[imba]lance algo🟩 INTRODUCTION

Hello, everyone!

Please take the time to review this description and source code to utilize this script to its fullest potential.

🟩 CONCEPTS

This is a trend indicator. The trend is the 0.5 fibonacci level for a certain period of time.

A trend change occurs when at least one candle closes above the level of 0.236 (for long) or below 0.786 (for short). Also it has massive amout of settings and features more about this below.

With good settings, the indicator works great on any market and any time frame!

A distinctive feature of this indicator is its backtest panel. With which you can dynamically view the results of setting up a strategy such as profit, what the deposit size is, etc.

Please note that the profit is indicated as a percentage of the initial deposit. It is also worth considering that all profit calculations are based on the risk % setting.

🟩 FEATURES

First, I want to show you what you see on the chart. And I’ll show you everything closer and in more detail.

1. Position

2. Statistic panel

3. Backtest panel

Indicator settings:

Let's go in order:

1. Strategies

This setting is responsible for loading saved strategies. There are only two preset settings, MANUAL and UNIVERSAL. If you choose any strategy other than MANUAL, then changing the settings for take profits, stop loss, sensitivity will not bring any results.

You can also save your customized strategies, this is discussed in a separate paragraph “🟩HOW TO SAVE A STRATEGY”

2. Sensitive

Responsible for the time period in bars to create Fibonacci levels

3. Start calculating date

This is the time to start backtesting strategies

4. Position group

Show checkbox - is responsible for displaying positions

Fill checkbox - is responsible for filling positions with background

Risk % - is responsible for what percentage of the deposit you are willing to lose if there is a stop loss

BE target - here you can choose when you reach which take profit you need to move your stop loss to breakeven

Initial deposit- starting deposit for profit calculation

5. Stoploss group

Fixed stoploss % checkbox - If choosed: stoploss will be calculated manually depending on the setting below( formula: entry_price * (1 - stoploss percent)) If NOT choosed: stoploss will be ( formula: fibonacci level(0.786/0.236) * (1 + stoploss percent))

6. Take profit group

This group of settings is responsible for how far from the entry point take profits will be and what % of the position to fix

7. RSI

Responsible for configuring the built-in RSI. Suitable bars will be highlighted with crosses above or below, depending on overbought/oversold

8. Infopanels group

Here I think everything is clear, you can hide or show information panels

9. Developer mode

If enabled, all events that occur will be shown, for example, reaching a take profit or stop loss with detailed information about the unfixed balance of the position

🟩 HOW TO USE

Very simple. All you need is to wait for the trend to change to long or short, you will immediately see a stop loss and four take profits, and you will also see prices. Like in this picture:

🟩 ALERTS

There are 3 types of alerts:

1. Long signal

2. Short signal

3. Any alert() function call - will be send to you json with these fields

{

"side": "LONG",

"entry": "64.454",

"tp1": "65.099",

"tp2": "65.743",

"tp3": "66.388",

"tp4": "67.032",

"winrate": "35.42%",

"strategy": "MANUAL",

"beTargetTrigger": "1",

"stop": "64.44"

}

🟩 HOW TO SAVE A STRATEGY

First, you need to make sure that the “MANUAL” strategy is selected in the strategy settings.

After this, you can start selecting parameters that will show the largest profit in the statistics panel.

I have highlighted what you need to pay attention to when choosing a strategy

Let's assume you have set up a strategy. The main question is how to preserve it?

Let’s say the strategy turned out with the following parameters:

Next we need to find this section of code:

// STRATS

selector(string strategy_name) =>

strategy_settings = Strategy_settings.new()

switch strategy_name

"MANUAL" =>

strategy_settings.sensitivity := 18

strategy_settings.risk_percent := 1

strategy_settings.break_even_target := "1"

strategy_settings.tp1_percent := 1

strategy_settings.tp1_percent_fix := 40

strategy_settings.tp2_percent := 2

strategy_settings.tp2_percent_fix := 30

strategy_settings.tp3_percent := 3

strategy_settings.tp3_percent_fix := 20

strategy_settings.tp4_percent := 4

strategy_settings.tp4_percent_fix := 10

strategy_settings.fixed_stop := false

strategy_settings.sl_percent := 0.0

"UNIVERSAL" =>

strategy_settings.sensitivity := 20

strategy_settings.risk_percent := 1

strategy_settings.break_even_target := "1"

strategy_settings.tp1_percent := 1

strategy_settings.tp1_percent_fix := 40

strategy_settings.tp2_percent := 2

strategy_settings.tp2_percent_fix := 30

strategy_settings.tp3_percent := 3

strategy_settings.tp3_percent_fix := 20

strategy_settings.tp4_percent := 4

strategy_settings.tp4_percent_fix := 10

strategy_settings.fixed_stop := false

strategy_settings.sl_percent := 0.0

// "NEW STRATEGY" =>

// strategy_settings.sensitivity := 20

// strategy_settings.risk_percent := 1

// strategy_settings.break_even_target := "1"

// strategy_settings.tp1_percent := 1

// strategy_settings.tp1_percent_fix := 40

// strategy_settings.tp2_percent := 2

// strategy_settings.tp2_percent_fix := 30

// strategy_settings.tp3_percent := 3

// strategy_settings.tp3_percent_fix := 20

// strategy_settings.tp4_percent := 4

// strategy_settings.tp4_percent_fix := 10

// strategy_settings.fixed_stop := false

// strategy_settings.sl_percent := 0.0

strategy_settings

// STRATS

Let's uncomment on the latest strategy called "NEW STRATEGY" rename it to "SOL 5m" and change the sensitivity:

// STRATS

selector(string strategy_name) =>

strategy_settings = Strategy_settings.new()

switch strategy_name

"MANUAL" =>

strategy_settings.sensitivity := 18

strategy_settings.risk_percent := 1

strategy_settings.break_even_target := "1"

strategy_settings.tp1_percent := 1

strategy_settings.tp1_percent_fix := 40

strategy_settings.tp2_percent := 2

strategy_settings.tp2_percent_fix := 30

strategy_settings.tp3_percent := 3

strategy_settings.tp3_percent_fix := 20

strategy_settings.tp4_percent := 4

strategy_settings.tp4_percent_fix := 10

strategy_settings.fixed_stop := false

strategy_settings.sl_percent := 0.0

"UNIVERSAL" =>

strategy_settings.sensitivity := 20

strategy_settings.risk_percent := 1

strategy_settings.break_even_target := "1"

strategy_settings.tp1_percent := 1

strategy_settings.tp1_percent_fix := 40

strategy_settings.tp2_percent := 2

strategy_settings.tp2_percent_fix := 30

strategy_settings.tp3_percent := 3

strategy_settings.tp3_percent_fix := 20

strategy_settings.tp4_percent := 4

strategy_settings.tp4_percent_fix := 10

strategy_settings.fixed_stop := false

strategy_settings.sl_percent := 0.0

"SOL 5m" =>

strategy_settings.sensitivity := 15

strategy_settings.risk_percent := 1

strategy_settings.break_even_target := "1"

strategy_settings.tp1_percent := 1

strategy_settings.tp1_percent_fix := 40

strategy_settings.tp2_percent := 2

strategy_settings.tp2_percent_fix := 30

strategy_settings.tp3_percent := 3

strategy_settings.tp3_percent_fix := 20

strategy_settings.tp4_percent := 4

strategy_settings.tp4_percent_fix := 10

strategy_settings.fixed_stop := false

strategy_settings.sl_percent := 0.0

strategy_settings

// STRATS

Now let's find this code:

strategy_input = input.string(title = "STRATEGY", options = , defval = "MANUAL", tooltip = "EN:\nTo manually configure the strategy, select MANUAL otherwise, changing the settings won't have any effect\nRU:\nЧтобы настроить стратегию вручную, выберите MANUAL в противном случае изменение настроек не будет иметь никакого эффекта")

And let's add our new strategy there, it turned out like this:

strategy_input = input.string(title = "STRATEGY", options = , defval = "MANUAL", tooltip = "EN:\nTo manually configure the strategy, select MANUAL otherwise, changing the settings won't have any effect\nRU:\nЧтобы настроить стратегию вручную, выберите MANUAL в противном случае изменение настроек не будет иметь никакого эффекта")

That's all. Our new strategy is now saved! It's simple! Now we can select it in the list of strategies:

Komut dosyalarını "通达信+选股公式+换手率+0.5+源码" için ara

Auto Fibonacci Retracement // Atilla YurtsevenOverview:

This Pine Script™ is a specialized tool for traders, designed to automatically plot Fibonacci retracement levels over a user-defined date range in trading charts. It also indicates the extent of price retracement within these levels.

