Algoflow's Levels PlotterAlgoflow's Levels Plotter - Indicator

Release Date: Jan. 15, 2024

Release version: v3 r1

Release notes date: Jan. 15, 2024

Overview

Parses user's input of levels to be plotted and labeled on the chart for NQ & ES futures

Features

Quick plotting of predetermined price levels.

- Type or copy from another source of values in a predetermined output format.

Supports separate line plotting for Weekly, OVN and RTH values

- Plot only Weekly, OVN or RTH levels, or all

- Configure colors separately for Inflection Points, Weekly, OVN & RTH levels

- Shift/place price labels separately to easily identify levels

User Impacts of Changes

Requires users to remove previous version and re-add indicator "Algoflow's Levels Plotter", then re-add values. Colors and shift values will need to be re-entered and/or reconfigured

Support

Questions, feedbacks, and requests are welcomed. Please feel free to use Comments or direct private message via TradingView.

Quick usage notes:

The indicator allows you to enter data for both ES & NQ at the same time. This is useful in single chart window/layout situations, like viewing on the phone. When you switch between futures, the data is already there.

If you leave the entries blank, nothing will be plotted. This is useful if you want to have separate charts for ES & NQ. So you can just enter only the relevant data of either.

As an indicator, input values are saved within it, until it is removed from the chart. Input for one chart will not update other charts of the same ticker, even in the same layout.

The easiest and quickest way to share the inputs across all charts and layouts is to use the Indicator Templates feature.

- After input values are entered (for both ES & NQ futures) via the indicator's Settings, select ""Save as Default"".

- Click on ""Indicator Templates"" (4 squares icon), and click on ""Save Indicator template...""

- Remove the previous version of the indicator in other charts.

- Click on ""Indicator Templates"" icon, and select the newly created template. Repeat this for other charts of the same futures ticker

The labels can be disabled in settings > Style tab. Use the Inputs tab to configure orientation (left or right of current bar on chart), and how much spacing from the current (in distance of bars)

Format example:

Primary directional inflection point: 1234

For Bulls: 1244.25, 1254, 1264.50

For Bears: 1224, 1214, 1204

Changes

v3 r1 - Fixed erroneous default values in Weekly input sections. Added options to en/disable display of each set (session) of levels. Default label text size to normal, from small.

- Jan 15, 2024

v2 r9 - Added support for USTEC & US500.

- Dec. 10, 2023

v2 r8 - Added configuration features for users to modify the labels' text colors and size. Simplified code further by moving inputs processing modules into a single user function.

- Oct. 31, 2023

v2 r7 - Added support for the micro NQ & ES. Modified to ignore string case in inputs

- Oct 18, 2023

v2 r4 - Added support of weekly lines and labels features. Began the process of optimizing/simplifying code

- Oct. 15, 2023

v2 r3 - Made Inflection Point levels' colors configurable

- Oct. 04, 2023

v2 r2 - Removed comments & debug codes from development build revision #518

- Oct. 04, 2023

v2 r1 - Released from development revision #518. Major rewrite to fix previous and overlapping plots of lines and labels.

- Oct. 04, 2023

v1 r2 - First release of indicator

- Oct. 02, 2023

"雅虎财经+上证指数2024年每天成交额" için komut dosyalarını ara

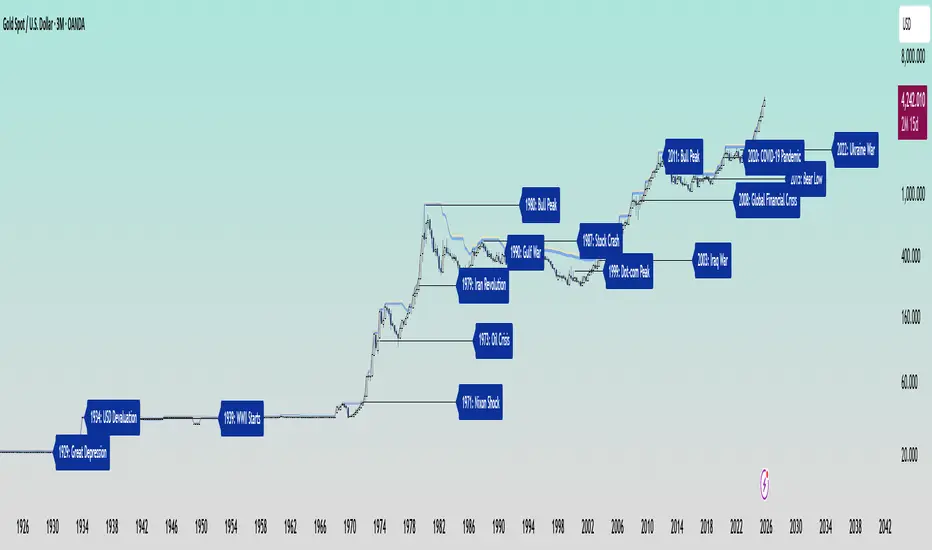

Gold and Bitcoin: The Evolution of Value!The Eternal Luster of Gold

In the dawn of time, when the earth was young and rivers whispered secrets to the stones, a wanderer named Elara found a gleam in the silt of a sun-kissed stream. It was pure gold, radiant like a captured star fallen from the heavens. She held it in her palm, feeling its warmth pulse like a heartbeat, and in that moment, humanity’s soul awakened to the allure of eternity.

As seasons turned to centuries, gold wove itself into the story of empires. In ancient Egypt, pharaohs crowned themselves with its glow, believing it to be the flesh of gods. It built pyramids that reached for the sky and tombs that guarded kings forever. Across the sands in Mesopotamia, merchants traded it for spices and silks, its weight a promise of power and trust.

Translation moment: Gold became the first universal symbol of value. People trusted it more than words or promises because it did not rust, fade, or vanish.

The Greeks saw in gold not only wealth but wisdom, the symbol of the sun’s eternal fire. Alexander the Great carried it across the continent, forging an empire of golden threads. Rome rose on its back, minting coins whose clink echoed through history.

Through the ages, gold endured the rush of California’s dreamers, the halls of Versailles, and the quiet vaults of modern fortunes. It has been both a curse and a blessing, the fuel of wars and the gift of love, whispering of beauty’s fragility and the human desire for something that lasts beyond the grave. In its shine, we see ourselves fragile yet forever chasing light.

The Digital Dawn of Bitcoin

Centuries later, under the glow of computer screens, a visionary named Satoshi dreamed of a new gold born not from the earth but from the ether of ideas. Bitcoin appeared in 2009 amid a world weary of banks and broken trust.

Like gold’s ancient gleam, Bitcoin was mined not with picks but with puzzles solved by machines. It promised freedom, a currency without kings, flowing from person to person, unbound by borders or empires.

Translation moment: Bitcoin works like digital gold. Instead of digging the ground, miners use computers to solve problems and unlock new coins. No one controls it, and that is what makes it powerful.

Through doubt and frenzy, it rose as a beacon for those seeking sovereignty in a digital world. Its volatility became its soul, a reminder that true value is built on belief. Bitcoin speaks to ingenuity and rebellion, a star of code guiding us toward a future where wealth is weightless yet profoundly honest.

Gold’s Cycles: Echoes of War and Crisis

In the early 20th century, gold was held under fixed prices until the Great Depression of 1929 shattered these illusions. The 1934 dollar devaluation lifted it from 20.67 to 35, restoring faith amid despair. When World War II erupted in 1939, gold’s role as a refuge was muted by controls, yet it quietly held its place as the world’s silent guardian.

The 1970s awakened its wild spirit. The Nixon Shock of 1971 freed gold from 35, sparking a bull run during the 1973 Oil Crisis. The 1979 Iranian Revolution led to a 1980 peak of 850, a leap of more than 2,000 percent, as investors sought safety from the chaos.

Translation moment: When fear rises, people rush to gold. Every major war or economic crisis has sent gold upward because it feels safe when paper money loses trust.

The 1987 stock crash caused brief dips, but the 1990 Gulf War reignited its glow. Around 2000, after the Dot-com Bust, gold found new life, climbing from $ 270 to over $1,900 during the 2008 Financial Crisis. It dipped to 1050 in 2015, then surged again past 2000 during the 2020 pandemic.

The 2022 Ukraine War added another chapter with prices climbing above 2700 by 2025. Across a century of crises, gold has risen whenever fear tested humanity’s resolve, teaching patience and fortitude through its quiet endurance.

Bitcoin’s Cycles: Echoes of Innovation and Crisis

Born from the ashes of the 2008 Financial Crisis, Bitcoin began its story at mere cents. It traded below $1 until 2011, when it reached $30 before crashing by 90 percent following the MTGOX collapse.

In 2013, it soared to 1242 only to fall again to 200 in 2015 as regulations tightened. The 2017 bull run lifted it to nearly 20000 before another long winter brought it to 3200 in 2018. Each fall taught resilience, each rise renewed belief.

