Chaithanya Tattva Volume Zones📜 "Chaitanya Tattva" Volume Zones:-

A Sacred Framework of Supply, Demand & Market Energy

In the world of financial markets, price is said to reflect all information. But the true pulse of the market — its life force, its intent, and its moment of truth — is most vividly expressed not in price itself, but in volume.

Chaitanya Tattva Volume Zones is a spiritually inspired volume-based tool that transforms your chart into a canvas of market consciousness, revealing moments where supply and demand engage in visible energetic spikes. These moments are often disguised as ordinary candles, but with this tool, you uncover zones of intent — footprints left by the market’s deeper intelligence.

🌟 Why “Chaitanya Tattva”?

Chaitanya (चैतन्य) is a Sanskrit word meaning consciousness, awareness, or the spark of life energy. It is that which animates — the subtle intelligence behind all movement.

Tattva (तत्त्व) refers to essence, truth, or the underlying principle of a thing. In classical yogic philosophy, the tattvas are the elemental building blocks of reality.

Together, Chaitanya Tattva represents the conscious essence — the living pulse that animates the market through volume surges and imbalances.

This tool is not just a technical indicator — it is a spiritual observation device that aligns with the rhythm of volume and price action. It doesn't predict the market. It reveals when the market has already spoken — loudly, clearly, and energetically.

📈 What Does the Tool Do?

Chaitanya Tattva Volume Zones identifies exceptional volume spikes within the recent price history and visually marks the areas where market intent has been most active.

Specifically, the tool:

Scans for volume spikes that exceed all the volume of the last N bars (default is 20)

Confirms whether the spike happened on a bullish candle (close > open) or bearish candle (close < open)

For a bullish spike, it marks a Supply Zone — the area between the high and close of the candle

For a bearish spike, it marks a Demand Zone — the area between the low and close

Visually paints these zones with soft translucent boxes (red for supply, green for demand) that extend forward across multiple bars

🧘♂️ The Spiritual Framework

🔴 Supply = "Agni" — The Fire of Expansion

When a bullish candle erupts with historically high volume, it symbolizes the fire (Agni) of market optimism and upward expansion. It means that buyers have absorbed available supply at that level and established dominance — but such fire may also signal exhaustion, making it a potential supply barrier if price returns.

These Supply Zones are areas where:

Sellers are likely to re-engage

Smart money may be unloading

Future resistance can be anticipated

But unlike traditional indicators, this tool doesn’t guess. It reacts only to a clear volume-based event — when market energy surges — and locks in that awareness through zone marking.

🟢 Demand = "Prithvi" — The Grounding of Price

On the other hand, a bearish candle with extremely high volume represents the Earth (Prithvi) — grounding the price with firm hands. A strong volume drop often means buyers are stepping in, absorbing the selling pressure.

These Demand Zones are areas where:

Buying interest is proven

Market memory is stored

Future support can be expected

By respecting these zones, you're aligning your trading with natural market boundaries — not theoretical ones.

🧠 How Is It Different from Regular Volume Tools?

While most volume indicators show bars on a lower panel, they leave interpretation up to the trader. “High” or “low” becomes subjective.

Chaitanya Tattva Volume Zones is different:

It quantifies "spike": a bar must exceed all previous N volumes

It qualifies the intent: was the spike bullish or bearish?

It marks zones on the price chart: no need to guess levels

It preserves market memory: the zones persist visually for easy reference

In essence, this tool doesn’t just report volume — it interprets volume’s context and visually encodes it into the chart.

🧘 How to Use

1. Support/Resistance Mapping

Use the tool to understand where volume proved itself. If price revisits a red zone, expect possible rejection (resistance). If price revisits a green zone, expect possible absorption (support).

2. Entry Triggers

You may enter:

Long near demand zones if bullish confirmation appears

Short near supply zones if bearish confirmation appears

3. Stop Placement

Stops can be placed just beyond the zone boundary to align with areas where smart money historically defended.

4. Breakout Confidence

When price breaks through one of these zones with momentum, it often signals a new energetic wave — the old balance has been overcome.

🔔 Key Features

Volume spike detection across any timeframe

Clear visual zones — no clutter, no lag

Highly customizable: zone width, volume lookback, colors

Philosophy-aligned with supply and demand theory, Wyckoff, and Order Flow

🌌 A Metaphysical View of Volume

In yogic science, volume is akin to Prana — life-force energy. A market is not moved by price alone but by intent, force, and participation — all encoded in volume.

Just as a human body pulses with blood when action intensifies, the market pulses with volume when institutional decisions are made.

These pulses become sacred footprints — and Chaitanya Tattva Volume Zones helps you walk mindfully among them.

🔮 Final Thoughts

In a sea of indicators that shout at you with every tick, Chaitanya Tattva is calm. It speaks only when energy concentrates, only when the market sends a signal born of intent.

It doesn’t predict.

It doesn’t repaint.

It simply shows the truth, when the truth becomes undeniable.

Like a sage that speaks only when needed, it waits for volume to prove itself — then draws a memory into space, a zone where traders can re-align their actions with what the market has already honored.

Use it not just to trade —

But to listen.

To observe.

To follow the Chaitanya — the conscious pulse of the market’s own breath.

"META股价历史数据" için komut dosyalarını ara

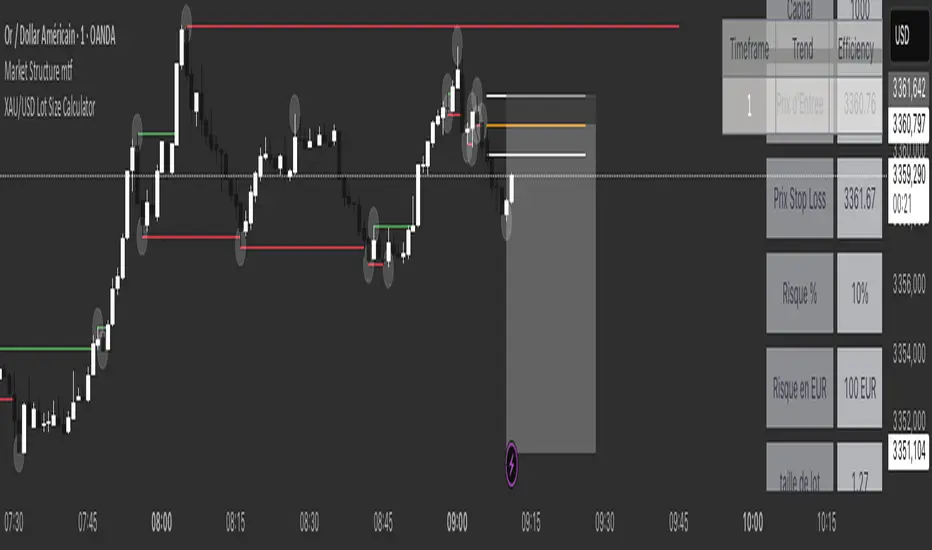

XAU/USD Lot Size CalculatorThis indicator automatically calculates the optimal lot size for XAUUSD (gold) based on the level of risk the trader wants to take. It is designed for traders using MetaTrader 4 or 5 and helps adjust position size according to the specific volatility of gold. The user can set the percentage of capital they are willing to risk on a single trade, for example 1%. The indicator also takes into account the stop loss level, which can be entered in pips or in dollars, as well as the account size (balance or equity).

Based on these parameters, it calculates the exact lot size that matches the risk amount. It then displays on the chart the recommended lot size, the risk amount in dollars, the pip value for XAUUSD, and a confirmation of the stop loss level. This type of indicator is useful for maintaining disciplined risk management and avoiding position sizing errors, especially on a highly volatile asset like gold.

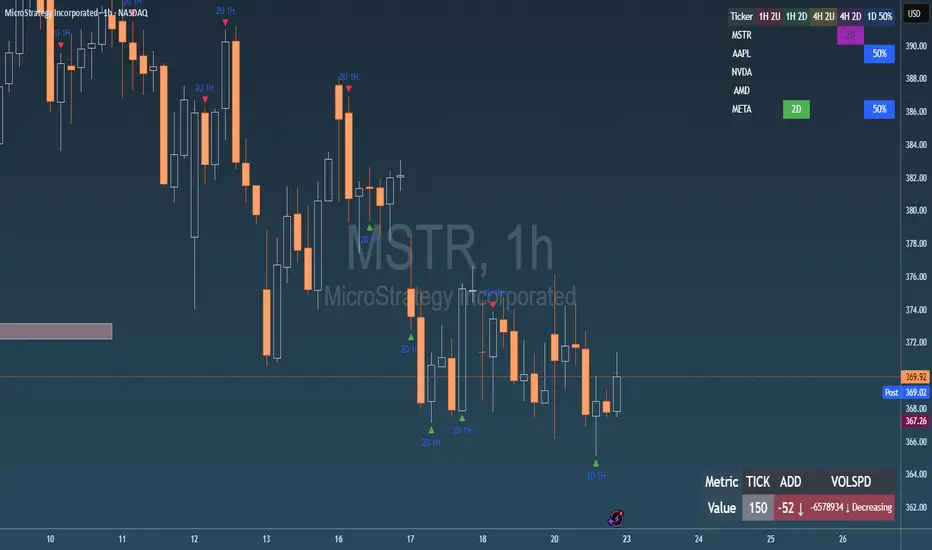

Failed 2U/2D + 50% Retrace Scanner📈 Multi-Ticker Failed 2U/2D Scanner with Daily Retrace & Market Breadth Table

This TradingView indicator is a multi-symbol price action scanner designed to catch high-probability reversal signals using The Strat’s failed 2U/2D patterns and daily 50% retrace logic, while also displaying market breadth metrics ( USI:TICK and USI:ADD ) for context.

