Cardwell RSI by TQ📌 Cardwell RSI – Enhanced Relative Strength Index

This indicator is based on Andrew Cardwell’s RSI methodology , extending the classic RSI with tools to better identify bullish/bearish ranges and trend dynamics.

In uptrends, RSI tends to hold between 40–80 (Cardwell bullish range).

In downtrends, RSI tends to stay between 20–60 (Cardwell bearish range).

Key Features :

Standard RSI with configurable length & source

Fast (9) & Slow (45) RSI Moving Averages (toggleable)

Cardwell Core Levels (80 / 60 / 40 / 20) – enabled by default

Base Bands (70 / 50 / 30) in dotted style

Optional custom levels (up to 3)

Alerts for MA crosses and level crosses

Data Window metrics: RSI vs Fast/Slow MA differences

How to Use :

Monitor RSI behavior inside Cardwell’s bullish (40–80) and bearish (20–60) ranges

Watch RSI crossovers with Fast (9) and Slow (45) MAs to confirm momentum or trend shifts

Use levels and alerts as confluence with your trading strategy

Default Settings :

RSI Length: 14

MA Type: WMA

Fast MA: 9 (hidden by default)

Slow MA: 45 (hidden by default)

Cardwell Levels (80/60/40/20): ON

Base Bands (70/50/30): ON

"黄金近20年走势" için komut dosyalarını ara

ADX MTF mura visionOverview

ADX MTF — mura vision measures trend strength and visualizes a higher-timeframe (HTF) ADX on any chart. The current-TF ADX is drawn as a line; the HTF ADX is rendered as “step” segments to reflect closed HTF bars without repainting. Optional soft fills highlight the 20–25 (trend forming) and 40–50 (strong trend) zones.

How it works

ADX (current TF) : Classic Wilder formulation using DI components and RMA smoothing.

HTF ADX : Requested via request.security(..., lookahead_off, gaps_off).

When a new HTF bar opens, the previous value is frozen as a horizontal segment.

The current HTF bar is shown as a live moving segment.

This staircase look is expected on lower timeframes.

Auto timeframe mapping

If “Auto” is selected, the HTF is derived from the chart TF:

<30m → 60m, 30–<240m → 240m, 240m–<1D → 1D, 1D → 1W, 1W/2W → 1M, ≥1M → same.

Inputs

DI Length and ADX Smoothing — core ADX parameters.

Higher Time Frame — Auto or a fixed TF.

Line colors/widths for current ADX and HTF ADX.

Fill zone 20–25 and Fill zone 40–50 — optional light background fills.

Number of HTF ADX Bars — limits stored HTF segments to control chart load.

Reading the indicator

ADX < 20: typically range-bound conditions; trend setups require extra caution.

20–25: trend emergence; breakouts and continuation structures gain validity.

40–50: strong trend; favor continuation and manage with trailing stops.

>60 and turning down: possible trend exhaustion or transition toward range.

Note: ADX measures strength, not direction. Combine with your directional filter (e.g., price vs. MA, +DI/−DI, structure/levels).

Non-repainting behavior

HTF values use lookahead_off; closed HTF bars are never revised.

The only moving piece is the live segment for the current HTF bar.

Best practices

Use HTF ADX as a regime filter; time entries with the current-TF ADX rising through your threshold.

Pair with ATR-based stops and a MA/structure filter for direction.

Consider higher thresholds on highly volatile altcoins.

Performance notes

The script draws line segments for HTF bars. If your chart becomes heavy, reduce “Number of HTF ADX Bars.”

Disclaimer

This script is for educational purposes only and does not constitute financial advice. Trading involves risk.

EMA/VWAP SuiteEMA/VWAP Suite

Overview

The EMA/VWAP Suite is a versatile and customizable Pine Script indicator designed for traders who want to combine Exponential Moving Averages (EMAs) and Volume Weighted Average Prices (VWAPs) in a single, powerful tool. It overlays up to eight EMAs and six VWAPs (three anchored, three rolling) on the chart, each with percentage difference labels to show how far the current price is from these key levels. This indicator is perfect for technical analysis, supporting strategies like trend following, mean reversion, and VWAP-based trading.

By default, the indicator displays eight EMAs and a session-anchored VWAP (AVWAP 1, in fuchsia) with their respective percentage difference labels, keeping the chart clean yet informative. Other VWAPs and their bands are disabled by default but can be enabled and customized as needed. The suite is designed to minimize clutter while providing maximum flexibility for traders.

Features

- Eight Customizable EMAs: Plot up to eight EMAs with user-defined lengths (default: 3, 9, 19, 38, 50, 65, 100, 200), each with a unique color for easy identification.

- EMA Percentage Difference Labels: Show the percentage difference between the current price and each EMA, displayed only for visible EMAs when enabled.

- Three Anchored VWAPs: Plot VWAPs anchored to the start of a session, week, or month, with customizable source, offset, and band multipliers. AVWAP 1 (session-anchored, fuchsia) is enabled by default.

- Three Rolling VWAPs: Plot VWAPs calculated over fixed periods (default: 20, 50, 100), with customizable source, offset, and band multipliers.

- VWAP Bands: Optional upper and lower bands for each VWAP, based on standard deviation with user-defined multipliers.

- VWAP Percentage Difference Labels: Display the percentage difference between the current price and each VWAP, shown only for visible VWAPs. Enabled by default to show the AVWAP 1 label.

- Customizable Colors: Each VWAP has a user-defined color via input settings, with labels matching the VWAP line colors (e.g., AVWAP 1 defaults to fuchsia).

Flexible Display Options: Toggle individual EMAs, VWAPs, bands, and labels on or off to reduce chart clutter.

Settings

The indicator is organized into intuitive setting groups:

EMA Settings

Show EMA 1–8 : Toggle each EMA on or off (default: all enabled).

EMA 1–8 Length : Set the period for each EMA (default: 3, 9, 19, 38, 50, 65, 100, 200).

Show EMA % Difference Labels : Enable/disable percentage difference labels for all EMAs (default: enabled).

EMA Label Font Size (8–20) : Adjust the font size for EMA labels (default: 10, mapped to “tiny”).

Anchored VWAP 1–3 Settings

Show AVWAP 1–3 : Toggle each anchored VWAP on or off (default: AVWAP 1 enabled, others disabled).

AVWAP 1–3 Color : Set the color for each VWAP line and its label (default: fuchsia for AVWAP 1, purple for AVWAP 2, teal for AVWAP 3).

AVWAP 1–3 Anchor : Choose the anchor period (“Session,” “Week,” “Month”; default: Session for AVWAP 1, Week for AVWAP 2, Month for AVWAP 3).

AVWAP 1–3 Source : Select the price source (default: hlc3).

AVWAP 1–3 Offset : Set the horizontal offset for the VWAP line (default: 0).

Show AVWAP 1–3 Bands : Toggle upper/lower bands (default: disabled).

AVWAP 1–3 Band Multiplier : Adjust the standard deviation multiplier for bands (default: 1.0).

Rolling VWAP 1–3 Settings

Show RVWAP 1–3 : Toggle each rolling VWAP on or off (default: disabled).

RVWAP 1–3 Color : Set the color for each VWAP line and its label (default: navy for RVWAP 1, maroon for RVWAP 2, fuchsia for RVWAP 3).

RVWAP 1–3 Period Length : Set the period for the rolling VWAP (default: 20, 50, 100).

RVWAP 1–3 Source : Select the price source (default: hlc3).

RVWAP 1–3 Offset : Set the horizontal offset (default: 0).

Show RVWAP 1–3 Bands : Toggle upper/lower bands (default: disabled).

RVWAP 1–3 Band Multiplier : Adjust the standard deviation multiplier for bands (default: 1.0).

VWAP Label Settings

Show VWAP % Difference Labels : Enable/disable percentage difference labels for all VWAPs (default: enabled, showing AVWAP 1 label).

VWAP Label Font Size (8–20) : Adjust the font size for VWAP labels (default: 10, mapped to “tiny”).

How It Works

EMAs : Calculated using ta.ema(close, length) for each user-defined period. Percentage differences are computed as ((close - ema) / close) * 100 and displayed as labels for visible EMAs when show_ema_labels is enabled.

Anchored VWAPs : Calculated using ta.vwap(source, anchor, 1), where the anchor is determined by the selected timeframe (Session, Week, or Month). Bands are computed using the standard deviation from ta.vwap.

Rolling VWAPs : Calculated using ta.vwap(source, length), with bands based on ta.stdev(source, length).

Labels : Updated on each new bar (ta.barssince(ta.change(time) != 0) == 0) to show percentage differences. Labels are only displayed for visible EMAs/VWAPs to avoid clutter.

Color Matching: VWAP labels use the same color as their corresponding VWAP lines, set via input settings (e.g., avwap1_color for AVWAP 1).

Example Use Cases

- Trend Following: Use longer EMAs (e.g., 100, 200) to identify trends and shorter EMAs (e.g., 3, 9) for entry/exit signals.

- Mean Reversion: Monitor percentage difference labels to spot overbought/oversold conditions relative to EMAs or VWAPs.

- VWAP Trading: Use the default session-anchored AVWAP 1 for intraday trading, adding weekly/monthly VWAPs or rolling VWAPs for broader context.

- Intraday Analysis: Leverage the session-anchored AVWAP 1 (enabled by default) for day trading, with bands as support/resistance zones.