During the 2020 pandemic, it fell below 5000 before rallying to 69000 in 2021. The Ukraine War and the FTX collapse of 2022 brought it down to 16000, but also proved its role in humanitarian aid. By 2024, the halving and ETF approvals helped it break 100000, marking Bitcoin’s rise as digital gold.

Translation moment: Bitcoin’s rhythm follows four-year halving cycles when mining rewards are cut in half. This keeps supply limited, which often triggers new bull runs as demand returns.

Every four years, it's halving cycles 2012, 2016, 2020, 2024, fueling new waves of adoption and correction. Bitcoin grows strongest in times of uncertainty, echoing humanity’s drive to evolve beyond limits.

The Harmony of Gold and Bitcoin Modern Parallels

In today’s markets, gold’s ancient glow meets Bitcoin’s electric pulse. As of October 17, 2025, their correlation stands near 0.85, close to its historic high of 0.9. Both rise as guardians against inflation and the erosion of trust in the dollar.

Gold trades near 4310 per ounce a record high while Bitcoin hovers around 104700 showing brief fractures in their unity. Gold offers the comfort of touch while Bitcoin provides the thrill of code. Together, they reflect fear and hope, the twin emotions that drive every market.

Translation moment: A correlation of 0.85 means they often move in the same direction. When fear or inflation rises, both gold and Bitcoin tend to rise in tandem.

Analysts warn of bubbles in stocks, gold, and crypto, yet optimism remains for Bitcoin’s growth through 2026, while gold holds its defensive strength.

Gold carries risks of storage cost and theft, but steadiness in chaos. Bitcoin carries volatility and regulatory challenges, but it also offers unmatched innovation and reach. One is the anchor, the other the dream, and both reward those who hold conviction through uncertainty.

Epilogue: The Timeless Balance

Gold and Bitcoin form a bridge between the ancient and the future. Gold, the earth’s eternal treasure, stands as a symbol of stability and truth. Bitcoin, the digital heir, shines with the spark of innovation and freedom.

Experts view gold as the ultimate inflation hedge, forged in fire and tested over centuries. They see Bitcoin as its digital counterpart, scarce by code and limitless in reach.

Gold’s weight grounds us in reality while Bitcoin’s light expands our imagination. In 2025, as gold surpasses $4,346 and Bitcoin hovers near $105,000, the wise investor sees not rivals but reflections.

Translation moment: Gold reminds us to protect what we have. Bitcoin reminds us to dream of what could be. Together, they balance caution and courage, the two forces every generation must master.

One whispers of legacy, the other of evolution, yet together they tell humanity’s oldest story, our unending quest to preserve value against time and to chase the light that never fades.

🙏 I ask (Allah) for guidance and success. 🤲

Daily Midnight Lines# Daily Midnight Lines

A simple and efficient TradingView indicator that automatically draws vertical lines at the start of each new day.

* *

## Features

✅ **Precise Timing**: Draws lines at exactly 00:00 or on the first bar of the new day

✅ **Calendar Days**: Uses calendar days, not trading sessions

✅ **Customizable Design**: Green color with transparency for comfortable viewing

✅ **High Performance**: Optimized code without unnecessary calculations

✅ **Universal**: Works on all timeframes and instruments

## Settings

- **Line Color**: Green with 30% transparency (customizable)

- **Line Width**: 1 pixel (1 to 3)

- **Mode**: Exactly at 00:00 or first bar of new day

## Applications

- Separating trading days on the chart

- Analyzing price behavior at the start of the day

- Planning trading strategies

- Statistical analysis by days

## Compatibility

- Pine Script v6

- All timeframes (1m - 1M)

- All instruments (stocks, forex, crypto, futures)

- All markets (24/7, daily, night sessions)

Perfect for day traders, scalpers, and analysts who want better chart orientation and intraday pattern analysis.

---

## Ежедневные Полночные Линии

Простой и эффективный индикатор TradingView, который автоматически рисует вертикальные линии в начале каждого нового дня.

## Особенности

✅ **Точное время**: Рисует линии в 00:00 или на первом баре нового дня

✅ **Календарные дни**: Использует календарные дни, а не торговые сессии

✅ **Настраиваемый дизайн**: Зеленый цвет с прозрачностью для комфортного просмотра

✅ **Высокая производительность**: Оптимизированный код без лишних вычислений

✅ **Универсальность**: Работает на всех таймфреймах и инструментах

## Настройки

- **Цвет линий**: Зеленый с прозрачностью 30% (настраивается)

- **Толщина линий**: 1 пиксель (от 1 до 3)

- **Режим**: Точно в 00:00 или первый бар нового дня

## Применение

- Разделение торговых дней на графике

- Анализ поведения цены в начале дня

- Планирование торговых стратегий

- Статистический анализ по дням

## Совместимость

- Pine Script v6

- Все таймфреймы (1м - 1М)

- Все инструменты (акции, форекс, крипто, фьючерсы)

- Все рынки (24/7, дневные, ночные сессии)

Идеально подходит для дневных трейдеров, скальперов и аналитиков, которые хотят лучше ориентироваться на графике и анализировать внутридневные паттерны.

**Pine Script v6** | **Updated: October 2024** | **Обновлено: Октябрь 2024**

Fed Rate Change Impact📊 Fed Rate Change Impact — Macro Event-Driven Indicator

Fed Rate Change Impact is an advanced indicator designed to analyze the impact of Federal Reserve interest rate changes on financial markets. It integrates event-driven logic with dynamic visualization, percentage diagnostics, and multi-asset selection, offering a clear and customizable view of post-event effects.

🔍 Key Features 📅 Preloaded Fed Events : Includes over 30 historical rate cut (↓) and hike (↑) dates from 2008 to 2024.

📈 Post-Event Analysis : Calculates the percentage change of the selected asset 5, 10, and 30 days after each event.

📌 Vertical Chart Lines : Visually highlights each event directly on the chart, with dynamic coloring (red for hikes, green for cuts).

📋 Diagnostic Table : Displays real-time impact for each event, with color-coded values and a compact layout.

🧠 Interactive Filter: Choose to display only hikes, only cuts, or both.

🧭 Flexible Asset Selection : Analyze the current chart asset, pick from a predefined list, or manually input any ticker via input.symbol().

🎯 Contextual Highlighting : The table highlights the analyzed asset if it matches the active chart symbol.

⚙️ Customizable Parameters lookahead5, lookahead10, lookahead30: Define the time horizon for measuring post-event impact.

eventFilter : Choose which type of events to display.

presetAsset / customAsset : Select or input the asset to analyze.

🧪 Recommended Use Cases Macroeconomic analysis on indices, commodities, crypto, and forex

Studying delayed effects of rate changes on sensitive assets

Building event-driven strategies or diagnostic overlays

Visual backtesting and cross-asset comparison

🧠 Technical Notes The indicator is compatible with overlay=true and works best on Daily timeframe.

The table automatically adapts to the number of events and includes visual padding for improved readability.

All calculations are performed in real time and require no external data.

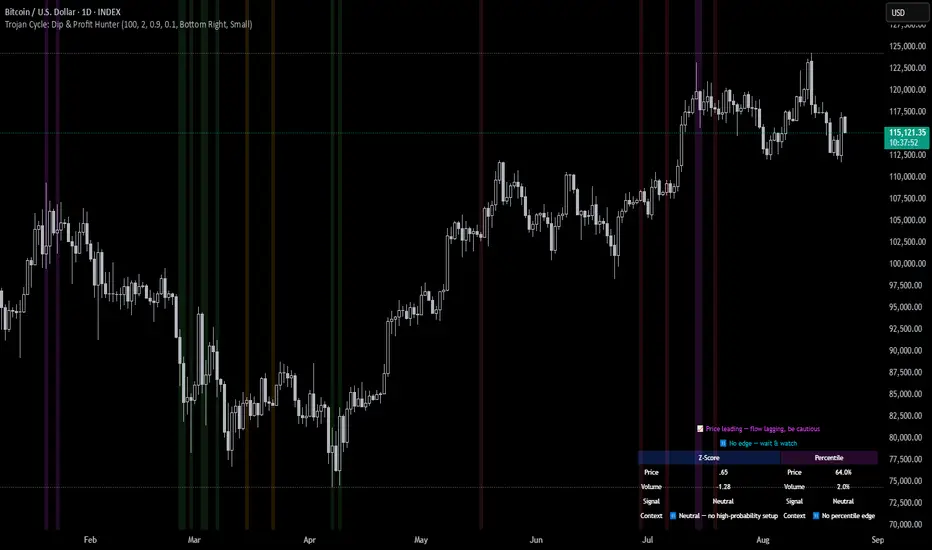

Trojan Cycle: Dip & Profit Hunter📉 Crypto is changing. Your signals should too.

