Super MTF Clouds (4x3 Pairs)Overview:

This script is based on Ripster's MTF clouds, which transcends the standard moving average cloud indicator by offering a powerful and deeply customizable Multi-Timeframe (MTF) analysis. Instead of being limited to the moving averages of your current charts from the current timeframe, this tool allows you to project and visualize the trend and key support/resistance zones from up to 4 different timeframes simultaneously. User can input up to 6 different EMA values which will form 3 pairs of EMA clouds, for each of the timeframes.

The primary purpose is to provide traders with immediate confluence. By observing how price interacts with moving average clouds from higher timeframes (e.g., Hourly, Daily, Weekly), you can make more informed decisions on your active trading timeframe (e.g., 10 Minute). It's designed as a complete MTF Cloud toolkit, allowing you to display all necessary MTFs in a single script to build a comprehensive view of the market structure without having to flick to different timeframe to look for cloud positions.

Key features:

Four Independent Multi-Timeframe Slots: Each slot can be assigned any timeframe available on TradingView (e.g., D, W, M, 4H).

Three MA Pairs Per Timeframe: For each timeframe, configure up to three separate MA clouds (e.g., a 9/12 EMA pair, a 20/50 EMA pair, and a 100/200 SMA pair).

Complete Customisation: For every single moving average (24 in total), you can independently control:

MA Type: Choose between EMA or SMA.

Length: Any period you require.

Line Color: Full colour selection.

Line Thickness: Adjust the visual weight of each line.

Cloud Control: For every pair (12 in total), you can set the fill colour and transparency.

How To Use This Script:

This tool is best used for confirmation and context. Here are some practical strategies that one can adopt:

Trend Confluence: Before taking a trade based on a signal on your current timeframe, glance at the higher timeframe clouds. If you see a buy signal on the 15-minute chart and the price is currently trading above a thick, bullish Daily cloud, the probability of that trade succeeding is significantly higher. Conversely, shorting into strong HTF support is a low-probability trade.

Dynamic Support & Resistance: The edges of the higher timeframe clouds often act as powerful, dynamic levels of support and resistance. A pullback to the 4-Hour 50 EMA on your 15-minute chart can be a prime area to look for entries in the direction of the larger trend.

Gauging Market Regimes: Use the toggles in the settings to quickly switch between different views. You can have a "risk-on" view with short-term clouds and a "macro" view with weekly and monthly clouds. This helps you adapt your trading style to the current market conditions.

Key Settings:

1. Global Setting

Source For All MAs: This determines the price data point used for every single moving average calculation.

Default: hl2 (an average of the High and Low of each bar). This gives a smooth midpoint price.

Options: You can change this to Close (the most common method), Open, High, Low, or ohlc4 (an average of the open, high, low, and close), among others.

Recommendation: For most standard trend analysis, the default hl2 is the common choice.

2. The Timeframe Group Structure

The rest of the settings are organized into four identical, collapsible groups: "Timeframe 1 Settings" through "Timeframe 4 Settings". Each group acts as a self-contained control panel for one multi-timeframe view.

Within each timeframe group, you have two master controls:

Enable Timeframe: This is the main power switch for the entire group. Uncheck this box to instantly hide all three clouds and lines associated with this timeframe. This is perfect for quickly decluttering your chart or focusing on a different set of analyses.

Timeframe: This dropdown menu is the heart of the MTF feature. Here, you select the higher timeframe you want to analyse (e.g., 1D for Daily, 1W for Weekly, 4H for 4-Hour). All calculations for the three pairs within this group will be based on the timeframe you select here.

3. Pair-Specific Controls

Inside each timeframe group, there are three sections for "Pair 1", "Pair 2", and "Pair 3". These control each individual moving average cloud.

Enable Pair: Just like the master switch for the timeframe, this checkbox turns a single cloud and its two MA lines on or off.

For each pair, the settings are further broken down:

Moving Average Lines (A and B): These two rows control the two moving averages that form the cloud. 'A' is typically used for the shorter-period MA and 'B' for the longer-period one.

Type (A/B): A dropdown menu to select either EMA (Exponential Moving Average) or SMA (Simple Moving Average). EMAs react more quickly to recent price changes, while SMAs are smoother and react more slowly.

Length (A/B): The lookback period for the moving average (e.g., 21, 50, 200).

Color (A/B): Sets the specific colour of the MA line itself on your chart.

Cloud Fill Settings

Fill Color: This controls the colour of the shaded area (the "cloud") between the two moving average lines. For a consistent look, you can set this to the same colour as your shorter MA line.

Transparency: Controls how see-through the cloud is, on a scale of 0 to 100. 0 is a solid, opaque colour, while 100 is completely invisible. The default of 85 provides a light, "cloud-like" appearance that doesn't obscure the price action.

----------------------------------------------------------------------

If anything is not clear please let me know!

"12月4号是什么星座" için komut dosyalarını ara

MC Geopolitical Tension Events📌 Script Title: Geopolitical Tension Events

📖 Description:

This script highlights key geopolitical and military tension events from 1914 to 2024 that have historically impacted global markets.

It automatically plots vertical dashed lines and labels on the chart at the time of each major event. This allows traders and analysts to visually assess how markets have responded to global crises, wars, and significant political instability over time.

🧠 Use Cases:

Historical backtesting: Understand how market responded to past geopolitical shocks.

Contextual analysis: Add macro context to technical setups.

🗓️ List of Geopolitical Tension Events in the Script

Date Event Title Description

1914-07-28 WWI Begins Outbreak of World War I following the assassination of Archduke Franz Ferdinand.

1929-10-24 Wall Street Crash Black Thursday, the start of the 1929 stock market crash.

1939-09-01 WWII Begins Germany invades Poland, starting World War II.

1941-12-07 Pearl Harbor Japanese attack on Pearl Harbor; U.S. enters WWII.

1945-08-06 Hiroshima Bombing First atomic bomb dropped on Hiroshima by the U.S.

1950-06-25 Korean War Begins North Korea invades South Korea.

1962-10-16 Cuban Missile Crisis 13-day standoff between the U.S. and USSR over missiles in Cuba.

1973-10-06 Yom Kippur War Egypt and Syria launch surprise attack on Israel.

1979-11-04 Iran Hostage Crisis U.S. Embassy in Tehran seized; 52 hostages taken.

1990-08-02 Gulf War Begins Iraq invades Kuwait, triggering U.S. intervention.

2001-09-11 9/11 Attacks Coordinated terrorist attacks on the U.S.

2003-03-20 Iraq War Begins U.S.-led invasion of Iraq to remove Saddam Hussein.

2008-09-15 Lehman Collapse Bankruptcy of Lehman Brothers; peak of global financial crisis.

2014-03-01 Crimea Crisis Russia annexes Crimea from Ukraine.

2020-01-03 Soleimani Strike U.S. drone strike kills Iranian General Qasem Soleimani.

2022-02-24 Ukraine Invasion Russia launches full-scale invasion of Ukraine.

2023-10-07 Hamas-Israel War Hamas launches attack on Israel, sparking war in Gaza.

2024-01-12 Red Sea Crisis Houthis attack ships in Red Sea, prompting Western naval response.

Momentum Flip Pro - Advanced ZigZag Trading SystemMomentum Flip Pro - Advanced ZigZag Trading System

Complete User Guide

📊 What This Indicator Does

The Momentum Flip Pro is an advanced position-flipping trading system that automatically identifies trend reversals using ZigZag patterns combined with momentum analysis. It's designed for traders who want to always be in the market, flipping between long and short positions at optimal reversal points.

