CryptoFlux Dynamo [JOAT]CryptoFlux Dynamo: Velocity Scalping Strategy

WHAT THIS STRATEGY IS

CryptoFlux Dynamo is an open-source Pine Script v6 strategy designed for momentum-based scalping on cryptocurrency perpetual futures. It combines multiple technical analysis methods into a unified system that adapts its behavior based on current market volatility conditions.

This script is published open-source so you can read, understand, and modify the complete logic. The description below explains everything the strategy does so that traders who cannot read Pine Script can fully understand how it works before using it.

HOW THIS STRATEGY IS ORIGINAL AND WHY THE INDICATORS ARE COMBINED

This strategy uses well-known indicators (MACD, EMA, RSI, MFI, Bollinger Bands, Keltner Channels, ATR). The originality is not in the individual indicators themselves, but in the specific way they are integrated into a regime-adaptive system. Here is the detailed justification for why these components are combined and how they work together:

The Problem Being Solved:

Standard indicator-based strategies use fixed thresholds. For example, a typical MACD strategy might enter when the histogram crosses above zero. However, in cryptocurrency markets, volatility changes dramatically throughout the day and week. A MACD crossover during a low-volatility consolidation period has very different implications than the same crossover during a high-volatility trending period. Using the same entry thresholds and stop distances in both conditions leads to either:

Too many false signals during consolidation (if thresholds are loose)

Missing valid opportunities during expansion (if thresholds are tight)

Stops that are too tight during volatility spikes (causing premature exits)

Stops that are too wide during compression (giving back profits)

The Solution Approach:

This strategy first classifies the current volatility regime using normalized ATR (ATR as a percentage of price), then dynamically adjusts ALL other parameters based on that classification. This creates a context-aware system rather than a static threshold comparison.

How Each Component Contributes to the System:

ATR-Based Regime Classification (The Foundation)

The strategy calculates ATR over 21 periods, smooths it with a 13-period EMA to reduce noise from wicks, then divides by price to get a normalized percentage. This ATR% is classified into three regimes:

- Compression (ATR% < 0.8%): Market is consolidating, breakouts are more likely but false signals are common

- Expansion (ATR% 0.8% - 1.6%): Normal trending conditions

- Velocity (ATR% > 1.6%): High volatility, larger moves but also larger adverse excursions

This regime classification then controls stop distances, profit targets, trailing stop offsets, and signal strength requirements. The regime acts as a "meta-parameter" that tunes the entire system.

EMA Ribbon (8/21/34) - Trend Structure Detection

The three EMAs establish trend direction and structure. When EMA 8 > EMA 21 > EMA 34, the trend structure is bullish. The slope of the middle EMA (21) is calculated over 8 bars and converted to degrees using arctangent. This slope measurement quantifies trend strength, not just direction.

Why these specific periods? The 8/21/34 sequence follows Fibonacci-like spacing and provides good separation on 5-minute cryptocurrency charts. The fast EMA (8) responds to immediate price action, the mid EMA (21) represents the short-term trend, and the slow EMA (34) acts as a trend filter.

The EMA ribbon works with the regime classification: during compression regimes, the strategy requires stronger ribbon alignment before entry because false breakouts are more common.

MACD (8/21/5) - Momentum Measurement

The MACD uses faster parameters (8/21/5) than the standard (12/26/9) because cryptocurrency markets move faster than traditional markets. The histogram is smoothed with a 5-period EMA to reduce noise.

The key innovation is the adaptive histogram baseline. Instead of using a fixed threshold, the strategy calculates a rolling baseline from the smoothed absolute histogram value, then multiplies by a sensitivity factor (1.15). This means the threshold for "significant momentum" automatically adjusts based on recent momentum levels.

The MACD works with the regime classification: during velocity regimes, the histogram baseline is effectively higher because recent momentum has been stronger, preventing entries on relatively weak momentum.

RSI (21 period) and MFI (21 period) - Independent Momentum Confirmation

RSI measures momentum using price changes only. MFI (Money Flow Index) measures momentum using price AND volume. By requiring both to confirm, the strategy filters out price moves that lack volume support.

The 21-period length is longer than typical (14) to reduce noise on 5-minute charts. The trigger threshold (55 for longs, 45 for shorts) is slightly offset from 50 to require momentum in the trade direction, not just neutral readings.

These indicators work together: a signal requires RSI > 55 AND MFI > 55 for longs. This dual confirmation reduces false signals from price manipulation or low-volume moves.

Bollinger Bands (1.5 mult) and Keltner Channels (1.8 mult) - Squeeze Detection

When Bollinger Bands contract inside Keltner Channels, volatility is compressing and a breakout is likely. This is the "squeeze" condition. When the bands expand back outside the channels, the squeeze "releases."

The strategy uses a 1.5 multiplier for Bollinger Bands (tighter than standard 2.0) and 1.8 for Keltner Channels. These values were chosen to identify meaningful squeezes on 5-minute cryptocurrency charts without triggering too frequently.

The squeeze detection works with the regime classification: squeeze releases during compression regimes receive additional signal strength points because breakouts from consolidation are more significant.

Volume Impulse Detection - Institutional Participation Filter

The strategy calculates a volume baseline (34-period SMA) and standard deviation. A "volume impulse" is detected when current volume exceeds the baseline by 1.15x OR when the volume z-score exceeds 0.5.

This filter ensures entries occur when there is meaningful market participation, not during low-volume periods where price moves are less reliable.

Volume impulse is required for all entries and adds points to the composite signal strength score.

Cycle Oscillator - Trend Alignment Filter

The strategy calculates a 55-period EMA as a cycle basis, then measures price deviation from this basis as a percentage. When price is more than 0.15% above the cycle basis, the cycle is bullish. When more than 0.15% below, the cycle is bearish.

This filter prevents counter-trend entries. Long signals require bullish cycle alignment; short signals require bearish cycle alignment.

BTC Dominance Filter (Optional) - Market Regime Filter

The strategy can optionally use BTC.D (Bitcoin Dominance) as a market regime filter. When BTC dominance is rising (slope > 0.12), the market is in "risk-off" mode and long entries on altcoins are filtered. When dominance is falling (slope < -0.12), short entries are filtered.

This filter is optional because the BTC.D data feed may lag during low-liquidity periods.

How The Components Work Together (The Mashup Justification):

The strategy uses a composite scoring system where each signal pathway contributes points:

Trend Break pathway (30 points): Requires EMA ribbon alignment + positive slope + price breaks above recent structure high

Momentum Surge pathway (30 points): Requires MACD histogram > adaptive baseline + MACD line > signal + RSI > 55 + MFI > 55 + volume impulse

Squeeze Release pathway (25 points): Requires BB inside KC (squeeze) then release + momentum bias + histogram confirmation

Micro Pullback pathway (15 points): Requires shallow retracement to fast EMA within established trend + histogram confirmation + volume impulse

Additional modifiers:

+5 points if volume impulse is present, -5 if absent

+5 points in velocity regime, -2 in compression regime

+5 points if cycle is aligned, -5 if counter-trend

A trade only executes when the composite score reaches the minimum threshold (default 55) AND all filters agree (session, cycle bias, BTC dominance if enabled).

This scoring system is the core innovation: instead of requiring ALL conditions to be true (which would generate very few signals) or ANY condition to be true (which would generate too many false signals), the strategy requires ENOUGH conditions to be true, with different conditions contributing different weights based on their reliability.

HOW THE STRATEGY CALCULATES ENTRIES AND EXITS

Entry Logic:

1. Calculate current volatility regime from ATR%

2. Calculate all indicator values (MACD, EMA, RSI, MFI, squeeze, volume)

3. Evaluate each signal pathway and sum points

4. Check all filters (session, cycle, dominance, kill switch)

5. If composite score >= 55 AND all filters pass, generate entry signal

6. Calculate position size based on risk per trade and regime-adjusted stop distance

7. Execute entry with regime name as comment

Position Sizing Formula:

RiskCapital = Equity * (0.65 / 100)

StopDistance = ATR * StopMultiplier(regime)

RawQuantity = RiskCapital / StopDistance

MaxQuantity = Equity * (12 / 100) / Price

Quantity = min(RawQuantity, MaxQuantity)

Quantity = round(Quantity / 0.001) * 0.001

This ensures each trade risks approximately 0.65% of equity regardless of volatility, while capping total exposure at 12% of equity.

