Time based Insights [Digit23]Description:

The NSE Trading Time Insights indicator is a powerful tool designed for traders on the National Stock Exchange (NSE) of India. It provides a comprehensive overview of different trading sessions throughout the day, offering valuable insights into market characteristics and potential trading strategies for each time period.

Key Features:

1. Dynamic Session Display: The indicator automatically detects the current trading session and highlights it in the table.

2. Customizable Table: Users can choose to display either a full table showing all sessions or focus on the current session only.

3. User-Editable Content: Time ranges, session characteristics, and trading insights are fully customizable by the user.

4. Visual Customization: Table position and color scheme can be adjusted to suit individual preferences.

5. Market Status Indicator: Clearly shows when the market is closed.

Sessions Covered:

1. Opening Bell

2. Mid-Morning

3. Lunch Hour

4. Early Afternoon

5. Power Hour

For each session, the indicator displays:

- Time Range

- Session Name

- Market Characteristics

- Trading Insights

Customization Options:

- Table Position: Choose from top-left, top-right, bottom-left, or bottom-right of the chart.

- Color Scheme: Customize colors for header, cells, highlighting, and market closed status.

- Session Details: Edit time ranges, characteristics, and trading insights for each session.

Usage:

This indicator is particularly useful for:

1. New traders learning about intraday market dynamics on the NSE.

2. Experienced traders looking for a quick reference of session characteristics.

3. Traders developing or refining time-based trading strategies.

4. Anyone seeking to understand the typical flow of the trading day on the NSE.

Note:

The indicator uses the chart's time to determine the current session. Ensure your chart is set to the correct time zone for accurate results.

Disclaimer:

This indicator is for informational purposes only. The provided insights and characteristics are general in nature and may not reflect current market conditions. Always conduct your own analysis and risk assessment before making trading decisions.

"Table" için komut dosyalarını ara

Position Size Calculator for ContractDescription:

Position Size Calculator is a versatile Pine Script tool designed to help traders manage their risk and position sizing effectively. This script calculates essential trading metrics and visualizes them directly on your chart, helping you make informed trading decisions.

Features:

- Account Size & Risk Management:

- Account Size: Input your total account balance to calculate position sizes.

- Maximum Risk: Define how much of your account you are willing to risk per trade in dollars.

- Pip Value: Set the value of a single pip for one contract, which is crucial for calculating risk

and position size.

Trade Setup Visualization:

- Entry Price: Specify the price at which you plan to enter the trade.

- Stop Loss: Define your stop loss level to manage your risk.

- Take Profit: Set your target profit level for the trade.

- Visualize the Entry, Stop Loss, and Take Profit levels on your chart with customizable line

colors and text sizes.

- View the distance in pips between the Entry, Stop Loss, and Take Profit levels.

Position Size Calculation:

- Calculates the number of contracts to open based on your risk tolerance and the pip value.

- Displays the maximum number of contracts you can open given your risk parameters.

Customizable Table Display:

- Table Position: Choose the position of the summary table on the chart (Top-Left, Top-Right,

Bottom-Left, Bottom-Right, etc.).

- Table Text Size: Adjust the text size for the summary table.

- Table Background Color: Set the background color for the summary table.

- Table Border Color: Customize the border color of the summary table.

How to Use:

1- Input your Account Size: Enter your current account balance.

2- Set Maximum Risk and Pip Value: Define how much you're willing to risk per trade and the

pip value for your contract.

3- Define Trade Levels: Input your desired Entry Price, Stop Loss, and Take Profit levels.

4- Customize Visuals: Adjust the line styles and table settings to fit your preferences.

5- View Calculations: The script will display the distance in pips and the calculated position

size directly on your chart.

Example Usage:

Example to calculate the value of 1 pips with 1 contract:

Inputs:

Account Size: Your total trading account balance.

Maximum Risk: Risk amount per trade in dollars.

Pip Value: Value of one pip for a single contract.

Entry Price: The price at which you plan to enter the trade.

Stop Loss: The level at which you will exit the trade to cut losses.

Take Profit: The target price to lock in profits.

Line Text Size: Size of the text for the Entry, Stop Loss, and Take Profit lines.

Line Extend: Option to extend the lines for visual clarity.

Table Position: Position of the summary table on the chart.

Table Text Size: Size of the text in the summary table.

Table Background Color: Background color of the summary table.

Table Border Color: Border color of the summary table.

Visuals:

Entry Price, Stop Loss, and Take Profit levels are clearly marked on the chart.

Summary Table with important trade metrics displayed.

Live Economic Calendar by toodegrees⚠️ PLEASE READ ⚠️

Although this indicator is accurate in showcasing live and upcoming News Events, checking the original sources is always suggested. This indicator aims to save Time, but due to limitations it may not be 100% correct 100% of the Time.

Description:

The Live Economic Calendar indicator seamlessly integrates with external news sources to provide real-Time, upcoming, and past financial news directly on your Tradingview chart.

By having a clear understanding of when news are planned to be released, as well as their respective impact, analysts can prepare their weeks and days in advance. These injections of volatility can be harnessed by analysts to support their thesis, or may want to be avoided to ensure higher probability market conditions. Fundamentals and news releases transcend the boundaries of technical analysis, as their effects are difficult to predict or estimate.

Designed for both novice and experienced traders, the Live Economic Calendar indicator enhances your analysis by keeping you informed of the latest and upcoming market-moving news.

This is achieved with three different visual components:

News Table: A dedicated News Table shows the Day of the Week, Date, Time of the Day, Currency, Expected Impact, and News Name for each event (in chronological order). Once a news event has occurred, or the day is over, it will be greyed out – helping to focus on the next upcoming news events.

News Lines: Vertical lines plotted in the future help analysts monitor upcoming news events; vertical lines in the past help analysts spot and backtest previous news events that already occurred.

News Labels: Color-coded news labels will plot once the news events have occurred. This not only gives analysts a minimalistic visual cue, but also retains the information of which news were released at that Time in their tooltips.

Forex Factory Calendar News Feed:

The Forex Factory Data Feed includes news events from January 2007 to the present. The data is updated daily. Please see the Technical Description below for more information.

Forex Factory provides news for all major currencies and markets:

Australia (AUD)

Canada (CAD)

Switzerland (CHF)

China (CNY)

European Union (EUR)

United Kingdom (GBP)

Japan (JPY)

New Zealand (NZD)

United States of America (USD)

Further, there are four types of news impact, defined by respective color-coding which is retained to avoid confusion:

⚪ Holiday

🟡 Low Impact

🟠 Medium Impact

🔴 High Impact

News' Time of the day data is in 24H format, and 'All Day' news are marked at Daily candle open.

⚠️ Original Release Notes ⚠️

The original release of this indicator supports the Forex Factory News Calendar in EST (New York Time). Future updates will include multiple news sources, as well as supporting different Timezones.

Given Data limitations, the Daily chart can omit some data due to the market being close on some days. This will be fixed in the future once an efficient solution is implemented.

Key Features:

Impact-Based News Filtering: Filter news items based on their expected impact (holiday, low, medium, high) to focus on the most market-critical information.

Symbol-Specific News: Automatically filter news to display only what's relevant to the currency pair or trading symbol you are analyzing.

Custom Currency News: Want to see more than the news relevant to the current symbol? Toggle which markets' news you are most interested in.

Chart History: Keep your charts clean by displaying only the drawings of Today's news, or This Week's news.

Custom Lookback: Look further back in Time by choosing a custom number of Lookback Days, allowing you to backtest and keep in mind salient news events from the past.

Line and Label Customization: Both the News Lines and Labels are highly customizable (except the colors), allowing you to make the indicator yours.

Table History: Choose whether to focus on Today's news only, or the news for This Week.

Table Customization: The table colors and position are highly customizable, allowing you to make it fit your visual preference and your layouts' aesthetic.

"Wondering how it's done? 👇"

Technical Description:

This script utilizes Pine Seeds , a service integrated with TradingView for importing custom data. This stunning feature enables users to upload and access custom End Of Day (EOD) data, which can be updated as frequently as five times daily.