Key Features:

Date Range Customization: Users can specify the start and end dates to focus the analysis on a particular trading period.

Dynamic Fibonacci Levels: The script includes various Fibonacci ratios (0.0, 0.236, 0.382, 0.5, 0.618, 0.786, 1.0), with the flexibility to enable or disable individual levels.

Visual Customization: Each Fibonacci level can be customized for color and line style (solid, dotted, dashed). Labels for each level are also configurable.

Retracement Measurement: The script not only draws the Fibonacci levels but also measures and displays how much the price has retraced within these levels.

Extension and Additional Options: Users have options to extend the Fibonacci lines and additional features such as using close values, trend drawing, date range display, and more.

Technical Insights:

The script identifies high and low values within the selected time frame, assessing the market's trend direction.

Within the specified date range, this script effortlessly plots the Fibonacci levels automatically, bringing clarity and precision to your market analysis as it unfolds.

The tool's adaptability makes it suitable for various trading styles and chart preferences.

Intended Use:

This script is particularly valuable for technical analysts and traders who use Fibonacci retracements to identify potential support and resistance areas and understand the depth of market corrections or rallies.

Disclaimer:

This Pine Script™ is offered 'as is', without any guarantees or warranties. It is intended for informational purposes and should not be taken as investment advice. Atilla Yurtseven, the creator of this script, assumes no responsibility for any financial losses or gains that may result from its usage. Users should perform their own due diligence and consult with professional advisors before making any investment decisions.

Remember to follow and comment!

Trade smart, stay safe

Atilla Yurtseven

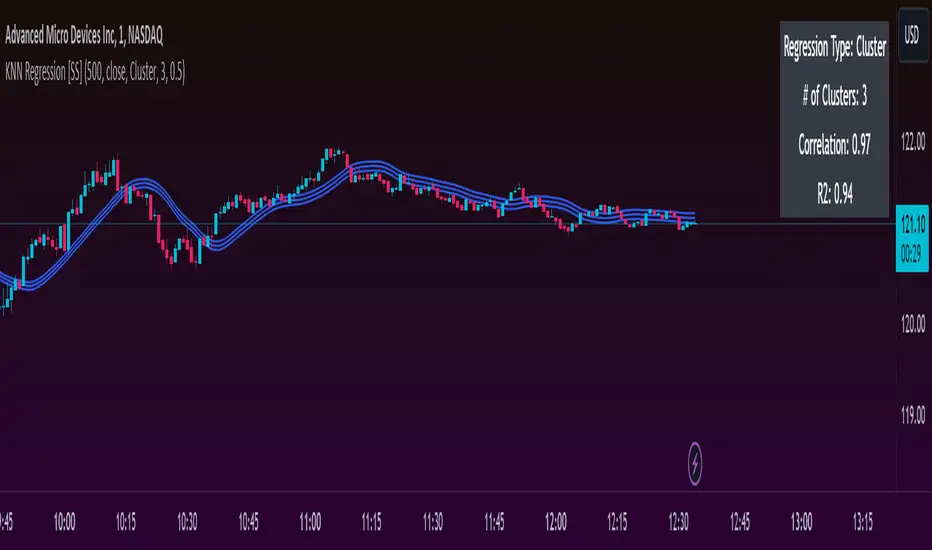

KNN ATR Dual Range Predictions [SS]Excited to release this indicator!

I wanted to do a machine learning, ATR based indicator for a while, but I first had to learn about machine learning algos haha.

Now that I have created a KNN based regression methodology (shared in a previous indicator), I can finally do it!

So this is a Nearest Known Neighbor or KNN regression based indicator that uses ATR (average ranges) to predict future ranges.

It operates by calculating the move from High to Open and Open to Low and performing KNN regression to look for other, similar instances of similar movements and what followed those movements.

It provides for 2 methods of KNN regression, the traditional Cluster method (where it identifies a number of clusters within a tolerance range and averages them out), or the method of last instance (where it finds the most recent identical instance and plots the result from that).

You can toggle the parameters as you wish, including the:

a) Type of Regression

b) Number of Clusters

c) Tolerance for Clusters

Others functions:

The indicator provides for the ability to view 2 different timeframe targets. The default calculation is the current timeframe you are on. So if you are on the 1 minute, 5 minute or 1 hour, it will automatically default the primary range to this timeframe. This cannot be changed.

But it permits for a second prediction to be calculated for a timeframe you can specify. The example in the chart above is the 1 hour overlaid on the 5 minute chart.

You can see how the model is performing in the statistics table. The statistics table can be removed as well if you don't want it overlaid on your chart.

You can also toggle off and on the various ranges. IF you only want to visualize 1 hour levels on a 5 minute chart, you can toggle off the bands and just view the higher tf data. Inversely, if you only want the current timeframe data and not the higher tf data, you can toggle the higher tf data off as well.

General Use Tips:

Some general use tips include:

🎯The default settings are appropriate for most common tickers. Because this is performing an autoregression on itself, the parameters tend to be more tight vs. performing dual correlation between two separate tickers which are sizably different in scale (which would require a higher tolerance).

Here is an example of YM1!, which is a sizably larger ticker, however it is performing well with the current settings.

🎯 If you get not great results from your ranges or an error in the correlation table, something like this:

It means the parameters are too tight for what you want to do and it is having trouble identifying other, similar cases (in this case, the lookback length was significantly shortened). The first step is to:

a) Expand your lookback range (up to 500 is usually sufficient). This should resolve most issues in most cases. If not:

b) If you are using the Cluster method, try broadening your cluster tolerance by 0.5 increments.

Between those two implementations, you should get a functional model. And it actually honestly hasn't happened to me in general use, I had to force that example by significantly shortening the lookback period.

Concluding Remarks

And that's pretty much the indicator.

I hope you enjoy it! I was really excited to be finally able to do it, like I said I attempted to do this for a while but needed to research the whole KNN process and how its performed.

Enjoy and leave your comments and questions below!

KNN Regression [SS]Another indicator release, I know.

But note, this isn't intended to be a stand-alone indicator, this is just a functional addition for those who program Machine Learning algorithms in Pinescript! There isn't enough content here to merit creating a library for (it's only 1 function), but it's a really useful function for those who like machine learning and Nearest Known Neighbour Algos (or KNN).

About the indicator:

This indicator creates a function to perform KNN-based regression.

In contrast to traditional linear regression, KNN-based regression has the following advantages over linear regression:

Advantages of KNN Regression vs. Linear Regression:

🎯 Non-linearity: KNN is a non-parametric method, meaning it makes no assumptions about the underlying data distribution. This allows it to capture non-linear relationships between features and the target variable.

🎯Simple Implementation: KNN is conceptually simple and easy to understand. It doesn't require the estimation of parameters, making it straightforward to implement.

🎯Robust to Outliers: KNN is less sensitive to outliers compared to linear regression. Outliers can have a significant impact on linear regression models, but KNN tends to be less affected.

Disadvantages of KNN Regression vs. Linear Regression:

🎯 Resource Intensive for Computation: Because KNN operates on identifying the nearest neighbors in a dataset, each new instance has to be searched for and identified within the dataset, vs. linear regression which can create a coefficient-based model and draw from the coefficient for each new data point.

🎯Curse of Dimensionality: KNN performance can degrade with an increasing number of features, leading to a "curse of dimensionality." This is because, in high-dimensional spaces, the concept of proximity becomes less meaningful.

🎯Sensitive to Noise: KNN can be sensitive to noisy data, as it relies on the local neighborhood for predictions. Noisy or irrelevant features may affect its performance.

Which is better?

I am very biased, coming from a statistics background. I will always love linear regression and will always prefer it over KNN. But depending on what you want to accomplish, KNN makes sense. If you are using highly skewed data or data that you cannot identify linearity in, KNN is probably preferable.

However, if you require precise estimations of ranges and outliers, such as creating co-integration models, I would advise sticking with linear regression. However, out of curiosity, I exported the function into a separate dummy indicator and pulled in data from QQQ to predict SPY close, and the results are actually very admirable:

And plotted with showing the standard error variance:

Pretty impressive, I must say I was a little shocked, it's really giving linear regression a run for its money. In school I was taught LinReg is the gold standard for modeling, nothing else compares. So as with most things in trading, this is challenging some biases of mine ;).

Functionality of the function

I have permitted 3 types of KNN regression. Traditional KNN regression, as I understand it, revolves around clustering. ( Clustering refers to identifying a cluster, normally 3, of identical cases and averaging out the Dependent variable in each of those cases) . Clustering is great, but when you are working with a finite dataset, identifying exact matches for 2 or 3 clusters can be challenging when you are only looking back at 500 candles or 1000 candles, etc.

So to accommodate this, I have added a functionality to clustering called "Tolerance". And it allows you to set a tolerance level for your Euclidean distance parameters. As a default, I have tested this with a default of 0.5 and it has worked great and no need to change even when working with large numbers such as NQ and ES1!.

However, I have added 2 additional regression types that can be done with KNN.

#1 One is a regression by the last IDENTICAL instance, which will find the most recent instance of a similar Independent variable and pull the Dependent variable from that instance. Or

#2 Average from all IDENTICAL instances.

Using the function

The code has the instructions for integrating the function into your own code, the parameters, and such, so I won't exhaust you with the boring details about that here.

But essentially, it exports 3, float variables, the Result, the Correlation, and the simplified R2.

As this is KNN regression, there are no coefficients, slopes, or intercepts and you do not need to test for linearity before applying it.

Also, the output can be a bit choppy, so I tend to like to throw in a bit of smoothing using the ta.sma function at a deault of 14.

For example, here is SPY from QQQ smoothed as a 14 SMA:

And it is unsmoothed:

It seems relatively similar but it does make a bit of an aesthetic difference. And if you are doing it over 14, there is no data loss and it is still quite reactive to changes in data.

And that's it! Hopefully you enjoy and find some interesting uses for this function in your own scripts :-).

Safe trades everyone!

TTP Big Whale ExplorerThe Big Whale Explorer is an indicator that looks into the ratio of large wallets deposits vs withdrawals.

Whales tend to sale their holding when they transfer their holdings into exchanges and they tend to hold when they withdraw.

In this overlay indicator you'll be able to see in an oscillator format the moves of large wallets.

The moves above 1.5 turn into red symbolising that they are starting to distribute. This can eventually have an impact in the price by causing anything from a mild pullback to a considerable crash depending on how much is being actually sold into the market.

Moves below 0.5 mean that the large whales are heavily accumulating and withdrawing. During these periods price could still pullback or even crash but eventually the accumulation can take prices to new highs.

Instructions:

1) Load INDEX:BTCUSD or BNC:BLX to get the most historic data as possible

2) use the daily timeframe

3) load the indicator into the chart

Immediate rebalanceGuided by the new ICT tutoring, I create this versatile Immediate Rebalance indicator

This indicator shows a different way on how to view the "Spikes or Shadows", based on the direction of the price this indicator divides the "Spike or Shadows" into levels 0.5 - 0.75 - 0.25 Fibonacci, giving the possibility to view the levels both in normal or in pre-Macro times

The user has the possibility to:

- Choose to have Spike levels shown in MultiTimeframe

- Choose to show Sike levels only Bullish or only Bearish

- Choose to show Sike levels only in pre-Macro/Macro times

- Choose to view the maximum amount of levels with Max Show

The indicator must be used as ICT shows in its concepts, the indicator takes into consideration the last 2 candles already closed so on the candle that is forming it is possible to expect reactions on the levels it marks, below is an example of how to use it in MultiTimeframe

Below I show an example on how to set the indicator to see Immediate Rebalance in Macro times

Below is an example of when not to take the indicator into consideration

Take Profit ModelThis Indicator allows you to define 9 Taking Profit levels between your floor price and a target price you define for 10 selectable Assets and tweak the levels to your preference. It does not do any fancy dynamic calculations, it just draws lines on the chart where you want them so that you have an easy reference for when to take profit (or not).

Example:

So, if your floor price for an asset is e.g. $10 and your target price is $110 (its up to you to define, who knows right, I do not have a crystal ball), You have a range of $100 where you can set your levels as follows

The first level is the Floor price you entered = $10

Formula: Level x (Target - Floor) + Floor = Take Profit level

Levels

0.1 x (110 - 10) + 10 = $20

0.2 x (110 - 10) + 10 = $30

0.3 x (110 - 10) + 10 = $40

0.4 x (110 - 10) + 10 = $50

0.5 x (110 - 10) + 10 = $60

0.6 x (110 - 10) + 10 = $70

0.7 x (110 - 10) + 10 = $80

0.8 x (110 - 10) + 10 = $90

0.9 x (110 - 10) + 10 = $100

And finally the last level is drawn for the target price

Target Price = $110

To change the settings, go to the cog icon of the Indicator, select the assets (Tickers) you have and next enter a value between 0 and 1 (as shown above) for each level, and if you want a different color. Instead of using 0.1-0.9 you e.g. can also use Fibonacci numbers like 0.235, 0.382, 0.618, 0.786 and disable (using the check mark) the rest of the levels. Experiment with this as you see fit.

Make sure that the chart you are looking at in TradingView is the same as you select in the indicator configuration e.g. COINBASE:BTCUSD should be selected as the chart as well as the Ticker in the configuration.

The Start date of the script is configurable (one date across all assets and levels)

The colors of the Levels is configurable (I am colorblind so go wild)

The standard values in the script are just examples, you need to determine the values that apply in your case and do your own research.

Your feedback is most welcome

WU Sahm Recession Indicator The Sahm Recession Indicator devised by Economist Claudia Sahm is a rather insightful tool that captures the onset of recessions by utilizing unemployment data, which can provide more real-time insights compared to quarterly GDP reports. If the three-month simple moving average (SMA) of the unemployment rate exceeds the minimum unemployment rate of the previous 12 months by 0.5 percentage points, it indicates a high likelihood of a recession.

This script allows you to visualize this indicator and set up alerts for when this criterion indicates that a recession could be coming.

Volume and Price Z-Score [Multi-Asset] - By LeviathanThis script offers in-depth Z-Score analytics on price and volume for 200 symbols. Utilizing visualizations such as scatter plots, histograms, and heatmaps, it enables traders to uncover potential trade opportunities, discern market dynamics, pinpoint outliers, delve into the relationship between price and volume, and much more.

A Z-Score is a statistical measurement indicating the number of standard deviations a data point deviates from the dataset's mean. Essentially, it provides insight into a value's relative position within a group of values (mean).

- A Z-Score of zero means the data point is exactly at the mean.

- A positive Z-Score indicates the data point is above the mean.

- A negative Z-Score indicates the data point is below the mean.

For instance, a Z-Score of 1 indicates that the data point is 1 standard deviation above the mean, while a Z-Score of -1 indicates that the data point is 1 standard deviation below the mean. In simple terms, the more extreme the Z-Score of a data point, the more “unusual” it is within a larger context.

If data is normally distributed, the following properties can be observed:

- About 68% of the data will lie within ±1 standard deviation (z-score between -1 and 1).

- About 95% will lie within ±2 standard deviations (z-score between -2 and 2).

- About 99.7% will lie within ±3 standard deviations (z-score between -3 and 3).

Datasets like price and volume (in this context) are most often not normally distributed. While the interpretation in terms of percentage of data lying within certain ranges of z-scores (like the ones mentioned above) won't hold, the z-score can still be a useful measure of how "unusual" a data point is relative to the mean.

The aim of this indicator is to offer a unique way of screening the market for trading opportunities by conveniently visualizing where current volume and price activity stands in relation to the average. It also offers features to observe the convergent/divergent relationships between asset’s price movement and volume, observe a single symbol’s activity compared to the wider market activity and much more.

Here is an overview of a few important settings.

Z-SCORE TYPE

◽️ Z-Score Type: Current Z-Score

Calculates the z-score by comparing current bar’s price and volume data to the mean (moving average with any custom length, default is 20 bars). This indicates how much the current bar’s price and volume data deviates from the average over the specified period. A positive z-score suggests that the current bar's price or volume is above the mean of the last 20 bars (or the custom length set by the user), while a negative z-score means it's below that mean.

Example: Consider an asset whose current price and volume both show deviations from their 20-bar averages. If the price's Z-Score is +1.5 and the volume's Z-Score is +2.0, it means the asset's price is 1.5 standard deviations above its average, and its trading volume is 2 standard deviations above its average. This might suggest a significant upward move with strong trading activity.

◽️ Z-Score Type: Average Z-Score

Calculates the custom-length average of symbol's z-score. Think of it as a smoothed version of the Current Z-Score. Instead of just looking at the z-score calculated on the latest bar, it considers the average behavior over the last few bars. By doing this, it helps reduce sudden jumps and gives a clearer, steadier view of the market.

Example: Instead of a single bar, imagine the average price and volume of an asset over the last 5 bars. If the price's 5-bar average Z-Score is +1.0 and the volume's is +1.5, it tells us that, over these recent bars, both the price and volume have been consistently above their longer-term averages, indicating sustained increase.

◽️ Z-Score Type: Relative Z-Score

Calculates a relative z-score by comparing symbol’s current bar z-score to the mean (average z-score of all symbols in the group). This is essentially a z-score of a z-score, and it helps in understanding how a particular symbol's activity stands out not just in its own historical context, but also in relation to the broader set of symbols being analyzed. In other words, while the primary z-score tells you how unusual a bar's activity is for that specific symbol, the relative z-score informs you how that "unusualness" ranks when compared to the entire group's deviations. This can be particularly useful in identifying symbols that are outliers even among outliers, indicating exceptionally unique behaviors or opportunities.

Example: If one asset's price Z-Score is +2.5 and volume Z-Score is +3.0, but the group's average Z-Scores are +0.5 for price and +1.0 for volume, this asset’s Relative Z-Score would be high and therefore stand out. This means that asset's price and volume activities are notably high, not just by its own standards, but also when compared to other symbols in the group.

DISPLAY TYPE

◽️ Display Type: Scatter Plot

The Scatter Plot is a visual tool designed to represent values for two variables, in this case the Z-Scores of price and volume for multiple symbols. Each symbol has it's own dot with x and y coordinates:

X-Axis: Represents the Z-Score of price. A symbol further to the right indicates a higher positive deviation in its price from its average, while a symbol to the left indicates a negative deviation.

Y-Axis: Represents the Z-Score of volume. A symbol positioned higher up on the plot suggests a higher positive deviation in its trading volume from its average, while one lower down indicates a negative deviation.

Here are some guideline insights of plot positioning:

- Top-Right Quadrant (High Volume-High Price): Symbols in this quadrant indicate a scenario where both the trading volume and price are higher than their respective mean.

- Top-Left Quadrant (High Volume-Low Price): Symbols here reflect high trading volumes but prices lower than the mean.

- Bottom-Left Quadrant (Low Volume-Low Price): Assets in this quadrant have both low trading volume and price compared to their mean.

- Bottom-Right Quadrant (Low Volume-High Price): Symbols positioned here have prices that are higher than their mean, but the trading volume is low compared to the mean.

The plot also integrates a set of concentric squares which serve as visual guides:

- 1st Square (1SD): Encapsulates symbols that have Z-Scores within ±1 standard deviation for both price and volume. Symbols within this square are typically considered to be displaying normal behavior or within expected range.

- 2nd Square (2SD): Encapsulates those with Z-Scores within ±2 standard deviations. Symbols within this boundary, but outside the 1 SD square, indicate a moderate deviation from the norm.

- 3rd Square (3SD): Represents symbols with Z-Scores within ±3 standard deviations. Any symbol outside this square is deemed to be a significant outlier, exhibiting extreme behavior in terms of either its price, its volume, or both.

By assessing the position of symbols relative to these squares, traders can swiftly identify which assets are behaving typically and which are showing unusual activity. This visualization simplifies the process of spotting potential outliers or unique trading opportunities within the market. The farther a symbol is from the center, the more it deviates from its typical behavior.

◽️ Display Type: Columns

In this visualization, z-scores are represented using columns, where each symbol is presented horizontally. Each symbol has two distinct nodes:

- Left Node: Represents the z-score of volume.

- Right Node: Represents the z-score of price.

The height of these nodes can vary along the y-axis between -4 and 4, based on the z-score value:

- Large Positive Columns: Signify a high or positive z-score, indicating that the price or volume is significantly above its average.

- Large Negative Columns: Represent a low or negative z-score, suggesting that the price or volume is considerably below its average.

- Short Columns Near 0: Indicate that the price or volume is close to its mean, showcasing minimal deviation.

This columnar representation provides a clear, intuitive view of how each symbol's price and volume deviate from their respective averages.

◽️ Display Type: Circles

In this visualization style, z-scores are depicted using circles. Each symbol is horizontally aligned and represented by:

- Solid Circle: Represents the z-score of price.

- Transparent Circle: Represents the z-score of volume.

The vertical position of these circles on the y-axis ranges between -4 and 4, reflecting the z-score value:

- Circles Near the Top: Indicate a high or positive z-score, suggesting the price or volume is well above its average.

- Circles Near the Bottom: Represent a low or negative z-score, pointing to the price or volume being notably below its average.

- Circles Around the Midline (0): Highlight that the price or volume is close to its mean, with minimal deviation.

◽️ Display Type: Delta Columns

There's also an option to utilize Z-Score Delta Columns. For each symbol, a single column is presented, depicting the difference between the z-score of price and the z-score of volume.

The z-score delta essentially captures the disparity between how much the price and volume deviate from their respective mean:

- Positive Delta: Indicates that the z-score of price is greater than the z-score of volume. This suggests that the price has deviated more from its average than the volume has from its own average. Such a scenario could point to price movements being more significant or pronounced compared to the changes in volume.

- Negative Delta: Represents that the z-score of volume is higher than the z-score of price. This might mean that there are substantial volume changes, yet the price hasn't moved as dramatically. This can be indicative of potential build-up in trading interest without an equivalent impact on price.

- Delta Close to 0: Means that the z-scores for price and volume are almost equal, indicating their deviations from the average are in sync.

◽️ Display Type: Z-Volume/Z-Price Heatmap

This visualization offers a heatmap either for volume z-scores or price z-scores across all symbols. Here's how it's presented:

Each symbol is allocated its own horizontal row. Within this row, bar-by-bar data is displayed using a color gradient to represent the z-score values. The heatmap employs a user-defined gradient scale, where a chosen "cold" color represents low z-scores and a chosen "hot" color signifies high z-scores. As the z-score increases or decreases, the colors transition smoothly along this gradient, providing an intuitive visual indication of the z-score's magnitude.

- Cold Colors: Indicate values significantly below the mean (negative z-score)

- Mild Colors: Represent values close to the mean, suggesting minimal deviation.

- Hot Colors: Indicate values significantly above the mean (positive z-score)

This heatmap format provides a rapid, visually impactful means to discern how each symbol's price or volume is behaving relative to its average. The color-coded rows allow you to quickly spot outliers.

VOLUME TYPE

The "Volume Type" input allows you to choose the nature of volume data that will be factored into the volume z-score calculation. The interpretation of indicator’s data changes based on this input. You can opt between:

- Volume (Regular Volume): This is the classic measure of trading volume, which represents the volume traded in a given time period - bar.

- OBV (On-Balance Volume): OBV is a momentum indicator that accumulates volume on up bars and subtracts it on down bars, making it a cumulative indicator that sort of measures buying and selling pressure.

Interpretation Implications:

- For Volume Type: Regular Volume:

Positive Z-Score: Indicates that the trading volume is above its average, meaning there's unusually high trading activity .

Negative Z-Score: Suggests that the trading volume is below its average, signifying unusually low trading activity.

- For Volume Type: OBV:

Positive Z-Score: Signifies that “buying pressure” is above its average.

Negative Z-Score: Signifies that “selling pressure” is above its average.

When comparing Z-Score of OBV to Z-Score of price, we can observe several scenarios. If Z-Price and Z-Volume are convergent (have similar z-scores), we can say that the directional price movement is supported by volume. If Z-Price and Z-Volume are divergent (have very different z-scores or one of them being zero), it suggests a potential misalignment between price movement and volume support, which might hint at possible reversals or weakness.

Euclidean Distance Predictive Candles [SS]Finally releasing this, its been in the works for the past 2 weeks and has undergone many iterations.

I am not sure if I am 100% happy with it yet, but I guess its best to release and get feedback to make improvements.

So this is the Euclidean distance predictive candle indicator and what it does is exactly what it sounds like, it uses Euclidean distance to identify similar candles and then plot the candles and range that immediately proceeded like candles.

While this is using a general machine learning/data science approach (Euclidean distance), I do not employ the KNN (Nearest Neighbors) algo into this. The reason being is it simply offered no predictive advantage than isolating for the last case. I tried it, I didn't like it, the results were not improve and, at times, acutally hindered so I ditched it. Perhaps it was my approach but using some other KNN indicators, I just don't really find them all that more advantageous to simply relying on the Law of Large Numbers and collecting more data rather than less data (which we will get into later in this explanation).

So using this indicator:

There is a lot of customizability here. And the reason is, not all settings are going to work the same for all tickers. To help you narrow down your parameters, I have included various backtest results that show you how the model is performing. You see in the AMZN chart above, with the current settings, it is performing optimally, with a cumulative range pass of 99% (meaning that, of all the cases, the indicator accurately predicted the next day high OR low range 99% of the time), and the ability to predict the candle slightly over 52%.

The recommended settings, from me, are as follows:

So these are generally my recommended settings.

Euclidian Tolerance: This will determine the parameters to look for similar candles. In general, the lower the tolerance, the greater the precision. I recommend keeping it between 0.5, for tickers with larger prices (like ES1! futures or NQ1!) or 0.05 for tickers with lower TPs, like SPY or QQQ.

If the ED Tolerance is too extreme that the indicator cannot find identical setups, it will alert you:

But in general, the more precise you can get it, the better.

Anchor Type: You will see the option to anchor by "Predicted Open" or by "Previous Close". I suggest sticking with anchoring by predicted open. All this means is, it is going to anchor your range, candle, high and low targets by the predicted open price. Anchoring by previous close will anchor by the close of yesterday. Both work okay, but in general the results from anchoring to predicted open have higher pass rates and more accurately depict the candle.

Euclidean Distance Measurement Type: You can choose to measure by candle body or from high to low wicks. I haven't played around with measuring from high to low wicks all that much, because candle body tends to do the job. But remember, ED is a neutral measurement. Which means, its not going to distinguish between a red or green candle, just the formation of the candle. Thus, I tend to recommend, pragmatically, not to necessarily rely on the candle being red or green, but one the formation of the candle (where are the wicks going, are there more bearish wicks or bullish wicks) etc. Examples will follow.

Range Prediction Type: You can filter the range prediction type by last instance (in which, it will pull the previous identical candle and plot the next candle that followed it, adjusted for the current ranges) or "Average of All Cases". So this is where we need to talk a little bit about the law of large numbers.

In general, in statistics, when you have a huge amount of random data, the law of large numbers stipulates that, within this randomness should be repeated events. This is why sometimes chart patterns work, sometimes they don't. When we filter by the average of all cases, we are relying on the law of large numbers. In general, if you are getting good Backtest readings from Last Instance, then you don't need to use this function. But it provides an alternative insight into potential candle formations next day. Its not a bad idea to compare between the two and look for similarities and differences.

So now that we have covered the boring details, let's get into how to use the indicator and some examples.

So the indicator is plotting the range and candle for the next day. As such, we are not looking at the current candle being plotted, but we are looking at the previous candle (see image below for example):

The green arrow shows the prediction for Friday, along with the corresponding result. The purple arrow shows the prediction for Monday which we have yet to realize.

So remember when you are using this, you need to look at the previous candle, and not the candle that it is currently plotting with realtime data, because it is plotting for the next candle.

If you are plotting by last instance, the indicator will tell you which day it is pulling its data from if you have opted to toggle on the demographic data:

You can see the green arrow pointing to the date where it is pulling from. This data serves as the example candle with the candle proceeding this date being the anchored candle (or the predicted candle).

Price Targets and Probability:

In the chart, you can see the green arrow pointing to the green portion of the table. In this table, it will give you the current TPs. These represent the current time target price, which means, the TPs shown here are for Friday. On Monday, the table will update with the TPs for Monday, etc. If you want to view the TPs in advance, you can view them from the actual candle itself.

Below the TPs, you see a bullish 7:6. It means, in a total of 13 cases, the next candle was bullish 7 times and bearish 6 times. Where do we see the number of cases? In the demographic table as well:

Auxiliary functions

Because you are using the previous candle, if you want to avoid confusion, you can have the indicator plot the price targets over the predicted candle, to anchor your attention so to speak. Simply select "Label" in the "Show Price Targets" section, which will look like this:

You can also ask the indicator to plot the demographic data of Higher High, Low, etc. information. What this does is simply looks at all the cases and plots how many times higher highs, lows, lower lows, highs etc. were made:

This will just count all of the cases identified and plot the number of times higher highs, lows, etc. were made.

Concluding Remarks

This is a kind of complex indicator and I can appreciate it may take some getting used to.

I will try to post a tutorial video at some point next week for it, so stay tuned for that.

But this isn't designed to make your life more complicated, just to help give you insights into potential outcomes for the next day or hour or 5 minute (it can be used on all timeframes).

If you find it helpful, great! If not, that's okay, too :-).

Please be aware, this is not my forte of indicators. I am not a data scientist or programmer. My background is in Epi and we don't use these types of data science approaches, so if you have any suggestions or critiques, feel free to share them below.

Otherwise, I hope you enjoy!

Take care everyone and safe trades!

Market Internals (TICK, ADD, VOLD, TRIN, VIX)OVERVIEW

This script allows you to perform data transformations on Market Internals, across exchanges, and specify signal parameters, to more easily identify sentiment extremes.

Notable transformations include:

1. Cumulative session values

2. Directional bull-bear Ratios and Percent Differences

3. Data Normalization

4. Noise Reduction

This kind of data interaction is very useful for understanding the relationship between two mutually exclusive metrics, which is the essence of Market Internals: Up vs. Down. Even so, they are not possible with symbol expressions alone. And the kind of symbol expression needed to produce baseline data that can be reliably transformed is opaque to most traders, made worse by the fact that prerequisite symbol expressions themselves are not uniform across symbols. It's very nuanced, and if this last bit was confusing … exactly.

All this to say, rather than forcing that burden onto you, I've baked the baseline symbol expressions into the indicator so: 1) the transform functions consistently ingest the baseline data in the correct format and 2) you don't have to spend time trying to figure it all out. Trading is hard. There's no need to make it harder.

INPUTS

Indicator

Allows you to specify the base Market Internal and Exchange data to use. The list of Market Internals is simplified to their fundamental representation (TICK, ADD, VOLD, TRIN, VIX, ABVD, TKCD), and the list of Exchange data is limited to the most common (NYSE, NASDAQ, All US Stocks). There are also options for basic exchange combinations (Sum or Average of NYSE & NASDAQ).

Mode

Short for "Plot Mode", this is where you specify the bars style (Candles, Bars, Line, Circles, Columns) and the source value (used for single value plots and plot color changes).

Scale

This is the first and second data transformation grouped together. The default is to show the origin data as it might appear on a chart. You can then specify if each bar should retain it's unique value (Bar Value) or be added to a running total (Cumulative). You can also specify if you would like the data to remain unaltered (Raw) or converted to a directional ratio (Ratio) or a percentage (Percent Diff). These options determine the scale of the plot.

Both Ratio and Percent Diff. convert a given symbol into a positive or negative number, where positive numbers are bullish and negative numbers are bearish.

Ratio will divide Bull values by Bear values, then further divide -1 by the quotient if it is less than 1. For example, if "0.5" was the quotient, the Ratio would be "-2".

Percent Diff. subtracts Bear values from Bull values, then divides that difference by the sum of Bull and Bear values multiplied by 100. If a Bull value was "3" and Bear value was "7", the difference would be "-4", the sum would be "10", and the Percent Diff. would be "-40", as the difference is both bearish and 40% of total.

Ratio Norm. Threshold

This is the third data transformation . While quotients can be less than 1, directional ratios are never less than 1. This can lead to barcode-like artifacts as plots transition between positive and negative values, visually suggesting the change is much larger than it actually is. Normalizing the data can resolve this artifact, but undermines the utility of ratios. If, however, only some of the data is normalized, the artifact can be resolved without jeopardizing its contextual usefulness.

The utility of ratios is how quickly they communicate proportional differences. For example, if one side is twice as big as the other, "2" communicates this efficiently. This necessarily means the numerical value of ratios is worth preserving. Also, below a certain threshold, the utility of ratios is diminished. For example, an equal distribution being represented as 0, 1, 1:1, 50/50, etc. are all equally useful. Thus, there is a threshold, above which we want values to be exact, and below which the utility of linear visual continuity is more important. This setting accounts for that threshold.

When this setting is enabled, a ratio will be normalized to 0 when 1:1, scaled linearly toward the specified threshold when greater than 1:1, and then retain its exact value when the threshold is crossed. For example, with a threshold of "2", 1:1 = 0, 1.5:1 = 1, 2:1 = 2, 3:1 = 3, etc.

With all this in mind, most traders will want to set the ratios threshold at a level where accuracy becomes more important than visual continuity. If this level is unknown, "2" is a good baseline.

Reset cumulative total with each new session

Cumulative totals can be retained indefinitely or be reset each session. When enabled, each session has its own cumulative total. When disabled, the cumulative total is maintained indefinitely.

Show Signal Ranges

Because everything in this script is designed to make identifying sentiment extremes easier, an obvious inclusion would be to not only display ranges that are considered extreme for each Market Internal, but to also change the color of the plot when it is within, or beyond, that range. That is exactly what this setting does.

Override Max & Min

While the min-max signal levels have reasonable defaults for each symbol and transformation type, the Override Max and Override Min options allow you to … (wait for it) … override the max … and min … signal levels. This may be useful should you find a different level to be more suitable for your exact configuration.

