Multi-Timeframe (MTF) Dashboard by RiTzMulti-Timeframe Dashboard

Shows values of different Indiactors on Multiple-Timeframes for the selected script/symbol

VWAP : if LTP is trading above VWAP then Bullish else if LTP is trading below VWAP then Bearish.

ST(21,1) : if LTP is trading above Supertrend (21,1) then Bullish , else if LTP is trading below Supertrend (21,1) then Bearish.

ST(14,2) : if LTP is trading above Supertrend (14,2) then Bullish , else if LTP is trading below Supertrend (14,2) then Bearish.

ST(10,3) : if LTP is trading above Supertrend (10,3) then Bullish , else if LTP is trading below Supertrend (10,3) then Bearish.

RSI(14) : Shows value of RSI (14) for the current timeframe.

ADX : if ADX is > 75 and DI+ > DI- then "Bullish ++".

if ADX is < 75 but >50 and DI+ > DI- then "Bullish +".

if ADX is < 50 but > 25 and DI+ > DI- then "Bullish".

if ADX is above 75 and DI- > DI+ then "Bearish ++".

if ADX is < 75 but > 50 and DI- > DI+ then "Bearish+".

if ADX is < 50 but > 25 and DI- > DI+ then "Bearish".

if ADX is < 25 then "Neutral".

MACD : if MACD line is above Signal Line then "Bullish", else if MACD line is below Signal Line then "Bearish".

PH-PL : "< PH > PL" means LTP is trading between Previous Timeframes High(PH) & Previous Timeframes Low(PL) which indicates Rangebound-ness.

"> PH" means LTP is trading above Previous Timeframes High(PH) which indicates Bullish-ness.

"< PL" means LTP is trading below Previous Timeframes Low(PL) which indicates Bearish-ness.

Alligator : If Lips > Teeth > Jaw then Bullish.

If Lips < Teeth < Jaw then Bearish.

If Lips > Teeth and Teeth < Jaw then Neutral/Sleeping.

If Lips < Teeth and Teeth > Jaw then Neutral/Sleeping.

Settings :

Style settings :-

Dashboard Location: Location of the dashboard on the chart

Dashboard Size: Size of the dashboard on the chart

Bullish Cell Color: Select the color of cell whose value is showing Bullish-ness.

Bearish Cell Color: Select the color of cell whose value is showing Bearish-ness.

Neutral Cell Color: Select the color of cell whose value is showing Rangebound-ness.

Cell Transparency: Select Transparency of cell.

Column Settings :-

You can select which Indicators values should be displayed/hidden.

Timeframe Settings :-

You can select which timeframes values should be displayed/hidden.

Note :- I'm not a pro Developer/Coder , so if there are any mistakes or any suggestions for improvements in the code then do let me know!

Note :- Use in Live market , might show wrong values for timeframes other than current timeframe in closed market!!

"25年黄金价格走势预测" için komut dosyalarını ara

Nifty / Banknifty Dashboard by RiTzNifty / Banknifty Dashboard :

Shows Values of different Indicators on current Timeframe for the selected Index & it's main constituents according to weightage in index.

customized for Nifty & Banknifty (You can customize it according to your needs for the markets/indexes you trade in)

Interpretation :-

VWAP : if LTP is trading above VWAP then Bullish else if LTP is trading below VWAP then Bearish.

ST(21,1) : if LTP is trading above Supertrend (21,1) then Bullish , else if LTP is trading below Supertrend (21,1) then Bearish.

ST(14,2) : if LTP is trading above Supertrend (14,2) then Bullish , else if LTP is trading below Supertrend (14,2) then Bearish.

ST(10,3) : if LTP is trading above Supertrend (10,3) then Bullish , else if LTP is trading below Supertrend (10,3) then Bearish.

RSI(14) : Shows value of RSI (14) for the current timeframe.

ADX : if ADX is > 75 and DI+ > DI- then "Bullish ++".

if ADX is < 75 but >50 and DI+ > DI- then "Bullish +".

if ADX is < 50 but > 25 and DI+ > DI- then "Bullish".

if ADX is above 75 and DI- > DI+ then "Bearish ++".

if ADX is < 75 but > 50 and DI- > DI+ then "Bearish+".

if ADX is < 50 but > 25 and DI- > DI+ then "Bearish".

if ADX is < 25 then "Neutral".

MACD : if MACD line is above Signal Line then "Bullish", else if MACD line is below Signal Line then "Bearish".

PDH-PDL : "< PDH > PDL" means LTP is trading between Previous Days High(PDH) & Previous Days Low(PDL) which indicates Rangebound-ness.

"> PDH" means LTP is trading above Previous Days High(PDH) which indicates Bullish-ness.

"< PDL" means LTP is trading below Previous Days Low(PDL) which indicates Bearish-ness.

Alligator : If Lips > Teeth > Jaw then Bullish.

If Lips < Teeth < Jaw then Bearish.

If Lips > Teeth and Teeth < Jaw then Neutral/Sleeping.

If Lips < Teeth and Teeth > Jaw then Neutral/Sleeping.

Settings :

Style settings :-

Dashboard Location: Location of the dashboard on the chart

Dashboard Size: Size of the dashboard on the chart

Bullish Cell Color: Select the color of cell whose value is showing Bullish-ness.

Bearish Cell Color: Select the color of cell whose value is showing Bearish-ness.

Neutral Cell Color: Select the color of cell whose value is showing Rangebound-ness.

Cell Transparency: Select Transparency of cell.

Columns Settings :-

You can select which Indicators values should be displayed/hidden.

Rows Settings :-

You can select which Stocks/Symbols values should be displayed/hidden.

Symbol Settings :-

Here you can select the Index & Stocks/Symbols

Dashboard for Index : select Nifty/Banknifty

if you select Nifty then Nifty spot, Nifty current Futures and the stocks with most weightage in Nifty index will be displayed on the Dashboard/Table.

if you select Banknifty then Banknifty spot, Banknifty current Futures and the stocks with most weightage in Banknifty index will be displayed on the Dashboard/Table.

You can Customise it according to your needs, you can choose any Symbols you want to use.

Note :- This is inspired from "RankDelta" by AsitPati and "Nifty and Bank Nifty Dashboard v2" by cvsk123 (Both these scripts are closed source!)

I'm not a pro Developer/Coder , so if there are any mistakes or any suggestions for improvements in the code then do let me know!

EMA+MACDA simple script using EMA 25 and EMA 50 with MACD. Enter long when EMA 25 crossover ema 50 and MACD line > 0, enter short when EMA 50 crossover ema 25 and MACD < 0

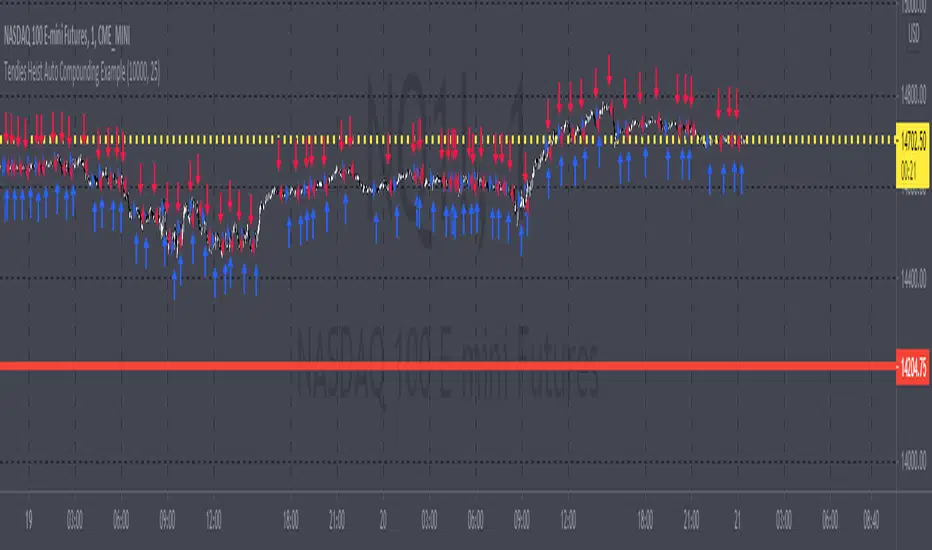

Tendies Heist Auto Compounding ExampleThis is an example of how we can use compounding to control our position size. This example shows how we can automatically add and reduce position size based on account equity. The "initial capital" in properties is the starting account equity. At default its set to 100,000. If our max position size is set to 25 then the very first position that's taken has a position size of 10, IF our leverage is set to 10,000. Account equity divided by leverage equals position size. So in that example 100,000 divided by 10,000 in leverage gives us a max position size of 10. However the max position size was set to 25 meaning we would need 250k in equity for it to open a position size of 25 with the leverage set at 10k. Now if the initial capital was set to 100,000 and the max position size was set to 5 and leverage remained at 10,000, all though 100,000 divided by 10,000 equals 10 it will ONLY open a position size of 5, because the max position size in this example was set at 5. Since this works for strategies you may look through the trade log on the posted back test and check out the position size, you can see in this back test the default 100k is used for the initial capital and the default 10k was used for the leverage. You will be able to see as this logic loses money it takes contracts away and as it gains money it adds contracts. I'm using trading view's basic strategy logic example to provide an example of how the compounding logic works.