This data can be imported in one of two formats:

Single Value: integer or float

Candle Data: open, high, low, close, volume

Upon encountering Pine Seeds, I recognized its potential for importing financial news events. Given that Forex Factory is a primary source of financial news in my personal analysis, integrating it into my layouts seemed like an exciting opportunity. This integration is expected to provide significant value to users looking to integrate additional news feeds all in one place.

Development Challenges:

Format Limitations: News events must be converted into numerical values for import, due to the required Pine Seeds format.

Amount of Data: With all currencies considered, the system may encounter over 40 news events in a single day.

Data Availability: The reliance on End Of Day (EOD) data means that information for the current day is displayed with a delay, and accessing future data is not possible.

Solutions:

Encoding: Each news event is encoded as an integer in the "DCHHMMITYP" format.

D = day of the week

C = currency

HHMM = Time of day

I = news impact

TYP = event ID (see Event Library A and Event Library B )

To ensure data assignment for each candle across the open, high, low, close, and volume series, the value "999" is used as a placeholder:

Importing: Utilizing the encoding system, up to five news events per day can be imported for a singular Pine Seeds custom symbol.

By creating multiple custom Pine Seeds Symbols, efficient imports of a larger number of events is then easily achievable. Nine unique symbols have been established, accommodating up to 45 news events per day.

These symbols are searchable, and accessible as " TOODEGREES_FOREX_FACTORY_SLOT_N " where N ranges from 1 to 9.

The Pine Seeds data feed appears as follows:

Uploading Schedule: To ensure analysts are informed about current and upcoming week's news, events are uploaded one week in advance.

This approach is vital for preparing for potential market impacts across various asset classes and currencies, allowing visibility of an entire week's news ahead of Time.

Data Scraping:

Unfortunately Forex Factory doesn't offer an API to fetch their news feed.

Hence an ad hoc python scraper was developed to read and save news events from January 2007 till the present leveraging Selenium. The scraper algorithm is part of a larger script responsible for scraping data, formatting data, and creating all necessary datasets.

The pseudo-code for the python script is as follows:

Read and save news event data on Forex Factory

Format day of the week, currency, Time of the day, and impact data for the Encoding

Encode and save News Event IDs – Event ID dataset is created

Format news data for Pine Seeds (roll-back date by one week, assign news to open, high, low, close, and volume values)

Create Pine Seeds Datasets

This script is ran everyday at Futures market close (16:00 EST) to update the last part of the each dataset, ensuring accuracy, and taking into account last-minute news additions or revisions.

Once the data (next week's news) is imported by the Live Economic Calendar indicator, it's immediately decoded by leveraging the Forex Factory Decoding Library , and saved into an array.

Upon a new week open, the decoded data is used to plot news events on the chart and in the news table.

See the inner workings of these processes in the Forex Factory Utility Library .

Although these libraries are specifically built for this indicator, feel free to use them to create your own scripts. Looking forward to see what the Pine Script community comes up with!

Thank you for making it this far. Enjoy!

Ciao,

toodegrees

This tool is available ONLY on the TradingView platform.

Terms and Conditions

Our charting tools are provided for informational and educational purposes only and do not constitute financial, investment, or trading advice. Our charting tools are not designed to predict market movements or provide specific recommendations. Users should be aware that past performance is not indicative of future results and should not be relied upon for making financial decisions. By using our charting tools, the user agrees that Toodegrees and the Toodegrees Team are not responsible for any decisions made based on the information provided by these charting tools. The user assumes full responsibility and liability for any actions taken and the consequences thereof, including any loss of money or investments that may occur as a result of using these products. Hence, by using these charting tools, the user accepts and acknowledges that Toodegrees and the Toodegrees Team are not liable nor responsible for any unwanted outcome that arises from the development, or the use of these charting tools. Finally, the user indemnifies Toodegrees and the Toodegrees Team from any and all liability.

By continuing to use these charting tools, the user acknowledges and agrees to the Terms and Conditions outlined in this legal disclaimer.

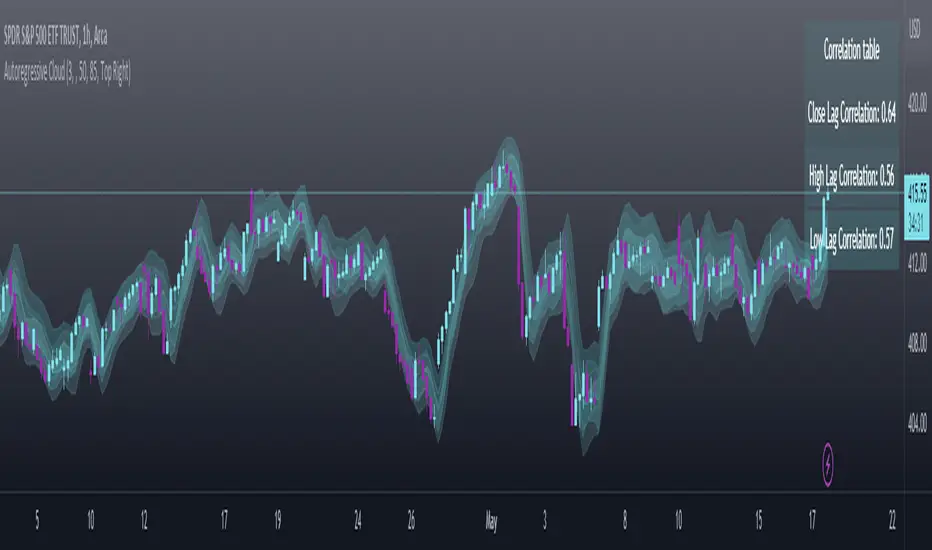

Autoregressive CloudHello,

I am releasing this indicator called the Autoregressive Cloud Indicator.

What it does:

The indicator performs an autoregression analysis on 3 price variables of a ticker, those being the High, the Low and the Close. It uses a 1-lag system and looks back at the previous close, high and low’s effect on the proceeding high, low and close. It then plots out the anticipated range for the ticker based on the autoregression analysis, as well as displays the lag-correlation (autocorrelation) in a table.

What is Autoregression analysis?

Autoregression is a modelling technique used to describe a time series based on its own past values. It assumes that the current value of a variable is a linear combination of its previous values and a random error term.

And what is autocorrelation?

Autocorrelation measures the correlation between a time series and its lagged values. It quantifies the degree to which the current value of a series is related to its past values at different lags, indicating any patterns or dependencies in the data over time. Autoregression and autocorrelation are closely related concepts used to analyze and model time series data.

So how does it work?

The indicator calculates autoregressive values for the close, high, and low prices of a security based on the specified lookback length (which is defaulted to 50). It then plots three sets of clouds representing the smoothed autoregressive values for each price component (done using the SMA function). The transparency of the clouds can be adjusted using the "Transparency" input. Additionally, the code includes a correlation table that displays the correlation coefficients between the lagged values of the close, high, and low prices. The table's position can be customized using the "Position" input.

The indicator defaults to the chart timeframe; however, you can manually adjust the indicator to display the range for whatever timeframe you would like. You can view the 30 minute, 15 or even hourly range on the 1 minute or 5 minute chart if you want.

The indicator will show the anticipated “true trading range” of the stock based on the autoregression and autocorrelation of all 3 variables:

Above is SPY on the 5 minute timeframe with 15 minute levels overlayed. Here, you can see the anticipated trading range for that 15 minute time period.

Using the Correlation Table:

The correlation table displays the Pearson Coefficient for all 3 autoregressions.

A positive correlation: A positive autocorrelation indicates a positive relationship between past and current values of a time series variable. It suggests that when the variable has a high value at a certain time, it is more likely to have a high value in the future, and when it has a low value, it is more likely to have a low value in the future. This positive autocorrelation can imply persistence or trend in the data, indicating that past values can provide useful information for predicting future values. The rule of thumb is anything over 0.5 is considered significant.

A positive correlation among all 3 variables also indicates an uptrend. If you see a strong positive (i.e. the values are all greater than 0.8), it indicates an incredibly decisive and strong uptrend.

A negative correlation: A negative autocorrelation indicates an inverse relationship between past and current values of a time series variable. It suggests that when the variable has a high value at a certain time, it is more likely to have a low value in the future, and vice versa. This negative autocorrelation can imply mean reversion or oscillatory behavior in the data, where extreme values tend to be followed by values closer to the average. It indicates that past values can provide useful information for predicting future values by anticipating a reversal in the direction of the variable. The rule of thumb is anything below or equal to -0.5 is considered significant.