Stop Loss Calculation:

Stop distance is ATR multiplied by a regime-specific multiplier:

Compression regime: 1.05x ATR (tighter stops because moves are smaller)

Expansion regime: 1.55x ATR (standard stops)

Velocity regime: 2.1x ATR (wider stops to avoid premature exits during volatility)

Take Profit Calculation:

Target distance is ATR multiplied by regime-specific multiplier and base risk/reward:

Compression regime: 1.6x ATR * 1.8 base R:R * 0.9 regime bonus = approximately 2.6x ATR

Expansion regime: 2.05x ATR * 1.8 base R:R * 1.0 regime bonus = approximately 3.7x ATR

Velocity regime: 2.8x ATR * 1.8 base R:R * 1.15 regime bonus = approximately 5.8x ATR

Trailing Stop Logic:

When adaptive trailing is enabled, the strategy calculates a trailing offset based on ATR and regime:

Compression regime: 1.1x base offset (looser trailing to avoid noise)

Expansion regime: 1.0x base offset (standard)

Velocity regime: 0.8x base offset (tighter trailing to lock in profits during fast moves)

The trailing stop only activates when it would be tighter than the initial stop.

Momentum Fail-Safe Exits:

The strategy closes positions early if momentum reverses:

Long positions close if MACD histogram turns negative OR EMA ribbon structure breaks (fast EMA crosses below mid EMA)

Short positions close if MACD histogram turns positive OR EMA ribbon structure breaks

This prevents holding through momentum reversals even if stop loss hasn't been hit.

Kill Switch:

If maximum drawdown exceeds 6.5%, the strategy disables new entries until manually reset. This prevents continued trading during adverse conditions.

HOW TO USE THIS STRATEGY

Step 1: Apply to Chart

Use a 5-minute chart of a high-liquidity cryptocurrency perpetual (BTC/USDT, ETH/USDT recommended)

Ensure at least 200 bars of history are loaded for indicator stabilization

Use standard candlestick charts only (not Heikin Ashi, Renko, or other non-standard types)

Step 2: Understand the Visual Elements

EMA Ribbon: Three lines (8/21/34 periods) showing trend structure. Bullish when stacked upward, bearish when stacked downward.

Background Color: Shows current volatility regime

- Indigo/dark blue = Compression (low volatility)

- Purple = Expansion (normal volatility)

- Magenta/pink = Velocity (high volatility)

Bar Colors: Reflect signal strength divergence. Brighter colors indicate stronger directional bias.

Triangle Markers: Entry signals. Up triangles below bars = long entry. Down triangles above bars = short entry.

Dashboard (top-right): Real-time display of regime, ATR%, signal strengths, position status, stops, targets, and risk metrics.

Step 3: Interpret the Dashboard

Regime: Current volatility classification (Compression/Expansion/Velocity)

ATR%: Normalized volatility as percentage of price

Long/Short Strength: Current composite signal scores (0-100)

Cycle Osc: Price deviation from 55-period EMA as percentage

Dominance: BTC.D slope and filter status

Position: Current position direction or "Flat"

Stop/Target: Current stop loss and take profit levels

Kill Switch: Status of drawdown protection

Volume Z: Current volume z-score

Impulse: Whether volume impulse condition is met

Step 4: Adjust Parameters for Your Needs

For more conservative trading: Increase "Minimum Composite Signal Strength" to 65 or higher

For more aggressive trading: Decrease to 50 (but expect more false signals)

For higher timeframes (15m+): Increase "Structure Break Window" to 12-15, increase "RSI Momentum Trigger" to 58

For lower liquidity pairs: Increase "Volume Impulse Multiplier" to 1.3, increase slippage in strategy properties

To disable short selling: Uncheck "Enable Short Structure"

To disable BTC dominance filter: Uncheck "BTC Dominance Confirmation"

STRATEGY PROPERTIES (BACKTEST SETTINGS)

These are the exact settings used in the strategy's Properties dialog box. You must use these same settings when evaluating the backtest results shown in the publication:

Initial Capital: $100,000

Justification: This amount is higher than typical retail accounts. I chose this value to demonstrate percentage-based returns that scale proportionally. The strategy uses percentage-based position sizing (0.65% risk per trade), so a $10,000 account would see the same percentage returns with 10x smaller position sizes. The absolute dollar amounts in the backtest should be interpreted as percentages of capital.

Commission: 0.04% (commission_value = 0.04)

Justification: This reflects typical perpetual futures exchange fees. Major exchanges charge between 0.02% (maker) and 0.075% (taker). The 0.04% value is a reasonable middle estimate. If your exchange charges different fees, adjust this value accordingly. Higher fees will reduce net profitability.

Slippage: 1 tick

Justification: This is conservative for liquid pairs like BTC/USDT on major exchanges during normal conditions. For less liquid altcoins or during high volatility, actual slippage may be higher. If you trade less liquid pairs, increase this value to 2-3 ticks for more realistic results.

Pyramiding: 1

Justification: No position stacking. The strategy holds only one position at a time. This simplifies risk management and prevents overexposure.

calc_on_every_tick: true

Justification: The strategy evaluates on every price update, not just bar close. This is necessary for scalping timeframes where waiting for bar close would miss opportunities. Note that this setting means backtest results may differ slightly from bar-close-only evaluation.

calc_on_order_fills: true

Justification: The strategy recalculates immediately after order fills for faster response to position changes.

RISK PER TRADE JUSTIFICATION

The default risk per trade is 0.65% of equity. This is well within the TradingView guideline that "risking more than 5-10% on a trade is not typically considered viable."

With the 12% maximum exposure cap, even if the strategy takes multiple consecutive losses, the total risk remains manageable. The kill switch at 6.5% drawdown provides additional protection by halting new entries during adverse conditions.

The position sizing formula ensures that stop distance (which varies by regime) is accounted for, so actual risk per trade remains approximately 0.65% regardless of volatility conditions.

SAMPLE SIZE CONSIDERATIONS

For statistically meaningful backtest results, you should select a dataset that generates at least 100 trades. On 5-minute BTC/USDT charts, this typically requires:

2-3 months of data during normal market conditions

1-2 months during high-volatility periods

3-4 months during low-volatility consolidation periods

The strategy's selectivity (requiring 55+ composite score plus all filters) means it generates fewer signals than less filtered approaches. If your backtest shows fewer than 100 trades, extend the date range or reduce the minimum signal strength threshold.

Fewer than 100 trades produces statistically unreliable results. Win rate, profit factor, and other metrics can vary significantly with small sample sizes.

STRATEGY DESIGN COMPROMISES AND LIMITATIONS

Every strategy involves trade-offs. Here are the compromises made in this design and the limitations you should understand:

Selectivity vs. Opportunity Trade-off

The 55-point minimum threshold filters many potential trades. This reduces false signals but also misses valid setups that don't meet all criteria. Lowering the threshold increases trade frequency but decreases win rate. There is no "correct" threshold; it depends on your preference for fewer higher-quality signals vs. more signals with lower individual quality.

Regime Classification Lag

The ATR-based regime detection uses historical data (21 periods + 13-period smoothing). It cannot predict sudden volatility spikes. During flash crashes or black swan events, the strategy may be classified in the wrong regime for several bars before the classification updates. This is an inherent limitation of any lagging indicator.

Indicator Parameter Sensitivity

The default parameters (MACD 8/21/5, EMA 8/21/34, RSI 21, etc.) are tuned for BTC/ETH perpetuals on 5-minute charts during 2024 market conditions. Different assets, timeframes, or market regimes may require different parameters. There is no guarantee that parameters optimized on historical data will perform similarly in the future.

BTC Dominance Filter Limitations

The CRYPTOCAP:BTC.D data feed may lag during low-liquidity periods or weekends. The dominance slope calculation uses a 5-bar SMA, adding additional delay. If you notice the filter behaving unexpectedly, consider disabling it.

Backtest vs. Live Execution Differences

TradingView backtesting does not replicate actual broker execution. Key differences:

Backtests assume perfect fills at calculated prices; real execution involves order book depth, latency, and partial fills

The calc_on_every_tick setting improves backtest realism but still cannot capture sub-bar price action or order book dynamics

Commission and slippage settings are estimates; actual costs vary by exchange, time of day, and market conditions

Funding rates on perpetual futures are not modeled in backtests and can significantly impact profitability over time

Exchange-specific limitations (position limits, liquidation mechanics, order types) are not modeled

Market Condition Dependencies

This strategy is designed for trending and breakout conditions. During extended sideways consolidation with no clear direction, the strategy may generate few signals or experience whipsaws. No strategy performs well in all market conditions.