Monitored Symbols:

SPY, SPX, QQQ, IWM, NVDA, AMD, AAPL, META, MSTR

🔍 Detection Logic

1. Failed 2U / Failed 2D Setups

Failed 2U: Price breaks above the previous candle’s high but closes back below the open → Bearish reversal

Failed 2D: Price breaks below the previous candle’s low but closes back above the open → Bullish reversal

Timeframes Monitored:

🕐 1-Hour (1H)

⏰ 4-Hour (4H)

2. Daily 50% Candle Retrace

Checks if price has retraced 50% or more of the previous day’s candle body

Highlights potential trend exhaustion or reversal confluence

3. Market Breadth Metrics (Display Only)

USI:TICK : Measures real-time NYSE up vs. down ticks

USI:ADD : Advance-Decline Line (net advancing stocks)

Not used in signal logic — just displayed in the table for overall market context

🖼️ Visual Elements

✅ Chart Markers

🔺 Red/Green Arrows for 1H Failed 2U/2D

🟨 Yellow Squares for 4H Failed 2U/2D

Visual markers are plotted directly on the relevant candles

📊 Signal Table

Lists all 9 tickers in rows

Columns for:

1H Signal

4H Signal

Daily 50% Retrace

USI:TICK Value

USI:ADD Value

Color-Coded Cells:

🔴 Red = Failed 2U

🟢 Green = Failed 2D

⚠️ Highlight if 50% Daily Retrace condition is true

🟦 Neutral-colored cells for TICK/ADD numeric display

🔔 Alerts

Hardcoded alerts fire when:

A 1H or 4H Failed 2U/2D is detected

The Daily 50% retrace condition is met

Each alert is labeled clearly by symbol and timeframe:

"META 4H Failed 2D"

"AAPL Daily 50% Retrace"

🎯 Use Case

Built for:

Reversal traders using The Strat

Swing or intraday traders watching hourly setups

Traders wanting quick visual context on market breadth without relying on it for confirmation

Monitoring multiple tickers in one clean view

This is scan 2

Add scan 1 for spx, spy, iwm, qqq, aapl

This indicator is not financial advice. Use the alerts to check out chart and when tickers trigger.

Ergodic Market Divergence (EMD)Ergodic Market Divergence (EMD)

Bridging Statistical Physics and Market Dynamics Through Ensemble Analysis

The Revolutionary Concept: When Physics Meets Trading

After months of research into ergodic theory—a fundamental principle in statistical mechanics—I've developed a trading system that identifies when markets transition between predictable and unpredictable states. This indicator doesn't just follow price; it analyzes whether current market behavior will persist or revert, giving traders a scientific edge in timing entries and exits.

The Core Innovation: Ergodic Theory Applied to Markets

What Makes Markets Ergodic or Non-Ergodic?

In statistical physics, ergodicity determines whether a system's future resembles its past. Applied to trading:

Ergodic Markets (Mean-Reverting)

- Time averages equal ensemble averages

- Historical patterns repeat reliably

- Price oscillates around equilibrium

- Traditional indicators work well

Non-Ergodic Markets (Trending)

- Path dependency dominates

- History doesn't predict future

- Price creates new equilibrium levels

- Momentum strategies excel

The Mathematical Framework

The Ergodic Score combines three critical divergences:

Ergodic Score = (Price Divergence × Market Stress + Return Divergence × 1000 + Volatility Divergence × 50) / 3

Where:

Price Divergence: How far current price deviates from market consensus

Return Divergence: Momentum differential between instrument and market

Volatility Divergence: Volatility regime misalignment

Market Stress: Adaptive multiplier based on current conditions

The Ensemble Analysis Revolution

Beyond Single-Instrument Analysis

Traditional indicators analyze one chart in isolation. EMD monitors multiple correlated markets simultaneously (SPY, QQQ, IWM, DIA) to detect systemic regime changes. This ensemble approach:

Reveals Hidden Divergences: Individual stocks may diverge from market consensus before major moves

Filters False Signals: Requires broader market confirmation

Identifies Regime Shifts: Detects when entire market structure changes

Provides Context: Shows if moves are isolated or systemic

Dynamic Threshold Adaptation

Unlike fixed-threshold systems, EMD's boundaries evolve with market conditions:

Base Threshold = SMA(Ergodic Score, Lookback × 3)

Adaptive Component = StDev(Ergodic Score, Lookback × 2) × Sensitivity

Final Threshold = Smoothed(Base + Adaptive)

This creates context-aware signals that remain effective across different market environments.

The Confidence Engine: Know Your Signal Quality

Multi-Factor Confidence Scoring

Every signal receives a confidence score based on:

Signal Clarity (0-35%): How decisively the ergodic threshold is crossed

Momentum Strength (0-25%): Rate of ergodic change

Volatility Alignment (0-20%): Whether volatility supports the signal

Market Quality (0-20%): Price convergence and path dependency factors

Real-Time Confidence Updates

The Live Confidence metric continuously updates, showing:

- Current opportunity quality

- Market state clarity

- Historical performance influence

- Signal recency boost

- Visual Intelligence System

Adaptive Ergodic Field Bands

Dynamic bands that expand and contract based on market state:

Primary Color: Ergodic state (mean-reverting)

Danger Color: Non-ergodic state (trending)

Band Width: Expected price movement range

Squeeze Indicators: Volatility compression warnings

Quantum Wave Ribbons

Triple EMA system (8, 21, 55) revealing market flow:

Compressed Ribbons: Consolidation imminent

Expanding Ribbons: Directional move developing

Color Coding: Matches current ergodic state

Phase Transition Signals

Clear entry/exit markers at regime changes:

Bull Signals: Ergodic restoration (mean reversion opportunity)

Bear Signals: Ergodic break (trend following opportunity)

Confidence Labels: Percentage showing signal quality

Visual Intensity: Stronger signals = deeper colors

Professional Dashboard Suite

Main Analytics Panel (Top Right)

Market State Monitor

- Current regime (Ergodic/Non-Ergodic)

- Ergodic score with threshold

- Path dependency strength

- Quantum coherence percentage

Divergence Metrics

- Price divergence with severity

- Volatility regime classification

- Strategy mode recommendation

- Signal strength indicator

Live Intelligence

- Real-time confidence score

- Color-coded risk levels

- Dynamic strategy suggestions

Performance Tracking (Left Panel)

Signal Analytics

- Total historical signals

- Win rate with W/L breakdown

- Current streak tracking

- Closed trade counter

Regime Analysis

- Current market behavior

- Bars since last signal

- Recommended actions

- Average confidence trends

Strategy Command Center (Bottom Right)

Adaptive Recommendations

- Active strategy mode

- Primary approach (mean reversion/momentum)

- Suggested indicators ("weapons")

- Entry/exit methodology

- Risk management guidance

- Comprehensive Input Guide

Core Algorithm Parameters

Analysis Period (10-100 bars)

Scalping (10-15): Ultra-responsive, more signals, higher noise

Day Trading (20-30): Balanced sensitivity and stability

Swing Trading (40-100): Smooth signals, major moves only Default: 20 - optimal for most timeframes

Divergence Threshold (0.5-5.0)

Hair Trigger (0.5-1.0): Catches every wiggle, many false signals

Balanced (1.5-2.5): Good signal-to-noise ratio

Conservative (3.0-5.0): Only extreme divergences Default: 1.5 - best risk/reward balance

Path Memory (20-200 bars)

Short Memory (20-50): Recent behavior focus, quick adaptation

Medium Memory (50-100): Balanced historical context

Long Memory (100-200): Emphasizes established patterns Default: 50 - captures sufficient history without lag

Signal Spacing (5-50 bars)

Aggressive (5-10): Allows rapid-fire signals

Normal (15-25): Prevents clustering, maintains flow

Conservative (30-50): Major setups only Default: 15 - optimal trade frequency

Ensemble Configuration

Select markets for consensus analysis:

SPY: Broad market sentiment

QQQ: Technology leadership

IWM: Small-cap risk appetite

DIA: Blue-chip stability

More instruments = stronger consensus but potentially diluted signals

Visual Customization

Color Themes (6 professional options):

Quantum: Cyan/Pink - Modern trading aesthetic

Matrix: Green/Red - Classic terminal look

Heat: Blue/Red - Temperature metaphor

Neon: Cyan/Magenta - High contrast

Ocean: Turquoise/Coral - Calming palette

Sunset: Red-orange/Teal - Warm gradients

Display Controls:

