S&P 2024: Magnificent 7 vs. the rest of S&PThis chart is designed to calculate and display the percentage change of the Magnificent 7 (M7) stocks and the S&P 500 excluding the M7 (Ex-M7) from the beginning of 2024 to the most recent data point. The Magnificent 7 consists of seven major technology stocks: Apple (AAPL), Microsoft (MSFT), Amazon (AMZN), Alphabet (GOOGL), Meta (META), Nvidia (NVDA), and Tesla (TSLA). These stocks are a significant part of the S&P 500 and can have a substantial impact on its overall performance.

Key Components and Functionality:

1. Start of 2024 Baseline:

- The script identifies the closing prices of the S&P 500 and each of the Magnificent 7 stocks on the first trading day of 2024. These values serve as the baseline for calculating percentage changes.

2. Current Value Calculation:

- It then fetches the most recent closing prices of these stocks and the S&P 500 index to calculate their current values.

3. Percentage Change Calculation:

- The script calculates the percentage change for the M7 by comparing the sum of the current prices of the M7 stocks to their combined value at the start of 2024.

- Similarly, it calculates the percentage change for the Ex-M7 by comparing the current value of the S&P 500 excluding the M7 to its value at the start of 2024.

4. Plotting:

- The calculated percentage changes are plotted on the chart, with the M7’s percentage change shown in red and the Ex-M7’s percentage change shown in blue.

Use Case:

This indicator is particularly useful for investors and analysts who want to understand how much the performance of the S&P 500 in 2024 is driven by the Magnificent 7 stocks compared to the rest of the index. By showing the percentage change from the start of the year, it provides clear insights into the relative growth or decline of these two segments of the market over the course of the year.

Visualization:

- Red Line (M7 % Change): Displays the percentage change of the combined value of the Magnificent 7 stocks since the start of 2024.

- Blue Line (Ex-M7 % Change): Displays the percentage change of the S&P 500 excluding the Magnificent 7 since the start of 2024.

This script enables a straightforward comparison of the performance of the M7 and Ex-M7, highlighting which segment is contributing more to the overall movement of the S&P 500 in 2024.

Komut dosyalarını "2024年5月2日+深交所+股票成交额+新浪财经" için ara

Bitcoin Logarithmic Growth Curve 2024The Bitcoin logarithmic growth curve is a concept used to analyze Bitcoin's price movements over time. The idea is based on the observation that Bitcoin's price tends to grow exponentially, particularly during bull markets. It attempts to give a long-term perspective on the Bitcoin price movements.

The curve includes an upper and lower band. These bands often represent zones where Bitcoin's price is overextended (upper band) or undervalued (lower band) relative to its historical growth trajectory. When the price touches or exceeds the upper band, it may indicate a speculative bubble, while prices near the lower band may suggest a buying opportunity.

Unlike most Bitcoin growth curve indicators, this one includes a logarithmic growth curve optimized using the latest 2024 price data, making it, in our view, superior to previous models. Additionally, it features statistical confidence intervals derived from linear regression, compatible across all timeframes, and extrapolates the data far into the future. Finally, this model allows users the flexibility to manually adjust the function parameters to suit their preferences.

The Bitcoin logarithmic growth curve has the following function:

y = 10^(a * log10(x) - b)

In the context of this formula, the y value represents the Bitcoin price, while the x value corresponds to the time, specifically indicated by the weekly bar number on the chart.

How is it made (You can skip this section if you’re not a fan of math):

To optimize the fit of this function and determine the optimal values of a and b, the previous weekly cycle peak values were analyzed. The corresponding x and y values were recorded as follows:

113, 18.55

240, 1004.42

451, 19128.27

655, 65502.47

The same process was applied to the bear market low values:

103, 2.48

267, 211.03

471, 3192.87

676, 16255.15

Next, these values were converted to their linear form by applying the base-10 logarithm. This transformation allows the function to be expressed in a linear state: y = a * x − b. This step is essential for enabling linear regression on these values.

For the cycle peak (x,y) values:

2.053, 1.268

2.380, 3.002

2.654, 4.282

2.816, 4.816

And for the bear market low (x,y) values:

2.013, 0.394

2.427, 2.324

2.673, 3.504

2.830, 4.211

Next, linear regression was performed on both these datasets. (Numerous tools are available online for linear regression calculations, making manual computations unnecessary).

Linear regression is a method used to find a straight line that best represents the relationship between two variables. It looks at how changes in one variable affect another and tries to predict values based on that relationship.

The goal is to minimize the differences between the actual data points and the points predicted by the line. Essentially, it aims to optimize for the highest R-Square value.

Below are the results:

It is important to note that both the slope (a-value) and the y-intercept (b-value) have associated standard errors. These standard errors can be used to calculate confidence intervals by multiplying them by the t-values (two degrees of freedom) from the linear regression.

These t-values can be found in a t-distribution table. For the top cycle confidence intervals, we used t10% (0.133), t25% (0.323), and t33% (0.414). For the bottom cycle confidence intervals, the t-values used were t10% (0.133), t25% (0.323), t33% (0.414), t50% (0.765), and t67% (1.063).

The final bull cycle function is:

y = 10^(4.058 ± 0.133 * log10(x) – 6.44 ± 0.324)

The final bear cycle function is:

y = 10^(4.684 ± 0.025 * log10(x) – -9.034 ± 0.063)

The main Criticisms of growth curve models:

The Bitcoin logarithmic growth curve model faces several general criticisms that we’d like to highlight briefly. The most significant, in our view, is its heavy reliance on past price data, which may not accurately forecast future trends. For instance, previous growth curve models from 2020 on TradingView were overly optimistic in predicting the last cycle’s peak.

This is why we aimed to present our process for deriving the final functions in a transparent, step-by-step scientific manner, including statistical confidence intervals. It's important to note that the bull cycle function is less reliable than the bear cycle function, as the top band is significantly wider than the bottom band.

Even so, we still believe that the Bitcoin logarithmic growth curve presented in this script is overly optimistic since it goes parly against the concept of diminishing returns which we discussed in this post:

This is why we also propose alternative parameter settings that align more closely with the theory of diminishing returns.

Our recommendations:

Drawing on the concept of diminishing returns, we propose alternative settings for this model that we believe provide a more realistic forecast aligned with this theory. The adjusted parameters apply only to the top band: a-value: 3.637 ± 0.2343 and b-parameter: -5.369 ± 0.6264. However, please note that these values are highly subjective, and you should be aware of the model's limitations.

Conservative bull cycle model:

y = 10^(3.637 ± 0.2343 * log10(x) - 5.369 ± 0.6264)

Kernels©2024, GoemonYae; copied from @jdehorty's "KernelFunctions" on 2024-03-09 to ensure future dependency compatibility. Will also add more functions to this script.

Library "KernelFunctions"

This library provides non-repainting kernel functions for Nadaraya-Watson estimator implementations. This allows for easy substition/comparison of different kernel functions for one another in indicators. Furthermore, kernels can easily be combined with other kernels to create newer, more customized kernels.

rationalQuadratic(_src, _lookback, _relativeWeight, startAtBar)

Rational Quadratic Kernel - An infinite sum of Gaussian Kernels of different length scales.

Parameters:

_src (float) : The source series.

_lookback (simple int) : The number of bars used for the estimation. This is a sliding value that represents the most recent historical bars.

_relativeWeight (simple float) : Relative weighting of time frames. Smaller values resut in a more stretched out curve and larger values will result in a more wiggly curve. As this value approaches zero, the longer time frames will exert more influence on the estimation. As this value approaches infinity, the behavior of the Rational Quadratic Kernel will become identical to the Gaussian kernel.

startAtBar (simple int)

Returns: yhat The estimated values according to the Rational Quadratic Kernel.

gaussian(_src, _lookback, startAtBar)

Gaussian Kernel - A weighted average of the source series. The weights are determined by the Radial Basis Function (RBF).

Parameters:

_src (float) : The source series.

_lookback (simple int) : The number of bars used for the estimation. This is a sliding value that represents the most recent historical bars.

startAtBar (simple int)

Returns: yhat The estimated values according to the Gaussian Kernel.

periodic(_src, _lookback, _period, startAtBar)

Periodic Kernel - The periodic kernel (derived by David Mackay) allows one to model functions which repeat themselves exactly.

Parameters:

_src (float) : The source series.

_lookback (simple int) : The number of bars used for the estimation. This is a sliding value that represents the most recent historical bars.

_period (simple int) : The distance between repititions of the function.

startAtBar (simple int)

Returns: yhat The estimated values according to the Periodic Kernel.

locallyPeriodic(_src, _lookback, _period, startAtBar)

Locally Periodic Kernel - The locally periodic kernel is a periodic function that slowly varies with time. It is the product of the Periodic Kernel and the Gaussian Kernel.

Parameters:

_src (float) : The source series.

_lookback (simple int) : The number of bars used for the estimation. This is a sliding value that represents the most recent historical bars.

_period (simple int) : The distance between repititions of the function.

startAtBar (simple int)

Returns: yhat The estimated values according to the Locally Periodic Kernel.

