WaveTrend With Divs & RSI(STOCH) Divs by WeloTradesWaveTrend with Divergences & RSI(STOCH) Divergences by WeloTrades

Overview

The "WaveTrend With Divergences & RSI(STOCH) Divergences" is an advanced Pine Script™ indicator designed for TradingView, offering a multi-dimensional analysis of market conditions. This script integrates several technical indicators—WaveTrend, Money Flow Index (MFI), RSI, and Stochastic RSI—into a cohesive tool that identifies both regular and hidden divergences across these indicators. These divergences can indicate potential market reversals and provide critical trading opportunities.

This indicator is not just a simple combination of popular tools; it offers extensive customization options, organized data presentation, and valuable trading signals that are easy to interpret. Whether you're a day trader or a long-term investor, this script enhances your ability to make informed decisions.

Originality and Usefulness

The originality of this script lies in its integration and the synergy it creates among the indicators used. Rather than merely combining multiple indicators, this script allows them to work together, enhancing each other's strengths. For example, by identifying divergences across WaveTrend, RSI, and Stochastic RSI simultaneously, the script provides multiple layers of confirmation, which reduces the likelihood of false signals and increases the reliability of trading signals.

The usefulness of this script is apparent in its ability to offer a consolidated view of market dynamics. It not only simplifies the analytical process by combining different indicators but also provides deeper insights through its divergence detection features. This comprehensive approach is designed to help traders identify potential market reversals, confirm trends, and ultimately make more informed trading decisions.

How the Components Work Together

1. Cross-Validation of Signals

WaveTrend: This indicator is primarily used to identify overbought and oversold conditions, as well as potential buy and sell signals. WaveTrend's ability to smooth price data and reduce noise makes it a reliable tool for identifying trend reversals.

RSI & Stochastic RSI: These momentum oscillators are used to measure the speed and change of price movements. While RSI identifies general overbought and oversold conditions, Stochastic RSI offers a more granular view by tracking the RSI’s level relative to its high-low range over a period of time. When these indicators align with WaveTrend signals, it adds a layer of confirmation that enhances the reliability of the signals.

Money Flow Index (MFI): This volume-weighted indicator assesses the inflow and outflow of money in an asset, giving insights into buying and selling pressure. By analyzing the MFI alongside WaveTrend and RSI indicators, the script can cross-validate signals, ensuring that buy or sell signals are supported by actual market volume.

Example Bullish scenario:

When a bullish divergence is detected on the RSI and confirmed by a corresponding bullish signal on the WaveTrend, along with an increasing Money Flow Index, the probability of a successful trade setup increases. This cross-validation minimizes the risk of acting on false signals, which might occur when relying on a single indicator.

Example Bearish scenario:

When a bearish divergence is detected on the RSI and confirmed by a corresponding bearish signal on the WaveTrend, along with an decreasing Money Flow Index, the probability of a successful trade setup increases. This cross-validation minimizes the risk of acting on false signals, which might occur when relying on a single indicator.

2. Divergence Detection and Market Reversals

Regular Divergences: Occur when the price action and an indicator (like RSI or WaveTrend) move in opposite directions. Regular bullish divergence signals a potential upward reversal when the price makes a lower low while the indicator makes a higher low. Conversely, regular bearish divergence suggests a downward reversal when the price makes a higher high, but the indicator makes a lower high.

Hidden Divergences: These occur when the price action and indicator move in the same direction, but with different momentum. Hidden bullish divergence suggests the continuation of an uptrend, while hidden bearish divergence suggests the continuation of a downtrend. By detecting these divergences across multiple indicators, the script identifies potential trend reversals or continuations with greater accuracy.

Example: The script might detect a regular bullish divergence on the WaveTrend while simultaneously identifying a hidden bullish divergence on the RSI. This combination suggests that while a trend reversal is possible, the overall market sentiment remains bullish, providing a nuanced view of the market.

A Regular Bullish Divergence Example:

A Hidden Bullish Divergence Example:

A Regular Bearish Divergence Example:

A Hidden Bearish Divergence Example:

3. Trend Strength and Sentiment Analysis

WaveTrend: Measures the strength and direction of the trend. By identifying the extremes of market sentiment (overbought and oversold levels), WaveTrend provides early signals for potential reversals.

Money Flow Index (MFI): Assesses the underlying sentiment by analyzing the flow of money. A rising MFI during an uptrend confirms strong buying pressure, while a falling MFI during a downtrend confirms selling pressure. This helps traders assess whether a trend is likely to continue or reverse.

RSI & Stochastic RSI: Offer a momentum-based perspective on the trend’s strength. High RSI or Stochastic RSI values indicate that the asset may be overbought, suggesting a potential reversal. Conversely, low values indicate oversold conditions, signaling a possible upward reversal.

Example:

During a strong uptrend, the WaveTrend & RSI's might signal overbought conditions, suggesting caution. If the MFI also shows decreasing buying pressure and the RSI reaches extreme levels, these indicators together suggest that the trend might be weakening, and a reversal could be imminent.

Example:

During a strong downtrend, the WaveTrend & RSI's might signal oversold conditions, suggesting caution. If the MFI also shows increasing buying pressure and the RSI reaches extreme levels, these indicators together suggest that the trend might be weakening, and a reversal could be imminent.

Conclusion

The "WaveTrend With Divergences & RSI(STOCH) Divergences" script offers a powerful, integrated approach to technical analysis by combining trend, momentum, and sentiment indicators into a single tool. Its unique value lies in the cross-validation of signals, the ability to detect divergences, and the comprehensive view it provides of market conditions. By offering traders multiple layers of analysis and customization options, this script is designed to enhance trading decisions, reduce false signals, and provide clearer insights into market dynamics.

WAVETREND

Display of WaveTrend:

Display of WaveTrend Setting:

WaveTrend Indicator Explanation

The WaveTrend indicator helps identify overbought and oversold conditions, as well as potential buy and sell signals. Its flexibility allows traders to adapt it to various strategies, making it a versatile tool in technical analysis.

WaveTrend Input Settings:

WT MA Source: Default: HLC3

What it is: The data source used for calculating the WaveTrend Moving Average.

What it does: Determines the input data to smooth price action and filter noise.

Example: Using HLC3 (average of High, Low, Close) provides a smoother data representation compared to using just the closing price.

Length (WT MA Length): Default: 3

What it is: The period used to calculate the Moving Average.

What it does: Adjusts the sensitivity of the WaveTrend indicator, where shorter lengths respond more quickly to price changes.

Example: A length of 3 is ideal for short-term analysis, providing quick reactions to price movements.

WT Channel Length & Average: Default: WT Channel Length = 9, Average = 12

What it is: Lengths used to calculate the WaveTrend channel and its average.

What it does: Smooths out the WaveTrend further, reducing false signals by averaging over a set period.

Example: Higher values reduce noise and help in identifying more reliable trends.

Channel: Style, Width, and Color:

What it is: Customization options for the WaveTrend channel's appearance.

What it does: Adjusts how the channel is displayed, including line style, width, and color.

Example: Choosing an area style with a distinct color can make the WaveTrend indicator clearly visible on the chart.

WT Buy & Sell Signals:

What it is: Settings to enable and customize buy and sell signals based on WaveTrend.

What it does: Allows for the display of buy/sell signals and customization of their shapes and colors.

When it gives a Buy Signal: Generated when the WaveTrend line crosses below an oversold level and then rises back, indicating a potential upward price movement.

When it gives a Sell Signal: Triggered when the WaveTrend line crosses above an overbought level and then declines, suggesting a possible downward trend.

Example: The script identifies these signals based on mean reversion principles, where prices tend to revert to the mean after reaching extremes. Traders can use these signals to time their entries and exits effectively.

WAVETREND OVERBOUGTH AND OVERSOLD LEVELS

Display of WaveTrend with Overbought & Oversold Levels:

Display of WaveTrend Overbought & Oversold Levels Settings:

WaveTrend Overbought & Oversold Levels Explanation

WT OB & OS Levels: Default: OB Level 1 = 53, OB Level 2 = 60, OS Level 1 = -53, OS Level 2 = -60

What it is: The default overbought and oversold levels used by the WaveTrend indicator to signal potential market reversals.

