Industry Group Strength - IndiaPresenting the Industry Group Strength Indicator for India market, designed to help traders identify top-performing stocks within specific industry groups that are predefined.

⦿ Identifies Leading Stocks in Industry Groups

⦿ Analyses the following metrics

YTD Return : Measures stock performance from the start of the year.

RS Rating : Relative Strength rating for user-selected periods.

% Return : Percentage return over a user-selected lookback period.

Features

This indicator dynamically recognises the industry group of the current stock on the chart and ranks stocks within that group based on predefined data points. Traders can add this indicator to focus on top-performing stocks relative to their industry.

⦿ Color-coded for Easy Visualisation

You can choose from the following key metrics to rank stocks:

YTD Return

RS Rating

% Return

⦿ Table Format with Performance Metrics Compact mode

Vertical View

Horizontal View

All of the three metrics are shown in the compact mode and the current stock that is viewed is highlighted!

Vertical view

Horizontal view

Stock Ranking

Stocks are ranked based on their performance within industry groups, enabling traders to easily spot leaders and laggards in each sector. Color-coded gradients visually represent the stocks’ performance rankings, with higher percentile rankings indicating better performance.

Relative Strength (RS)

Relative Strength (RS) compares a stock’s performance against the benchmark index. The RS value is normalized from 1 to 99, making it easier to compare across different stocks. A rising RS value indicates that the stock is outperforming the market, helping traders quickly gauge relative performance within industry groups.

Limitations

At the time of developing this indicator, Pine requests are limited to 40 per script so the predefined symbols had to be filtered to 40 per Industry group

Stocks Filters

Filters that are used to filter the stocks in an Industry group to have maximum of 40 stocks

⦿ Auto, Chemical, Engineering, Finance, Pharma

Market Cap >= 1000 Crores and Market Cap <= 60000 Crores

Price >= 30 and Price <= 6000

50 Days Average ( Price * Volume ) >= 6 Crores

⦿ For rest of the Industry groups

Market Cap >= 1000 Crores and Market Cap <= 100000 Crores

Price >= 20 and Price <= 10000

50 Days Average ( Price * Volume ) >= 3 Crores

Credits

This indicator is forked from the Script for US market by @Amphibiantrading Thanks Brandon for the beginning of this indicator.

This indicator is built on TradingView’s new dynamic requests feature, thanks to @PineCoders for making this possible!

Komut dosyalarını "6000亿美元" için ara

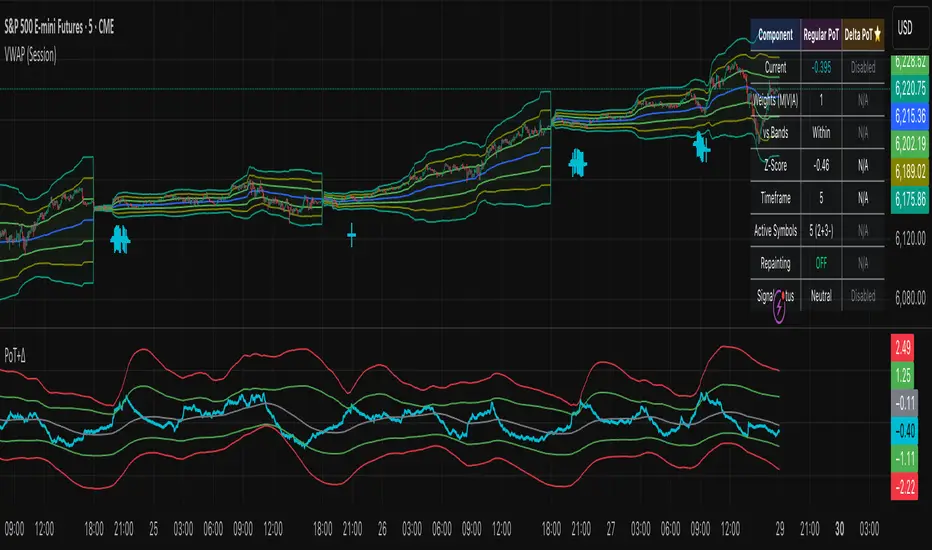

Project SynthIntroducing Project Synth !

Inspired by Pace of Tape and Cumulative Delta I created Project Synth in order to aggregate volume flow data across multiple marketsfor two primary reasions:

Traditional orderflow tools are not available on Tradingview. My script attempts to bring an original; calculus-based approach to creating not only an alternative for traditional orderflow tools, but also a more accurate one.

