"神户胜利+VS+磐田喜悦" için komut dosyalarını ara

200/100 vs 190/80 EMA [jarederaj]Track the 200/100 EMA cross Vs the 180/90 EMA cross. Also, see the dates when these periods start on the chart.

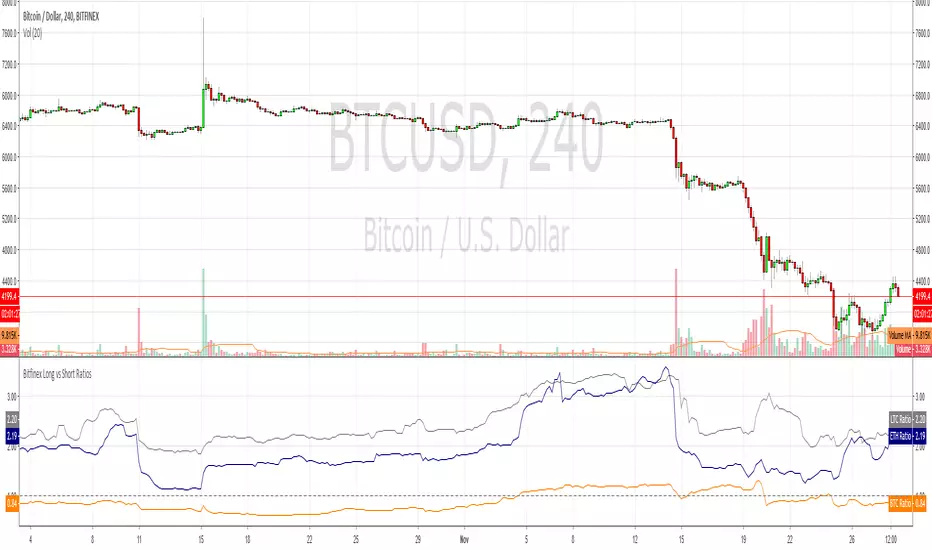

Bitfinex Long vs Short RatiosWas impressed with the 'Longs vs Shorts Ratio' idea from the tweet below so I coded an indicator, enjoy.

twitter.com

Compare - Oscillator vs BTC momentumI've made a simple indicator to compare the momentum of a trading pair against the momentum of BTC to the dollar. I use it to see how a pair is affected by BTC's momentum... I wouldnt use it to trade off alone, but it can be a useful tool alongside other indicators.

The time range can be adjusted, but I wouldnt reccomend setting it to anything over 12M, or under 1W.... as I'm not sure if it would work.

Any feedback is welcome!

This is an idea I had after looking at a wonderful visualisation made by BarclayJames, link below:

www.tradingview.com

비트코인 한국 프리미엄 캔들 차트 (Bithumb vs Bitfinex) by 호재박스 슈퍼스타지표명: 비트코인 한국 프리미엄 캔들 차트 (Bithumb vs Bitfinex)

제작자: 호재박스 슈퍼스타

홈페이지: hozaebox.com

BTCUSD long vs short ratio+rsiJust a script I want to share with friends on a discord

orange/green line : longs vs short ratio (100 = only longs, 0 = only shorts)

purple line : RSI of (longs-shorts)

Bitcoin Exchanges Premium (Incl Int & GBTC) vs GdaxShows the exchange premiums internationally (Hong Kong, Luxembourg, Korea, Japan, China) vs Gdax. Also includes GBTC Trust price (adjusted).

Index Vs Futures v4.0 (dashed edition)Generalized script of

Originally designed for bitcoin, but can be used to compare between futures and index (or any two symbol expressions).

Conventions:

- green background := futures deviates 'way above' index

- red background := futures deviates 'way below' index

VS Score [SpiritualHealer117]An experimental indicator that uses historical prices and readings of technical indicators to give the probability that stock and crypto prices will be in a certain range on the next close. This indicator may be helpful for options traders or for traders who want to see the probability of a move.

It classifies returns into five categories:

Extreme Rise - Over 2 standard deviations above normal returns

Rise - Between 0.5 standard deviations and 2 standard deviations above normal returns

Flat - Falling in the range of +/- 0.5 standard deviations of normal returns

Fall - Between 0.5 standard deviations and 2 standard deviations below normal returns

Extreme Fall - Over 2 standard deviations below normal returns

It is an adaptive probability model, which trains on the previous 1000 data points, and is calculated by creating probability vectors for the current reading of the PPO, MA, volume histogram, and previous return, and combining them into one probability vector.

Adaptive Genesis Engine [AGE]ADAPTIVE GENESIS ENGINE (AGE)

Pure Signal Evolution Through Genetic Algorithms

Where Darwin Meets Technical Analysis

🧬 WHAT YOU'RE GETTING - THE PURE INDICATOR

This is a technical analysis indicator - it generates signals, visualizes probability, and shows you the evolutionary process in real-time. This is NOT a strategy with automatic execution - it's a sophisticated signal generation system that you control .

What This Indicator Does:

Generates Long/Short entry signals with probability scores (35-88% range)

Evolves a population of up to 12 competing strategies using genetic algorithms

Validates strategies through walk-forward optimization (train/test cycles)

Visualizes signal quality through premium gradient clouds and confidence halos

Displays comprehensive metrics via enhanced dashboard

Provides alerts for entries and exits

Works on any timeframe, any instrument, any broker

What This Indicator Does NOT Do:

Execute trades automatically

Manage positions or calculate position sizes

Place orders on your behalf

Make trading decisions for you

This is pure signal intelligence. AGE tells you when and how confident it is. You decide whether and how much to trade.

🔬 THE SCIENCE: GENETIC ALGORITHMS MEET TECHNICAL ANALYSIS

What Makes This Different - The Evolutionary Foundation

Most indicators are static - they use the same parameters forever, regardless of market conditions. AGE is alive . It maintains a population of competing strategies that evolve, adapt, and improve through natural selection principles:

Birth: New strategies spawn through crossover breeding (combining DNA from fit parents) plus random mutation for exploration

Life: Each strategy trades virtually via shadow portfolios, accumulating wins/losses, tracking drawdown, and building performance history

Selection: Strategies are ranked by comprehensive fitness scoring (win rate, expectancy, drawdown control, signal efficiency)

Death: Weak strategies are culled periodically, with elite performers (top 2 by default) protected from removal

Evolution: The gene pool continuously improves as successful traits propagate and unsuccessful ones die out

This is not curve-fitting. Each new strategy must prove itself on out-of-sample data through walk-forward validation before being trusted for live signals.

🧪 THE DNA: WHAT EVOLVES

Every strategy carries a 10-gene chromosome controlling how it interprets market data:

Signal Sensitivity Genes

Entropy Sensitivity (0.5-2.0): Weight given to market order/disorder calculations. Low values = conservative, require strong directional clarity. High values = aggressive, act on weaker order signals.

Momentum Sensitivity (0.5-2.0): Weight given to RSI/ROC/MACD composite. Controls responsiveness to momentum shifts vs. mean-reversion setups.

Structure Sensitivity (0.5-2.0): Weight given to support/resistance positioning. Determines how much price location within swing range matters.

Probability Adjustment Genes

Probability Boost (-0.10 to +0.10): Inherent bias toward aggressive (+) or conservative (-) entries. Acts as personality trait - some strategies naturally optimistic, others pessimistic.

Trend Strength Requirement (0.3-0.8): Minimum trend conviction needed before signaling. Higher values = only trades strong trends, lower values = acts in weak/sideways markets.

Volume Filter (0.5-1.5): Strictness of volume confirmation. Higher values = requires strong volume, lower values = volume less important.

Risk Management Genes

ATR Multiplier (1.5-4.0): Base volatility scaling for all price levels. Controls whether strategy uses tight or wide stops/targets relative to ATR.

Stop Multiplier (1.0-2.5): Stop loss tightness. Lower values = aggressive profit protection, higher values = more breathing room.

Target Multiplier (1.5-4.0): Profit target ambition. Lower values = quick scalping exits, higher values = swing trading holds.

Adaptation Gene

Regime Adaptation (0.0-1.0): How much strategy adjusts behavior based on detected market regime (trending/volatile/choppy). Higher values = more reactive to regime changes.

The Magic: AGE doesn't just try random combinations. Through tournament selection and fitness-weighted crossover, successful gene combinations spread through the population while unsuccessful ones fade away. Over 50-100 bars, you'll see the population converge toward genes that work for YOUR instrument and timeframe.

📊 THE SIGNAL ENGINE: THREE-LAYER SYNTHESIS

Before any strategy generates a signal, AGE calculates probability through multi-indicator confluence:

Layer 1 - Market Entropy (Information Theory)

Measures whether price movements exhibit directional order or random walk characteristics:

The Math:

Shannon Entropy = -Σ(p × log(p))

Market Order = 1 - (Entropy / 0.693)

What It Means:

High entropy = choppy, random market → low confidence signals

Low entropy = directional market → high confidence signals

Direction determined by up-move vs down-move dominance over lookback period (default: 20 bars)

Signal Output: -1.0 to +1.0 (bearish order to bullish order)

Layer 2 - Momentum Synthesis

Combines three momentum indicators into single composite score:

Components:

RSI (40% weight): Normalized to -1/+1 scale using (RSI-50)/50

Rate of Change (30% weight): Percentage change over lookback (default: 14 bars), clamped to ±1

MACD Histogram (30% weight): Fast(12) - Slow(26), normalized by ATR

Why This Matters: RSI catches mean-reversion opportunities, ROC catches raw momentum, MACD catches momentum divergence. Weighting favors RSI for reliability while keeping other perspectives.

