APEX - Moving Averages [v1]A moving average is the most known indicator that takes into consideration price from the last several periods of the price and calculates a smoothed line also known as a Moving average. This way you will cut out a lot of the noise and have a different view.

The most common usage is the moving average crossover system when you buy and sell when a crossover happens. This system is in general not very profitable but can be used effectively in trending markets.

There is really no general rule to what length should be used. The most well-known and respected lengths are 20 / 50 / 100 / 200 for almost all average. These values are respected as strong resistance and support levels. but if you plan to use a crossover Systems the most profitable settings tend to be when the averages are close together 14 and 28 etc. But this is an area I would appeal to for you to really try out what works and what does not.

Other uses of moving averages are the following:

Crossover system

Moving averages are pointing up and price crosses below (Buy Pullback)

The slow-moving average is Below the fast moving average to help to identify possible bullishness

Can be used as support and resistance lines

If you are an advanced user you may want to try out the following techniques:

Create your own moving average by combining several of those together with the source function

Using the Average True Range to create Keltner Channels

Using Standard deviation to create Bollinger bands (Bollinger bands are also accessible on their own)

You can use Moving averages to smooth the noise on other indicators such as RSI / CCI / MFI

Komut dosyalarını "28年大学生毕业人数" için ara

TRADING VIEW INDICATOR - PINE TUTORIAL 5After a long gap, I have written the 5th tutorial for the pine script. You can find the others below, if you read through all of these you should be good to do your own writing.

This script mimics the Trading View Indicator . For example this one below.

www.tradingview.com

It shows the net result of the 28 indicator, either as buy or sell. I have worked hard to make sure it matches the trading view results but I am not in hundred percent agreement with tradingView on SMA, EMA and Ichimoku indicator.

There are many commented plots because I needed to check separately if each indicator is working correctly.

Someone else wrote this code but they did not make it public. It took me about 3 weeks to write this and to be honest it could be cleaner and better commented.

If you find any mistake please let me know. I hope it will be useful in your learning.

Creating long term bitcoin data

One of the problems, with bitcoin, is that we miss long term bitcoin data. There is not a single source from which to gather the value of bitcoin in any moment from it's inception. Or at least from when it was first exchanged into exchanges. If you look at coinmarketcap the data go back to the 28 apr 2013. But mtgox started in July 2010. If you go to yahoo, you will be able to gather data, but once you start working with this data you soon find out how poor is it. Basically it follows mtgox data while mtgox was alive, and then switched to some other exchange. But this means that we see a sudden jump in data which makes any indicator go wild. Basically it's really difficult to gather long term data on bitcoin. Also consider that mtgox did not just "go away" when it stopped trading. But in the database here it is still present with the fixed exchange rate of when it stopped.

So I tried to create the data we need. How? By taking three exchanges, and taking the median between them. The three exchanges I took were MTGOX: , BITFINEX: and KRAKEN: XBTUSD . We cannot avoid mtgox because it's the only source of data for the first years. But then as soon as the other exchanges come in we are going to use the median between them.

The indicator must be overlaid on another chart. And I use the forex usdeur which I then hide (If someone has a better idea, maybe something which is open 24/7, I would be happy to hear it).

Phase Change IndexPhase Change Index script.

This indicator was developed and described by M. H. Pee (Stocks & Commodities V.22:5 (28-37): Phase Change Index).

Other indicators of M. H. Pee:

RSI Oversold bounce - Scaling in levels (30, 28, 26, 24, 22, 20)Oversold bounce entry levels based on RSI

Helps to gauge levels for scaling into a position based on oversold rsi levels.

Trading The Loonie (CADUSD)A port of the trading strategy described at technical.traders.com

"In “Trading The Loonie,” which appeared in the December 2015 issue of STOCKS & COMMODITIES, author Markos Katsanos

explains the heavy correlation between the Canadian dollar and crude oil. He then goes on to describe how one could

trade this correlation. Using similar logic as that employed in Bollinger Bands, Katsanos has built a study to

provide buy and sell signals for trading the Canadian dollar future."