A negative correlation among all 3 variables also indicates a downtrend. If you see a strong negative (i.e. the values are all less than or equal to -0.8), it indicates an incredibly decisive and strong downtrend.

Uses of the Indicator:

The indicator can be used for the following functions:

1. Day trading and scalping within an expected range;

2. Determining the strength or weakness of an uptrend or downtrend on various timeframes;

3. Determining the relationship between previous values and past performance and its effect on future performance;

4. Can alert to changes in trend direction in advance (you may see high, low or close turn negative before others, signifying that weakness is beginning to materialize in an uptrend, or inverse in a downtrend (value changes positive)).

Customizability:

SMA: The autoregression data is smoothed by a 3 period lookback. You can change this if you want, but in order for the indicator to present the true trading range, it is recommended to leave it at <= 3.

Lookback Length: This is the length of the lookback period for the autoregression and autocorrelation functions.

Transparency settings: You can adjust the transparency of the clouds manually.

Timeframe: You can adjust the timeframe, as explained above, to display the timeframe of interest. When you adjust the timeframe, the data will all reflect that timeframe and not necessarily the current TF you have open (i.e. you select 30 minutes while viewing it on the 5 minute, it will show the data for the 30 minute TF period).

Video Tutorial:

I have prepared a video outlining the indicator and also explaining the theory of autoregression/correlation. You can find it below:

Let me know any comments, questions or suggestions below.

Thank you for taking the time to read/watch and check out this indicator.

Safe trades everyone!

store - larger data storage for complex item typesLibrary "store"

Object/Property Storage System Semi-Simplified. .

It's a helpful toolset while designing UDT's as it remains flexible,

this helps in not having to remap an entire script while tinkering.

Set an object up, and add as man properties as yyou wish.

a property can be one of any pine built in types. so a single

object can contain sa, ohlc each with a color, a float, an assigned int

and those 4 props each have 3 sub-assigned values.

as in demo, the alternating table object has 2 different tables

it's a pseudo more complex wa to create our own flexible

version of a UDT, but that will not ~break~ on library updates

so you can update awa without fear, as this libb will no change

saving ou the hassle of creating UDT's that continually change.

set(dict, _object, _prop, _item)

Add/Updates item to storage. Autoselects subclass dictionary on set

Parameters:

dict : (dictionary) dict.type subdictionary (req for overload)

_object : (string) object name

_prop

_item : () item to set

Returns: item item wwith column/row

set(dict, _object, _prop, _item)

Parameters:

dict

_object

_prop

_item

set(dict, _object, _prop, _item)

Parameters:

dict

_object

_prop

_item

set(dict, _object, _prop, _item)

Parameters:

dict

_object

_prop

_item

set(dict, _object, _prop, _item)

Parameters:

dict

_object

_prop

_item

set(dict, _object, _prop, _item)

Parameters:

dict

_object

_prop

_item

set(dict, _object, _prop, _item)

Parameters:

dict

_object

_prop

_item

set(dict, _object, _prop, _item)

Parameters:

dict

_object

_prop

_item

set(dict, _object, _prop, _item)

Parameters:

dict

_object

_prop

_item

set(dict, _object, _prop, _item)

Parameters:

dict

_object

_prop

_item

set(dict, _index, _item)

Parameters:

dict

_index

_item

set(dict, _index, _item)

Parameters:

dict

_index

_item

set(dict, _index, _item)

Parameters:

dict

_index

_item

set(dict, _index, _item)

Parameters:

dict

_index

_item

set(dict, _index, _item)

Parameters:

dict

_index

_item

set(dict, _index, _item)

Parameters:

dict

_index

_item

set(dict, _index, _item)

Parameters:

dict

_index

_item

set(dict, _index, _item)

Parameters:

dict

_index

_item

set(dict, _index, _item)

Parameters:

dict

_index

_item

set(dict, _index, _item)

Parameters:

dict

_index

_item

get(typedict, _object, _prop)

Get item by object name and property (string)

Parameters:

typedict : (dict) dict.type subdictionary (req for overload)

_object : (string) object name

_prop

Returns: item from storage

get(typedict, _object, _prop)

Parameters:

typedict

_object

_prop

get(typedict, _object, _prop)

Parameters:

typedict

_object

_prop

get(typedict, _object, _prop)

Parameters:

typedict

_object

_prop

get(typedict, _object, _prop)

Parameters:

typedict

_object

_prop

get(typedict, _object, _prop)

Parameters:

typedict

_object

_prop

get(typedict, _object, _prop)

Parameters:

typedict

_object

_prop

get(typedict, _object, _prop)

Parameters:

typedict

_object

_prop

get(typedict, _object, _prop)

Parameters:

typedict

_object

_prop

get(typedict, _object, _prop)

Parameters:

typedict

_object

_prop

get(typedict, _index)

Parameters:

typedict

_index

get(typedict, _index)

Parameters:

typedict

_index

get(typedict, _index)

Parameters:

typedict

_index

get(typedict, _index)

Parameters:

typedict

_index

get(typedict, _index)

Parameters:

typedict

_index

get(typedict, _index)

Parameters:

typedict

_index

get(typedict, _index)

Parameters:

typedict

_index

get(typedict, _index)

Parameters:

typedict

_index

get(typedict, _index)

Parameters:

typedict

_index

get(typedict, _index)

Parameters:

typedict

_index

remove(typedict, _object, _prop)

Remove a specific property from an object

Parameters:

typedict : (dict) dict.type subdictionary (req for overload)

_object : (string) object name

_prop

Returns: item from storage

remove(typedict, _object, _prop)

Parameters:

typedict

_object

_prop

remove(typedict, _object, _prop)

Parameters:

typedict

_object

_prop

remove(typedict, _object, _prop)

Parameters:

typedict

_object

_prop

remove(typedict, _object, _prop)

Parameters:

typedict

_object

_prop

remove(typedict, _object, _prop)

Parameters:

typedict

_object

_prop

remove(typedict, _object, _prop)

Parameters:

typedict

_object

_prop

remove(typedict, _object, _prop)

Parameters:

typedict

_object

_prop

remove(typedict, _object, _prop)

Parameters:

typedict

_object

_prop

remove(typedict, _object, _prop)

Parameters:

typedict

_object

_prop

remove(typedict, _index)

Parameters:

typedict

_index

remove(typedict, _index)

Parameters:

typedict

_index

remove(typedict, _index)

Parameters:

typedict

_index

remove(typedict, _index)

Parameters:

typedict

_index

remove(typedict, _index)

Parameters:

typedict

_index

remove(typedict, _index)

Parameters:

typedict

_index

remove(typedict, _index)

Parameters:

typedict

_index

remove(typedict, _index)

Parameters:

typedict

_index

remove(typedict, _index)

Parameters:

typedict

_index

remove(typedict, _index)

Parameters:

typedict

_index

delete(_dict, _object)

Remove a complete Object and all props

Parameters:

_dict

_object : (string) object name

Returns: item from storage

delete(_dict, _index)

Parameters:

_dict

_index

wipe(_dict, _object, _prop)

Remove Property slot for all 10 item types

Parameters:

_dict : (dictionary) The full dictionary item

_object : (string) object name

_prop

Returns: item from storage

wipe(_dict, _index)

Parameters:

_dict

_index

init(_Objlim, _Proplim)

Create New Dictionary ready to use (9999 size limit - (_objlim +_Proplim) for row/column 0)

# Full dictionary with all types

> start with this

Parameters:

_Objlim : (int) maximum objects (think horizontal)

_Proplim : (int) maximum properties per obj (vertical)

Returns: dictionary typoe object

boxdict

Fields:

keys

items

booldict

Fields:

keys

items

colordict

Fields:

keys

items

floatdict

Fields:

keys

items

intdict

Fields:

keys

items

labeldict

Fields:

keys

items

linedict

Fields:

keys

items

linefilldict

Fields:

keys

items

stringdict

Fields:

keys

items

tabledict

Fields:

keys

items

dictionary

Fields:

boxs

bools

colors

floats

ints

labels

lines

linefills

strings

tables

keys

item

Fields:

objCol

propRow

object

property

actionItem

dictionaries

Dictionar OF dictionaries

Fields:

dicts

ahpuhelperLibrary "ahpuhelper"