Signal Output: -1.0 to +1.0 (strong bearish to strong bullish)

Layer 3 - Structure Analysis

Evaluates price position within swing range (default: 50-bar lookback):

Position Classification:

Bottom 20% of range = Support Zone → bullish bounce potential

Top 20% of range = Resistance Zone → bearish rejection potential

Middle 60% = Neutral Zone → breakout/breakdown monitoring

Signal Logic:

At support + bullish candle = +0.7 (strong buy setup)

At resistance + bearish candle = -0.7 (strong sell setup)

Breaking above range highs = +0.5 (breakout confirmation)

Breaking below range lows = -0.5 (breakdown confirmation)

Consolidation within range = ±0.3 (weak directional bias)

Signal Output: -1.0 to +1.0 (bearish structure to bullish structure)

Confluence Voting System

Each layer casts a vote (Long/Short/Neutral). The system requires minimum 2-of-3 agreement (configurable 1-3) before generating a signal:

Examples:

Entropy: Bullish, Momentum: Bullish, Structure: Neutral → Signal generated (2 long votes)

Entropy: Bearish, Momentum: Neutral, Structure: Neutral → No signal (only 1 short vote)

All three bullish → Signal generated with +5% probability bonus

This is the key to quality. Single indicators give too many false signals. Triple confirmation dramatically improves accuracy.

📈 PROBABILITY CALCULATION: HOW CONFIDENCE IS MEASURED

Base Probability:

Raw_Prob = 50% + (Average_Signal_Strength × 25%)

Then AGE applies strategic adjustments:

Trend Alignment:

Signal with trend: +4%

Signal against strong trend: -8%

Weak/no trend: no adjustment

Regime Adaptation:

Trending market (efficiency >50%, moderate vol): +3%

Volatile market (vol ratio >1.5x): -5%

Choppy market (low efficiency): -2%

Volume Confirmation:

Volume > 70% of 20-bar SMA: no change

Volume below threshold: -3%

Volatility State (DVS Ratio):

High vol (>1.8x baseline): -4% (reduce confidence in chaos)

Low vol (<0.7x baseline): -2% (markets can whipsaw in compression)

Moderate elevated vol (1.0-1.3x): +2% (trending conditions emerging)

Confluence Bonus:

All 3 indicators agree: +5%

2 of 3 agree: +2%

Strategy Gene Adjustment:

Probability Boost gene: -10% to +10%

Regime Adaptation gene: scales regime adjustments by 0-100%

Final Probability: Clamped between 35% (minimum) and 88% (maximum)

Why These Ranges?

Below 35% = too uncertain, better not to signal

Above 88% = unrealistic, creates overconfidence

Sweet spot: 65-80% for quality entries

🔄 THE SHADOW PORTFOLIO SYSTEM: HOW STRATEGIES COMPETE

Each active strategy maintains a virtual trading account that executes in parallel with real-time data:

Shadow Trading Mechanics

Entry Logic:

Calculate signal direction, probability, and confluence using strategy's unique DNA

Check if signal meets quality gate:

Probability ≥ configured minimum threshold (default: 65%)

Confluence ≥ configured minimum (default: 2 of 3)

Direction is not zero (must be long or short, not neutral)

Verify signal persistence:

Base requirement: 2 bars (configurable 1-5)

Adapts based on probability: high-prob signals (75%+) enter 1 bar faster, low-prob signals need 1 bar more

Adjusts for regime: trending markets reduce persistence by 1, volatile markets add 1

Apply additional filters:

Trend strength must exceed strategy's requirement gene

Regime filter: if volatile market detected, probability must be 72%+ to override

Volume confirmation required (volume > 70% of average)

If all conditions met for required persistence bars, enter shadow position at current close price

Position Management:

Entry Price: Recorded at close of entry bar

Stop Loss: ATR-based distance = ATR × ATR_Mult (gene) × Stop_Mult (gene) × DVS_Ratio

Take Profit: ATR-based distance = ATR × ATR_Mult (gene) × Target_Mult (gene) × DVS_Ratio

Position: +1 (long) or -1 (short), only one at a time per strategy

Exit Logic:

Check if price hit stop (on low) or target (on high) on current bar

Record trade outcome in R-multiples (profit/loss normalized by ATR)

Update performance metrics:

Total trades counter incremented

Wins counter (if profit > 0)

Cumulative P&L updated

Peak equity tracked (for drawdown calculation)

Maximum drawdown from peak recorded

Enter cooldown period (default: 8 bars, configurable 3-20) before next entry allowed

Reset signal age counter to zero

Walk-Forward Tracking:

During position lifecycle, trades are categorized:

Training Phase (first 250 bars): Trade counted toward training metrics

Testing Phase (next 75 bars): Trade counted toward testing metrics (out-of-sample)

Live Phase (after WFO period): Trade counted toward overall metrics

Why Shadow Portfolios?

No lookahead bias (uses only data available at the bar)

Realistic execution simulation (entry on close, stop/target checks on high/low)

Independent performance tracking for true fitness comparison

Allows safe experimentation without risking capital

Each strategy learns from its own experience

🏆 FITNESS SCORING: HOW STRATEGIES ARE RANKED

Fitness is not just win rate. AGE uses a comprehensive multi-factor scoring system:

Core Metrics (Minimum 3 trades required)

Win Rate (30% of fitness):

WinRate = Wins / TotalTrades

Normalized directly (0.0-1.0 scale)

Total P&L (30% of fitness):

Normalized_PnL = (PnL + 300) / 600

Clamped 0.0-1.0. Assumes P&L range of -300R to +300R for normalization scale.

Expectancy (25% of fitness):

Expectancy = Total_PnL / Total_Trades

Normalized_Expectancy = (Expectancy + 30) / 60

Clamped 0.0-1.0. Rewards consistency of profit per trade.

Drawdown Control (15% of fitness):

Normalized_DD = 1 - (Max_Drawdown / 15)

Clamped 0.0-1.0. Penalizes strategies that suffer large equity retracements from peak.

Sample Size Adjustment

Quality Factor:

<50 trades: 1.0 (full weight, small sample)

50-100 trades: 0.95 (slight penalty for medium sample)

100 trades: 0.85 (larger penalty for large sample)

Why penalize more trades? Prevents strategies from gaming the system by taking hundreds of tiny trades to inflate statistics. Favors quality over quantity.

Bonus Adjustments

Walk-Forward Validation Bonus:

if (WFO_Validated):

Fitness += (WFO_Efficiency - 0.5) × 0.1

Strategies proven on out-of-sample data receive up to +10% fitness boost based on test/train efficiency ratio.

Signal Efficiency Bonus (if diagnostics enabled):

if (Signals_Evaluated > 10):

Pass_Rate = Signals_Passed / Signals_Evaluated

Fitness += (Pass_Rate - 0.1) × 0.05

Rewards strategies that generate high-quality signals passing the quality gate, not just profitable trades.

Final Fitness: Clamped at 0.0 minimum (prevents negative fitness values)

Result: Elite strategies typically achieve 0.50-0.75 fitness. Anything above 0.60 is excellent. Below 0.30 is prime candidate for culling.

🔬 WALK-FORWARD OPTIMIZATION: ANTI-OVERFITTING PROTECTION

This is what separates AGE from curve-fitted garbage indicators.

The Three-Phase Process

Every new strategy undergoes a rigorous validation lifecycle:

Phase 1 - Training Window (First 250 bars, configurable 100-500):

Strategy trades normally via shadow portfolio

All trades count toward training performance metrics

System learns which gene combinations produce profitable patterns

Tracks independently: Training_Trades, Training_Wins, Training_PnL

Phase 2 - Testing Window (Next 75 bars, configurable 30-200):

Strategy continues trading without any parameter changes

Trades now count toward testing performance metrics (separate tracking)

This is out-of-sample data - strategy has never seen these bars during "optimization"

Tracks independently: Testing_Trades, Testing_Wins, Testing_PnL

Phase 3 - Validation Check:

Minimum_Trades = 5 (configurable 3-15)

IF (Train_Trades >= Minimum AND Test_Trades >= Minimum):

WR_Efficiency = Test_WinRate / Train_WinRate

Expectancy_Efficiency = Test_Expectancy / Train_Expectancy

WFO_Efficiency = (WR_Efficiency + Expectancy_Efficiency) / 2

IF (WFO_Efficiency >= 0.55): // configurable 0.3-0.9

Strategy.Validated = TRUE

Strategy receives fitness bonus

ELSE:

Strategy receives 30% fitness penalty

ELSE:

Validation deferred (insufficient trades in one or both periods)

What Validation Means

Validated Strategy (Green "✓ VAL" in dashboard):

Performed at least 55% as well on unseen data compared to training data

Gets fitness bonus: +(efficiency - 0.5) × 0.1

Receives priority during tournament selection for breeding

More likely to be chosen as active trading strategy

Unvalidated Strategy (Orange "○ TRAIN" in dashboard):

Failed to maintain performance on test data (likely curve-fitted to training period)

Receives 30% fitness penalty (0.7x multiplier)

Makes strategy prime candidate for culling

Can still trade but with lower selection probability

Insufficient Data (continues collecting):

Hasn't completed both training and testing periods yet

OR hasn't achieved minimum trade count in both periods

Validation check deferred until requirements met

Why 55% Efficiency Threshold?