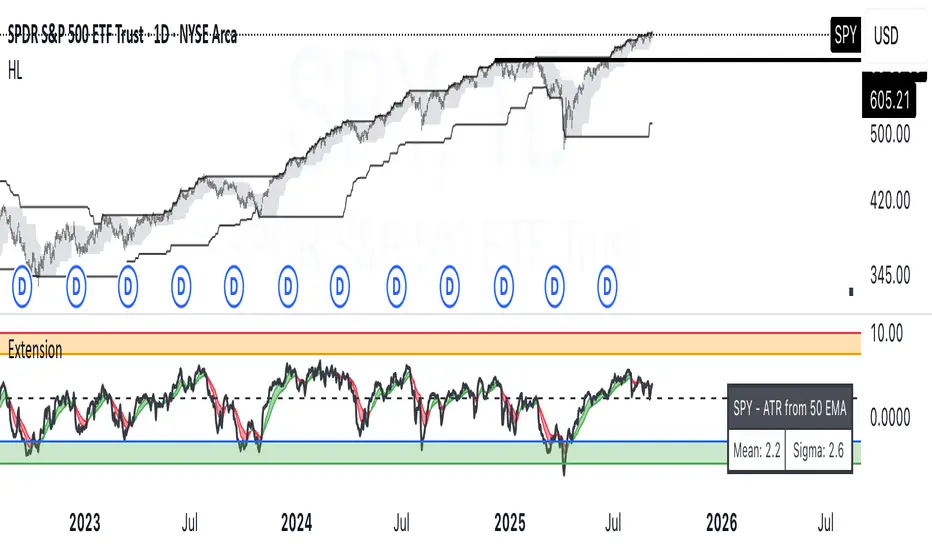

ATR Extension from Moving Average, with Robust Sigma Bands

# ATR Extension from Moving Average, with Robust Sigma Bands

**What it does**

This indicator measures how far price is from a selected moving average, expressed in **ATR multiples**, then overlays **robust sigma bands** around the long run central tendency of that extension. Positive values mean price is extended above the MA, negative values mean price is extended below the MA. The signal adapts to volatility through ATR, which makes comparisons consistent across symbols and regimes.

**Why it can help**

* Normalizes distance to an MA by ATR, which controls for changing volatility

* Uses the **bar’s extreme** against the MA, not just the close, so it captures true stretch

* Computes a **median** and **standard deviation** of the extension over a multi-year window, which yields simple, intuitive bands for trend and mean-reversion decisions

---

## Inputs

* **MA length**: default 50, options 200, 64, 50, 20, 9, 4, 3

* **MA timeframe**: Daily or Weekly. The MA is computed on the chosen higher timeframe through `request.security`.

* **MA type**: EMA or SMA

* **Years lookback**: 1 to 10 years, default 5. This sets the sample for the median and sigma calculation, `years * 365` bars.

* **Line width**: visual width of the plotted extension series

* **Table**: optional on-chart table that displays the current long run **median** and **sigma** of the extension, with selectable text size

**Fixed parameters in this release**

* **ATR length**: 20 on the daily timeframe

* **ATR type**: classic ATR. ADR percent is not enabled in this version.

---

## Plots and colors

* **Main plot**: “Extension from 50d EMA” by default. Value is in **ATR multiples**.

* **Reference lines**:

* `median` line, black dashed

* +2σ orange, +3σ red

* −2σ blue, −3σ green

---

## How it is calculated

1. **Moving average** on the selected higher timeframe: EMA or SMA of `close`.

2. **Extreme-based distance** from MA, as a percent of price:

* If `close > MA`, use `(high − MA) / close * 100`

* Else, use `(low − MA) / close * 100`

3. **ATR percent** on the daily timeframe: `ATR(20) / close * 100`

4. **ATR multiples**: extension percent divided by ATR percent

5. **Robust center and spread** over the chosen lookback window:

* Center: **median** of the ATR-multiple series

* Spread: **standard deviation** of that series

* Bands: center ± 1σ, 2σ, 3σ, with 2σ and 3σ drawn

This design yields an intuitive unit scale. A value of **+2.0** means price is about 2 ATR above the selected MA by the most stretched side of the current bar. A value of **−3.0** means roughly 3 ATR below.

---

## Practical use

* **Trend continuation**

* Sustained readings near or above **+1σ** together with a rising MA often signal healthy momentum.

* **Mean reversion**

* Spikes into **±2σ** or **±3σ** can identify stretched conditions for fade setups in range or late-trend environments.

* **Regime awareness**

* The **median** moves slowly. When median drifts positive for many months, the market spends more time extended above the MA, which often marks bullish regimes. The opposite applies in bearish regimes.

**Notes**

* The MA can be set to Weekly while ATR remains Daily. This is deliberate, it keeps the normalization stable for most symbols.

* On very short intraday charts, the extension remains meaningful since it references the session’s extreme against a higher-timeframe MA and a daily ATR.

* Symbols with short histories may not fill the lookback window. Bands will adapt as data accrues.

---

## Table overlay

Enable **Table → Show** to see:

* “ATR from \”

* Current **median** and **sigma** of the extension series for your lookback

---

## Recommended settings

* **Swing equities**: 50 EMA on Daily, 5 to 7 years

* **Index trend work**: 200 EMA on Daily, 10 years

* **Position trading**: 20 or 50 EMA on Weekly MA, 5 to 10 years

---

## Interpretation examples

* Reading **+2.7** with price above a rising 50 EMA, near prior highs

* Strong trend extension, consider pyramiding in trend systems or waiting for a pullback if you are a mean-reverter.

* Reading **−2.2** into multi-month support with flattening MA

* Stretch to the downside that often mean-reverts, size entries based on your system rules.

---

## Credits

The concept of measuring stretch from a moving average in ATR units has a rich community history. This implementation and its presentation draw on ideas popularized by **Jeff Sun**, **SugarTrader**, and **Steve D Jacobs**. Thanks to each for their contributions to ATR-based extension thinking.

---

## License

This script and description are distributed under **MPL-2.0**, consistent with the header in the source code.

---

## Changelog

* **v1.0**: Initial public release. Daily ATR normalization, EMA or SMA on D or W timeframe, robust median and sigma bands, optional table.

---

## Disclaimer

This tool is for educational use only. It is not financial advice. Always test on your own data and strategies, then manage risk accordingly.

ForecastForecast (FC), indicator documentation

Type: Study, not a strategy

Primary timeframe: 1D chart, most plots and the on-chart table only render on daily bars

Inspiration: Robert Carver’s “forecast” concept from Advanced Futures Trading Strategies, using normalized, capped signals for comparability across markets

⸻

What the indicator does

FC builds a volatility-normalized momentum forecast for a chosen symbol, optionally versus a benchmark. It combines an EWMAC composite with a channel breakout composite, then caps the result to a common scale. You can run it in three data modes:

• Absolute: Forecast of the selected symbol

• Relative: Forecast of the ratio symbol / benchmark

• Combined: Average of Absolute and Relative

A compact table can summarize the current forecast, short-term direction on the forecast EMAs, correlation versus the benchmark, and ATR-scaled distances to common price EMAs.

⸻

PineScreener, relative-strength screening

This indicator is excellent for screening on relative strength in PineScreener, since the forecast is volatility-normalized and capped on a common scale.

Available PineScreener columns

PineScreener reads the plotted series. You will see at least these columns:

• FC, the capped forecast

• from EMA20, (price − EMA20) / ATR in ATR multiples

• from EMA50, (price − EMA50) / ATR in ATR multiples

• ATR, ATR as a percent of price

• Corr, weekly correlation with the chosen benchmark

Relative mode and Combined mode are recommended for cross-sectional screens. In Relative mode the calculation uses symbol / benchmark, so ensure the ratio ticker exists for your data source.

⸻

How it works, step by step

1. Volatility model

Compute exponentially weighted mean and variance of daily percent returns on D, annualize, optionally blend with a long lookback using 10y %, then convert to a price-scaled sigma.

2. EWMAC momentum, three legs

Daily legs: EMA(8) − EMA(32), EMA(16) − EMA(64), EMA(32) − EMA(128).

Divide by price-scaled sigma, multiply by leg scalars, cap to Cap = 20, average, then apply a small FDM factor.

3. Breakout momentum, three channels

Smoothed position inside 40, 80, and 160 day channels, each scaled, then averaged.

4. Composite forecast

Average the EWMAC composite and the breakout composite, then cap to ±20.

Relative mode runs the same logic on symbol / benchmark.

Combined mode averages Absolute and Relative composites.

5. Weekly correlation

Pearson correlation between weekly closes of the asset and the benchmark over a user-set length.

6. Direction overlay

Two EMAs on the forecast series plus optional green or red background by sign, and optional horizontal level shading around 0, ±5, ±10, ±15, ±20.

⸻

Plots

• FC, capped forecast on the daily chart

• 8-32 Abs, 8-32 Rel, single-leg EWMAC plus breakout view

• 8-32-128 Abs, 8-32-128 Rel, three-leg composite views

• from EMA20, from EMA50, (price − EMA) / ATR

• ATR, ATR as a percent of price

• Corr, weekly correlation with the benchmark

• Forecast EMA1 and EMA2, EMAs of the forecast with an optional fill

• Backgrounds and guide lines, optional sign-based background, optional 0, ±5, ±10, ±15, ±20 guides

Most plots and the table are gated by timeframe.isdaily. Set the chart to 1D to see them.

