Tuga SupertrendDescription

This strategy uses the Supertrend indicator enhanced with commission and slippage filters to capture trends on the daily chart. It’s designed to work on any asset but is especially effective in markets with consistent movements.

Use the date inputs to set the backtest period (default: from January 1, 2018, through today, June 30, 2025).

The default input values are optimized for the daily chart. For other timeframes, adjust the parameters to suit the asset you’re testing.

Release Notes

June 30, 2025

• Updated default backtest period to end on June 30, 2025.

• Default commission adjusted to 0.1 %.

• Slippage set to 3 ticks.

• Default slippage set to 3 ticks.

• Simplified the strategy name to “Tuga Supertrend”.

Default Parameters

Parameter Default Value

Supertrend Period 10

Multiplier (Factor) 3

Commission 0.1 %

Slippage 3 ticks

Start Date January 1, 2018

End Date June 30, 2025

"山子高科2025年一季度财务报告关键指标" için komut dosyalarını ara

Gold and Bitcoin: The Evolution of Value!The Eternal Luster of Gold

In the dawn of time, when the earth was young and rivers whispered secrets to the stones, a wanderer named Elara found a gleam in the silt of a sun-kissed stream. It was pure gold, radiant like a captured star fallen from the heavens. She held it in her palm, feeling its warmth pulse like a heartbeat, and in that moment, humanity’s soul awakened to the allure of eternity.

As seasons turned to centuries, gold wove itself into the story of empires. In ancient Egypt, pharaohs crowned themselves with its glow, believing it to be the flesh of gods. It built pyramids that reached for the sky and tombs that guarded kings forever. Across the sands in Mesopotamia, merchants traded it for spices and silks, its weight a promise of power and trust.

Translation moment: Gold became the first universal symbol of value. People trusted it more than words or promises because it did not rust, fade, or vanish.

The Greeks saw in gold not only wealth but wisdom, the symbol of the sun’s eternal fire. Alexander the Great carried it across the continent, forging an empire of golden threads. Rome rose on its back, minting coins whose clink echoed through history.

Through the ages, gold endured the rush of California’s dreamers, the halls of Versailles, and the quiet vaults of modern fortunes. It has been both a curse and a blessing, the fuel of wars and the gift of love, whispering of beauty’s fragility and the human desire for something that lasts beyond the grave. In its shine, we see ourselves fragile yet forever chasing light.

The Digital Dawn of Bitcoin

Centuries later, under the glow of computer screens, a visionary named Satoshi dreamed of a new gold born not from the earth but from the ether of ideas. Bitcoin appeared in 2009 amid a world weary of banks and broken trust.

Like gold’s ancient gleam, Bitcoin was mined not with picks but with puzzles solved by machines. It promised freedom, a currency without kings, flowing from person to person, unbound by borders or empires.

Translation moment: Bitcoin works like digital gold. Instead of digging the ground, miners use computers to solve problems and unlock new coins. No one controls it, and that is what makes it powerful.

Through doubt and frenzy, it rose as a beacon for those seeking sovereignty in a digital world. Its volatility became its soul, a reminder that true value is built on belief. Bitcoin speaks to ingenuity and rebellion, a star of code guiding us toward a future where wealth is weightless yet profoundly honest.

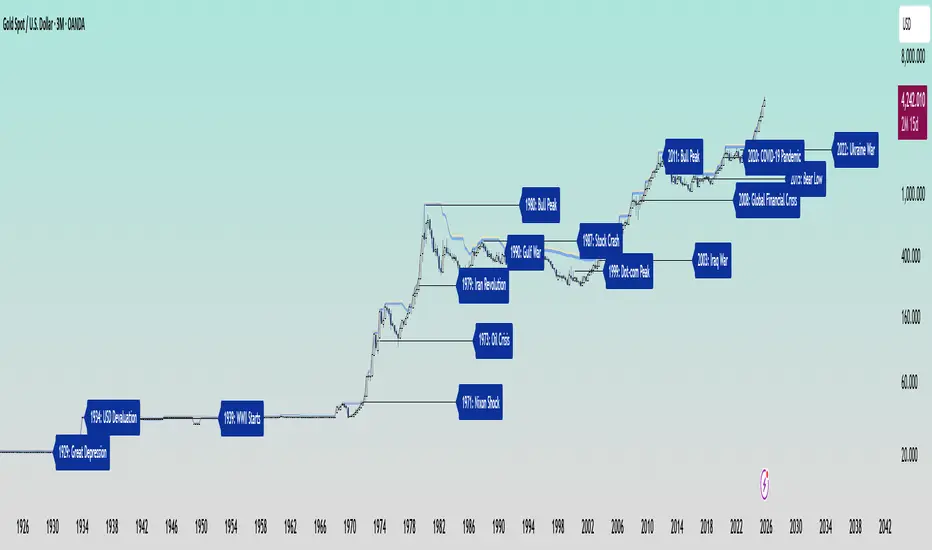

Gold’s Cycles: Echoes of War and Crisis

In the early 20th century, gold was held under fixed prices until the Great Depression of 1929 shattered these illusions. The 1934 dollar devaluation lifted it from 20.67 to 35, restoring faith amid despair. When World War II erupted in 1939, gold’s role as a refuge was muted by controls, yet it quietly held its place as the world’s silent guardian.

The 1970s awakened its wild spirit. The Nixon Shock of 1971 freed gold from 35, sparking a bull run during the 1973 Oil Crisis. The 1979 Iranian Revolution led to a 1980 peak of 850, a leap of more than 2,000 percent, as investors sought safety from the chaos.

Translation moment: When fear rises, people rush to gold. Every major war or economic crisis has sent gold upward because it feels safe when paper money loses trust.

The 1987 stock crash caused brief dips, but the 1990 Gulf War reignited its glow. Around 2000, after the Dot-com Bust, gold found new life, climbing from $ 270 to over $1,900 during the 2008 Financial Crisis. It dipped to 1050 in 2015, then surged again past 2000 during the 2020 pandemic.

The 2022 Ukraine War added another chapter with prices climbing above 2700 by 2025. Across a century of crises, gold has risen whenever fear tested humanity’s resolve, teaching patience and fortitude through its quiet endurance.

Bitcoin’s Cycles: Echoes of Innovation and Crisis

Born from the ashes of the 2008 Financial Crisis, Bitcoin began its story at mere cents. It traded below $1 until 2011, when it reached $30 before crashing by 90 percent following the MTGOX collapse.

In 2013, it soared to 1242 only to fall again to 200 in 2015 as regulations tightened. The 2017 bull run lifted it to nearly 20000 before another long winter brought it to 3200 in 2018. Each fall taught resilience, each rise renewed belief.

During the 2020 pandemic, it fell below 5000 before rallying to 69000 in 2021. The Ukraine War and the FTX collapse of 2022 brought it down to 16000, but also proved its role in humanitarian aid. By 2024, the halving and ETF approvals helped it break 100000, marking Bitcoin’s rise as digital gold.

Translation moment: Bitcoin’s rhythm follows four-year halving cycles when mining rewards are cut in half. This keeps supply limited, which often triggers new bull runs as demand returns.

Every four years, it's halving cycles 2012, 2016, 2020, 2024, fueling new waves of adoption and correction. Bitcoin grows strongest in times of uncertainty, echoing humanity’s drive to evolve beyond limits.

The Harmony of Gold and Bitcoin Modern Parallels

In today’s markets, gold’s ancient glow meets Bitcoin’s electric pulse. As of October 17, 2025, their correlation stands near 0.85, close to its historic high of 0.9. Both rise as guardians against inflation and the erosion of trust in the dollar.

Gold trades near 4310 per ounce a record high while Bitcoin hovers around 104700 showing brief fractures in their unity. Gold offers the comfort of touch while Bitcoin provides the thrill of code. Together, they reflect fear and hope, the twin emotions that drive every market.

Translation moment: A correlation of 0.85 means they often move in the same direction. When fear or inflation rises, both gold and Bitcoin tend to rise in tandem.

Analysts warn of bubbles in stocks, gold, and crypto, yet optimism remains for Bitcoin’s growth through 2026, while gold holds its defensive strength.

Gold carries risks of storage cost and theft, but steadiness in chaos. Bitcoin carries volatility and regulatory challenges, but it also offers unmatched innovation and reach. One is the anchor, the other the dream, and both reward those who hold conviction through uncertainty.

Epilogue: The Timeless Balance

Gold and Bitcoin form a bridge between the ancient and the future. Gold, the earth’s eternal treasure, stands as a symbol of stability and truth. Bitcoin, the digital heir, shines with the spark of innovation and freedom.

Experts view gold as the ultimate inflation hedge, forged in fire and tested over centuries. They see Bitcoin as its digital counterpart, scarce by code and limitless in reach.

Gold’s weight grounds us in reality while Bitcoin’s light expands our imagination. In 2025, as gold surpasses $4,346 and Bitcoin hovers near $105,000, the wise investor sees not rivals but reflections.