If a strategy earned 10R during training but only 5.5R during testing, it still proved an edge exists beyond random luck. Requiring 100% efficiency would be unrealistic - market conditions change between periods. But requiring >50% ensures the strategy didn't completely degrade on fresh data.

The Protection: Strategies that work great on historical data but fail on new data are automatically identified and penalized. This prevents the population from being polluted by overfitted strategies that would fail in live trading.

🌊 DYNAMIC VOLATILITY SCALING (DVS): ADAPTIVE STOP/TARGET PLACEMENT

AGE doesn't use fixed stop distances. It adapts to current volatility conditions in real-time.

Four Volatility Measurement Methods

1. ATR Ratio (Simple Method):

Current_Vol = ATR(14) / Close

Baseline_Vol = SMA(Current_Vol, 100)

Ratio = Current_Vol / Baseline_Vol

Basic comparison of current ATR to 100-bar moving average baseline.

2. Parkinson (High-Low Range Based):

For each bar: HL = log(High / Low)

Parkinson_Vol = sqrt(Σ(HL²) / (4 × Period × log(2)))

More stable than close-to-close volatility. Captures intraday range expansion without overnight gap noise.

3. Garman-Klass (OHLC Based):

HL_Term = 0.5 × ²

CO_Term = (2×log(2) - 1) × ²

GK_Vol = sqrt(Σ(HL_Term - CO_Term) / Period)

Most sophisticated estimator. Incorporates all four price points (open, high, low, close) plus gap information.

4. Ensemble Method (Default - Median of All Three):

Ratio_1 = ATR_Current / ATR_Baseline

Ratio_2 = Parkinson_Current / Parkinson_Baseline

Ratio_3 = GK_Current / GK_Baseline

DVS_Ratio = Median(Ratio_1, Ratio_2, Ratio_3)

Why Ensemble?

Takes median to avoid outliers and false spikes

If ATR jumps but range-based methods stay calm, median prevents overreaction

If one method fails, other two compensate

Most robust approach across different market conditions

Sensitivity Scaling

Scaled_Ratio = (Raw_Ratio) ^ Sensitivity

Sensitivity 0.3: Cube root - heavily dampens volatility impact

Sensitivity 0.5: Square root - moderate dampening

Sensitivity 0.7 (Default): Balanced response to volatility changes

Sensitivity 1.0: Linear - full 1:1 volatility impact

Sensitivity 1.5: Exponential - amplified response to volatility spikes

Safety Clamps: Final DVS Ratio always clamped between 0.5x and 2.5x baseline to prevent extreme position sizing or stop placement errors.

How DVS Affects Shadow Trading

Every strategy's stop and target distances are multiplied by the current DVS ratio:

Stop Loss Distance:

Stop_Distance = ATR × ATR_Mult (gene) × Stop_Mult (gene) × DVS_Ratio

Take Profit Distance:

Target_Distance = ATR × ATR_Mult (gene) × Target_Mult (gene) × DVS_Ratio

Example Scenario:

ATR = 10 points

Strategy's ATR_Mult gene = 2.5

Strategy's Stop_Mult gene = 1.5

Strategy's Target_Mult gene = 2.5

DVS_Ratio = 1.4 (40% above baseline volatility - market heating up)

Stop = 10 × 2.5 × 1.5 × 1.4 = 52.5 points (vs. 37.5 in normal vol)

Target = 10 × 2.5 × 2.5 × 1.4 = 87.5 points (vs. 62.5 in normal vol)

Result:

During volatility spikes: Stops automatically widen to avoid noise-based exits, targets extend for bigger moves

During calm periods: Stops tighten for better risk/reward, targets compress for realistic profit-taking

Strategies adapt risk management to match current market behavior

🧬 THE EVOLUTIONARY CYCLE: SPAWN, COMPETE, CULL

Initialization (Bar 1)

AGE begins with 4 seed strategies (if evolution enabled):

Seed Strategy #0 (Balanced):

All sensitivities at 1.0 (neutral)

Zero probability boost

Moderate trend requirement (0.4)

Standard ATR/stop/target multiples (2.5/1.5/2.5)

Mid-level regime adaptation (0.5)

Seed Strategy #1 (Momentum-Focused):

Lower entropy sensitivity (0.7), higher momentum (1.5)

Slight probability boost (+0.03)

Higher trend requirement (0.5)

Tighter stops (1.3), wider targets (3.0)

Seed Strategy #2 (Entropy-Driven):

Higher entropy sensitivity (1.5), lower momentum (0.8)

Slight probability penalty (-0.02)

More trend tolerant (0.6)

Wider stops (1.8), standard targets (2.5)

Seed Strategy #3 (Structure-Based):

Balanced entropy/momentum (0.8/0.9), high structure (1.4)

Slight probability boost (+0.02)

Lower trend requirement (0.35)

Moderate risk parameters (1.6/2.8)

All seeds start with WFO validation bypassed if WFO is disabled, or must validate if enabled.

Spawning New Strategies

Timing (Adaptive):

Historical phase: Every 30 bars (configurable 10-100)

Live phase: Every 200 bars (configurable 100-500)

Automatically switches to live timing when barstate.isrealtime triggers

Conditions:

Current population < max population limit (default: 8, configurable 4-12)

At least 2 active strategies exist (need parents)

Available slot in population array

Selection Process:

Run tournament selection 3 times with different seeds

Each tournament: randomly sample active strategies, pick highest fitness

Best from 3 tournaments becomes Parent 1

Repeat independently for Parent 2

Ensures fit parents but maintains diversity

Crossover Breeding:

For each of 10 genes:

Parent1_Fitness = fitness

Parent2_Fitness = fitness

Weight1 = Parent1_Fitness / (Parent1_Fitness + Parent2_Fitness)

Gene1 = parent1's value

Gene2 = parent2's value

Child_Gene = Weight1 × Gene1 + (1 - Weight1) × Gene2

Fitness-weighted crossover ensures fitter parent contributes more genetic material.

Mutation:

For each gene in child:

IF (random < mutation_rate):

Gene_Range = GENE_MAX - GENE_MIN

Noise = (random - 0.5) × 2 × mutation_strength × Gene_Range

Mutated_Gene = Clamp(Child_Gene + Noise, GENE_MIN, GENE_MAX)

Historical mutation rate: 20% (aggressive exploration)

Live mutation rate: 8% (conservative stability)

Mutation strength: 12% of gene range (configurable 5-25%)

Initialization of New Strategy:

Unique ID assigned (total_spawned counter)

Parent ID recorded

Generation = max(parent generations) + 1

Birth bar recorded (for age tracking)

All performance metrics zeroed

Shadow portfolio reset

WFO validation flag set to false (must prove itself)

Result: New strategy with hybrid DNA enters population, begins trading in next bar.

Competition (Every Bar)

All active strategies:

Calculate their signal based on unique DNA

Check quality gate with their thresholds

Manage shadow positions (entries/exits)

Update performance metrics

Recalculate fitness score

Track WFO validation progress

Strategies compete indirectly through fitness ranking - no direct interaction.

Culling Weak Strategies

Timing (Adaptive):

Historical phase: Every 60 bars (configurable 20-200, should be 2x spawn interval)

Live phase: Every 400 bars (configurable 200-1000, should be 2x spawn interval)

Minimum Adaptation Score (MAS):

Initial MAS = 0.10

MAS decays: MAS × 0.995 every cull cycle

Minimum MAS = 0.03 (floor)

MAS represents the "survival threshold" - strategies below this fitness level are vulnerable.

Culling Conditions (ALL must be true):

Population > minimum population (default: 3, configurable 2-4)

At least one strategy has fitness < MAS

Strategy's age > culling interval (prevents premature culling of new strategies)

Strategy is not in top N elite (default: 2, configurable 1-3)

Culling Process:

Find worst strategy:

For each active strategy:

IF (age > cull_interval):

Fitness = base_fitness

IF (not WFO_validated AND WFO_enabled):

Fitness × 0.7 // 30% penalty for unvalidated

IF (Fitness < MAS AND Fitness < worst_fitness_found):

worst_strategy = this_strategy

worst_fitness = Fitness

IF (worst_strategy found):

Count elite strategies with fitness > worst_fitness

IF (elite_count >= elite_preservation_count):

Deactivate worst_strategy (set active flag = false)

Increment total_culled counter

Elite Protection:

Even if a strategy's fitness falls below MAS, it survives if fewer than N strategies are better. This prevents culling when population is generally weak.