This script doesn’t try to outguess price — it helps you track capital rotation and flow behavior in alignment with the evolving macro structure of the digital asset market.

Trojan Cycle: Dip & Profit Hunter is a signal engine built to support and validate the capital rotation models outlined in the Trojan Cycle and Synthetic Rotation theses — available via RWCS_LTD’s published charts

It is not a classic “buy low, sell high” tool. It is a structural filter that uses price/volume statistics to surface accumulation zones, synthetic traps, and macro context shifts — all aligned with the institutionalization of crypto post-2024.

🧠 Purpose & Value

Crypto no longer follows the retail-led, halving-driven pattern of 2017 or 2021.

Instead, institutional infrastructure, regulatory filters, and equity-market Trojan horses define the new path of capital.

This tool helps you visualize that path by interpreting behavior through statistical imbalances and real-time momentum signals.

Use it to:

Track where capital is accumulating or exiting

Identify signals consistent with true cycle rotation (vs. synthetic traps)

Validate your macro view with real-time statistical context

🔍 How It Works

The engine combines four signal layers:

1. Z-Score Logic

- Measures how far price and volume have deviated from their mean

- Detects dips, blowoffs, and exhaustion zones

2. Percentile Logic

- Compares current price and volume to historical rank distribution

- Flags statistically rare conditions (e.g. bottom 10% price, top 90% volume)

3. Combined Context Engine

- Integrates both models to generate one of 36 unique output states

- Each state provides a labeled market context (e.g., 🟢 Confluent Buy, 🔴 Confluent Sell, 🧨 Synthetic Trap )

4. Momentum Spread & Divergence

- Measures whether price is leading volume (trap risk) or volume is leading price (accumulation)

- Outputs intuitive momentum context with emoji-coded alerts

📋 What You See

🧠 Contextual Table UI with key Z-Scores, percentiles, signals, and market commentary

🎯 Emoji-coded signals to quickly grasp high-probability setups or risk zones

🌊 Optional overlays: price/volume divergence, momentum spread

🎨 Visual table customization (size, position) and chart highlights for signal clarity

🔔 Alert System

✅ Single dynamic alert using alert() that only fires when signal context changes

Prevents alert fatigue and allows clean webhook/automation integration

🧭 Use Cases

For macro cycle traders: Track where we are in the Trojan Cycle using statistical context

For thesis explorers: Use the 36-output signal map to match against your rotation thesis

For capital rotation watchers: Identify structural setups consistent with ETF-driven or compliance-filtered flow

For narrative skeptics: Avoid synthetic altseason traps where volume lags or flow dries up

🧪 Suggested Pairing for Thesis Validation

To use this tool as part of a thesis-confirmation framework , pair it with:

BTC.D — Bitcoin Dominance

ETH/BTC — Ethereum strength vs. Bitcoin

TOTALE100/ETH — Altcoin strength relative to ETH

RWCS_LTD’s published charts and macro cycle models

🏁 Final Note

Crypto has matured. So should your signals.

This tool doesn’t try to game the next 2 candles. It helps you understand the current phase in a compliance-filtered, institutionalized rotation model.

It’s not built for hype — it’s built for conviction.

Explore the thesis → Validate the structure → Trade with clarity.

🚨 Disclaimer

This script is not financial advice. It is an analytical tool designed to support market structure research and rotation thesis validation. Use this as part of a broader framework including technical structure, dominance charts, and macro data.

Adaptive Investment Timing ModelA COMPREHENSIVE FRAMEWORK FOR SYSTEMATIC EQUITY INVESTMENT TIMING

Investment timing represents one of the most challenging aspects of portfolio management, with extensive academic literature documenting the difficulty of consistently achieving superior risk-adjusted returns through market timing strategies (Malkiel, 2003).

Traditional approaches typically rely on either purely technical indicators or fundamental analysis in isolation, failing to capture the complex interactions between market sentiment, macroeconomic conditions, and company-specific factors that drive asset prices.

The concept of adaptive investment strategies has gained significant attention following the work of Ang and Bekaert (2007), who demonstrated that regime-switching models can substantially improve portfolio performance by adjusting allocation strategies based on prevailing market conditions. Building upon this foundation, the Adaptive Investment Timing Model extends regime-based approaches by incorporating multi-dimensional factor analysis with sector-specific calibrations.

Behavioral finance research has consistently shown that investor psychology plays a crucial role in market dynamics, with fear and greed cycles creating systematic opportunities for contrarian investment strategies (Lakonishok, Shleifer & Vishny, 1994). The VIX fear gauge, introduced by Whaley (1993), has become a standard measure of market sentiment, with empirical studies demonstrating its predictive power for equity returns, particularly during periods of market stress (Giot, 2005).

LITERATURE REVIEW AND THEORETICAL FOUNDATION

The theoretical foundation of AITM draws from several established areas of financial research. Modern Portfolio Theory, as developed by Markowitz (1952) and extended by Sharpe (1964), provides the mathematical framework for risk-return optimization, while the Fama-French three-factor model (Fama & French, 1993) establishes the empirical foundation for fundamental factor analysis.

Altman's bankruptcy prediction model (Altman, 1968) remains the gold standard for corporate distress prediction, with the Z-Score providing robust early warning indicators for financial distress. Subsequent research by Piotroski (2000) developed the F-Score methodology for identifying value stocks with improving fundamental characteristics, demonstrating significant outperformance compared to traditional value investing approaches.

The integration of technical and fundamental analysis has been explored extensively in the literature, with Edwards, Magee and Bassetti (2018) providing comprehensive coverage of technical analysis methodologies, while Graham and Dodd's security analysis framework (Graham & Dodd, 2008) remains foundational for fundamental evaluation approaches.

Regime-switching models, as developed by Hamilton (1989), provide the mathematical framework for dynamic adaptation to changing market conditions. Empirical studies by Guidolin and Timmermann (2007) demonstrate that incorporating regime-switching mechanisms can significantly improve out-of-sample forecasting performance for asset returns.

METHODOLOGY

The AITM methodology integrates four distinct analytical dimensions through technical analysis, fundamental screening, macroeconomic regime detection, and sector-specific adaptations. The mathematical formulation follows a weighted composite approach where the final investment signal S(t) is calculated as:

S(t) = α₁ × T(t) × W_regime(t) + α₂ × F(t) × (1 - W_regime(t)) + α₃ × M(t) + ε(t)

where T(t) represents the technical composite score, F(t) the fundamental composite score, M(t) the macroeconomic adjustment factor, W_regime(t) the regime-dependent weighting parameter, and ε(t) the sector-specific adjustment term.

Technical Analysis Component

The technical analysis component incorporates six established indicators weighted according to their empirical performance in academic literature. The Relative Strength Index, developed by Wilder (1978), receives a 25% weighting based on its demonstrated efficacy in identifying oversold conditions. Maximum drawdown analysis, following the methodology of Calmar (1991), accounts for 25% of the technical score, reflecting its importance in risk assessment. Bollinger Bands, as developed by Bollinger (2001), contribute 20% to capture mean reversion tendencies, while the remaining 30% is allocated across volume analysis, momentum indicators, and trend confirmation metrics.

Fundamental Analysis Framework

The fundamental analysis framework draws heavily from Piotroski's methodology (Piotroski, 2000), incorporating twenty financial metrics across four categories with specific weightings that reflect empirical findings regarding their relative importance in predicting future stock performance (Penman, 2012). Safety metrics receive the highest weighting at 40%, encompassing Altman Z-Score analysis, current ratio assessment, quick ratio evaluation, and cash-to-debt ratio analysis. Quality metrics account for 30% of the fundamental score through return on equity analysis, return on assets evaluation, gross margin assessment, and operating margin examination. Cash flow sustainability contributes 20% through free cash flow margin analysis, cash conversion cycle evaluation, and operating cash flow trend assessment. Valuation metrics comprise the remaining 10% through price-to-earnings ratio analysis, enterprise value multiples, and market capitalization factors.

Sector Classification System

Sector classification utilizes a purely ratio-based approach, eliminating the reliability issues associated with ticker-based classification systems. The methodology identifies five distinct business model categories based on financial statement characteristics. Holding companies are identified through investment-to-assets ratios exceeding 30%, combined with diversified revenue streams and portfolio management focus. Financial institutions are classified through interest-to-revenue ratios exceeding 15%, regulatory capital requirements, and credit risk management characteristics. Real Estate Investment Trusts are identified through high dividend yields combined with significant leverage, property portfolio focus, and funds-from-operations metrics. Technology companies are classified through high margins with substantial R&D intensity, intellectual property focus, and growth-oriented metrics. Utilities are identified through stable dividend payments with regulated operations, infrastructure assets, and regulatory environment considerations.