Translation moment: Gold reminds us to protect what we have. Bitcoin reminds us to dream of what could be. Together, they balance caution and courage, the two forces every generation must master.

One whispers of legacy, the other of evolution, yet together they tell humanity’s oldest story, our unending quest to preserve value against time and to chase the light that never fades.

🙏 I ask (Allah) for guidance and success. 🤲

Bitcoin Cycle History Visualization [SwissAlgo]BTC 4-Year Cycle Tops & Bottoms

Historical visualization of Bitcoin's market cycles from 2010 to present, with projections based on weighted averages of past performance.

-----------------------------------------------------------------

CALCULATION METHODOLOGY

Why Bottom-to-Bottom Cycle Measurement?

This indicator defines cycles as bottom-to-bottom periods. This is one of several valid approaches to Bitcoin cycle analysis:

- Focuses on market behavior (price bottoms) rather than supply schedule events (halving-to-halving)

- Bottoms may offer good reference points for some analytical purposes

- Tops tend to be extended periods that are harder to define precisely

- Aligns with how some traditional asset cycles are measured and the timing observed in the broader "risk-on" assets category

- Halving events are shown separately (yellow backgrounds) for reference

- Neither halving-based nor bottom-based measurement is inherently superior

Different analysts prefer different cycle definitions based on their analytical goals. This approach prioritizes observable market turning points.

Cycle Date Definitions

- Approximate monthly ranges used for each event (e.g., Nov 2022 bottom = Nov 1-30, 2022)

- Cycle 1: Jul 2010 bottom → Jun 2011 top → Nov 2011 bottom

- Cycle 2: Nov 2011 bottom → Dec 2013 top → Jan 2015 bottom

- Cycle 3: Jan 2015 bottom → Dec 2017 top → Dec 2018 bottom

- Cycle 4: Dec 2018 bottom → Nov 2021 top → Nov 2022 bottom

- Future cycles will be added as new top/bottom dates become firm

Duration Calculations

- Days = timestamp difference converted to days (milliseconds ÷ 86,400,000)

- Bottom → Top: days from cycle bottom to peak

- Top → Bottom: days from peak to next cycle bottom

- Bottom → Bottom: full cycle duration (sum of above)

Price Change Calculations

- % Change = ((New Price - Old Price) / Old Price) × 100

- Example: $200 → $19,700 = ((19,700 - 200) / 200) × 100 = 9,750% gain

- Approximate historical prices used (rounded to significant figures)

Weighted Average Formula

Recent cycles weighted more heavily to reflect the evolved market structure:

- Cycle 1 (2010-2011): EXCLUDED (too early-stage, tiny market cap)

- Cycle 2 (2011-2015): Weight = 1x

- Cycle 3 (2015-2018): Weight = 3x

- Cycle 4 (2018-2022): Weight = 5x

Formula: Weighted Avg = (C2×1 + C3×3 + C4×5) / (1+3+5)

Example for Bottom→Top days: (761×1 + 1065×3 + 1066×5) / 9 = 1,032 days

Projection Method

- Projected Top Date = Nov 2022 bottom + weighted avg Bottom→Top days

- Projected Bottom Date = Nov 2022 bottom + weighted avg Bottom→Bottom days

- Current days elapsed compared to weighted averages

- Warning symbol (⚠) shown when the current cycle exceeds the historical average

Technical Implementation

- Historical cycle dates are hardcoded (not algorithmically detected)

- Dates represent approximate monthly ranges for each event

- The indicator will be updated as the Cycle 5 top and bottom dates become confirmed

- Updates require manual code maintenance - not automatic

- Users should verify they're using the latest version for current cycle data

-----------------------------------------------------------------

FEATURES

- Background highlights for historical tops (red), bottoms (green), and halving events (yellow)

- Data table showing cycle durations and price changes

- Visual cycle boundary boxes with subtle coloring

- Projected timeframes displayed as dashed vertical lines

- Toggle on/off for each visual element

- Customizable background colors

-----------------------------------------------------------------

DISPLAY SETTINGS

- Show/hide cycle tops, bottoms, halvings, data table, and cycle boxes

- Customizable background colors for each event type

- Clean, institutional-grade visual design suitable for analysis

UPDATES & MAINTENANCE

This indicator is maintained as new cycle events occur. When Cycle 5's top and bottom are confirmed with sufficient time elapsed, the code and projections will be updated accordingly. Check for the latest version periodically.

OPEN SOURCE

Code available for review, modification, and improvement. Educational transparency is prioritized.

-----------------------------------------------------------------

IMPORTANT LIMITATIONS

⚠ EXTREMELY SMALL SAMPLE SIZE

Based on only 4 complete cycles (2011-2022). In statistical analysis, this is insufficient for reliable predictions.

⚠ CHANGED MARKET STRUCTURE

Bitcoin's market has fundamentally evolved since early cycles:

- 2010-2015: Tiny market cap, retail-only, unregulated

- 2024-2025: Institutional adoption, spot ETFs, regulatory frameworks, macro correlation

The environment that created past patterns no longer exists in the same form.

⚠ NO PREDICTIVE GUARANTEE

Historical patterns can and do break. Market cycles are not laws of physics. Past performance does not guarantee future results. The next cycle may not follow historical averages.

⚠ LENGTHENING CYCLE THEORY

Some analysts believe cycles are extending over time (diminishing returns, maturing market). If true, simple averaging underestimates future cycle lengths.

⚠ SELF-FULFILLING PROPHECY RISK

The halving narrative may be partially circular - it works because people believe it works. Sufficient changes in market structure or participant behavior can invalidate the pattern.

⚠ APPROXIMATE DATA

Historical prices rounded to significant figures. Exact bottom/top dates vary by exchange. Month-long ranges are used for simplicity.

EDUCATIONAL USE ONLY

This indicator is designed for historical analysis and understanding Bitcoin's past behavior. It is NOT:

- Trading advice or financial recommendations

- A guarantee or prediction of future price movements

- Suitable as a sole basis for investment decisions

- A replacement for fundamental or technical analysis

The projections show "what if the pattern continues exactly" - not "what will happen."

Always conduct independent research, understand the risks, and consult qualified financial advisors before making investment decisions. Only invest what you can afford to lose.

Jackson Hole Meetings - Lines and LabelsThis TradingView Pine Script indicator marks the dates of the Federal Reserve’s annual Jackson Hole Economic Symposium meetings on your chart. For each meeting date from 2020 through 2025, it draws a red dashed vertical line directly on the corresponding daily bar. Additionally, it places a label above the bar indicating the year of the meeting (e.g., "JH 2025").

Features:

Marks all known Jackson Hole meeting dates from 2020 to 2025.

Draws a vertical dashed line on each meeting day for clear visual identification.

Displays a label above the candle with the meeting year.

Works best on daily timeframe charts.

Helps traders quickly spot potential market-moving events related to Jackson Hole meetings.

Use this tool to visually correlate price action with these key Federal Reserve events and enhance your trading analysis.

VWATR + VIX + VVIX Trend Regime### 🤖 VWATR + VIX + VVIX Trend Regime — Your Ultimate Volatility Dashboard! 📊

This isn't just another indicator; it's a comprehensive dashboard that brings together everything you need to understand market volatility focused on Futures. It merges price-based movement with market-wide fear and sentiment, giving you a powerful edge in your trading and risk management. Think of it as your personal volatility sidekick, ready to help you navigate market uncertainty like a pro!

***

### ✨ What's Inside?

* **VWATR (Volume-Weighted ATR):** A super-smart measure of price movement that pays close attention to where the big money is flowing.

* **VIX (The "Fear Gauge"):** Tracks the expected volatility of the S&P 500, essentially telling you how nervous the market is feeling.

* **VVIX (The "VIX of VIX"):** This one's for the pros! It measures how volatile the VIX itself is, giving you an early heads-up on potential fear spikes.

* **VX Term Structure:** A clever way to see if traders are preparing for a crisis. It compares the two nearest VIX futures to spot a rare signal called "backwardation."

* **Z-Scores:** It helps you spot when VIX and VVIX are at historic highs or lows, making it easier to predict when things might return to normal.

* **Divergence Score:** A unique tool to flag potential market shifts when the VIX and VVIX start moving in completely different directions.

* **Regime Classification:** The script automatically labels the market as "Full Panic," "Known Crisis," "Surface Calm," "Stress," or "Normal," so you always know where you stand.

* **Gradient Bars:** A visual treat! The background of your chart changes color to reflect real-time volatility shifts, giving you an instant feel for the market's mood.

* **Alerts:** Get push notifications on your phone for key events like "Full Panic" or "Backwardation" so you never miss a beat.

***

### 📝 Panel/Table Outputs

This is your mission control! The on-screen table gives you a clean summary of the current market regime, VIX and VVIX values, their ratios, term structure, Z-scores, and signals. Everything you need, right where you can see it.

***

### 🚀 How to Get Started

1. **Check your data:** You'll need access to real-time data for VIX, VVIX, VX1!, and VX2!. A paid subscription might be necessary for this.