Result: Weak strategies removed from population, freeing slots for new spawns. Gene pool improves over time.

Selection for Display (Every Bar)

AGE chooses one strategy to display signals:

Best fitness = -1

Selected = none

For each active strategy:

Fitness = base_fitness

IF (WFO_validated):

Fitness × 1.3 // 30% bonus for validated strategies

IF (Fitness > best_fitness):

best_fitness = Fitness

selected_strategy = this_strategy

Display selected strategy's signals on chart

Result: Only the highest-fitness (optionally validated-boosted) strategy's signals appear as chart markers. Other strategies trade invisibly in shadow portfolios.

🎨 PREMIUM VISUALIZATION SYSTEM

AGE includes sophisticated visual feedback that standard indicators lack:

1. Gradient Probability Cloud (Optional, Default: ON)

Multi-layer gradient showing signal buildup 2-3 bars before entry:

Activation Conditions:

Signal persistence > 0 (same directional signal held for multiple bars)

Signal probability ≥ minimum threshold (65% by default)

Signal hasn't yet executed (still in "forming" state)

Visual Construction:

7 gradient layers by default (configurable 3-15)

Each layer is a line-fill pair (top line, bottom line, filled between)

Layer spacing: 0.3 to 1.0 × ATR above/below price

Outer layers = faint, inner layers = bright

Color transitions from base to intense based on layer position

Transparency scales with probability (high prob = more opaque)

Color Selection:

Long signals: Gradient from theme.gradient_bull_mid to theme.gradient_bull_strong

Short signals: Gradient from theme.gradient_bear_mid to theme.gradient_bear_strong

Base transparency: 92%, reduces by up to 8% for high-probability setups

Dynamic Behavior:

Cloud grows/shrinks as signal persistence increases/decreases

Redraws every bar while signal is forming

Disappears when signal executes or invalidates

Performance Note: Computationally expensive due to linefill objects. Disable or reduce layers if chart performance degrades.

2. Population Fitness Ribbon (Optional, Default: ON)

Histogram showing fitness distribution across active strategies:

Activation: Only draws on last bar (barstate.islast) to avoid historical clutter

Visual Construction:

10 histogram layers by default (configurable 5-20)

Plots 50 bars back from current bar

Positioned below price at: lowest_low(100) - 1.5×ATR (doesn't interfere with price action)

Each layer represents a fitness threshold (evenly spaced min to max fitness)

Layer Logic:

For layer_num from 0 to ribbon_layers:

Fitness_threshold = min_fitness + (max_fitness - min_fitness) × (layer / layers)

Count strategies with fitness ≥ threshold

Height = ATR × 0.15 × (count / total_active)

Y_position = base_level + ATR × 0.2 × layer

Color = Gradient from weak to strong based on layer position

Line_width = Scaled by height (taller = thicker)

Visual Feedback:

Tall, bright ribbon = healthy population, many fit strategies at high fitness levels

Short, dim ribbon = weak population, few strategies achieving good fitness

Ribbon compression (layers close together) = population converging to similar fitness

Ribbon spread = diverse fitness range, active selection pressure

Use Case: Quick visual health check without opening dashboard. Ribbon growing upward over time = population improving.

3. Confidence Halo (Optional, Default: ON)

Circular polyline around entry signals showing probability strength:

Activation: Draws when new position opens (shadow_position changes from 0 to ±1)

Visual Construction:

20-segment polyline forming approximate circle

Center: Low - 0.5×ATR (long) or High + 0.5×ATR (short)

Radius: 0.3×ATR (low confidence) to 1.0×ATR (elite confidence)

Scales with: (probability - min_probability) / (1.0 - min_probability)

Color Coding:

Elite (85%+): Cyan (theme.conf_elite), large radius, minimal transparency (40%)

Strong (75-85%): Strong green (theme.conf_strong), medium radius, moderate transparency (50%)

Good (65-75%): Good green (theme.conf_good), smaller radius, more transparent (60%)

Moderate (<65%): Moderate green (theme.conf_moderate), tiny radius, very transparent (70%)

Technical Detail:

Uses chart.point array with index-based positioning

5-bar horizontal spread for circular appearance (±5 bars from entry)

Curved=false (Pine Script polyline limitation)

Fill color matches line color but more transparent (88% vs line's transparency)

Purpose: Instant visual probability assessment. No need to check dashboard - halo size/brightness tells the story.

4. Evolution Event Markers (Optional, Default: ON)

Visual indicators of genetic algorithm activity:

Spawn Markers (Diamond, Cyan):

Plots when total_spawned increases on current bar

Location: bottom of chart (location.bottom)

Color: theme.spawn_marker (cyan/bright blue)

Size: tiny

Indicates new strategy just entered population

Cull Markers (X-Cross, Red):

Plots when total_culled increases on current bar

Location: bottom of chart (location.bottom)

Color: theme.cull_marker (red/pink)

Size: tiny

Indicates weak strategy just removed from population

What It Tells You:

Frequent spawning early = population building, active exploration

Frequent culling early = high selection pressure, weak strategies dying fast

Balanced spawn/cull = healthy evolutionary churn

No markers for long periods = stable population (evolution plateaued or optimal genes found)

5. Entry/Exit Markers

Clear visual signals for selected strategy's trades:

Long Entry (Triangle Up, Green):

Plots when selected strategy opens long position (position changes 0 → +1)

Location: below bar (location.belowbar)

Color: theme.long_primary (green/cyan depending on theme)

Transparency: Scales with probability:

Elite (85%+): 0% (fully opaque)

Strong (75-85%): 10%

Good (65-75%): 20%

Acceptable (55-65%): 35%

Size: small

Short Entry (Triangle Down, Red):

Plots when selected strategy opens short position (position changes 0 → -1)

Location: above bar (location.abovebar)

Color: theme.short_primary (red/pink depending on theme)

Transparency: Same scaling as long entries

Size: small

Exit (X-Cross, Orange):

Plots when selected strategy closes position (position changes ±1 → 0)

Location: absolute (at actual exit price if stop/target lines enabled)

Color: theme.exit_color (orange/yellow depending on theme)

Transparency: 0% (fully opaque)

Size: tiny

Result: Clean, probability-scaled markers that don't clutter chart but convey essential information.

6. Stop Loss & Take Profit Lines (Optional, Default: ON)

Visual representation of shadow portfolio risk levels:

Stop Loss Line:

Plots when selected strategy has active position

Level: shadow_stop value from selected strategy

Color: theme.short_primary with 60% transparency (red/pink, subtle)

Width: 2

Style: plot.style_linebr (breaks when no position)

Take Profit Line:

Plots when selected strategy has active position

Level: shadow_target value from selected strategy

Color: theme.long_primary with 60% transparency (green, subtle)

Width: 2

Style: plot.style_linebr (breaks when no position)

Purpose:

Shows where shadow portfolio would exit for stop/target

Helps visualize strategy's risk/reward ratio

Useful for manual traders to set similar levels

Disable for cleaner chart (recommended for presentations)

7. Dynamic Trend EMA

Gradient-colored trend line that visualizes trend strength:

Calculation:

EMA(close, trend_length) - default 50 period (configurable 20-100)

Slope calculated over 10 bars: (current_ema - ema ) / ema × 100

Color Logic:

Trend_direction:

Slope > 0.1% = Bullish (1)

Slope < -0.1% = Bearish (-1)

Otherwise = Neutral (0)

Trend_strength = abs(slope)

Color = Gradient between:

- Neutral color (gray/purple)

- Strong bullish (bright green) if direction = 1

- Strong bearish (bright red) if direction = -1

Gradient factor = trend_strength (0 to 1+ scale)

Visual Behavior:

Faint gray/purple = weak/no trend (choppy conditions)

Light green/red = emerging trend (low strength)

Bright green/red = strong trend (high conviction)

Color intensity = trend strength magnitude

Transparency: 50% (subtle, doesn't overpower price action)

Purpose: Subconscious awareness of trend state without checking dashboard or indicators.

8. Regime Background Tinting (Subtle)

Ultra-low opacity background color indicating detected market regime:

Regime Detection:

Efficiency = directional_movement / total_range (over trend_length bars)

Vol_ratio = current_volatility / average_volatility

IF (efficiency > 0.5 AND vol_ratio < 1.3):

Regime = Trending (1)

ELSE IF (vol_ratio > 1.5):

Regime = Volatile (2)

ELSE:

Regime = Choppy (0)

Background Colors:

Trending: theme.regime_trending (dark green, 92-93% transparency)

Volatile: theme.regime_volatile (dark red, 93% transparency)

Choppy: No tint (normal background)

Purpose:

Subliminal regime awareness

Helps explain why signals are/aren't generating

Trending = ideal conditions for AGE

Volatile = fewer signals, higher thresholds applied

Choppy = mixed signals, lower confidence

Important: Extremely subtle by design. Not meant to be obvious, just subconscious context.

📊 ENHANCED DASHBOARD

Comprehensive real-time metrics in single organized panel (top-right position):

Dashboard Structure (5 columns × 14 rows)

Header Row:

Column 0: "🧬 AGE PRO" + phase indicator (🔴 LIVE or ⏪ HIST)

Column 1: "POPULATION"

Column 2: "PERFORMANCE"

Column 3: "CURRENT SIGNAL"

Column 4: "ACTIVE STRATEGY"

Column 0: Market State

Regime (📈 TREND / 🌊 CHAOS / ➖ CHOP)

DVS Ratio (current volatility scaling factor, format: #.##)

Trend Direction (▲ BULL / ▼ BEAR / ➖ FLAT with color coding)

Trend Strength (0-100 scale, format: #.##)

Column 1: Population Metrics

Active strategies (count / max_population)

Validated strategies (WFO passed / active total)

Current generation number

Total spawned (all-time strategy births)

Total culled (all-time strategy deaths)

Column 2: Aggregate Performance

Total trades across all active strategies

Aggregate win rate (%) - color-coded:

Green (>55%)

Orange (45-55%)

Red (<45%)

Total P&L in R-multiples - color-coded by positive/negative

Best fitness score in population (format: #.###)

MAS - Minimum Adaptation Score (cull threshold, format: #.###)

Column 3: Current Signal Status

Status indicator:

"▲ LONG" (green) if selected strategy in long position

"▼ SHORT" (red) if selected strategy in short position

"⏳ FORMING" (orange) if signal persisting but not yet executed

"○ WAITING" (gray) if no active signal

Confidence percentage (0-100%, format: #.#%)

Quality assessment:

"🔥 ELITE" (cyan) for 85%+ probability

"✓ STRONG" (bright green) for 75-85%

"○ GOOD" (green) for 65-75%

"- LOW" (dim) for <65%

Confluence score (X/3 format)

Signal age:

"X bars" if signal forming

"IN TRADE" if position active

"---" if no signal

Column 4: Selected Strategy Details

Strategy ID number (#X format)

Validation status:

"✓ VAL" (green) if WFO validated

"○ TRAIN" (orange) if still in training/testing phase

Generation number (GX format)

Personal fitness score (format: #.### with color coding)

Trade count

P&L and win rate (format: #.#R (##%) with color coding)

Color Scheme:

Panel background: theme.panel_bg (dark, low opacity)

Panel headers: theme.panel_header (slightly lighter)

Primary text: theme.text_primary (bright, high contrast)

Secondary text: theme.text_secondary (dim, lower contrast)

Positive metrics: theme.metric_positive (green)

Warning metrics: theme.metric_warning (orange)

Negative metrics: theme.metric_negative (red)

Special markers: theme.validated_marker, theme.spawn_marker

Update Frequency: Only on barstate.islast (current bar) to minimize CPU usage

Purpose:

Quick overview of entire system state

No need to check multiple indicators

Trading decisions informed by population health, regime state, and signal quality

Transparency into what AGE is thinking

🔍 DIAGNOSTICS PANEL (Optional, Default: OFF)

Detailed signal quality tracking for optimization and debugging:

Panel Structure (3 columns × 8 rows)

Position: Bottom-right corner (doesn't interfere with main dashboard)

Header Row:

Column 0: "🔍 DIAGNOSTICS"

Column 1: "COUNT"

Column 2: "%"

Metrics Tracked (for selected strategy only):

Total Evaluated:

Every signal that passed initial calculation (direction ≠ 0)

Represents total opportunities considered

✓ Passed:

Signals that passed quality gate and executed

Green color coding

Percentage of evaluated signals

Rejection Breakdown:

⨯ Probability:

Rejected because probability < minimum threshold

Most common rejection reason typically

⨯ Confluence:

Rejected because confluence < minimum required (e.g., only 1 of 3 indicators agreed)

⨯ Trend:

Rejected because signal opposed strong trend

Indicates counter-trend protection working

⨯ Regime:

Rejected because volatile regime detected and probability wasn't high enough to override

Shows regime filter in action

⨯ Volume:

Rejected because volume < 70% of 20-bar average

Indicates volume confirmation requirement

Color Coding:

Passed count: Green (success metric)

Rejection counts: Red (failure metrics)

Percentages: Gray (neutral, informational)

Performance Cost: Slight CPU overhead for tracking counters. Disable when not actively optimizing settings.

How to Use Diagnostics

Scenario 1: Too Few Signals

Evaluated: 200

Passed: 10 (5%)

⨯ Probability: 120 (60%)

⨯ Confluence: 40 (20%)

⨯ Others: 30 (15%)

Diagnosis: Probability threshold too high for this strategy's DNA.

Solution: Lower min probability from 65% to 60%, or allow strategy more time to evolve better DNA.

Scenario 2: Too Many False Signals

Evaluated: 200

Passed: 80 (40%)

Strategy win rate: 45%

Diagnosis: Quality gate too loose, letting low-quality signals through.

Solution: Raise min probability to 70%, or increase min confluence to 3 (all indicators must agree).

Scenario 3: Regime-Specific Issues

⨯ Regime: 90 (45% of rejections)

Diagnosis: Frequent volatile regime detection blocking otherwise good signals.

Solution: Either accept fewer trades during chaos (recommended), or disable regime filter if you want signals regardless of market state.

Optimization Workflow:

Enable diagnostics

Run 200+ bars

Analyze rejection patterns

Adjust settings based on data

Re-run and compare pass rate

Disable diagnostics when satisfied

⚙️ CONFIGURATION GUIDE

🧬 Evolution Engine Settings

Enable AGE Evolution (Default: ON):

ON: Full genetic algorithm (recommended for best results)

OFF: Uses only 4 seed strategies, no spawning/culling (static population for comparison testing)

Max Population (4-12, Default: 8):

Higher = more diversity, more exploration, slower performance

Lower = faster computation, less exploration, risk of premature convergence

Sweet spot: 6-8 for most use cases

4 = minimum for meaningful evolution

12 = maximum before diminishing returns

Min Population (2-4, Default: 3):

Safety floor - system never culls below this count

Prevents population extinction during harsh selection

Should be at least half of max population

Elite Preservation (1-3, Default: 2):

Top N performers completely immune to culling

Ensures best genes always survive

1 = minimal protection, aggressive selection

2 = balanced (recommended)

3 = conservative, slower gene pool turnover

Historical: Spawn Interval (10-100, Default: 30):

Bars between spawning new strategies during historical data

Lower = faster evolution, more exploration

Higher = slower evolution, more evaluation time per strategy

30 bars = ~1-2 hours on 15min chart

Historical: Cull Interval (20-200, Default: 60):

Bars between culling weak strategies during historical data

Should be 2x spawn interval for balanced churn

Lower = aggressive selection pressure

Higher = patient evaluation

Live: Spawn Interval (100-500, Default: 200):

Bars between spawning during live trading

Much slower than historical for stability

Prevents population chaos during live trading

200 bars = ~1.5 trading days on 15min chart

Live: Cull Interval (200-1000, Default: 400):

Bars between culling during live trading

Should be 2x live spawn interval

Conservative removal during live trading

Historical: Mutation Rate (0.05-0.40, Default: 0.20):

Probability each gene mutates during breeding (20% = 2 out of 10 genes on average)

Higher = more exploration, slower convergence

Lower = more exploitation, faster convergence but risk of local optima

20% balances exploration vs exploitation

Live: Mutation Rate (0.02-0.20, Default: 0.08):

Mutation rate during live trading

Much lower for stability (don't want population to suddenly degrade)

8% = mostly inherits parent genes with small tweaks

Mutation Strength (0.05-0.25, Default: 0.12):

How much genes change when mutated (% of gene's total range)

0.05 = tiny nudges (fine-tuning)

0.12 = moderate jumps (recommended)

0.25 = large leaps (aggressive exploration)

Example: If gene range is 0.5-2.0, 12% strength = ±0.18 possible change

📈 Signal Quality Settings

Min Signal Probability (0.55-0.80, Default: 0.65):

Quality gate threshold - signals below this never generate

0.55-0.60 = More signals, accept lower confidence (higher risk)

0.65 = Institutional-grade balance (recommended)

0.70-0.75 = Fewer but higher-quality signals (conservative)

0.80+ = Very selective, very few signals (ultra-conservative)

Min Confluence Score (1-3, Default: 2):

Required indicator agreement before signal generates

1 = Any single indicator can trigger (not recommended - too many false signals)

2 = Requires 2 of 3 indicators agree (RECOMMENDED for balance)

3 = All 3 must agree (very selective, few signals, high quality)

Base Persistence Bars (1-5, Default: 2):

Base bars signal must persist before entry

System adapts automatically:

High probability signals (75%+) enter 1 bar faster

Low probability signals (<68%) need 1 bar more

Trending regime: -1 bar (faster entries)

Volatile regime: +1 bar (more confirmation)

1 = Immediate entry after quality gate (responsive but prone to whipsaw)

2 = Balanced confirmation (recommended)

3-5 = Patient confirmation (slower but more reliable)

Cooldown After Trade (3-20, Default: 8):