Reduce Noise

This is the fourth data transformation . While the previous Ratio Norm. Threshold linearly stretches values between a threshold and 0, this setting will exponentially squash values closer to 0 if below the lower signal level.

The purpose of this is to compress data below the signal range, then amplify it as it approaches the signal level. If we are trying to identify extremes (the signal), minimizing values that are not extreme (the noise) can help us visually focus on what matters.

Always keep both signal zones visible

Some traders like to zoom in close to the bars. Others prefer to keep a wider focus. For those that like to zoom in, if both signals were always visible, the bar values can appear squashed and difficult to discern. For those that keep a wider focus, if both signals were not always visible, it's possible to lose context if a signal zone is vertically beyond the pane. This setting allows you to decide which scenario is best for you.

Plot Colors

These define the default color, within signal color, and beyond signal color for Bullish and Bearish directions.

Plot colors should be relative to zero

When enabled, the plot will inherit Bullish colors when above zero and Bearish colors when below zero. When disabled and Directional Colors are enabled (below), the plot will inherit the default Bullish color when rising, and the default Bearish color when falling. Otherwise, the plot will use the default Bullish color for all directions.

Directional colors

When the plot colors should be relative to zero (above), this changes the opacity of a bars color if moving toward zero, where "100" percent is the full value of the original color and "0" is transparent. When the plot colors are NOT relative to zero, the plot will inherit Bullish colors when rising and Bearish colors when falling.

Differentiate RTH from ETH

Market Internal data is typically only available during regular trading hours. When this setting is enabled, the background color of the indicator will change as a reminder that data is not available outside regular trading hours (RTH), if the chart is showing electronic trading hours (ETH).

Show zero line

Similar to always keeping signal zones visible (further up), some traders prefer zooming in while others prefer a wider context. This setting allows you to specify the visibility of the zero line to best suit your trading style.

Linear Regression

Polynomial regressions are great for capturing non-linear patterns in data. TradingView offers a "linear regression curve", which this script is using as a substitute. If you're unfamiliar with either term, think of this like a better moving average.

Symbol

While the Market Internal symbol will display in the status line of the indicator, the status line can be small and require more than a quick glance to read properly. Enabling this setting allows you to specify if / where / how the symbol should display on the indicator to make distinguishing between Market Internals more efficient.

Speaking of symbols, this indicator is designed for, and limited to, the following …

TICK - The TICK subtracts the total number of stocks making a downtick from the total number of stocks making an uptick.

ADD - The Advance Decline Difference subtracts the total number of stocks below yesterdays close from the total number of stocks above yesterdays close.

VOLD - The Volume Difference subtracts the total declining volume from the total advancing volume.

TRIN - The Arms Index (aka. Trading Index) divides the ratio of Advancing Stocks / Volume by the ratio of Declining Stocks / Volume. Given the inverse correlation of this index to market movement, when transforming it to a Ratio or Percent Diff., its values are inverted to preserve the bull-bear sentiment of the transformations.

VIX - The CBOE Volatility Index is derived from SPX index option prices, generating a 30-day forward projection of volatility. Given the inverse correlation of this index to market movement, when transforming it to a Ratio or Percent Diff., its values are inverted and normalized to the sessions first bar to preserve the bull-bear sentiment of the transformations. Note: If you do not have a Cboe CGIF subscription , VIX data will be delayed and plot unexpectedly.

ABVD - The Above VWAP Difference is an unofficial index measuring all stocks above VWAP as a percent difference. For the purposes of this indicator (and brevity), TradingViews PCTABOVEVWAP has has been shortened to simply be ABVD.

TKCD - The Tick Cumulative Difference is an unofficial index that subtracts the total number of market downticks from the total number of market upticks. Where "the TICK" (further up) is a measurement of stocks ticking up and down, TKCD is a measurement of the ticks themselves. For the purposes of this indicator (and brevity), TradingViews UPTKS and DNTKS symbols have been shorted to simply be TKCD.

INSPIRATION

I recently made an indicator automatically identifying / drawing daily percentage levels , based on 4 assumptions. One of these assumptions is about trend days. While trend days do not represent the majority of days, they can have big moves worth understanding, for both capitalization and risk mitigation.

To this end, I discovered:

• Article by Linda Bradford Raschke about Capturing Trend Days.

• Video of Garrett Drinon about Trend Day Trading.

• Videos of Ryan Trost about How To Use ADD and TICK.

• Article by Jason Ruchel about Overview of Key Market Internals.

• Including links to resources outside of TradingView violates the House Rules, but they're not hard to find, if interested.

These discoveries inspired me adopt the underlying symbols in my own trading. I also found myself wanting to make using them easier, the net result being this script.

While coding everything, I also discovered a few symbols I believe warrant serious consideration. Specifically the Percent Above VWAP symbols and the Up Ticks / Down Ticks symbols (referenced as ABVD and TKCD in this indicator, for brevity). I found transforming ABVD or TKCD into a Ratio or Percent Diff. to be an incredibly useful and worthy inclusion.

ABVD is a Market Breadth cousin to Brian Shannon's work, and TKCD is like the 3rd dimension of the TICKs geometry. Enjoy.

Custom Engulfing PatternThis script identifies bullish and bearish engulfing candlestick patterns based on user-defined criteria. It highlights the engulfing patterns on the chart for easy visualization. The script allows for customization of certain parameters to fine-tune the engulfing pattern detection according to the user's preferences.

Features:

Wick Ratio: Define a ratio to ensure that the body of both the current and previous candles comprises a significant portion of the total candle range.

Opposite Candle Condition: Ensures that the current and previous candles are of opposite types (one bullish and one bearish).

Body Size Relative to Previous Candles: Ensures that the body of the current candle is larger than the average body size of a specified number of previous candles.

Body Size Comparison: Ensures that the body of the engulfing candle is not more than 150% of the body of the previous candle.

Color Highlighting: Highlights bullish engulfing patterns in green and bearish engulfing patterns in red on the chart for easy identification.

Parameters:

tolerance (default: 0.0001): A tolerance value to account for minor price discrepancies when comparing candle open and close prices.

wick (default: 0.5): A ratio to define the significance of the candle body relative to the total candle range.

prevCandles (default: 6): Specifies the number of previous candles to consider when calculating the average body size for the body size relative condition.

Usage:

Adjust the tolerance, wick, and prevCandles parameters as needed to fine-tune the engulfing pattern detection to suit your trading style or the specific characteristics of the asset being analyzed. The script will highlight engulfing patterns on the chart, allowing for quick visual identification of potential trading opportunities based on these classic candlestick patterns.

Please note that this script is intended for educational and illustrative purposes. It should not be used as financial advice. Always conduct your own analysis and consult with a financial advisor before making any trading decisions.

RSI + FIB HH LL StopLoss Finder/Contrarian TradesThis indicator is a multi-timeframe indicator that works in any timeframe.

It takes a price reading of the highest or lowest bar in the past based on Fibonacci numbers and plots it.

In addition, the RSI smoothed by a 5-day moving average can be used to detect signs that previous highs or lows will be reached in advance.

This gives insight into determining stop-loss values or entering the market in a contrarian manner.

This is an example of BTCUSDT 4Hour Chart

Here is BTCUSDT 1Hour Chart

For scalpers BTCUSDT 15min Chart Example

Fibonacci Number is 1, 1, 2, 3, 5, 8, 13, 21, 34, 55, 89, 144, 233, 377, 610, 987, 1597, ...

FIbonacci Ratio is 0.236, 0.382, 0.5, 0.618, 1, 1.618, 2.618, 4.236, ...

Range Breakout Signals (Intrabar) [LuxAlgo]The Range Breakout Signals (Intrabar) is a novel indicator highlighting trending/ranging intrabar candles and providing signals when the price breaks the extremities of a ranging intrabar candles.

🔶 USAGE

The indicator highlights candles with trending intrabar prices, with uptrending candles being highlighted in green, and down-trending candles being highlighted in red.

This highlighting is affected by the selected intrabar timeframe, with a lower timeframe returning a more precise estimation of a candle trending/ranging state.

When a candle intrabar prices are ranging the body of the candle is hidden from the chart, and one upper & lower extremities are displayed, the upper extremity is equal to the candle high and the lower extremity to the candle low. Price breaking one of these extremities generates a signal.

The indicator comes with two modes, "Trend Following" and "Reversal", these modes determine the extremities that need to be broken in order to return a signal. The "Trend Following" mode as its name suggests will provide trend-following signals, while "Reversal" will aim at providing early signals suggesting a potential reversal.

🔶 DETAILS

To determine if intrabar prices are trending or ranging we calculate the r-squared of the intrabar data, if the r-squared is above 0.5 it would suggest that lower time frame prices are trending, else ranging.

This approach allows almost obtaining a "settings" free indicator, which is uncommon. The intrabar timeframe setting only controls the intrabar precision, with a timeframe significantly lower than the chart timeframe returning more intrabar data as a result, this however might not necessarily affect the displayed information by the indicator.

🔶 SETTINGS

Intrabar Timeframe: Timeframe used to retrieve the intrabar data within a chart candle. Must be lower than the user chart timeframe.

Auto: Select the intrabar timeframe automatically. This setting is more adapted to intraday charts.

Mode: Signal generation mode.

Filter Out Successive Signals: Allows removing successive signals of the same type, returning a more easily readable chart.

Ehlers SuperSmootherJohn F. Ehlers has provided the SuperSmoother filter in several of his works, including his book "Cyclical Analytics for Traders", Chapter 3.

The SuperSmoother filter is utilized whenever one might typically apply a moving average of any kind. The outcome is that the output signal from the SuperSmoother filter displays significantly less lag compared to an equivalent amount of smoothing from a moving average. The lag difference between a moving average and the SuperSmoother filter becomes even more pronounced when critical periods are extended.

Market data contains noise, and the purpose of smoothing filters is to mitigate this noise. In fact, there are various types of noise inherent in market data. One type of noise is systemic, originating from random trading activities. Another type is aliasing noise, which arises due to the use of discrete data. Aliasing noise dominates the data when considering shorter cycle durations.

It's tempting to perceive market data as a continuous wave, but that's a misconception. Taking the closing price as representative of a bar provides just a single data point. Whether you opt for the midpoint between the high and low instead of the closing price, you're still limited to one sample per bar. Given the discrete nature of this data, certain spectral implications must be considered. For instance, the shortest feasible analysis period (without aliasing) is a two-bar cycle. This is referred to as the Nyquist frequency, at 0.5 cycles per sample.

An ideally sampled two-beat sinusoidal cycle becomes rectified when discretized. However, peak sampling for the cycle isn't always guaranteed, and interference between the sampling rate and the data frequency results in aliasing noise. This noise decreases as the data period lengthens. For example, a four-beat cycle implies four samples per cycle. With more samples, the sampled data provides a better representation of the sinusoidal component. The replica becomes even more accurate for an eight-bar data component. The increased precision of discrete data signifies that aliasing noise decreases as cycle durations expand.

A smoothing filter should possess the selectivity to reduce the aliasing noise below systemic noise levels. Given that aliasing noise increases by 6 dB per octave above the filter's selected cutoff frequency and the SuperSmoother's attenuation rate is 12 dB per octave, the SuperSmoother filter emerges as an effective tool to virtually eliminate aliasing noise in its output signal.

There are already several SuperSmoother indicators on Tradingview, but I like to structure the code and highlight the main components as functions rather than hiding them in the code. I hope this is useful for those who are starting to learn Pine Script.

Fibonacci Ranges (Real-Time) [LuxAlgo]The "Fibonacci Ranges" indicator combines Fibonacci ratio-derived ranges (channels), together with a Fibonacci pattern of the latest swing high/low.

🔶 USAGE

The indicator draws real-time ranges based on Fibonacci ratios as well as retracements. Breakouts from a Fibonacci Channel are also indicated by labels, indicating a potential reversal.

Each range extremity/area can also be used as support/resistance.

🔶 CONCEPTS

Fibonacci Channels

Latest Fibonacci

Both, Latest Fibonacci and Fibonacci Channels , display different Fibonacci levels (labels not included in the code):

However, the 2 react in a totally different way.

🔹 Fibonacci Channels

2 conditions must be fulfilled until a Fibonacci Channel is displayed:

New swing high/low

close has to be between chosen limits/levels ( Break level )

As visual guidance, chosen Break levels are accentuated by 2 small gray blocks:

Once the channel is displayed, it will remain visible until x consecutive bars break out of the chosen Break level at closing time.

• x consecutive bars is set by Break count .

The amount of breaks is counted in the code. When the price, without breaking the user-set limit, closes back between the 2 levels, the count is reset to 0.

By enabling Channels and Shadows you can see previous channels (" Shadows ", which is always delayed with 1 bar)

Previous channels can be helpful in finding potential support/resistance areas, especially from large channel blocks

The more narrow Break levels are set the less chance the price closes between these 2 levels, and the quicker close breaks out.

In other words, narrow levels give fewer & smaller channels, broader levels give more & larger channels.

Note:

• swing settings: L & R

• Break count (x consecutive bars that close outside chosen levels to invalidate the Fibonacci Channel )

will also be of influence in displaying the channels.

• Show breaks enable you to visualize signals when there is a break:

• Alerts can also be set ( Break Down / Break Up )

🔹 Latest Fibonacci

This displays the Fibonacci levels between the latest swing high and swing low, independently from the Fibonacci Channel .

The Lastest Fibonacci can be helpful in detecting the current trend against the larger Fibonacci Channel .

🔶 SETTINGS

🔹 Swing Settings

L: set left of pivothigh / pivotlow

R: set right of pivothigh / pivotlow

🔹 Fibonacci Channels

Channel : Channel / Channels + Shadows / None

Break level

-0.382 - 1.382

0.000 - 1.000

0.236 - 0.764

0.382 - 0.618

Break count

🔹 Fibonacci

Toggle

Colours: [ -0.382 - 0 ], [ 0.236 - 0.382 ], [ 0.5 ], [ 0.618 - 0.764 ], [ 1 - 1.382 ]

Contrast Color LibraryThis lightweight library provides a utility method that analyzes any provided background color and automatically chooses the optimal black or white foreground color to ensure maximum visual contrast and readability.

🟠 Algorithm

The library utilizes the HSP Color Model to calculate the brightness of the background color. The formula for this calculation is as follows:

brightness = sqrt(0.299 * R^2 + 0.587 * G^2 + 0.114 * B^2 )

The library chooses black as the foreground color if the brightness exceeds the threshold (default 0.5), and white otherwise.

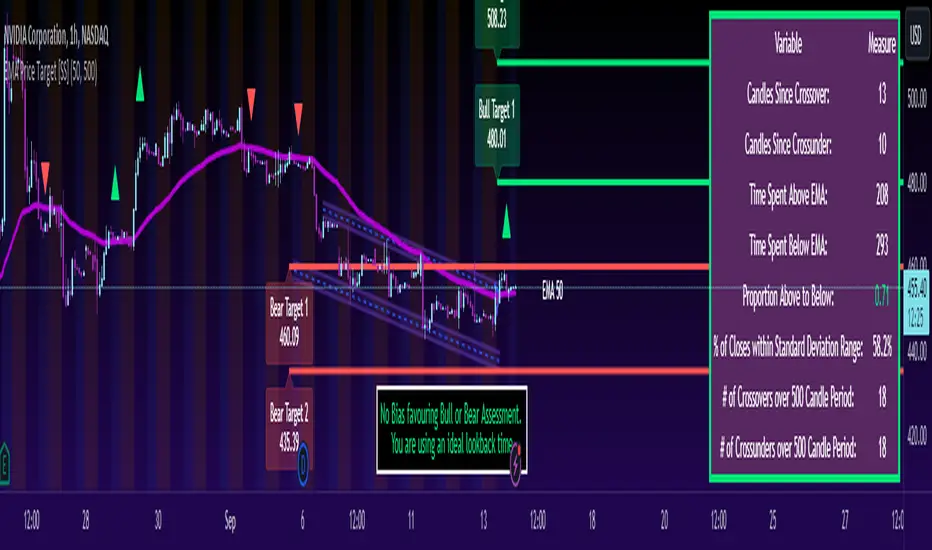

ATR Based EMA Price Targets [SS]As requested...

This is a spinoff of my EMA 9/21 cross indicator with price targets.

A few of you asked for a simple EMA crossover version and that is what this is.

I have, of course, added a bit of extra functionality to it, assuming you would want to transition from another EMA indicator to this one, I tried to leave it somewhat customizable so you can get the same type of functionality as any other EMA based indicator just with the added advantage of having an ATR based assessment added on. So lets get into the details:

What it does:

Same as my EMA 9/21, simply performs a basic ATR range analysis on a ticker, calculating the average move it does on a bullish or bearish cross.

How to use it:

So there are quite a few functions of this indicator. I am going to break them down one by one, from most basic to the more complex.

Plot functions:

EMA is Customizable: The EMA is customizable. If you want the 200, 100, 50, 31, 9, whatever you want, you just have to add the desired EMA timeframe in the settings menu.