2. **Add it to your chart:** Use the indicator on any chart (we've set it to `overlay=false`) to get your full volatility dashboard.

3. **Tweak it to perfection:** Head over to the Settings panel to customize the thresholds, colors, and your all-important "Jolt Value."

4. **Start trading smarter:** Use the dashboard to inform your trades, hedge your portfolio, and manage risk with confidence.

***

### ⚙️ Customization & Key Settings

* `showVWATR`: Toggle your price-volatility metric on or off.

* `showExpectedVol`: See the expected volatility as a percentage of the current price.

* `joltLevel`: This is a very important line on your chart! It's your personal trigger for when volatility is getting a little too wild. More on this below.

* `enableGradientBars`: Turn the awesome colored background on or off.

* `enableTable`: Hide or show your information table.

* `VIX/VVIX/VX1!/VX2! symbols`: If your broker uses different symbols for these, you can change them here.

* `VIX/VVIX thresholds`: Adjust these levels to fine-tune the indicator to your personal risk tolerance.

***

### 💡 Jolt Value: A Quick Guide for Smart Traders 🧠

The **jolt value** is your personal tripwire for volatility. Think of it as a warning light on your car's dashboard. You set the level, and when volatility (VWATR) crosses that line, you get an instant signal that something interesting is happening.

**How to Set Your Jolt Value:**

The ideal jolt value is dynamic. You want to keep it just a little above the current VIX level to stay alert without getting too many false alarms.

| Current VIX Level | Market Regime | Recommended Jolt Value |

| :--- | :--- | :--- |

| Under 15 | Calm/Complacent | 15–16 |

| 15–20 | Typical/Normal | 16–18 |

| 20–30 | Cautious/Active | 18–22 |

| Over 30 | Stress/Panic | 30+ |

**A Pro Tip for August 2025:** Since the VIX is hovering around 14.7, setting your jolt value to **16.5** is a great starting point for keeping an eye on things. If the VIX starts to climb above 20, you should adjust your jolt level to match the new reality.

***

### ⚠️ Important Things to Note

* You might experience some data delays if you're not on a paid TradingView plan or your broker does not provide real-time data for the VIX also VIX is only active during NY session, so it's not advised to use it outside of normal trading hours!

Multi-EMA Crossover StrategyMulti-EMA Crossover Strategy

This strategy uses multiple exponential moving average (EMA) crossovers to identify bullish trends and execute long trades. The approach involves progressively stronger signals as different EMA pairs cross, indicating increasing bullish momentum. Each crossover triggers a long entry, and the intensity of bullish sentiment is reflected in the color of the bars on the chart. Conversely, bearish trends are represented by red bars.

Strategy Logic:

First Long Entry: When the 1-day EMA crosses above the 5-day EMA, it signals initial bullish momentum.

Second Long Entry: When the 3-day EMA crosses above the 10-day EMA, it confirms stronger bullish sentiment.

Third Long Entry: When the 5-day EMA crosses above the 20-day EMA, it indicates further trend strength.

Fourth Long Entry: When the 10-day EMA crosses above the 40-day EMA, it suggests robust long-term bullish momentum.

The bar colors reflect these conditions:

More blue bars indicate stronger bullish sentiment as more short-term EMAs are above their longer-term counterparts.

Red bars represent bearish conditions when short-term EMAs are below longer-term ones.

Example: Bitcoin Trading on a Daily Timeframe

Bullish Scenario:

Imagine Bitcoin is trading at $30,000 on March 31, 2025:

First Signal: The 1-day EMA crosses above the 5-day EMA at $30,000. This suggests initial upward momentum, prompting a small long entry.

Second Signal: A few days later, the 3-day EMA crosses above the 10-day EMA at $31,000. This confirms strengthening bullish sentiment; another long position is added.

Third Signal: The 5-day EMA crosses above the 20-day EMA at $32,500, indicating further upward trend development; a third long entry is executed.

Fourth Signal: Finally, the 10-day EMA crosses above the 40-day EMA at $34,000. This signals robust long-term bullish momentum; a fourth long position is entered.

Bearish Scenario:

Suppose Bitcoin reverses from $34,000 to $28,000:

The 1-day EMA crosses below the 5-day EMA at $33,500.

The 3-day EMA dips below the 10-day EMA at $32,000.

The 5-day EMA falls below the 20-day EMA at $30,000.

The final bearish signal occurs when the 10-day EMA drops below the 40-day EMA at $28,000.

The bars turn increasingly red as bearish conditions strengthen.

Advantages of This Strategy:

Progressive Confirmation: Multiple crossovers provide layered confirmation of trend strength.

Visual Feedback: Bar colors help traders quickly assess market sentiment and adjust positions accordingly.

Flexibility: Suitable for trending markets like Bitcoin during strong rallies or downturns.

Limitations:

Lagging Signals: EMAs are lagging indicators and may react slowly to sudden price changes.

False Breakouts: Crossovers in choppy markets can lead to whipsaws or false signals.

This strategy works best in trending markets and should be combined with additional risk management techniques, e.g., stop loss or optimal position sizes (Kelly Criterion).

Cash And Carry Arbitrage BTC Compare Month 6 by SeoNo1Detailed Explanation of the BTC Cash and Carry Arbitrage Script

Script Title: BTC Cash And Carry Arbitrage Month 6 by SeoNo1

Short Title: BTC C&C ABT Month 6

Version: Pine Script v5

Overlay: True (The indicators are plotted directly on the price chart)

Purpose of the Script

This script is designed to help traders analyze and track arbitrage opportunities between the spot market and futures market for Bitcoin (BTC). Specifically, it calculates the spread and Annual Percentage Yield (APY) from a cash-and-carry arbitrage strategy until a specific expiry date (in this case, June 27, 2025).

The strategy helps identify profitable opportunities when the futures price of BTC is higher than the spot price. Traders can then buy BTC in the spot market and short BTC futures contracts to lock in a risk-free profit.

1. Input Settings

Spot Symbol: The real-time BTC spot price from Binance (BTCUSDT).

Futures Symbol: The BTC futures contract that expires in June 2025 (BTCUSDM2025).

Expiry Date: The expiration date of the futures contract, set to June 27, 2025.

These inputs allow users to adjust the symbols or expiry date according to their trading needs.

2. Price Data Retrieval

Spot Price: Fetches the latest closing price of BTC from the spot market.

Futures Price: Fetches the latest closing price of BTC futures.

Spread: The difference between the futures price and the spot price (futures_price - spot_price).

The spread indicates how much higher (or lower) the futures price is compared to the spot market.

3. Time to Maturity (TTM) and Annual Percentage Yield (APY) Calculation

Current Date: Gets the current timestamp.

Time to Maturity (TTM): The number of days left until the futures contract expires.

APY Calculation:

Formula:

APY = ( Spread / Spot Price ) x ( 365 / TTM Days ) x 100

This represents the annualized return from holding a cash-and-carry arbitrage position if the trader buys BTC at the spot price and sells BTC futures.

4. Display Information Table on the Chart

A table is created on the chart's top-right corner showing the following data:

Metric: Labels such as Spread and APY

Value: Displays the calculated spread and APY

The table automatically updates at the latest bar to display the most recent data.

5. Alert Condition

This sets an alert condition that triggers every time the script runs.

In practice, users can modify this alert to trigger based on specific conditions (e.g., APY exceeds a threshold).

6. Plotting the APY and Spread

APY Plot: Displays the annualized yield as a blue line on the chart.

Spread Plot: Visualizes the futures-spot spread as a red line.

This helps traders quickly identify arbitrage opportunities when the spread or APY reaches desirable levels.

How to Use the Script

Monitor Arbitrage Opportunities:

A positive spread indicates a potential cash-and-carry arbitrage opportunity.

The larger the APY, the more profitable the arbitrage opportunity could be.

Timing Trades:

Execute a buy on the BTC spot market and simultaneously sell BTC futures when the APY is attractive.

Close both positions upon futures contract expiry to realize profits.

Risk Management:

Ensure you have sufficient margin to hold both positions until expiry.

Monitor funding rates and volatility, which could affect returns.

Conclusion

This script is an essential tool for traders looking to exploit price discrepancies between the BTC spot market and futures market through a cash-and-carry arbitrage strategy. It provides real-time data on spreads, annualized returns (APY), and visual alerts, helping traders make informed decisions and maximize their profit potential.

Ripple (XRP) Model PriceAn article titled Bitcoin Stock-to-Flow Model was published in March 2019 by "PlanB" with mathematical model used to calculate Bitcoin model price during the time. We know that Ripple has a strong correlation with Bitcoin. But does this correlation have a definite rule?

In this study, we examine the relationship between bitcoin's stock-to-flow ratio and the ripple(XRP) price.

The Halving and the stock-to-flow ratio

Stock-to-flow is defined as a relationship between production and current stock that is out there.

SF = stock / flow

The term "halving" as it relates to Bitcoin has to do with how many Bitcoin tokens are found in a newly created block. Back in 2009, when Bitcoin launched, each block contained 50 BTC, but this amount was set to be reduced by 50% every 210,000 blocks (about 4 years). Today, there have been three halving events, and a block now only contains 6.25 BTC. When the next halving occurs, a block will only contain 3.125 BTC. Halving events will continue until the reward for minors reaches 0 BTC.

