a stop or take profit level using an offset in ticks from the current entry price.

These functions can be used to plot stop or take profit levels on the chart, or as arguments to the `limit` and `stop` parameters in strategy.exit() function calls.

Note that these calculated levels flip automatically with the position's bias.

For example, using `ticksToStopLevel()` will calculate a stop level under the entry price for a long position, and above the entry price for a short position.

There are also two functions to assist in calculating a position size using the entry's stop and a fixed risk expressed as a percentage of the current account's equity. By varying the position size this way, you ensure that entries with different stop levels risk the same proportion of equity.

█ NOTES

Example code using some of the library's functions is included at the end of the library. To see it in action, copy the library's code to a new script in the Pine Editor, and “Add to chart”.

For each trade, the code displays:

• The entry level in orange.

• The stop level in fuchsia.

• The take profit level in green.

The stop and take profit levels automatically flip sides based on whether the current position is long or short.

Labels near the last trade's levels display the percentages used to calculate them, which can be changed in the script's inputs.

We plot markers for entries and exits because strategy code in libraries does not display the usual markers for them.

Look first. Then leap.

█ FUNCTIONS

percentToTicks(percent) Converts a percentage of the average entry price to ticks.

Parameters:

percent : (series int/float) The percentage of `strategy.position_avg_price` to convert to ticks. 50 is 50% of the entry price.

Returns: (float) A value in ticks.

percentToPrice(percent) Converts a percentage of the average entry price to a price.

Parameters:

percent : (series int/float) The percentage of `strategy.position_avg_price` to convert to price. 50 is 50% of the entry price.

Returns: (float) A value in the symbol's quote currency (USD for BTCUSD).

percentToCurrency(price, percent) Converts the percentage of a price to money.

Parameters:

price : (series int/float) The symbol's price.

percent : (series int/float) The percentage of `price` to calculate.

Returns: (float) A value in the symbol's currency.

percentProfit(exitPrice) Calculates the profit (as a percentage of the position's `strategy.position_avg_price` entry price) if the trade is closed at `exitPrice`.

Parameters:

exitPrice : (series int/float) The potential price to close the position.

Returns: (float) Percentage profit for the current position if closed at the `exitPrice`.

priceToTicks(price) Converts a price to ticks.

Parameters:

price : (series int/float) Price to convert to ticks.

Returns: (float) A quantity of ticks.

ticksToPrice(price) Converts ticks to a price offset from the average entry price.

Parameters:

price : (series int/float) Ticks to convert to a price.

Returns: (float) A price level that has a distance from the entry price equal to the specified number of ticks.

ticksToCurrency(ticks) Converts ticks to money.

Parameters:

ticks : (series int/float) Number of ticks.

Returns: (float) Money amount in the symbol's currency.

ticksToStopLevel(ticks) Calculates a stop loss level using a distance in ticks from the current `strategy.position_avg_price` entry price. This value can be plotted on the chart, or used as an argument to the `stop` parameter of a `strategy.exit()` call. NOTE: The stop level automatically flips based on whether the position is long or short.

Parameters:

ticks : (series int/float) The distance in ticks from the entry price to the stop loss level.

Returns: (float) A stop loss level for the current position.

ticksToTpLevel(ticks) Calculates a take profit level using a distance in ticks from the current `strategy.position_avg_price` entry price. This value can be plotted on the chart, or used as an argument to the `limit` parameter of a `strategy.exit()` call. NOTE: The take profit level automatically flips based on whether the position is long or short.

Parameters:

ticks : (series int/float) The distance in ticks from the entry price to the take profit level.

Returns: (float) A take profit level for the current position.

calcPositionSizeByStopLossTicks(stopLossTicks, riskPercent) Calculates the position size needed to implement a given stop loss (in ticks) corresponding to `riskPercent` of equity.

Parameters:

stopLossTicks : (series int) The stop loss (in ticks) that will be used to protect the position.

riskPercent : (series int/float) The maximum risk level as a percent of current equity (`strategy.equity`).

Returns: (int) A quantity of contracts.

calcPositionSizeByStopLossPercent(stopLossPercent, riskPercent, entryPrice) Calculates the position size needed to implement a given stop loss (%) corresponding to `riskPercent` of equity.

Parameters:

stopLossPercent : (series int/float) The stop loss in percent that will be used to protect the position.

riskPercent : (series int/float) The maximum risk level as a percent of current equity (`strategy.equity`).

entryPrice : (series int/float) The entry price of the position.

Returns: (int) A quantity of contracts.

exitPercent(id, lossPercent, profitPercent, qty, qtyPercent, comment, when, alertMessage) A wrapper of the `strategy.exit()` built-in which adds the possibility to specify loss & profit in as a value in percent. NOTE: this function may work incorrectly with pyramiding turned on due to the use of `strategy.position_avg_price` in its calculations of stop loss and take profit offsets.

