Trend Magic Real-Time Cross for TradersPostTrend Magic Real-Time Cross for TradersPost. IIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIIII

Komut dosyalarını "富国恒生港股通高股息低波动ETF发起式联接A+高股息低波动优势" için ara

HTF Candles [theUltimator5]Overlay higher timeframe candles on any lower timeframe chart with real-time updates.

This indicator displays the full structure of each higher timeframe (HTF) candle—including open-close bodies and full wicks—directly on your current chart. Great for multi-timeframe traders who want to align short-term entries with broader market context.

🔹 Features:

View higher timeframe candles (e.g., 1H, 4H, Daily) on intraday charts

Dynamic candle bodies that update in real-time

Accurate wick representation with auto-redrawing

Customizable bullish/bearish colors and transparency

Efficient object management for minimal clutter

🛠️ How to Use:

Add this indicator to a lower timeframe chart (e.g., 1m, 5m, or 15m).

Select a higher timeframe (must be greater than your chart timeframe).

Customize your candle colors and transparency for better visibility.

Watch as each higher timeframe candle evolves live with every bar.

📌 Example: Use a 5-minute chart with a 1-hour HTF overlay to track hourly market structure without switching timeframes.

Dr. Keith Wade Momentum SignalsThis is a heikin Ashli strategy combined with an 18 moving average crossover. Entry at cross of 18 EMA and exit at change of heikin Ashi

Reversal Signal avec TICK + RSIThis indicator is a potential reversal indicator for SCALPING, don't use it for swing. It's base on TICK and on an overbrought/oversold condition of the RSI. You can play with the setting, typicaly I like my TICK to be over reacting an 800/-800 and my rsi over 20 and 80, but it give not enough signal. So I set the TICK signal at 651/-651 and the RSI at 25/75. This indicator is made for SP500 and Nasdaq, so SPY/QQQ/SPX/ES/NQ should work well. It's the first version of it, so maybe I'll add so more data to it to increase signal and lower false one. For now I've test it on live market yet(26/7/25).

The RSI is Fast(5 period), I like to use it on the 1 or 5 min chart.

Please not that it only work during 9h30am to 4pm EST.(Because of the TICK)

Feel free to try and even comment. Don't be harsh on me, it's my first try!

(Sorry for my 'english' it's not my first language)

FAUCON

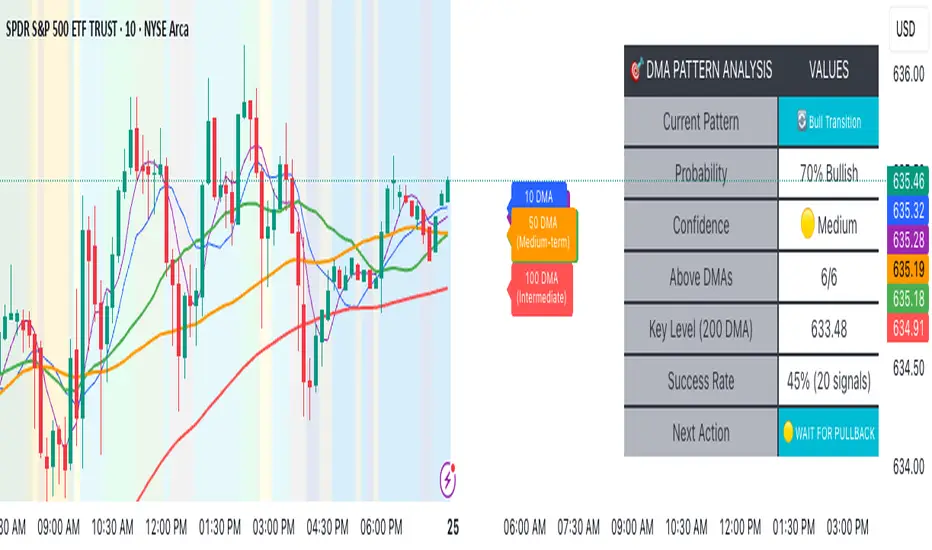

Advanced DMA Pattern Detection SystemAdvanced DMA Pattern Detection System with Smart Intelligence

Professional-grade moving average indicator that combines traditional DMA analysis with advanced pattern recognition and probabilistic forecasting.

Core Features:

6 Key DMAs (5, 10, 20, 50, 100, 200) with descriptive labels showing trading purpose

Advanced Pattern Recognition - Detects Institutional Accumulation, Distribution Phases, Bull/Bear Transitions, and Choppy Markets

Probability Engine - Assigns confidence scores (0-100%) with Low/Medium/High classifications

Historical Validation - Tracks success rate of last 20 pattern signals for real performance data

Smart Alert System - Only triggers on significant pattern changes (20%+ probability shifts)

Dual Display System:

Movable Information Table - Shows current pattern, probability, confidence level, success rate, and recommended action

Chart Alerts & Background Colors - Visual confirmation of high-confidence setups (80%+ patterns)

Traditional DMA Labels - Clear identification of each average's trading significance

Complete Customization:

Master on/off controls for entire system

Individual toggles for all components (DMAs, table, alerts, colors)

Adjustable alert sensitivity (Conservative/Medium/Aggressive)

6 table positions to fit any chart layout

Perfect For: Swing traders, position traders, and anyone wanting systematic trend analysis with quantified probability scores rather than subjective interpretation.

Bottom Line: Transforms basic moving averages into an intelligent trading system that tells you exactly what the market structure means and what to do about it.

Worthy Asset StrategyThis strategy is designed with a two-part philosophy: a regime filter and a value-based accumulation approach.