Key Features:

Automatically flips positions at each ZigZag reversal point

Dynamic stop loss placement at exact ZigZag levels

Real-time trading dashboard with performance metrics

Capital tracking and ROI calculation

Three momentum engines to choose from

🎯 How It Works

Entry Signal: When a ZigZag point appears (circle on chart), the indicator:

Exits current position (if any)

Immediately enters opposite position

Places stop loss at the exact ZigZag price

Exit Signal: Positions are closed when the next ZigZag appears, then immediately reversed

Position Management:

Long Entry: ZigZag bottom (momentum turns UP)

Short Entry: ZigZag peak (momentum turns DOWN)

Stop Loss: Always at the ZigZag entry price

Take Profit: Next ZigZag point (automatic position flip)

⚙️ Recommended Settings

For Day Trading (5m-15m timeframes):

Momentum Engine: Quantum

- RSI Length: 9-12

- Quantum Factor: 3.5-4.0

- RSI Smoothing: 3-5

- Threshold: 8-10

For Swing Trading (1H-4H timeframes):

Momentum Engine: MACD

- Fast Length: 12

- Slow Length: 26

- Signal Smoothing: 9

- MA Type: EMA

For Position Trading (Daily):

Momentum Engine: Moving Average

- Average Type: EMA or HMA

- Length: 20-50

📈 How to Use for Trading

Add to Chart:

Add indicator to your chart

Set your starting capital

Choose your preferred momentum engine

Understanding Signals:

Green circles: Strong bullish momentum reversal

Red circles: Strong bearish momentum reversal

Purple circles: Normal momentum reversal

Entry labels: Show exact entry points with tooltips

Trading Rules:

Enter LONG when you see an up arrow + green/purple circle

Enter SHORT when you see a down arrow + red/purple circle

Stop loss is automatically at the ZigZag level

Hold until next ZigZag appears (exit + reverse)

Risk Management:

Risk per trade = Entry Price - Stop Loss

Position size = (Capital * Risk %) / Risk per trade

Recommended risk: 1-2% per trade

💡 Best Practices

Market Conditions:

Works best in trending markets

Excellent for volatile pairs (crypto, forex majors)

Avoid during low volume/consolidation

Timeframe Selection:

Lower timeframes (5m-15m): More signals, higher noise

Higher timeframes (1H+): Fewer signals, higher reliability

Sweet spot: 15m-1H for most traders

Momentum Engine Selection:

Quantum: Best for volatile markets (crypto, indices)

MACD: Best for trending markets (forex, stocks)

Moving Average: Best for smooth trends (commodities)

📊 Dashboard Interpretation

The trading dashboard shows:

Current Capital: Your running balance

Position: Current trade direction

Entry/Stop: Your risk levels

Statistics: Win rate and performance

ROI: Overall return on investment

⚠️ Important Notes

Always Active: This system is always in a position (long or short)

No Neutral: You're either long or short, never flat

Automatic Reversal: Positions flip at each signal

Stop Loss: Fixed at entry ZigZag level (doesn't trail)

🎮 Quick Start Guide

Beginners: Start with default settings on 1H timeframe

Test First: Use paper trading to understand the signals

Small Size: Begin with 1% risk per trade

Track Results: Monitor the dashboard statistics

Adjust: Fine-tune momentum settings based on results

🔧 Customization Tips

Color Signals: Enable to see momentum strength

Dashboard Position: Move to preferred screen location

Visual Settings: Adjust colors for your theme

Alerts: Set up for automated notifications

This indicator is ideal for traders who prefer an always-in-market approach with clear entry/exit rules and automated position management. The key to success is choosing the right momentum engine for your market and maintaining disciplined risk management.

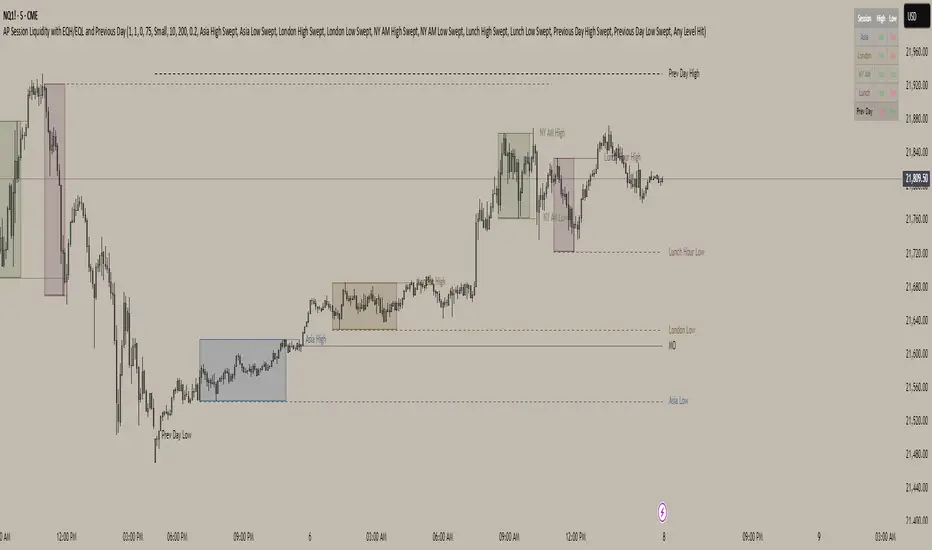

AP Session Liquidity with EQH/EQL and Previous DayThis indicator plots key intraday session highs and lows, along with essential market structure levels, to help traders identify areas of interest, potential liquidity zones, and high-probability trade setups. It includes the Asia Session High and Low (typically 00:00–08:00 UTC), London Session High and Low (08:00–12:00 UTC), New York AM Session High and Low (12:00–15:00 UTC), and New York Lunch High and Low (15:00–17:00 UTC). Additionally, it displays the Previous Day’s High and Low for context on recent price action, as well as automatically detected Equal Highs and Lows based on configurable proximity settings to highlight potential liquidity pools or engineered price levels. These session levels are widely used by institutional traders and are critical for analyzing market behavior during time-based volatility windows. Traders can use this indicator to anticipate breakouts, fakeouts, and reversals around session boundaries—such as liquidity grabs at Asia highs/lows before the London or New York sessions—or to identify key consolidation and expansion zones. Equal Highs and Lows serve as magnets for price, offering insight into potential stop hunts or inducement zones. This tool is ideal for day traders, scalpers, and smart money concept practitioners, and includes full customization for session timings, color schemes, line styles, and alert conditions. Whether you're trading price action, ICT concepts, or supply and demand, this indicator provides a powerful framework for intraday analysis.

Line Strategy v6Line Indicator for TradingView

This Pine Script indicator identifies the largest candles on both 5-minute and 1-hour timeframes within the last 240 five-minute bars. It provides visual markers and detailed information to help traders spot significant price movements.

Key Features

Dual Timeframe Analysis:

Identifies largest candle on 5-minute timeframe

Identifies largest candle on 1-hour timeframe (aggregated from 12 five-minute candles)

Visual Markers:

Blue label marks the highest-range 5-minute candle

Purple background highlights the highest-range hourly candle period

Information Table:

Shows price ranges for both timeframes

Displays precise timestamps for identified candles

Color-coded for quick reference

Progress Indicator:

Shows how many bars have been collected (out of 240 required)

How It Works

Data Collection:

Stores high, low, timestamp, and bar index of the last 240 five-minute candles

Automatically updates with each new bar

5-Minute Analysis:

Scans all 5-minute candles to find the one with the largest price range (high - low)

Marks this candle with a blue label showing its range

Hourly Analysis:

Groups 12 five-minute candles to form each hourly candle

Finds the hourly candle with the largest price range

Highlights the entire hour period with a purple background

Information Display:

Creates a table in the top-right corner showing:

Range values for both timeframes

Timestamps of identified candles

Time period of the largest hourly candle

Usage Instructions

Apply the indicator to any 5-minute chart

Wait for the indicator to collect 240 bars (about 20 trading hours)

Results will appear automatically:

Blue label on the largest 5-minute candle

Purple background on the largest hourly candle period

Information table with detailed metrics

Customization Options

You can easily adjust these aspects by modifying the code:

Colors of markers and table cells

Transparency levels of background highlights

Precision of range values displayed

Position of the information table

The indicator is optimized for performance and works in both historical and real-time modes.

DCA Investment Tracker Pro [tradeviZion]DCA Investment Tracker Pro: Educational DCA Analysis Tool

An educational indicator that helps analyze Dollar-Cost Averaging strategies by comparing actual performance with historical data calculations.

---

💡 Why I Created This Indicator

As someone who practices Dollar-Cost Averaging, I was frustrated with constantly switching between spreadsheets, calculators, and charts just to understand how my investments were really performing. I wanted to see everything in one place - my actual performance, what I should expect based on historical data, and most importantly, visualize where my strategy could take me over the long term .

What really motivated me was watching friends and family underestimate the incredible power of consistent investing. When Napoleon Bonaparte first learned about compound interest, he reportedly exclaimed "I wonder it has not swallowed the world" - and he was right! Yet most people can't visualize how their $500 monthly contributions today could become substantial wealth decades later.

Traditional DCA tracking tools exist, but they share similar limitations:

Require manual data entry and complex spreadsheets

Use fixed assumptions that don't reflect real market behavior

Can't show future projections overlaid on actual price charts

Lose the visual context of what's happening in the market

Make compound growth feel abstract rather than tangible

I wanted to create something different - a tool that automatically analyzes real market history, detects volatility periods, and shows you both current performance AND educational projections based on historical patterns right on your TradingView charts. As Warren Buffett said: "Someone's sitting in the shade today because someone planted a tree a long time ago." This tool helps you visualize your financial tree growing over time.

This isn't just another calculator - it's a visualization tool that makes the magic of compound growth impossible to ignore.

---

🎯 What This Indicator Does

This educational indicator provides DCA analysis tools. Users can input investment scenarios to study:

Theoretical Performance: Educational calculations based on historical return data

Comparative Analysis: Study differences between actual and theoretical scenarios

Historical Projections: Theoretical projections for educational analysis (not predictions)

Performance Metrics: CAGR, ROI, and other analytical metrics for study

Historical Analysis: Calculates historical return data for reference purposes

---

🚀 Key Features

Volatility-Adjusted Historical Return Calculation

Analyzes 3-20 years of actual price data for any symbol

Automatically detects high-volatility stocks (meme stocks, growth stocks)

Uses median returns for volatile stocks, standard CAGR for stable stocks

Provides conservative estimates when extreme outlier years are detected

Smart fallback to manual percentages when data insufficient

Customizable Performance Dashboard

Educational DCA performance analysis with compound growth calculations

Customizable table sizing (Tiny to Huge text options)

9 positioning options (Top/Middle/Bottom + Left/Center/Right)

Theme-adaptive colors (automatically adjusts to dark/light mode)

Multiple display layout options

Future Projection System

Visual future growth projections

Timeframe-aware calculations (Daily/Weekly/Monthly charts)

1-30 year projection options

Shows projected portfolio value and total investment amounts

Investment Insights

Performance vs benchmark comparison

ROI from initial investment tracking

Monthly average return analysis

Investment milestone alerts (25%, 50%, 100% gains)

Contribution tracking and next milestone indicators

---

📊 Step-by-Step Setup Guide

1. Investment Settings 💰

Initial Investment: Enter your starting lump sum (e.g., $60,000)

Monthly Contribution: Set your regular DCA amount (e.g., $500/month)

Return Calculation: Choose "Auto (Stock History)" for real data or "Manual" for fixed %

Historical Period: Select 3-20 years for auto calculations (default: 10 years)

Start Year: When you began investing (e.g., 2020)

Current Portfolio Value: Your actual portfolio worth today (e.g., $150,000)

2. Display Settings 📊

Table Sizes: Choose from Tiny, Small, Normal, Large, or Huge

Table Positions: 9 options - Top/Middle/Bottom + Left/Center/Right

Visibility Toggles: Show/hide Main Table and Stats Table independently

3. Future Projection 🔮

Enable Projections: Toggle on to see future growth visualization

Projection Years: Set 1-30 years ahead for analysis

Live Example - NASDAQ:META Analysis:

Settings shown: $60K initial + $500/month + Auto calculation + 10-year history + 2020 start + $150K current value

---

🔬 Pine Script Code Examples

Core DCA Calculations:

// Calculate total invested over time

months_elapsed = (year - start_year) * 12 + month - 1

total_invested = initial_investment + (monthly_contribution * months_elapsed)

// Compound growth formula for initial investment

theoretical_initial_growth = initial_investment * math.pow(1 + annual_return, years_elapsed)

// Future Value of Annuity for monthly contributions

monthly_rate = annual_return / 12

fv_contributions = monthly_contribution * ((math.pow(1 + monthly_rate, months_elapsed) - 1) / monthly_rate)

// Total expected value

theoretical_total = theoretical_initial_growth + fv_contributions

Volatility Detection Logic:

// Detect extreme years for volatility adjustment

extreme_years = 0

for i = 1 to historical_years

yearly_return = ((price_current / price_i_years_ago) - 1) * 100

if yearly_return > 100 or yearly_return < -50

extreme_years += 1

// Use median approach for high volatility stocks

high_volatility = (extreme_years / historical_years) > 0.2

calculated_return = high_volatility ? median_of_returns : standard_cagr

Performance Metrics:

// Calculate key performance indicators

absolute_gain = actual_value - total_invested

total_return_pct = (absolute_gain / total_invested) * 100

roi_initial = ((actual_value - initial_investment) / initial_investment) * 100

cagr = (math.pow(actual_value / initial_investment, 1 / years_elapsed) - 1) * 100

---

📊 Real-World Examples

See the indicator in action across different investment types:

Stable Index Investments:

AMEX:SPY (SPDR S&P 500) - Shows steady compound growth with standard CAGR calculations

Classic DCA success story: $60K initial + $500/month starting 2020. The indicator shows SPY's historical 10%+ returns, demonstrating how consistent broad market investing builds wealth over time. Notice the smooth theoretical growth line vs actual performance tracking.

MIL:VUAA (Vanguard S&P 500 UCITS) - Shows both data limitation and solution approaches

Data limitation example: VUAA shows "Manual (Auto Failed)" and "No Data" when default 10-year historical setting exceeds available data. The indicator gracefully falls back to manual percentage input while maintaining all DCA calculations and projections.

MIL:VUAA (Vanguard S&P 500 UCITS) - European ETF with successful 5-year auto calculation

Solution demonstration: By adjusting historical period to 5 years (matching available data), VUAA auto calculation works perfectly. Shows how users can optimize settings for newer assets. European market exposure with EUR denomination, demonstrating DCA effectiveness across different markets and currencies.

NYSE:BRK.B (Berkshire Hathaway) - Quality value investment with Warren Buffett's proven track record

Value investing approach: Berkshire Hathaway's legendary performance through DCA lens. The indicator demonstrates how quality companies compound wealth over decades. Lower volatility than tech stocks = standard CAGR calculations used.

High-Volatility Growth Stocks:

NASDAQ:NVDA (NVIDIA Corporation) - Demonstrates volatility-adjusted calculations for extreme price swings

High-volatility example: NVIDIA's explosive AI boom creates extreme years that trigger volatility detection. The indicator automatically switches to "Median (High Vol): 50%" calculations for conservative projections, protecting against unrealistic future estimates based on outlier performance periods.

NASDAQ:TSLA (Tesla) - Shows how 10-year analysis can stabilize volatile tech stocks

Stable long-term growth: Despite Tesla's reputation for volatility, the 10-year historical analysis (34.8% CAGR) shows consistent enough performance that volatility detection doesn't trigger. Demonstrates how longer timeframes can smooth out extreme periods for more reliable projections.

NASDAQ:META (Meta Platforms) - Shows stable tech stock analysis using standard CAGR calculations

Tech stock with stable growth: Despite being a tech stock and experiencing the 2022 crash, META's 10-year history shows consistent enough performance (23.98% CAGR) that volatility detection doesn't trigger. The indicator uses standard CAGR calculations, demonstrating how not all tech stocks require conservative median adjustments.

Notice how the indicator automatically detects high-volatility periods and switches to median-based calculations for more conservative projections, while stable investments use standard CAGR methods.

---

📈 Performance Metrics Explained

Current Portfolio Value: Your actual investment worth today

Expected Value: What you should have based on historical returns (Auto) or your target return (Manual)

Total Invested: Your actual money invested (initial + all monthly contributions)

Total Gains/Loss: Absolute dollar difference between current value and total invested

Total Return %: Percentage gain/loss on your total invested amount

ROI from Initial Investment: How your starting lump sum has performed

CAGR: Compound Annual Growth Rate of your initial investment (Note: This shows initial investment performance, not full DCA strategy)

vs Benchmark: How you're performing compared to the expected returns

---

⚠️ Important Notes & Limitations

Data Requirements: Auto mode requires sufficient historical data (minimum 3 years recommended)

CAGR Limitation: CAGR calculation is based on initial investment growth only, not the complete DCA strategy

Projection Accuracy: Future projections are theoretical and based on historical returns - actual results may vary

Timeframe Support: Works ONLY on Daily (1D), Weekly (1W), and Monthly (1M) charts - no other timeframes supported

Update Frequency: Update "Current Portfolio Value" regularly for accurate tracking

---

📚 Educational Use & Disclaimer

This analysis tool can be applied to various stock and ETF charts for educational study of DCA mathematical concepts and historical performance patterns.

Study Examples: Can be used with symbols like AMEX:SPY , NASDAQ:QQQ , AMEX:VTI , NASDAQ:AAPL , NASDAQ:MSFT , NASDAQ:GOOGL , NASDAQ:AMZN , NASDAQ:TSLA , NASDAQ:NVDA for learning purposes.

EDUCATIONAL DISCLAIMER: This indicator is a study tool for analyzing Dollar-Cost Averaging strategies. It does not provide investment advice, trading signals, or guarantees. All calculations are theoretical examples for educational purposes only. Past performance does not predict future results. Users should conduct their own research and consult qualified financial professionals before making any investment decisions.

---

© 2025 TradeVizion. All rights reserved.

OpenAI Signal Generator - Enhanced Accuracy# AI-Powered Trading Signal Generator Guide

## Overview

This is an advanced trading signal generator that combines multiple technical indicators using AI-enhanced logic to generate high-accuracy trading signals. The indicator uses a sophisticated combination of RSI, MACD, Bollinger Bands, EMAs, ADX, and volume analysis to provide reliable buy/sell signals with comprehensive market analysis.

## Key Features

### 1. Multi-Indicator Analysis

- **RSI (Relative Strength Index)**

- Length: 14 periods (default)

- Overbought: 70 (default)

- Oversold: 30 (default)

- Used for identifying overbought/oversold conditions

- **MACD (Moving Average Convergence Divergence)**

- Fast Length: 12 (default)

- Slow Length: 26 (default)

- Signal Length: 9 (default)

- Identifies trend direction and momentum

- **Bollinger Bands**

- Length: 20 periods (default)

- Multiplier: 2.0 (default)

- Measures volatility and potential reversal points

- **EMAs (Exponential Moving Averages)**

- Fast EMA: 9 periods (default)

- Slow EMA: 21 periods (default)

- Used for trend confirmation

- **ADX (Average Directional Index)**

- Length: 14 periods (default)

- Threshold: 25 (default)

- Measures trend strength

- **Volume Analysis**

- MA Length: 20 periods (default)

- Threshold: 1.5x average (default)

- Confirms signal strength

### 2. Advanced Features

- **Customizable Signal Frequency**

- Daily

- Weekly

- 4-Hour

- Hourly

- On Every Close

- **Enhanced Filtering**

- EMA crossover confirmation

- ADX trend strength filter

- Volume confirmation

- ATR-based volatility filter

- **Comprehensive Alert System**

- JSON-formatted alerts

- Detailed technical analysis

- Multiple timeframe analysis

- Customizable alert frequency

## How to Use

### 1. Initial Setup

1. Open TradingView and create a new chart

2. Select your preferred trading pair

3. Choose an appropriate timeframe

4. Apply the indicator to your chart

### 2. Configuration

#### Basic Settings

- **Signal Frequency**: Choose how often signals are generated

- Daily: Signals at the start of each day

- Weekly: Signals at the start of each week

- 4-Hour: Signals every 4 hours

- Hourly: Signals every hour

- On Every Close: Signals on every candle close

- **Enable Signals**: Toggle signal generation on/off

- **Include Volume**: Toggle volume analysis on/off

#### Technical Parameters

##### RSI Settings

- Adjust `rsi_length` (default: 14)

- Modify `rsi_overbought` (default: 70)

- Modify `rsi_oversold` (default: 30)

##### EMA Settings

- Fast EMA Length (default: 9)

- Slow EMA Length (default: 21)

##### MACD Settings

- Fast Length (default: 12)

- Slow Length (default: 26)

- Signal Length (default: 9)

##### Bollinger Bands

- Length (default: 20)

- Multiplier (default: 2.0)

##### Enhanced Filters

- ADX Length (default: 14)

- ADX Threshold (default: 25)

- Volume MA Length (default: 20)

- Volume Threshold (default: 1.5)

- ATR Length (default: 14)

- ATR Multiplier (default: 1.5)

### 3. Signal Interpretation

#### Buy Signal Requirements

1. RSI crosses above oversold level (30)

2. Price below lower Bollinger Band

3. MACD histogram increasing

4. Fast EMA above Slow EMA

5. ADX above threshold (25)

6. Volume above threshold (if enabled)

7. Market volatility check (if enabled)

#### Sell Signal Requirements

1. RSI crosses below overbought level (70)

2. Price above upper Bollinger Band

3. MACD histogram decreasing

4. Fast EMA below Slow EMA

5. ADX above threshold (25)

6. Volume above threshold (if enabled)

7. Market volatility check (if enabled)

### 4. Visual Indicators

#### Chart Elements

- **Moving Averages**

- SMA (Blue line)

- Fast EMA (Yellow line)

- Slow EMA (Purple line)

- **Bollinger Bands**

- Upper Band (Green line)

- Middle Band (Orange line)

- Lower Band (Green line)

- **Signal Markers**

- Buy Signals: Green triangles below bars

- Sell Signals: Red triangles above bars

- **Background Colors**

- Light green: Buy signal period

- Light red: Sell signal period

### 5. Alert System

#### Alert Types

1. **Signal Alerts**

- Generated when buy/sell conditions are met

- Includes comprehensive technical analysis

- JSON-formatted for easy integration

2. **Frequency-Based Alerts**

- Daily/Weekly/4-Hour/Hourly/Every Close

- Includes current market conditions

- Technical indicator values

#### Alert Message Format

```json

{

"symbol": "TICKER",

"side": "BUY/SELL/NONE",

"rsi": "value",

"macd": "value",

"signal": "value",

"adx": "value",

"bb_upper": "value",

"bb_middle": "value",

"bb_lower": "value",

"ema_fast": "value",

"ema_slow": "value",

"volume": "value",

"vol_ma": "value",

"atr": "value",

"leverage": 10,

"stop_loss_percent": 2,

"take_profit_percent": 5

}

```

## Best Practices

### 1. Signal Confirmation

- Wait for multiple confirmations

- Consider market conditions

- Check volume confirmation

- Verify trend strength with ADX

### 2. Risk Management

- Use appropriate position sizing

- Implement stop losses (default 2%)

- Set take profit levels (default 5%)

- Monitor market volatility

### 3. Optimization

- Adjust parameters based on:

- Trading pair volatility

- Market conditions

- Timeframe

- Trading style

### 4. Common Mistakes to Avoid

1. Trading without volume confirmation

2. Ignoring ADX trend strength

3. Trading against the trend

4. Not considering market volatility

5. Overtrading on weak signals

## Performance Monitoring

Regularly review:

1. Signal accuracy

2. Win rate

3. Average profit per trade

4. False signal frequency

5. Performance in different market conditions

## Disclaimer

This indicator is for educational purposes only. Past performance is not indicative of future results. Always use proper risk management and trade responsibly. Trading involves significant risk of loss and is not suitable for all investors.

PinBar Finder | @CRYPTOKAZANCEVPinBar Finder | @CRYPTOKAZANCEV

This script helps traders identify high-probability reversal points based on price action, specifically Pin Bars — a well-known candlestick pattern used in technical analysis.

What does the indicator do?

It detects bullish and bearish Pin Bars using a custom method for wick-to-body ratio and filters based on historical volatility (pseudo-ATR). A label appears on the chart with detailed info on wick and body size when a valid signal is found.

How does it work?

- The indicator calculates a pseudo-ATR based on the percentage range of the last 1000 candles.

- It then multiplies this value by a user-defined factor (default: 1.1) to set a dynamic threshold for wick size.

- Bullish Pin Bars are detected when the lower wick is at least 1.1 times the body and greater than the dynamic ATR.

- Bearish Pin Bars are detected when the upper wick meets similar conditions.

- Signals are shown using chart labels with exact wick/body percentages.

- Alerts are included for automation or integration with trading bots.

How to use it?

- Add the indicator to any timeframe and asset.

- Use the alerts to notify you when a Pin Bar appears.

- Ideal for traders who use candlestick reversal strategies or combine price action with other confluence tools.

- You can adjust the wick length multiplier to fit the volatility of the instrument.

What makes it original?

Unlike many public scripts that use fixed ratios, this script adapts wick length detection based on recent volatility (pseudo-ATR logic). This makes it more dynamic and suitable for different markets and timeframes.

Developed by: @ZeeZeeMon

Original author name on chart: @CRYPTOKAZANCEV

This script is open-source and educational. Use at your own discretion.

PinBar Finder | @CRYPTOKAZANCEV

Этот скрипт помогает трейдерам находить точки потенциального разворота на основе прайс-экшена, а именно — свечного паттерна «Пин-бар». Индикатор автоматически определяет бычьи и медвежьи пин-бары с учетом адаптивных параметров волатильности.

Что делает индикатор?

Скрипт ищет свечи, у которых тень в несколько раз превышает тело (пин-бары), и отображает на графике точную информацию о длине тела и тени. Это полезно для трейдеров, использующих свечные сигналы на разворот.

Как работает?

- Рассчитывается псевдо-ATR по 1000 последним свечам на основе процентного диапазона high-low.

- Этот ATR умножается на заданный множитель (по умолчанию: 1.1), чтобы динамически задать минимальную длину тени.

- Бычий пин-бар определяется, когда нижняя тень больше тела в 1.1 раза и превышает ATR.

- Медвежий пин-бар — аналогично, но для верхней тени.

- Индикатор отображает лейблы с точными значениями тела и тени.

- Реализованы условия для оповещений (alerts).