⸻

Inputs

Symbol selection

• Absolute, Relative, Combined

• Vs. benchmark for Relative mode and correlation, choices: SPY, QQQ, XLE, GLD

• Ticker or Freeform, for Freeform use full TradingView notation, for example NASDAQ:AAPL

Engine selection

• Include:

• 8-32-128, three EWMAC legs plus three breakouts

• 8-32, simplified view based on the 8-32 leg plus a 40-day breakout

EMA, applied to the forecast

• EMA1, EMA2, with line-width controls, plus color and opacity

Volatility

• Span, EW volatility span for daily returns

• 10y %, blend of long-run volatility

• Thresh, Too volatile, placeholders in this version

Background

• Horizontal bg, level shading, enabled by default

• Long BG, Hedge BG, colors and opacities

Show

• Table, Header, Direction, Gain, Extension

• Corr, Length for correlation row

Table settings

• Position, background, opacity, text size, text color

Lines

• 0-lines, 10-lines, 5-lines, level guides

⸻

Reading the outputs

• Forecast > 0, bullish tilt; Forecast < 0, bearish or hedge tilt

• ±10 and ±20 indicate strength on a uniform scale

• EMA1 vs EMA2 on the forecast, EMA1 above EMA2 suggests improving momentum

• Table rows, label colored by sign, current forecast value plus a green or red dot for the forecast EMA cross, optional daily return percent, weekly correlation, and ATR-scaled EMA9, EMA20, EMA50 distances

⸻

Data handling, repainting, and performance

• Daily and weekly series are fetched with request.security().

• Calculations use closed bars, values can update until the bar closes.

• No lookahead, historical values do not repaint.

• Weekly correlation updates during the week, it finalizes on weekly close.

• On intraday charts most visuals are hidden by design.

⸻

Good practice and limitations

• This is a research indicator, not a trading system.

• The fixed Cap = 20 keeps a common scale, extreme moves will be clipped.

• Relative mode depends on the ratio symbol / benchmark, ensure both legs have data for your feed.

⸻

Credits

Concept inspired by Robert Carver’s forecast methodology in Advanced Futures Trading Strategies. Implementation details, parameters, and visuals are specific to this script.

⸻

Changelog

• First version

⸻

Disclaimer

For education and research only, not financial advice. Always test on your market and data feed, consider costs and slippage before using any indicator in live decisions.

Penguin Trend with RSI on DiffVisualizes volatility regime via the percent spread between the upper Bollinger Band and the upper Keltner Channel, with bar colors from a lightweight trend engine and an RSI computed on the Diff signal. Supports SMA/EMA/WMA/RMA/HMA/VWMA/VWAP and an optional calculation timeframe. Defaults preserve the original look and behavior.

Penguin Trend with RSI on Diff shows expansion vs. compression in price action by comparing two classic volatility envelopes. It computes:

Diff% = (UpperBB − UpperKC) / UpperKC × 100

• Diff > 0: Bollinger Bands are wider than Keltner Channels → expansion / momentum regime

• Diff < 0: BB narrower than KC → compression / squeeze regime

A white “Average Diff” line smooths Diff% (default: SMA(5)) to highlight regime shifts. Bars are colored only when Diff > 0 to focus on expansion phases. A lightweight trend engine defines four states from a fast/slow MA bias and a short “thrust” MA on ohlc4:

• Green: Bullish bias and thrust > fast MA (healthy upside thrust)

• Red: Bearish bias and thrust < fast MA (healthy downside thrust)

• Yellow: Bullish bias but thrust ≤ fast MA (pullback/weakness)

• Blue: Bearish bias but thrust ≥ fast MA (bear rally/short squeeze)

RSI on Diff:

The indicator adds an RSI applied to Diff% to gauge momentum of the expansion/compression signal itself. Choose between Built-in RSI or a manual RMA-based computation, and optionally smooth it. Default OB/OS lines are 70/30.

How it works:

• Bollinger Bands (BB): Basis = selected MA of src (default SMA(20)); Width = StdDev × Mult (default 2.0)

• Keltner Channels (KC): Basis = selected MA of src (default SMA(20)); Width = ATR(kcATR) × Mult (defaults 20 and 2.0)

• Diff%: Safe division guards against division-by-zero

• MA engine: Select SMA / EMA / WMA / RMA / HMA / VWMA / VWAP for BB/KC bases, Average Diff, and trend components (VWAP is session-anchored)

• Calculation timeframe: Compute internals on a chosen TF via request.security() while viewing any chart TF

Inputs (key):

• Calculation timeframe: Empty = chart TF; set e.g., 60/240 to compute on that TF

• BB: Length, StdDev Mult, MA Type

• KC: Basis Length, ATR Length, Multiplier, MA Type

• Average Diff: Length and MA Type

• RSI on Diff: RSI Length, Method (Built-in or Manual RMA), Smoothing Length, OB/OS levels, show/hide

• Trend Engine: Fast/Slow lengths & MA type, Signal (kept for completeness), Thrust MA length & type

• Display/Visibility: Paint bars only when Diff > 0; show zero line; “true Blue” color toggle; show/hide Diff columns and Average Diff

How to use:

1. Regime changes: Watch Diff% or Average Diff crossing 0. Above zero favors momentum/continuation setups; below zero suggests compression and potential breakout conditions.

2. State confirmation: During expansion (Diff > 0), prioritize Green/Red for aligned thrust; treat Yellow/Blue as cautionary/contrarian.

3. RSI on Diff: Use OB/OS and crossovers for timing entries/exits or for confirming/negating expansion strength.

Alerts:

• Diff crosses above/below 0

• Average Diff crosses above/below 0

• RSI(Diff) crosses above OB / below OS

• State changes: GREEN / RED / YELLOW / BLUE

Notes & limitations:

• VWAP is session-anchored and best on intraday data. If not applicable on the selected calculation TF, the script automatically falls back to EMA.

• Defaults (SMA(20) for BB/KC, multipliers 2.0, SMA(5) Average Diff, original trend coloring and bar painting) preserve the original appearance.

• RSI on Diff is plotted in the same pane for a compact workflow; you can hide it or split into a separate indicator if desired.

Release notes:

v6.0 — Upgraded to Pine v6. Added multi-MA options (SMA/EMA/WMA/RMA/HMA/VWMA/VWAP), calculation timeframe, RSI on Diff (Built-in or Manual RMA) with smoothing, safe division guard, optional zero line, and optional true Blue color. Defaults retain the original behavior.

License / disclaimer:

© waranyu.trkm — MIT License. Educational use only; not financial advice.

Penguin TrendMeasures the volatility regime by comparing the upper Bollinger Band to the upper Keltner Channel and colors bars with a lightweight trend state. Supports SMA/EMA/WMA/RMA/HMA/VWMA/VWAP and a selectable calculation timeframe. Default settings preserve the original look and behavior.

Penguin Trend visualizes expansion vs. compression in price action by comparing two classic volatility envelopes. It computes:

Diff% = (UpperBB − UpperKC) / UpperKC × 100

* Diff > 0: Bollinger Bands are wider than Keltner Channels -> expansion / momentum regime.

* Diff < 0: BB narrower than KC -> compression / squeeze regime.

A white “Average Difference” line smooths Diff% (default: SMA(5)) to help spot regime shifts.

Trend coloring (kept from original):

Bars are colored only when Diff > 0 to emphasize expansion phases. A lightweight trend engine defines four states using a fast/slow MA bias and a short “thrust” MA applied to ohlc4:

* Green: Bullish bias and thrust > fast MA (healthy upside thrust).

* Red: Bearish bias and thrust < fast MA (healthy downside thrust).

* Yellow: Bullish bias but thrust ≤ fast MA (pullback/weakness).

* Blue: Bearish bias but thrust ≥ fast MA (bear rally/short squeeze).

Note: By default, Blue renders as Yellow to preserve the original visual style. Enable “Use true BLUE color” if you prefer Aqua for Blue.

How it works (under the hood):

* Bollinger Bands (BB): Basis = selected MA of src (default SMA(20)). Width = StdDev × Mult (default 2.0).

* Keltner Channels (KC): Basis = selected MA of src (default SMA(20)). Width = ATR(kcATR) × Mult (defaults 20 and 2.0).

* Diff%: Safe division guards against division-by-zero.

* MA engine: You can choose SMA / EMA / WMA / RMA / HMA / VWMA / VWAP for BB/KC bases, Diff smoothing, and the trend components (VWAP is session-anchored).

* Calculation timeframe: Set “Calculation timeframe” to compute all internals on a chosen TF via request.security() while viewing any chart TF.

Inputs (key ones):

* Calculation timeframe: Empty = use chart TF; if set (e.g., 60), all internals compute on that TF.

* BB: Length, StdDev Mult, MA Type.

* KC: Basis Length, ATR Length, Multiplier, MA Type.

* Smoothing: Average Length & MA Type for the “Average Difference” line.

* Trend Engine: Fast/Slow lengths & MA type; Signal (kept for completeness); Thrust length & MA type (defaults replicate original behavior).

* Display: Paint bars only when Diff > 0; optional Zero line; optional true Blue color.

How to use:

1. Regime changes: Watch Diff% or Average Diff crossing 0. Above zero favors momentum/continuation setups; below zero suggests compression and potential breakout conditions.

2. State confirmation: Use bar colors to qualify expansion: Green/Red indicate expansion aligned with trend thrust; Yellow/Blue flag weaker/contrarian thrust during expansion.

3. Multi-timeframe analysis: Run calculations on a higher TF (e.g., H1/H4) while trading a lower TF chart to smooth noise.

Alerts:

* Diff crosses above/below 0.

* Average Diff crosses above/below 0.

* State changes: GREEN / RED / YELLOW / BLUE.

Notes & limitations:

* VWAP is session-anchored and best on intraday data. If not applicable on the selected calculation TF, the script automatically falls back to EMA.

* Default parameters (SMA(20) for BB/KC, multipliers 2.0, SMA(5) smoothing, trend logic and bar painting) preserve the original appearance.

Release notes:

v6.0 — Rewritten in Pine v6 with structured inputs and guards. Multi-MA support (SMA/EMA/WMA/RMA/HMA/VWMA/VWAP). Calculation timeframe via request.security() for multi-TF workflows. Safe division; optional zero line; optional true Blue color. Original visuals and behavior preserved by default.

License / disclaimer:

© waranyu.trkm — MIT License. Educational use only; not financial advice.