Cryptocurrency-Specific Risks

Cryptocurrency markets operate 24/7 without session boundaries. This means:

No natural "overnight" risk reduction

Volatility can spike at any time

Liquidity varies significantly by time of day

Exchange outages or issues can occur at any time

WHAT THIS STRATEGY DOES NOT DO

To be straightforward about limitations:

This strategy does not guarantee profits. Past backtest performance does not indicate future results.

This strategy does not predict the future. It reacts to current conditions based on historical patterns.

This strategy does not account for funding rates, which can significantly impact perpetual futures profitability.

This strategy does not model exchange-specific execution issues (partial fills, requotes, outages).

This strategy does not adapt to fundamental news events or black swan scenarios.

This strategy is not optimized for all market conditions. It may underperform during extended consolidation.

IMPORTANT RISK WARNINGS

Past performance does not guarantee future results. The backtest results shown reflect specific historical market conditions and parameter settings. Markets change constantly, and strategies that performed well historically may underperform or lose money in the future. A single backtest run does not constitute proof of future profitability.

Trading involves substantial risk of loss. Cryptocurrency derivatives are highly volatile instruments. You can lose your entire investment. Only trade with capital you can afford to lose completely.

This is not financial advice. This strategy is provided for educational and informational purposes only. It does not constitute investment advice, trading recommendations, or any form of financial guidance. The author is not a licensed financial advisor.

You are responsible for your own decisions. Before using this strategy with real capital:

Thoroughly understand the code and logic by reading the open-source implementation

Forward test with paper trading or very small positions for an extended period

Verify that commission, slippage, and execution assumptions match your actual trading environment

Understand that live results will differ from backtest results

Consider consulting with a qualified financial advisor

No guarantees or warranties. This strategy is provided "as is" without any guarantees of profitability, accuracy, or suitability for any purpose. The author is not responsible for any losses incurred from using this strategy.

OPEN-SOURCE CODE STRUCTURE

The strategy code is organized into these sections for readability:

Configuration Architecture: Input parameters organized into logical groups (Core Controls, Optimization Constants, Regime Intelligence, Signal Pathways, Risk Architecture, Visualization)

Helper Functions: calcQty() for position sizing, clamp01() and normalize() for value normalization, calcMFI() for Money Flow Index calculation

Core Indicator Engine: EMA ribbon, ATR and regime classification, MACD with adaptive baseline, RSI, MFI, volume analytics, cycle oscillator, BTC dominance filter, squeeze detection

Signal Pathway Logic: Trend break, momentum surge, squeeze release, micro pullback pathways with composite scoring

Entry/Exit Orchestration: Signal filtering, position sizing, entry execution, stop/target calculation, trailing stop logic, momentum fail-safe exits

Visualization Layer: EMA plots, regime background, bar coloring, signal labels, dashboard table

You can read and modify any part of the code. Understanding the logic before deployment is strongly recommended.

- Made with passion by officialjackofalltrades

"Futures" için komut dosyalarını ara

Auto Position CalculatorA position sizing tool that automatically detects the instrument you're trading and calculates the correct position size based on your risk parameters.

What It Does

This indicator calculates how many contracts, lots, or shares to trade based on your account size, risk percentage, and stop loss distance. It auto-detects the instrument type and adjusts the point/pip value accordingly.

Supported Instruments

Futures: NQ, MNQ, ES, MES, YM, MYM, RTY, M2K, CL, MCL, GC, MGC

Forex: All major pairs (USD, EUR, GBP, JPY, etc.)

Index CFDs: NAS100, US500, US30, GER40, UK100

Metals: XAU, XAG

Crypto and Stocks: Automatic detection

How to Use

Set your account size and risk % in settings

Click the settings icon and place Entry, Stop Loss, and Take Profit on the chart

The position size and risk calculations appear automatically

Levels auto-reset at your chosen session (Asia, London, or New York open)

Limitations

CFD and forex pip values assume standard lot sizing - your broker may differ

Auto-detection relies on ticker naming conventions, which vary by broker/data feed

Session reset times are based on ET (Eastern Time)

Session Anchored OIWAP [Arjo]The Session Anchored OIWAP (Open Interest Weighted Average Price) indicator shows you a weighted average price that uses Open Interest (OI) changes during different trading sessions . It divides the day into four clear sessions: Opening Hour , Morning Session , Mid-Day Session , and Closing Session .

For each session , it calculates a weighted average price using both market price and open interest data from futures . This line updates as the session progresses and resets when a new session starts .

You can also see optional deviation bands that you visually compare to how far the market price is moving away from the session’s weighted average. This indicator also helps you watch how Open Interest changes connect with price movements during specific market hours.

Concepts

This tool works on a few simple ideas:

Session anchoring

Each session starts fresh. The indicator resets and begins a new calculation when a new time block begins. This allows users to visually study each session independently.

Open-interest weighting

Instead of treating all price moves equally, price changes linked to higher open-interest activity have more influence on the OIWAP. This gives a weighted reflection of where the market has been trading during the session.

Averaging and smoothing

The OIWAP line blends many price data points into one smooth curve, making it easier to follow than raw price movement.

Volatility display with bands

The upper and lower bands are placed at ±0.5 standard deviation from the OIWAP line. These bands simply help you see when price stretches further away than usual from the session average.

Features

Four Independent Session Calculations: Shows separate OIWAP lines for Opening Hour (default: 09:15-10:15), Morning (10:15-11:30), Mid-Day (11:30-14:00), and Closing (14:00-15:30) sessions

Open Interest Weighting: Uses absolute OI change as the weight instead of traditional volume

Customizable Session Times: You can change the time ranges for each session to match your market or what you need

Optional Deviation Bands: You can turn ±0.5 standard deviation bands on or off around each OIWAP line

Color-Coded Sessions: Each session has its own color so you can tell them apart easily

Selective Display: You can turn individual sessions and bands on or off

Data Availability Check: Shows you a notification when Open Interest data isn't available for your symbol

Adjustable Position Timeframe: You can calculate OI changes on different timeframes (Chart, Daily, 15min, 30min, 60min, 120min)

How to use

Add this indicator to a chart of any symbol that has Open Interest data ( from futures or derivatives contracts). Once you add it, you'll see colored lines showing the OIWAP for each session you enable, along with optional deviation bands.

Adjusting Settings:

Turn individual sessions on or off using the checkboxes in the " Sessions " section

Change session colors to match your chart or what looks good to you

Turn deviation bands on or off using the " Show Bands " option in the Display settings

Change session time ranges in the " Session Times " section to match your market hours or what you want to analyze

Change the Position Timeframe if you want to see OI changes calculated on a different time period

Visual Interpretation:

Each OIWAP line shows you the OI-weighted average price for that session

The deviation bands show you how much prices spread out, weighted by OI changes

You can watch how price interacts with these levels to see where significant OI activity happened

Different sessions may show different OIWAP levels, showing you how the OI-price relationship changes throughout the trading day

Note:

This indicator needs Open Interest data to work. If OI data isn't available for your symbol, you'll see a message in the center of your chart. This indicator works only with derivatives markets like futures and options in the Indian Market where OI data is publicly available.

Conclusion

The Session Anchored OIWAP indicator is designed to support structured market observation by combining price, open interest, and session anchoring into a clear visual format. It helps users study market behavior during different parts of the day without generating trading instructions or outcomes.

Disclaimer

This indicator is for educational and visual-analysis purposes only. It does not provide trading signals , financial advice, or guaranteed outcomes . You should perform your own research and consult a licensed financial professional when needed. All trading decisions are solely the responsibility of the user.