What it does: When the WaveTrend crosses above the OB levels, it indicates an overbought condition, potentially signaling a reversal or selling opportunity. Conversely, when it crosses below the OS levels, it indicates an oversold condition, potentially signaling a reversal or buying opportunity.

Example: A trader might use these levels to time entry or exit points, such as selling when the WaveTrend crosses into the overbought zone or buying when it crosses into the oversold zone.

Show OB/OS Levels: Default: True

What it is: Toggle options to show or hide the overbought and oversold levels on your chart.

What it does: When enabled, these levels will be visually represented on your chart, helping you to easily identify when the market reaches these critical thresholds.

Example: Displaying these levels can help you quickly see when the WaveTrend is approaching or has crossed into overbought or oversold territory, allowing for more informed trading decisions.

Line Style, Width, and Color for OB/OS Levels:

What it is: Options to customize the appearance of the OB and OS levels on your chart, including line style (solid, dotted, dashed), line width, and color.

What it does: These settings allow you to adjust how prominently these levels are displayed on your chart, which can help you better visualize and respond to overbought or oversold conditions.

Example: Setting a thicker, dashed line in a contrasting color can make these levels stand out more clearly, aiding in quick visual identification.

Example of Use:

Scenario: A trader wants to identify potential selling points when the market is overbought. They set the OB levels at 53 and 60, choosing a solid, red line style to make these levels clear on their chart. As the WaveTrend crosses above 53, they monitor for further price action, and upon crossing 60, they consider initiating a sell order.

WAVETREND DIVERGENCES

Display of WaveTrend Divergence:

Display of WaveTrend Divergence Setting:

WaveTrend Divergence Indicator Explanation

The WaveTrend Divergence feature helps identify potential reversal points in the market by highlighting divergences between the price and the WaveTrend indicator. Divergences can signal a shift in market momentum, indicating a possible trend reversal. This component allows traders to visualize and customize divergence detection on their charts.

WaveTrend Divergence Input Settings:

Potential Reversal Range: Default: 28

What it is: The number of bars to look back when detecting potential tops and bottoms.

What it does: Sets the range for identifying possible reversal points based on historical data.

Example: A setting of 28 looks back across the last 28 bars to find reversal points, offering a balance between responsiveness and reliability.

Reversal Minimum LVL OB & OS: Default: OB = 35, OS = -35

What it is: The minimum overbought and oversold levels required for detecting potential reversals.

What it does: Adjusts the thresholds that trigger a reversal signal based on the WaveTrend indicator.

Example: A higher OB level reduces the sensitivity to overbought conditions, potentially filtering out false reversal signals.

Lookback Bar Left & Right: Default: Left = 10, Right = 1

What it is: The number of bars to the left and right used to confirm a top or bottom.

What it does: Helps determine the position of peaks and troughs in the price action.

Example: A larger left lookback captures more extended price action before the peak, while a smaller right lookback focuses on the immediate past.

Lookback Range Min & Max: Default: Min = 5, Max = 60

What it is: The minimum and maximum range for the lookback period when identifying divergences.

What it does: Fine-tunes the detection of divergences by controlling the range over which the indicator looks back.

Example: A wider range increases the chances of detecting divergences across different market conditions.

R.Div Minimum LVL OB & OS: Default: OB = 53, OS = -53

What it is: The threshold levels for detecting regular divergences.

What it does: Adjusts the sensitivity of the regular divergence detection.

Example: Higher thresholds make the detection more conservative, identifying only stronger divergence signals.

H.Div Minimum LVL OB & OS: Default: OB = 20, OS = -20

What it is: The threshold levels for detecting hidden divergences.

What it does: Similar to regular divergence settings but for hidden divergences, which can indicate potential reversals that are less obvious.

Example: Lower thresholds make the hidden divergence detection more sensitive, capturing subtler market shifts.

Divergence Label Options:

What it is: Options to display and customize labels for regular and hidden divergences.

What it does: Allows users to visually differentiate between regular and hidden divergences using customizable labels and colors.

Example: Using different colors and symbols for regular (R) and hidden (H) divergences makes it easier to interpret signals on the chart.

Text Size and Color:

What it is: Customization options for the size and color of divergence labels.

What it does: Adjusts the readability and visibility of divergence labels on the chart.

Example: Larger text size may be preferred for charts with a lot of data, ensuring divergence labels stand out clearly.

FAST & SLOW MONEY FLOW INDEX

Display of Fast & Slow Money Flow:

Display of Fast & Slow Money Flow Setting:

Fast Money Flow Indicator Explanation

The Fast Money Flow indicator helps traders identify the flow of money into and out of an asset over a shorter time frame. By tracking the volume-weighted average of price movements, it provides insights into buying and selling pressure in the market, which can be crucial for making timely trading decisions.

Fast Money Flow Input Settings:

Fast Money Flow: Length: Default: 9

What it is: The period used for calculating the Fast Money Flow.

What it does: Determines the sensitivity of the Money Flow calculation. A shorter length makes the indicator more responsive to recent price changes, while a longer length provides a smoother signal.

Example: A length of 9 is suitable for traders looking to capture quick shifts in market sentiment over a short period.

Fast MFI Area Multiplier: Default: 5

What it is: A multiplier applied to the Money Flow area calculation.

What it does: Adjusts the size of the Money Flow area on the chart, effectively amplifying or reducing the visual impact of the indicator.

Example: A higher multiplier can make the Money Flow more prominent on the chart, aiding in the quick identification of significant money flow changes.

Y Position (Y Pos): Default: 0

What it is: The vertical position adjustment for the Fast Money Flow plot on the chart.

What it does: Allows you to move the Money Flow plot up or down on the chart to avoid overlap with other indicators.

Example: Adjusting the Y Position can be useful if you have multiple indicators on the chart and need to maintain clarity.

Fast MFI Style, Width, and Color:

What it is: Customization options for how the Fast Money Flow is displayed on the chart.

What it does: Enables you to choose between different plot styles (line or area), set the line width, and select colors for positive and negative money flow.

Example: Using different colors for positive (green) and negative (red) money flow helps to visually distinguish between periods of buying and selling pressure.

Slow Money Flow Indicator Explanation

The Slow Money Flow indicator tracks the flow of money into and out of an asset over a longer time frame. It provides a broader perspective on market sentiment, smoothing out short-term fluctuations and highlighting longer-term trends.

Slow Money Flow Input Settings:

Slow Money Flow: Length: Default: 12

What it is: The period used for calculating the Slow Money Flow.

What it does: A longer period smooths out short-term fluctuations, providing a clearer view of the overall money flow trend.

Example: A length of 12 is often used by traders looking to identify sustained trends rather than short-term volatility.

Slow MFI Area Multiplier: Default: 5

What it is: A multiplier applied to the Slow Money Flow area calculation.

What it does: Adjusts the size of the Money Flow area on the chart, helping to emphasize the indicator’s significance.

Example: Increasing the multiplier can help highlight the Money Flow in markets with less volatile price action.

Y Position (Y Pos): Default: 0

What it is: The vertical position adjustment for the Slow Money Flow plot on the chart.

What it does: Allows for vertical repositioning of the Money Flow plot to maintain chart clarity when used with other indicators.

Example: Adjusting the Y Position ensures that the Slow Money Flow indicator does not overlap with other key indicators on the chart.

Slow MFI Style, Width, and Color:

What it is: Customization options for the visual display of the Slow Money Flow on the chart.

What it does: Allows you to choose the plot style (line or area), set the line width, and select colors to differentiate positive and negative money flow.

Example: Customizing the colors for the Slow Money Flow allows traders to quickly distinguish between buying and selling trends in the market.

RSI

Display of RSI:

Display of RSI Setting:

RSI Indicator Explanation

The Relative Strength Index (RSI) is a momentum oscillator that measures the speed and change of price movements. It is typically used to identify overbought or oversold conditions in the market, providing traders with potential signals for buying or selling.

RSI Input Settings:

RSI Source: Default: Close

What it is: The data source used for calculating the RSI.

What it does: Determines which price data (e.g., close, open) is used in the RSI calculation, affecting how the indicator reflects market conditions.

Example: Using the closing price is standard practice, as it reflects the final agreed-upon price for a given time period.