Как использовать?

- Добавьте индикатор на нужный график и таймфрейм.

- Настройте alerts, чтобы не пропустить сигналы.

- Особенно полезен для трейдеров, работающих со свечным анализом, стратегиями разворота, а также в сочетании с другими индикаторами.

В чем оригинальность?

В отличие от многих скриптов, использующих фиксированные параметры, здесь используется динамический расчет длины тени на основе волатильности. Это делает скрипт адаптивным к рынку и таймфрейму.

Разработчик: @ZeeZeeMon

Оригинальное имя автора на графике: @CRYPTOKAZANCEV

Скрипт является открытым и предназначен для образовательных целей. Используйте на своё усмотрение.

FVG Premium [no1x]█ OVERVIEW

This indicator provides a comprehensive toolkit for identifying, visualizing, and tracking Fair Value Gaps (FVGs) across three distinct timeframes (current chart, a user-defined Medium Timeframe - MTF, and a user-defined High Timeframe - HTF). It is designed to offer traders enhanced insight into FVG dynamics through detailed state monitoring (formation, partial fill, full mitigation, midline touch), extensive visual customization for FVG representation, and a rich alert system for timely notifications on FVG-related events.

█ CONCEPTS

This indicator is built upon the core concept of Fair Value Gaps (FVGs) and their significance in price action analysis, offering a multi-layered approach to their detection and interpretation across different timeframes.

Fair Value Gaps (FVGs)

A Fair Value Gap (FVG), also known as an imbalance, represents a range in price delivery where one side of the market (buying or selling) was more aggressive, leaving an inefficiency or an "imbalance" in the price action. This concept is prominently featured within Smart Money Concepts (SMC) and Inner Circle Trader (ICT) methodologies, where such gaps are often interpreted as footprints left by "smart money" due to rapid, forceful price movements. These methodologies suggest that price may later revisit these FVG zones to rebalance a prior inefficiency or to seek liquidity before continuing its path. These gaps are typically identified by a three-bar pattern:

Bullish FVG : This is a three-candle formation where the second candle shows a strong upward move. The FVG is the space created between the high of the first candle (bottom of FVG) and the low of the third candle (top of FVG). This indicates a strong upward impulsive move.

Bearish FVG : This is a three-candle formation where the second candle shows a strong downward move. The FVG is the space created between the low of the first candle (top of FVG) and the high of the third candle (bottom of FVG). This indicates a strong downward impulsive move.

FVGs are often watched by traders as potential areas where price might return to "rebalance" or find support/resistance.

Multi-Timeframe (MTF) Analysis

The indicator extends FVG detection beyond the current chart's timeframe (Low Timeframe - LTF) to two higher user-defined timeframes: Medium Timeframe (MTF) and High Timeframe (HTF). This allows traders to:

Identify FVGs that might be significant on a broader market structure.

Observe how FVGs from different timeframes align or interact.

Gain a more comprehensive perspective on potential support and resistance zones.

FVG State and Lifecycle Management

The indicator actively tracks the lifecycle of each detected FVG:

Formation : The initial identification of an FVG.

Partial Fill (Entry) : When price enters but does not completely pass through the FVG. The indicator updates the "current" top/bottom of the FVG to reflect the filled portion.

Midline (Equilibrium) Touch : When price touches the 50% level of the FVG.

Full Mitigation : When price completely trades through the FVG, effectively "filling" or "rebalancing" the gap. The indicator records the mitigation time.

This state tracking is crucial for understanding how price interacts with these zones.

FVG Classification (Large FVG)

FVGs can be optionally classified as "Large FVGs" (LV) if their size (top to bottom range) exceeds a user-defined multiple of the Average True Range (ATR) for that FVG's timeframe. This helps distinguish FVGs that are significantly larger relative to recent volatility.

Visual Customization and Information Delivery

A key concept is providing extensive control over how FVGs are displayed. This control is achieved through a centralized set of visual parameters within the indicator, allowing users to configure numerous aspects (colors, line styles, visibility of boxes, midlines, mitigation lines, labels, etc.) for each timeframe. Additionally, an on-chart information panel summarizes the nearest unmitigated bullish and bearish FVG levels for each active timeframe, providing a quick glance at key price points.

█ FEATURES

This indicator offers a rich set of features designed to provide a highly customizable and comprehensive Fair Value Gap (FVG) analysis experience. Users can tailor the FVG detection, visual representation, and alerting mechanisms across three distinct timeframes: the current chart (Low Timeframe - LTF), a user-defined Medium Timeframe (MTF), and a user-defined High Timeframe (HTF).

Multi-Timeframe FVG Detection and Display

The core strength of this indicator lies in its ability to identify and display FVGs from not only the current chart's timeframe (LTF) but also from two higher, user-selectable timeframes (MTF and HTF).

Timeframe Selection: Users can specify the exact MTF (e.g., "60", "240") and HTF (e.g., "D", "W") through dedicated inputs in the "MTF (Medium Timeframe)" and "HTF (High Timeframe)" settings groups. The visibility of FVGs from these higher timeframes can be toggled independently using the "Show MTF FVGs" and "Show HTF FVGs" checkboxes.

Consistent Detection Logic: The FVG detection logic, based on the classic three-bar imbalance pattern detailed in the 'Concepts' section, is applied consistently across all selected timeframes (LTF, MTF, HTF)

Timeframe-Specific Visuals: Each timeframe's FVGs (LTF, MTF, HTF) can be customized with unique colors for bullish/bearish states and their mitigated counterparts. This allows for easy visual differentiation of FVGs originating from different market perspectives.

Comprehensive FVG Visualization Options

The indicator provides extensive control over how FVGs are visually represented on the chart for each timeframe (LTF, MTF, HTF).

FVG Boxes:

Visibility: Main FVG boxes can be shown or hidden per timeframe using the "Show FVG Boxes" (for LTF), "Show Boxes" (for MTF/HTF) inputs.

Color Customization: Colors for bullish, bearish, active, and mitigated FVG boxes (including Large FVGs, if classified) are fully customizable for each timeframe.

Box Extension & Length: FVG boxes can either be extended to the right indefinitely ("Extend Boxes Right") or set to a fixed length in bars ("Short Box Length" or "Box Length" equivalent inputs).

Box Labels: Optional labels can display the FVG's timeframe and fill percentage on the box. These labels are configurable for all timeframes (LTF, MTF, and HTF). Please note: If FVGs are positioned very close to each other on the chart, their respective labels may overlap. This can potentially lead to visual clutter, and it is a known behavior in the current version of the indicator.

Box Borders: Visibility, width, style (solid, dashed, dotted), and color of FVG box borders are customizable per timeframe.

Midlines (Equilibrium/EQ):

Visibility: The 50% level (midline or EQ) of FVGs can be shown or hidden for each timeframe.

Style Customization: Width, style, and color of the midline are customizable per timeframe. The indicator tracks if this midline has been touched by price.

Mitigation Lines:

Visibility: Mitigation lines (representing the FVG's opening level that needs to be breached for full mitigation) can be shown or hidden for each timeframe. If shown, these lines are always extended to the right.

Style Customization: Width, style, and color of the mitigation line are customizable per timeframe.

Mitigation Line Labels: Optional price labels can be displayed on mitigation lines, with a customizable horizontal bar offset for positioning. For optimal label placement, the following horizontal bar offsets are recommended: 4 for LTF, 8 for MTF, and 12 for HTF.

Persistence After Mitigation: Users can choose to keep mitigation lines visible even after an FVG is fully mitigated, with a distinct color for such lines. Importantly, this option is only effective if the general setting 'Hide Fully Mitigated FVGs' is disabled, as otherwise, the entire FVG and its lines will be removed upon mitigation.

FVG State Management and Behavior

The indicator tracks and visually responds to changes in FVG states.

Hide Fully Mitigated FVGs: This option, typically found in the indicator's general settings, allows users to automatically remove all visual elements of an FVG from the chart once price has fully mitigated it. This helps maintain chart clarity by focusing on active FVGs.

Partial Fill Visualization: When price enters an FVG, the indicator offers a dynamic visual representation: the portion of the FVG that has been filled is shown as a "mitigated box" (typically with a distinct color), while the original FVG box shrinks to clearly highlight the remaining, unfilled portion. This two-part display provides an immediate visual cue about how much of the FVG's imbalance has been addressed and what potential remains within the gap.

Visual Filtering by ATR Proximity: To help users focus on the most relevant price action, FVGs can be dynamically hidden if they are located further from the current price than a user-defined multiple of the Average True Range (ATR). This behavior is controlled by the "Filter Band Width (ATR Multiple)" input; setting this to zero disables the filter entirely, ensuring all detected FVGs remain visible regardless of their proximity to price.