Note, don't forget to add the syntax below to your strategy.entry call for this logic to work.

qty = size

Tendies Heist LLC 2021

Ichimoku Kinkō HyōThe Ichimoku Kinko Hyo is an trading system developed by the late Goichi Hosoda (pen name "Ichimokusanjin") when he was the general manager of the business conditions department of Miyako Shinbun, the predecessor of the Tokyo Shimbun. Currently, it is a registered trademark of Economic Fluctuation Research Institute Co., Ltd., which is run by the bereaved family of Hosoda as a private research institute.

The Ichimoku Kinko Hyo is composed of time theory, price range theory (target price theory) and wave movement theory. Ichimoku means "At One Glace". The equilibrium table is famous for its span, but the first in the equilibrium table is the time relationship.

In the theory of time, the change date is the day after the number of periods classified into the basic numerical value such as 9, 17, 26, etc., the equal numerical value that takes the number of periods of the past wave motion, and the habit numerical value that appears for each issue is there. The market is based on the idea that the buying and selling equilibrium will move in the wrong direction. Another feature is that time is emphasized in order to estimate when changes will occur.

In the price range theory, there are E・V・N・NT calculated values and multiple values of 4 to 8E as target values. In addition, in order to determine the momentum and direction of the market, we will consider other price ranges and ying and yang numbers.

If the calculated value is realized on the change date calculated by each numerical value, the market price is likely to reverse.

転換線 (Tenkansen) (Conversion Line) = (highest price in the past 9 periods + lowest price) ÷ 2

基準線 (Kijunsen) (Base Line) = (highest price in the past 26 periods + lowest price) ÷ 2

It represents Support/Resistance for 16 bars. It is a 50% Fibonacci Retracement. The Kijun sen is knows as the "container" of the trend. It is prefect to use as an initial stop and/or trailing stop.

先行スパン1 (Senkou span 1) (Lagging Span 1) = {(conversion value + reference value) ÷ 2} 25 periods ahead (26 periods ahead including the current day, that is)

先行スパン2 (Senkou span 2) (Lagging Span 2) = {(highest price in the past 52 periods + lowest price) ÷ 2} 25 periods ahead (26 periods ahead including the current day, that is)

遅行スパン (Chikou span) (Lagging Span) = (current candle closing price) plotted 26 periods before (that is, including the current day) 25 periods ago

It is the only Ichimoku indicator that uses the closing price. It is used for momentum of the trend.

The area surrounded by the two lagging span lines is called a cloud. This is the foundation of the system. It determines the sentiment (Bull/Bear) for the insrument. If price is above the cloud, the instrument is bullish. If price is below the cloud, the instrument is bearish.

-

The wave theory of the Ichimoku Kinko Hyo has the following waves.

All about the rising market. If it is the falling market, the opposite is true.

I wave rise one market price.

V wave the market price that raises and lowers.

N wave the market price for raising, lowering, and raising.

P wave the high price depreciates and the low price rises with the passage of time. Leave either.

Y wave the high price rises and the low price falls with the passage of time. Leave either.

S wave A market in which the lowered market rebounds and rises at the previous high level.

There are the above 6 types but the basis of the Ichimoku Kinko Hyo is the N wave of 3 waves.

In Elliott wave theory and similar theories, basically there are 5 waves but 5 waves are a series of 2 and 3 waves N, 3 for 7 waves, 4 for 9 waves and so on.

Even if it keep continuing, it will be based on N wave. In addition, since the P wave and the Y wave are separated from each other, they can be seen as N waves from a large perspective.

-

There are basic E・V・N・NT calculated values and several other calculation methods for the Ichimoku Kinko Hyo. It is the only calculated value that gives a concrete value in the Ichimoku Kinko Hyo, which is difficult to understand, but since we focus only on the price difference and do not consider the supply and demand, it is forbidden to stick to the calculated value alone.

(The calculation method of the following five calculated values is based on the rising market price, which is raised from the low price A to the high price B and lowered from the high price B to the low price C. Therefore, the low price C is higher than the low price A)

E calculated value The amount of increase from the low price A to the high price B is added to the high price B. = B + (BA)

V calculated value Adds the amount of decline from the high price B to the low price C to the high price B. = B + (BC)

N calculated value The amount of increase from the low price A to the high price B is added to the low price C. = C + (BA)

NT calculated value Adds the amount of increase from the low price A to the low price C to the low price C. = C + (CA)

4E calculated value (four-layer double / quadruple value) Adds three times the amount of increase from the low price A to the high price B to the high price B. = B + 3 × (BA)

Calculated value of P wave The upper price is devalued and the lower price is rounded up, and the price range of both is the same.

Calculated value of Y wave The upper price is rounded up and the lower price is rounded down, and the price range of both is the same.

SALEH MACD Donchian + EMA & MACD + ADXI gathered all the signals coming from the MACD & Donchian channels indicators and filtered them with EMA 200 or ADX > 25 indicators (which both of them show the trend),

and put them on the chart to show me the buy and sell signals;

the signals rules are as following:

BUY:

when we have an uptrend ( the price is above the EMA 200 or ADX > 25 ) & the macd line cross up the signal line while they are both under the 0 level of histogram it generates buy signals.

SELL:

when we have a downtrend ( the price is below the EMA 200 or ADX > 25) & the macd line cross below the signal line while they are both above the 0 level of histogram it generates sell signals.

Donchian channel works as a confirmation for the macd signal.

this signals work best at London session, you can also filter them by chandelier exit indicator.

RSI of VWAP [SHORT selling]This is SHORT selling version of RSIofVWAP strategy. Settings and Logic are totally different from LONG side version , hence I am publishing it as a new strategy.

Settings

============

VWAP of RSI Length 15

Slow EMA Length 200

Short entry level 25

Cover short level 70

stop loss 5

SHORT Entry

============

condition1 : When RSIofVWAP crossdown below 25 and VWAP is below ema200

condition2: When weekly RSIofVWAP crossdown 70 and VWAP (note : session vwap , not weekly vwap) is below ema200

condition3: Use VIX value , if you want to short when the price is above ema200

vwap RSI crossing down 70 and VIX RSI is cossing up 70

enter short ... This is like falling knife :-)

I need to add the code -- later

if any of above condition is TRUE , SHORT entry will be taken

Take Profit

============

When close less than short entry price and RSIofVWAp is crossing up 25 , take profit ...close 1/3 of the position

Exit

============

When RSIofVWAP crossing up 70 level

Stop Loss

============

Stop Loss is set to 5%

Note:

1. When strategy is in SHORT position , background and bar color changes to gray

2. When strategy is already in short position , possible entries are shown in yellow background

3. RSI Length 15 is working most of the equities on hourly chart. ( RSI length 9 and 14 also works good , but not for all ... You may want to try which setting works for your symbol)

4. weekly VWAP (blue color) is also plotted by default ... you can disable it if you dont want to see it. But there is advantage keeping it on the chart , you can notice whenever weekly VWAP crosses above 70 line , trend is UP ... if you have LONG position you can hold on it ... Hurray :-)

Warning

============

For the educational purposes only

Triple EMA Scalper low lag stratHi all,

This strategy is based on the Amazing scalper for majors with risk management by SoftKill21

The change is in lines 11-20 where the sma's are replaced with Triple ema's to

lower the lag.