In order to detect genuine buying and selling pressure that cannot be easily manipulated. I did this because while I've always enjoyed concept behind both of those tools, I did not think they captured enough data to be useful. By analyzing assets that move together (positive correlation) and assets that move inversely (negative correlation), my system aims to fix the fundamental problems with those indicators and create an objective view of market sentiment based on aggregate orderflow.

Some more detailed explanations (using QQQ and SQQQ as an example):

Inverse Market Dynamics (QQQ vs SQQQ):

In an inverse market like SQQQ, aggressive buyers hit the ask when they expect the underlying (QQQ) to fall, while passive buyers wait on the bid hoping for cheaper inverse exposure. When QQQ rallies, SQQQ sees aggressive selling (people dumping their bearish bets) hitting bids, while passive sellers sit on the ask hoping to exit at better prices. The aggression flows opposite to the underlying market direction.

Why Utilizing Both Markets Provides A More Accurate Delta:

Watching both QQQ and SQQQ gives cross-validation - real buying pressure in QQQ should coincide with selling pressure in SQQQ. If you see buying in QQQ but also buying in SQQQ, that's a conflicting signal suggesting the move might be artificial or driven by other factors. The inverse relationship acts as a confirmation filter, making false signals much harder to generate.

Multiple Markets = Authentic Pressure:

The more unique, important markets you track, the harder it becomes to create fake delta moves. Real institutional buying/selling pressure affects multiple correlated assets simultaneously in predictable patterns - you can't easily manipulate tech stocks, treasury bonds, VIX, and currency pairs all at once to create a false signal. Each additional market acts as a fraud detection layer, ensuring the delta measurement reflects genuine ecosystem-wide buying and selling pressure rather than isolated manipulation or noise.

My Suggestions For Usage:

In order to keep the explanation simple and short for now, I suggest using it just like a cumulative delta indicator. For example: let's say you were watching CME_MINI:ES1! , and you had a resistance level at 6000. When the price reaches your resistance level, you would be looking for a significant divergence between price and Delta. Price : rising, Delta : falling. This means that even though the price was going up, strong and aggressive sellers are jumping in more and more, this can be used as a confirmation tool for a resistance level.

Notes For Moderators, Authors and Users:

Firstly, to the best of my knowledge, I have not been able to find many tools built around the concept of cumulative delta or pace of tape. While I know there are a couple projects, none to the magnitude of synthetically recreating these tools via an algorithm designed around basic calculus principles. While tools like Volume Delta are built in, they do not attempt to capture an accurate picture of aggregated orderflow from what I understand.

Secondly, it needs to be noted that tool aims to create an approximation of buying and selling pressure. To my knowledge it is not possible to create an accurate full picture, at least not within the limitations of Tradingview.

Polyline PlusThis library introduces the `PolylinePlus` type, which is an enhanced version of the built-in PineScript `polyline`. It enables two features that are absent from the built-in type:

1. Developers can now efficiently add or remove points from the polyline. In contrast, the built-in `polyline` type is immutable, requiring developers to create a new instance of the polyline to make changes, which is cumbersome and incurs a significant performance penalty.

2. Each `PolylinePlus` instance can theoretically hold up to ~1M points, surpassing the built-in `polyline` type's limit of 10K points, as long as it does not exceed the memory limit of the PineScript runtime.

Internally, each `PolylinePlus` instance utilizes an array of `line`s and an array of `polyline`s. The `line`s array serves as a buffer to store lines formed by recently added points. When the buffer reaches its capacity, it flushes the contents and converts the lines into polylines. These polylines are expected to undergo fewer updates. This approach is similiar to the concept of "Buffered I/O" in file and network systems. By connecting the underlying lines and polylines, this library achieves an enhanced polyline that is dynamic, efficient, and capable of surpassing the maximum number of points imposed by the built-in polyline.

🔵 API

Step 1: Import this library

import algotraderdev/polylineplus/1 as pp

// remember to check the latest version of this library and replace the 1 above.

Step 2: Initialize the `PolylinePlus` type.

var p = pp.PolylinePlus.new()

There are a few optional params that developers can specify in the constructor to modify the behavior and appearance of the polyline instance.

var p = pp.PolylinePlus.new(

// If true, the drawing will also connect the first point to the last point, resulting in a closed polyline.

closed = false,

// Determines the field of the chart.point objects that the polyline will use for its x coordinates. Either xloc.bar_index (default), or xloc.bar_time.

xloc = xloc.bar_index,

// Color of the polyline. Default is blue.

line_color = color.blue,

// Style of the polyline. Default is line.style_solid.

line_style = line.style_solid,

// Width of the polyline. Default is 1.

line_width = 1,

// The maximum number of points that each built-in `polyline` instance can contain.