- Toggle each visual component

- Adjust transparency levels

- Scale dashboard text

- Show/hide confidence scores

- Trading Strategies by Market State

- Ergodic State Strategy (Primary Color Bands)

Market Characteristics

- Price oscillates predictably

- Support/resistance hold

- Volume patterns repeat

- Mean reversion dominates

Optimal Approach

Entry: Fade moves at band extremes

Target: Middle band (equilibrium)

Stop: Just beyond outer bands

Size: Full confidence-based position

Recommended Tools

- RSI for oversold/overbought

- Bollinger Bands for extremes

- Volume profile for levels

- Non-Ergodic State Strategy (Danger Color Bands)

Market Characteristics

- Price trends persistently

- Levels break decisively

- Volume confirms direction

- Momentum accelerates

Optimal Approach

Entry: Breakout from bands

Target: Trail with expanding bands

Stop: Inside opposite band

Size: Scale in with trend

Recommended Tools

- Moving average alignment

- ADX for trend strength

- MACD for momentum

- Advanced Features Explained

Quantum Coherence Metric

Measures phase alignment between individual and ensemble behavior:

80-100%: Perfect sync - strong mean reversion setup

50-80%: Moderate alignment - mixed signals

0-50%: Decoherence - trending behavior likely

Path Dependency Analysis

Quantifies how much history influences current price:

Low (<30%): Technical patterns reliable

Medium (30-50%): Mixed influences

High (>50%): Fundamental shift occurring

Volatility Regime Classification

Contextualizes current volatility:

Normal: Standard strategies apply

Elevated: Widen stops, reduce size

Extreme: Defensive mode required

Signal Strength Indicator

Real-time opportunity quality:

- Distance from threshold

- Momentum acceleration

- Cross-validation factors

Risk Management Framework

Position Sizing by Confidence

90%+ confidence = 100% position size

70-90% confidence = 75% position size

50-70% confidence = 50% position size

<50% confidence = 25% or skip

Dynamic Stop Placement

Ergodic State: ATR × 1.0 from entry

Non-Ergodic State: ATR × 2.0 from entry

Volatility Adjustment: Multiply by current regime

Multi-Timeframe Alignment

- Check higher timeframe regime

- Confirm ensemble consensus

- Verify volume participation

- Align with major levels

What Makes EMD Unique

Original Contributions

First Ergodic Theory Trading Application: Transforms abstract physics into practical signals

Ensemble Market Analysis: Revolutionary multi-market divergence system

Adaptive Confidence Engine: Institutional-grade signal quality metrics

Quantum Coherence: Novel market alignment measurement

Smart Signal Management: Prevents clustering while maintaining responsiveness

Technical Innovations

Dynamic Threshold Adaptation: Self-adjusting sensitivity

Path Memory Integration: Historical dependency weighting

Stress-Adjusted Scoring: Market condition normalization

Real-Time Performance Tracking: Built-in strategy analytics

Optimization Guidelines

By Timeframe

Scalping (1-5 min)

Period: 10-15

Threshold: 0.5-1.0

Memory: 20-30

Spacing: 5-10

Day Trading (5-60 min)

Period: 20-30

Threshold: 1.5-2.5

Memory: 40-60

Spacing: 15-20

Swing Trading (1H-1D)

Period: 40-60

Threshold: 2.0-3.0

Memory: 80-120

Spacing: 25-35

Position Trading (1D-1W)

Period: 60-100

Threshold: 3.0-5.0

Memory: 100-200

Spacing: 40-50

By Market Condition

Trending Markets

- Increase threshold

- Extend memory

- Focus on breaks

Ranging Markets

- Decrease threshold

- Shorten memory

- Focus on restores

Volatile Markets

- Increase spacing

- Raise confidence requirement

- Reduce position size

- Integration with Other Analysis

- Complementary Indicators

For Ergodic States

- RSI divergences

- Bollinger Band squeezes

- Volume profile nodes

- Support/resistance levels

For Non-Ergodic States

- Moving average ribbons

- Trend strength indicators

- Momentum oscillators

- Breakout patterns

- Fundamental Alignment

- Check economic calendar

- Monitor sector rotation

- Consider market themes

- Evaluate risk sentiment

Troubleshooting Guide

Too Many Signals:

- Increase threshold

- Extend signal spacing

- Raise confidence minimum

Missing Opportunities

- Decrease threshold

- Reduce signal spacing

- Check ensemble settings

Poor Win Rate

- Verify timeframe alignment

- Confirm volume participation

- Review risk management

Disclaimer

This indicator is for educational and informational purposes only. It does not constitute financial advice. Trading involves substantial risk of loss and is not suitable for all investors. Past performance does not guarantee future results.

The ergodic framework provides unique market insights but cannot predict future price movements with certainty. Always use proper risk management, conduct your own analysis, and never risk more than you can afford to lose.

This tool should complement, not replace, comprehensive trading strategies and sound judgment. Markets remain inherently unpredictable despite advanced analysis techniques.

Transform market chaos into trading clarity with Ergodic Market Divergence.

Created with passion for the TradingView community

Trade with insight. Trade with anticipation.

— Dskyz , for DAFE Trading Systems

RSI and CCICombined RSI and CCI Indicator for MetaTrader

The Combined RSI and CCI Indicator is a powerful hybrid momentum oscillator designed to merge the strengths of two popular indicators—the Relative Strength Index (RSI) and the Commodity Channel Index (CCI)—into a single, visually intuitive chart window. This tool enhances traders’ ability to identify overbought and oversold conditions, divergences, trend strength, and potential reversal zones with improved precision.

Purpose

By integrating RSI and CCI, this indicator helps filter out false signals that often occur when using each tool independently. It is especially useful for swing trading, trend confirmation, and spotting high-probability entry/exit zones. This dual-oscillator approach combines RSI’s relative momentum insights with CCI’s deviation-based analysis to produce a more reliable signal structure.

Key Features

Dual Oscillator Display: Plots both RSI and CCI on the same subwindow for easy comparison and correlation analysis.

Customizable Parameters:

RSI Period and Level (default: 14)

CCI Period and Typical Price Type (default: 20, TP)

Overbought/Oversold Levels for both indicators

Color-Coded Zones:

Background highlights when both RSI and CCI enter overbought/oversold territory, signaling high potential reversal zones.

Combined Signal Logic (Optional Feature):

Buy Signal: RSI < 30 and CCI < -100

Sell Signal: RSI > 70 and CCI > 100

These can be visualized as arrows or plotted as signal markers.

Trend Filter Overlay (Optional):

Can be combined with a moving average or price action filter to confirm trend direction before accepting signals.

Divergence Detection (Advanced Option):

Optional plotting of bullish or bearish divergence where both indicators diverge from price action.

Multi-Timeframe Compatibility:

Allows the use of higher timeframe RSI/CCI values to confirm signals on lower timeframes.

Benefits

Improved Signal Accuracy: Using both RSI and CCI together helps avoid false breakouts and whipsaws.

More Informed Decision-Making: Correlating momentum (RSI) with deviation (CCI) provides a well-rounded picture of market behavior.

Efficient Charting: Saves screen space and cognitive load by combining two indicators into one clean panel.

Scalable Strategy Integration: Can be used in discretionary trading or coded into automated strategies/alerts.

Use Case Example

In a ranging market, the indicator highlights zones where both RSI and CCI are oversold, alerting traders to potential bounce opportunities.

In trending markets, it confirms trend strength when RSI and CCI are both aligned with trend direction.

When RSI is diverging from price but CCI isn’t, it can be a clue of weakening momentum, helping traders scale out or avoid traps.

This combined indicator offers a versatile, high-performance toolset for traders looking to elevate their technical analysis by leveraging multiple momentum perspectives simultaneously.

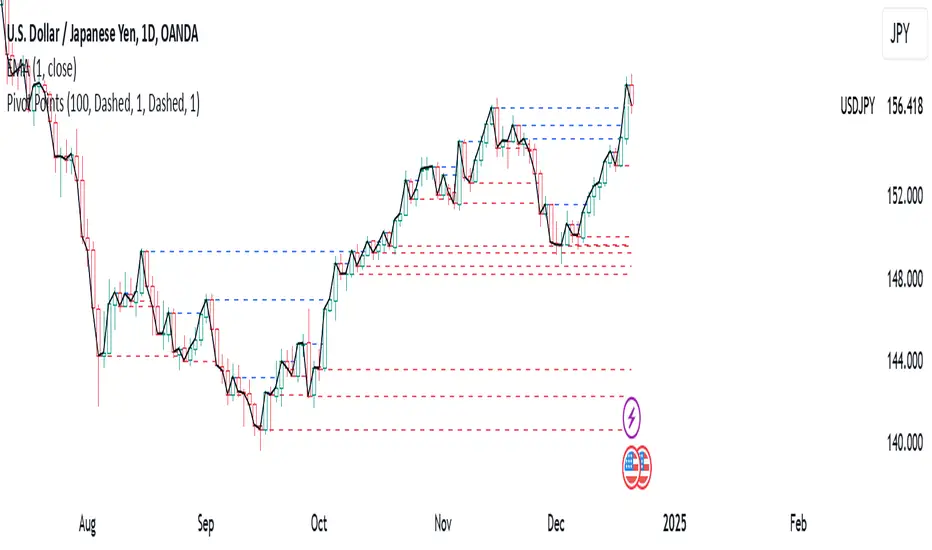

Daily Open Levels (Custom Pips)Daily Open Levels Indicator

Overview: The Daily Open Levels indicator is a simple but powerful tool designed for intraday traders who focus on the daily open price and pip-based levels for decision-making. This indicator helps you visualize key price levels based on the daily opening price, with configurable upper and lower levels calculated in pips. It is especially useful for tracking price movements relative to the previous day’s open and can help traders identify breakout zones, potential support/resistance, and key entry/exit points.

eatures:

Daily Open Price: The indicator automatically calculates and plots the daily open of the current trading day.