With each halving, the stock-to-flow ratio increased and Bitcoin experienced a huge bull market that absolutely crushed its previous all-time high. But what exactly does this affect the price of Ripple?

Price Model

I have used Bitcoin's stock-to-flow ratio and Ripple's price data from April 1, 2014 to November 3, 2021 (Daily Close-Price) as the statistical population.

Then I used linear regression to determine the relationship between the natural logarithm of the Ripple price and the natural logarithm of the Bitcoin's stock-to-flow (BSF).

You can see the results in the image below:

Basic Equation : ln(Model Price) = 3.2977 * ln(BSF) - 12.13

The high R-Squared value (R2 = 0.83) indicates a large positive linear association.

Then I "winsorized" the statistical data to limit extreme values to reduce the effect of possibly spurious outliers (This process affected less than 4.5% of the total price data).

ln(Model Price) = 3.3297 * ln(BSF) - 12.214

If we raise the both sides of the equation to the power of e, we will have:

============================================

Final Equation:

■ Model Price = Exp(- 12.214) * BSF ^ 3.3297

Where BSF is Bitcoin's stock-to-flow

============================================

If we put current Bitcoin's stock-to-flow value (54.2) into this equation we get value of 2.95USD. This is the price which is indicated by the model.

There is a power law relationship between the market price and Bitcoin's stock-to-flow (BSF). Power laws are interesting because they reveal an underlying regularity in the properties of seemingly random complex systems.

I plotted XRP model price (black) over time on the chart.

Estimating the range of price movements

I also used several bands to estimate the range of price movements and used the residual standard deviation to determine the equation for those bands.

Residual STDEV = 0.82188

ln(First-Upper-Band) = 3.3297 * ln(BSF) - 12.214 + Residual STDEV =>

ln(First-Upper-Band) = 3.3297 * ln(BSF) – 11.392 =>

■ First-Upper-Band = Exp(-11.392) * BSF ^ 3.3297

In the same way:

■ First-Lower-Band = Exp(-13.036) * BSF ^ 3.3297

I also used twice the residual standard deviation to define two extra bands:

■ Second-Upper-Band = Exp(-10.570) * BSF ^ 3.3297

■ Second-Lower-Band = Exp(-13.858) * BSF ^ 3.3297

These bands can be used to determine overbought and oversold levels.

Estimating of the future price movements

Because we know that every four years the stock-to-flow ratio, or current circulation relative to new supply, doubles, this metric can be plotted into the future.

At the time of the next halving event, Bitcoins will be produced at a rate of 450 BTC / day. There will be around 19,900,000 coins in circulation by August 2025

It is estimated that during first year of Bitcoin (2009) Satoshi Nakamoto (Bitcoin creator) mined around 1 million Bitcoins and did not move them until today. It can be debated if those coins might be lost or Satoshi is just waiting still to sell them but the fact is that they are not moving at all ever since. We simply decrease stock amount for 1 million BTC so stock to flow value would be:

BSF = (19,900,000 – 1.000.000) / (450 * 365) =115.07

Thus, Bitcoin's stock-to-flow will increase to around 115 until AUG 2025. If we put this number in the equation:

Model Price = Exp(- 12.214) * 114 ^ 3.3297 = 36.06$

Ripple has a fixed supply rate. In AUG 2025, the total number of coins in circulation will be about 56,000,000,000. According to the equation, Ripple's market cap will reach $2 trillion.

Note that these studies have been conducted only to better understand price movements and are not a financial advice.

Multi-Timeframe MACD with Color Mix (Nikko)Multi-Timeframe MACD with Color Mix (Nikko) Indicator

This documentation explains the benefits of the "Multi-Timeframe MACD with Color Mix (Nikko)" indicator for traders and provides easy-to-follow steps on how to use it. Written as of 05:06 AM +07 on Saturday, October 04, 2025, this guide focuses on helping you, as a trader, get the most out of this tool with clear, practical advice before diving into the technical details.

Benefits for Traders

1. Multi-Timeframe Insight

This indicator lets you see momentum trends across 15-minute, 1-hour, 1-day, and 1-week timeframes all on one chart. This big-picture view helps you catch both quick market moves and long-term trends without flipping between charts, saving you time and giving you a fuller understanding of the market.

2. Visual Momentum Representation

The background changes from red to green based on short-term (15m) momentum, giving you a quick, easy-to-see signal—red means bearish (prices might drop), and green means bullish (prices might rise). The histogram uses a mix of red, green, and blue colors to show the combined strength of the 1-hour, 1-day, and 1-week timeframes, helping you spot strong trends at a glance (e.g., a bright mix for strong momentum, darker for weaker).

3. Enhanced Decision-Making

The background and histogram colors work together to confirm trends across different timeframes, making it less likely you’ll act on a false signal. This helps you feel more confident when deciding when to buy, sell, or hold.

4. Proactive Alert System

You can set alerts to notify you when the percentage of bullish timeframes hits your chosen levels (e.g., below 10% for bearish, above 90% for bullish). This keeps you in the loop on big momentum shifts without needing to watch the chart all day—perfect for when you’re busy.

5. Flexibility and Efficiency

You can turn timeframes on or off, adjust settings like speed of the moving averages, and tweak transparency to fit your trading style—whether you’re a fast scalper or a patient swing trader. Everything is shown on one chart, saving you effort, and the colors make it simple to read, even if you’re new to trading.

How to Use It

Getting Started

Add the Indicator: Load the "Multi-Timeframe MACD with Color Mix (Nikko)" onto your TradingView chart using the Pine Script editor or indicator library.

Pick Your Timeframes: Turn on the timeframes that match your trading—use 15m and 1h for quick trades, or 1d and 1w for longer holds—using the enable_15m, enable_1h, enable_1d, enable_1w, and enable_background options.

Reading the Colors

Background Gradient: Watch for red to signal bearish 15m momentum and green for bullish momentum. Adjust the Background_transparency (default 75%, or 25% opacity) if the chart feels too busy—try lowering it to 50 for clearer candlesticks in fast markets.

Histogram and EMA Colors:

The histogram and its Exponential Moving Average (EMA) line show a mix of red (1-week), green (1-day), and blue (1-hour) based on how strong the momentum is in each timeframe.

Brighter colors mean stronger momentum—white (all bright) shows all timeframes are pushing up hard, while darker shades (like gray or black) mean weaker or mixed momentum.

Turn off a timeframe (e.g., enable_1h = false) to see how it changes the color mix and focus on what matters to you.

Setting Alerts

Set Your Levels: Choose a threshold_low (default 10%) and threshold_high (default 90%) based on your comfort zone or past market patterns to catch big turns.

Get Notifications: Use TradingView alerts to get pings when the market hits your set levels, so you can act without staring at the screen.

Practical Tips

Pair with Other Tools: Use it with support/resistance lines or the RSI to double-check your moves and build a solid plan.

Tweak Settings: Adjust fast_length, slow_length, and signal_smoothing to match your asset’s speed, and bump up the lookback (default 50) for steadier trends in wild markets.

Practice First: Test different timeframe combos on a demo account to find what works best for you.

Understanding the Colors (Simple Explanation)

How Colors Work

The histogram and its EMA line use a color mix based on a simple idea from color theory, like mixing paints with red, green, and blue (RGB):

Red comes from the 1-week timeframe, green from 1-day, and blue from 1-hour.

When all three timeframes show strong upward momentum, they blend into bright white—the brightest color, like a super-bright light telling you the market’s roaring up.

If some timeframes are weak or pulling down, the mix gets darker (like gray or black), warning you the momentum might not be solid.

Brighter is Better

Bright Colors = Strong Opportunity: The brighter the histogram and EMA (closer to white), the more all your chosen timeframes are in agreement that prices are rising. This is your signal to think about buying or holding, as it points to a powerful trend you can ride.

Dark Colors = Caution: A darker mix (toward black) means some timeframes are lagging or bearish, suggesting you might wait or consider selling. It’s like a dim light saying, “Hold on, check again.”

Benefit in Practice: Watching the brightness helps you jump on the best trades fast. For example, a bright white histogram on a green background is like a green traffic light—go for it! A dark gray on red is like a red light—pause and rethink. This quick color check can save you from bad moves and boost your profits when the trend is strong.

Why It Helps

These colors are your fast friend in trading. A bright histogram means all your timeframes are cheering for an uptrend, giving you the confidence to act. A dull one tells you to be careful, helping you avoid traps. It’s like having a color-coded guide to pick the hottest market moments!

Technical Details

Input Parameters

Fast Length (default: 12): Short-term moving average speed.

Slow Length (default: 26): Long-term moving average speed.

Source (default: close): Price data used.

Signal Smoothing (default: 9): Smooths the signal line.

MA Type (default: EMA): Choose EMA or SMA.