Happy Trading

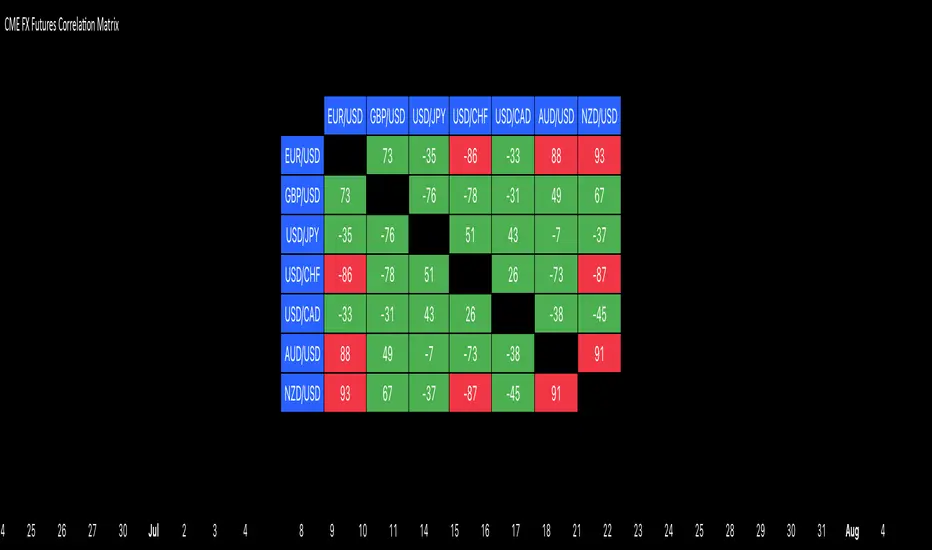

CME FX Futures Correlation MatrixThis indicator calculates the correlation between major CME FX futures and displays it in a visual table. It shows how closely pairs like EUR/USD, GBP/USD, USD/JPY, USD/CHF, USD/CAD, AUD/USD, and NZD/USD move together or in opposite directions.

The indicator inherits the timeframe of the chart it’s applied to.

Color coding:

Red: strong correlation (absolute value > 80%), both positive and negative

Green: moderate/low correlation

How to launch it

Apply the indicator to a CME chart (e.g., EUR/USD futures).

Set Numbers of Bars Back to the desired lookback period (default 100).

The table appears in the center of the chart, showing correlation percentages between all major FX futures.

Opening-Range BreakoutNote: Default trading date range looks mediocre. Set date range to "Entire History" to see full effect of the strategy. 50.91% profitable trades, 1.178 profit factor, steady profits and limited drawdown. Total P&L: $154,141.18, Max Drawdown: $18,624.36. High R^2

█ Overview

The Opening-Range Breakout strategy is a mechanical, session‑based day‑trading system designed to capture the initial burst of directional momentum immediately following the market open. It defines a user‑configurable “opening range” window, measures its high and low boundaries, then places breakout stop orders at those levels once the range closes. Built‑in filters on minimum range width, reward‑to‑risk ratios, and optional reversal logic help refine entries and manage risk dynamically.

█ How It Works

Opening‑Range Formation

Between 9:30–10:15 AM ET (configurable), the script tracks the highest high and lowest low to form the day’s opening range box.

On the first bar after the range window closes, the range high (OR_high) and low (OR_low) are “locked in.”

Range‑Width Filter

To avoid false breakouts in low‑volatility mornings, the range must be at least X% of the current price (default 0.35%).

If the measured opening-range width < minimum threshold, no orders are placed that day.

Entry & Order Placement

Long: a stop‑buy order at the opening‑range high.

Short: a stop‑sell order at the opening‑range low.

Only one side can trigger (or both if reverse logic is enabled after a losing trade).

Risk Management

Once triggered, each trade uses an ATR‑style stop-loss defined as a percentage retracement of the range (default 50% of range width).

Profit target is set at a configurable Reward/Risk Ratio (default 1.1×).

Optional: Reverse on Stop‑Loss – if the initial breakout loses, immediately reverse into the opposite side on the same day.

Session Exit

Any open positions are closed at the end of the regular trading day (default 3:45 PM ET window end, with hard flat at session close).

Visual cues are provided via green (range high) and red (range low) step‑line plots directly on the chart, allowing you to see the range box and breakout triggers in real time.

█ Why It Works

Early Momentum Capture: The first 15 – 60 minutes of trading encapsulate overnight news digestion and institutional order flow, creating a well‑defined volatility “range.”

Mechanical Discipline: Clear, rule‑based entries and exits remove emotional guesswork, ensuring consistency.

Volatility Filtering: By requiring a minimum range width, the system avoids choppy, low‑range days where false breakouts are common.

Dynamic Sizing: Stops and targets scale with the opening range, adapting automatically to each day’s volatility environment.

█ How to Use

Set Your Instruments & Timeframe

-Apply to any futures contract on a 1‑ to 5‑minute chart.

-Ensure chart timezone is set to America/New_York.

Configure Inputs

-Opening‑Range Window: e.g. “0930-1015” for a 45‑minute range.

-Min. OR Width (%): e.g. 0.35 for 0.35% of current price.

-Reward/Risk Ratio: e.g. 1.1 for a modest profit target above your stop.

-Max OR Retracement %: e.g. 50 to set stop at 50% of range width.

-One Trade Per Day: toggle to limit to a single breakout.

-Reverse on Stop Loss: toggle to flip direction after a losing breakout.

Monitor the Chart

-Watch the green and red range boundaries form during the session open.

-Orders will automatically submit on the first bar after the range window closes, conditioned on your filters.

Review & Adjust

-Backtest across multiple months to validate performance on your preferred contract.

-Tweak range duration, minimum width, and R/R multiple to fit your risk tolerance and desired win‑rate vs. expectancy balance.

█ Settings Reference

Input Defaults

Opening‑Range Window - Time window to form OR (HHMM-HHMM) - 0930–1015

Regular Trading Day - Full session for EOD flat (HHMM-HHMM) - 0930–1545

Min. OR Width (%) - Minimum OR size as % of close to trigger orders - 0.35

Reward/Risk Ratio - Profit target multiple of stop‑loss distance - 1.1

Max OR Retracement (%) - % of OR width to use as stop‑loss distance - 50

One Trade Per Day - Limit to a single breakout order per day - false

Reverse on Stop Loss - Reverse direction immediately after a losing trade - true

Disclaimer

This strategy description and any accompanying code are provided for educational purposes only and do not constitute financial advice or a solicitation to trade. Futures trading involves substantial risk, including possible loss of capital. Past performance is not indicative of future results. Traders should assess their own risk tolerance and conduct thorough backtesting and forward-testing before committing real capital.

Forward Curve Visualization ToolProvide the spot symbol and the futures product root, and the script automatically scans all relevant contracts for you—no more tedious manual searches. The result is a clean, intuitive chart showing the live forward curve in real time.

It also detects contango or backwardation conditions (based on spot < F1 < F2 < F3).

Future Features:

Plot historical snapshots of the curve (1 day, 1 week, or 1 month ago) to understand market trends over time.

Display additional metrics such as annualized basis, cost of carry (CoC), and even volume or open interest for deeper insights.

If you trade futures and watch the forward curve, this script will give you the actionable data you need and get more ideas or features you’d like to see. Let’s build them together!

Disclaimer

Please remember that past performance may not be indicative of future results.

Due to various factors, including changing market conditions, the strategy may no longer perform as well as in historical backtesting.

This post and the script don’t provide any financial advice.

Metals:Backwardation/ContangoMETALS: Gold , Silver , Copper ( GC , SI, HG)

Quickly visualize carrying charge market vs backwardized market by comparing the price of the next 2 years of futures contracts.

Carrying charge (contract prices increasing into the future) = normal, representing the costs of carrying/storage of a commodity. When this is flipped to Backwardation (contract prices decreasing into the future): its a bullish sign: Buyers want this commodity, and they want it NOW.

Note: indicator does not map to time axis in the same way as price; it simply plots the progression of contract months out into the future; left to right; so timeframe DOESN'T MATTER for this plot

There's likely some more efficient way to write this; e.g. when plotting for Gold ( GC ); 21 of the security requests are redundant; but they are still made; and can make this slower to load

TO UPDATE(once a year will do): in REQUEST CONTRACTS section, delete old contracts (top) and add new ones (bottom). Then in PLOTTING section, Delete old contract labels (bottom); add new contract labels (top); adjust the X in 'bar_index-(X+_historical)' numbers accordingly

This is one of three similar indicators: Meats | Metals | Grains

-If you want to build from this; to work on other commodities ; be aware that Tradingview limits the number of contract calls to 40 (hence the 3 seperate indicators)

Tips:

-Right click and reset chart if you can't see the plot; or if you have trouble with the scaling.