MA Type (Moving Average Type): Default: SMA

What it is: The type of moving average applied to the RSI for smoothing purposes.

What it does: Changes the smoothing technique of the RSI, impacting how quickly the indicator responds to price movements.

Example: Using an Exponential Moving Average (EMA) will make the RSI more sensitive to recent price changes compared to a Simple Moving Average (SMA).

RSI Length: Default: 14

What it is: The period over which the RSI is calculated.

What it does: Adjusts the sensitivity of the RSI. A shorter length (e.g., 7) makes the RSI more responsive to recent price changes, while a longer length (e.g., 21) smooths out the indicator, reducing the number of signals.

Example: A 14-period RSI is commonly used for identifying overbought and oversold conditions, providing a balance between sensitivity and reliability.

RSI Plot Style, Width, and Color:

What it is: Options to customize the appearance of the RSI line on the chart.

What it does: Allows you to adjust the visual representation of the RSI, including the line width and color.

Example: Setting a thicker line width and a bright color like yellow can make the RSI more visible on the chart, aiding in quick analysis.

Display of RSI with RSI Moving Average:

RSI Moving Average Explanation

The RSI Moving Average adds a smoothing layer to the RSI, helping to filter out noise and provide clearer signals. It is particularly useful for confirming trend strength and identifying potential reversals.

RSI Moving Average Input Settings:

MA Length: Default: 14

What it is: The period over which the Moving Average is calculated on the RSI.

What it does: Adjusts the smoothing of the RSI, helping to reduce false signals and provide a clearer trend indication.

Example: A 14-period moving average on the RSI can smooth out short-term fluctuations, making it easier to spot genuine overbought or oversold conditions.

MA Plot Style, Width, and Color:

What it is: Customization options for how the RSI Moving Average is displayed on the chart.

What it does: Allows you to adjust the line width and color, helping to differentiate the Moving Average from the main RSI line.

Example: Using a contrasting color for the RSI Moving Average (e.g., magenta) can help it stand out against the main RSI line, making it easier to interpret the indicator.

STOCHASTIC RSI

Display of Stochastic RSI:

Display of Stochastic RSI Setting:

Stochastic RSI Indicator Explanation

The Stochastic RSI (Stoch RSI) is a momentum oscillator that measures the level of the RSI relative to its high-low range over a set period of time. It is used to identify overbought and oversold conditions, providing potential buy and sell signals based on momentum shifts.

Stochastic RSI Input Settings:

Stochastic RSI Length: Default: 14

What it is: The period over which the Stochastic RSI is calculated.

What it does: Adjusts the sensitivity of the Stochastic RSI. A shorter length makes the indicator more responsive to recent price changes, while a longer length smooths out the fluctuations, reducing noise.

Example: A length of 14 is commonly used to identify momentum shifts over a medium-term period, providing a balanced view of potential overbought or oversold conditions.

Display of Stochastic RSI %K Line:

Stochastic RSI %K Line Explanation

The %K line in the Stochastic RSI is the main line that tracks the momentum of the RSI over the chosen period. It is the faster-moving component of the Stochastic RSI, often used to identify entry and exit points.

Stochastic RSI %K Input Settings:

%K Length: Default: 3

What it is: The period used for smoothing the %K line of the Stochastic RSI.

What it does: Smoothing the %K line helps reduce noise and provides a clearer signal for potential market reversals.

Example: A smoothing length of 3 is common, offering a balance between responsiveness and noise reduction, making it easier to spot significant momentum shifts.

%K Plot Style, Width, and Color:

What it is: Customization options for the visual representation of the %K line.

What it does: Allows you to adjust the appearance of the %K line on the chart, including line width and color, to fit your visual preferences.

Example: Setting a blue color and a medium width for the %K line makes it stand out clearly on the chart, helping to identify key points of momentum change.

%K Fill Color (Above):

What it is: The fill color that appears above the %K line on the chart.

What it does: Adds visual clarity by shading the area above the %K line, making it easier to interpret the direction and strength of momentum.

Example: Using a light blue fill color above the %K line can help emphasize bullish momentum, making it visually prominent.

Display of Stochastic RSI %D Line:

Stochastic RSI %D Line Explanation

The %D line in the Stochastic RSI is a moving average of the %K line and acts as a signal line. It is slower-moving compared to the %K line and is often used to confirm signals or identify potential reversals when it crosses the %K line.

Stochastic RSI %D Input Settings:

%D Length: Default: 3

What it is: The period used for smoothing the %D line of the Stochastic RSI.

What it does: Smooths out the %D line, making it less sensitive to short-term fluctuations and more reliable for identifying significant market signals.

Example: A length of 3 is often used to provide a smoothed signal line that can help confirm trends or reversals indicated by the %K line.

%D Plot Style, Width, and Color:

What it is: Customization options for the visual representation of the %D line.

What it does: Allows you to adjust the appearance of the %D line on the chart, including line width and color, to match your preferences.

Example: Setting an orange color and a thicker line width for the %D line can help differentiate it from the %K line, making crossover points easier to spot.

%D Fill Color (Below):

What it is: The fill color that appears below the %D line on the chart.

What it does: Adds visual clarity by shading the area below the %D line, making it easier to interpret bearish momentum.

Example: Using a light orange fill color below the %D line can highlight bearish conditions, making it visually easier to identify.

RSI & STOCHASTIC RSI OVERBOUGHT AND OVERSOLD LEVELS

Display of RSI & Stochastic with Overbought & Oversold Levels:

Display of RSI & Stochastic Overbought & Oversold Settings:

RSI & Stochastic Overbought & Oversold Levels Explanation

The Overbought (OB) and Oversold (OS) levels for RSI and Stochastic RSI indicators are key thresholds that help traders identify potential reversal points in the market. These levels are used to determine when an asset is likely overbought or oversold, which can signal a potential trend reversal.

RSI & Stochastic Overbought & Oversold Input Settings:

RSI & Stochastic Level 1 Overbought (OB) & Oversold (OS): Default: OB Level = 170, OS Level = 130

What it is: The first set of thresholds for determining overbought and oversold conditions for both RSI and Stochastic RSI indicators.

What it does: When the RSI or Stochastic RSI crosses above the overbought level, it suggests that the asset might be overbought, potentially signaling a sell opportunity. Conversely, when these indicators drop below the oversold level, it suggests the asset might be oversold, potentially signaling a buy opportunity.

Example: If the RSI crosses above 170, traders might look for signs of a potential trend reversal to the downside, while a cross below 130 might indicate a reversal to the upside.

RSI & Stochastic Level 2 Overbought (OB) & Oversold (OS): Default: OB Level = 180, OS Level = 120

What it is: The second set of thresholds for determining overbought and oversold conditions for both RSI and Stochastic RSI indicators.

What it does: These levels provide an additional set of reference points, allowing traders to differentiate between varying degrees of overbought and oversold conditions, potentially leading to more refined trading decisions.

Example: When the RSI crosses above 180, it might indicate an extreme overbought condition, which could be a stronger signal for a sell, while a cross below 120 might indicate an extreme oversold condition, which could be a stronger signal for a buy.

RSI & Stochastic Overbought (OB) Band Customization:

OB Level 1: Width, Style, and Color:

What it is: Customization options for the visual appearance of the first overbought band on the chart.

What it does: Allows you to set the line width, style (solid, dotted, dashed), and color for the first overbought band, enhancing its visibility on the chart.

Example: A dashed red line with medium width can clearly indicate the first overbought level, helping traders quickly identify when this threshold is crossed.

OB Level 2: Width, Style, and Color:

What it is: Customization options for the visual appearance of the second overbought band on the chart.

What it does: Allows you to set the line width, style, and color for the second overbought band, providing a clear distinction from the first band.

Example: A dashed red line with a slightly thicker width can represent a more significant overbought level, making it easier to differentiate from the first level.

RSI & Stochastic Oversold (OS) Band Customization:

OS Level 1: Width, Style, and Color:

What it is: Customization options for the visual appearance of the first oversold band on the chart.

What it does: Allows you to set the line width, style (solid, dotted, dashed), and color for the first oversold band, making it visually prominent.