The original author is SoftKill21. His explanation is repeated below:

Best suited for 1M time frame and majors currency pairs.

Note that I tried it at 3M time frame.

Its made of :

Ema ( exponential moving average ) , long period 25

Ema ( exponential moving average ) Predictive, long period 50,

Ema ( exponential moving average ) Predictive, long period 100

Risk management , risking % of equity per trade using stop loss and take profits levels.

Long Entry:

When the Ema 25 cross up through the 50 Ema and 100 EMA . and we are in london or new york session( very important the session, imagine if we have only american or european currencies, its best to test it)

Short Entry:

When the Ema 25 cross down through the 50 Ema and 100 EMA , and we are in london or new york session( very important the session, imagine if we have only american or european currencies, its best to test it)

Exit:

TargetPrice: 5-10 pips

Stop loss: 9-12 pips

Amazing scalper for majors with risk managementHello,

Today I am glad to bring you an amazing simple and efficient scalper strategy.

Best suited for 1M time frame and majors currency pairs.

Its made of :

Ema (exponential moving average) , long period 25

Ema(exponential moving average) Predictive, long period 50,

Ema(exponential moving average) Predictive, long period 100

Risk management , risking % of equity per trade using stop loss and take profits levels.

Long Entry:

When the Ema 25 cross up through the 50 Ema and 100 EMA. and we are in london or new york session( very important the session, imagine if we have only american or european currencies, its best to test it)

Short Entry:

When the Ema 25 cross down through the 50 Ema and 100 EMA, and we are in london or new york session( very important the session, imagine if we have only american or european currencies, its best to test it)

Exit:

TargetPrice: 5-10 pips

Stop loss: 9-12 pips

Hope you enjoy it :)

ADX + DI x Upgraded to Pine v4 x KingThiesAverage Directional Movement Index

Momentum based tool to measure trend strength on scale of 1-100

Similar to the aroon but incorporates a 3rd measure, while aroon uses two

The majority of these calculations were pre-existing in older pine scripts but have since been updated

signals are given when -DI and +DI cross, ADX illustrates corresponding strength at time of cross

Full Intro

ADX can help investors to identify trend strengths, as di - di determines the trend direction, while d - d is an impulse indicator. If the ADX is below 20, it can be considered impulsive, while it is above 25 on a trend line.

A trading signal can be generated when the di - DI line is switched to d - d and vice versa. If the di-line crosses and the ADX is above 20 (ideally 25), a potential buy signal could ebb away.

If the ADX is above 20, there is the possibility of potential short selling if the DI crosses over DI. You can also use crosses to get out of the current deal if you need it for a long time.

If the di-line is crossed and the Adx is below 20 (or 25), there may be opportunities to enter the potential for short trading, but only if di are above or below DI or if the price is trendy and may not prove to be the ideal time to start trading.

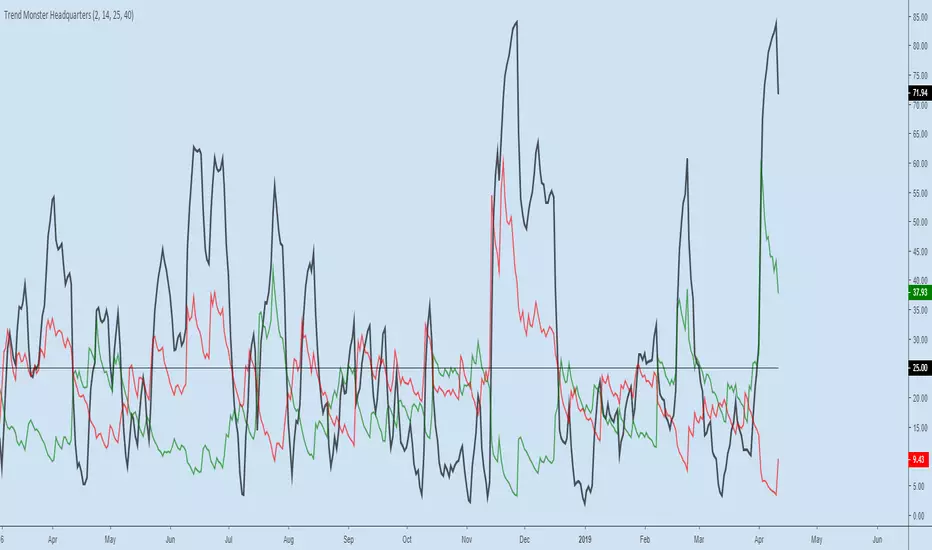

Trend Monster HeadquartersADX-DMI enhanced & modified for faster reaction

ADX (black line) above 80 = mega-trend peaked, reversal imminent, rare case scenario

ADX (black line) above 60 = trend topping out, reversal possible, depending on other indicators

ADX (black line) above 25 threshold = trend strenghening

DMI- (red line) - above 25 - bear trend strenghening

DMI+ (green line) - above 25 - bull trend strenghening

DMI- (red line) - coming off the bottom - bull trend weakening

DMI+ (green line) - coming off the bottom - bear trend weakening

BB and RSI Indicator Alert v0.3 by JustUncleLI have just recently revised this indicator alert for public release. This is for the 60sec Bollinger Band break Binary Option traders.

This indicator alert is a variation of one found in a well known Broker's marketing videos. It uses Bollinger bands, RSI and moving averages. Included is a pre-warning alert condition. The strategy and settings are designed for 1min charts and Binary Options, but it could work for up to 15 min charts.

The default settings are BB(14,2) and RSI(11) with 75/25 Levels boundaries. To be a valid trade the RSI needs to be within 75/25 channel. The optional Market direction filter is enabled by default and is calculated by two EMA (200 and 50):

When 200ema rising and 50ema above 200ema then market going up.

When 200ema falling and 50ema below 200ema then market going down.

A potential Bollinger Break reversal trades identified by shapes: The purple diamond is the pre-warning purple alert and the green and red pointers with the PUT/CALL labels are the trade alerts. Make Binary Option trade in specified direction 60sec (or can also use 120sec trade without Martingale).

* Notes and Hints *

The original videos specified a Martingale money management strategy, be careful using this management. When I use Martingale I recommend go to 3 levels: 10, 25, 65 if no win at 65 stop trading this alert and start next alert back at 10, you should recovery loss by future wins given you are able to get a reasonable ITM rate with this strategy. Alternatively instead of using Martingale use 120sec Binary Option trade.

Be wary of break alerts on a steep Bollinger, they tend to keep running away for awhile, especially if steep on both sides of Bollinger channel.

As with most of this style of indicator the alert conditions will redraw until the candle is closed. For me this is okay, as it is an Alert is only to a potential trade and final decision to trade is made by me.

You need to practise this and be aware of market news, sessions boundaries, slow trading periods etc. Plan your periods of when you should trade, I prefer Asian session before lunch and London sessions.

Insync Index [LazyBear]BB Support + Histo mode

-------------------------------

Code: pastebin.com

Show enclosing BB

Show Insync as Histo:

v02 - Configurable levels

---------------------------------

Small update to allow configuring the 95/75/25/5 levels.

Latest source code: pastebin.com

v01 - orginal description

---------------------------------

Insync Index, by Norm North, is a consensus indicator. It uses RSI, MACD, MFI, DPO, ROC, Stoch, CCI and %B to calculate a composite signal. Basically, this index shows that when a majority of underlying indicators is in sync, a turning point is near.

There are couple of ways to use this indicator.

- Buy when crossing up 5, sell when crossing down 95.

- Market is typically bullish when index is above 50, bearish when below 50. This can be a great confirmation signal for price action + trend lines.

Also, since this is typical oscillator, look for divergences between price and index.

Levels 75/25 are early warning levels. Note that, index > 75 (and less than 95) should be considered very bullish and index below 25 (but above 5) as very bearish. Levels 95/5 are equivalent to traditional OB/OS levels.

The various values of the underlying components can be tuned via options page. I have also provided an option to color bars based on the index value.