Parameters:

id : (series string) The order identifier of the `strategy.exit()` call.

lossPercent : (series int/float) Stop loss as a percent of the entry price.

profitPercent : (series int/float) Take profit as a percent of the entry price.

qty : (series int/float) Number of contracts/shares/lots/units to exit a trade with. The default value is `na`.

qtyPercent : (series int/float) The percent of the position's size to exit a trade with. If `qty` is `na`, the default value of `qty_percent` is 100.

comment : (series string) Optional. Additional notes on the order.

when : (series bool) Condition of the order. The order is placed if it is true.

alertMessage : (series string) An optional parameter which replaces the {{strategy.order.alert_message}} placeholder when it is used in the "Create Alert" dialog box's "Message" field.

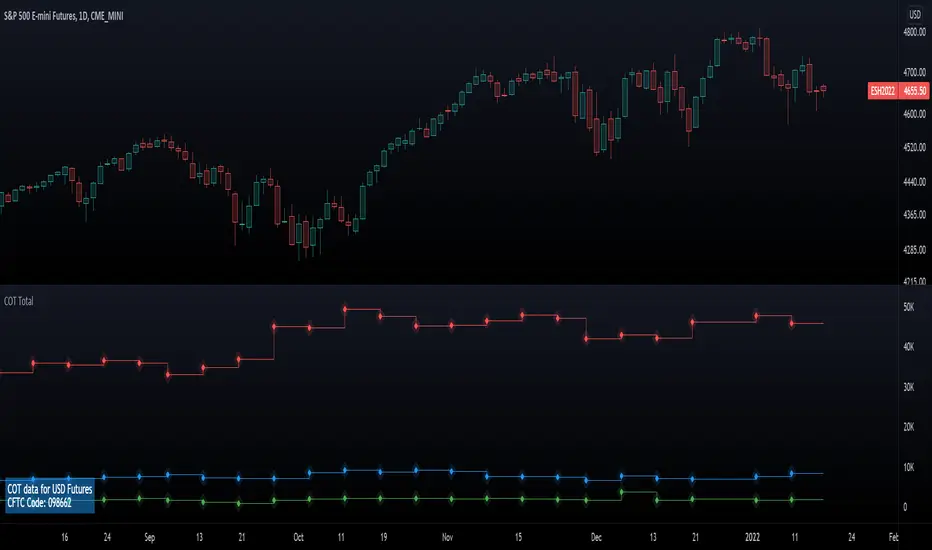

Commitment of Traders: Legacy Metrics█ OVERVIEW

This indicator displays the Commitment of Traders (COT) legacy data for futures markets.

█ CONCEPTS

Commitment of Traders (COT) data is tallied by the Commodity Futures Trading Commission (CFTC) , a US federal agency that oversees the trading of derivative markets such as futures in the US. It is weekly data that provides traders with information about open interest for an asset. The CFTC oversees derivative markets traded on different exchanges, so COT data is available for assets that can be traded on CBOT, CME, NYMEX, COMEX, and ICEUS.

A detailed description of the COT report can be found on the CFTC's website .

COT data is separated into three notable reports: Legacy, Disaggregated, and Financial. This indicator presents data from the legacy report, which is broken down by exchange. Legacy reports break down the reportable open interest positions into two classifications: non-commercial and commercial traders.

Our other COT indicators are:

• Commitment of Traders: Disaggregated Metrics

• Commitment of Traders: Financial Metrics

• Commitment of Traders: Total

█ HOW TO USE IT

Load the indicator on an active chart (see here if you don't know how).

By default, the indicator uses the chart's symbol to derive the COT data it displays. You can also specify a CFTC code in the "CFTC code" field of the script's inputs to display COT data from a symbol different than the chart's.

The rest of this section documents the script's input fields.

Metric

Each metric represents a different column of the Commitment of Traders report. Details are available in the explanatory notes on the CFTC's website .

Here is a summary of the metrics:

• "Open Interest" is the total of all futures and/or option contracts entered into and not yet offset by a transaction, by delivery, by exercise, etc.

The aggregate of all long open interest is equal to the aggregate of all short open interest.

• "Traders Total" is the number of all unique reportable traders, regardless of the trading direction.

• "Traders Total Reportable/Traders Noncommercial/Traders Commercial" are the quantities of traders reported to hold any position with the specified direction.

All of a trader's reported futures positions in a commodity are classified as commercial if the trader uses futures contracts in that particular commodity for hedging.

To determine the total number of reportable traders in a market, a trader is counted only once, whether or not the trader appears in more than one category.

• "Total Reportable/Noncommercial/Commercial Positions" are all positions held by all reportable/non-commercial/commercial traders.