Standard Deviation Bands are an option: If you like to have standard deviation bands added to your EMA's, you can select to show the standard deviation band. It will plot the standard deviation for the desired EMA timeframe (so if it is the EMA 200, it will plot the Standard Deviation on the EMA 200).

Plotting Crossovers: You can have the indicator plot green arrows for bullish crosses and red arrows for bearish crosses. I have smoothed out this function slightly by only having it signal a crossover when it breaks and holds. I pulled this over to the alert condition functions as well, so you are not constantly being alerted when it is bouncing over and below an EMA. Only once it chooses a direction, holds and moves up or down, will it alert to a true crossover.

Plotting labels: The indicator will default to plotting the price target labels and the EMA label. You can toggle these on and off in the EMA settings menu.

Trend Assessment Settings:

In addition to plotting the EMA itself and signaling the ATR ranges, the EMA will provide you will demographic information about the trend and price action behaviour around the EMA. You can see an example in the image below:

This will provide you with a breakdown of the statistics on the EMA over the designated lookback period, such as the number of crosses, the time above and below the EMA and the amount the EMA has remained within its standard deviation bands.

Where this is important is the proportion assessment. And what the proportion assessment is doing is its measuring the amount of time the ticker is spending either above or below the EMA.

Ideally, you should have relatively equal and uniform durations above and below. This would be a proportion of between 0.5 and 1.5 Above to Below. Now, you don't have to remember this because you can ask the indicator to do the assessment for you. It will be displayed at the bottom of your chart in a table that you can toggle on and off:

Example of a Uniform Assessment:

Example of a biased assessment:

Keep in mind, if you are using those very laggy EMAs (like the 50, 200, 100 etc.) on the daily timeframe, you aren't going to get uniformity in the data. This is because, stocks are technically already biased to the upside over time. Thus, when you are looking at the big picture, the bull bias thesis of the stock market is in play.

But for the smaller and moderate timeframes, owning to the randomness of price action, you can generally get uniformity in data representation by simply adjusting your lookback period.

To adjust your lookback period, you simply need to change the timeframe for the ATR lookback length. I suggest no less than 500 and probably no more than 1,500 candles, and work within this range. But you can use what the indicator indicates is appropriate.

Of course, all of these charts can be turned off and you are left with a clean looking EMA indicator:

And an example with the standard deviation bands toggled on:

And that, my friends, is the indicator.

Hopefully this is what you wanted, let me know if you have any suggestions.

Enjoy and safe trades!

Risk Management and Positionsize - MACD exampleMastering Risk Management

Risk management is the cornerstone of successful trading, and it's often the difference between turning a profit and suffering a loss. In light of its importance, I share a risk management tool which you can use for your trading strategies. The script not only assists in position sizing but also comes with built-in technical features that help in market timing. Let's delve into the nitty-gritty details.

Input Parameter: MarginFactor

One of the key features of the script is the MarginFactor input parameter. This element lets you control the portion of your equity used for placing each trade. A MarginFactor of -0.5 means 50% of your total equity will be deployed in placing the position size. Although Tradingview has a built-in option to adjust position sizing in a same way, I personally prefer to have the logic in my pinecode script. The main reason is userexperience in managing and testing different settings for different charts, timeframes and instruments (with the same strategy).

Stoploss and MarginFactor

If your strategy has a 4% stop-loss, you can choose to use only 50% of your equity by setting the MarginFactor to -0.5. In this case, you are effectively risking only 2% of your total capital per trade, which aligns well with the widely-accepted rule of thumb suggesting a 1-2% risk per trade. Similar if your stoploss is only 1% you can choose to change the MarginFactor to 1, resulting in a positionsize of 200% of your equity. The total risk would be again 2% per trade if your stoploss is set to 1%.

Max Drawdown and MarginFactor

Your MarginFactor setting can also be aligned with the maximum drawdown of your strategy, seen during a backtested period of 2-3 years. For example, if the max drawdown is 15%, you could calibrate your MarginFactor accordingly to limit your risk exposure.

Option to Toggle Number of Contracts

The script offers the option to toggle between using a percentage of equity for position sizing or specifying a fixed number of contracts. Utilizing a percentage of equity might yield unrealistic backtest results, especially over longer periods. This occurs because as the capital grows, the absolute position size also increases, potentially inflating the accumulated returns generated by the backtester. On the other hand, setting a fixed number of contracts as your position size offers a more stable and realistic ROI over the backtested period, as it removes the compounding effect on position sizes.

Key Features Strategy

MACD High Time Frame Entry and Exit Logic

The strategy employs a high time frame MACD (Moving Average Convergence Divergence) to make entry and exit decisions. You can easily adjust the timeframe settings and MACD settings in the inputsection to trade on lower timeframes. For more information on the HTF MACD with dynamic smoothing see:

Moving Average High Time Frame Filter

To reduce market 'noise', the strategy incorporates a high time frame moving average filter. This ensures that the trades are aligned with the dominant market trend (trading the trend). In the inputsection traders can easily switch between different type of moving averages. For more information about this HTF filter see:

Dynamic Smoothing

The script includes a feature for dynamic smoothing. The script contains The timeframeToMinutes(tf) function to convert any given time frame into its equivalent in minutes. For example, a daily (D) time frame is converted into 1440 minutes, a weekly (W) into 10,080 minutes, and so forth. Next the smoothing factor is calculated by dividing the minutes of the higher time frame by those of the current time frame. Finally, the script applies a Simple Moving Average (SMA) over the MACD, SIGNAL, and HIST values, MA filter using the dynamically calculated smoothing factor.

User Convenience: One of the major benefits is that traders don't need to manually adjust the smoothing factor when switching between different time frames. The script does this dynamically.

Visual Consistency: Dynamic smoothing helps traders to more accurately visualize and interpret HTF indicators when trading on lower time frames.

Time Frame Restriction: It's crucial to note that the operational time frame should always be lower than the time frame selected in the input sections for dynamic smoothing to function as intended.

By incorporating this dynamic smoothing logic, the script offers traders a nuanced yet straightforward way to adapt High Time Frame indicators for lower time frame trading, enhancing both adaptability and user experience.

Limitations: Exit Strategy

It's crucial to note that the script comes with a simplified exit strategy, devoid of features like a stop-loss, trailing stop-loss or multiple take profits. This means that while the script focuses on entries and risk management, it might result in higher losses if market conditions unexpectedly turn unfavorable.

Conclusion

Effective risk management is pivotal for trading success, and this TradingView script is designed to give you a better idea how to implement positions sizing with your preferred strategy. However, it's essential to note that this tool should not be considered financial advice. Always perform your due diligence and consult with financial advisors before making any trading decisions.

Feel free to use this risk management tool as building block in your trading scripts, Happy Trading!

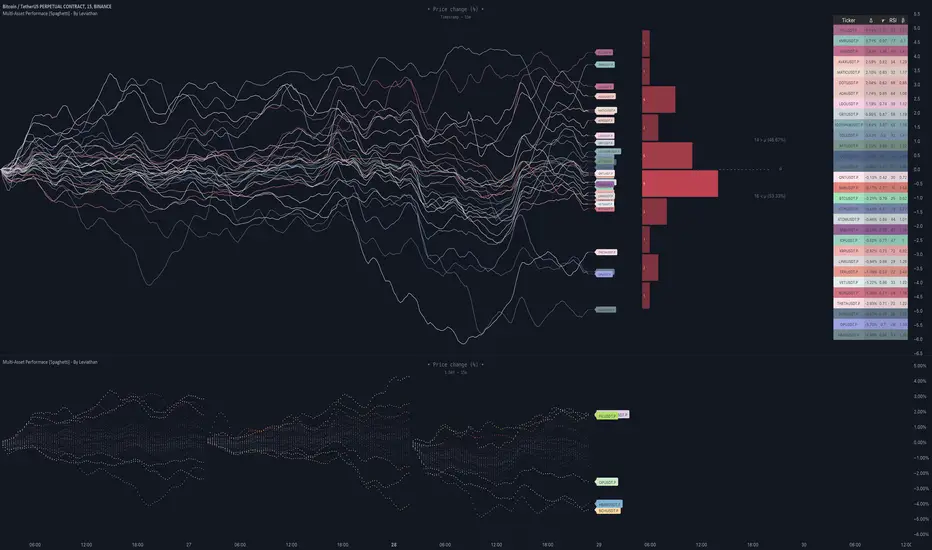

Multi-Asset Performance [Spaghetti] - By LeviathanThis indicator visualizes the cumulative percentage changes or returns of 30 symbols over a given period and offers a unique set of tools and data analytics for deeper insight into the performance of different assets.