🟩 Regime Filter:

If the S&P 500 (SPX) is trading above its 200-period EMA, a green background is shown below the chart, signaling a favorable market regime.

If the SPX is below the 200 EMA, the background turns red, indicating a less favorable environment.

📉 Buy Signals:

Buy signals are generated by red candles that drop a certain percentage from their open — essentially treating these pullbacks as discount opportunities.

The idea is to accumulate more of a selected asset when it becomes temporarily cheaper.

💎 Philosophy & Execution:

I only apply this strategy to assets I’ve personally researched and believe to be fundamentally valuable.

If a Buy signal occurs and the SPX is trading above its 200 EMA (i.e., the background is green), I enter the position.

Once in the trade, I follow this logic:

If the position reaches +1.5% profit, I sell it.

If it doesn’t reach profit and goes into a loss, I simply hold.

I don’t sell at a loss because I believe in the long-term value of the asset.

If the price drops further, I accumulate more — aiming to lower my average cost and eventually exit at a profit once the asset recovers.

This approach is based on the mindset of treating drawdowns as discounts, not danger.

"The more it drops, the more I accumulate — because I see value, not risk."

This is still a work in progress, and I’m actively refining it over time.

⚠️ Note: The sell logic is not yet visible on the chart and will be added in a future update.

QTR Sector Fund Performance vs SPY - by LMAnalyzes various market sectors and compares the last several quarters to the performance of the SPY. The goal is to seek out the sectors that have underperformed for several quarters in the hopes that they would overperform in the next quarter.

SPY, QQQ, VIX - Multi TF Trend Table***CURRENTLY IN BACKTESTING PHASE***

This TradingView script creates a real-time multi-timeframe trend status table for SPY, QQQ, and VIX using the Ripster-style EMA cloud logic.

🔍 What It Shows:

Current Price (1 Min): Live snapshot of each symbol.

10min Trend (5/12 EMA): Short-term momentum.

10min Trend (34/50 EMA): Intermediate-term direction.

1 Hour Trend: Higher timeframe trend.

Daily Trend: Long-term trend using 5/12 and 34/55 EMA alignment.

Each cell is color-coded:

✅ Green = Bullish

❌ Red = Bearish

Yellow can be used for neutral if customized.

⚙️ How It Works:

Uses request.security() to pull multi-timeframe EMA values for each symbol.

Compares fast/slow EMAs to determine bullish or bearish alignment.

The table is refreshed live and placed in a corner of your choice.

✅ Ideal For:

Trend traders using Ripster EMA clouds

SPY/QQQ/VIX correlation watchers

Traders seeking real-time trend clarity across multiple timeframes

Daily Moving Average to Intraday ChartPlaces 200D, 100D, 50D SMAs as well as the 20D EMA onto intraday charts. (Script v6)

Multi-Timeframe EMA Table (Woche, Tag, 4h, 1h)Title: Multi-Timeframe EMA Table (Weekly, Daily, 4h, 1h)

Description:

This Pine Script indicator provides a concise and clear Multi-Timeframe (MTF) Exponential Moving Average (EMA) analysis directly on your TradingView chart. It displays the EMA values for the 1-hour, 4-hour, 1-day, and 1-week timeframes in a customizable table.

Features:

Clear Table Display: Shows the current EMA values for predefined higher timeframes (1h, 4h, Day, Week).

Dynamic Status: The status column immediately visualizes whether the current price of your chart is above (Green) or below (Red) its respective Multi-Timeframe EMA.

Customizable EMA Length: The length of the EMA can be easily adjusted via the indicator settings, allowing you to tailor it to your preferred analysis.

Visual Confirmation: The corresponding Multi-Timeframe EMA lines are optionally plotted directly on the chart to visually confirm the table values.

Non-Repainting: The displayed EMA values and lines are programmed to be non-repainting, meaning their values do not change on already closed candles.

This indicator is a useful tool for traders who want to quickly get an overview of the EMA's position across different timeframes without constantly switching their chart timeframe. It's ideal for confirming trends and identifying support and resistance levels from a higher perspective.

🟡🔵🟢🔴Beginner's Assistant by carljchapman🟡🔵🟢🔴

Overview

This indicator dynamically marks highs and lows of the premarket (4:00am-9:30amEST) and opening range. It displays Fair Value Gaps, 9 and 21 period Exponential Moving Averages (EMA) and the Volume Weighted Average Price (VWAP). To really help beginners, it marks suggested entry points on the chart with green or red triangles, when a reasonable trend appears.

Features

Automatically draws blue lines for Premarket High and Low values

Dynamically marks the opening Range region

Visual entry signals for long and short opportunities

Primarily used for stocks/funds , but works with forex and crypto

Quick configuration settings to tailor details for your experience level

Mobile friendly mode

Supports alerts

How To Use

Open your chart, and select a 1 or 2 minute timeframe.

Watch for green triangles and red triangles, hinting at entries for long or short positions. Pay particular attention to the price action as it approaches the bounds of the opening range and the premarket levels. I suggest also using a MACD indicator for confirmation of the trend.

For scalping 0dte Options, switch frequently between the 1 ,2 and 5 minute or higher timeframes. Do this so you will not miss an entry opportunity or be unaware of the overall trend.

As a beginner, until you have refined your strategy and develop risk management, take profits as low as 10%. A small profit can quickly become a much larger loss. With 0dte options, time will devour your profits even when the price doesn’t budge.

What makes this indicator so beginner friendly?

Charts with too many lines and colors are are a nightmare for beginners! And empty charts do not tell the whole story. Simple checkboxes in the configuration settings let you turn on and off features to match your comfort level. As you become more familiar you might try turning off the suggested entries to see if you would have selected the same or better ones yourself. Just one example of how you will learn and verify your knowledge. You will quickly spot Opening Range Breakouts and more.