Helper Library for Auto Harmonic Patterns UltimateX. It is not meaningful for others. This is supposed to be private library. But, publishing it to make sure that I don't delete accidentally. Some functions may be useful for coders.

insert_open_trades_table_column(showOpenTrades, table_id, column, colors, values, intStatus, harmonicTrailingStartState, lblSizeOpenTrades)

add data to open trades table column

Parameters:

showOpenTrades : flag to show open trades table

table_id : Table Id

column : refers to pattern data

colors : backgroud and text color array

values : cell values

intStatus : status as integer

harmonicTrailingStartState : trailing Start state as per configs

lblSizeOpenTrades : text size

Returns: nextColumn

populate_closed_stats(ClosedStatsPosition, bullishCounts, bearishCounts, bullishRetouchCounts, bearishRetouchCounts, bullishSizeMatrix, bearishSizeMatrix, bullishRR, bearishRR, allPatternLabels, flags, rowMain, rowHeaders)

populate closed stats for harmonic patterns

Parameters:

ClosedStatsPosition : Table position for closed stats

bullishCounts : Matrix containing bullish trade stats

bearishCounts : Matrix containing bearish trade stats

bullishRetouchCounts : Matrix containing bullish trade stats for those which retouched entry

bearishRetouchCounts : Matrix containing bearish trade stats for those which retouched entry

bullishSizeMatrix : Matrix containing data about size of bullish patterns

bearishSizeMatrix : Matrix containing data about size of bearish patterns

bullishRR : Matrix containing Risk Reward data of bullish patterns

bearishRR : Matrix containing Risk Reward data of bearish patterns

allPatternLabels : array containing pattern labels

flags : display flags

rowMain : Pattern header data

rowHeaders : header grouping data

Returns: void

get_rr_details(patternTradeDetails, harmonicTrailingStartState, disableTrail, breakEvenTrail)

calculate and return risk reward based on targets and stops

Parameters:

patternTradeDetails : array containing stop, entry and targets

harmonicTrailingStartState : trailing point

disableTrail : If set, ignores trailing point

breakEvenTrail : If set, trailing does not go beyond breakeven.

Returns: nextColumn

DebugConsoleLibrary "DebugConsole"

Methods for debuging/output into a table, console like style.

init(size) initiate property variables.

Parameters:

size : int, console line size.

Returns: tuple, table and string array.

queue(console_id, new_line) Regular Queue, will be called once every bar its called.

Parameters:

console_id : string array, console configuration array.

new_line : string, with contents for new line.

Returns: void.

queue_one(console_id, new_line) Queue only one time, will not repeat itself.

Parameters:

console_id : string array, console configuration array.

new_line : string, with contents for new line.

Returns: void.

update(table_id, console_id) Update method for the console screen.

Parameters:

table_id : table, table to update console text.

console_id : string array, console configuration array.

Returns: void.

Total Returns indicator by PtahXPtahX Total Returns – True Total-Return View for Any Symbol

Most charts only show price. This script shows what your position actually did once you include dividends and, optionally, inflation.

What this indicator does

1. Builds a Total Return series

You choose how dividends are treated:

* Reinvest (default): All gross dividends are automatically reinvested into more shares on the ex-dividend bar.

* Cash: Dividends are kept as cash added on top of your initial position.

* Ignore: Price only, like a regular chart.

This answers: “If I bought once at the start and held, how much would that position be worth now, given this dividend policy?”

2. Optional inflation-adjusted (real) returns

You can also plot a real total-return line, which adjusts for inflation using a CPI series.

This answers: “How did my purchasing power change after inflation?”

3. Stats window and exponential trendline

You can pick the time window:

* Since inception (full available history)

* YTD

* Last 1 Year

* Last 5 Years

* Custom start date

For that window, the script:

* Normalizes Total Return to 1.0 at the window start.

* Fits an exponential trendline (pink) to the normalized series.

* Displays a stats table in the bottom-right showing:

• Overall Return (%) over the selected range

• CAGR (compound annual growth rate, % per year)

• Trendline growth (% per year)

• R² of the trendline (fit quality)

• A separate “Since inception” block (overall return and CAGR from the first bar on the chart)

How to use it

1. Add the indicator to your chart.

2. Open the settings:

Total Return & Dividends

* Dividend mode

• Reinvest: closest to a true total-return curve (default).

• Cash: price plus cash dividends.

• Ignore: price only.

* Plot inflation-adjusted TR line

• Turn this on if you want to see a real (CPI-adjusted) total-return line.

Inflation / Real Returns

* Inflation country code and field code

• Leave defaults if you just want a standard CPI series.

* Use real TR for stats & trendline

• On: stats and trendline use the inflation-adjusted curve.

• Off: stats use the nominal (non-adjusted) total return.

Stats Range & Trendline

* Stats range: Since inception, YTD, 1 Year, 5 Years, or Custom date.

* Custom date: set year, month, and day if you choose “Custom date”.

* Plot TR exponential trendline: show or hide the pink curve.

* Show stats table / Show Overall Return / Show Trendline stats: toggle what appears in the table.

3. Zoom and change timeframe as usual. The stats range is based on calendar time (YTD, 1Y, 5Y, etc.), not bar count, so the numbers stay meaningful as you change resolutions.

How to read the outputs

* Teal line: Nominal Total Return (using your chosen dividend mode).

* Orange line (if enabled): Real (inflation-adjusted) Total Return.

* Pink line (if enabled): Exponential trendline for the selected stats window.

On the right edge, small labels show the latest value of each active line.

In the bottom-right stats table:

* Overall Return: total percentage gain or loss over the chosen stats range.

* CAGR: the smoothed annual rate that would turn 1.0 into the current value over that range.

* Exponential Trendline: the average trendline growth per year and the R².

• R² near 1 means prices follow a clean exponential path.

• Lower R² means more noise or sideways movement around the trend.

* Range: which window those stats apply to (YTD, 1Y, 5Y, etc.).

* Since inception: overall return and CAGR from the first bar on the chart up to the latest bar, independent of the current stats range.

Use this when you want to compare true performance, not just price – especially for dividend-heavy ETFs, funds, and income strategies.

Уровни SL/TP и значение ATR первого часаSession Range SL/TP Levels with Advanced ATR

Overview

The Session Range SL/TP Levels indicator is a comprehensive tool designed for session-based trading strategies, particularly for breakouts. It identifies the high and low of a user-defined time range (e.g., the Asian session) and uses a sophisticated, customizable Average True Range (ATR) calculation to project key Stop Loss (SL) and Take Profit (TP) levels.

This indicator helps traders visualize potential entry and exit points based on the volatility of a specific trading session, with all crucial data presented in a clean on-screen table.

Key Features

Customizable Trading Session: Define any time range to establish your core trading zone. The indicator will automatically find the high and low of this period.

Advanced ATR Calculation: The indicator uses an ATR calculated on a 5-minute timeframe for higher precision. You can customize:

The ATR length and smoothing method (RMA, SMA, EMA, WMA).

A unique percentage reduction from the ATR to create a more conservative volatility buffer.

Volatility-Based SL/TP Levels: Automatically calculates and plots multiple SL and TP levels for both long and short scenarios based on user-defined multipliers of the modified ATR.

Comprehensive On-Screen Display: A detailed on-screen table provides all critical data at a glance, including:

The original 5-min ATR value.

The modified ATR after the percentage reduction.

Three custom ATR-multiple values for quick reference.

All calculated SL and TP price levels for both Long and Short setups.

Copy-Friendly Data Logging: With a single click in the settings, you can print all calculated values into the Pine Logs panel, allowing for easy copying and pasting into other applications or trading journals.

How to Use

Define Your Session: In the settings, enter the time for the trading session you want to analyze (e.g., "0200-0300" for a part of the Asian session).

Identify the Range: The indicator will draw the high and low of this session once the time period is complete.

Plan Your Trade: The calculated levels provide potential targets for breakout trades.

For a Long Trade: If the price breaks above the session high, the green Take Profit lines (TP1, TP2, TP3) serve as potential exit points, while the Stop Loss (Long) level serves as a volatility-based stop.