More info: The Insync Index by Norm North, TASC Jan 1995

drive.google.com

List of my free indicators: bit.ly

List of my app-store indicators: blog.tradingview.com

(Support doc: bit.ly)

SuperScript Filtered (Stable)🔎 What This Indicator Does

The indicator is a trend and momentum filter.

It looks at multiple well-known technical tools (T3 moving averages, RSI, TSI, and EMA trend) and assigns a score to the current market condition.

• If most tools are bullish → score goes up.

• If most tools are bearish → score goes down.

• Only when the score is very strong (above +75 or below -75), it prints a Buy or Sell signal.

This helps traders focus only on high-probability setups instead of reacting to every small wiggle in price.

________________________________________

⚙️ How It Works

1. T3 Trend Check

o Compares a fast and slow T3 moving average.

o If the fast T3 is above the slow T3 → bullish signal.

o If it’s below → bearish signal.

2. RSI Check

o Uses the Relative Strength Index.

o If RSI is above 50 → bullish momentum.

o If RSI is below 50 → bearish momentum.

3. TSI Check

o Uses the True Strength Index.

o If TSI is above its signal line → bullish momentum.

o If TSI is below → bearish momentum.

4. EMA Trend Check

o Looks at two exponential moving averages (fast and slow).

o If price is above both → bullish.

o If price is below both → bearish.

5. Score System

o Each condition contributes +25 (bullish) or -25 (bearish).

o The total score can range from -100 to +100.

o Score ≥ +75 → Strong Buy

o Score ≤ -75 → Strong Sell

6. Signal Filtering

o Only one buy is allowed until a sell appears (and vice versa).

o A minimum bar gap is enforced between signals to avoid clutter.

________________________________________

📊 How It Appears on the Chart

• Green “BUY” label below candles → when multiple signals agree and the market is strongly bullish.

• Red “SELL” label above candles → when multiple signals agree and the market is strongly bearish.

• Background softly shaded green or red → highlights bullish or bearish conditions.

No messy tables, no clutter — just clear trend-based entries.

________________________________________

🎯 How Traders Can Use It

This indicator is designed to help traders by:

1. Filtering Noise

o Instead of reacting to every small crossover or RSI blip, it waits until at least 3–4 conditions agree.

o This avoids entering weak trades.

2. Identifying Strong Trend Shifts

o When a Buy or Sell arrow appears, it usually signals a shift in momentum that can lead to a larger move.

3. Reducing Overtrading

o By limiting signals, traders won’t be tempted to jump in and out unnecessarily.

4. Trade Confirmation

o Traders can use the signals as confirmation for their own setups.

o Example: If your strategy says “go long” and the indicator also shows a strong Buy, that trade has more conviction.

5. Alert Automation

o Built-in alerts mean you don’t have to watch the chart all day.

o You’ll be notified only when a strong signal appears.

________________________________________

⚡ When It Helps the Most

• Works best in trending markets (bullish or bearish).

• Very useful on higher timeframes (1h, 4h, daily) for swing trading.

• Can also work on lower timeframes (5m, 15m) if combined with higher timeframe trend filtering.

________________________________________

👉 In short

This indicator is a signal filter + trend detector. It combines four powerful tools into one scoring system, and only tells you to act when the odds are stacked in your favor.

________________________________________

Bollinger Bands with 4 Moving AveragesCombines Bollinger Bands (BB) with up to four optional Moving Averages (MA) to read volatility, trend direction, and dynamic support–resistance in one overlay.

How It Works

BB: basis = MA(length, type) with standard deviation mult. upper = basis + dev, lower = basis − dev.

MA1–MA4: additional averages you can toggle (default only MA4/200 enabled).

Key Features

Flexible basis MA type for BB: SMA / EMA / RMA (Wilder) / WMA / VWMA.

Four optional MAs with independent length, color, and width (defaults: 7, 25, 99, 200; only 200 on by default).

Offset to shift BB for visual testing.

Overlay on price with shaded band between Upper–Lower.

Inputs & Defaults

BB Length = 20, StdDev = 2.0, Source = close.

Basis MA Type = SMA.

MA4 active (200), MA1–MA3 off (7/25/99 ready).

Offset = 0.

Practical Use

Use BB for volatility context: squeeze → potential breakout; expansion → strong trend.

Treat Basis / Upper / Lower as dynamic levels:

Pullbacks to Basis often become decision zones in trends.

Upper/Lower touches = relative extremes.

Add MA4(200) for primary bias; enable MA1–MA3 for finer timing.

Typical behavior:

Price > MA200 and rising basis → bullish bias; watch pullbacks to basis/MA25-like zones.

Price < MA200 and falling basis → bearish bias; watch rejections at basis/MAs.

Common Signals (not financial advice)

Breakout + BB expansion confirms momentum.

Squeeze + basis break can preface volatility expansion.

Confluence: Lower touch + fast MA in uptrends → mean-reversion setups; inverse for downtrends.

Notes

MA1–MA4 are SMA in the code; BB basis follows the selected MA type.

Test across timeframes; tune length and mult to the asset.

Disclaimer

Visual tool only. Combine with risk management, multi-timeframe confirmation, and a tested plan.

Irrationality Index by CRYPTO_ADA_BTC"The market can be irrational longer than you can stay solvent" ~ John Maynard Keynes

This indicator, the Irrationality Index, measures how far the current market price has deviated from a smoothed estimate of its "fair value," normalized for recent volatility. It provides traders with a visual sense of when the market may be behaving irrationally, without giving direct buy or sell signals.

How it works:

1. Fair Value Calculation

The indicator estimates a "fair value" for the asset using a combination of a long-term EMA (exponential moving average) and a linear regression trend over a configurable period. This fair value serves as a smoothed baseline for price, balancing trend-following and mean-reversion.

2. Volatility-Adjusted Z-Score

The deviation between price and fair value is measured in standard deviations of recent log returns:

Z = (log(price) - log(fairValue)) / volatility

This standardization accounts for different volatility environments, allowing comparison across assets.

3. Irrationality Score (0–100)

The Z-score is transformed using a logistic mapping into a 0–100 scale:

- 50 → price near fair value (rational zone)

- >75 → high irrationality, price stretched above fair value

- >90 → extreme irrationality, unsustainable extremes

- <25 → high irrationality, price stretched below fair value

- <10 → extreme bearish irrationality

4. Price vs Fair Value (% deviation)

The indicator plots the percentage difference between price and fair value:

pctDiff = (price - fairValue) / fairValue * 100

- Positive values → Percentage above fair value (optimistic / overvalued)

- Negative values → Percentage below fair value (pessimistic / undervalued)

Visuals:

- Irrationality (%) Line (0–100) shows irrationality level.

- Background Colors: Yellow= high bullish irrationality, Green= extreme bullish irrationality, Orange= high bearish irrationality, Red= extreme bearish irrationality.

- Price - FairValue (%) plot: price deviation vs fair value (%), Colored green above 0 and red below 0.

- Label: display actual price, estimated fair value, and Z-score for the latest bar.

- Alerts: configurable thresholds for high and extreme irrationality.

How to read it:

- 50 → Market trading near fair value.

- >75 / >90 → Price may be irrationally high; risk of pullback increases.

- <25 / <10 → Price may be irrationally low; potential rebound zones, but trends can continue.

- Price - FairValue (%) plot → visual guide for % price stretch relative to fair value.

Notes / Warnings:

- Measures relative deviation, not fundamental value!

- High irrationality scores do not automatically indicate trades; markets can remain can be irrational longer than you can stay solvent .

- Best used with other tools: momentum, volume, divergence, and multi-timeframe analysis.

Algo MA💎 (V.4.3)Algo MA💎 V.4.3 - Multi-EMA System with Advanced Candle Analysis

**Algo MA💎 V.4.3** is a comprehensive trend analysis system that combines multiple EMA configurations with advanced candle coloring, support/resistance detection, and integrated trade management dashboards. This indicator provides a complete visual trading environment with sophisticated trend identification and portfolio tracking capabilities.