Why are the triangle pointers not simply above or below the bars?

As a beginner, I like to review charts to see how much the price changed, then estimate how much a contract would move based on its delta. A mouthful, I know. But what price does an arrow pointing up below a bar reflect? Would I have entered at the open or close, low or high? This indicator helps by putting the marker close to the price when indicated. It can even display the actual price on the bar. This is helpful for you to make fast calculations without a measuring tool.

I am an experienced trader. Can this help me make winning trades?

Sure. It can also help you make losing ones! Profit is not guaranteed with any indicator or strategy. This indicator is designed to assist you as you learn and while you trade. You won't see the words BUY or SELL. This is not a signal bot! It is merely a tool to assist you. You can learn a lot by spending time observing price movement using this indicator without ever making a single trade.

🟡🔵🟢🔴

Daily EMAs (8, 21 & 50) with BandDescription:

This script plots the Daily EMAs (8, 21, and 50) on any intraday or higher timeframe chart. It provides a clear, multi-timeframe view of market trends by using daily exponential moving averages (EMAs) and a dynamic visual band. I use this on the major indexes to decide if I should be mostly longing or shorting assets.

-In addition to identifying the trend structure, the 8-Day EMA often serves as a key area where buyers or sellers may become active, depending on the market direction:

-In an uptrend, the 8 EMA can act as a dynamic support zone, where buyers tend to re-enter on pullbacks.

-In a downtrend, the same EMA may act as resistance, where sellers become more aggressive.

-The script also includes a colored band between the 8 and 21 EMAs to highlight the short-term trend bias:

-Green fill = 8 EMA is above the 21 EMA (bullish structure).

Blue fill = 8 EMA is below the 21 EMA (bearish structure).

The 50-Day EMA is included to give additional context for intermediate-term trend direction.

Features:

- Daily EMA levels (8, 21, and 50) calculated regardless of current chart timeframe.

- 8 EMA acts as a potential buyer/seller zone based on trend direction.

- Color-coded band between 8 and 21 EMAs:

- Green = Bullish short-term bias

- Blue = Bearish short-term bias

- Customizable price source and EMA offset.

- Suitable for trend trading, pullback entries, and higher-timeframe confirmation.

Use Cases:

Identify key dynamic support/resistance areas using the 8 EMA.

Assess short-, medium-, and intermediate-term trend structure at a glance.

Enhance confluence for entry/exit signals on lower timeframes.

% / ATR Buy, Target, Stop + Overlay & P/L% / ATR Buy, Target, Stop + Overlay & P/L

This tool combines volatility‑based and fixed‑percentage trade planning into a single, on‑chart overlay—with built‑in profit‑and‑loss estimates. Toggle between ATR or percentage modes, plot your Buy, Target and Stop levels, and see the dollar gain or loss for a specified position size—all in one interactive table and chart display.

NOTE: To activate plotted lines, price labels, P/L rows and table values, enter a Buy Price greater than zero.

What It Does

Mode Toggle: Choose between “ATR” (volatility‑based) or “%” (fixed‑percentage) calculations.

Buy Price Input: Manually enter your entry price.

ATR Mode:

Target = Buy + (ATR × Target Multiplier)

Stop = Buy − (ATR × Stop Multiplier)

Percentage Mode:

Target = Buy × (1 + Target % / 100)

Stop = Buy × (1 – Stop % / 100)

P/L Estimates: Specify a dollar amount to “invest” at your Buy price, and the script calculates:

Gain ($): Profit if Target is hit

Loss ($): Cost if Stop is hit

Visual Overlay: Draws horizontal lines for Buy, Target and Stop, with optional price labels on the chart scale.

Interactive Table: Displays Buy, Target, Stop, ATR/timeframe info (in ATR mode), percentages (in % mode), and P/L rows.

Customization Options

Line Settings:

Choose color, style (solid/dashed/dotted), and width for Buy, Target, Stop lines.

Extend lines rightward only or in both directions.

Table Settings:

Position the table (top/bottom × left/right).

Toggle individual rows: Buy Price; Target (multiplier or %); Stop (multiplier or %); Target ATR %; Stop ATR %; ATR Time Frame; ATR Value; Gain ($); Loss ($).

Customize text colors for each row and background transparency.

General Inputs:

ATR length and optional ATR timeframe override (e.g. use daily ATR on an intraday chart).

Target/Stop multipliers or percentages.

Dollar Amount for P/L calculations.

How to Use It for Trading

Plan Your Entry: Enter your intended Buy Price and position size (dollar amount).

Select Mode: Toggle between ATR or % mode depending on whether you prefer volatility‑based or fixed offsets.

Assess R:R and P/L: Instantly see your Target, Stop levels, and potential profit or loss in dollars.

Visual Reference: Lines and price labels update in real time as you tweak inputs—ideal for live trading, backtesting or trade journaling.

Ideal For

Traders who want both volatility‑based and percentage‑based exit options in one tool

Those who need on‑chart P/L estimates based on position size

Swing and intraday traders focused on objective, rule‑based trade management

Anyone who uses ATR for adaptive stops/targets or fixed percentages for simpler exits

Strategy Chameleon [theUltimator5]Have you ever looked at an indicator and wondered to yourself "Is this indicator actually profitable?" Well now you can test it out for yourself with the Strategy Chameleon!

Strategy Chameleon is a versatile, signal-agnostic trading strategy designed to adapt to any external indicator or trading system. Like a chameleon changes colors to match its environment, this strategy adapts to match any buy/sell signals you provide, making it the ultimate backtesting and automation tool for traders who want to test multiple strategies without rewriting code.