For a Short Trade: If the price breaks below the session low, the red Take Profit lines serve as potential targets, with the Stop Loss (Short) level as the corresponding stop.

Reference the Table: Use the on-screen table to see the exact price levels and ATR values without needing to hover over the lines.

Daily 50‑ & 200‑SMA Ceiling Radar — EnhancedDescription:

This custom TradingView indicator, developed by Trader Malik and licensed under Trades Per Minute, is a powerful visual tool for identifying how price behaves relative to major daily moving averages — the 50-SMA and 200-SMA. It helps traders quickly understand key technical dynamics such as trend alignment, MA proximity, and short-term momentum sentiment — all displayed on a clean, minimal overlay with visual alerts and an adjustable data table.

FEATURES

1. Daily 50 & 200 Simple Moving Averages (SMA):**

- Displayed directly on the chart using distinct blue and orange lines.

- These serve as primary trend filters and support/resistance zones.

2. Price Highlighting:

- A red background flashes momentarily when the price crosses either the 50-SMA or 200-SMA.

- A green background fills the chart when price is above both MAs (bullish zone).

- A red background persists if price is below both MAs (bearish zone).

3. MA Gap Analysis Table:

- 50-SMA Row**: Shows % gap between 50-SMA and 200-SMA.

- 200-SMA Row**: Shows % gap between 200-SMA and 50-SMA.

- Sentiment Row**: Displays short-term trend bias based on the slope of the past 7 daily closes — Bullish, Neutral, or Bearish.

USER SETTINGS

Table Location: Choose between **Top Right** or **Bottom Right** of the chart.

Table Size: Select **Small**, **Medium**, or **Large** to suit screen preferences and layout aesthetics.

This script is **intellectual property of Trades Per Minute** and distributed by **Trader Malik** for use under licensing terms. Redistribution or repurposing without authorization is strictly prohibited.

OBV Strength Relative to Volume (Lakhs View)OBV Strength Relative to Volume (Lakhs View)

Description:

to provide a compact yet powerful insight into volume momentum and price conviction. It's tailored for traders and analysts in markets like India, where high-volume stocks are often better interpreted in lakhs.

💡 Key Features:

OBV Calculation: Cumulative OBV is computed based on price movement direction and volume contribution.

OBV Strength (%): Measures the percentage strength of OBV relative to total volume over a user-defined period. It reflects how strongly volume is contributing to price movements.

Lakhs View: Both OBV and Volume are scaled to lakhs for cleaner readability and practical analysis in high-volume securities.

Historical Table Display:

Displays date-wise OBV, Volume, and OBV Strength for the last N candles (customizable).

Automatically updates every 5 bars or on each bar for real-time analysis.

Color-coded cells for quick visual recognition.

⚙️ Inputs:

OBV Strength Period: Number of bars used to calculate OBV strength (default = 5).

Number of Days in Table: Number of recent bars shown in the on-chart table (default = 5).

📈 Plots:

OBV (Lakhs) – Aqua line.

Volume (Lakhs) – Orange columns.

OBV Strength (%) – Green line indicating momentum strength based on volume.

📍 Ideal Use:

Use this indicator to:

Spot divergences between OBV and price.

Assess the strength of volume behind a trend.

Track consistency and spikes in volume-backed price moves.

Quickly scan recent trends with a clear numerical and visual table.

SignalWatcherThis script provides real-time monitoring of multiple technical indicators and generates visual alerts and configurable alarms:

Inputs & Mini-GUI

MACD Settings: Activation, fast, slow and signal line lengths.

RSI Settings: Activation, period length, overbought and oversold thresholds.

ADX Settings: Activation, period length, smoothing and trend strength thresholds.

Volume Settings: Activation, length of the volume MA, factor for detecting volume peaks.

Global Alert: A single composite alert for all signals.

Plot Settings: Activation and deactivation of the plot displays for RSI, MACD (lines) and ADX. Color and width selection for each line.

Display Table: Activation of the status table.

Calculations

MACD: Generates macdLine and signalLine, detects crossovers (bullish) and crossunders (bearish).

RSI: Calculates rsi_val, compares with rsi_ob and rsi_os to determine overbought/oversold.

ADX: Uses ta.dmi() to determine adx_val and checks against adx_thresh for trend strength.

Volume Spike: Exceptional trading activity detected by moving average (vol_ma) and factor (vol_factor).

Alert conditions

Six individual alertcondition() calls: MACD ↑/↓, RSI Overbought/Oversold, ADX Strong Trend, Volume Spike.

Optional composite alert (enable_global): A single notification when one of the indicator signals strikes.

Visual overlays

Alarm overlay (bottom right): Red table with text lines for currently triggered signals.

Status Table (bottom left): Overview of all indicators with current status (On/Off, Values, Thresholds).

Plots in the chart

RSI, MACD Line & Signal Line, ADX: Are displayed as lines if activated in the GUI; configurable colors & line thicknesses.

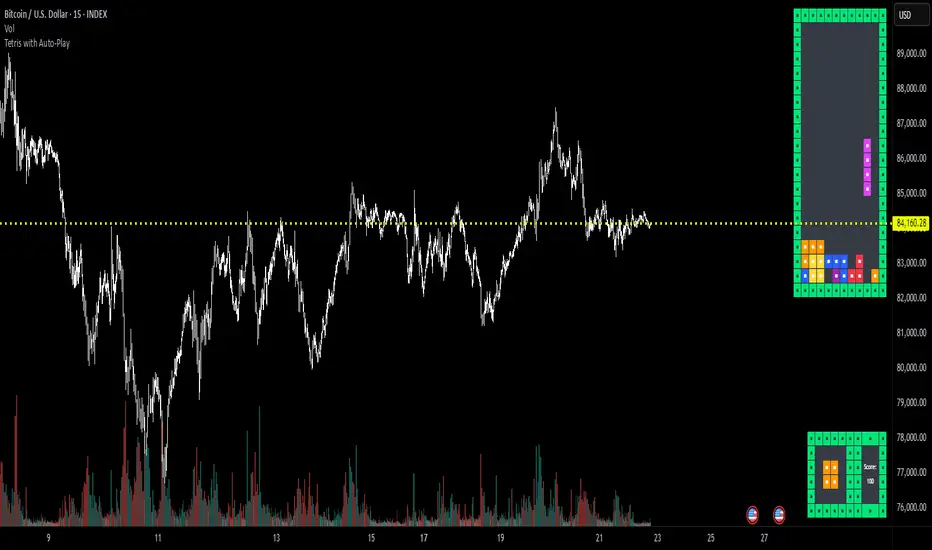

Tetris with Auto-PlayThis indicator is implemented in Pine Script™ v6 and serves as a demonstration of TradingView's capabilities. The core concept is to simulate a classic Tetris game by creating a grid-based environment and managing game state entirely within Pine Script.

Key Technical Aspects:

Grid Representation:

The script defines a custom grid structure using a user-defined type that holds the grid’s dimensions and a one-dimensional array to simulate a two-dimensional board. This structure is used to track occupied cells, clear full rows, and determine stack height.

Piece Management:

A second custom type is used to represent the state of a tetromino piece, including its type, rotation, and position. The code includes functions to calculate the block offsets for each tetromino based on its rotation state.

Collision Detection and Piece Locking:

Dedicated functions check for collisions against the grid borders and existing blocks. When a collision is detected during a downward move, the piece is locked into the grid, and any complete lines are cleared.

AIgo-Driven Placement:

The script incorporates a simple heuristic to determine the best placement for the next tetromino. It simulates different rotations and horizontal positions, evaluating each based on aggregated column height, cleared lines, holes, and bumpiness. This decision-making process is encapsulated in an AI-like function that returns the optimal rotation and placement.

Rendering Using Tables:

The visual representation is managed via TradingView’s table objects. The game board is rendered with a bordered layout, while a separate preview table displays the next piece and the current score. Each cell is updated with text and background colors that correspond to the state of the game.

Execution Flow and Timing:

The main execution loop handles real-time updates by dropping pieces at set intervals and checking for game-over conditions. The code leverages persistent variables and time comparisons to control game speed and manage transitions between piece drops.

Executing:

Add the indicator to the chart

It starts playing itself till game over

There are no parameters to change in this version but the grid in the code directly

p.s. Sadly we have no interactive buttons in the current pinescript versions to play ourself, but its about the possibilitys what we could do ;-)

Maybe in a future version there is more possible, if i find time to enhance and expand the idea

Have fun :-)

ROC + SMI Auto Adjust

This indicator combines the Rate of Change (ROC) and the Stochastic Momentum Index (SMI) with automatically adjusted parameters for different time frames (short, medium, long). It normalizes the ROC to match the SMI levels, displays the ROC as a histogram and the SMI as lines, highlights overbought/oversold zones and includes a settings table. Ideal for analyzing momentum on different time frames.

Key Features:

Automatic Parameter Adjustment:

The script detects the current chart time frame (e.g. 1-minute, 1-hour, daily) and adjusts the parameters for the ROC and SMI accordingly.

Parameters such as ROC length, SMI length and smoothing periods are optimized for short, medium and long term time frames.

Rate of Change (ROC):

ROC measures the percentage change in price over a specified period.

The script normalizes the ROC values to match the SMI range, making it easier to compare the two indicators on the same scale.

The ROC is displayed as a histogram, where positive values are colored green and negative values are colored red.

Stochastic Momentum Index (SMI):

SMI is a momentum oscillator that identifies overbought and oversold conditions.

The script calculates the SMI and its signal line, plotting them on the chart.

Overbought and oversold levels are displayed as dotted lines for convenience.

SMI and SMI Signal Crossover:

When the main SMI crosses the signal line from below upwards, it may be a buy signal (bullish signal).

When the SMI crosses the signal line from above downwards, it may be a sell signal (bearish signal).

Configurable Inputs:

Users can use the automatically adjusted settings or manually override the parameters (e.g. ROC length, SMI length, smoothing periods).

Overbought and oversold levels for SMI are also configurable.

Parameter Table:

A table is displayed on the chart showing the current parameters (e.g. timeframe, ROC length, SMI length) for transparency and debugging.

The position of the table is configurable (e.g. top left, bottom right).

How it works:

The script first detects the chart timeframe and classifies it as short-term (e.g. 1M, 5M), medium-term (e.g. 1H, 4H) or long-term (e.g. D1, W1).

Based on the timeframe, it sets default values for the ROC and SMI parameters.

ROC and SMI are calculated and normalized so that they can be compared on the same scale.

ROC is displayed as a histogram, while SMI and its signal line are displayed as lines.

Overbought and oversold levels are displayed as horizontal lines.

Use cases:

Trend identification: ROC helps to identify the strength of the trend, while SMI indicates overbought/oversold conditions.

Momentum analysis: The combination of ROC and SMI provides insight into both price momentum and potential reversals.

Time frame flexibility: The auto-adjustment feature makes the script suitable for scalping (short-term), swing trading (medium-term) and long-term investing.

MEMEQUANTMEMEQUANT

This script is a comprehensive and specialized tool designed for tracking trends and money flow within meme coins and DEX tokens. By combining various features such as trend lines, Fibonacci levels, and category-based indices, it helps traders make informed decisions in highly volatile markets.

Key Features:

1. Category-Based Indices:

• Tracks the performance of token categories like:

• AI Agent Tokens

• AI Tokens

• Animal Tokens

• Murad Picks

• Each category consists of leader tokens, which are selected based on their higher market cap and trading volume. These tokens act as benchmarks for their respective categories.

• Visualizes category indices in a line chart to identify trends and compare money flow between categories.

2. Fibonacci Correction Zones:

• Highlights key retracement levels (e.g., 60%, 70%, 80%).

• These levels are crucial for identifying potential reversal zones, commonly observed in meme coin trading patterns.

• Fully customizable to match individual trading strategies.

3. Trend Lines:

• Automatically detects major support and resistance levels.

• Separates long-term and short-term trend lines, allowing traders to focus on significant price movements.

4. Enhanced Info Table:

• Provides real-time insights, including:

• % Distance from All-Time High (ATH)

• Current Trading Volume

• 50-bar Average Volume

• Volume Change Percentage

• Displays information in an easy-to-read table on the chart.

5. Customizable Settings:

• Users can adjust transparency, colors, and ranges for Fibonacci zones, trend lines, and the table.

• Enables or disables individual features (e.g., Fibonacci, trend lines, table) based on preferences.

How It Works:

1. Tracking Money Flow Across Categories:

• The script calculates the market cap to volume ratio for each category of tokens to help identify the dominant trend.

• A higher ratio indicates greater liquidity and stability, while a lower ratio suggests higher volatility or price manipulation.

2. Identifying Retracement Patterns:

• Leverages common retracement behaviors (e.g., 70% correction levels) observed in meme coins to detect potential reversal zones.

• Combines this with trend line analysis for additional confirmation.

3. Leader Tokens as Indicators:

• Each category is represented by its leader tokens, which have historically higher liquidity and market cap. This allows the script to accurately reflect the overall trend in each category.

When to Use:

• Trend Analysis: To identify which category (e.g., AI Tokens or Animal Tokens) is leading the market.

• Reversal Zones: To spot potential support or resistance levels using Fibonacci zones.

• Money Flow: To understand how capital is moving across different token categories in real time.

Who Is This For?

This script is tailored for:

• Traders specializing in meme coins and DEX tokens.

• Those looking for an edge in trend-based trading by analyzing market cap, volume, and retracement levels.

• Anyone aiming to track money flow dynamics between different token categories.

Future Updates:

This is the initial version of the script. Future updates may include:

• Support for additional token categories and DEX data.

• More advanced pattern recognition and alerts for volume and price anomalies.

• Enhanced visualization for historical data trends.

With this tool, traders can combine money flow analysis with the 60-70% retracement strategy, turning it into a powerful assistant for navigating the fast-paced world of meme coins and DEX tokens.

This script is designed to provide meaningful insights and practical utility for traders, adhering to TradingView’s standards for originality, clarity, and user value.

Market Movement After OpenDescription:

This script provides a detailed visualization of market movements during key trading hours: the German market opening (08:00–09:00 UTC+1) and the US market opening (15:30–16:30 UTC+1). It is designed to help traders analyze price behavior in these critical trading periods by capturing and presenting movement patterns and trends directly on the chart and in an interactive table.

Key Features:

Market Movement Analysis:

Tracks the price movement during the German market's first hour (08:00–09:00 UTC+1) and the US market's opening session (15:30–16:30 UTC+1).

Analyzes whether the price moved up or down during these intervals.

Visual Representation:

Dynamically colored price lines indicate upward (green) or downward (red) movement during the respective periods.

Labels ("DE" for Germany and "US" for the United States) mark key moments in the chart.

Historical Data Table:

Displays the past 10 trading days' movement trends in an interactive table, including:

Date: Trading date.

German Market Movement: Up (▲), Down (▼), or Neutral (-) for 08:00–09:00 UTC+1.

US Market Movement: Up (▲), Down (▼), or Neutral (-) for 15:30–16:30 UTC+1.

The table uses color coding for easy interpretation: green for upward movements, red for downward, and gray for neutral.

Real-Time Updates:

Automatically updates during live trading sessions to reflect the most recent movements.

Highlights incomplete periods (e.g., ongoing sessions) to indicate their status.

Customizable:

Suitable for intraday analysis or broader studies of market trends.

Designed to overlay directly on any price chart.

Use Case:

This script is particularly useful for traders who focus on market openings, which are often characterized by high volatility and significant price movements. By providing a clear visual representation of historical and live data, it aids in understanding and capitalizing on market trends during these critical periods.

Notes:

The script works best when the chart is set to the appropriate timezone (UTC+1 for the German market or your local equivalent).

For precise trading decisions, consider combining this script with other technical indicators or trading strategies.

Feel free to share feedback or suggest additional features to enhance the script!

Adapted RSI w/ Multi-Asset Regime Detection v1.1The relative strength index (RSI) is a momentum indicator used in technical analysis. RSI measures the speed and magnitude of an asset's recent price changes to detect overbought or oversold conditions in the price of said asset.

In addition to identifying overbought and oversold assets, the RSI can also indicate whether your desired asset may be primed for a trend reversal or a corrective pullback in price. It can signal when to buy and sell.