• "Non-reportable Positions" is derived by subtracting total long and short "Reportable Positions" from the total open interest.

Accordingly, the number of traders involved and the commercial/non-commercial classification of each trader are unknown.

• "Concentration Gross/Net LT 4/8 TDR" is the percentage of open interest held by 4/8 of the largest traders, by gross/net positions,

without regard to whether they are classified as commercial or non-commercial. The Net position ratios are computed after offsetting each trader’s equal long and short positions.

A reportable trader with relatively large, balanced long and short positions in a single market, therefore,

may be among the four and eight largest traders in both the gross long and gross short categories, but will probably not be included among the four and eight largest traders on a net basis.

Direction

Each metric is available for a particular set of directions. Valid directions for each metric are specified with its name in the "Metric" field's dropdown menu.

Type

Possible values are: All, Old, Other. When commodities have a well-defined marketing season or crop year (e.g. Wheat or Lean Hogs futures), this determines how the data is aggregated. Detailed explanation can be found in the "Old and Other Futures" section of the CTFC Explanatory Notes linked above. The "Major Markets for Which the COT Data Is Shown by Crop Year" table in the Explanatory Notes specifies the commodities that this distinction applies to; selecting "Old" for any of the commodities not in that list will return the same data as in "All", while selecting "Other" will return 0.

COT Selection Mode

This field's value determines how the script determines which COT data to return from the chart's symbol:

- "Root" uses the root of a futures symbol ("ES" for "ESH2020").

- "Base currency" uses the base currency in a forex pair ("EUR" for "EURUSD").

- "Currency" uses the quote currency, i.e., the currency the symbol is traded in ("JPY" for "TSE:9984" or "USDJPY").

- "Auto" tries all modes, in turn.

If no COT data can be found, a runtime error is generated.

Note that if the "CTFC Code" input field contains a code, it will override this input.

Futures/Options

Specifies the type of Commitment of Traders data to display: data concerning only Futures, only Options, or both.

CTFC Code

Instead of letting the script generate the CFTC COT code from the chart and the "COT Selection Mode" input when this field is empty, you can specify an unrelated CFTC COT code here, e.g., 001602 for wheat futures.

Look first. Then leap.

Commitment of Traders: Disaggregated Metrics█ OVERVIEW

This indicator displays the Commitment of Traders (COT) Disaggregated data for futures markets.

█ CONCEPTS

Commitment of Traders (COT) data is tallied by the Commodity Futures Trading Commission (CFTC) , a US federal agency that oversees the trading of derivative markets such as futures in the US. It is weekly data that provides traders with information about open interest for an asset. The CFTC oversees derivative markets traded on different exchanges, so COT data is available for assets that can be traded on CBOT, CME, NYMEX, COMEX, and ICEUS.

A detailed description of the COT report can be found on the CFTC's website .

COT data is separated into three notable reports: Legacy, Disaggregated, and Financial. This indicator presents data from the Disaggregated report. The disaggregated reports are broken down by agriculture, petroleum and products, natural gas and products, electricity and metals and other physical contracts. The Disaggregated reports break down the reportable open interest positions into four classifications: Producer/Merchant/Processor/User, Swap Dealers, Managed Money, and Other Reportables.

Our other COT indicators are:

• Commitment of Traders: Legacy Metrics

• Commitment of Traders: Financial Metrics

• Commitment of Traders: Total

█ HOW TO USE IT

Load the indicator on an active chart (see here if you don't know how).

By default, the indicator uses the chart's symbol to derive the COT data it displays. You can also specify a CFTC code in the "CFTC code" field of the script's inputs to display COT data from a symbol different than the chart's.

The rest of this section documents the script's input fields.

Metric

Each metric represents a different column of the Commitment of Traders report. Details are available in the explanatory notes on the CFTC's website .

Here is a summary of the metrics:

• "Open Interest" is the total of all futures and/or option contracts entered into and not yet offset by a transaction, by delivery, by exercise, etc.

The aggregate of all long open interest is equal to the aggregate of all short open interest.

• "Traders Total" is the quantity of all unique reportable traders, regardless of the trading direction.

• "Traders Producer Merchant" is the number of traders classified as a "producer/merchant/processor/user" reported holding any position with the specified direction.

A "producer/merchant/processor/user" is an entity that predominantly engages in the production, processing, packing or handling of a physical commodity and

uses the futures markets to manage or hedge risks associated with those activities.

• "Traders Swap" is the number of traders classified as "swap dealers" reported holding any position with the specified direction.

A "swap dealer" is an entity that deals primarily in swaps for a commodity and uses the futures markets to manage or hedge the risk associated with those swaps transactions.

The swap dealer’s counterparties may be speculative traders, like hedge funds, or traditional commercial clients that are managing risk arising from their dealings in the physical commodity.