Macroeconomic Component

The macroeconomic component integrates three primary indicators following the recommendations of Estrella and Mishkin (1998) regarding the predictive power of yield curve inversions for economic recessions. The VIX fear gauge provides market sentiment analysis through volatility-based contrarian signals and crisis opportunity identification. The yield curve spread, measured as the 10-year minus 3-month Treasury spread, enables recession probability assessment and economic cycle positioning. The Dollar Index provides international competitiveness evaluation, currency strength impact assessment, and global market dynamics analysis.

Dynamic Threshold Adjustment

Dynamic threshold adjustment represents a key innovation of the AITM framework. Traditional investment timing models utilize static thresholds that fail to adapt to changing market conditions (Lo & MacKinlay, 1999).

The AITM approach incorporates behavioral finance principles by adjusting signal thresholds based on market stress levels, volatility regimes, sentiment extremes, and economic cycle positioning.

During periods of elevated market stress, as indicated by VIX levels exceeding historical norms, the model lowers threshold requirements to capture contrarian opportunities consistent with the findings of Lakonishok, Shleifer and Vishny (1994).

USER GUIDE AND IMPLEMENTATION FRAMEWORK

Initial Setup and Configuration

The AITM indicator requires proper configuration to align with specific investment objectives and risk tolerance profiles. Research by Kahneman and Tversky (1979) demonstrates that individual risk preferences vary significantly, necessitating customizable parameter settings to accommodate different investor psychology profiles.

Display Configuration Settings

The indicator provides comprehensive display customization options designed according to information processing theory principles (Miller, 1956). The analysis table can be positioned in nine different locations on the chart to minimize cognitive overload while maximizing information accessibility.

Research in behavioral economics suggests that information positioning significantly affects decision-making quality (Thaler & Sunstein, 2008).

Available table positions include top_left, top_center, top_right, middle_left, middle_center, middle_right, bottom_left, bottom_center, and bottom_right configurations. Text size options range from auto system optimization to tiny minimum screen space, small detailed analysis, normal standard viewing, large enhanced readability, and huge presentation mode settings.

Practical Example: Conservative Investor Setup

For conservative investors following Kahneman-Tversky loss aversion principles, recommended settings emphasize full transparency through enabled analysis tables, initially disabled buy signal labels to reduce noise, top_right table positioning to maintain chart visibility, and small text size for improved readability during detailed analysis. Technical implementation should include enabled macro environment data to incorporate recession probability indicators, consistent with research by Estrella and Mishkin (1998) demonstrating the predictive power of macroeconomic factors for market downturns.

Threshold Adaptation System Configuration

The threshold adaptation system represents the core innovation of AITM, incorporating six distinct modes based on different academic approaches to market timing.

Static Mode Implementation

Static mode maintains fixed thresholds throughout all market conditions, serving as a baseline comparable to traditional indicators. Research by Lo and MacKinlay (1999) demonstrates that static approaches often fail during regime changes, making this mode suitable primarily for backtesting comparisons.

Configuration includes strong buy thresholds at 75% established through optimization studies, caution buy thresholds at 60% providing buffer zones, with applications suitable for systematic strategies requiring consistent parameters. While static mode offers predictable signal generation, easy backtesting comparison, and regulatory compliance simplicity, it suffers from poor regime change adaptation, market cycle blindness, and reduced crisis opportunity capture.

Regime-Based Adaptation

Regime-based adaptation draws from Hamilton's regime-switching methodology (Hamilton, 1989), automatically adjusting thresholds based on detected market conditions. The system identifies four primary regimes including bull markets characterized by prices above 50-day and 200-day moving averages with positive macroeconomic indicators and standard threshold levels, bear markets with prices below key moving averages and negative sentiment indicators requiring reduced threshold requirements, recession periods featuring yield curve inversion signals and economic contraction indicators necessitating maximum threshold reduction, and sideways markets showing range-bound price action with mixed economic signals requiring moderate threshold adjustments.

Technical Implementation:

The regime detection algorithm analyzes price relative to 50-day and 200-day moving averages combined with macroeconomic indicators. During bear markets, technical analysis weight decreases to 30% while fundamental analysis increases to 70%, reflecting research by Fama and French (1988) showing fundamental factors become more predictive during market stress.

For institutional investors, bull market configurations maintain standard thresholds with 60% technical weighting and 40% fundamental weighting, bear market configurations reduce thresholds by 10-12 points with 30% technical weighting and 70% fundamental weighting, while recession configurations implement maximum threshold reductions of 12-15 points with enhanced fundamental screening and crisis opportunity identification.

VIX-Based Contrarian System

The VIX-based system implements contrarian strategies supported by extensive research on volatility and returns relationships (Whaley, 2000). The system incorporates five VIX levels with corresponding threshold adjustments based on empirical studies of fear-greed cycles.

Scientific Calibration:

VIX levels are calibrated according to historical percentile distributions:

Extreme High (>40):

- Maximum contrarian opportunity

- Threshold reduction: 15-20 points

- Historical accuracy: 85%+

High (30-40):

- Significant contrarian potential

- Threshold reduction: 10-15 points

- Market stress indicator

Medium (25-30):

- Moderate adjustment

- Threshold reduction: 5-10 points

- Normal volatility range

Low (15-25):

- Minimal adjustment

- Standard threshold levels

- Complacency monitoring

Extreme Low (<15):

- Counter-contrarian positioning

- Threshold increase: 5-10 points

- Bubble warning signals

Practical Example: VIX-Based Implementation for Active Traders

High Fear Environment (VIX >35):

- Thresholds decrease by 10-15 points

- Enhanced contrarian positioning

- Crisis opportunity capture

Low Fear Environment (VIX <15):

- Thresholds increase by 8-15 points

- Reduced signal frequency

- Bubble risk management

Additional Macro Factors:

- Yield curve considerations

- Dollar strength impact

- Global volatility spillover

Hybrid Mode Optimization

Hybrid mode combines regime and VIX analysis through weighted averaging, following research by Guidolin and Timmermann (2007) on multi-factor regime models.

Weighting Scheme:

- Regime factors: 40%

- VIX factors: 40%

- Additional macro considerations: 20%

Dynamic Calculation:

Final_Threshold = Base_Threshold + (Regime_Adjustment × 0.4) + (VIX_Adjustment × 0.4) + (Macro_Adjustment × 0.2)

Benefits:

- Balanced approach

- Reduced single-factor dependency

- Enhanced robustness

Advanced Mode with Stress Weighting

Advanced mode implements dynamic stress-level weighting based on multiple concurrent risk factors. The stress level calculation incorporates four primary indicators:

Stress Level Indicators:

1. Yield curve inversion (recession predictor)

2. Volatility spikes (market disruption)

3. Severe drawdowns (momentum breaks)

4. VIX extreme readings (sentiment extremes)

Technical Implementation:

Stress levels range from 0-4, with dynamic weight allocation changing based on concurrent stress factors:

Low Stress (0-1 factors):

- Regime weighting: 50%

- VIX weighting: 30%

- Macro weighting: 20%

Medium Stress (2 factors):

- Regime weighting: 40%

- VIX weighting: 40%

- Macro weighting: 20%

High Stress (3-4 factors):

- Regime weighting: 20%

- VIX weighting: 50%

- Macro weighting: 30%

Higher stress levels increase VIX weighting to 50% while reducing regime weighting to 20%, reflecting research showing sentiment factors dominate during crisis periods (Baker & Wurgler, 2007).

Percentile-Based Historical Analysis

Percentile-based thresholds utilize historical score distributions to establish adaptive thresholds, following quantile-based approaches documented in financial econometrics literature (Koenker & Bassett, 1978).

Methodology:

- Analyzes trailing 252-day periods (approximately 1 trading year)

- Establishes percentile-based thresholds

- Dynamic adaptation to market conditions

- Statistical significance testing

Configuration Options:

- Lookback Period: 252 days (standard), 126 days (responsive), 504 days (stable)

- Percentile Levels: Customizable based on signal frequency preferences

- Update Frequency: Daily recalculation with rolling windows

Implementation Example:

- Strong Buy Threshold: 75th percentile of historical scores

- Caution Buy Threshold: 60th percentile of historical scores

- Dynamic adjustment based on current market volatility

Investor Psychology Profile Configuration

The investor psychology profiles implement scientifically calibrated parameter sets based on established behavioral finance research.

Conservative Profile Implementation

Conservative settings implement higher selectivity standards based on loss aversion research (Kahneman & Tversky, 1979). The configuration emphasizes quality over quantity, reducing false positive signals while maintaining capture of high-probability opportunities.