Timeframe and Scaling

Timeframes: 15m, 1h, 1d, 1w, with on/off switches.

Lookback Period (default: 50): Sets the data window for trends.

Background Transparency (default: 75%): Controls background see-through level.

MACD Calculation

Per Timeframe: Uses request.security():

MACD Line: ta.ema(src, fast_length) - ta.ema(src, slow_length).

Signal Line: ta.ema(MACD, signal_length).

Histogram: (macd - signal) / 3.0.

Background Gradient

15m Normalization: norm_value = (hist_15m - hist_15m_min) / max(hist_15m_range, 1e-10), limited to 0-1.

RGB Mix: Red drops from 255 to 0, green rises from 0 to 255, blue stays 0.

Apply: color.new(color.rgb(r_val, g_val, b_val), Background_transparency).

Histogram and EMA Colors

Color Assignment:

1h: Blue (#0000FF) if hist_1h >= 0, else black.

1d: Green (#00FF00) if hist_1d >= 0, else black.

1w: Red (#FF0000) if hist_1w >= 0, else black.

Final Color: final_color = color.rgb(min(r, 255), min(g, 255), min(b, 255)).

Plotting: Histogram and EMA use final_color; MACD (#2962FF), signal (#FF6D00).

Alerts

Bullish Percentage: bullish_pct = (bullish_count / bullish_total) * 100, counting hist >= 0.

Triggers: Below threshold_low or above threshold_high.

--------------------------------------------------------------------

Conclusion

The "Multi-Timeframe MACD with Color Mix (Nikko)" is your all-in-one tool to spot trends, confirm moves, and trade smarter with its bright, easy-to-read colors. By using it wisely, you can sharpen your market edge and trade with more confidence.

This README is tailored for traders and reflects the indicator's practical value as of 05:06 AM +07 on October 04, 2025.

Enhanced Retail vs Institutional ActivityThis script highlights market activity in real-time, making it easier to infer the type of market participants driving price and volume changes.

Here’s a list of what the script analyzes:

Volume:

Current volume of the candle.

Moving average of volume over a specified number of periods.

Volume spikes: Current volume compared to a threshold multiple of the moving average.

Price Movement:

Percentage change in price between the current and previous candle.

Identifies significant price changes based on a user-defined threshold.

Institutional Activity:

High volume spikes combined with significant price movements.

Retail Activity:

Periods without volume spikes or significant price changes.

VWAP (Volume-Weighted Average Price):

The average traded price over a specified lookback period, weighted by volume, used as a benchmark.

Market Context Visualization:

Background colors to differentiate institutional (red) and retail (green) activity.

Overlays for:

-Volume bars.

-Average volume line.

-VWAP line.

In summary:

Red = Institutional activity: High volume + significant price change.

Green = Retail activity: Low volume or insignificant price change.

---------------------------------------------------------------------------------------------------------------------

Analysis Explanation:

I’m forecasting that Bitcoin will retest its November 12th low (~$85,098.75) around January 20th, 2025, where the horizontal support line intersects with the downtrend line. This conclusion is based on the following:

Trend Analysis:

The chart shows a clear downtrend with price respecting the descending trendline.

The intersection of the horizontal support and the downtrend line on January 20th indicates a confluence point where price action may gravitate.

Volume and Activity Insights:

Using the Retail vs Institutional Activity indicator, the chart highlights periods dominated by institutional (red background) or retail (green background) activity.

Current price action is in a green zone, suggesting predominantly retail participation with lower volume and insignificant price movements.

Retail vs Institutional Dynamics:

Institutional activity (red zones) aligns with significant price movements and volume spikes, often marking key turning points or trends.

The recent green retail-dominated periods suggest a lack of strong momentum, which may lead to continued price decline until institutions re-enter around the confluence area.

Volume Observations:

Volume remains relatively low during the current retail phase, indicating weak buying pressure.

A potential surge in institutional activity (red zones) near the support level could trigger a rebound or breakdown.

I expect Bitcoin’s price to drop further and test the November 12th low near $85,098.75 on January 20th, 2025. This projection is supported by the convergence of the downtrend line and horizontal support, low retail-driven volume, and historical institutional activity patterns observed using the "Retail vs Institutional Activity" indicator.

Advanced VWAP CalendarThe Advanced VWAP Calendar is a designed to plot Volume Weighted Average Price (VWAP) lines anchored to user-defined and preset time periods, including weekly, monthly, quarterly, and custom anchors. As of August 15, 2025, this indicator provides traders with a robust tool for analyzing price trends relative to volume-weighted averages, with clear labeling and extensive customization options. Below is a summary of its key features and functionality, with technical details and code references updated to focus on user-facing behavior and presentation, while preserving all other aspects of the original summary.

Key Features

Multiple Time Period VWAPs:

Weekly VWAPs: Supports up to five VWAPs for a user-selected month and year, starting at midnight each Monday (e.g., W1 Aug 2025, W2 Aug 2025). Enabled via a single toggle, with anchors automatically set to the first Monday of the chosen month.

Monthly VWAPs: Plots VWAPs for all 12 months of a selected year (e.g., Jan 2025, Feb 2025) or a single user-specified month/year. Labels use month abbreviations (e.g., "Aug 2025").

Quarterly VWAPs: Covers four quarters of a selected year (e.g., Q1 2025, Q2 2025), with options to enable all quarters or individual ones (Q1–Q4).

Legacy VWAPs: Provides monthly and quarterly VWAPs for a user-selected legacy year (e.g., 2024), labeled with a "Legacy" prefix (e.g., "Legacy Jan 2024," "Legacy Q1 2024"), with similar enablement options.

Custom VWAPs: Includes 10 fully customizable VWAPs, each with user-defined anchor times, labels (e.g., "Q1 2025"), colors, line widths (1–5), text colors, bubble styles, text sizes (8–40), and background options.

Clear and Dynamic Labeling:

Labels appear to the right of the chart, showing the VWAP value (e.g., "Q1 2025 123.45").

Weekly labels follow a "W# Month Year" format (e.g., "W1 Aug 2025").

Monthly labels use abbreviated months (e.g., "Aug 2025"), while quarterly labels use "Q# Year" (e.g., "Q3 2025").

Legacy labels include a "Legacy" prefix (e.g., "Legacy Q1 2024").

Labels support customizable text sizes (tiny to huge) and can be displayed with or without a background, with optional bubble styles.

Flexible Customization:

Each VWAP can be enabled or disabled independently, with user inputs for anchor times, labels, and visual properties.

Colors are predefined for weekly (red, orange, blue, green, purple), monthly (varied), quarterly (red, blue, green, yellow), and legacy VWAPs, but custom VWAPs allow any color selection.

Line widths and text sizes are adjustable, ensuring visual clarity and chart readability.

This indicator was a dual effort, code was heavily contributed in effort by AzDxB, major credit and THANKS goes to him www.tradingview.com

Hosoda’s CloudsMany investors aim to develop trading systems with a high win rate, mistakenly associating it with substantial profits. In reality, high returns are typically achieved through greater exposure to market trends, which inevitably lowers the win rate due to increased risk and more volatile conditions.

The system I present, called “Hosoda’s Clouds” in honor of Goichi Hosoda , the creator of the Ichimoku Kinko Hyo indicator, is likely one of the first profitable systems many traders will encounter. Designed to capture trends, it performs best in markets with clear directional movements and is less suitable for range-bound markets like Forex, which often exhibit lateral price action.

This system is not recommended for low timeframes, such as minute charts, due to the random and emotionally driven nature of price movements in those periods. For a deeper exploration of this topic, I recommend reading my article “Timeframe is Everything”, which discusses the critical importance of selecting the appropriate timeframe.

I suggest testing and applying the “Hosoda’s Clouds” strategy on assets with a strong trending nature and a proven track record of performance. Ideal markets include Tesla (1-hour, 4-hour, and daily), BTC/USDT (daily), SPY (daily), and XAU/USD (daily), as these have consistently shown clear directional trends over time.

Commissions and Configuration

Commissions can be adjusted in the system’s settings to suit individual needs. For evaluating the effectiveness of “Hosoda’s Clouds,” I’ve used a standard commission of $1 per order as a baseline, though this can be modified in the code to accommodate different brokers or preferences.

The margin per trade is set to $1,000 by default, but users are encouraged to experiment with different margin settings in the configuration to match their trading style.

Rules of the “Hosoda’s Clouds” System (Bullish Strategy)

This strategy is designed to capture trending movements in bullish markets using the Ichimoku Kinko Hyo indicator. The rules are as follows:

Long Entry: A long position is triggered when the Tenkan-sen crosses above the Kijun-sen below the Ichimoku cloud, identifying potential reversals or bounces in a bearish context.

Stop Loss (SL): Placed at the low of the candle 12 bars prior to the entry candle. This setting has proven optimal in my tests, but it can be adjusted in the code based on risk tolerance.

Take Profit (TP): The position is closed when the Tenkan-sen crosses below the bottom of the Ichimoku cloud (the minimum of Senkou Span A and Senkou Span B).

Notes on the Code

margin_long=0: Ideal for strategies requiring a fixed position size, particularly useful for manual entries or testing with a constant capital allocation.

margin_long=100: Recommended for high-frequency systems where positions are closed quickly, simulating gradual growth based on realized profits and reflecting real-world broker constraints.

System Performance

The following performance metrics account for $1 per order commissions and were tested on the specified assets and timeframes:

Tesla (H1)

Trades: 148

Win Rate: 29.05%

Period: Jan 2, 2014 – Jan 6, 2020 (+172%)

Simple Annual Growth Rate: +34.3%

Trades: 130

Win Rate: 30.77%

Period: Jan 2, 2020 – Sep 24, 2025 (+858.90%)

Simple Annual Growth Rate: +150.7%

Tesla (H4)

Trades: 102

Win Rate: 32.35%

Period: Jun 29, 2010 – Sep 24, 2025 (+11,356.36%)

Simple Annual Growth Rate: +758.5%

Tesla (Daily)

Trades: 56

Win Rate: 35.71%

Period: Jun 29, 2010 – Sep 24, 2025 (+3,166.64%)

Simple Annual Growth Rate: +211.5%

BTC/USDT (Daily)

Trades: 44

Win Rate: 31.82%

Period: Sep 30, 2017 – Sep 24, 2025 (+2,592.23%)

Simple Annual Growth Rate: +324.8%

SPY (Daily)

Trades: 81

Win Rate: 37.04%

Period: Jan 23, 1993 – Sep 24, 2025 (+476.90%)

Simple Annual Growth Rate: +14.3%

XAU/USD (Daily)

Trades: 216

Win Rate: 32.87%

Period: Jan 6, 1833 – Sep 24, 2025 (+5,241.73%)

Simple Annual Growth Rate: +27.1%

SPX (Daily)

Trades: 217

Win Rate: 38.25%

Period: Feb 1, 1871 – Sep 24, 2025 (+16,791.02%)

Simple Annual Growth Rate: +108.1%

Conclusion

With the “ Hosoda’s Clouds ” strategy, I aim to showcase the potential of technical analysis to generate consistent profits in trending markets, challenging recent doubts about its effectiveness. My goal is for this system to serve as both a practical tool for traders and a source of inspiration for the trading community I deeply respect. I hope it encourages the creation of new strategies, fosters creativity in technical analysis, and empowers traders to approach the markets with confidence and discipline.

EMA + VWMA + ATR Smoothed BuySell (merged) - TOM ZENG 202509Logic and Functionality Analysis

The script is divided into three main logical sections: EMA trend analysis, ATR-based signal generation, and VWMA smoothing.

1. EMA Trend Analysis (EMA Fan) 📈

This section uses a series of Exponential Moving Averages (EMAs) to identify trends. You've wisely chosen a set of EMA lengths (8, 21, 50, 200) that are commonly used in trading. These numbers are often derived from the Fibonacci sequence and are believed to offer a good balance of sensitivity to recent price action while still reflecting the underlying trend.

Purpose: The EMAs serve as dynamic support and resistance levels. When the price is above the EMAs and they are fanned out in ascending order (short-term EMA above long-term EMA), it indicates a strong uptrend. Conversely, a descending order indicates a downtrend.

Customization: The code allows you to easily adjust the EMA lengths in the inputs section, giving you control over the sensitivity of your trend analysis.

2. ATR Trailing Stop (Buy/Sell Signals) 🎯

This is the core of the indicator's signal-generating capability. It uses the Average True Range (ATR) to create a dynamic trailing stop line. The ATR measures volatility, so the stop line adjusts automatically to wider price swings.

Logic: The script uses a var float variable xATRTrailingStop to store the value of the stop line from the previous bar. The code then determines the current bar's stop line by comparing the current price to the previous bar's stop line and using math.max and math.min to smoothly move the line along with the trend.

Signal Generation: The pos variable tracks whether the trend is long (pos = 1) or short (pos = -1). The isLong and isShort variables act as a state machine, ensuring that the "Buy" and "Sell" signals are only triggered once at the exact point of a crossover, rather than on every subsequent bar.

Visuals & Alerts: The plotshape functions create labels directly on the chart, and the barcolor function changes the color of the candlesticks, providing a clear visual representation of the current trend state. The alertcondition functions are crucial for automation, allowing you to set up notifications for when a signal occurs.

3. VWMA and Combined Average 🌊

This section introduces a Volume-Weighted Moving Average (VWMA), which gives more weight to periods of high trading volume. This makes the VWMA more responsive to significant moves that are backed by strong institutional buying or selling.

Combined Logic: The avg1 variable creates a new line by averaging the VWMA and the xATRTrailingStop line. This is an innovative approach to blend two different types of analysis—volume-based trend and volatility-based risk management—into a single, smoothed line. It can act as an additional filter or a unique trading signal on its own.

Summary

Your code is a very effective and clean example of a multi-faceted indicator. It correctly implements a robust ATR trailing stop for signals while also providing valuable trend context through EMAs and volume analysis through VWMA. The combination of these elements makes it a powerful tool for a trader looking for a comprehensive view of the market.

AInfluence Manual Data Input Utility Indicator V101AInfluence (Manual Data Input Utility Indicator) V101

Overview

This utility indicator enables you to plot an external data series directly on your TradingView chart. It is designed for users who want to correlate custom datasets, such as sentiment analysis, economic data, or other external metrics, with price action.

Instructions

1. Add the indicator to your chart.

2. Go into the indicator's "Settings" panel.

3. Paste your pre-formatted data into the text input field.

Data Formatting Rules

The script requires a specific format for each data point, which consists of a numerical value and a timestamp

• Structure: Each data point must be on a new line.

• Limit: You can paste a maximum of 146 records.

Example Data:

93.1562,2025-09-06 00:59:11

94.9062,2025-09-06 01:59:21

93.4062,2025-09-06 02:59:18

95.2188,2025-09-06 03:59:31

93.4062,2025-09-06 04:59:21

91.4583,2025-09-06 05:58:51

93.7812,2025-09-06 06:59:17

The source code for this indicator is open and accessible.

Golden Cross 50/200Simplicity characterizes each of my trading systems and methods. On this occasion, I present a trend-following strategy with simple rules and high profitability.

System Rules:

-Long entries when the 50 EMA crosses above the 200 EMA.

-Stop Loss (SL) placed at the low of 15 candles prior to the entry candle.

-Take Profit (TP) triggered when the 50 EMA crosses below the 200 EMA.

As with any trend-following system, we sacrifice win rate for profitability, and of course, we will focus on traditional markets with a consistent trend-following nature over time.

Recommended Markets and Timeframes:

BTCUSDT H6

August 17, 2017 - October 20, 2025 Total trades: 30

Profitability: +1,682.99%

Win rate: 40%

Outperforms Buy & Hold

BTCUSDT H4

August 17, 2017 - October 20, 2025 Total trades: 42

Profitability: +12,213.49% (high and stable performance curve)

Win rate: 40%

Outperforms Buy & Hold

BTCUSDT H2

August 17, 2017 - October 20, 2025 Total trades: 95

Profitability: +2,363.80%

Win rate: 24.21%

Matches Buy & Hold

BTCUSDT H1

August 17, 2017 - October 20, 2025 Total trades: 203

Profitability: +1,045% (stable performance curve)

Win rate: 25.62%

BTCUSDT 30M

August 17, 2017 - October 20, 2025 Total trades: 393

Profitability: +4,205.51% (high and stable performance curve)

Win rate: 27.74%

Outperforms Buy & Hold

BTCUSDT 15M

August 17, 2017 - October 20, 2025 Total trades: 821

Profitability: +1,311.97%

Win rate: 23.14%

Timeframes such as Daily, 12-hour, 8-hour, and even 5-minute charts are profitable with this system, so feel free to experiment.

Other markets and timeframes to observe include:

-XAUUSD (H1, H4, H6, H8, Daily)

-SPX (Daily: +21,302% profitability since 1871 in 40 trades)

-Tesla (H1, H2, H4, H6, especially M30 and M15)

-Apple (M5, M15, M30, H1, H2, H4…)

-Warner Bros (M5, M15, M30…)

-GOOGL (M5, M15, M30, H1, H2, H4, H6…)

-AMZN (M5, M15, M30, H2, H4, H6…)

-META (M5, M15, M30, H1, H2, H4…)

-NVDA (M5, M15, M30, H1, H2, H4…)

This system not only generates significant profitability but also performs very well in traditional markets, even on lower timeframes like 5-minute charts. In many cases, the returns far exceed Buy & Hold.

I hope this strategy is useful to you. Follow my Spanish-speaking profile if you want to see my market analyses, and send me your good vibes!

Boilerplate Configurable Strategy [Yosiet]This is a Boilerplate Code!

Hello! First of all, let me introduce myself a little bit. I don't come from the world of finance, but from the world of information and communication technologies (ICT) where we specialize in data processing with the aim of automating it and eliminating all human factors and actors in the processes. You could say that I am an algotrader.

That said, in my journey through trading in recent years I have understood that this world is often shown to be incomplete. All those who want to learn about trading only end up learning a small part of what it really entails, they only seek to learn how to read candlesticks. Therefore, I want to share with the entire community a fraction of what I have really understood it to be.

As a computer scientist, the most important thing is the data, it is the raw material of our work and without data you simply cannot do anything. Entropy is simple: Data in -> Data is transformed -> Data out.

The quality of the outgoing data will directly depend on the incoming data, there is no greater mystery or magic in the process. In trading it is no different, because at the end of the day it is nothing more than data. As we often say, if garbage comes in, garbage comes out.

Most people focus on the results only, on the outgoing data, because in the end we all want the same thing, to make easy money. Very few pay attention to the input data, much less to the process.

Now, I am not here to delude you, because there is no bigger lie than easy money, but I am here to give you a boilerplate code that will help you create strategies where you only have to concentrate on the quality of the incoming data.

To the Point

The code is a strategy boilerplate that applies the technique that you decide to customize for the criteria for opening a position. It already has the other factors involved in trading programmed and automated.

1. The Entry

This section of the boilerplate is the one that each individual must customize according to their needs and knowledge. The code is offered with two simple, well-known strategies to exemplify how the code can be reused for your own benefits.

For the purposes of this post on tradingview, I am going to use the simplest of the known strategies in trading for entries: SMA Crossing

// SMA Cross Settings

maFast = ta.sma(close, length)

maSlow = ta.sma(open, length)

The Strategy Properties for all cases published here:

For Stock TSLA H1 From 01/01/2025 To 02/15/2025

For Crypto XMR-USDT 30m From 01/01/2025 To 02/15/2025

For Forex EUR-USD 5m From 01/01/2025 To 02/15/2025

But the goal of this post is not to sell you a dream, else to show you that the same Entry decision works very well for some and does not for others and with this boilerplate code you only have to think of entries, not exits.

2. Schedules, Days, Sessions

As you know, there are an infinite number of markets that are susceptible to the sessions of each country and the news that they announce during those sessions, so the code already offers parameters so that you can condition the days and hours of operation, filter the best time parameters for a specific market and time frame.

3. Data Filtering

The data offered in trading are numerical series presented in vectors on a time axis where an endless number of mathematical equations can be applied to process them, with matrix calculation and non-linear regressions being the best, in my humble opinion.

4. Read Fundamental Macroeconomic Events, News

The boilerplate has integration with the tradingview SDK to detect when news will occur and offers parameters so that you can enable an exclusion time margin to not operate anything during that time window.

5. Direction and Sense

In my experience I have found the peculiarity that the same algorithm works very well for a market in a time frame, but for the same market in another time frame it is only a waste of time and money. So now you can easily decide if you only want to open LONG, SHORT or both side positions and know how effective your strategy really is.

6. Reading the money, THE PURPOSE OF EVERYTHING

The most important section in trading and the reason why many clients usually hire me as a financial programmer, is reading and controlling the money, because in the end everyone wants to win and no one wants to lose. Now they can easily parameterize how the money should flow and this is the genius of this boilerplate, because it is what will really decide if an algorithm (Indicator: A bunch of math equations) for entries will really leave you good money over time.

7. Managing the Risk, The Ego Destroyer

Many trades, little money. Most traders focus on making money and none of them know about statistics and the few who do know something about it, only focus on the winrate. Well, with this code you can unlock what really matters, the true success criteria to be able to live off of trading: Profit Factor, Sortino Ratio, Sharpe Ratio and most importantly, will you really make money?

8. Managing Emotions

Finally, the main reason why many lose money is because they are very bad at managing their emotions, because with this they will no longer need to do so because the boilerplate has already programmed criteria to chase the price in a position, cut losses and maximize profits.

In short, this is a boilerplate code that already has the data processing and data output ready, you only have to worry about the data input.

“And so the trader learned: the greatest edge was not in predicting the storm, but in building a boat that could not sink.”

DISCLAIMER

This post is intended for programmers and quantitative traders who already have a certain level of knowledge and experience. It is not intended to be financial advice or to sell you any money-making script, if you use it, you do so at your own risk.

WASDE DatesOverview

WASDE Dates — a small, focused event indicator that displays confirmed USDA WASDE release dates for 2025 on the chart and marks each release day. The indicator is designed to be a lightweight timing tool for traders who want clean visual reminders and optional alerts around USDA WASDE publications.

Features

• Shows official WASDE release dates for 2025 in a compact chart table.

• Draws on-chart markers and a dotted vertical line on WASDE release days.

• Two alert conditions you can enable in TradingView: "WASDE Day Alert" and "WASDE 24h Reminder".

• Simple table position control (Top/Bottom, Left/Right) in the indicator settings.

• Minimal, self-contained code — no external data feeds or permissions required.

How to use

1. Apply the indicator to any chart and timeframe.

2. Use the indicator settings to choose table position.

3. Enable Alerts (if desired) via TradingView Alerts → choose “WASDE Day Alert” or “WASDE 24h Reminder”.

4. This version contains 2025 confirmed dates only — verify dates for live trading and enable alerts as needed.

Design & rationale

This indicator is intentionally not a technical trading signal. It is an event scheduler focused on clarity and low overhead: combine it with your existing setup to avoid being surprised by WASDE publications and to quickly inspect price action around these event dates.

Limitations & disclaimer

• This script shows **confirmed 2025** WASDE dates only. It does not provide trading advice or entry/exit signals. Use at your own risk.

• Double-check official USDA publishing times before executing trades.

• No external links or contact information are included in this description to comply with TradingView publishing rules.

Feature outlook (V2)

Planned V2 (future release): enhanced countdown (days → hours/minutes), optional inclusion of estimated 2026 dates marked as (TBC), and an invite-only/protected advanced version with reaction overlays (T+1/T+3) and extended alert options. V2 will be announced on this script page when ready.

Changelog

v1 — public release: 2025 confirmed dates, release markers, alerts, table position control.

Dskyz (DAFE) Adaptive Regime - Quant Machine ProDskyz (DAFE) Adaptive Regime - Quant Machine Pro:

Buckle up for the Dskyz (DAFE) Adaptive Regime - Quant Machine Pro, is a strategy that’s your ultimate edge for conquering futures markets like ES, MES, NQ, and MNQ. This isn’t just another script—it’s a quant-grade powerhouse, crafted with precision to adapt to market regimes, deliver multi-factor signals, and protect your capital with futures-tuned risk management. With its shimmering DAFE visuals, dual dashboards, and glowing watermark, it turns your charts into a cyberpunk command center, making trading as thrilling as it is profitable.

Unlike generic scripts clogging up the space, the Adaptive Regime is a DAFE original, built from the ground up to tackle the chaos of futures trading. It identifies market regimes (Trending, Range, Volatile, Quiet) using ADX, Bollinger Bands, and HTF indicators, then fires trades based on a weighted scoring system that blends candlestick patterns, RSI, MACD, and more. Add in dynamic stops, trailing exits, and a 5% drawdown circuit breaker, and you’ve got a system that’s as safe as it is aggressive. Whether you’re a newbie or a prop desk pro, this strat’s your ticket to outsmarting the markets. Let’s break down every detail and see why it’s a must-have.

Why Traders Need This Strategy

Futures markets are a gauntlet—fast moves, volatility spikes (like the April 28, 2025 NQ 1k-point drop), and institutional traps that punish the unprepared. Meanwhile, platforms are flooded with low-effort scripts that recycle old ideas with zero innovation. The Adaptive Regime stands tall, offering:

Adaptive Intelligence: Detects market regimes (Trending, Range, Volatile, Quiet) to optimize signals, unlike one-size-fits-all scripts.

Multi-Factor Precision: Combines candlestick patterns, MA trends, RSI, MACD, volume, and HTF confirmation for high-probability trades.

Futures-Optimized Risk: Calculates position sizes based on $ risk (default: $300), with ATR or fixed stops/TPs tailored for ES/MES.

Bulletproof Safety: 5% daily drawdown circuit breaker and trailing stops keep your account intact, even in chaos.

DAFE Visual Mastery: Pulsing Bollinger Band fills, dynamic SL/TP lines, and dual dashboards (metrics + position) make signals crystal-clear and charts a work of art.

Original Craftsmanship: A DAFE creation, built with community passion, not a rehashed clone of generic code.

Traders need this because it’s a complete, adaptive system that blends quant smarts, user-friendly design, and DAFE flair. It’s your edge to trade with confidence, cut through market noise, and leave the copycats in the dust.

Strategy Components

1. Market Regime Detection

The strategy’s brain is its ability to classify market conditions into five regimes, ensuring signals match the environment.

How It Works:

Trending (Regime 1): ADX > 20, fast/slow EMA spread > 0.3x ATR, HTF RSI > 50 or MACD bullish (htf_trend_bull/bear).

Range (Regime 2): ADX < 25, price range < 3% of close, no HTF trend.

Volatile (Regime 3): BB width > 1.5x avg, ATR > 1.2x avg, HTF RSI overbought/oversold.

Quiet (Regime 4): BB width < 0.8x avg, ATR < 0.9x avg.

Other (Regime 5): Default for unclear conditions.

Indicators: ADX (14), BB width (20), ATR (14, 50-bar SMA), HTF RSI (14, daily default), HTF MACD (12,26,9).

Why It’s Brilliant:

Regime detection adapts signals to market context, boosting win rates in trending or volatile conditions.

HTF RSI/MACD add a big-picture filter, rare in basic scripts.

Visualized via gradient background (green for Trending, orange for Range, red for Volatile, gray for Quiet, navy for Other).

2. Multi-Factor Signal Scoring

Entries are driven by a weighted scoring system that combines candlestick patterns, trend, momentum, and volume for robust signals.

Candlestick Patterns:

Bullish: Engulfing (0.5), hammer (0.4 in Range, 0.2 else), morning star (0.2), piercing (0.2), double bottom (0.3 in Volatile, 0.15 else). Must be near support (low ≤ 1.01x 20-bar low) with volume spike (>1.5x 20-bar avg).

Bearish: Engulfing (0.5), shooting star (0.4 in Range, 0.2 else), evening star (0.2), dark cloud (0.2), double top (0.3 in Volatile, 0.15 else). Must be near resistance (high ≥ 0.99x 20-bar high) with volume spike.

Logic: Patterns are weighted higher in specific regimes (e.g., hammer in Range, double bottom in Volatile).

Additional Factors:

Trend: Fast EMA (20) > slow EMA (50) + 0.5x ATR (trend_bull, +0.2); opposite for trend_bear.

RSI: RSI (14) < 30 (rsi_bull, +0.15); > 70 (rsi_bear, +0.15).

MACD: MACD line > signal (12,26,9, macd_bull, +0.15); opposite for macd_bear.

Volume: ATR > 1.2x 50-bar avg (vol_expansion, +0.1).

HTF Confirmation: HTF RSI < 70 and MACD bullish (htf_bull_confirm, +0.2); RSI > 30 and MACD bearish (htf_bear_confirm, +0.2).

Scoring:

bull_score = sum of bullish factors; bear_score = sum of bearish. Entry requires score ≥ 1.0.

Example: Bullish engulfing (0.5) + trend_bull (0.2) + rsi_bull (0.15) + htf_bull_confirm (0.2) = 1.05, triggers long.

Why It’s Brilliant:

Multi-factor scoring ensures signals are confirmed by multiple market dynamics, reducing false positives.

Regime-specific weights make patterns more relevant (e.g., hammers shine in Range markets).

HTF confirmation aligns with the big picture, a quant edge over simplistic scripts.

3. Futures-Tuned Risk Management

The risk system is built for futures, calculating position sizes based on $ risk and offering flexible stops/TPs.

Position Sizing:

Logic: Risk per trade (default: $300) ÷ (stop distance in points * point value) = contracts, capped at max_contracts (default: 5). Point value = tick value (e.g., $12.5 for ES) * ticks per point (4) * contract multiplier (1 for ES, 0.1 for MES).

Example: $300 risk, 8-point stop, ES ($50/point) → 0.75 contracts, rounded to 1.

Impact: Precise sizing prevents over-leverage, critical for micro contracts like MES.

Stops and Take-Profits:

Fixed: Default stop = 8 points, TP = 16 points (2:1 reward/risk).

ATR-Based: Stop = 1.5x ATR (default), TP = 3x ATR, enabled via use_atr_for_stops.

Logic: Stops set at swing low/high ± stop distance; TPs at 2x stop distance from entry.

Impact: ATR stops adapt to volatility, while fixed stops suit stable markets.

Trailing Stops:

Logic: Activates at 50% of TP distance. Trails at close ± 1.5x ATR (atr_multiplier). Longs: max(trail_stop_long, close - ATR * 1.5); shorts: min(trail_stop_short, close + ATR * 1.5).

Impact: Locks in profits during trends, a game-changer in volatile sessions.

Circuit Breaker:

Logic: Pauses trading if daily drawdown > 5% (daily_drawdown = (max_equity - equity) / max_equity).

Impact: Protects capital during black swan events (e.g., April 27, 2025 ES slippage).

Why It’s Brilliant:

Futures-specific inputs (tick value, multiplier) make it plug-and-play for ES/MES.

Trailing stops and circuit breaker add pro-level safety, rare in off-the-shelf scripts.

Flexible stops (ATR or fixed) suit different trading styles.

4. Trade Entry and Exit Logic

Entries and exits are precise, driven by bull_score/bear_score and protected by drawdown checks.

Entry Conditions:

Long: bull_score ≥ 1.0, no position (position_size <= 0), drawdown < 5% (not pause_trading). Calculates contracts, sets stop at swing low - stop points, TP at 2x stop distance.

Short: bear_score ≥ 1.0, position_size >= 0, drawdown < 5%. Stop at swing high + stop points, TP at 2x stop distance.

Logic: Tracks entry_regime for PNL arrays. Closes opposite positions before entering.

Exit Conditions:

Stop-Loss/Take-Profit: Hits stop or TP (strategy.exit).

Trailing Stop: Activates at 50% TP, trails by ATR * 1.5.

Emergency Exit: Closes if price breaches stop (close < long_stop_price or close > short_stop_price).

Reset: Clears stop/TP prices when flat (position_size = 0).

Why It’s Brilliant:

Score-based entries ensure multi-factor confirmation, filtering out weak signals.

Trailing stops maximize profits in trends, unlike static exits in basic scripts.

Emergency exits add an extra safety layer, critical for futures volatility.

5. DAFE Visuals

The visuals are pure DAFE magic, blending function with cyberpunk flair to make signals intuitive and charts stunning.

Shimmering Bollinger Band Fill:

Display: BB basis (20, white), upper/lower (green/red, 45% transparent). Fill pulses (30–50 alpha) by regime, with glow (60–95 alpha) near bands (close ≥ 0.995x upper or ≤ 1.005x lower).

Purpose: Highlights volatility and key levels with a futuristic glow.

Visuals make complex regimes and signals instantly clear, even for newbies.

Pulsing effects and regime-specific colors add a DAFE signature, setting it apart from generic scripts.

BB glow emphasizes tradeable levels, enhancing decision-making.

Chart Background (Regime Heatmap):

Green — Trending Market: Strong, sustained price movement in one direction. The market is in a trend phase—momentum follows through.

Orange — Range-Bound: Market is consolidating or moving sideways, with no clear up/down trend. Great for mean reversion setups.

Red — Volatile Regime: High volatility, heightened risk, and larger/faster price swings—trade with caution.

Gray — Quiet/Low Volatility: Market is calm and inactive, with small moves—often poor conditions for most strategies.

Navy — Other/Neutral: Regime is uncertain or mixed; signals may be less reliable.

Bollinger Bands Glow (Dynamic Fill):

Neon Red Glow — Warning!: Price is near or breaking above the upper band; momentum is overstretched, watch for overbought conditions or reversals.

Bright Green Glow — Opportunity!: Price is near or breaking below the lower band; market could be oversold, prime for bounce or reversal.

Trend Green Fill — Trending Regime: Fills between bands with green when the market is trending, showing clear momentum.

Gold/Yellow Fill — Range Regime: Fills with gold/aqua in range conditions, showing the market is sideways/oscillating.

Magenta/Red Fill — Volatility Spike: Fills with vivid magenta/red during highly volatile regimes.

Blue Fill — Neutral/Quiet: A soft blue glow for other or uncertain market states.

Moving Averages:

Display: Blue fast EMA (20), red slow EMA (50), 2px.

Purpose: Shows trend direction, with trend_dir requiring ATR-scaled spread.

Dynamic SL/TP Lines:

Display: Pulsing colors (red SL, green TP for Trending; yellow/orange for Range, etc.), 3px, with pulse_alpha for shimmer.

Purpose: Tracks stops/TPs in real-time, color-coded by regime.

6. Dual Dashboards

Two dashboards deliver real-time insights, making the strat a quant command center.

Bottom-Left Metrics Dashboard (2x13):

Metrics: Mode (Active/Paused), trend (Bullish/Bearish/Neutral), ATR, ATR avg, volume spike (YES/NO), RSI (value + Oversold/Overbought/Neutral), HTF RSI, HTF trend, last signal (Buy/Sell/None), regime, bull score.

Display: Black (29% transparent), purple title, color-coded (green for bullish, red for bearish).

Purpose: Consolidates market context and signal strength.

Top-Right Position Dashboard (2x7):

Metrics: Regime, position side (Long/Short/None), position PNL ($), SL, TP, daily PNL ($).

Display: Black (29% transparent), purple title, color-coded (lime for Long, red for Short).

Purpose: Tracks live trades and profitability.

Why It’s Brilliant:

Dual dashboards cover market context and trade status, a rare feature.

Color-coding and concise metrics guide beginners (e.g., green “Buy” = go).

Real-time PNL and SL/TP visibility empower disciplined trading.

7. Performance Tracking