**Core Innovation & Originality**

This system uniquely integrates seven distinct analytical components:

1. **Dual-EMA Signal Engine** - Primary trend detection using 9/21 EMA crossovers with customizable sensitivity

2. **Advanced Candle Classification** - Multi-layer candle coloring with two sensitivity levels (violet/rose) based on ATR calculations

3. **Trend Confirmation System** - Secondary 20/50 EMA trend filter with dynamic cloud visualization

4. **Zero Lag EMA Implementation** - 144-period Zero Lag EMA with directional color coding for reduced lag trend analysis

5. **RSI Extreme Detection** - Overbought (75) and oversold (25) level identification with visual markers

6. **Dynamic Support/Resistance** - Pivot-based support and resistance level calculation with 50-bar lookback

7. **Integrated Trade Management** - Three customizable dashboard tables for real-time portfolio tracking

**System Architecture & Functionality**

**Primary Signal Generation:**

The core system uses a 9-period EMA and 21-period EMA comparison to generate directional bias. When EMA9 > EMA21, the system indicates bullish conditions; when EMA9 < EMA21, it signals bearish conditions. This creates the foundation for all visual elements and trend analysis.

**Advanced Candle Coloring Logic:**

The system employs a sophisticated three-layer candle coloring approach:

- **Green Candles**: EMA9 > EMA21 (bullish trend)

- **Red Candles**: EMA9 < EMA21 (bearish trend)

- **Violet Candles**: EMAs within sensitivity_violet * ATR(14) range (consolidation)

- **Rose Candles**: EMAs within sensitivity_rose * ATR(14) range (tight consolidation)

**Sensitivity-Based Classification:**

Two independent sensitivity parameters allow fine-tuning of consolidation detection:

- **Violet Sensitivity (0.3 default)**: Broader consolidation zones

- **Rose Sensitivity (0.1 default)**: Tighter consolidation zones

**Zero Lag EMA Implementation:**

Uses advanced calculation: `zlema = ema(src + src - src , length)` where lag = floor((length-1)/2). This reduces the inherent lag of traditional EMAs while maintaining smoothness.

**Trend Confirmation Framework:**

The 20/50 EMA system provides trend context with visual cloud fills:

- **Blue Cloud**: 20 EMA > 50 EMA (bullish trend environment)

- **Red Cloud**: 20 EMA < 50 EMA (bearish trend environment)

**Unique Visual Features**

**Multi-Layer Candle System:**

The indicator plots up to four candle layers simultaneously:

1. **Base Candles**: Primary EMA-based trend colors

2. **Violet Consolidation**: ATR-adjusted consolidation detection

3. **Rose Consolidation**: Tighter consolidation identification

4. **Bearish Overlay**: Optional bearish candle highlighting

**Support/Resistance Detection:**

Uses pivot point calculations with 50-bar left and right parameters:

- **Green Lines**: Resistance levels from pivot highs

- **Red Lines**: Support levels from pivot lows

- **Dynamic Updates**: Lines adjust based on price action

**RSI Extreme Markers:**

- **Red Triangles**: First occurrence of RSI > 75 (overbought)

- **Green Triangles**: First occurrence of RSI < 25 (oversold)

**Integrated Dashboard System**

**Trade Management Tables:**

Three independent dashboard tables provide comprehensive trade tracking:

- **Stock Information**: Ticker symbol and trade direction (BUY/SELL)

- **Order Details**: Entry price, stop loss, and take profit levels

- **Position Status**: Real-time trade monitoring with color-coded status

**Dashboard Customization:**

- **Positioning**: Bottom-right, bottom-center, bottom-left placement options

- **Color Coding**: Green for BUY positions, red for SELL positions

- **Manual Entry**: User-customizable fields for trade parameters

**Volume Analysis Integration**

**Volume Oscillator:**

Implements short (5) and long (10) EMA volume comparison:

`osc = 100 * (short_volume_ema - long_volume_ema) / long_volume_ema`

This provides additional confirmation for trend strength and potential reversals.

**Usage Instructions**

**Trend Identification:**

- **Primary Trend**: Monitor 9/21 EMA relationship and candle colors

- **Trend Strength**: Observe Zero Lag EMA color (green=bullish, red=bearish)

- **Trend Context**: Use 20/50 EMA cloud for higher timeframe bias

**Entry Signal Recognition:**

- **Bullish Setup**: Green candles + blue trend cloud + support level test

- **Bearish Setup**: Red candles + red trend cloud + resistance level test

- **Consolidation**: Violet/rose candles indicate ranging conditions

**Risk Management Application:**

- **Support/Resistance**: Use pivot levels for stop placement and targets

- **RSI Extremes**: Monitor overbought/oversold conditions for reversal potential

- **Dashboard Tracking**: Utilize tables for position management

**Advanced Analysis:**

- **Sensitivity Adjustment**: Modify violet/rose parameters for market volatility

- **Multi-Timeframe**: Apply system across different timeframes for confluence

- **Volume Confirmation**: Use volume oscillator for signal validation

**Customization Options**

**EMA Parameters:**

- **Main Flow EMAs**: Adjustable 9/21 period settings

- **Trend EMAs**: Customizable 20/50 period configuration

- **Zero Lag EMA**: Modifiable 144-period length

**Visual Settings:**

- **Candle Display**: Toggle bearish candle overlay

- **Trend Visualization**: Show/hide trend cloud and EMAs

- **Support/Resistance**: Enable/disable pivot level display

- **RSI Markers**: Control overbought/oversold triangle display

**Dashboard Configuration:**

- **Table Display**: Independent control for three dashboard tables

- **Trade Details**: Customizable entry, stop, and target fields

- **Position Status**: Manual BUY/SELL/neutral designation

**Alert System**

Built-in alert conditions for:

- **Bullish Signal**: EMA9 crosses above EMA21

- **Bearish Signal**: EMA9 crosses below EMA21

**Important Considerations**

This system works optimally in trending markets with clear directional bias. During consolidation periods, focus on violet/rose candle identification and range-bound strategies. The multiple EMA layers provide comprehensive trend analysis but may generate conflicting signals during choppy conditions.

The dashboard tables serve as trade management tools but require manual input for position tracking. The system combines established EMA techniques with original sensitivity-based consolidation detection and advanced visual presentation methods.

**Disclaimer**: This indicator is designed for educational and analytical purposes. The dashboard tables are for position tracking only and do not execute trades automatically. Past performance does not guarantee future results. Always implement proper risk management and consider multiple confirmation methods before making trading decisions.

Grand Master's Candlestick Dominance (ATR Enhanced)### Grand Master's Candlestick Dominance (ATR Enhanced)

**Overview**

Unleash the ancient wisdom of Japanese candlestick charting with a modern twist! This comprehensive Pine Script v5 strategy and indicator scans for over 75 classic and advanced candlestick patterns (bullish, bearish, and neutral), assigning dynamic strength scores (1-10) to each for precise signal filtering. Enhanced with Average True Range (ATR) for volatility-aware body size validation, it dominates the markets by combining timeless pattern recognition with robust confirmation layers. Whether used as a backtestable strategy or visual indicator, it empowers traders to spot high-probability reversals, continuations, and indecision setups with surgical accuracy.

Inspired by Steve Nison's *Japanese Candlestick Charting Techniques*, this tool elevates pattern analysis beyond basics—think Hammers, Engulfing patterns, Morning Stars, and rare gems like Abandoned Baby or Concealing Baby Swallow—all consolidated into intelligent arrays for real-time averaging and prioritization.

**Key Features**

- **Extensive Pattern Library**:

- **Bullish (25+ patterns)**: Hammer (8.0), Bullish Engulfing (10.0), Morning Star (7.0), Three White Soldiers (9.0), Dragonfly Doji (8.0), and more (e.g., Rising Three, Unique Three River Bottom).

- **Bearish (25+ patterns)**: Hanging Man (8.0), Bearish Engulfing (10.0), Evening Star (7.0), Three Black Crows (9.0), Gravestone Doji (8.0), and exotics like Upside Gap Two Crows or Stalled Pattern.

- **Neutral/Indecision (34+ patterns)**: Doji variants (Long-Legged, Four Price), Spinning Tops, Harami Crosses, and multi-bar setups like Upside Tasuki Gap or Advancing Block.

Each pattern includes duration tracking (1-5 bars) and ATR-adjusted body/shadow criteria for relevance in volatile conditions.

- **Smart Confirmation Filters** (All Toggleable):

- **Trend Alignment**: 20-period SMA (customizable) ensures entries align with the prevailing trend; optional higher timeframe (e.g., Daily) MA crossover for multi-timeframe confluence.

