EMA EnvelopeThis is an attempt to convert gunbot's SG strategy into a proper TradingView strategy. The problem is that SG Sell Level relies on % above purchase price, which we don't actually know in TradingView. So we could try to get the average of the next bar or something, which maybe this is what the Slippage setting is? I'm not sure.

Anyways, using % above EMA does actually work as a strategy a bit. It's nothing like Turtle Rules by tmr0 though!

Will keep working on this gradually; feedback greatly appreciated!

"TradingView+手机版" için komut dosyalarını ara

CMC Macro Regime PanelOverview (what it is):

A macro‑regime gate built entirely from TradingView-native symbols (CRYPTOCAP, FRED, DXY/VIX, HYG/LQD). It aggregates central‑bank liquidity (Fed balance sheet − RRP − Treasury General Account), USD strength, credit conditions, stablecoin flows/dominance, tech beta and BTC–NDX co‑move into one normalized score (CLRC). The panel outputs Risk‑ON/OFF regimes, an Early 3/5 pre‑signal, and an automatic BTC vs ETH vs ALTs preference. It is intentionally scoped to Daily & Weekly reads (no intraday timing). Publish with a clean chart and a clear description as per TradingView rules.

TradingView

Why we also use other TradingView screens (and why that is compliant)

This script pulls data via request.security() from official TV symbols only; users often want to open the raw series on separate charts to sanity‑check:

CRYPTOCAP indices: TOTAL, TOTAL2, TOTAL3 (market cap aggregates) and dominance tickers like BTC.D, USDT.D. Helpful for regime & rotation (ALTs vs BTC). TradingView provides definitions for crypto market cap and dominance symbols.

TradingView

+3

TradingView

+3

TradingView

+3

FRED releases: WALCL (Fed assets, weekly), RRPONTSYD (ON RRP, daily), WTREGEN (TGA, weekly), M2SL (M2, monthly). These are the official macro sources exposed on TV.

FRED

+3

FRED

+3

FRED

+3

Risk proxies: TVC:DXY (USD index), TVC:VIX (implied vol), AMEX:HYG/AMEX:LQD (credit), NASDAQ:NDX (tech beta), BINANCE:ETHBTC. VIX/NDX relationship is well-documented; VIX measures 30‑day expected S&P500 vol.

TradingView

+2

TradingView

+2

Compliance note: Using multiple screens is optional for users, but it explains/justifies how components work together (a requirement for public scripts). Keep publication chart clean; use extra screens only to illustrate in the description.

TradingView

How it works (high level)

Liquidity block (Weekly/Monthly)

Net Liquidity = WALCL − RRPONTSYD − WTREGEN (YoY z‑score). WALCL is weekly (as of Wednesday) via H.4.1; RRP is daily; TGA is a Fed liability series. M2 YoY is monthly.

FRED

+3

FRED

+3

FRED

+3

Risk conditions (Daily)

DXY 3‑month momentum (inverted), VIX level (inverted), Credit (HYG/LQD ratio or HY OAS). VIX is a 30‑day constant‑maturity implied vol index per Cboe methodology.

Cboe

+1

Crypto‑internal (Daily)

Stablecoins (USDT+USDC+DAI 30‑day log change), USDT dominance (20‑day, inverted), TOTAL3 (63‑day momentum). Dominance symbols on TV follow a documented formula.

TradingView

Beta & co‑move (Daily)

NDX 63‑day momentum, BTC↔NDX 90‑day correlation.

All components become z‑scores (optionally clipped), weighted, missing inputs drop and weights renormalize. We never use lookahead; we confirm on bar close to avoid repainting per Pine docs (barstate.isconfirmed, multi‑TF).

TradingView

+2

TradingView

+2

What you see on the chart

White line (CLRC) = macro regime score.

Background: Green = Risk‑ON, Red = Risk‑OFF, Teal = Early 3/5 (pre‑signal).

Table: shows each component’s z‑score and the Preference: BTC / ETH / ALTs / Mixed.

Signals & interpretation

Designed for Daily (1D) and Weekly (1W) only.

Regime gates (default Fast preset):

Enter ON: CLRC ≥ +0.8; Hold ON while ≥ +0.5.

Enter OFF: CLRC ≤ −1.0; Hold OFF while ≤ −0.5.

0 / ±1 reading: CLRC is a standardized composite.

~0 = neutral baseline (no macro edge).

≥ +1 = strong macro tailwind (≈ +1σ).

≤ −1 = strong headwind (≈ −1σ).

Early 3/5 (teal): a fast pre‑signal when at least 3 of 5 daily checks align: USDT.D↓, DXY↓, VIX↓, HYG/LQD↑, ETHBTC↑ or TOTAL3↑. It often precedes a full ON flip—use for pre‑positioning rather than full sizing.

BTC/ETH/ALTs selector (only when ON):

ALTs when BTC.D↓ and (ETHBTC↑ or TOTAL3↑) ⇒ rotate down the risk curve.

BTC when BTC.D↑ and ETHBTC↓ ⇒ keep it concentrated.

ETH when ETHBTC↑ while BTC.D flat/up ⇒ add ETH beta.

(Dominance mechanics are documented by TV.)

TradingView

Dissonance (incompatibility) rules — when to stand down

Use these overrides to avoid false comfort:

CLRC > +1 but USDT.D↑ and/or VIX spikes day‑over‑day → downgrade to Neutral; wait for USDT.D to stabilize and VIX to cool (VIX is a fear gauge of 30‑day expectation).

Cboe Global Markets

CLRC > +1 but DXY↑ sharply (USD squeeze) → size below normal; require DXY momentum to roll over.

CLRC < −1 but Early 3/5 = true two days in a row → start reducing underweights; look for ON flip within a few bars.

NetLiq improving (W) but credit (HYG/LQD) deteriorating (D) → treat as mixed regime; prefer BTC over ALTs.

How to use (step‑by‑step)

A. Read on Daily (1D) — main regime

Open CRYPTOCAP:TOTAL3, 1D (panel applied).

Wait for bar close (use alerts on confirmed bar). Pine docs recommend barstate.isconfirmed to avoid repainting on realtime bars.

TradingView

If ON, check Preference (BTC / ETH / ALTs).

Then drop to 4H on your trading pair for micro entries (this indicator itself is not for intraday timing).

B. Confirm weekly macro (1W) — once per week)

Review WALCL/RRP/TGA after the H.4.1 release on Thursdays ~4:30 pm ET. WALCL is “Weekly, as of Wednesday”; M2 is Monthly—so do not expect daily responsiveness from these.

Federal Reserve

+2

FRED

+2

Recommended check times (practical schedule)

Daily regime read: right after your chart’s daily close (confirmed bar). For consistent timing across crypto, many users set chart timezone to UTC and read ~00:05 UTC; you can change chart timezone in TV’s settings.

TradingView

In‑day monitoring: optional spot checks 16:00 & 20:00 UTC (DXY/VIX move during US hours), but act only after the daily bar confirms.

Weekly macro pass: Thu 21:30–22:30 UTC (after H.4.1 4:30 pm ET) or Fri after daily close, to let weekly FRED series propagate.

Federal Reserve

Limitations & data latency (be explicit)

Higher‑TF data & confirmation: FRED weekly/monthly series will not reflect intraday risk in crypto; we aggregate them for regime, not for entry timing.

Repainting 101: Realtime bars move until close. This script does not use lookahead and follows Pine guidance on multi‑TF series; still, always act on confirmed bars.

TradingView

+1

Public‑library compliance: Title EN‑only; description starts in EN; clean chart; justify component mash‑up; no lookahead; no unrealistic claims.

TradingView

Alerts you can use

“Macro Risk‑ON (entry)” — fires on ON flip (confirmed bar).

“Macro Risk‑OFF (entry)” — fires on OFF flip.

“Early 3/5” — fires when the teal pre‑signal appears (not a regime flip).

“Preference change” — BTC/ETH/ALTs toggles while ON.

Publish note: Alerts are fine; just avoid implying guaranteed accuracy/performance.

TradingView

Background research (why these inputs matter)

Liquidity → Crypto: Fed H.4.1 timing and series definitions (WALCL, RRP, TGA) formalize the “net liquidity” concept used here.

FRED

+3

Federal Reserve

+3

FRED

+3

Stablecoins ↔ Non‑stable crypto: empirical work shows bi‑directional causality between stablecoin market cap and non‑stable crypto cap; stablecoin growth co‑moves with broader crypto activity.

Global liquidity link: world liquidity positively relates to total crypto market cap; lagged effects are observed at monthly horizons.

VIX/Uncertainty effect: fear shocks impair BTC’s “safe haven” behavior; VIX is a meaningful risk‑off read.

Advanced RSI — Mark 4 RSI was introduced by J. Welles Wilder Jr. in 1978 in New Concepts in Technical Trading Systems. It measures the velocity of gains vs. losses on a bounded 0–100 scale and popularized the 14-period lookback with 70/30 guide rails for overbought/oversold. Over time, traders added variations (different lengths, thresholds, smoothing, adaptive levels), but the core idea stayed the same: momentum turns often precede price turns.

and i initially started to make minor adjustments for personal use like changing the default to 17 , and using Tradingviews official RSI which comes with a MA embedded. but it was not enough. especially the visuals.

so, for this public release Mark 4 i enhanced RSI by incorporating :

1. Dual-Length Fusion

Two RSI periods (default 17 + 21) blended then lightly smoothed (TEMA by default) → steadier

line without dulling turns.

2. Adaptive OB/OS (ATR-aware) for fewer whipsaws.

3. OB/OS alt solution:

Brief yellow segments appear only at local extremes (default: >72 tops, <32 bottoms) to

emphasize exhaustion without repainting the whole line.

4. Signals you can actually see

Triangle markers for:

Bullish: RSI crossing up through adaptive OS (and still <40 at the cross).

Bearish: RSI crossing down through adaptive OB (and still >60 at the cross).

“Strong Bull/Bear” background nudges appear when momentum is pushing beyond the

bands.