• "Traders Managed Money" is the number of traders classified as "money managers" reported holding any position with the specified direction.

A "money manager" is a registered trader that is engaged in managing and conducting organized futures trading on behalf of clients.

• "Traders Other Reportable" is the number of reportable traders that are not placed in any of the three categories specified above.

• "Traders Total Reportable" is the number of traders reported holding any position with the specified direction.

To determine the total number of reportable traders in a market, a trader is counted only once whether or not the trader appears in more than one category.

As a result, the sum of the numbers of traders in each separate category typically exceeds the total number of reportable traders.

• "Producer Merchant/Swap/Managed Money/Total Reportable/Other Reportable Positions" is all positions held by the traders of the specified category.

• "Nonreportable Positions" is the long and short open interest derived by subtracting the total long and short reportable positions from the total open interest.

Accordingly, the number of traders involved and the classification of each trader are unknown.

• "Concentration Gross/Net LE 4/8 TDR" is the percentage of open interest held by 4/8 of the largest traders (entities), by Gross/Net positions, without regard to how they are classified.

The Net position ratios are computed after offsetting each trader’s equal long and short positions.

A reportable trader with relatively large, balanced long and short positions in a single market,

therefore, may be among the four and eight largest traders in both the gross long and gross short categories,

but will probably not be included among the four and eight largest traders on a net basis.

Direction

Each metric is available for a particular set of directions. Valid directions for each metric are specified with its name in the "Metric" field's dropdown menu.

Type

Possible values are: All, Old, Other. When commodities have a well-defined marketing season or crop year (e.g. Wheat or Lean Hogs futures), this determines how the data is aggregated. Detailed explanation can be found in the "Old and Other Futures" section of the CTFC Explanatory Notes linked above. The "Major Markets for Which the COT Data Is Shown by Crop Year" table in the Explanatory Notes specifies the commodities that this distinction applies to; selecting "Old" for any of the commodities not in that list will return the same data as in "All", while selecting "Other" will return 0.

Futures/Options

Specifies the type of Commitment of Traders data to display: data concerning only Futures, only Options, or both.

CTFC Code

Instead of letting the script generate the CFTC COT code from the chart and the "COT Selection Mode" input when this field is empty, you can specify an unrelated CFTC COT code here, e.g., 001602 for wheat futures.

Look first. Then leap.

Commitment of Traders: Financial Metrics█ OVERVIEW

This indicator displays the Commitment of Traders (COT) financial data for futures markets.

█ CONCEPTS

Commitment of Traders (COT) data is tallied by the Commodity Futures Trading Commission (CFTC) , a US federal agency that oversees the trading of derivative markets such as futures in the US. It is weekly data that provides traders with information about open interest for an asset. The CFTC oversees derivative markets traded on different exchanges, so COT data is available for assets that can be traded on CBOT, CME, NYMEX, COMEX, and ICEUS.

A detailed description of the COT report can be found on the CFTC's website .

COT data is separated into three notable reports: Legacy, Disaggregated, and Financial. This indicator presents data from the COT Financial (Traders in Financial Futures) report. The Financial report includes financial contracts, such as currencies, US Treasury securities, Eurodollars, stocks, VIX and Bloomberg commodity index. As such, the TFF data is limited to financial-related tickers. The TFF report breaks down the reportable open interest positions into four classifications: Dealer/Intermediary, Asset Manager/Institutional, Leveraged Funds, and Other Reportables.

Our other COT indicators are:

• Commitment of Traders: Legacy Metrics

• Commitment of Traders: Disaggregated Metrics

• Commitment of Traders: Total

█ HOW TO USE IT

Load the indicator on an active chart (see here if you don't know how).

By default, the indicator uses the chart's symbol to derive the COT data it displays. You can also specify a CFTC code in the "CFTC code" field of the script's inputs to display COT data from a symbol different than the chart's.

The rest of this section documents the script's input fields.

Metric

Each metric represents a different column of the Commitment of Traders report. Details are available in the explanatory notes on the CFTC's website .

Here is a summary of the metrics:

• "Open Interest" is the total of all futures and/or option contracts entered into and not yet offset by a transaction, by delivery, by exercise, etc.

The aggregate of all long open interest is equal to the aggregate of all short open interest.

• "Traders Total" is the number of all unique reportable traders, regardless of the trading direction.

• "Traders Dealer" is the number of traders classified as a "Dealer/Intermediary" reported holding any position with the specified direction.

A "producer/merchant/processor/user" is an entity typically described as the “sell side” of the market.

Though they may not predominately sell futures, they do design and sell various financial assets to clients.

They tend to have matched books or offset their risk across markets and clients.

Futures contracts are part of the pricing and balancing of risk associated with the products they sell and their activities.