Example: A dashed green line with medium width can highlight the first oversold level, helping traders identify potential buying opportunities.

OS Level 2: Width, Style, and Color:

What it is: Customization options for the visual appearance of the second oversold band on the chart.

What it does: Allows you to set the line width, style, and color for the second oversold band, providing an additional visual cue for extreme oversold conditions.

Example: A dashed green line with a thicker width can represent a more significant oversold level, offering a stronger visual cue for potential buying opportunities.

RSI DIVERGENCES

Display of RSI Divergence Labels:

Display of RSI Divergence Settings:

RSI Divergence Lookback Explanation

The RSI Divergence settings allow traders to customize the parameters for detecting divergences between the RSI (Relative Strength Index) and price action. Divergences occur when the price moves in the opposite direction to the RSI, potentially signaling a trend reversal. These settings help refine the accuracy of divergence detection by adjusting the lookback period and range. ( NOTE: This setting only imply to the RSI. This doesn't effect the STOCHASTIC RSI. )

RSI Divergence Lookback Input Settings:

Lookback Left: Default: 10

What it is: The number of bars to look back from the current bar to detect a potential divergence.

What it does: Defines the left-side lookback period for identifying pivot points in the RSI, which are used to spot divergences. A longer lookback period may capture more significant trends but could also miss shorter-term divergences.

Example: A setting of 10 bars means the script will consider pivot points up to 10 bars before the current bar to check for divergence patterns.

Lookback Right: Default: 1

What it is: The number of bars to look forward from the current bar to complete the divergence pattern.

What it does: Defines the right-side lookback period for confirming a potential divergence. This setting helps ensure that the identified divergence is valid by allowing the script to check subsequent bars for confirmation.

Example: A setting of 1 bar means the script will look at the next bar to confirm the divergence pattern, ensuring that the signal is reliable.

Lookback Range Min: Default: 5

What it is: The minimum range of bars required to detect a valid divergence.

What it does: Sets a lower bound on the range of bars considered for divergence detection. A lower minimum range might capture more frequent but possibly less significant divergences.

Example: Setting the minimum range to 5 ensures that only divergences spanning at least 5 bars are considered, filtering out very short-term patterns.

Lookback Range Max: Default: 60

What it is: The maximum range of bars within which a divergence can be detected.

What it does: Sets an upper bound on the range of bars considered for divergence detection. A larger maximum range might capture more significant divergences but could also include less relevant long-term patterns.

Example: Setting the maximum range to 60 bars allows the script to detect divergences over a longer timeframe, capturing more extended divergence patterns that could indicate major trend reversals.

RSI Divergence Explanation

RSI divergences occur when the RSI indicator and price action move in opposite directions, signaling potential trend reversals. This section of the settings allows traders to customize the appearance and detection of both regular and hidden bullish and bearish divergences.

RSI Divergence Input Settings:

R. Bullish Div Label: Default: True

What it is: An option to display labels for regular bullish divergences.

What it does: Enables or disables the visibility of labels that mark regular bullish divergences, where the price makes a lower low while the RSI makes a higher low, indicating a potential upward reversal.

Example: A trader might use this to spot buying opportunities in a downtrend when a bullish divergence suggests the trend may be reversing.

Bullish Label Color, Line Width, and Line Color:

What it is: Settings to customize the appearance of regular bullish divergence labels.

What it does: Allows you to choose the color of the labels, adjust the width of the divergence lines, and select the color for these lines.

Example: Selecting a green label color and a distinct line width makes bullish divergences easily recognizable on your chart.

R. Bearish Div Label: Default: True

What it is: An option to display labels for regular bearish divergences.

What it does: Enables or disables the visibility of labels that mark regular bearish divergences, where the price makes a higher high while the RSI makes a lower high, indicating a potential downward reversal.

Example: A trader might use this to spot selling opportunities in an uptrend when a bearish divergence suggests the trend may be reversing.

Bearish Label Color, Line Width, and Line Color:

What it is: Settings to customize the appearance of regular bearish divergence labels.

What it does: Allows you to choose the color of the labels, adjust the width of the divergence lines, and select the color for these lines.

Example: Choosing a red label color and a specific line width makes bearish divergences clearly stand out on your chart.

H. Bullish Div Label: Default: False

What it is: An option to display labels for hidden bullish divergences.

What it does: Enables or disables the visibility of labels that mark hidden bullish divergences, where the price makes a higher low while the RSI makes a lower low, indicating potential continuation of an uptrend.

Example: A trader might use this to confirm an existing uptrend when a hidden bullish divergence signals continued buying strength.

Hidden Bullish Label Color, Line Width, and Line Color:

What it is: Settings to customize the appearance of hidden bullish divergence labels.

What it does: Allows you to choose the color of the labels, adjust the width of the divergence lines, and select the color for these lines.

Example: A softer green color with a thinner line width might be chosen to subtly indicate hidden bullish divergences, keeping the chart clean while providing useful information.

H. Bearish Div Label: Default: False

What it is: An option to display labels for hidden bearish divergences.

What it does: Enables or disables the visibility of labels that mark hidden bearish divergences, where the price makes a lower high while the RSI makes a higher high, indicating potential continuation of a downtrend.

Example: A trader might use this to confirm an existing downtrend when a hidden bearish divergence signals continued selling pressure.

Hidden Bearish Label Color, Line Width, and Line Color:

What it is: Settings to customize the appearance of hidden bearish divergence labels.

What it does: Allows you to choose the color of the labels, adjust the width of the divergence lines, and select the color for these lines.

Example: A muted red color with a thinner line width might be selected to indicate hidden bearish divergences without overwhelming the chart.

Divergence Text Size and Color: Default: S (Small)

What it is: Settings to adjust the size and color of text labels for RSI divergences.

What it does: Allows you to customize the size and color of text labels that display the divergence information on the chart.

Example: Choosing a small text size with a bright white color can make divergence labels easily readable without taking up too much space on the chart.

STOCHASTIC DIVERGENCES

Display of Stochastic RSI Divergence Labels:

Display of Stochastic RSI Divergence Settings:

Stochastic RSI Divergence Explanation

Stochastic RSI divergences occur when the Stochastic RSI indicator and price action move in opposite directions, signaling potential trend reversals. These settings allow traders to customize the detection and visual representation of both regular and hidden bullish and bearish divergences in the Stochastic RSI.

Stochastic RSI Divergence Input Settings:

R. Bullish Div Label: Default: True

What it is: An option to display labels for regular bullish divergences in the Stochastic RSI.

What it does: Enables or disables the visibility of labels that mark regular bullish divergences, where the price makes a lower low while the Stochastic RSI makes a higher low, indicating a potential upward reversal.

Example: A trader might use this to spot buying opportunities in a downtrend when a bullish divergence in the Stochastic RSI suggests the trend may be reversing.

Bullish Label Color, Line Width, and Line Color:

What it is: Settings to customize the appearance of regular bullish divergence labels in the Stochastic RSI.

What it does: Allows you to choose the color of the labels, adjust the width of the divergence lines, and select the color for these lines.

Example: Selecting a blue label color and a distinct line width makes bullish divergences in the Stochastic RSI easily recognizable on your chart.

R. Bearish Div Label: Default: True

What it is: An option to display labels for regular bearish divergences in the Stochastic RSI.

What it does: Enables or disables the visibility of labels that mark regular bearish divergences, where the price makes a higher high while the Stochastic RSI makes a lower high, indicating a potential downward reversal.

Example: A trader might use this to spot selling opportunities in an uptrend when a bearish divergence in the Stochastic RSI suggests the trend may be reversing.

Bearish Label Color, Line Width, and Line Color:

What it is: Settings to customize the appearance of regular bearish divergence labels in the Stochastic RSI.

What it does: Allows you to choose the color of the labels, adjust the width of the divergence lines, and select the color for these lines.

Example: Choosing an orange label color and a specific line width makes bearish divergences in the Stochastic RSI clearly stand out on your chart.

H. Bullish Div Label: Default: False

What it is: An option to display labels for hidden bullish divergences in the Stochastic RSI.

What it does: Enables or disables the visibility of labels that mark hidden bullish divergences, where the price makes a higher low while the Stochastic RSI makes a lower low, indicating potential continuation of an uptrend.

Example: A trader might use this to confirm an existing uptrend when a hidden bullish divergence in the Stochastic RSI signals continued buying strength.

Hidden Bullish Label Color, Line Width, and Line Color:

What it is: Settings to customize the appearance of hidden bullish divergence labels in the Stochastic RSI.

What it does: Allows you to choose the color of the labels, adjust the width of the divergence lines, and select the color for these lines.

Example: A softer blue color with a thinner line width might be chosen to subtly indicate hidden bullish divergences, keeping the chart clean while providing useful information.

H. Bearish Div Label: Default: False

What it is: An option to display labels for hidden bearish divergences in the Stochastic RSI.

What it does: Enables or disables the visibility of labels that mark hidden bearish divergences, where the price makes a lower high while the Stochastic RSI makes a higher high, indicating potential continuation of a downtrend.

Example: A trader might use this to confirm an existing downtrend when a hidden bearish divergence in the Stochastic RSI signals continued selling pressure.

Hidden Bearish Label Color, Line Width, and Line Color:

What it is: Settings to customize the appearance of hidden bearish divergence labels in the Stochastic RSI.

What it does: Allows you to choose the color of the labels, adjust the width of the divergence lines, and select the color for these lines.

Example: A muted orange color with a thinner line width might be selected to indicate hidden bearish divergences without overwhelming the chart.

Divergence Text Size and Color: Default: S (Small)

What it is: Settings to adjust the size and color of text labels for Stochastic RSI divergences.

What it does: Allows you to customize the size and color of text labels that display the divergence information on the chart.

Example: Choosing a small text size with a bright white color can make divergence labels easily readable without taking up too much space on the chart.

Alert System:

Custom Alerts for Divergences and Reversals:

What it is: The script includes customizable alert conditions to notify you of detected divergences or potential reversals based on WaveTrend, RSI, and Stochastic RSI.

What it does: Helps you stay informed of key market movements without constantly monitoring the charts, enabling timely decisions.

Example: Setting an alert for regular bearish divergence on the WaveTrend could notify you of a potential sell opportunity as soon as it is detected.

How to Use Alerts:

Set up custom alerts in TradingView based on these conditions to be notified of potential trading opportunities. Alerts are triggered when the indicator detects conditions that match the selected criteria, such as divergences or potential reversals.

By following the detailed guidelines and examples above, you can effectively use and customize this powerful indicator to suit your trading strategy.

For further understanding and customization, refer to the input settings within the script and adjust them to match your trading style and preferences.

How Components Work Together

Synergy and Cross-Validation: The indicator combines multiple layers of analysis to validate trading signals. For example, a WaveTrend buy signal that coincides with a bullish divergence in RSI and positive fast money flow is likely to be more reliable than any single indicator’s signal. This cross-validation reduces the likelihood of false signals and enhances decision-making.

Comprehensive Market Analysis: Each component plays a role in analyzing different aspects of the market. WaveTrend focuses on trend strength, Money Flow indicators assess market sentiment, while RSI and Stochastic RSI offer detailed views of price momentum and potential reversals.

Ideal For

Traders who require a reliable, multifaceted tool for detecting market trends and reversals.

Investors seeking a deeper understanding of market dynamics across different timeframes and conditions, whether in forex, equities, or cryptocurrency markets.

This script is designed to provide a comprehensive tool for technical analysis, combining multiple indicators and divergence detection into one versatile and customizable script. It is especially useful for traders who want to monitor various indicators simultaneously and look for convergence or divergence signals across different technical tools.

Acknowledgements

Special thanks to these amazing creators for inspiration and their creations:

I want to thank these amazing creators for creating there amazing indicators , that inspired me and also gave me a head start by making this indicator! Without their amazing indicators it wouldn't be possible!

vumanchu: VuManChu Cipher B Divergences.

MisterMoTa: RSI + Divergences + Alerts .

DevLucem: Plain Stochastic Divergence.

Note

This indicator is designed to be a powerful tool in your trading arsenal. However , it is essential to backtest and adjust the settings according to your trading strategy before applying it to live trading . If you have any questions or need further assistance, feel free to reach out.

Komut dosyalarını "10年期国债+交易单位+价格" için ara

Volume Insignts AnalyzerDescription:

The Volume Insight Analyzer is an advanced Pine Script designed for traders who want a comprehensive view of volume dynamics on their charts. This script combines multiple volume-based indicators to help identify key trading opportunities, including significant volume days, volume dry-ups, and pocket pivots.

Key Features:

VDU (Volume Dry-Up) Detection: Automatically identifies and marks days when the volume is significantly below its moving average, helping to spot potential breakout or breakdown points. Customizable volume thresholds allow for tailored analysis based on your trading strategy. The Volume Dry-Up label appears when the volume is substantially below its average level and the price is near a key moving average. This condition indicates a period of equilibrium between supply and demand, suggesting a potential low-risk entry point for traders.

Pocket Pivot Analysis using 5 and 10 Length Pocket Pivots: Highlights days with exceptionally high volume compared to recent history, indicating potential pocket pivots. Visual markers on the chart and volume bars color-coded for 5 and 10-day lengths. Pocket pivot points are identified when the volume on a given day exceeds the maximum volume observed over the past several days. Specifically, a 5-day pocket pivot point is marked when today's volume surpasses the highest selling volume of the last 5 days. A cluster of 5-day pocket pivot points within a base is a strong indicator of stock strength. Similarly, a 10-day pocket pivot point following a Volume Dry-Up (VDU) suggests a potential entry opportunity. Moreover, a pre-existing cluster of 5-day pocket pivot points before a 10-day pocket pivot point provides greater conviction in the trade.

Volume Moving Averages: Set different lengths for primary and secondary moving averages to track volume trends over daily, weekly, and monthly timeframes. Options to display moving average lines on the volume chart.

Volume Visualization:

a. Major and Minor Volume Bars: Option to display bars that are either above or below average volume levels. Adjustable settings to show or hide these bars based on user preference.

b. Volume Bar Coloring: Volume bars are color-coded based on significant volume thresholds, including green for bullish signals, red for bearish signals, and orange for volume dry-ups.

Volume Metrics Table: A customizable table that displays real-time volume metrics including Relative Volume (RVOL), Turnover, and the number of high volume days. The table can be oriented horizontally or vertically and styled according to your theme preferences.

Visual Indicators:

a) Volume Dry-Up (VDU) Labels: Clearly marked VDU events with textual annotations on the chart.

b) Bullish and Bearish Arrows: Arrows indicating potential bullish or bearish closes based on volume analysis, enhancing decision-making.

Customization Options:

a) Dark and Light Theme Support: Toggle between dark and light themes to match your chart settings.

b) Adjustable Parameters: Easily configure input settings such as volume thresholds, MA lengths, and table display options to fit your trading style.

How to Use:

Set Parameters: Adjust the script settings such as volume thresholds, moving average lengths, and display preferences according to your analysis needs.

Analyze Volume Patterns: Use the indicators and visual markers provided by the script to identify significant volume patterns and potential trading signals.

Monitor Metrics: Refer to the volume metrics table for a quick overview of key volume-related statistics and trends.

Make Informed Decisions: Utilize the visual cues and volume data provided by the script to enhance your trading strategy and make more informed decisions.

Disclaimer:

This script is for informational purposes only and should not be considered as trading advice. Use it in conjunction with other analysis tools and consult with a financial advisor if needed. Trading involves risk, and past performance does not guarantee future results.

MA DifferenceThe MA Difference indicator shows 3 histograms representing differences in moving averages between a base MA (10) and 3 MA's: short (20), medium (50), and long (200). It also shows an exponentially weighted trend line which can indicate breakout opportunities, has alerts on all base <-> X crossovers, and shows potential consolidation zones where MA differences are below a user-defined tolerance.

The suggested way to use this indicator is to place a trade when the trend line is above the histogram (and filling the space between them). This indicates that the current MA values are significantly above or below the expected range and that prices are in the midst of breaking out. You may also consult the consolidation zones to eliminate false breakouts and momentary changes in trend. You may also consult the various short, medium, and long crossovers and crossunders to time entries and exits accordingly.