- **Support/Resistance (S/R)**: Pivot-based levels with 0.01% tolerance to confirm bounces or breaks.

- **Volume Surge**: 20-period volume MA with 1.5x spike multiplier to validate momentum.

- **ATR Body Sizing**: Filters small bodies (<0.3x ATR) and long bodies (>0.8x ATR) for context-aware pattern reliability.

- **Follow-Through**: Ensures post-pattern confirmation via bullish/bearish closes or closes beyond prior bars.

Minimum average strength (default 7.0) and individual pattern thresholds (5.0) prevent weak signals.

- **Entry & Exit Logic**:

- **Long Entry**: Bullish average strength ≥7.0 (outweighing bearish), uptrend, volume spike, near support, follow-through, and HTF alignment.

- **Short Entry**: Mirror for bearish dominance in downtrends near resistance.

- **Exits**: Bearish/neutral shift, or fixed TP (5%) / SL (2%)—pyramiding disabled, 10% equity sizing.

- Backtest range: Jan 1, 2020 – Dec 31, 2025 (editable). Initial capital: $10,000.

- **Interactive Dashboard** (Top-Right Panel):

Real-time insights including:

- Market phase (e.g., "Bullish Phase (Avg Str: 8.2)"), active pattern (e.g., "BULLISH: Bullish Engulfing (Str: 10.0, Bars: 2)"), and trend status.

- Strength breakdowns (Bull/Bear/Neutral counts & averages).

- Filter status (e.g., "Volume: ✔ Spike", "ATR: Enabled (L:0.8, S:0.3)").

- Backtest stats: Total trades, win rate, streak, and last entry/exit details (price & timestamp).

Toggle mode: Strategy (live trades) or Indicator (signals only).

- **Advanced Alerts** (15+ Toggleable Types):

Set up via TradingView's "Any alert() function call" for bar-close triggers:

- Entry/Exit signals with strength & pattern details.

- Strong patterns (≥2 bullish/bearish), neutral indecision, volume spikes.

- S/R breakouts, HTF reversals, high-confidence singles (≥8.0 strength).

- Conflicting signals, MA crossovers, ATR volatility bursts, multi-bar completions.

Example: "STRONG BULLISH PATTERN detected! Strength: 9.5 | Top Pattern: Three White Soldiers | Trend: Up".

**Customization & Usage Tips**

- **Inputs Groups**: Strategy toggles, confirmations, exits, backtest dates, and 15+ alert switches—all intuitively grouped.

- **Optimization**: Tune min strengths for aggressive (lower) or conservative (higher) trading; enable/disable filters to suit your style (e.g., disable S/R for scalping).

- **Best For**: Forex, stocks, crypto on 1H–Daily charts. Test on historical data to refine TP/SL.

- **Limitations**: No external data installs; relies on built-in TA functions. Patterns are probabilistic—combine with your risk management.

Master the candles like a grandmaster. Deploy on TradingView, backtest relentlessly, and let dominance begin! Questions? Drop a comment.

*Version: 1.0 | Updated: September 2025 | Credits: Built on Pine Script v5 with nods to Nison's timeless techniques.*

Tape Speed Pulse (Pace + Direction) [v6 + Climax]Tape Speed Pulse (Pace + Direction)

One-liner:

A lightweight “tape pulse” that turns intraday bursts of buying/selling into an easy-to-read histogram, with surge, slowdown, and climax (exhaustion) markers for fast decision-making. Use on sec and min charts.

What it measures

Pace (RVOL): current bar volume vs the recent average (smoothed).

Direction proxy: uptick/downtick by comparing close to close .

Pulse (histogram): direction × pace, so you see who’s pushing and how fast.

Colors

- Lime = Buy surge (pace ≥ threshold & upticking)

- Red = Sell surge (pace ≥ threshold & downticking)

- Teal = Buy pressure, sub-threshold

- Orange = Sell pressure, sub-threshold

- Faded/gray = Near-neutral pace (below the Neutral Band)

Lines (toggleable)

-White = Pace (RVOL)

- Yellow = Slowdown line = a drop of X% from the last 30-bar peak pace

Background tint mirrors the current state so you can glance risk: greenish for buy pressure, reddish for sell pressure.

Signals & alerts

- BUY surge – fires when pace crosses above the surge threshold with uptick direction (optional acceleration & uptick streak filters; cooldown prevents spam).

- SELL surge – mirror logic to downside.

- Slowdown – fires when pace crosses below the yellow slowdown line while direction ≤ 0 (early fade warning).

Climax (exhaustion)

- Buy Climax: previous bar was a buy surge with a large upper wick; current bar slows (below slowdown line) and direction ≤ 0.

- Sell Climax: mirror (large lower wick → slowdown → direction ≥ 0).

- Great for trimming/tight stops or fade setups at obvious spikes.

- Create alerts via Add alert → Condition: this indicator → choose the specific alert (BUY surge, SELL surge, Slowdown, Buy Climax, Sell Climax).

How to use it (playbook)

- Longs (e.g., VWAP reclaim / micro pullback)

- Only take entries when the pulse is teal→lime (buy pressure to buy surge).

- Into prior highs/VWAP bands, take partials on lime spikes.

- If you get a Slowdown dot and bars turn orange/red, tighten or exit.

Shorts (failed reclaim / lower-high)

- Look for teal→orange→red with rising pace at a level.

- Add confidence if a Buy Climax printed right before (exhaustion).

- Risk above the spike; don’t fight true ignitions out of bases.

Simple guardrails

- Avoid new longs when the histogram is orange/red; avoid new shorts when teal/lime.

- Use with VWAP + 9/20 EMA or your levels. The pulse is confirmation, not the whole thesis.

Inputs (what they do & when to tweak)

- Pace lookback (bars) – window for average volume. Lower = faster; higher = steadier.

Too jumpy? raise it. Missing quick bursts? lower it.

- Smoothing EMA (bars) – smooths pace. Higher = calmer.

Use 4–6 during the open; 3–4 midday.

- Surge threshold (× RVOL) – how fast counts as a surge.

Too many surges? raise it. Too late? lower it slightly.

- Slowdown drop from 30-bar max (%) – how far below the recent peak pace to call a slowdown.

Higher % = later slowdown; lower % = earlier warning.

- Neutral band (× RVOL) – paces below this fade to gray.

Raise to clean up noise; lower to see subtle pressure.

- Min seconds between signals – cooldown to prevent spam.

Increase in chop; reduce if you want more pings.

- BUY/SELL: min consecutive upticks/downticks – tiny streak filter.

Raise to avoid wiggles; lower for earlier signals.

Require pace accelerating into signal – ON = avoid stall breakouts; OFF = earlier pings.

Climax options: wick % threshold & “require slowdown cross”.

Raise wick% / require cross to be stricter; lower to catch more fades.

Quick presets

- Low-float runner, 5–10s chart

- Lookback 20, Smoothing 3–4, Surge 2.2–2.8, Slowdown 35–45, Neutral 1.0–1.2, Cooldown 15–25s, Streaks 2–3, Accel ON.

- Thick large-cap, 1-min

- Lookback 20–30, Smoothing 5–7, Surge 1.5–1.9, Slowdown 25–35, Neutral 0.8–1.0, Cooldown 30–60s, Streaks 2, Accel ON.

- Open vs Midday vs Power Hour

- Open: higher Surge, more Smoothing, longer Cooldown.

- Midday: lower Surge, less Smoothing to catch subtler pushes.

- Power hour: moderate Surge; keep Slowdown on for exits.

Reading common patterns

- Ignition (likely continuation): lime spike out of a base that holds above a level while pace stays above yellow.

- Exhaustion (likely fade): lime spike late in a run with upper wick → Slowdown → orange/red. The Buy Climax diamond is your tell.

Limits / notes

This is an OHLCV-based proxy (TradingView Pine can’t read raw tape/DOM). It won’t match Bookmap/Jigsaw tick-for-tick, but it’s fast and objective.

Use with levels and a risk plan. Past performance ≠ future results. Educational only.

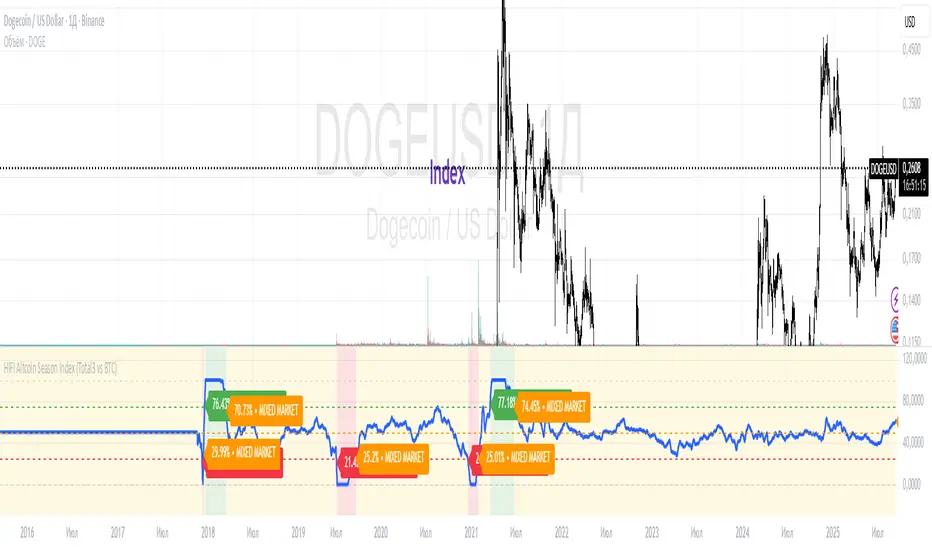

HIFI Altcoin Season Index (Total3 vs BTC)This indicator helps you determine whether the crypto market is in an "altcoin season" or a "bitcoin season." It doesn't compare every single altcoin to Bitcoin individually; instead, it uses a more efficient approach.

Methodology

The index calculates the difference in price performance over a selected period (default 90 days) between the total market capitalization of altcoins without Ethereum (TOTAL3) and Bitcoin (BTC).

Interpretation

Value above 75: TOTAL3 is showing significantly stronger growth than BTC, indicating an ALTCOIN SEASON. 🚀

Value below 25: BTC is outperforming TOTAL3, indicating a BITCOIN SEASON. 👑

Value between 25 and 75: The market is in a mixed or neutral phase. 🤷

Benefits

This method avoids the technical limitations of Pine Script when requesting data for a large number of symbols, making the indicator stable and reliable.

Disclaimer: This indicator is a tool for market analysis and should not be considered financial advice.

ATR Future Movement Range Projection

The "ATR Future Movement Range Projection" is a custom TradingView Pine Script indicator designed to forecast potential price ranges for a stock (or any asset) over short-term (1-month) and medium-term (3-month) horizons. It leverages the Average True Range (ATR) as a measure of volatility to estimate how far the price might move, while incorporating recent momentum bias based on the proportion of bullish (green) vs. bearish (red) candles. This creates asymmetric projections: in bullish periods, the upside range is larger than the downside, and vice versa.

The indicator is overlaid on the chart, plotting horizontal lines for the projected high and low prices for both timeframes. Additionally, it displays a small table in the top-right corner summarizing the projected prices and the percentage change required from the current close to reach them. This makes it useful for traders assessing potential targets, risk-reward ratios, or option strategies, as it combines volatility forecasting with directional sentiment.

Key features:

- **Volatility Basis**: Uses weekly ATR to derive a stable daily volatility estimate, avoiding noise from shorter timeframes.

- **Momentum Adjustment**: Analyzes recent candle colors to tilt projections toward the prevailing trend (e.g., more upside if more green candles).

- **Time Horizons**: Fixed at 1 month (21 trading days) and 3 months (63 trading days), assuming ~21 trading days per month (excluding weekends/holidays).

- **User Adjustable**: The ATR length/lookback (default 50) can be tweaked via inputs.

- **Visuals**: Green/lime lines for highs, red/orange for lows; a semi-transparent table for quick reference.

- **Limitations**: This is a probabilistic projection based on historical volatility and momentum—it doesn't predict direction with certainty and assumes volatility persists. It ignores external factors like news, earnings, or market regimes. Best used on daily charts for stocks/ETFs.

The indicator doesn't generate buy/sell signals but helps visualize "expected" ranges, similar to how implied volatility informs option pricing.

### How It Works Step-by-Step

The script executes on each bar update (typically daily timeframe) and follows this logic:

1. **Input Configuration**:

- ATR Length (Lookback): Default 50 bars. This controls both the ATR calculation period and the candle count window. You can adjust it in the indicator settings.

2. **Calculate Weekly ATR**:

- Fetches the ATR from the weekly timeframe using `request.security` with a length of 50 weeks.

- ATR measures average price range (high-low, adjusted for gaps), representing volatility.

3. **Derive Daily ATR**:

- Divides the weekly ATR by 5 (approximating 5 trading days per week) to get an equivalent daily volatility estimate.

- Example: If weekly ATR is $5, daily ATR ≈ $1.

4. **Define Projection Periods**:

- 1 Month: 21 trading days.

- 3 Months: 63 trading days (21 × 3).

- These are hardcoded but based on standard trading calendar assumptions.

5. **Compute Base Projections**:

- Base projection = Daily ATR × Days in period.

- This gives the total expected movement (range) without direction: e.g., for 3 months, $1 daily ATR × 63 = $63 total range.

6. **Analyze Candle Momentum (Win Rate)**:

- Counts green candles (close > open) and red candles (close < open) over the last 50 bars (ignores dojis where close == open).

- Total colored candles = green + red.

- Win rate = green / total colored (as a fraction, e.g., 0.7 for 70%). Defaults to 0.5 if no colored candles.

- This acts as a simple momentum proxy: higher win rate implies bullish bias.

7. **Adjust Projections Asymmetrically**:

- Upside projection = Base projection × Win rate.

- Downside projection = Base projection × (1 - Win rate).

- This skews the range: e.g., 70% win rate means 70% of the total range allocated to upside, 30% to downside.

8. **Calculate Projected Prices**:

- High = Current close + Upside projection.

- Low = Current close - Downside projection.

- Done separately for 1M and 3M.

9. **Plot Lines**:

- 3M High: Solid green line.

- 3M Low: Solid red line.

- 1M High: Dashed lime line.

- 1M Low: Dashed orange line.

- Lines extend horizontally from the current bar onward.

10. **Display Table**:

- A 3-column table (Projection, Price, % Change) in the top-right.

- Rows for 1M High/Low and 3M High/Low, color-coded.

- % Change = ((Projected price - Close) / Close) × 100.

- Updates dynamically with new data.

The entire process repeats on each new bar, so projections evolve as volatility and momentum change.

### Examples

Here are two hypothetical examples using the indicator on a daily chart. Assume it's applied to a stock like AAPL, but with made-up data for illustration. (In TradingView, you'd add the script to see real outputs.)

#### Example 1: Bullish Scenario (High Win Rate)

- Current Close: $150.

- Weekly ATR (50 periods): $10 → Daily ATR: $10 / 5 = $2.

- Last 50 Candles: 35 green, 15 red → Total colored: 50 → Win Rate: 35/50 = 0.7 (70%).

- Base Projections:

- 1M: $2 × 21 = $42.

- 3M: $2 × 63 = $126.

- Adjusted Projections:

- 1M Upside: $42 × 0.7 = $29.4 → High: $150 + $29.4 = $179.4 (+19.6%).

- 1M Downside: $42 × 0.3 = $12.6 → Low: $150 - $12.6 = $137.4 (-8.4%).

- 3M Upside: $126 × 0.7 = $88.2 → High: $150 + $88.2 = $238.2 (+58.8%).

- 3M Downside: $126 × 0.3 = $37.8 → Low: $150 - $37.8 = $112.2 (-25.2%).

- On the Chart: Green/lime lines skewed higher; table shows bullish % changes (e.g., +58.8% for 3M high).

- Interpretation: Suggests stronger potential upside due to recent bullish momentum; useful for call options or long positions.

#### Example 2: Bearish Scenario (Low Win Rate)

- Current Close: $50.

- Weekly ATR (50 periods): $3 → Daily ATR: $3 / 5 = $0.6.