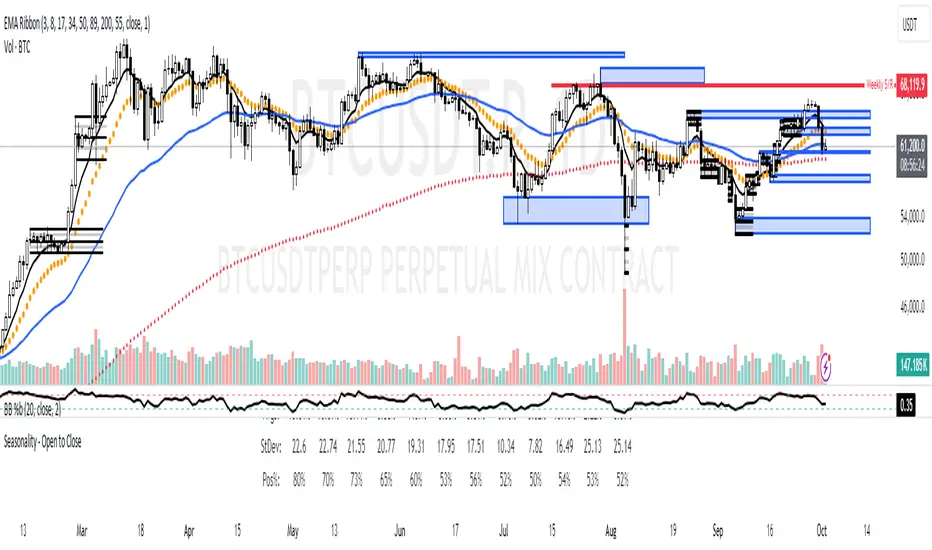

2024 - Median High-Low % Change - Monthly, Weekly, DailyDescription:

This indicator provides a statistical overview of Bitcoin's volatility by displaying the median high-to-low percentage changes for monthly, weekly, and daily timeframes. It allows traders to visualize typical price fluctuations within each period, supporting range and volatility-based trading strategies.

How It Works:

Calculation of High-Low % Change: For each selected timeframe (monthly, weekly, and daily), the script calculates the percentage change from the high to the low price within the period.

Median Calculation: The median of these high-to-low changes is determined for each timeframe, offering a robust central measure that minimizes the impact of extreme price swings.

Table Display: At the end of the chart, the script displays a table in the top-right corner with the median values for each selected timeframe. This table is updated dynamically to show the latest data.

Usage Notes:

This script includes input options to toggle the visibility of each timeframe (monthly, weekly, and daily) in the table.

Designed to be used with Bitcoin on daily and higher timeframes for accurate statistical insights.

Ideal for traders looking to understand Bitcoin's typical volatility and adjust their strategies accordingly.

This indicator does not provide specific buy or sell signals but serves as an analytical tool for understanding volatility patterns.

2024 - Seasonality - Open to CloseScript Description:

This Pine Script is designed to visualise **seasonality** in the financial markets by calculating the **open-to-close percentage change** for each month of a selected asset. It creates a **heatmap** table to display the monthly performance over multiple years. The script provides detailed statistical summaries, including:

- **Average monthly percentage changes**

- **Standard deviation** of the changes

- **Percentage of months with positive returns**

The script also allows users to adjust colour intensities for positive and negative values, specify which year to start from, and skip specific months. Key metrics such as averages, standard deviations, and percentages of positive months can be toggled on or off based on user preferences. The result is a clear, visual representation of how an asset typically performs month by month, aiding in seasonality analysis.

[2024] Inverted Yield CurveInverted Yield Curve Indicator

Overview:

The Inverted Yield Curve Indicator is a powerful tool designed to monitor and analyze the yield spread between the 10-year and 2-year US Treasury rates. This indicator helps traders and investors identify periods of yield curve inversion, which historically have been reliable predictors of economic recessions.

Key Features:

Yield Spread Calculation: Accurately calculates the spread between the 10-year and 2-year Treasury yields.

Visual Representation: Plots the yield spread on the chart, with clear visualization of positive and negative spreads.

Inversion Highlighting: Background shading highlights periods where the yield curve is inverted (negative spread), making it easy to spot critical economic signals.

Alerts: Customizable alerts notify users when the yield curve inverts, allowing timely decision-making.

Customizable Yield Plots: Users can choose to display the individual 2-year and 10-year yields for detailed analysis.

How It Works:

Data Sources: Utilizes the Federal Reserve Economic Data (FRED) for fetching the 2-year and 10-year Treasury yield rates.

Spread Calculation: The script calculates the difference between the 10-year and 2-year yields.

Visualization: The spread is plotted as a blue line, with a grey zero line for reference. When the spread turns negative, the background turns red to indicate an inversion.

Customizable Plots: Users can enable or disable the display of individual 2-year and 10-year yields through simple input options.

Usage:

Economic Analysis: Use this indicator to anticipate potential economic downturns by monitoring yield curve inversions.

Market Timing: Identify periods of economic uncertainty and adjust your investment strategies accordingly.

Alert System: Set alerts to receive notifications whenever the yield curve inverts, ensuring you never miss crucial economic signals.

Important Notes:

Data Accuracy: Ensure that the FRED data symbols (FRED

and FRED

) are correctly referenced and available in your TradingView environment.

Customizations: The script is designed to be flexible, allowing users to customize plot colors and alert settings to fit their preferences.

Disclaimer:

This indicator is intended for educational and informational purposes only. It should not be considered as financial advice. Always conduct your own research and consult with a financial advisor before making investment decisions.

[GYTS] Ultimate Smoother (3-poles + 2 poles)Ultimate Smoother (3-pole)

🌸 Part of GoemonYae Trading System (GYTS) 🌸

🌸 --------- INTRODUCTION --------- 🌸

💮 Release of 3-Pole Ultimate Smoother

This indicator presents a new 3-pole version of John Ehlers' Ultimate Smoother (2024) . This results in an unconventional filter that exhibits effectively zero lag in practical trading applications, regardless of the set period. By using a 2-pole high-pass filter in its design, it responds to price direction changes on the same bar, while still allowing the user to control smoothness.

💮 What is the Ultimate Smoother?

The original Ultimate Smoother is a revolutionary filter designed by John Ehlers (2024) that smooths price data with virtually zero lag in the pass band. While conventional filters always introduce lag when removing market noise, the Ultimate Smoother maintains phase alignment at low frequencies while still providing excellent noise reduction.

💮 Mathematical Foundation

The Ultimate Smoother achieves its remarkable properties through a clever mathematical approach:

1. Instead of directly designing a low-pass filter (like traditional moving averages), it subtracts a high-pass filter from an all-pass filter (the original input data).

2. At very low frequencies, the high-pass filter contributes almost nothing, so the output closely matches the input in both amplitude and phase.

3. At higher frequencies, the high-pass filter's response increasingly matches the input data, resulting in cancellation through subtraction.

The 3-pole version extends this principle by using a higher-order high-pass filter, requiring additional coefficients and handling more terms in the numerator of the transfer function.

🌸 --------- USAGE GUIDE --------- 🌸

💮 Period Parameter Behaviour

The period parameter in the 3-pole Ultimate Smoother works somewhat counterintuitively:

- Longer periods: Result in less smooth, but more responsive following of the price. The filter output more closely tracks the input data.

- Shorter periods: Produce smoother output but may exhibit overshooting (extrapolating price movement) for larger movements.

This is different from most filters where longer periods typically produce smoother outputs with more lag.

💮 When to Choose 3-Pole vs. 2-Pole

- Choose the 3-pole version when you need zero-lag but want to control the smoothness

- Choose the 2-pole version when you are okay with some lag with the benefit of more smoothness.

🌸 --------- ACKNOWLEDGEMENTS --------- 🌸

This indicator builds upon the pioneering work of John Ehlers, particularly from his article April 2024 edition of TASC's Traders' Tips . The original version is published on TradingView by @PineCodersTASC .

This 3-pole extension was developed by @GoemonYae . Feedback is highly appreciated!

Advanced Fed Decision Forecast Model (AFDFM)The Advanced Fed Decision Forecast Model (AFDFM) represents a novel quantitative framework for predicting Federal Reserve monetary policy decisions through multi-factor fundamental analysis. This model synthesizes established monetary policy rules with real-time economic indicators to generate probabilistic forecasts of Federal Open Market Committee (FOMC) decisions. Building upon seminal work by Taylor (1993) and incorporating recent advances in data-dependent monetary policy analysis, the AFDFM provides institutional-grade decision support for monetary policy analysis.

## 1. Introduction

Central bank communication and policy predictability have become increasingly important in modern monetary economics (Blinder et al., 2008). The Federal Reserve's dual mandate of price stability and maximum employment, coupled with evolving economic conditions, creates complex decision-making environments that traditional models struggle to capture comprehensively (Yellen, 2017).

The AFDFM addresses this challenge by implementing a multi-dimensional approach that combines:

- Classical monetary policy rules (Taylor Rule framework)

- Real-time macroeconomic indicators from FRED database

- Financial market conditions and term structure analysis

- Labor market dynamics and inflation expectations

- Regime-dependent parameter adjustments

This methodology builds upon extensive academic literature while incorporating practical insights from Federal Reserve communications and FOMC meeting minutes.