See Also:

- Backtesting and forwardtesting (of TradingView Strategies)

- 9 Mistakes Quants Make that Cause Backtests to Lie (blog.quantopian.com)

- When Backtests Meet Reality (financial-hacker.com)

- Why MT4 backtesting does not work (www.stevehopwoodforex.com)

Ichimoku Cloud StrategyBased on the trading strategy described at

stockcharts.com

See Also:

- Backtesting and forwardtesting (of TradingView Strategies)

- 9 Mistakes Quants Make that Cause Backtests to Lie

- When Backtests Meet Reality

- Why MT4 backtesting does not work

Mean-Reversion Swing Trading Strategy v1A port of the TradeStation EasyLanguage code for a mean-revision strategy described at

traders.com

"In “Mean-Reversion Swing Trading,” which appeared in the December 2016 issue of STOCKS & COMMODITIES, author Ken Calhoun

describes a trading methodology where the trader attempts to enter an existing trend after there has been a pullback.

He suggests looking for 50% pullbacks in strong trends and waiting for price to move back in the direction of the trend

before entering the trade."

See Also:

- 9 Mistakes Quants Make that Cause Backtests to Lie (blog.quantopian.com)

- When Backtests Meet Reality (financial-hacker.com)

- Why MT4 backtesting does not work (www.stevehopwoodforex.com)

Trend Trigger FactorTrend Trigger Factor indicator script. This indicator was originally developed by M. H. Pee (Stocks & Commodities V.22:12 (28-36): Trend Trigger Factor).

Estimate exchange/broker fee commission from trade volumeThis script is used to estimate how much an exchange/broker makes off a particular pair/symbol. If Coinbase(GDAX) has a 0.25% taker fee and a 0.15% maker fee per trade and you estimate the average commission fee at 0.19% then you simple input that, and how many periods you'd like to know the total fee for (30 periods on the 1 day chart = last 30 days, 28 periods on 4 hour chart = last 7 days, etc).

This is for broad estimates of a single pair and only works well on exchanges that show only the volume on that exchange (stock markets may be less useful for this tool).

THIS TOOL IS TO PROVIDE A BROAD ESTIMATE , NOT AN EXACT FIGURE!

// percentage fee rate is entered as a percent: 3.5=3.5%, not 350%.

// pbtc , the one for calculating the USD value of fees that are in bitcoin, uses the price at time fees were realized. IE chart is on

// 1 day interval and XBARFEE is set at 4, then PBTC gives the USD value as if the exchange sold all btc at the end of each day for

// 4 days. i.e.:

// Day 1: BTCUSD= $5000 fees=1.5, Day 2: BTCUSD = $5000 fees=3.0, Day 3 BTCUSD = $10,000 fees=1.0, Day 4 BTCUSD = $20,000 fees=1.0

// PBTC would NOT show (1.5+ 3 + 1 + 1) = 6.5 * $20k = $130,000. It would do: (1.5*5000)+(3*5000)... = $52,500.

Free Strategy #08 (Combo of #01 and #02) (ES / SPY)This strategy was designed to be traded on daily data on the ES and SPY—the strategy was originally developed for NinjaTrader, which displays daily ES data based on RTH hours instead of 24 hours (1440 minute) like TradingView does, so we are presenting the results on the SPY until we figure out how to overcome this hurdle.

The strategy combines the two ideas from strategy #01 and strategy #02 .

Strategy #08

Quantity 100

Slippage: 2 ticks

Commission: 4.95 per order

Net Profit: 26,044.60

Max Drawdown: 3,947.60

Buy and Hold (Custom)

Quantity 100

Slippage: 2 ticks

Commission: 4.95 per order

Entry Long: 1993-02-01 @ 43.99

Exit Long: 2017-07-28 @ 246.34

Net Profit: 20,225.10

Max Drawdown: 9,042.00

Free Strategy #02 (ES / SPY)This strategy was designed to be traded on daily data on the ES and SPY—the strategy was originally developed for NinjaTrader, which displays daily ES data based on RTH hours instead of 24 hours (1440 minute) like TradingView does, so we are presenting the results on the SPY until we figure out how to overcome this hurdle.

Strategy #02

Quantity 100

Slippage: 2 ticks

Commission: 4.95 per order

Net Profit: 10,118.30

Max Drawdown: 4.037.60

Buy and Hold (Custom)

Quantity 100

Slippage: 2 ticks

Commission: 4.95 per order

Entry Long: 1993-02-01 @ 43.99

Exit Long: 2017-07-28 @ 246.34

Net Profit: 20,225.10

Max Drawdown: 9,042.00

Percentage Volume Oscillator (PVO) Copyright by HPotter v1.0 28/04/2017

The Percentage Volume Oscillator (PVO) is a momentum oscillator for volume.