Upper and Lower Levels: Configurable upper and lower levels based on a user-defined pip interval. These levels can act as potential resistance or support zones.

Adjustable Pip Interval: You can customize the pip distance for the upper and lower levels to suit different trading styles and volatility.

Works for All Pairs: Option to automatically detect JPY pairs with a different pip value (0.1), or you can manually select your pair setting.

Color Customization: You can choose different colors for the daily open line, upper levels, and lower levels for easy visualization.

Immediate Visual Feedback: The indicator immediately draws the lines on the chart when added, without waiting for any market data.

How It Works:

The daily open price is retrieved from the current trading day, and horizontal lines are drawn at this price level, as well as at pip-based distances above and below it.

The pip distance is calculated using the Pip Interval setting and can be adjusted for any pair. For example, a 225-pip interval would create lines at 225 pips above and below the daily open.

The indicator dynamically updates every minute to reflect new daily opens and adjustments for each trading day.

Lines are drawn using the HLine (horizontal line) objects in MetaTrader 5, making them easy to spot and follow.

Parameters:

Pip Interval: Defines the pip distance for upper and lower levels (e.g., 225 pips). This affects how far above and below the daily open the levels are drawn.

Number of Levels: Sets how many upper and lower levels are drawn.

JPY Pairs: An option to adjust the pip value for JPY pairs (0.1 pip for JPY pairs vs. 0.01 pip for others).

Line Colors: Customize the colors for the daily open, upper levels, and lower levels.

Style & Width: Adjust the style (solid/dashed) and width of the lines to match your preferences.

Big 7 NASDAQ📊 Big 7 NASDAQ % Change Heatmap with Trend Arrows

This indicator displays a real-time performance table for the "Big 7" NASDAQ stocks:

Apple (AAPL), Microsoft (MSFT), Amazon (AMZN), Google (GOOGL), Meta (META), Tesla (TSLA), and Nvidia (NVDA).

🔎 Features:

Live Daily % Change: Calculates the percentage change between today’s open and the current price.

Color Gradient: Background color intensity reflects the strength of the move (from mild to strong bullish/bearish).

Trend Arrows: Visual arrows 🔺 (up) and 🔻 (down) represent the direction of movement.

Position Mode Selector:

"Buy" – highlights with green tones

"Sell" – highlights with red tones

"Neutral" – uses dynamic coloring based on individual stock moves

📍 Placement:

The table is positioned in the top-right corner of the chart for easy reference without cluttering your main view.

XAUUSD Correlation IndicatorXAUUSD Correlation Indicator

Questo indicatore per TradingView calcola e visualizza la correlazione tra il prezzo di XAUUSD (oro) e una serie di altri asset finanziari, tra cui valute (EURUSD, AUDUSD, NZDUSD, GBPUSD), metalli preziosi (platino, argento), indici azionari (SPX500, DJI, NASDAQ) e il dollaro statunitense (DXY).

L'indicatore offre:

1. Correlazione: Calcola la correlazione tra XAUUSD e gli altri asset su un periodo personalizzabile, dove un numero superiore allo 0 indica una correlazione positiva ed un numero inferiore allo 0 indica una correlazione negativa.

2. Variazione percentuale: Mostra la variazione percentuale dei prezzi degli asset rispetto all'apertura.

3. Visualizzazione personalizzabile: Permette di ordinare i dati in base alla correlazione o alla variazione percentuale.

4. Tabella interattiva: I risultati sono visualizzati in una tabella colorata, con opzioni per personalizzare i colori di sfondo, testo e bordi.

Ideale per trader e analisti che vogliono monitorare le relazioni tra l'oro e altri mercati in tempo reale, questo strumento aiuta a identificare opportunità di trading basate su correlazioni e tendenze di mercato.

Walk Forward PatternsINTRO

In Euclidean geometry, every mathematical output has a planar projection. 'Walk Forward Patterns' can be considered a practical example of this concept. On the other hand, this indicator might also be viewed as an experiment in 'how playing with Lego as a child contributes to time series analysis' :)

OVERVIEW

This script dynamically generates the necessary optimization and testing ranges for Walk Forward Analysis based on user-defined bar count and length inputs. It performs automatic calculations for each step, offers 8 different window options depending on the inputs, and visualizes the results dynamically. I should also note that most of the window models consist of original patterns I have created.

ADDITIONAL INFO : WHAT IS WALK FORWARD ANALYSIS?

Although it is not the main focus of this indicator, providing a brief definition of Walk Forward Analysis can be helpful in correctly interpreting the results it generates. Walk Forward Analysis (WFA) is a systematic method for optimizing parameters and validating trading strategies. It involves dividing historical data into variable segments, where a strategy is first optimized on an in-sample period and then tested on an out-of-sample period. This process repeats by shifting the windows forward, ensuring that each test evaluates the strategy on unseen data, helping to assess its robustness and adaptability in real market conditions.

ORIGINALITY

There are very few studies on Walk Forward Analysis in TradingView. Even worse, there are no any open-source studies available. Someone has to start somewhere, I suppose. And in my personal opinion, determining the optimization and backtest intervals is the most challenging part of WFA. These intervals serve as a prerequisite for automated parameter optimization. I felt the need to publish this pattern module, which I use in my own WFA models, partly due to this gap on community scripts.

INDICATOR MECHANICS

To use the indicator effectively, you only need to perform four simple tasks:

Specify the total number of bars in your chart in the 'Bar Index' parameter.

Define the optimization (In-Sample Test) length.

Define the testing (Out-Of-Sample Test) length.

Finally, select the window type.

The indicator automatically models everything else (including the number of steps) based on your inputs. And the result; you now have a clear idea of which bars to use for your Walk Forward tests!

A COMMONLY USED WINDOW SELECTION METHOD: ROLLING

A more concrete definition of Walk Forward Analysis, specifically for the widely used Rolling method, can be described as follows:

Parameters that have performed well over a certain period are identified (Optimization: In-Sample).

These parameters are then tested on a shorter, subsequent period (Backtest: Out-of-Sample).

The process is repeated forward in time (At each step, the optimization and backtest periods are shifted by the backtest length).

If the cumulative percentage profit obtained from the backtest results is greater than half of the historical optimization profit, the strategy is considered "successful."

If the strategy is successful, the most recent (untested) optimization values are used for live trading.

OTHER WINDOW OPTIONS

ANCHORED: That's a pattern based on progressively expanding optimization ranges at each step. Backtest ranges move forward in a staircase-like manner.

STATIC: Optimization ranges remain fixed, while backtest ranges are shifted forward.

BLOCKED: Optimization ranges are shifted forward in groups of three blocks. Backtest ranges are also shifted in a staircase manner, even at the cost of creating gaps from the optimization end bars.

TRIANGULAR: Optimization ranges are shifted forward in triangular regions, while backtest ranges move in a staircase pattern.

RATIO: The optimization length increases by 25% of the initial step’s fixed length at each step. In other words, the length grows by 25% of the first step's length incrementally. Backtest ranges always start from the bar where the optimization ends.

FIBONACCI: A variation of the Ratio method, where the optimization shift factor is set to 0.618

RANDOM WALK

Unlike the window models explained above, we can also generate optimization and backtest ranges completely randomly—offering almost unlimited variations! When you select the "Random" option in the "Window" parameter on the indicator interface, random intervals are generated based on various trigonometric calculations. By changing the numerical value in the '🐒' parameter, you can create entirely unique patterns.

WHY THE 🐒 EMOJI?

Two reasons.

First, I think that as humanity, we are a species of tailless primates who become happy when we understand things :). At least evolutionarily. The entire history of civilization is built on the effort to express the universe in a scale we can comprehend. 'Knowledge' is an invention born from this effort, which is why we feel happiness when we 'understand'. Second, I can't think of a better metaphor for randomness than a monkey sitting at a keyboard. See: Monkey Test.

Anyway, I’m rambling :)

NOTES

The indicator generates results for up to 100 steps. As the number of steps increases, the table may extend beyond the screen—don’t forget to zoom out!

FINAL WORDS

I haven’t published a Walk Forward script yet . However, there seem to be examples that can perform parameter optimization in the true sense of the word, producing more realistic results without falling into overfitting in my library. Hopefully, I’ll have the chance to publish one in the coming weeks. Sincerely thanks to Kıvanç Özbilgiç, Robert Pardo, Kevin Davey, Ernest P. Chan for their inspiring publishments.

DISCLAIMER

That's just a script, nothing more. I hope it helps everyone. Do not forget to manage your risk. And trade as safely as possible. Best of luck!

© dg_factor

MAG 7 - Weighted Multi-Symbol Momentum + ExtrasOverview

This indicator aggregates the percentage change of multiple symbols into a single “weighted momentum” value. You can set individual weights to emphasize or de-emphasize particular stocks. The script plots two key items:

The default tickers in the script are:

AAPL (Apple)

AMZN (Amazon)

NVDA (NVIDIA)

MSFT (Microsoft)

GOOGL (Alphabet/Google)

TSLA (Tesla)

META (Meta Platforms/Facebook)

Raw Weighted Momentum (Histogram):

Each bar represents the combined (weighted) percentage change across your chosen symbols for that bar.

Bars are colored green if the momentum is above zero, or red if below zero.

Smoothed Momentum (Yellow Line):

An Exponential Moving Average (EMA) of the raw momentum for a smoother trend view.

Helps visualize when short-term momentum is accelerating or decelerating relative to its average.

Features

Symbol Inputs: Up to seven user-defined tickers, with weights for each symbol.

Smoothing Period: Set a custom lookback length to calculate the EMA (or switch to SMA in the code if you prefer).

Table Display: A built-in table in the top-right corner lists each symbol’s real-time percentage change, plus the total weighted momentum.

Alerts:

Configure alerts for when the weighted momentum crosses above or below user-defined thresholds.

Helps you catch major shifts in sentiment across multiple symbols.

How To Use

Select Symbols & Weights: In the indicator’s settings, specify the tickers you want to monitor and their corresponding weights. Weights default to 1 (equal weighting).

Watch the Bars vs. Zero:

Bars above zero mean a positive weighted momentum (the basket is collectively moving up).

Bars below zero mean negative weighted momentum (the basket is collectively under pressure).

Check the Yellow Line: The EMA of momentum.

If the bars consistently stay above the line, short-term momentum is stronger than its recent average.

If the bars dip below the line, momentum is weakening relative to its average.

Review the Table: Quick snapshot of each symbol’s daily percentage change plus the total basket momentum, all color-coded red or green.

Caution & Tips

This indicator measures rate of change, not absolute price levels. A rising momentum can still be part of a larger downtrend.

Always combine momentum readings with other technical and/or fundamental signals for confirmation.

For better reliability, experiment with different smoothing lengths to suit your trading style (shorter for scalping, longer for swing or positional approaches).

Milvetti_Pineconnector_LibraryLibrary "Milvetti_Pineconnector_Library"

This library has methods that provide practical signal transmission for Pineconnector.Developed By Milvetti

buy(licenseId, symbol, risk, sl, tp, beTrigger, beOffset, trailTrig, trailDist, trailStep, atrTimeframe, atrTrigger, atrPeriod, atrMultiplier, atrShift, spread, accFilter, secret, comment)

Create a buy order message

Parameters:

licenseId (string) : License Id. This is a unique identifier found in the Pineconnector Licensing Dashboard.

symbol (string) : Symbol. Default is syminfo.ticker

risk (float) : Risk. Function depends on the “Volume Type” selected in the EA

sl (float) : StopLoss. Place stop-loss. Computation is based on the Target Type selected in the EA. Default is 0(inactive)

tp (float) : TakeProfit. Place take-profit. Computation is based on the Target Type selected in the EA. Default is 0(inactive)

beTrigger (float) : Breakeven will be activated after the position gains this number of pips. Ensure > 0

beOffset (float) : Offset from entry price. 0 means the SL will be placed exactly at entry price. 1 means 1 pip above the entry price for buy trades and 1 pip below for sell trades.

trailTrig (int) : Trailing stop-loss will be activated after a trade gains this number of pips. Default is 0(inactive)

trailDist (int) : SL will be opened at traildist after trailtrig is met, even if you do not have a SL placed.. Default is 0(inactive)

trailStep (int) : Moves trailing stop-loss once price moves to favourable by a specified number of pips. Default is 0(inactive)

atrTimeframe (string) : ATR Trailing Stop will be based on the specified timeframe in minutes and will only update once per bar close. Default is Timeframe.Period

atrTrigger (float) : Activate the trigger of ATR Trailing after market moves favourably by a number of pips. Default is 0(inactive)

atrPeriod (int) : ATR averaging period. Default is 0

atrMultiplier (float) : Multiple of ATR to utilise in the new SL computation. Default is 1

atrShift (float) : Relative shift of price information, 0 uses latest candle, 1 uses second last, etc. Default is 0

spread (float) : Enter the position only if the spread is equal or less than the specified value in pips. Default is 0(inactive)

accFilter (float) : Enter the position only if the account requirement is met. Default is 0(inactive)

secret (string)

comment (string) : Comment. Add a string into the order’s comment section. Default is "Symbol+Timeframe"

sell(licenseId, symbol, risk, sl, tp, beTrigger, beOffset, trailTrig, trailDist, trailStep, atrTimeframe, atrTrigger, atrPeriod, atrMultiplier, atrShift, spread, accFilter, secret, comment)

Create a buy order message

Parameters:

licenseId (string) : License Id. This is a unique identifier found in the Pineconnector Licensing Dashboard.

symbol (string) : Symbol. Default is syminfo.ticker

risk (float) : Risk. Function depends on the “Volume Type” selected in the EA

sl (float) : StopLoss. Place stop-loss. Computation is based on the Target Type selected in the EA. Default is 0(inactive)

tp (float) : TakeProfit. Place take-profit. Computation is based on the Target Type selected in the EA. Default is 0(inactive)

beTrigger (float) : Breakeven will be activated after the position gains this number of pips. Ensure > 0

beOffset (float) : Offset from entry price. 0 means the SL will be placed exactly at entry price. 1 means 1 pip above the entry price for buy trades and 1 pip below for sell trades.

trailTrig (int) : Trailing stop-loss will be activated after a trade gains this number of pips. Default is 0(inactive)

trailDist (int) : SL will be opened at traildist after trailtrig is met, even if you do not have a SL placed.. Default is 0(inactive)

trailStep (int) : Moves trailing stop-loss once price moves to favourable by a specified number of pips. Default is 0(inactive)

atrTimeframe (string) : ATR Trailing Stop will be based on the specified timeframe in minutes and will only update once per bar close. Default is Timeframe.Period

atrTrigger (float) : Activate the trigger of ATR Trailing after market moves favourably by a number of pips. Default is 0(inactive)

atrPeriod (int) : ATR averaging period. Default is 0

atrMultiplier (float) : Multiple of ATR to utilise in the new SL computation. Default is 1

atrShift (float) : Relative shift of price information, 0 uses latest candle, 1 uses second last, etc. Default is 0

spread (float) : Enter the position only if the spread is equal or less than the specified value in pips. Default is 0(inactive)

accFilter (float) : Enter the position only if the account requirement is met. Default is 0(inactive)

secret (string)

comment (string) : Comment. Add a string into the order’s comment section. Default is "Symbol+Timeframe"

buyLimit(licenseId, symbol, pending, risk, sl, tp, beTrigger, beOffset, trailTrig, trailDist, trailStep, atrTimeframe, atrTrigger, atrPeriod, atrMultiplier, atrShift, spread, accFilter, secret, comment)

Create a buy limit order message

Parameters:

licenseId (string) : License Id. This is a unique identifier found in the Pineconnector Licensing Dashboard.

symbol (string) : Symbol. Default is syminfo.ticker

pending (float) : Computing pending order entry price. EA Options: Pips, Specified Price, Percentage

risk (float) : Risk. Function depends on the “Volume Type” selected in the EA

sl (float) : StopLoss. Place stop-loss. Computation is based on the Target Type selected in the EA. Default is 0(inactive)

tp (float) : TakeProfit. Place take-profit. Computation is based on the Target Type selected in the EA. Default is 0(inactive)

beTrigger (float) : Breakeven will be activated after the position gains this number of pips. Ensure > 0

beOffset (float) : Offset from entry price. 0 means the SL will be placed exactly at entry price. 1 means 1 pip above the entry price for buy trades and 1 pip below for sell trades.

trailTrig (int) : Trailing stop-loss will be activated after a trade gains this number of pips. Default is 0(inactive)

trailDist (int) : SL will be opened at traildist after trailtrig is met, even if you do not have a SL placed.. Default is 0(inactive)

trailStep (int) : Moves trailing stop-loss once price moves to favourable by a specified number of pips. Default is 0(inactive)

atrTimeframe (string) : ATR Trailing Stop will be based on the specified timeframe in minutes and will only update once per bar close. Default is Timeframe.Period

atrTrigger (float) : Activate the trigger of ATR Trailing after market moves favourably by a number of pips. Default is 0(inactive)

atrPeriod (int) : ATR averaging period. Default is 0

atrMultiplier (float) : Multiple of ATR to utilise in the new SL computation. Default is 1

atrShift (float) : Relative shift of price information, 0 uses latest candle, 1 uses second last, etc. Default is 0

spread (float) : Enter the position only if the spread is equal or less than the specified value in pips. Default is 0(inactive)

accFilter (float) : Enter the position only if the account requirement is met. Default is 0(inactive)

secret (string)

comment (string) : Comment. Add a string into the order’s comment section. Default is "Symbol+Timeframe"

buyStop(licenseId, symbol, pending, risk, sl, tp, beTrigger, beOffset, trailTrig, trailDist, trailStep, atrTimeframe, atrTrigger, atrPeriod, atrMultiplier, atrShift, spread, accFilter, secret, comment)

Create a buy stop order message

Parameters:

licenseId (string) : License Id. This is a unique identifier found in the Pineconnector Licensing Dashboard.

symbol (string) : Symbol. Default is syminfo.ticker

pending (float) : Computing pending order entry price. EA Options: Pips, Specified Price, Percentage

risk (float) : Risk. Function depends on the “Volume Type” selected in the EA

sl (float) : StopLoss. Place stop-loss. Computation is based on the Target Type selected in the EA. Default is 0(inactive)

tp (float) : TakeProfit. Place take-profit. Computation is based on the Target Type selected in the EA. Default is 0(inactive)

beTrigger (float) : Breakeven will be activated after the position gains this number of pips. Ensure > 0

beOffset (float) : Offset from entry price. 0 means the SL will be placed exactly at entry price. 1 means 1 pip above the entry price for buy trades and 1 pip below for sell trades.

trailTrig (int) : Trailing stop-loss will be activated after a trade gains this number of pips. Default is 0(inactive)

trailDist (int) : SL will be opened at traildist after trailtrig is met, even if you do not have a SL placed.. Default is 0(inactive)

trailStep (int) : Moves trailing stop-loss once price moves to favourable by a specified number of pips. Default is 0(inactive)

atrTimeframe (string) : ATR Trailing Stop will be based on the specified timeframe in minutes and will only update once per bar close. Default is Timeframe.Period

atrTrigger (float) : Activate the trigger of ATR Trailing after market moves favourably by a number of pips. Default is 0(inactive)

atrPeriod (int) : ATR averaging period. Default is 0

atrMultiplier (float) : Multiple of ATR to utilise in the new SL computation. Default is 1

atrShift (float) : Relative shift of price information, 0 uses latest candle, 1 uses second last, etc. Default is 0

spread (float) : Enter the position only if the spread is equal or less than the specified value in pips. Default is 0(inactive)

accFilter (float) : Enter the position only if the account requirement is met. Default is 0(inactive)

secret (string)

comment (string) : Comment. Add a string into the order’s comment section. Default is "Symbol+Timeframe"

sellLimit(licenseId, symbol, pending, risk, sl, tp, beTrigger, beOffset, trailTrig, trailDist, trailStep, atrTimeframe, atrTrigger, atrPeriod, atrMultiplier, atrShift, spread, accFilter, secret, comment)

Create a sell limit order message

Parameters:

licenseId (string) : License Id. This is a unique identifier found in the Pineconnector Licensing Dashboard.

symbol (string) : Symbol. Default is syminfo.ticker

pending (float) : Computing pending order entry price. EA Options: Pips, Specified Price, Percentage

risk (float) : Risk. Function depends on the “Volume Type” selected in the EA

sl (float) : StopLoss. Place stop-loss. Computation is based on the Target Type selected in the EA. Default is 0(inactive)

tp (float) : TakeProfit. Place take-profit. Computation is based on the Target Type selected in the EA. Default is 0(inactive)

beTrigger (float) : Breakeven will be activated after the position gains this number of pips. Ensure > 0

beOffset (float) : Offset from entry price. 0 means the SL will be placed exactly at entry price. 1 means 1 pip above the entry price for buy trades and 1 pip below for sell trades.

trailTrig (int) : Trailing stop-loss will be activated after a trade gains this number of pips. Default is 0(inactive)

trailDist (int) : SL will be opened at traildist after trailtrig is met, even if you do not have a SL placed.. Default is 0(inactive)

trailStep (int) : Moves trailing stop-loss once price moves to favourable by a specified number of pips. Default is 0(inactive)

atrTimeframe (string) : ATR Trailing Stop will be based on the specified timeframe in minutes and will only update once per bar close. Default is Timeframe.Period

atrTrigger (float) : Activate the trigger of ATR Trailing after market moves favourably by a number of pips. Default is 0(inactive)

atrPeriod (int) : ATR averaging period. Default is 0

atrMultiplier (float) : Multiple of ATR to utilise in the new SL computation. Default is 1

atrShift (float) : Relative shift of price information, 0 uses latest candle, 1 uses second last, etc. Default is 0

spread (float) : Enter the position only if the spread is equal or less than the specified value in pips. Default is 0(inactive)

accFilter (float) : Enter the position only if the account requirement is met. Default is 0(inactive)

secret (string)

comment (string) : Comment. Add a string into the order’s comment section. Default is "Symbol+Timeframe"

sellStop(licenseId, symbol, pending, risk, sl, tp, beTrigger, beOffset, trailTrig, trailDist, trailStep, atrTimeframe, atrTrigger, atrPeriod, atrMultiplier, atrShift, spread, accFilter, secret, comment)

Create a sell stop order message

Parameters:

licenseId (string) : License Id. This is a unique identifier found in the Pineconnector Licensing Dashboard.

symbol (string) : Symbol. Default is syminfo.ticker

pending (float) : Computing pending order entry price. EA Options: Pips, Specified Price, Percentage

risk (float) : Risk. Function depends on the “Volume Type” selected in the EA

sl (float) : StopLoss. Place stop-loss. Computation is based on the Target Type selected in the EA. Default is 0(inactive)

tp (float) : TakeProfit. Place take-profit. Computation is based on the Target Type selected in the EA. Default is 0(inactive)

beTrigger (float) : Breakeven will be activated after the position gains this number of pips. Ensure > 0

beOffset (float) : Offset from entry price. 0 means the SL will be placed exactly at entry price. 1 means 1 pip above the entry price for buy trades and 1 pip below for sell trades.

trailTrig (int) : Trailing stop-loss will be activated after a trade gains this number of pips. Default is 0(inactive)

trailDist (int) : SL will be opened at traildist after trailtrig is met, even if you do not have a SL placed.. Default is 0(inactive)

trailStep (int) : Moves trailing stop-loss once price moves to favourable by a specified number of pips. Default is 0(inactive)

atrTimeframe (string) : ATR Trailing Stop will be based on the specified timeframe in minutes and will only update once per bar close. Default is Timeframe.Period

atrTrigger (float) : Activate the trigger of ATR Trailing after market moves favourably by a number of pips. Default is 0(inactive)

atrPeriod (int) : ATR averaging period. Default is 0

atrMultiplier (float) : Multiple of ATR to utilise in the new SL computation. Default is 1

atrShift (float) : Relative shift of price information, 0 uses latest candle, 1 uses second last, etc. Default is 0

spread (float) : Enter the position only if the spread is equal or less than the specified value in pips. Default is 0(inactive)

accFilter (float) : Enter the position only if the account requirement is met. Default is 0(inactive)

secret (string)

comment (string) : Comment. Add a string into the order’s comment section. Default is "Symbol+Timeframe"

Pivot PointsPivot Points Indicator

The Pivot Points indicator highlights areas on the chart where candles close in opposite colors. These points occur when the price shifts from bullish to bearish, or vice versa, indicating potential reversals or continuation patterns. These points are more easily seen on a line chart and represent areas where the price changes direction to create peak formations.

Foundational Concepts

Before diving into the indicator, it’s important to understand a few key concepts:

When price is trending upward, it creates higher highs and higher lows. Each high or low acts as a pivot point. In an uptrend, the price is more likely to break the previous high (pivot point) and continue higher. You can enter a buy trade when the price breaks the previous high, anticipating the continuation of the trend.

When price is trending downward, it creates lower lows and lower highs. Each high or low is also a pivot point. In a downtrend, the price is more likely to break the previous low (pivot point) and continue lower. You can enter a sell trade when the price breaks the previous low, anticipating the continuation of the trend.

For reversal trades, it’s helpful to be familiar with chart patterns like double tops, double bottoms, and head and shoulders. The Pivot Points indicator can assist in identifying these patterns, helping you determine entry points, as well as where to place your stop loss.

Recommended Setup

It’s recommended to have two charts open side by side: one displaying a line chart and the other showing a candlestick chart, with the Pivot Points indicator applied to both. This setup allows you to easily identify the market structure and price action as it approaches these levels. You can also add a 20-period Simple Moving Average (SMA) to both charts to help identify the overall trend. Additionally, consider adding the Relative Strength Index (RSI) to the line chart to confirm overbought or oversold conditions.

This approach can be used on any timeframe.

Contributing

If you have suggestions, improvements, or bug fixes, I encourage you to submit pull requests. Collaboration helps make the indicator more versatile and useful for everyone.

Disclaimer

Any trading decisions you make are entirely your responsibility.

The MetaTrader 5 version of this indicator is available on my GitHub repository: roshaneforde/pivot-points-indicator

Enhanced Trading Alerts# Enhanced Multi-Symbol EMA Trading System with Smart Alerts

## 📊 Overview

A powerful multi-symbol trading system that monitors up to 6 symbols simultaneously for high-probability trading setups using advanced EMA crossover strategies, enhanced with volume confirmation and RSI filters. Perfect for swing traders and position traders focusing on quality tech stocks.

## 🎯 Key Features

- **Multi-Symbol Monitoring**: Simultaneously tracks 6 different symbols

- **Advanced EMA Strategy**: Uses dual EMA system (320 & 820 periods) for trend confirmation

- **Volume Validation**: Confirms signals with volume surge analysis

- **RSI Filter**: Adds momentum confirmation to avoid false signals

- **Smart Risk Management**: Automatic stop-loss and take-profit calculations

- **Detailed Alerts**: Comprehensive alert messages with key price levels

## 📈 Trading Signals

### Buy Signals Generated When:

- Price crosses above the slow EMA (820)

- Fast EMA (320) confirms the trend

- RSI is in optimal range (not overbought)

- Volume surge confirms the movement

- Risk levels automatically calculated

### Sell Signals Generated When:

- Price crosses below the slow EMA (820)

- Fast EMA (320) confirms the downtrend

- RSI confirms momentum shift

- Volume surge validates the movement

## ⚙️ Customizable Parameters

- **EMA Lengths**: Adjust fast and slow EMA periods

- **Volume Threshold**: Set minimum volume surge multiplier

- **RSI Settings**: Customize overbought/oversold levels

- **Risk Management**: Adjustable stop-loss and take-profit percentages

- **Symbol Selection**: Choose any 6 symbols to monitor

## 🎨 Visual Elements

- Blue line: Fast EMA (320)

- Red line: Slow EMA (820)

- Purple line: RSI indicator

- Clear visual representation of trend changes

## 📱 Smart Alerts

Detailed alert messages include:

- Symbol name and signal type

- Current price level

- RSI value

- Stop-loss price

- Take-profit target

- Volume surge multiplier

## 💡 Best Practices

1. **Timeframe Selection**:

- Best suited for 1H, 4H, or Daily timeframes

- Can be adapted for swing or position trading

2. **Risk Management**:

- Use suggested stop-loss levels

- Follow take-profit targets

- Consider volume confirmation strength

3. **Multiple Chart Setup**:

- Create multiple instances for more symbols

- Group correlated assets together

- Use different alert sounds for different setups

## 🎓 Usage Tips

- Monitor strongest tech stocks for best results

- Combine with market sentiment analysis

- Use volume surge as quality filter

- Wait for all conditions to align before trading

- Consider overall market conditions

## ⚠️ Risk Warning

This indicator is for informational purposes only. Always conduct your own analysis and consider your risk tolerance before trading. Past performance does not guarantee future results.

## 📌 Version History

- v1.0: Initial release with multi-symbol support

- v1.1: Added volume surge confirmation

- v1.2: Enhanced alert system with risk levels

- v1.3: Added RSI filter and improved signal quality

## 🔄 Regular Updates

Subscribe to this script for regular updates and improvements. Feel free to suggest features in the comments section.

## 📗 Default Symbols

- TSLA (Tesla)

- NVDA (NVIDIA)

- AVGO (Broadcom)

- TSM (Taiwan Semiconductor)

- META (Meta Platforms)

- AMZN (Amazon)

You can customize these symbols to match your trading preferences.

Good luck trading! 🍀

The Most Powerful TQQQ EMA Crossover Trend Trading StrategyTQQQ EMA Crossover Strategy Indicator

Meta Title: TQQQ EMA Crossover Strategy - Enhance Your Trading with Effective Signals

Meta Description: Discover the TQQQ EMA Crossover Strategy, designed to optimize trading decisions with fast and slow EMA crossovers. Learn how to effectively use this powerful indicator for better trading results.

Key Features

The TQQQ EMA Crossover Strategy is a powerful trading tool that utilizes Exponential Moving Averages (EMAs) to identify potential entry and exit points in the market. Key features of this indicator include:

**Fast and Slow EMAs:** The strategy incorporates two EMAs, allowing traders to capture short-term trends while filtering out market noise.

**Entry and Exit Signals:** Automated signals for entering and exiting trades based on EMA crossovers, enhancing decision-making efficiency.

**Customizable Parameters:** Users can adjust the lengths of the EMAs, as well as take profit and stop loss multipliers, tailoring the strategy to their trading style.

**Visual Indicators:** Clear visual plots of the EMAs and exit points on the chart for easy interpretation.

How It Works

The TQQQ EMA Crossover Strategy operates by calculating two EMAs: a fast EMA (default length of 20) and a slow EMA (default length of 50). The core concept is based on the crossover of these two moving averages:

- When the fast EMA crosses above the slow EMA, it generates a *buy signal*, indicating a potential upward trend.

- Conversely, when the fast EMA crosses below the slow EMA, it produces a *sell signal*, suggesting a potential downward trend.

This method allows traders to capitalize on momentum shifts in the market, providing timely signals for trade execution.

Trading Ideas and Insights

Traders can leverage the TQQQ EMA Crossover Strategy in various market conditions. Here are some insights:

**Scalping Opportunities:** The strategy is particularly effective for scalping in volatile markets, allowing traders to make quick profits on small price movements.

**Swing Trading:** Longer-term traders can use this strategy to identify significant trend reversals and capitalize on larger price swings.

**Risk Management:** By incorporating customizable stop loss and take profit levels, traders can manage their risk effectively while maximizing potential returns.

How Multiple Indicators Work Together

While this strategy primarily relies on EMAs, it can be enhanced by integrating additional indicators such as:

- **Relative Strength Index (RSI):** To confirm overbought or oversold conditions before entering trades.

- **Volume Indicators:** To validate breakout signals, ensuring that price movements are supported by sufficient trading volume.

Combining these indicators provides a more comprehensive view of market dynamics, increasing the reliability of trade signals generated by the EMA crossover.

Unique Aspects

What sets this indicator apart is its simplicity combined with effectiveness. The reliance on EMAs allows for smoother signals compared to traditional moving averages, reducing false signals often associated with choppy price action. Additionally, the ability to customize parameters ensures that traders can adapt the strategy to fit their unique trading styles and risk tolerance.

How to Use

To effectively utilize the TQQQ EMA Crossover Strategy:

1. **Add the Indicator:** Load the script onto your TradingView chart.

2. **Set Parameters:** Adjust the fast and slow EMA lengths according to your trading preferences.

3. **Monitor Signals:** Watch for crossover points; enter trades based on buy/sell signals generated by the indicator.

4. **Implement Risk Management:** Set your stop loss and take profit levels using the provided multipliers.

Regularly review your trading performance and adjust parameters as necessary to optimize results.

Customization

The TQQQ EMA Crossover Strategy allows for extensive customization:

- **EMA Lengths:** Change the default lengths of both fast and slow EMAs to suit different time frames or market conditions.

- **Take Profit/Stop Loss Multipliers:** Adjust these values to align with your risk management strategy. For instance, increasing the take profit multiplier may yield larger gains but could also increase exposure to market fluctuations.

This flexibility makes it suitable for various trading styles, from aggressive scalpers to conservative swing traders.

Conclusion

The TQQQ EMA Crossover Strategy is an effective tool for traders seeking an edge in their trading endeavors. By utilizing fast and slow EMAs, this indicator provides clear entry and exit signals while allowing for customization to fit individual trading strategies. Whether you are a scalper looking for quick profits or a swing trader aiming for larger moves, this indicator offers valuable insights into market trends.

Incorporate it into your TradingView toolkit today and elevate your trading performance!

MMRI Chart (Primary)The **Mannarino Market Risk Indicator (MMRI)** is a financial risk measurement tool created by financial strategist Gregory Mannarino. It’s designed to assess the risk level in the stock market and economy based on current bond market conditions and the strength of the U.S. dollar. The MMRI considers factors like the U.S. 10-Year Treasury Yield and the Dollar Index (DXY), which indicate investor confidence in government debt and the dollar's purchasing power, respectively.

The formula for MMRI uses the 10-Year Treasury Yield multiplied by the Dollar Index, divided by a constant (1.61) to normalize the risk measure. A higher MMRI score suggests increased market risk, while a lower score indicates more stability. Mannarino has set certain thresholds to interpret the MMRI score:

- **Below 100**: Low risk.

- **100–200**: Moderate risk.

- **200–300**: High risk.

- **Above 300**: Extreme risk, indicating market instability and potential downturns.

This tool aims to provide insight into economic conditions that may affect asset classes like stocks, bonds, and precious metals. Mannarino often updates MMRI scores and risk analyses in his public market updates.