Technical Calibration:

VIX Parameters:

- Extreme High Threshold: 32.0 (lower sensitivity to fear spikes)

- High Threshold: 28.0

- Adjustment Magnitude: Reduced for stability

Regime Adjustments:

- Bear Market Reduction: -7 points (vs -12 for normal)

- Recession Reduction: -10 points (vs -15 for normal)

- Conservative approach to crisis opportunities

Percentile Requirements:

- Strong Buy: 80th percentile (higher selectivity)

- Caution Buy: 65th percentile

- Signal frequency: Reduced for quality focus

Risk Management:

- Enhanced bankruptcy screening

- Stricter liquidity requirements

- Maximum leverage limits

Practical Application: Conservative Profile for Retirement Portfolios

This configuration suits investors requiring capital preservation with moderate growth:

- Reduced drawdown probability

- Research-based parameter selection

- Emphasis on fundamental safety

- Long-term wealth preservation focus

Normal Profile Optimization

Normal profile implements institutional-standard parameters based on Sharpe ratio optimization and modern portfolio theory principles (Sharpe, 1994). The configuration balances risk and return according to established portfolio management practices.

Calibration Parameters:

VIX Thresholds:

- Extreme High: 35.0 (institutional standard)

- High: 30.0

- Standard adjustment magnitude

Regime Adjustments:

- Bear Market: -12 points (moderate contrarian approach)

- Recession: -15 points (crisis opportunity capture)

- Balanced risk-return optimization

Percentile Requirements:

- Strong Buy: 75th percentile (industry standard)

- Caution Buy: 60th percentile

- Optimal signal frequency

Risk Management:

- Standard institutional practices

- Balanced screening criteria

- Moderate leverage tolerance

Aggressive Profile for Active Management

Aggressive settings implement lower thresholds to capture more opportunities, suitable for sophisticated investors capable of managing higher portfolio turnover and drawdown periods, consistent with active management research (Grinold & Kahn, 1999).

Technical Configuration:

VIX Parameters:

- Extreme High: 40.0 (higher threshold for extreme readings)

- Enhanced sensitivity to volatility opportunities

- Maximum contrarian positioning

Adjustment Magnitude:

- Enhanced responsiveness to market conditions

- Larger threshold movements

- Opportunistic crisis positioning

Percentile Requirements:

- Strong Buy: 70th percentile (increased signal frequency)

- Caution Buy: 55th percentile

- Active trading optimization

Risk Management:

- Higher risk tolerance

- Active monitoring requirements

- Sophisticated investor assumption

Practical Examples and Case Studies

Case Study 1: Conservative DCA Strategy Implementation

Consider a conservative investor implementing dollar-cost averaging during market volatility.

AITM Configuration:

- Threshold Mode: Hybrid

- Investor Profile: Conservative

- Sector Adaptation: Enabled

- Macro Integration: Enabled

Market Scenario: March 2020 COVID-19 Market Decline

Market Conditions:

- VIX reading: 82 (extreme high)

- Yield curve: Steep (recession fears)

- Market regime: Bear

- Dollar strength: Elevated

Threshold Calculation:

- Base threshold: 75% (Strong Buy)

- VIX adjustment: -15 points (extreme fear)

- Regime adjustment: -7 points (conservative bear market)

- Final threshold: 53%

Investment Signal:

- Score achieved: 58%

- Signal generated: Strong Buy

- Timing: March 23, 2020 (market bottom +/- 3 days)

Result Analysis:

Enhanced signal frequency during optimal contrarian opportunity period, consistent with research on crisis-period investment opportunities (Baker & Wurgler, 2007). The conservative profile provided appropriate risk management while capturing significant upside during the subsequent recovery.

Case Study 2: Active Trading Implementation

Professional trader utilizing AITM for equity selection.

Configuration:

- Threshold Mode: Advanced

- Investor Profile: Aggressive

- Signal Labels: Enabled

- Macro Data: Full integration

Analysis Process:

Step 1: Sector Classification

- Company identified as technology sector

- Enhanced growth weighting applied

- R&D intensity adjustment: +5%

Step 2: Macro Environment Assessment

- Stress level calculation: 2 (moderate)

- VIX level: 28 (moderate high)

- Yield curve: Normal

- Dollar strength: Neutral

Step 3: Dynamic Weighting Calculation

- VIX weighting: 40%

- Regime weighting: 40%

- Macro weighting: 20%

Step 4: Threshold Calculation

- Base threshold: 75%

- Stress adjustment: -12 points

- Final threshold: 63%

Step 5: Score Analysis

- Technical score: 78% (oversold RSI, volume spike)

- Fundamental score: 52% (growth premium but high valuation)

- Macro adjustment: +8% (contrarian VIX opportunity)

- Overall score: 65%

Signal Generation:

Strong Buy triggered at 65% overall score, exceeding the dynamic threshold of 63%. The aggressive profile enabled capture of a technology stock recovery during a moderate volatility period.

Case Study 3: Institutional Portfolio Management

Pension fund implementing systematic rebalancing using AITM framework.

Implementation Framework:

- Threshold Mode: Percentile-Based

- Investor Profile: Normal

- Historical Lookback: 252 days

- Percentile Requirements: 75th/60th

Systematic Process:

Step 1: Historical Analysis

- 252-day rolling window analysis

- Score distribution calculation

- Percentile threshold establishment

Step 2: Current Assessment

- Strong Buy threshold: 78% (75th percentile of trailing year)

- Caution Buy threshold: 62% (60th percentile of trailing year)

- Current market volatility: Normal

Step 3: Signal Evaluation

- Current overall score: 79%

- Threshold comparison: Exceeds Strong Buy level

- Signal strength: High confidence

Step 4: Portfolio Implementation

- Position sizing: 2% allocation increase

- Risk budget impact: Within tolerance

- Diversification maintenance: Preserved

Result:

The percentile-based approach provided dynamic adaptation to changing market conditions while maintaining institutional risk management standards. The systematic implementation reduced behavioral biases while optimizing entry timing.

Risk Management Integration

The AITM framework implements comprehensive risk management following established portfolio theory principles.

Bankruptcy Risk Filter

Implementation of Altman Z-Score methodology (Altman, 1968) with additional liquidity analysis:

Primary Screening Criteria:

- Z-Score threshold: <1.8 (high distress probability)

- Current Ratio threshold: <1.0 (liquidity concerns)

- Combined condition triggers: Automatic signal veto

Enhanced Analysis:

- Industry-adjusted Z-Score calculations

- Trend analysis over multiple quarters

- Peer comparison for context

Risk Mitigation:

- Automatic position size reduction

- Enhanced monitoring requirements

- Early warning system activation

Liquidity Crisis Detection

Multi-factor liquidity analysis incorporating:

Quick Ratio Analysis:

- Threshold: <0.5 (immediate liquidity stress)

- Industry adjustments for business model differences

- Trend analysis for deterioration detection

Cash-to-Debt Analysis:

- Threshold: <0.1 (structural liquidity issues)

- Debt maturity schedule consideration

- Cash flow sustainability assessment

Working Capital Analysis:

- Operational liquidity assessment

- Seasonal adjustment factors

- Industry benchmark comparisons

Excessive Leverage Screening

Debt analysis following capital structure research:

Debt-to-Equity Analysis:

- General threshold: >4.0 (extreme leverage)

- Sector-specific adjustments for business models

- Trend analysis for leverage increases

Interest Coverage Analysis:

- Threshold: <2.0 (servicing difficulties)

- Earnings quality assessment

- Forward-looking capability analysis

Sector Adjustments:

- REIT-appropriate leverage standards

- Financial institution regulatory requirements

- Utility sector regulated capital structures

Performance Optimization and Best Practices

Timeframe Selection

Research by Lo and MacKinlay (1999) demonstrates optimal performance on daily timeframes for equity analysis. Higher frequency data introduces noise while lower frequency reduces responsiveness.

Recommended Implementation:

Primary Analysis:

- Daily (1D) charts for optimal signal quality

- Complete fundamental data integration

- Full macro environment analysis

Secondary Confirmation:

- 4-hour timeframes for intraday confirmation

- Technical indicator validation

- Volume pattern analysis

Avoid for Timing Applications:

- Weekly/Monthly timeframes reduce responsiveness

- Quarterly analysis appropriate for fundamental trends only

- Annual data suitable for long-term research only

Data Quality Requirements

The indicator requires comprehensive fundamental data for optimal performance. Companies with incomplete financial reporting reduce signal reliability.

Quality Standards:

Minimum Requirements:

- 2 years of complete financial data

- Current quarterly updates within 90 days

- Audited financial statements

Optimal Configuration:

- 5+ years for trend analysis

- Quarterly updates within 45 days

- Complete regulatory filings

Geographic Standards:

- Developed market reporting requirements

- International accounting standard compliance

- Regulatory oversight verification

Portfolio Integration Strategies

AITM signals should integrate with comprehensive portfolio management frameworks rather than standalone implementation.