• "Traders Asset Manager" is the number of traders classified as "Asset Manager/Institutional" reported holding any position with the specified direction.

These are institutional investors, including pension funds, endowments, insurance companies,

mutual funds and those portfolio/investment managers whose clients are predominantly institutional.

• "Traders Leveraged Funds" is the number of traders classified as "Leveraged Funds" reported holding any position with the specified direction.

These are typically hedge funds and various types of money managers. The traders may be engaged in managing and

conducting proprietary futures trading and trading on behalf of speculative clients.

• "Traders Other Reportable" is the number of reportable traders that are not placed in any of the three categories specified above.

The traders in this category mostly are using markets to hedge business risk, whether that risk is related to foreign exchange, equities or interest rates.

This category includes corporate treasuries, central banks, smaller banks, mortgage originators, credit unions and any other reportable traders not assigned to the other three categories.

• "Traders Total Reportable" is the number of all traders reported holding any position with the specified direction.

To determine the total number of reportable traders in a market, a trader is counted only once whether or not the trader appears in more than one category.

As a result, the sum of the numbers of traders in each separate category typically exceeds the total number of reportable traders.

• "Dealer/Asset Manager/Leveraged Funds/Total Reportable/Other Reportable Positions -- all positions held by the traders of the specified category.

• "Nonreportable Positions" is the long and short open interest derived by subtracting the total long and short reportable positions from the total open interest.

Accordingly, the number of traders involved and the commercial/non-commercial classification of each trader are unknown.

• "Concentration Gross/Net LT 4/8 TDR" is the percentage of open interest held by 4/8 of the largest traders, by gross/net positions,

without regard to whether they are classified as commercial or non-commercial. The Net position ratios are computed after offsetting each trader’s equal long and short positions.

A reportable trader with relatively large, balanced long and short positions in a single market, therefore,

may be among the four and eight largest traders in both the gross long and gross short categories, but will probably not be included among the four and eight largest traders on a net basis.

Direction

Each metric is available for a particular set of directions. Valid directions for each metric are specified with its name in the "Metric" field's dropdown menu.

COT Selection Mode

This field's value determines how the script determines which COT data to return from the chart's symbol:

- "Root" uses the root of a futures symbol ("ES" for "ESH2020").

- "Base currency" uses the base currency in a forex pair ("EUR" for "EURUSD").

- "Currency" uses the quote currency, i.e., the currency the symbol is traded in ("JPY" for "TSE:9984" or "USDJPY").

- "Auto" tries all modes, in turn.

If no COT data can be found, a runtime error is generated.

Note that if the "CTFC Code" input field contains a code, it will override this input.

Futures/Options

Specifies the type of Commitment of Traders data to display: data concerning only Futures, only Options, or both.

CTFC Code

Instead of letting the script generate the CFTC COT code from the chart and the "COT Selection Mode" input when this field is empty, you can specify an unrelated CFTC COT code here, e.g., 001602 for wheat futures.

Look first. Then leap.

Commitment of Traders: Total█ OVERVIEW

This indicator displays the Commitment of Traders (COT) totals data for futures markets.

█ CONCEPTS

Commitment of Traders (COT) data is tallied by the Commodity Futures Trading Commission (CFTC) , a US federal agency that oversees the trading of derivative markets such as futures in the US. It is weekly data that provides traders with information about open interest for an asset. The CFTC oversees derivative markets traded on different exchanges, so COT data is available for assets that can be traded on CBOT, CME, NYMEX, COMEX, and ICEUS.

A detailed description of the COT report can be found on the CFTC's website .

COT data is separated into three notable reports: Legacy, Disaggregated, and Financial. This indicator presents specific data from the COT Legacy report. The Total data details the positions held by various traders: Commercial Hedgers (traders registered with CFTC that use futures contracts in that particular commodity for hedging), Large Traders (traders registered with CFTC that do not hedge that particular commodity) and Small Traders (not registered with CFTC).

Our other COT indicators are:

• Commitment of Traders: Legacy Metrics

• Commitment of Traders: Disaggregated Metrics

• Commitment of Traders: Financial Metrics

█ HOW TO USE IT

Load the indicator on an active chart (see here if you don't know how).

By default, the indicator uses the chart's symbol to derive the COT data it displays. You can also specify a CFTC code in the "CFTC code" field of the script's inputs to display COT data from a symbol different than the chart's.

The rest of this section documents the script's input fields.

COT Selection Mode

This field's value determines how the script determines which COT data to return from the chart's symbol:

- "Root" uses the root of a futures symbol ("ES" for "ESH2020").

- "Base currency" uses the base currency in a forex pair ("EUR" for "EURUSD").

- "Currency" uses the quote currency, i.e., the currency the symbol is traded in ("JPY" for "TSE:9984" or "USDJPY").