T-Virus Sentiment [hapharmonic]🧬 T-Virus Sentiment: Visualize the Market's DNA

Remember the iconic T-Virus vial from the first Resident Evil? That powerful, swirling helix of potential has always fascinated me. It sparked an idea: what if we could visualize the market's underlying health in a similar way? What if we could capture the "genetic code" of market sentiment and contain it within a dynamic, 3D indicator? This project is the result of that idea, brought to life with Pine Script.

The indicator's main goal is to measure the strength and direction of market sentiment by analyzing the "genetic code" of price action through a variety of trusted indicators. The result is displayed as a liquid level within a DNA helix, a bubble density representing buying pressure, and a T-Virus mascot that reflects the overall mood.

🧐 Core Concept: How It Works

The primary output of the indicator is the "Active %" gauge you see on the right side of the vial. This percentage represents the overall sentiment score, calculated as an average from 7 different technical analysis tools. Each tool is analyzed on every bar and assigned a score from 1 (strong bearish pressure) to 5 (strong bullish potential).

In this indicator, we re-imagine market dynamics through the lens of a viral outbreak. A strong bear market is like a virus taking hold, pulling all technical signals down into a state of weakness. Conversely, a powerful bull market is like an antiviral serum ; positive signals rise and spread toward the top of the vial, indicating that the system is being injected with strength.

This is not just another line on a chart. It's a comprehensive sentiment dashboard designed to give an immediate, at-a-glance understanding of the confluence between 7 classic technical indicators. The incredible 3D model of the vial itself was inspired by a design concept found here .

⚛️ The 4 Core Elements of T-Virus Sentiment

These four elements work in harmony to give a complete, multi-faceted picture of market sentiment. Each component tells a different part of the story.

The Virus Mascot: An instant emotional cue. This character provides the quickest possible read on the overall market mood, combining sentiment with volume pressure.

The Antiviral Serum Level: The main quantitative output. This is the liquid level in the DNA helix and the percentage gauge on the right, representing the average sentiment score from all 7 indicators.

Buy Pressure & Bubble Density: This visualizes volume flow. The density of bubbles represents the intensity of accumulation (buying) versus distribution (selling). It's the "power" behind the move.

The Signal Distribution: This shows the confluence (or dispersion) of sentiment. Are all signals bullish and clustered at the top, or are they scattered, indicating a conflicted market? The position of the indicator labels is crucial, as each is assigned to one of five distinct zones:

Base Bottom: The market is at its weakest. Signals here suggest strong bearish control and distribution.

Lower Zone: The market is still bearish, but signals may be showing early signs of accumulation or bottoming.

Neutral Core (Center): A state of balance or sideways consolidation. The market is waiting for a new direction.

Upper Zone: Bullish momentum is becoming clear. Signals are strengthening and showing bullish control.

Top Cap: The market is "heating up" with strong bullish sentiment, potentially nearing overbought conditions.

🐂🐻 The Virus Mascot: The At-a-Glance Indicator

This character acts as a shortcut to confirm market health. It combines the sentiment score with volume, preventing false confidence in a low-volume rally.

Its state is determined by a dual-check: the overall "Antiviral Serum Level" and the "Buy Pressure" must both be above 50%.

Green & Smiling: The 'all clear' signal. This means that not only is the overall technical sentiment bullish, but it's also being supported by real buying pressure. This is a sign of a healthy bull market.

Red & Angry: A warning sign. This appears if either the sentiment is weak, or a bullish sentiment is not being confirmed by buying volume. The latter could indicate a potential "bull trap" or an exhaustive move.

This mascot can be disabled from the settings page under "Virus Mascot Styling" if a cleaner look is preferred.

🫧 Bubble Density: Gauging Buy vs. Sell Pressure

The bubbles visualize the battle between buyers and sellers. There are two modes to control how this is calculated:

Mode 1: Visible Range (The 'Big Picture' View)

This default mode is best for getting a broad, contextual understanding of the current session. It dynamically analyzes the volume of every single candlestick currently visible on the screen to calculate the buy/sell pressure ratio. It answers the question: "Over the entire period I'm looking at, who is in control?" As you zoom in or out, the calculation adapts.

Mode 2: Custom Lookback (The 'Precision' View)

This mode is for traders who need to analyze short-term pressure. You can define a fixed number of recent bars to analyze, which is perfect for scalping or understanding the volume dynamics leading into a key level. It answers the question: "What is happening right now ?" In the example above, a lookback of 2 focuses only on the most recent action, clearly showing intense, immediate selling pressure (few bubbles) and a corresponding drop in the sentiment score to 29%.

ℹ️ Interactive Tooltips: Dive Deeper

We believe in transparency, not 'black box' indicators. This feature transforms the indicator from a visual aid into an active learning tool.

Simply hover the mouse over any indicator label (like EMA, OBV, etc.) to get a detailed tooltip. It will explain the specific data points and thresholds that signal met to be placed in its current zone. This helps build trust in the signals and allows users to fine-tune the indicator settings to better match their own trading style.

🎯 The Scoring Logic Breakdown

The "Antiviral Serum Level" gauge is the average score from 7 technical analysis tools. Each is graded on a 5-point scale (1=Strong Bearish to 5=Strong Bullish). Here’s a detailed, transparent look at how each "gene" is evaluated:

Relative Strength Index (RSI)

Measures momentum and overbought/oversold conditions.

Group 1 (Strong Bearish): RSI > 80 (Extreme Overbought)

Group 2 (Bearish): 70 < RSI ≤ 80 (Overbought)

Group 3 (Neutral): 30 ≤ RSI ≤ 70

Group 4 (Bullish): 20 ≤ RSI < 30 (Oversold)

Group 5 (Strong Bullish): RSI < 20 (Extreme Oversold)

Exponential Moving Averages (EMA)

Evaluates the trend's strength and structure based on the alignment of multiple EMAs (9, 21, 50, 100, 200, 250).

Group 1 (Strong Bearish): A perfect bearish sequence (9 < 21 < 50 < ...)

Group 2 (Bearish Transition): Early signs of a potential reversal (e.g., 9 > 21 but still below 50)

Group 3 (Neutral / Mixed): MAs are intertwined or showing a partial bullish sequence.

Group 4 (Bullish): A strong bullish sequence is forming (e.g., 9 > 21 > 50 > 100)

Group 5 (Strong Bullish): A perfect bullish sequence (9 > 21 > 50 > 100 > 200 > 250)

Moving Average Convergence Divergence (MACD)

Analyzes the relationship between two moving averages to gauge momentum.

Group 1 (Strong Bearish): MACD & Histogram are negative and momentum is falling.

Group 2 (Weakening Bearish): MACD is negative but the histogram is rising or positive.

Group 3 (Neutral / Crossover): A crossover event is occurring near the zero line.

Group 4 (Bullish): MACD & Histogram are positive.

Group 5 (Strong Bullish): MACD & Histogram are positive, rising strongly, and accelerating.

Average Directional Index (ADX)

Measures trend strength, not direction. The score is based on both ADX value and the dominance of DI+ vs DI-.

Group 1 (Bearish / No Trend): ADX < 20 and DI- is dominant.

Group 2 (Developing Bearish Trend): 20 ≤ ADX < 25 and DI- is dominant.

Group 3 (Neutral / Indecision): Trend is weak or DI+ and DI- are nearly equal.

Group 4 (Developing Bullish Trend): 25 ≤ ADX ≤ 40 and DI+ is dominant.

Group 5 (Strong Bullish Trend): ADX > 40 and DI+ is dominant.

Ichimoku Cloud (IKH)

A comprehensive indicator that defines support/resistance, momentum, and trend direction.

Group 1 (Strong Bearish): Price is below the Kumo, Tenkan < Kijun, and Chikou is below price.

Group 2 (Bearish): Price is inside or below the Kumo, with mixed secondary signals.

Group 3 (Neutral / Ranging): Price is inside the Kumo, often with a Tenkan/Kijun cross.

Group 4 (Bullish): Price is above the Kumo with strong primary signals.

Group 5 (Strong Bullish): All signals are aligned bullishly: price above Kumo, bullish Tenkan/Kijun cross, bullish future Kumo, and Chikou above price.

Bollinger Bands (BB)

Measures volatility and relative price levels.

Group 1 (Strong Bearish): Price is below the lower band.

Group 2 (Bearish Territory): Price is between the lower band and the basis line.

Group 3 (Neutral): Price is hovering around the basis line.

Group 4 (Bullish Territory): Price is between the basis line and the upper band.

Group 5 (Strong Bullish): Price is above the upper band.

On-Balance Volume (OBV)

Uses volume flow to predict price changes. The score is based on OBV's trend and its position relative to its moving average.

Group 1 (Strong Bearish): OBV is below its MA and falling.

Group 2 (Weakening Bearish): OBV is below its MA but showing signs of rising.

Group 3 (Neutral): OBV is very close to its MA.

Group 4 (Bullish): OBV is above its MA and rising.

Group 5 (Strong Bullish): OBV is above its MA, rising strongly, and showing signs of a volume spike.

🧭 How to Use the T-Virus Sentiment Indicator

IMPORTANT: This indicator is a sentiment dashboard , not a direct buy/sell signal generator. Its strength lies in showing confluence and providing a quick, holistic view of the market's technical health.

Confirmation Tool: Use the "Active %" gauge to confirm a trade setup from your primary strategy. For example, if you see a bullish chart pattern, a high and rising sentiment score can add confidence to your trade.

Momentum & Trend Gauge: A consistently high score (e.g., > 75%) suggests strong, established bullish momentum. A consistently low score (< 25%) suggests strong bearish control. A score hovering around 50% often indicates a ranging or indecisive market.

Divergence & Warning System: Pay attention to divergences. If the price is making new highs but the sentiment score is failing to follow or is actively decreasing, it could be an early warning sign that the underlying momentum is weakening.

