Yelober_Momentum_BreadthMI# Yelober_Momentum_BreadthMI: Market Breadth Indicator Analysis

## Overview

The Yelober_Momentum_BreadthMI is a comprehensive market breadth indicator designed to monitor market internals across NYSE and NASDAQ exchanges. It tracks several key metrics including up/down volume ratios, TICK readings, and trend momentum to provide traders with real-time insights into market direction, strength, and potential turning points.

## Indicator Components

This indicator displays a table with data for:

- NYSE breadth metrics

- NASDAQ breadth metrics

- NYSE TICK data and trends

- NASDAQ TICK (TICKQ) data and trends

## Table Columns and Interpretation

### Column 1: Market

Identifies the data source:

- **NYSE**: New York Stock Exchange data

- **NASDAQ**: NASDAQ exchange data

- **Tick**: NYSE TICK index

- **TickQ**: NASDAQ TICK index

### Column 2: Ratio

Shows the current ratio values with different calculations depending on the row:

- **For NYSE/NASDAQ rows**: Displays the up/down volume ratio

- Positive values (green): More up volume than down volume

- Negative values (red): More down volume than up volume

- The magnitude indicates the strength of the imbalance

- **For Tick/TickQ rows**: Shows the ratio of positive to negative ticks plus the current TICK reading in parentheses

- Format: "Ratio (Current TICK value)"

- Positive values (green): More stocks ticking up than down

- Negative values (red): More stocks ticking down than up

### Column 3: Trend

Displays the directional trend with both a symbol and value:

- **For NYSE/NASDAQ rows**: Shows the VOLD (volume difference) slope

- "↗": Rising trend (positive slope)

- "↘": Falling trend (negative slope)

- "→": Neutral/flat trend (minimal slope)

- **For Tick/TickQ rows**: Shows the slope of the ratio history

- Color-coding: Green for positive momentum, Red for negative momentum, Gray for neutral

The trend column is particularly important as it shows the current momentum of the market. The indicator applies specific thresholds for color-coding:

- NYSE: Green when normalized value > 2, Red when < -2

- NASDAQ: Green when normalized value > 3.5, Red when < -3.5

- TICK/TICKQ: Green when slope > 0.01, Red when slope < -0.01

## How to Use This Indicator

### Basic Interpretation

1. **Market Direction**: When multiple rows show green ratios and upward trends, it suggests strong bullish market internals. Conversely, red ratios and downward trends indicate bearish internals.

2. **Market Breadth**: The magnitude of the ratios indicates how broad-based the market movement is. Higher absolute values suggest stronger market breadth.

3. **Momentum Shifts**: When trend arrows change direction or colors shift, it may signal a potential reversal or change in market momentum.

4. **Divergences**: Look for divergences between different markets (NYSE vs NASDAQ) or between ratios and trends, which can indicate potential market turning points.

### Advanced Usage

- **Volume Normalization**: The indicator includes options to normalize volume data (none, tens, thousands, millions, 10th millions) to handle different exchange scales.

- **Trend Averaging**: The slope calculation uses an averaging period (default: 5) to smooth out noise and identify more reliable trend signals.

## Examples for Interpretation

### Example 1: Strong Bullish Market

```

| Market | Ratio | Trend |

|--------|---------|-----------|

| NYSE | 1.75 | ↗ 2.85 |

| NASDAQ | 2.10 | ↗ 4.12 |

| Tick | 2.45 (485) | ↗ 0.05 |

| TickQ | 1.95 (320) | ↗ 0.03 |

```

**Interpretation**: All metrics are positive and trending upward (green), indicating a strong, broad-based rally. The high ratio values show significant bullish dominance. This suggests continuation of the upward move with good momentum.

### Example 2: Weakening Market

```

| Market | Ratio | Trend |

|--------|---------|-----------|

| NYSE | 0.45 | ↘ -1.50 |

| NASDAQ | 0.85 | → 0.30 |

| Tick | 0.95 (105) | ↘ -0.02 |

| TickQ | 1.20 (160) | → 0.00 |

```

**Interpretation**: The market is showing mixed signals with positive but low ratios, while NYSE and TICK trends are turning negative. NASDAQ shows neutral to slightly positive momentum. This divergence often occurs near market tops or during consolidation phases. Traders should be cautious and consider reducing position sizes.

### Example 3: Negative Market Turning Positive

```

| Market | Ratio | Trend |

|--------|---------|-----------|

| NYSE | -1.25 | ↗ 1.75 |

| NASDAQ | -0.95 | ↗ 2.80 |

| Tick | -1.35 (-250) | ↗ 0.04 |

| TickQ | -1.10 (-180) | ↗ 0.02 |

```

**Interpretation**: This is a potential bottoming pattern. Current ratios are still negative (red) showing overall negative breadth, but the trends are all positive (green arrows), indicating improving momentum. This divergence often occurs at market bottoms and could signal an upcoming reversal. Look for confirmation with price action before establishing long positions.

### Example 4: Mixed Market with Divergence

```

| Market | Ratio | Trend |

|--------|---------|-----------|

| NYSE | 1.45 | ↘ -2.25 |

| NASDAQ | -0.85 | ↘ -3.80 |

| Tick | 1.20 (230) | ↘ -0.03 |

| TickQ | -0.75 (-120) | ↘ -0.02 |

```

**Interpretation**: There's a significant divergence between NYSE (positive ratio) and NASDAQ (negative ratio), while all trends are negative. This suggests sector rotation or a market that's weakening but with certain segments still showing strength. Often seen during late-stage bull markets or in transitions between leadership groups. Consider reducing risk exposure and focusing on relative strength sectors.

## Practical Trading Applications

1. **Confirmation Tool**: Use this indicator to confirm price movements. Strong breadth readings in the direction of the price trend increase confidence in trade decisions.

2. **Early Warning System**: Watch for divergences between price and breadth metrics, which often precede market turns.

3. **Intraday Trading**: The real-time nature of TICK and volume data makes this indicator valuable for day traders to gauge intraday momentum shifts.

4. **Market Regime Identification**: Sustained readings can help identify whether the market is in a trend or chop regime, allowing for appropriate strategy selection.

This breadth indicator is most effective when used in conjunction with price action and other technical indicators rather than in isolation.

"新泻天鹅vs川崎前锋" için komut dosyalarını ara

Trend Flow Trail [AlgoAlpha]OVERVIEW

This script overlays a custom hybrid indicator called the Money Flow Trail which combines a volatility-based trend-following trail with a volume-weighted momentum oscillator. It’s built around two core components: the AlphaTrail—a dynamic band system influenced by Hull MA and volatility—and a smoothed Money Flow Index (MFI) that provides insights into buying or selling pressure. Together, these tools are used to color bars, generate potential reversal markers, and assist traders in identifying trend continuation or exhaustion phases in any market or timeframe.

CONCEPTS

The AlphaTrail calculates a volatility-adjusted channel around price using the Hull Moving Average as the base and an EMA of range as the spread. It adaptively shifts based on price interaction to capture trend reversals while avoiding whipsaws. The direction (bullish or bearish) determines both the band being tracked and how the trail locks in. The Money Flow Index (MFI) is derived from hlc3 and volume, measuring buying vs selling pressure, and is further smoothed with a short Hull MA to reduce noise while preserving structure. These two systems work in tandem: AlphaTrail governs directional context, while MFI refines the timing.

FEATURES

Dynamic AlphaTrail line with regime switching logic that controls directional bias and bar coloring.

Smoothed MFI with gradient coloring to visually communicate pressure and exhaustion levels.

Overbought/oversold thresholds (80/20), mid-level (50), and custom extreme zones (90/10) for deeper signal granularity.

Built-in take-profit signal logic: crossover of MFI into overbought with bullish AlphaTrail, or into oversold with bearish AlphaTrail.

Visual fills between price and AlphaTrail for clearer confirmation during trend phases.

Alerts for regime shifts, MFI crossovers, trail interactions, and bar color regime changes.

USAGE

Add the indicator to any chart. Use the AlphaTrail plot to define trend context: bullish (trailing below price) or bearish (trailing above). MFI values give supporting confirmation—favor long setups when MFI is rising and above 50 in a bullish regime, and shorts when MFI is falling and below 50 in a bearish regime. The colored fills help visually track strength; sharp changes in MFI crossing 80/20 or 90/10 zones often precede pullbacks or reversals. Use the plotted circles as optional take-profit signals when MFI and trend are extended. Adjust AlphaTrail length/multiplier and MFI smoothing to better match the asset’s volatility profile.

Path of Least ResistancePath of Least Resistance (PLR)

Concept Overview

The Path of Least Resistance indicator identifies key zones on your chart that act like "muddy" or "sticky" areas where price tends to get bogged down, creating choppy and unpredictable price action. Between these zones lie the "empty spaces" - clear paths where price can move freely with momentum and direction.

The Analogy: Muddy Fields vs Open Roads

Think of your chart like a landscape:

🟫 ZONES (Muddy/Sticky Areas)

Fair Value Gaps (FVGs) from higher timeframes

Pivot wick zones from higher timeframe pivots

Areas where price gets "stuck" and churns

Like walking through thick mud - slow, choppy, unpredictable movement

Price action becomes erratic and difficult to trade

🟢 EMPTY SPACES (Open Roads)

The clear areas between zones

Where price can move freely with momentum

Like driving on an open highway - smooth, directional movement

The "Path of Least Resistance" for price movement

Trading Philosophy

AVOID Trading Within Zones:

Price action is typically choppy and unpredictable

Higher probability of false signals and whipsaws

Like trying to drive through mud - you'll get stuck

TRADE Through the Empty Spaces:

Look for moves that travel between zones

Price tends to move with momentum and direction

Higher probability setups with cleaner price action

Like taking the highway instead of back roads

Zone Types Detected

Fair Value Gaps (FVGs)

Imbalances from higher timeframe candles

Areas where price "owes" a return visit

Often act as magnets, creating choppy price action

Pivot Wick Zones

Upper and lower wicks from higher timeframe pivots

Rejection areas where price previously struggled

Often create resistance/support that leads to choppy movement

Color Coding System

The zones dynamically change color based on current price position:

🔴 RED ZONES : Price is below the zone (bearish context)

🟢 GREEN ZONES : Price is above the zone (bullish context)

🔘 GRAY ZONES : Price is within the zone (neutral/choppy area)

The "Mum Trades" Strategy

The best trades - what we call "Mum trades" (trades so obvious even your mum could spot them) - happen in the empty spaces between zones:

✅ High Probability Characteristics:

Clear directional movement between zones

Less noise and false signals

Higher momentum and follow-through

Cleaner technical patterns

❌ Avoid These Areas:

Trading within the muddy zones

Expecting clean moves through sticky areas

Fighting against the natural flow of price

Key Features

Auto Timeframe Detection : Automatically selects appropriate higher timeframe

Dynamic Zone Management : Overlapping zones are automatically cleaned up

Real-time Alerts : Get notified when price enters/exits zones

Visual Clarity : Clean zone display with extending boundaries

How to Use

Identify the Zones : Let the indicator mark the muddy areas

Find the Paths : Look for clear spaces between zones

Plan Your Trades : Target moves that travel through empty space

Avoid the Mud : Stay away from trading within the zones

Follow the Flow : Trade with the path of least resistance

Remember

Price, like water, always seeks the path of least resistance. By identifying where that path is clear (empty spaces) versus where it's obstructed (zones), you can align your trading with the natural flow of the market rather than fighting against it.

The goal is simple: Trade the highways, avoid the mud.

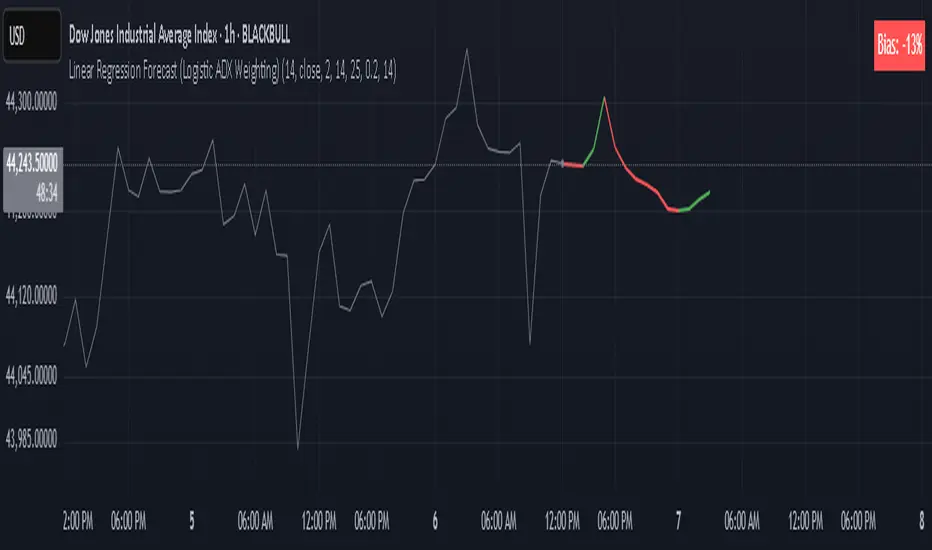

Linear Regression Forecast (ADX Adaptive)Linear Regression Forecast (ADX Adaptive)

This indicator is a dynamic price projection tool that combines multiple linear regression forecasts into a single, adaptive forecast curve. By integrating trend strength via the ADX and directional bias, it aims to visualize how price might evolve in different market environments—from strong trends to mean-reverting conditions.

Core Concept:

This tool builds forward price projections based on a blend of linear regression models with varying lookback lengths (from 2 up to a user-defined max). It then adjusts those projections using two key mechanisms:

ADX-Weighted Forecast Blending

In trending conditions (high ADX), the model follows the raw forecast direction. In ranging markets (low ADX), the forecast flips or reverts, biasing toward mean-reversion. A logistic transformation of directional bias, controlled by a steepness parameter, determines how aggressively this blending reacts to price behavior.

Volatility Scaling

The forecast’s magnitude is scaled based on ADX and directional conviction. When trends are unclear (low ADX or neutral bias), the projection range expands to reflect greater uncertainty and volatility.

How It Works:

Regression Curve Generation

For each regression length from 2 to maxLength, a forward projection is calculated using least-squares linear regression on the selected price source. These forecasts are extrapolated into the future.

Directional Bias Calculation

The forecasted points are analyzed to determine a normalized bias value in the range -1 to +1, where +1 means strongly bullish, -1 means strongly bearish, and 0 means neutral.

Logistic Bias Transformation

The raw bias is passed through a logistic sigmoid function, with a user-defined steepness. This creates a probability-like weight that favors either following or reversing the forecast depending on market context.

ADX-Based Weighting

ADX determines the weighting between trend-following and mean-reversion modes. Below ADX 20, the model favors mean-reversion. Above 25, it favors trend-following. Between 20 and 25, it linearly blends the two.

Blended Forecast Curve

Each forecast point is blended between trend-following and mean-reverting values, scaled for volatility.

What You See:

Forecast Lines: Projected future price paths drawn in green or red depending on direction.

Bias Plot: A separate plot showing post-blend directional bias as a percentage, where +100 is strongly bullish and -100 is strongly bearish.

Neutral Line: A dashed horizontal line at 0 percent bias to indicate neutrality.

User Inputs:

-Max Regression Length

-Price Source

-Line Width

-Bias Steepness

-ADX Length and Smoothing

Use Cases:

Visualize expected price direction under different trend conditions

Adjust trading behavior depending on trending vs ranging markets

Combine with other tools for deeper analysis

Important Notes:

This indicator is for visualization and analysis only. It does not provide buy or sell signals and should not be used in isolation. It makes assumptions based on historical price action and should be interpreted with market context.

Disguised Candles by The School of Dalal StreetDisguised Candles corrects one of the subtle visual distortions present in normal candlestick charts — the mismatch between the close of one candle and the open of the next.

On many instruments (especially at day/session breaks), the next candle’s open often jumps due to price gaps or data feed behavior. This can make reading the flow of price action harder than necessary.

Disguised Candles fixes this by plotting synthetic candles where the open of each candle is forced to match the close of the previous one — creating a visually continuous flow of price.

Real candles are made fully transparent, so only the "corrected" candles are visible.

This allows traders to:

Visualize price flow as a smooth path

Better spot true directional shifts and trends

Avoid distractions caused by technical gaps that are not meaningful to their strategy

🚀 Pure visual clarity. No noise from false opens.

How it works:

The open of each synthetic candle = close of previous real candle

High, Low, Close remain unchanged

Colors are based on Close vs Corrected Open

Real chart candles are hidden under a transparent overlay

Use this as a clean canvas for trend analysis or as a foundation for building new visual systems.

CDP - Counter-Directional-Pivot🎯 CDP - Counter-Directional-Pivot

📊 Overview

The Counter-Directional-Pivot (CDP) indicator calculates five critical price levels based on the previous day's OHLC data, specifically designed for multi-timeframe analysis. Unlike standard pivot points, CDP levels are calculated using a unique formula that identifies potential reversal zones where price action often changes direction.

⚡ What Makes This Script Original

This implementation solves several technical challenges that existing pivot indicators face:

🔄 Multi-Timeframe Consistency: Values remain identical across all timeframes (1m, 5m, 1h, daily) - a common problem with many pivot implementations

🔒 Intraday Stability: Uses advanced value-locking technology to prevent the "stepping" effect that occurs when pivot lines shift during the trading session

💪 Robust Data Handling: Optimized for both liquid and illiquid stocks with enhanced data synchronization

🧮 CDP Calculation Formula

The indicator calculates five key levels using the previous day's High (H), Low (L), and Close (C):

CDP = (H + L + C) ÷ 3 (Central Decision Point)

AH = 2×CDP + H – 2×L (Anchor High - Strong Resistance)

NH = 2×CDP – L (Near High - Moderate Resistance)

AL = 2×CDP – 2×H + L (Anchor Low - Strong Support)

NL = 2×CDP – H (Near Low - Moderate Support)

✨ Key Features

🎨 Visual Elements

📈 Five Distinct Price Levels: Each with customizable colors and line styles

🏷️ Smart Label System: Shows exact price values for each level

📋 Optional Value Table: Displays all levels in an organized table format

🎯 Clean Chart Display: Minimal visual clutter while maximizing information

⚙️ Technical Advantages

🔐 Session-Locked Values: Prices are locked at market open, preventing intraday shifts

🔄 Multi-Timeframe Sync: Perfect consistency between daily and intraday charts

✅ Data Validation: Built-in checks ensure reliable calculations

🚀 Performance Optimized: Efficient code structure for fast loading

💼 Trading Applications

🔄 Reversal Zones: AH and AL often act as strong turning points

💥 Breakout Confirmation: Price movement beyond these levels signals trend continuation

🛡️ Risk Management: Use levels for stop-loss and take-profit placement

🏗️ Market Structure: Understand daily ranges and potential price targets

📚 How to Use

🚀 Basic Setup

Add the indicator to your chart (works on any timeframe)

Customize colors for easy identification of support/resistance zones

Enable the value table for quick reference of exact price levels

📈 Trading Strategy Examples

🟢 Long Bias: Look for bounces at NL or AL levels

🔴 Short Bias: Watch for rejections at NH or AH levels

💥 Breakout Trading: Enter positions when price decisively breaks through anchor levels

↔️ Range Trading: Use CDP as the central reference point for range-bound markets

🎯 Advanced Strategy Combinations

RSI Integration for Enhanced Signals: 📊

📉 Oversold Bounces: Combine RSI below 30 with price touching AL/NL levels for high-probability long entries

📈 Overbought Rejections: Look for RSI above 70 with price rejecting AH/NH levels for short opportunities

🔍 Divergence Confirmation: When RSI shows bullish divergence at support levels (AL/NL) or bearish divergence at resistance levels (AH/NH), it often signals stronger reversal potential

⚡ Momentum Confluence: RSI crossing 50 while price breaks through CDP can confirm trend direction changes

⚙️ Configuration Options

🎨 Line Customization: Adjust width, style (solid/dashed/dotted), and colors

👁️ Display Preferences: Toggle individual levels, labels, and value table

📍 Table Position: Place the value table anywhere on your chart

🔔 Alert System: Get notifications when price crosses key levels

🔧 Technical Implementation Details

🎯 Data Reliability

The script uses request.security() with lookahead settings to ensure historical accuracy while maintaining real-time functionality. The value-locking mechanism prevents the common issue where pivot levels shift during the trading day.

🔄 Multi-Timeframe Logic

⏰ Intraday Charts: Display previous day's calculated levels as stable horizontal lines

📅 Daily Charts: Show current day's levels based on yesterday's OHLC

🔍 Consistency Check: All timeframes reference the same source data

🤔 Why CDP vs Standard Pivots?

Counter-Directional Pivots often provide more accurate reversal points than traditional pivot calculations because they incorporate the relationship between high/low ranges and closing prices more effectively. The formula creates levels that better reflect market psychology and institutional trading behaviors.

💡 Best Practices

💧 Use on liquid markets for most reliable results

📊 RSI Combination: Add RSI indicator for overbought/oversold confirmation and divergence analysis

📊 Combine with volume analysis for confirmation

🔍 Consider multiple timeframe analysis (daily levels on hourly charts)

📝 Test thoroughly in paper trading before live implementation

💪 Example Market Applications

NASDAQ:AAPL AAPL - Tech stock breakouts through AH levels

$NYSE:SPY SPY - Index trading with CDP range analysis

NASDAQ:TSLA TSLA - Volatile stock reversals at AL/NL levels

⚠️ This indicator is designed for educational and analytical purposes. Always combine with proper risk management and additional technical analysis tools.

StatMetricsLibrary "StatMetrics"

A utility library for common statistical indicators and ratios used in technical analysis.

Includes Z-Score, correlation, PLF, SRI, Sharpe, Sortino, Omega ratios, and normalization tools.

zscore(src, len)

Calculates the Z-score of a series

Parameters:

src (float) : The input price or series (e.g., close)

len (simple int) : The lookback period for mean and standard deviation

Returns: Z-score: number of standard deviations the input is from the mean

corr(x, y, len)

Computes Pearson correlation coefficient between two series

Parameters:

x (float) : First series

y (float) : Second series

len (simple int) : Lookback period

Returns: Correlation coefficient between -1 and 1

plf(src, longLen, shortLen, smoothLen)

Calculates the Price Lag Factor (PLF) as the difference between long and short Z-scores, normalized and smoothed

Parameters:

src (float) : Source series (e.g., close)

longLen (simple int) : Long Z-score period

shortLen (simple int) : Short Z-score period

smoothLen (simple int) : Hull MA smoothing length

Returns: Smoothed and normalized PLF oscillator

sri(signal, len)

Computes the Statistical Reliability Index (SRI) based on trend persistence

Parameters:

signal (float) : A price or signal series (e.g., smoothed PLF)

len (simple int) : Lookback period for smoothing and deviation

Returns: Normalized trend reliability score

sharpe(src, len)

Calculates the Sharpe Ratio over a period

Parameters:

src (float) : Price series (e.g., close)

len (simple int) : Lookback period

Returns: Sharpe ratio value

sortino(src, len)

Calculates the Sortino Ratio over a period, using only downside volatility

Parameters:

src (float) : Price series

len (simple int) : Lookback period

Returns: Sortino ratio value

omega(src, len)

Calculates the Omega Ratio as the ratio of upside to downside return area

Parameters:

src (float) : Price series

len (simple int) : Lookback period

Returns: Omega ratio value

beta(asset, benchmark, len)

Calculates beta coefficient of asset vs benchmark using rolling covariance

Parameters:

asset (float) : Series of the asset (e.g., close)

benchmark (float) : Series of the benchmark (e.g., SPX close)

len (simple int) : Lookback window

Returns: Beta value (slope of linear regression)

alpha(asset, benchmark, len)

Calculates rolling alpha of an asset relative to a benchmark

Parameters:

asset (float) : Series of the asset (e.g., close)

benchmark (float) : Series of the benchmark (e.g., SPX close)

len (simple int) : Lookback window

Returns: Alpha value (excess return not explained by Beta exposure)

skew(x, len)

Computes skewness of a return series

Parameters:

x (float) : Input series (e.g., returns)

len (simple int) : Lookback period

Returns: Skewness value

kurtosis(x, len)

Computes kurtosis of a return series

Parameters:

x (float) : Input series (e.g., returns)

len (simple int) : Lookback period

Returns: Kurtosis value

cv(x, len)

Calculates Coefficient of Variation

Parameters:

x (float) : Input series (e.g., returns or prices)

len (simple int) : Lookback period

Returns: CV value

autocorr(x, len)

Calculates autocorrelation with 1-lag

Parameters:

x (float) : Series to test

len (simple int) : Lookback window

Returns: Autocorrelation at lag 1

stderr(x, len)

Calculates rolling standard error of a series

Parameters:

x (float) : Input series

len (simple int) : Lookback window

Returns: Standard error (std dev / sqrt(n))

info_ratio(asset, benchmark, len)

Calculates the Information Ratio

Parameters:

asset (float) : Asset price series

benchmark (float) : Benchmark price series

len (simple int) : Lookback period

Returns: Information ratio (alpha / tracking error)

tracking_error(asset, benchmark, len)

Measures deviation from benchmark (Tracking Error)

Parameters:

asset (float) : Asset return series

benchmark (float) : Benchmark return series

len (simple int) : Lookback window

Returns: Tracking error value

max_drawdown(x, len)

Computes maximum drawdown over a rolling window

Parameters:

x (float) : Price series

len (simple int) : Lookback window

Returns: Rolling max drawdown percentage (as a negative value)

zscore_signal(z, ob, os)

Converts Z-score into a 3-level signal

Parameters:

z (float) : Z-score series

ob (float) : Overbought threshold

os (float) : Oversold threshold

Returns: -1, 0, or 1 depending on signal state

r_squared(x, y, len)

Calculates rolling R-squared (coefficient of determination)

Parameters:

x (float) : Asset returns

y (float) : Benchmark returns

len (simple int) : Lookback window

Returns: R-squared value (0 to 1)

entropy(x, len)

Approximates Shannon entropy using log returns

Parameters:

x (float) : Price series

len (simple int) : Lookback period

Returns: Approximate entropy

zreversal(z)

Detects Z-score reversals to the mean

Parameters:

z (float) : Z-score series

Returns: +1 on upward reversal, -1 on downward

momentum_rank(x, len)

Calculates relative momentum strength

Parameters:

x (float) : Price series

len (simple int) : Lookback window

Returns: Proportion of lookback where current price is higher

normalize(x, len)

Normalizes a series to a 0–1 range over a period

Parameters:

x (float) : The input series

len (simple int) : Lookback period

Returns: Normalized value between 0 and 1

composite_score(score1, score2, score3)

Combines multiple normalized scores into a composite score

Parameters:

score1 (float)

score2 (float)

score3 (float)

Returns: Average composite score

GStrategy 1000Pepe 15mTrend Following Candlestick Strategy with EMA Filter and Exit Delay

Strategy Concept

This strategy combines candlestick patterns with EMA trend filtering to identify high-probability trade entries, featuring:

Entry Signals: Hammer and Engulfing patterns confirmed by EMA trend

Trend Filter: Fast EMA (20) vs Slow EMA (50) crossover system

Risk Management: 5% stop-loss + 1% trailing stop

Smart Exit: 2-bar delay after exit signals to avoid whipsaws

Key Components

Trend Identification:

Uptrend: Fast EMA > Slow EMA AND rising

Downtrend: Fast EMA < Slow EMA AND falling

Entry Conditions:

pinescript

// Bullish Entry (Long)

longCondition = (Hammer OR Bullish Engulfing)

AND Uptrend

AND no existing position

// Bearish Entry (Short)

shortCondition = Bearish Engulfing

AND Downtrend

AND no existing position

Exit Mechanics:

Primary Exit: EMA crossover (Fast crosses Slow)

Delayed Execution: Waits 2 full candles after signal

Emergency Exits:

5% fixed stop-loss

1% trailing stop

Visual Dashboard:

Colored EMA lines (Blue=Fast, Red=Slow)

Annotated candlestick patterns

Background highlighting for signals

Distinct markers for entries/exits

Unique Features

Pattern Recognition:

Enhanced Hammer detection (strict body/wick ratios)

Multi-candle engulfing confirmation

Trend-Confirmation:

Requires price and EMA alignment

Filters counter-trend patterns

Exit Optimization:

pinescript

// Delay implementation

if exit_signal_triggered

counter := 2 // Start countdown

else if counter > 0

counter -= 1 // Decrement each bar

exit_trade = (counter == 1) // Execute on final bar

Risk Parameters

Parameter Value Description

Stop Loss 5% Fixed risk per trade

Trailing Stop 1% Locks in profits

Exit Delay 2 bars Reduces false exits

Position Size 100% No pyramiding

Visualization Examples

🟢 Green Triangle: Bullish entry

🔴 Red Triangle: Bearish entry

⬇️ Blue X: Long exit (after delay)

⬆️ Green X: Short exit (after delay)

🎯 Pattern Labels: Identifies hammer/engulfing

Recommended Use

Timeframes: 1H-4H (reduces noise)

Markets: Trend-prone assets (FX, indices)

Best Conditions: Strong trending markets

Avoid: Choppy/Ranging markets

Candle Range % vs 8-Candle AvgCandle % Indicator – Measure Candle Strength by Range %

**Overview:**

The *Candle % Indicator* helps traders visually and analytically gauge the strength or significance of a price candle relative to its recent historical context. This is particularly useful for detecting breakout moves, volatility shifts, or overextended candles that may signal exhaustion.

**What It Does:**

* Calculates the **percentage range** of the current candle compared to the **average range of the past N candles**.

* Highlights candles that exceed a user-defined threshold (e.g., 150% of the average range).

* Useful for **filtering out extreme candles** that might represent anomalies or unsustainable moves.

* Can be combined with other strategies (like EMA crossovers, support/resistance breaks, etc.) to improve signal quality.

**Use Case Examples:**

***Filter out fakeouts** in breakout strategies by ignoring candles that are overly large and may revert.

***Volatility control**: Avoid entries when market conditions are erratic.

**Confluence**: Combine with EMA or RSI signals for refined entries.

**How to Read:**

* If a candle is larger than the average range by more than the set percentage (default 150%), it's flagged (e.g., no entry signal or optional visual marker).

* Ideal for intraday, swing, or algorithmic trading setups.

**Customizable Inputs:**

**Lookback Period**: Number of previous candles to calculate the average range.

**% Threshold**: Maximum percentage a candle can exceed the average before being filtered or marked.

Liquidity Engulfing (Nephew_Sam_)🔥 Liquidity Engulfing Multi-Timeframe Detector

This indicator finds engulfing bars which have swept liquidity from its previous candle. You can use it across 6 timeframes with fibonacci entries.

⚡ Key Features

6 Customizable Timeframes - Complete market structure analysis

Smart Liquidity Detection - Finds patterns that sweep liquidity then reverse

Real-Time Status Table - Confirmed vs unconfirmed patterns with color coding

Fibonacci Integration - 5 customizable fib levels for precise entries

HTF → LTF Strategy - Spot reversals on higher timeframes, enter on lower timeframe fibs

📈 Engulfing Rules

Bullish: Current candle bullish + previous bearish + current low < previous low + current close > previous open

Bearish: Current candle bearish + previous bullish + current high > previous high + current close < previous open

Langlands-Operadic Möbius Vortex (LOMV)Langlands-Operadic Möbius Vortex (LOMV)

Where Pure Mathematics Meets Market Reality

A Revolutionary Synthesis of Number Theory, Category Theory, and Market Dynamics

🎓 THEORETICAL FOUNDATION

The Langlands-Operadic Möbius Vortex represents a groundbreaking fusion of three profound mathematical frameworks that have never before been combined for market analysis:

The Langlands Program: Harmonic Analysis in Markets

Developed by Robert Langlands (Fields Medal recipient), the Langlands Program creates bridges between number theory, algebraic geometry, and harmonic analysis. In our indicator:

L-Function Implementation:

- Utilizes the Möbius function μ(n) for weighted price analysis

- Applies Riemann zeta function convergence principles

- Calculates quantum harmonic resonance between -2 and +2

- Measures deep mathematical patterns invisible to traditional analysis

The L-Function core calculation employs:

L_sum = Σ(return_val × μ(n) × n^(-s))

Where s is the critical strip parameter (0.5-2.5), controlling mathematical precision and signal smoothness.

Operadic Composition Theory: Multi-Strategy Democracy

Category theory and operads provide the mathematical framework for composing multiple trading strategies into a unified signal. This isn't simple averaging - it's mathematical composition using:

Strategy Composition Arity (2-5 strategies):

- Momentum analysis via RSI transformation

- Mean reversion through Bollinger Band mathematics

- Order Flow Polarity Index (revolutionary T3-smoothed volume analysis)

- Trend detection using Directional Movement

- Higher timeframe momentum confirmation

Agreement Threshold System: Democratic voting where strategies must reach consensus before signal generation. This prevents false signals during market uncertainty.

Möbius Function: Number Theory in Action

The Möbius function μ(n) forms the mathematical backbone:

- μ(n) = 1 if n is a square-free positive integer with even number of prime factors

- μ(n) = -1 if n is a square-free positive integer with odd number of prime factors

- μ(n) = 0 if n has a squared prime factor

This creates oscillating weights that reveal hidden market periodicities and harmonic structures.

🔧 COMPREHENSIVE INPUT SYSTEM

Langlands Program Parameters

Modular Level N (5-50, default 30):

Primary lookback for quantum harmonic analysis. Optimized by timeframe:

- Scalping (1-5min): 15-25

- Day Trading (15min-1H): 25-35

- Swing Trading (4H-1D): 35-50

- Asset-specific: Crypto 15-25, Stocks 30-40, Forex 35-45

L-Function Critical Strip (0.5-2.5, default 1.5):

Controls Riemann zeta convergence precision:

- Higher values: More stable, smoother signals

- Lower values: More reactive, catches quick moves

- High frequency: 0.8-1.2, Medium: 1.3-1.7, Low: 1.8-2.3

Frobenius Trace Period (5-50, default 21):

Galois representation lookback for price-volume correlation:

- Measures harmonic relationships in market flows

- Scalping: 8-15, Day Trading: 18-25, Swing: 25-40

HTF Multi-Scale Analysis:

Higher timeframe context prevents trading against major trends:

- Provides market bias and filters signals

- Improves win rates by 15-25% through trend alignment

Operadic Composition Parameters

Strategy Composition Arity (2-5, default 4):

Number of algorithms composed for final signal:

- Conservative: 4-5 strategies (higher confidence)

- Moderate: 3-4 strategies (balanced approach)

- Aggressive: 2-3 strategies (more frequent signals)

Category Agreement Threshold (2-5, default 3):

Democratic voting minimum for signal generation:

- Higher agreement: Fewer but higher quality signals

- Lower agreement: More signals, potential false positives

Swiss-Cheese Mixing (0.1-0.5, default 0.382):

Golden ratio φ⁻¹ based blending of trend factors:

- 0.382 is φ⁻¹, optimal for natural market fractals

- Higher values: Stronger trend following

- Lower values: More contrarian signals

OFPI Configuration:

- OFPI Length (5-30, default 14): Order Flow calculation period

- T3 Smoothing (3-10, default 5): Advanced exponential smoothing

- T3 Volume Factor (0.5-1.0, default 0.7): Smoothing aggressiveness control

Unified Scoring System

Component Weights (sum ≈ 1.0):

- L-Function Weight (0.1-0.5, default 0.3): Mathematical harmony emphasis

- Galois Rank Weight (0.1-0.5, default 0.2): Market structure complexity

- Operadic Weight (0.1-0.5, default 0.3): Multi-strategy consensus

- Correspondence Weight (0.1-0.5, default 0.2): Theory-practice alignment

Signal Threshold (0.5-10.0, default 5.0):

Quality filter producing:

- 8.0+: EXCEPTIONAL signals only

- 6.0-7.9: STRONG signals

- 4.0-5.9: MODERATE signals

- 2.0-3.9: WEAK signals

🎨 ADVANCED VISUAL SYSTEM

Multi-Dimensional Quantum Aura Bands

Five-layer resonance field showing market energy:

- Colors: Theme-matched gradients (Quantum purple, Holographic cyan, etc.)

- Expansion: Dynamic based on score intensity and volatility

- Function: Multi-timeframe support/resistance zones

Morphism Flow Portals

Category theory visualization showing market topology:

- Green/Cyan Portals: Bullish mathematical flow

- Red/Orange Portals: Bearish mathematical flow

- Size/Intensity: Proportional to signal strength

- Recursion Depth (1-8): Nested patterns for flow evolution

Fractal Grid System

Dynamic support/resistance with projected L-Scores:

- Multiple Timeframes: 10, 20, 30, 40, 50-period highs/lows

- Smart Spacing: Prevents level overlap using ATR-based minimum distance

- Projections: Estimated signal scores when price reaches levels

- Usage: Precise entry/exit timing with mathematical confirmation

Wick Pressure Analysis

Rejection level prediction using candle mathematics:

- Upper Wicks: Selling pressure zones (purple/red lines)

- Lower Wicks: Buying pressure zones (purple/green lines)

- Glow Intensity (1-8): Visual emphasis and line reach

- Application: Confluence with fractal grid creates high-probability zones

Regime Intensity Heatmap

Background coloring showing market energy:

- Black/Dark: Low activity, range-bound markets

- Purple Glow: Building momentum and trend development

- Bright Purple: High activity, strong directional moves

- Calculation: Combines trend, momentum, volatility, and score intensity

Six Professional Themes

- Quantum: Purple/violet for general trading and mathematical focus

- Holographic: Cyan/magenta optimized for cryptocurrency markets

- Crystalline: Blue/turquoise for conservative, stability-focused trading

- Plasma: Gold/magenta for high-energy volatility trading

- Cosmic Neon: Bright neon colors for maximum visibility and aggressive trading

📊 INSTITUTIONAL-GRADE DASHBOARD

Unified AI Score Section

- Total Score (-10 to +10): Primary decision metric

- >5: Strong bullish signals

- <-5: Strong bearish signals

- Quality ratings: EXCEPTIONAL > STRONG > MODERATE > WEAK

- Component Analysis: Individual L-Function, Galois, Operadic, and Correspondence contributions

Order Flow Analysis

Revolutionary OFPI integration:

- OFPI Value (-100% to +100%): Real buying vs selling pressure

- Visual Gauge: Horizontal bar chart showing flow intensity

- Momentum Status: SHIFTING, ACCELERATING, STRONG, MODERATE, or WEAK

- Trading Application: Flow shifts often precede major moves

Signal Performance Tracking

- Win Rate Monitoring: Real-time success percentage with emoji indicators

- Signal Count: Total signals generated for frequency analysis

- Current Position: LONG, SHORT, or NONE with P&L tracking

- Volatility Regime: HIGH, MEDIUM, or LOW classification

Market Structure Analysis

- Möbius Field Strength: Mathematical field oscillation intensity

- CHAOTIC: High complexity, use wider stops

- STRONG: Active field, normal position sizing

- MODERATE: Balanced conditions

- WEAK: Low activity, consider smaller positions

- HTF Trend: Higher timeframe bias (BULL/BEAR/NEUTRAL)

- Strategy Agreement: Multi-algorithm consensus level

Position Management

When in trades, displays:

- Entry Price: Original signal price

- Current P&L: Real-time percentage with risk level assessment

- Duration: Bars in trade for timing analysis

- Risk Level: HIGH/MEDIUM/LOW based on current exposure

🚀 SIGNAL GENERATION LOGIC

Balanced Long/Short Architecture

The indicator generates signals through multiple convergent pathways:

Long Entry Conditions:

- Score threshold breach with algorithmic agreement

- Strong bullish order flow (OFPI > 0.15) with positive composite signal

- Bullish pattern recognition with mathematical confirmation

- HTF trend alignment with momentum shifting

- Extreme bullish OFPI (>0.3) with any positive score

Short Entry Conditions:

- Score threshold breach with bearish agreement

- Strong bearish order flow (OFPI < -0.15) with negative composite signal

- Bearish pattern recognition with mathematical confirmation

- HTF trend alignment with momentum shifting

- Extreme bearish OFPI (<-0.3) with any negative score

Exit Logic:

- Score deterioration below continuation threshold

- Signal quality degradation

- Opposing order flow acceleration

- 10-bar minimum between signals prevents overtrading

⚙️ OPTIMIZATION GUIDELINES

Asset-Specific Settings

Cryptocurrency Trading:

- Modular Level: 15-25 (capture volatility)

- L-Function Precision: 0.8-1.3 (reactive to price swings)

- OFPI Length: 10-20 (fast correlation shifts)

- Cascade Levels: 5-7, Theme: Holographic

Stock Index Trading:

- Modular Level: 25-35 (balanced trending)

- L-Function Precision: 1.5-1.8 (stable patterns)

- OFPI Length: 14-20 (standard correlation)

- Cascade Levels: 4-5, Theme: Quantum

Forex Trading:

- Modular Level: 35-45 (smooth trends)

- L-Function Precision: 1.6-2.1 (high smoothing)

- OFPI Length: 18-25 (disable volume amplification)

- Cascade Levels: 3-4, Theme: Crystalline

Timeframe Optimization

Scalping (1-5 minute charts):

- Reduce all lookback parameters by 30-40%

- Increase L-Function precision for noise reduction

- Enable all visual elements for maximum information

- Use Small dashboard to save screen space

Day Trading (15 minute - 1 hour):

- Use default parameters as starting point

- Adjust based on market volatility

- Normal dashboard provides optimal information density

- Focus on OFPI momentum shifts for entries

Swing Trading (4 hour - Daily):

- Increase lookback parameters by 30-50%

- Higher L-Function precision for stability

- Large dashboard for comprehensive analysis

- Emphasize HTF trend alignment

🏆 ADVANCED TRADING STRATEGIES

The Mathematical Confluence Method

1. Wait for Fractal Grid level approach

2. Confirm with projected L-Score > threshold

3. Verify OFPI alignment with direction

4. Enter on portal signal with quality ≥ STRONG

5. Exit on score deterioration or opposing flow

The Regime Trading System

1. Monitor Aether Flow background intensity

2. Trade aggressively during bright purple periods

3. Reduce position size during dark periods

4. Use Möbius Field strength for stop placement

5. Align with HTF trend for maximum probability

The OFPI Momentum Strategy

1. Watch for momentum shifting detection

2. Confirm with accelerating flow in direction

3. Enter on immediate portal signal

4. Scale out at Fibonacci levels

5. Exit on flow deceleration or reversal

⚠️ RISK MANAGEMENT INTEGRATION

Mathematical Position Sizing

- Use Galois Rank for volatility-adjusted sizing

- Möbius Field strength determines stop width

- Fractal Dimension guides maximum exposure

- OFPI momentum affects entry timing

Signal Quality Filtering

- Trade only STRONG or EXCEPTIONAL quality signals

- Increase position size with higher agreement levels

- Reduce risk during CHAOTIC Möbius field periods

- Respect HTF trend alignment for directional bias

🔬 DEVELOPMENT JOURNEY

Creating the LOMV was an extraordinary mathematical undertaking that pushed the boundaries of what's possible in technical analysis. This indicator almost didn't happen. The theoretical complexity nearly proved insurmountable.

The Mathematical Challenge

Implementing the Langlands Program required deep research into:

- Number theory and the Möbius function

- Riemann zeta function convergence properties

- L-function analytical continuation

- Galois representations in finite fields

The mathematical literature spans decades of pure mathematics research, requiring translation from abstract theory to practical market application.

The Computational Complexity

Operadic composition theory demanded:

- Category theory implementation in Pine Script

- Multi-dimensional array management for strategy composition

- Real-time democratic voting algorithms

- Performance optimization for complex calculations

The Integration Breakthrough

Bringing together three disparate mathematical frameworks required:

- Novel approaches to signal weighting and combination

- Revolutionary Order Flow Polarity Index development

- Advanced T3 smoothing implementation

- Balanced signal generation preventing directional bias

Months of intensive research culminated in breakthrough moments when the mathematics finally aligned with market reality. The result is an indicator that reveals market structure invisible to conventional analysis while maintaining practical trading utility.

🎯 PRACTICAL IMPLEMENTATION

Getting Started

1. Apply indicator with default settings

2. Select appropriate theme for your markets

3. Observe dashboard metrics during different market conditions

4. Practice signal identification without trading

5. Gradually adjust parameters based on observations

Signal Confirmation Process

- Never trade on score alone - verify quality rating

- Confirm OFPI alignment with intended direction

- Check fractal grid level proximity for timing

- Ensure Möbius field strength supports position size

- Validate against HTF trend for bias confirmation

Performance Monitoring

- Track win rate in dashboard for strategy assessment

- Monitor component contributions for optimization

- Adjust threshold based on desired signal frequency

- Document performance across different market regimes

🌟 UNIQUE INNOVATIONS

1. First Integration of Langlands Program mathematics with practical trading

2. Revolutionary OFPI with T3 smoothing and momentum detection

3. Operadic Composition using category theory for signal democracy

4. Dynamic Fractal Grid with projected L-Score calculations

5. Multi-Dimensional Visualization through morphism flow portals

6. Regime-Adaptive Background showing market energy intensity

7. Balanced Signal Generation preventing directional bias

8. Professional Dashboard with institutional-grade metrics

📚 EDUCATIONAL VALUE

The LOMV serves as both a practical trading tool and an educational gateway to advanced mathematics. Traders gain exposure to:

- Pure mathematics applications in markets

- Category theory and operadic composition

- Number theory through Möbius function implementation

- Harmonic analysis via L-function calculations

- Advanced signal processing through T3 smoothing

⚖️ RESPONSIBLE USAGE

This indicator represents advanced mathematical research applied to market analysis. While the underlying mathematics are rigorously implemented, markets remain inherently unpredictable.

Key Principles:

- Use as part of comprehensive trading strategy

- Implement proper risk management at all times

- Backtest thoroughly before live implementation

- Understand that past performance does not guarantee future results

- Never risk more than you can afford to lose

The mathematics reveal deep market structure, but successful trading requires discipline, patience, and sound risk management beyond any indicator.

🔮 CONCLUSION

The Langlands-Operadic Möbius Vortex represents a quantum leap forward in technical analysis, bringing PhD-level pure mathematics to practical trading while maintaining visual elegance and usability.

From the harmonic analysis of the Langlands Program to the democratic composition of operadic theory, from the number-theoretic precision of the Möbius function to the revolutionary Order Flow Polarity Index, every component works in mathematical harmony to reveal the hidden order within market chaos.

This is more than an indicator - it's a mathematical lens that transforms how you see and understand market structure.

Trade with mathematical precision. Trade with the LOMV.

*"Mathematics is the language with which God has written the universe." - Galileo Galilei*

*In markets, as in nature, profound mathematical beauty underlies apparent chaos. The LOMV reveals this hidden order.*

— Dskyz, Trade with insight. Trade with anticipation.

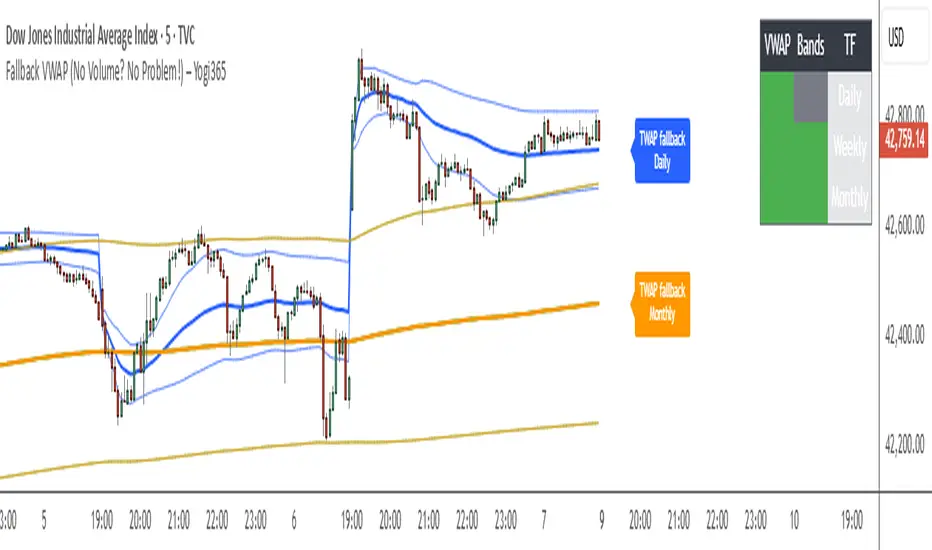

Fallback VWAP (No Volume? No Problem!) – Yogi365Fallback VWAP (No Volume? No Problem!) – Yogi365

This script plots Daily, Weekly, and Monthly VWAPs with ±1 Standard Deviation bands. When volume data is missing or zero (common in indices or illiquid assets), it automatically falls back to a TWAP-style calculation, ensuring that your VWAP levels always remain visible and accurate.

Features:

Daily, Weekly, and Monthly VWAPs with ±1 Std Dev bands.

Auto-detection of missing volume and seamless fallback.

Clean, color-coded trend table showing price vs VWAP/bands.

Uses hlc3 for VWAP source.

Labels indicate when fallback is used.

Best Used On:

Any asset or index where volume is unavailable.

Intraday and swing trading.

Works on all timeframes but optimized for overlay use.

How it Works:

If volume == 0, the script uses a constant fallback volume (1), turning the VWAP into a TWAP (Time-Weighted Average Price) — still useful for intraday or index-based analysis.

This ensures consistent plotting on instruments like indices (e.g., NIFTY, SENSEX,DJI etc.) which might not provide volume on TradingView.

Trend Persistence Counter (TPC) by riskcipher🧭 Trend Persistence Counter (TPC) – A Simple Price Action Trend Duration Tool

Trend Persistence Counter (TPC) is a lightweight indicator that counts how long a trend persists after a breakout.

It is entirely based on price action, without using any moving averages or smoothing. The goal is to give a simple, rule-based view of trend continuity.

🧠 How It Works (Logic Overview)

This indicator switches between two modes: bullish and bearish.

If close > previous high, the counter enters bullish mode, and starts at +1

While in bullish mode:

If close >= previous low → continue the uptrend → +1 each bar

If close < previous low → trend ends → reset to 0, switch to bearish mode

If close < previous low, the counter enters bearish mode, and starts at -1

While in bearish mode:

If close <= previous high → continue the downtrend → -1 each bar

If close > previous high → trend ends → reset to 0, switch to bullish mode

This provides a bar-by-bar count of trend persistence based on whether price holds structure.

🎯 Use Cases

Track how long a trend continues after a breakout

Quickly detect when trend structure breaks

Help visually filter “strong” vs “weak” moves

Build logic-based alerts (e.g., trend continues for N bars)

🔍 Why Use This Instead of Traditional Indicators?

This is not meant to replace moving averages or trend filters.

But it offers some advantages for those who prefer structure-based logic:

Feature TPC

Based on Price Action ✅ Yes

Uses Lagging Filters ❌ No moving average or smoothing

Trend Duration Measurement ✅ Counts valid consecutive moves

Complexity ⚪ Very simple and transparent

It’s a simple concept and easy to understand, but still useful when combined with other tools or visualized on its own.

⚙️ Technical Notes

Works on any timeframe or instrument

The value is positive during bullish persistence, negative during bearish

Value resets to 0 when trend structure breaks

All logic is calculated bar-by-bar, in real time

✅ Example Usage Ideas

Highlight candles when TPC value crosses a certain threshold (e.g., strong breakout continuation)

Use the zero-cross as a potential reversal warning

Filter trend signals in your existing strategies

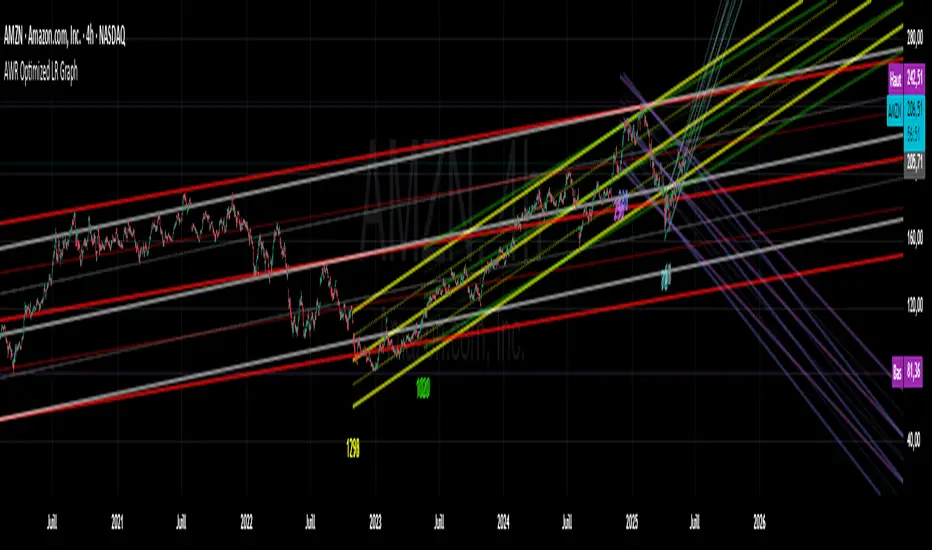

AWR Optimized LR GraphHello Trading Viewers !

Drawing linear regression channels at the best place and for many periods can be time consuming.

In the library, I've found some indicators that draw 1 or 2 but based on fixed number of bars or a duration...

Not always relevant, that's why I decide to create this indicator.

It calculates 8 linear regression channels according to 8 differents configurable periods.

Each time, the indicator will calculate for each specified duration range the best linear regression line & channel (2 standard regressions) for that period and then plot it on the graph.

You can settle how many linear regression channels you want to display.

For period, defaults configurations (number of candles studied) are :

Period 1

min1 = 33

max1 = 66

Period 2

min2 = 67

max2 = 128

Period 3

min3 = 129

max3 = 255

Period 4

min4 = 256

max4 = 510

Period 5

min5 = 511

max5 = 1020

Period 6

min6 = 1021

max6 = 2040

Period 7

min7 = 2041

max7 = 3500

Period 8

min8 = 3501

max8 = 4999

This default settings provide short-term, mid term, long term and a very long-term view.

You have to go back on the chart to display the channels that start on previous period that are currently not on the screen.

You can set a specific color for each linear regression channels.

The linear regression line is based on the least squares method, meaning: it calculates along each period the gap between a linear & the price & squarred it. Then it defines the linear in order to have always the least distance between price and the linear.

The more the price deviates from its regression line, the more statistically likely it is to return to its regression line.

Application of Regression Lines in Trading

Regression lines are widely used in trading and financial analysis to understand market trends and make informed predictions. Here are some key applications:

1. Trend Identification – Traders use regression lines to visualize the general direction of a stock or asset price, helping to confirm an upward or downward trend.

2. Price Predictions – Linear regression models assist in estimating future price movements based on historical data, allowing traders to anticipate changes.

3. Risk Assessment – By analyzing the slope and variation of a regression line, traders can gauge market volatility and potential risks.

4. Support and Resistance Levels – Regression channels help traders identify support and resistance zones, providing insight into optimal entry and exit points in a trend.

5. You can also use the short period linear regression channels vs the long period linear regression channels to identify important pivot points.

Combined ATPC & MACD DivergenceTrend Optimizer + Divergence Finder in One Unified Tool

🔍 Overview:

This powerful dual-system indicator merges two proven analytical engines:

✅ The Algorganic Typical Price Channel (ATPC) — a custom trend oscillator that highlights mean-reversion and directional bias.

✅ A refined MACD system with divergence detection, enhanced with an adjusted Donchian midline for real-time trend strength filtering.

Together, they provide a high-confidence, multi-signal system ideal for swing trading, scalping, or confirming reversals with context.

⚙️ Core Components & Logic

🧠 1. ATPC Engine (Trend Commodity Index)

A momentum and volatility-normalized oscillator based on the typical price (H+L+C)/3:

TrendCI Line (Blue) – Main trend signal based on smoothed CCI logic.

TrendLine2 (Orange) – A slower smoothing of TrendCI for crossovers.

Key Zones (customizable):

🔴 Ultra Overbought: +73

🟣 Overbought: +58

🟣 Oversold: -58

🔴 Ultra Oversold: -73

Trade Logic:

✅ Buy Signal: TrendCI crosses above TrendLine2 while in oversold zone

❌ Sell Signal: TrendCI crosses below TrendLine2 while in overbought zone

Additional visual feedback:

Histogram Bars show strength and direction of momentum shift

Green/Red Circles highlight potential long/short setups

📉 2. MACD System + Divergence Finder

Classic MACD enhanced with a Donchian Midline overlay to filter trend bias.

🔷 MACD Line and 🟠 Signal Line show crossover momentum

🟩/🟥 Histogram shows distance from the signal line

🟪 Adjusted Donchian Midline dynamically adapts to range-bound vs trending environments

Background Color provides real-time trend state:

✅ Green = Bullish Trend

❌ Red = Bearish Trend

No color = Neutral / Choppy

MACD Boundaries (user-defined):

Overbought: +1.0

Oversold: -1.0

🔀 3. Divergence Detection

Spot hidden power shifts before price reacts:

🔼 Positive Divergence – Price makes lower lows, but MACD histogram rises

🔽 Negative Divergence – Price makes higher highs, but MACD histogram weakens

These are visually marked with:

Green “+Div” label (bullish reversal cue)

Red “–Div” label (bearish exhaustion signal)

🎯 How to Use It

For Trend Traders:

Stay in sync with macro trend using MACD histogram + background

Use ATPC crossovers for precision entries

Avoid signals during neutral background (chop filter)

For Reversal Traders:

Look for bullish +Div with ATPC buy signal in oversold zone

Look for bearish –Div with ATPC sell signal in overbought zone

Mid-Donchian line can act as confluence or breakout trigger

For Scalpers & Intraday Traders:

Combine with VWAP, liquidity zones, or order flow levels

ATPC crossovers + MACD histogram zero-line flip = potential scalp entry

Use histogram slope and divergence to avoid false momentum traps

🧩 Customizable Inputs

🎛️ ATPC: Channel & Smoothing lengths, overbought/oversold thresholds

🎛️ MACD: Fast/slow EMAs, signal smoothing, Donchian period, bounds

🎨 Fully theme-compatible with adjustable colors and line styles

🔔 Alerts (Add Your Own)

While this version doesn’t contain built-in alerts, you can easily add alerts based on:

buySignal or sellSignal from ATPC logic

Histogram cross zero or trend flip

MACD Divergence event

📜 “This indicator doesn't just show signals—it tells a story about who’s in control of the market, and when that control might be slipping.”

Not-So-Average True Range (nsATR)Not-So-Average True Range (nsATR)

*By Sherlock_MacGyver*

---

Long Story Short

The nsATR is a complete overhaul of traditional ATR analysis. It was designed to solve the fundamental issues with standard ATR, such as lag, lack of contextual awareness, and equal treatment of all volatility events.

Key innovations include:

* A smarter ATR that reacts dynamically when price movement exceeds normal expectations.

* Envelope zones that distinguish between moderate and extreme volatility conditions.

* A long-term ATR baseline that adds historical context to current readings.

* A compression detection system that flags when the market is coiled and ready to break out.

This indicator is designed for traders who want to see volatility the way it actually behaves — contextually, asymmetrically, and with predictive power.

---

What Is This Thing?

Standard ATR (Average True Range) has limitations:

* It smooths too slowly (using Wilder's RMA), which delays detection of meaningful moves.

* It lacks context — no way to know if current volatility is high or low relative to history.

* It treats all volatility equally, regardless of scale or significance.

nsATR** was built from scratch to overcome these weaknesses by applying:

* Amplification of large True Range spikes.

* Visual envelope zones for detecting volatility regimes.

* A long-term context line to anchor current readings.

* Multi-factor compression analysis to anticipate breakouts.

---

Core Features

1. Breach Detection with Amplification

When True Range exceeds a user-defined threshold (e.g., ATR × 1.2), it is amplified using a power function to reflect nonlinear volatility. This amplified value is then smoothed and cascades into future ATR values, affecting the indicator beyond a single bar.

2. Direction Tagging

Volatility spikes are tagged as upward or downward based on basic price momentum (close vs previous close). This provides visual context for how volatility is behaving in real-time.

3. Envelope Zones

Two adaptive envelopes highlight the current volatility regime:

* Stage 1: Moderate volatility (default: ATR × 1.5)

* Stage 2: Extreme volatility (default: ATR × 2.0)

Breaching these zones signals meaningful expansion in volatility.

4. Long-Term Context Baseline

A 200-period simple moving average of the classic ATR establishes whether current readings are above or below long-term volatility expectations.

5. Multi-Signal Compression Detection

Flags potential breakout conditions when:

* ATR is below its long-term baseline

* Price Bollinger Bands are compressed

* RSI Bollinger Bands are also compressed

All three signals must align to plot a "Volatility Confluence Dot" — an early warning of potential expansion.

---

Chart Outputs

In the Indicator Pane:

* Breach Amplified ATR (Orange line)

* Classic ATR baseline (White line)

* Long-Term context baseline (Cyan line)

* Stage 1 and Stage 2 Envelopes (Purple and Yellow lines)

On the Price Chart:

* Triangles for breach direction (green/red)

* Diamonds for compression zones

* Optional background coloring for visual clarity

---

Alerts

Built-in alert conditions:

1. ATR breach detected

2. Stage 1 envelope breached

3. Stage 2 envelope breached

4. Compression zone detected

---

Customization

All components are modular. Traders can adjust:

* Display toggles for each visual layer

* Colors and line widths

* Breach threshold and amplification power

* Envelope sensitivity

* Compression sensitivity and lookback windows

Some options are disabled by default to reduce clutter but can be turned on for more aggressive signal detection.

---

Real-Time Behavior (Non-Repainting Clarification)

The indicator updates in real time on the current bar as new data comes in. This is expected behavior for live trading tools. Once a bar closes, values do not change. In other words, the indicator *does not repaint history* — but the current bar can update dynamically until it closes.

---

Use Cases

* Day traders: Use compression zones to anticipate volatility surges.

* Swing traders: Use envelope breaches for regime awareness.

* System developers: Replace standard ATR in your logic for better responsiveness.

* Risk managers: Use directional volatility signals to better model exposure.

---

About the Developer

Sherlock_MacGyver develops original trading systems that question default assumptions and solve real trader problems.

5-Day APM for Forex PairsThis script calculates the 5-Day Average Pip Movement (APM) for major Forex pairs.

It displays the average daily range (in pips) over the past 5 trading days using true high-low price movement.

The script is optimized for clarity and minimalism — showing a single floating label on the main chart for pairs like GBPUSD, USDJPY, EURUSD, etc.

Automatically adjusts pip calculation for JPY pairs (×100) and other pairs (×10000).

✅ Great for identifying high-volatility vs low-volatility conditions

✅ Clean design with no clutter

✅ Only works on major FX pairs (whitelisted)

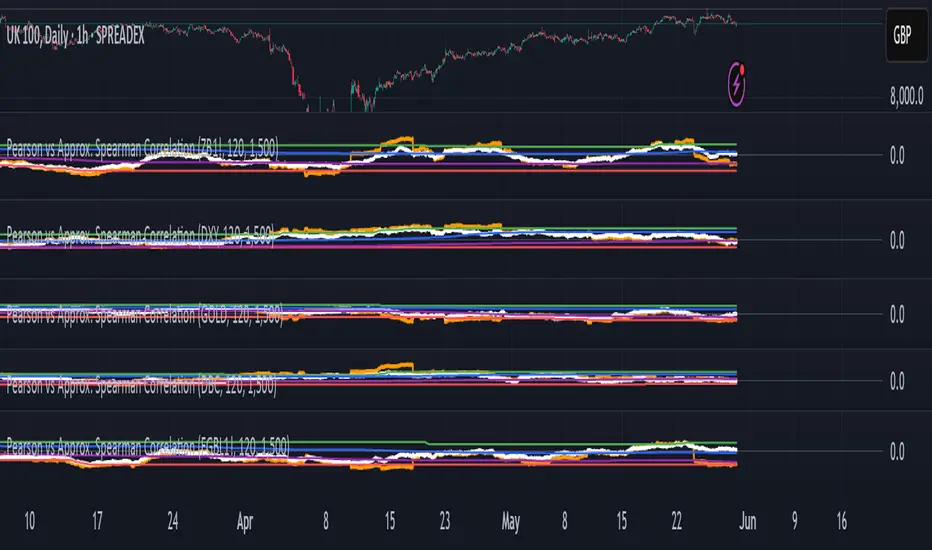

Pearson vs Approx. Spearman CorrelationThis indicator displays the rolling Pearson and approximate Spearman correlation between the chart's asset and a second user-defined asset, based on log returns over a customizable window.

Features:

- Pearson correlation of log returns (standard linear dependency measure)

- Approximate Spearman correlation, using percentile ranks to better capture nonlinear and monotonic relationships

/ Horizontal lines showing:

Maximum and minimum correlation values over a statistical window

1st quartile (25%) and 3rd quartile (75%) — helpful for identifying statistically high or low regimes

This script is useful for identifying dynamic co-movements, regime changes, or correlation breakdowns between assets — applicable in risk management, portfolio construction, and pairs trading strategies.

Symbol vs Benchmark Performance & Volatility TableThis tool puts the current symbol’s performance and volatility side-by-side with any benchmark —NASDAQ, S&P 500, NIFTY or a custom index of your choice.

A quick glance shows whether the stock is outperforming, lagging, or just moving with the market.

⸻

Features

• ✅ Returns over 1W, 1M, 3M, 6M, 12M

• 🔄 Benchmark comparison with optional difference row

• ⚡ Volatility snapshot (20D, 60D, or 252D)

• 🎛️ Fully customizable:

• Show/hide rows and timeframes

• Switch between default or custom benchmarks

• Pick position, size, and colors

Built to answer a simple, everyday question — “How’s this really doing compared to the broader market?”

Thanks to @BeeHolder, whose performance table originally inspired this.

Hope it makes your analysis a little easier and quicker.

Project SynthIntroducing Project Synth !

Inspired by Pace of Tape and Cumulative Delta I created Project Synth in order to aggregate volume flow data across multiple marketsfor two primary reasions:

Traditional orderflow tools are not available on Tradingview. My script attempts to bring an original; calculus-based approach to creating not only an alternative for traditional orderflow tools, but also a more accurate one.

In order to detect genuine buying and selling pressure that cannot be easily manipulated. I did this because while I've always enjoyed concept behind both of those tools, I did not think they captured enough data to be useful. By analyzing assets that move together (positive correlation) and assets that move inversely (negative correlation), my system aims to fix the fundamental problems with those indicators and create an objective view of market sentiment based on aggregate orderflow.

Some more detailed explanations (using QQQ and SQQQ as an example):

Inverse Market Dynamics (QQQ vs SQQQ):

In an inverse market like SQQQ, aggressive buyers hit the ask when they expect the underlying (QQQ) to fall, while passive buyers wait on the bid hoping for cheaper inverse exposure. When QQQ rallies, SQQQ sees aggressive selling (people dumping their bearish bets) hitting bids, while passive sellers sit on the ask hoping to exit at better prices. The aggression flows opposite to the underlying market direction.

Why Utilizing Both Markets Provides A More Accurate Delta:

Watching both QQQ and SQQQ gives cross-validation - real buying pressure in QQQ should coincide with selling pressure in SQQQ. If you see buying in QQQ but also buying in SQQQ, that's a conflicting signal suggesting the move might be artificial or driven by other factors. The inverse relationship acts as a confirmation filter, making false signals much harder to generate.

Multiple Markets = Authentic Pressure:

The more unique, important markets you track, the harder it becomes to create fake delta moves. Real institutional buying/selling pressure affects multiple correlated assets simultaneously in predictable patterns - you can't easily manipulate tech stocks, treasury bonds, VIX, and currency pairs all at once to create a false signal. Each additional market acts as a fraud detection layer, ensuring the delta measurement reflects genuine ecosystem-wide buying and selling pressure rather than isolated manipulation or noise.

My Suggestions For Usage:

In order to keep the explanation simple and short for now, I suggest using it just like a cumulative delta indicator. For example: let's say you were watching CME_MINI:ES1! , and you had a resistance level at 6000. When the price reaches your resistance level, you would be looking for a significant divergence between price and Delta. Price : rising, Delta : falling. This means that even though the price was going up, strong and aggressive sellers are jumping in more and more, this can be used as a confirmation tool for a resistance level.

Notes For Moderators, Authors and Users:

Firstly, to the best of my knowledge, I have not been able to find many tools built around the concept of cumulative delta or pace of tape. While I know there are a couple projects, none to the magnitude of synthetically recreating these tools via an algorithm designed around basic calculus principles. While tools like Volume Delta are built in, they do not attempt to capture an accurate picture of aggregated orderflow from what I understand.

Secondly, it needs to be noted that tool aims to create an approximation of buying and selling pressure. To my knowledge it is not possible to create an accurate full picture, at least not within the limitations of Tradingview.

SD Median MVRV-Z🧠 Overview

SD Median MVRV-Z is a trend-following indicator that uses on-chain valuation signals as a supportive filter. It blends the momentum of the MVRV Z-score with a dynamic median-based price structure to provide cleaner, more reliable directional signals. This tool is designed to identify when price and trend align with favorable broader context — not to pinpoint overbought or oversold extremes.

🧩 Key Features

Trend-Following Core: Signals are built around directional strength, not reversion.

MVRV Z-Score Momentum: Utilizes the statistical momentum of Market Cap vs Realized Cap as a macro trend driver.

Rolling Median Filter: Applies a price-based condition to ensure trend signals are not triggered during short-term counter-moves or noise.

Threshold Customization: Input controls allow traders to define the strength required to trigger long or short signals.

Dynamic Visualization: Candle coloring and filled zones provide instant feedback on current market regime.

🔍 How It Works

Trend Signal: The MVRV ratio is normalized via Z-scoring to produce a momentum-like signal based on how far current valuation deviates from its rolling average.

Price Filter: A rolling median and standard deviation of price define an upper and lower band. These serve to filter out MVRV-Z signals that occur when price is moving against the perceived direction.

Signal Logic:

Long signal = MVRV-Z above threshold and price is not in the lower volatility band.

Short signal = MVRV-Z below threshold, regardless of price band (more aggressive condition).

Directional Engine (CD): Encodes the market regime state (1 for long, -1 for short, 0 for neutral), and drives all visual outputs.

🔁 Use Cases & Applications

Momentum Confirmation: Identify when on-chain momentum and price structure both confirm a trend direction.

Reduced Whipsawing: Filter out weak or conflicting trend signals that would otherwise lead to false entries.

Best Suited for BTC: This indicator is specifically tailored for Bitcoin, using BTC’s Market Cap and Realized Cap data from on-chain sources.

✅ Conclusion

SD Median MVRV-Z is a trend-centric tool that ensures directional conviction by requiring agreement between price structure and underlying market momentum. It is not meant to detect tops or bottoms, but instead to help traders participate in sustainable moves with greater confidence.

⚠️ Disclaimer

The content provided by this indicator is for educational and informational purposes only. Nothing herein constitutes financial or investment advice. Trading and investing involve risk, including the potential loss of capital. Always backtest and apply risk management suited to your strategy.

21-Day Trend Direction📈 21-Day Trend Direction Indicator

📊 How It Works:

🎯 Trend Detection Logic:

Analyzes last 21 daily candles

Calculates total price change from start to end

Compares against sideways threshold (default 2%)

Counts bullish vs bearish days

Tracks higher highs and lower lows

📈 Trend Classifications:

• 📈 UPTREND: Price change > +2% over 21 days

• 📉 DOWNTREND: Price change < -2% over 21 days

• ➡️ SIDEWAYS: Price change between -2% and +2%

💪 Trend Strength Levels:

• 🔥 Very Strong: >5% price change

• 💪 Strong: 3-5% price change

• 📊 Moderate: 1.5-3% price change

• 📉 Weak: <1.5% price change

🎨 Visual Features:

📋 Information Table Shows:

• Trend Direction with color coding

• Price Change % over 21 days

• Trend Strength classification

• Bull/Bear Days count

• Higher Highs/Lower Lows count

• Analysis Period (customizable)

📊 Chart Indicators:

• Trend Line (21-day moving average)

• Background Color for quick trend identification

• Trend Arrows (▲ ▼ ➡) on chart

• Customizable display options

⚙️ Customizable Settings:

🎯 Analysis Settings:

• Lookback Days: 5-50 days (default: 14)

• Sideways Threshold: 0.5-10% (default: 2%)

• Trend Strength: Low/Medium/High sensitivity

🎨 Display Options:

• Table Position: 9 different positions

• Table Size: Tiny to Large

• Show/Hide: Table, Trend Line, Background, Arrows

🚨 Alert Options:

• Trend Change to Uptrend

• Trend Change to Downtrend

• Trend Change to Sideways

This indicator gives you a clear, objective view of the 21-day trend with multiple confirmation signals! 🚀

Smooth BTCSPL [GiudiceQuantico] – Dual Smoothed MAsSmooth BTCSPL – Dual Smoothed MAs

What it measures

• % of Bitcoin addresses in profit vs loss (on-chain tickers).

• Spread = profit % − loss % → quick aggregate-sentiment gauge.

• Optional alpha-decay normalisation ⇒ keeps the curve on a 0-1 scale across cycles.

User inputs

• Use Alpha-Decay Adjusted Input (true/false).

• Fast MA – type (SMA / EMA / WMA / VWMA) & length (default 100).

• Slow MA – type & length (default 200).

• Colours – Bullish (#00ffbb) / Bearish (magenta).

Computation flow