- "Auto" tries all modes, in turn.

If no COT data can be found, a runtime error is generated.

Note that if the "CTFC Code" input field contains a code, it will override this input.

Futures/Options

Specifies the type of Commitment of Traders data to display: data concerning only Futures, only Options, or both.

Display

Determines the direction of the metrics requested from the CTFC report.

CTFC Code

Instead of letting the script generate the CFTC COT code from the chart and the "COT Selection Mode" input when this field is empty, you can specify an unrelated CFTC COT code here, e.g., 001602 for wheat futures.

Look first. Then leap.

CAGR Custom Range█ OVERVIEW

This script calculates an annualized Compound Annual Growth Rate from two points in time which you can select on the chart. It previews an upcoming feature where Pine scripts will be able to provide users with interactive inputs for time and price values.

👉🏼 We are looking for feedback on our first take of this feature.

Please comment in this publication's "Comments" section if you have suggestions for improvement.

█ HOW TO USE IT

When you first load this script on a chart, you will enter the new interactive selection mode. At that point, the script is waiting for you to pick two points in time on your chart by clicking on the chart. Once you select the two points, the script will find the close value for each of the two selected bars, and calculate the CAGR value from them. It will then display a line between the two points, and the CAGR value above or below the last point in time.

If the CAGR value is positive, the line and label will display in their "up" color (see the "🠅" color in the script's "Settings/Inputs" tab), otherwise they appear in their "down" color (the "🠇" color in the inputs). You can also control the line's width from the inputs.

You have the option of comparing the chart's CAGR value with that of another symbol, which you specify in the "Compare to" input. When a comparison is made, the label's background color will be dependent on the result of the comparison. The line's color will still be determined by the chart's value.

Once time points have been selected on the chart and the script is displaying the line, you can change the time points by clicking on the script's name on the chart. A small, blue rectangular handle will then appear for each point, which you can then grab and move. If you reset the inputs using the "Defaults/Reset Settings" button in the script's inputs, the two time points will reset to the beginning of September and October 2021, respectively.

█ CONCEPTS

The CAGR is a notional, annualized growth rate that assumes all profits are reinvested. It calculates from the close value of the two end points. It does not account for drawdowns, so it does not calculate risk. It can be used as a yardstick to compare the performance of two instruments. Because it annualizes values, the function requires a minimum of one day between the two end points (annualizing returns over smaller periods of times doesn't produce very meaningful figures).

█ LIMITATIONS

• The two selected points must be distant from a minimum of one day. A runtime error will occur otherwise.

• There is currently no way to restart the interactive mode from scratch without re-adding the script to the chart.

• The points in time you select on one chart may map quite differently on other charts,

depending on their constituent bars (e.g., intraday charts for 24x7 and conventional markets).

█ FOR PINE CODERS

• Our script uses the most recent version of Pine, as the `//@version=5` compiler directive indicates.

• Interactive inputs were a long-standing and highly-requested feature by our beloved community of Pine coders.

We hope you find this first step promising, as it opens up entirely new possibilities for both Pine coders and script users.

You can, for example, use interactive inputs to draw shapes with your scripts, or support and resistance levels, etc.

We're sure you'll come up with more creative uses of the feature than we could ever dream up )

• Interactive inputs are implemented for input.time() and input.price() , the specialized input functions now available in v5.

See the User Manual's new page on inputs for more information about them.

You can also create one interactive input for both time and price values

by using the same `inline` argument in a pair of input.time() and input.price() function calls.

• Our min/max filtering when initializing `entryTime` and `exitTime` will handle cases where

the script user inverts the two points on the chart.

• The script uses the new runtime.error() function to throw an error in the `if days < 1` conditional structure.

• We use the `cagr()` function from our recently-published ta Pine library .

Pine libraries — not to be confused with the Public Library showcasing scripts published by our community of Pine coders —

are one of the new features available with the recent Pine v5.

• Note that our `strRightOf()` function cannot be used to generate ticker identifier strings for use in `request.*()` functions.

This is because it produces results of "series" form while the functions require

arguments of "simple" form for their `symbol` or `ticker` parameters.

Have a look at our new User Manual page on Pine's Type system if you need to brush up on Pine forms and types.

• We use a simple, repainting request.security() call because our calculations are not used to generate orders or alerts.

• We document our user-defined functions using the same compiler directives used in exported functions in libraries.

It will make conversion of those functions to library format easier if we ever choose to do so.

• We use two Unicode hair spaces (U+200A) to push the "%" sign slightly away from values in our str.format() calls.

While the impact is minimal, it increases readability.

• Note the `priceIsHigh` logic used to determine if we place the label above or below bars.

When price is higher than recent prices, we place the label above the bar, otherwise we place it below.

It's not foolproof but it provides optimal positioning most of the time.

• The point of the complicated "bool" expression initializing `displayCAGR` is to ensure that we only draw the line and labels once.

When no comparison with another symbol is made, this occurs the first time we encounter a non- na value from the `cagr()` function.

When a comparison is required, it occurs the first time both values are not na .

• Before all mentions of "CAGR" in our description, we use a Unicode zero-width space (U+200B)

to prevent the auto-linking feature to kick in for the term.

This prevents the dashed underscore and a link like this (CAGR) from appearing every time "CAGR" is mentioned.

• With Pine v5, the `study()` declaration statement was renamed to indicator() .

Accordingly, we will be eliminating the use of the "study" term from documentation and the UI.

The generic "script" term will continue to designate Pine code that can be an indicator, a strategy or a library, when applicable.

• We followed our new Style guide recommendations to write our script.

• We used the techniques explained in the How We Write and Format Script Descriptions publication by PineCoders.

• That's it! We've covered all the new features and tricks we used. We sincerely hope you enjoy the new interactive inputs,

and please remember to comment here if you have suggestions for improvement. 💙

Look first. Then leap.

taLibrary "ta"

█ OVERVIEW

This library holds technical analysis functions calculating values for which no Pine built-in exists.

Look first. Then leap.

█ FUNCTIONS

cagr(entryTime, entryPrice, exitTime, exitPrice)

It calculates the "Compound Annual Growth Rate" between two points in time. The CAGR is a notional, annualized growth rate that assumes all profits are reinvested. It only takes into account the prices of the two end points — not drawdowns, so it does not calculate risk. It can be used as a yardstick to compare the performance of two instruments. Because it annualizes values, the function requires a minimum of one day between the two end points (annualizing returns over smaller periods of times doesn't produce very meaningful figures).

Parameters:

entryTime : The starting timestamp.

entryPrice : The starting point's price.

exitTime : The ending timestamp.

exitPrice : The ending point's price.

Returns: CAGR in % (50 is 50%). Returns `na` if there is not >=1D between `entryTime` and `exitTime`, or until the two time points have not been reached by the script.

█ v2, Mar. 8, 2022

Added functions `allTimeHigh()` and `allTimeLow()` to find the highest or lowest value of a source from the first historical bar to the current bar. These functions will not look ahead; they will only return new highs/lows on the bar where they occur.

allTimeHigh(src)

Tracks the highest value of `src` from the first historical bar to the current bar.

Parameters:

src : (series int/float) Series to track. Optional. The default is `high`.

Returns: (float) The highest value tracked.

allTimeLow(src)

Tracks the lowest value of `src` from the first historical bar to the current bar.

Parameters:

src : (series int/float) Series to track. Optional. The default is `low`.

Returns: (float) The lowest value tracked.

█ v3, Sept. 27, 2022

This version includes the following new functions:

aroon(length)

Calculates the values of the Aroon indicator.

Parameters:

length (simple int) : (simple int) Number of bars (length).

Returns: ( [float, float ]) A tuple of the Aroon-Up and Aroon-Down values.

coppock(source, longLength, shortLength, smoothLength)

Calculates the value of the Coppock Curve indicator.

Parameters:

source (float) : (series int/float) Series of values to process.

longLength (simple int) : (simple int) Number of bars for the fast ROC value (length).

shortLength (simple int) : (simple int) Number of bars for the slow ROC value (length).

smoothLength (simple int) : (simple int) Number of bars for the weigted moving average value (length).

Returns: (float) The oscillator value.

dema(source, length)

Calculates the value of the Double Exponential Moving Average (DEMA).

Parameters:

source (float) : (series int/float) Series of values to process.

length (simple int) : (simple int) Length for the smoothing parameter calculation.

Returns: (float) The double exponentially weighted moving average of the `source`.

dema2(src, length)

An alternate Double Exponential Moving Average (Dema) function to `dema()`, which allows a "series float" length argument.

Parameters:

src : (series int/float) Series of values to process.

length : (series int/float) Length for the smoothing parameter calculation.

Returns: (float) The double exponentially weighted moving average of the `src`.

dm(length)

Calculates the value of the "Demarker" indicator.

Parameters:

length (simple int) : (simple int) Number of bars (length).

Returns: (float) The oscillator value.

donchian(length)

Calculates the values of a Donchian Channel using `high` and `low` over a given `length`.

Parameters:

length (int) : (series int) Number of bars (length).

Returns: ( [float, float, float ]) A tuple containing the channel high, low, and median, respectively.

ema2(src, length)

An alternate ema function to the `ta.ema()` built-in, which allows a "series float" length argument.

Parameters:

src : (series int/float) Series of values to process.

length : (series int/float) Number of bars (length).

Returns: (float) The exponentially weighted moving average of the `src`.

eom(length, div)

Calculates the value of the Ease of Movement indicator.

Parameters:

length (simple int) : (simple int) Number of bars (length).

div (simple int) : (simple int) Divisor used for normalzing values. Optional. The default is 10000.

Returns: (float) The oscillator value.

frama(source, length)

The Fractal Adaptive Moving Average (FRAMA), developed by John Ehlers, is an adaptive moving average that dynamically adjusts its lookback period based on fractal geometry.

Parameters:

source (float) : (series int/float) Series of values to process.

length (int) : (series int) Number of bars (length).

Returns: (float) The fractal adaptive moving average of the `source`.

ft(source, length)

Calculates the value of the Fisher Transform indicator.

Parameters:

source (float) : (series int/float) Series of values to process.

length (simple int) : (simple int) Number of bars (length).

Returns: (float) The oscillator value.

ht(source)

Calculates the value of the Hilbert Transform indicator.

Parameters:

source (float) : (series int/float) Series of values to process.

Returns: (float) The oscillator value.

ichimoku(conLength, baseLength, senkouLength)

Calculates values of the Ichimoku Cloud indicator, including tenkan, kijun, senkouSpan1, senkouSpan2, and chikou. NOTE: offsets forward or backward can be done using the `offset` argument in `plot()`.

Parameters:

conLength (int) : (series int) Length for the Conversion Line (Tenkan). The default is 9 periods, which returns the mid-point of the 9 period Donchian Channel.

baseLength (int) : (series int) Length for the Base Line (Kijun-sen). The default is 26 periods, which returns the mid-point of the 26 period Donchian Channel.

senkouLength (int) : (series int) Length for the Senkou Span 2 (Leading Span B). The default is 52 periods, which returns the mid-point of the 52 period Donchian Channel.

Returns: ( [float, float, float, float, float ]) A tuple of the Tenkan, Kijun, Senkou Span 1, Senkou Span 2, and Chikou Span values. NOTE: by default, the senkouSpan1 and senkouSpan2 should be plotted 26 periods in the future, and the Chikou Span plotted 26 days in the past.

ift(source)

Calculates the value of the Inverse Fisher Transform indicator.

Parameters:

source (float) : (series int/float) Series of values to process.

Returns: (float) The oscillator value.

kvo(fastLen, slowLen, trigLen)

Calculates the values of the Klinger Volume Oscillator.

Parameters:

fastLen (simple int) : (simple int) Length for the fast moving average smoothing parameter calculation.

slowLen (simple int) : (simple int) Length for the slow moving average smoothing parameter calculation.

trigLen (simple int) : (simple int) Length for the trigger moving average smoothing parameter calculation.

Returns: ( [float, float ]) A tuple of the KVO value, and the trigger value.

pzo(length)

Calculates the value of the Price Zone Oscillator.

Parameters:

length (simple int) : (simple int) Length for the smoothing parameter calculation.

Returns: (float) The oscillator value.

rms(source, length)

Calculates the Root Mean Square of the `source` over the `length`.

Parameters:

source (float) : (series int/float) Series of values to process.

length (int) : (series int) Number of bars (length).

Returns: (float) The RMS value.

rwi(length)

Calculates the values of the Random Walk Index.

Parameters:

length (simple int) : (simple int) Lookback and ATR smoothing parameter length.

Returns: ( [float, float ]) A tuple of the `rwiHigh` and `rwiLow` values.

stc(source, fast, slow, cycle, d1, d2)

Calculates the value of the Schaff Trend Cycle indicator.

Parameters:

source (float) : (series int/float) Series of values to process.

fast (simple int) : (simple int) Length for the MACD fast smoothing parameter calculation.

slow (simple int) : (simple int) Length for the MACD slow smoothing parameter calculation.

cycle (simple int) : (simple int) Number of bars for the Stochastic values (length).

d1 (simple int) : (simple int) Length for the initial %D smoothing parameter calculation.

d2 (simple int) : (simple int) Length for the final %D smoothing parameter calculation.

Returns: (float) The oscillator value.

stochFull(periodK, smoothK, periodD)

Calculates the %K and %D values of the Full Stochastic indicator.

Parameters:

periodK (simple int) : (simple int) Number of bars for Stochastic calculation. (length).

smoothK (simple int) : (simple int) Number of bars for smoothing of the %K value (length).

periodD (simple int) : (simple int) Number of bars for smoothing of the %D value (length).

Returns: ( [float, float ]) A tuple of the slow %K and the %D moving average values.

stochRsi(lengthRsi, periodK, smoothK, periodD, source)

Calculates the %K and %D values of the Stochastic RSI indicator.

Parameters:

lengthRsi (simple int) : (simple int) Length for the RSI smoothing parameter calculation.

periodK (simple int) : (simple int) Number of bars for Stochastic calculation. (length).