- Last 50 Candles: 20 green, 30 red → Total colored: 50 → Win Rate: 20/50 = 0.4 (40%).

- Base Projections:

- 1M: $0.6 × 21 = $12.6.

- 3M: $0.6 × 63 = $37.8.

- Adjusted Projections:

- 1M Upside: $12.6 × 0.4 = $5.04 → High: $50 + $5.04 = $55.04 (+10.1%).

- 1M Downside: $12.6 × 0.6 = $7.56 → Low: $50 - $7.56 = $42.44 (-15.1%).

- 3M Upside: $37.8 × 0.4 = $15.12 → High: $50 + $15.12 = $65.12 (+30.2%).

- 3M Downside: $37.8 × 0.6 = $22.68 → Low: $50 - $22.68 = $27.32 (-45.4%).

- On the Chart: Red/orange lines skewed lower; table highlights larger downside % (e.g., -45.4% for 3M low).

- Interpretation: Indicates bearish risk; might prompt protective puts or short strategies.

#### Example 3: Neutral Scenario (Balanced Win Rate)

- Current Close: $100.

- Weekly ATR: $5 → Daily ATR: $1.

- Last 50 Candles: 25 green, 25 red → Win Rate: 0.5 (50%).

- Projections become symmetric:

- 1M: Base $21 → Upside/Downside $10.5 each → High $110.5 (+10.5%), Low $89.5 (-10.5%).

- 3M: Base $63 → Upside/Downside $31.5 each → High $131.5 (+31.5%), Low $68.5 (-31.5%).

- Interpretation: Pure volatility-based range, no directional bias—ideal for straddle options or range trading.

In real use, test on historical data: e.g., if past projections captured actual moves ~68% of the time (1 standard deviation for ATR), it validates the volatility assumption. Adjust the lookback for different assets (shorter for volatile cryptos, longer for stable blue-chips).

BTC/USD 3-Min Binary Prediction [v7.2 EN]BTC/USD 3-Minute Binary Prediction Indicator v7.2 - Complete Guide

Overview

This is an advanced technical analysis indicator designed for Bitcoin/USD binary options trading with 3-minute expiration times. The system aims for an 83% win rate by combining multiple analysis layers and pattern recognition.

How It Works

Core Prediction Logic

- Timeframe: Predicts whether BTC price will be ±$25 higher (HIGH) or lower (LOW) after 3 minutes

- Entry Signals: Generates HIGH/LOW signals when confidence exceeds threshold (default 75%)

- Verification: Automatically tracks and displays win/loss statistics in real-time

5-Layer Filter System

The indicator uses a sophisticated scoring system (0-100 points):

1. Trend Filter (25 points) - Analyzes EMA alignments and price momentum

2. Leading Indicators (25 points) - RSI and MACD divergence analysis

3. Volume Confirmation (20 points) - Detects unusual volume patterns

4. Support/Resistance (15 points) - Identifies key price levels

5. Momentum Alignment (15 points) - Measures acceleration and deceleration

Pattern Recognition

Automatically detects and visualizes:

- Double Tops/Bottoms - Reversal patterns

- Triangles - Ascending, descending, symmetrical

- Channels - Trending price channels

- Candlestick Patterns - Engulfing, hammer, hanging man

Multi-Timeframe Analysis

- Uses 1-minute and 5-minute data for confirmation

- Aligns multiple timeframes for higher probability trades

- Monitors trend consistency across timeframes

Key Features

Display Panels

1. Statistics Panel (Top Right)

- Overall win rate percentage

- Hourly performance (wins/losses)

- Daily performance

- Current system status

2. Analysis Panel (Left Side)

- Market trend analysis

- RSI status (overbought/oversold)

- Volume conditions

- Filter scores for each component

- Final HIGH/LOW/WAIT decision

Visual Signals

- Green Triangle (↑) = HIGH prediction

- Red Triangle (↓) = LOW prediction

- Yellow Background = Entry opportunity

- Blue Background = Waiting for result

Configuration Options

Basic Settings

- Range Width: Target price movement (default $50 = ±$25)

- Min Confidence: Minimum confidence to enter (default 75%)

- Max Daily Trades: Risk management limit (default 5)

Filters (Can be toggled on/off)

- Trend Filter

- Volume Confirmation

- Support/Resistance Filter

- Momentum Alignment

Display Options

- Show/hide signals, statistics, analysis

- Minimal Mode for cleaner charts

- EMA line visibility

Important Risk Warnings

Binary Options Trading Risks:

1. High Risk Product - Binary options are extremely risky and banned in many countries

2. Not Investment Advice - This tool is for educational/analytical purposes only

3. No Guaranteed Returns - Past performance doesn't predict future results

4. Capital at Risk - You can lose your entire investment in seconds

Technical Limitations:

- Requires stable internet connection

- Performance varies with market conditions

- High volatility can reduce accuracy

- Not suitable for news events or low liquidity periods

Best Practices

1. Paper Trade First - Test thoroughly on demo accounts

2. Risk Management - Never risk more than 1-2% per trade

3. Market Conditions - Works best in normal volatility conditions

4. Avoid Major Events - Don't trade during major news releases

5. Monitor Performance - Track your actual results vs displayed statistics

Setup Instructions

1. Add to TradingView chart (BTC/USD preferred)

2. Use 30-second or 1-minute chart timeframe

3. Adjust settings based on your risk tolerance

4. Monitor F-Score (should be >65 for entries)

5. Wait for clear HIGH/LOW signals with high confidence

Alert Configuration

The indicator provides three alert types:

- HIGH Signal alerts

- LOW Signal alerts

- General entry opportunity alerts

Legal Disclaimer

Binary options trading may not be legal in your jurisdiction. Many countries including the USA, Canada, and EU nations have restrictions or outright bans on binary options. Always check local regulations and consult with financial advisors before trading.

Remember: This is a technical analysis tool, not a money-printing machine. Successful trading requires discipline, risk management, and continuous learning. The displayed statistics are historical and don't guarantee future performance.

Weekly pecentage tracker by PRIVATE

Settings Picture below this link: 👇

i.ibb.co

What it is

A lightweight “Weekly % Tracker” overlay that lets you manually enter weekly performance (in percent) for XAUUSD + up to 10 FX pairs, then shows:

a small table panel with each enabled symbol and its % result

one TOTAL row (Sum / Average / Compounded across all enabled symbols)

an optional mini badge showing the % for a single selected symbol

Nothing is auto-calculated from price—you type the % yourself.

Key settings

Panel: show/hide, position, number of decimals, colors (background, text, green/red).

Total mode:

Sum – adds percentages

Average – mean of enabled rows

Compounded –

(

∏

(

1

+

𝑝

/

100

)

−

1

)

×

100

(∏(1+p/100)−1)×100

Symbols:

XAUUSD (toggle + label + % input)

10 FX pairs (each has On/Off, label text, % input). You can rename labels to any symbol text you want.

Mini badge: show/hide, position, and symbol to display.

How it works

Overlay indicator: overlay=true; just draws UI on the chart (no plots).

Arrays (syms, vals, ons) collect the row data in order: XAU first, then FX1…FX10.

Helpers:

posFrom() converts a position string (e.g., “Top Right”) into a position.* constant.

wp_col() picks green/red/neutral based on the sign of the %.

wp_round() rounds values to the selected decimals.

calc_total() computes the TOTAL with the chosen mode over enabled rows only.

Table creation logic:

Counts how many rows are enabled.

If none enabled or panel is off: the panel table is deleted, so no box/background is visible.

If enabled and on: the panel is (re)created at the chosen position.

On each last bar (barstate.islast), it clears the table to transparent (bgcolor=na) and then fills one row per enabled symbol, followed by a single TOTAL row.

Mini badge:

Always (re)created on position change.

Shows selected symbol’s % (or “-” if that symbol isn’t enabled or has no value).

Colors text green/red by sign.

Notes & limits

It’s manual input—the script doesn’t read trades or P/L from price.

You can rename each row’s label to match any symbol name you want.

When no rows are enabled, the panel disappears entirely (no empty background).

Designed to be light: only draws tables; no heavy plotting.

If you want the TOTAL row to be optional, or different color thresholds, or CSV-style export/import of the values, say the word and I’ll add it.