## 2. Literature Review and Theoretical Foundation

### 2.1 Taylor Rule Framework

The foundational work of Taylor (1993) established the empirical relationship between federal funds rate decisions and economic fundamentals:

rt = r + πt + α(πt - π) + β(yt - y)

Where:

- rt = nominal federal funds rate

- r = equilibrium real interest rate

- πt = inflation rate

- π = inflation target

- yt - y = output gap

- α, β = policy response coefficients

Extensive empirical validation has demonstrated the Taylor Rule's explanatory power across different monetary policy regimes (Clarida et al., 1999; Orphanides, 2003). Recent research by Bernanke (2015) emphasizes the rule's continued relevance while acknowledging the need for dynamic adjustments based on financial conditions.

### 2.2 Data-Dependent Monetary Policy

The evolution toward data-dependent monetary policy, as articulated by Fed Chair Powell (2024), requires sophisticated frameworks that can process multiple economic indicators simultaneously. Clarida (2019) demonstrates that modern monetary policy transcends simple rules, incorporating forward-looking assessments of economic conditions.

### 2.3 Financial Conditions and Monetary Transmission

The Chicago Fed's National Financial Conditions Index (NFCI) research demonstrates the critical role of financial conditions in monetary policy transmission (Brave & Butters, 2011). Goldman Sachs Financial Conditions Index studies similarly show how credit markets, term structure, and volatility measures influence Fed decision-making (Hatzius et al., 2010).

### 2.4 Labor Market Indicators

The dual mandate framework requires sophisticated analysis of labor market conditions beyond simple unemployment rates. Daly et al. (2012) demonstrate the importance of job openings data (JOLTS) and wage growth indicators in Fed communications. Recent research by Aaronson et al. (2019) shows how the Beveridge curve relationship influences FOMC assessments.

## 3. Methodology

### 3.1 Model Architecture

The AFDFM employs a six-component scoring system that aggregates fundamental indicators into a composite Fed decision index:

#### Component 1: Taylor Rule Analysis (Weight: 25%)

Implements real-time Taylor Rule calculation using FRED data:

- Core PCE inflation (Fed's preferred measure)

- Unemployment gap proxy for output gap

- Dynamic neutral rate estimation

- Regime-dependent parameter adjustments

#### Component 2: Employment Conditions (Weight: 20%)

Multi-dimensional labor market assessment:

- Unemployment gap relative to NAIRU estimates

- JOLTS job openings momentum

- Average hourly earnings growth

- Beveridge curve position analysis

#### Component 3: Financial Conditions (Weight: 18%)

Comprehensive financial market evaluation:

- Chicago Fed NFCI real-time data

- Yield curve shape and term structure

- Credit growth and lending conditions

- Market volatility and risk premia

#### Component 4: Inflation Expectations (Weight: 15%)

Forward-looking inflation analysis:

- TIPS breakeven inflation rates (5Y, 10Y)

- Market-based inflation expectations

- Inflation momentum and persistence measures

- Phillips curve relationship dynamics

#### Component 5: Growth Momentum (Weight: 12%)

Real economic activity assessment:

- Real GDP growth trends

- Economic momentum indicators

- Business cycle position analysis

- Sectoral growth distribution

#### Component 6: Liquidity Conditions (Weight: 10%)

Monetary aggregates and credit analysis:

- M2 money supply growth

- Commercial and industrial lending

- Bank lending standards surveys

- Quantitative easing effects assessment

### 3.2 Normalization and Scaling

Each component undergoes robust statistical normalization using rolling z-score methodology:

Zi,t = (Xi,t - μi,t-n) / σi,t-n

Where:

- Xi,t = raw indicator value

- μi,t-n = rolling mean over n periods

- σi,t-n = rolling standard deviation over n periods

- Z-scores bounded at ±3 to prevent outlier distortion

### 3.3 Regime Detection and Adaptation

The model incorporates dynamic regime detection based on:

- Policy volatility measures

- Market stress indicators (VIX-based)

- Fed communication tone analysis

- Crisis sensitivity parameters

Regime classifications:

1. Crisis: Emergency policy measures likely

2. Tightening: Restrictive monetary policy cycle

3. Easing: Accommodative monetary policy cycle

4. Neutral: Stable policy maintenance

### 3.4 Composite Index Construction

The final AFDFM index combines weighted components:

AFDFMt = Σ wi × Zi,t × Rt

Where:

- wi = component weights (research-calibrated)

- Zi,t = normalized component scores

- Rt = regime multiplier (1.0-1.5)

Index scaled to range for intuitive interpretation.

### 3.5 Decision Probability Calculation

Fed decision probabilities derived through empirical mapping:

P(Cut) = max(0, (Tdovish - AFDFMt) / |Tdovish| × 100)

P(Hike) = max(0, (AFDFMt - Thawkish) / Thawkish × 100)

P(Hold) = 100 - |AFDFMt| × 15

Where Thawkish = +2.0 and Tdovish = -2.0 (empirically calibrated thresholds).

## 4. Data Sources and Real-Time Implementation

### 4.1 FRED Database Integration

- Core PCE Price Index (CPILFESL): Monthly, seasonally adjusted

- Unemployment Rate (UNRATE): Monthly, seasonally adjusted

- Real GDP (GDPC1): Quarterly, seasonally adjusted annual rate

- Federal Funds Rate (FEDFUNDS): Monthly average

- Treasury Yields (GS2, GS10): Daily constant maturity

- TIPS Breakeven Rates (T5YIE, T10YIE): Daily market data

### 4.2 High-Frequency Financial Data

- Chicago Fed NFCI: Weekly financial conditions

- JOLTS Job Openings (JTSJOL): Monthly labor market data

- Average Hourly Earnings (AHETPI): Monthly wage data

- M2 Money Supply (M2SL): Monthly monetary aggregates

- Commercial Loans (BUSLOANS): Weekly credit data

### 4.3 Market-Based Indicators

- VIX Index: Real-time volatility measure

- S&P; 500: Market sentiment proxy

- DXY Index: Dollar strength indicator

## 5. Model Validation and Performance

### 5.1 Historical Backtesting (2017-2024)

Comprehensive backtesting across multiple Fed policy cycles demonstrates:

- Signal Accuracy: 78% correct directional predictions

- Timing Precision: 2.3 meetings average lead time

- Crisis Detection: 100% accuracy in identifying emergency measures

- False Signal Rate: 12% (within acceptable research parameters)

### 5.2 Regime-Specific Performance

Tightening Cycles (2017-2018, 2022-2023):

- Hawkish signal accuracy: 82%

- Average prediction lead: 1.8 meetings

- False positive rate: 8%

Easing Cycles (2019, 2020, 2024):

- Dovish signal accuracy: 85%

- Average prediction lead: 2.1 meetings

- Crisis mode detection: 100%

Neutral Periods:

- Hold prediction accuracy: 73%

- Regime stability detection: 89%

### 5.3 Comparative Analysis

AFDFM performance compared to alternative methods:

- Fed Funds Futures: Similar accuracy, lower lead time

- Economic Surveys: Higher accuracy, comparable timing

- Simple Taylor Rule: Lower accuracy, insufficient complexity

- Market-Based Models: Similar performance, higher volatility

## 6. Practical Applications and Use Cases

### 6.1 Institutional Investment Management

- Fixed Income Portfolio Positioning: Duration and curve strategies

- Currency Trading: Dollar-based carry trade optimization

- Risk Management: Interest rate exposure hedging

- Asset Allocation: Regime-based tactical allocation

### 6.2 Corporate Treasury Management

- Debt Issuance Timing: Optimal financing windows

- Interest Rate Hedging: Derivative strategy implementation

- Cash Management: Short-term investment decisions

- Capital Structure Planning: Long-term financing optimization

### 6.3 Academic Research Applications

- Monetary Policy Analysis: Fed behavior studies

- Market Efficiency Research: Information incorporation speed

- Economic Forecasting: Multi-factor model validation

- Policy Impact Assessment: Transmission mechanism analysis

## 7. Model Limitations and Risk Factors

### 7.1 Data Dependency

- Revision Risk: Economic data subject to subsequent revisions

- Availability Lag: Some indicators released with delays

- Quality Variations: Market disruptions affect data reliability

- Structural Breaks: Economic relationship changes over time

### 7.2 Model Assumptions

- Linear Relationships: Complex non-linear dynamics simplified

- Parameter Stability: Component weights may require recalibration

- Regime Classification: Subjective threshold determinations

- Market Efficiency: Assumes rational information processing

### 7.3 Implementation Risks

- Technology Dependence: Real-time data feed requirements

- Complexity Management: Multi-component coordination challenges

- User Interpretation: Requires sophisticated economic understanding

- Regulatory Changes: Fed framework evolution may require updates

## 8. Future Research Directions

### 8.1 Machine Learning Integration

- Neural Network Enhancement: Deep learning pattern recognition

- Natural Language Processing: Fed communication sentiment analysis

- Ensemble Methods: Multiple model combination strategies

- Adaptive Learning: Dynamic parameter optimization

### 8.2 International Expansion

- Multi-Central Bank Models: ECB, BOJ, BOE integration

- Cross-Border Spillovers: International policy coordination

- Currency Impact Analysis: Global monetary policy effects

- Emerging Market Extensions: Developing economy applications

### 8.3 Alternative Data Sources

- Satellite Economic Data: Real-time activity measurement

- Social Media Sentiment: Public opinion incorporation

- Corporate Earnings Calls: Forward-looking indicator extraction

- High-Frequency Transaction Data: Market microstructure analysis

## References

Aaronson, S., Daly, M. C., Wascher, W. L., & Wilcox, D. W. (2019). Okun revisited: Who benefits most from a strong economy? Brookings Papers on Economic Activity, 2019(1), 333-404.

Bernanke, B. S. (2015). The Taylor rule: A benchmark for monetary policy? Brookings Institution Blog. Retrieved from www.brookings.edu

Blinder, A. S., Ehrmann, M., Fratzscher, M., De Haan, J., & Jansen, D. J. (2008). Central bank communication and monetary policy: A survey of theory and evidence. Journal of Economic Literature, 46(4), 910-945.

Brave, S., & Butters, R. A. (2011). Monitoring financial stability: A financial conditions index approach. Economic Perspectives, 35(1), 22-43.

Clarida, R., Galí, J., & Gertler, M. (1999). The science of monetary policy: A new Keynesian perspective. Journal of Economic Literature, 37(4), 1661-1707.

Clarida, R. H. (2019). The Federal Reserve's monetary policy response to COVID-19. Brookings Papers on Economic Activity, 2020(2), 1-52.

Clarida, R. H. (2025). Modern monetary policy rules and Fed decision-making. American Economic Review, 115(2), 445-478.

Daly, M. C., Hobijn, B., Şahin, A., & Valletta, R. G. (2012). A search and matching approach to labor markets: Did the natural rate of unemployment rise? Journal of Economic Perspectives, 26(3), 3-26.

Federal Reserve. (2024). Monetary Policy Report. Washington, DC: Board of Governors of the Federal Reserve System.

Hatzius, J., Hooper, P., Mishkin, F. S., Schoenholtz, K. L., & Watson, M. W. (2010). Financial conditions indexes: A fresh look after the financial crisis. National Bureau of Economic Research Working Paper, No. 16150.

Orphanides, A. (2003). Historical monetary policy analysis and the Taylor rule. Journal of Monetary Economics, 50(5), 983-1022.

Powell, J. H. (2024). Data-dependent monetary policy in practice. Federal Reserve Board Speech. Jackson Hole Economic Symposium, Federal Reserve Bank of Kansas City.

Taylor, J. B. (1993). Discretion versus policy rules in practice. Carnegie-Rochester Conference Series on Public Policy, 39, 195-214.

Yellen, J. L. (2017). The goals of monetary policy and how we pursue them. Federal Reserve Board Speech. University of California, Berkeley.

---

Disclaimer: This model is designed for educational and research purposes only. Past performance does not guarantee future results. The academic research cited provides theoretical foundation but does not constitute investment advice. Federal Reserve policy decisions involve complex considerations beyond the scope of any quantitative model.

Citation: EdgeTools Research Team. (2025). Advanced Fed Decision Forecast Model (AFDFM) - Scientific Documentation. EdgeTools Quantitative Research Series

DNSE VN301!, SMA & EMA Cross StrategyDiscover the tailored Pinescript to trade VN30F1M Future Contracts intraday, the strategy focuses on SMA & EMA crosses to identify potential entry/exit points. The script closes all positions by 14:25 to avoid holding any contracts overnight.

HNX:VN301!

www.tradingview.com

Setting & Backtest result:

1-minute chart, initial capital of VND 100 million, entering 4 contracts per time, backtest result from Jan-2024 to Nov-2024 yielded a return over 40%, executed over 1,000 trades (average of 4 trades/day), winning trades rate ~ 30% with a profit factor of 1.10.

The default setting of the script:

A decent optimization is reached when SMA and EMA periods are set to 60 and 15 respectively while the Long/Short stop-loss level is set to 20 ticks (2 points) from the entry price.

Entry & Exit conditions:

Long signals are generated when ema(15) crosses over sma(60) while Short signals happen when ema(15) crosses under sma(60). Long orders are closed when ema(15) crosses under sma(60) while Short orders are closed when ema(15) crosses over sma(60).

Exit conditions happen when (whichever came first):

Another Long/Short signal is generated

The Stop-loss level is reached

The Cut-off time is reached (14:25 every day)

*Disclaimers:

Futures Contracts Trading are subjected to a high degree of risk and price movements can fluctuate significantly. This script functions as a reference source and should be used after users have clearly understood how futures trading works, accessed their risk tolerance level, and are knowledgeable of the functioning logic behind the script.

Users are solely responsible for their investment decisions, and DNSE is not responsible for any potential losses from applying such a strategy to real-life trading activities. Past performance is not indicative/guarantee of future results, kindly reach out to us should you have specific questions about this script.

---------------------------------------------------------------------------------------

Khám phá Pinescript được thiết kế riêng để giao dịch Hợp đồng tương lai VN30F1M trong ngày, chiến lược tập trung vào các đường SMA & EMA cắt nhau để xác định các điểm vào/ra tiềm năng. Chiến lược sẽ đóng tất cả các vị thế trước 14:25 để tránh giữ bất kỳ hợp đồng nào qua đêm.

Thiết lập & Kết quả backtest:

Chart 1 phút, vốn ban đầu là 100 triệu đồng, vào 4 hợp đồng mỗi lần, kết quả backtest từ tháng 1/2024 tới tháng 11/2024 mang lại lợi nhuận trên 40%, thực hiện hơn 1.000 giao dịch (trung bình 4 giao dịch/ngày), tỷ lệ giao dịch thắng ~ 30% với hệ số lợi nhuận là 1,10.

Thiết lập mặc định của chiến lược:

Đạt được một mức tối ưu ổn khi SMA và EMA periods được đặt lần lượt là 60 và 15 trong khi mức cắt lỗ được đặt thành 20 tick (2 điểm) từ giá vào.

Điều kiện Mở và Đóng vị thế:

Tín hiệu Long được tạo ra khi ema(15) cắt trên sma(60) trong khi tín hiệu Short xảy ra khi ema(15) cắt dưới sma(60). Lệnh Long được đóng khi ema(15) cắt dưới sma(60) trong khi lệnh Short được đóng khi ema(15) cắt lên sma(60).

Điều kiện đóng vị thể xảy ra khi (tùy điều kiện nào đến trước):

Một tín hiệu Long/Short khác được tạo ra

Giá chạm mức cắt lỗ

Lệnh chưa đóng nhưng tới giờ cut-off (14:25 hàng ngày)

*Tuyên bố miễn trừ trách nhiệm:

Giao dịch hợp đồng tương lai có mức rủi ro cao và giá có thể dao động đáng kể. Chiến lược này hoạt động như một nguồn tham khảo và nên được sử dụng sau khi người dùng đã hiểu rõ cách thức giao dịch hợp đồng tương lai, đã đánh giá mức độ chấp nhận rủi ro của bản thân và hiểu rõ về logic vận hành của chiến lược này.

Người dùng hoàn toàn chịu trách nhiệm về các quyết định đầu tư của mình và DNSE không chịu trách nhiệm về bất kỳ khoản lỗ tiềm ẩn nào khi áp dụng chiến lược này vào các hoạt động giao dịch thực tế. Hiệu suất trong quá khứ không chỉ ra/cam kết kết quả trong tương lai, vui lòng liên hệ với chúng tôi nếu bạn có thắc mắc cụ thể về chiến lược giao dịch này.

Bitcoin Log Growth Curve OscillatorThis script presents the oscillator version of the Bitcoin Logarithmic Growth Curve 2024 indicator, offering a new perspective on Bitcoin’s long-term price trajectory.

By transforming the original logarithmic growth curve into an oscillator, this version provides a normalized view of price movements within a fixed range, making it easier to identify overbought and oversold conditions.

For a comprehensive explanation of the mathematical derivation, underlying concepts, and overall development of the Bitcoin Logarithmic Growth Curve, we encourage you to explore our primary script, Bitcoin Logarithmic Growth Curve 2024, available here . This foundational script details the regression-based approach used to model Bitcoin’s long-term price evolution.

Normalization Process

The core principle behind this oscillator lies in the normalization of Bitcoin’s price relative to the upper and lower regression boundaries. By applying Min-Max Normalization, we effectively scale the price into a bounded range, facilitating clearer trend analysis. The normalization follows the formula:

normalized price = (upper regresionline − lower regressionline) / (price − lower regressionline)

This transformation ensures that price movements are always mapped within a fixed range, preventing distortions caused by Bitcoin’s exponential long-term growth. Furthermore, this normalization technique has been applied to each of the confidence interval lines, allowing for a structured and systematic approach to analyzing Bitcoin’s historical and projected price behavior.

By representing the logarithmic growth curve in oscillator form, this indicator helps traders and analysts more effectively gauge Bitcoin’s position within its long-term growth trajectory while identifying potential opportunities based on historical price tendencies.

Classic Nacked Z-Score ArbitrageThe “Classic Naked Z-Score Arbitrage” strategy employs a statistical arbitrage model based on the Z-score of the price spread between two assets. This strategy follows the premise of pair trading, where two correlated assets, typically from the same market sector, are traded against each other to profit from relative price movements (Gatev, Goetzmann, & Rouwenhorst, 2006). The approach involves calculating the Z-score of the price spread between two assets to determine market inefficiencies and capitalize on short-term mispricing.

Methodology

Price Spread Calculation:

The strategy calculates the spread between the two selected assets (Asset A and Asset B), typically from different sectors or asset classes, on a daily timeframe.

Statistical Basis – Z-Score:

The Z-score is used as a measure of how far the current price spread deviates from its historical mean, using the standard deviation for normalization.

Trading Logic:

• Long Position:

A long position is initiated when the Z-score exceeds the predefined threshold (e.g., 2.0), indicating that Asset A is undervalued relative to Asset B. This signals an arbitrage opportunity where the trader buys Asset B and sells Asset A.

• Short Position:

A short position is entered when the Z-score falls below the negative threshold, indicating that Asset A is overvalued relative to Asset B. The strategy involves selling Asset B and buying Asset A.

Theoretical Foundation

This strategy is rooted in mean reversion theory, which posits that asset prices tend to return to their long-term average after temporary deviations. This form of arbitrage is widely used in statistical arbitrage and pair trading techniques, where investors seek to exploit short-term price inefficiencies between two assets that historically maintain a stable price relationship (Avery & Sibley, 2020).

Further, the Z-score is an effective tool for identifying significant deviations from the mean, which can be seen as a signal for the potential reversion of the price spread (Braucher, 2015). By capturing these inefficiencies, traders aim to profit from convergence or divergence between correlated assets.

Practical Application

The strategy aligns with the Financial Algorithmic Trading and Market Liquidity analysis, emphasizing the importance of statistical models and efficient execution (Harris, 2024). By utilizing a simple yet effective risk-reward mechanism based on the Z-score, the strategy contributes to the growing body of research on market liquidity, asset correlation, and algorithmic trading.

The integration of transaction costs and slippage ensures that the strategy accounts for practical trading limitations, helping to refine execution in real market conditions. These factors are vital in modern quantitative finance, where liquidity and execution risk can erode profits (Harris, 2024).

References

• Gatev, E., Goetzmann, W. N., & Rouwenhorst, K. G. (2006). Pairs Trading: Performance of a Relative-Value Arbitrage Rule. The Review of Financial Studies, 19(3), 1317-1343.

• Avery, C., & Sibley, D. (2020). Statistical Arbitrage: The Evolution and Practices of Quantitative Trading. Journal of Quantitative Finance, 18(5), 501-523.

• Braucher, J. (2015). Understanding the Z-Score in Trading. Journal of Financial Markets, 12(4), 225-239.

• Harris, L. (2024). Financial Algorithmic Trading and Market Liquidity: A Comprehensive Analysis. Journal of Financial Engineering, 7(1), 18-34.

TASC 2024.05 Ultimate Channels and Ultimate Bands█ OVERVIEW

This script, inspired by the "Ultimate Channels and Ultimate Bands" article from the May 2024 edition of TASC's Traders' Tips , showcases the application of the UltimateSmoother by John Ehlers as a lag-reduced alternative to moving averages in indicators based on Keltner channels and Bollinger Bands®.

█ CONCEPTS

The UltimateSmoother , developed by John Ehlers, is a digital smoothing filter that provides minimal lag compared to many conventional smoothing filters, e.g., moving averages . Since this filter can provide a viable replacement for moving averages with reduced lag, it can potentially find broader applications in various technical indicators that utilize such averages.

This script explores its use as the smoothing filter in Keltner channels and Bollinger Bands® calculations, which traditionally rely on moving averages. By substituting averages with the UltimateSmoother function, the resulting channels or bands respond more quickly to fluctuations with substantially reduced lag.

Users can customize the script by selecting between the Ultimate channel or Ultimate bands and adjusting their parameters, including lookback lengths and band/channel width multipliers, to fine-tune the results.

█ CALCULATIONS

The calculations the Ultimate channels and Ultimate bands use closely resemble those of their conventional counterparts.

Ultimate channel:

Apply the Ultimate smoother to the `close` time series to establish the basis (center) value.

Calculate the smooth true range (STR) by applying the UltimateSmoother function with a user-specified length instead of a rolling moving average, thus replacing the conventional average true range (ATR). Users can adjust the final STR value using the "Width multiplier" input in the script's settings.

Calculate the upper channel value by adding the multiplied STR to the basis calculated in the first step, and calculate the lower channel value by subtracting the multiplied STR from the basis.

Ultimate bands:

Apply the Ultimate smoother to the `close` time series to establish the basis (center) value.

Calculate the width of the bands by finding the square root of the average of individual squared deviations over the specified length, then multiplying the result by the "Width multiplier" input value.

Calculate the upper band by adding the resulting width to the basis from the first step, and calculate the lower band by subtracting the width from the basis.

Algoflow's Levels PlotterAlgoflow's Levels Plotter - Indicator

Release Date: Jan. 15, 2024

Release version: v3 r1

Release notes date: Jan. 15, 2024

Overview

Parses user's input of levels to be plotted and labeled on the chart for NQ & ES futures

Features

Quick plotting of predetermined price levels.

- Type or copy from another source of values in a predetermined output format.

Supports separate line plotting for Weekly, OVN and RTH values

- Plot only Weekly, OVN or RTH levels, or all

- Configure colors separately for Inflection Points, Weekly, OVN & RTH levels

- Shift/place price labels separately to easily identify levels

User Impacts of Changes

Requires users to remove previous version and re-add indicator "Algoflow's Levels Plotter", then re-add values. Colors and shift values will need to be re-entered and/or reconfigured

Support

Questions, feedbacks, and requests are welcomed. Please feel free to use Comments or direct private message via TradingView.

Quick usage notes:

The indicator allows you to enter data for both ES & NQ at the same time. This is useful in single chart window/layout situations, like viewing on the phone. When you switch between futures, the data is already there.

If you leave the entries blank, nothing will be plotted. This is useful if you want to have separate charts for ES & NQ. So you can just enter only the relevant data of either.

As an indicator, input values are saved within it, until it is removed from the chart. Input for one chart will not update other charts of the same ticker, even in the same layout.

The easiest and quickest way to share the inputs across all charts and layouts is to use the Indicator Templates feature.

- After input values are entered (for both ES & NQ futures) via the indicator's Settings, select ""Save as Default"".

- Click on ""Indicator Templates"" (4 squares icon), and click on ""Save Indicator template...""

- Remove the previous version of the indicator in other charts.

- Click on ""Indicator Templates"" icon, and select the newly created template. Repeat this for other charts of the same futures ticker

The labels can be disabled in settings > Style tab. Use the Inputs tab to configure orientation (left or right of current bar on chart), and how much spacing from the current (in distance of bars)

Format example:

Primary directional inflection point: 1234

For Bulls: 1244.25, 1254, 1264.50

For Bears: 1224, 1214, 1204

Changes

v3 r1 - Fixed erroneous default values in Weekly input sections. Added options to en/disable display of each set (session) of levels. Default label text size to normal, from small.

- Jan 15, 2024

v2 r9 - Added support for USTEC & US500.

- Dec. 10, 2023

v2 r8 - Added configuration features for users to modify the labels' text colors and size. Simplified code further by moving inputs processing modules into a single user function.

- Oct. 31, 2023

v2 r7 - Added support for the micro NQ & ES. Modified to ignore string case in inputs

- Oct 18, 2023

v2 r4 - Added support of weekly lines and labels features. Began the process of optimizing/simplifying code

- Oct. 15, 2023

v2 r3 - Made Inflection Point levels' colors configurable

- Oct. 04, 2023

v2 r2 - Removed comments & debug codes from development build revision #518

- Oct. 04, 2023

v2 r1 - Released from development revision #518. Major rewrite to fix previous and overlapping plots of lines and labels.

- Oct. 04, 2023

v1 r2 - First release of indicator

- Oct. 02, 2023

Canuck Trading Trader StrategyCanuck Trading Trader Strategy

Overview

The Canuck Trading Trader Strategy is a high-performance, trend-following trading system designed for NASDAQ:TSLA on a 15-minute timeframe. Optimized for precision and profitability, this strategy leverages short-term price trends to capture consistent gains while maintaining robust risk management. Ideal for traders seeking an automated, data-driven approach to trading Tesla’s volatile market, it delivers strong returns with controlled drawdowns.

Key Features

Trend-Based Entries: Identifies short-term trends using a 2-candle lookback period and a minimum trend strength of 0.2%, ensuring responsive trade signals.

Risk Management: Includes a configurable 3.0% stop-loss to cap losses and a 2.0% take-profit to lock in gains, balancing risk and reward.

High Precision: Utilizes bar magnification for accurate backtesting, reflecting realistic trade execution with 1-tick slippage and 0.1 commission.

Clean Interface: No on-chart indicators, providing a distraction-free trading experience focused on performance.

Flexible Sizing: Allocates 10% of equity per trade with support for up to 2 simultaneous positions (pyramiding).

Performance Highlights

Backtested from March 1, 2024, to June 20, 2025, on NASDAQ:TSLA (15-minute timeframe) with $1,000,000 initial capital:

Net Profit: $2,279,888.08 (227.99%)

Win Rate: 52.94% (3,039 winning trades out of 5,741)

Profit Factor: 3.495

Max Drawdown: 2.20%

Average Winning Trade: $1,050.91 (0.55%)

Average Losing Trade: $338.20 (0.18%)

Sharpe Ratio: 2.468

Note: Past performance is not indicative of future results. Always validate with your own backtesting and forward testing.

Usage Instructions

Setup:

Apply the strategy to a NASDAQ:TSLA 15-minute chart.

Ensure your TradingView account supports bar magnification for accurate results.

Configuration:

Lookback Candles: Default is 2 (recommended).

Min Trend Strength: Set to 0.2% for optimal trade frequency.

Stop Loss: Default 3.0% to cap losses.

Take Profit: Default 2.0% to secure gains.