PVO measures the difference between two volume-based moving averages as a

percentage of the larger moving average. As with MACD and the Percentage Price

Oscillator (PPO), it is shown with a signal line, a histogram and a centerline.

PVO is positive when the shorter volume EMA is above the longer volume EMA and

negative when the shorter volume EMA is below. This indicator can be used to define

the ups and downs for volume, which can then be use to confirm or refute other signals.

Typically, a breakout or support break is validated when PVO is rising or positive.

Open/Close Vertical Line by WiscoDishOpen and close lines. I used a 4 minute timeframe, so the open price goes on 08:28-08:32 central time for the 8:30 open. You can change those times if you want, just copy/paste the script and edit.

SPYIX EMAVariation on idea at url below using SPYIX from BATS instead of VIX

from marketsci.wordpress.com

Aids in identifying changes in volatility direction.

EDIT: just noticed that URL is now password protected. The concept from the author is simple: use EMA and SMA smoothing of the VIX as two signal lines. When they cross you have a change in VIX direction. I simply coded that for SPYIX which is a slightly different (but theoretically similar) index vs VIX. SPYIX provides intraday updates without a subscription so this indicator can be used for intraday tracking.

Rob RSI Stoch MACD Combo Alert//Created by Robert Nance on 5/28/16. Additional credit to vdubus.

//This was a special request from rich15stan. It combines my original RSI Stoch extremes with vdubus’ MACD VXI.

//This script will give you red or green columns as an indication for oversold/overbought,

//based upon the rsi and stochastic both being at certain levels. The default oversold is at 35.

//If Stochastic and RSI fall below 35, you will get a green column. Play with your levels to see how

//your stock reacts. It now adds the MACD crossover, plotted as a blue circle.

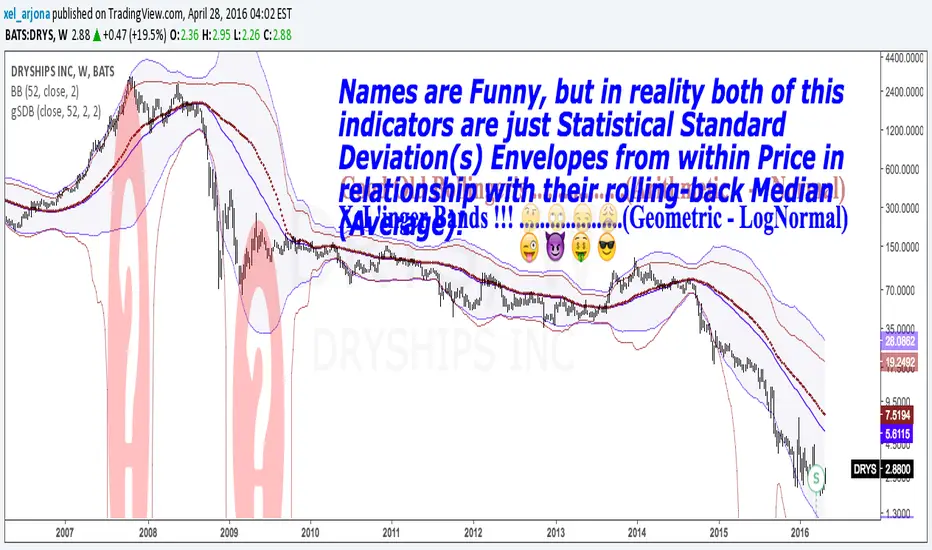

GEOMETRIC STANDARD DEVIATION BANDS v1 by @XeL_ArjonaGEOMETRIC STANDARD DEVIATION BANDS

Ver.1 By Ricardo M Arjona @XeL_Arjona

DISCLAIMER:

The Following indicator/code IS NOT intended to be a formal investment advice or recommendation by the author, nor should be construed as such. Users will be fully responsible by their use regarding their own trading vehicles/assets.

The embedded code and ideas within this work are FREELY AND PUBLICLY available on the Web for NON LUCRATIVE ACTIVITIES and must remain as is.

WHAT'S THIS?

This IS NOT the wheel "Re-Invention"... This is exactly what the name says: A pair of Envelope Bands to measure "volatility", constructed at statistical relation from within price series and their Rolling back MEAN (Simple Moving Average). YES, What Mr. Bollinger did and put it's name to this simple, cleaver and popular formula.

This time, I took the time to make another simple mod, but seems to me to be quite functional in REAL VOLATILE assets like in the example chart: TO USE THEIR GEOMETRIC MODE!!