⚙️ Settings & Customization

The indicator is highly customizable to fit any trading style.

Position & Anchor: Control where the vial appears on the chart.

Styling (Vial, Helix, etc.): Nearly every visual element can be color-customized.

Signals: This is where the real power is. All underlying indicator parameters (RSI length, MACD settings, etc.) can be fine-tuned to match a personal strategy. The text labels can also be disabled if the chart feels cluttered.

Enjoy visualizing the market's DNA with the T-Virus Sentiment indicator

Reversal Radars — Berk v2.0 (Bottom & Top)1) Combined script (Dip+Tepe)

Title:

Reversal Radars — Berk v2.0 (Bottom & Top)

Description (EN):

What it does

Two high-probability reversal detectors in one indicator: a Bottom Reversal Radar (long bias) and a Top Reversal Radar (short/hedge bias). Each radar aggregates multiple conditions into a single score and triggers when Score ≥ Threshold.

How it works

RSI regime shift: Bottom = recovery after oversold (touched 30, crosses up 35). Top = roll-over from overbought (touched 70, crosses down 65).

MACD cross: Bull (up) for bottoms, Bear (down) for tops.

EMA8 filter: Close above (bottom) / below (top) EMA(8).

Structure break (BOS): Close above recent swing high / below recent swing low (lookbackBars, using precomputed highest/lowest to avoid inconsistencies).

EMA200 proximity: Price within a configurable band (default −5% … +2%).

Volume expansion: Volume ≥ SMA(20) × multiplier (default 1.5×).

Divergence: Pivot-confirmed (3/3) bullish (bottom) or bearish (top) RSI divergence.

Scoring: RSI shift +2, divergence +2, MACD +1, EMA8 +1, BOS +1, Volume +1, EMA200 band +1.

Signals & Alerts

Bottom: label “DÖNÜŞ↑” and alert “Dipten Dönüş — Ana Sinyal” when scoreLong ≥ thrLong.

Top: label “DÖNÜŞ↓” and alert “Tepeden Dönüş — Ana Sinyal” when scoreShort ≥ thrShort.

Use Once per bar close for stable alerts.

Inputs

lenRSI, rsiOS=30, rsiRecover=35, rsiOB=70, rsiFall=65, volLen=20, volMult=1.5, lookbackBars=5, ema200 band (−5…+2%), thrLong/thrShort, toggles for Bottom/Top.

Timeframes & tips

Best on Daily/4H. Tighten thresholds (e.g., 4) and raise volume multiplier (1.8–2.0×) on lower TFs or thin liquidity.

No-repaint note

Evaluated on bar close; pivot divergences confirm with a natural ~3-bar delay.

Disclaimer

Educational use only. Not financial advice.

Tags: reversal, divergence, rsi, macd, ema, volume, trend, screener, stocks, crypto, bist

2) Bottom-only (Dip)

Title:

Bottom Reversal Radar — Berk v1.4

Description (EN):

Purpose

Scores bottoming conditions and triggers when Score ≥ Threshold (default 3).

Components

RSI recovery after oversold (30→35), MACD bull cross, close above EMA8, BOS above recent swing high, near-EMA200 band (−5…+2%), volume ≥ SMA(20)×1.5, and pivot-confirmed (3/3) bullish RSI divergence. Weights: RSI +2, Divergence +2, others +1.

Usage

Add to chart, set alert “Dipten Dönüş — Ana Sinyal”, Once per bar close. Works on any timeframe (need ≥200 bars for EMA200). Daily/4H recommended.

No-repaint

Bar-close evaluation; divergence confirms with ~3 bars.

Tags: bottom, reversal, rsi, macd, ema, volume, divergence

3) Top-only (Tepe)

Title:

Top Reversal Radar — Berk v1.0

Description (EN):

Purpose

Detects topping risk and triggers when Score ≥ Threshold (default 3) for exits/hedges.

Components

RSI roll-over from overbought (70→65), MACD bear cross, close below EMA8, BOS below recent swing low, near-EMA200 band, volume ≥ SMA(20)×1.5, and pivot-confirmed (3/3) bearish RSI divergence. Weights: RSI +2, Divergence +2, others +1.

Usage

Add to chart, set alert “Tepeden Dönüş — Ana Sinyal”, Once per bar close. Daily/4H preferred; tighten thresholds on lower TFs.

No-repaint

Bar-close evaluation; divergence confirms with ~3 bars.

Tags: top, reversal, rsi, macd, ema, volume, divergence

Extended CANSLIM Indicator❖ Extended CANSLIM Indicator.

The Extended CANSLIM indicator is an indicator that concentrates all the tools usually used by CANSLIM traders.

It shows a table where all the stock fundamental information is shown at once first for the last quarter and then up to 5 years back.

The fundamental data is checked against well known CANSLIM validation criteria and is shown over 4 state levels.

1. Good = Value is CANSLIM Compliant.

2. Acceptable = Value is not CANSLIM compliant but still good. value is shown with a lighter background color.

3. Warning = Value deserves special attention. Value is shown over orange background color.

3. Stop = Value is non CANSLIM compliant or indicates a stop trading condition. Value is shown over red background color.

The indicator has also a set of technical tools calculated on price or index and shown directly on the chart.

❖ Fundamental data shown in the table.

The table is arranged in 4 sets of data:

1. Table Header, showing Indicator and Company data.

2. CANSLIM.

3. 3Rs: RS Rating, Revenue and ROE.

4. Extra Data: Piotroski score, ATR, Trend Days, D to E, Avg Vol and Vol today.

Sets 3 and 4 can be hidden from the table.

❖ Indicator and Compay Data.

The table header shows, Indicator name and version.

It then displays Company Name, sector and industry, human size and its capitalization.

❖ CANSLIM Data.

Displays either genuine CANSLIM data from TradinView or custom data as best effort when that data cannot be obtained in TV.

C = EPS diluted growth, Quarterly YoY.

>= 25% = Good, >= 0% = Acceptable, < 0% = Stop

A = EPS diluted growth, Annual YoY.

>= 25% = Good, >= 0% = Acceptable, < 0% = Stop

N = New High as best effort (Cust).

Always Good

S = Float shares as best effort.

Always Good

L = One year performance relative to S&P 500 (Cust),

Positive : 0% .. 50% = Neutral, 50%+ = Leader, 80%+ = Leader+, 100%+ = Leader++

Negative : 0% .. -10% = Laggard, -10% .. -30% = Laggard+, -30%+ = Laggard++

>= 50% = Good, >= 0% = Acceptable, >= -10% Warning, < -10% = Stop

I = Accumulation/Distribution days over last 25 days as a clue for institutional support (Cust).

A delta is calculated by subtracting Distribution to Accumulation days.

> 0 = Good, = 0 = Acceptable, < 0 = Warning, < -5 = Stop

M = Market direction and exposure measured on S&500 closing between averages (Cust).

Varies from 0% Full Bear to 100% Full Bull

>= 80% = Good, >= 60% = Acceptable, >= 40% = Warning, < 40% = Stop

❖ Extra non CANSLIM Data.

RS = RS Rating.

>= 90 = Good, >= 80 = Accept, >= 50 = Warning, < 50 = Stop

Rev. = Revenue Growth Quarterly YoY.

>= 0% = Good, <0% = Stop

ROE = Return on Equity, Quarterly YoY.

>= 17% = Good, >= 0% = Acceptable, < 0% = Stop

Piotr. = Piotroski Score, www.investopedia.com (TV)

>= 7 = Good, >= 4 = Acceptable, < 4 = Stop

ATR = Average True Range over the last 20 days (Cust).

0% - 2% = Acceptable, 2% - 4% = Ideal, 4% - 6% = Warning, 5%+ = Stop.

Trend Days = Days since EMA150 is over EMA200 (Cust).

Always Good

D. to E. = Days left before Earnings. Maybe not a good idea buying just before earnings (Cust).

>= 28 = Good, >= 21 = Acceptable, >= 14 = Warning, < 14 = Stop

Avg Vol. = 50d Average Volume (Cust).

>= 100K = Good, < 100K = Acceptable

Vol. Today = Today's percentage volume compared to 50d average (Cust).

Always Good.

❖ Historical Data.

Optionally selectable historical data can be displayed for C, A, Revenue and ROE up to 20 quarters if available.

Quarterly numbers can also be displayed for A, C and Revenue.

Information can be shown in Chronological or Reverse Chronological order (default).

Increasing growth quarters are shown in white, while diminuing ones are shown in Yellow.

Transition from Losing to Profitable quarters are shown with an exclamation mark ‘!’

Finally, losing quarters are shown between parenthesis.

❖ MAs on chart.

Displays 200, 100, 50 and 20 days MAs on chart.

The MAs are also automatically scaled in the 1W time frame.

❖ New 52 Week High on chart.

A sun is shown on the chart the first time that a new 52 week high is reached.

The N cell shows a filled sun when a 52 week high is no older than a month, an lighter sun when it’s no older than a quarter or a moon otherwise.

❖ Pocket Pivots on chart.

Small triangles below the price are signaling pocket pivots.

❖ Bases on chart, formerly Darvas Boxes.

Draw bases as defined by Darvas boxes, both top or bottom of bases can be selected to be shown in order to only show resistance or support.

❖ Market exposure/direction indicator.

When charting S&P500 (SPX), Nasdaq 100 Index (NDX), Nasdaq composite (IXIC) or Dow Jownes Index (DJIA), the indicator switches to Market Exposure indicator, showing also Accumulation/Distribution days when volume information is available. This indication which varies from 0% to 100% is what is shown under the M letter in the CANSLIM table which is calculated on the S&P500.

❖ Follow Through Days indicator.