Alternative Usage Example: Mitigation Lines as Key Support/Resistance Levels

For traders preferring a minimalist chart focused on key Fair Value Gap (FVG) levels, the indicator's visualization settings can be customized to display only FVG mitigation lines. This approach leverages these lines as potential support and resistance zones, reflecting areas where price might revisit to address imbalances.

To configure this view:

Disable FVG Boxes: Turn off "Show FVG Boxes" (for LTF) or "Show Boxes" (for MTF/HTF) for the desired timeframes.

Hide Midlines: Disable the visibility of the 50% FVG Midlines (Equilibrium/EQ).

Ensure Mitigation Lines are Visible: Keep "Mitigation Lines" enabled.

Retain All Mitigation Lines:

Disable the "Hide Fully Mitigated FVGs" option in the general settings.

Enable the feature to "keep mitigation lines visible even after an FVG is fully mitigated". This ensures lines from all FVGs (active or fully mitigated) remain on the chart, which is only effective if "Hide Fully Mitigated FVGs" is disabled.

This setup offers:

A Decluttered Chart: Focuses solely on the FVG opening levels.

Precise S/R Zones: Treats mitigation lines as specific points for potential price reactions.

Historical Level Analysis: Includes lines from past, fully mitigated FVGs for a comprehensive view of significant price levels.

For enhanced usability with this focused view, consider these optional additions:

The on-chart Information Panel can be activated to display a quick summary of the nearest unmitigated FVG levels.

Mitigation Line Labels can also be activated for clear price level identification. A customizable horizontal bar offset is available for positioning these labels; for example, offsets of 4 for LTF, 8 for MTF, and 12 for HTF can be effective.

FVG Classification (Large FVG)

This feature allows for distinguishing FVGs based on their size relative to market volatility.

Enable Classification: Users can enable "Classify FVG (Large FVG)" to identify FVGs that are significantly larger than average.

ATR-Based Threshold: An FVG is classified as "Large" if its height (price range) is greater than or equal to the Average True Range (ATR) of its timeframe multiplied by a user-defined "Large FVG Threshold (ATR Multiple)". The ATR period for this calculation is also configurable.

Dedicated Colors: Large FVGs (both bullish/bearish and active/mitigated) can be assigned unique colors, making them easily distinguishable on the chart.

Panel Icon: Large FVGs are marked with a special icon in the Info Panel.

Information Panel

An on-chart panel provides a quick summary of the nearest unmitigated FVG levels.

Visibility and Position: The panel can be shown/hidden and positioned in any of the nine standard locations on the chart (e.g., Top Right, Middle Center).

Content: It displays the price levels of the nearest unmitigated bullish and bearish FVGs for LTF, MTF (if active), and HTF (if active). It also indicates if these nearest FVGs are Large FVGs (if classification is enabled) using a selectable icon.

Styling: Text size, border color, header background/text colors, default text color, and "N/A" cell background color are customizable.

Highlighting: Background and text colors for the cells displaying the overall nearest bullish and bearish FVG levels (across all active timeframes) can be customized to draw attention to the most proximate FVG.

Comprehensive Alert System

The indicator offers a granular alert system for various FVG-related events, configurable for each timeframe (LTF, MTF, HTF) independently. Users can enable alerts for:

New FVG Formation: Separate alerts for new bullish and new bearish FVG formations.

FVG Entry/Partial Fill: Separate alerts for price entering a bullish FVG or a bearish FVG.

FVG Full Mitigation: Separate alerts for full mitigation of bullish and bearish FVGs.

FVG Midline (EQ) Touch: Separate alerts for price touching the midline of a bullish or bearish FVG.

Alert messages are detailed, providing information such as the timeframe, FVG type (bull/bear, Large FVG), relevant price levels, and timestamps.

█ NOTES

This section provides additional information regarding the indicator's usage, performance considerations, and potential interactions with the TradingView platform. Understanding these points can help users optimize their experience and troubleshoot effectively.

Performance and Resource Management

Maximum FVGs to Track : The "Max FVGs to Track" input (defaulting to 25) limits the number of FVG objects processed for each category (e.g., LTF Bullish, MTF Bearish). Increasing this value significantly can impact performance due to more objects being iterated over and potentially drawn, especially when multiple timeframes are active.

Drawing Object Limits : To manage performance, this script sets its own internal limits on the number of drawing objects it displays. While it allows for up to approximately 500 lines (max_lines_count=500) and 500 labels (max_labels_count=500), the number of FVG boxes is deliberately restricted to a maximum of 150 (max_boxes_count=150). This specific limit for boxes is a key performance consideration: displaying too many boxes can significantly slow down the indicator, and a very high number is often not essential for analysis. Enabling all visual elements for many FVGs across all three timeframes can cause the indicator to reach these internal limits, especially the stricter box limit

Optimization Strategies : To help you manage performance, reduce visual clutter, and avoid exceeding drawing limits when using this indicator, I recommend the following strategies:

Maintain or Lower FVG Tracking Count: The "Max FVGs to Track" input defaults to 25. I find this value generally sufficient for effective analysis and balanced performance. You can keep this default or consider reducing it further if you experience performance issues or prefer a less dense FVG display.

Utilize Proximity Filtering: I suggest activating the "Filter Band Width (ATR Multiple)" option (found under "General Settings") to display only those FVGs closer to the current price. From my experience, a value of 5 for the ATR multiple often provides a good starting point for balanced performance, but you should feel free to adjust this based on market volatility and your specific trading needs.

Hide Fully Mitigated FVGs: I strongly recommend enabling the "Hide Fully Mitigated FVGs" option. This setting automatically removes all visual elements of an FVG from the chart once it has been fully mitigated by price. Doing so significantly reduces the number of active drawing objects, lessens computational load, and helps maintain chart clarity by focusing only on active, relevant FVGs.

Disable FVG Display for Unused Timeframes: If you are not actively monitoring certain higher timeframes (MTF or HTF) for FVG analysis, I advise disabling their display by unchecking "Show MTF FVGs" or "Show HTF FVGs" respectively. This can provide a significant performance boost.

Simplify Visual Elements: For active FVGs, consider hiding less critical visual elements if they are not essential for your specific analysis. This could include box labels, borders, or even entire FVG boxes if, for example, only the mitigation lines are of interest for a particular timeframe.

Settings Changes and Platform Limits : This indicator is comprehensive and involves numerous calculations and drawings. When multiple settings are changed rapidly in quick succession, it is possible, on occasion, for TradingView to issue a "Runtime error: modify_study_limit_exceeding" or similar. This can cause the indicator to temporarily stop updating or display errors.

Recommended Approach : When adjusting settings, it is advisable to wait a brief moment (a few seconds) after each significant change. This allows the indicator to reprocess and update on the chart before another change is made

Error Recovery : Should such a runtime error occur, making a minor, different adjustment in the settings (e.g., toggling a checkbox off and then on again) and waiting briefly will typically allow the indicator to recover and resume correct operation. This behavior is related to platform limitations when handling complex scripts with many inputs and drawing objects.

Multi-Timeframe (MTF/HTF) Data and Behavior

HTF FVG Confirmation is Essential: : For an FVG from a higher timeframe (MTF or HTF) to be identified and displayed on your current chart (LTF), the three-bar pattern forming the FVG on that higher timeframe must consist of fully closed bars. The indicator does not draw speculative FVGs based on incomplete/forming bars from higher timeframes.

Data Retrieval and LTF Processing: The indicator may use techniques like lookahead = barmerge.lookahead_on for timely data retrieval from higher timeframes. However, the actual detection of an FVG occurs after all its constituent bars on the HTF have closed.

Appearance Timing on LTF (1 LTF Candle Delay): As a natural consequence of this, an FVG that is confirmed on an HTF (i.e., its third bar closes) will typically become visible on your LTF chart one LTF bar after its confirmation on the HTF.

Example: Assume an FVG forms on a 30-minute chart at 15:30 (i.e., with the close of the 30-minute bar that covers the 15:00-15:30 period). If you are monitoring this FVG on a 15-minute chart, the indicator will detect this newly formed 30-minute FVG while processing the data for the 15-minute bar that starts at 15:30 and closes at 15:45. Therefore, the 30-minute FVG will become visible on your 15-minute chart at the earliest by 15:45 (i.e., with the close of that relevant 15-minute LTF candle). This means the HTF FVG is reflected on the LTF chart with a delay equivalent to one LTF candle.

FVG Detection and Display Logic

Fair Value Gaps (FVGs) on the current chart timeframe (LTF) are detected based on barstate.isconfirmed. This means the three-bar pattern must be complete with closed bars before an FVG is identified. This confirmation method prevents FVGs from being prematurely identified on the forming bar.