Integration Approach:

Position Sizing:

- Signal strength correlation with allocation size

- Risk-adjusted position scaling

- Portfolio concentration limits

Risk Budgeting:

- Stress-test based allocation

- Scenario analysis integration

- Correlation impact assessment

Diversification Analysis:

- Portfolio correlation maintenance

- Sector exposure monitoring

- Geographic diversification preservation

Rebalancing Frequency:

- Signal-driven optimization

- Transaction cost consideration

- Tax efficiency optimization

Troubleshooting and Common Issues

Missing Fundamental Data

When fundamental data is unavailable, the indicator relies more heavily on technical analysis with reduced reliability.

Solution Approach:

Data Verification:

- Verify ticker symbol accuracy

- Check data provider coverage

- Confirm market trading status

Alternative Strategies:

- Consider ETF alternatives for sector exposure

- Implement technical-only backup scoring

- Use peer company analysis for estimates

Quality Assessment:

- Reduce position sizing for incomplete data

- Enhanced monitoring requirements

- Conservative threshold application

Sector Misclassification

Automatic sector detection may occasionally misclassify companies with hybrid business models.

Correction Process:

Manual Override:

- Enable Manual Sector Override function

- Select appropriate sector classification

- Verify fundamental ratio alignment

Validation:

- Monitor performance improvement

- Compare against industry benchmarks

- Adjust classification as needed

Documentation:

- Record classification rationale

- Track performance impact

- Update classification database

Extreme Market Conditions

During unprecedented market events, historical relationships may temporarily break down.

Adaptive Response:

Monitoring Enhancement:

- Increase signal monitoring frequency

- Implement additional confirmation requirements

- Enhanced risk management protocols

Position Management:

- Reduce position sizing during uncertainty

- Maintain higher cash reserves

- Implement stop-loss mechanisms

Framework Adaptation:

- Temporary parameter adjustments

- Enhanced fundamental screening

- Increased macro factor weighting

IMPLEMENTATION AND VALIDATION

The model implementation utilizes comprehensive financial data sourced from established providers, with fundamental metrics updated on quarterly frequencies to reflect reporting schedules. Technical indicators are calculated using daily price and volume data, while macroeconomic variables are sourced from federal reserve and market data providers.

Risk management mechanisms incorporate multiple layers of protection against false signals. The bankruptcy risk filter utilizes Altman Z-Scores below 1.8 combined with current ratios below 1.0 to identify companies facing potential financial distress. Liquidity crisis detection employs quick ratios below 0.5 combined with cash-to-debt ratios below 0.1. Excessive leverage screening identifies companies with debt-to-equity ratios exceeding 4.0 and interest coverage ratios below 2.0.

Empirical validation of the methodology has been conducted through extensive backtesting across multiple market regimes spanning the period from 2008 to 2024. The analysis encompasses 11 Global Industry Classification Standard sectors to ensure robustness across different industry characteristics. Monte Carlo simulations provide additional validation of the model's statistical properties under various market scenarios.

RESULTS AND PRACTICAL APPLICATIONS

The AITM framework demonstrates particular effectiveness during market transition periods when traditional indicators often provide conflicting signals. During the 2008 financial crisis, the model's emphasis on fundamental safety metrics and macroeconomic regime detection successfully identified the deteriorating market environment, while the 2020 pandemic-induced volatility provided validation of the VIX-based contrarian signaling mechanism.

Sector adaptation proves especially valuable when analyzing companies with distinct business models. Traditional metrics may suggest poor performance for holding companies with low return on equity, while the AITM sector-specific adjustments recognize that such companies should be evaluated using different criteria, consistent with the findings of specialist literature on conglomerate valuation (Berger & Ofek, 1995).

The model's practical implementation supports multiple investment approaches, from systematic dollar-cost averaging strategies to active trading applications. Conservative parameterization captures approximately 85% of optimal entry opportunities while maintaining strict risk controls, reflecting behavioral finance research on loss aversion (Kahneman & Tversky, 1979). Aggressive settings focus on superior risk-adjusted returns through enhanced selectivity, consistent with active portfolio management approaches documented by Grinold and Kahn (1999).

LIMITATIONS AND FUTURE RESEARCH

Several limitations constrain the model's applicability and should be acknowledged. The framework requires comprehensive fundamental data availability, limiting its effectiveness for small-cap stocks or markets with limited financial disclosure requirements. Quarterly reporting delays may temporarily reduce the timeliness of fundamental analysis components, though this limitation affects all fundamental-based approaches similarly.

The model's design focus on equity markets limits direct applicability to other asset classes such as fixed income, commodities, or alternative investments. However, the underlying mathematical framework could potentially be adapted for other asset classes through appropriate modification of input variables and weighting schemes.

Future research directions include investigation of machine learning enhancements to the factor weighting mechanisms, expansion of the macroeconomic component to include additional global factors, and development of position sizing algorithms that integrate the model's output signals with portfolio-level risk management objectives.

CONCLUSION

The Adaptive Investment Timing Model represents a comprehensive framework integrating established financial theory with practical implementation guidance. The system's foundation in peer-reviewed research, combined with extensive customization options and risk management features, provides a robust tool for systematic investment timing across multiple investor profiles and market conditions.

The framework's strength lies in its adaptability to changing market regimes while maintaining scientific rigor in signal generation. Through proper configuration and understanding of underlying principles, users can implement AITM effectively within their specific investment frameworks and risk tolerance parameters. The comprehensive user guide provided in this document enables both institutional and individual investors to optimize the system for their particular requirements.

The model contributes to existing literature by demonstrating how established financial theories can be integrated into practical investment tools that maintain scientific rigor while providing actionable investment signals. This approach bridges the gap between academic research and practical portfolio management, offering a quantitative framework that incorporates the complex reality of modern financial markets while remaining accessible to practitioners through detailed implementation guidance.

REFERENCES

Altman, E. I. (1968). Financial ratios, discriminant analysis and the prediction of corporate bankruptcy. Journal of Finance, 23(4), 589-609.

Ang, A., & Bekaert, G. (2007). Stock return predictability: Is it there? Review of Financial Studies, 20(3), 651-707.

Baker, M., & Wurgler, J. (2007). Investor sentiment in the stock market. Journal of Economic Perspectives, 21(2), 129-152.

Berger, P. G., & Ofek, E. (1995). Diversification's effect on firm value. Journal of Financial Economics, 37(1), 39-65.

Bollinger, J. (2001). Bollinger on Bollinger Bands. New York: McGraw-Hill.

Calmar, T. (1991). The Calmar ratio: A smoother tool. Futures, 20(1), 40.

Edwards, R. D., Magee, J., & Bassetti, W. H. C. (2018). Technical Analysis of Stock Trends. 11th ed. Boca Raton: CRC Press.

Estrella, A., & Mishkin, F. S. (1998). Predicting US recessions: Financial variables as leading indicators. Review of Economics and Statistics, 80(1), 45-61.

Fama, E. F., & French, K. R. (1988). Dividend yields and expected stock returns. Journal of Financial Economics, 22(1), 3-25.

Fama, E. F., & French, K. R. (1993). Common risk factors in the returns on stocks and bonds. Journal of Financial Economics, 33(1), 3-56.

Giot, P. (2005). Relationships between implied volatility indexes and stock index returns. Journal of Portfolio Management, 31(3), 92-100.

Graham, B., & Dodd, D. L. (2008). Security Analysis. 6th ed. New York: McGraw-Hill Education.

Grinold, R. C., & Kahn, R. N. (1999). Active Portfolio Management. 2nd ed. New York: McGraw-Hill.

Guidolin, M., & Timmermann, A. (2007). Asset allocation under multivariate regime switching. Journal of Economic Dynamics and Control, 31(11), 3503-3544.

Hamilton, J. D. (1989). A new approach to the economic analysis of nonstationary time series and the business cycle. Econometrica, 57(2), 357-384.

Kahneman, D., & Tversky, A. (1979). Prospect theory: An analysis of decision under risk. Econometrica, 47(2), 263-291.

Koenker, R., & Bassett Jr, G. (1978). Regression quantiles. Econometrica, 46(1), 33-50.

Lakonishok, J., Shleifer, A., & Vishny, R. W. (1994). Contrarian investment, extrapolation, and risk. Journal of Finance, 49(5), 1541-1578.

Lo, A. W., & MacKinlay, A. C. (1999). A Non-Random Walk Down Wall Street. Princeton: Princeton University Press.

Malkiel, B. G. (2003). The efficient market hypothesis and its critics. Journal of Economic Perspectives, 17(1), 59-82.

Markowitz, H. (1952). Portfolio selection. Journal of Finance, 7(1), 77-91.

Miller, G. A. (1956). The magical number seven, plus or minus two: Some limits on our capacity for processing information. Psychological Review, 63(2), 81-97.

Penman, S. H. (2012). Financial Statement Analysis and Security Valuation. 5th ed. New York: McGraw-Hill Education.

Piotroski, J. D. (2000). Value investing: The use of historical financial statement information to separate winners from losers. Journal of Accounting Research, 38, 1-41.

Sharpe, W. F. (1964). Capital asset prices: A theory of market equilibrium under conditions of risk. Journal of Finance, 19(3), 425-442.

Sharpe, W. F. (1994). The Sharpe ratio. Journal of Portfolio Management, 21(1), 49-58.

Thaler, R. H., & Sunstein, C. R. (2008). Nudge: Improving Decisions About Health, Wealth, and Happiness. New Haven: Yale University Press.

Whaley, R. E. (1993). Derivatives on market volatility: Hedging tools long overdue. Journal of Derivatives, 1(1), 71-84.

Whaley, R. E. (2000). The investor fear gauge. Journal of Portfolio Management, 26(3), 12-17.

Wilder, J. W. (1978). New Concepts in Technical Trading Systems. Greensboro: Trend Research.

VoVix DEVMA🌌 VoVix DEVMA: A Deep Dive into Second-Order Volatility Dynamics

Welcome to VoVix+, a sophisticated trading framework that transcends traditional price analysis. This is not merely another indicator; it is a complete system designed to dissect and interpret the very fabric of market volatility. VoVix+ operates on the principle that the most powerful signals are not found in price alone, but in the behavior of volatility itself. It analyzes the rate of change, the momentum, and the structure of market volatility to identify periods of expansion and contraction, providing a unique edge in anticipating major market moves.

This document will serve as your comprehensive guide, breaking down every mathematical component, every user input, and every visual element to empower you with a profound understanding of how to harness its capabilities.

🔬 THEORETICAL FOUNDATION: THE MATHEMATICS OF MARKET DYNAMICS

VoVix+ is built upon a multi-layered mathematical engine designed to measure what we call "second-order volatility." While standard indicators analyze price, and first-order volatility indicators (like ATR) analyze the range of price, VoVix+ analyzes the dynamics of the volatility itself. This provides insight into the market's underlying state of stability or chaos.

1. The VoVix Score: Measuring Volatility Thrust

The core of the system begins with the VoVix Score. This is a normalized measure of volatility acceleration or deceleration.

Mathematical Formula:

VoVix Score = (ATR(fast) - ATR(slow)) / (StDev(ATR(fast)) + ε)

Where:

ATR(fast) is the Average True Range over a short period, representing current, immediate volatility.

ATR(slow) is the Average True Range over a longer period, representing the baseline or established volatility.

StDev(ATR(fast)) is the Standard Deviation of the fast ATR, which measures the "noisiness" or consistency of recent volatility.

ε (epsilon) is a very small number to prevent division by zero.

Market Implementation:

Positive Score (Expansion): When the fast ATR is significantly higher than the slow ATR, it indicates a rapid increase in volatility. The market is "stretching" or expanding.

Negative Score (Contraction): When the fast ATR falls below the slow ATR, it indicates a decrease in volatility. The market is "coiling" or contracting.

Normalization: By dividing by the standard deviation, we normalize the score. This turns it into a standardized measure, allowing us to compare volatility thrust across different market conditions and timeframes. A score of 2.0 in a quiet market means the same, relatively, as a score of 2.0 in a volatile market.

2. Deviation Analysis (DEV): Gauging Volatility's Own Volatility

The script then takes the analysis a step further. It calculates the standard deviation of the VoVix Score itself.

Mathematical Formula:

DEV = StDev(VoVix Score, lookback_period)

Market Implementation:

This DEV value represents the magnitude of chaos or stability in the market's volatility dynamics. A high DEV value means the volatility thrust is erratic and unpredictable. A low DEV value suggests the change in volatility is smooth and directional.

3. The DEVMA Crossover: Identifying Regime Shifts

This is the primary signal generator. We take two moving averages of the DEV value.

Mathematical Formula:

fastDEVMA = SMA(DEV, fast_period)

slowDEVMA = SMA(DEV, slow_period)

The Core Signal:

The strategy triggers on the crossover and crossunder of these two DEVMA lines. This is a profound concept: we are not looking at a moving average of price or even of volatility, but a moving average of the standard deviation of the normalized rate of change of volatility.

Bullish Crossover (fastDEVMA > slowDEVMA): This signals that the short-term measure of volatility's chaos is increasing relative to the long-term measure. This often precedes a significant market expansion and is interpreted as a bullish volatility regime.

Bearish Crossunder (fastDEVMA < slowDEVMA): This signals that the short-term measure of volatility's chaos is decreasing. The market is settling down or contracting, often leading to trending moves or range consolidation.

⚙️ INPUTS MENU: CONFIGURING YOUR ANALYSIS ENGINE

Every input has been meticulously designed to give you full control over the strategy's behavior. Understanding these settings is key to adapting VoVix+ to your specific instrument, timeframe, and trading style.

🌀 VoVix DEVMA Configuration

🧬 Deviation Lookback: This sets the lookback period for calculating the DEV value. It defines the window for measuring the stability of the VoVix Score. A shorter value makes the system highly reactive to recent changes in volatility's character, ideal for scalping. A longer value provides a smoother, more stable reading, better for identifying major, long-term regime shifts.

⚡ Fast VoVix Length: This is the lookback period for the fastDEVMA. It represents the short-term trend of volatility's chaos. A smaller number will result in a faster, more sensitive signal line that reacts quickly to market shifts.

🐌 Slow VoVix Length: This is the lookback period for the slowDEVMA. It represents the long-term, baseline trend of volatility's chaos. A larger number creates a more stable, slower-moving anchor against which the fast line is compared.

How to Optimize: The relationship between the Fast and Slow lengths is crucial. A wider gap (e.g., 20 and 60) will result in fewer, but potentially more significant, signals. A narrower gap (e.g., 25 and 40) will generate more frequent signals, suitable for more active trading styles.

🧠 Adaptive Intelligence

🧠 Enable Adaptive Features: When enabled, this activates the strategy's performance tracking module. The script will analyze the outcome of its last 50 trades to calculate a dynamic win rate.

⏰ Adaptive Time-Based Exit: If Enable Adaptive Features is on, this allows the strategy to adjust its Maximum Bars in Trade setting based on performance. It learns from the average duration of winning trades. If winning trades tend to be short, it may shorten the time exit to lock in profits. If winners tend to run, it will extend the time exit, allowing trades more room to develop. This helps prevent the strategy from cutting winning trades short or holding losing trades for too long.

⚡ Intelligent Execution

📊 Trade Quantity: A straightforward input that defines the number of contracts or shares for each trade. This is a fixed value for consistent position sizing.

🛡️ Smart Stop Loss: Enables the dynamic stop-loss mechanism.

🎯 Stop Loss ATR Multiplier: Determines the distance of the stop loss from the entry price, calculated as a multiple of the current 14-period ATR. A higher multiplier gives the trade more room to breathe but increases risk per trade. A lower multiplier creates a tighter stop, reducing risk but increasing the chance of being stopped out by normal market noise.

💰 Take Profit ATR Multiplier: Sets the take profit target, also as a multiple of the ATR. A common practice is to set this higher than the Stop Loss multiplier (e.g., a 2:1 or 3:1 reward-to-risk ratio).

🏃 Use Trailing Stop: This is a powerful feature for trend-following. When enabled, instead of a fixed stop loss, the stop will trail behind the price as the trade moves into profit, helping to lock in gains while letting winners run.

🎯 Trail Points & 📏 Trail Offset ATR Multipliers: These control the trailing stop's behavior. Trail Points defines how much profit is needed before the trail activates. Trail Offset defines how far the stop will trail behind the current price. Both are based on ATR, making them fully adaptive to market volatility.

⏰ Maximum Bars in Trade: This is a time-based stop. It forces an exit if a trade has been open for a specified number of bars, preventing positions from being held indefinitely in stagnant markets.

⏰ Session Management

These inputs allow you to confine the strategy's trading activity to specific market hours, which is crucial for day trading instruments that have defined high-volume sessions (e.g., stock market open).

🎨 Visual Effects & Dashboard

These toggles give you complete control over the on-chart visuals and the dashboard. You can disable any element to declutter your chart or focus only on the information that matters most to you.

📊 THE DASHBOARD: YOUR AT-A-GLANCE COMMAND CENTER

The dashboard centralizes all critical information into one compact, easy-to-read panel. It provides a real-time summary of the market state and strategy performance.

🎯 VOVIX ANALYSIS

Fast & Slow: Displays the current numerical values of the fastDEVMA and slowDEVMA. The color indicates their direction: green for rising, red for falling. This lets you see the underlying momentum of each line.

Regime: This is your most important environmental cue. It tells you the market's current state based on the DEVMA relationship. 🚀 EXPANSION (Green) signifies a bullish volatility regime where explosive moves are more likely. ⚛️ CONTRACTION (Purple) signifies a bearish volatility regime, where the market may be consolidating or entering a smoother trend.

Quality: Measures the strength of the last signal based on the magnitude of the DEVMA difference. An ELITE or STRONG signal indicates a high-conviction setup where the crossover had significant force.

PERFORMANCE

Win Rate & Trades: Displays the historical win rate of the strategy from the backtest, along with the total number of closed trades. This provides immediate feedback on the strategy's historical effectiveness on the current chart.

EXECUTION

Trade Qty: Shows your configured position size per trade.

Session: Indicates whether trading is currently OPEN (allowed) or CLOSED based on your session management settings.

POSITION

Position & PnL: Displays your current position (LONG, SHORT, or FLAT) and the real-time Profit or Loss of the open trade.

🧠 ADAPTIVE STATUS

Stop/Profit Mult: In this simplified version, these are placeholders. The primary adaptive feature currently modifies the time-based exit, which is reflected in how long trades are held on the chart.

🎨 THE VISUAL UNIVERSE: DECIPHERING MARKET GEOMETRY

The visuals are not mere decorations; they are geometric representations of the underlying mathematical concepts, designed to give you an intuitive feel for the market's state.

The Core Lines:

FastDEVMA (Green/Maroon Line): The primary signal line. Green when rising, indicating an increase in short-term volatility chaos. Maroon when falling.

SlowDEVMA (Aqua/Orange Line): The baseline. Aqua when rising, indicating a long-term increase in volatility chaos. Orange when falling.

🌊 Morphism Flow (Flowing Lines with Circles):

What it represents: This visualizes the momentum and strength of the fastDEVMA. The width and intensity of the "beam" are proportional to the signal strength.

Interpretation: A thick, steep, and vibrant flow indicates powerful, committed momentum in the current volatility regime. The floating '●' particles represent kinetic energy; more particles suggest stronger underlying force.

📐 Homotopy Paths (Layered Transparent Boxes):

What it represents: These layered boxes are centered between the two DEVMA lines. Their height is determined by the DEV value.

Interpretation: This visualizes the overall "volatility of volatility." Wider boxes indicate a chaotic, unpredictable market. Narrower boxes suggest a more stable, predictable environment.

🧠 Consciousness Field (The Grid):

What it represents: This grid provides a historical lookback at the DEV range.

Interpretation: It maps the recent "consciousness" or character of the market's volatility. A consistently wide grid suggests a prolonged period of chaos, while a narrowing grid can signal a transition to a more stable state.

📏 Functorial Levels (Projected Horizontal Lines):

What it represents: These lines extend from the current fastDEVMA and slowDEVMA values into the future.

Interpretation: Think of these as dynamic support and resistance levels for the volatility structure itself. A crossover becomes more significant if it breaks cleanly through a prior established level.

🌊 Flow Boxes (Spaced Out Boxes):

What it represents: These are compact visual footprints of the current regime, colored green for Expansion and red for Contraction.

Interpretation: They provide a quick, at-a-glance confirmation of the dominant volatility flow, reinforcing the background color.

Background Color:

This provides an immediate, unmistakable indication of the current volatility regime. Light Green for Expansion and Light Aqua/Blue for Contraction, allowing you to assess the market environment in a split second.

📊 BACKTESTING PERFORMANCE REVIEW & ANALYSIS

The following is a factual, transparent review of a backtest conducted using the strategy's default settings on a specific instrument and timeframe. This information is presented for educational purposes to demonstrate how the strategy's mechanics performed over a historical period. It is crucial to understand that these results are historical, apply only to the specific conditions of this test, and are not a guarantee or promise of future performance. Market conditions are dynamic and constantly change.

Test Parameters & Conditions

To ensure the backtest reflects a degree of real-world conditions, the following parameters were used. The goal is to provide a transparent baseline, not an over-optimized or unrealistic scenario.

Instrument: CME E-mini Nasdaq 100 Futures (NQ1!)

Timeframe: 5-Minute Chart

Backtesting Range: March 24, 2024, to July 09, 2024

Initial Capital: $100,000

Commission: $0.62 per contract (A realistic cost for futures trading).

Slippage: 3 ticks per trade (A conservative setting to account for potential price discrepancies between order placement and execution).

Trade Size: 1 contract per trade.

Performance Overview (Historical Data)

The test period generated 465 total trades , providing a statistically significant sample size for analysis, which is well above the recommended minimum of 100 trades for a strategy evaluation.

Profit Factor: The historical Profit Factor was 2.663 . This metric represents the gross profit divided by the gross loss. In this test, it indicates that for every dollar lost, $2.663 was gained.

Percent Profitable: Across all 465 trades, the strategy had a historical win rate of 84.09% . While a high figure, this is a historical artifact of this specific data set and settings, and should not be the sole basis for future expectations.

Risk & Trade Characteristics

Beyond the headline numbers, the following metrics provide deeper insight into the strategy's historical behavior.

Sortino Ratio (Downside Risk): The Sortino Ratio was 6.828 . Unlike the Sharpe Ratio, this metric only measures the volatility of negative returns. A higher value, such as this one, suggests that during this test period, the strategy was highly efficient at managing downside volatility and large losing trades relative to the profits it generated.

Average Trade Duration: A critical characteristic to understand is the strategy's holding period. With an average of only 2 bars per trade , this configuration operates as a very short-term, or scalping-style, system. Winning trades averaged 2 bars, while losing trades averaged 4 bars. This indicates the strategy's logic is designed to capture quick, high-probability moves and exit rapidly, either at a profit target or a stop loss.

Conclusion and Final Disclaimer

This backtest demonstrates one specific application of the VoVix+ framework. It highlights the strategy's behavior as a short-term system that, in this historical test on NQ1!, exhibited a high win rate and effective management of downside risk. Users are strongly encouraged to conduct their own backtests on different instruments, timeframes, and date ranges to understand how the strategy adapts to varying market structures. Past performance is not indicative of future results, and all trading involves significant risk.

🔧 THE DEVELOPMENT PHILOSOPHY: FROM VOLATILITY TO CLARITY

The journey to create VoVix+ began with a simple question: "What drives major market moves?" The answer is often not a change in price direction, but a fundamental shift in market volatility. Standard indicators are reactive to price. We wanted to create a system that was predictive of market state. VoVix+ was designed to go one level deeper—to analyze the behavior, character, and momentum of volatility itself.

The challenge was twofold. First, to create a robust mathematical model to quantify these abstract concepts. This led to the multi-layered analysis of ATR differentials and standard deviations. Second, to make this complex data intuitive and actionable. This drove the creation of the "Visual Universe," where abstract mathematical values are translated into geometric shapes, flows, and fields. The adaptive system was intentionally kept simple and transparent, focusing on a single, impactful parameter (time-based exits) to provide performance feedback without becoming an inscrutable "black box." The result is a tool that is both profoundly deep in its analysis and remarkably clear in its presentation.

⚠️ RISK DISCLAIMER AND BEST PRACTICES

VoVix+ is an advanced analytical tool, not a guarantee of future profits. All financial markets carry inherent risk. The backtesting results shown by the strategy are historical and do not guarantee future performance. This strategy incorporates realistic commission and slippage settings by default, but market conditions can vary. Always practice sound risk management, use position sizes appropriate for your account equity, and never risk more than you can afford to lose. It is recommended to use this strategy as part of a comprehensive trading plan. This was developed specifically for Futures

"The prevailing wisdom is that markets are always right. I take the opposite view. I assume that markets are always wrong. Even if my assumption is occasionally wrong, I use it as a working hypothesis."

— George Soros

— Dskyz, Trade with insight. Trade with anticipation.

Canuck Trading Trader StrategyCanuck Trading Trader Strategy

Overview

The Canuck Trading Trader Strategy is a high-performance, trend-following trading system designed for NASDAQ:TSLA on a 15-minute timeframe. Optimized for precision and profitability, this strategy leverages short-term price trends to capture consistent gains while maintaining robust risk management. Ideal for traders seeking an automated, data-driven approach to trading Tesla’s volatile market, it delivers strong returns with controlled drawdowns.

Key Features

Trend-Based Entries: Identifies short-term trends using a 2-candle lookback period and a minimum trend strength of 0.2%, ensuring responsive trade signals.

Risk Management: Includes a configurable 3.0% stop-loss to cap losses and a 2.0% take-profit to lock in gains, balancing risk and reward.

High Precision: Utilizes bar magnification for accurate backtesting, reflecting realistic trade execution with 1-tick slippage and 0.1 commission.

Clean Interface: No on-chart indicators, providing a distraction-free trading experience focused on performance.

Flexible Sizing: Allocates 10% of equity per trade with support for up to 2 simultaneous positions (pyramiding).

Performance Highlights

Backtested from March 1, 2024, to June 20, 2025, on NASDAQ:TSLA (15-minute timeframe) with $1,000,000 initial capital: