RVI_HTFThe "RVI_HTF" indicator is a tool designed to assist traders in analyzing market trends using the Relative Vigor Index (RVI) across different timeframes. It enables users to customize various aspects of the indicator's appearance and behavior. By monitoring the RVI on different timeframes, tracking its relationship with the moving average, and paying attention to extreme arrows above the 80 or below the 20 line, traders can anticipate potential reversals, trends, or changes in market momentum.

Above 80 Line: When the RVI moves above the 80 line, it suggests that the market may be overbought. Extreme upward arrows (indicating potential sell signals) can be a sign that a bullish trend might be reaching an exhaustion point. Traders may anticipate a possible trend reversal or pullback.

Below 20 Line: When the RVI dips below the 20 line, it implies that the market might be oversold. Extreme downward arrows (indicating potential buy signals) can be an early signal of a potential bullish reversal. Traders may anticipate an upcoming uptrend or bounce.

Crossing Above Moving Average: When the RVI crosses above its moving average on the selected timeframe, it can serve as an early indication of potential bullish strength in the market. This suggests that buying pressure may be increasing.

Crossing Below Moving Average: Conversely, when the RVI crosses below its moving average, it can signal potential bearish momentum. This indicates that selling pressure may be gaining strength.

Variables:

Timeframe (TF) Selection:

The indicator allows you to select the timeframe for the RVI calculation. You can choose from various options such as 1 minute (1), 5 minutes (5), 15 minutes (15), 30 minutes (30), 60 minutes (60), 240 minutes (240), Daily (D), Weekly (W), Monthly (M), or use "Auto" to automatically select a higher timeframe based on your current chart's timeframe.

Moving Average Type (MA_Type):

Function: Allows users to select the type of moving average used in RVI calculations.

Options: You can select from various moving average types, including:

SMA (Simple Moving Average)

EMA (Exponential Moving Average)

SMMA (Smoothed Moving Average, also known as RMA)

WMA (Weighted Moving Average)

VWMA (Volume Weighted Moving Average)

DEMA (Double Exponential Moving Average)

Moving Average Length (MA_Length):

Function: Permits users to set the number of periods for the selected moving average type.

Purpose: Controls the sensitivity of the RVI indicator. Longer lengths provide smoother results, while shorter lengths react more quickly to price changes.

Up Arrow Color (upArrowColor):

Function: Enables users to customize the color of arrows that indicate potential Overbought areas. (Only shown when the TF is same as or lower than the chart TF)

Down Arrow Color (downArrowColor):

Function: Allows users to specify the color of downward-pointing arrows signaling potential Oversold areas. (Only shown when the TF is same as or lower than the chart TF)

RVI Up Color (firstColor):

Function: Defines the color of the RVI line when it indicates a bullish condition on the higher timeframe.

RVI Down Color (secondColor):

Function: Specifies the color of the RVI line when it suggests a bearish condition on the higher timeframe.

RVI-Based Moving Average Up Color (firstColorMA):

Function: Customizes the color of the RVI-based moving average line when it indicates a bullish condition.

RVI-Based Moving Average Down Color (secondColorMA):

Function: Defines the color of the RVI-based moving average line when it suggests a bearish condition.

"股票开盘前15分钟交易规则" için komut dosyalarını ara

Heatmap MACD Strategy - Pineconnector (Dynamic Alerts)Hello traders

This script is an upgrade of this template script.

Heatmap MACD Strategy

Pineconnector

Pineconnector is a trading bot software that forwards TradingView alerts to your Metatrader 4/5 for automating trading.

Many traders don't know how to dynamically create Pineconnector-compatible alerts using the data from their TradingView scripts.

Traders using trading bots want their alerts to reflect the stop-loss/take-profit/trailing-stop/stop-loss to breakeven options from your script and then create the orders accordingly.

This script showcases how to create Pineconnector alerts dynamically.

Pineconnector doesn't support alerts with multiple Take Profits.

As a workaround, for 2 TPs, I had to open two trades.

It's not optimal, as we end up paying more spreads for that extra trade - however, depending on your trading strategy, it may not be a big deal.

TradingView Alerts

1) You'll have to create one alert per asset X timeframe = 1 chart.

Example : 1 alert for EUR/USD on the 5 minutes chart, 1 alert for EUR/USD on the 15-minute chart (assuming you want your bot to trade the EUR/USD on the 5 and 15-minute timeframes)

2) For each alert, the alert message is pre-configured with the text below

{{strategy.order.alert_message}}

Please leave it as it is.

It's a TradingView native variable that will fetch the alert text messages built by the script.

3) Don't forget to set the webhook URL in the Notifications tab of the TradingView alerts UI.

EA configuration

The Pyramiding in the EA on Metatrader must be set to 2 if you want to trade with 2 TPs => as it's opening 2 trades.

If you only want 1 TP, set the EA Pyramiding to 1.

Regarding the other EA settings, please refer to the Pineconnector documentation on their website.

Logger

The Pineconnector commands are logged in the TradingView logger.

You'll find more information about it from this TradingView blog post

Important Notes

1) This multiple MACDs strategy doesn't matter much.

I could have selected any other indicator or concept for this script post.

I wanted to share an example of how you can quickly upgrade your strategy, making it compatible with Pineconnector.

2) The backtest results aren't relevant for this educational script publication.

I used realistic backtesting data but didn't look too much into optimizing the results, as this isn't the point of why I'm publishing this script.

3) This template is made to take 1 trade per direction at any given time.

Pyramiding is set to 1 on TradingView.

The strategy default settings are:

Initial Capital: 100000 USD

Position Size: 1 contract

Commission Percent: 0.075%

Slippage: 1 tick

No margin/leverage used

For example, those are realistic settings for trading CFD indices with low timeframes but not the best possible settings for all assets/timeframes.

Concept

The Heatmap MACD Strategy allows selecting one MACD in five different timeframes.

You'll get an exit signal whenever one of the 5 MACDs changes direction.

Then, the strategy re-enters whenever all the MACDs are in the same direction again.

It takes:

long trades when all the 5 MACD histograms are bullish

short trades when all the 5 MACD histograms are bearish

You can select the same timeframe multiple times if you don't need five timeframes.

For example, if you only need the 30min, the 1H, and 2H, you can set your timeframes as follow:

30m

30m

30m

1H

2H

Risk Management Features

All the features below are pips-based.

Stop-Loss

Trailing Stop-Loss

Stop-Loss to Breakeven after a certain amount of pips has been reached

Take Profit 1st level and closing X% of the trade

Take Profit 2nd level and close the remaining of the trade

Custom Exit

I added the option ON/OFF to close the opened trade whenever one of the MACD diverges with the others.

Help me help the community

If you see any issue when adding your strategy logic to that template regarding the orders fills on your Metatrader, please let me know in the comments.

I'll use your feedback to make this template more robust. :)

What's next?

I'll publish a more generic template built as a connector so you can connect any indicator to that Pineconnector template.

Then, I'll publish a template for Capitalise AI, ProfitView, AutoView, and Alertatron.

Thank you

Dave

skThis Pine Script is an indicator designed to mark and highlight specific trading sessions on a TradingView chart. Here's a description of the script's functionality:

1. *Session Selection*: The script allows you to select a session time frame using the `session_input` input. The available options for session time frames are "D" (daily), "W" (weekly), "M" (monthly), "H" (hourly), "15" (15 minutes), "5" (5 minutes), and "1" (1 minute).

2. *Session Times*: You can specify the start and end times for three different trading sessions - CBDR (Central Bank Dealer Range), Asia, and London - using the corresponding input options. These times are specified in Indian Standard Time (IST).

3. *Time Calculation*: The script calculates the start and end times for each session based on the specified hours and minutes. It uses the `timestamp` function to create time objects for these sessions.

4. *Session Highlighting*: The script creates rectangles on the chart to highlight each session:

- CBDR Session: A gray rectangle is drawn during the CBDR session time.

- Asia Session: Another gray rectangle is drawn during the Asia session time.

- London Session: A green rectangle is drawn at the top of the chart during the London session time.

5. *Transparency*: The rectangles have a transparency level of 90%, allowing you to see the price data beneath them while still marking the sessions.

6. *Overlay*: The indicator is set to overlay on the price chart, so it doesn't obstruct the price data.

7. *Customization*: You can customize the session times and appearance by adjusting the input values in the settings panel of the indicator.

Overall, this script provides a visual way to identify and highlight specific trading sessions on your TradingView chart, helping traders understand price action in different market sessions.

libHTF[without request.security()]Library "libHTF"

libHTF: use HTF values without request.security()

This library enables to use HTF candles without request.security().

Basic data structure

Using to access values in the same manner as series variable.

The last member of HTF array is always latest current TF's data.

If new bar in HTF(same as last bar closes), new member is pushed to HTF array.

2nd from the last member of HTF array is latest fixed(closed) bar.

HTF: How to use

1. set TF

tf_higher() function selects higher TF. TF steps are ("1","5","15","60","240","D","W","M","3M","6M","Y").

example:

tfChart = timeframe.period

htf1 = tf_higher(tfChart)

2. set HTF matrix

htf_candle() function returns 1 bool and 1 matrix.

bool is a flag for start of new candle in HTF context.

matrix is HTF candle data(0:open,1:time_open,2:close,3:time_close,4:high,5:time:high,6:low,7:time_low).

example:

=htf_candle(htf1)

3. how to access HTF candle data

you can get values using .lastx() method.

please be careful, return value is always float evenif it is "time". you need to cast to int time value when using for xloc.bartime.

example:

htf1open=m1.lastx("open")

htf1close=m1.lastx("close")

//if you need to use histrical value.

lastopen=open

lasthtf1open=m1.lastx("open",1)

4. how to store Data of HTF context

you have to use array to store data of HTF context.

array.htf_push() method handles the last member of array. if new_bar in HTF, it push new member. otherwise it set value to the last member.

example:

array a_close=array.new(1,na)

a_close.htf_push(b_new_bar1,m1.lastx("close"))

HTFsrc: How to use

1. how to setup src.

set_src() function is set current tf's src from string(open/high/low/close/hl2/hlc3/ohlc4/hlcc4).

set_htfsrc() function returns src array of HTF candle.

example:

_src="ohlc4"

src=set_src(_src)

htf1src=set_htfsrc(_src,b_new_bar1,m1)

(if you need to use HTF src in series float)

s_htf1src=htf1src.lastx()

HighLow: How to use

1. set HTF arrays

highlow() and htfhighlow() function calculates high/low and return high/low prices and time.

the functions return 1 int and 8arrays.

int is a flag for new high(1) or new low(-1).

arrays are high/low and return high/low data. float for price, int for time.

example

=

highlow()

=

htfhighlow(m1)

2. how to access HighLow data

you can get values using .lastx() method.

example:

if i_renew==1

myhigh=a_high.lastx()

//if you need to use histrical value.

myhigh=a_high.lastx(1)

other functions

functions for HTF candle matrix or HTF src array in this script are

htf_sma()/htf_ema()/htf_rma()

htf_rsi()/htf_rci()/htf_dmi()

method lastx(arrayid, lastindex)

method like array.last. it returns lastindex from the last member, if parameter is set.

Namespace types: float

Parameters:

arrayid (float )

lastindex (int) : (int) default value is "0"(the last member). if you need to access historical value, increment it(same manner as series vars).

Returns: float value of lastindex from the last member of the array. returns na, if fail.

method lastx(arrayid, lastindex)

method like array.last. it returns lastindex from the last member, if parameter is set.

Namespace types: int

Parameters:

arrayid (int )

lastindex (int) : (int) default value is "0"(the last member). if you need to access historical value, increment it(same manner as series vars).

Returns: int value of lastindex from the last member of the array. returns na, if fail.

method lastx(m, _type, lastindex)

method for handling htf matrix.

Namespace types: matrix

Parameters:

m (matrix) : (matrix) matrix for htf candle.

_type (string) : (string) value type of htf candle:

lastindex (int) : (int) default value is "0"(the last member).

Returns: (float) value of htf candle. (caution: need to cast float to int to use time values!)

method set_last(arrayid, val)

method to set a value of the last member of the array. it sets value to the last member.

Namespace types: float

Parameters:

arrayid (float )

val (float) : (float) value to set.

Returns: nothing

method htf_push(arrayid, b, val)

method to push new member to htf context. if new bar in htf, it works as push. else it works as set_last.

Namespace types: float

Parameters:

arrayid (float )

b (bool) : (bool) true:push,false:set_last

val (float) : (float) _f the value to set.

Returns: nothing

method tf_higher(tf)

method to set higher tf from tf string. TF steps are .

Namespace types: series string, simple string, input string, const string

Parameters:

tf (string) : (string) tf string

Returns: (string) string of higher tf.

htf_candle(_tf, _TZ)

build htf candles

Parameters:

_tf (string) : (string) tf string.

_TZ (string) : of timezone. default value is "GMT+3".

Returns: bool for new bar@htf and matrix for snapshot of htf candle

set_src(_src_type)

set src.

Parameters:

_src_type (string) : (string) type of source:

Returns: (series float) src value

set_htfsrc(_src_type, _nb, _m)

set htf src.

Parameters:

_src_type (string) : (string) type of source:

_nb (bool) : (bool) flag of new bar

_m (matrix) : (matrix) matrix for htf candle.

Returns: (array) array of src value

is_up()

last_is_up()

peak_bottom(_latest, _last)

Parameters:

_latest (bool)

_last (bool)

htf_is_up(_m)

Parameters:

_m (matrix)

htf_last_is_up(_m)

Parameters:

_m (matrix)

highlow(_b_bartime_price)

Parameters:

_b_bartime_price (bool)

htfhighlow(_m, _b_bartime_price)

Parameters:

_m (matrix)

_b_bartime_price (bool)

htf_sma(_a_src, _len)

Parameters:

_a_src (float )

_len (int)

htf_rma(_a_src, _new_bar, _len)

Parameters:

_a_src (float )

_new_bar (bool)

_len (int)

htf_ema(_a_src, _new_bar, _len)

Parameters:

_a_src (float )

_new_bar (bool)

_len (int)

htf_rsi(_a_src, _new_bar, _len)

Parameters:

_a_src (float )

_new_bar (bool)

_len (int)

rci(_src, _len)

Parameters:

_src (float)

_len (int)

htf_rci(_a_src, _len)

Parameters:

_a_src (float )

_len (int)

htf_dmi(_m, _new_bar, _len, _ma_type)

Parameters:

_m (matrix)

_new_bar (bool)

_len (int)

_ma_type (string)

TASC 2023.09 The Weekly Factor█ OVERVIEW

TASC's September 2023 edition of Traders' Tips features an article written by Andrea Unger titled “The Weekly Factor", discussing the application of price patterns as filters for trade entries. This script implements a sample trading strategy presented in the article for demonstration purposes only. It explores how the strategy's equity curve might benefit from filtering trade entries using a specific price pattern.

█ CONCEPTS

Pattern filters represent valuable tools that assess current market conditions based on price movements and determine when those conditions become more favorable for trade entries.

The filter used and tested in this article is a metric called the "weekly factor", which measures the price range over the last five trading days and compares it to the open of the session five days ago and the close of the session one day ago (i.e., the "body" of the five-day period). When the five-day body is small compared to the five-day range, this could indicate "indecision" or "compression", potentially followed by a price expansion. Thus, the weekly factor metric can help identify areas in the market where a period of compression might signal a potential breakout.

This script demonstrates the use of the weekly factor for a sample intraday trading strategy (intended for educational and exploratory purposes only). In this strategy, the entry signal is triggered when a 15-minute bar breaks out of the previous day's high-low range, and the position is closed at the end of the day.

█ CALCULATIONS

The script uses two timeframes:

• The strategy entries are processed on the 15-minute timeframe.

• The weekly factor is obtained from the daily timeframe using the request.security function and the following formula:

math.abs(open - close ) < RangeFilter * (ta.highest(5) - ta.lowest(5) )

Here, RangeFilter is an input that can be optimized to find the favorable ratio between the five-day body and the five-day range. Smaller RangeFilter values will lead to fewer trade entries. A RangeFilter value of 1 is equivalent to turning off the filtering altogether.

Multi-Timeframe Trend Detector [Alifer]Here is an easy-to-use and customizable multi-timeframe visual trend indicator.

The indicator combines Exponential Moving Averages (EMA), Moving Average Convergence Divergence (MACD), and Relative Strength Index (RSI) to determine the trend direction on various timeframes: 15 minutes (15M), 30 minutes (30M), 1 hour (1H), 4 hours (4H), 1 day (1D), and 1 week (1W).

EMA Trend : The script calculates two EMAs for each timeframe: a fast EMA and a slow EMA. If the fast EMA is greater than the slow EMA, the trend is considered Bullish; if the fast EMA is less than the slow EMA, the trend is considered Bearish.

MACD Trend : The script calculates the MACD line and the signal line for each timeframe. If the MACD line is above the signal line, the trend is considered Bullish; if the MACD line is below the signal line, the trend is considered Bearish.

RSI Trend : The script calculates the RSI for each timeframe. If the RSI value is above a specified Bullish level, the trend is considered Bullish; if the RSI value is below a specified Bearish level, the trend is considered Bearish. If the RSI value is between the Bullish and Bearish levels, the trend is Neutral, and no arrow is displayed.

Dashboard Display :

The indicator prints arrows on the dashboard to represent Bullish (▲ Green) or Bearish (▼ Red) trends for each timeframe.

You can easily adapt the Dashboard colors (Inputs > Theme) for visibility depending on whether you're using a Light or Dark theme for TradingView.

Usage :

You can adjust the indicator's settings such as theme (Dark or Light), EMA periods, MACD parameters, RSI period, and Bullish/Bearish levels to adapt it to your specific trading strategies and preferences.

Disclaimer :

This indicator is designed to quickly help you identify the trend direction on multiple timeframes and potentially make more informed trading decisions.

You should consider it as an extra tool to complement your strategy, but you should not solely rely on it for making trading decisions.

Always perform your own analysis and risk management before executing trades.

The indicator will only show a Dashboard. The EMAs, RSI and MACD you see on the chart image have been added just to demonstrate how the script works.

DETAILED SCRIPT EXPLANATION

INPUTS:

theme : Allows selecting the color theme (options: "Dark" or "Light").

emaFastPeriod : The period for the fast EMA.

emaSlowPeriod : The period for the slow EMA.

macdFastLength : The fast length for MACD calculation.

macdSlowLength : The slow length for MACD calculation.

macdSignalLength : The signal length for MACD calculation.

rsiPeriod : The period for RSI calculation.

rsiBullishLevel : The level used to determine Bullish RSI condition, when RSI is above this value. It should always be higher than rsiBearishLevel.

rsiBearishLevel : The level used to determine Bearish RSI condition, when RSI is below this value. It should always be lower than rsiBullishLevel.

CALCULATIONS:

The script calculates EMAs on multiple timeframes (15-minute, 30-minute, 1-hour, 4-hour, daily, and weekly) using the request.security() function.

Similarly, the script calculates MACD values ( macdLine , signalLine ) on the same multiple timeframes using the request.security() function along with the ta.macd() function.

RSI values are also calculated for each timeframe using the request.security() function along with the ta.rsi() function.

The script then determines the EMA trends for each timeframe by comparing the fast and slow EMAs using simple boolean expressions.

Similarly, it determines the MACD trends for each timeframe by comparing the MACD line with the signal line.

Lastly, it determines the RSI trends for each timeframe by comparing the RSI values with the Bullish and Bearish RSI levels.

PLOTTING AND DASHBOARD:

Color codes are defined based on the EMA, MACD, and RSI trends for each timeframe. Green for Bullish, Red for Bearish.

A dashboard is created using the table.new() function, displaying the trend information for each timeframe with arrows representing Bullish or Bearish conditions.

The dashboard will appear in the top-right corner of the chart, showing the Bullish and Bearish trends for each timeframe (15M, 30M, 1H, 4H, 1D, and 1W) based on EMA, MACD, and RSI analysis. Green arrows represent Bullish trends, red arrows represent Bearish trends, and no arrows indicate Neutral conditions.

INFO ON USED INDICATORS:

1 — EXPONENTIAL MOVING AVERAGE (EMA)

The Exponential Moving Average (EMA) is a type of moving average (MA) that places a greater weight and significance on the most recent data points.

The EMA is calculated by taking the average of the true range over a specified period. The true range is the greatest of the following:

The difference between the current high and the current low.

The difference between the previous close and the current high.

The difference between the previous close and the current low.

The EMA can be used by traders to produce buy and sell signals based on crossovers and divergences from the historical average. Traders often use several different EMA lengths, such as 10-day, 50-day, and 200-day moving averages.

The formula for calculating EMA is as follows:

Compute the Simple Moving Average (SMA).

Calculate the multiplier for weighting the EMA.

Calculate the current EMA using the following formula:

EMA = Closing price x multiplier + EMA (previous day) x (1-multiplier)

2 — MOVING AVERAGE CONVERGENCE DIVERGENCE (MACD)

The Moving Average Convergence Divergence (MACD) is a popular trend-following momentum indicator used in technical analysis. It helps traders identify changes in the strength, direction, momentum, and duration of a trend in a financial instrument's price.

The MACD is calculated by subtracting a longer-term Exponential Moving Average (EMA) from a shorter-term EMA. The most commonly used time periods for the MACD are 26 periods for the longer EMA and 12 periods for the shorter EMA. The difference between the two EMAs creates the main MACD line.

Additionally, a Signal Line (usually a 9-period EMA) is computed, representing a smoothed version of the MACD line. Traders watch for crossovers between the MACD line and the Signal Line, which can generate buy and sell signals. When the MACD line crosses above the Signal Line, it generates a bullish signal, indicating a potential uptrend. Conversely, when the MACD line crosses below the Signal Line, it generates a bearish signal, indicating a potential downtrend.

In addition to the MACD line and Signal Line crossovers, traders often look for divergences between the MACD and the price chart. Divergence occurs when the MACD is moving in the opposite direction of the price, which can suggest a potential trend reversal.

3 — RELATIVE STRENGHT INDEX (RSI):

The Relative Strength Index (RSI) is another popular momentum oscillator used by traders to assess the overbought or oversold conditions of a financial instrument. The RSI ranges from 0 to 100 and measures the speed and change of price movements.

The RSI is calculated based on the average gain and average loss over a specified period, commonly 14 periods. The formula involves several steps:

Calculate the average gain over the specified period.

Calculate the average loss over the specified period.

Calculate the relative strength (RS) by dividing the average gain by the average loss.

Calculate the RSI using the following formula: RSI = 100 - (100 / (1 + RS))

The RSI oscillates between 0 and 100, where readings above 70 are considered overbought, suggesting that the price may have risen too far and could be due for a correction. Readings below 30 are considered oversold, suggesting that the price may have dropped too much and could be due for a rebound.

Traders often use the RSI to identify potential trend reversals. For example, when the RSI crosses above 30 from below, it may indicate the start of an uptrend, and when it crosses below 70 from above, it may indicate the start of a downtrend. Additionally, traders may look for bullish or bearish divergences between the RSI and the price chart, similar to the MACD analysis, to spot potential trend changes.

BTFD strategy [3min]Hello

I would like to introduce a very simple strategy to buy lows and sell with minimal profit

This strategy works very well in the markets when there is no clear trend and in other words, the trend going sideways

this strategy works very well for stable financial markets like spx500, nasdaq100 and dow jones 30

two indicators were used to determine the best time to enter the market:

volume + rsi values

volume is usually the number of stocks or contracts traded over a certain period of time. Thus, it is an important indicator of market activity and liquidity. Each transaction constitutes an individual exchange between the buyer and the seller and constitutes the trading volume of a given instrument or asset.

The RSI measures the strength of uptrends versus downtrends. The signal is the entry or exit of the indicator value of the oversold or overbought level of the market. It is assumed that a value below or equal 30 indicates an oversold level of the market, and an RSI value above or equal 70 indicates an overbought level.

the strategy uses a maximum of 5 market entries after each candle that meets the condition

uses 5 target point levels to close the position:

tp1= 0.4%

tp2= 0.6%

tp3= 0.8%

tp4= 1.0%

tp5= 1.2%

after reaching a given profit value, a piece of the position is cut off gradually, where tp5 closes 100% of the remaining position

each time you enter a position, a stop loss of 5.0% is set, which is quite a high value, however, when buying each, sometimes very active downward price movement, you need a lot of space for market decisions in which direction it wants to go

to determine the level of stop loss and target point I used a piece of code by RafaelZioni , here is the script from which a piece of code was taken

this strategy is used for automation, however, I would recommend brokers that have the lowest commission values when opening and closing positions, because the strategy generates very high commission costs

Enjoy and trade safe ;)

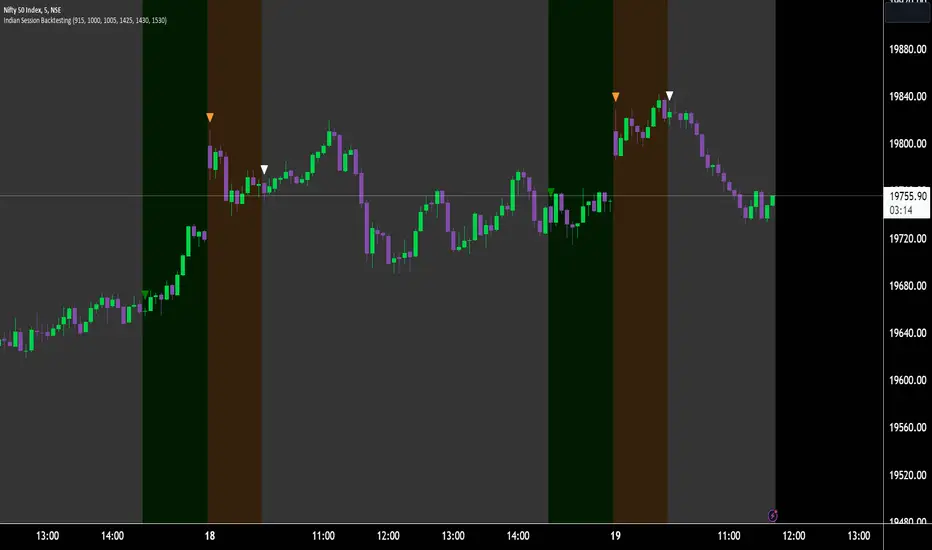

Indian Market Sessions for BacktestingThis indicator is designed to increase the quality of your backtesting in the Indian Market.

NSE & BSE run from 9:15 am IST to 3:30 pm IST.

Naturally different times have different kinds of volatility.

On your chart you will find premarked -

Saffron - 9:15 am to 10:30 am - Opening Session - High Volatility Observed Historically

White - 10:35 am to 2:25 pm - Middle Session - Lower Volatility Observed Historically

Green - 2:30 pm to 3:30 pm - Closing Session - Medium to High Volatility Observed Historically

You will also find the start of each session marked with an arrow.

Feel free to change the times from the input settings and the color and visibility from the style settings.

_______________

Usage:

When you backtest any strategies, say moving average crossovers, also mark the sessions in your sheet which will help you further increase accuracy.

Feel free to drop your doubts in the comments.

Volatility Capture RSI-Bollinger - Strategy [presentTrading]- Introduction and how it is different

The 'Volatility Capture RSI-Bollinger - Strategy ' is a trading strategy that combines the concepts of Bollinger Bands (BB), Relative Strength Index (RSI), and Simple Moving Average (SMA) to generate trading signals. The uniqueness of this strategy is it calculates which is a dynamic level between the upper and lower Bollinger Bands based on the closing price. This unique feature allows the strategy to adapt to market volatility and price movements.

The market in Crypto and Stock are highly volatile, making them suitable for a strategy that uses Bollinger Bands. The RSI can help identify overbought or oversold conditions in this often speculative market.

BTCUSD 4hr chart

(700.hk) 3hr chart

Remember, the effectiveness of a trading strategy also depends on other factors such as the timeframe used, the specific settings of the indicators, and the overall market conditions. It's always recommended to backtest and paper trade a strategy before using it in live trading.

- Strategy, How it Works

Dynamic Bollinger Band: The strategy works by first calculating the upper and lower Bollinger Bands based on the user-defined length and multiplier. It then uses the Bollinger Bands and the closing price to dynamically adjust the presentBollingBand value. In the end, it generates a long signal when the price crosses over the present Bolling Band and a short signal when the price crosses under the present Bolling Band.

RSI: If the user has chosen to use RSI for signals, the strategy also calculates the RSI and its SMA, and uses these to generate additional long and short signals. The RSI-based signals are only used if the 'Use RSI for signals' option is set to true.

The strategy then checks the chosen trading direction and enters a long or short position accordingly. If the trading direction is set to 'Both', the strategy can enter both long and short positions.

Finally, the strategy exits a position when the close price crosses under the present Bolling Band for a long position, or crosses over the present Bolling Band for a short position.

- Trade direction

The strategy also includes a trade direction parameter, allowing the user to choose whether to enter long trades, short trades, or both. This makes the strategy adaptable to different market conditions and trading styles.

- Usage

1. Set the input parameters as per your trading preferences. You can choose the price source, the length of the moving average, the multiplier for the ATR, whether to use RSI for signals, the RSI and SMA periods, the bought and sold range levels, and the trading direction.

2. The strategy will then generate buy and sell signals based on these parameters. You can use these signals to enter and exit trades.

- Default settings

1. Source: hlc3

2. Length: 50

3. Multiplier: 2.7183

4. Use RSI for signals: True

5. RSI Period: 10

6. SMA Period: 5

7. Bought Range Level: 55

8. Sold Range Level: 50

9. Trade Direction: Both

- Strategy's default Properties

1. Default Quantity Type: 'strategy.percent_of_equity'

2. commission_value= 0.1, commission_type=strategy.commission.percent, slippage= 1: These parameters set the commission and slippage for the strategy. The commission is set to 0.1% of the trade value, and the slippage (the difference between the expected price of a trade and the price at which the trade is executed) is set to 1.

3. default_qty_type = strategy.percent_of_equity, default_qty_value = 15: These parameters set the default quantity for trades. The default_qty_type is set to strategy.percent_of_equity, which means that the size of each trade will be a percentage of the account equity. The default_qty_value is set to 15, which means that each trade will be 15% of the account equity.

4. initial_capital= 10000: This parameter sets the initial capital for the strategy to $10,000.

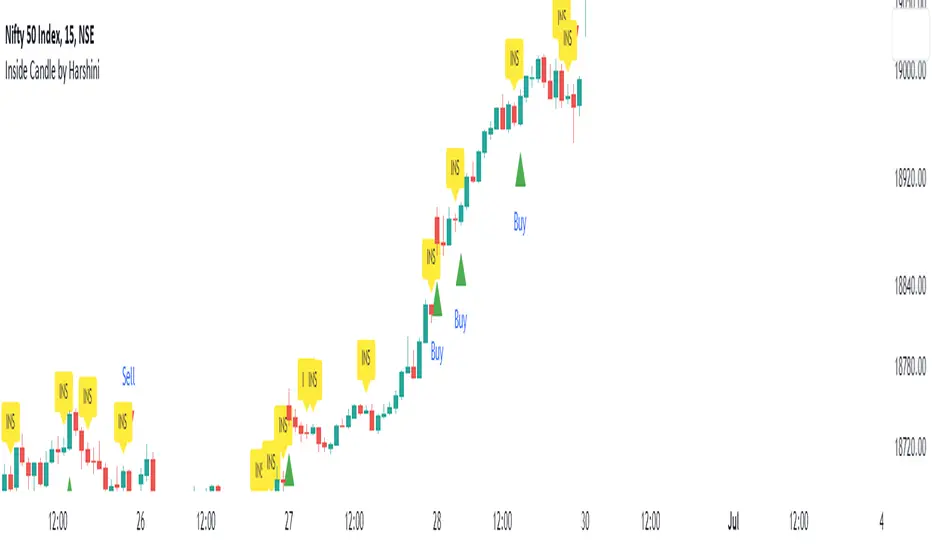

Inside Candle by HarshiniThe concept behind this indicator is that the inside candle indicates a pause in the current move and the following candle after inside candle will indicate the direction of the next move. This indicator informs you when an inside candle is formed and based on the next candle, it gives you buy/sell signal.

When an inside candle is formed, a label will appear above the candle, which makes it very easy to identify the inside candle in live charts. Once the inside candle is formed, the Buy/Sell signal depends on the next candle. If the candle formed after the inside candle gives a breakout above then "Buy" signal is indicated, you can take a trade with 1:2 risk reward. Similarly if the next candle gives a breakout below, then a "Sell" signal is generated and you can take a sell with 1:2 risk reward. This indicator can be applied to any chart like stocks, crypto, commodities etc...

Here's how you can trade using this indicator:

1) Apply this indicator in a 15 mins time frame :

Even though this indicator identifies inside candle formation in almost every time frame, it works very well when applied to a 15 mins chart.

2) Always keep minimum 1:2 Risk Reward :

While taking trades initially, stick on to 1:2 risk reward. If there are other confluences as well along with the inside candle, you can book target accordingly.

Note : It is observed that this indicator works well in a trending market and not in ranging bound market.

RSI Divergence Screener by zdmreThis screener tracks the following for up to 20 assets:

-All selected tickers will be screened in same timeframes (as in the chart).

-Values in table indicate that how many days passed after the last Bullish or Bearish of RSI Divergence.

For example, when BTCUSDT appears Bullish-Days Ago (15) , Bitcoin has switched to a Bullish Divergence signal 15 days ago.

Thanks to @QuantNomad and @MUQWISHI for building the base for this screener.

*Use it at your own risk

Note:

Screener shows the information about the RSI Divergence Scanner by zdmre with default settings.

Based indicator:

RSI Dot Party - All Lengths From 1 To 120The RSI Dot Party indicator displays all RSI lengths from 1 to 120 as different colored dots on the chart.

🔶 Purpose

Show the reversal point of price action to time entries and exits.

🔶 USAGE

When a dot displays it is a indication of the reversal of the price/trend. The larger the dot the more likely it is to reverse.

The Default settings generates dots for extreme cases where the RSI is over = 90 or under = 10 for every RSI length in the range of 1-120.

Example if the RSI of length 1 or 2 or 3 or 4 or ... or 15 or 16 or 17 or ... or 80 or 81 or 82 or ... if any of does RSI crosses a boundary a dot is shown.

A boundary is the over/under the RSI oscillates in.

Customize the settings until the dots match up with the high and lows of past price action.

🔶 SETTINGS

🔹 Source

Source 1: Is the First Source RSI is calculated from

Source 2: Is the Second Source RSI is calculated from

🔹 Meta Settings

Hours back to draw: To speed up the script calculate it only draws a set number of hours back, default is 300 hours back in time to draw then it cuts off.

Show Dots: Show or disable dots

Show Bar Color: Color the bars for each RSI incident

Filter Cross: Filters and only shows dots when the RSI crosses above or bellow a boundary. If not all candles above or bellow the boundaries will display a dot.

Dots Location Absolute: Instead of showing the dots above or bellow the candle, the dots will show up on the top and bottom of the window.

🔹 7 RSI Groups

There are a total of 7 RSI colors.

Range Very Tiny: Default Color Green

Range Tiny: Default Color Purple

Range Small: Default Color Yellow

Range Normal: Default Color Red

Range Large: Default Color Blue

Range Huge: Default Color Dark Purple

Range Very Huge: Default Color White

🔹 RSI Group Settings

Hi/Low Color: Change the Color of that group.

Start/End: The Start and End range of this RSI color. Example if start = 5 and end = 10 the RSI of 5,6,7,8,9,10 will be displayed on the chart for that color, if any of does RSI goes above or bellow the boundary a dot is displayed on that candle.

Delay: The RSI needs to be above or bellow a boundary for x number of candles before displaying a dot. For example if delay = 2 and the RSI is over = 70 for 2 candles then it will display a dot.

Under/Over: Boundaries that indicate when to draw a dot, if over = 70 and RSI crosses above 70 a dot is displayed.

🔹 Show

Section that allows you to disable RSI grounds you dont want to see, this also removes them from the alert signal generated.

Show Low: Show or disable Low RSI dots

Show High: Show or disable High RSI dots

🔶 ALERTS

Alert for all New RSIs Dots Created in real time

The alert generated depends on what groups are showing or not, if the green group is disabled for example the alert will not be generated.

🔶 Warning

When a dot shows up it can continue moving. For example if a purple dot shows itself above a 15 minute candle, if that candle/price continue to extend up the dot will move up with it.

Dots can also disappear occasionally if the RSI moves in and out of a boundary within that candles life span.

🔶 Community

I hope you guys find this useful, if you have any questions or feature requests leave me a comment! Take care :D

Positive Volatility and Volume GaugeThis is my first published script. It is a real volatility gauge that allows the user to see the real volatility of a given candle on the 15-min time frame. It also has the SMA of real volatility and volume available.

It provides the user to identify high volatility points that can lead to reversals back to the mid-point of said high volatility.

You can change the threshold of the signal line. For the 15-min time frame, I suggest that the 1.5-2.5 threshold be used for the best view.

Good luck and let me know if you have any questions or suggestions. I'm always open to learning.

Thank you!

Initial Balance Panel Strategy for BitcoinInitial Balance Strategy

Initial Balance Strategy uses a source code of "Initial Balance Monitoring Panel" that build from "Initial Balance Markets Time Zones - Overall Highest and Lowest".

Initial Balance is based on the highest and lowest price action within the first 60 minutes of trading. Reading online this can depict which way the market can trend for the session. More information about Initial Balance Panel you can read at the end of the article.

Strategy idea

The main idea is to catch the trend move when most of the 16 Crypto pairs break the Low or High levels together. I found good results when 15 of 16 pairs is break that levels and after we manage the trade within some trail stop indicator, I choose Volatility Stop for this strategy.

Additional Strategy idea

The second one idea that was not made is to catch the pullback after fully green/red zones in Initial Balance Panel become white. That mean the main trend can be finished and we can try to catch good pullback in opposite direction.

Binance Crypto pairs

The strategy use the 16 default Crypto currencies pairs from the Binance. As additional variations of the strategy can be changing the currencies pairs and their number.

List of default pairs:

BINANCE:BTCUSDT, BINANCE:ETHUSDT, BINANCE:EOSUSDT, BINANCE:LTCUSDT, BINANCE:XRPUSDT, BINANCE:DASHUSDT, BINANCE:IOTAUSDT, BINANCE:NEOUSDT, BINANCE:QTUMUSDT, BINANCE:XMRUSDT, BINANCE:ZECUSDT, BINANCE:ETCUSDT, BINANCE:ADAUSDT, BINANCE:XTZUSDT, BINANCE:LINKUSDT, BINANCE:DOTUSDT

Summary

The strategy works very well for a buy trades with settings 15 crypto pairs of 16 that follow the trend with breaking the long initial balance level.

Initial Balance Monitoring Panel

Allows you to have an instant view of 16 Crypto pairs within a monitoring panel, monitoring Initial Balance (Asia, London, New York Stock Exchanges).

The code can easily be changed to suit the crypto pairs you are trading.

The setup of my chart would also include this indicator and the "Initial Balance Markets Time Zones - Overall Highest and Lowest" (with all IBs enabled) as shown above.

Initial Balance is based on the highest and lowest price action within the first 60 minutes of trading. Reading online this can depict which way the market can trend for the session.

The indicator has been coded for Crypto (so other symbols may not work as expected).

Though Initial Balance is based off the first 60 minutes of the trading markets opening, but Crypto is 24/7, this indicator looks at how Asia, London and New York Stock Exchanges opening trading can affect Crypto price action.

Source: Initial Balance Monitoring Panel

Buying/Selling Pressure Cycle (PreCy)No lag estimation of the buying/selling pressure for each candle.

----------------------------------------------------------------------------------------------------

WHY PreCY?

How much bearish pressure is there behind a group of bullish candles ?

Is this bearish pressure increasing?

When might it overcome the bullish pressure?

Those were my questions when I started this indicator. It lead me through the rabbit hole, where I discovered some secrets about the market. So I pushed deeper, and developped it a lot more, in order to understand what is really happening "behind the scene".

There are now 3 ways to read this indicator. It might look complicated at first, but the reward is to be able to anticipate and understand a lot more.

You can show/hide all the plots in the settings. So you can choose the way you prefer to use it.

----------------------------------------------------------------------------------------------------

FIRST WAY TO READ PreCy : The SIGNAL line

Go in the settings of PreCy, in "DISPLAY", uncheck "The pivot lines of the SIGNAL" and "The CYCLE areas". Make sure "The SIGNAL line" is checked.

The SIGNAL shows an estimation of the buying/selling pressure of each candle, going from 100 (100% bullish candle) to -100 (100% bearish candle). A doji would be shown close to zero.

Formula: Estimated % of buying pressure - Estimated % of selling pressure

It is a very choppy line in general, but its colors help make sense of it.

When this choppiness alternates between the extremes, then there is not much pressure on each candle, and it's very unpredictable.

When the pressure increases, the SIGNAL's amplitude changes. It "compresses", meaning there is some interest in the market. It can compress by alternating above and below zero, or it can stay above zero (bullish), or below zero (bearish) for a while.

When the SIGNAL becomes linear (in opposition to choppy), there is a lot of pressure, and it is directional. The participants agree for a move in a chosen direction.

The trajectory of the SIGNAL can help anticipate when a move is going to happen (directional increase of pressure), or stop (returning to zero) and possibly reverse (crossing zero).

Advanced uses:

The SIGNAL can make more sense on a specific timeframe, that would be aligned with the frequency of the orders at that moment. So it is a good idea to switch between timeframes until it gets less choppy, and more directional.

It is interesting to follow any regular progression of the SIGNAL, as it can reveal the intentions of the market makers to go in a certain direction discretely. There can be almost no volume and no move in the price action, yet the SIGNAL gets linear and moves away from one extreme, slowly crosses the zeroline, and pushes to the other extreme at the same time as the amplitude of the price action increases drastically.

----------------------------------------------------------------------------------------------------

SECOND WAY TO READ PreCy : The PIVOTS of the SIGNAL line

Go in the settings of PreCy, in "DISPLAY", and uncheck "The CYCLE areas". Make sure "The SIGNAL line" and "The pivot lines of the SIGNAL" are checked.

The PIVOTS help make sense of the apparent chaos of the SIGNAL. They can reveal the overall direction of the choppy moves.

Especially when the 2 PIVOTS lines are parallel and oriented.

----------------------------------------------------------------------------------------------------

THIRD WAY TO READ PreCy : The CYCLE

Go in the settings of PreCy, in "DISPLAY", and uncheck "The SIGNAL line" and "The pivot lines of the SIGNAL". Make sure "The CYCLE areas" is checked.

The CYCLE is a Moving Average of the SIGNAL in relation to each candle's size.

Formula: 6 periods Moving Average of the SIGNAL * (body of the current candle / 200 periods Moving Average of the candle's bodies)

The result goes from 200 to -200.

The CYCLE shows longer term indications of the pressures of the market.

Analysing the trajectory of the CYCLE can help predict the direction of the price.

When the CYCLE goes above or below the gray low intensity zone, it signals some interest in the move.

When the CYCLE stays above 100 or below -100, it is a sign of strength in the move.

When it stayed out of the gray low intensity zone, then returns inside it, it is a strong signal of a probable change of behavior.

----------------------------------------------------------------------------------------------------

ALERTS

In the settings, you can pick the alerts you're interested in.

To activate them, right click on the chart (or alt+a), choose "Add alert on Buying/Selling Pressure Cycle (PreCy)" then "Any alert()", then "Create".

Feel free to activate them on different timeframes. The alerts show which timeframe they are from (ex: "TF:15" for the 15 minutes TF).

I have added a lot more conditions to my PreCy, taken from FREMA Trend, for ex. You can do the same with your favorite scripts, to make PreCy more accurate for your style.

----------------------------------------------------------------------------------------------------

Borrowed scripts:

To estimate the buying and selling pressures, PreCy uses the wicks calculations of "Volume net histogram" by RafaelZioni

To filter the alerts, PreCy uses the calculations of "Amplitude" by Koholintian:

----------------------------------------------------------------------------------------------------

DO NOT BASE YOUR TRADING DECISIONS ON 1 SINGLE INDICATOR'S SIGNALS.

Always confirm your ideas by other means, like price action and indicators of a different nature.

Supply and DemandThis is a "Supply and Demand" script designed to help traders spot potential levels of supply (resistance) and demand (support) in the market by identifying pivot points from past price action.

Differences from Other Scripts:

Unlike many pivot point scripts, this one offers a greater degree of customization and flexibility, allowing users to determine how many ranges of pivot points they wish to plot (up to 10), as well as the number of the most recent ranges to display.

Furthermore, it allows users to restrict the plotting of pivot points to specific timeframes (15 minutes, 30 minutes, 1 hour, 4 hours, and daily) using a toggle input. This is useful for traders who wish to focus on these popular trading timeframes.

This script also uses the color.new function for a more transparent plotting, which is not commonly used in many scripts.

How to Use:

The script provides two user inputs:

"Number of Ranges to Plot (1-10)": This determines how many 10-bar ranges of pivot points the script will calculate and potentially plot.

"Number of Last Ranges to Show (1-?)": This determines how many of the most recent ranges will be displayed on the chart.

"Limit to specific timeframes?": This is a toggle switch. When turned on, the script only plots pivot points if the current timeframe is one of the following: 15 minutes, 30 minutes, 1 hour, 4 hours, or daily.

The pivot points are plotted as circles on the chart, with pivot highs in red and pivot lows in green. The transparency level of these plots can be adjusted in the script.

Market and Conditions:

This script is versatile and can be used in any market, including Forex, commodities, indices, or cryptocurrencies. It's best used in trending markets where supply and demand levels are more likely to be respected. However, like all technical analysis tools, it's not foolproof and should be used in conjunction with other indicators and analysis techniques to confirm signals and manage risk.

A technical analyst, or technician, uses chart patterns and indicators to predict future price movements. The "Supply and Demand" script in question can be an invaluable tool for a technical analyst for the following reasons:

Identifying Support and Resistance Levels : The pivot points plotted by this script can act as potential levels of support and resistance. When the price of an asset approaches these pivot points, it might bounce back (in case of support) or retreat (in case of resistance). These levels can be used to set stop-loss and take-profit points.

Timeframe Analysis : The ability to limit the plotting of pivot points to specific timeframes is useful for multiple timeframe analysis. For instance, a trader might use a longer timeframe to determine the overall trend and a shorter one to decide the optimal entry and exit points.

Customization : The user inputs provided by the script allow a technician to customize the ranges of pivot points according to their unique trading strategy. They can choose the number of ranges to plot and the number of the most recent ranges to display on the chart.

Confirmation of Other Indicators : If a pivot point coincides with a signal from another indicator (for instance, a moving average crossover or a relative strength index (RSI) divergence), it could provide further confirmation of that signal, increasing the chances of a successful trade.

Transparency in Plots : The use of the color.new function allows for more transparent plotting. This feature can prevent the chart from becoming too cluttered when multiple ranges of pivot points are plotted, making it easier for the analyst to interpret the data.

In summary, this script can be used by a technical analyst to pinpoint potential trading opportunities, validate signals from other indicators, and customize the display of pivot points to suit their individual trading style and strategy. Always remember, however, that no single indicator should be used in isolation, and effective risk management strategies should always be employed.

RSI, SRSI, MACD and DMI cross - Open source codeHello,

I'm a passionate trader who has spent years studying technical analysis and exploring different trading strategies. Through my research, I've come to realize that certain indicators are essential tools for conducting accurate market analysis and identifying profitable trading opportunities. In particular, I've found that the RSI, SRSI, MACD cross, and Di cross indicators are crucial for my trading success.

Detailed explanation:

The RSI is a momentum indicator that measures the strength of price movements. It is calculated by comparing the average of gains and losses over a certain period of time. In this indicator, the RSI is calculated based on the close price with a length of 14 periods.

The Stochastic RSI is a combination of the Stochastic Oscillator and the RSI. It is used to identify overbought and oversold conditions of the market. In this indicator, the Stochastic RSI is calculated based on the RSI with a length of 14 periods.

The MACD is a trend-following momentum indicator that shows the relationship between two moving averages of prices. It consists of two lines, the MACD line and the signal line, which are used to generate buy and sell signals. In this indicator, the MACD is calculated based on the close price with fast and slow lengths of 12 and 26 periods, respectively, and a signal length of 9 periods.

The DMI is a trend-following indicator that measures the strength of directional movement in the market. It consists of three lines, the Positive Directional Indicator (+DI), the Negative Directional Indicator (-DI), and the Average Directional Index (ADX), which are used to generate buy and sell signals. In this indicator, the DMI is calculated with a length of 14 periods and an ADX smoothing of 14 periods.

The indicator generates buy signals when certain conditions are met for each of these indicators.

1) For the RSI, a buy signal is generated when the RSI is below or equal to 35 and the Stochastic RSI %K is below or equal to 15, or when the RSI is below or equal to 28 the Stochastic RSI %K is below or equal to 15 or when the RSI is below or equal to 25 and the Stochastic RSI %K is below or equal to 10 or when the RSI is below or equal to 28.

2) For the MACD, a buy signal is generated when the MACD line is below 0, there is a change in the histogram from negative to positive, the MACD line and histogram are negative in the previous period, and the current histogram value is greater than 0.

3) For the DMI, a buy signal is generated when the Positive Directional Indicator (+DI) crosses above the Negative Directional Indicator (-DI), and the -DI is less than the +DI.

The indicator generates sell signals when certain conditions are met for each of these indicators:

1) For the RSI, a sell signal is generated when the RSI is above or equal to 75 and the Stochastic RSI %K is above or equal to 85, or when the RSI is above or equal to 80 and the Stochastic RSI %K is above or equal to 85, or when the RSI is above or equal to 85 and the Stochastic RSI %K is above or equal to 90 or when the RSI is above or equal to 82.

2)For the MACD, a sell signal is generated when the MACD line is above 0, there is a change in the histogram from positive to negative, the MACD line and histogram are positive in the previous period, and the current histogram value is less than the previous histogram value. On the other hand, a buy signal is generated when the MACD line is below 0, there is a change in the histogram from negative to positive, the MACD line and histogram are negative in the previous period, and the current histogram value is greater than the previous histogram value.

3)For the DMI a bearish signal is generated when plusDI crosses above minusDI, indicating that bulls are losing strength and bears are taking control.

The indicator uses a combination of these four indicators to generate potential buy and sell signals. The buy signals are generated when RSI and SRSI values are in oversold conditions, while sell signals are generated when RSI and SRSI values are in overbought conditions. The indicator also uses MACD crossovers and DMI crossovers to generate additional buy and sell signals.

When a signal is strong?

The use of multiple signals within a specific timeframe can increase the accuracy and reliability of the signals generated by this indicator. It is recommended to look for at least two signals within a range of 5-8 candles in order to increase the probability of a successful trade.

Why it's original?

1) There is no indicator in the library that combine all of these indicators and give you a 360 view

2)The combination of the RSI, Stochastic RSI, MACD, and DMI indicators in a single script it's unique and not available in the libray.

3)The specific parameters and conditions used to calculate the signals may be unique and not found in other scripts or libraries.

4)The use of plotshape() to plot the signals as shapes on the chart may be unique compared to other scripts that simply plot lines or bars to indicate signals.

5)The use of alertcondition() to trigger alerts based on the signals may be unique compared to other scripts that do not have custom alert functionality.

Keep attention!

It is important to note that no trading indicator or strategy is foolproof, and there is always a risk of losses in trading. While this indicator may provide useful information for making conclusions, it should not be used as the sole basis for making trading decisions. Traders should always use proper risk management techniques and consider multiple factors when making trading decisions.

Support me:)

If you find this new indicator helpful in your trading analysis, I would greatly appreciate your support! Please consider giving it a like, leaving feedback, or sharing it with your trading network. Your engagement will not only help me improve this tool but will also help other traders discover it and benefit from its features. Thank you for your support!

Kitchen [ilovealgotrading]

OVERVIEW:

Kitchen is a strategy that aims to trade in the direction of the trend by using supertrend and stochRsi data by calculating at different time values.

IMPLEMENTATION DETAILS – SETTINGS:

First of all, let's understand the supertrend and stocrsi indicators.

How do you read and use Super Trend for trading ?

The price is often going upwards when it breaks the super trend line while keeping its position above the indication level.

When the market is in a bullish trend, the indicator becomes green. The indicator level will act as trendline support in such a scenario. The color of the indicator changes to red to indicate a negative trend once the price crosses the support line. The price uses the super trend level as a trendline resistance during a bearish move.

In our strategy, if our 1-hour and 4-hour supertrend lines show the up or down train in the same direction at the same time, we can assume that a train is forming here.

Why do I use the time of 1 hour and 4 hours ?

When I did a backtest from the past to the present, I discovered that the most accurate and consistent time zones are the 1 hour and 4 hour time zones.

By the way we can change our short term timeframe(1H) and long term timeframe(4H) from settings panel.

How do you read and use the Stoch-RSI Indicator?

This indicator analyzes price dynamics automatically to detect overbought and oversold locations.

The indicator includes:

- The primary line, which typically has values between 0 and 100;

- Two dynamic levels for overbought and oversold conditions.

IF our stoch-rsi indicator value has fallen below our lower boundary line, the oversold event has been observed in the price, if our stoch-rsi value breaks up our bottom line after becoming oversold, we think that the price will start the recovery phase.(The case is also true for the opposite.)

However, this does not always apply and we need additional approvals, Therefore, our 1H and 4H supertrrend indicator provides us with additional confirmation.

Buy Condition:

Our 1H(short term) and 4H(long term) supertrrend indicator, has given the buy signal(green line and yellow line), and if our stochrsi indicator has broken our oversold line up on the past 15 bars, the buy signal is formed here.

Sell Condition:

Our 1H(short term) and 4H(long term) supertrrend indicator, has given the sell signal(red line and orange line), and if our stochrsi indicator has broken our overbuy line down on the past 15 bars, the sell signal is formed here.

Stop Loss or Take Profit Conditions:

Exit Long Senerio:

All conditions are completed, the buy signal has arrived and we have entered a LONG trade, the 1-hour supertrend line follows the price rise(yellow line), if the price breaks below the 1-hour super trend line and a sell condition occurs for 1H timeframe for supertrend indcator, LONG trade will exit here.

Exit Short Senerio:

All conditions are completed, the Sell signal has arrived and we have entered a SHORT trade, the 1-hour supertrend line follows the price down(orange line), if the price breaks up the 1-hour super trend line and a buy condition occurs for 1H timeframe for supertrend indcator, SHORT trade will exit here.

What can you change in the settings panel?

1-We can set Start and End date for backtest and future alarms

2-We can set ATR length and Factor for supertrend indicator

3-We can set our short term and long term timeframe value

4-We can set StochRsi Up and Low limit to confirm buy and sell conditions

5-We can set stochrsi retroactive approval length

6-We can set stochrsi values or the length

7-We can set Dollar cost for per position

8- We can choose the direction of our positions, we can set only LONG, only SHORT or both directions.

9-IF you want to place automatic buy and sell orders with this strategy, you can paste your codes into the Long open-close or Short open-close message sections.

For example

IF you write your alert window this code {{strategy.order.alert_message}}.

When trigger Long signal you will get dynamically what you pasted here for Long Open Message

ALSO:

Please do not open trades without properly managing your risk and psychology!!!

If you have any ideas what to add to my work to add more sources or make calculations cooler, suggest in DM .

Pivot Highs&lows: Short/Medium/Long-term + Spikeyness FilterShows Pivot Highs & Lows defined or 'Graded' on a fractal basis: Short-term, medium-term and long-term. Also applies 'Spikeyness' condition by default to filter-out weak/rounded pivots

ES1! 4hr chart (CME) shown above, with lookback = 15; clearly identifying the major highs & lows on the basis of how they are fractally 'nested' within lesser Pivots.

-- in the above chart Short term pivot highs (STH) are simply represented by green 'ʌ', and short-term pivot lows (STL) are simply represented by orange 'v'.

//Basics: (as applying to pivot highs, the following is reversed for pivot lows)

-Short term highs (STH) are simple pivot highs, albeit refined from standard with the 'spikeyness' filter.

-Medium-term highs (MTH) are defined as having a lower STH on either side of them.

-Long-term highs (LTH) are defined as having a lower MTH on either side of them.

//Purpose:

-Education: Quick and easy visualization of the strength or importance of a pivot high or low; a way of grading them based on their larger context.

-Backtesting: use in combination with other trading methods when backtesting to see the relative significance and price sensitivity of LTHs/LTLs compared to lower grade highs and lows.

//Settings:

-Choose Pivot lookback/lookforward bars: One setting, the basis from which all further pivot calculations are done.

-Toggle on/off 'Spikeyness' condition to filter-out weak/rounded/unimpressive pivot highs or lows (default is ON).

-Toggle on/off each of STH, MTH, LTH, STL, MTL, LTL; and choose label text-styles/colors/sizes independently.

-Set text Vertically, horizonally, or simply use 'ʌ' or 'v' symbols if you want to declutter your chart.

//Usage notes:

-Pivots take time to print (lookback bars must have elapsed before confirmation). Fractally nested pivots as here (i.e. a LTH), take even longer to print/confirm, so please be patient.

-Works across timeframes & Assets. Different timeframes may require slightly tweaked lookback/forward settings for optimal use; default is 15 bars.

Example usage with just symbolic labels short-term, med-term, long-term with 1x, 2x and 3x ʌ/v respectively:

Leveraged Share Conversion IndicatorHello everyone,

Releasing my leveraged share conversion indicator.

I noticed that the option traders have all the fun and resources but the share traders don't really have many resources in terms of adjusting or profits on leveraged and inverse shares. So, I decided to change that this this indicator!

What it does:

In a nut shell, the calculator converts one share to the price of another through the use of a regression based analysis.

There are multiple pre-stored libraries available in the indicator, including IWM, SPY, BTC and QQQ.

However, if the ticker you want to convert is not in one of the pre-defined libraries, you can select "Use Alternative Ticker" and indicate the stock you wish to convert.

Using Libraries:

If the conversion you want is available in one of the libraries, simply select the conversion you would like. For example, if you want to convert SPY to SPXU, select that conversion. The indicator will then launch up the conversion results which it will display in a dashboard to the right and will also display the plotted conversion on a chart (see imagine below:

In the dashboard, the indicator will show you:

a) The conversion result: This is the most likely price based on the analysis

b) The standard error: This is the degree of error within the conversion. This is the basis of the upper and lower bands. In statistics, we can add and subtract the standard error from the likely result to get the "Upper" and "Lower" Confidence levels of assessment. This is just a fancy way of saying the range in which our predicted result will fall. So, for example, in the image above it shows you the price of SPXU is assessed to be around 16$ based on SPY's price. The standard error range is 15-17. This means that, the majority of the time, based on this SPY close price, SPXU should fall between 15-17$ with the most likely result being the 16$ range.

Why is there error?

Because leveraged shares have an inherent decay in them. The degree of decay can be captured utilizing the standard error. So at any given time, the small changes in price fluctuations caused by the fact that the share is leveraged can be assessed and displayed using standard error measurements.

c) The current correlation: This is important! Because if the stocks are not strongly correlated, it tells you there is a problem. In general, a perfect correlation is 1 or -1 (perfectly negative correlation or inverse correlation) and a bad correlation is anything under 0.5 or -0.5. So, for an INVERSE leveraged share, you would expect the correlation to read a negative value. Ideally -1. Because the inverse share is doing the opposite of the underlying (if the underlying goes up, the inverse goes down and vice versa). For a non-inverse leveraged share, the correlation should read a positive value. As the underlying goes up, so too does the leveraged.

Manual Conversion using Library:

If you are using a pre-defined library but want to convert a manual close price, simply select "Enable manual conversion" at the bottom of the settings and then type in the manual close price. If you are converting SPY to SPXU, type in the manual close price of SPY to get the result in SPXU and vice versa.

Using an Alternative Ticker:

If the ticker you want is not available in a pre-defined library (i.e. UDOW, BOIL, APPU, TSLL, etc.), simply select "Use Alternative Ticker" in the settings menu. When you select this, make sure your chart is set to the dominant chart. The "Dominant chart" is the chart of the underlying. So, if you want TSLA to TSLL, be sure you have the TSLA chart open and then set your Alternative Ticker to TSLL or TSLQ.

The process of using an Alternative Ticker remains the same. If you wish to enter a manual close price, simply select "Enable Manual Conversion".

Special Considerations:

The indicator uses 1 hour candles. Thus, please leave your dominant chart set on the 1 hour time frame to avoid confusing the indicator.

The lookback period of the manual conversion is 10, 1 hour candles. As such, the results should not be used to make longer term predictions (i.e. anything over 6 months is pushing the capabilities of a manual conversion but fair game for the pre-defined library conversions which use more longer-term data).

You can technically use the indicator to make assessments between 2 separate equities. For example, the relationship between QQQ and ARKK, SPY and DIA, IWM and SPY, etc. If there is a good enough correlation, you can use it to make predictions of the opposing ticker. For example, if DIA goes to 340, what would SPY likely do? And vice versa.

As always, I have prepared a tutorial and getting started video for your reference:

As always, let me know your questions and requests/recommendations for the indicator below. This indicator is my final reference indicator in my 3 part reference indicator release. I will be going back over the feedback to make improvements based on the suggestions I have received. So please feel free to leave any suggestions here and I will take them into consideration for improvement!

Thank you for checking this out and as always, safe trades!

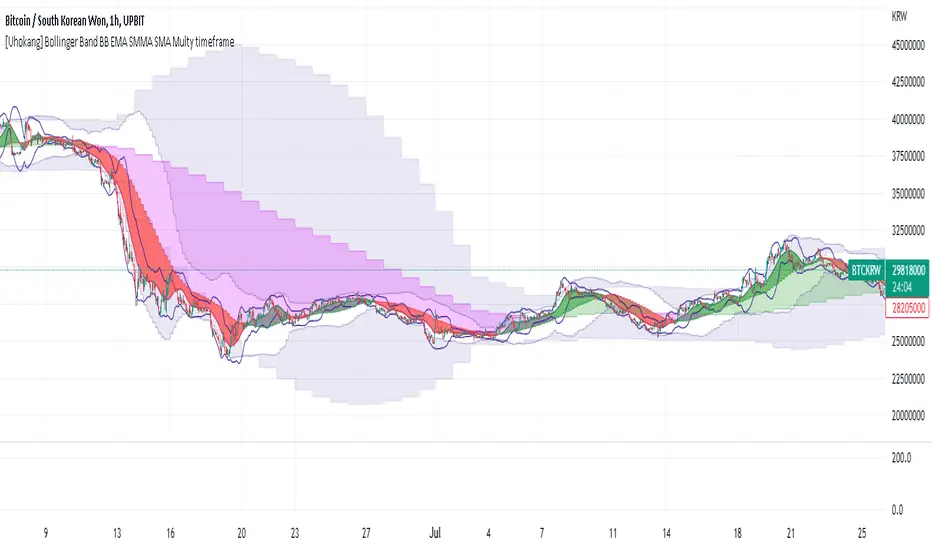

[Uhokang] Bollinger Band BB EMA SMMA SMA Multy timeframeYou can view indicators from the specified upper timeframe together.

( Bollinger Bands, SMMA, EMA, SMA )

If it is based on a 1-hour bar, you can see indicators for 4-hour bars and 1-day bars at the same time.

=> =>

Minutes

1 => 5 => 30

2 => 10 => 60

3 => 15 => 90

4 => 20 => 120

5 => 30 => 120

6 => 30 => 120

10 => 60 => 240

15 => 60 => 240

30 => 120 => 480

45 => 180 => 450

over Hours

1 => 4 => D

2 => 8 => 2D

3 => 12 => 3D

4 => D => W

D => W => M

W => M => Y

RSI Multi Symbol/Time Frame DetectorThis code is an implementation of the Relative Strength Index (RSI) indicator, which is a popular momentum indicator used in technical analysis. The RSI measures the strength of an asset's price action and provides information on whether the asset is overbought or oversold. The code also calculates a moving average of the RSI and allows the user to choose the type of moving average to be calculated (SMA, EMA, SMMA, WMA, or VWMA).

The user can select from different time frames (5, 15, 60, or 240), symbols (SP:SPX, OANDA:EURUSD, or OANDA:NZDUSD), RSI lengths, and moving average types and lengths.

The code starts by defining a function called "ma" for calculating different types of moving averages. This function takes as input the source data for the moving average calculation (the RSI), the length of the moving average, and the type of moving average. The function uses a switch statement to return the appropriate calculation based on the inputted moving average type.

Next, the code calculates the RSI and its moving average. The RSI is calculated using the well-known formula for the RSI, which involves calculating the average gains and losses over a specified period of time and then dividing the average gains by the average losses. The moving average is calculated using the "ma" function defined earlier.

Finally, the code allows the user to choose the symbol and time frame to be used in the RSI calculation, as well as the length of the RSI and the moving average, and the type of moving average. The user can choose from three symbols (SP:SPX, OANDA:EURUSD, OANDA:NZDUSD) and four time frames (5, 15, 60, and 240 minutes). The code then uses the "request.security" function to retrieve the RSI calculation for the selected symbol and time frame.

Note: This code is example for you to use multi timeframe/symbol in your indicator or Strategy , also prevent Repainting Calculation

Strategy Myth-Busting #13 - MultiEMA+BXTrender - [SP/MYN]#13 on the Myth-Busting bench, we are automating the "I Found The Highest Win Rate 15 Minute Scalping Trading Strategy Ever" strategy from "TradeIQ" who claims to have backtested this manually and achieved 410% profit over 100 trades within 6 months on Natural Gas with 79 Wins / 21 Losses with an astounding 3.96% Max Drawdown.

It was quite challenging emulating the same subjective EMA pullback logic along with the dependent sequencing of events necessary to enter a trade and we might improve on this to make it better in the future. Super kudos to @spdoinkal who helped with this strategy. If you have ideas on how this could be improved on, would love to hear about them.

As is, we were unable to substantiate similar results to what was manually backtested by TradeIQ, we do however see potential here. Given some optimizations and improvements to the the entry logic accommodating for a wider more variable margin after pullbacks reestablish above/below the fast EMA we think the performance of this strategy could certainly be improved upon. So not sure if we have totally myth busted this completely at this point in time.

This strategy uses a combination of 2 open-source public indicators:

3 EMA's (Trading View Internal)

B-Xtrender by Puppytherapy

Three separate (21), (89) and (200) EMA's are used as a means to confirm and keep entry out of ranged markets. When the 3 EMA's are all clumped up together with no distance it's indicative of a flat or ranged market. This is then used in conjunction with B-XTrender as a means to detect the trend direction. B-XTrender which is a trend following indicator originally published in the IFTA Journal by Bharat Jhunjhunwala. It uses both a short and long term lengths along with a compound EMA used as a means to smooth and sample trend direction.

Trading Rules

15 min candles but other lower time-frames

Stop Loss on previous swing high/low

No Take Profit, Exit on new red/green circles from BX-Trender

Long

EMA Green (21) on top, White (89)in middle and red (200) on bottom and there is distance between EMA's need to be spaced, otherwise in a ranged market

Price action must pull back into 89 EMA (White line) either close or touching it.

Once pullback occurs wait for BX Trender to issue a new green circle and BX Trend line must be green and above 0

Price action must also pull up back above the (Green Line) EMA 21

Short

EMA Red (200) on top, White (89) in middle and Green (21) on bottom and there is distance between EMA's need to be spaced, otherwise in a ranged market

Price action must pull back into 89 EMA (White line) either close or touching it.

Once pullback occurs wait for BX Trender to issue a new red circle and BX Trend line must be red and below 0

Price action must also pull up back below the (green Line) EMA 21

If you know of or have a strategy you want to see myth-busted or just have an idea for one, please feel free to message me.