Alerts

Alert Setup : To receive alerts from this indicator, you must first ensure you have enabled the specific alert conditions you are interested in within the indicator's own settings (see 'Comprehensive Alert System' under the 'FEATURES' section). Once configured, open TradingView's 'Create Alert' dialog. In the 'Condition' tab, select this indicator's name, and crucially, choose the 'Any alert() function call' option from the dropdown list. This setup allows the indicator to trigger alerts based on the precise event conditions you have activated in its settings

Alert Frequency : Alerts are designed to trigger once per bar close (alert.freq_once_per_bar_close) for the specific event.

User Interface (UI) Tips

Settings Group Icons: In the indicator settings menu, timeframe-specific groups are marked with star icons for easier navigation: 🌟 for LTF (Current Chart Timeframe), 🌟🌟 for MTF (Medium Timeframe), and 🌟🌟🌟 for HTF (High Timeframe).

Dependent Inputs: Some input settings are dependent on others being enabled. These dependencies are visually indicated in the settings menu using symbols like "↳" (dependent setting on the next line), "⟷" (mutually exclusive inline options), or "➜" (directly dependent inline option).

Settings Layout Overview: The indicator settings are organized into logical groups for ease of use. Key global display controls – such as toggles for MTF FVGs, HTF FVGs (along with their respective timeframe selectors), and the Information Panel – are conveniently located at the very top within the '⚙️ General Settings' group. This placement allows for quick access to frequently adjusted settings. Other sections provide detailed customization options for each timeframe (LTF, MTF, HTF), specific FVG components, and alert configurations.

█ FOR Pine Script® CODERS

This section provides a high-level overview of the FVG Premium indicator's internal architecture, data flow, and the interaction between its various library components. It is intended for Pine Script™ programmers who wish to understand the indicator's design, potentially extend its functionality, or learn from its structure.

System Architecture and Modular Design

The indicator is architected moduarly, leveraging several custom libraries to separate concerns and enhance code organization and reusability. Each library has a distinct responsibility:

FvgTypes: Serves as the foundational data definition layer. It defines core User-Defined Types (UDTs) like fvgObject (for storing all attributes of an FVG) and drawSettings (for visual configurations), along with enumerations like tfType.

CommonUtils: Provides utility functions for common tasks like mapping user string inputs (e.g., "Dashed" for line style) to their corresponding Pine Script™ constants (e.g., line.style_dashed) and formatting timeframe strings for display.

FvgCalculations: Contains the core logic for FVG detection (both LTF and MTF/HTF via requestMultiTFBarData), FVG classification (Large FVGs based on ATR), and checking FVG interactions with price (mitigation, partial fill).

FvgObject: Implements an object-oriented approach by attaching methods to the fvgObject UDT. These methods manage the entire visual lifecycle of an FVG on the chart, including drawing, updating based on state changes (e.g., mitigation), and deleting drawing objects. It's responsible for applying the visual configurations defined in drawSettings.

FvgPanel: Manages the creation and dynamic updates of the on-chart information panel, which displays key FVG levels.

The main indicator script acts as the orchestrator, initializing these libraries, managing user inputs, processing data flow between libraries, and handling the main event loop (bar updates) for FVG state management and alerts.

Core Data Flow and FVG Lifecycle Management

The general data flow and FVG lifecycle can be summarized as follows:

Input Processing: User inputs from the "Settings" dialog are read by the main indicator script. Visual style inputs (colors, line styles, etc.) are consolidated into a types.drawSettings object (defined in FvgTypes). Other inputs (timeframes, filter settings, alert toggles) control the behavior of different modules. CommonUtils assists in mapping some string inputs to Pine constants.

FVG Detection:

For the current chart timeframe (LTF), FvgCalculations.detectFvg() identifies potential FVGs based on bar patterns.

For MTF/HTF, the main indicator script calls FvgCalculations.requestMultiTFBarData() to fetch necessary bar data from higher timeframes, then FvgCalculations.detectMultiTFFvg() identifies FVGs.

Newly detected FVGs are instantiated as types.fvgObject and stored in arrays within the main script. These objects also undergo classification (e.g., Large FVG) by FvgCalculations.

State Update & Interaction: On each bar, the main indicator script iterates through active FVG objects to manage their state based on price interaction:

Initially, the main script calls FvgCalculations.fvgInteractionCheck() to efficiently determine if the current bar's price might be interacting with a given FVG.

If a potential interaction is flagged, the main script then invokes methods directly on the fvgObject instance (e.g., updateMitigation(), updatePartialFill(), checkMidlineTouch(), which are part of FvgObject).

These fvgObject methods are responsible for the detailed condition checking and the actual modification of the FVG's state. For instance, the updateMitigation() and updatePartialFill() methods internally utilize specific helper functions from FvgCalculations (like checkMitigation() and checkPartialMitigation()) to confirm the precise nature of the interaction before updating the fvgObject’s state fields (such as isMitigated, currentTop, currentBottom, or isMidlineTouched).

Visual Rendering:

The FvgObject.updateDrawings() method is called for each fvgObject. This method is central to drawing management; it creates, updates, or deletes chart drawings (boxes, lines, labels) based on the FVG's current state, its prev_* (previous bar state) fields for optimization, and the visual settings passed via the drawSettings object.

Information Panel Update: The main indicator script determines the nearest FVG levels, populates a panelData object (defined in FvgPanelLib), and calls FvgPanel.updatePanel() to refresh the on-chart display.

Alert Generation: Based on the updated FVG states and user-enabled alert settings, the main indicator script constructs and triggers alerts using Pine Script's alert() function."

Key Design Considerations

UDT-Centric Design: The fvgObject UDT is pivotal, acting as a stateful container for all information related to a single FVG. Most operations revolve around creating, updating, or querying these objects.

State Management: To optimize drawing updates and manage FVG lifecycles, fvgObject instances store their previous bar's state (e.g., prevIsVisible, prevCurrentTop). The FvgObject.updateDrawings() method uses this to determine if a redraw is necessary, minimizing redundant drawing calls.

Settings Object: A drawSettings object is populated once (or when inputs change) and passed to drawing functions. This avoids repeatedly reading numerous input() values on every bar or within loops, improving performance.

Dynamic Arrays for FVG Storage: Arrays are used to store collections of fvgObject instances, allowing for dynamic management (adding new FVGs, iterating for updates).

Precision Entry Signals (RSI + MA12 Logic)Description:

This script provides precise entry signals based on a clean confluence of MA12 breakouts and RSI momentum, filtered by a VWMA (Volume-Weighted Moving Average) of the RSI.

-----------------------------------------------------------------------------------------------------------------

🔹 Long entry conditions:

- Candle opens below the 12-period MA and closes above it

- RSI crosses above its VWMA

- Previous candle is bearish (additional confirmation)

🔹 Short entry conditions:

- Candle opens above the 12-period MA and closes below it

- RSI crosses below its VWMA

- Previous candle is bullish

----------------------------------------------------------------------------------------------------------------

Once a signal is confirmed, the script automatically draws:

Entry line (at close price)

Stop Loss line (just below recent lows for long, or above highs for short)

Take Profit 1 (1R)

Take Profit 2 (2R)

Labels are attached to the lines for clarity: ENTRY, SL, TP1, and TP2.

⚠️ Note: This tool only provides entry signals and visual risk/reward guidance. It does not manage exits dynamically. Manual trade management is recommended.

This script is intended for active intraday traders, especially on lower timeframes like 3-minute, 5-minute or 15-minute charts.

---------------------------------------------------------------------------------------------------------------

🔧 Recommended companion indicator:

For better confirmation and visual tracking of the RSI/VWMA cross logic, it is strongly recommended to also use the companion script:

🔹 Relative Strength Index (with MA based cross signals)

→ Shows RSI and its moving average visually, with triangle plots on every valid cross.

→ Matches exactly the RSI/VWMA behavior used in this entry signal script.

📌 Important:

After adding the RSI script to your chart, make sure to set:

RSI Length = 14

MA Type = VWMA

MA Length = 20

This ensures it visually matches the logic used by the entry signal script.

Both indicators are fully open source and meant to be used together — especially when trading manually.

ICT Opening Range Projections (tristanlee85)ICT Opening Range Projections

This indicator visualizes key price levels based on ICT's (Inner Circle Trader) "Opening Range" concept. This 30-minute time interval establishes price levels that the algorithm will refer to throughout the session. The indicator displays these levels, including standard deviation projections, internal subdivisions (quadrants), and the opening price.