If you are an adept of the Low-cheat entry, then you will be highly interested by the Follow Through days indicator as measured in the S&P 500 and shown as diamonds on the chart.

The follow-through days are calculated on S&P500 but shown in current stock chart so you don’t need to chart the S&P 500 to know that a follow through day occurred.

Follow Through days show correctly on Daily time frame and most are also shown on the Weekly time frame as well.

They are also classified according to the market zone in which they occur:

0%-5% from peak = Pullback : FT day is not shown.

5%-10% from peak = Minor Correction : Minor FT days is shown.

10%-20% from peak = Correction : Intermediate FT days us shown

20+% from peak = Bear Market : Makor FT days is shown

❖ RS Line and Rating indicator.

A RS Line and Rating indicator can be added to the chart.

Relative Strength Rating Accuracy.

Please note that the RS Rating is not 100% accurate when compared to IBD values.

❖ Earning Line indicator.

An Earning Line indicator can be added to the chart.

❖ ATR Bands and ATR Trade calculator.

The motivation for this calculator came from my own need to enter trades on volatile stocks where the simple 7% Stop Loss rule doest not work.

It simply calculates the number of shares you can buy at any moment based on current stock price and using the lower ATR band as a stop loss.

A few words about the ATR Bands.

On this indicator the ATR bands are not drawn as a classical channel that follows the price.

The lower band is drawn as a support until it’s broken on a closing basis. It can’t be in a down trend.

The upper band is drawn as a resistance until it’s broken on a closing basis. It can’t be in an up trend.

The idea is that when price starts to fall down from a peak, it should not violate its lower band ATR and that means that we can use that level as a Stop Loss.

You must look back for the stock volatility and find out which ATR multiplier works well meaning that the ATR bands are not violated on normal pullbacks. By default, the indicator uses 5x multiplier.

❖ Extra things, visual features and default settings.

The first square cell of current quarter displays a check mark ‘V’ if the CANSLIM criteria is OK or acceptable or a cross ‘X’ otherwise.

The first square cell of historical C and Rev show respectively the count of last consecutive positive quarters.

There are different color themes from “Forest” to “Space” you can chose from to best fit your eyes.

You also have different table sizes going from “Micro” to “Huge” for better adjustment to the size of your display.

The default settings view show: Pocket Pivots, FT Days, MA50, RS Line and ATR Bands.

That's all, Enjoy!

Markov Chain [3D] | FractalystWhat exactly is a Markov Chain?

This indicator uses a Markov Chain model to analyze, quantify, and visualize the transitions between market regimes (Bull, Bear, Neutral) on your chart. It dynamically detects these regimes in real-time, calculates transition probabilities, and displays them as animated 3D spheres and arrows, giving traders intuitive insight into current and future market conditions.

How does a Markov Chain work, and how should I read this spheres-and-arrows diagram?

Think of three weather modes: Sunny, Rainy, Cloudy.

Each sphere is one mode. The loop on a sphere means “stay the same next step” (e.g., Sunny again tomorrow).

The arrows leaving a sphere show where things usually go next if they change (e.g., Sunny moving to Cloudy).

Some paths matter more than others. A more prominent loop means the current mode tends to persist. A more prominent outgoing arrow means a change to that destination is the usual next step.

Direction isn’t symmetric: moving Sunny→Cloudy can behave differently than Cloudy→Sunny.

Now relabel the spheres to markets: Bull, Bear, Neutral.

Spheres: market regimes (uptrend, downtrend, range).

Self‑loop: tendency for the current regime to continue on the next bar.

Arrows: the most common next regime if a switch happens.

How to read: Start at the sphere that matches current bar state. If the loop stands out, expect continuation. If one outgoing path stands out, that switch is the typical next step. Opposite directions can differ (Bear→Neutral doesn’t have to match Neutral→Bear).

What states and transitions are shown?

The three market states visualized are:

Bullish (Bull): Upward or strong-market regime.

Bearish (Bear): Downward or weak-market regime.

Neutral: Sideways or range-bound regime.

Bidirectional animated arrows and probability labels show how likely the market is to move from one regime to another (e.g., Bull → Bear or Neutral → Bull).

How does the regime detection system work?

You can use either built-in price returns (based on adaptive Z-score normalization) or supply three custom indicators (such as volume, oscillators, etc.).

Values are statistically normalized (Z-scored) over a configurable lookback period.

The normalized outputs are classified into Bull, Bear, or Neutral zones.

If using three indicators, their regime signals are averaged and smoothed for robustness.

How are transition probabilities calculated?

On every confirmed bar, the algorithm tracks the sequence of detected market states, then builds a rolling window of transitions.

The code maintains a transition count matrix for all regime pairs (e.g., Bull → Bear).

Transition probabilities are extracted for each possible state change using Laplace smoothing for numerical stability, and frequently updated in real-time.

What is unique about the visualization?

3D animated spheres represent each regime and change visually when active.

Animated, bidirectional arrows reveal transition probabilities and allow you to see both dominant and less likely regime flows.

Particles (moving dots) animate along the arrows, enhancing the perception of regime flow direction and speed.

All elements dynamically update with each new price bar, providing a live market map in an intuitive, engaging format.

Can I use custom indicators for regime classification?

Yes! Enable the "Custom Indicators" switch and select any three chart series as inputs. These will be normalized and combined (each with equal weight), broadening the regime classification beyond just price-based movement.

What does the “Lookback Period” control?

Lookback Period (default: 100) sets how much historical data builds the probability matrix. Shorter periods adapt faster to regime changes but may be noisier. Longer periods are more stable but slower to adapt.

How is this different from a Hidden Markov Model (HMM)?

It sets the window for both regime detection and probability calculations. Lower values make the system more reactive, but potentially noisier. Higher values smooth estimates and make the system more robust.

How is this Markov Chain different from a Hidden Markov Model (HMM)?

Markov Chain (as here): All market regimes (Bull, Bear, Neutral) are directly observable on the chart. The transition matrix is built from actual detected regimes, keeping the model simple and interpretable.

Hidden Markov Model: The actual regimes are unobservable ("hidden") and must be inferred from market output or indicator "emissions" using statistical learning algorithms. HMMs are more complex, can capture more subtle structure, but are harder to visualize and require additional machine learning steps for training.

A standard Markov Chain models transitions between observable states using a simple transition matrix, while a Hidden Markov Model assumes the true states are hidden (latent) and must be inferred from observable “emissions” like price or volume data. In practical terms, a Markov Chain is transparent and easier to implement and interpret; an HMM is more expressive but requires statistical inference to estimate hidden states from data.

Markov Chain: states are observable; you directly count or estimate transition probabilities between visible states. This makes it simpler, faster, and easier to validate and tune.

HMM: states are hidden; you only observe emissions generated by those latent states. Learning involves machine learning/statistical algorithms (commonly Baum–Welch/EM for training and Viterbi for decoding) to infer both the transition dynamics and the most likely hidden state sequence from data.

How does the indicator avoid “repainting” or look-ahead bias?

All regime changes and matrix updates happen only on confirmed (closed) bars, so no future data is leaked, ensuring reliable real-time operation.

Are there practical tuning tips?

Tune the Lookback Period for your asset/timeframe: shorter for fast markets, longer for stability.

Use custom indicators if your asset has unique regime drivers.

Watch for rapid changes in transition probabilities as early warning of a possible regime shift.

Who is this indicator for?

Quants and quantitative researchers exploring probabilistic market modeling, especially those interested in regime-switching dynamics and Markov models.

Programmers and system developers who need a probabilistic regime filter for systematic and algorithmic backtesting:

The Markov Chain indicator is ideally suited for programmatic integration via its bias output (1 = Bull, 0 = Neutral, -1 = Bear).

Although the visualization is engaging, the core output is designed for automated, rules-based workflows—not for discretionary/manual trading decisions.

Developers can connect the indicator’s output directly to their Pine Script logic (using input.source()), allowing rapid and robust backtesting of regime-based strategies.

It acts as a plug-and-play regime filter: simply plug the bias output into your entry/exit logic, and you have a scientifically robust, probabilistically-derived signal for filtering, timing, position sizing, or risk regimes.

The MC's output is intentionally "trinary" (1/0/-1), focusing on clear regime states for unambiguous decision-making in code. If you require nuanced, multi-probability or soft-label state vectors, consider expanding the indicator or stacking it with a probability-weighted logic layer in your scripting.

Because it avoids subjectivity, this approach is optimal for systematic quants, algo developers building backtested, repeatable strategies based on probabilistic regime analysis.

What's the mathematical foundation behind this?

The mathematical foundation behind this Markov Chain indicator—and probabilistic regime detection in finance—draws from two principal models: the (standard) Markov Chain and the Hidden Markov Model (HMM).

How to use this indicator programmatically?

The Markov Chain indicator automatically exports a bias value (+1 for Bullish, -1 for Bearish, 0 for Neutral) as a plot visible in the Data Window. This allows you to integrate its regime signal into your own scripts and strategies for backtesting, automation, or live trading.

Step-by-Step Integration with Pine Script (input.source)

Add the Markov Chain indicator to your chart.

This must be done first, since your custom script will "pull" the bias signal from the indicator's plot.

In your strategy, create an input using input.source()

Example:

//@version=5

strategy("MC Bias Strategy Example")

mcBias = input.source(close, "MC Bias Source")

After saving, go to your script’s settings. For the “MC Bias Source” input, select the plot/output of the Markov Chain indicator (typically its bias plot).

Use the bias in your trading logic

Example (long only on Bull, flat otherwise):

if mcBias == 1

strategy.entry("Long", strategy.long)

else

strategy.close("Long")

For more advanced workflows, combine mcBias with additional filters or trailing stops.

How does this work behind-the-scenes?

