50, 100, 200 SMAsA simple script that displays the 50, 100, and 200-period simple moving averages. Reduce clutter by combining them into one indicator!

"100万新币等于多少人民币" için komut dosyalarını ara

50,100,200 MA by CryptoLife71(FIXED)Updated the code by CryptoLife71 so that the 200ma shows correctly.

EMA 20/50/100/200Plots exponential moving average on four timeframes at once for rapid indication of momentum shift as well as slower-moving confirmations.

Displays EMA 20, 50, 100, and 200... default colors are hotter for faster timeframes, cooler for slower ones

DECL: 3 X Moving Average (50, 100 and 200 day)Basic Moving Average with 3 different intervals. Default: 50 day (blue), 100 day (red) and 200 day (purple)

BB 100 with Barcolors6/19/15 I added confirmation highlight bars to the code. In other words, if a candle bounced off the lower Bollinger band, it needed one more close above the previous candle to confirm a higher probability that a change in investor sentiment has reversed. Same is true for upper Bollinger band bounces. I also added confirmation highlight bars to the 100 sma (the basis). The idea is that lower and upper bands are potential points of support and resistance. The same is true of the basis if a trend is to continue. 6/28/15 I added a plotshape to identify closes above/below TLine. One thing this system points out is it operates best in a trend reversal. Consolidations will whipsaw the indicator too much. I have found that when this happens, if using daily candles, switch to hourly, 30 min, etc., to catch a better signal. Nothing moves in a straight line. As with any indicator, it is a tool to be used in conjunction with the art AND science of trading. As always, try the indicator for a time so that you are comfortable enough to use real money. This is designed to be used with "BB 25 with Barcolors".

BB 100 with Barcolors6/19/15 I added confirmation highlight bars to the code. In other words, if a candle bounced off the lower Bollinger band, it needed one more close above the previous candle to confirm a higher probability that a change in investor sentiment has reversed. Same is true for upper Bollinger band bounces. I also added confirmation highlight bars to the 100 sma (the basis). The idea is that lower and upper bands are potential points of support and resistance. The same is true of the basis if a trend is to continue. Nothing moves in a straight line. As with any indicator, it is a tool to be used in conjunction with the art AND science of trading. As always, try the indicator for a time so that you are comfortable enough to use real money. This is designed to be used with "BB 25 with Barcolors".

BB 100 with BarcolorsI cleaned up the highlight barcolor to reflect red or lime depending if it closed > or < the open.

The description is in the code. you want to catch bounces off the 25 (upper or lower) and 100 (upper or lower).

Works well on the hourly and 30 min charts. Haven't tested it beyond that. Haven't tested Forex, just equities.

EMA Keltner Channel 1D100/200 EMAs, along with Keltner Bands based off them. Colors correspond to actions you should be ready to take in the area. Use to set macro mindset.

Uses the security function to display only the 1D values.

Red= Bad

Orange = Not as Bad, but still Bad.

Yellow = Warning, might also be Bad.

Purple = Dip a toe in.

Blue = Give it a shot but have a little caution.

Green = It's second mortgage time.

ULTRA PRO SCALPING V6//@version=6

indicator("ULTRA PRO SCALPING V6", overlay=true, max_lines_count=500, max_labels_count=500)

// SETTINGS

lengthEMA = input.int(21, "EMA Trend")

riskRR = input.float(1.5, "Ratio TP/SL", step=0.1)

sl_pips = input.float(0.15, "Stop Loss (%)", step=0.01)

showTP_SL = input.bool(true, "Afficher TP & SL")

showSignals = input.bool(true, "Afficher Signaux")

// TREND FILTER

ema = ta.ema(close, lengthEMA)

plot(ema, "EMA", color=color.new(color.yellow, 0), linewidth=2)

// ENTRY SIGNALS

longSignal = ta.crossover(close, ema)

shortSignal = ta.crossunder(close, ema)

// TP/SL SYSTEM

var float lastSL = na

var float lastTP = na

if longSignal

lastSL := close * (1 - sl_pips/100)

lastTP := close + (close - lastSL) * riskRR

if shortSignal

lastSL := close * (1 + sl_pips/100)

lastTP := close - (lastSL - close) * riskRR

// DISPLAY

if showTP_SL and not na(lastSL)

line.new(bar_index-1, lastSL, bar_index, lastSL, color=color.red)

label.new(bar_index, lastSL, "SL", color=color.red)

if showTP_SL and not na(lastTP)

line.new(bar_index-1, lastTP, bar_index, lastTP, color=color.green)

label.new(bar_index, lastTP, "TP", color=color.green)

if showSignals and longSignal

label.new(bar_index, low, "BUY", color=color.green, style=label.style_label_up)

if showSignals and shortSignal

label.new(bar_index, high, "SELL", color=color.red, style=label.style_label_down)

// ALERTS

alertcondition(longSignal, "BUY Signal", "Signal d’achat détecté")

alertcondition(shortSignal, "SELL Signal", "Signal de vente détecté")

ES-VIX Daily Price Bands - Inner bands (80% and 50%)ES-VIX Daily Price Bands

This indicator plots dynamic intraday price bands for ES futures based on real-time volatility levels measured by the VIX (CBOE Volatility Index). The bands evolve throughout the trading day, providing volatility-adjusted price targets.

Formulas:

Upper Band = Daily Low + (ES Price × VIX ÷ √252 ÷ 100)

Lower Band = Daily High - (ES Price × VIX ÷ √252 ÷ 100)

The calculation uses the square root of 252 (trading days per year) to convert annualized VIX volatility into an expected daily move, then scales it as a percentage adjustment from the current day's extremes.

Features:

Real-time band calculation that updates throughout the trading session

Upper band (green) extends from the current day's low

Lower band (red) contracts from the current day's high

Inner upper band (green) at 50% of expected move

Inner lower band (red) at 50% of expected move

Middle Inner upper band (green) at 80% of expected move

Middle Inner lower band (red) at 80% of expected move

Shaded zone between bands for visual clarity

Information table displaying:

Current ES price and VIX level

Running daily high and low

Current upper and lower band values

ES-VIX Daily Price Bands - Inner bandsES-VIX Daily Price Bands

This indicator plots dynamic intraday price bands for ES futures based on real-time volatility levels measured by the VIX (CBOE Volatility Index). The bands evolve throughout the trading day, providing volatility-adjusted price targets.

Formulas:

Upper Band = Daily Low + (ES Price × VIX ÷ √252 ÷ 100)

Lower Band = Daily High - (ES Price × VIX ÷ √252 ÷ 100)

The calculation uses the square root of 252 (trading days per year) to convert annualized VIX volatility into an expected daily move, then scales it as a percentage adjustment from the current day's extremes.

Features:

Real-time band calculation that updates throughout the trading session

Upper band (green) extends from the current day's low

Lower band (red) contracts from the current day's high

Inner upper band (green) at 50% of expected move

Inner lower band (red) at 50% of expected move

Shaded zone between bands for visual clarity

Information table displaying:

Current ES price and VIX level

Running daily high and low

Current upper and lower band values

ES-VIX Daily Price BandsES-VIX Daily Price Bands

This indicator plots dynamic intraday price bands for ES futures based on real-time volatility levels measured by the VIX (CBOE Volatility Index). The bands evolve throughout the trading day, providing volatility-adjusted price targets.

Formulas:

Upper Band = Daily Low + (ES Price × VIX ÷ √252 ÷ 100)

Lower Band = Daily High - (ES Price × VIX ÷ √252 ÷ 100)

The calculation uses the square root of 252 (trading days per year) to convert annualized VIX volatility into an expected daily move, then scales it as a percentage adjustment from the current day's extremes.

Features:

Real-time band calculation that updates throughout the trading session

Upper band (green) extends from the current day's low

Lower band (red) contracts from the current day's high

Shaded zone between bands for visual clarity

Information table displaying:

Current ES price and VIX level

Running daily high and low

Current upper and lower band values

Dynamic Equity Allocation Model//@version=6

indicator('Dynamic Equity Allocation Model', shorttitle = 'DEAM', overlay = false, precision = 1, scale = scale.right, max_bars_back = 500)

// DYNAMIC EQUITY ALLOCATION MODEL

// Quantitative framework for dynamic portfolio allocation between stocks and cash.

// Analyzes five dimensions: market regime, risk metrics, valuation, sentiment,

// and macro conditions to generate allocation recommendations (0-100% equity).

//

// Uses real-time data from TradingView including fundamentals (P/E, ROE, ERP),

// volatility indicators (VIX), credit spreads, yield curves, and market structure.