Optional Divergence Tags

and

Tiny diamonds to flag potential bullish/bearish divergences (look-back based).

Info Table (can be hidden)

my Fav feature i included 5 colorways with modern themes.(pls check under INPUTS)

and i made all that to make the indicator visualization look awesome on high end displays.

Credits & acknowledgment

Inspired by the original RSI by J. Welles Wilder Jr. (1978).

Built to be modern, focused, and comfortable for long sessions—especially on dark/OLED displays.

THIS INDICATOR IS MORE THAN ENOUGH BUT I DO HAVE PRIVATE INDICATORS WITH DIFFERENT LOGIC FUNCTIONS.

I'm open for feedback/collaboration.

drsamc.

Volume Spike DetectorDetects a spike in Volume . based on volume on tradingviews. It highlights when volume is 1.5X of usual average

OB/OS adaptative v1.1# OB/OS Adaptative v1.1 - Multi-Timeframe Adaptive Overbought/Oversold Indicator

## Overview

The `tradingview_indicator_emas.pine` script is a sophisticated multi-timeframe indicator designed to identify dynamic overbought and oversold levels in financial markets. It combines EMA (Exponential Moving Average) crossovers and Bollinger Bands across monthly, weekly, and daily timeframes to create adaptive support and resistance levels that adjust to changing market conditions.

## Core Functionality

### Multi-Timeframe Analysis

The indicator analyzes three timeframes simultaneously:

- **Monthly (M)**: Long-term trend identification

- **Weekly (W)**: Intermediate-term trend identification

- **Daily (D)**: Short-term volatility measurement

### Technical Indicators Used

- **EMA 9 and EMA 20**: For trend identification and momentum assessment

- **Bollinger Bands (20-period)**: For volatility measurement and extreme level identification

- **Price action**: For confirmation of level validity and signal generation

## Key Features

### Adaptive Level Calculation

The indicator dynamically determines overbought and oversold levels based on market structure and trend bias:

#### Monthly Level Logic

- **Bullish Bias** (when monthly open > EMA20):

- Oversold = lower of EMA9 or EMA20

- Overbought = upper of EMA9 or Bollinger Upper Band

- **Bearish/Neutral Bias** (when monthly open ≤ EMA20):

- Oversold = Bollinger Lower Band

- Overbought = upper of EMA20 or EMA9

#### Weekly Level Logic

- **Bullish Bias** (when weekly open > EMA20):

- Oversold = lower of EMA9 or EMA20

- Overbought = Bollinger Upper Band

- **Bearish/Neutral Bias** (when weekly open ≤ EMA20):

- Oversold = Bollinger Lower Band

- Overbought = upper of EMA20 or EMA9

#### Daily Level Logic

- Simple Bollinger Bands:

- Oversold = Bollinger Lower Band

- Overbought = Bollinger Upper Band

### Final Level Determination

The indicator combines all three timeframes through a weighted averaging process:

1. Calculates initial values as the average of monthly, weekly, and daily levels

2. Ensures mathematical consistency by enforcing overbought_final ≥ oversold_final using min/max functions

3. Calculates a midpoint average level as the center of the range

### Visual Elements

- **Dynamic Lines**: Draws horizontal lines for current and previous period overbought, oversold, and average levels

- **Labels**: Places clear textual labels at the start of each period

- **Color Coding**:

- Red for overbought levels (resistance)

- Green for oversold levels (support)

- Blue for average levels (pivot point)

- **Transparency**: Previous period lines use semi-transparent colors to distinguish between current and historical levels

### Update Mechanism

- **Calculation Day**: User-defined day of the week (default: Monday)

- On the specified calculation day, the indicator:

- Updates all levels based on previous bar's data

- Draws new lines extending forward for a user-defined number of days

- Maintains previous period lines for comparison and trend analysis

- Automatically deletes and recreates lines to ensure clean visualization

### Proximity Detection

- Alerts when price approaches overbought/oversold levels (configurable distance in percentage)

- Helps identify potential reversal zones before actual crossovers occur

- Distance thresholds are user-configurable for both overbought and oversold conditions

### Alert Conditions

The indicator provides four distinct alert types:

1. **Cross below oversold**: Triggered when price crosses below the oversold level

2. **Cross above overbought**: Triggered when price crosses above the overbought level

3. **Near oversold**: Triggered when price approaches the oversold level within the configured distance

4. **Near overbought**: Triggered when price approaches the overbought level within the configured distance

### Debug Mode

When enabled, displays comprehensive debug information including:

- Current values for all levels (oversold, overbought, average)

- Timeframe-specific calculations and raw data points

- System status information (current day, calculation day, etc.)

- Lines existence and timing information

- Organized in multiple labels at different price levels to avoid overlap

## Configuration Parameters

| Parameter | Default Value | Description |

|---------|---------------|-------------|

| Short EMA (9) | 9 | Length for short-term EMA calculation |

| Long EMA (20) | 20 | Length for long-term EMA calculation |

| BB Length | 20 | Period for Bollinger Bands calculation |

| Std Dev | 2.0 | Standard deviation multiplier for Bollinger Bands |

| Distance to overbought (%) | 0.5 | Percentage threshold for "near overbought" alerts |

| Distance to oversold (%) | 0.5 | Percentage threshold for "near oversold" alerts |

| Calculation day | Monday | Day of week when levels are recalculated |

| Lookback days | 7 | Number of days to extend previous period lines backward |

| Forward days | 7 | Number of days to extend current period lines forward |

| Show Debug Labels | false | Toggle for comprehensive debug information display |

## Trading Applications

### Primary Use Cases

1. **Reversal Trading**: Identify potential reversal zones when price approaches overbought/oversold levels

2. **Trend Confirmation**: Use the adaptive nature of levels to confirm trend strength and direction

3. **Position Sizing**: Adjust position size based on distance from key levels

4. **Stop Placement**: Use opposite levels as dynamic stop-loss references

### Strategic Advantages

- **Adaptive Nature**: Levels adjust to changing market volatility and trend structure

- **Multi-Timeframe Confirmation**: Signals are validated across multiple timeframes

- **Visual Clarity**: Clear color-coded lines and labels enhance decision-making

- **Proactive Alerts**: "Near" conditions provide early warnings before crossovers

## Implementation Details

### Data Security

Uses `request.security()` function to fetch data from higher timeframes (monthly, weekly) while maintaining proper bar indexing with ` ` offset for open prices.

### Performance Optimization

- Uses `var` keyword to declare persistent variables that maintain state across bars

- Efficient line and label management with proper deletion before recreation

- Conditional execution of debug code to minimize performance impact

### Error Handling

- Comprehensive NA (not available) checks throughout the code

- Graceful degradation when data is unavailable for higher timeframes

- Mathematical safeguards to prevent invalid level calculations

## Conclusion

The OB/OS Adaptative v1.1 indicator represents a sophisticated approach to identifying market extremes by combining multiple technical analysis concepts. Its adaptive nature makes it particularly useful in trending markets where static levels may be less effective. The multi-timeframe approach provides a comprehensive view of market structure, while the visual elements and alert system enhance its practical utility for active traders.

Project SynthIntroducing Project Synth !

Inspired by Pace of Tape and Cumulative Delta I created Project Synth in order to aggregate volume flow data across multiple marketsfor two primary reasions:

Traditional orderflow tools are not available on Tradingview. My script attempts to bring an original; calculus-based approach to creating not only an alternative for traditional orderflow tools, but also a more accurate one.

In order to detect genuine buying and selling pressure that cannot be easily manipulated. I did this because while I've always enjoyed concept behind both of those tools, I did not think they captured enough data to be useful. By analyzing assets that move together (positive correlation) and assets that move inversely (negative correlation), my system aims to fix the fundamental problems with those indicators and create an objective view of market sentiment based on aggregate orderflow.

Some more detailed explanations (using QQQ and SQQQ as an example):

Inverse Market Dynamics (QQQ vs SQQQ):

In an inverse market like SQQQ, aggressive buyers hit the ask when they expect the underlying (QQQ) to fall, while passive buyers wait on the bid hoping for cheaper inverse exposure. When QQQ rallies, SQQQ sees aggressive selling (people dumping their bearish bets) hitting bids, while passive sellers sit on the ask hoping to exit at better prices. The aggression flows opposite to the underlying market direction.

Why Utilizing Both Markets Provides A More Accurate Delta:

Watching both QQQ and SQQQ gives cross-validation - real buying pressure in QQQ should coincide with selling pressure in SQQQ. If you see buying in QQQ but also buying in SQQQ, that's a conflicting signal suggesting the move might be artificial or driven by other factors. The inverse relationship acts as a confirmation filter, making false signals much harder to generate.

Multiple Markets = Authentic Pressure:

The more unique, important markets you track, the harder it becomes to create fake delta moves. Real institutional buying/selling pressure affects multiple correlated assets simultaneously in predictable patterns - you can't easily manipulate tech stocks, treasury bonds, VIX, and currency pairs all at once to create a false signal. Each additional market acts as a fraud detection layer, ensuring the delta measurement reflects genuine ecosystem-wide buying and selling pressure rather than isolated manipulation or noise.

My Suggestions For Usage:

In order to keep the explanation simple and short for now, I suggest using it just like a cumulative delta indicator. For example: let's say you were watching CME_MINI:ES1! , and you had a resistance level at 6000. When the price reaches your resistance level, you would be looking for a significant divergence between price and Delta. Price : rising, Delta : falling. This means that even though the price was going up, strong and aggressive sellers are jumping in more and more, this can be used as a confirmation tool for a resistance level.

Notes For Moderators, Authors and Users:

Firstly, to the best of my knowledge, I have not been able to find many tools built around the concept of cumulative delta or pace of tape. While I know there are a couple projects, none to the magnitude of synthetically recreating these tools via an algorithm designed around basic calculus principles. While tools like Volume Delta are built in, they do not attempt to capture an accurate picture of aggregated orderflow from what I understand.

Secondly, it needs to be noted that tool aims to create an approximation of buying and selling pressure. To my knowledge it is not possible to create an accurate full picture, at least not within the limitations of Tradingview.

Buffett Indicator with Historical Bubbles (Clean)The Buffett Indicator is a trusted macroeconomic gauge that compares the total US stock market capitalization to the nation’s GDP. Popularized by Warren Buffett, this metric highlights periods of overvaluation and undervaluation in the market.

This tool offers a clean and accurate visualization of the Buffett Indicator, enhanced with historical bubble annotations for key market events:

Dot-com Bubble (2000)

Global Financial Crisis Peak (2007)

COVID-19 Pre-crash Peak (2020)

Post-COVID Bull Market Peak (2021)

Features:

Dynamic Buffett Ratio (%) calculation using Wilshire 5000 Index as the market cap proxy.

Customizable GDP input for accuracy (update quarterly).

Visual thresholds for fair value, undervaluation, and overvaluation zones.

Historical event markers for educational and analytical context.

Optimized to display clearly across all timeframes: Daily, Weekly, Monthly.

How to Use:

Manually update the GDP input as new data is released.

Use this indicator for macro-level market sentiment analysis and valuation tracking.

Combine with other tools and risk management strategies for comprehensive market insights.

Disclaimer:

This indicator is for educational purposes only. It does not constitute financial advice. Always perform your own research and analysis.

Version: 1.0

we ask Allah reconcile and repay

#BuffettIndicator #MarketValuation #MacroAnalysis #BubbleDetector #LongTermInvestor #USMarket #Wilshire5000 #TradingViewScript

Smart Liquidity Wave [The_lurker]"Smart Liquidity Wave" هو مؤشر تحليلي متطور يهدف لتحديد نقاط الدخول والخروج المثلى بناءً على تحليل السيولة، قوة الاتجاه، وإشارات السوق المفلترة. يتميز المؤشر بقدرته على تصنيف الأدوات المالية إلى أربع فئات سيولة (ضعيفة، متوسطة، عالية، عالية جدًا)، مع تطبيق شروط مخصصة لكل فئة تعتمد على تحليل الموجات السعرية، الفلاتر المتعددة، ومؤشر ADX.

فكرة المؤشر

الفكرة الأساسية هي الجمع بين قياس السيولة اليومية الثابتة وتحليل ديناميكي للسعر باستخدام فلاتر متقدمة لتوليد إشارات دقيقة. المؤشر يركز على تصفية الضوضاء في السوق من خلال طبقات متعددة من التحليل، مما يجعله أداة ذكية تتكيف مع الأدوات المالية المختلفة بناءً على مستوى سيولتها.

طريقة عمل المؤشر

1- قياس السيولة:

يتم حساب السيولة باستخدام متوسط حجم التداول على مدى 14 يومًا مضروبًا في سعر الإغلاق، ويتم ذلك دائمًا على الإطار الزمني اليومي لضمان ثبات القيمة بغض النظر عن الإطار الزمني المستخدم في الرسم البياني.

يتم تصنيف السيولة إلى:

ضعيفة: أقل من 5 ملايين (قابل للتعديل).

متوسطة: من 5 إلى 20 مليون.

عالية: من 20 إلى 50 مليون.

عالية جدًا: أكثر من 50 مليون.

هذا الثبات في القياس يضمن أن تصنيف السيولة لا يتغير مع تغير الإطار الزمني، مما يوفر أساسًا موثوقًا للإشارات.

2- تحليل الموجات السعرية:

يعتمد المؤشر على تحليل الموجات باستخدام متوسطات متحركة متعددة الأنواع (مثل SMA، EMA، WMA، HMA، وغيرها) يمكن للمستخدم اختيارها وتخصيص فتراتها ، يتم دمج هذا التحليل مع مؤشرات إضافية مثل RSI (مؤشر القوة النسبية) وMFI (مؤشر تدفق الأموال) بوزن محدد (40% للموجات، 30% لكل من RSI وMFI) للحصول على تقييم شامل للاتجاه.

3- الفلاتر وطريقة عملها:

المؤشر يستخدم نظام فلاتر متعدد الطبقات لتصفية الإشارات وتقليل الضوضاء، وهي من أبرز الجوانب المخفية التي تعزز دقته:

الفلتر الرئيسي (Main Filter):

يعمل على تنعيم التغيرات السعرية السريعة باستخدام معادلة رياضية تعتمد على تحليل الإشارات (Signal Processing).

يتم تطبيقه على السعر لاستخراج الاتجاهات الأساسية بعيدًا عن التقلبات العشوائية، مع فترة زمنية قابلة للتعديل (افتراضي: 30).

يستخدم تقنية مشابهة للفلاتر عالية التردد (High-Pass Filter) للتركيز على الحركات الكبيرة.

الفلتر الفرعي (Sub Filter):

يعمل كطبقة ثانية للتصفية، مع فترة أقصر (افتراضي: 12)، لضبط الإشارات بدقة أكبر.

يستخدم معادلات تعتمد على الترددات المنخفضة للتأكد من أن الإشارات الناتجة تعكس تغيرات حقيقية وليست مجرد ضوضاء.

إشارة الزناد (Signal Trigger):

يتم تطبيق متوسط متحرك على نتائج الفلتر الرئيسي لتوليد خط إشارة (Signal Line) يُقارن مع عتبات محددة للدخول والخروج.

يمكن تعديل فترة الزناد (افتراضي: 3 للدخول، 5 للخروج) لتسريع أو تبطيء الإشارات.

الفلتر المربع (Square Filter):

خاصية مخفية تُفعّل افتراضيًا تعزز دقة الفلاتر عن طريق تضييق نطاق التذبذبات المسموح بها، مما يقلل من الإشارات العشوائية في الأسواق المتقلبة.

4- تصفية الإشارات باستخدام ADX:

يتم استخدام مؤشر ADX كفلتر نهائي للتأكد من قوة الاتجاه قبل إصدار الإشارة:

ضعيفة ومتوسطة: دخول عندما يكون ADX فوق 40، خروج فوق 50.

عالية: دخول فوق 40، خروج فوق 55.

عالية جدًا: دخول فوق 35، خروج فوق 38.

هذه العتبات قابلة للتعديل، مما يسمح بتكييف المؤشر مع استراتيجيات مختلفة.

5- توليد الإشارات:

الدخول: يتم إصدار إشارة شراء عندما تنخفض خطوط الإشارة إلى ما دون عتبة محددة (مثل -9) مع تحقق شروط الفلاتر، السيولة، وADX.

الخروج: يتم إصدار إشارة بيع عندما ترتفع الخطوط فوق عتبة (مثل 109 أو 106 حسب الفئة) مع تحقق الشروط الأخرى.

تُعرض الإشارات بألوان مميزة (أزرق للدخول، برتقالي للضعيفة والمتوسطة، أحمر للعالية والعالية جدًا) وبثلاثة أحجام (صغير، متوسط، كبير).

6- عرض النتائج:

يظهر مستوى السيولة الحالي في جدول في أعلى يمين الرسم البياني، مما يتيح للمستخدم معرفة فئة الأصل بسهولة.

7- دعم التنبيهات:

تنبيهات فورية لكل فئة سيولة، مما يسهل التداول الآلي أو اليدوي.

%%%%% الجوانب المخفية في الكود %%%%%

معادلات الفلاتر المتقدمة: يستخدم المؤشر معادلات رياضية معقدة مستوحاة من معالجة الإشارات لتنعيم البيانات واستخراج الاتجاهات، مما يجعله أكثر دقة من المؤشرات التقليدية.

التكيف التلقائي: النظام يضبط نفسه داخليًا بناءً على التغيرات في السعر والحجم، مع عوامل تصحيح مخفية (مثل معامل التنعيم في الفلاتر) للحفاظ على الاستقرار.

التوزيع الموزون: الدمج بين الموجات، RSI، وMFI يتم بأوزان محددة (40%، 30%، 30%) لضمان توازن التحليل، وهي تفاصيل غير ظاهرة مباشرة للمستخدم لكنها تؤثر على النتائج.

الفلتر المربع: خيار مخفي يتم تفعيله افتراضيًا لتضييق نطاق الإشارات، مما يقلل من التشتت في الأسواق ذات التقلبات العالية.

مميزات المؤشر

1- فلاتر متعددة الطبقات: تضمن تصفية الضوضاء وإنتاج إشارات موثوقة فقط.

2- ثبات السيولة: قياس السيولة اليومي يجعل التصنيف متسقًا عبر الإطارات الزمنية.

3- تخصيص شامل: يمكن تعديل حدود السيولة، عتبات ADX، فترات الفلاتر، وأنواع المتوسطات المتحركة.

4- إشارات مرئية واضحة: تصميم بصري يسهل التفسير مع تنبيهات فورية.

5- تقليل الإشارات الخاطئة: الجمع بين الفلاتر وADX يعزز الدقة ويقلل من التشتت.

إخلاء المسؤولية

لا يُقصد بالمعلومات والمنشورات أن تكون، أو تشكل، أي نصيحة مالية أو استثمارية أو تجارية أو أنواع أخرى من النصائح أو التوصيات المقدمة أو المعتمدة من TradingView.

#### **What is the Smart Liquidity Wave Indicator?**

"Smart Liquidity Wave" is an advanced analytical indicator designed to identify optimal entry and exit points based on liquidity analysis, trend strength, and filtered market signals. It stands out with its ability to categorize financial instruments into four liquidity levels (Weak, Medium, High, Very High), applying customized conditions for each category based on price wave analysis, multi-layered filters, and the ADX (Average Directional Index).

#### **Concept of the Indicator**

The core idea is to combine a stable daily liquidity measurement with dynamic price analysis using sophisticated filters to generate precise signals. The indicator focuses on eliminating market noise through multiple analytical layers, making it an intelligent tool that adapts to various financial instruments based on their liquidity levels.

#### **How the Indicator Works**

1. **Liquidity Measurement:**

- Liquidity is calculated using the 14-day average trading volume multiplied by the closing price, always based on the daily timeframe to ensure value consistency regardless of the chart’s timeframe.

- Liquidity is classified as:

- **Weak:** Less than 5 million (adjustable).

- **Medium:** 5 to 20 million.

- **High:** 20 to 50 million.

- **Very High:** Over 50 million.

- This consistency in measurement ensures that liquidity classification remains unchanged across different timeframes, providing a reliable foundation for signals.

2. **Price Wave Analysis:**

- The indicator relies on wave analysis using various types of moving averages (e.g., SMA, EMA, WMA, HMA, etc.), which users can select and customize in terms of periods.

- This analysis is integrated with additional indicators like RSI (Relative Strength Index) and MFI (Money Flow Index), weighted specifically (40% waves, 30% RSI, 30% MFI) to provide a comprehensive trend assessment.

3. **Filters and Their Functionality:**

- The indicator employs a multi-layered filtering system to refine signals and reduce noise, a key hidden feature that enhances its accuracy:

- **Main Filter:**

- Smooths rapid price fluctuations using a mathematical equation rooted in signal processing techniques.

- Applied to price data to extract core trends away from random volatility, with an adjustable period (default: 30).

- Utilizes a technique similar to high-pass filters to focus on significant movements.

- **Sub Filter:**

- Acts as a secondary filtering layer with a shorter period (default: 12) for finer signal tuning.

- Employs low-frequency-based equations to ensure resulting signals reflect genuine changes rather than mere noise.

- **Signal Trigger:**

- Applies a moving average to the main filter’s output to generate a signal line, compared against predefined entry and exit thresholds.

- Trigger period is adjustable (default: 3 for entry, 5 for exit) to speed up or slow down signals.

- **Square Filter:**

- A hidden feature activated by default, enhancing filter precision by narrowing the range of permissible oscillations, reducing random signals in volatile markets.

4. **Signal Filtering with ADX:**

- ADX is used as a final filter to confirm trend strength before issuing signals:

- **Weak and Medium:** Entry when ADX exceeds 40, exit above 50.

- **High:** Entry above 40, exit above 55.

- **Very High:** Entry above 35, exit above 38.

- These thresholds are adjustable, allowing the indicator to adapt to different trading strategies.

5. **Signal Generation:**

- **Entry:** A buy signal is triggered when signal lines drop below a specific threshold (e.g., -9) and conditions for filters, liquidity, and ADX are met.

- **Exit:** A sell signal is issued when signal lines rise above a threshold (e.g., 109 or 106, depending on the category) with all conditions satisfied.

- Signals are displayed in distinct colors (blue for entry, orange for Weak/Medium, red for High/Very High) and three sizes (small, medium, large).

6. **Result Display:**

- The current liquidity level is shown in a table at the top-right of the chart, enabling users to easily identify the asset’s category.

7. **Alert Support:**

- Instant alerts are provided for each liquidity category, facilitating both automated and manual trading.

#### **Hidden Aspects in the Code**

- **Advanced Filter Equations:** The indicator uses complex mathematical formulas inspired by signal processing to smooth data and extract trends, making it more precise than traditional indicators.

- **Automatic Adaptation:** The system internally adjusts based on price and volume changes, with hidden correction factors (e.g., smoothing coefficients in filters) to maintain stability.

- **Weighted Distribution:** The integration of waves, RSI, and MFI uses fixed weights (40%, 30%, 30%) for balanced analysis, a detail not directly visible but impactful on results.

- **Square Filter:** A hidden option, enabled by default, narrows signal range to minimize dispersion in high-volatility markets.

#### **Indicator Features**

1. **Multi-Layered Filters:** Ensures noise reduction and delivers only reliable signals.

2. **Liquidity Stability:** Daily liquidity measurement keeps classification consistent across timeframes.

3. **Comprehensive Customization:** Allows adjustments to liquidity thresholds, ADX levels, filter periods, and moving average types.

4. **Clear Visual Signals:** User-friendly design with easy-to-read visuals and instant alerts.

5. **Reduced False Signals:** Combining filters and ADX enhances accuracy and minimizes clutter.

#### **Disclaimer**

The information and publications are not intended to be, nor do they constitute, financial, investment, trading, or other types of advice or recommendations provided or endorsed by TradingView.

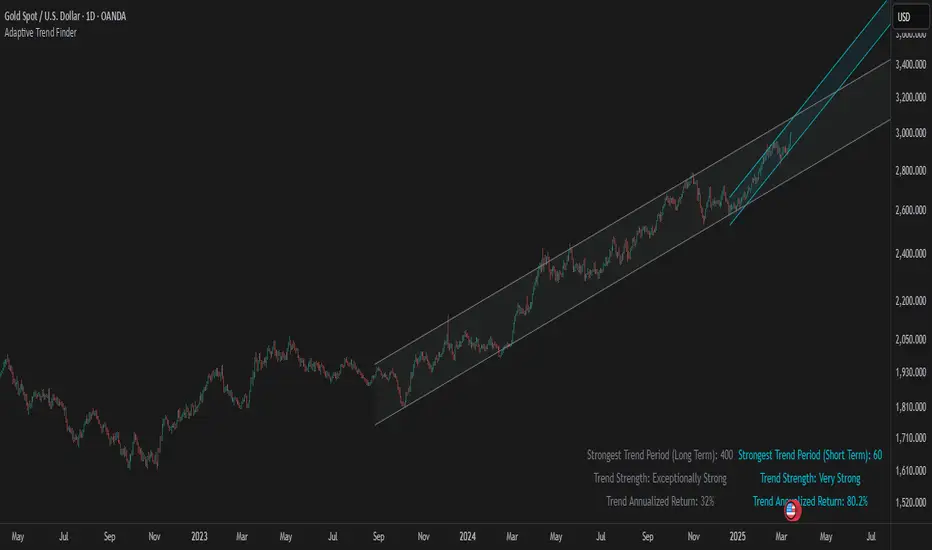

Adaptive Trend FinderAdaptive Trend Finder - The Ultimate Trend Detection Tool

Introducing Adaptive Trend Finder, the next evolution of trend analysis on TradingView. This powerful indicator is an enhanced and refined version of Adaptive Trend Finder (Log), designed to offer even greater flexibility, accuracy, and ease of use.

What’s New?

Unlike the previous version, Adaptive Trend Finder allows users to fully configure and adjust settings directly within the indicator menu, eliminating the need to modify chart settings manually. A major improvement is that users no longer need to adjust the chart's logarithmic scale manually in the chart settings; this can now be done directly within the indicator options, ensuring a smoother and more efficient experience. This makes it easier to switch between linear and logarithmic scaling without disrupting the analysis. This provides a seamless user experience where traders can instantly adapt the indicator to their needs without extra steps.

One of the most significant improvements is the complete code overhaul, which now enables simultaneous visualization of both long-term and short-term trend channels without needing to add the indicator twice. This not only improves workflow efficiency but also enhances chart readability by allowing traders to monitor multiple trend perspectives at once.

The interface has been entirely redesigned for a more intuitive user experience. Menus are now clearer, better structured, and offer more customization options, making it easier than ever to fine-tune the indicator to fit any trading strategy.

Key Features & Benefits

Automatic Trend Period Selection: The indicator dynamically identifies and applies the strongest trend period, ensuring optimal trend detection with no manual adjustments required. By analyzing historical price correlations, it selects the most statistically relevant trend duration automatically.

Dual Channel Display: Traders can view both long-term and short-term trend channels simultaneously, offering a broader perspective of market movements. This feature eliminates the need to apply the indicator twice, reducing screen clutter and improving efficiency.

Fully Adjustable Settings: Users can customize trend detection parameters directly within the indicator settings. No more switching chart settings – everything is accessible in one place.

Trend Strength & Confidence Metrics: The indicator calculates and displays a confidence score for each detected trend using Pearson correlation values. This helps traders gauge the reliability of a given trend before making decisions.

Midline & Channel Transparency Options: Users can fine-tune the visibility of trend channels, adjusting transparency levels to fit their personal charting style without overwhelming the price chart.

Annualized Return Calculation: For daily and weekly timeframes, the indicator provides an estimate of the trend’s performance over a year, helping traders evaluate potential long-term profitability.

Logarithmic Adjustment Support: Adaptive Trend Finder is compatible with both logarithmic and linear charts. Traders who analyze assets like cryptocurrencies, where log scaling is common, can enable this feature to refine trend calculations.

Intuitive & User-Friendly Interface: The updated menu structure is designed for ease of use, allowing quick and efficient modifications to settings, reducing the learning curve for new users.

Why is this the Best Trend Indicator?

Adaptive Trend Finder stands out as one of the most advanced trend analysis tools available on TradingView. Unlike conventional trend indicators, which rely on fixed parameters or lagging signals, Adaptive Trend Finder dynamically adjusts its settings based on real-time market conditions. By combining automatic trend detection, dual-channel visualization, real-time performance metrics, and an intuitive user interface, this indicator offers an unparalleled edge in trend identification and trading decision-making.

Traders no longer have to rely on guesswork or manually tweak settings to identify trends. Adaptive Trend Finder does the heavy lifting, ensuring that users are always working with the strongest and most reliable trends. The ability to simultaneously display both short-term and long-term trends allows for a more comprehensive market overview, making it ideal for scalpers, swing traders, and long-term investors alike.

With its state-of-the-art algorithms, fully customizable interface, and professional-grade accuracy, Adaptive Trend Finder is undoubtedly one of the most powerful trend indicators available.

Try it today and experience the future of trend analysis.

This indicator is a technical analysis tool designed to assist traders in identifying trends. It does not guarantee future performance or profitability. Users should conduct their own research and apply proper risk management before making trading decisions.

// Created by Julien Eche - @Julien_Eche

Casa_UtilsLibrary "Casa_Utils"

A collection of convenience and helper functions for indicator and library authors on TradingView

formatNumber(num)

My version of format number that doesn't have so many decimal places...

Parameters:

num (float) : The number to be formatted

Returns: The formatted number

getDateString(timestamp)

Convenience function returns timestamp in yyyy/MM/dd format.

Parameters:

timestamp (int) : The timestamp to stringify

Returns: The date string

getDateTimeString(timestamp)

Convenience function returns timestamp in yyyy/MM/dd hh:mm format.

Parameters:

timestamp (int) : The timestamp to stringify

Returns: The date string

getInsideBarCount()

Gets the number of inside bars for the current chart. Can also be passed to request.security to get the same for different timeframes.

Returns: The # of inside bars on the chart right now.

getLabelStyleFromString(styleString, acceptGivenIfNoMatch)

Tradingview doesn't give you a nice way to put the label styles into a dropdown for configuration settings. So, I specify them in the following format: "Center", "Left", "Lower Left", "Lower Right", "Right", "Up", "Upper Left", "Upper Right", "Plain Text", "No Labels". This function takes care of converting those custom strings back to the ones expected by tradingview scripts.

Parameters:

styleString (string)

acceptGivenIfNoMatch (bool) : If no match for styleString is found and this is true, the function will return styleString, otherwise it will return tradingview's preferred default

Returns: The string expected by tradingview functions

getTime(hourNumber, minuteNumber)

Given an hour number and minute number, adds them together and returns the sum. To be used by getLevelBetweenTimes when fetching specific price levels during a time window on the day.

Parameters:

hourNumber (int) : The hour number

minuteNumber (int) : The minute number

Returns: The sum of all the minutes

getHighAndLowBetweenTimes(start, end)

Given a start and end time, returns the high or low price during that time window.

Parameters:

start (int) : The timestamp to start with (# of seconds)

end (int) : The timestamp to end with (# of seconds)

Returns: The high or low value

getPremarketHighsAndLows()

Returns an expression that can be used by request.security to fetch the premarket high & low levels in a tuple.

Returns: (tuple)

getAfterHoursHighsAndLows()

Returns an expression that can be used by request.security to fetch the after hours high & low levels in a tuple.

Returns: (tuple)

getOvernightHighsAndLows()

Returns an expression that can be used by request.security to fetch the overnight high & low levels in a tuple.

Returns: (tuple)

getNonRthHighsAndLows()

Returns an expression that can be used by request.security to fetch the high & low levels for premarket, after hours and overnight in a tuple.

Returns: (tuple)

getLineStyleFromString(styleString, acceptGivenIfNoMatch)

Tradingview doesn't give you a nice way to put the line styles into a dropdown for configuration settings. So, I specify them in the following format: "Solid", "Dashed", "Dotted", "None/Hidden". This function takes care of converting those custom strings back to the ones expected by tradingview scripts.

Parameters:

styleString (string) : Plain english (or TV Standard) version of the style string

acceptGivenIfNoMatch (bool) : If no match for styleString is found and this is true, the function will return styleString, otherwise it will return tradingview's preferred default

Returns: The string expected by tradingview functions

getPercentFromPrice(price)

Get the % the current price is away from the given price.

Parameters:

price (float)

Returns: The % the current price is away from the given price.

getPositionFromString(position)

Tradingview doesn't give you a nice way to put the positions into a dropdown for configuration settings. So, I specify them in the following format: "Top Left", "Top Center", "Top Right", "Middle Left", "Middle Center", "Middle Right", "Bottom Left", "Bottom Center", "Bottom Right". This function takes care of converting those custom strings back to the ones expected by tradingview scripts.

Parameters:

position (string) : Plain english position string

Returns: The string expected by tradingview functions

getRsiAvgsExpression(rsiLength)

Call request.security with this as the expression to get the average up/down values that can be used with getRsiPrice (below) to calculate the price level where the supplied RSI level would be reached.

Parameters:

rsiLength (simple int) : The length of the RSI requested.

Returns: A tuple containing the avgUp and avgDown values required by the getRsiPrice function.

getRsiPrice(rsiLevel, rsiLength, avgUp, avgDown)

use the values returned by getRsiAvgsExpression() to calculate the price level when the provided RSI level would be reached.

Parameters:

rsiLevel (float) : The RSI level to find price at.

rsiLength (int) : The length of the RSI to calculate.

avgUp (float) : The average move up of RSI.

avgDown (float) : The average move down of RSI.

Returns: The price level where the provided RSI level would be met.

getSizeFromString(sizeString)

Tradingview doesn't give you a nice way to put the sizes into a dropdown for configuration settings. So, I specify them in the following format: "Auto", "Huge", "Large", "Normal", "Small", "Tiny". This function takes care of converting those custom strings back to the ones expected by tradingview scripts.

Parameters:

sizeString (string) : Plain english size string

Returns: The string expected by tradingview functions

getTimeframeOfChart()

Get the timeframe of the current chart for display

Returns: The string of the current chart timeframe

getTimeNowPlusOffset(candleOffset)

Helper function for drawings that use xloc.bar_time to help you know the time offset if you want to place the end of the drawing out into the future. This determines the time-size of one candle and then returns a time n candleOffsets into the future.

Parameters:

candleOffset (int) : The number of items to find singular/plural for.

Returns: The future time

getVolumeBetweenTimes(start, end)

Given a start and end time, returns the sum of all volume across bars during that time window.

Parameters:

start (int) : The timestamp to start with (# of seconds)

end (int) : The timestamp to end with (# of seconds)

Returns: The volume

isToday()

Returns true if the current bar occurs on today's date.

Returns: True if current bar is today

padLabelString(labelText, labelStyle)

Pads a label string so that it appears properly in or not in a label. When label.style_none is used, this will make sure it is left-aligned instead of center-aligned. When any other type is used, it adds a single space to the right so there is padding against the right end of the label.

Parameters:

labelText (string) : The string to be padded

labelStyle (string) : The style of the label being padded for.

Returns: The padded string

plural(num, singular, plural)

Helps format a string for plural/singular. By default, if you only provide num, it will just return "s" for plural and nothing for singular (eg. plural(numberOfCats)). But you can optionally specify the full singular/plural words for more complicated nomenclature (eg. plural(numberOfBenches, 'bench', 'benches'))

Parameters:

num (int) : The number of items to find singular/plural for.

singular (string) : The string to return if num is singular. Defaults to an empty string.

plural (string) : The string to return if num is plural. Defaults to 's' so you can just add 's' to the end of a word.

Returns: The singular or plural provided strings depending on the num provided.

timeframeInSeconds(timeframe)

Get the # of seconds in a given timeframe. Tradingview's timeframe.in_seconds() expects a simple string, and we often need to use series string, so this is an alternative to get you the value you need.

Parameters:

timeframe (string)

Returns: The number of secondsof that timeframe

timeframeOfChart()

Convert a timeframe string to a consistent standard.

Returns: The standard format for the string, or the unchanged value if it is unknown.

timeframeToString(timeframe)

Convert a timeframe string to a consistent standard.

Parameters:

timeframe (string)

Returns: (string) The standard format for the string, or the unchanged value if it is unknown.

stringToTimeframe(strTimeframe)

Convert an english-friendly timeframe string to a value that can be used by request.security. Specifically, this corrects hour strings (eg. 4h) to their numeric "minute" equivalent (eg. 240)

Parameters:

strTimeframe (string)

Returns: (string) The standard format for the string, or the unchanged value if it is unknown.

getPriceLabel(price, labelOffset, labelStyle, labelSize, labelColor, textColor)

Defines a label for the end of a price level line.

Parameters:

price (float) : The price level to render the label at.

labelOffset (int) : The number of candles to place the label to the right of price.

labelStyle (string) : A plain english string as defined in getLabelStyleFromString.

labelSize (string) : The size of the label.

labelColor (color) : The color of the label.

textColor (color) : The color of the label text (defaults to #ffffff)

Returns: The label that was created.

setPriceLabel(label, labelName, price, labelOffset, labelTemplate, labelStyle, labelColor, textColor)

Updates the label position & text based on price changes.

Parameters:

label (label) : The label to update.

labelName (string) : The name of the price level to be placed on the label.

price (float) : The price level to render the label at.

labelOffset (int) : The number of candles to place the label to the right of price.

labelTemplate (string) : The str.format template to use for the label. Defaults to: '{0}: {1} {2}{3,number,#.##}%' which means '{price}: {labelName} {+/-}{percentFromPrice}%'

labelStyle (string)

labelColor (color)

textColor (color)

getPriceLabelLine(price, labelOffset, labelColor, lineWidth)

Defines a line that will stretch from the plot line to the label.

Parameters:

price (float) : The price level to render the label at.

labelOffset (int) : The number of candles to place the label to the right of price.

labelColor (color)

lineWidth (int) : The width of the line. Defaults to 1.

setPriceLabelLine(line, price, labelOffset, lastTime, lineColor)

Updates the price label line based on price changes.

Parameters:

line (line) : The line to update.

price (float) : The price level to render the label at.

labelOffset (int) : The number of candles to place the label to the right of price.

lastTime (int) : The last time that the line should stretch from. Defaults to time.

lineColor (color)

Smart Volume S/R Pro [The_lurker]مؤشر "Smart Volume S/R Pro " هو أداة تحليل فني متقدمة مصممة لمساعدة المتداولين في تحديد مستويات الدعم والمقاومة القوية بناءً على حجم التداول، مع إضافة ميزات تحليلية متطورة مثل تصفية الاتجاه ، مناطق الثقة ، تقييم القوة ، حساب احتمالية الاختراق ، قياس السيولة ، تحديد الأهداف السعرية ، ومستويات فيبوناتشي . وايضا تقديم تسميات (Labels) بجانب كل مستوى دعم ومقاومة، تحتوي على أرقام ومعلومات دقيقة تعكس حالة السوق. هذه التسميات ليست مجرد زينة، بل أدوات تحليلية تساعد المتداولين على اتخاذ قرارات مستنيرة بناءً على بيانات السوقيهدف هذا المؤشر إلى توفير رؤية شاملة للسوق .

الوظائف الرئيسية للمؤشر

1- تحديد مستويات الدعم والمقاومة بناءً على حجم التداول العالي

يقوم المؤشر بتحليل الأشرطة (Bars) السابقة (حتى 300 شريط افتراضيًا) لتحديد النقاط التي شهدت أعلى مستويات حجم التداول.

يرسم خطوط أفقية تمثل مستويات المقاومة (عند أعلى سعر في تلك الأشرطة) والدعم (عند أدنى سعر)، ويمكن للمستخدم اختيار عدد الخطوط المعروضة (من 1 إلى 6).

2- تصفية الاتجاه باستخدام مؤشر ADX

يستخدم المؤشر مؤشر الاتجاه المتوسط (ADX) لتقييم قوة الاتجاه في السوق.

عندما تكون قوة الاتجاه عالية (تتجاوز عتبة محددة، 25 افتراضيًا)، يقلل المؤشر عدد مستويات الدعم والمقاومة المعروضة للتركيز فقط على المستويات الأكثر أهمية.

3- مناطق الثقة الديناميكية

يضيف المؤشر مناطق حول مستويات الدعم والمقاومة بناءً على متوسط المدى الحقيقي (ATR)، مما يساعد المتداولين على تصور النطاقات التي قد يتفاعل فيها السعر مع هذه المستويات.

يمكن تعديل عرض هذه المناطق باستخدام مضاعف ATR.

4- تقييم قوة المستويات

يحسب المؤشر قوة كل مستوى بناءً على حجم التداول، عدد المرات التي تم اختبار المستوى فيها (Touch Count)، وقرب السعر الحالي من المستوى.

يتم عرض درجة القوة (من 0 إلى 100) بجانب كل مستوى إذا تم تفعيل هذه الخاصية.

5- احتمالية الاختراق

يقدّر المؤشر احتمالية اختراق كل مستوى بناءً على الزخم (ROC)، قوة المستوى، والمسافة بين السعر الحالي والمستوى.

يظهر الاحتمال كنسبة مئوية إذا تم تفعيل الخيار، مما يساعد المتداولين على توقع الحركات المحتملة.

6- تحليل السيولة التاريخية

يقيس المؤشر السيولة حول كل مستوى بناءً على حجم التداول في النطاقات القريبة منه.

يمكن عرض قيم السيولة في التسميات أو استخدامها لتعديل عرض الخطوط (الخطوط الأكثر سيولة تظهر أعرض).

7- الأهداف السعرية

عند تفعيل هذه الخاصية، يحسب المؤشر أهداف سعرية للاختراق (Breakout) والارتداد (Reversal) بناءً على الزخم وقوة المستوى وATR.

يمكن عرض هذه الأهداف كنصوص في التسميات أو كخطوط أفقية على الرسم البياني.

8- مستويات فيبوناتشي

يرسم المؤشر مستويات فيبوناتشي (0.0، 0.236، 0.382، 0.5، 0.618، 0.786، 1.0) بناءً على أعلى وأدنى سعر في فترة النظرة الخلفية.

يمكن للمستخدم اختيار أي من هذه المستويات لعرضها أو إخفائها.

9- تنبيه شامل للاختراق

يوفر المؤشر تنبيهًا واحدًا يشمل جميع المستويات، حيث يُطلق التنبيه عندما يخترق السعر أي مستوى دعم أو مقاومة مع رسالة توضح نوع الاختراق والمستوى المخترق.

كيفية عمل المؤشر

الخطوة الأولى: يحدد المؤشر الأشرطة ذات الحجم العالي خلال فترة النظرة الخلفية المحددة (Lookback Period).

الخطوة الثانية: يرسم مستويات الدعم والمقاومة بناءً على أعلى وأدنى الأسعار في تلك الأشرطة، مع مراعاة عدد الخطوط المختارة من المستخدم.

الخطوة الثالثة: يطبق مرشح الاتجاه (إذا كان مفعلاً) لتقليل عدد المستويات في حالة الاتجاه القوي.

الخطوة الرابعة: يضيف التحليلات الإضافية مثل القوة، السيولة، احتمالية الاختراق، والأهداف السعرية، ويرسم مناطق الثقة ومستويات فيبوناتشي حسب الإعدادات.

الخطوة الخامسة: يراقب السعر ويطلق تنبيهًا عند الاختراق.

الإعدادات القابلة للتخصيص

1- فترة النظرة الخلفية (Lookback Period): عدد الأشرطة التي يتم تحليلها (افتراضيًا 300).

2- عدد الخطوط (Number of Lines): من 1 إلى 6 مستويات دعم ومقاومة.

3- الألوان والأنماط: يمكن تغيير ألوان الخطوط وأنماطها (ممتلئة، متقطعة، منقطة).

4- التسميات: تفعيل/تعطيل التسميات، وحجمها، وموقعها، ولون النص.

5- مرشح الاتجاه: تفعيل/تعطيل ADX، وتعديل طوله وعتبته.

6- مناطق الثقة: تفعيل/تعطيل، وتعديل طول ATR ومضاعفه.

7- القوة واحتمالية الاختراق: تفعيل/تعطيل العرض، وتعديل طول ROC.

8- السيولة: تفعيل/تعطيل تأثير السيولة على عرض الخطوط وقيمها في التسميات.

9- الأهداف السعرية: تفعيل/تعطيل الأهداف وعرضها كخطوط.

10- فيبوناتشي: اختيار المستويات المعروضة ولون الخطوط.

فوائد المؤشر

دقة عالية: يعتمد على حجم التداول لتحديد المستويات، مما يجعله أكثر موثوقية من المستويات العشوائية.

مرونة: يوفر خيارات تخصيص واسعة تتيح للمتداولين تكييفه حسب استراتيجياتهم.

تحليل شامل: يجمع بين الدعم والمقاومة، الاتجاه، السيولة، والأهداف في أداة واحدة.

سهولة الاستخدام: التسميات والتنبيهات تجعل من السهل متابعة السوق دون تعقيد.

==================================================================================تسميات (Labels) بجانب كل مستوى دعم ومقاومة، تحتوي على أرقام ومعلومات دقيقة تعكس حالة السوق. هذه التسميات ليست مجرد زينة، بل أدوات تحليلية تساعد المتداولين على اتخاذ قرارات مستنيرة بناءً على بيانات السوق. في هذا الشرح، سنستعرض كل رقم أو قيمة تظهر في التسميات ومعناها العملي.

مكونات التسميات

التسميات تظهر بجانب كل مستوى دعم (Support) ومقاومة (Resistance) وتبدأ بحرف "S" للدعم أو "R" للمقاومة، تليها مجموعة من الأرقام والقيم التي يمكن تفعيلها أو تعطيلها حسب إعدادات المستخدم. إليك تفصيل كل عنصر:

1- عدد اللمسات (Touch Count)

الرمز: يظهر مباشرة بعد "S" أو "R" (مثال: "R: 5" أو "S: 3").

المعنى: يشير إلى عدد المرات التي اختبر فيها السعر هذا المستوى دون اختراقه.

الفائدة: كلما زاد عدد اللمسات، كلما كان المستوى أقوى وأكثر أهمية. على سبيل المثال، إذا كان "R: 5"، فهذا يعني أن السعر ارتد من هذا المستوى 5 مرات، مما يجعله مقاومة قوية محتملة.

2- قوة المستوى (Strength Rating)

الرمز: يظهر بين قوسين مربعين (مثال: " ").

المعنى: قيمة من 0 إلى 100 تعكس قوة المستوى بناءً على عوامل مثل حجم التداول، عدد اللمسات، وقرب السعر الحالي من المستوى.

الفائدة: القيم العالية (مثل 75 أو أكثر) تشير إلى مستوى قوي يصعب اختراقه، بينما القيم المنخفضة (مثل 30 أو أقل) تدل على ضعف المستوى وسهولة اختراقه. يمكن للمتداول استخدام هذا لتحديد المستويات الأكثر موثوقية.

3- احتمالية الاختراق (Breakout Probability)

الرمز: يبدأ بحرف "B" متبوعًا بنسبة مئوية (مثال: "B: 60%").

المعنى: نسبة من 0% إلى 100% تُظهر احتمالية اختراق السعر للمستوى بناءً على الزخم الحالي، قوة المستوى، والمسافة بين السعر والمستوى.

الفائدة: نسبة مرتفعة (مثل 60% أو أكثر) تعني أن السعر قد يخترق المستوى قريبًا، بينما النسب المنخفضة (مثل 20%) تشير إلى احتمال ارتداد السعر. هذا مفيد لتوقع الحركة التالية.

4- قيمة السيولة (Liquidity Value)

الرمز: يبدأ بحرف "L" متبوعًا برقم (مثال: "L: 1200").

المعنى: يمثل متوسط حجم التداول في النطاق القريب من المستوى، مما يعكس السيولة التاريخية حوله.

الفائدة: القيم العالية تدل على وجود سيولة كبيرة، مما يعني أن السعر قد يتفاعل بقوة مع هذا المستوى (إما بالارتداد أو الاختراق). القيم المنخفضة تشير إلى سيولة ضعيفة، مما قد يجعل المستوى أقل تأثيرًا.

5- الأهداف السعرية (Price Targets)

الرمز: يبدأ بـ "BT" (هدف الاختراق) و"RT" (هدف الارتداد) متبوعين بأرقام (مثال: "BT: 150.50 RT: 148.20").

المعنى:

BT (Breakout Target): السعر المحتمل الذي قد يصل إليه السعر بعد اختراق المستوى.

RT (Reversal Target): السعر المحتمل الذي قد يصل إليه السعر إذا ارتد من المستوى.

الفائدة: تساعد المتداولين في تحديد نقاط الخروج المحتملة بعد الاختراق أو الارتداد، مما يسهل وضع خطة تداول دقيقة.

أمثلة عملية

تسمية مقاومة: "R: 4 B: 25% L: 1500 BT: 155.00 RT: 152.00"

المستوى اختُبر 4 مرات، قوته 80 (قوي جدًا)، احتمالية الاختراق 25% (منخفضة، أي احتمال ارتداد أعلى)، السيولة 1500 (مرتفعة)، هدف الاختراق 155.00، هدف الارتداد 152.00.

الاستنتاج: المستوى قوي ومن المرجح أن يرتد السعر منه، لكن إذا اخترق، فقد يصل إلى 155.00.

تسمية دعم: "S: 2 B: 70% L: 800 BT: 145.00 RT: 147.50"

المستوى اختُبر مرتين، قوته 40 (متوسطة إلى ضعيفة)، احتمالية الاختراق 70% (مرتفعة)، السيولة 800 (متوسطة)، هدف الاختراق 145.00، هدف الارتداد 147.50.

الاستنتاج: المستوى ضعيف ومن المحتمل أن يخترقه السعر ليهبط إلى 145.00.

كيفية الاستفادة من التسميات

تحديد القوة والضعف: استخدم قوة المستوى (Strength) لمعرفة ما إذا كان المستوى موثوقًا للارتداد أو عرضة للاختراق.

توقع الحركة: انظر إلى احتمالية الاختراق (Breakout Probability) لتحديد ما إذا كنت ستنتظر اختراقًا أو ترتدًا.

إدارة المخاطر: استخدم الأهداف السعرية (BT وRT) لتحديد نقاط جني الأرباح أو وقف الخسارة.

تقييم السيولة: ركز على المستويات ذات السيولة العالية لأنها غالبًا تكون نقاط تحول رئيسية في السوق.

تأكيد التحليل: ادمج عدد اللمسات مع القوة والسيولة للحصول على صورة كاملة عن أهمية المستوى.

تخصيص التسميات

يمكن للمستخدم تفعيل أو تعطيل أي من هذه القيم (القوة، الاحتمالية، السيولة، الأهداف) من إعدادات المؤشر.

يمكن أيضًا تغيير حجم التسميات (صغير، عادي، كبير)، موقعها (يمين، يسار، أعلى، أسفل)، ولون النص لتناسب احتياجاتك.

التسميات في هذا المؤشر هي بمثابة لوحة تحكم صغيرة بجانب كل مستوى دعم ومقاومة، تقدم لك معلومات فورية عن قوته، احتمالية اختراقه، سيولته، وأهدافه السعرية. بفهم هذه الأرقام، يمكنك تحسين قراراتك في التداول، سواء كنت تبحث عن نقاط دخول، خروج، أو إدارة مخاطر. إذا كنت تريد أداة تجمع بين البساطة والعمق التحليلي .

تنويه:

المؤشر هو أداة مساعدة فقط ويجب استخدامه مع التحليل الفني والأساسي لتحقيق أفضل النتائج.

إخلاء المسؤولية

لا يُقصد بالمعلومات والمنشورات أن تكون، أو تشكل، أي نصيحة مالية أو استثمارية أو تجارية أو أنواع أخرى من النصائح أو التوصيات المقدمة أو المعتمدة من TradingView.

The Smart Volume S/R Pro indicator is an advanced technical analysis tool designed to help traders identify strong support and resistance levels based on trading volume, with the addition of advanced analytical features such as trend filtering, confidence zones, strength assessment, breakout probability calculation, liquidity measurement, price target identification, and Fibonacci levels. It also provides labels next to each support and resistance level, containing accurate numbers and information that reflect the market condition. These labels are not just decorations, but analytical tools that help traders make informed decisions based on market data. This indicator aims to provide a comprehensive view of the market.

Main functions of the indicator

1- Identifying support and resistance levels based on high trading volume

The indicator analyzes previous bars (up to 300 bars by default) to identify the points that witnessed the highest levels of trading volume.

It draws horizontal lines representing resistance levels (at the highest price in those bars) and support (at the lowest price), and the user can choose the number of lines displayed (from 1 to 6).

2- Filtering the trend using the ADX indicator

The indicator uses the Average Directional Index (ADX) to assess the strength of a trend in the market.

When the strength of the trend is high (exceeding a specified threshold, 25 by default), the indicator reduces the number of support and resistance levels displayed to focus only on the most important levels.

3- Dynamic Confidence Zones

The indicator adds zones around support and resistance levels based on the Average True Range (ATR), helping traders visualize the ranges in which the price may interact with these levels.

The width of these zones can be adjusted using the ATR multiplier.

4- Assessing the Strength of Levels

The indicator calculates the strength of each level based on trading volume, the number of times the level has been tested (Touch Count), and the proximity of the current price to the level.

A strength score (from 0 to 100) is displayed next to each level if this feature is enabled.

5- Breakout Probability

The indicator estimates the probability of breaking each level based on momentum (ROC), the strength of the level, and the distance between the current price and the level.

The probability is displayed as a percentage if the option is enabled, helping traders anticipate potential moves.

6- Historical Liquidity Analysis

The indicator measures liquidity around each level based on the trading volume in the ranges near it.

The liquidity values can be displayed in the labels or used to adjust the width of the lines (the most liquid lines appear wider).

7- Price Targets

When this feature is enabled, the indicator calculates price targets for breakout and reversal based on momentum, level strength and ATR.

These targets can be displayed as text in the labels or as horizontal lines on the chart.

8- Fibonacci Levels

The indicator plots Fibonacci levels (0.0, 0.236, 0.382, 0.5, 0.618, 0.786, 1.0) based on the highest and lowest price in the lookback period.

The user can choose which of these levels to display or hide.

9- Comprehensive Breakout Alert

The indicator provides a single alert that includes all levels, where the alert is triggered when the price breaks any support or resistance level with a message explaining the type of breakout and the level broken.

How the indicator works

Step 1: The indicator identifies the bars with high volume during the specified Lookback Period.

Step 2: Draws support and resistance levels based on the highest and lowest prices in those bars, taking into account the number of lines selected by the user.

Step 3: Apply the trend filter (if enabled) to reduce the number of levels in case of a strong trend.

Step 4: Adds additional analyses such as strength, liquidity, breakout probability, and price targets, and draws confidence zones and Fibonacci levels according to the settings.

Step 5: Monitors the price and triggers an alert when the breakout occurs.

Customizable Settings

1- Lookback Period: Number of bars to analyze (default 300).

2- Number of Lines: From 1 to 6 support and resistance levels.

3- Colors and Styles: Line colors and styles can be changed (filled, dashed, dotted).

4- Labels: Enable/disable labels, their size, location, and text color.

5- Trend Filter: Enable/disable ADX, and modify its length and threshold.

6- Confidence Zones: Enable/disable, and modify the ATR length and multiplier.

7- Strength and Breakout Probability: Enable/disable the display, and modify the ROC length.

8- Liquidity: Enable/disable the effect of liquidity on the display of the lines and their values in the labels.

9- Price Targets: Enable/disable the targets and display them as lines.

10- Fibonacci: Choose the displayed levels and the color of the lines.

Indicator Benefits

High Accuracy: It relies on trading volume to determine the levels, which makes it more reliable than random levels.

Flexibility: It provides extensive customization options that allow traders to adapt it to their strategies.

Comprehensive Analysis: Combines support and resistance, trend, liquidity, and targets in one tool. Ease of Use: Labels and alerts make it easy to follow the market without complexity.

Labels next to each support and resistance level contain accurate numbers and information that reflect the market situation. These labels are not just decorations, but analytical tools that help traders make informed decisions based on market data. In this explanation, we will review each number or value that appears in the labels and their practical meaning.

Label Components

Labels appear next to each support and resistance level and begin with the letter "S" for support or "R" for resistance, followed by a set of numbers and values that can be enabled or disabled according to the user's settings. Here is a breakdown of each element:

1- Touch Count

Symbol: Appears immediately after "S" or "R" (example: "R: 5" or "S: 3").

Meaning: Indicates the number of times the price has tested this level without breaking it.

Benefit: The more touches, the stronger and more important the level. For example, if it is "R: 5", it means that the price has bounced off this level 5 times, making it a potentially strong resistance.

2- Strength Rating

Symbol: Appears between square brackets (example: " ").

Meaning: A value from 0 to 100 that reflects the strength of the level based on factors such as trading volume, number of touches, and proximity of the current price to the level.

Benefit: High values (such as 75 or more) indicate a strong level that is difficult to break, while low values (such as 30 or less) indicate a weak level that is easy to break. A trader can use this to determine the most reliable levels.

3- Breakout Probability

Symbol: Starts with the letter "B" followed by a percentage (example: "B: 60%").

Meaning: A percentage from 0% to 100% that shows the probability of the price breaking the level based on the current momentum, the strength of the level, and the distance between the price and the level.

Interest: A high percentage (such as 60% or more) means that the price may soon break through the level, while low percentages (such as 20%) indicate that the price may bounce. This is useful for anticipating the next move.

4- Liquidity Value

Symbol: Starts with the letter "L" followed by a number (example: "L: 1200").

Meaning: Represents the average trading volume in the range near the level, reflecting historical liquidity around it.

Interest: High values indicate high liquidity, meaning that the price may react strongly to this level (either by bouncing or breaking through). Low values indicate low liquidity, which may make the level less influential.

5- Price Targets

Symbol: Starts with "BT" (breakout target) and "RT" (rebound target) followed by numbers (example: "BT: 150.50 RT: 148.20").

Meaning:

BT (Breakout Target): The potential price that the price may reach after breaking the level.

RT (Reversal Target): The potential price that the price may reach if it rebounds from the level.

Utility: Helps traders identify potential exit points after a breakout or rebound, making it easier to develop an accurate trading plan.

Working examples

Resistance label: "R: 4 B: 25% L: 1500 BT: 155.00 RT: 152.00"

Level tested 4 times, strength 80 (very strong), probability of breakout 25% (low, i.e. higher probability of rebound), liquidity 1500 (high), breakout target 155.00, rebound target 152.00.

Conclusion: The level is strong and the price is likely to rebound from it, but if it breaks, it may reach 155.00.

Support Label: "S: 2 B: 70% L: 800 BT: 145.00 RT: 147.50"

Level tested twice, Strength 40 (medium to weak), Breakout Probability 70% (high), Liquidity 800 (medium), Breakout Target 145.00, Rebound Target 147.50.

Conclusion: The level is weak and the price is likely to break it to drop to 145.00.

How to use labels

Determine strength and weakness: Use the level's strength to see if the level is reliable for a bounce or vulnerable to a breakout.

Predict the move: Look at the Breakout Probability to determine whether to wait for a breakout or a bounce.

Risk Management: Use price targets (BT and RT) to set take profit or stop loss points.

Liquidity Evaluation: Focus on levels with high liquidity as they are often key turning points in the market.

Analysis Confirmation: Combine the number of touches with strength and liquidity to get a complete picture of the level’s importance.

Customize Labels

The user can enable or disable any of these values (strength, probability, liquidity, targets) from the indicator settings.

The size of the labels (small, normal, large), their position (right, left, top, bottom), and the color of the text can also be changed to suit your needs.

The labels in this indicator act as a small dashboard next to each support and resistance level, providing you with instant information about its strength, probability of breakout, liquidity, and price targets. By understanding these numbers, you can improve your trading decisions, whether you are looking for entry points, exit points, or risk management. If you want a tool that combines simplicity with analytical depth.

Disclaimer:

The indicator is an auxiliary tool only and should be used in conjunction with technical and fundamental analysis for best results.

Disclaimer

The information and posts are not intended to be, or constitute, any financial, investment, trading or other types of advice or recommendations provided or endorsed by TradingView.

Ichimoku(TF)This Pine Script indicator is a comprehensive Ichimoku Cloud implementation designed for TradingView. Its uniqueness lies in the precisely calculated settings for each timeframe, offering a tailored Ichimoku experience across different chart resolutions.

Key Features:

Timeframe-Specific Presets: The indicator includes a wide range of pre-defined settings optimized for various timeframes (1m, 2m, 3m, 5m, 10m, 15m, 30m, 45m, 1H, 2H, 3H, 4H, 6H, 12H, 18H, 1D, 3D, 1W, 1M). This ensures accurate Ichimoku calculations and relevant signals for your chosen timeframe.

Ichimoku Cloud: Plots the standard Ichimoku Cloud components: Tenkan-sen (Conversion Line), Kijun-sen (Base Line), Senkou Span A & B (Leading Spans), and Chikou Span (Lagging Span).

Configurable Display: Allows toggling the Ichimoku Cloud display, coloring bars based on the trend (above or below the cloud), and customizing table visibility, style, font size and position.

Trend Analysis Table: A summary table provides a quick overview of the current trend based on Ichimoku components. It assesses the strength of the trend based on the price's relation to the Tenkan-sen, Kijun-sen, Kumo Cloud, Chikou Span and Kumo Twist. The table offers both detailed and short styles.

Buy/Sell Signals: Generates buy and sell signals based on Tenkan-sen/Kijun-sen crossovers.

Uniqueness:

The primary advantage of this indicator is its meticulous configuration for different timeframes. Instead of using a single set of parameters for all timeframes, it provides optimized values that are more suitable for specific chart resolutions. The summary table provides an easy and quick way to assess the trend.

Этот индикатор Pine Script представляет собой комплексную реализацию облака Ишимоку, разработанную для TradingView. Его уникальность заключается в точно рассчитанных настройках для каждого таймфрейма, предлагая индивидуальный опыт Ишимоку для различных разрешений графиков.

Ключевые особенности:

Предустановки для конкретных таймфреймов: Индикатор включает в себя широкий спектр предопределенных настроек, оптимизированных для различных таймфреймов (1m, 2m, 3m, 5m, 10m, 15m, 30m, 45m, 1H, 2H, 3H, 4H, 6H, 12H, 18H, 1D, 3D, 1W, 1M). Это обеспечивает точные вычисления Ишимоку и релевантные сигналы для выбранного вами таймфрейма.

Облако Ишимоку: Отображает стандартные компоненты облака Ишимоку: Tenkan-sen (линия конверсии), Kijun-sen (базовая линия), Senkou Span A & B (ведущие диапазоны) и Chikou Span (запаздывающий диапазон).

Настраиваемое отображение: Позволяет переключать отображение облака Ишимоку, окрашивать бары в зависимости от тренда (выше или ниже облака), а также настраивать видимость таблицы, стиль, размер шрифта и положение.

Таблица анализа тренда: Сводная таблица обеспечивает быстрый обзор текущего тренда на основе компонентов Ишимоку. Он оценивает силу тренда на основе отношения цены к Tenkan-sen, Kijun-sen, облаку Kumo, Chikou Span и Kumo Twist. Таблица предлагает как подробный, так и краткий стили.

Сигналы покупки/продажи: Генерирует сигналы покупки и продажи на основе пересечений Tenkan-sen/Kijun-sen.

Уникальность:

Основным преимуществом этого индикатора является его тщательная настройка для разных таймфреймов. Вместо использования единого набора параметров для всех таймфреймов он предоставляет оптимизированные значения, которые больше подходят для конкретных разрешений графиков. Сводная таблица обеспечивает простой и быстрый способ оценки тренда.

Dynamic Range Finder [The_lurker]هو أداة تهدف إلى تحديد نطاق السعر الديناميكي بناءً على التقلبات ومتوسط الأسعار . حيث يتم التعرف على مناطق التوحيد السعري (Consolidation) ويعطي إشارات شراء وبيع عند اختراق أو كسر هذا النطاق .

// يفضل استخدام المؤشر على اطار 4 ساعات واكثر //

مميزات المؤشر :

1- اكتشاف النطاق السعري الديناميكي

- يقوم المؤشر بحساب متوسط السعر خلال فترة محددة ومقارنة الإغلاقات الحديثة بمدى تقلب الأسعار (ATR) لمعرفة ما إذا كان السعر يتحرك داخل نطاق معين.

2- تحديد الاختراقات Breakout Signals

- عند اختراق السعر الحد العلوي للنطاق، يظهر المؤشر إشارة شراء (BUY).

- عند كسر السعر الحد السفلي للنطاق، يظهر المؤشر إشارة بيع (SELL).

3- دعم أنماط متعددة للمتوسطات المتحركة

- يسمح للمستخدمين باختيار نوع المتوسط المتحرك (SMA، EMA، WMA) المستخدم في حساب متوسط السعر.

4- إعدادات مخصصة للفلترة بحجم التداول (اختياري)

- فلترة حجم التداول هي ميزة اختيارية في المؤشر تسمح بتصفية إشارات الشراء والبيع بناءً على قوة الحجم المتداول مما يعزز دقة الإشارات عن طريق التأكد من أن الاختراقات السعرية مدعومة بحجم تداول قوي

5- تصميم مرن مع تخصيص للألوان والأنماط

- يمكن للمستخدمين تغيير ألوان النطاق وإشارات البيع والشراء حسب رغبتهم.

6- تنبيهات آلية عند حدوث كسر أو اختراق

- يتضمن تنبيهات (Alerts) عند حدوث إشارة بيع أو شراء.

كيف يعمل المؤشر؟

* يتم حساب متوسط السعر خلال الفترة المحددة (rangePeriod).

* يتم حساب التقلب السعري (ATR) ومضاعفته بمعامل النطاق (rangeMultiplier).

* يتم رسم مستطيل يعبر عن النطاق السعري بين (متوسط السعر ± التقلب).

* إذا تجاوز السعر الحد العلوي → إشارة شراء (BUY).

* إذا كسر السعر الحد السفلي → إشارة بيع (SELL).

* يمكن تصفية الإشارات باستخدام حجم التداول (اختياري).

1.0 → الحجم الحالي يجب أن يكون على الأقل مساويًا للمتوسط.

1.2 → الحجم الحالي يجب أن يكون أعلى من المتوسط بنسبة 20%.

1.5 → الحجم الحالي يجب أن يكون أعلى من المتوسط بنسبة 50%.

تنويه:

المؤشر هو أداة مساعدة فقط ويجب استخدامه مع التحليل الفني والأساسي لتحقيق أفضل النتائج.

إخلاء المسؤولية

لا يُقصد بالمعلومات والمنشورات أن تكون، أو تشكل، أي نصيحة مالية أو استثمارية أو تجارية أو أنواع أخرى من النصائح أو التوصيات المقدمة أو المعتمدة من TradingView.

It is a tool that aims to determine the dynamic price range based on fluctuations and average prices. Consolidation areas are identified and buy and sell signals are given when this range is breached or broken.

// It is preferable to use the indicator on a 4-hour frame or more //

Features of the indicator:

1- Detecting the dynamic price range

- The indicator calculates the average price over a specific period and compares recent closings with the price volatility range (ATR) to see if the price is moving within a specific range.

2- Identifying Breakout Signals

- When the price breaks the upper limit of the range, the indicator shows a buy signal (BUY).

- When the price breaks the lower limit of the range, the indicator shows a sell signal (SELL).

3- Support for multiple moving average patterns

- Allows users to choose the type of moving average (SMA, EMA, WMA) used to calculate the average price.

4- Custom settings for filtering by trading volume (optional)

- Trading volume filtering is an optional feature in the indicator that allows filtering buy and sell signals based on the strength of the trading volume, which enhances the accuracy of the signals by ensuring that price breakouts are supported by strong trading volume

5- Flexible design with customization of colors and patterns

- Users can change the colors of the range and buy and sell signals as they wish.

6- Automatic alerts when a breakout or breakout occurs

- Includes alerts when a buy or sell signal occurs.

How does the indicator work?

* The average price is calculated over the specified period (rangePeriod).

* The price volatility (ATR) is calculated and multiplied by the range factor (rangeMultiplier).

* A rectangle is drawn that represents the price range between (average price ± volatility).

* If the price exceeds the upper bound → a buy signal (BUY).

* If the price breaks the lower bound → a sell signal (SELL).

* Signals can be filtered using trading volume (optional).

1.0 → Current volume should be at least equal to the average.