TradingView’s input.source() lets you use any plot from another indicator as a real-time, “live” data feed in your own script (source).

The selected bias signal is available to your Pine code as a variable, enabling logical decisions based on regime (trend-following, mean-reversion, etc.).

This enables powerful strategy modularity : decouple regime detection from entry/exit logic, allowing fast experimentation without rewriting core signal code.

Integrating 45+ Indicators with Your Markov Chain — How & Why

The Enhanced Custom Indicators Export script exports a massive suite of over 45 technical indicators—ranging from classic momentum (RSI, MACD, Stochastic, etc.) to trend, volume, volatility, and oscillator tools—all pre-calculated, centered/scaled, and available as plots.

// Enhanced Custom Indicators Export - 45 Technical Indicators

// Comprehensive technical analysis suite for advanced market regime detection

//@version=6

indicator('Enhanced Custom Indicators Export | Fractalyst', shorttitle='Enhanced CI Export', overlay=false, scale=scale.right, max_labels_count=500, max_lines_count=500)

// |----- Input Parameters -----| //

momentum_group = "Momentum Indicators"

trend_group = "Trend Indicators"

volume_group = "Volume Indicators"

volatility_group = "Volatility Indicators"

oscillator_group = "Oscillator Indicators"

display_group = "Display Settings"

// Common lengths

length_14 = input.int(14, "Standard Length (14)", minval=1, maxval=100, group=momentum_group)

length_20 = input.int(20, "Medium Length (20)", minval=1, maxval=200, group=trend_group)

length_50 = input.int(50, "Long Length (50)", minval=1, maxval=200, group=trend_group)

// Display options

show_table = input.bool(true, "Show Values Table", group=display_group)

table_size = input.string("Small", "Table Size", options= , group=display_group)

// |----- MOMENTUM INDICATORS (15 indicators) -----| //

// 1. RSI (Relative Strength Index)

rsi_14 = ta.rsi(close, length_14)

rsi_centered = rsi_14 - 50

// 2. Stochastic Oscillator

stoch_k = ta.stoch(close, high, low, length_14)

stoch_d = ta.sma(stoch_k, 3)

stoch_centered = stoch_k - 50

// 3. Williams %R

williams_r = ta.stoch(close, high, low, length_14) - 100

// 4. MACD (Moving Average Convergence Divergence)

= ta.macd(close, 12, 26, 9)

// 5. Momentum (Rate of Change)

momentum = ta.mom(close, length_14)

momentum_pct = (momentum / close ) * 100

// 6. Rate of Change (ROC)

roc = ta.roc(close, length_14)

// 7. Commodity Channel Index (CCI)

cci = ta.cci(close, length_20)

// 8. Money Flow Index (MFI)

mfi = ta.mfi(close, length_14)

mfi_centered = mfi - 50

// 9. Awesome Oscillator (AO)

ao = ta.sma(hl2, 5) - ta.sma(hl2, 34)

// 10. Accelerator Oscillator (AC)

ac = ao - ta.sma(ao, 5)

// 11. Chande Momentum Oscillator (CMO)

cmo = ta.cmo(close, length_14)

// 12. Detrended Price Oscillator (DPO)

dpo = close - ta.sma(close, length_20)

// 13. Price Oscillator (PPO)

ppo = ta.sma(close, 12) - ta.sma(close, 26)

ppo_pct = (ppo / ta.sma(close, 26)) * 100

// 14. TRIX

trix_ema1 = ta.ema(close, length_14)

trix_ema2 = ta.ema(trix_ema1, length_14)

trix_ema3 = ta.ema(trix_ema2, length_14)

trix = ta.roc(trix_ema3, 1) * 10000

// 15. Klinger Oscillator

klinger = ta.ema(volume * (high + low + close) / 3, 34) - ta.ema(volume * (high + low + close) / 3, 55)

// 16. Fisher Transform

fisher_hl2 = 0.5 * (hl2 - ta.lowest(hl2, 10)) / (ta.highest(hl2, 10) - ta.lowest(hl2, 10)) - 0.25

fisher = 0.5 * math.log((1 + fisher_hl2) / (1 - fisher_hl2))

// 17. Stochastic RSI

stoch_rsi = ta.stoch(rsi_14, rsi_14, rsi_14, length_14)

stoch_rsi_centered = stoch_rsi - 50

// 18. Relative Vigor Index (RVI)

rvi_num = ta.swma(close - open)

rvi_den = ta.swma(high - low)

rvi = rvi_den != 0 ? rvi_num / rvi_den : 0

// 19. Balance of Power (BOP)

bop = (close - open) / (high - low)

// |----- TREND INDICATORS (10 indicators) -----| //

// 20. Simple Moving Average Momentum

sma_20 = ta.sma(close, length_20)

sma_momentum = ((close - sma_20) / sma_20) * 100

// 21. Exponential Moving Average Momentum

ema_20 = ta.ema(close, length_20)

ema_momentum = ((close - ema_20) / ema_20) * 100

// 22. Parabolic SAR

sar = ta.sar(0.02, 0.02, 0.2)

sar_trend = close > sar ? 1 : -1

// 23. Linear Regression Slope

lr_slope = ta.linreg(close, length_20, 0) - ta.linreg(close, length_20, 1)

// 24. Moving Average Convergence (MAC)

mac = ta.sma(close, 10) - ta.sma(close, 30)

// 25. Trend Intensity Index (TII)

tii_sum = 0.0

for i = 1 to length_20

tii_sum += close > close ? 1 : 0

tii = (tii_sum / length_20) * 100

// 26. Ichimoku Cloud Components

ichimoku_tenkan = (ta.highest(high, 9) + ta.lowest(low, 9)) / 2

ichimoku_kijun = (ta.highest(high, 26) + ta.lowest(low, 26)) / 2

ichimoku_signal = ichimoku_tenkan > ichimoku_kijun ? 1 : -1

// 27. MESA Adaptive Moving Average (MAMA)

mama_alpha = 2.0 / (length_20 + 1)

mama = ta.ema(close, length_20)

mama_momentum = ((close - mama) / mama) * 100

// 28. Zero Lag Exponential Moving Average (ZLEMA)

zlema_lag = math.round((length_20 - 1) / 2)

zlema_data = close + (close - close )

zlema = ta.ema(zlema_data, length_20)

zlema_momentum = ((close - zlema) / zlema) * 100

// |----- VOLUME INDICATORS (6 indicators) -----| //

// 29. On-Balance Volume (OBV)

obv = ta.obv

// 30. Volume Rate of Change (VROC)

vroc = ta.roc(volume, length_14)

// 31. Price Volume Trend (PVT)

pvt = ta.pvt

// 32. Negative Volume Index (NVI)

nvi = 0.0

nvi := volume < volume ? nvi + ((close - close ) / close ) * nvi : nvi

// 33. Positive Volume Index (PVI)

pvi = 0.0

pvi := volume > volume ? pvi + ((close - close ) / close ) * pvi : pvi

// 34. Volume Oscillator

vol_osc = ta.sma(volume, 5) - ta.sma(volume, 10)

// 35. Ease of Movement (EOM)

eom_distance = high - low

eom_box_height = volume / 1000000

eom = eom_box_height != 0 ? eom_distance / eom_box_height : 0

eom_sma = ta.sma(eom, length_14)

// 36. Force Index

force_index = volume * (close - close )

force_index_sma = ta.sma(force_index, length_14)

// |----- VOLATILITY INDICATORS (10 indicators) -----| //

// 37. Average True Range (ATR)

atr = ta.atr(length_14)

atr_pct = (atr / close) * 100

// 38. Bollinger Bands Position

bb_basis = ta.sma(close, length_20)

bb_dev = 2.0 * ta.stdev(close, length_20)

bb_upper = bb_basis + bb_dev

bb_lower = bb_basis - bb_dev

bb_position = bb_dev != 0 ? (close - bb_basis) / bb_dev : 0

bb_width = bb_dev != 0 ? (bb_upper - bb_lower) / bb_basis * 100 : 0

// 39. Keltner Channels Position

kc_basis = ta.ema(close, length_20)

kc_range = ta.ema(ta.tr, length_20)

kc_upper = kc_basis + (2.0 * kc_range)

kc_lower = kc_basis - (2.0 * kc_range)

kc_position = kc_range != 0 ? (close - kc_basis) / kc_range : 0

// 40. Donchian Channels Position

dc_upper = ta.highest(high, length_20)

dc_lower = ta.lowest(low, length_20)

dc_basis = (dc_upper + dc_lower) / 2

dc_position = (dc_upper - dc_lower) != 0 ? (close - dc_basis) / (dc_upper - dc_lower) : 0

// 41. Standard Deviation

std_dev = ta.stdev(close, length_20)

std_dev_pct = (std_dev / close) * 100

// 42. Relative Volatility Index (RVI)

rvi_up = ta.stdev(close > close ? close : 0, length_14)

rvi_down = ta.stdev(close < close ? close : 0, length_14)

rvi_total = rvi_up + rvi_down

rvi_volatility = rvi_total != 0 ? (rvi_up / rvi_total) * 100 : 50

// 43. Historical Volatility

hv_returns = math.log(close / close )

hv = ta.stdev(hv_returns, length_20) * math.sqrt(252) * 100

// 44. Garman-Klass Volatility

gk_vol = math.log(high/low) * math.log(high/low) - (2*math.log(2)-1) * math.log(close/open) * math.log(close/open)

gk_volatility = math.sqrt(ta.sma(gk_vol, length_20)) * 100

// 45. Parkinson Volatility

park_vol = math.log(high/low) * math.log(high/low)

parkinson = math.sqrt(ta.sma(park_vol, length_20) / (4 * math.log(2))) * 100

// 46. Rogers-Satchell Volatility

rs_vol = math.log(high/close) * math.log(high/open) + math.log(low/close) * math.log(low/open)

rogers_satchell = math.sqrt(ta.sma(rs_vol, length_20)) * 100

// |----- OSCILLATOR INDICATORS (5 indicators) -----| //

// 47. Elder Ray Index

elder_bull = high - ta.ema(close, 13)

elder_bear = low - ta.ema(close, 13)

elder_power = elder_bull + elder_bear

// 48. Schaff Trend Cycle (STC)

stc_macd = ta.ema(close, 23) - ta.ema(close, 50)

stc_k = ta.stoch(stc_macd, stc_macd, stc_macd, 10)

stc_d = ta.ema(stc_k, 3)

stc = ta.stoch(stc_d, stc_d, stc_d, 10)