// INPUT PARAMETERS

group1 = 'Model Configuration'

model_type = input.string('Adaptive', 'Allocation Model Type', options = , group = group1, tooltip = 'Conservative: Slower to increase equity, Aggressive: Faster allocation changes, Adaptive: Dynamic based on regime')

use_crisis_detection = input.bool(true, 'Enable Crisis Detection System', group = group1, tooltip = 'Automatic detection and response to crisis conditions')

use_regime_model = input.bool(true, 'Use Market Regime Detection', group = group1, tooltip = 'Identify Bull/Bear/Crisis regimes for dynamic allocation')

group2 = 'Portfolio Risk Management'

target_portfolio_volatility = input.float(12.0, 'Target Portfolio Volatility (%)', minval = 3, maxval = 20, step = 0.5, group = group2, tooltip = 'Target portfolio volatility (Cash reduces volatility: 50% Equity = ~10% vol, 100% Equity = ~20% vol)')

max_portfolio_drawdown = input.float(15.0, 'Maximum Portfolio Drawdown (%)', minval = 5, maxval = 35, step = 2.5, group = group2, tooltip = 'Maximum acceptable PORTFOLIO drawdown (not market drawdown - portfolio with cash has lower drawdown)')

enable_portfolio_risk_scaling = input.bool(true, 'Enable Portfolio Risk Scaling', group = group2, tooltip = 'Scale allocation based on actual portfolio risk characteristics (recommended)')

risk_lookback = input.int(252, 'Risk Calculation Period (Days)', minval = 60, maxval = 504, group = group2, tooltip = 'Period for calculating volatility and risk metrics')

group3 = 'Component Weights (Total = 100%)'

w_regime = input.float(35.0, 'Market Regime Weight (%)', minval = 0, maxval = 100, step = 5, group = group3)

w_risk = input.float(25.0, 'Risk Metrics Weight (%)', minval = 0, maxval = 100, step = 5, group = group3)

w_valuation = input.float(20.0, 'Valuation Weight (%)', minval = 0, maxval = 100, step = 5, group = group3)

w_sentiment = input.float(15.0, 'Sentiment Weight (%)', minval = 0, maxval = 100, step = 5, group = group3)

w_macro = input.float(5.0, 'Macro Weight (%)', minval = 0, maxval = 100, step = 5, group = group3)

group4 = 'Crisis Detection Thresholds'

crisis_vix_threshold = input.float(40, 'Crisis VIX Level', minval = 30, maxval = 80, group = group4, tooltip = 'VIX level indicating crisis conditions (COVID peaked at 82)')

crisis_drawdown_threshold = input.float(15, 'Crisis Drawdown Threshold (%)', minval = 10, maxval = 30, group = group4, tooltip = 'Market drawdown indicating crisis conditions')

crisis_credit_spread = input.float(500, 'Crisis Credit Spread (bps)', minval = 300, maxval = 1000, group = group4, tooltip = 'High yield spread indicating crisis conditions')

group5 = 'Display Settings'

show_components = input.bool(false, 'Show Component Breakdown', group = group5, tooltip = 'Display individual component analysis lines')

show_regime_background = input.bool(true, 'Show Dynamic Background', group = group5, tooltip = 'Color background based on allocation signals')

show_reference_lines = input.bool(false, 'Show Reference Lines', group = group5, tooltip = 'Display allocation percentage reference lines')

show_dashboard = input.bool(true, 'Show Analytics Dashboard', group = group5, tooltip = 'Display comprehensive analytics table')

show_confidence_bands = input.bool(false, 'Show Confidence Bands', group = group5, tooltip = 'Display uncertainty quantification bands')

smoothing_period = input.int(3, 'Smoothing Period', minval = 1, maxval = 10, group = group5, tooltip = 'Smoothing to reduce allocation noise')

background_intensity = input.int(95, 'Background Intensity (%)', minval = 90, maxval = 99, group = group5, tooltip = 'Higher values = more transparent background')

// Styling Options

color_scheme = input.string('EdgeTools', 'Color Theme', options = , group = 'Appearance', tooltip = 'Professional color themes')

use_dark_mode = input.bool(true, 'Optimize for Dark Theme', group = 'Appearance')

main_line_width = input.int(3, 'Main Line Width', minval = 1, maxval = 5, group = 'Appearance')

// DATA RETRIEVAL

// Market Data

sp500 = request.security('SPY', timeframe.period, close)

sp500_high = request.security('SPY', timeframe.period, high)

sp500_low = request.security('SPY', timeframe.period, low)

sp500_volume = request.security('SPY', timeframe.period, volume)

// Volatility Indicators

vix = request.security('VIX', timeframe.period, close)

vix9d = request.security('VIX9D', timeframe.period, close)

vxn = request.security('VXN', timeframe.period, close)

// Fixed Income and Credit

us2y = request.security('US02Y', timeframe.period, close)

us10y = request.security('US10Y', timeframe.period, close)

us3m = request.security('US03MY', timeframe.period, close)

hyg = request.security('HYG', timeframe.period, close)

lqd = request.security('LQD', timeframe.period, close)

tlt = request.security('TLT', timeframe.period, close)

// Safe Haven Assets

gold = request.security('GLD', timeframe.period, close)

usd = request.security('DXY', timeframe.period, close)

yen = request.security('JPYUSD', timeframe.period, close)

// Financial data with fallback values

get_financial_data(symbol, fin_id, period, fallback) =>

data = request.financial(symbol, fin_id, period, ignore_invalid_symbol = true)

na(data) ? fallback : data

// SPY fundamental metrics

spy_earnings_per_share = get_financial_data('AMEX:SPY', 'EARNINGS_PER_SHARE_BASIC', 'TTM', 20.0)

spy_operating_earnings_yield = get_financial_data('AMEX:SPY', 'OPERATING_EARNINGS_YIELD', 'FY', 4.5)

spy_dividend_yield = get_financial_data('AMEX:SPY', 'DIVIDENDS_YIELD', 'FY', 1.8)

spy_buyback_yield = get_financial_data('AMEX:SPY', 'BUYBACK_YIELD', 'FY', 2.0)

spy_net_margin = get_financial_data('AMEX:SPY', 'NET_MARGIN', 'TTM', 12.0)

spy_debt_to_equity = get_financial_data('AMEX:SPY', 'DEBT_TO_EQUITY', 'FY', 0.5)

spy_return_on_equity = get_financial_data('AMEX:SPY', 'RETURN_ON_EQUITY', 'FY', 15.0)

spy_free_cash_flow = get_financial_data('AMEX:SPY', 'FREE_CASH_FLOW', 'TTM', 100000000)

spy_ebitda = get_financial_data('AMEX:SPY', 'EBITDA', 'TTM', 200000000)

spy_pe_forward = get_financial_data('AMEX:SPY', 'PRICE_EARNINGS_FORWARD', 'FY', 18.0)

spy_total_debt = get_financial_data('AMEX:SPY', 'TOTAL_DEBT', 'FY', 500000000)

spy_total_equity = get_financial_data('AMEX:SPY', 'TOTAL_EQUITY', 'FY', 1000000000)

spy_enterprise_value = get_financial_data('AMEX:SPY', 'ENTERPRISE_VALUE', 'FY', 30000000000)

spy_revenue_growth = get_financial_data('AMEX:SPY', 'REVENUE_ONE_YEAR_GROWTH', 'TTM', 5.0)

// Market Breadth Indicators

nya = request.security('NYA', timeframe.period, close)

rut = request.security('IWM', timeframe.period, close)

// Sector Performance

xlk = request.security('XLK', timeframe.period, close)

xlu = request.security('XLU', timeframe.period, close)

xlf = request.security('XLF', timeframe.period, close)

// MARKET REGIME DETECTION

// Calculate Market Trend

sma_20 = ta.sma(sp500, 20)

sma_50 = ta.sma(sp500, 50)

sma_200 = ta.sma(sp500, 200)

ema_10 = ta.ema(sp500, 10)

// Market Structure Score

trend_strength = 0.0

trend_strength := trend_strength + (sp500 > sma_20 ? 1 : -1)

trend_strength := trend_strength + (sp500 > sma_50 ? 1 : -1)

trend_strength := trend_strength + (sp500 > sma_200 ? 2 : -2)

trend_strength := trend_strength + (sma_50 > sma_200 ? 2 : -2)

// Volatility Regime

returns = math.log(sp500 / sp500 )

realized_vol_20d = ta.stdev(returns, 20) * math.sqrt(252) * 100

realized_vol_60d = ta.stdev(returns, 60) * math.sqrt(252) * 100

ewma_vol = ta.ema(math.pow(returns, 2), 20)

realized_vol = math.sqrt(ewma_vol * 252) * 100

vol_premium = vix - realized_vol

// Drawdown Calculation

running_max = ta.highest(sp500, risk_lookback)

current_drawdown = (running_max - sp500) / running_max * 100

// Regime Score

regime_score = 0.0

// Trend Component (40%)

if trend_strength >= 4

regime_score := regime_score + 40

regime_score

else if trend_strength >= 2

regime_score := regime_score + 30

regime_score

else if trend_strength >= 0

regime_score := regime_score + 20

regime_score

else if trend_strength >= -2

regime_score := regime_score + 10

regime_score

else

regime_score := regime_score + 0

regime_score

// Volatility Component (30%)

if vix < 15

regime_score := regime_score + 30

regime_score

else if vix < 20

regime_score := regime_score + 25

regime_score

else if vix < 25

regime_score := regime_score + 15

regime_score

else if vix < 35

regime_score := regime_score + 5

regime_score

else

regime_score := regime_score + 0

regime_score

// Drawdown Component (30%)

if current_drawdown < 3

regime_score := regime_score + 30

regime_score

else if current_drawdown < 7

regime_score := regime_score + 20

regime_score

else if current_drawdown < 12

regime_score := regime_score + 10

regime_score

else if current_drawdown < 20

regime_score := regime_score + 5

regime_score

else

regime_score := regime_score + 0

regime_score

// Classify Regime

market_regime = regime_score >= 80 ? 'Strong Bull' : regime_score >= 60 ? 'Bull Market' : regime_score >= 40 ? 'Neutral' : regime_score >= 20 ? 'Correction' : regime_score >= 10 ? 'Bear Market' : 'Crisis'