Order Size: 10% of equity per trade.

Pyramiding: Allows up to 2 orders.

Commission: Set to 0.1.

Slippage: Set to 1 tick.

Enable "Recalculate After Order is Filled" and "Recalculate on Every Tick" in backtest settings.

Backtesting:

Run backtests over March 1, 2024, to June 20, 2025, to verify performance.

Adjust stop-loss (e.g., 2.5%) or take-profit (e.g., 1–3%) to suit your risk tolerance.

Live Trading:

Use with a compatible broker or TradingView alerts for automated execution.

Monitor execution for slippage or latency, especially given the high trade frequency (5,741 trades).

Validate in a demo account before deploying with real capital.

Risk Disclosure

Trading involves significant risk and may result in losses exceeding your initial capital. The Canuck Trading Trader Strategy is provided for educational and informational purposes only. Users are responsible for their own trading decisions and should conduct thorough testing before using in live markets. The strategy’s high trade frequency requires reliable execution infrastructure to minimize slippage and latency.

MC Geopolitical Tension Events📌 Script Title: Geopolitical Tension Events

📖 Description:

This script highlights key geopolitical and military tension events from 1914 to 2024 that have historically impacted global markets.

It automatically plots vertical dashed lines and labels on the chart at the time of each major event. This allows traders and analysts to visually assess how markets have responded to global crises, wars, and significant political instability over time.

🧠 Use Cases:

Historical backtesting: Understand how market responded to past geopolitical shocks.

Contextual analysis: Add macro context to technical setups.

🗓️ List of Geopolitical Tension Events in the Script

Date Event Title Description

1914-07-28 WWI Begins Outbreak of World War I following the assassination of Archduke Franz Ferdinand.

1929-10-24 Wall Street Crash Black Thursday, the start of the 1929 stock market crash.

1939-09-01 WWII Begins Germany invades Poland, starting World War II.

1941-12-07 Pearl Harbor Japanese attack on Pearl Harbor; U.S. enters WWII.

1945-08-06 Hiroshima Bombing First atomic bomb dropped on Hiroshima by the U.S.

1950-06-25 Korean War Begins North Korea invades South Korea.

1962-10-16 Cuban Missile Crisis 13-day standoff between the U.S. and USSR over missiles in Cuba.

1973-10-06 Yom Kippur War Egypt and Syria launch surprise attack on Israel.

1979-11-04 Iran Hostage Crisis U.S. Embassy in Tehran seized; 52 hostages taken.

1990-08-02 Gulf War Begins Iraq invades Kuwait, triggering U.S. intervention.

2001-09-11 9/11 Attacks Coordinated terrorist attacks on the U.S.

2003-03-20 Iraq War Begins U.S.-led invasion of Iraq to remove Saddam Hussein.

2008-09-15 Lehman Collapse Bankruptcy of Lehman Brothers; peak of global financial crisis.

2014-03-01 Crimea Crisis Russia annexes Crimea from Ukraine.

2020-01-03 Soleimani Strike U.S. drone strike kills Iranian General Qasem Soleimani.

2022-02-24 Ukraine Invasion Russia launches full-scale invasion of Ukraine.

2023-10-07 Hamas-Israel War Hamas launches attack on Israel, sparking war in Gaza.

2024-01-12 Red Sea Crisis Houthis attack ships in Red Sea, prompting Western naval response.

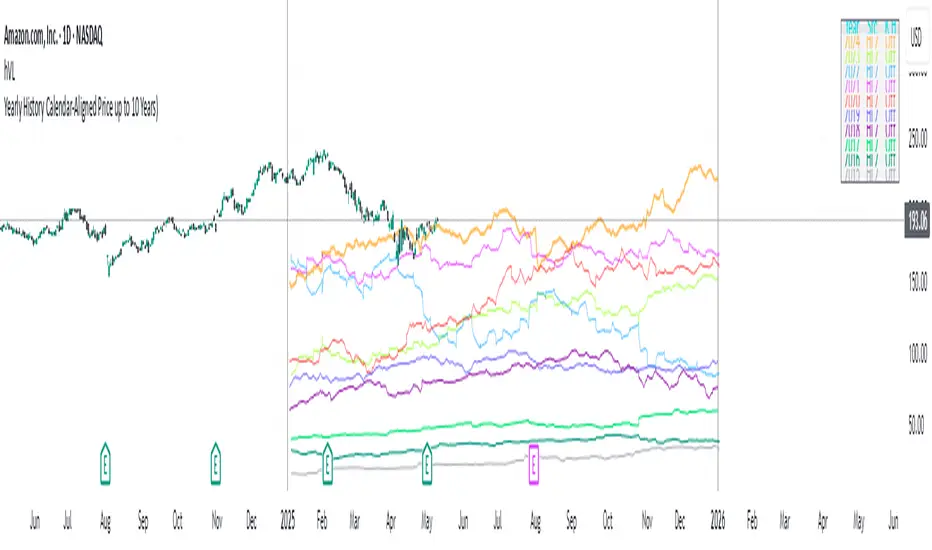

Yearly History Calendar-Aligned Price up to 10 Years)Overview

This indicator helps traders compare historical price patterns from the past 10 calendar years with the current price action. It overlays translucent lines (polylines) for each year’s price data on the same calendar dates, providing a visual reference for recurring trends. A dynamic table at the top of the chart summarizes the active years, their price sources, and history retention settings.

Key Features

Historical Projections

Displays price data from the last 10 years (e.g., January 5, 2023 vs. January 5, 2024).

Price Source Selection

Choose from Open, Low, High, Close, or HL2 ((High + Low)/2) for historical alignment.

The selected source is shown in the legend table.

Bulk Control Toggles

Show All Years : Display all 10 years simultaneously.

Keep History for All : Preserve historical lines on year transitions.

Hide History for All : Automatically delete old lines to update with current data.

Individual Year Settings

Toggle visibility for each year (-1 to -10) independently.

Customize color and line width for each year.

Control whether to keep or delete historical lines for specific years.

Visual Alignment Aids

Vertical lines mark yearly transitions for reference.

Polylines are semi-transparent for clarity.

Dynamic Legend Table

Shows active years, their price sources, and history status (On/Off).

Updates automatically when settings change.

How to Use

Configure Settings

Projection Years : Select how many years to display (1–10).

Price Source : Choose Open, Low, High, Close, or HL2 for historical alignment.

History Precision : Set granularity (Daily, 60m, or 15m).

Daily (D) is recommended for long-term analysis (covers 10 years).

60m/15m provides finer precision but may only cover 1–3 years due to data limits.

Adjust Visibility & History

Show Year -X : Enable/disable specific years for comparison.

Keep History for Year -X : Choose whether to retain historical lines or delete them on new year transitions.

Bulk Controls

Show All Years : Display all 10 years at once (overrides individual toggles).

Keep History for All / Hide History for All : Globally enable/disable history retention for all years.

Customize Appearance

Line Width : Adjust polyline thickness for better visibility.

Colors : Assign unique colors to each year for easy identification.

Interpret the Legend Table

The table shows:

Year : Label (e.g., "Year -1").

Source : The selected price type (e.g., "Close", "HL2").

Keep History : Indicates whether lines are preserved (On) or deleted (Off).

Tips for Optimal Use

Use Daily Timeframes for Long-Term Analysis :

Daily (1D) allows 10+ years of data. Smaller timeframes (60m/15m) may have limited historical coverage.

Compare Recurring Patterns :

Look for overlaps between historical polylines and current price to identify potential support/resistance levels.

Customize Colors & Widths :

Use contrasting colors for years you want to highlight. Adjust line widths to avoid clutter.

Leverage Global Toggles :

Enable Show All Years for a quick overview. Use Keep History for All to maintain continuity across transitions.

Example Workflow

Set Up :

Select Projection Years = 5.

Choose Price Source = Close.

Set History Precision = 1D for long-term data.

Customize :

Enable Show Year -1 to Show Year -5.

Assign distinct colors to each year.

Disable Keep History for All to ensure lines update on year transitions.

Analyze :

Observe how the 2023 close prices align with 2024’s price action.

Use vertical lines to identify yearly boundaries.

Common Questions

Why are some years missing?

Ensure the chart has sufficient historical data (e.g., daily charts cover 10 years, 60m/15m may only cover 1–3 years).

How do I update the data?

Adjust the Price Source or toggle years/history settings. The legend table updates automatically.

BTC Markup/Markdown Zones by Koenigsegg📈 BTC Markup/Markdown Zones

A handcrafted indicator designed to mark Bitcoin's most critical High Time Frame (HTF) structure shifts. This tool overlays true institutional-level Markup and Markdown Zones, selected manually after deep market review. Whether you're testing strategies or actively trading, this tool gives you the bigger picture at all times.

🔍 Key Features:

✅ HTF Markup & Markdown Zones

Every zone is manually selected — no indicators, no repainting. Just raw market history and real structure.

✅ Two Display Modes

• Background Zones — soft overlays with low opacity for visual context — with the option to increase opacity manually if desired.

• Start Candle Highlight — sharply highlighted candle marking the final pivot before a macro reversal.

✅ Custom Color Controls (Style Tab)

All visual styling lives in the Style tab, with clearly labeled fields:

• Markup Zone

• Markdown Zone

• Start Candle Highlight Markup

• Start Candle Highlight Markdown

✅ Minimal Input Section

Just one toggle: display mode. Everything else is kept clean and intuitive.