// 49. Coppock Curve

coppock_roc1 = ta.roc(close, 14)

coppock_roc2 = ta.roc(close, 11)

coppock = ta.wma(coppock_roc1 + coppock_roc2, 10)

// 50. Know Sure Thing (KST)

kst_roc1 = ta.roc(close, 10)

kst_roc2 = ta.roc(close, 15)

kst_roc3 = ta.roc(close, 20)

kst_roc4 = ta.roc(close, 30)

kst = ta.sma(kst_roc1, 10) + 2*ta.sma(kst_roc2, 10) + 3*ta.sma(kst_roc3, 10) + 4*ta.sma(kst_roc4, 15)

// 51. Percentage Price Oscillator (PPO)

ppo_line = ((ta.ema(close, 12) - ta.ema(close, 26)) / ta.ema(close, 26)) * 100

ppo_signal = ta.ema(ppo_line, 9)

ppo_histogram = ppo_line - ppo_signal

// |----- PLOT MAIN INDICATORS -----| //

// Plot key momentum indicators

plot(rsi_centered, title="01_RSI_Centered", color=color.purple, linewidth=1)

plot(stoch_centered, title="02_Stoch_Centered", color=color.blue, linewidth=1)

plot(williams_r, title="03_Williams_R", color=color.red, linewidth=1)

plot(macd_histogram, title="04_MACD_Histogram", color=color.orange, linewidth=1)

plot(cci, title="05_CCI", color=color.green, linewidth=1)

// Plot trend indicators

plot(sma_momentum, title="06_SMA_Momentum", color=color.navy, linewidth=1)

plot(ema_momentum, title="07_EMA_Momentum", color=color.maroon, linewidth=1)

plot(sar_trend, title="08_SAR_Trend", color=color.teal, linewidth=1)

plot(lr_slope, title="09_LR_Slope", color=color.lime, linewidth=1)

plot(mac, title="10_MAC", color=color.fuchsia, linewidth=1)

// Plot volatility indicators

plot(atr_pct, title="11_ATR_Pct", color=color.yellow, linewidth=1)

plot(bb_position, title="12_BB_Position", color=color.aqua, linewidth=1)

plot(kc_position, title="13_KC_Position", color=color.olive, linewidth=1)

plot(std_dev_pct, title="14_StdDev_Pct", color=color.silver, linewidth=1)

plot(bb_width, title="15_BB_Width", color=color.gray, linewidth=1)

// Plot volume indicators

plot(vroc, title="16_VROC", color=color.blue, linewidth=1)

plot(eom_sma, title="17_EOM", color=color.red, linewidth=1)

plot(vol_osc, title="18_Vol_Osc", color=color.green, linewidth=1)

plot(force_index_sma, title="19_Force_Index", color=color.orange, linewidth=1)

plot(obv, title="20_OBV", color=color.purple, linewidth=1)

// Plot additional oscillators

plot(ao, title="21_Awesome_Osc", color=color.navy, linewidth=1)

plot(cmo, title="22_CMO", color=color.maroon, linewidth=1)

plot(dpo, title="23_DPO", color=color.teal, linewidth=1)

plot(trix, title="24_TRIX", color=color.lime, linewidth=1)

plot(fisher, title="25_Fisher", color=color.fuchsia, linewidth=1)

// Plot more momentum indicators

plot(mfi_centered, title="26_MFI_Centered", color=color.yellow, linewidth=1)

plot(ac, title="27_AC", color=color.aqua, linewidth=1)

plot(ppo_pct, title="28_PPO_Pct", color=color.olive, linewidth=1)

plot(stoch_rsi_centered, title="29_StochRSI_Centered", color=color.silver, linewidth=1)

plot(klinger, title="30_Klinger", color=color.gray, linewidth=1)

// Plot trend continuation

plot(tii, title="31_TII", color=color.blue, linewidth=1)

plot(ichimoku_signal, title="32_Ichimoku_Signal", color=color.red, linewidth=1)

plot(mama_momentum, title="33_MAMA_Momentum", color=color.green, linewidth=1)

plot(zlema_momentum, title="34_ZLEMA_Momentum", color=color.orange, linewidth=1)

plot(bop, title="35_BOP", color=color.purple, linewidth=1)

// Plot volume continuation

plot(nvi, title="36_NVI", color=color.navy, linewidth=1)

plot(pvi, title="37_PVI", color=color.maroon, linewidth=1)

plot(momentum_pct, title="38_Momentum_Pct", color=color.teal, linewidth=1)

plot(roc, title="39_ROC", color=color.lime, linewidth=1)

plot(rvi, title="40_RVI", color=color.fuchsia, linewidth=1)

// Plot volatility continuation

plot(dc_position, title="41_DC_Position", color=color.yellow, linewidth=1)

plot(rvi_volatility, title="42_RVI_Volatility", color=color.aqua, linewidth=1)

plot(hv, title="43_Historical_Vol", color=color.olive, linewidth=1)

plot(gk_volatility, title="44_GK_Volatility", color=color.silver, linewidth=1)

plot(parkinson, title="45_Parkinson_Vol", color=color.gray, linewidth=1)

// Plot final oscillators

plot(rogers_satchell, title="46_RS_Volatility", color=color.blue, linewidth=1)

plot(elder_power, title="47_Elder_Power", color=color.red, linewidth=1)

plot(stc, title="48_STC", color=color.green, linewidth=1)

plot(coppock, title="49_Coppock", color=color.orange, linewidth=1)

plot(kst, title="50_KST", color=color.purple, linewidth=1)

// Plot final indicators

plot(ppo_histogram, title="51_PPO_Histogram", color=color.navy, linewidth=1)

plot(pvt, title="52_PVT", color=color.maroon, linewidth=1)

// |----- Reference Lines -----| //

hline(0, "Zero Line", color=color.gray, linestyle=hline.style_dashed, linewidth=1)

hline(50, "Midline", color=color.gray, linestyle=hline.style_dotted, linewidth=1)

hline(-50, "Lower Midline", color=color.gray, linestyle=hline.style_dotted, linewidth=1)

hline(25, "Upper Threshold", color=color.gray, linestyle=hline.style_dotted, linewidth=1)

hline(-25, "Lower Threshold", color=color.gray, linestyle=hline.style_dotted, linewidth=1)

// |----- Enhanced Information Table -----| //

if show_table and barstate.islast

table_position = position.top_right

table_text_size = table_size == "Tiny" ? size.tiny : table_size == "Small" ? size.small : size.normal

var table info_table = table.new(table_position, 3, 18, bgcolor=color.new(color.white, 85), border_width=1, border_color=color.gray)

// Headers

table.cell(info_table, 0, 0, 'Category', text_color=color.black, text_size=table_text_size, bgcolor=color.new(color.blue, 70))

table.cell(info_table, 1, 0, 'Indicator', text_color=color.black, text_size=table_text_size, bgcolor=color.new(color.blue, 70))

table.cell(info_table, 2, 0, 'Value', text_color=color.black, text_size=table_text_size, bgcolor=color.new(color.blue, 70))

// Key Momentum Indicators

table.cell(info_table, 0, 1, 'MOMENTUM', text_color=color.purple, text_size=table_text_size, bgcolor=color.new(color.purple, 90))

table.cell(info_table, 1, 1, 'RSI Centered', text_color=color.purple, text_size=table_text_size)

table.cell(info_table, 2, 1, str.tostring(rsi_centered, '0.00'), text_color=color.purple, text_size=table_text_size)

table.cell(info_table, 0, 2, '', text_color=color.blue, text_size=table_text_size)

table.cell(info_table, 1, 2, 'Stoch Centered', text_color=color.blue, text_size=table_text_size)

table.cell(info_table, 2, 2, str.tostring(stoch_centered, '0.00'), text_color=color.blue, text_size=table_text_size)

table.cell(info_table, 0, 3, '', text_color=color.red, text_size=table_text_size)

table.cell(info_table, 1, 3, 'Williams %R', text_color=color.red, text_size=table_text_size)

table.cell(info_table, 2, 3, str.tostring(williams_r, '0.00'), text_color=color.red, text_size=table_text_size)

table.cell(info_table, 0, 4, '', text_color=color.orange, text_size=table_text_size)

table.cell(info_table, 1, 4, 'MACD Histogram', text_color=color.orange, text_size=table_text_size)

table.cell(info_table, 2, 4, str.tostring(macd_histogram, '0.000'), text_color=color.orange, text_size=table_text_size)

table.cell(info_table, 0, 5, '', text_color=color.green, text_size=table_text_size)

table.cell(info_table, 1, 5, 'CCI', text_color=color.green, text_size=table_text_size)

table.cell(info_table, 2, 5, str.tostring(cci, '0.00'), text_color=color.green, text_size=table_text_size)

// Key Trend Indicators

table.cell(info_table, 0, 6, 'TREND', text_color=color.navy, text_size=table_text_size, bgcolor=color.new(color.navy, 90))

table.cell(info_table, 1, 6, 'SMA Momentum %', text_color=color.navy, text_size=table_text_size)