-Right click and add to new scale if you prefer this not to overlay directly on price. Or move to new pane below.

--Added historical input: input days back in time; to see the historical shape of the Futures curve via selecting 'days back' snapshot

updated 15th June 2022

© twingall

Grains:Backwardation/ContangoGRAINS: Wheat , Soybeans , Corn (ZW, ZS, ZC )

Quickly visualize carrying charge market vs backwardized market by comparing the price of the next 2 years of futures contracts.

Carrying charge (contract prices increasing into the future) = normal, representing the costs of carrying/storage of a commodity. When this is flipped to Backwardation (contract prices decreasing into the future): its a bullish sign: Buyers want this commodity, and they want it NOW.

The above chart shows a nice example of backwardation.

Note: indicator does not map to time axis in the same way as price; it simply plots the progression of contract months out into the future; left to right; so timeframe DOESN'T MATTER for this plot

There's likely some more efficient way to write this; e.g. when plotting for Wheat (ZW); 15 of the security requests are redundant; but they are still made; and can make this slower to load

TO UPDATE(once a year will do): in REQUEST CONTRACTS section, delete old contracts (top) and add new ones (bottom). Then in PLOTTING section, Delete old contract labels (bottom); add new contract labels (top); adjust the X in 'bar_index-(X+_historical)' numbers accordingly

This is one of three similar indicators: Meats | Metals | Grains

-If you want to build from this; to work on other commodities ; be aware that Tradingview limits the number of contract calls to 40 (hence the 3 seperate indicators)

Tips:

-Right click and reset chart if you can't see the plot; or if you have trouble with the scaling.

-Right click and add to new scale if you prefer this not to overlay directly on price. Or move to new pane below.

--Added historical input: input days back in time; to see the historical shape of the Futures curve via selecting 'days back' snapshot

updated 15th June 2022

© twingall

Settlement priceThis script is meant to be used intraday, on futures products.

It charts the previous day/week/month settlement price as a constant level intraday.

The settlement price of a product is calculated by the exchange at the end of each day. It is shown in the D/W/M chart as the close price. The settlement price does not coincide with the last close price intraday, thus creating the need of a script like this.

The settlement price can be a pivotal price in intraday futures trading, as it can act as support or resistance

You can select the resolution of the settlement by the "Resolution" input

Satoshi Frame Risk FrameSatoshi Frame Risk Frame

Trade with structure, not emotion.

Satoshi Frame – Risk Frame is a minimalist capital and risk management tool designed for traders who value discipline over hype.

This indicator helps you:

Calculate position size based on fixed risk

Control margin usage with leverage awareness

Visualize risk before entering any trade

Stay consistent across different market conditions

Built for futures and leveraged trading, Risk Frame focuses on one rule only:

Protect your capital first. Profits come later.

This is the first public release by Satoshi Frame —

a framework, not a signal .

Cumulative Intraday Volume with Long/Short LabelsThis indicator calculates a running total of volume for each trading day, then shows on the price chart when that total crosses levels you choose. Every day at 6:00 PM Eastern Time, the total goes back to zero so it always reflects only the current day’s activity. From that moment on, each time a new candle appears the indicator looks at whether the candle closed higher than it opened or lower. If it closed higher, the candle’s volume is added to the running total; if it closed lower, the same volume amount is subtracted. As a result, the total becomes positive when buyers have dominated so far today and negative when sellers have dominated.

Because futures markets close at 6 PM ET, the running total resets exactly then, mirroring the way most intraday traders think in terms of a single session. Throughout the day, you will see this running total move up or down according to whether more volume is happening on green or red candles. Once the total goes above a number you specify (for example, one hundred thousand contracts), the indicator will place a small “Long” label at that candle on the main price chart to let you know buying pressure has reached that level. Similarly, once the total goes below a negative number you choose (for example, minus one hundred thousand), a “Short” label will appear at that candle to signal that selling pressure has reached your chosen threshold. You can set these threshold numbers to whatever makes sense for your trading style or the market you follow.

Because raw volume alone never turns negative, this design uses candle direction as a sign. Green candles (where the close is higher than the open) add volume, and red candles (where the close is lower than the open) subtract volume. Summing those signed volume values tells you in a single number whether buying or selling has been stronger so far today. That number resets every evening, so it does not carry over any buying or selling from previous sessions.

Once you have this indicator on your chart, you simply watch the “summed volume” line as it moves throughout the day. If it climbs past your long threshold, you know buyers are firmly in control and a long entry might make sense. If it falls past your short threshold, you know sellers are firmly in control and a short entry might make sense. In quieter markets or times of low volume, you might use a smaller threshold so that even modest buying or selling pressure will trigger a label. During very active periods, a larger threshold will prevent too many signals when volume spikes frequently.

This approach is straightforward but can be surprisingly powerful. It does not rely on complex formulas or hidden statistical measures. Instead, it simply adds and subtracts daily volume based on candle color, then alerts you when that total reaches levels you care about. Over several years of historical testing, this formula has shown an ability to highlight moments when intraday sentiment shifts decisively from buyers to sellers or vice versa. Because the indicator resets every day at 6 PM, it always reflects only today’s sentiment and remains easy to interpret without carrying over past data. You can use it on any intraday timeframe, but it works especially well on five-minute or fifteen-minute charts for futures contracts.

If you want a clear gauge of whether buyers or sellers are dominating in real time, and you prefer a rule-based method rather than a complex model, this indicator gives you exactly that. It shows net buying or selling pressure at a glance, resets each session like most intraday traders do, and marks the moments when that pressure crosses the levels you decide are important. By combining a daily reset with signed volume, you get a single number that tells you precisely what the crowd is doing at any given moment, without any of the guesswork or hidden calculations that more complicated indicators often carry.

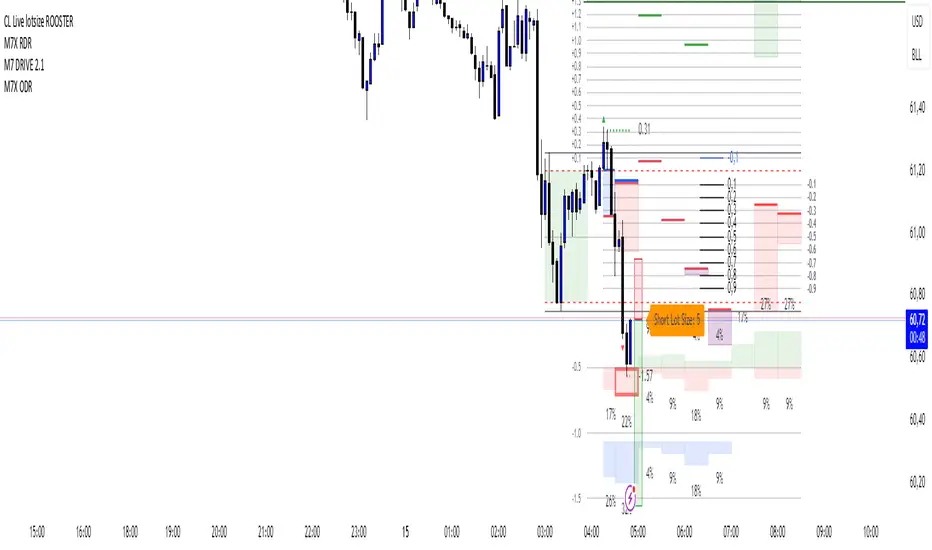

CL Live lotsize ROOSTER📄 Description:

This is a utility script designed for manual futures traders who enter with market orders and want to size their positions precisely based on $ risk.

⚙️ Features:

✅ Calculates live contract size based on:

A fixed dollar risk amount (e.g. $100)

A manually set static stop-loss price

The live market price as your entry

✅ Uses a configurable risk-reward ratio (e.g. 1:3)

✅ Plots entry, stop, and target levels on the chart

✅ Displays calculated contract size as a floating label

🎯 Why this tool?

Built to support fast execution workflows , this tool helps traders who:

Enter trades at candle close or open

Want to pre-calculate their market order size before the signal

Prefer a visual, consistent, real-time R:R validation system

Avoid fumbling with the long/short position tool at the last second

🔧 Settings:

Static Stop-Loss Price: Enter the price level where you'd place your SL

Account Risk ($): How much you’re willing to risk per trade

Risk-Reward Ratio: Set your target multiplier (e.g. 3 for 3R)

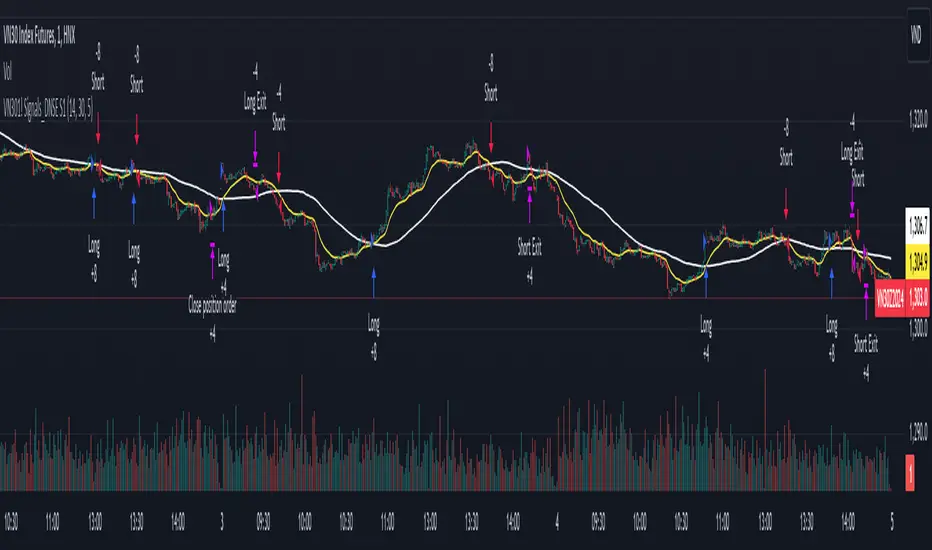

DNSE VN301!, SMA & EMA Cross StrategyDiscover the tailored Pinescript to trade VN30F1M Future Contracts intraday, the strategy focuses on SMA & EMA crosses to identify potential entry/exit points. The script closes all positions by 14:25 to avoid holding any contracts overnight.

HNX:VN301!

www.tradingview.com

Setting & Backtest result:

1-minute chart, initial capital of VND 100 million, entering 4 contracts per time, backtest result from Jan-2024 to Nov-2024 yielded a return over 40%, executed over 1,000 trades (average of 4 trades/day), winning trades rate ~ 30% with a profit factor of 1.10.

The default setting of the script:

A decent optimization is reached when SMA and EMA periods are set to 60 and 15 respectively while the Long/Short stop-loss level is set to 20 ticks (2 points) from the entry price.

Entry & Exit conditions:

Long signals are generated when ema(15) crosses over sma(60) while Short signals happen when ema(15) crosses under sma(60). Long orders are closed when ema(15) crosses under sma(60) while Short orders are closed when ema(15) crosses over sma(60).

Exit conditions happen when (whichever came first):

Another Long/Short signal is generated

The Stop-loss level is reached

The Cut-off time is reached (14:25 every day)

*Disclaimers:

Futures Contracts Trading are subjected to a high degree of risk and price movements can fluctuate significantly. This script functions as a reference source and should be used after users have clearly understood how futures trading works, accessed their risk tolerance level, and are knowledgeable of the functioning logic behind the script.

Users are solely responsible for their investment decisions, and DNSE is not responsible for any potential losses from applying such a strategy to real-life trading activities. Past performance is not indicative/guarantee of future results, kindly reach out to us should you have specific questions about this script.

---------------------------------------------------------------------------------------

Khám phá Pinescript được thiết kế riêng để giao dịch Hợp đồng tương lai VN30F1M trong ngày, chiến lược tập trung vào các đường SMA & EMA cắt nhau để xác định các điểm vào/ra tiềm năng. Chiến lược sẽ đóng tất cả các vị thế trước 14:25 để tránh giữ bất kỳ hợp đồng nào qua đêm.

Thiết lập & Kết quả backtest:

Chart 1 phút, vốn ban đầu là 100 triệu đồng, vào 4 hợp đồng mỗi lần, kết quả backtest từ tháng 1/2024 tới tháng 11/2024 mang lại lợi nhuận trên 40%, thực hiện hơn 1.000 giao dịch (trung bình 4 giao dịch/ngày), tỷ lệ giao dịch thắng ~ 30% với hệ số lợi nhuận là 1,10.

Thiết lập mặc định của chiến lược:

Đạt được một mức tối ưu ổn khi SMA và EMA periods được đặt lần lượt là 60 và 15 trong khi mức cắt lỗ được đặt thành 20 tick (2 điểm) từ giá vào.

Điều kiện Mở và Đóng vị thế:

Tín hiệu Long được tạo ra khi ema(15) cắt trên sma(60) trong khi tín hiệu Short xảy ra khi ema(15) cắt dưới sma(60). Lệnh Long được đóng khi ema(15) cắt dưới sma(60) trong khi lệnh Short được đóng khi ema(15) cắt lên sma(60).

Điều kiện đóng vị thể xảy ra khi (tùy điều kiện nào đến trước):

Một tín hiệu Long/Short khác được tạo ra

Giá chạm mức cắt lỗ

Lệnh chưa đóng nhưng tới giờ cut-off (14:25 hàng ngày)

*Tuyên bố miễn trừ trách nhiệm:

Giao dịch hợp đồng tương lai có mức rủi ro cao và giá có thể dao động đáng kể. Chiến lược này hoạt động như một nguồn tham khảo và nên được sử dụng sau khi người dùng đã hiểu rõ cách thức giao dịch hợp đồng tương lai, đã đánh giá mức độ chấp nhận rủi ro của bản thân và hiểu rõ về logic vận hành của chiến lược này.

Người dùng hoàn toàn chịu trách nhiệm về các quyết định đầu tư của mình và DNSE không chịu trách nhiệm về bất kỳ khoản lỗ tiềm ẩn nào khi áp dụng chiến lược này vào các hoạt động giao dịch thực tế. Hiệu suất trong quá khứ không chỉ ra/cam kết kết quả trong tương lai, vui lòng liên hệ với chúng tôi nếu bạn có thắc mắc cụ thể về chiến lược giao dịch này.

Failed Breakdown Detection'Failed Breakdowns' are a popular set up for long entries.

In short, the set up requires:

1) A significant low is made ('initial low')

2) Initial low is undercut with a new low

3) Price action then 'reclaims' the initial low by moving +8-10 points from the initial low

This script aims at detecting such set ups. It was coded with the ES Futures 15 minute chart in mind but may be useful on other instruments and time frames.

Business Logic:

1) Uses pivot lows to detect 'significant' initial lows

2) Uses amplitude threshold to detect a new low beneath the initial low; used /u/ben_zen script for this

3) Looks for a valid reclaim - a green candle that occurs within 10 bars of the new low

4) Price must reclaim at least 8 points for the set up to be valid

5) If a signal is detected, the initial low value (pivot low) is stored in array that prevents duplicate signals from being generated.

6) FBD Signal is plotted on the chart with "X"

7) Pivot low detection is plotted on the chart with "P" and a label

8) New lows are plotted on the chart with a blue triangle

Notes:

User input

- My preference is to use the defaults as is, but as always feel free to experiment

- Can modify pivot length but in my experience 10/10 work best for pivot lows

- New low detection - 55 bars and 0.05 amplitude work well based on visual checks of signals

- Can modify the number of points needed to reclaim a low, and the # of bars limit under which this must occur.

Alerts:

- Alerts are available for detection of new lows and detection of failed breakdowns

- Alerts are also available for these signals but only during 7:30PM-4PM EST - 'prime time' US trading hours

Limitations:

- Current version of the script only compares new lows to the most recent pivot low, does not look at anything prior to that

- Best used as a discretionary signal

Visit /u/ben_zen's Profile:

www.tradingview.com

Profile Link www.tradingview.com

[ElThibZ] - Futures Lot Size CalculatorI’m sharing a simple script to calculate position size for futures.

You only need to enter:

the risk in USD you’re willing to take

the stop-loss distance in ticks

The script will automatically calculate the correct position size (number of contracts) and display it in the table.

This tool is designed to avoid sizing mistakes, especially on futures where contract multipliers and tick values can easily lead to incorrect risk calculations.

I hope it will be as useful to you as it has been for me.

VWATR + VIX + VVIX Trend Regime### 🤖 VWATR + VIX + VVIX Trend Regime — Your Ultimate Volatility Dashboard! 📊

This isn't just another indicator; it's a comprehensive dashboard that brings together everything you need to understand market volatility focused on Futures. It merges price-based movement with market-wide fear and sentiment, giving you a powerful edge in your trading and risk management. Think of it as your personal volatility sidekick, ready to help you navigate market uncertainty like a pro!

***

### ✨ What's Inside?

* **VWATR (Volume-Weighted ATR):** A super-smart measure of price movement that pays close attention to where the big money is flowing.

* **VIX (The "Fear Gauge"):** Tracks the expected volatility of the S&P 500, essentially telling you how nervous the market is feeling.

* **VVIX (The "VIX of VIX"):** This one's for the pros! It measures how volatile the VIX itself is, giving you an early heads-up on potential fear spikes.

* **VX Term Structure:** A clever way to see if traders are preparing for a crisis. It compares the two nearest VIX futures to spot a rare signal called "backwardation."

* **Z-Scores:** It helps you spot when VIX and VVIX are at historic highs or lows, making it easier to predict when things might return to normal.

* **Divergence Score:** A unique tool to flag potential market shifts when the VIX and VVIX start moving in completely different directions.

* **Regime Classification:** The script automatically labels the market as "Full Panic," "Known Crisis," "Surface Calm," "Stress," or "Normal," so you always know where you stand.

* **Gradient Bars:** A visual treat! The background of your chart changes color to reflect real-time volatility shifts, giving you an instant feel for the market's mood.

* **Alerts:** Get push notifications on your phone for key events like "Full Panic" or "Backwardation" so you never miss a beat.

***

### 📝 Panel/Table Outputs

This is your mission control! The on-screen table gives you a clean summary of the current market regime, VIX and VVIX values, their ratios, term structure, Z-scores, and signals. Everything you need, right where you can see it.

***

### 🚀 How to Get Started

1. **Check your data:** You'll need access to real-time data for VIX, VVIX, VX1!, and VX2!. A paid subscription might be necessary for this.

2. **Add it to your chart:** Use the indicator on any chart (we've set it to `overlay=false`) to get your full volatility dashboard.

3. **Tweak it to perfection:** Head over to the Settings panel to customize the thresholds, colors, and your all-important "Jolt Value."

4. **Start trading smarter:** Use the dashboard to inform your trades, hedge your portfolio, and manage risk with confidence.

***

### ⚙️ Customization & Key Settings

* `showVWATR`: Toggle your price-volatility metric on or off.

* `showExpectedVol`: See the expected volatility as a percentage of the current price.

* `joltLevel`: This is a very important line on your chart! It's your personal trigger for when volatility is getting a little too wild. More on this below.

* `enableGradientBars`: Turn the awesome colored background on or off.

* `enableTable`: Hide or show your information table.

* `VIX/VVIX/VX1!/VX2! symbols`: If your broker uses different symbols for these, you can change them here.

* `VIX/VVIX thresholds`: Adjust these levels to fine-tune the indicator to your personal risk tolerance.

***

### 💡 Jolt Value: A Quick Guide for Smart Traders 🧠

The **jolt value** is your personal tripwire for volatility. Think of it as a warning light on your car's dashboard. You set the level, and when volatility (VWATR) crosses that line, you get an instant signal that something interesting is happening.

**How to Set Your Jolt Value:**

The ideal jolt value is dynamic. You want to keep it just a little above the current VIX level to stay alert without getting too many false alarms.

| Current VIX Level | Market Regime | Recommended Jolt Value |

| :--- | :--- | :--- |

| Under 15 | Calm/Complacent | 15–16 |

| 15–20 | Typical/Normal | 16–18 |

| 20–30 | Cautious/Active | 18–22 |

| Over 30 | Stress/Panic | 30+ |

**A Pro Tip for August 2025:** Since the VIX is hovering around 14.7, setting your jolt value to **16.5** is a great starting point for keeping an eye on things. If the VIX starts to climb above 20, you should adjust your jolt level to match the new reality.

***

### ⚠️ Important Things to Note

* You might experience some data delays if you're not on a paid TradingView plan or your broker does not provide real-time data for the VIX also VIX is only active during NY session, so it's not advised to use it outside of normal trading hours!

EMA Trend Dashboard

Trend Indicator using 3 custom EMA lines. Displays a table with 5 rows(position configurable)

-First line shows relative position of EMA lines to each other and outputs Bull, Weak Bull, Flat, Weak Bear, or Bear. EMA line1 should be less than EMA line2 and EMA line 2 should be less than EMA line3. Default is 9,21,50.

-Second through fourth line shows the slant of each EMA line. Up, Down, or Flat. Threshold for what is considered a slant is configurable. Also added a "steep" threshold configuration for steep slants.

-Fifth line shows exhaustion and is a simple, configurable calculation of the distance between EMA line1 and EMA line2.

--Lines one and five change depending on its value but ALL other colors are able to be changed.

--Default is somewhat set to work well with Micro E-mini Futures but this indicator can be changed to work on anything. I created it to help get a quick overview of short-term trend on futures. I used ChatGPT to help but I am still not sure if it actually took longer because of it.

Fed Fund Futures Custom AverageThis indicator helps traders track the expected average interest rate for the upcoming 12 months based on Fed Fund Futures. It calculates the average price of the next 12 monthly futures contracts and also shows the spread against the 1-Year US Treasury yield (US01Y). This can be useful for understanding market expectations regarding interest rate changes and identifying trading opportunities related to interest rate movements.

Arbitrage B3's IBOV FuturesThis indicator was made to calculate and show the spread between the B3's Ibovespa Futures and B3's Ibovespa Index increased by the Interest until the contract expiration date.

The orange line "Arbitrage" is the spread.

Inputs:

Annual Interest Rate (%) -> Interest Rate that you want to be used to calculate the Interest of B3's IBOV Index.

Working Days Until Contract Expires -> How many business days you have between your actual date and the expiration date of the Futures.

Recommended TimeFrame to evaluate the "Arbitrage": 1 MIN

EMA Fractal Bias"EMA Fractal Bias" overlays on TradingView charts to detect directional bias for scalping on futures like NQ/ES.

It computes three smoothed EMAs (fast 3/2, mid 9/3, slow 20/5, configurable) for stacking checks (bullish: fast > mid > slow; bearish: reverse).

Williams Fractals (period 2 default) identify potential breaks: close above up-fractal high for long, below down-fractal low for short.

Bias logic: Tracks last up/down fractal. On break, if stacked aligns, sets bias (long/short) and resets broken fractal. If no stack, sets pending flag and neutral bias; confirms on later bars if stack turns true.

Shading teal for long, purple for short, orange for neutral, with intra-bar previews.

Debug toggle adds event labels and status on last bar.

Non-repainting, evaluates on close.

Session Opening Bar RangeSession Opening Bar Range (OBR) - Advanced Opening Range Indicator with Statistical Analysis

Overview

The Session First Bar Range (FBR) indicator is a comprehensive tool that captures and projects key levels based on the first bar of a user-defined trading session. Unlike traditional daily opening range indicators, this script allows traders to focus on specific session windows (New York RTH, London, Asia, etc.) and analyze price behavior relative to the initial momentum established in that session's opening bar.

What makes this indicator unique is its combination of three distinct projection methodologies: statistical analysis based on historical range data, Fibonacci extensions, and fixed-point rotation levels commonly used by institutional traders. To our knowledge, this is the only opening range indicator that incorporates statistical standard deviation levels calculated from historical first bar ranges, making it both a technical and probabilistic tool.

Core Concept

The opening range concept is based on the principle that the initial price action of a trading session often sets the tone for the remainder of that session.

Professional traders have long observed that:

The first bar's high and low act as key reference points

Price often respects or breaks these levels with significance

Expansion beyond the opening range tends to occur in measurable increments

This indicator takes these observations and enhances them with:

Historical probability analysis - "Based on the last 60 sessions, price typically extends X standard deviations beyond the opening range"

Proportional projections - Fibonacci-based extensions showing where measured moves typically target

Fixed-point rotations - Institutional rotation levels (e.g., 65 points for NQ, 15 points for ES)

How It Works

Session Detection & First Bar Capture

The indicator uses Pine Script's time() function with timezone support to precisely detect when a trading session begins. When the first bar of the selected timeframe occurs within the session window, the script captures:

High (H): The high of the first bar

Low (L): The low of the first bar

Mid (M): The midpoint (hl2) of the first bar

Critical Detail: These levels are fixed from the first bar only - they do not update as the session progresses. This differs from many "opening range" indicators that use a time period (e.g., first 30 minutes). Here, you select the bar timeframe (default 5-minute), and only that single first bar's range is captured.

Statistical Level Calculation

The indicator maintains a rolling array of the last N session's first bar ranges (default: 60 sessions). For each new session, it calculates:

Average Range: Mean of historical first bar ranges

Standard Deviation: Volatility of those ranges

Projection Levels: High/Low ± (Average Range + Std Dev × Multiplier)

This provides probability-based levels. For example, a +2σ level suggests: "Historically, price extending this far beyond the opening range is a 2-standard-deviation event (approximately 95th percentile)."

Fibonacci Extensions

Using the first bar range as the base unit (100%), the indicator projects Fibonacci levels:

100% extension: One full range above the high / below the low

1.618x extension: (Default) Golden ratio projection

2.618x, 3.618x extensions: Additional Fibonacci levels

Calculation: Range = H - L, then Target = H + (Range × Multiplier) for upside projections.

OR Rotation Levels

These are fixed-point increments from the first bar's high and low. Unlike percentage-based methods, rotations use absolute point values:

NQ traders often use 65-point increments

ES traders often use 15-point increments

Gold/bonds use different values

The indicator draws 5 levels above the high (R+1 through R+5) and 5 below the low (R-1 through R-5), each separated by your specified point increment.

Features:

Session Options

Pre-configured Sessions:

New York RTH (9:30am - 4:00pm)

New York Futures (8:00am - 5:00pm)

London (2:00am - 8:00am)

Asia (7:00pm - 2:00am)

Midnight to 5pm

ZB/Gold/Silver OR (8:20am - 4:00pm)

CL OR (9:00am - 4:00pm)

Custom Session: Define your own start/end times in HHMM format

Timezone Support: All sessions respect the selected timezone (default: America/New_York)

Customizable Timeframe

Select any timeframe for the first bar (1min, 5min, 15min, etc.)

Default: 5-minute bars

Important: This is the timeframe for the first bar capture, independent of your chart's timeframe

Display Options

Historical Ranges: Show/hide past session ranges (with configurable limit to manage performance)

Line Styles: Choose between Solid, Dashed, or Dotted for range lines and midline

Label Position: Left or Right side of range

Show Prices: Optionally display actual price values on labels

Custom Colors: Fully customizable colors for all components

Statistical Levels

Lookback Period: Number of historical sessions to analyze (default: 60)

Two Multiplier Levels: Default 1σ and 2σ, fully adjustable

Separate styling: Different line styles (dashed vs dotted) for each sigma level

Optional Labels: Show/hide sigma notation labels

Fibonacci Extensions

Four Extension Levels: 100%, 1.618x, 2.618x, 3.618x (all customizable)

Bidirectional: Projections both above and below the opening range

Optional Labels: Toggle percentage/multiplier labels

OR Rotation Levels

Configurable Increment: Set the point value for your instrument

Five Levels Each Direction: R±1 through R±5

Dynamic Labels: Show both rotation number and point value (e.g., "R+1 (65)")

Three Line Styles: Solid, Dashed, or Dotted

How to Use

Setup

Add the indicator to your chart

Select your trading session from the dropdown

Set the timeframe for first bar capture (typically 5-15 minutes)

Configure which projection methods you want to see (Statistical, Fibonacci, and/or Rotations)

For Day Traders

Scenario: Trading NQ during New York RTH

Session: Select "New York RTH (9:30am - 4:00pm)"

Timeframe: 5-minute (captures 9:30-9:35 bar)

Enable: OR Rotations with 65-point increments

Strategy:

Watch for acceptance/rejection at rotation levels

Use R+1/R-1 as initial profit targets

R+2/R-2 as extended targets

Statistical levels show when price is in "outlier" territory

and rotation levels

Performance Notes

The indicator limits objects to stay within TradingView's constraints (500 max)

If you enable all features, reduce "Maximum Historical Ranges" to prevent slowdown

Typical configuration: 10-20 historical ranges with all features enabled works well

Settings Guide

Session Settings

Session: Choose from pre-configured sessions or "Custom"

Custom Session Start/End: HHMM format (e.g., "0930" for 9:30am)

Timezone: Critical for accurate session detection

Opening Bar Format

Timeframe: The bar size for capturing the first bar's range

Show Midline: Toggle the mid-point line

Show Historical Ranges: Display previous sessions (recommended: leave ON)

Maximum Historical Ranges: Limit history to manage performance (1-500)

Range Style / MidLine Style: Solid, Dashed, or Dotted

Position: Label placement (Left or Right)

Show Prices: Include actual price values on labels

Statistical Levels

Lookback Periods: How many historical first bar ranges to analyze (default: 60)

Std Dev Multiplier 1/2: The sigma levels to project (default: 1.0 and 2.0)

All visual settings (colors, line width, label size)

Fibonacci Extensions

Show Fib Extensions: Enable/disable Fibonacci projections

Measured Move Extensions 1-4: The multipliers (default: 1.618, 2.618, 3.618, 4.618)

Visual customization options

OR Rotations

Rotation Increment: The point value for your instrument

NQ: 65 points

ES: 15 points

Adjust for other instruments based on their typical rotation behavior

Show Rotation Labels: Display level numbers and point values

Visual customization options

Use Cases

Gap Trading: When price gaps away from previous day's close, the first bar range shows the initial gap acceptance/rejection zone

Breakout Confirmation: Price breaking and holding above the first bar high with volume suggests trend day potential. Rotation levels provide measured targets.

Reversal Identification: Price reaching +2σ statistical level = rare event, potential exhaustion

Range Bound Days: Price oscillating between first bar high/low suggests range-bound session; trade reversals at extremes

Institutional Level Awareness: OR Rotations at 65 points (NQ) align with levels professional traders watch

Technical Notes

The indicator uses request.security() with lookahead=barmerge.lookahead_on to ensure the first bar levels are captured correctly

All drawing objects (lines, labels, fills) are managed in arrays with automatic cleanup to prevent memory issues

The statistical calculations use array.avg() and array.stdev() for accurate probability estimates

Rotation levels use individual line variables (like Fibonacci) rather than loops for reliability

Summary

This indicator is original in its combination of three distinct methodologies for projecting levels from a session's opening range:

Statistical Analysis - No other opening range indicator (to our knowledge) calculates standard deviation projections from historical first bar ranges

Time-Based Session Flexibility - Most OR indicators use only daily or fixed time periods; this allows any custom session window

Multiple Projection Methods - Traders can use statistical, Fibonacci, AND rotation levels together or separately

Future Risk CalculatorCreated out of revenge against the difficulty of controlling psychology, greed, and risk management. Designed for cryptocurrency futures trading by following the risk management principles from Kevin Sailly. Very welcome if there are suggestions and input to improve the quality of this "indicator". Please use wisely.

How to use:

1. Open indicator settings.

2. Fill out all the forms. (Note: I make Max Loss Risk only has 5 options. Because, you know, to control the greed. You can choose by considering your risk profiles and market condition)

3. All of the information and calculation will appear on the label (right side of the bar chart) and top-right box.

4. You can adjust the three prices (target, entry, and stop) by clicking any part of the indicator. There will be three dots in the middle of the chart window (align with three prices). Click that dots and drag them up/down to customize according to your wishes. The price order must be correct, for LONG direction the price order from the top is target-entry-stop. Vice versa for SHORT direction. There will be "SETUP ERROR" text in the top-right box if the price order is not correct.

"Never, ever argue with your trading system." (by Michael Covel)

Regards,

Ircham

ES/NQ Levels: ON / PD(RTH) / PW / PM + ATH (NY)Simple script adding lines for

Overnight high

Overnight low

Previous day high

Previous day low

Previous week high

Previous week low

Previous month high

Previous month low

All time high

You can enable/disable each one and select the color.

Only works on futures.