// NOTE: this is not to be confused with the maximum of points that each `PolylinePlus` instance can contain.

max_points_per_builtin_polyline = 10000,

// The number of lines to keep in the buffer. If more points are to be added while the buffer is full, then all the lines in the buffer will be flushed into the poylines.

// The higher the number, the less frequent we'll need to // flush the buffer, and thus lead to better performance.

// NOTE: the maximum total number of lines per chart allowed by PineScript is 500. But given there might be other places where the indicator or strategy are drawing lines outside this polyline context, the default value is 50 to be safe.

lines_bffer_size = 50)

Step 3: Push / Pop Points

// Push a single point

p.push_point(chart.point.now())

// Push multiple points

chart.point points = array.from(p1, p2, p3) // Where p1, p2, p3 are all chart.point type.

p.push_points(points)

// Pop point

p.pop_point()

// Resets all the points in the polyline.

p.set_points(points)

// Deletes the polyline.

p.delete()

🔵 Benchmark

Below is a simple benchmark comparing the performance between `PolylinePlus` and the native `polyline` type for incrementally adding 10K points to a polyline.

import algotraderdev/polylineplus/2 as pp

var t1 = 0

var t2 = 0

if bar_index < 10000

int start = timenow

var p = pp.PolylinePlus.new(xloc = xloc.bar_time, closed = true)

p.push_point(chart.point.now())

t1 += timenow - start

start := timenow

var polyline pl = na

var points = array.new()

points.push(chart.point.now())

if not na(pl)

pl.delete()

pl := polyline.new(points)

t2 += timenow - start

if barstate.islast

log.info('{0} {1}', t1, t2)

For this benchmark, `PolylinePlus` took ~300ms, whereas the native `polyline` type took ~6000ms.

We can also fine-tune the parameters for `PolylinePlus` to have a larger buffer size for `line`s and a smaller buffer for `polyline`s.

var p = pp.PolylinePlus.new(xloc = xloc.bar_time, closed = true, lines_buffer_size = 500, max_points_per_builtin_polyline = 1000)

With the above optimization, it only took `PolylinePlus` ~80ms to process the same 10K points, which is ~75x the performance compared to the native `polyline`.

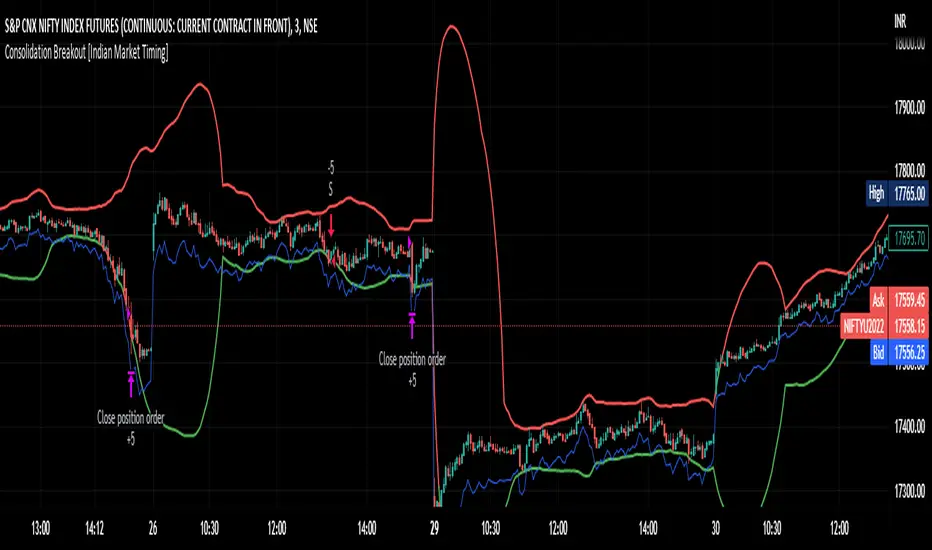

Consolidation Breakout [Indian Market Timing]OK let's get started ,

A Day Trading (Intraday) Consolidation Breakout Indication Strategy that explains time condition for Indian Markets .

The commission is also included in the strategy .

The basic idea is ,

1) Price crosses above upper band , indicated by a color change (green) is the Long condition .

2) Price crosses below lower band , indicated by a color change (red) is the Short condition .

3) ATR is used for trailing after entry

// ═══════════════════════════════//

// ————————> TIME CONDITION <————————— //

// ═══════════════════════════════//

The Indian Markets open at 9:15am and closes at 3:30pm.

The time_condition specifies the time at which Entries should happen .

"Close All" function closes all the trades at 2:57pm.

All open trades get closed at 2:57pm , because some brokers dont allow you to place fresh intraday orders after 3pm.

NSE:NIFTY1!

// ═══════════════════════════════════════════════ //

// ————————> BACKTEST RESULTS ( 114 CLOSED TRADES )<————————— //

// ═══════════════════════════════════════════════ //

LENGTH , MULT (factor) and ATR can be changed for better backtest results.

The strategy applied to NIFTY (3 min Time-Frame and contract size 5) gives us 60% profitability , as shown below

It was tested for a period a 8 months with a Profit Factor of 2.2 , avg Trade of 6000Rs profit and Sharpe Ratio : 0.67

The graph has a Linear Curve with consistent profits.

NSE:NIFTY1!

Save it favorites.

Apply it to your charts Now !!

Thank me later ;)

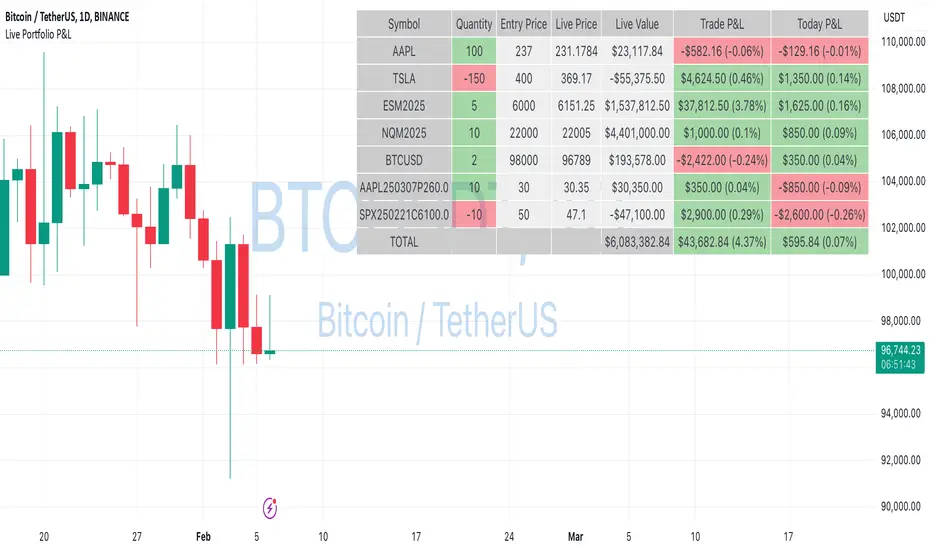

Live Portfolio P<his script calculates live P&L (Profit & Loss) for up to 40 instruments — stocks, ETFs, options, futures, and Forex pairs supported by TradingView. Instead of juggling numerous inputs, you paste your portfolio in CSV format into a single text field, and the script handles the rest. It parses each position and displays a comprehensive table showing the symbol, current price, position value, total P&L, and today’s P&L—all updated in real time.

Key Features

CSV Portfolio Input – Effortlessly import all your positions at once without filling in multiple fields. You can export the position from your broker, save it in the required format, and paste it into this script.

Supports Various Asset Classes – Works with any instrument that TradingView provides data for, including futures, options, and Forex.

Up to 40 Instruments – Track a broad and diverse set of holdings in one place.

Real-Time Updates – Get immediate feedback on live price changes, total value, and current P&L.

Today’s P&L – Monitor your daily performance to gauge short-term trends.

CSV is consumed in the following format:

Symbol (supported TradingView instruments)

Entry Price

Quantity (negative for short position)

Lot Size (for futures/options, it might not be one)

For example:

AAPL,237,100,1

TSLA,400,-150,1

ESM2025,6000,5,50

Planned Enhancements

Multi-Currency Support – Automatically convert and display your positions’ values in different currencies.

Advanced Metrics – Get deeper insights with calculations for drawdown, Sharpe ratio, and more.

Risk Management Tools – Set stop-loss and take-profit levels and receive alerts when thresholds are hit.

Option Greeks & Margin Calculations – Manage complex option strategies and track margin requirements.

Questions for You

What additional features would you like to see?

Are there any specific metrics or analytics you’d find especially valuable?

How might this script fit into your current trading workflow?

Feel free to share your thoughts and suggestions. Your feedback will help shape future updates and make this tool even more helpful for traders like you!

Disclaimer

Please remember that past performance may not be indicative of future results.

Due to various factors, including changing market conditions, the strategy may no longer perform as well as in historical backtesting.

This post and the script don’t provide any financial advice.

Enhanced Volume Profile█ OVERVIEW

The Enhanced Volume Profile (EVP) is an indicator designed to plot a volume profile on the chart based on either the visible chart range or a fixed lookback period. The script helps analyze the distribution of volume at different price levels over time, providing insights into areas of high trading activity and potential support/resistance zones.

█ KEY FEATURES

1. Visible Chart Range vs. Fixed Lookback Depth

Visible Chart Range

- Default analysis mode

- Calculates profile based on visible portion of the chart

- Dynamically updates with chart view changes

Fixed Lookback Depth

- Optional alternative to visible range

- Uses specified number of bars (10-3000)

- Provides consistent analysis depth

- Independent of chart view

2. Custom Resolution

Auto-Resolution Mode

Automatically selects timeframes based on chart's current timeframe:

≤ 1 minute: Uses 1-minute resolution

≤ 5 minutes: Uses 1-minute resolution

≤ 15 minutes: Uses 5-minute resolution

≤ 1 hour: Uses 5-minute resolution

≤ 4 hours: Uses 15-minute resolution

≤ 12 hours: Uses 15-minute resolution

≤ 1 day: Uses 1-hour resolution

≤ 3 days: Uses 2-hours resolution

≤ 1 week: Uses 4-hours resolution

Custom Resolution Override

Optional override of auto-resolution system

Provides control over data granularity

Must be lower than or equal to chart's timeframe

Falls back to auto-resolution if validation fails

3. Volume Profile Resolution

Adjustable number of points (10-400)

Controls profile granularity

Higher resolution provides more detail

Balance between precision and performance

4. Point of Control (PoC)

Identifies price level with highest traded volume

Optional display with customizable appearance

Adjustable line thickness (1-30)

Configurable color

5. Value Area (VA)

Shows price range of majority trading volume

Adjustable coverage (5-95%), default is 68%

Customizable boundary lines

Configurable lines color and thickness (1-20)

█ INPUT PARAMETERS

Lookback Settings

Use Visible Chart Range

- Default: true

- Calculates profile based on visible bars

- Ideal for focused analysis

Fixed Lookback Bars

- Range: 10-3000

- Default: 200

- Used when visible range is disabled

Resolution Settings

Enable Custom Resolution

- Default: false

- Overrides auto-resolution

Custom Resolution

- Default: 1-minute

- Changes automatically when "Enable Custom Resolution" is disabled

Volume Profile Appearance

Profile Resolution

- Range: 10-400

- Default: 200

- Controls detail level

Profile Width Scale

- Range: 1-50

- Default: 15

- Adjusts profile width

Right Offset

- Range: 0-500

- Default: 20

- Controls spacing from price bars

Profile Fill Color

- Default: #5D606B (70% transparency)

Point of Control Settings

Show Point of Control

- Default: true

- Toggles PoC visibility

PoC Line Thickness

- Range: 1-30

- Default: 1

PoC Line Color

- Default: Red

Value Area Settings

Show Value Area

- Default: true

- Toggles VA lines

Value Area Coverage

- Range: 5-95%

- Default: 68%

Value Area Line Color

- Default: Blue

Value Area Line Thickness

- Range: 1-20

- Default: 1

█ TECHNICAL IMPLEMENTATION DETAILS

Exceeding Bars Management

The script dynamically adjusts the number of bars used in the volume profile calculation based on the selected timeframe and the maximum allowed bars (max_bars_back).

If the total number of bars exceeds the predefined threshold (6000 bars), the script reduces the lookback period (lookback_bars) by trimming some of the historical data, ensuring the chart does not become overloaded with data.

The adjustment is made based on the ratio of bars per candle (bars_per_candle), ensuring that the volume profile remains computationally efficient while maintaining its relevance.

█ EXAMPLE USE CASES

1. Visible Range Mode

For analyzing a recent trend and focusing on only the visible part of the chart, enabling the "Use Visible Chart Range" option calculates the profile based on the current view, without considering historical data outside the visible area.

2. Fixed Lookback Depth

For analyzing a specific period in the past (e.g., the last 200 bars), disabling the visible range and setting a fixed lookback depth of 200 bars ensures the profile always considers the last 200 bars, regardless of the visible range.

3. Custom Resolution

If there’s a need for greater control over the timeframe used for volume profile calculations (e.g., using a 5-minute resolution on a 15-minute chart), enabling custom resolution and setting the desired timeframe provides this control.

HAPPY TRADING ✌️