🟪 What It Does

The Opening Range is a crucial 30-minute window where market algorithms establish significant price levels. ICT theory suggests this range forms the basis for daily price movement.

This script helps you:

Mark the high, low, and opening price of each session.

Divide the range into quadrants (premium, discount, and midpoint/Consequent Encroachment).

Project potential price targets beyond the range using configurable standard deviation multiples .

🟪 How to Use It

This tool aids in time-based technical analysis rooted in ICT's Opening Range model, helping you observe price interaction with algorithmic levels.

Example uses include:

Identifying early structural boundaries.

Observing price behavior within premium/discount zones.

Visualizing initial displacement from the range to anticipate future moves.

Comparing price reactions at projected standard deviation levels.

Aligning price action with significant times like London or NY Open.

Note: This indicator provides a visual framework; it does not offer trade signals or interpretations.

🟪 Key Information

Time Zone: New York time (ET) is required on your chart.

Sessions: Supports multiple sessions, including NY midnight, NY AM, NY PM, and three custom timeframes.

Time Interval: Supports multi-timeframe up to 15 minutes. Best used on a 1-minute chart for accuracy.

🟪 Session Options

The Opening Range interval is configurable for up to 6 sessions:

Pre-defined ICT Sessions:

NY Midnight: 12:00 AM – 12:30 AM ET

NY AM: 9:30 AM – 10:00 AM ET

NY PM: 1:30 PM – 2:00 PM ET

Custom Sessions:

Three user-defined start/end time pairs.

This example shows a custom session from 03:30 - 04:00:

🟪 Understanding the Levels

The Opening Price is the open of the first 1-minute candle within the chosen session.

At session close, the Opening Range is calculated using its High and Low . An optional swing-based mode uses swing highs/lows for range boundaries.

The range is divided into quadrants by its midpoint ( Consequent Encroachment or CE):

Upper Quadrant: CE to high (premium).

Lower Quadrant: Low to CE (discount).

These subdivisions help visualize internal range dynamics, where price often reacts during algorithmic delivery.

🟪 Working with Ranges

By default, the range is determined by the highest high and lowest low of the 30-minute session:

A range can also be determined by the highest/lowest swing points:

Quadrants outline the premium and discount of a range that price will reference:

Small ranges still follow the same algorithmic logic, but may be deemed insignificant for one's trading. These can be filtered in the settings by specifying a minimum ticks limit. In this example, the range is 42 ticks (10.5 points) but the indicator is configured for 80 ticks (20 points). We can select which levels will plot if the range is below the limit. Here, only the 00:00 opening price is plotted:

You may opt to include the range high/low, quadrants, and projections as well. This will plot a red (configurable) range bracket to indicate it is below the limit while plotting the levels:

🟪 Price Projections

Projections extend beyond the Opening Range using standard deviations, framing the market beyond the initial session and identifying potential targets. You define the standard deviation multiples (e.g., 1.0, 1.5, 2.0).

Both positive and negative extensions are displayed, symmetrically projected from the range's high and low.

The Dynamic Levels option plots only the next projection level once price crosses the previous extreme. For example, only the 0.5 STDEV level plots until price reaches it, then the 1.0 level appears, and so on. This continues up to your defined maximum projections, or indefinitely if standard deviations are set to 0.

This example shows dynamic levels for a total of 6 sessions, only 1 of which meet a configured minimum limit of 50 ticks:

Small ranges followed by significant displacement are impacted the most with the number of levels plotted. You may hide projections when configuring the minimum ticks.

A fixed standard deviation will plot levels in both directions, regardless of the price range. Here, we plot up to 3.0 which hiding projections for small ranges:

🟪 Legal Disclaimer

This indicator is provided for informational and educational purposes only. It is not financial advice, and should not be construed as a recommendation to buy or sell any financial instrument. Trading involves substantial risk, and you could lose a significant amount of money. Past performance is not indicative of future results. Always consult with a qualified financial professional before making any trading or investment decisions. The creators and distributors of this indicator assume no responsibility for your trading outcomes.

ICT TIME ELEMENTS [KaninFX]## Overview

The ICT Time Elements indicator is a comprehensive trading tool designed to visualize the most critical market sessions and timeframes according to Inner Circle Trader (ICT) methodology. This indicator helps traders identify high-probability trading opportunities by highlighting key market sessions, killzones, and liquidity periods throughout the trading day.

## Key Features

### 🕐 Complete ICT Time Framework

- **Asian Range**: 8:00 PM - 12:00 AM (NY Time) - Evening consolidation period

- **London Killzone**: 2:00 AM - 5:00 AM (NY Time) - European market opening liquidity

- **NY Killzone**: 7:00 AM - 10:00 AM (NY Time) - US market opening with high volatility

- **Silver Bullet Sessions**:

- London Silver Bullet: 3:00 AM - 4:00 AM

- AM Silver Bullet: 10:00 AM - 11:00 AM

- PM Silver Bullet: 2:00 PM - 3:00 PM

- **Lunch Hours**: 5:00 AM - 7:00 AM & 12:00 PM - 1:00 PM (Lower volatility periods)

- **News Embargo**: 8:30 AM - 9:30 AM (High impact news release window)

- **20-Minute Macros**: :50 to :10 minutes of each hour (Short-term reversal periods)

- **True Day Close**: 4:00 PM - 4:30 PM (Official market close)

### 🎨 Visual Customization

- **Multiple Themes**: Dark, Light, and Custom color schemes

- **Adjustable Opacity**: Control zone transparency (0-100%)

- **Font Customization**: Tiny, Small, Normal, Large text sizes

- **Custom Colors**: Personalize each zone with your preferred colors

- **Professional Display**: Clean histogram visualization with zone labels

### 🌍 Multi-Timezone Support

Built-in support for major trading centers:

- America/New_York (Default)

- America/Chicago

- America/Los_Angeles

- Europe/London

- Asia/Tokyo

- Asia/Shanghai

- Australia/Sydney

### 📊 Smart Information Display

- **Real-time Zone Detection**: Automatically identifies current active session

- **Zone Labels**: Clear labeling at the center of each time period

- **Current Zone Indicator**: Arrow pointer showing the active session

- **Comprehensive Info Table**: Quick reference for all time zones and their schedules

- **Flexible Table Positioning**: Place info table in any corner of your chart

### ⚡ Performance Optimized

- **Memory Management**: Automatic cleanup of old labels to maintain performance

- **Efficient Processing**: Optimized time calculations for smooth operation

- **Resource Control**: Limited label generation to prevent system overload

## How It Works

The indicator continuously monitors the current time against predefined ICT session schedules. When price action enters a recognized time zone, the indicator:

1. **Highlights the Period**: Colors the histogram bar according to the active session

2. **Labels the Zone**: Places descriptive text identifying the current market condition

3. **Updates Info Table**: Shows current session status and complete schedule

4. **Tracks Macro Periods**: Identifies 20-minute reversal windows within major sessions

### Special Features

- **Macro Detection**: Automatically identifies when current time falls within a 20-minute macro period

- **Session Overlap Handling**: Properly manages overlapping time zones with priority logic

- **Dynamic Color Adjustment**: Theme-aware color selection for optimal visibility

## Best Use Cases

### For ICT Traders

- Identify optimal entry times during killzone sessions

- Recognize silver bullet opportunities for quick scalps

- Avoid trading during lunch hour consolidations

- Prepare for news embargo volatility

### For Session Traders

- Track major market session transitions

- Plan trading strategy around high-liquidity periods

- Understand global market flow and timing

### For Swing Traders

- Identify macro trend continuation points

- Time position entries during optimal sessions

- Understand market structure changes across sessions

## Installation & Setup

1. Add the indicator to your TradingView chart

2. Select your preferred timezone from the dropdown

3. Choose theme (Dark/Light) or customize colors

4. Adjust font size and table position to your preference

5. Enable/disable features as needed for your trading style

## Pro Tips

- **Combine with Price Action**: Use time zones alongside support/resistance levels

- **Focus on Killzones**: Highest probability setups occur during London and NY killzones

- **Watch Silver Bullets**: These 1-hour windows often provide excellent reversal opportunities

- **Respect Lunch Hours**: Lower volatility periods - consider smaller position sizes

- **News Embargo Awareness**: Prepare for potential whipsaws during 8:30-9:30 AM

## Conclusion

The ICT Time Elements indicator transforms complex ICT timing concepts into an easy-to-read visual tool. Whether you're a beginner learning ICT methodology or an experienced trader looking to optimize your timing, this indicator provides the essential market session awareness needed for successful trading.

*Compatible with all TradingView plans and timeframes. Works best on 1-minute to 1-hour charts for optimal session visualization.*

cd_respect2_EQ_Cx🔹 Overview: