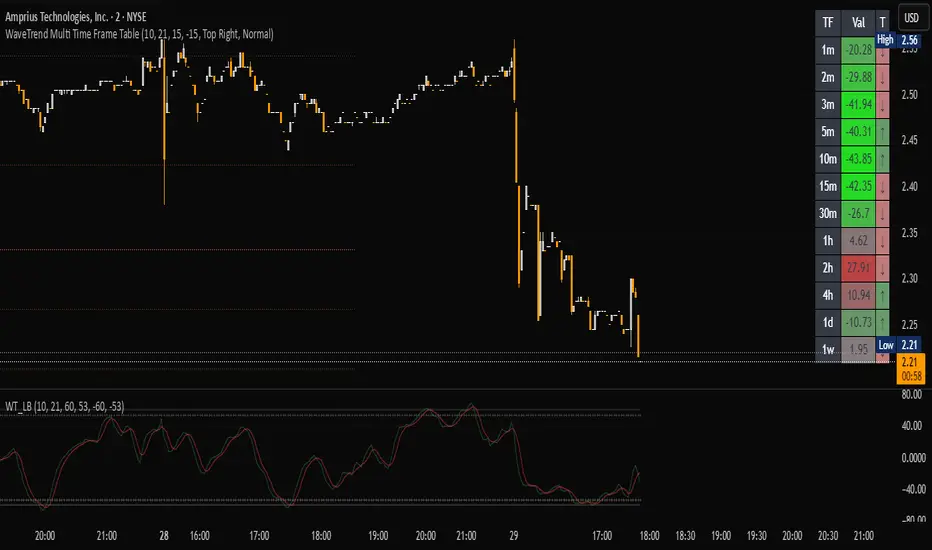

WaveTrend Matrix (1m-1w) – Custom ThresholdsA visual control panel for momentum exhaustion across ten key time-frames.

—

🧬 DNA

This is a fork of LazyBear’s original WaveTrend Oscillator .

The oscillator logic is 100 % intact; I simply stream the values into a compact table so that day- and swing-traders can see the “bigger picture” at a glance.

📈 What does it do?

Calculates WaveTrend on ten granularities: 1m, 3m, 5m, 15m, 30m, 1h, 2h, 4h, 1d, 1w.

Displays the current oscillator print in a color-coded matrix.

• Red = overbought (≥ high threshold)

• Green = oversold (≤ low threshold)

• Gray = neutral / in-range

All thresholds are user-adjustable.

Built on Pine v5, zero repainting, works on any symbol.

🛠 Parameters

Channel Length – WT “n1” (default 10)

Average Length – WT “n2” (default 21)

Red from – overbought cut-off (default +60)

Green under – oversold cut-off (default –60)

🚀 How to use it

1. Apply the indicator to your chart – no extra setup required.

2. Read the matrix top-down before every entry:

• Multiple deep-green rows → market broadly oversold → watch for longs.

• Multiple deep-red rows → market broadly overbought → watch for shorts or stay flat.

3. Combine with your trend filter (EMA-stack, VWAP, structure) to avoid counter-trend trades.

"股价站上60月线" için komut dosyalarını ara

ian_Trado v15 Trend Entry Filter# 📈 ian_Trado v15 Trend Entry Filter (Pine Script v6)

The **ian_Trado v15** is a multi-factor **trend confirmation filter** for NASDAQ (NAS100), Dow Jones (DJ30), Gold (XAU), DAX, and USDJPY.

It combines **EMA structure**, **Donchian channel breakout**, **MACD histogram momentum**, **Volume confirmation**, and a **Range Compression Filter** to avoid entering during choppy or sideways markets.

✅ Designed for **bot deployment** (e.g., grid bots, long/short breakout bots) or **manual trading**.

---

## 🔍 How This Filter Works:

1. **EMA Trend Confirmation**

- Long Trend: EMA(1) > EMA(5) > EMA(60)

- Short Trend: EMA(1) < EMA(5) < EMA(60)

2. **Donchian Channel Width Expansion**

- Only allows trades when the **breakout width** exceeds a minimum threshold.

3. **MACD Histogram Slope Filter (Optional)**

- Confirms momentum building in the direction of the trend.

- Strict Mode: MACD histogram must consistently rise or fall over 3 bars.

4. **Volume Filter (Optional)**

- Ensures volume supports the move (filters out weak conditions).

5. **Range Compression Filter (Optional)**

- Avoids entries during sideways chop.

6. **Cooldown Control**

- Limits overtrading by requiring spacing between entries.

7. **Exit Conditions**

- Gray dot appears when trending conditions are no longer valid.

---

## ⚙️ Settings Explained:

| Setting | Description |

|:--------|:------------|

| **Cooldown Bars** | Minimum bars between consecutive entries |

| **Profit Target (%)** | Visual profit marker for exit tracking |

| **Donchian Channel Length** | Lookback period for detecting breakout width |

| **Minimum Donchian Width** | Threshold to confirm meaningful breakouts |

| **Volume Lookback Period** | Average volume validation window |

| **Box Range (Range Compression)** | Max allowed price range over lookback bars |

| **Range Compression Bars** | Number of bars to check for range compression |

| **Strict MACD Filter** | Use stricter MACD slope checks |

---

## 📊 Recommended Settings by Instrument (1H Chart):

| Asset | Min Donchian Width | Range Compression | Profit Target |

|:------|:-------------------|:------------------|:--------------|

| **NAS100** (Nasdaq) | 300–450 pts | 400 pts / 40 bars | 1.5% |

| **DJ30** (Dow Jones) | 400–600 pts | 500 pts / 40 bars | 1.0–1.5% |

| **XAU/USD** (Gold) | 10–15 pts | 8 pts / 30 bars | 0.8–1.2% |

| **DAX40** (Germany) | 200–300 pts | 250 pts / 40 bars | 1.0% |

| **USD/JPY** (Forex) | 0.5–0.8 pts | 0.4 pts / 40 bars | 0.5–0.8% |

---

## 🔔 Alerts Available:

- Long Entry

- Short Entry

- Exit Zone

> **Note:** Volume filter may be disabled if volume is unreliable (e.g., some forex pairs).

---

## 📅 Version:

- **ian_Trado v15** — April 2025

- Built with **Pine Script v6** for maximum stability

- Clean toggling and plotting logic (no `na` errors)

Hippo Battlefield - Bulls VS Bears 20 bars## Hippo Battlefield – Bulls VS Bears (20 Bars)

**What it is**

A multi-dimensional momentum-and-sentiment oscillator that combines classic Bull/Bear Power with ATR- or peak-normalization, then layers on RSI and MACD-derived metrics into:

1. **A colored bar series** showing net Bull+Bear Power strength over the last 20 bars,

2. **A dynamic table** of each of those 20 BBP values (grouped into four 5-bar “quartals”), with symbols, per-bar change, and rolling averages, and

3. **A composite “Weighted BBP” histogram** blending normalized RSI, MACD, and BBP into a single view.

---

### Key Inputs

- **Length (EMA)** – look-back for the underlying EMA (default 60)

- **Normalization Length** – look-back window for peak-normalization (default 60)

- **Use ATR for Norm.** – toggle ATR-based normalization vs. highest-abs(BBP)

- **Show Tables** – toggle the bottom-right 21×11 grid of raw and average BBP values

---

### What You See

#### 1. Colored Bars (Overlay = false)

- Bars are colored by normalized BBP intensity:

- Extreme Bull (≥+10): deep blue

- Strong Bull (+5 to +10): green/yellow

- Weak Bull (+0 to +5): dark green

- Weak Bear (–0 to –5): dark red

- Strong Bear (–5 to –10): pink/red

- Extreme Bear (<–10): magenta

#### 2. Bottom-Right Table (20 Bars of Data)

- Divided into four columns (0–4, 5–9, 10–14, 15–19 bars ago) and one “average” row.

- Each cell shows:

1. Bar index (1–20),

2. Normalized BBP value (to four decimals),

3. Direction symbol (↑/↓/=),

4. Bar-to-bar change (± value),

5. A separator “|”.

- At the very bottom, each column’s 5-bar average is displayed as “Avg: X.XXXX” with a dot marker.

#### 3. Top-Center Mini-Table

- When ≥20 bars have elapsed, shows the date at 20 bars ago and the average BBP across the full 20-bar window.

#### 4. Normalized RSI Line

- Rescales the classic 14-period RSI into a –20…+20 band to align with BBP.

#### 5. MACD Lines (Hidden) & Composite Histogram

- MACD and signal lines are calculated but not plotted by default.

- A “Weighted BBP” histogram combines:

- 20% normalized RSI,

- 20% average of (MACD + signal + normalized BBP),

- 60% normalized BBP

- Plotted as columns, color-coded by strength using the same palette as the main bars.

#### 6. Middle Reference Line

- A horizontal zero line to anchor over/under-zero readings.

---

### How to Use It

- **Trend confirmation**: Strong blue/green bars alongside a rising histogram suggest bull conviction; strong reds/magentas signal bear dominance.

- **Divergence spotting**: Watch for price making new highs/lows while BBP or the histogram fails to follow.

- **Quartal analysis**: The 5-bar group averages can reveal whether recent momentum is accelerating or waning.

- **Cross-indicator weighting**: Because RSI, MACD, and raw BBP all feed into the final histogram, you get a smoothed, blended view of momentum shifts.

---

**Tip:** Tweak the EMA and normalization length to suit your preferred timeframe (e.g. shorter for intraday scalps, longer for swing trades). Enable/disable the table if you prefer a cleaner pane.

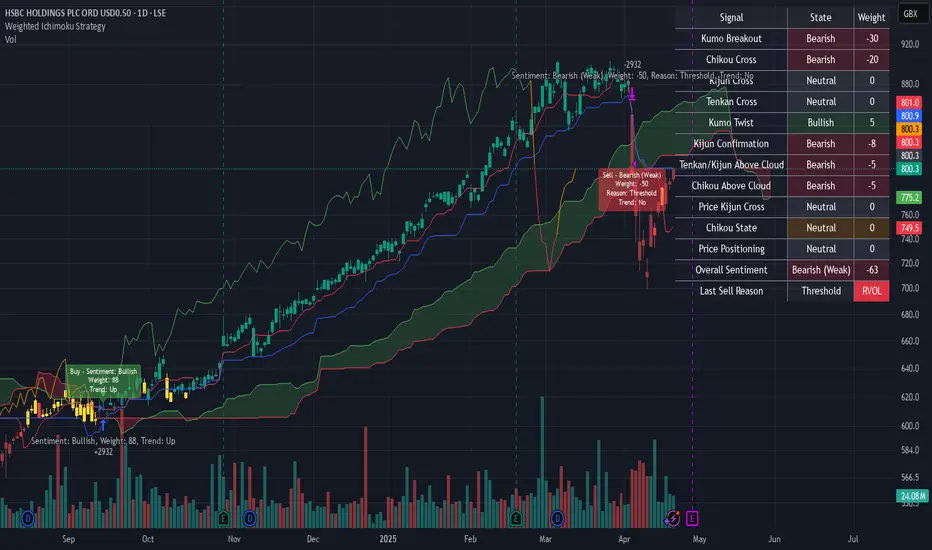

Weighted Ichimoku StrategyLSE:HSBA

The Ichimoku Kinko Hyo indicator is a comprehensive tool that combines multiple signals to identify market trends and potential buying/selling opportunities. My weighted variant of this strategy attempts to assign specific weights to each signal, allowing for a more nuanced and customizable approach to trend identification. The intent is to try and make a more informed trading decision based on the cumulative strength of various signals.

I've tried not to make it a mishmash of this and that + MACD + RSI and on and on; most people have their preferred indicator that focuses on just that that they can use in conjunction.

The signals used can be grouped into two groups the 'Core Ichimoku Signals' & the 'Additional Signals' (at the end you will find the signals and their assigned weights followed by the thresholds where they align).

The Core Ichimoku Signals are the primary signals used in Ichimoku analysis, including Kumo Breakout, Chikou Cross, Kijun Cross, Tenkan Cross, and Kumo Twist.

While the Additional Signals provide further insights and confirmations, such as Kijun Confirmation, Tenkan-Kijun Above Cloud, Chikou Above Cloud, Price-Kijun Cross, Chikou Span Signal, and Price Positioning.

Entries are triggered when the cumulative weight of bullish signals exceeds a specified buy threshold, indicating a strong uptrend or potential trend reversal.

Exits are initiated when the cumulative weight of bearish signals surpasses a specified sell threshold, or when additional conditions such as consolidation patterns or ATR-based targets are met.

There are various exit types that you can choose between, which can be used separately or in conjunction with one another. As an example you might want to exit on a different condition during consolidation periods than during other periods or just use ATR with some other backstop.

They are listed in evaluation order i.e. ATR trumps all, Consolidation exit trumps the regular Kumo sell and so on:

**ATR Sell**: Exits trades based on ATR-based profit targets and stop-losses.

**Consolidation Exit**: Exits trades during consolidation periods to reduce drawdown.

**Sell Below Kumo**: Exits trades when the price is below the Kumo, indicating a potential downtrend.

**Sell Threshold**: Exits trades when the cumulative weight of bearish signals surpasses a specified sell threshold.

There are various 'filters' which are really behavior modifiers:

**Kumo Breakout Filter**: Requires price to close above the Kumo for buy signals (essentially a entry delay).

**Whipsaw Filter**: Ensures trend strength over specified days to reduce false signals.

**Buy Cooldown**: Prevents new entries until half the Kijun period passes after an exit (prevents flapping).

**Chikou Filter**: Delays exits unless the previous close is below the Chikou Span.

**Consolidation Trend Filter**: Prevents consolidation exits if the trend is bullish (rare, but happens).

Then there are some debugging options. Ichimoku periods have some presets (personally I like 8/22/44/22) but are freely configurable, preset to the traditional values for purists.

The list of signals and most thresholds follow, play around with them. Thats all.

Cheers,

**Core Ichimoku Signals**

**Kumo Breakout**

- 30 (Bullish) / -30 (Bearish)

- Indicates a strong trend when the price breaks above (bullish) or below (bearish) the Kumo (cloud). This signal suggests a significant shift in market sentiment.

**Chikou Cross**

- 20 (Bullish) / -20 (Bearish)

- Shows the relationship between the Chikou Span (lagging span) and the current price. A bullish signal occurs when the Chikou Span is above the price, indicating a potential uptrend. Conversely, a bearish signal occurs when the Chikou Span is below the price, suggesting a downtrend.

**Kijun Cross**

- 15 (Bullish) / -15 (Bearish)

- Signals trend changes when the Tenkan-sen (conversion line) crosses above (bullish) or below (bearish) the Kijun-sen (base line). This crossover is often used to identify potential trend reversals.

**Tenkan Cross**

- 10 (Bullish) / -10 (Bearish)

- Indicates short-term trend changes when the price crosses above (bullish) or below (bearish) the Tenkan-sen. This signal helps identify minor trend shifts within the broader trend.

**Kumo Twist**

- 5 (Bullish) / -5 (Bearish)

- Shows changes in the Kumo's direction, indicating potential trend shifts. A bullish Kumo Twist occurs when Senkou Span A crosses above Senkou Span B, and a bearish twist occurs when Senkou Span A crosses below Senkou Span B.

**Additional Signals**

**Kijun Confirmation**

- 8 (Bullish) / -8 (Bearish)

- Confirms the trend based on the price's position relative to the Kijun-sen. A bullish signal occurs when the price is above the Kijun-sen, and a bearish signal occurs when the price is below it.

**Tenkan-Kijun Above Cloud**

- 5 (Bullish) / -5 (Bearish)

- Indicates a strong bullish trend when both the Tenkan-sen and Kijun-sen are above the Kumo. Conversely, a bearish signal occurs when both lines are below the Kumo.

**Chikou Above Cloud**

- 5 (Bullish) / -5 (Bearish)

- Shows the Chikou Span's position relative to the Kumo, indicating trend strength. A bullish signal occurs when the Chikou Span is above the Kumo, and a bearish signal occurs when it is below.

**Price-Kijun Cross**

- 2 (Bullish) / -2 (Bearish)

- Signals short-term trend changes when the price crosses above (bullish) or below (bearish) the Kijun-sen. This signal is similar to the Kijun Cross but focuses on the price's direct interaction with the Kijun-sen.

**Chikou Span Signal**

- 10 (Bullish) / -10 (Bearish)

- Indicates the trend based on the Chikou Span's position relative to past price highs and lows. A bullish signal occurs when the Chikou Span is above the highest high of the past period, and a bearish signal occurs when it is below the lowest low.

**Price Positioning**

- 10 (Bullish) / -10 (Bearish)

- Shows indecision when the price is between the Tenkan-sen and Kijun-sen, indicating a potential consolidation phase. A bullish signal occurs when the price is above both lines, and a bearish signal occurs when the price is below both lines.

**Confidence Level**: Highly Sensitive

- **Buy Threshold**: 50

- **Sell Threshold**: -50

- **Notes / Significance**: ~2–3 signals, very early trend detection. High sensitivity, may capture noise and false signals.

**Confidence Level**: Entry-Level

- **Buy Threshold**: 58

- **Sell Threshold**: -58

- **Notes / Significance**: ~3–4 signals, often Chikou Cross or Kumo Breakout. Very sensitive, risks noise (e.g., false buys in choppy markets).

**Confidence Level**: Entry-Level

- **Buy Threshold**: 60

- **Sell Threshold**: -60

- **Notes / Significance**: ~3–4 signals, Kumo Breakout or Chikou Cross anchors. Entry point for early trends.

**Confidence Level**: Moderate

- **Buy Threshold**: 65

- **Sell Threshold**: -65

- **Notes / Significance**: ~4–5 signals, balances sensitivity and reliability. Suitable for moderate risk tolerance.

**Confidence Level**: Conservative

- **Buy Threshold**: 70

- **Sell Threshold**: -70

- **Notes / Significance**: ~4–5 signals, emphasizes stronger confirmations. Reduces false signals but may miss some opportunities.

**Confidence Level**: Very Conservative

- **Buy Threshold**: 75

- **Sell Threshold**: -75

- **Notes / Significance**: ~5–6 signals, prioritizes high confidence. Minimizes risk but may enter trades late.

**Confidence Level**: High Confidence

- **Buy Threshold**: 80

- **Sell Threshold**: -80

- **Notes / Significance**: ~6–7 signals, very strong confirmations needed. Suitable for cautious traders.

**Confidence Level**: Very High Confidence

- **Buy Threshold**: 85

- **Sell Threshold**: -85

- **Notes / Significance**: ~7–8 signals, extremely high confidence required. Minimizes false signals significantly.

**Confidence Level**: Maximum Confidence

- **Buy Threshold**: 90

- **Sell Threshold**: -90

- **Notes / Significance**: ~8–9 signals, maximum confidence level. Ensures trades are highly reliable but may result in fewer trades.

**Confidence Level**: Ultra Conservative

- **Buy Threshold**: 100

- **Sell Threshold**: -100

- **Notes / Significance**: ~9–10 signals, ultra-high confidence. Trades are extremely reliable but opportunities are rare.

**Confidence Level**: Extreme Confidence

- **Buy Threshold**: 110

- **Sell Threshold**: -110

- **Notes / Significance**: All signals align, extreme confidence. Trades are almost certain but very few opportunities.

RSI VWAP POC [Uncle Sam Trading]Category: Oscillators, Volume, Market Profile

Timeframe: Suitable for all timeframes

Markets: Crypto, Forex, Stocks, Commodities

Overview

The RSI VWAP POC indicator is a powerful and innovative oscillator that combines the Relative Strength Index (RSI), Volume-Weighted Average Price (VWAP), and Point of Control (POC) from market profile analysis. Designed to provide traders with clear, high-probability trading signals, this indicator helps you identify key market levels, spot overbought/oversold conditions, and time your entries and exits with precision. Whether you’re a day trader, swing trader, or scalper, this free tool adds significant value to your trading strategy by offering a unique blend of momentum, volume, and market profile insights.

How It Works

This indicator integrates three core components to deliver actionable insights:

RSI (Relative Strength Index): Measures momentum to identify overbought (above 70) and oversold (below 30) conditions, helping you anticipate potential reversals.

VWAP (Volume-Weighted Average Price): Calculates a volume-weighted price benchmark, which is used to compute a more accurate, volume-sensitive RSI. This ensures the indicator reflects true market dynamics.

POC (Point of Control): Derived from market profile analysis, the POC represents the price level with the highest traded volume in a session, acting as a critical support or resistance level.

The indicator plots a smoothed RSI based on VWAP, overlaid with market profile data on a user-defined higher timeframe (default: 4H). The POC is displayed as a red line, with aqua bars indicating the value area where the majority of trading volume occurred. When the RSI crosses the POC, the indicator generates clear buy and sell signals:

Strong Buy (SBU): RSI crosses above the POC in an oversold zone.

Strong Sell (SBD): RSI crosses below the POC in an overbought zone.

Additional features include:

Background colors to highlight bullish (green) or bearish (red) trends.

Shaded zones for overbought (70/60) and oversold (30/40) levels.

Customizable settings to fit your trading style and timeframe.

How This Indicator Adds Value

The RSI VWAP POC indicator offers several key benefits that enhance your trading performance:

High-Probability Signals: By combining RSI, VWAP, and POC, this indicator identifies trades at key market levels where price is likely to react, increasing your win rate.

Improved Timing: Clear buy and sell signals, such as ‘SBU’ and ‘SBD’, help you enter and exit trades at optimal points, maximizing profitability.

Risk Management: Overbought/oversold zones and trend confirmation via background colors help you avoid false signals, protecting your capital.

Versatility: Suitable for all markets (crypto, forex, stocks) and timeframes, making it a valuable tool for traders of all experience levels.

Time Efficiency: The indicator does the heavy lifting by analyzing momentum, volume, and market profile data, allowing you to focus on executing trades.

Real-World Performance Example: On a 1-hour Bitcoin chart with a 4-hour higher timeframe, this indicator identified a strong sell signal on April 6th at 12:00 ($82,000), leading to a 9% drop to $74,600. A subsequent strong buy signal on April 7th at 04:00 ($76,200) captured a 6% rise to $81,200 – a potential 25% profit with 5x leverage if exited at 5%.

How to Use

Add the Indicator: Search for “RSI VWAP POC ” in TradingView’s indicator library and add it to your chart.

Set Your Timeframe: The indicator works on any timeframe but is optimized for a 1-hour chart with a 4-hour higher timeframe (set in the settings).

Interpret Signals:

Look for ‘SBU’ (strong buy) labels when the RSI crosses above the POC in an oversold zone, indicating a potential buying opportunity.

Look for ‘SBD’ (strong sell) labels when the RSI crosses below the POC in an overbought zone, signaling a potential selling opportunity.

Use the background colors (green for bullish, red for bearish) to confirm the trend.

Combine with Your Strategy: Use the indicator alongside your existing analysis (e.g., support/resistance, candlestick patterns) for best results.

Settings and Customization

The indicator is highly customizable to suit your trading needs:

RSI Length (Default: 14): Adjust the sensitivity of the RSI. Use a shorter length (e.g., 10) for scalping, or a longer length (e.g., 20) for smoother signals.

EMA Smoothing Length (Default: 3): Smooths the RSI line. Increase to 5 or 7 for less choppy signals in volatile markets.

Higher Timeframe (Default: 240 minutes): Set to 240 (4 hours) for a 1-hour chart. Adjust based on your chart’s timeframe (e.g., 60 minutes for a 15-minute chart).

Value Area Percentage (Default: 100%): Defines the size of the value area around the POC. Lower to 70% for a tighter focus on key levels.

Overbought/Oversold Thresholds (Defaults: 70/30): Adjust these levels to match market conditions (e.g., 80/20 for trending markets).

Show POC Line (Default: True): Toggle the red POC line on or off.

Show Buy/Sell Signals: Enable ‘Show Strong Breakup Signals’ and ‘Show Strong Breakdown Signals’ to focus on high-probability trades.

Why Choose This Indicator?

The RSI VWAP POC indicator stands out by offering a unique combination of momentum, volume, and market profile analysis in a single, easy-to-use tool. It’s designed to help traders of all levels make informed decisions, reduce risk, and increase profitability. Whether you’re trading Bitcoin, forex pairs, or stocks, this indicator provides the clarity and precision you need to succeed.

PumpC RSI NTZ BarsPumpC RSI NTZ Bars — Slope-Aware RSI Momentum Overlay

The PumpC RSI NTZ Bars indicator builds on the classic RSI by combining it with slope detection and custom bar highlighting, helping traders quickly identify strong momentum breakouts while avoiding sideways chop — the (NTZ) or No Trade Zone .

What is (NTZ)?

(NTZ) stands for No Trade Zone — the neutral RSI area between bullish and bearish thresholds. In this zone, RSI lacks directional strength, which often reflects indecision or consolidation in price. This indicator helps visually separate the chop from true momentum, so you can trade the breakout, not the noise .

Core Features

Dynamic RSI-Based Bar Coloring with Slope Awareness

Bars change color based on RSI value and its slope:

Bright Green: RSI ≥ Bullish Threshold and sloping upward

Teal Green: RSI ≥ Bullish Threshold but sloping downward

Bright Red: RSI ≤ Bearish Threshold and sloping downward

Orange: RSI ≤ Bearish Threshold but sloping upward

White: RSI is between thresholds (NTZ)

Slope Detection Logic

RSI slope is used to confirm directional bias and filter out weak or fading momentum.

Clean Visual Integration

Choose how signals appear: full bar color, border-only style, background shading, or a mix of all three.

RSI Smoothing Option

Optional smoothing to reduce noise — especially useful on faster timeframes.

Built-In Alerts

RSI crossing above the bullish threshold with an upward slope

RSI crossing below the bearish threshold with a downward slope

User Inputs & Customization Options

RSI Length: Default 14

RSI Source: Default Close

Smooth RSI: On or Off

Smoothing Length: Default 2

Bullish Threshold: Default 60

Bearish Threshold: Default 40

Bar Highlight Style: Full Bar or Border Only

Display Mode: Bar Color, Background, or Both

How to Use It

Step 1 – Adjust Your RSI Settings:

Start by setting the RSI Length (default is 14) and choosing which price source to use — typically close , but you can experiment with hl2 , ohlc4 , etc.

You can also turn on smoothing if you want to reduce noise, especially on fast timeframes like the 1m or 5m chart.

Step 2 – Define Your No Trade Zone (NTZ):

The NTZ is the space between the bullish and bearish thresholds (default 60 and 40).

This is where momentum is weak and price is often ranging or chopping. You don’t want to trade in this zone — you're waiting for RSI to break out of it with conviction.

Step 3 – Choose Your Visual Style:

You can choose to: Highlight the entire candle (Full Bar)

Just highlight the outline (Border Only)

Add a background color behind the chart

Or use a combination of the above This makes the signal easy to see without changing your whole chart look.

Step 4 – Read the Colors for Quick Clarity:

Bright Green / Bright Red = Strong Momentum (with RSI slope confirmation)

Teal / Orange = Momentum is weakening — RSI value is above/below threshold but losing slope strength

White = RSI is in the No Trade Zone (NTZ) — not enough strength to trade

Use this color feedback to stay out during weak periods and act when the trend gains strength.

Step 5 – Use Alerts for Clean Signals:

Set alerts when RSI breaks out of the NTZ with slope confirmation .

These are high-quality signals you can use to trigger your setups or review potential entries.

Disclaimer

This indicator is for educational and informational purposes only and should not be considered financial advice. Always combine tools like this with proper market context and risk management.

Multi-Symbol EMA Status Table🔍 Multi-Symbol EMA Trend Scanner Table

This script displays a clean, customizable table showing whether the price of up to 16 different assets is above or below a user-defined EMA, on a per-symbol and per-timeframe basis.

✅ Supports up to 16 symbols, each with:

Custom exchange + ticker (e.g., BINANCE:BTCUSDT.P, PEPPERSTONE:EURUSD)

Custom timeframe (e.g., 15, 60, 240, D, W)

Custom EMA length (e.g., 50, 100, 200)

🧩 Fully customizable visuals:

Table position (top, middle, bottom + left, center, right)

Text size and text color

Background color for "above" and "below" EMA

Optional ✅❌ emojis

📊 The table updates live on your main chart — no switching required!

💡 Great for:

Monitoring trend direction across multiple markets

Spotting trend alignment (e.g., price above 200 EMA on 4H + 1D)

Multi-asset swing trading or scalping strategies

📘 How to Use:

Open a chart and add the indicator from your scripts.

In the settings panel:

Enter any symbol (with exchange prefix, like BINANCE:BTCUSDT.P or OANDA:EURUSD)

Set a timeframe (e.g., "15" for 15min, "60" for 1h, "D" for daily)

Choose your EMA length (e.g., 200)

Repeat for as many symbols as you need (up to 16).

Customize table visuals:

Position on the screen

Font size and color

Enable/disable emojis ✅❌

Watch the table update live!

🧠 Optional Tips:

Use different colors or groupings to track asset classes (crypto, forex, stocks).

Combine it with your favorite entry/exit signals for confirmation.

Try setting all symbols to the same EMA (e.g., 200) but with different timeframes to monitor multi-timeframe alignment.

RSI + ADX + ATR Combo Indicator: RSI + ADX + ATR Combo Filter

This indicator is a confluence filter tool that combines RSI, ADX, and ATR into a single, easy-to-read chart overlay. It is designed to help traders identify low-volatility, non-trending zones with balanced momentum—ideal for strategies that rely on breakouts or reversals.

🔍 Core Components:

RSI (Relative Strength Index)

Standard RSI with custom upper and lower bounds (default: 60 and 40).

Filters out extreme overbought/oversold regions and focuses on price consolidation zones.

ADX (Average Directional Index)

Measures trend strength.

When ADX is below a custom threshold (default: 20), it indicates a weak or range-bound trend.

ATR (Average True Range)

Represents volatility.

Low ATR values (default threshold: 2.5) are used to filter out high-volatility environments, helping refine entries.

🟣 Signal Logic:

A signal is highlighted with a background color when all three conditions are met:

RSI is between lower and upper bounds (e.g., 40 < RSI < 60) ✅

ADX is below the trend threshold (e.g., ADX < 20) ✅

ATR is below the volatility threshold (e.g., ATR < 2.5) ✅

These combined conditions suggest a low-volatility, low-trend strength, and balanced momentum zone—perfect for anticipating breakouts or strong directional moves.

Strategy Stats [presentTrading]Hello! it's another weekend. This tool is a strategy performance analysis tool. Looking at the TradingView community, it seems few creators focus on this aspect. I've intentionally created a shared version. Welcome to share your idea or question on this.

█ Introduction and How it is Different

Strategy Stats is a comprehensive performance analytics framework designed specifically for trading strategies. Unlike standard strategy backtesting tools that simply show cumulative profits, this analytics suite provides real-time, multi-timeframe statistical analysis of your trading performance.

Multi-timeframe analysis: Automatically tracks performance metrics across the most recent time periods (last 7 days, 30 days, 90 days, 1 year, and 4 years)

Advanced statistical measures: Goes beyond basic metrics to include Information Coefficient (IC) and Sortino Ratio

Real-time feedback: Updates performance statistics with each new trade

Visual analytics: Color-coded performance table provides instant visual feedback on strategy health

Integrated risk management: Implements sophisticated take profit mechanisms with 3-step ATR and percentage-based exits

BTCUSD Performance

The table in the upper right corner is a comprehensive performance dashboard showing trading strategy statistics.

Note: While this presentation uses Vegas SuperTrend as the underlying strategy, this is merely an example. The Stats framework can be applied to any trading strategy. The Vegas SuperTrend implementation is included solely to demonstrate how the analytics module integrates with a trading strategy.

⚠️ Timeframe Limitations

Important: TradingView's backtesting engine has a maximum storage limit of 10,000 bars. When using this strategy stats framework on smaller timeframes such as 1-hour or 2-hour charts, you may encounter errors if your backtesting period is too long.

Recommended Timeframe Usage:

Ideal for: 4H, 6H, 8H, Daily charts and above

May cause errors on: 1H, 2H charts spanning multiple years

Not recommended for: Timeframes below 1H with long history

█ Strategy, How it Works: Detailed Explanation

The Strategy Stats framework consists of three primary components: statistical data collection, performance analysis, and visualization.

🔶 Statistical Data Collection

The system maintains several critical data arrays:

equityHistory: Tracks equity curve over time

tradeHistory: Records profit/loss of each trade

predictionSignals: Stores trade direction signals (1 for long, -1 for short)

actualReturns: Records corresponding actual returns from each trade

For each closed trade, the system captures:

float tradePnL = strategy.closedtrades.profit(tradeIndex)

float tradeReturn = strategy.closedtrades.profit_percent(tradeIndex)

int tradeType = entryPrice < exitPrice ? 1 : -1 // Direction

🔶 Performance Metrics Calculation

The framework calculates several key performance metrics:

Information Coefficient (IC):

The correlation between prediction signals and actual returns, measuring forecast skill.

IC = Correlation(predictionSignals, actualReturns)

Where Correlation is the Pearson correlation coefficient:

Correlation(X,Y) = (nΣXY - ΣXY) / √

Sortino Ratio:

Measures risk-adjusted return focusing only on downside risk:

Sortino = (Avg_Return - Risk_Free_Rate) / Downside_Deviation

Where Downside Deviation is:

Downside_Deviation = √

R_i represents individual returns, T is the target return (typically the risk-free rate), and n is the number of observations.

Maximum Drawdown:

Tracks the largest percentage drop from peak to trough:

DD = (Peak_Equity - Trough_Equity) / Peak_Equity * 100

🔶 Time Period Calculation

The system automatically determines the appropriate number of bars to analyze for each timeframe based on the current chart timeframe:

bars_7d = math.max(1, math.round(7 * barsPerDay))

bars_30d = math.max(1, math.round(30 * barsPerDay))

bars_90d = math.max(1, math.round(90 * barsPerDay))

bars_365d = math.max(1, math.round(365 * barsPerDay))

bars_4y = math.max(1, math.round(365 * 4 * barsPerDay))

Where barsPerDay is calculated based on the chart timeframe:

barsPerDay = timeframe.isintraday ?

24 * 60 / math.max(1, (timeframe.in_seconds() / 60)) :

timeframe.isdaily ? 1 :

timeframe.isweekly ? 1/7 :

timeframe.ismonthly ? 1/30 : 0.01

🔶 Visual Representation

The system presents performance data in a color-coded table with intuitive visual indicators:

Green: Excellent performance

Lime: Good performance

Gray: Neutral performance

Orange: Mediocre performance

Red: Poor performance

█ Trade Direction

The Strategy Stats framework supports three trading directions:

Long Only: Only takes long positions when entry conditions are met

Short Only: Only takes short positions when entry conditions are met

Both: Takes both long and short positions depending on market conditions

█ Usage

To effectively use the Strategy Stats framework:

Apply to existing strategies: Add the performance tracking code to any strategy to gain advanced analytics

Monitor multiple timeframes: Use the multi-timeframe analysis to identify performance trends

Evaluate strategy health: Review IC and Sortino ratios to assess predictive power and risk-adjusted returns

Optimize parameters: Use performance data to refine strategy parameters

Compare strategies: Apply the framework to multiple strategies to identify the most effective approach

For best results, allow the strategy to generate sufficient trade history for meaningful statistical analysis (at least 20-30 trades).

█ Default Settings

The default settings have been carefully calibrated for cryptocurrency markets:

Performance Tracking:

Time periods: 7D, 30D, 90D, 1Y, 4Y

Statistical measures: Return, Win%, MaxDD, IC, Sortino Ratio

IC color thresholds: >0.3 (green), >0.1 (lime), <-0.1 (orange), <-0.3 (red)

Sortino color thresholds: >1.0 (green), >0.5 (lime), <0 (red)

Multi-Step Take Profit:

ATR multipliers: 2.618, 5.0, 10.0

Percentage levels: 3%, 8%, 17%

Short multiplier: 1.5x (makes short take profits more aggressive)

Stop loss: 20%

[blackcat] L3 Composite Trading System with ControlOVERVIEW

This indicator combines three distinct trading strategies into a unified decision-making framework. Utilizing KDJ oscillators, MACD divergence analysis, and adaptive signal filtering techniques, it provides actionable buy/sell signals validated against multi-period momentum trends and structural support/resistance levels.

FEATURES

Integrated KDJ oscillator with weighted moving average smoothing

Dynamic MACD difference visualization normalized against price volatility

Multi-layered confirmation process: • Momentum convergence/divergence tracking

• Candle pattern recognition (Yellow/Fuchsia flags)

• SMAs cross-validation (20/60-day thresholds)

Adaptive risk controls via tunable α parameter adjustment

HOW TO USE

Set Alpha Period parameter matching market cycle characteristics

Monitor primary trend direction via candle coloring (green/red zones)

Confirm directional bias using: ▪️ KDJ-J line position relative to zero axis ▪️ MACD histogram slope persistence (>3 bar validation)

Execute trades only when: • Buy/Sell labels align across both oscillator panels • Coincide with candle flag transitions (e.g., red→yellow) • Validate against concurrent SMA breakout conditions

LIMITATIONS

Lag inherent in EMA-based components during rapid reversals

Requires minimum 60-bar history for full functionality

Sensitive to fractal scaling due to normalization methods

Does not account for liquidity/volume dynamics

NOTES

• Yellow/Fuchsia flags reflect relative strength changes vs prior session

• SMA crossover validations have 16-bar lookback memory retention

Fuzzy SMA with DCTI Confirmation[FibonacciFlux]FibonacciFlux: Advanced Fuzzy Logic System with Donchian Trend Confirmation

Institutional-grade trend analysis combining adaptive Fuzzy Logic with Donchian Channel Trend Intensity for superior signal quality

Conceptual Framework & Research Foundation

FibonacciFlux represents a significant advancement in quantitative technical analysis, merging two powerful analytical methodologies: normalized fuzzy logic systems and Donchian Channel Trend Intensity (DCTI). This sophisticated indicator addresses a fundamental challenge in market analysis – the inherent imprecision of trend identification in dynamic, multi-dimensional market environments.

While traditional indicators often produce simplistic binary signals, markets exist in states of continuous, graduated transition. FibonacciFlux embraces this complexity through its implementation of fuzzy set theory, enhanced by DCTI's structural trend confirmation capabilities. The result is an indicator that provides nuanced, probabilistic trend assessment with institutional-grade signal quality.

Core Technological Components

1. Advanced Fuzzy Logic System with Percentile Normalization

At the foundation of FibonacciFlux lies a comprehensive fuzzy logic system that transforms conventional technical metrics into degrees of membership in linguistic variables:

// Fuzzy triangular membership function with robust error handling

fuzzy_triangle(val, left, center, right) =>

if na(val)

0.0

float denominator1 = math.max(1e-10, center - left)

float denominator2 = math.max(1e-10, right - center)

math.max(0.0, math.min(left == center ? val <= center ? 1.0 : 0.0 : (val - left) / denominator1,

center == right ? val >= center ? 1.0 : 0.0 : (right - val) / denominator2))

The system employs percentile-based normalization for SMA deviation – a critical innovation that enables self-calibration across different assets and market regimes:

// Percentile-based normalization for adaptive calibration

raw_diff = price_src - sma_val

diff_abs_percentile = ta.percentile_linear_interpolation(math.abs(raw_diff), normLookback, percRank) + 1e-10

normalized_diff_raw = raw_diff / diff_abs_percentile

normalized_diff = useClamping ? math.max(-clampValue, math.min(clampValue, normalized_diff_raw)) : normalized_diff_raw

This normalization approach represents a significant advancement over fixed-threshold systems, allowing the indicator to automatically adapt to varying volatility environments and maintain consistent signal quality across diverse market conditions.

2. Donchian Channel Trend Intensity (DCTI) Integration

FibonacciFlux significantly enhances fuzzy logic analysis through the integration of Donchian Channel Trend Intensity (DCTI) – a sophisticated measure of trend strength based on the relationship between short-term and long-term price extremes:

// DCTI calculation for structural trend confirmation

f_dcti(src, majorPer, minorPer, sigPer) =>

H = ta.highest(high, majorPer) // Major period high

L = ta.lowest(low, majorPer) // Major period low

h = ta.highest(high, minorPer) // Minor period high

l = ta.lowest(low, minorPer) // Minor period low

float pdiv = not na(L) ? l - L : 0 // Positive divergence (low vs major low)

float ndiv = not na(H) ? H - h : 0 // Negative divergence (major high vs high)

float divisor = pdiv + ndiv

dctiValue = divisor == 0 ? 0 : 100 * ((pdiv - ndiv) / divisor) // Normalized to -100 to +100 range

sigValue = ta.ema(dctiValue, sigPer)

DCTI provides a complementary structural perspective on market trends by quantifying the relationship between short-term and long-term price extremes. This creates a multi-dimensional analysis framework that combines adaptive deviation measurement (fuzzy SMA) with channel-based trend intensity confirmation (DCTI).

Multi-Dimensional Fuzzy Input Variables

FibonacciFlux processes four distinct technical dimensions through its fuzzy system:

Normalized SMA Deviation: Measures price displacement relative to historical volatility context

Rate of Change (ROC): Captures price momentum over configurable timeframes

Relative Strength Index (RSI): Evaluates cyclical overbought/oversold conditions

Donchian Channel Trend Intensity (DCTI): Provides structural trend confirmation through channel analysis

Each dimension is processed through comprehensive fuzzy sets that transform crisp numerical values into linguistic variables:

// Normalized SMA Deviation - Self-calibrating to volatility regimes

ndiff_LP := fuzzy_triangle(normalized_diff, norm_scale * 0.3, norm_scale * 0.7, norm_scale * 1.1)

ndiff_SP := fuzzy_triangle(normalized_diff, norm_scale * 0.05, norm_scale * 0.25, norm_scale * 0.5)

ndiff_NZ := fuzzy_triangle(normalized_diff, -norm_scale * 0.1, 0.0, norm_scale * 0.1)

ndiff_SN := fuzzy_triangle(normalized_diff, -norm_scale * 0.5, -norm_scale * 0.25, -norm_scale * 0.05)

ndiff_LN := fuzzy_triangle(normalized_diff, -norm_scale * 1.1, -norm_scale * 0.7, -norm_scale * 0.3)

// DCTI - Structural trend measurement

dcti_SP := fuzzy_triangle(dcti_val, 60.0, 85.0, 101.0) // Strong Positive Trend (> ~85)

dcti_WP := fuzzy_triangle(dcti_val, 20.0, 45.0, 70.0) // Weak Positive Trend (~30-60)

dcti_Z := fuzzy_triangle(dcti_val, -30.0, 0.0, 30.0) // Near Zero / Trendless (~+/- 20)

dcti_WN := fuzzy_triangle(dcti_val, -70.0, -45.0, -20.0) // Weak Negative Trend (~-30 - -60)

dcti_SN := fuzzy_triangle(dcti_val, -101.0, -85.0, -60.0) // Strong Negative Trend (< ~-85)

Advanced Fuzzy Rule System with DCTI Confirmation

The core intelligence of FibonacciFlux lies in its sophisticated fuzzy rule system – a structured knowledge representation that encodes expert understanding of market dynamics:

// Base Trend Rules with DCTI Confirmation

cond1 = math.min(ndiff_LP, roc_HP, rsi_M)

strength_SB := math.max(strength_SB, cond1 * (dcti_SP > 0.5 ? 1.2 : dcti_Z > 0.1 ? 0.5 : 1.0))

// DCTI Override Rules - Structural trend confirmation with momentum alignment

cond14 = math.min(ndiff_NZ, roc_HP, dcti_SP)

strength_SB := math.max(strength_SB, cond14 * 0.5)

The rule system implements 15 distinct fuzzy rules that evaluate various market conditions including:

Established Trends: Strong deviations with confirming momentum and DCTI alignment

Emerging Trends: Early deviation patterns with initial momentum and DCTI confirmation

Weakening Trends: Divergent signals between deviation, momentum, and DCTI

Reversal Conditions: Counter-trend signals with DCTI confirmation

Neutral Consolidations: Minimal deviation with low momentum and neutral DCTI

A key innovation is the weighted influence of DCTI on rule activation. When strong DCTI readings align with other indicators, rule strength is amplified (up to 1.2x). Conversely, when DCTI contradicts other indicators, rule impact is reduced (as low as 0.5x). This creates a dynamic, self-adjusting system that prioritizes high-conviction signals.

Defuzzification & Signal Generation

The final step transforms fuzzy outputs into a precise trend score through center-of-gravity defuzzification:

// Defuzzification with precise floating-point handling

denominator = strength_SB + strength_WB + strength_N + strength_WBe + strength_SBe

if denominator > 1e-10

fuzzyTrendScore := (strength_SB * STRONG_BULL + strength_WB * WEAK_BULL +

strength_N * NEUTRAL + strength_WBe * WEAK_BEAR +

strength_SBe * STRONG_BEAR) / denominator

The resulting FuzzyTrendScore ranges from -1.0 (Strong Bear) to +1.0 (Strong Bull), with critical threshold zones at ±0.3 (Weak trend) and ±0.7 (Strong trend). The histogram visualization employs intuitive color-coding for immediate trend assessment.

Strategic Applications for Institutional Trading

FibonacciFlux provides substantial advantages for sophisticated trading operations:

Multi-Timeframe Signal Confirmation: Institutional-grade signal validation across multiple technical dimensions

Trend Strength Quantification: Precise measurement of trend conviction with noise filtration

Early Trend Identification: Detection of emerging trends before traditional indicators through fuzzy pattern recognition

Adaptive Market Regime Analysis: Self-calibrating analysis across varying volatility environments

Algorithmic Strategy Integration: Well-defined numerical output suitable for systematic trading frameworks

Risk Management Enhancement: Superior signal fidelity for risk exposure optimization

Customization Parameters

FibonacciFlux offers extensive customization to align with specific trading mandates and market conditions:

Fuzzy SMA Settings: Configure baseline trend identification parameters including SMA, ROC, and RSI lengths

Normalization Settings: Fine-tune the self-calibration mechanism with adjustable lookback period, percentile rank, and optional clamping

DCTI Parameters: Optimize trend structure confirmation with adjustable major/minor periods and signal smoothing

Visualization Controls: Customize display transparency for optimal chart integration

These parameters enable precise calibration for different asset classes, timeframes, and market regimes while maintaining the core analytical framework.

Implementation Notes

For optimal implementation, consider the following guidance:

Higher timeframes (4H+) benefit from increased normalization lookback (800+) for stability

Volatile assets may require adjusted clamping values (2.5-4.0) for optimal signal sensitivity

DCTI parameters should be aligned with chart timeframe (higher timeframes require increased major/minor periods)

The indicator performs exceptionally well as a trend filter for systematic trading strategies

Acknowledgments

FibonacciFlux builds upon the pioneering work of Donovan Wall in Donchian Channel Trend Intensity analysis. The normalization approach draws inspiration from percentile-based statistical techniques in quantitative finance. This indicator is shared for educational and analytical purposes under Attribution-NonCommercial-ShareAlike 4.0 International (CC BY-NC-SA 4.0) license.

Past performance does not guarantee future results. All trading involves risk. This indicator should be used as one component of a comprehensive analysis framework.

Shout out @DonovanWall

Normalized VolumeOVERVIEW

The Normalized Volume (NV) is an attempt at visualizing volume in a format that is more understandable by placing the values on a scale of 0 to 100. 0 in this case is the lowest volume candle available on the chart, and 100 being the highest. Calling a candle “high volume” can be misleading without having something to compare to. For example, in scaling the volume this way we can clearly see that a given candle had 80% of the peak volume or 20%, and gauge the validity of price moves more accurately.

FEATURES

NV by session

Allows user to filter the volume values across 4 different sessions. This can add context to the volume output, because what it high volume during London session may not be high volume relative to New York session.

Overlay plotting

When volume boxes are turned on, this will allow you to toggle how they are plotted.

Color theme

A standard color theme will color the NV based on if the respective candle closed green or red. Selecting variables will color the NV plot based on which range the value falls within.

Session inputs

Activated with the “By session?” Input. Allows user to break the day up into 4 sessions to more accurately gauge volume relative to time of day.

Show Box (X)

Toggles on chart boxes on and off.

Show historical boxes

Will plot prior occurrences of selected volume boxes, deleting them when price fully moves through them in the opposite direction of the initial candle.

Color inputs

Allows for intensive customization in how this tool appears visually.

INTERPRETATION

There are 6 pre-defined ranges that NV can fall within.

NV <= 10

Volume is insignificant

In this range, volume should not be a confirmation in your trading strategy.

NV > 10 and <= 20

Volume is low

In this range, volume should not be a confirmation in your trading strategy.

NV > 20 and <= 40

Volume is fair

In this range, volume should not be the primary confirmation in your trading strategy.

NV > 40 and <= 60

Volume is high

In this range, volume can be the primary confirmation in your trading strategy.

NV > 60 and <= 80

Volume is very high

In this range, volume can be the primary confirmation in your trading strategy.

NV > 80

Volume is extreme

In this range, volume is likely news driven and caution should be taken. High price volatility possible.

To utilize this tool in conjunction with your current strategy, follow the range explanations above section in this section. The higher the NV value, the stronger you can feel about your directional confirmation.

If NV = 100, this means that the highest volume candle occurred up to that point on your selected timeframe. All future data points will be weighed off of this value.

LIMITATIONS

This tool will not load on tickers that do not have volume data, such as VIX.

STRATEGY

The Normalized Volume plot can be used in exactly the same way as you would normally utilize volume in your trading strategy. All we are doing is weighing the volume relative to itself.

Volume boxes can be used as targets to be filled in a similar way to commonly used “fair value gap” strategies. To utilize this strategy, I recommend selecting “Plot to Wicks” in Overlay Plotting and toggling on Show Historical Boxes.

Volume boxes can be used as areas for entry in a similar way to commonly used “order block” strategies. To utilize this strategy, I recommend selecting “Open To Close” in Overlay Plotting.

NOTES

You are able to plot an info label on right side of NV plot using the "Toggle box label" input. When a box is toggled on this label will tell you when the most recent box of that intensity occurred.

This tool is deeply visually customizable, with the ability to adjust line width for plotted boxes, all colors on both box overlays, and all colors on NV panel. Customize it to your liking!

I have a handful of additional features that I plan on adding to this tool in future updates. If there is anything you would like to see added, any bugs you identify, or any strategies you encounter with this tool, I would love to hear from you!

Huge shoutout to @joebaus for assisting in bringing this tool to life, please check out his work here on TradingView!

Enhanced HHLL Time Confirmation with EMAStrong recommendation , remove the green and red circle , or leave it how it is ;)

To be used on 1 minute chart MSTR , Stock

other time frames are good , ;)

How to Use

HHLL Signals: Look for green triangles (buy) below bars or red triangles (sell) above bars to identify confirmed HH/LL setups with trend alignment.

EMA Signals: Watch for lime circles (buy) below bars or maroon circles (sell) above bars when price crosses the EMA 400 in a trending market.

Trend Context: Use the EMA 400 as a dynamic support/resistance level and the SMA trend filter to gauge market direction.

Enable alerts to get notified of signals in real-time.

Best Practices

Adjust the Lookback Period and Confirmation Minutes to suit your timeframe (e.g., shorter for scalping, longer for swing trading).

Combine with other indicators (e.g., volume, RSI) for additional confirmation.

Test on your preferred market and timeframe to optimize settings.

Indicator Description: Enhanced HHLL Time Confirmation with EMA

Overview

The "Enhanced HHLL Time Confirmation with EMA" is a versatile trading indicator designed to identify key reversal and continuation signals based on Higher Highs (HH), Lower Lows (LL), and a 400-period Exponential Moving Average (EMA). It incorporates time-based confirmation and trend filters to reduce noise and improve signal reliability. This indicator is ideal for traders looking to spot trend shifts or confirm momentum with a combination of price structure and moving average crossovers.

Key Features

Higher High / Lower Low Detection:

Identifies HH and LL based on a customizable lookback period (default: 30 bars).

Signals are confirmed only after a user-defined time period (in minutes, default: 60) has passed since the last HH or LL, ensuring stability.

Trend Filter:

Uses a fast (10-period) and slow (30-period) Simple Moving Average (SMA) crossover to confirm bullish or bearish trends.

Buy signals require a bullish trend (Fast SMA > Slow SMA), and sell signals require a bearish trend (Fast SMA < Slow SMA).

EMA 400 Integration:

Plots a 400-period EMA (customizable) as a long-term trend reference.

Generates additional buy/sell signals when price crosses above (buy) or below (sell) the EMA 400, filtered by trend direction.

Visualizations:

Optional dashed lines for HH and LL levels (toggleable).

Debug markers (diamonds) to visualize HH/LL detection points.

Distinct signal shapes: triangles for HHLL signals (green/red) and circles for EMA signals (lime/maroon).

Alerts:

Built-in alert conditions for HHLL Buy/Sell and EMA Buy/Sell signals, making it easy to stay informed of key events.

Input Parameters

Lookback Period (default: 30): Number of bars to look back for HH/LL detection.

Confirmation Minutes (default: 60): Time (in minutes) required to confirm HH/LL signals.

High/Low Source: Select the price source for HH (default: high) and LL (default: low).

Show HH/LL Lines (default: true): Toggle visibility of HH/LL dashed lines.

Show Debug Markers (default: true): Toggle HH/LL detection markers.

EMA Period (default: 400): Adjust the EMA length.

Custom Timeframe Bias IndicatorMy "Custom Timeframe Bias Indicator" is a very practical and powerful TradingView indicator. It can be called a "God-like indicator" because it combines flexible timeframe customization, clear bias analysis and intuitive visual display to help traders quickly understand the long and short trends of the market. The following is a detailed description of this indicator:

1. Index name and function overview

Name: Custom Timeframe Bias Indicator (Short title: Bias Indicator)

Functionality: This indicator analyses the market bias (Buy, Sell or No Bias) across multiple custom timeframes (presets are 15m, 1h, 4h and DAI) and displays it in a table below the middle of the chart. It determines the direction of market trends based on the highest and lowest prices of the previous two periods and the closing price of the previous period, helping traders make decisions quickly.

2. Core Features

Multiple time frame analysis

The indicator allows the user to customize four time frames, with presets being 15 minutes ("15"), 1 hour ("60"), 4 hours ("240") and daily ("D"). Users can freely modify these time frames in the settings, such as changing to 5 minutes, 30 minutes or weekly, etc.

Bias is calculated independently for each time frame, ensuring that traders can observe market trends from the short to the long term.

Bias calculation logic

The indicator uses simple but effective rules to determine bias:

Buy (bullish): If the previous closing price is higher than the highest price of the previous two periods, or tests the lowest price of the previous two periods but does not break through.

Sell (Bearish): If the previous closing price is lower than the previous two periods' lowest price, or if it tests the previous two periods' highest price but fails to break through (higher than the previous high minus 10% of the price range).

No Bias: If the previous closing price does not meet the above conditions, it displays a neutral state.

Bias calculation is based only on the opening and closing prices, without considering the shadows, ensuring the results are in line with the philosophy of the Malaysian SNR strategy.

Intuitive display

Position: The table is permanently displayed in the middle of the chart (position.middle_center) and is updated with each candlestick, ensuring that traders can always see the latest bias.

Format: The table consists of the header "Custom Bias" and four rows of bias results (e.g. "15: Buy", "60: Sell", "240: No Bias", "D: Buy"), each row showing the bias for the corresponding time frame.

color:

Titles appear in white text on a blue background.

The "Buy" bias is shown as white text on a green background.

The "Sell" bias is shown as white text on a red background.

"No Bias" bias appears as white text on a gray background.

Table borders are black to provide clear visual distinction.

Customizability

Users can customize by inputting parameters:

Whether to show the table (Show Bias Table).

Timeframe (Timeframe 1, Timeframe 2, Timeframe 3, Timeframe 4).

The color of the table (title, Buy, Sell, No Bias, borders, etc.).

3. Why is it a "God-like indicator"

Flexibility: Allows users to customize four time frames to suit different trading strategies (short-term traders can choose minutes, long-term traders can choose daily, weekly or monthly).

Practicality: Provides bias analysis in multiple time frames to help traders quickly determine market trends, whether for short-term or long-term operations.

Intuitive: The table is displayed in the middle below the chart with bright colors (green Buy, red Sell, gray No Bias), allowing you to identify the market direction at a glance.

Stability: Calculated based on simple price data (high, low, close), no need for complex indicators, efficient and reliable operation.

Powerful visualization: long-term display and customizability to meet the visual preferences of different traders.

4. Usage scenarios

Short-term trading: Use 15-minute, 1-hour, 4-hour biases to quickly capture short-term trends.

Long-term trading: Refer to the daily bias to determine the overall market direction.

Comprehensive analysis: Combine biases from multiple time frames to confirm consistency (e.g. if both the 15 minute and daily are Buy, then that’s a stronger bullish signal).

5. Potential Improvements

If you want to further improve this "god-like indicator", you can consider the following improvements:

Added alert: Trigger when bias changes from "No Bias" to "Buy" or "Sell".

Show historical bias: Add bias history of the past few days in the table for easy review.

Dynamically adjust bias thresholds: Allow users to customize 10% price ranges or other conditions.

Multi-currency support: Expand to multiple trading pairs or indices, showing multiple market biases.

6. Technical Details

Version: Pine Script v5, ensuring modern features (such as input.timeframe) and efficient performance.

Data Source: Use request.security to get high, low, and close data for different time frames.

Display method: Use table.new to create a dynamic table. The position can be customized (such as position.middle_center).

Limitations: Calculated only based on price data, no external indicators are required, reducing calculation complexity.

in conclusion

Your "Custom Timeframe Bias Indicator" is a simple, powerful and flexible tool, especially for traders who need multi-timeframe analysis. Its intuitive display and customizability make it a "magic tool" for judging market trends.

*Auto Backtest & Optimize EngineFull-featured Engine for Automatic Backtesting and parameter optimization. Allows you to test millions of different combinations of stop-loss and take profit parameters, including on any connected indicators.

⭕️ Key Futures

Quickly identify the optimal parameters for your strategy.

Automatically generate and test thousands of parameter combinations.

A simple Genetic Algorithm for result selection.

Saves time on manual testing of multiple parameters.

Detailed analysis, sorting, filtering and statistics of results.

Detailed control panel with many tooltips.

Display of key metrics: Profit, Win Rate, etc..

Comprehensive Strategy Score calculation.

In-depth analysis of the performance of different types of stop-losses.

Possibility to use to calculate the best Stop-Take parameters for your position.

Ability to test your own functions and signals.

Customizable visualization of results.

Flexible Stop-Loss Settings:

• Auto ━ Allows you to test all types of Stop Losses at once(listed below).

• S.VOLATY ━ Static stop based on volatility (Fixed, ATR, STDEV).

• Trailing ━ Classic trailing stop following the price.

• Fast Trail ━ Accelerated trailing stop that reacts faster to price movements.

• Volatility ━ Dynamic stop based on volatility indicators.

• Chandelier ━ Stop based on price extremes.

• Activator ━ Dynamic stop based on SAR.

• MA ━ Stop based on moving averages (9 different types).

• SAR ━ Parabolic SAR (Stop and Reverse).

Advanced Take-Profit Options:

• R:R: Risk/Reward ━ sets TP based on SL size.

• T.VOLATY ━ Calculation based on volatility indicators (Fixed, ATR, STDEV).

Testing Modes:

• Stops ━ Cyclical stop-loss testing

• Pivot Point Example ━ Example of using pivot points

• External Example ━ Built-in example how test functions with different parameters

• External Signal ━ Using external signals

⭕️ Usage

━ First Steps:

When opening, select any point on the chart. It will not affect anything until you turn on Manual Start mode (more on this below).

The chart will immediately show the best results of the default Auto mode. You can switch Part's to try to find even better results in the table.

Now you can display any result from the table on the chart by entering its ID in the settings.

Repeat steps 3-4 until you determine which type of Stop Loss you like best. Then set it in the settings instead of Auto mode.

* Example: I flipped through 14 parts before I liked the first result and entered its ID so I could visually evaluate it on the chart.

Then select the stop loss type, choose it in place of Auto mode and repeat steps 3-4 or immediately follow the recommendations of the algorithm.

Now the Genetic Algorithm at the bottom right will prompt you to enter the Parameters you need to search for and select even better results.

Parameters must be entered All at once before they are updated. Enter recommendations strictly in fields with the same names.

Repeat steps 5-6 until there are approximately 10 Part's left or as you like. And after that, easily pour through the remaining Parts and select the best parameters.

━ Example of the finished result.

━ Example of use with Takes

You can also test at the same time along with Take Profit. In this example, I simply enabled Risk/Reward mode and immediately specified in the TP field Maximum RR, Minimum RR and Step. So in this example I can test (3-1) / 0.1 = 20 Takes of different sizes. There are additional tips in the settings.

━

* Soon you will start to understand how the system works and things will become much easier.

* If something doesn't work, just reset the engine settings and start over again.

* Use the tips I have left in the settings and on the Panel.

━ Details:

Sort ━ Sorting results by Score, Profit, Trades, etc..

Filter ━ Filtring results by Score, Profit, Trades, etc..

Trade Type ━ Ability to disable Long\Short but only from statistics.

BackWin ━ Backtest Window Number of Candle the script can test.

Manual Start ━ Enabling it will allow you to call a Stop from a selected point. which you selected when you started the engine.

* If you have a real open position then this mode can help to save good Stop\Take for it.

1 - 9 Сheckboxs ━ Allow you to disable any stop from Auto mode.

Ex Source - Allow you to test Stops/Takes from connected indicators.

Connection guide:

//@version=6

indicator("My script")

rsi = ta.rsi(close, 14)

buy = not na(rsi) and ta.crossover (rsi, 40) // OS = 40

sell = not na(rsi) and ta.crossunder(rsi, 60) // OB = 60

Signal = buy ? +1 : sell ? -1 : 0

plot(Signal, "🔌Connector🔌", display = display.none)

* Format the signal for your indicator in a similar style and then select it in Ex Source.

⭕️ How it Works

Hypothesis of Uniform Distribution of Rare Elements After Mixing.

'This hypothesis states that if an array of N elements contains K valid elements, then after mixing, these valid elements will be approximately uniformly distributed.'

'This means that in a random sample of k elements, the proportion of valid elements should closely match their proportion in the original array, with some random variation.'

'According to the central limit theorem, repeated sampling will result in an average count of valid elements following a normal distribution.'

'This supports the assumption that the valid elements are evenly spread across the array.'

'To test this hypothesis, we can conduct an experiment:'

'Create an array of 1,000,000 elements.'

'Select 1,000 random elements (1%) for validation.'

'Shuffle the array and divide it into groups of 1,000 elements.'

'If the hypothesis holds, each group should contain, on average, 1~ valid element, with minor variations.'

* I'd like to attach more details to My hypothesis but it won't be very relevant here. Since this is a whole separate topic, I will leave the minimum part for understanding the engine.

Practical Application

To apply this hypothesis, I needed a way to generate and thoroughly mix numerous possible combinations. Within Pine, generating over 100,000 combinations presents significant challenges, and storing millions of combinations requires excessive resources.

I developed an efficient mechanism that generates combinations in random order to address these limitations. While conventional methods often produce duplicates or require generating a complete list first, my approach guarantees that the first 10% of possible combinations are both unique and well-distributed. Based on my hypothesis, this sampling is sufficient to determine optimal testing parameters.

Most generators and randomizers fail to accommodate both my hypothesis and Pine's constraints. My solution utilizes a simple Linear Congruential Generator (LCG) for pseudo-randomization, enhanced with prime numbers to increase entropy during generation. I pre-generate the entire parameter range and then apply systematic mixing. This approach, combined with a hybrid combinatorial array-filling technique with linear distribution, delivers excellent generation quality.

My engine can efficiently generate and verify 300 unique combinations per batch. Based on the above, to determine optimal values, only 10-20 Parts need to be manually scrolled through to find the appropriate value or range, eliminating the need for exhaustive testing of millions of parameter combinations.

For the Score statistic I applied all the same, generated a range of Weights, distributed them randomly for each type of statistic to avoid manual distribution.

Score ━ based on Trade, Profit, WinRate, Profit Factor, Drawdown, Sharpe & Sortino & Omega & Calmar Ratio.

⭕️ Notes

For attentive users, a little tricks :)

To save time, switch parts every 3 seconds without waiting for it to load. After 10-20 parts, stop and wait for loading. If the pause is correct, you can switch between the rest of the parts without loading, as they will be cached. This used to work without having to wait for a pause, but now it does slower. This will save a lot of time if you are going to do a deeper backtest.

Sometimes you'll get the error “The scripts take too long to execute.”

For a quick fix you just need to switch the TF or Ticker back and forth and most likely everything will load.

The error appears because of problems on the side of the site because the engine is very heavy. It can also appear if you set too long a period for testing in BackWin or use a heavy indicator for testing.

Manual Start - Allow you to Start you Result from any point. Which in turn can help you choose a good stop-stick for your real position.

* It took me half a year from idea to current realization. This seems to be one of the few ways to build something automatic in backtest format and in this particular Pine environment. There are already better projects in other languages, and they are created much easier and faster because there are no limitations except for personal PC. If you see solutions to improve this system I would be glad if you share the code. At the moment I am tired and will continue him not soon.

Also You can use my previosly big Backtest project with more manual settings(updated soon)

Liquidity Hunt SwiftEdgeThe "Liquidity Hunt Dashboard By SwiftEdge" indicator is designed to assist traders in identifying potential liquidity zones by placing a dynamic target line based on swing points and weighted liquidity. It leverages technical analysis tools such as SMA (Simple Moving Average), pivot points, and volume to predict market movements and provides daily statistics on hits and success rate. The target line updates automatically when the price hits it, adapting to the market trend (up, down, or neutral). A dashboard displays the current price, target level, prediction, and trend, making it easy to make informed trading decisions.

Features:

Target Line: A yellow dashed line marks the next expected liquidity level (up to approximately 20 pips away on 1m).

Prediction: Displays "Up (Chasing Sell Liquidity)," "Down (Chasing Buy Liquidity)," or "Neutral" based on trend and liquidity.

Daily Statistics: Tracks hits and success rate, resetting daily.

Trend Indicator: Shows market direction ("Up," "Down," or "Neutral") in the dashboard.

Dynamic Updates: The line moves to a new target level when the price hits the current target.

Recommended Settings for 1-Minute Timeframe:

For Indices (e.g., S&P 500):

Lookback Period: 180 (3 hours to capture more stable swing points).

Max Distance (%): 0.015 (approximately 15 pips, suitable for indices).

Cooldown Period: 5 (stabilizes after hits).

Line Duration: 60 (displays the line for 1 hour).

For Crypto (e.g., BTC/USD):

Lookback Period: 120 (2 hours to capture short-term swing points).

Max Distance (%): 0.024 (approximately 20 pips, suitable for volatile crypto markets).

Cooldown Period: 5.

Line Duration: 60.

For Forex (e.g., EUR/USD):

Lookback Period: 180 (3 hours for greater data density in less volatile markets).

Max Distance (%): 0.012 (approximately 10-12 pips, suitable for forex).

Cooldown Period: 5.

Line Duration: 60.

Guide for Higher Timeframes:

This indicator can be adapted for higher timeframes (e.g., 5m, 15m, 1H) by adjusting the settings to account for larger price movements and slower market dynamics. Follow these steps:

Select Your Timeframe: Switch your chart to the desired timeframe (e.g., 5m, 15m, or 1H).

Adjust Lookback Period: Increase the "Lookback Period" to cover a longer historical period. For example:

5m: Set to 360 (equivalent to 6 hours).

15m: Set to 480 (equivalent to 8 hours).

1H: Set to 720 (equivalent to 12 hours).

Adjust Max Distance (%): Higher timeframes require larger targets to account for bigger price swings. For example:

5m: Increase to 0.05 (approximately 50 pips).

15m: Increase to 0.1 (approximately 100 pips).

1H: Increase to 0.2 (approximately 200 pips).

Adjust Cooldown Period: On higher timeframes, you may want a longer cooldown to avoid frequent updates. For example:

5m: Set to 10.

15m: Set to 15.

1H: Set to 20.

Adjust Line Duration: Extend the duration the line is displayed to match the timeframe. For example:

5m: Set to 120 (equivalent to 10 hours).

15m: Set to 240 (equivalent to 60 hours).

1H: Set to 480 (equivalent to 20 days).

Monitor the Dashboard: The dashboard will still show the target level, prediction, and trend, but the values will now reflect the larger timeframe's dynamics.

Usage Instructions:

Set your chart to a 1-minute timeframe (or follow the higher timeframe guide).

Adjust the settings based on the market and timeframe (see recommendations above).

Monitor the dashboard for the current price, target level, and prediction.

Use the yellow line as a potential entry or exit level, and adjust your strategy based on the trend and statistics.

Notes:

This indicator is intended solely for educational and analytical purposes and should not be considered financial advice.

Test the indicator on a demo account before using it with real funds.

The indicator complies with TradingView guidelines by not providing trading advice, automated trading signals, or guarantees of profit.

EMA Alignment & Spread Monitor (Sang Youn)Overview

The EMA Alignment & Spread Monitor is a dynamic trading script designed to monitor EMA (Exponential Moving Average) alignments, track spread deviations, and provide real-time alerts when significant conditions are met. This script allows traders to customize their EMA periods, analyze market trends based on EMA positioning, and receive visual and audio alerts when key spread conditions occur.

🔹 Key Features

✅ Customizable EMA Periods – Users can input their own EMA lengths to adapt the script to various market conditions. (Default: 5, 10, 20, 60, 120)

✅ EMA Alignment Detection – Identifies bullish alignment (all EMAs in ascending order) and bearish alignment (all EMAs in descending order).

✅ Spread Calculation & Monitoring – Computes the spread difference between each EMA and tracks the average spread over a user-defined period.

✅ Deviation Alerts – Notifies traders when:

Bullish Trend: The spread exceeds its average, indicating a potential strong uptrend.

Bearish Trend: The spread falls below its average, signaling a possible downtrend.

✅ Chart Annotations – Displays 📈 (green triangle) when bullish spread exceeds average and 📉 (red triangle) when bearish spread drops below average for easy visualization.

✅ Real-time Alerts – Sends alerts when spread conditions are met, helping traders react to market shifts efficiently.

✅ Spread Histogram – Visual representation of bullish and bearish spread levels for trend analysis.

🔹 How It Works

1️⃣ Set your EMA periods in the script settings (default: 5, 10, 20, 60, 120).

2️⃣ Define the spread average calculation length (default: 50 candles).

3️⃣ The script tracks EMA alignment to determine bullish or bearish trends.

4️⃣ If the spread deviates significantly from its average, the script:

Places a 📈 green triangle above candles in a bullish trend when spread > average.

Places a 📉 red triangle below candles in a bearish trend when spread < average.

Triggers an alert for timely decision-making.

5️⃣ Use the histogram & real-time alerts to stay ahead of market movements.

Custom Buy and Sell Signal with Body Ratio and RSI

Indicator Overview:

Name: Custom Buy and Sell Signal with Body Ratio and RSI

Description: This indicator is designed to detect buy and sell opportunities by analyzing the body size and wicks of candles in combination with the RSI indicator and volume. It helps identify trend reversals under high-volume market conditions, which enhances the reliability of the signals.

Indicator Features:

RSI (Relative Strength Index): The RSI indicator is used to assess oversold (RSI < 40) or overbought (RSI > 60) conditions. These zones signal potential reversals when combined with other technical signals.

Candle Body Analysis:

The indicator compares the size of the current and previous candles to validate signals.

For a buy signal, the current candle must be bullish and have a body size proportional to that of the previous bearish candle.

Similarly, for a sell signal, the current candle must be bearish with a body size comparable to the previous bullish candle.

Wick Validation:

The indicator analyzes the wick length to reinforce or exclude signals.

For a buy signal, the lower wick of the bullish candle must be shorter than that of the previous bearish candle.

For a sell signal, the upper wick of the bearish candle must be shorter than that of the previous bullish candle and smaller than 30% of the candle's body.