Histograms

The 3 histograms represent the differences between:

Base MA (10) and Short MA (20)

Base MA (10) and Medium MA (50)

Base MA (10) and Long MA (200)

All 4 moving average values can be configured in the indicator's settings. Consistency in direction and color of the histogram indicates a consistent trend across the various moving averages.

Trend Line

The trend line is an exponentially weighted average of the 3 moving averages, scaled by a factor configurable in the settings. When using the trend line, shading will be applied to the difference between the extremes of the histogram and the trend line to indicate that the chart is in a "breakout zone" and is beyond the normal, gradual sway of price action.

Crossovers/Crossunders

You may optionally turn on crossovers and crossunders in the indicator's settings to display when a short, medium, or long crossover occurs against the base moving average. Likewise, alerts are available for each crossover and crossunder for each of the 3 moving average convergences.

Consolidation Zones

Consolidation zones, as well as a line representing the current amount of consolidation, can also be optionally drawn on the chart. These indicate when a security is likely in consolidation, according to the spread of various MA values.

LBR-S310ROC @shrilssOriginally made by Linda Raschke, The S310ROC Indicator combines the Rate of Change (ROC) indicator with the 3-10 Oscillator (Modified MACD) and plots to capture rapid price movements and gauge market momentum.

- Rate of Change (ROC): This component of the indicator measures the percentage change in price over a specified short interval, which can be set by the user (default is 2 days). It is calculated by subtracting the closing price from 'X' days ago from the current close.

- 3-10 Oscillator (MACD; 3,10,16): This is a specialized version of the Moving Average Convergence Divergence (MACD) but uses simple moving averages instead of exponential. Using a fast moving average of 3 days and a slow moving average of 10 days with a smoothing period of 16.

- ROC Dots: A great feature based on the oscillator's readings. Dots are displayed directly on the oscillator or the price chart to provide visual momentum cues:

- Aqua Dots: Appear when all lines (ROC, MACD, Slowline) are sloping downwards, indicating bearish momentum and potentially signaling a sell opportunity.

- White Dots: Appear when all lines are sloping upwards, suggesting bullish momentum and possibly a buy signal.

Interest Rate DifferentialInterest Rate Differential Indicator

Description:

This Pine Script indicator displays the interest rate spread between two countries, illustrating the differential in 10-year bond yields (or other maturities on the curve). By default, it compares the 10-year bond yield of Germany (DE10Y) with that of the United States (US10Y), for EUR/USD pair analysis. Change the yields to compare other pairs. The spread between the rates of the curve of two countries provides traders and analysts with insights into the carry cost and interest rate dynamics between these economies. The indicator is crucial for assessing the relative strength of the bond market and the economic outlook (including inflation expectations and risk premium) of the selected countries, aiding in trade decisions and market analysis.

Tradução para Português Brasileiro

Título: Indicador de Diferencial de Juros (DE10Y-US10Y)

Descrição:

Este indicador em Pine Script exibe o spread de juros entre dois países, mostrando o diferencial de yields dos títulos de 10 anos (ou de outro vencimento na curva). Por padrão, ele compara o rendimento do título de 10 anos da Alemanha (DE10Y) com o dos Estados Unidos (US10Y), para análise do par EUR/USD. Mude os yields para outros pares. O spread entre as taxas do curva entre 2 países proporciona aos traders e analistas uma visão do custo de carrego e da dinâmica das taxas de juros entre estas economias. O indicador é fundamental para avaliar a força relativa do mercado de títulos e a perspectiva econômica (assim como expectativa de inflação e prêmio de risco) entre os países dos yields selecionados, auxiliando em decisões de trade e análise de mercado.

Volume Spike IndicatorHello dear traders,

Today we're discussing an indicator I've coded: the Volume Spike Indicator (VSI).

The indicator isn't a groundbreaking invention and certainly not a novelty. Nevertheless, I haven't seen this version of the indicator on TradingView before, so I'd like to introduce it.

1. The Origin of the Idea:

We're all familiar with volume charts: A volume chart visually represents the trading activity for a specific asset over a certain period, indicating the total number of shares or contracts traded.

We also know that volume spikes can significantly impact the market. A volume spike represents an extreme anomaly, a day, week, or month with an extraordinary amount of trading. However, recognizing these spikes in practice isn't always straightforward. What constitutes high volume? How do we define and identify it? The answers to these questions aren't easy.

It's commonly said that a volume spike could be identified if the volume is 25% more than the average of the two weeks prior, but how do you measure this 25%? It's not always easy to calculate, especially in real-time.

This challenge led me to develop the concept into an indicator.

How Does It Work?

Imagine being able to "feel" the market's energy like a surfer feels the ocean. The VSI does something similar by examining trading volume and comparing it to what has been typical over the past few weeks. Here's a quick look at the magic behind it:

Step 1: Establishing the Baseline: We start by establishing a baseline, i.e., the average trading volume over a given period. Let's use the last 10 days as the default setting. We choose 10 days because, in the traditional stock market, 10 days represent two weeks if you subtract weekends. This gives us a fixed line to compare against.

Step 2: Recognizing Peaks: Next, we look for days when the trading volume significantly exceeds this average. The size of the jump is where you have a say. You can set a threshold, such as 25%, to define what you consider a volume spike.

Step 3: The Calculation: This is where the math comes into play. We calculate the percentage change in today's volume compared to the average volume of the last 10 days. For example, if today's volume is 30% above the average and you've set your threshold at 25%, the VSI will recognize this as a spike.

Step 4: Visual Cue: These spikes are then plotted on a graph, with each spike represented as a bar. The height of the bar indicates the spike's percentage size, so you can see at a glance how significant a spike is.

Step 5: Intuitive Color Coding: For quick analysis, the VSI employs a color-coding system. Exceptionally high peaks, such as those exceeding a 100% increase, are highlighted in blue to emphasize their importance. Other peaks are shown in red, creating a visual hierarchy for quick volume data interpretation.

Why This Matters:

Identifying these spikes can help pinpoint the beginning or end of a trend. The idea is that when trading peaks at a certain level, there might be no more buyers or sellers willing to engage at that price level. Volume peaks, and a reversal is likely imminent. It's a simple yet effective concept. Therefore, it's crucial to use this indicator in the context of the trend, as not every spike carries the same significance.

Customizable:

The beauty of the VSI lies in its flexibility. Trading futures? You might want to adjust the averaging period to 14 days to better suit your market. You have full control over the settings to tailor them to your trading style.

Interpreting the Figures:

A positive percentage indicates a volume spike above the average – the higher the percentage, the more significant the spike.

If the percentage exceeds a certain threshold (which you can set, e.g., 25%), it signals a volume spike, indicating increased market activity that could precede significant price movement.

What makes the VSI genuinely adaptable is your ability to tweak the parameters to suit your needs.

Are you trading in a volatile market? Extend the SMA period to smooth out the noise. Trading in a 24-hour market? Adjust the length of your SMA. Seeking finer details? Shorten it. The VSI is yours to adapt to your trading strategy.

---------------------------------------------------------------------------------------------------------------------

As we wrap up this introduction to the Volume Spike Indicator, I hope you're as excited about its potential as I am. This tool, born out of curiosity and a desire for clarity in the vast ocean of market data, is designed to be your ally in navigating the waves of trading activity.

Remember, the true power of the VSI lies not just in its ability to highlight significant volume spikes, but in its adaptability to your unique trading style and needs. Whether you're charting courses through the tumultuous seas of day trading or navigating the broader currents of long-term investments, the VSI is here to offer insights and guidance.

I encourage you to experiment with it, customize it, and see how it can enhance your trading strategy. And as you do, remember that every tool, no matter how powerful, is just one piece of the puzzle. Combine the VSI with your knowledge, experience, and intuition to make informed and strategic trading decisions.

Thank you for taking the time to explore the Volume Spike Indicator with me.