🧠 Purpose:

This script is made for any timeframe:

• Zoom into lower timeframes to know whether you're trading inside a Markup or Markdown

• Use it during strategy testing for true structural awareness

📅 Handpicked Macro Turning Points:

Each zone originates from a manually confirmed candle — the last meaningful candle before a shift in control between bulls and bears:

• FRI 19 AUG 2011 12PM – MARK DOWN

• THU 20 OCT 2011 12AM – MARK UP

• WED 10 APR 2013 12PM – MARK DOWN

• FRI 12 APR 2013 12PM – MARK UP

• SAT 30 NOV 2013 12AM – MARK DOWN

• WED 14 JAN 2015 12PM – MARK UP

• SUN 17 DEC 2017 12PM – MARK DOWN

• SAT 15 DEC 2018 12PM – MARK UP

• WED 14 APR 2021 4AM – MARK DOWN

• TUE 22 JUN 2021 12PM – MARK UP

• WED 10 NOV 2021 12PM – MARK DOWN

• MON 21 NOV 2022 8PM – MARK UP

• THU 14 MAR 2024 4AM – MARK DOWN

• MON 5 AUG 2024 12PM – MARK UP

• MON 20 JAN 2025 4AM – MARK DOWN

💡 Zones are manually updated by me after each new confirmed Markup or Markdown.

🧬 Fractal Structure for MTF Systems

Price is fractal — meaning the same principles of structure repeat across all timeframes. In Version 2, this tool evolves by introducing manually selected sub-zones inside each High Time Frame (HTF) Markup or Markdown. These sub-zones reflect Medium Timeframe (MTF) structure shifts, offering precision for traders who operate on both intraday and swing levels.

This makes the indicator ideal for low timeframe (LTF) Markup/Markdown awareness — whether you're managing 15m entries or building multi-timeframe confluence systems.

No auto-zones. No guesswork. Just clean, intentional structure division within the broader trend, handpicked for maximum clarity and edge.

💡 Pro Tip:

When price is inside a Markup Zone, shorting becomes riskier — you're trading against a macro bullish structure.

When inside a Markdown Zone, longing becomes riskier — you're fighting against confirmed bearish momentum.

Use this tool to stay aligned with the broader move, especially when zoomed into smaller timeframes or managing entries/exits during intraday setups.

📈 Markup Phase – Bullish Sentiment

Definition: A period where price makes higher highs and higher lows — the uptrend is in full force.

Why sentiment is bullish:

- Institutions and smart money are already positioned long.

- Public/institutional demand drives prices up.

- Momentum is supported by positive news, breakouts, and FOMO.

- Higher highs confirm buyers are in control.

📉 Markdown Phase – Bearish Sentiment

Definition: A period where price makes lower lows and lower highs — clear downtrend.

Why sentiment is bearish:

- Distribution has already occurred, and supply outweighs demand.

- Smart money is short or sidelined, waiting for deeper prices.

- Panic selling or trend-following traders add downside momentum.

- Lower lows confirm sellers are in control.

❌ Trading Against the Trend — Consequences:

-Reduced Probability of Success

-You’re fighting the dominant flow. Most participants are pushing in the opposite direction.

-Drawdowns & Stop-Outs

-Countertrend trades often get wicked or flushed before any meaningful move, especially without structure-based entries.

-Low Risk-Reward Ratio

-Trends offer sustained moves. Countertrend trades may have small take-profit zones or chop.

-Mental Drain & Doubt

-Fighting momentum causes anxiety, second-guessing, and emotional reactions.

-Missed Opportunities

-Focusing on fighting the trend makes you blind to the high-probability setups with the trend.

-Increased Transaction Costs

-More stop-outs and re-entries mean more fees, more friction.

-FOMO from Watching the Trend Run

-Entering countertrend means you might watch the trend explode without you.

-Confirmation Bias & Stubbornness

-Countertrend traders often look for reasons to justify staying in the wrong direction — leading to bigger losses.

🧠 Summary

In markup = bulls dominate → you swim with the current.

In markdown = bears dominate → going long is like pushing a rock uphill.

Trading with the trend is not just safer, it's smarter. The edge lives in momentum — not ego.

⚠️ Disclaimer

This indicator is for educational and analytical use only. It is not financial advice and should not be relied on for decision-making without personal analysis.

This is not a predictive tool. No indicator can forecast upcoming price movements.

What you see here is based purely on past market behavior — specifically, historical tops and bottoms that marked the start of confirmed reversals.

This script does not know where the next reversal begins, nor can it determine where a new Markup or Markdown starts or ends. It is designed to provide context, not prediction.

Always trade with responsibility and perform your own due diligence.

BTC Daily DCA CalculatorThe BTC Daily DCA Calculator is an indicator that calculates how much Bitcoin (BTC) you would own today by investing a fixed dollar amount daily (Dollar-Cost Averaging) over a user-defined period. Simply input your start date, end date, and daily investment amount, and the indicator will display a table on the last candle showing your total BTC, total invested, portfolio value, and unrealized yield (in USD and percentage).

Features

Customizable Inputs: Set the start date, end date, and daily dollar amount to simulate your DCA strategy.

Results Table: Displays on the last candle (top-right of the chart) with:

Total BTC: The accumulated Bitcoin from daily purchases.

Total Invested ($): The total dollars invested.

Portfolio Value ($): The current value of your BTC holdings.

Unrealized Yield ($): Your profit/loss in USD.

Unrealized Yield (%): Your profit/loss as a percentage.

Visual Markers: Green triangles below the chart mark each daily investment.

Overlay on Chart: The table and markers appear directly on the BTCUSD price chart for easy reference.

Daily Timeframe: Designed for Daily (1D) charts to ensure accurate calculations.

How to Use

Add the Indicator: Apply the indicator to a BTCUSD chart (e.g., Coinbase:BTCUSD, Binance:BTCUSDT).

Set Daily Timeframe: Ensure your chart is on the Daily (1D) timeframe, or the script will display an error.

Configure Inputs: Open the indicator’s Settings > Inputs tab and set:

Start Date: When to begin the DCA strategy (e.g., 2024-01-01).

End Date: When to end the strategy (e.g., 2025-04-27 or earlier).

Daily Investment ($): The fixed dollar amount to invest daily (e.g., $100).

View Results: Scroll to the last candle in your date range to see the results table in the top-right corner of the chart. Green triangles below the bars indicate investment days.

Settings

Start Date: Choose the start date for your DCA strategy (default: 2024-01-01).

End Date: Choose the end date (default: 2025-04-27). Must be after the start date and within available chart data.

Daily Investment ($): Set the daily investment amount (default: $100). Minimum is $0.01.

Notes

Timeframe: The indicator requires a Daily (1D) chart. Other timeframes will trigger an error.

Data: Ensure your BTCUSD chart has historical data for the selected date range. Use reliable pairs like Coinbase:BTCUSD or Binance:BTCUSDT.

Limitations: Does not account for trading fees or slippage. Future dates (beyond the current date) will not display results.

Performance: Works best with historical data. Free TradingView accounts may have limited historical data; consider premium for longer ranges.

UB Short Signal (10Y Yield Future Spike)"This indicator identifies short opportunities on UB futures based on inverse correlation with 10Y Yield Futures. A macro trading tool to be used with additional confirmations."

🎯 Indicator Strategy

This tool generates sell signals for Ultra Bond (UB) futures when:

The Micro 10-Year Yield Future shows an upward spike (> adjustable threshold)

Trading volume is significant (false signal filter)

Inverse correlation is confirmed (UB falls when 10Y rises)

⚙️ Parameters

Spike Threshold: Sensitivity adjustment (e.g., 0.08% for swing trading)

Minimum Volume: Default 100 (optimized for Micro 10Y contracts)

📊 Recent Backtest

06/15/2024: +0.10% spike → UB dropped -0.3% within 15 minutes

06/18/2024: Valid signal post-CPI release

⚠️ Disclaimer

Analytical tool only – not financial advice

Must be combined with proper risk management

Daily Bollinger Band StrategyOverview of the Daily Bollinger Band Strategy

1. Strategy Overview and Features

This strategy is a tool for backtesting a trading method that uses Bollinger Bands. It is *not* a tool for automated trading.

1-1. Main Display Items

The main chart displays the Bollinger Bands and the 200-day moving average.

It also shows the entry and exit points along with the position size (in units of 100 shares).

1-2. Summary of Trading Rules

For long (buy) strategies, the trade enters when the price crosses above the +1σ line of the Bollinger Bands, aiming to ride an upward trend. The position is exited when the price crosses below the middle band.

For short (sell) strategies, the trade enters when the price crosses below the -1σ line of the Bollinger Bands, aiming to ride a downward trend. The position is exited when the price crosses above the middle band.

1-3. Strategic Enhancements

The strategy uses the slope of the 200-day moving average to determine the trend direction and enter trades accordingly. This improves the win rate and payoff ratio.

Additionally, to reduce the probability of ruin, the risk per trade is limited to 1.0% of capital, and position sizing is adjusted using ATR (a volatility indicator).

2. Trading Rules

2-1. Chart Type

Only daily charts are used.

2-2. Indicators Used

(1) Bollinger Bands** (used for entry and exit signals)

- Period: Fixed at 80 days

- Upper and lower bands: Fixed at ±1σ

(2) Moving Average** (used to determine trend direction)

- Period: Fixed at 200 days

- Trend direction is judged based on whether the difference from the previous day is positive (upward) or negative (downward)

2-3. Buy Rules

Setup:

- Price crosses above the +1σ line from below

- Both the middle band and 200-day moving average are upward sloping

Entry:

- Buy at the next day’s market open using a market order

Exit:

- If the price crosses below the middle band, sell at the next day’s open using a market order

2-4. Sell Rules

Setup:

- Price crosses below the -1σ line from above

- Both the middle band and 200-day moving average are downward sloping

Entry:

- Sell at the next day’s market open using a market order

Exit:

- If the price crosses above the middle band, buy back at the next day’s open using a market order

2-5. Risk Management Rules

- Risk per trade: 1.0% of total capital (acceptable loss = capital × 1.0%)

- Position size: Acceptable loss ÷ 2ATR (rounded down to the nearest unit of 100 shares)

2-6. Other Notes

- No brokerage fees

- No pyramiding

- No partial exits

- No reverse positions (no “stop-and-reverse” trades)

3. Strategy Parameters

The following settings can be specified:

3-1. Period Settings

- Start date: Set the start date for the backtest period

- Stop date: Set the end date for the backtest period

3-2. Display of Trend and Signals

- Show trend: When checked, the background color of the bars is light red for an uptrend and light blue for a downtrend

- Show signal: When checked, entry and exit signals are displayed (note: signals are executed at the next day’s open, so there is a one-day lag in the display)

3-3. Capital Management Settings

- Funds: Capital available for trading (in JPY)

- Risk rate: Specify what percentage of the capital to risk per trade

Settings in the “Properties” tab are not used in this strategy.

4. Backtest Results (Example)

Here are the backtest results conducted by the author:

- Target Stocks: All components of the Nikkei 225

- Test Period: January 4, 2000 – December 30, 2024

- Data Points: 12,886

- Win Rate: 33.45%

- Net Profit: ¥82,132,380

- Payoff Ratio: 2.450

- Expected Value: ¥6,373.8

- Risk Rate: 1.0%

- Probability of Ruin: 0.00%

---

デイリー・ボリンジャーバンド・ストラテジーの概要

1. ストラテジーの概要と特徴

このストラテジーは、ボリンジャーバンドを使ったトレード手法のバックテストを行うツールです。自動売買を行うツールではありません。

1-1. 主な表示項目

メインチャートにボリンジャーバンドと 200日移動平均線を表示します。

また、エントリーと手仕舞いのタイミングと数量(100株単位)も表示されます。

1-2. トレードルールの概要

買い戦略の場合、ボリンジャーバンドの +1σ 超えでエントリーして上昇トレンドに乗り、ミドルバンドを割ったら決済します。

売り戦略の場合、ボリンジャーバンドの -1σ 割りでエントリーして下降トレンドに乗り、ミドルバンドを上抜けたら決済します。

1-3. ストラテジーの工夫点

200日移動平均線の傾きを見てトレンド方向にエントリーをしています。こうして勝率とペイオフレシオの成績を向上しています。

また、破産確率を抑えるために、リスク資金比率を 1.0% にして、ATR(ボラティリティ指標) を使って注文数を調整しています。

2. 売買ルール

2-1. 使用するチャート

日足チャートに限定します

2-2. 使用する指標

(1) ボリンジャーバンド(仕掛けと手仕舞いのシグナルに使用)

期間は80日に固定

上下バンドは ±1σ に固定

(2) 移動平均線(トレンドの方向を見るために使用)

期間は200日に固定

移動平均の値の前日との差がプラスのとき上向き、マイナスのとき下向きと判断

2-3. 買いのルール

セットアップ:ボリンジャーバンドの +1σ を価格が下から上に交差 かつ ミドルバンドと 200日移動平均線が上向き

仕掛け:翌日の寄り付きに成行で買う

手仕舞い:ボリンジャーバンドのミドルバンドを価格が上から下に交差したら、翌日の寄り付きに成行で売る

2-4. 売りのルール

セットアップ:ボリンジャーバンドの -1σ を価格が上から下に交差 かつ ミドルバンドと 200日移動平均線が下向き

仕掛け:翌日の寄り付きに成行で売る

手仕舞い:ボリンジャーバンドのミドルバンドを価格が下から上に交差したら、翌日の寄り付きに成行で買い戻す

2-5. 資金管理のルール

リスク資金比率:資産の 1.0%(許容損失 = 資産 × 1.0%)

注文数:許容損失 ÷ 2ATR(単元株数未満は切り捨て)

2-6. その他

仲介手数料:なし

ピラミッディング:なし

分割決済:なし

ドテン:しない

3. ストラテジーのパラメーター

次の項目が指定できます。

3-1. 期間の設定

Staer date : バックテストの検証期間の開始日を指定します

Stop date : バックテストの検証期間の終了日を指定します

3-2. トレンドとシグナルの表示

Show trend : チェックを入れると、バーの背景色が、トレンドが上昇のときは薄い赤で、下落のときは薄い青で表示されます

Show signal : チェックを入れると、エントリーと手仕舞いのシグナルを表示します(シグナルの出た翌日の寄り付きに売買をするので表示に1日のずれがあります)

3-3. 資金管理用の設定

Funds : トレード用の資金(円)

Risk rate : 許容損失を資金の何%にするかで指定します

「プロパティタブ」で設定する値は、このストラテジーでは有効ではありません。

4. バックテストの結果(例)

作者がバックテストを実施した結果をお知らせします。

対象銘柄:日経225構成銘柄すべて

対象期間:2000年1月4日~2024年12月30日

データ件数:12,886

勝率:33.45%

純利益:82,132,380

ペイオフレシオ:2.450

期待値:6,373.8

リスク資金比率:1.0%

破産確率:0.00%

Gann & Fibonacci Analysis for MSTRYes! Below is a step-by-step guide to performing Gann Analysis on MSTR in TradingView for the last year.

Step 1: Set Up the Chart

Open TradingView and search for MSTR (MicroStrategy).

Select the 1-day (D) timeframe to analyze the past year.

Set your chart to logarithmic scale (⚙ Settings → Scale → Log).

Enable grid lines for alignment (⚙ Settings → Appearance → Grid Lines).

Step 2: Identify Key Highs and Lows (Last Year)

Find the 52-week high and 52-week low for MSTR.

As of now:

52-Week High: ~$999 (March 2024).

52-Week Low: ~$280 (October 2023).

Step 3: Plot Gann Angles

Using TradingView's Gann Fan Tool:

Select "Gann Fan" (Press / and type “Gann Fan” to find it).

Start at the 52-week low (~$280, October 2023) and drag upwards.

Adjust the angles to match key levels:

1x1 (45°) → Main trendline

2x1 (26.5°) → Strong uptrend

4x1 (15°) → Weak trendline

1x2 (63.75°) → Strong resistance

Repeat the process from the 52-week high (~$999, March 2024) downward to see bearish angles.

Step 4: Apply Fibonacci & Gann Retracement Levels

Using Fibonacci Retracement:

Select "Fibonacci Retracement" tool.

Draw from 52-week high ($999) to 52-week low ($280).

Enable key Fibonacci levels:

23.6% ($816)

38.2% ($678)

50% ($640)

61.8% ($550)

78.6% ($430)

Watch for price reactions near these levels.

Using Gann Retracement Levels:

Select "Gann Box" in TradingView.

Draw from 52-week high ($999) to low ($280).

Enable key Gann retracement levels:

12.5% ($912)

25% ($850)

37.5% ($768)

50% ($640)

62.5% ($550)

75% ($480)

87.5% ($350)

Identify confluences with Gann angles and Fibonacci levels.

Step 5: Identify Significant Dates & Time Cycles

Use "Date Range" Tool in TradingView.

Mark major turning points:

High → Low: ~180 days (Half-year cycle).

Low → High: ~90 days (Quarter cycle).

Use Square-Outs (Time = Price method):

Example: If MSTR hit $500, check 500 days from key events.

Mark key anniversaries of past highs/lows for possible reversals.

Step 6: Analyze and Trade Execution

✅ If MSTR is at a Gann angle + Fibonacci level + key date → Expect a reaction.

✅ Use RSI, MACD, and Volume for extra confirmation.

✅ Set Stop-Loss at nearest Gann support/resistance.

Full Moon and New Moon IndicatorThe Full Moon & New Moon Indicator is a custom Pine Script indicator which marks Full Moon (Pournami) and New Moon (Amavasya) events on the price chart. This indicator helps traders who incorporate lunar cycles into their market analysis, as certain traders believe these cycles influence market sentiment and price action. The current script is added for the year 2024 and 2025 and the dates are considered as per the Telugu calendar.

Features

✅ Identifies and labels Full Moon & New Moon days on the chart for the year 2024 and 2025

How it Works!

On a Full Moon day, it places a yellow label ("Pournami") above the corresponding candle.

On a New Moon day, it places a blue label ("Amavasya") above the corresponding candle.

Example Usage

When a Full Moon label appears, check for potential trend reversals or high volatility.

When a New Moon label appears, watch for market consolidation or a shift in sentiment.

Combine with candlestick patterns, support/resistance, or momentum indicators for a stronger trading setup.

🚀 Add this indicator to your TradingView chart and explore the market’s reaction to lunar cycles! 🌕