Bars to wait after exit before next entry allowed

Prevents overtrading and revenge trading

3 = Minimal cooldown (active trading)

8 = Balanced (recommended)

15-20 = Conservative (position trading)

Entropy Length (10-50, Default: 20):

Lookback period for market order/disorder calculation

Lower = more responsive to regime changes (noisy)

Higher = more stable regime detection (laggy)

20 = works across most timeframes

Momentum Length (5-30, Default: 14):

Period for RSI/ROC calculations

14 = standard (RSI default)

Lower = more signals, less reliable

Higher = fewer signals, more reliable

Structure Length (20-100, Default: 50):

Lookback for support/resistance swing range

20 = short-term swings (day trading)

50 = medium-term structure (recommended)

100 = major structure (position trading)

Trend EMA Length (20-100, Default: 50):

EMA period for trend detection and direction bias

20 = short-term trend (responsive)

50 = medium-term trend (recommended)

100 = long-term trend (position trading)

ATR Period (5-30, Default: 14):

Period for volatility measurement

14 = standard ATR

Lower = more responsive to vol changes

Higher = smoother vol calculation

📊 Volatility Scaling (DVS) Settings

Enable DVS (Default: ON):

Dynamic volatility scaling for adaptive stop/target placement

Highly recommended to leave ON

OFF only for testing fixed-distance stops

DVS Method (Default: Ensemble):

ATR Ratio: Simple, fast, single-method (good for beginners)

Parkinson: High-low range based (good for intraday)

Garman-Klass: OHLC based (sophisticated, considers gaps)

Ensemble: Median of all three (RECOMMENDED - most robust)

DVS Memory (20-200, Default: 100):

Lookback for baseline volatility comparison

20 = very responsive to vol changes (can overreact)

100 = balanced adaptation (recommended)

200 = slow, stable baseline (minimizes false vol signals)

DVS Sensitivity (0.3-1.5, Default: 0.7):

How much volatility affects scaling (power-law exponent)

0.3 = Conservative, heavily dampens vol impact (cube root)

0.5 = Moderate dampening (square root)

0.7 = Balanced response (recommended)

1.0 = Linear, full 1:1 vol response

1.5 = Aggressive, amplified response (exponential)

🔬 Walk-Forward Optimization Settings

Enable WFO (Default: ON):

Out-of-sample validation to prevent overfitting

Highly recommended to leave ON

OFF only for testing or if you want unvalidated strategies

Training Window (100-500, Default: 250):

Bars for in-sample optimization

100 = fast validation, less data (risky)

250 = balanced (recommended) - about 1-2 months on daily, 1-2 weeks on 15min

500 = patient validation, more data (conservative)

Testing Window (30-200, Default: 75):

Bars for out-of-sample validation

Should be ~30% of training window

30 = minimal test (fast validation)

75 = balanced (recommended)

200 = extensive test (very conservative)

Min Trades for Validation (3-15, Default: 5):

Required trades in BOTH training AND testing periods

3 = minimal sample (risky, fast validation)

5 = balanced (recommended)

10+ = conservative (slow validation, high confidence)

WFO Efficiency Threshold (0.3-0.9, Default: 0.55):

Minimum test/train performance ratio required

0.30 = Very loose (test must be 30% as good as training)

0.55 = Balanced (recommended) - test must be 55% as good

0.70+ = Strict (test must closely match training)

Higher = fewer validated strategies, lower risk of overfitting

🎨 Premium Visuals Settings

Visual Theme:

Neon Genesis: Cyberpunk aesthetic (cyan/magenta/purple)

Carbon Fiber: Industrial look (blue/red/gray)

Quantum Blue: Quantum computing (blue/purple/pink)

Aurora: Northern lights (teal/orange/purple)

⚡ Gradient Probability Cloud (Default: ON):

Multi-layer gradient showing signal buildup

Turn OFF if chart lags or for cleaner look

Cloud Gradient Layers (3-15, Default: 7):

More layers = smoother gradient, more CPU intensive

Fewer layers = faster, blockier appearance

🎗️ Population Fitness Ribbon (Default: ON):

Histogram showing fitness distribution

Turn OFF for cleaner chart

Ribbon Layers (5-20, Default: 10):

More layers = finer fitness detail

Fewer layers = simpler histogram

⭕ Signal Confidence Halo (Default: ON):

Circular indicator around entry signals

Size/brightness scales with probability

Minimal performance cost

🔬 Evolution Event Markers (Default: ON):

Diamond (spawn) and X (cull) markers

Shows genetic algorithm activity

Minimal performance cost

🎯 Stop/Target Lines (Default: ON):

Shows shadow portfolio stop/target levels

Turn OFF for cleaner chart (recommended for screenshots/presentations)

📊 Enhanced Dashboard (Default: ON):

Comprehensive metrics panel

Should stay ON unless you want zero overlays

🔍 Diagnostics Panel (Default: OFF):

Detailed signal rejection tracking

Turn ON when optimizing settings

Turn OFF during normal use (slight performance cost)

📈 USAGE WORKFLOW - HOW TO USE THIS INDICATOR

Phase 1: Initial Setup & Learning

Add AGE to your chart

Recommended timeframes: 15min, 30min, 1H (best signal-to-noise ratio)

Works on: 5min (day trading), 4H (swing trading), Daily (position trading)

Load 1000+ bars for sufficient evolution history

Let the population evolve (100+ bars minimum)

First 50 bars: Random exploration, poor results expected

Bars 50-150: Population converging, fitness improving

Bars 150+: Stable performance, validated strategies emerging

Watch the dashboard metrics

Population should grow toward max capacity

Generation number should advance regularly

Validated strategies counter should increase

Best fitness should trend upward toward 0.50-0.70 range

Observe evolution markers

Diamond markers (cyan) = new strategies spawning

X markers (red) = weak strategies being culled

Frequent early activity = healthy evolution

Activity slowing = population stabilizing

Be patient. Evolution takes time. Don't judge performance before 150+ bars.

Phase 2: Signal Observation

Watch signals form

Gradient cloud builds up 2-3 bars before entry

Cloud brightness = probability strength

Cloud thickness = signal persistence

Check signal quality

Look at confidence halo size when entry marker appears

Large bright halo = elite setup (85%+)

Medium halo = strong setup (75-85%)

Small halo = good setup (65-75%)

Verify market conditions

Check trend EMA color (green = uptrend, red = downtrend, gray = choppy)

Check background tint (green = trending, red = volatile, clear = choppy)

Trending background + aligned signal = ideal conditions

Review dashboard signal status

Current Signal column shows:

Status (Long/Short/Forming/Waiting)

Confidence % (actual probability value)

Quality assessment (Elite/Strong/Good)

Confluence score (2/3 or 3/3 preferred)

Only signals meeting ALL quality gates appear on chart. If you're not seeing signals, population is either still learning or market conditions aren't suitable.

Phase 3: Manual Trading Execution

When Long Signal Fires:

Verify confidence level (dashboard or halo size)

Confirm trend alignment (EMA sloping up, green color)

Check regime (preferably trending or choppy, avoid volatile)

Enter long manually on your broker platform

Set stop loss at displayed stop line level (if lines enabled), or use your own risk management

Set take profit at displayed target line level, or trail manually

Monitor position - exit if X marker appears (signal reversal)

When Short Signal Fires:

Same verification process

Confirm downtrend (EMA sloping down, red color)

Enter short manually

Use displayed stop/target levels or your own

AGE tells you WHEN and HOW CONFIDENT. You decide WHETHER and HOW MUCH.

Phase 4: Set Up Alerts (Never Miss a Signal)

Right-click on indicator name in legend

Select "Add Alert"

Choose condition:

"AGE Long" = Long entry signal fired

"AGE Short" = Short entry signal fired

"AGE Exit" = Position reversal/exit signal

Set notification method:

Sound alert (popup on chart)

Email notification

Webhook to phone/trading platform

Mobile app push notification

Name the alert (e.g., "AGE BTCUSD 15min Long")

Save alert

Recommended: Set alerts for both long and short, enable mobile push notifications. You'll get alerted in real-time even if not watching charts.

Phase 5: Monitor Population Health

Weekly Review:

Check dashboard Population column:

Active count should be near max (6-8 of 8)

Validated count should be >50% of active

Generation should be advancing (1-2 per week typical)

Check dashboard Performance column:

Aggregate win rate should be >50% (target: 55-65%)

Total P&L should be positive (may fluctuate)

Best fitness should be >0.50 (target: 0.55-0.70)

MAS should be declining slowly (normal adaptation)

Check Active Strategy column:

Selected strategy should be validated (✓ VAL)

Personal fitness should match best fitness

Trade count should be accumulating

Win rate should be >50%

Warning Signs:

Zero validated strategies after 300+ bars = settings too strict or market unsuitable

Best fitness stuck <0.30 = population struggling, consider parameter adjustment

No spawning/culling for 200+ bars = evolution stalled (may be optimal or need reset)

Aggregate win rate <45% sustained = system not working on this instrument/timeframe

Health Check Pass:

50%+ strategies validated

Best fitness >0.50

Aggregate win rate >52%

Regular spawn/cull activity

Selected strategy validated

Phase 6: Optimization (If Needed)

Enable Diagnostics Panel (bottom-right) for data-driven tuning:

Problem: Too Few Signals

Evaluated: 200

Passed: 8 (4%)

⨯ Probability: 140 (70%)

Solutions:

Lower min probability: 65% → 60% or 55%

Reduce min confluence: 2 → 1

Lower base persistence: 2 → 1

Increase mutation rate temporarily to explore new genes

Check if regime filter is blocking signals (⨯ Regime high?)

Problem: Too Many False Signals

Evaluated: 200

Passed: 90 (45%)

Win rate: 42%

Solutions:

Raise min probability: 65% → 70% or 75%

Increase min confluence: 2 → 3

Raise base persistence: 2 → 3

Enable WFO if disabled (validates strategies before use)

Check if volume filter is being ignored (⨯ Volume low?)

Problem: Counter-Trend Losses

⨯ Trend: 5 (only 5% rejected)

Losses often occur against trend

Solutions:

System should already filter trend opposition

May need stronger trend requirement

Consider only taking signals aligned with higher timeframe trend

Use longer trend EMA (50 → 100)

Problem: Volatile Market Whipsaws

⨯ Regime: 100 (50% rejected by volatile regime)

Still getting stopped out frequently

Solutions:

System is correctly blocking volatile signals

Losses happening because vol filter isn't strict enough

Consider not trading during volatile periods (respect the regime)

Or disable regime filter and accept higher risk

Optimization Workflow:

Enable diagnostics

Run 200+ bars with current settings

Analyze rejection patterns and win rate

Make ONE change at a time (scientific method)

Re-run 200+ bars and compare results

Keep change if improvement, revert if worse

Disable diagnostics when satisfied

Never change multiple parameters at once - you won't know what worked.

Phase 7: Multi-Instrument Deployment

AGE learns independently on each chart:

Recommended Strategy:

Deploy AGE on 3-5 different instruments

Different asset classes ideal (e.g., ES futures, EURUSD, BTCUSD, SPY, Gold)

Each learns optimal strategies for that instrument's personality

Take signals from all 5 charts

Natural diversification reduces overall risk

Why This Works:

When one market is choppy, others may be trending

Different instruments respond to different news/catalysts

Portfolio-level win rate more stable than single-instrument

Evolution explores different parameter spaces on each chart

Setup:

Same settings across all charts (or customize if preferred)

Set alerts for all

Take every validated signal across all instruments

Position size based on total account (don't overleverage any single signal)

⚠️ REALISTIC EXPECTATIONS - CRITICAL READING

What AGE Can Do

✅ Generate probability-weighted signals using genetic algorithms

✅ Evolve strategies in real-time through natural selection

✅ Validate strategies on out-of-sample data (walk-forward optimization)

✅ Adapt to changing market conditions automatically over time

✅ Provide comprehensive metrics on population health and signal quality

✅ Work on any instrument, any timeframe, any broker

✅ Improve over time as weak strategies are culled and fit strategies breed

What AGE Cannot Do

❌ Win every trade (typical win rate: 55-65% at best)

❌ Predict the future with certainty (markets are probabilistic, not deterministic)

❌ Work perfectly from bar 1 (needs 100-150 bars to learn and stabilize)

❌ Guarantee profits under all market conditions

❌ Replace your trading discipline and risk management

❌ Execute trades automatically (this is an indicator, not a strategy)

❌ Prevent all losses (drawdowns are normal and expected)

❌ Adapt instantly to regime changes (re-learning takes 50-100 bars)

Performance Realities

Typical Performance After Evolution Stabilizes (150+ bars):

Win Rate: 55-65% (excellent for trend-following systems)

Profit Factor: 1.5-2.5 (realistic for validated strategies)

Signal Frequency: 5-15 signals per 100 bars (quality over quantity)

Drawdown Periods: 20-40% of time in equity retracement (normal trading reality)

Max Consecutive Losses: 5-8 losses possible even with 60% win rate (probability says this is normal)

Evolution Timeline:

Bars 0-50: Random exploration, learning phase - poor results expected, don't judge yet

Bars 50-150: Population converging, fitness climbing - results improving

Bars 150-300: Stable performance, most strategies validated - consistent results

Bars 300+: Mature population, optimal genes dominant - best results

Market Condition Dependency:

Trending Markets: AGE excels - clear directional moves, high-probability setups

Choppy Markets: AGE struggles - fewer signals generated, lower win rate

Volatile Markets: AGE cautious - higher rejection rate, wider stops, fewer trades

Market Regime Changes:

When market shifts from trending to choppy overnight

Validated strategies can become temporarily invalidated

AGE will adapt through evolution, but not instantly

Expect 50-100 bar re-learning period after major regime shifts

Fitness may temporarily drop then recover

This is NOT a holy grail. It's a sophisticated signal generator that learns and adapts using genetic algorithms. Your success depends on:

Patience during learning periods (don't abandon after 3 losses)

Proper position sizing (risk 0.5-2% per trade, not 10%)

Following signals consistently (cherry-picking defeats statistical edge)

Not abandoning system prematurely (give it 200+ bars minimum)

Understanding probability (60% win rate means 40% of trades WILL lose)

Respecting market conditions (trending = trade more, choppy = trade less)

Managing emotions (AGE is emotionless, you need to be too)

Expected Drawdowns:

Single-strategy max DD: 10-20% of equity (normal)

Portfolio across multiple instruments: 5-15% (diversification helps)

Losing streaks: 3-5 consecutive losses expected periodically

No indicator eliminates risk. AGE manages risk through:

Quality gates (rejecting low-probability signals)

Confluence requirements (multi-indicator confirmation)

Persistence requirements (no knee-jerk reactions)

Regime awareness (reduced trading in chaos)

Walk-forward validation (preventing overfitting)

But it cannot prevent all losses. That's inherent to trading.

🔧 TECHNICAL SPECIFICATIONS

Platform: TradingView Pine Script v5

Indicator Type: Overlay indicator (plots on price chart)

Execution Type: Signals only - no automatic order placement

Computational Load:

Moderate to High (genetic algorithms + shadow portfolios)

8 strategies × shadow portfolio simulation = significant computation

Premium visuals add additional load (gradient cloud, fitness ribbon)

TradingView Resource Limits (Built-in Caps):

Max Bars Back: 500 (sufficient for WFO and evolution)

Max Labels: 100 (plenty for entry/exit markers)

Max Lines: 150 (adequate for stop/target lines)

Max Boxes: 50 (not heavily used)

Max Polylines: 100 (confidence halos)

Recommended Chart Settings:

Timeframe: 15min to 1H (optimal signal/noise balance)

5min: Works but noisier, more signals

4H/Daily: Works but fewer signals

Bars Loaded: 1000+ (ensures sufficient evolution history)

Replay Mode: Excellent for testing without risk

Performance Optimization Tips:

Disable gradient cloud if chart lags (most CPU intensive visual)

Disable fitness ribbon if still laggy

Reduce cloud layers from 7 to 3

Reduce ribbon layers from 10 to 5

Turn off diagnostics panel unless actively tuning

Close other heavy indicators to free resources

Browser/Platform Compatibility:

Works on all modern browsers (Chrome, Firefox, Safari, Edge)

Mobile app supported (full functionality on phone/tablet)

Desktop app supported (best performance)

Web version supported (may be slower on older computers)

Data Requirements:

Real-time or delayed data both work

No special data feeds required

Works with TradingView's standard data

Historical + live data seamlessly integrated

🎓 THEORETICAL FOUNDATIONS

AGE synthesizes advanced concepts from multiple disciplines:

Evolutionary Computation

Genetic Algorithms (Holland, 1975): Population-based optimization through natural selection metaphor

Tournament Selection: Fitness-based parent selection with diversity preservation

Crossover Operators: Fitness-weighted gene recombination from two parents

Mutation Operators: Random gene perturbation for exploration of new parameter space

Elitism: Preservation of top N performers to prevent loss of best solutions

Adaptive Parameters: Different mutation rates for historical vs. live phases

Technical Analysis

Support/Resistance: Price structure within swing ranges

Trend Following: EMA-based directional bias

Momentum Analysis: RSI, ROC, MACD composite indicators

Volatility Analysis: ATR-based risk scaling

Volume Confirmation: Trade activity validation

Information Theory

Shannon Entropy (1948): Quantification of market order vs. disorder

Signal-to-Noise Ratio: Directional information vs. random walk

Information Content: How much "information" a price move contains

Statistics & Probability

Walk-Forward Analysis: Rolling in-sample/out-of-sample optimization

Out-of-Sample Validation: Testing on unseen data to prevent overfitting

Monte Carlo Principles: Shadow portfolio simulation with realistic execution

Expectancy Theory: Win rate × avg win - loss rate × avg loss

Probability Distributions: Signal confidence quantification

Risk Management

ATR-Based Stops: Volatility-normalized risk per trade

Volatility Regime Detection: Market state classification (trending/choppy/volatile)

Drawdown Control: Peak-to-trough equity measurement

R-Multiple Normalization: Performance measurement in risk units

Machine Learning Concepts

Online Learning: Continuous adaptation as new data arrives

Fitness Functions: Multi-objective optimization (win rate + expectancy + drawdown)

Exploration vs. Exploitation: Balance between trying new strategies and using proven ones

Overfitting Prevention: Walk-forward validation as regularization

Novel Contribution:

AGE is the first TradingView indicator to apply genetic algorithms to real-time indicator parameter optimization while maintaining strict anti-overfitting controls through walk-forward validation.

Most "adaptive" indicators simply recalibrate lookback periods or thresholds. AGE evolves entirely new strategies through competitive selection - it's not parameter tuning, it's Darwinian evolution of trading logic itself.

The combination of:

Genetic algorithm population management

Shadow portfolio simulation for realistic fitness evaluation

Walk-forward validation to prevent overfitting

Multi-indicator confluence for signal quality

Dynamic volatility scaling for adaptive risk

...creates a system that genuinely learns and improves over time while avoiding the curse of curve-fitting that plagues most optimization approaches.

🏗️ DEVELOPMENT NOTES

This project represents months of intensive development, facing significant technical challenges:

Challenge 1: Making Genetics Actually Work

Early versions spawned garbage strategies that polluted the gene pool:

Random gene combinations produced nonsensical parameter sets

Weak strategies survived too long, dragging down population

No clear convergence toward optimal solutions

Solution:

Comprehensive fitness scoring (4 factors: win rate, P&L, expectancy, drawdown)

Elite preservation (top 2 always protected)

Walk-forward validation (unproven strategies penalized 30%)

Tournament selection (fitness-weighted breeding)

Adaptive culling (MAS decay creates increasing selection pressure)

Challenge 2: Balancing Evolution Speed vs. Stability

Too fast = population chaos, no convergence. Too slow = can't adapt to regime changes.

Solution:

Dual-phase timing: Fast evolution during historical (30/60 bar intervals), slow during live (200/400 bar intervals)

Adaptive mutation rates: 20% historical, 8% live

Spawn/cull ratio: Always 2:1 to prevent population collapse

Challenge 3: Shadow Portfolio Accuracy

Needed realistic trade simulation without lookahead bias:

Can't peek at future bars for exits

Must track multiple portfolios simultaneously

Stop/target checks must use bar's high/low correctly

Solution:

Entry on close (realistic)

Exit checks on current bar's high/low (realistic)

Independent position tracking per strategy

Cooldown periods to prevent unrealistic rapid re-entry

ATR-normalized P&L (R-multiples) for fair comparison across volatility regimes

Challenge 4: Pine Script Compilation Limits

Hit TradingView's execution limits multiple times:

Too many array operations

Too many variables

Too complex conditional logic

Solution:

Optimized data structures (single DNA array instead of 8 separate arrays)

Minimal visual overlays (only essential plots)

Efficient fitness calculations (vectorized where possible)

Strategic use of barstate.islast to minimize dashboard updates

Challenge 5: Walk-Forward Implementation

Standard WFO is difficult in Pine Script:

Can't easily "roll forward" through historical data

Can't re-optimize strategies mid-stream

Must work in real-time streaming environment

Solution:

Age-based phase detection (first 250 bars = training, next 75 = testing)

Separate metric tracking for train vs. test

Efficiency calculation at fixed interval (after test period completes)

Validation flag persists for strategy lifetime

Challenge 6: Signal Quality Control

Early versions generated too many signals with poor win rates:

Single indicators produced excessive noise

No trend alignment

No regime awareness

Instant entries on single-bar spikes

Solution:

Three-layer confluence system (entropy + momentum + structure)

Minimum 2-of-3 agreement requirement

Trend alignment checks (penalty for counter-trend)

Regime-based probability adjustments

Persistence requirements (signals must hold multiple bars)

Volume confirmation

Quality gate (probability + confluence thresholds)

The Result

A system that:

Truly evolves (not just parameter sweeps)

Truly validates (out-of-sample testing)

Truly adapts (ongoing competition and breeding)

Stays within TradingView's platform constraints

Provides institutional-quality signals

Maintains transparency (full metrics dashboard)

Development time: 3+ months of iterative refinement

Lines of code: ~1500 (highly optimized)

Test instruments: ES, NQ, EURUSD, BTCUSD, SPY, AAPL

Test timeframes: 5min, 15min, 1H, Daily

🎯 FINAL WORDS

The Adaptive Genesis Engine is not just another indicator - it's a living system that learns, adapts, and improves through the same principles that drive biological evolution. Every bar it observes adds to its experience. Every strategy it spawns explores new parameter combinations. Every strategy it culls removes weakness from the gene pool.

This is evolution in action on your charts.

You're not getting a static formula locked in time. You're getting a system that thinks , that competes , that survives through natural selection. The strongest strategies rise to the top. The weakest die. The gene pool improves generation after generation.

AGE doesn't claim to predict the future - it adapts to whatever the future brings. When markets shift from trending to choppy, from calm to volatile, from bullish to bearish - AGE evolves new strategies suited to the new regime.

Use it on any instrument. Any timeframe. Any market condition. AGE will adapt.

This indicator gives you the pure signal intelligence. How you choose to act on it - position sizing, risk management, execution discipline - that's your responsibility. AGE tells you when and how confident . You decide whether and how much .

Trust the process. Respect the evolution. Let Darwin work.

"In markets, as in nature, it is not the strongest strategies that survive, nor the most intelligent - but those most responsive to change."

Taking you to school. — Dskyz, Trade with insight. Trade with anticipation.

— Happy Holiday's

Luxy Sector & Industry RS AnalyzerEver wonder why some stocks soar while others in the same sector barely move? Or why your perfectly timed entry still loses money? Possibly the answer can be found in Relative Strength.

The Luxy Sector & Industry RS Analyzer solves a critical problem that most traders overlook: picking strong stocks in strong sectors AND strong industries . It's not enough for a stock to go up - you want stocks that are crushing their competition at both the sector AND industry level. This indicator does the heavy lifting by automatically comparing your stock against its sector ETF, industry ETF, the broader market, sector leader, and industry leader, giving you a complete multi-level picture of relative performance.

What makes this different?

- Automatic sector AND industry detection - no manual setup required

- Multi-level hierarchy analysis: Market → Sector → Industry → Stock

- Multi-timeframe analysis (1 month to 1 year) in one glance

- Industry ETF mapping (30+ industries covered)

- Clear 0-100 scoring system with letter grades (A+ to F)

- Works on stocks, crypto, forex, and commodities

- Real-time updates with anti-repaint protection

Think of it as your performance dashboard - instantly showing you if you're trading a champion or a laggard at every level of the market hierarchy.

METHODOLOGY & ATTRIBUTION

This indicator is based on classical Relative Strength (RS) analysis principles from technical analysis. RS methodology compares an asset's price performance against a benchmark to identify relative outperformance or underperformance. This concept has been used by professional traders and institutions for decades.

Key Concepts Used:

Relative Strength (RS) - Classical technical analysis concept measuring comparative performance

Multi-Level Hierarchy Analysis - Market → Sector → Industry → Stock comparison

Sector Rotation Analysis - Identifying which sectors are leading or lagging the market

Industry Rotation Analysis - Identifying which industries are leading within their sectors

Multi-period Performance Analysis - Evaluating strength across multiple timeframes

Beta Calculation - Standard statistical measure of volatility relative to a benchmark

DISCLAIMER: This indicator is for educational and informational purposes only. It should not be considered financial advice or a recommendation to buy or sell. Past performance does not guarantee future results. Trading involves risk and may not be suitable for all investors. Always do your own research and consult with a financial advisor before making investment decisions.

with all rows visible - capture when stock has strong RS score (70+) so users can see what a "good" setup looks like]

WHAT THE INDICATOR SHOWS

1. AUTOMATIC ASSET TYPE DETECTION

The indicator automatically identifies what you're analyzing and adjusts accordingly:

Stocks - Compares to sector ETF (XLK, XLF, XLV, etc.) and SPY

Crypto - Compares to Total Crypto Market Cap and Bitcoin

Forex - Compares to relevant currency index (DXY, EXY, etc.)

Commodities - Compares to Gold (GLD) as benchmark

Indices - Compares to broader market indices

How it works: The indicator reads your chart's asset type and ticker, then automatically maps it to the correct sector or benchmark. For stocks, it uses intelligent sector detection (looking at the sector field) to match you with the right sector ETF. For example:

- Technology stocks get compared to XLK (Technology Select Sector SPDR)

- Financial stocks get compared to XLF (Financial Select Sector SPDR)

- Healthcare stocks get compared to XLV (Health Care Select Sector SPDR)

This happens instantly when you add the indicator to any chart - no configuration needed.

2. SECTOR & MARKET BENCHMARKS

What is a Sector ETF?

A sector ETF is an exchange-traded fund that tracks a specific industry group. For example, XLK contains all major technology companies. By comparing your stock to its sector ETF, you can see if your stock is outperforming or underperforming its peers.