The RSI will oscillate between 0 and 100. Traditionally, an RSI reading of 70 or above indicates an overbought condition. A reading of 30 or below indicates an oversold condition.

The RSI is one of the most popular technical indicators. I intend to offer a fresh spin.

Adapted RSI w/ Multi-Asset Regime Detection

Our Adapted RSI makes necessary improvements to the original Relative Strength Index (RSI) by combining multi-timeframe analysis with multi-asset monitoring and providing traders with an efficient way to analyse market-wide conditions across different timeframes and assets simultaneously. The indicator automatically detects market regimes and generates clear signals based on RSI levels, presenting this data in an organised, easy-to-read format through two dynamic tables. Simplicity is key, and having access to more RSI data at any given time, allows traders to prepare more effectively, especially when trading markets that "move" together.

How we calculate the RSI

First, the RSI identifies price changes between periods, calculating gains and losses from one look-back period to the next. This look-back period averages gains and losses over 14 periods, which in this case would be 14 days, and those gains/losses are calculated based on the daily closing price. For example:

Average Gain = Sum of Gains over the past 14 days / 14

Average Loss = Sum of Losses over the past 14 days / 14

Then we calculate the Relative Strength (RS):

RS = Average Gain / Average Loss

Finally, this is converted to the RSI value:

RSI = 100 - (100 / (1 + RS))

Key Features

Our multi-timeframe RSI indicator enhances traditional technical analysis by offering synchronised Daily, Weekly, and Monthly RSI readings with automatic regime detection. The multi-asset monitoring system allows tracking of up to 10 different assets simultaneously, with pre-configured major pairs that can be customised to any asset selection. The signal generation system provides clear market guidance through automatic regime detection and a five-level signal system, all presented through a sophisticated visual interface with dynamic RSI line colouring and customisable display options.

Quick Guide to Use it

Begin by adding the indicator to your chart and configuring your preferred assets in the "Asset Comparison" settings.

Position the two information tables according to your preference.

The main table displays RSI analysis across three timeframes for your current asset, while the asset table shows a comparative analysis of all monitored assets.

Signals are colour-coded for instant recognition, with green indicating bullish conditions and red for bearish conditions. Pay special attention to regime changes and signal transitions, using multi-timeframe confluence to identify stronger signals.

How it Works (Regime Detection & Signals)

When we say 'Regime', a regime is determined by a persistent trend or in this case momentum and by leveraging this for RSI, which is a momentum oscillator, our indicator employs a relatively simple regime detection system that classifies market conditions as either Bullish (RSI > 50) or Bearish (RSI < 50). Our benchmark between a trending bullish or bearish market is equal to 50. By leveraging a simple classification system helps determine the probability of trend continuation and the weight given to various signals. Whilst we could determine a Neutral regime for consolidating markets, we have employed a 'neutral' signal generation which will be further discussed below...

Signal generation occurs across five distinct levels:

Strong Buy (RSI < 15)

Buy (RSI < 30)

Neutral (RSI 30-70)

Sell (RSI > 70)

Strong Sell (RSI > 85)

Each level represents different market conditions and probability scenarios. For instance, extreme readings (Strong Buy/Sell) indicate the highest probability of mean reversion, while neutral readings suggest equilibrium conditions where traders should focus on the overall regime bias (Bullish/Bearish momentum).

This approach offers traders a new and fresh spin on a popular and well-known tool in technical analysis, allowing traders to make better and more informed decisions from the well presented information across multiple assets and timeframes. Experienced and beginner traders alike, I hope you enjoy this adaptation.

Trend Signals with TP & SL [UAlgo] StrategyThe "Trend Signals with TP & SL Strategy" is a trading strategy designed to capture trend continuation signals while incorporating sophisticated risk management techniques. This strategy is tailored for traders who wish to capitalize on trending market conditions with precise entry and exit points, automatically calculating Take Profit (TP) and Stop Loss (SL) levels based on either Average True Range (ATR) or percentage values. The strategy aims to enhance trade management by preventing multiple simultaneous positions and dynamically adapting to changing market conditions.

This strategy is highly configurable, allowing traders to adjust sensitivity, the ATR calculation method, and the cloud moving average length. Additionally, the strategy can display buy and sell signals directly on the chart, along with visual representation of entry points, stop losses, and take profits. It also features a cloud-based trend analysis using a MACD-driven color fill that indicates the strength and direction of the trend.

🔶 Key Features

Configurable Trend Continuation Signals:

Source Selection: The strategy uses the midpoint of the high-low range as the default source, but it is adjustable.

Sensitivity: The sensitivity of the trend signals can be adjusted using a multiplier, ranging from 0.5 to 5.

ATR Calculation: The strategy allows users to choose between two ATR calculation methods for better adaptability to different market conditions.

Cloud Moving Average: Traders can adjust the cloud moving average length, which is used in conjunction with MACD to provide a visual trend indication.

Take Profit & Stop Loss Management:

ATR-Based or Percent-Based: The strategy offers flexibility in setting TP and SL levels, allowing traders to choose between ATR-based multipliers or fixed percentage values.

Dynamic Adjustment: TP and SL levels are dynamically adjusted according to the selected method, ensuring trades are managed based on real-time market conditions.

Prevention of Multiple Positions:

Single Position Control: To reduce risk and enhance strategy reliability, the strategy includes an option to prevent multiple positions from being opened simultaneously.

Visual Trade Indicators:

Buy/Sell Signals: Clearly displays buy and sell signals on the chart for easy interpretation.

Entry, SL, and TP Lines: Draws lines for entry price, stop loss, and take profit directly on the chart, helping traders to monitor trades visually.

Trend Cloud: A color-filled cloud based on MACD and the cloud moving average provides a visual cue of the trend’s direction and strength.

Performance Summary Table:

In-Chart Statistics: A table in the top right of the chart displays key performance metrics, including total trades, wins, losses, and win rate percentage, offering a quick overview of the strategy’s effectiveness.

🔶 Interpreting the Indicator

Trend Signals: The strategy identifies trend continuation signals based on price action relative to an ATR-based threshold. A buy signal is generated when the price crosses above a key level, indicating an uptrend. Conversely, a sell signal occurs when the price crosses below a level, signaling a downtrend.

Cloud Visualization: The cloud, derived from MACD and moving averages, changes color to reflect the current trend. A positive cloud in aqua suggests an uptrend, while a red cloud indicates a downtrend. The transparency of the cloud offers further nuance, with more solid colors denoting stronger trends.

Entry and Exit Management: Once a trend signal is generated, the strategy automatically sets TP and SL levels based on your chosen method (ATR or percentage). The stop loss and take profit lines will appear on the chart, showing where the strategy will exit the trade. If the price reaches either the SL or TP, the trade is closed, and the respective line is deleted from the chart.

Performance Metrics: The strategy’s performance is tracked in real-time with an in-chart table. This table provides essential information about the number of trades executed, the win/loss ratio, and the overall win rate. This information helps traders assess the strategy's effectiveness and make necessary adjustments.

This strategy is designed for those who seek to engage with trending markets, offering robust tools for entry, exit, and overall trade management. By understanding and leveraging these features, traders can potentially improve their trading outcomes and risk management.

🔷 Related Script

🔶 Disclaimer

Use with Caution: This indicator is provided for educational and informational purposes only and should not be considered as financial advice. Users should exercise caution and perform their own analysis before making trading decisions based on the indicator's signals.

Not Financial Advice: The information provided by this indicator does not constitute financial advice, and the creator (UAlgo) shall not be held responsible for any trading losses incurred as a result of using this indicator.

Backtesting Recommended: Traders are encouraged to backtest the indicator thoroughly on historical data before using it in live trading to assess its performance and suitability for their trading strategies.

Risk Management: Trading involves inherent risks, and users should implement proper risk management strategies, including but not limited to stop-loss orders and position sizing, to mitigate potential losses.

No Guarantees: The accuracy and reliability of the indicator's signals cannot be guaranteed, as they are based on historical price data and past performance may not be indicative of future results.

Stef's Dollar Volume CounterStef's Dollar Volume Counter is my second script that I've worked on and coded. I am proud of this script because it does something very, very important: it counts the AMOUNT of money traded, not just the amount shares/contracts traded. This is key for understanding where the big and small money is.