🎯 Key Features

1) Connects ANY external indicator's buy/sell signals

Works with RSI, MACD, moving averages, custom indicators, or any Pine Script output

Simply connect your indicator's signal output to the strategy inputs

2) Multiple Stop Loss Types:

Percentage-based stops

ATR (Average True Range) dynamic stops

Fixed point stops

3) Advanced Trailing Stop System:

Percentage trailing

ATR-based trailing

Fixed point trailing

4) Flexible Take Profit Options:

Risk:Reward ratio targeting

Percentage-based profits

ATR-based profits

Fixed point profits

5) Trading Direction Control

Long Only - Bull market strategies

Short Only - Bear market strategies

Both - Full market strategies

6) Time-Based Filtering

Optional trading session restrictions

Customize active trading hours

Perfect for day trading strategies

📈 How It Works

Signal Detection: The strategy monitors your connected buy/sell signals

Entry Logic: Executes trades when signals trigger during valid time periods

Risk Management: Automatically applies your chosen stop loss and take profit levels

Trailing System: Dynamically adjusts stops to lock in profits

Performance Tracking: Real-time statistics table showing win rate and performance

⚙️ Setup Instructions

0) Add indicator you want to test, then add the Strategy to your chart

Connect Your Signals:

imgur.com

Go to strategy settings → Signal Sources

1) Set "Buy Signal Source" to your indicator's buy output

2) Set "Sell Signal Source" to your indicator's sell output

3) Choose table position - This simply changes the table location on the screen

4) Set trading direction preference - Buy only? Sell only? Both directions?

imgur.com

5) Set your preferred stop loss type and level

You can set the stop loss to be either percentage based or ATR and fully configurable.

6) Enable trailing stops if desired

imgur.com

7) Configure take profit settings

8) Toggle time filter to only consider specific time windows or trading sessions.

🚀 Use Cases

Test various indicators to determine feasibility and/or profitability.

Compare different signal sources quickly

Validate trading ideas with consistent risk management

Portfolio Management

Apply uniform risk management across different strategies

Standardize stop loss and take profit rules

Monitor performance consistently

Automation Ready

Built-in alert conditions for automated trading

Compatible with trading bots and webhooks

Easy integration with external systems

⚠️ Important Notes

This strategy requires external signals to function

Default settings use 10% of equity per trade

Pyramiding is disabled (one position at a time)

Strategy calculates on bar close, not every tick

🔗 Integration Examples

Works perfectly with:

RSI strategies (connect RSI > 70 for sells, RSI < 30 for buys)

Moving average crossovers

MACD signal line crosses

Bollinger Band strategies

Custom oscillators and indicators

Multi-timeframe strategies

📋 Default Settings

Position Size: 10% of equity

Stop Loss: 2% percentage-based

Trailing Stop: 1.5% percentage-based (enabled)

Take Profit: Disabled (optional)

Trade Direction: Both long and short

Time Filter: Disabled

10/20 MA Coil: Progressive Colors & Multi-Day BreakoutThis indicator detects price “coil” setups and highlights potential breakout or breakdown opportunities using moving average alignment and volatility compression.

Features:

• Coil Detection:

• Identifies consolidation when:

• The 10 and 20 MAs are tightly aligned (within user-defined tolerance)

• Price is above both MAs and within 1.5x ADR of them

• The 50 MA is rising

• Progressive Coil Coloring:

• Coil candles are colored in progressively darker orange as the streak continues

• Bullish Breakout Signal:

• Triggers when a green candle follows a coiled bar

• The candle’s body must be greater than or equal to 1 ATR

• Colored lime green

• Bearish Breakdown Signal:

• Triggers when a red candle follows a coiled bar

• The candle’s body must be greater than or equal to 1 ATR to the downside

• Colored black

• Custom Candle Rendering:

• Candle body color represents coil or breakout state

• Wick and border are red or green to reflect price direction

• Optional Debug Tools:

• Coil streak, ATR, and distance from MAs can be plotted for deeper analysis

This script is designed for traders looking to spot price compression and prepare for high-probability moves following low-volatility setups.

ATR Trailing Stop with ATR Targets [v6]What the Indicator Does

This custom TradingView indicator is designed for active traders who want to automate and visualize their trailing stop management and target setting, using true market volatility. It combines the Average True Range (ATR) with dynamic market structure logic to:

Trail a stop-loss behind major swings in real time, using 2×ATR (adjustable) from the highest high in uptrends or the lowest low in downtrends.

Flip trading bias between bullish and bearish when the stop is breached.

Identify and plot three profit targets (at 1, 2, and 3 ATR from the breakout/flip point) after every stop-flip, helping traders scale out or set take-profits objectively.

Maintain a visible presence on your chart every bar to avoid indicator errors, with color and labeling for clear distinction between long/short phases.

How the Indicator Works

1. ATR Calculation

ATR Period and Multiplier: You select your preferred ATR length (default is 14 bars) and a multiplier (default is 2.0).

Volatility Adjustment: ATR measures the average "true" bar range, so the trailing stop and targets adapt to current volatility.

2. Trailing Stop Logic

Uptrend (bullish bias): The indicator tracks the highest high made since the last bearish-to-bullish flip and sets the stop at - .

The stop only raises (never lowers) during an uptrend, protecting gains in strong moves.

Downtrend (bearish bias): Tracks the lowest low made since the last bullish-to-bearish flip, with stop at + .

The stop only lowers (never raises) in a downtrend.