S&P 2024: Magnificent 7 vs. the rest of S&PThis chart is designed to calculate and display the percentage change of the Magnificent 7 (M7) stocks and the S&P 500 excluding the M7 (Ex-M7) from the beginning of 2024 to the most recent data point. The Magnificent 7 consists of seven major technology stocks: Apple (AAPL), Microsoft (MSFT), Amazon (AMZN), Alphabet (GOOGL), Meta (META), Nvidia (NVDA), and Tesla (TSLA). These stocks are a significant part of the S&P 500 and can have a substantial impact on its overall performance.

Key Components and Functionality:

1. Start of 2024 Baseline:

- The script identifies the closing prices of the S&P 500 and each of the Magnificent 7 stocks on the first trading day of 2024. These values serve as the baseline for calculating percentage changes.

2. Current Value Calculation:

- It then fetches the most recent closing prices of these stocks and the S&P 500 index to calculate their current values.

3. Percentage Change Calculation:

- The script calculates the percentage change for the M7 by comparing the sum of the current prices of the M7 stocks to their combined value at the start of 2024.

- Similarly, it calculates the percentage change for the Ex-M7 by comparing the current value of the S&P 500 excluding the M7 to its value at the start of 2024.

4. Plotting:

- The calculated percentage changes are plotted on the chart, with the M7’s percentage change shown in red and the Ex-M7’s percentage change shown in blue.

Use Case:

This indicator is particularly useful for investors and analysts who want to understand how much the performance of the S&P 500 in 2024 is driven by the Magnificent 7 stocks compared to the rest of the index. By showing the percentage change from the start of the year, it provides clear insights into the relative growth or decline of these two segments of the market over the course of the year.

Visualization:

- Red Line (M7 % Change): Displays the percentage change of the combined value of the Magnificent 7 stocks since the start of 2024.

- Blue Line (Ex-M7 % Change): Displays the percentage change of the S&P 500 excluding the Magnificent 7 since the start of 2024.

This script enables a straightforward comparison of the performance of the M7 and Ex-M7, highlighting which segment is contributing more to the overall movement of the S&P 500 in 2024.

[Pandora] Error Function Treasure Trove - ERF/ERFI/Sigmoids+PRAISE:

At this time, I have to graciously thank the wonderful minds behind the new "Pine Profiler Mode" (PPM). Directly prior to this release, it allowed me to ascertain script performance even more. While I usually write mostly in highly optimized Pine code, PPM visually identified a few bottlenecks that would otherwise be hard to identify. Anyone who contributed to PPMs creation and testing before release... BRAVO!!! I commend all of those who assisted in it's state-of-the-art engineering and inception, well done!

BACKSTORY:

This script is specifically being released in defense of another member, an exceptionally unique PhD. It was brought to my attention that a script-mod-event occurred, regarding the publishing of a measly antiquated error function (ERF) calculation within his script. This sadly resulted in the now former member jumping ship after receiving unmannerly responses amidst his curious inquiries as to why his erf() was modded. To forbid rusty and rudimentary formulations because a mod-on-duty is temporally offended by a non-nefarious release of code, is in MY opinion an injustice to principles of perpetuating open-source code intended to benefit thousands to millions of community members. While Pine is the heart and soul of TV, the mathematical concepts contributed from the minds of members is the inspirational fuel of curiosity that powers it's pertinent reason to exist and evolve.

It is an indisputable fact that most members are not greatly skilled Pine Poets. Many members may be incapable of innovating robust function code in Pine, even if they have one or more PhDs. We ALL come from various disciplines of mathematical comprehension and education. Some mathematicians are not greatly skilled at coding, while some coders are not exceptional at math. So... what am I to do to attempt to resolve this circumstantial challenge??? Those who know me best are aware that I will always side with "the right side of history" in order to accomplish my primary self-defined missions I choose to accept. Serving as an algorithmic advocate, I felt compelled to intercede by compiling numerous error functions into elegant code of very high caliber that any and every TV member may choose to employ, so this ERROR never happens again.

After weeks of contemplation into algorithms I knew little about, I prioritized myself to resolve an unanticipated matter by creating advanced formulas of exquisitely crafted error functions refined to the best of my current abilities. My aversion for unresolved problems motivated me to eviscerate error function insufficiencies with many more rigid formulations beyond what is thought to exist. ERF needed a proper algorithmic exorcism anyways. In my furiosity, I contemplated an array of madMAXimum diplomatic demolition methods, choosing the chain saw massacre technique to slaughter dysfunctionalities I encountered on a battered ERF roadway. This resulted in prolific solutions that should assuredly endure the test of time. Poetically, as you will come to see, I am ripping the lid off of Pandora's box of error functions in this case to correct wrongs into a splendid bundle of rights for members.

INTENTION:

Error function (ERF) enthusiasts... PREPARE FOR GLORY!! The specific purpose of this script is to deprecate classic error functions with the creation of a fierce and formidable army of superior formulations, each having varying attributes of computational complexity with differing absolute error ranges in their results for multiple compute scenarios. This is NOT an indicator... It is intended to allow members to embark on endeavors to advance the profound knowledge base of this growing worldwide community of 60+ million inquisitive minds. For those of you who believe computational mathematics and statistics is near completion at its finest; I am here to inform you, this is ridiculous to ponder. We are no where near statistical excellence that can and will exist eventually. At this time, metaphorically speaking, we are merely scratching microns off of the surface of the skin of a statistical apple Isaac Newton once pondered.

THIS RELEASE:

Following weeks of pondering methodical experiments beyond the ordinary, I am liberating these wild notions of my error function explorations to the entire globe as copyleft code, not just Pine. This Pandora's basket of ERFs is being openly disclosed for the sake of the sanctity of mathematics, empirical science (not the garbage we are told by CONTROLocrats to blindly trust), revolutionary cutting edge engineering, cosmology, physics, information technology, artificial intelligence, and EVERY other mathematical branch of human knowledge being discovered over centuries. I do believe James Glaisher would favor my aims concerning ERF aspirations embracing the "Power of Pine".

The included functions are intended for TV members to use in any way they see fit. This is a gift to ALL members to foster future innovative excellence on this platform. Any attempt to moderate this code without notification of "self-evident clear and just cause" will be considered an irrevocable egregious action. The original foundational PURPOSE of establishing script moderation (I clearly remember) was primarily to maintain active vigilance over a growing community against intentional nefarious actions and/or behaviors in blatant disrespect to other author's works AND also thwart rampant copypasting bandit operations, all while accommodating balanced principles of fairness for an educational community cause via open source publishing that should support future algorithmic inventions well beyond my lifespan.

APPLICATIONS:

The related error functions are used in probability theory, statistics, and numerous and engineering scientific disciplines. Its key characteristics and applications are innumerable in computational realms. Its versatility and significance make it a fundamental tool in arenas of quantitative analysis and scientific research...

Probability Theory - Is widely used in probability theory to calculate probabilities and quantiles of the normal distribution.

Statistics - It's related to the Gaussian integral and plays a crucial role in statistics, especially in hypothesis testing and confidence interval calculations.

Physics - In physics, it arises in the study of diffusion equations, quantum mechanics, and heat conduction problems.

Engineering - Applications exist in engineering disciplines such as signal processing, control theory, and telecommunications.

Error Analysis - It's employed in error analysis and uncertainty quantification.

Numeric Approximations - Due to its lack of a closed-form expression, numerical methods are often employed to approximate erf/erfi().

AI, LLMs, & MACHINE LEARNING:

The error function (ERF) is indispensable to various AI applications, particularly due to its relation to Gaussian distributions and error analysis. It is used in Gaussian processes for regression and classification, probabilistic inference for Bayesian networks, soft margin computation in SVMs, neural networks involving Gaussian activation functions or noise, and clustering algorithms like Gaussian Mixture Models. Improved ERF approximations can enhance precision in these applications, reduce computational complexity, handle outliers and noise better, and improve optimization and convergence, possibly leading to more accurate, efficient, and robust AI systems.

BONUS ALGORITHMS:

While ERFs are versatile, its opposite also exists in the form of inverse error functions (ERFIs). I have also included a modified form of the inverse fisher transform along side MY sigmoid (sigmyod). I am uncertain what sigmyod() may be used for, but it's a culmination of my examinations deep into "sigmoid domains", something I am fascinated by. Whatever implications it may possess, I am unveiling it along with it's cousin functions. For curious minds, this quality of composition seen here is ideally what underlies what I would term "Pandora functionality" that empowers my Pandora indication. I go through hordes of formulations, testing, and inspection to find what appears to be the most beneficial logical/mathematical equation to apply...

SCRIPT OPERATION:

To showcase the characteristics and performance of my ERF/ERFI formulations, I devised a multi-modal script. By using bar_index , I generated a broad sequence of numeric values to input into the first ERF/ERFI parameter. These sequences allow you to inspect the contours of the error function's outputs for both ERF and ERFI. When combined with compute-intensive precision functions (CIPFs), the polynomial function output values can be subtracted from my CIPFs to obtain results of absolute error, displaying the accuracy of the many polynomial estimation functions I tuned in testing for Pine's float environment.