// RISK-BASED ALLOCATION

// Calculate Market Risk

parkinson_hl = math.log(sp500_high / sp500_low)

parkinson_vol = parkinson_hl / (2 * math.sqrt(math.log(2))) * math.sqrt(252) * 100

garman_klass_vol = math.sqrt((0.5 * math.pow(math.log(sp500_high / sp500_low), 2) - (2 * math.log(2) - 1) * math.pow(math.log(sp500 / sp500 ), 2)) * 252) * 100

market_volatility_20d = math.max(ta.stdev(returns, 20) * math.sqrt(252) * 100, parkinson_vol)

market_volatility_60d = ta.stdev(returns, 60) * math.sqrt(252) * 100

market_drawdown = current_drawdown

// Initialize risk allocation

risk_allocation = 50.0

if enable_portfolio_risk_scaling

// Volatility-based allocation

vol_based_allocation = target_portfolio_volatility / math.max(market_volatility_20d, 5.0) * 100

vol_based_allocation := math.max(0, math.min(100, vol_based_allocation))

// Drawdown-based allocation

dd_based_allocation = 100.0

if market_drawdown > 1.0

dd_based_allocation := max_portfolio_drawdown / market_drawdown * 100

dd_based_allocation := math.max(0, math.min(100, dd_based_allocation))

dd_based_allocation

// Combine (conservative)

risk_allocation := math.min(vol_based_allocation, dd_based_allocation)

// Dynamic adjustment

current_equity_estimate = 50.0

estimated_portfolio_vol = current_equity_estimate / 100 * market_volatility_20d

estimated_portfolio_dd = current_equity_estimate / 100 * market_drawdown

vol_utilization = estimated_portfolio_vol / target_portfolio_volatility

dd_utilization = estimated_portfolio_dd / max_portfolio_drawdown

risk_utilization = math.max(vol_utilization, dd_utilization)

risk_adjustment_factor = 1.0

if risk_utilization > 1.0

risk_adjustment_factor := math.exp(-0.5 * (risk_utilization - 1.0))

risk_adjustment_factor := math.max(0.5, risk_adjustment_factor)

risk_adjustment_factor

else if risk_utilization < 0.9

risk_adjustment_factor := 1.0 + 0.2 * math.log(1.0 / risk_utilization)

risk_adjustment_factor := math.min(1.3, risk_adjustment_factor)

risk_adjustment_factor

risk_allocation := risk_allocation * risk_adjustment_factor

risk_allocation

else

vol_scalar = target_portfolio_volatility / math.max(market_volatility_20d, 10)

vol_scalar := math.min(1.5, math.max(0.2, vol_scalar))

drawdown_penalty = 0.0

if current_drawdown > max_portfolio_drawdown

drawdown_penalty := (current_drawdown - max_portfolio_drawdown) / max_portfolio_drawdown

drawdown_penalty := math.min(1.0, drawdown_penalty)

drawdown_penalty

risk_allocation := 100 * vol_scalar * (1 - drawdown_penalty)

risk_allocation

risk_allocation := math.max(0, math.min(100, risk_allocation))

// VALUATION ANALYSIS

// Valuation Metrics

actual_pe_ratio = spy_earnings_per_share > 0 ? sp500 / spy_earnings_per_share : spy_pe_forward

actual_earnings_yield = nz(spy_operating_earnings_yield, 0) > 0 ? spy_operating_earnings_yield : 100 / actual_pe_ratio

total_shareholder_yield = spy_dividend_yield + spy_buyback_yield

// Equity Risk Premium (multi-method calculation)

method1_erp = actual_earnings_yield - us10y

method2_erp = actual_earnings_yield + spy_buyback_yield - us10y

payout_ratio = spy_dividend_yield > 0 and actual_earnings_yield > 0 ? spy_dividend_yield / actual_earnings_yield : 0.4

sustainable_growth = spy_return_on_equity * (1 - payout_ratio) / 100

method3_erp = spy_dividend_yield + sustainable_growth * 100 - us10y

implied_growth = spy_revenue_growth * 0.7

method4_erp = total_shareholder_yield + implied_growth - us10y

equity_risk_premium = method1_erp * 0.35 + method2_erp * 0.30 + method3_erp * 0.20 + method4_erp * 0.15

ev_ebitda_ratio = spy_enterprise_value > 0 and spy_ebitda > 0 ? spy_enterprise_value / spy_ebitda : 15.0

debt_equity_health = spy_debt_to_equity < 1.0 ? 1.2 : spy_debt_to_equity < 2.0 ? 1.0 : 0.8

// Valuation Score

base_valuation_score = 50.0

if equity_risk_premium > 4

base_valuation_score := 95

base_valuation_score

else if equity_risk_premium > 3

base_valuation_score := 85

base_valuation_score

else if equity_risk_premium > 2

base_valuation_score := 70

base_valuation_score

else if equity_risk_premium > 1

base_valuation_score := 55

base_valuation_score

else if equity_risk_premium > 0

base_valuation_score := 40

base_valuation_score

else if equity_risk_premium > -1

base_valuation_score := 25

base_valuation_score

else

base_valuation_score := 10

base_valuation_score

growth_adjustment = spy_revenue_growth > 10 ? 10 : spy_revenue_growth > 5 ? 5 : 0

margin_adjustment = spy_net_margin > 15 ? 5 : spy_net_margin < 8 ? -5 : 0

roe_adjustment = spy_return_on_equity > 20 ? 5 : spy_return_on_equity < 10 ? -5 : 0

valuation_score = base_valuation_score + growth_adjustment + margin_adjustment + roe_adjustment

valuation_score := math.max(0, math.min(100, valuation_score * debt_equity_health))

// SENTIMENT ANALYSIS

// VIX Term Structure

vix_term_structure = vix9d > 0 ? vix / vix9d : 1

backwardation = vix_term_structure > 1.05

steep_backwardation = vix_term_structure > 1.15

// Safe Haven Flows

gold_momentum = ta.roc(gold, 20)

dollar_momentum = ta.roc(usd, 20)

yen_momentum = ta.roc(yen, 20)

treasury_momentum = ta.roc(tlt, 20)

safe_haven_flow = gold_momentum * 0.3 + treasury_momentum * 0.3 + dollar_momentum * 0.25 + yen_momentum * 0.15

// Advanced Sentiment Analysis

vix_percentile = ta.percentrank(vix, 252)

vix_zscore = (vix - ta.sma(vix, 252)) / ta.stdev(vix, 252)

vix_momentum = ta.roc(vix, 5)

vvix_proxy = ta.stdev(vix_momentum, 20) * math.sqrt(252)

risk_reversal_proxy = (vix - realized_vol) / realized_vol

// Sentiment Score

base_sentiment = 50.0

vix_adjustment = 0.0

if vix_zscore < -1.5

vix_adjustment := 40

vix_adjustment

else if vix_zscore < -0.5

vix_adjustment := 20

vix_adjustment

else if vix_zscore < 0.5

vix_adjustment := 0

vix_adjustment

else if vix_zscore < 1.5

vix_adjustment := -20

vix_adjustment

else

vix_adjustment := -40

vix_adjustment

term_structure_adjustment = backwardation ? -15 : steep_backwardation ? -30 : 5

vvix_adjustment = vvix_proxy > 2.0 ? -10 : vvix_proxy < 1.0 ? 10 : 0

sentiment_score = base_sentiment + vix_adjustment + term_structure_adjustment + vvix_adjustment

sentiment_score := math.max(0, math.min(100, sentiment_score))

// MACRO ANALYSIS

// Yield Curve

yield_spread_2_10 = us10y - us2y

yield_spread_3m_10 = us10y - us3m

// Credit Conditions

hyg_return = ta.roc(hyg, 20)

lqd_return = ta.roc(lqd, 20)

tlt_return = ta.roc(tlt, 20)

hyg_duration = 4.0

lqd_duration = 8.0

tlt_duration = 17.0

hyg_log_returns = math.log(hyg / hyg )

lqd_log_returns = math.log(lqd / lqd )

hyg_volatility = ta.stdev(hyg_log_returns, 20) * math.sqrt(252)

lqd_volatility = ta.stdev(lqd_log_returns, 20) * math.sqrt(252)

hyg_yield_proxy = -math.log(hyg / hyg ) * 100

lqd_yield_proxy = -math.log(lqd / lqd ) * 100

tlt_yield = us10y

hyg_spread = (hyg_yield_proxy - tlt_yield) * 100

lqd_spread = (lqd_yield_proxy - tlt_yield) * 100

hyg_distance = (hyg - ta.lowest(hyg, 252)) / (ta.highest(hyg, 252) - ta.lowest(hyg, 252))

lqd_distance = (lqd - ta.lowest(lqd, 252)) / (ta.highest(lqd, 252) - ta.lowest(lqd, 252))

default_risk_proxy = 2.0 - (hyg_distance + lqd_distance)

credit_spread = hyg_spread * 0.5 + (hyg_volatility - lqd_volatility) * 1000 * 0.3 + default_risk_proxy * 200 * 0.2

credit_spread := math.max(50, credit_spread)

credit_market_health = hyg_return > lqd_return ? 1 : -1

flight_to_quality = tlt_return > (hyg_return + lqd_return) / 2

// Macro Score

macro_score = 50.0

yield_curve_score = 0

if yield_spread_2_10 > 1.5 and yield_spread_3m_10 > 2

yield_curve_score := 40

yield_curve_score

else if yield_spread_2_10 > 0.5 and yield_spread_3m_10 > 1

yield_curve_score := 30

yield_curve_score

else if yield_spread_2_10 > 0 and yield_spread_3m_10 > 0

yield_curve_score := 20

yield_curve_score

else if yield_spread_2_10 < 0 or yield_spread_3m_10 < 0

yield_curve_score := 10

yield_curve_score

else

yield_curve_score := 5

yield_curve_score

credit_conditions_score = 0

if credit_spread < 200 and not flight_to_quality

credit_conditions_score := 30

credit_conditions_score

else if credit_spread < 400 and credit_market_health > 0

credit_conditions_score := 20

credit_conditions_score

else if credit_spread < 600

credit_conditions_score := 15

credit_conditions_score

else if credit_spread < 1000

credit_conditions_score := 10

credit_conditions_score

else

credit_conditions_score := 0

credit_conditions_score

financial_stability_score = 0

if spy_debt_to_equity < 0.5 and spy_return_on_equity > 15

financial_stability_score := 20

financial_stability_score

else if spy_debt_to_equity < 1.0 and spy_return_on_equity > 10

financial_stability_score := 15

financial_stability_score

else if spy_debt_to_equity < 1.5

financial_stability_score := 10

financial_stability_score

else

financial_stability_score := 5

financial_stability_score

macro_score := yield_curve_score + credit_conditions_score + financial_stability_score

macro_score := math.max(0, math.min(100, macro_score))

// CRISIS DETECTION

crisis_indicators = 0

if vix > crisis_vix_threshold

crisis_indicators := crisis_indicators + 1

crisis_indicators

if vix > 60

crisis_indicators := crisis_indicators + 2

crisis_indicators

if current_drawdown > crisis_drawdown_threshold

crisis_indicators := crisis_indicators + 1

crisis_indicators

if current_drawdown > 25

crisis_indicators := crisis_indicators + 1

crisis_indicators

if credit_spread > crisis_credit_spread

crisis_indicators := crisis_indicators + 1

crisis_indicators

sp500_roc_5 = ta.roc(sp500, 5)

tlt_roc_5 = ta.roc(tlt, 5)

if sp500_roc_5 < -10 and tlt_roc_5 < -5

crisis_indicators := crisis_indicators + 2

crisis_indicators

volume_spike = sp500_volume > ta.sma(sp500_volume, 20) * 2

sp500_roc_1 = ta.roc(sp500, 1)

if volume_spike and sp500_roc_1 < -3

crisis_indicators := crisis_indicators + 1

crisis_indicators

is_crisis = crisis_indicators >= 3

is_severe_crisis = crisis_indicators >= 5

// FINAL ALLOCATION CALCULATION

// Convert regime to base allocation

regime_allocation = market_regime == 'Strong Bull' ? 100 : market_regime == 'Bull Market' ? 80 : market_regime == 'Neutral' ? 60 : market_regime == 'Correction' ? 40 : market_regime == 'Bear Market' ? 20 : 0

// Normalize weights

total_weight = w_regime + w_risk + w_valuation + w_sentiment + w_macro

w_regime_norm = w_regime / total_weight

w_risk_norm = w_risk / total_weight

w_valuation_norm = w_valuation / total_weight

w_sentiment_norm = w_sentiment / total_weight

w_macro_norm = w_macro / total_weight

// Calculate Weighted Allocation

weighted_allocation = regime_allocation * w_regime_norm + risk_allocation * w_risk_norm + valuation_score * w_valuation_norm + sentiment_score * w_sentiment_norm + macro_score * w_macro_norm

// Apply Crisis Override

if use_crisis_detection

if is_severe_crisis

weighted_allocation := math.min(weighted_allocation, 10)

weighted_allocation

else if is_crisis

weighted_allocation := math.min(weighted_allocation, 25)

weighted_allocation

// Model Type Adjustment

model_adjustment = 0.0

if model_type == 'Conservative'

model_adjustment := -10

model_adjustment

else if model_type == 'Aggressive'

model_adjustment := 10

model_adjustment

else if model_type == 'Adaptive'

recent_return = (sp500 - sp500 ) / sp500 * 100

if recent_return > 5

model_adjustment := 5

model_adjustment

else if recent_return < -5

model_adjustment := -5

model_adjustment

// Apply adjustment and bounds

final_allocation = weighted_allocation + model_adjustment

final_allocation := math.max(0, math.min(100, final_allocation))

// Smooth allocation

smoothed_allocation = ta.sma(final_allocation, smoothing_period)

// Calculate portfolio risk metrics (only for internal alerts)

actual_portfolio_volatility = smoothed_allocation / 100 * market_volatility_20d

actual_portfolio_drawdown = smoothed_allocation / 100 * current_drawdown

// VISUALIZATION

// Color definitions

var color primary_color = #2196F3

var color bullish_color = #4CAF50

var color bearish_color = #FF5252

var color neutral_color = #808080

var color text_color = color.white

var color bg_color = #000000

var color table_bg_color = #1E1E1E

var color header_bg_color = #2D2D2D

switch color_scheme // Apply color scheme

'Gold' =>

primary_color := use_dark_mode ? #FFD700 : #DAA520

bullish_color := use_dark_mode ? #FFA500 : #FF8C00

bearish_color := use_dark_mode ? #FF5252 : #D32F2F

neutral_color := use_dark_mode ? #C0C0C0 : #808080

text_color := use_dark_mode ? color.white : color.black

bg_color := use_dark_mode ? #000000 : #FFFFFF

table_bg_color := use_dark_mode ? #1A1A00 : #FFFEF0

header_bg_color := use_dark_mode ? #2D2600 : #F5F5DC

header_bg_color

'EdgeTools' =>

primary_color := use_dark_mode ? #4682B4 : #1E90FF

bullish_color := use_dark_mode ? #4CAF50 : #388E3C

bearish_color := use_dark_mode ? #FF5252 : #D32F2F

neutral_color := use_dark_mode ? #708090 : #696969

text_color := use_dark_mode ? color.white : color.black

bg_color := use_dark_mode ? #000000 : #FFFFFF

table_bg_color := use_dark_mode ? #0F1419 : #F0F8FF

header_bg_color := use_dark_mode ? #1E2A3A : #E6F3FF

header_bg_color

'Behavioral' =>

primary_color := #808080

bullish_color := #00FF00

bearish_color := #8B0000

neutral_color := #FFBF00

text_color := use_dark_mode ? color.white : color.black

bg_color := use_dark_mode ? #000000 : #FFFFFF

table_bg_color := use_dark_mode ? #1A1A1A : #F8F8F8

header_bg_color := use_dark_mode ? #2D2D2D : #E8E8E8

header_bg_color

'Quant' =>

primary_color := #808080

bullish_color := #FFA500

bearish_color := #8B0000

neutral_color := #4682B4

text_color := use_dark_mode ? color.white : color.black

bg_color := use_dark_mode ? #000000 : #FFFFFF

table_bg_color := use_dark_mode ? #0D0D0D : #FAFAFA

header_bg_color := use_dark_mode ? #1A1A1A : #F0F0F0

header_bg_color

'Ocean' =>

primary_color := use_dark_mode ? #20B2AA : #008B8B

bullish_color := use_dark_mode ? #00CED1 : #4682B4

bearish_color := use_dark_mode ? #FF4500 : #B22222

neutral_color := use_dark_mode ? #87CEEB : #2F4F4F

text_color := use_dark_mode ? #F0F8FF : #191970

bg_color := use_dark_mode ? #001F3F : #F0F8FF

table_bg_color := use_dark_mode ? #001A2E : #E6F7FF

header_bg_color := use_dark_mode ? #002A47 : #CCF2FF

header_bg_color

'Fire' =>

primary_color := use_dark_mode ? #FF6347 : #DC143C

bullish_color := use_dark_mode ? #FFD700 : #FF8C00

bearish_color := use_dark_mode ? #8B0000 : #800000

neutral_color := use_dark_mode ? #FFA500 : #CD853F

text_color := use_dark_mode ? #FFFAF0 : #2F1B14

bg_color := use_dark_mode ? #2F1B14 : #FFFAF0

table_bg_color := use_dark_mode ? #261611 : #FFF8F0

header_bg_color := use_dark_mode ? #3D241A : #FFE4CC

header_bg_color

'Matrix' =>

primary_color := use_dark_mode ? #00FF41 : #006400

bullish_color := use_dark_mode ? #39FF14 : #228B22

bearish_color := use_dark_mode ? #FF073A : #8B0000

neutral_color := use_dark_mode ? #00FFFF : #008B8B

text_color := use_dark_mode ? #C0FF8C : #003300

bg_color := use_dark_mode ? #0D1B0D : #F0FFF0

table_bg_color := use_dark_mode ? #0A1A0A : #E8FFF0

header_bg_color := use_dark_mode ? #112B11 : #CCFFCC

header_bg_color

'Arctic' =>

primary_color := use_dark_mode ? #87CEFA : #4169E1

bullish_color := use_dark_mode ? #00BFFF : #0000CD

bearish_color := use_dark_mode ? #FF1493 : #8B008B

neutral_color := use_dark_mode ? #B0E0E6 : #483D8B

text_color := use_dark_mode ? #F8F8FF : #191970

bg_color := use_dark_mode ? #191970 : #F8F8FF

table_bg_color := use_dark_mode ? #141B47 : #F0F8FF

header_bg_color := use_dark_mode ? #1E2A5C : #E0F0FF

header_bg_color

// Transparency settings

bg_transparency = use_dark_mode ? 85 : 92

zone_transparency = use_dark_mode ? 90 : 95

band_transparency = use_dark_mode ? 70 : 85

table_transparency = use_dark_mode ? 80 : 15

// Allocation color

alloc_color = smoothed_allocation >= 80 ? bullish_color : smoothed_allocation >= 60 ? color.new(bullish_color, 30) : smoothed_allocation >= 40 ? primary_color : smoothed_allocation >= 20 ? color.new(bearish_color, 30) : bearish_color

// Dynamic background

var color dynamic_bg_color = na

if show_regime_background

if smoothed_allocation >= 70

dynamic_bg_color := color.new(bullish_color, background_intensity)

dynamic_bg_color

else if smoothed_allocation <= 30

dynamic_bg_color := color.new(bearish_color, background_intensity)

dynamic_bg_color

else if smoothed_allocation > 60 or smoothed_allocation < 40

dynamic_bg_color := color.new(primary_color, math.min(99, background_intensity + 2))

dynamic_bg_color

bgcolor(dynamic_bg_color, title = 'Allocation Signal Background')

// Plot main allocation line

plot(smoothed_allocation, 'Equity Allocation %', color = alloc_color, linewidth = math.max(1, main_line_width))

// Reference lines (static colors for hline)

hline_bullish_color = color_scheme == 'Gold' ? use_dark_mode ? #FFA500 : #FF8C00 : color_scheme == 'EdgeTools' ? use_dark_mode ? #4CAF50 : #388E3C : color_scheme == 'Behavioral' ? #00FF00 : color_scheme == 'Quant' ? #FFA500 : color_scheme == 'Ocean' ? use_dark_mode ? #00CED1 : #4682B4 : color_scheme == 'Fire' ? use_dark_mode ? #FFD700 : #FF8C00 : color_scheme == 'Matrix' ? use_dark_mode ? #39FF14 : #228B22 : color_scheme == 'Arctic' ? use_dark_mode ? #00BFFF : #0000CD : #4CAF50

hline_bearish_color = color_scheme == 'Gold' ? use_dark_mode ? #FF5252 : #D32F2F : color_scheme == 'EdgeTools' ? use_dark_mode ? #FF5252 : #D32F2F : color_scheme == 'Behavioral' ? #8B0000 : color_scheme == 'Quant' ? #8B0000 : color_scheme == 'Ocean' ? use_dark_mode ? #FF4500 : #B22222 : color_scheme == 'Fire' ? use_dark_mode ? #8B0000 : #800000 : color_scheme == 'Matrix' ? use_dark_mode ? #FF073A : #8B0000 : color_scheme == 'Arctic' ? use_dark_mode ? #FF1493 : #8B008B : #FF5252

hline_primary_color = color_scheme == 'Gold' ? use_dark_mode ? #FFD700 : #DAA520 : color_scheme == 'EdgeTools' ? use_dark_mode ? #4682B4 : #1E90FF : color_scheme == 'Behavioral' ? #808080 : color_scheme == 'Quant' ? #808080 : color_scheme == 'Ocean' ? use_dark_mode ? #20B2AA : #008B8B : color_scheme == 'Fire' ? use_dark_mode ? #FF6347 : #DC143C : color_scheme == 'Matrix' ? use_dark_mode ? #00FF41 : #006400 : color_scheme == 'Arctic' ? use_dark_mode ? #87CEFA : #4169E1 : #2196F3

hline(show_reference_lines ? 100 : na, '100% Equity', color = color.new(hline_bullish_color, 70), linestyle = hline.style_dotted, linewidth = 1)

hline(show_reference_lines ? 80 : na, '80% Equity', color = color.new(hline_bullish_color, 40), linestyle = hline.style_dashed, linewidth = 1)

hline(show_reference_lines ? 60 : na, '60% Equity', color = color.new(hline_bullish_color, 60), linestyle = hline.style_dotted, linewidth = 1)

hline(50, '50% Balanced', color = color.new(hline_primary_color, 50), linestyle = hline.style_solid, linewidth = 2)

hline(show_reference_lines ? 40 : na, '40% Equity', color = color.new(hline_bearish_color, 60), linestyle = hline.style_dotted, linewidth = 1)

hline(show_reference_lines ? 20 : na, '20% Equity', color = color.new(hline_bearish_color, 40), linestyle = hline.style_dashed, linewidth = 1)

hline(show_reference_lines ? 0 : na, '0% Equity', color = color.new(hline_bearish_color, 70), linestyle = hline.style_dotted, linewidth = 1)

// Component plots

plot(show_components ? regime_allocation : na, 'Regime', color = color.new(#4ECDC4, 70), linewidth = 1)

plot(show_components ? risk_allocation : na, 'Risk', color = color.new(#FF6B6B, 70), linewidth = 1)

plot(show_components ? valuation_score : na, 'Valuation', color = color.new(#45B7D1, 70), linewidth = 1)

plot(show_components ? sentiment_score : na, 'Sentiment', color = color.new(#FFD93D, 70), linewidth = 1)

plot(show_components ? macro_score : na, 'Macro', color = color.new(#6BCF7F, 70), linewidth = 1)

// Confidence bands

upper_band = plot(show_confidence_bands ? math.min(100, smoothed_allocation + ta.stdev(smoothed_allocation, 20)) : na, color = color.new(neutral_color, band_transparency), display = display.none, title = 'Upper Band')

lower_band = plot(show_confidence_bands ? math.max(0, smoothed_allocation - ta.stdev(smoothed_allocation, 20)) : na, color = color.new(neutral_color, band_transparency), display = display.none, title = 'Lower Band')

fill(upper_band, lower_band, color = show_confidence_bands ? color.new(neutral_color, zone_transparency) : na, title = 'Uncertainty')

// DASHBOARD

if show_dashboard and barstate.islast

var table dashboard = table.new(position.top_right, 2, 20, border_width = 1, bgcolor = color.new(table_bg_color, table_transparency))

table.clear(dashboard, 0, 0, 1, 19)

// Header

header_color = color.new(header_bg_color, 20)

dashboard_text_color = text_color

table.cell(dashboard, 0, 0, 'DEAM', text_color = dashboard_text_color, bgcolor = header_color, text_size = size.normal)

table.cell(dashboard, 1, 0, model_type, text_color = dashboard_text_color, bgcolor = header_color, text_size = size.normal)

// Core metrics

table.cell(dashboard, 0, 1, 'Equity Allocation', text_color = dashboard_text_color, text_size = size.small)

table.cell(dashboard, 1, 1, str.tostring(smoothed_allocation, '##.#') + '%', text_color = alloc_color, text_size = size.small)

table.cell(dashboard, 0, 2, 'Cash Allocation', text_color = dashboard_text_color, text_size = size.small)

cash_color = 100 - smoothed_allocation > 70 ? bearish_color : primary_color

table.cell(dashboard, 1, 2, str.tostring(100 - smoothed_allocation, '##.#') + '%', text_color = cash_color, text_size = size.small)

// Signal

signal_text = 'NEUTRAL'

signal_color = primary_color

if smoothed_allocation >= 70

signal_text := 'BULLISH'

signal_color := bullish_color

signal_color

else if smoothed_allocation <= 30

signal_text := 'BEARISH'

signal_color := bearish_color

signal_color

table.cell(dashboard, 0, 3, 'Signal', text_color = dashboard_text_color, text_size = size.small)

table.cell(dashboard, 1, 3, signal_text, text_color = signal_color, text_size = size.small)

// Market Regime

table.cell(dashboard, 0, 4, 'Regime', text_color = dashboard_text_color, text_size = size.small)

regime_color_display = market_regime == 'Strong Bull' or market_regime == 'Bull Market' ? bullish_color : market_regime == 'Neutral' ? primary_color : market_regime == 'Crisis' ? bearish_color : bearish_color

table.cell(dashboard, 1, 4, market_regime, text_color = regime_color_display, text_size = size.small)

// VIX

table.cell(dashboard, 0, 5, 'VIX Level', text_color = dashboard_text_color, text_size = size.small)

vix_color_display = vix < 20 ? bullish_color : vix < 30 ? primary_color : bearish_color

table.cell(dashboard, 1, 5, str.tostring(vix, '##.##'), text_color = vix_color_display, text_size = size.small)

// Market Drawdown

table.cell(dashboard, 0, 6, 'Market DD', text_color = dashboard_text_color, text_size = size.small)

market_dd_color = current_drawdown < 5 ? bullish_color : current_drawdown < 10 ? primary_color : bearish_color

table.cell(dashboard, 1, 6, '-' + str.tostring(current_drawdown, '##.#') + '%', text_color = market_dd_color, text_size = size.small)

// Crisis Detection

table.cell(dashboard, 0, 7, 'Crisis Detection', text_color = dashboard_text_color, text_size = size.small)

crisis_text = is_severe_crisis ? 'SEVERE' : is_crisis ? 'CRISIS' : 'Normal'

crisis_display_color = is_severe_crisis or is_crisis ? bearish_color : bullish_color

table.cell(dashboard, 1, 7, crisis_text, text_color = crisis_display_color, text_size = size.small)

// Real Data Section

financial_bg = color.new(primary_color, 85)

table.cell(dashboard, 0, 8, 'REAL DATA', text_color = dashboard_text_color, bgcolor = financial_bg, text_size = size.small)

table.cell(dashboard, 1, 8, 'Live Metrics', text_color = dashboard_text_color, bgcolor = financial_bg, text_size = size.small)

// P/E Ratio

table.cell(dashboard, 0, 9, 'P/E Ratio', text_color = dashboard_text_color, text_size = size.small)

pe_color = actual_pe_ratio < 18 ? bullish_color : actual_pe_ratio < 25 ? primary_color : bearish_color

table.cell(dashboard, 1, 9, str.tostring(actual_pe_ratio, '##.#'), text_color = pe_color, text_size = size.small)

// ERP

table.cell(dashboard, 0, 10, 'ERP', text_color = dashboard_text_color, text_size = size.small)

erp_color = equity_risk_premium > 2 ? bullish_color : equity_risk_premium > 0 ? primary_color : bearish_color

table.cell(dashboard, 1, 10, str.tostring(equity_risk_premium, '##.##') + '%', text_color = erp_color, text_size = size.small)

// ROE

table.cell(dashboard, 0, 11, 'ROE', text_color = dashboard_text_color, text_size = size.small)

roe_color = spy_return_on_equity > 20 ? bullish_color : spy_return_on_equity > 10 ? primary_color : bearish_color

table.cell(dashboard, 1, 11, str.tostring(spy_return_on_equity, '##.#') + '%', text_color = roe_color, text_size = size.small)

// D/E Ratio

table.cell(dashboard, 0, 12, 'D/E Ratio', text_color = dashboard_text_color, text_size = size.small)

de_color = spy_debt_to_equity < 0.5 ? bullish_color : spy_debt_to_equity < 1.0 ? primary_color : bearish_color

table.cell(dashboard, 1, 12, str.tostring(spy_debt_to_equity, '##.##'), text_color = de_color, text_size = size.small)

// Shareholder Yield

table.cell(dashboard, 0, 13, 'Dividend+Buyback', text_color = dashboard_text_color, text_size = size.small)

yield_color = total_shareholder_yield > 4 ? bullish_color : total_shareholder_yield > 2 ? primary_color : bearish_color

table.cell(dashboard, 1, 13, str.tostring(total_shareholder_yield, '##.#') + '%', text_color = yield_color, text_size = size.small)

// Component Scores

component_bg = color.new(neutral_color, 80)

table.cell(dashboard, 0, 14, 'Components', text_color = dashboard_text_color, bgcolor = component_bg, text_size = size.small)

table.cell(dashboard, 1, 14, 'Scores', text_color = dashboard_text_color, bgcolor = component_bg, text_size = size.small)

table.cell(dashboard, 0, 15, 'Regime', text_color = dashboard_text_color, text_size = size.small)

regime_score_color = regime_allocation > 60 ? bullish_color : regime_allocation < 40 ? bearish_color : primary_color

table.cell(dashboard, 1, 15, str.tostring(regime_allocation, '##'), text_color = regime_score_color, text_size = size.small)

table.cell(dashboard, 0, 16, 'Risk', text_color = dashboard_text_color, text_size = size.small)

risk_score_color = risk_allocation > 60 ? bullish_color : risk_allocation < 40 ? bearish_color : primary_color

table.cell(dashboard, 1, 16, str.tostring(risk_allocation, '##'), text_color = risk_score_color, text_size = size.small)

table.cell(dashboard, 0, 17, 'Valuation', text_color = dashboard_text_color, text_size = size.small)

val_score_color = valuation_score > 60 ? bullish_color : valuation_score < 40 ? bearish_color : primary_color

table.cell(dashboard, 1, 17, str.tostring(valuation_score, '##'), text_color = val_score_color, text_size = size.small)

table.cell(dashboard, 0, 18, 'Sentiment', text_color = dashboard_text_color, text_size = size.small)

sent_score_color = sentiment_score > 60 ? bullish_color : sentiment_score < 40 ? bearish_color : primary_color

table.cell(dashboard, 1, 18, str.tostring(sentiment_score, '##'), text_color = sent_score_color, text_size = size.small)

table.cell(dashboard, 0, 19, 'Macro', text_color = dashboard_text_color, text_size = size.small)

macro_score_color = macro_score > 60 ? bullish_color : macro_score < 40 ? bearish_color : primary_color

table.cell(dashboard, 1, 19, str.tostring(macro_score, '##'), text_color = macro_score_color, text_size = size.small)

// ALERTS

// Major allocation changes

alertcondition(smoothed_allocation >= 80 and smoothed_allocation < 80, 'High Equity Allocation', 'Equity allocation reached 80% - Bull market conditions')

alertcondition(smoothed_allocation <= 20 and smoothed_allocation > 20, 'Low Equity Allocation', 'Equity allocation dropped to 20% - Defensive positioning')

// Crisis alerts

alertcondition(is_crisis and not is_crisis , 'CRISIS DETECTED', 'Crisis conditions detected - Reducing equity allocation')

alertcondition(is_severe_crisis and not is_severe_crisis , 'SEVERE CRISIS', 'Severe crisis detected - Maximum defensive positioning')

// Regime changes

regime_changed = market_regime != market_regime

alertcondition(regime_changed, 'Regime Change', 'Market regime has changed')

// Risk management alerts

risk_breach = enable_portfolio_risk_scaling and (actual_portfolio_volatility > target_portfolio_volatility * 1.2 or actual_portfolio_drawdown > max_portfolio_drawdown * 1.2)

alertcondition(risk_breach, 'Risk Breach', 'Portfolio risk exceeds target parameters')

// USAGE

// The indicator displays a recommended equity allocation percentage (0-100%).

// Example: 75% allocation = 75% stocks, 25% cash/bonds.

//

// The model combines market regime analysis (trend, volatility, drawdowns),

// risk management (portfolio-level targeting), valuation metrics (P/E, ERP),

// sentiment indicators (VIX term structure), and macro factors (yield curve,

// credit spreads) into a single allocation signal.

//

// Crisis detection automatically reduces exposure when multiple warning signals

// converge. Alerts available for major allocation shifts and regime changes.

//

// Designed for SPY/S&P 500 portfolio allocation. Adjust component weights and

// risk parameters in settings to match your risk tolerance.

View in Pine

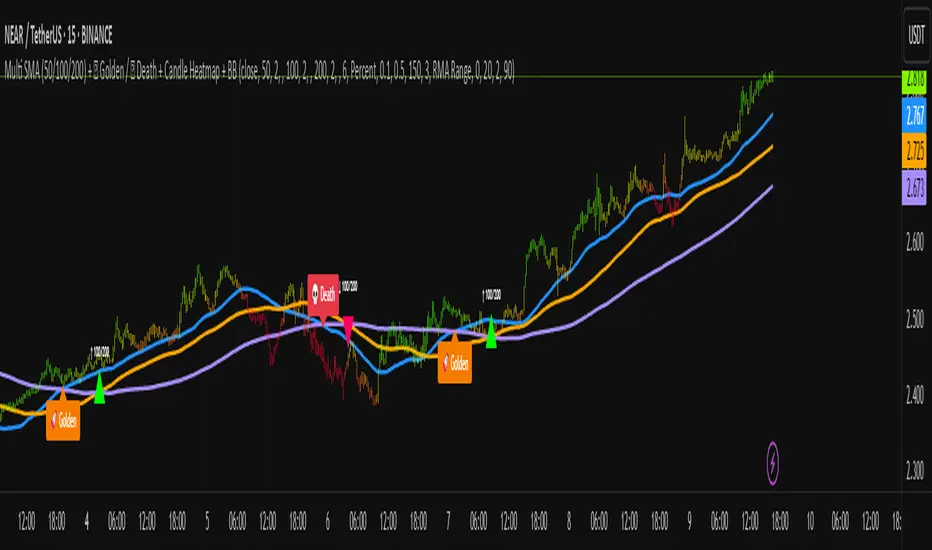

Multi SMA + Golden/Death + Heatmap + BB**Multi SMA (50/100/200) + Golden/Death + Candle Heatmap + BB**

A practical trend toolkit that blends classic 50/100/200 SMAs with clear crossover labels, special 🚀 Golden / 💀 Death Cross markers, and a readable candle heatmap based on a dynamic regression midline and volatility bands. Optional Bollinger Bands are included for context.

* See trend direction at a glance with SMAs.

* Get minimal, de-cluttered labels on important crosses (50↔100, 50↔200, 100↔200).

* Highlight big regime shifts with special Golden/Death tags.

* Read momentum and volatility with the candle heatmap.

* Add Bollinger Bands if you want classic mean-reversion context.

Designed to be lightweight, non-repainting on confirmed bars, and flexible across timeframes.

# What This Indicator Does (plain English)

* **Tracks trend** using **SMA 50/100/200** and lets you optionally compute each SMA on a higher or different timeframe (HTF-safe, no lookahead).

* **Prints labels** when SMAs cross each other (up or down). You can force signals only after bar close to avoid repaint.

* **Marks Golden/Death Crosses** (50 over/under 200) with special labels so major regime changes stand out.

* **Colors candles** with a **heatmap** built from a regression midline and volatility bands—greenish above, reddish below, with a smooth gradient.

* **Optionally shows Bollinger Bands** (basis SMA + stdev bands) and fills the area between them.

* **Includes alert conditions** for Golden and Death Cross so you can automate notifications.

---

# Settings — Simple Explanations

## Source

* **Source**: Price source used to calculate SMAs and Bollinger basis. Default: `close`.

## SMA 50

* **Show 50**: Turn the SMA(50) line on/off.

* **Length 50**: How many bars to average. Lower = faster but noisier.

* **Color 50** / **Width 50**: Visual style.

* **Timeframe 50**: Optional alternate timeframe for SMA(50). Leave empty to use the chart timeframe.

## SMA 100

* **Show 100**: Turn the SMA(100) line on/off.

* **Length 100**: Bars used for the mid-term trend.

* **Color 100** / **Width 100**: Visual style.

* **Timeframe 100**: Optional alternate timeframe for SMA(100).

## SMA 200

* **Show 200**: Turn the SMA(200) line on/off.

* **Length 200**: Bars used for the long-term trend.

* **Color 200** / **Width 200**: Visual style.

* **Timeframe 200**: Optional alternate timeframe for SMA(200).

## Signals (crossover labels)

* **Show crossover signals**: Prints triangle labels on SMA crosses (50↔100, 50↔200, 100↔200).

* **Wait for bar close (confirmed)**: If ON, signals only appear after the candle closes (reduces repaint).

* **Min bars between same-pair signals**: Minimum spacing to avoid duplicate labels from the same SMA pair too often.

* **Trend filter (buy: 50>100>200, sell: 50<100<200)**: Only show bullish labels when SMAs are stacked bullish (50 above 100 above 200), and only show bearish labels when stacked bearish.

### Label Offset

* **Offset mode**: Choose how to push labels away from price:

* **Percent**: Offset is a % of price.

* **ATR x**: Offset is ATR(14) × multiplier.

* **Percent of price (%)**: Used when mode = Percent.

* **ATR multiplier (for ‘ATR x’)**: Used when mode = ATR x.

### Label Colors

* **Bull color** / **Bear color**: Background of triangle labels.

* **Bull label text color** / **Bear label text color**: Text color inside the triangles.

## Golden / Death Cross

* **Show 🚀 Golden Cross (50↑200)**: Show a special “Golden” label when SMA50 crosses above SMA200.

* **Golden label color** / **Golden text color**: Styling for Golden label.

* **Show 💀 Death Cross (50↓200)**: Show a special “Death” label when SMA50 crosses below SMA200.

* **Death label color** / **Death text color**: Styling for Death label.

## Candle Heatmap

* **Enable heatmap candle colors**: Turns the heatmap on/off.

* **Length**: Lookback for the regression midline and volatility measure.

* **Deviation Multiplier**: Band width around the midline (bigger = wider).

* **Volatility basis**:

* **RMA Range** (smoothed high-low range)

* **Stdev** (standard deviation of close)

* **Upper/Middle/Lower color**: Gradient colors for the heatmap.

* **Heatmap transparency (0..100)**: 0 = solid, 100 = invisible.

* **Force override base candles**: Repaint base candles so heatmap stays visible even if your chart has custom coloring.

## Bollinger Bands (optional)

* **Show Bollinger Bands**: Toggle the overlay on/off.

* **Length**: Basis SMA length.

* **StdDev Multiplier**: Distance of bands from the basis in standard deviations.

* **Basis color** / **Band color**: Line colors for basis and bands.

* **Bands fill transparency**: Opacity of the fill between upper/lower bands.

---

# Features & How It Works

## 1) HTF-Safe SMAs

Each SMA can be calculated on the chart timeframe or a higher/different timeframe you choose. The script pulls HTF values **without lookahead** (non-repainting on confirmed bars).

## 2) Crossover Labels (Three Pairs)

* **50↔100**, **50↔200**, **100↔200**:

* **Triangle Up** label when the first SMA crosses **above** the second.

* **Triangle Down** label when it crosses **below**.

* Optional **Trend Filter** ensures only signals aligned with the overall stack (50>100>200 for bullish, 50<100<200 for bearish).

* **Debounce** spacing avoids repeated labels for the same pair too close together.

## 3) Golden / Death Cross Highlights

* **🚀 Golden Cross**: SMA50 crosses **above** SMA200 (often a longer-term bullish regime shift).

* **💀 Death Cross**: SMA50 crosses **below** SMA200 (often a longer-term bearish regime shift).

* Separate styling so they stand out from regular cross labels.

## 4) Candle Heatmap

* Builds a **regression midline** with **volatility bands**; colors candles by their position inside that channel.

* Smooth gradient: lower side → reddish, mid → yellowish, upper side → greenish.

* Helps you see momentum and “where price sits” relative to a dynamic channel.

## 5) Bollinger Bands (Optional)

* Classic **basis SMA** ± **StdDev** bands.

* Light visual context for mean-reversion and volatility expansion.

## 6) Alerts

* **Golden Cross**: `🚀 GOLDEN CROSS: SMA 50 crossed ABOVE SMA 200`

* **Death Cross**: `💀 DEATH CROSS: SMA 50 crossed BELOW SMA 200`

Add these to your alerts to get notified automatically.

---

# Tips & Notes

* For fewer false positives, keep **“Wait for bar close”** ON, especially on lower timeframes.

* Use the **Trend Filter** to align signals with the broader stack and cut noise.

* For HTF context, set **Timeframe 50/100/200** to higher frames (e.g., H1/H4/D) while you trade on a lower frame.

* Heatmap “Length” and “Deviation Multiplier” control smoothness and channel width—tune for your asset’s volatility.

Advanced Speedometer Gauge [PhenLabs]Advanced Speedometer Gauge

Version: PineScript™v6

📌 Description

The Advanced Speedometer Gauge is a revolutionary multi-metric visualization tool that consolidates 13 distinct trading indicators into a single, intuitive speedometer display. Instead of cluttering your workspace with multiple oscillators and panels, this gauge provides a unified interface where you can switch between different metrics while maintaining consistent visual interpretation.

Built on PineScript™ v6, the indicator transforms complex technical calculations into an easy-to-read semi-circular gauge with color-coded zones and a precision needle indicator. Each of the 13 available metrics has been carefully normalized to a 0-100 scale, ensuring that whether you’re analyzing RSI, volume trends, or volatility extremes, the visual interpretation remains consistent and intuitive.

The gauge is designed for traders who value efficiency and clarity. By consolidating multiple analytical perspectives into one compact display, you can quickly assess market conditions without the visual noise of traditional multi-indicator setups. All metrics are non-overlapping, meaning each provides unique insights into different aspects of market behavior.

🚀 Points of Innovation

13 selectable metrics covering momentum, volume, volatility, trend, and statistical analysis, all accessible through a single dropdown menu

Universal 0-100 normalization system that standardizes different indicator scales for consistent visual interpretation across all metrics

Semi-circular gauge design with 21 arc segments providing smooth precision and clear visual feedback through color-coded zones

Non-redundant metric selection ensuring each indicator provides unique market insights without analytical overlap

Advanced metrics including MFI (volume-weighted momentum), CCI (statistical deviation), Volatility Rank (extended lookback), Trend Strength (ADX-style), Choppiness Index, Volume Trend, and Price Distance from MA

Flexible positioning system with 5 chart locations, 3 size options, and fully customizable color schemes for optimal workspace integration

🔧 Core Components

Metric Selection Engine: Dropdown interface allowing instant switching between 13 different technical indicators, each with independent parameter controls

Normalization System: All metrics converted to 0-100 scale using indicator-specific algorithms that preserve the statistical significance of each measurement

Semi-Circular Gauge: Visual display using 21 arc segments arranged in curved formation with two-row thickness for enhanced visibility

Color Zone System: Three distinct zones (0-40 green, 40-70 yellow, 70-100 red) providing instant visual feedback on metric extremes

Needle Indicator: Dynamic pointer that positions across the gauge arc based on precise current metric value

Table Implementation: Professional table structure ensuring consistent positioning and rendering across different chart configurations

🔥 Key Features

RSI (Relative Strength Index): Classic momentum oscillator measuring overbought/oversold conditions with adjustable period length (default 14)

Stochastic Oscillator: Compares closing price to price range over specified period with smoothing, ideal for identifying momentum shifts

MFI (Money Flow Index): Volume-weighted RSI that combines price movement with volume to measure buying and selling pressure intensity

CCI (Commodity Channel Index): Measures statistical deviation from average price, normalized from typical -200 to +200 range to 0-100 scale

Williams %R: Alternative overbought/oversold indicator using high-low range analysis, inverted to match 0-100 scale conventions

Volume %: Current volume relative to moving average expressed as percentage, capped at 100 for extreme spikes

Volume Trend: Cumulative directional volume flow showing whether volume is flowing into up moves or down moves over specified period

ATR Percentile: Current Average True Range position within historical range using specified lookback period (default 100 bars)

Volatility Rank: Close-to-close volatility measured against extended historical range (default 252 days), differs from ATR in calculation method

Momentum: Rate of change calculation showing price movement speed, centered at 50 and normalized to 0-100 range

Trend Strength: ADX-style calculation using directional movement to quantify trend intensity regardless of direction

Choppiness Index: Measures market choppiness versus trending behavior, where high values indicate ranging markets and low values indicate strong trends

Price Distance from MA: Measures current price over-extension from moving average using standard deviation calculations

🎨 Visualization

Semi-Circular Arc Display: Curved gauge spanning from 0 (left) to 100 (right) with smooth progression and two-row thickness for visibility

Color-Coded Zones: Green zone (0-40) for low/oversold conditions, yellow zone (40-70) for neutral readings, red zone (70-100) for high/overbought conditions

Needle Indicator: Downward-pointing triangle (▼) positioned precisely at current metric value along the gauge arc

Scale Markers: Vertical line markers at 0, 25, 50, 75, and 100 positions with corresponding numerical labels below

Title Display: Merged cell showing “𓄀 PhenLabs” branding plus currently selected metric name in monospace font

Large Value Display: Current metric value shown with two decimal precision in large text directly below title

Table Structure: Professional table with customizable background color, text color, and transparency for minimal chart obstruction

📖 Usage Guidelines

Metric Selection

Select Metric: Default: RSI | Options: RSI, Stochastic, Volume %, ATR Percentile, Momentum, MFI (Money Flow), CCI (Commodity Channel), Williams %R, Volatility Rank, Trend Strength, Choppiness Index, Volume Trend, Price Distance | Choose the technical indicator you want to display on the gauge based on your current analytical needs

RSI Settings

RSI Length: Default: 14 | Range: 1+ | Controls the lookback period for RSI calculation, shorter periods increase sensitivity to recent price changes

Stochastic Settings

Stochastic Length: Default: 14 | Range: 1+ | Lookback period for stochastic calculation comparing close to high-low range

Stochastic Smooth: Default: 3 | Range: 1+ | Smoothing period applied to raw stochastic value to reduce noise and false signals

Volume Settings

Volume MA Length: Default: 20 | Range: 1+ | Moving average period used to calculate average volume for comparison with current volume

Volume Trend Length: Default: 20 | Range: 5+ | Period for calculating cumulative directional volume flow trend

ATR and Volatility Settings

ATR Length: Default: 14 | Range: 1+ | Period for Average True Range calculation used in ATR Percentile metric

ATR Percentile Lookback: Default: 100 | Range: 20+ | Historical range used to determine current ATR position as percentile

Volatility Rank Lookback (Days): Default: 252 | Range: 50+ | Extended lookback period for Volatility Rank metric using close-to-close volatility

Momentum and Trend Settings

Momentum Length: Default: 10 | Range: 1+ | Lookback period for rate of change calculation in Momentum metric

Trend Strength Length: Default: 20 | Range: 5+ | Period for directional movement calculations in ADX-style Trend Strength metric

Advanced Metric Settings

MFI Length: Default: 14 | Range: 1+ | Lookback period for Money Flow Index calculation combining price and volume

CCI Length: Default: 20 | Range: 1+ | Period for Commodity Channel Index statistical deviation calculation

Williams %R Length: Default: 14 | Range: 1+ | Lookback period for Williams %R high-low range analysis

Choppiness Index Length: Default: 14 | Range: 5+ | Period for calculating market choppiness versus trending behavior

Price Distance MA Length: Default: 50 | Range: 10+ | Moving average period used for Price Distance standard deviation calculation

Visual Customization

Position: Default: Top Right | Options: Top Left, Top Right, Bottom Left, Bottom Right, Middle Right | Controls gauge placement on chart for optimal workspace organization

Size: Default: Normal | Options: Small, Normal, Large | Adjusts overall gauge dimensions and text size for different monitor resolutions and preferences

Low Zone Color (0-40): Default: Green (#00FF00) | Customize color for low/oversold zone of gauge arc

Medium Zone Color (40-70): Default: Yellow (#FFFF00) | Customize color for neutral/medium zone of gauge arc

High Zone Color (70-100): Default: Red (#FF0000) | Customize color for high/overbought zone of gauge arc

Background Color: Default: Semi-transparent dark gray | Customize gauge background for contrast and chart integration

Text Color: Default: White (#FFFFFF) | Customize all text elements including title, value, and scale labels

✅ Best Use Cases

Quick visual assessment of market conditions when you need instant feedback on whether an asset is in extreme territory across multiple analytical dimensions

Workspace organization for traders who monitor multiple indicators but want to reduce chart clutter and visual complexity

Metric comparison by switching between different indicators while maintaining consistent visual interpretation through the 0-100 normalization

Overbought/oversold identification using RSI, Stochastic, Williams %R, or MFI depending on whether you prefer price-only or volume-weighted analysis

Volume analysis through Volume %, Volume Trend, or MFI to confirm price movements with corresponding volume characteristics

Volatility monitoring using ATR Percentile or Volatility Rank to identify expansion/contraction cycles and adjust position sizing

Trend vs range identification by comparing Trend Strength (high values = trending) against Choppiness Index (high values = ranging)

Statistical over-extension detection using CCI or Price Distance to identify when price has deviated significantly from normal behavior

Multi-timeframe analysis by duplicating the gauge on different timeframe charts to compare metric readings across time horizons

Educational purposes for new traders learning to interpret technical indicators through consistent visual representation

⚠️ Limitations

The gauge displays only one metric at a time, requiring manual switching to compare different indicators rather than simultaneous multi-metric viewing

The 0-100 normalization, while providing consistency, may obscure the raw values and specific nuances of each underlying indicator

Table-based visualization cannot be exported or saved as an image separately from the full chart screenshot

Optimal parameter settings vary by asset type, timeframe, and market conditions, requiring user experimentation for best results

💡 What Makes This Unique

Unified Multi-Metric Interface: The only gauge-style indicator offering 13 distinct metrics through a single interface, eliminating the need for multiple oscillator panels

Non-Overlapping Analytics: Each metric provides genuinely unique insights—MFI combines volume with price, CCI measures statistical deviation, Volatility Rank uses extended lookback, Trend Strength quantifies directional movement, and Choppiness Index measures ranging behavior

Universal Normalization System: All metrics standardized to 0-100 scale using indicator-appropriate algorithms that preserve statistical meaning while enabling consistent visual interpretation

Professional Visual Design: Semi-circular gauge with 21 arc segments, precision needle positioning, color-coded zones, and clean table implementation that maintains clarity across all chart configurations

Extensive Customization: Independent parameter controls for each metric, five position options, three size presets, and full color customization for seamless workspace integration

🔬 How It Works

1. Metric Calculation Phase:

All 13 metrics are calculated simultaneously on every bar using their respective algorithms with user-defined parameters

Each metric applies its own specific calculation method—RSI uses average gains vs losses, Stochastic compares close to high-low range, MFI incorporates typical price and volume, CCI measures deviation from statistical mean, ATR calculates true range, directional indicators measure up/down movement, and statistical metrics analyze price relationships

2. Normalization Process:

Each calculated metric is converted to a standardized 0-100 scale using indicator-appropriate transformations

Some metrics are naturally 0-100 (RSI, Stochastic, MFI, Williams %R), while others require scaling—CCI transforms from ±200 range, Momentum centers around 50, Volume ratio caps at 2x for 100, ATR and Volatility Rank calculate percentile positions, and Price Distance scales by standard deviations

3. Gauge Rendering:

The selected metric’s normalized value determines the needle position across 21 arc segments spanning 0-100

Each arc segment receives its color based on position—segments 0-8 are green zone, segments 9-14 are yellow zone, segments 15-20 are red zone

The needle indicator (▼) appears in row 5 at the column corresponding to the current metric value, providing precise visual feedback

4. Table Construction:

The gauge uses TradingView’s table system with merged cells for title and value display, ensuring consistent positioning regardless of chart configuration

Rows are allocated as follows: Row 0 merged for title, Row 1 merged for large value display, Row 2 for spacing, Rows 3-4 for the semi-circular arc with curved shaping, Row 5 for needle indicator, Row 6 for scale markers, Row 7 for numerical labels at 0/25/50/75/100

All visual elements update on every bar when barstate.islast is true, ensuring real-time accuracy without performance impact

💡 Note:

This indicator is designed for visual analysis and market condition assessment, not as a standalone trading system. For best results, combine gauge readings with price action analysis, support and resistance levels, and broader market context. Parameter optimization is recommended based on your specific trading timeframe and asset class. The gauge works on all timeframes but may require different parameter settings for intraday versus daily/weekly analysis. Consider using multiple instances of the gauge set to different metrics for comprehensive market analysis without switching between settings.