Cheers!

Any feedback or public modification(s) are quite welcome to the community....!

@XeL_Arjona

Apr 28 2016

BB 100 with Barcolors6/19/15 I added confirmation highlight bars to the code. In other words, if a candle bounced off the lower Bollinger band, it needed one more close above the previous candle to confirm a higher probability that a change in investor sentiment has reversed. Same is true for upper Bollinger band bounces. I also added confirmation highlight bars to the 100 sma (the basis). The idea is that lower and upper bands are potential points of support and resistance. The same is true of the basis if a trend is to continue. 6/28/15 I added a plotshape to identify closes above/below TLine. One thing this system points out is it operates best in a trend reversal. Consolidations will whipsaw the indicator too much. I have found that when this happens, if using daily candles, switch to hourly, 30 min, etc., to catch a better signal. Nothing moves in a straight line. As with any indicator, it is a tool to be used in conjunction with the art AND science of trading. As always, try the indicator for a time so that you are comfortable enough to use real money. This is designed to be used with "BB 25 with Barcolors".

BB 25 with Barcolors6/19/15 I added confirmation highlight bars to the code. In other words, if a candle bounced off the lower Bollinger band, it needed one more close above the previous candle to confirm a higher probability that a change in investor sentiment has reversed. Same is true for upper Bollinger band bounces. I also added confirmation highlight bars to the 100 sma (the basis). The idea is that lower and upper bands are potential points of support and resistance. The same is true of the basis if a trend is to continue. 6/28/15 I added a plotshape to identify closes above/below TLine. One thing this system points out is it operates best in a trend reversal. Consolidations will whipsaw the indicator too much. I have found that when this happens, if using daily candles, switch to hourly, 30 min, etc., to catch a better signal. Nothing moves in a straight line. As with any indicator, it is a tool to be used in conjunction with the art AND science of trading. As always, try the indicator for a time so that you are comfortable enough to use real money. This is designed to be used with "BB 100 with Barcolors".

Commodity channel index x2 v1Slightly enhenced CCI. Take a look how difference between slow and fast CCI displayed as histogram can predict possible reverse.

EDIT: fast = 14, slow = 28 works better.

CM RSI-2 Strategy Lower IndicatorRSI-2 Strategy

***At the bottom of the page is a link where you can download the PDF of the Backtesting Results.

This year I am focusing on learning from two of the best mentors in the Industry with outstanding track records for Creating Systems, and learning the what methods actually work as far as back testing.

I came across the RSI-2 system that Larry Connors developed. Larry has become famous for his technical indicators, but his RSI-2 system is what actually put him “On The Map” per se. At first glance I didn’t think it would work well, but I decided to code it and ran backtests on the S&P 100 In Down Trending Markets, Up Trending Markets, and both combined. I was shocked by the results. So I thought I would provide them for you. I also ran a test on the Major forex Pairs (12) for the last 5 years, and All Forex Pairs (80) from 11/28/2007 - 6/09/2014, impressive results also.

The RSI-2 Strategy is designed to use on Daily Bars, however it is a short term trading strategy. The average length of time in a trade is just over 2 days. But the results CRUSH the general market averages.

Detailed Description of Indicators, Rules Below:

Link For PDF of Detailed Trade Results

d.pr

Original Post

CM RSI-2 Strategy - Upper Indicators.RSI-2 Strategy

***At the bottom of the page is a link where you can download the PDF of the Backtesting Results.

This year I am focusing on learning from two of the best mentors in the Industry with outstanding track records for Creating Systems, and learning the what methods actually work as far as back testing.

I came across the RSI-2 system that Larry Connors developed. Larry has become famous for his technical indicators, but his RSI-2 system is what actually put him “On The Map” per se. At first glance I didn’t think it would work well, but I decided to code it and ran backtests on the S&P 100 In Down Trending Markets, Up Trending Markets, and both combined. I was shocked by the results. So I thought I would provide them for you. I also ran a test on the Major forex Pairs (12) for the last 5 years, and All Forex Pairs (80) from 11/28/2007 - 6/09/2014, impressive results also.

The RSI-2 Strategy is designed to use on Daily Bars, however it is a short term trading strategy. The average length of time in a trade is just over 2 days. But the results CRUSH the general market averages.

Detailed Description of Indicators, Rules Below:

Link For PDF of Detailed Trade Results

d.pr

Original Post