Flip Point: If price closes through the trailing stop, the current bias “flips,” and the logic reverses (bullish to bearish or vice versa). At the new close, flip price and bar index are stored for target calculation.

3. ATR Targets after Flip

After each stop flip:

Three targets—based on the new close price—are calculated and plotted:

Long flip (new bull bias): Target1 = close + 1×ATR, Target2 = close + 2×ATR, Target3 = close + 3×ATR.

Short flip (new bear bias): Target1 = close - 1×ATR, Target2 = close - 2×ATR, Target3 = close - 3×ATR.

These targets help with scaling out, partial profit-taking, or setting automated orders.

4. Visual Feedback

Trailing stop line: Green for long bias, red for short bias.

Targets: Distinct color-coded circles at 1, 2, 3 ATR levels from the most recent flip.

Flip Labels: Mark the bar and price where bias flipped (“Long Flip” or “Short Flip”) for quick pattern recognition.

Subtle background shading: Ensures TradingView's requirement for “indicator output every bar.”

How to Use This Indicator

Parameter Setup

ATR Period and Multiplier: Adjust to match the timeframe and volatility of your instrument.

Lower periods/multipliers for short-term/volatile trading.

Higher values for smoother signals or higher timeframes.

Starting Trend: Set to match the expected initial bias if the instrument has strong trend characteristics.

Trading Application

1. Daily Bias Approach

Establish your bias in line with your trading plan (e.g., only trade long if price is above the previous day's high, short below the previous day's low).

Only look for trades in the indicator's current bias direction, as expressed by the stop and background color.

2. Entry

Use the indicator as a real-time confirmation or trailing stop for your entries.

Breakout: Enter when price establishes the current bias, using the trailing stop as your risk level.

Reversal: Wait for a bias flip after an extended move; enter in the direction of the new bias.

VWAP Rebound: Combine with a VWAP bounce—enter only if the indicator bias supports your direction.

3. Exits/Targets

Trailing stop management: Move your stop according to the plotted line; exit if your stop is hit.

Profit-taking: Scale out or take profits as price approaches each ATR-based target.

Use the dynamic labeling to identify reversal flips and reset your plan if stopped or the bias changes.

4. Market Context

Filter and frame setups by watching correlated indicators (DXY, VIX, AUDJPY, put/call ratio) and upcoming news; trade only in the daily bias direction for best consistency.

5. Practical Tips

Combine this indicator with your custom watchlist and alert settings to get notified on flips or targets.

Review the last label ("Long Flip"/"Short Flip") and targets to plan partial exits.

Remember: ATR adapts to volatility, so the stop and targets stay proportionate even when price action shifts.

EMA Curl Strength+EMA Curl Strength+

Description:

This indicator provides a statistically normalized view of EMA slope momentum using Z-score transformation. By evaluating the rate of change of an EMA and comparing it against its historical behavior, the script highlights momentum shifts in a dynamic, adaptive way.

⸻

How It Works:

• Calculates the slope (percentage change) of a chosen EMA.

• Normalizes the slope using Z-score over a custom lookback period.

• Smooths the resulting signal and computes two signal lines for comparison.

• Assigns dynamic colors based on user-defined Z-score thresholds for mild, moderate, and strong momentum in both directions.

⸻

Visual Features:

• Gradient fill between the Z Curl Line and Signal 1 to highlight slope acceleration.

• Histogram showing the difference between the Z Curl Line and its signal.

• Optional signal crossover shapes between configurable pairs (e.g., Z Curl vs. Signal).

• Background highlights when the Z Curl Line exceeds ±2, indicating strong trending behavior.

⸻

Customization:

• Adjustable EMA length, smoothing lengths, signal lengths, histogram smoothing, and Z-score lookback.

• Separate color controls for:

• Z-score strength bands (mild/moderate/strong up/down)

• Histogram bars

• Signal lines

• Background highlight zones

• Crossover shapes

⸻

Use Cases:

• Momentum Confirmation: Confirm strength when Z Curl exceeds ±2 with matching background highlights.

• Trend Entry Timing: Look for trades when Z Curl crosses above or below the 0-line.

• Scalping: Capture quick directional moves when momentum accelerates.

• Trend Following: Use strong Z Curl values to confirm trade direction and filter sideways action.

• Divergence Detection: Spot divergences between price and Z Curl movement to anticipate reversals.

NFP RangesPlots the NFP daily ranges for NFP days. Includes extended hours ranges when the time frame is sub 1D, otherwise, only the daily range is taken.

NFP Dates are pre-populated through 2029 and historically through 2022. Will update script to include farther-out dates before they become necessary.

BuySell Volume Bar Chart• Separates estimated Buy and Sell volume per bar using price action logic

• Plots them in a dual-axis format: buy volume goes up, sell volume goes down

• Colors are dynamic — whichever side dominates gets the stronger color, the weaker side is shaded

• Includes a live difference metric (Δ Volume) as a third value in the indicator title

• Automatically filters out flat/no-move bars to avoid misleading spikes

The live difference metric ("Δ Volume") can be controlled.

This metric calculates the difference between the buying and selling volume live, where it takes the Buy Volume - Sell Volume.

This difference is then displayed in either green (BV > SV) or red (SV > BV). You can toggle it on/off by entering the indicator's settings or double tapping the indicator name on the TV chart.

Another pretty cool thing is the modular colors - you can customize your candle colors and shades to your liking within the code!