This script is totally different from other Volume scripts because it shows the amount of money traded, NOT the shares/contracts/coins etc. Also, more importantly, it is different from other volume indicators in the same space because this script is specifically focused on showcasing specific dollar volume amounts either as a table or as a label.

Here are the 5 key features you can utilize with this:

1. Customizable Gradient Colors for BIG money and SMALL money: Visually distinguishes between high and low dollar volumes. Change the colors as needed in the indicator settings menu.

2. Dollar Volume Counter Table: Positioned at the bottom right of the chart, this table provides quick insights into the highest, lowest, and average dollar volumes over a specified period. You can customize the time period in the settings menu.

3. "Wow! Much Money!" Labels: Highlights the top three recent highest dollar volumes within the visible chart area, emphasizing significant trading periods. Also, it's hilarious :)

4. Customize the period for volume analysis, ranging from 1 to 12 months or more, with the selected timeframe displayed in the table.

5. It opens as a new pane below the chart so that you can still analyze price and more, as needed.

Thanks for reading! I look forward to hearing your feedback. This script will be updated to expand on more concepts and I'll add some cool features soon.

Advanced Technical Range and Expectancy Estimator [SS]Hello everyone,

This indicator is a from of momentum based probability modelling. It is derived from my own approaches to probability modelling but just simplified a bit.

How it works:

The indicator looks at various technical, including stochastics, RSI, MFI and Z-Score, to determine the likely sentiment. All of these, with the exception of Z-Score, are momentum based indicators and can alert us to likely sentiment. However, instead of us making the subjective determination ourselves as to whether the RSI or MFI or Stochastics are bullish, the indicator will look at previous instances of these occurrences, and tally the bullish and bearish follow throughs that happened. It will also calculate the average target price that was hit, under similar conditions, on the same timeframe.

The Z-Score is your "tie breaker". It is not a momentum based indicator and measures something a little different (the standard deviation and over-extension of the stock). For this reason, it provides an alternative assessment and tends to be a bit more reliable in times of low momentum.

Back-test Results:

The indicator back-tests itself over the previous 100 candles. I have limited it to 100 candles for pragmatic considerations (it has to back-test each technical individually and increasing the BT length will slow and potentially error out the indicator) as well as accuracy considerations.

One thing I have noticed in my years of trying to crack the code and develop probability models for tickers, is historical accuracy doesn't always matter because sentiment is always changing. You need to see what it has done over the most recent 100 to 200 candles.

There are two back-test windows, one for the price targets and the other for the sentiment accuracy. The most effective/most accurate will highlight green, the least effective/least accurate will highlight red:

In the image above, you can see that the most accurate predictor of sentiment is Z-Score, with a 90.32% accuracy rate over the past 100 candles.

The most accurate predictor of price is MFI, with a 60% (for bull targets) and 42% (for bear targets)accuracy rate.

Anchoring Points:

The indicator permits you to anchor by two points. The default setting is anchoring by previous candle. If you plan to use this as an oscillator, to see the current prediction for the current candle you are viewing, then you will need to leave this default setting. It will pull the data from the previous candle and give you the data for the current candle you are on.

If you are assess the likely sentiment for the next day after the day has closed off, you will want to anchor by current candle. This will take the current technicals that the day has closed off with and run the assessment for you.

Customizability

You can customize the technicals by source and length of assessment.

They are all defaulted to the traditional settings of these indicators, but if you want to customize your model to try and improve or enhance accuracy in one way or another, you are free and able to do so!

I do suggest leaving the defaults as they seem to work particular well :-).

Thresholds

Thresholds are the tolerance levels that we permit for our technical search range. If you want them to be exactly identical, then you can set it to 0. If you want it to be extremely similar, you can set it to 0.01. This will hone in on the ranges you are interest in and you can see how it affects your accuracy by reviewing the results in the back-test tables.

Keep Static Colour Option

I want to make a quick note on the "Keep Static Colour" option that is in your settings menu.

The primary table that shows you the probability and price targets change colours based on the accuracy of the assessment. This is so, if you are using a mobile device or smaller screen and can't have the back-test results open at the same time, you can see still which are the most reliable results. However, if you have the back-test tables open and you find these colour changes too distracted, you can toggle on the "Keep Static Colour" and it will resort the colour of the table to a solid white:

Show Technicals

The indicator can show you the current technical values if you are using it in place of an oscillator. Its less pivotal as its making the assessment for you, but just for your reference if you want to see what the current MFI, Z-Score or Stochastics etc. are, you have that option as well.

All Timeframes Permitted

You can view Weekly, Monthly, Hourly, 5 minute, 1 minute, its all supported!

That's the indicator in a nutshell.

Hope you enjoy and leave your questions below.

Safe trades everyone!

Supertrend Forecast - vanAmsenHello everyone!

I am thrilled to present the "vanAmsen - Supertrend Forecast", an advanced tool that marries the simplicity of the Supertrend with comprehensive statistical insights.

Before we dive into the functionalities of this indicator, it's essential to understand its foundation and theory.

The Theory:

What exactly is the Supertrend?

The Supertrend, at its core, is a momentum oscillator. It's a tool that provides buy and sell signals based on the prevailing market trend. The underlying principle is straightforward: by analyzing average price data and volatility over a period, the Supertrend gives us a line that represents the trend direction.

However, trading isn't just about identifying trends; it's about understanding their strength, potential profitability, and historical accuracy. This is where statistics come into play. By incorporating statistical analysis into the Supertrend, we can gain deeper insights into the market's behavior.

Description:

The "vanAmsen - Supertrend Forecast" isn't just another Supertrend indicator. It's a comprehensive tool designed to offer traders a holistic view of market trends, backed by robust statistical analysis.

Key Features:

- Supertrend Line: A visual representation of the current market direction.

- Win Rate & Expected Return: Delve into the historical accuracy and profitability of the prevailing trend.

- Average Percentage Change: Understand the average price fluctuation for both winning and losing trends.

- Forecast Lines: Project future price movements based on historical data, providing a roadmap for potential scenarios.

- Interactive Table: A concise table in the top right, offering a snapshot of all vital metrics at a glance.

Usage:

- The bullish Supertrend line adopts an Aqua hue, indicating potential upward momentum.

- In contrast, the bearish line is painted in Orange, suggesting potential downtrends.

- Customize your chart by toggling labels, tables, and lines according to preference.

Recommendation:

The "vanAmsen - Supertrend Forecast" is undoubtedly a powerful tool in a trader's arsenal. However, it's imperative to combine it with other technical analysis tools and sound risk management practices. It's always prudent to backtest strategies with historical data before embarking on live trading.

Time Series Model IndicatorHello,

I am releasing this time series modelling indicator.

Brief overview of the indicator's functionality:

The Time Series Model indicator is a technical analysis tool that calculates and visualizes a linear regression line based on historical price data. It assesses the trend direction and provides an outer band around the regression line to indicate potential support and resistance levels. The indicator also detects outliers in the price data and calculates correlations between the time variable and the closing price. It offers various customization options such as input length, user-defined hours in advance, display settings for tables and fills, and the ability to show variable correlations. Overall, this indicator aims to help traders identify trends, potential reversals, and price extremes in a given time series.

Specific Functions:

Slope Calculations: The indicator calculates the slope and intercept of the regression line using the specified length of assessment (user defined). It also computes the residuals, standard error of the regression, and the upper and lower bounds of the standard error region. Additionally, it calculates multiple standard deviation bands around the regression line. The slope will change to green if the stock is in an uptrend and to red if the stock is in a downtrend.

Outliers: This feature detects extreme positive and negative outliers based on the z-score calculated from the price data. It highlights the outliers with a red background color to red if this option is selected.

Correlation to Time Assessments: This feature performs trend assessments based on the correlation between time and price data. It identifies uptrends, downtrends, falling trends, rising trends, etc.

Outerband Plots: This feature plots the regression line, standard error bands, and multiple standard deviation bands around the regression line. It also fills the areas between these lines.

Trend Assessment: This feature further assesses the trend based on the strength of the correlation. It identifies strong up or down trends, moderate trends, weak trends, no trend, etc.