Best Regards,

Karim Subhieh

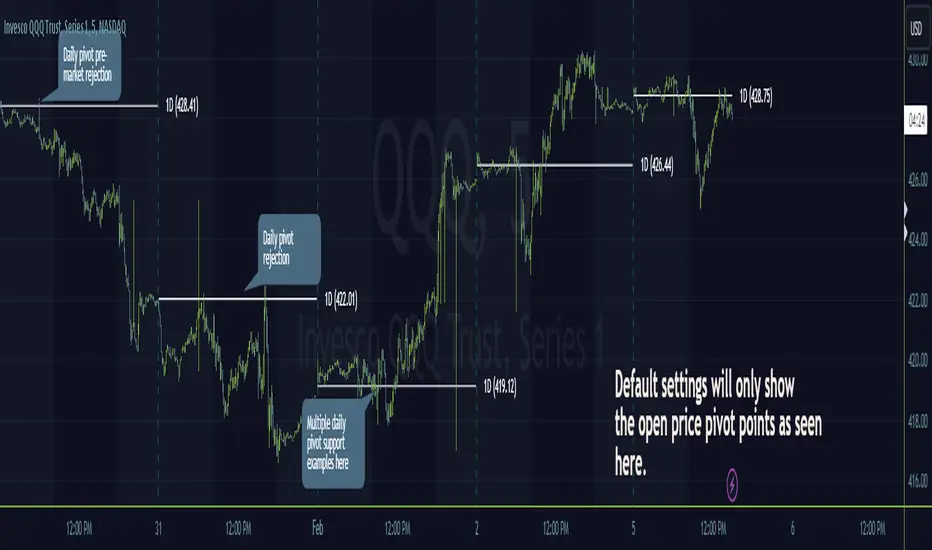

Timeframe PivotsUse this tool to plot open prices from any timeframe as a pivot level with the option to go advanced and turn on extensions (instructions below), which review the relationship between previous and current open prices to build range extensions up to six levels wide.

Please be aware extensions, nor vwap are not enabled by default! It is up to the user to determine how they wish to setup this indicator. Please read the full description for utilizing this indicator so that it's well known the complete feature set and understanding of how to enable additional plots, complete instruction is provided for all users below.

Default configuration example:

To enable extensions the user must open the indicator configuration by clicking the gear icon for "Timeframe Pivots", depending on screen resolution scrolling with mouse may need to occur in order to find the section labeled "Extensions", use the mouse or equivalent human interface device to check the checkbox to the right of the color plots and line type drop down.

Extensions enabled example:

Timeframe Selection

Timeframes available to the indicator are any timeframe the platform makes available to the user by default, or also if the TradingView user has higher tier plan to create custom timeframes - those should be available as well. To adjust timeframe the user must open the indicator configuration by clicking the gear icon for "Timeframe Pivots", depending on screen resolution scrolling with mouse may need to occur in order to find the input labeled "Timeframe", use the mouse or equivalent human interface device select the drop down and select timeframe suitable to users application.

How the extension width and extensions are calculated:

The exact process takes the new timeframe change open price calculates the difference between prior open, once that has been completed then it's divided in half to build extensions.

Code example:

Extension Width = (Open - Open ) / 2

How the extensions are calculated:

// +1 for positive extension, -1 for negative extension

(Extension Width * (Configured Multiplier * 1)) + Pivot Open Price

+1 Extension:

$5 * (1.0 * 1) + $400 = $405

-1 Extension:

$5 * (1.0 * -1) + $400 = $395

So it should be established how each projected extension, either positive or negative, is created.

Range bound market detection and notes:

One note regarding the ranges, sometimes the open prices of each period can be close in proximity to their predecessor, there's not enough range to build meaningful projections. In these situations this means the market is most likely range bound and prior range data is utilized to continue providing guidance. This addresses an issue with other pivot indicators that will instead blindly follow price and present useless pivot ranges.

It does this through detection of average half range widths, the last 14 ranges to be exact, if the current, (open - open / 2), half range width is smaller than the average, prior half range width will be used.

Code example:

// assume past half range widths are 10, 8, 9, 5, 14, 7, 7, 9, 10, 10, 4, 7, 7, 8

float v_halfRangeWidthToUseForExtensions = na

v_priorHalfRangeWidth = 10

v_avgHalfRangeWidth = 8.2 // past range widths sum = 115 / 14

v_newHalfRangeWidthToUseForExtensions = 2 // new open - open is tiny compared to avg

if v_newHalfRangeWidthToUseForExtensions < v_avgHalfRangeWidth

// replace new half range width with previous one

v_newHalfRangeWidthToUseForExtensions := v_priorHalfRangeWidth

In the code example above if the new half range width was above or equal to the rolling average, no adjustment would be made by the indicator.

VWAP

Additional feature of showing vwap, anchored to the same timeframe as the pivot, provides a trend and volume analysis within the confines of the pivots range.

The user must open the indicator configuration by clicking the gear icon for "Timeframe Pivots", scroll using mouse to the "VWAP" section and click the checkbox next to the "Source" field, past the color plots. They are not enabled by default!

The user can also add the bands for VWAP by clicking the checkbox next to the "Bands" field, past the color plots. They are not enabled by default!

VWAP calculations begin from open price of new timeframe change, then afterwards the "Source" set is utilized, the default is HLC3 which is standard for VWAP indicators.

Multiple Timeframe Analysis (MTFA)

It's simple to create a unique combination of favored timeframes for multiple timeframe analysis, consider daily, weekly and monthly combined analysis for powerful indications of market sentiment and directional bias.

Example MTFA demonstration:

Why was this created?

I created this while investigating the efficacy of open price ranges, it became apparent that these pivot ranges are some of the more price respecting pivots I've ever observed. I also grew tired of lack of price adherence to other pivot indicators widely available.

There exists a relationship between each timeframes open price in comparison to prior open price, if the market is willing to navigate to a prior lower open price from higher open price, it could be perceived as bearish and the extensions (if enabled as instructed above), could be suitable range based projections for future price movements.

Example comparison:

As can be seen, and there are many examples, where Timeframe Pivots provides more discreet levels and potential explanations for price movements.

Qullamaggie ADR and Volatility and Price Change IndicatorElevate your trading strategy with Qullamaggie ADR, a dynamic indicator inspired by the Kristjan Qullamaggie trading approach. Gain a deeper understanding of market dynamics, daily price movements, and potential turning points.

Key Features:

Qullamaggie ADR: Assess market volatility through the QullaADR, offering customizable time intervals (5, 10, 15, 20 days) to adapt to various trading styles.

Today's Change: Monitor price changes relative to the low of the current trading day, providing valuable intraday insights.

PrevDay price differentials from the previous day's low, aiding in the identification of potential trend reversals.

Track the percentage change from the opening price, offering a snapshot of intraday market sentiment.

Percent from 10-day SMA: Visualize the percentage difference between the closing price and a 10-day Simple Moving Average (SMA), a key trend-following indicator.

Usage:

Utilize QullaADR to set realistic profit targets and stop-loss levels based on current market conditions.

Identify potential trend shifts by observing changes from the previous day's low with Today's QullaChange.

Incorporate QullaPercent from 10-day SMA for trend confirmation and well-informed trading decisions.

Strategy Inspiration:

QullaADR draws inspiration from the Kristjan Qullamaggie trading strategy, aiming to complement your trading toolkit and enhance decision-making.

Disclaimer:

Trading involves risk, and past performance is not indicative of future results. Use this indicator as a supplementary tool within a comprehensive trading strategy.

Version: 1.0

Stock WatchOverview

Watch list are very common in trading, but most of them simply provide the means of tracking a list of symbols and their current price. Then, you click through the list and perform some additional analysis individually from a chart setup. What this indicator is designed to do is provide a watch list that employs a high/low price range analysis in a table view across multiple time ranges for a much faster analysis of the symbols you are watching.

Discussion

The concept of this Stock Watch indicator is best understood when you think in terms of a 52 Week Range indication on many financial web sites. Taken a given symbol, what is the high and the low over a 52 week range and then determine where current price is within that range from a percentage perspective between 0% and 100%.

With this concept in mind, let's see how this Stock Watch indicator is meant to benefit.

There are four different H/L ranges relative to the chart's setting and a Scope property. Let's use a three month (3M) chart as our example and set the indicator's Scope = 4. A 3M chart provides three months of data in a single candle, now when we set the Scope = 4 we are stating that 1X is going to look over four candles for the high/low range.

The Scope property is used to determine how many candles it is to scan to determine the high/low range for the corresponding 1X, 3X, 5X and 10X periods. This is how different time ranges are put into perspective. Using a 3M chart with Scope = 4 would represent the following time windows:

- 1X = 3M * 4 is a 12 Months or 1 Year High/Low Range

- 3X = 3M * 4 * 3 is a 36 Months or 3 Years High/Low Range

- 5X = 3M * 4 * 5 is a 60 Months or 5 Years High/Low Range

- 10X = 3M * 4 * 10 is a 120 Months or 10 Years High/Low Range.

With these calculations, the indicator then determines where current price is within each of these High/Low ranges from a percentage perspective between 0% and 100%.

Once the 0% to 100% value is calculated, it then will shade the value according to a color gradient from red to green (or any other two colors you set the indictor to). This color shading really helps to interpret current price quickly.

The greater power to this range and color shading comes when you are able to see where price is according to price history across the multiple time windows. In this example, there is quick analysis across 1 Year, 3 Year, 5 Year and 10 Year windows.

Now let's further improve this quick analysis over 15 different stocks for which the indicator allows you to watch up to at any one time.

For value traders this is huge, because we're always looking for the bargains and we wait for price to be in the value range. Using this indicator helps to instantly see if price has entered a value range before we decide to do further analysis with other charting and fundamental tools.

The Code

The heart of all this is really very simple as you can see in the following code snippet. We're simply looking for the highest high and lowest low across the different scopes and calculating the percentage of the range where current price is for each symbol being watched.

scope = baseScope

watch1X = math.round(((watchClose - ta.lowest(watchLow, scope)) / (ta.highest(watchHigh, scope) - ta.lowest(watchLow, scope))) * 100, 0)

table.cell(tblWatch, columnId, 2, str.format("{0, number, #}%", watch1X), text_size = size.small, text_color = colorText, bgcolor = getBackColor(watch1X))

//3X Lookback

scope := baseScope * 3

watch3X = math.round(((watchClose - ta.lowest(watchLow, scope)) / (ta.highest(watchHigh, scope) - ta.lowest(watchLow, scope))) * 100, 0)

table.cell(tblWatch, columnId, 3, str.format("{0, number, #}%", watch3X), text_size = size.small, text_color = colorText, bgcolor = getBackColor(watch3X))

Conclusion

The example I've laid out here are for large time windows, because I'm a long term investor. However, keep in mind that this can work on any chart setting, you just need to remember that your chart's time period and scope work together to determine what 1X, 3X, 5X and 10X represent.

Let me try and give you one last scenario on this. Consider your chart is set for a 60 minute chart, meaning each candle represents 60 minutes of time and you set the Stock Watch indicator to a scope = 4. These settings would now represent the following and you would be watching up to 15 different stocks across these windows at one time.

1X = 60 minutes * 4 is 240 minutes or 4 hours of time.

3X = 60 minutes * 4 * 3 = 720 minutes or 12 hours of time.

5X = 60 minutes * 4 * 5 = 1200 minutes or 20 hours of time.

10X = 60 minutes * 4 * 10 = 2400 minutes or 40 hours of time.

I hope you find value in my contribution to the cause of trading, and if you have any comments or critiques, I would love to here from you in the comments.

Backtest Strategy Optimizer Adapter - Supertrend ExampleSample Code

This is a sample code for my Backtest Strategy Optimizer Adapter library.

You can find the library at:

Backtest Strategy Optimizer Tester

With this indicator, you will be able to run one or multiple backtests with different variables (combinations). For example, you can run dozens of backtests of Supertrend at once with an increment factor of 0.1, or whatever you prefer. This way, you can easily grab the most profitable settings and use them in your strategy. The chart above shows different color plots, each indicating a profit backtest equal to tradingview backtesting system. This code uses my backtest library, available in my profile.

Below the code you should edit yourself

You can use ChatGPT or write a python script to autogenerate code for you.

// #################################################################

// # ENTRIES AND EXITS

// #################################################################

// You can use the link and code in the description to create

// your code for the desired number of entries / exits.

// #################################################################

// AUTO GENERATED CODE

// ▼▼▼▼▼▼▼▼▼▼▼▼▼▼▼▼▼▼▼▼▼▼▼▼▼▼▼▼▼▼▼▼▼▼▼▼▼▼▼▼▼▼▼▼▼▼▼▼▼▼▼▼▼▼▼▼▼▼▼▼▼▼▼▼▼

= ti.supertrend(10, 0.1)

= ti.supertrend(10, 0.2)

= ti.supertrend(10, 0.3)

= ti.supertrend(10, 0.4)

// 005 etc...

pnl_001 = backtest.profit(date_start, date_end, entry_001, exit_001)

pnl_002 = backtest.profit(date_start, date_end, entry_002, exit_002)

pnl_003 = backtest.profit(date_start, date_end, entry_003, exit_003)

pnl_004 = backtest.profit(date_start, date_end, entry_004, exit_004)

plot(pnl_001, title='0.1', color=backtest.color(001))

plot(pnl_002, title='0.2', color=backtest.color(002))

plot(pnl_003, title='0.3', color=backtest.color(003))

plot(pnl_004, title='0.4', color=backtest.color(004))

// Make sure you set the correct array size.

// The amount of tests + 1 (e.g. 4 tests you set it to 5)

var results_list = array.new_string(5)

if (ta.change(pnl_001))

array.set(results_list, 0, str.tostring(pnl_001) + '|0.1')

if (ta.change(pnl_002))

array.set(results_list, 1, str.tostring(pnl_002) + '|0.2')

if (ta.change(pnl_003))

array.set(results_list, 2, str.tostring(pnl_003) + '|0.3')

if (ta.change(pnl_004))

array.set(results_list, 3, str.tostring(pnl_004) + '|0.4')

// ▲▲▲▲▲▲▲▲▲▲▲▲▲▲▲▲▲▲▲▲▲▲▲▲▲▲▲▲▲▲▲▲▲▲▲▲▲▲▲▲▲▲▲▲▲▲▲▲▲▲▲▲▲▲▲▲▲▲▲▲▲▲▲▲▲

// AUTO GENERATED CODE

// #################################################################

Volume Profile with a few polylinesThe base of "Volume Profile with a few polylines" is another script of mine, Volume Profile (Maps) .

The structure of maps is used to gather the data. However, the drawings is done with polylines.

This enables coders to draw an entire volume profile with just a few polylines, while the range is broader.

This results in the benefit to draw more "lines" than with line.new() / box.new() alone.

🔶 CONCEPTS

🔹 Polylines

polyline.new creates a new polyline instance and displays it on the chart, sequentially connecting all of the points in the `points` array with line segments.

The segments in the drawing can be straight or curved depending on the `curved` parameter.

In this script, points are connected, starting from the bottom. The created line moves up until there is a price level where a volume value needs to be displayed,

at which the line goes to the left to the concerning volume value, coming back at the same price level until the line returns to its initial x-axis,

after which the line will continue to rise until all values are displayed.

A polyline can contain maximum 10000 points (10K).

Since the line has to go back and forth, each price/volume line takes 3 points.

In the case that 20K bars all have a different price, we would need 60K points, or just 6 polylines. A maximum of 100 polylines can be displayed.

The 3 highest volume values are displayed with line.new(), each with their own colour.

🔹 Maps

A map object is a collection that consists of key - value pairs

Each key is unique and can only appear once. When adding a new value with a key that the map already contains, that value replaces the old value associated with the key .

You can change the value of a particular key though, for example adding volume (value) at the same price (key), the latter technique is used in this script.

Volume is added to the map, associated with a particular price (default close, can be set at high, low, open,...)

When the map already contains the same price (key), the value (volume) is added to the existing volume at the associated price.

A map can contain maximum 50K values, which is more than enough to hold 20K bars (Basic 5K - Premium plan 20K), so the whole history can be put into a map.

🔹 Rounding function

This publication contains 2 round functions, which can be used to widen the Volume Profile

Round

• "Round" set at zero -> nothing changes to the source number

• "Round" set below zero -> x digit(s) after the decimal point, starting from the right side, and rounded.

• "Round" set above zero -> x digit(s) before the decimal point, starting from the right side, and rounded.

Example: 123456.789

0->123456.789

1->123456.79

2->123456.8