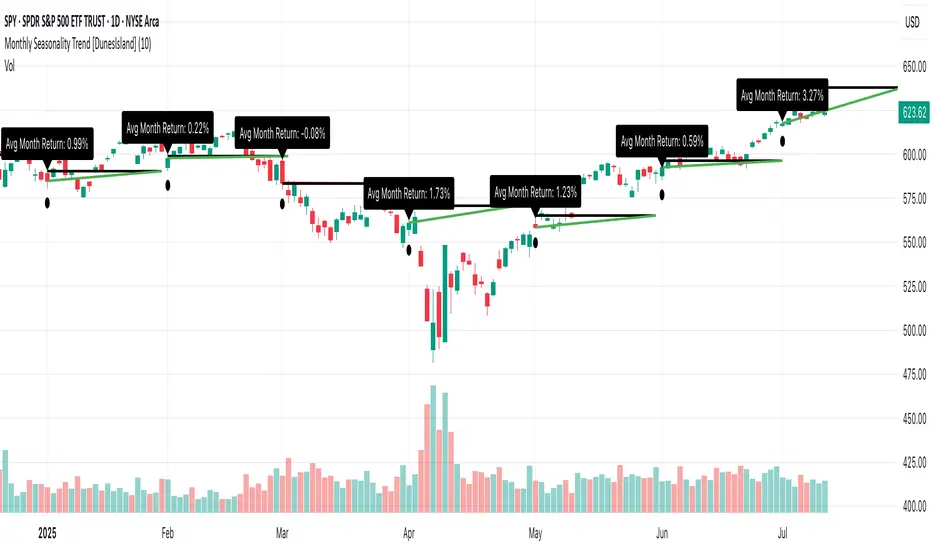

Monthly Seasonality Trend [DunesIsland]The Monthly Seasonality Trend is a indicator designed to analyze and visualize historical monthly seasonality patterns in financial markets. By calculating the average monthly return over a user-configurable lookback period (1 to 10 years), this indicator provides traders and investors with a clear projection of potential price movements for the current month, enabling data-driven decision-making.

How It Works

The indicator operates by retrieving monthly open and close prices for the specified lookback period (up to 10 years) and computing the average percentage return for the current month based on historical data. Key functionalities include:

Dynamic Trend Line: On the first trading day of each month, the indicator plots a line projecting the expected price trajectory, starting from the current close price and extending to the estimated end-of-month price based on the average historical return. The line is colored green for anticipated price increases or red for expected declines, offering an intuitive visual cue.

Average Return Label: A label is displayed at the start of each month, detailing the calculated average historical return for that month, expressed as a percentage, to provide context for the projected trend.

First Trading Day Marker: A small circle is plotted below the bar on the first trading day of each month, clearly marking the start of the projection period.

Adaptive Bar Counting: The indicator dynamically adjusts the length of the trend line based on the actual number of trading days in the previous month, ensuring accurate projections.

How to Interpret

Bullish Projection (Green Line): Indicates that historical data suggests an average price increase for the current month, potentially signaling buying opportunities.

Bearish Projection (Red Line): Suggests an average price decline based on historical trends, which may prompt caution or short-selling strategies.

Historical Context: The average return label provides a quantitative measure of past performance, helping traders assess the reliability of the projected trend.

Divergence Strategy [Trendoscope®]🎲 Overview

The Divergence Strategy is a sophisticated TradingView strategy that enhances the Divergence Screener by adding automated trade signal generation, risk management, and trade visualization. It leverages the screener’s robust divergence detection to identify bullish, bearish, regular, and hidden divergences, then executes trades with precise entry, stop-loss, and take-profit levels. Designed for traders seeking automated trading solutions, this strategy offers customizable trade parameters and visual feedback to optimize performance across various markets and timeframes.

For core divergence detection features, including oscillator options, trend detection methods, zigzag pivot analysis, and visualization, refer to the Divergence Screener documentation. This description focuses on the strategy-specific enhancements for automated trading and risk management.

🎲 Strategy Features

🎯Automated Trade Signal Generation

Trade Direction Control : Restrict trades to long-only or short-only to align with market bias or strategy goals, preventing conflicting orders.

Divergence Type Selection : Choose to trade regular divergences (bullish/bearish), hidden divergences, or both, targeting reversals or trend continuations.

Entry Type Options :

Cautious : Enters conservatively at pivot points and exits quickly to minimize risk exposure.

Confident : Enters aggressively at the latest price and holds longer to capture larger moves.

Mixed : Combines conservative entries with delayed exits for a balanced approach.

Market vs. Stop Orders: Opt for market orders for instant execution or stop orders for precise price entry.

🎯 Enhanced Risk Management

Risk/Reward Ratio : Define a risk-reward ratio (default: 2.0) to set profit targets relative to stop-loss levels, ensuring consistent trade sizing.

Bracket Orders : Trades include entry, stop-loss, and take-profit levels calculated from divergence pivot points, tailored to the entry type and risk-reward settings.

Stop-Loss Placement : Stops are strategically set (e.g., at recent pivot or last price point) based on entry type, balancing risk and trade validity.

Order Cancellation : Optionally cancel pending orders when a divergence is broken (e.g., price moves past the pivot in the wrong direction), reducing invalid trades. This feature is toggleable for flexibility.

🎯 Trade Visualization

Target and Stop Boxes : Displays take-profit (lime) and stop-loss (orange) levels as boxes on the price chart, extending 10 bars forward for clear visibility.

Dynamic Trade Updates : Trade visualizations are added, updated, or removed as trades are executed, canceled, or invalidated, ensuring accurate feedback.

Overlay Integration : Trade levels overlay the price chart, complementing the screener’s oscillator-based divergence lines and labels.

🎯 Strategy Default Configuration

Capital and Sizing : Set initial capital (default: $1,000,000) and position size (default: 20% of equity) for realistic backtesting.

Pyramiding : Allows up to 4 concurrent trades, enabling multiple divergence-based entries in trending markets.

Commission and Margin : Accounts for commission (default: 0.01%) and margin (100% for long/short) to reflect trading costs.

Performance Optimization : Processes up to 5,000 bars dynamically, balancing historical analysis and real-time execution.

🎲 Inputs and Configuration

🎯Trade Settings

Direction : Select Long or Short (default: Long).

Divergence : Trade Regular, Hidden, or Both divergence types (default: Both).

Entry/Exit Type : Choose Cautious, Confident, or Mixed (default: Cautious).

Risk/Reward : Set the risk-reward ratio for profit targets (default: 2.0).

Use Market Order : Enable market orders for immediate entry (default: false, uses limit orders).

Cancel On Break : Cancel pending orders when divergence is broken (default: true).

🎯Inherited Settings

The strategy inherits all inputs from the Divergence Screener, including:

Oscillator Settings : Oscillator type (e.g., RSI, CCI), length, and external oscillator option.

Trend Settings : Trend detection method (Zigzag, MA Difference, External), MA type, and length.

Zigzag Settings : Zigzag length (fixed repaint = true).

🎲 Entry/Exit Types for Divergence Scenarios

The Divergence Strategy offers three Entry/Exit Type options—Cautious, Confident, and Mixed—which determine how trades are entered and exited based on divergence pivot points. This section explains how these settings apply to different divergence scenarios, with placeholders for screenshots to illustrate each case.

The divergence pattern forms after 3 pivots. The stop and entry levels are formed on one of these levels based on Entry/Exit types.

🎯Bullish Divergence (Reversal)

A bullish divergence occurs when price forms a lower low, but the oscillator forms a higher low, signaling a potential upward reversal.

💎 Cautious:

Entry : At the pivot high point for a conservative entry.

Exit : Stop-loss at the last pivot point (previous low that is higher than the current pivot low); take-profit at risk-reward ratio. Canceled if price breaks below the pivot (if Cancel On Break is enabled).

Behavior : Enters after confirmation and exits quickly to limit downside risk.

💎Confident:

Entry : At the last pivot low, (previous low which is higher than the current pivot low) for an aggressive entry.

Exit : Stop-loss at recent pivot low, which is the lowest point; take-profit at risk-reward ratio. Canceled if price breaks below the pivot. (lazy exit)

Behavior : Enters early to capture trend continuation, holding longer for gains.

💎Mixed:

Entry : At the pivot high point (conservative).

Exit : Stop-loss at the recent pivot point that has resulted in lower low (lazy exit). Canceled if price breaks below the pivot.

Behavior : Balances entry caution with extended holding for trend continuation.

🎯Bearish Divergence (Reversal)

A bearish divergence occurs when price forms a higher high, but the oscillator forms a lower high, indicating a potential downward reversal.

💎Cautious:

Entry : At the pivot low point (lower high) for a conservative short entry.

Exit : Stop-loss at the previous pivot high point (previous high); take-profit at risk-reward ratio. Canceled if price breaks above the pivot (if Cancel On Break is enabled).

Behavior : Enters conservatively and exits quickly to minimize risk.

💎Confident:

Entry : At the last price point (previous high) for an aggressive short entry.

Exit : Stop-loss at the pivot point; take-profit at risk-reward ratio. Canceled if price breaks above the pivot.

Behavior : Enters early to maximize trend continuation, holding longer.

💎Mixed:

Entry : At the previous piot high point (conservative).

Exit : Stop-loss at the last price point (delayed exit). Canceled if price breaks above the pivot.

Behavior : Combines conservative entry with extended holding for downtrend gains.

🎯Bullish Hidden Divergence (Continuation)

A bullish hidden divergence occurs when price forms a higher low, but the oscillator forms a lower low, suggesting uptrend continuation. In case of Hidden bullish divergence, b]Entry is always on the previous pivot high (unless it is a market order)

💎Cautious:

Exit : Stop-loss at the recent pivot low point (higher than previous pivot low); take-profit at risk-reward ratio. Canceled if price breaks below the pivot (if Cancel On Break is enabled).

Behavior : Enters after confirmation and exits quickly to limit downside risk.

💎Confident:

Exit : Stop-loss at previous pivot low, which is the lowest point; take-profit at risk-reward ratio. Canceled if price breaks below the pivot. (lazy exit)

Behavior : Enters early to capture trend continuation, holding longer for gains.

🎯Bearish Hidden Divergence (Continuation)

A bearish hidden divergence occurs when price forms a lower high, but the oscillator forms a higher high, suggesting downtrend continuation. In case of Hidden Bearish divergence, b]Entry is always on the previous pivot low (unless it is a market order)

💎Cautious:

Exit : Stop-loss at the latest pivot high point (which is a lower high); take-profit at risk-reward ratio. Canceled if price breaks above the pivot (if Cancel On Break is enabled).

Behavior : Enters conservatively and exits quickly to minimize risk.

💎Confident/Mixed:

Exit : Stop-loss at the previous pivot high point; take-profit at risk-reward ratio. Canceled if price breaks above the pivot.

Behavior : Uses the late exit point to hold longer.

🎲 Usage Instructions

🎯Add to Chart:

Add the Divergence Strategy to your TradingView chart.

The oscillator and divergence signals appear in a separate pane, with trade levels (target/stop boxes) overlaid on the price chart.

🎯Configure Settings:

Adjust trade settings (direction, divergence type, entry type, risk-reward, market orders, cancel on break).

Modify inherited Divergence Screener settings (oscillator, trend method, zigzag length) as needed.

Enable/disable alerts for divergence notifications.

🎯Interpret Signals:

Long Trades: Triggered on bullish or bullish hidden divergences (if allowed), shown with green/lime lines and labels.

Short Trades: Triggered on bearish or bearish hidden divergences (if allowed), shown with red/orange lines and labels.

Monitor lime (target) and orange (stop) boxes for trade levels.

Review strategy performance metrics (e.g., profit/loss, win rate) in the strategy tester.

🎯Backtest and Optimize:

Use TradingView’s strategy tester to evaluate performance on historical data.

Fine-tune risk-reward, entry type, position sizing, and cancellation settings to suit your market and timeframe.

For questions, suggestions, or support, contact Trendoscope via TradingView or official support channels. Stay tuned for updates and enhancements to the Divergence Strategy!

Trading CalculatorTrading Calculator Indicator

VIBE CODED WITH GROK 3

The Trading Calculator is a Pine Script indicator designed to perform quick and useful trading-related calculations directly on your chart. It allows traders to execute basic arithmetic operations—such as addition, subtraction, multiplication, and division—as well as calculate percent change and average using either numerical values or trading variables (e.g., close, open, high, low, volume). The indicator displays its results in a table that resembles a calculator interface, making it both functional and visually intuitive. Unlike typical indicators, it does not overlay on the price chart but instead appears in a separate pane.

Inputs

Formula (new | old): First value or variable (e.g., 100, close, close ). Example: close uses the current closing price.

Operator: Mathematical operation (e.g., Plus, Minus, Multiply). Example: Plus adds the two inputs.

Second Input: Second value or variable (e.g., 50, open, close ). Example: open uses the current opening price.

Risk Distribution HistogramStatistical risk visualization and analysis tool for any ticker 📊

The Risk Distribution Histogram visualizes the statistical distribution of different risk metrics for any financial instrument. It converts risk data into histograms with quartile-based color coding, so that traders can understand their risk, tail-risks, exposure patterns and make data-driven decisions based on empirical evidence rather than assumptions.

The indicator supports multiple risk calculation methods, each designed for different aspects of market analysis, from general volatility assessment to tail risk analysis.

Risk Measurement Methods

Standard Deviation

Captures raw daily price volatility by measuring the dispersion of price movements. Ideal for understanding overall market conditions and timing volatility-based strategies.

Use case: Options trading and volatility analysis.

Average True Range (ATR)

Measures true range as a percentage of price, accounting for gaps and limit moves. Valuable for position sizing across different price levels.

Use case: Position sizing and stop-loss placement.

The chart above illustrates how ATR statistical distribution can be used by looking at the ATR % of price distribution. For example, 90% of the movements are below 5%.

Downside Deviation

Only considers negative price movements, making it ideal for checking downside risk and capital protection rather than capturing upside volatility.

Use case: Downside protection strategies and stop losses.

Drawdown Analysis

Tracks peak-to-trough declines, providing insight into maximum loss potential during different market conditions.

Use case: Risk management and capital preservation.

The chart above illustrates tale risk for the asset (TQQQ), showing that it is possible to have drawdowns higher than 20%.

Entropy-Based Risk (EVaR)

Uses information theory to quantify market uncertainty. Higher entropy values indicate more unpredictable price action, valuable for detecting regime changes.

Use case: Advanced risk modeling and tail-risk.

VIX Histogram

Incorporates the market's fear index directly into analysis, showing how current volatility expectations compare to historical patterns. The CAPITALCOM:VIX histogram is independent from the ticker on the chart.

Use case: Volatility trading and market timing.

Visual Features

The histogram uses quartile-based color coding that immediately shows where current risk levels stand relative to historical patterns:

Green (Q1): Low Risk (0-25th percentile)

Yellow (Q2): Medium-Low Risk (25-50th percentile)

Orange (Q3): Medium-High Risk (50-75th percentile)

Red (Q4): High Risk (75-100th percentile)

The data table provides detailed statistics, including:

Count Distribution: Historical observations in each bin

PMF: Percentage probability for each risk level

CDF: Cumulative probability up to each level

Current Risk Marker: Shows your current position in the distribution

Trading Applications

When current risk falls into upper quartiles (Q3 or Q4), it signals conditions are riskier than 50-75% of historical observations. This guides position sizing and portfolio adjustments.

Key applications:

Position sizing based on empirical risk distributions

Monitoring risk regime changes over time

Comparing risk patterns across timeframes

Risk distribution analysis improves trade timing by identifying when market conditions favor specific strategies.

Enter positions during low-risk periods (Q1)

Reduce exposure in high-risk periods (Q4)

Use percentile rankings for dynamic stop-loss placement

Time volatility strategies using distribution patterns

Detect regime shifts through distribution changes

Compare current conditions to historical benchmarks

Identify outlier events in tail regions

Validate quantitative models with empirical data

Configuration Options

Data Collection

Lookback Period: Control amount of historical data analyzed

Date Range Filtering: Focus on specific market periods

Sample Size Validation: Automatic reliability warnings

Histogram Customization

Bin Count: 10-50 bins for different detail levels

Auto/Manual Bin Width: Optimize for your data range

Visual Preferences: Custom colors and font sizes

Implementation Guide

Start with Standard Deviation on daily charts for the most intuitive introduction to distribution-based risk analysis.

Method Selection: Begin with Standard Deviation

Setup: Use daily charts with 20-30 bins

Interpretation: Focus on quartile transitions as signals

Monitoring: Track distribution changes for regime detection

The tool provides comprehensive statistics including mean, standard deviation, quartiles, and current position metrics like Z-score and percentile ranking.

Enjoy, and please let me know your feedback! 😊🥂