Killzones And Macros LibraryKillzones & Macros Library for Trading Sessions

This Pine Script library is designed to help traders identify and act during high-volatility trading windows, commonly referred to as "Killzones." These are specific times during the day when institutional traders are most active, resulting in increased liquidity and price movement. The library provides boolean fields that return true when the current time falls within one of the killzones or macroeconomic event windows, allowing for enhanced trade timing and precision.

Killzones Include:

London Open, New York Open, Midnight Open, London Lunch, New York PM, and more.

Capture high-volume periods like Power Hour, Equities Open, and Asian Range.

Macros:

Identify key moments like London 02:33, New York 08:50, and other significant times aligned with market movements or events.

This library is perfect for integrating into your custom strategies, backtesting, or setting alerts for optimal trade execution during major trading sessions and events.

"如何用wind搜索股票的发行价和份数" için komut dosyalarını ara

ICT Asian Range and KillzonesThis TradingView indicator highlights key trading sessions and their price ranges on a chart. It identifies the Asian Range and the Killzones for both the London Open and New York Open sessions. Here’s a brief breakdown:

Asian Range:

Defines the high and low price levels during the Asian trading session (between the specified start and end hours, default 00:00 to 04:00 UTC).

Plots horizontal lines to mark the highest and lowest prices reached during the Asian session.

Adds labels showing the values of these high and low points after the session ends.

London and New York Killzones:

Identifies the “Killzones” or key trading windows for the London Open (default 06:00 to 09:00 UTC) and the New York Open (default 11:00 to 14:00 UTC).

Tracks the high and low price levels within these windows and plots rectangles ("boxes") on the chart to visualize these ranges.

The boxes are color-coded and customizable, indicating potential areas of high market activity or volatility.

Customizable Visuals:

Users can adjust the colors, border widths, and other visual properties for better clarity and chart integration.

[ALGOA+] Markov Chains Library by @metacamaleoLibrary "MarkovChains"

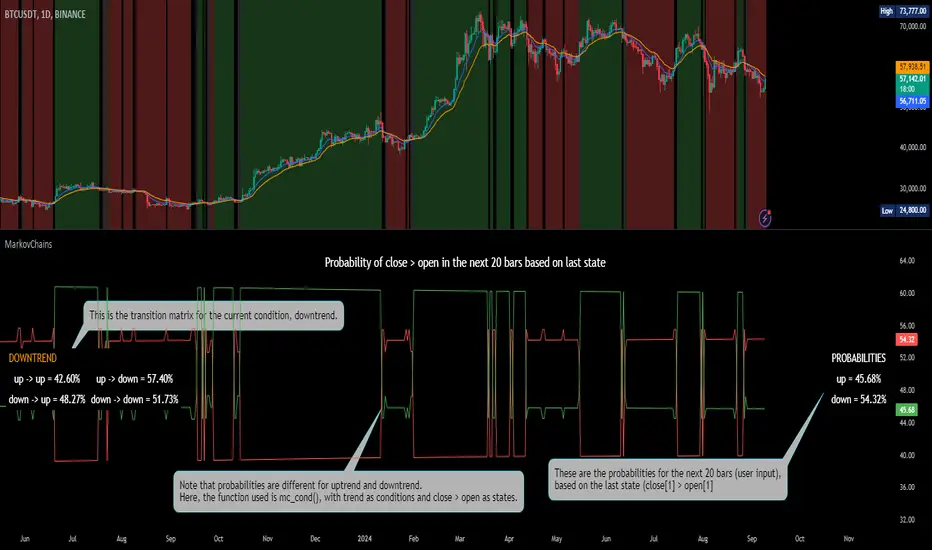

Markov Chains library by @metacamaleo. Created in 09/08/2024.

This library provides tools to calculate and visualize Markov Chain-based transition matrices and probabilities. This library supports two primary algorithms: a rolling window Markov Chain and a conditional Markov Chain (which operates based on specified conditions). The key concepts used include Markov Chain states, transition matrices, and future state probabilities based on past market conditions or indicators.

Key functions:

- `mc_rw()`: Builds a transition matrix using a rolling window Markov Chain, calculating probabilities based on a fixed length of historical data.

- `mc_cond()`: Builds a conditional Markov Chain transition matrix, calculating probabilities based on the current market condition or indicator state.

Basically, you will just need to use the above functions on your script to default outputs and displays.

Exported UDTs include:

- s_map: An UDT variable used to store a map with dummy states, i.e., if possible states are bullish, bearish, and neutral, and current is bullish, it will be stored

in a map with following keys and values: "bullish", 1; "bearish", 0; and "neutral", 0. You will only use it to customize your own script, otherwise, it´s only for internal use.

- mc_states: This UDT variable stores user inputs, calculations and MC outputs. As the above, you don´t need to use it, but you may get features to customize your own script.

For example, you may use mc.tm to get the transition matrix, or the prob map to customize the display. As you see, functions are all based on mc_states UDT. The s_map UDT is used within mc_states´s s array.

Optional exported functions include:

- `mc_table()`: Displays the transition matrix in a table format on the chart for easy visualization of the probabilities.

- `display_list()`: Displays a map (or array) of string and float/int values in a table format, used for showing transition counts or probabilities.

- `mc_prob()`: Calculates and displays probabilities for a given number of future bars based on the current state in the Markov Chain.

- `mc_all_states_prob()`: Calculates probabilities for all states for future bars, considering all possible transitions.

The above functions may be used to customize your outputs. Use the returned variable mc_states from mc_rw() and mc_cond() to display each of its matrix, maps or arrays using mc_table() (for matrices) and display_list() (for maps and arrays) if you desire to debug or track the calculation process.

See the examples in the end of this script.

Have good trading days!

Best regards,

@metacamaleo

-----------------------------

KEY FUNCTIONS

mc_rw(state, length, states, pred_length, show_table, show_prob, table_position, prob_position, font_size)

Builds the transition matrix for a rolling window Markov Chain.

Parameters:

state (string) : The current state of the market or system.

length (int) : The rolling window size.

states (array) : Array of strings representing the possible states in the Markov Chain.

pred_length (int) : The number of bars to predict into the future.

show_table (bool) : Boolean to show or hide the transition matrix table.

show_prob (bool) : Boolean to show or hide the probability table.

table_position (string) : Position of the transition matrix table on the chart.

prob_position (string) : Position of the probability list on the chart.

font_size (string) : Size of the table font.

Returns: The transition matrix and probabilities for future states.

mc_cond(state, condition, states, pred_length, show_table, show_prob, table_position, prob_position, font_size)

Builds the transition matrix for conditional Markov Chains.

Parameters:

state (string) : The current state of the market or system.

condition (string) : A string representing the condition.

states (array) : Array of strings representing the possible states in the Markov Chain.

pred_length (int) : The number of bars to predict into the future.

show_table (bool) : Boolean to show or hide the transition matrix table.

show_prob (bool) : Boolean to show or hide the probability table.

table_position (string) : Position of the transition matrix table on the chart.

prob_position (string) : Position of the probability list on the chart.

font_size (string) : Size of the table font.

Returns: The transition matrix and probabilities for future states based on the HMM.

Rolling Calmar Ratio with Ref Ticker V1.0 [ADRIDEM]Overview

The Rolling Calmar Ratio with Ref Ticker script is designed to offer a comprehensive view of the Calmar ratios for a selected reference ticker and the current ticker. This script helps investors compare risk-adjusted returns between two assets over a rolling period, providing insights into their relative performance and risk. Below is a detailed presentation of the script and its unique features.

Unique Features of the New Script

Reference Ticker Comparison : Allows users to compare the Calmar ratio of the current ticker with a reference ticker, providing a relative performance analysis. Default ticker is BTCUSDT but can be changed.

Customizable Rolling Window : Enables users to set the length for the rolling window, adapting to different market conditions and timeframes. The default value is 252 bars, which approximates one year of trading days, but it can be adjusted as needed.

Smoothing Option : Includes an option to apply a smoothing simple moving average (SMA) to the Calmar ratios, helping to reduce noise and highlight trends. The smoothing length is customizable, with a default value of 14 bars.

Visual Indicators : Plots the smoothed Calmar ratios for both the reference ticker and the current ticker, with distinct colors for easy comparison. Additionally, a horizontal line helps identify key levels.

Dynamic Background Color : Adds a gray-blue transparent background between the Calmar ratio levels of 0 and 1, highlighting the critical region where risk-adjusted returns are assessed.

Originality and Usefulness

This script uniquely combines the analysis of Calmar ratios for a reference ticker and the current ticker, providing a comparative view of their risk-adjusted returns. The inclusion of a customizable rolling window and smoothing option enhances its adaptability and usefulness in various market conditions.

Signal Description

The script includes several features that highlight potential insights into the risk-adjusted returns of the assets:

Reference Ticker Calmar Ratio : Plotted as a red line, this represents the smoothed Calmar ratio for the user-selected reference ticker.

Current Ticker Calmar Ratio : Plotted as a white line, this represents the smoothed Calmar ratio for the current ticker.

Horizontal Lines and Background Color : A line at 0 helps to quickly identify the regions of positive and negative risk-adjusted returns.

These features assist in identifying relative performance differences and confirming the strength or weakness of risk-adjusted returns between the two tickers.

Detailed Description

Input Variables

Length for Rolling Window (`length`) : Defines the range for calculating the rolling Calmar ratio. Default is 252.

Smoothing Length (`smoothing_length`) : The number of periods for the smoothing SMA. Default is 14.

Reference Ticker (`ref_ticker`) : The ticker symbol for the reference asset. Default is "BINANCE:BTCUSDT".

Functionality

Calmar Ratio Calculation : The script calculates the cumulative returns and maximum drawdown for both the reference ticker and the current ticker. These values are used to compute the Calmar ratio.

```pine

ref_cumulativeReturn = (ref_close / ta.valuewhen(ta.lowest(ref_close, length) == ref_close, ref_close, 0)) - 1

ref_rollingMax = ta.highest(ref_close, length)

ref_drawdown = (ref_close - ref_rollingMax) / ref_rollingMax

ref_maxDrawdown = ta.lowest(ref_drawdown, length)

ref_calmarRatio = ref_cumulativeReturn / math.abs(ref_maxDrawdown)

current_cumulativeReturn = (close / ta.valuewhen(ta.lowest(close, length) == close, close, 0)) - 1

current_rollingMax = ta.highest(close, length)

current_drawdown = (close - current_rollingMax) / current_rollingMax

current_maxDrawdown = ta.lowest(current_drawdown, length)

current_calmarRatio = current_cumulativeReturn / math.abs(current_maxDrawdown)

```

Smoothing : A simple moving average is applied to the Calmar ratios to smooth the data.

```pine

smoothed_ref_calmarRatio = ta.sma(ref_calmarRatio, smoothing_length)

smoothed_current_calmarRatio = ta.sma(current_calmarRatio, smoothing_length)

```

Plotting : The script plots the smoothed Calmar ratios for both the reference ticker and the current ticker, along with a horizontal line.

```pine

plot(smoothed_ref_calmarRatio, title="Ref Ticker Calmar Ratio", color=color.rgb(255, 82, 82, 50), linewidth=2)

plot(smoothed_current_calmarRatio, title="Current Ticker Calmar Ratio", color=color.white, linewidth=2)

h0 = hline(0, "Zero Line", color=color.gray)

fill(h0, h1, color=color.rgb(33, 150, 243, 90), title="Background")

```

How to Use

Configuring Inputs : Adjust the detection length and smoothing length as needed. Set the reference ticker to the desired asset for comparison.

Interpreting the Indicator : Use the plotted Calmar ratios and horizontal line to assess the relative risk-adjusted returns of the reference and current tickers.

Signal Confirmation : Look for differences in the Calmar ratios to identify potential performance advantages or weaknesses. The horizontal line helps to highlight key levels of risk-adjusted returns.

This script provides a detailed comparative view of risk-adjusted returns, aiding in more informed decision-making by highlighting key differences between the reference ticker and the current ticker.

Rolling Sortino Ratio with Ref Ticker V1.0 [ADRIDEM]Overview

The Rolling Sortino Ratio with Ref Ticker script is designed to offer a comprehensive view of the Sortino ratios for a selected reference ticker and the current ticker. This script helps investors compare risk-adjusted returns between two assets over a rolling period, providing insights into their relative performance and risk. Below is a detailed presentation of the script and its unique features.

Unique Features of the New Script

Reference Ticker Comparison : Allows users to compare the Sortino ratio of the current ticker with a reference ticker, providing a relative performance analysis. Default ticker is BTCUSDT but can be changed.

Customizable Rolling Window : Enables users to set the length for the rolling window, adapting to different market conditions and timeframes. The default value is 252 bars, which approximates one year of trading days, but it can be adjusted as needed.

Smoothing Option : Includes an option to apply a smoothing simple moving average (SMA) to the Sortino ratios, helping to reduce noise and highlight trends. The smoothing length is customizable, with a default value of 4 bars.

Visual Indicators : Plots the smoothed Sortino ratios for both the reference ticker and the current ticker, with distinct colors for easy comparison. Additionally, horizontal lines and a shaded background help identify key levels.

Dynamic Background Color : Adds a gray-blue transparent background between the Sortino ratio levels of 0 and 1, highlighting the critical region where risk-adjusted returns are assessed.

Originality and Usefulness

This script uniquely combines the analysis of Sortino ratios for a reference ticker and the current ticker, providing a comparative view of their risk-adjusted returns. The inclusion of a customizable rolling window and smoothing option enhances its adaptability and usefulness in various market conditions.

Signal Description

The script includes several features that highlight potential insights into the risk-adjusted returns of the assets:

Reference Ticker Sortino Ratio : Plotted as a red line, this represents the smoothed Sortino ratio for the user-selected reference ticker.

Current Ticker Sortino Ratio : Plotted as a white line, this represents the smoothed Sortino ratio for the current ticker.

Horizontal Lines and Background Color : Lines at 0 and 1, along with a shaded background between these levels, help to quickly identify the regions of positive and strong risk-adjusted returns.

These features assist in identifying relative performance differences and confirming the strength or weakness of risk-adjusted returns between the two tickers.

Detailed Description

Input Variables

Length for Rolling Window (`length`) : Defines the range for calculating the rolling Sortino ratio. Default is 252.

Smoothing Length (`smoothing_length`) : The number of periods for the smoothing SMA. Default is 4.

Annual Risk-Free Rate (`riskFreeRate`) : The annual risk-free rate used in the Sortino ratio calculation. Default is 0.02 (2%).

Reference Ticker (`ref_ticker`) : The ticker symbol for the reference asset. Default is "BINANCE:BTCUSDT".

Functionality

Sortino Ratio Calculation : The script calculates the daily returns, mean return, and downside deviation for both the reference ticker and the current ticker. These values are used to compute the annualized Sortino ratio.

```pine

ref_dailyReturn = ta.change(ref_close) / ref_close

ref_meanReturn = ta.sma(ref_dailyReturn, length)

ref_downsideDeviation = ta.stdev(math.min(ref_dailyReturn, 0), length)

ref_annualizedReturn = ref_meanReturn * length

ref_annualizedDownsideDev = ref_downsideDeviation * math.sqrt(length)

ref_sortinoRatio = (ref_annualizedReturn - riskFreeRate) / ref_annualizedDownsideDev

```

Smoothing : A simple moving average is applied to the Sortino ratios to smooth the data.

```pine

smoothed_ref_sortinoRatio = ta.sma(ref_sortinoRatio, smoothing_length)

smoothed_current_sortinoRatio = ta.sma(current_sortinoRatio, smoothing_length)

```

Plotting : The script plots the smoothed Sortino ratios for both the reference ticker and the current ticker, along with horizontal lines and a shaded background.

```pine

plot(smoothed_ref_sortinoRatio, title="Ref Ticker Sortino Ratio", color=color.rgb(255, 82, 82, 50), linewidth=2)

plot(smoothed_current_sortinoRatio, title="Current Ticker Sortino Ratio", color=color.white, linewidth=2)

h0 = hline(0, "Zero Line", color=color.gray)

h1 = hline(1, "One Line", color=color.gray)

fill(h0, h1, color=color.rgb(33, 150, 243, 90), title="Background")

```

How to Use

Configuring Inputs : Adjust the detection length, smoothing length, and risk-free rate as needed. Set the reference ticker to the desired asset for comparison.

Interpreting the Indicator : Use the plotted Sortino ratios and background shading to assess the relative risk-adjusted returns of the reference and current tickers.

Signal Confirmation : Look for differences in the Sortino ratios to identify potential performance advantages or weaknesses. The background shading helps to highlight key levels of risk-adjusted returns.

This script provides a detailed comparative view of risk-adjusted returns, aiding in more informed decision-making by highlighting key differences between the reference ticker and the current ticker.

Rolling Sharpe Ratio with Ref Ticker V1.0 [ADRIDEM]Overview

The Rolling Sharpe Ratio with Ref Ticker script is designed to offer a comprehensive view of the Sharpe ratios for a selected reference ticker and the current ticker. This script helps investors compare risk-adjusted returns between two assets over a rolling period, providing insights into their relative performance and risk. Below is a detailed presentation of the script and its unique features.

Unique Features of the New Script

Reference Ticker Comparison : Allows users to compare the Sharpe ratio of the current ticker with a reference ticker, providing a relative performance analysis. Default ticker is BTCUSDT but can be changed.

Customizable Rolling Window : Enables users to set the length for the rolling window, adapting to different market conditions and timeframes. The default value is 252 bars, which approximates one year of trading days, but it can be adjusted as needed.

Smoothing Option : Includes an option to apply a smoothing simple moving average (SMA) to the Sharpe ratios, helping to reduce noise and highlight trends. The smoothing length is customizable, with a default value of 4 bars.

Visual Indicators : Plots the smoothed Sharpe ratios for both the reference ticker and the current ticker, with distinct colors for easy comparison. Additionally, horizontal lines and a shaded background help identify key levels.

Dynamic Background Color : Adds a gray-blue transparent background between the Sharpe ratio levels of 0 and 1, highlighting the critical region where risk-adjusted returns are assessed.

Originality and Usefulness

This script uniquely combines the analysis of Sharpe ratios for a reference ticker and the current ticker, providing a comparative view of their risk-adjusted returns. The inclusion of a customizable rolling window and smoothing option enhances its adaptability and usefulness in various market conditions.

Signal Description

The script includes several features that highlight potential insights into the risk-adjusted returns of the assets:

Reference Ticker Sharpe Ratio : Plotted as a red line, this represents the smoothed Sharpe ratio for the user-selected reference ticker.

Current Ticker Sharpe Ratio : Plotted as a white line, this represents the smoothed Sharpe ratio for the current ticker.

Horizontal Lines and Background Color : Lines at 0 and 1, along with a shaded background between these levels, help to quickly identify the regions of positive and strong risk-adjusted returns.

These features assist in identifying relative performance differences and confirming the strength or weakness of risk-adjusted returns between the two tickers.

Detailed Description

Input Variables

Length for Rolling Window (`length`) : Defines the range for calculating the rolling Sharpe ratio. Default is 252.

Smoothing Length (`smoothing_length`) : The number of periods for the smoothing SMA. Default is 4.

Annual Risk-Free Rate (`riskFreeRate`) : The annual risk-free rate used in the Sharpe ratio calculation. Default is 0.02 (2%).

Reference Ticker (`ref_ticker`) : The ticker symbol for the reference asset. Default is "BINANCE:BTCUSDT".

Functionality

Sharpe Ratio Calculation : The script calculates the daily returns, mean return, and standard deviation for both the reference ticker and the current ticker. These values are used to compute the annualized Sharpe ratio.

```pine

ref_dailyReturn = ta.change(ref_close) / ref_close

ref_meanReturn = ta.sma(ref_dailyReturn, length)

ref_stdDevReturn = ta.stdev(ref_dailyReturn, length)

ref_annualizedReturn = ref_meanReturn * length

ref_annualizedStdDev = ref_stdDevReturn * math.sqrt(length)

ref_sharpeRatio = (ref_annualizedReturn - riskFreeRate) / ref_annualizedStdDev

```

Smoothing : A simple moving average is applied to the Sharpe ratios to smooth the data.

```pine

smoothed_ref_sharpeRatio = ta.sma(ref_sharpeRatio, smoothing_length)

smoothed_current_sharpeRatio = ta.sma(current_sharpeRatio, smoothing_length)

```

Plotting : The script plots the smoothed Sharpe ratios for both the reference ticker and the current ticker, along with horizontal lines and a shaded background.

```pine

plot(smoothed_ref_sharpeRatio, title="Ref Ticker Sharpe Ratio", color=color.rgb(255, 82, 82, 50), linewidth=2)

plot(smoothed_current_sharpeRatio, title="Current Ticker Sharpe Ratio", color=color.white, linewidth=2)

h0 = hline(0, "Zero Line", color=color.gray)

h1 = hline(1, "One Line", color=color.gray)

fill(h0, h1, color=color.rgb(33, 150, 243, 90), title="Background")

```

How to Use

Configuring Inputs : Adjust the detection length, smoothing length, and risk-free rate as needed. Set the reference ticker to the desired asset for comparison.

Interpreting the Indicator : Use the plotted Sharpe ratios and background shading to assess the relative risk-adjusted returns of the reference and current tickers.

Signal Confirmation : Look for differences in the Sharpe ratios to identify potential performance advantages or weaknesses. The background shading helps to highlight key levels of risk-adjusted returns.

This script provides a detailed comparative view of risk-adjusted returns, aiding in more informed decision-making by highlighting key differences between the reference ticker and the current ticker.

Double Vegas SuperTrend Enhanced - Strategy [presentTrading]

█ Introduction and How It Is Different

The "Double Vegas SuperTrend Enhanced" strategy is a sophisticated trading system that combines two Vegas SuperTrend Enhanced. Very Powerful!

Let's celebrate the joy of Children's Day on June 1st! Enjoyyy!

BTCUSD LS performance

The strategy aims to pinpoint market trends with greater accuracy and generate trades that align with the overall market direction.

This approach differentiates itself by integrating volatility adjustments and leveraging the Vegas Channel's width to refine the SuperTrend calculations, resulting in a dynamic and responsive trading system.

Additionally, the strategy incorporates customizable take-profit and stop-loss levels, providing traders with a robust framework for risk management.

-> check Vegas SuperTrend Enhanced - Strategy

█ Strategy, How It Works: Detailed Explanation

🔶 Vegas Channel and SuperTrend Calculations

The strategy initiates by calculating the Vegas Channel, which is derived from a simple moving average (SMA) and the standard deviation (STD) of the closing prices over a specified window length. This channel helps in measuring market volatility and forms the basis for adjusting the SuperTrend indicator.

Vegas Channel Calculation:

- vegasMovingAverage = SMA(close, vegasWindow)

- vegasChannelStdDev = STD(close, vegasWindow)

- vegasChannelUpper = vegasMovingAverage + vegasChannelStdDev

- vegasChannelLower = vegasMovingAverage - vegasChannelStdDev

SuperTrend Multiplier Adjustment:

- channelVolatilityWidth = vegasChannelUpper - vegasChannelLower

- adjustedMultiplier = superTrendMultiplierBase + volatilityAdjustmentFactor * (channelVolatilityWidth / vegasMovingAverage)

The adjusted multiplier enhances the SuperTrend's sensitivity to market volatility, making it more adaptable to changing market conditions.

BTCUSD Local picture.

🔶 Average True Range (ATR) and SuperTrend Values

The ATR is computed over a specified period to measure market volatility. Using the ATR and the adjusted multiplier, the SuperTrend upper and lower levels are determined.

ATR Calculation:

- averageTrueRange = ATR(atrPeriod)

**SuperTrend Calculation:**

- superTrendUpper = hlc3 - (adjustedMultiplier * averageTrueRange)

- superTrendLower = hlc3 + (adjustedMultiplier * averageTrueRange)

The SuperTrend levels are continuously updated based on the previous values and the current market trend direction. The market trend is determined by comparing the closing prices with the SuperTrend levels.

Trend Direction:

- If close > superTrendLowerPrev, then marketTrend = 1 (bullish)

- If close < superTrendUpperPrev, then marketTrend = -1 (bearish)

🔶 Trade Entry and Exit Conditions

The strategy generates trade signals based on the alignment of both SuperTrends. Trades are executed only when both SuperTrends indicate the same market direction.

Entry Conditions:

- Long Position: Both SuperTrends must signal a bullish trend.

- Short Position: Both SuperTrends must signal a bearish trend.

Exit Conditions:

- Positions are exited if either SuperTrend reverses its trend direction.

- Additional conditions include holding periods and configurable take-profit and stop-loss levels.

█ Trade Direction

The strategy allows traders to specify the desired trade direction through a customizable input setting. Options include:

- Long: Only enter long positions.

- Short: Only enter short positions.

- Both: Enter both long and short positions based on the market conditions.

█ Usage

To utilize the "Double Vegas SuperTrend Enhanced" strategy, traders need to configure the input settings according to their trading preferences and market conditions. The strategy includes parameters for ATR periods, Vegas Channel window lengths, SuperTrend multipliers, volatility adjustment factors, and risk management settings such as hold days, take-profit, and stop-loss percentages.

█ Default Settings

The strategy comes with default settings that can be adjusted to fit individual trading styles:

- trade Direction: Both (allows trading in both long and short directions for maximum flexibility).

- ATR Periods: 10 for SuperTrend 1 and 5 for SuperTrend 2 (shorter ATR period results in more sensitivity to recent price movements).

- Vegas Window Lengths: 100 for SuperTrend 1 and 200 for SuperTrend 2 (longer window length results in smoother moving averages and less sensitivity to short-term volatility).

- SuperTrend Multipliers: 5 for SuperTrend 1 and 7 for SuperTrend 2 (higher multipliers lead to wider SuperTrend channels, reducing the frequency of trades).

- Volatility Adjustment Factors: 5 for SuperTrend 1 and 7 for SuperTrend 2 (higher adjustment factors increase the responsiveness to changes in market volatility).

- Hold Days: 5 (defines the minimum duration a position is held, ensuring trades are not exited prematurely).

- Take Profit: 30% (sets the target profit level to lock in gains).

- Stop Loss: 20% (sets the maximum acceptable loss level to mitigate risk).

7 hours a day by Yasser (YWMAAAWORLD)Hey there, traders! Today, we're diving into a nifty Pine Script called "7 hours a day," crafted by me Yasser (YWMAAAWorld). So, what's the scoop?

Imagine having a tool that highlights specific times on your chart like clockwork, making your trading day a breeze. That's precisely what this script does. It's like having a personal assistant reminding you of the important moments in the market.

Picture this: as the clock strikes 8:00 PM and 3:00 AM, our script draws these magical lines on your chart. These aren't just any lines; they're your guides, marking the boundaries of a crucial 7-hour period. Think of it as your trading sanctuary within the chaos of the market.

But wait, there's more! Our script isn't just about pretty lines. It's smart too. It knows when it's a weekend or Monday morning, so you can kick back and relax without unnecessary clutter on your chart.

Now, here's where the magic really happens. Within these 7-hour windows, our script calculates the highest and lowest price points, giving you a clear picture of market dynamics during those crucial hours. It's like having a crystal ball revealing the market's secrets.

So, whether you're a seasoned trader or just starting, "7 hours a day" is your trusty sidekick, guiding you through the twists and turns of the market with style and precision. Say goodbye to guesswork and hello to clarity in your trading journey!

it is believed that market ranges within these 7-hour windows, and when broken up or down you could expect a momentum price movement.

Momentum Ghost Machine [ChartPrime]Momentum Ghost Machine (ChartPrime) is designed to be the next generation in momentum/rate of change analysis. This indicator utilizes the properties of one of our favorite filters to create a more accurate and stable momentum oscillator by using a high quality filtered delayed signal to do the momentum comparison.

Traditional momentum/roc uses the raw price data to compare current price to previous price to generate a directional oscillator. This leaves the oscillator prone to false readings and noisy outputs that leave traders unsure of the real likelihood of a future movement. One way to mitigate this issue would be to use some sort of moving average. Unfortunately, this can only go so far because simple moving average algorithms result in a poor reconstruction of the actual shape of the underlying signal.

The windowed sinc low pass filter is a linear phase filter, meaning that it doesn't change the shape or size of the original signal when applied. This results in a faithful reconstruction of the original signal, but without the "high frequency noise". Just like any filter, the process of applying it requires that we have "future" samples resulting in a time delay for real time applications. Fortunately this is a great thing in the context of a momentum oscillator because we need some representation of past price data to compare the current price data to. By using an ideal low pass filter to generate this delayed signal we can super charge the momentum oscillator and fix the majority of issues its predecessors had.

This indicator has a few extra features that other momentum/roc indicators dont have. One major yet simple improvement is the inclusion of a moving average to help gauge the rate of change of this indicator. Since we included a moving average, we thought it would only be appropriate to add a histogram to help visualize the relationship between the signal and its average. To go further with this we have also included linear extrapolation to further help you predict the momentum and direction of this oscillator. Included with this extrapolation we have also added the histogram in the extrapolation to further enhance its visual interpretation. Finally, the inclusion of a candle coloring feature really drives how the utility of the Momentum Machine .

There are three distinct options when using the candle coloring feature: Direct, MA, and Both. With direct the candles will be colored based on the indicators direction and polarity. When it is above zero and moving up, it displays a green color. When it is above zero and moving down it will display a light green color. Conversely, when the indicator is below zero and moving down it displays a red color, and when it it moving up and below zero it will display a light red color. MA coloring will color the candles just like a MACD. If the signal is above its MA and moving up it will display a green color, and when it is above its MA and moving down it will display a light green color.

When the signal is below its MA and moving down it will display a red color, and when its below its ma and moving up it will display a light red color. Both combines the two into a single color scheme providing you with the best of both worlds. If the indicator is above zero it will display the MA colors with a slight twist. When the indicator is moving down and is below its MA it will display a lighter color than before, and when it is below zero and is above its MA it will display a darker color color.

Length of 50 with a smoothing of 100

Length of 50 with a smoothing of 25

By default, the indicator is set to a momentum length of 50, with a post smoothing of 2. We have chosen the longer period for the momentum length to highlight the performance of this indicator compared to its ancestors. A major point to consider with this indicator is that you can only achieve so much smoothing for a chosen delay. This is because more data is required to produce a smoother signal at a specified length. Once you have selected your desired momentum length you can then select your desired momentum smoothing . This is made possible by the use of the windowed sinc low pass algorithm because it includes a frequency cutoff argument. This means that you can have as little or as much smoothing as you please without impacting the period of the indicator. In the provided examples above this paragraph is a visual representation of what is going on under the hood of this indicator. The blue line is the filtered signal being compared to the current closing price. As you can see, the filtered signal is very smooth and accurately represents the underlying price action without noise.

We hope that users can find the same utility as we did in this indicator and that it levels up your analysis utilizing the momentum oscillator or rate of change.

Enjoy

aproxLibrary "aprox"

It's a library of the aproximations of a price or Series float it uses Fourier transform and

Euler's Theoreum for Homogenus White noice operations. Calling functions without source value it automatically take close as the default source value.

Copy this indicator to see how each approximations interact between each other.

import Celje_2300/aprox/1 as aprox

//@version=5

indicator("Close Price with Aproximations", shorttitle="Close and Aproximations", overlay=false)

// Sample input data (replace this with your own data)

inputData = close

// Plot Close Price

plot(inputData, color=color.blue, title="Close Price")

dtf32_result = aprox.DTF32()

plot(dtf32_result, color=color.green, title="DTF32 Aproximation")

fft_result = aprox.FFT()

plot(fft_result, color=color.red, title="DTF32 Aproximation")

wavelet_result = aprox.Wavelet()

plot(wavelet_result, color=color.orange, title="Wavelet Aproximation")

wavelet_std_result = aprox.Wavelet_std()

plot(wavelet_std_result, color=color.yellow, title="Wavelet_std Aproximation")

DFT3(xval, _dir)

Parameters:

xval (float)

_dir (int)

//@version=5

import Celje_2300/aprox/1 as aprox

indicator("Example - DFT3", shorttitle="DFT3 Example", overlay=true)

// Sample input data (replace this with your own data)

inputData = close

// Apply DFT3

result = aprox.DFT3(inputData, 2)

// Plot the result

plot(result, color=color.blue, title="DFT3 Result")

DFT2(xval, _dir)

Parameters:

xval (float)

_dir (int)

//@version=5

import Celje_2300/aprox/1 as aprox

indicator("Example - DFT2", shorttitle="DFT2 Example", overlay=true)

// Sample input data (replace this with your own data)

inputData = close

// Apply DFT2

result = aprox.DFT2(inputData, inputData, 1)

// Plot the result

plot(result, color=color.green, title="DFT2 Result")

//@version=5

import Celje_2300/aprox/1 as aprox

indicator("Example - DFT2", shorttitle="DFT2 Example", overlay=true)

// Sample input data (replace this with your own data)

inputData = close

// Apply DFT2

result = aprox.DFT2(inputData, 1)

// Plot the result

plot(result, color=color.green, title="DFT2 Result")

FFT(xval)

FFT: Fast Fourier Transform

Parameters:

xval (float)

Returns: Aproxiated source value

//@version=5

import Celje_2300/aprox/1 as aprox

indicator("Example - FFT", shorttitle="FFT Example", overlay=true)

// Sample input data (replace this with your own data)

inputData = close

// Apply FFT

result = aprox.FFT(inputData)

// Plot the result

plot(result, color=color.red, title="FFT Result")

DTF32(xval)

DTF32: Combined Discrete Fourier Transforms

Parameters:

xval (float)

Returns: Aproxiated source value

//@version=5

import Celje_2300/aprox/1 as aprox

indicator("Example - DTF32", shorttitle="DTF32 Example", overlay=true)

// Sample input data (replace this with your own data)

inputData = close

// Apply DTF32

result = aprox.DTF32(inputData)

// Plot the result

plot(result, color=color.purple, title="DTF32 Result")

whitenoise(indic_, _devided, minEmaLength, maxEmaLength, src)

whitenoise: Ehler's Universal Oscillator with White Noise, without extra aproximated src

Parameters:

indic_ (float)

_devided (int)

minEmaLength (int)

maxEmaLength (int)

src (float)

Returns: Smoothed indicator value

//@version=5

import Celje_2300/aprox/1 as aprox

indicator("Example - whitenoise", shorttitle="whitenoise Example", overlay=true)

// Sample input data (replace this with your own data)

inputData = close

// Apply whitenoise

result = aprox.whitenoise(aprox.FFT(inputData))

// Plot the result

plot(result, color=color.orange, title="whitenoise Result")

whitenoise(indic_, dft1, _devided, minEmaLength, maxEmaLength, src)

whitenoise: Ehler's Universal Oscillator with White Noise and DFT1

Parameters:

indic_ (float)

dft1 (float)

_devided (int)

minEmaLength (int)

maxEmaLength (int)

src (float)

Returns: Smoothed indicator value

//@version=5

import Celje_2300/aprox/1 as aprox

indicator("Example - whitenoise with DFT1", shorttitle="whitenoise-DFT1 Example", overlay=true)

// Sample input data (replace this with your own data)

inputData = close

// Apply whitenoise with DFT1

result = aprox.whitenoise(inputData, aprox.DFT1(inputData))

// Plot the result

plot(result, color=color.yellow, title="whitenoise-DFT1 Result")

smooth(dft1, indic__, _devided, minEmaLength, maxEmaLength, src)

smooth: Smoothing source value with help of indicator series and aproximated source value

Parameters:

dft1 (float)

indic__ (float)

_devided (int)

minEmaLength (int)

maxEmaLength (int)

src (float)

Returns: Smoothed source series

//@version=5

import Celje_2300/aprox/1 as aprox

indicator("Example - smooth", shorttitle="smooth Example", overlay=true)

// Sample input data (replace this with your own data)

inputData = close

// Apply smooth

result = aprox.smooth(inputData, aprox.FFT(inputData))

// Plot the result

plot(result, color=color.gray, title="smooth Result")

smooth(indic__, _devided, minEmaLength, maxEmaLength, src)

smooth: Smoothing source value with help of indicator series

Parameters:

indic__ (float)

_devided (int)

minEmaLength (int)

maxEmaLength (int)

src (float)

Returns: Smoothed source series

//@version=5

import Celje_2300/aprox/1 as aprox

indicator("Example - smooth without DFT1", shorttitle="smooth-NoDFT1 Example", overlay=true)

// Sample input data (replace this with your own data)

inputData = close

// Apply smooth without DFT1

result = aprox.smooth(aprox.FFT(inputData))

// Plot the result

plot(result, color=color.teal, title="smooth-NoDFT1 Result")

vzo_ema(src, len)

vzo_ema: Volume Zone Oscillator with EMA smoothing

Parameters:

src (float)

len (simple int)

Returns: VZO value

vzo_sma(src, len)

vzo_sma: Volume Zone Oscillator with SMA smoothing

Parameters:

src (float)

len (int)

Returns: VZO value

vzo_wma(src, len)

vzo_wma: Volume Zone Oscillator with WMA smoothing

Parameters:

src (float)

len (int)

Returns: VZO value

alma2(series, windowsize, offset, sigma)

alma2: Arnaud Legoux Moving Average 2 accepts sigma as series float

Parameters:

series (float)

windowsize (int)

offset (float)

sigma (float)

Returns: ALMA value

Wavelet(src, len, offset, sigma)

Wavelet: Wavelet Transform

Parameters:

src (float)

len (int)

offset (simple float)

sigma (simple float)

Returns: Wavelet-transformed series

//@version=5

import Celje_2300/aprox/1 as aprox

indicator("Example - Wavelet", shorttitle="Wavelet Example", overlay=true)

// Sample input data (replace this with your own data)

inputData = close

// Apply Wavelet

result = aprox.Wavelet(inputData)

// Plot the result

plot(result, color=color.blue, title="Wavelet Result")

Wavelet_std(src, len, offset, mag)

Wavelet_std: Wavelet Transform with Standard Deviation

Parameters:

src (float)

len (int)

offset (float)

mag (int)

Returns: Wavelet-transformed series

//@version=5

import Celje_2300/aprox/1 as aprox

indicator("Example - Wavelet_std", shorttitle="Wavelet_std Example", overlay=true)

// Sample input data (replace this with your own data)

inputData = close

// Apply Wavelet_std

result = aprox.Wavelet_std(inputData)

// Plot the result

plot(result, color=color.green, title="Wavelet_std Result")

[S] Rolling TrendlineThe Rolling Linear Regression Trendline is a sophisticated technical analysis tool designed to offer traders a dynamic view of market trends over a selectable period. This indicator employs linear regression to calculate and plot a trendline that best fits the closing prices within a specified window, either defined by a number of bars or a set period in days, independent of the chart's timeframe.

Key Features:

Dynamic Window Selection: Users can choose the calculation window based on a fixed number of bars or days, providing flexibility to adapt to different trading strategies and timeframes. For the 'days' option, the indicator calculates the equivalent number of bars based on the chart's timeframe, ensuring relevance across various market conditions and trading sessions.

Linear Regression Analysis: At its core, the indicator uses linear regression to identify the trend direction by calculating the slope and intercept of the trendline. This method offers a statistical approach to trend analysis, highlighting potential uptrends or downtrends based on the positioning and direction of the trendline.

Customizable Period: Traders can input their desired period (N), allowing for tailored analysis. Whether it's short-term movements or longer-term trends, the indicator can adjust to focus on specific time horizons, enhancing its utility across different trading styles and objectives.

Applications:

Trend Identification: By plotting a trendline that mathematically fits the closing prices over the chosen period, traders can quickly identify the prevailing market trend, aiding in bullish or bearish decision-making.

Support and Resistance: The trendline can also serve as a dynamic level of support or resistance, offering potential entry or exit points based on the price's interaction with the trendline.

Strategic Planning: With the ability to adjust the calculation window, traders can align the indicator with their trading strategy, whether focusing on intraday movements or broader swings.

Using this indicator with other parameters can widen you view of the market and help identifying trends

MA+ ProjectionThe "MA+ Projection" indicator is designed to visualize the potential future direction of a moving average, taking into account the impact of historical data loss. It is primarily aimed at providing a practical perspective on how moving averages could evolve as older data points are no longer considered.

Key Features:

Supported Moving Averages: SMA, EMA, WMA, VWMA, and VAWMA (Volume Adjusted WMA).

Flexible Time Span Settings: Customize the moving average length in bars, minutes, or days.

Adjustable Projection Scope: Set a percentage of the measurement to project forward.

Projection 'Cone': Show/hide the deviation and control the multiple.

Use Last Source Value: An option to add the latest known value to the moving window instead of only letting the window shrink. (Enabled by default.)

How It Works:

Given the specified parameters, it takes the selected moving average type (a known formula like SMA, EMA, or WMA), and projects the future data points by continuing to move the data 'window' forward without adding any more data. By default, it extends the average by assuming the price hasn't changed after the last bar. Alternatively, the projection can be the result of shrinking the window as it moves forward without adding any new data points.

Note:

This tool is for visual projection, not prediction. Its purpose is to aid in the analysis of potential future trends based on historical data, not to provide definitive market forecasts.

savitzkyGolay, KAMA, HPOverview

This trading indicator integrates three distinct analytical tools: the Savitzky-Golay Filter, Kaufman Adaptive Moving Average (KAMA), and Hodrick-Prescott (HP) Filter. It is designed to provide a comprehensive analysis of market trends and potential trading signals.

Components

Hodrick-Prescott (HP) Filter

Purpose: Smooths out the price data to identify the underlying trend.

Parameters: Lambda: Controls the smoothness. Range: 50 to 1600.

Impact of Parameters:

Increasing Lambda: This makes the trend line more responsive to short-term market fluctuations, suitable for short-term analysis. A higher Lambda value decreases the degree of smoothing, making the trend line follow recent market movements more closely.

Decreasing Lambda: A lower Lambda value makes the trend line smoother and less responsive to short-term market fluctuations, ideal for longer-term trend analysis. Decreasing Lambda increases the degree of smoothing, thereby filtering out minor market movements and focusing more on the long-term trend.

Kaufman Adaptive Moving Average (KAMA):

Purpose: An adaptive moving average that adjusts to price volatility.

Parameters: Length, Fast Length, Slow Length: Define the sensitivity and adaptiveness of KAMA.

Impact of Parameters:

Adjusting Length affects the base period for efficiency ratio, altering the overall sensitivity.

Fast Length and Slow Length control the speed of KAMA’s adaptation. A smaller Fast Length makes KAMA more sensitive to price changes, while a larger Slow Length makes it less sensitive.

Savitzky-Golay Filter:

Purpose: Smooths the price data using polynomial regression.

Parameters: Window Size: Determines the size of the moving window (7, 9, 11, 15, 21).

Impact of Parameters:

A larger Window Size results in a smoother curve, which is more effective for identifying long-term trends but can delay reaction to recent market changes.

A smaller Window Size makes the curve more responsive to short-term price movements, suitable for short-term trading strategies.

General Impact of Parameters

Adjusting these parameters can significantly alter the signals generated by the indicator. Users should fine-tune these settings based on their trading style, the characteristics of the traded asset, and market conditions to optimize the indicator's performance.

Signal Logic

Buy Signal: The trend from the HP filter is below both the KAMA and the Savitzky-Golay SMA, and none of these indicators are flat.

Sell Signal: The trend from the HP filter is above both the KAMA and the Savitzky-Golay SMA, and none of these indicators are flat.

Usage

Due to the combination of smoothing algorithms and adaptability, this indicator is highly effective at identifying emerging trends for both initiating long and short positions.

IMPORTANT : Although the code and user settings incorporate measures to limit false signals due to lateral (sideways) movement, they do not completely eliminate such occurrences. Users are strongly advised to avoid signals that emerge during simultaneous lateral movements of all three indicators.

Despite the indicator's success in historical data analysis using its signals alone, it is highly recommended to use this code in combination with other indicators, patterns, and zones. This is particularly important for determining exit points from positions, which can significantly enhance trading results.

Limitations and Recommendations

The indicator has shown excellent performance on the weekly time frame (TF) with the following settings:

Savitzky-Golay (SG): 11

Hodrick-Prescott (HP): 100

Kaufman Adaptive Moving Average (KAMA): 20, 2, 30

For the monthly TF, the recommended settings are:

SG: 15

HP: 100

KAMA: 30, 2, 35

Note: The monthly TF is quite variable. With these settings, there may be fewer signals, but they tend to be more relevant for long-term investors. Based on a sample of 40 different stocks from various countries and sectors, most exhibited an average trade return in the thousands of percent.

It's important to note that while these settings have been successful in past performance, market conditions vary and past performance is not indicative of future results. Users are encouraged to experiment with these settings and adjust them according to their individual needs and market analysis.

As this is my first developed trading indicator, I am very open to and appreciative of any suggestions or comments. Your feedback is invaluable in helping me refine and improve this tool. Please feel free to share your experiences, insights, or any recommendations you may have.

Adaptive Oscillator constructor [lastguru]Adaptive Oscillators use the same principle as Adaptive Moving Averages. This is an experiment to separate length generation from oscillators, offering multiple alternatives to be combined. Some of the combinations are widely known, some are not. Note that all Oscillators here are normalized to -1..1 range. This indicator is based on my previously published public libraries and also serve as a usage demonstration for them. I will try to expand the collection (suggestions are welcome), however it is not meant as an encyclopaedic resource , so you are encouraged to experiment yourself: by looking on the source code of this indicator, I am sure you will see how trivial it is to use the provided libraries and expand them with your own ideas and combinations. I give no recommendation on what settings to use, but if you find some useful setting, combination or application ideas (or bugs in my code), I would be happy to read about them in the comments section.

The indicator works in three stages: Prefiltering, Length Adaptation and Oscillators.

Prefiltering is a fast smoothing to get rid of high-frequency (2, 3 or 4 bar) noise.

Adaptation algorithms are roughly subdivided in two categories: classic Length Adaptations and Cycle Estimators (they are also implemented in separate libraries), all are selected in Adaptation dropdown. Length Adaptation used in the Adaptive Moving Averages and the Adaptive Oscillators try to follow price movements and accelerate/decelerate accordingly (usually quite rapidly with a huge range). Cycle Estimators, on the other hand, try to measure the cycle period of the current market, which does not reflect price movement or the rate of change (the rate of change may also differ depending on the cycle phase, but the cycle period itself usually changes slowly).

Chande (Price) - based on Chande's Dynamic Momentum Index (CDMI or DYMOI), which is dynamic RSI with this length

Chande (Volume) - a variant of Chande's algorithm, where volume is used instead of price

VIDYA - based on VIDYA algorithm. The period oscillates from the Lower Bound up (slow)

VIDYA-RS - based on Vitali Apirine's modification of VIDYA algorithm (he calls it Relative Strength Moving Average). The period oscillates from the Upper Bound down (fast)

Kaufman Efficiency Scaling - based on Efficiency Ratio calculation originally used in KAMA

Deviation Scaling - based on DSSS by John F. Ehlers

Median Average - based on Median Average Adaptive Filter by John F. Ehlers

Fractal Adaptation - based on FRAMA by John F. Ehlers

MESA MAMA Alpha - based on MESA Adaptive Moving Average by John F. Ehlers

MESA MAMA Cycle - based on MESA Adaptive Moving Average by John F. Ehlers , but unlike Alpha calculation, this adaptation estimates cycle period

Pearson Autocorrelation* - based on Pearson Autocorrelation Periodogram by John F. Ehlers

DFT Cycle* - based on Discrete Fourier Transform Spectrum estimator by John F. Ehlers

Phase Accumulation* - based on Dominant Cycle from Phase Accumulation by John F. Ehlers

Length Adaptation usually take two parameters: Bound From (lower bound) and To (upper bound). These are the limits for Adaptation values. Note that the Cycle Estimators marked with asterisks(*) are very computationally intensive, so the bounds should not be set much higher than 50, otherwise you may receive a timeout error (also, it does not seem to be a useful thing to do, but you may correct me if I'm wrong).

The Cycle Estimators marked with asterisks(*) also have 3 checkboxes: HP (Highpass Filter), SS (Super Smoother) and HW (Hann Window). These enable or disable their internal prefilters, which are recommended by their author - John F. Ehlers . I do not know, which combination works best, so you can experiment.

Chande's Adaptations also have 3 additional parameters: SD Length (lookback length of Standard deviation), Smooth (smoothing length of Standard deviation) and Power ( exponent of the length adaptation - lower is smaller variation). These are internal tweaks for the calculation.

Oscillators section offer you a choice of Oscillator algorithms:

Stochastic - Stochastic

Super Smooth Stochastic - Super Smooth Stochastic (part of MESA Stochastic) by John F. Ehlers

CMO - Chande Momentum Oscillator

RSI - Relative Strength Index

Volume-scaled RSI - my own version of RSI. It scales price movements by the proportion of RMS of volume

Momentum RSI - RSI of price momentum

Rocket RSI - inspired by RocketRSI by John F. Ehlers (not an exact implementation)

MFI - Money Flow Index

LRSI - Laguerre RSI by John F. Ehlers

LRSI with Fractal Energy - a combo oscillator that uses Fractal Energy to tune LRSI gamma

Fractal Energy - Fractal Energy or Choppiness Index by E. W. Dreiss

Efficiency ratio - based on Kaufman Adaptive Moving Average calculation

DMI - Directional Movement Index (only ADX is drawn)

Fast DMI - same as DMI, but without secondary smoothing

If no Adaptation is selected (None option), you can set Length directly. If an Adaptation is selected, then Cycle multiplier can be set.

Before an Oscillator, a High Pass filter may be executed to remove cyclic components longer than the provided Highpass Length (no High Pass filter, if Highpass Length = 0). Both before and after the Oscillator a Moving Average can be applied. The following Moving Averages are included: SMA, RMA, EMA, HMA , VWMA, 2-pole Super Smoother, 3-pole Super Smoother, Filt11, Triangle Window, Hamming Window, Hann Window, Lowpass, DSSS. For more details on these Moving Averages, you can check my other Adaptive Constructor indicator:

The Oscillator output may be renormalized and postprocessed with the following Normalization algorithms:

Stochastic - Stochastic

Super Smooth Stochastic - Super Smooth Stochastic (part of MESA Stochastic) by John F. Ehlers

Inverse Fisher Transform - Inverse Fisher Transform

Noise Elimination Technology - a simplified Kendall correlation algorithm "Noise Elimination Technology" by John F. Ehlers

Except for Inverse Fisher Transform, all Normalization algorithms can have Length parameter. If it is not specified (set to 0), then the calculated Oscillator length is used.

More information on the algorithms is given in the code for the libraries used. I am also very grateful to other TradingView community members (they are also mentioned in the library code) without whom this script would not have been possible.

Runners & Laggers (scanner)Firstly, seems to me this may only work with crypto but I know nothing about the other sectors so i could be wrong. I was trying to think up a good way to find moving coins(other than by volume bc theres holes in the results when using it this way). Thought this was an interesting concept so decided to publish it as I've seen no others like it (though i did not extensively search for it. We need to start with a little Tradingview(TV) common knowledge. When there is no update of trades/volume in a candle TV does not print the candle. So when looking at (let's say) a 1 second chart, if the coin being observed by the user has no update from a trade in the time of that 1 sec candle it is skipped over. This means that a coin with a ton of volume might fill an entire 60 seconds with 60 candles and conversely with a low volume coin there could be as little as 0 1-second candles. BUT even for normally low volume coins, when a pump is beginning with the coin it could literally go from 0 1-second candles within a minute to 60 1-second candles within the next minute. ***NOTE: This DOES NOT show ANY information if the coin is going up or down but rather that a LOT more trading volume is occurring than normal.*** What this script does is scans (via request.security feature) up to 40 coins at a time and counts how many candles are printed within a user set timespan calculated in minute. 1 candle print per incremented timeframe that the chart is on. ie. if the chart is a 1 min chart it counts how many 1 min candles are printed. So, (as is in the captured image for the script) if you wanted to count how many 5 second candles are printed for each coin in 1 min then you would have to put the charts timeframe on 5sec and the setting titled 'Window of TIME(in minutes) to count bars' as 1.0 (which bc it's in minutes 1.0m = 60sec and bc 60s / 5s = 12 there would be 12 possible values that each coin can be at depending on how many bars are counted within that 1min/60sec. *** I will update to show an image of what I'm talking about here. Now, the exchange I'm scanning here is Kucoin's Margin Coins. There are 170 something coins total but I removed a few i didn't care for to make it a round 40 coins per set (there being 4 sets of 40 coins total=160 coins being scanned). To scan all 4 sets the indicator must be added 4 times to the chart and a different 'set' selected for each iteration of the script on the chart. Free users can only scan 3 at the most. All others can scan all 4 sets. In the script you can change the exchange and coins as necessary. If there done so and there are not 40 coins total just put '' '' in the extra coins spots that are not filled and the script will skip over these blankly filled spots. The suffix (traded pair) for the tickerID on all Kucoin's Margin Coin's is USDT so that's what i have inputted in the main function on line 46 (will need to be changed if that differs from the coins you want to scan. Next in the line of settings is 'Window of TIME(in minutes) to count bars' which has already been discussed. Following that is the setting "Table Shows" which the results are all in a table and the table will present the coins that have either "Passed" or "Failed" depending on which you choose. The next setting determines what passes or fails. If there are 12 possible rows for the coins to be in (as described above) then this setting is the "Pass/Fail Cutoff" level. So if you want to show all the coins that are in rows 11 and 12 (as in the image at top) then 11 should be selected here. At this point you will see all the coins that have a lot of volume in them. Finding coin names in the table that are usually not with a ton of volume will present your present movers. NOTE: coins like BTC and ETH will almost always be in these levels so it does not indicate anything different from the norm of these coins. Last setting is the ability to show the table on the main window or not. Hope you enjoy and find use in it. BTW this screener format is the same as the others I have published. If you like, check those out too. If you find difficulty using then refer to those as well as they have additional info in them on how to use the scanner and its format. Lastly, in the script is the ability to print the plots and labels but I commented them out bc its really just a jumbled mess. In the commented out sections there is a Random Color Function (provided by @hewhomustnotbenamed which was developed on the basis of Function-HSL-color by @RicardoSantos. All right, peace brothers....and sisters.

**** Also, I see how the "levels" could be confusing so I will put them into a % format soon (probably not today) so that the "Pass/Fail Cutoff" can be in % format so that if "passed" is chosen and 50% is chosen (in the new setting that will be changed) then it'll show you all the coins that have more than 50% of the bars printed within the time window chosen. Goodluck in all your trading adventures. ChasinAlts out.

JohnEhlersFourierTransformLibrary "JohnEhlersFourierTransform"

Fourier Transform for Traders By John Ehlers, slightly modified to allow to inspect other than the 8-50 frequency spectrum.

reference:

www.mesasoftware.com

high_pass_filter(source) Detrended version of the data by High Pass Filtering with a 40 Period cutoff

Parameters:

source : float, data source.

Returns: float.

transformed_dft(source, start_frequency, end_frequency) DFT by John Elhers.

Parameters:

source : float, data source.

start_frequency : int, lower bound of the frequency window, must be a positive number >= 0, window must be less than or 30.

end_frequency : int, upper bound of the frequency window, must be a positive number >= 0, window must be less than or 30.

Returns: tuple with float, float array.

db_to_rgb(db, transparency) converts the frequency decibels to rgb.

Parameters:

db : float, decibels value.

transparency : float, transparency value.

Returns: color.

BjCandlePatternsLibrary "BjCandlePatterns"

Patterns is a Japanese candlestick pattern recognition Library for developers. Functions here within detect viable setups in a variety of popular patterns. Please note some patterns are without filters such as comparisons to average candle sizing, or trend detection to allow the author more freedom.

doji(dojiSize, dojiWickSize) Detects "Doji" candle patterns

Parameters:

dojiSize : (float) The relationship of body to candle size (ie. body is 5% of total candle size). Default is 5.0 (5%)

dojiWickSize : (float) Maximum wick size comparative to the opposite wick. (eg. 2 = bottom wick must be less than or equal to 2x the top wick). Default is 2

Returns: (series bool) True when pattern detected

dLab(showLabel, labelColor, textColor) Produces "Doji" identifier label

Parameters:

showLabel : (bool) Shows label when input is true. Default is false

labelColor : (series color) Color of the label border and arrow

textColor : (series color) Text color

Returns: (series label) A label visible at the chart level intended for the title pattern

bullEngulf(maxRejectWick, mustEngulfWick) Detects "Bullish Engulfing" candle patterns

Parameters:

maxRejectWick : (float) Maximum rejection wick size.

The maximum wick size as a percentge of body size allowable for a top wick on the resolution candle of the pattern. 0.0 disables the filter.

eg. 50 allows a top wick half the size of the body. Default is 0% (Disables wick detection).

mustEngulfWick : (bool) input to only detect setups that close above the high prior effectively engulfing the candle in its entirety. Default is false

Returns: (series bool) True when pattern detected

bewLab(showLabel, labelColor, textColor) Produces "Bullish Engulfing" identifier label

Parameters:

showLabel : (bool) Shows label when input is true. Default is false

labelColor : (series color) Color of the label border and arrow

textColor : (series color) Text color

Returns: (series label) A label visible at the chart level intended for the title pattern

bearEngulf(maxRejectWick, mustEngulfWick) Detects "Bearish Engulfing" candle patterns

Parameters:

maxRejectWick : (float) Maximum rejection wick size.

The maximum wick size as a percentge of body size allowable for a bottom wick on the resolution candle of the pattern. 0.0 disables the filter.

eg. 50 allows a botom wick half the size of the body. Default is 0% (Disables wick detection).

mustEngulfWick : (bool) Input to only detect setups that close below the low prior effectively engulfing the candle in its entirety. Default is false

Returns: (series bool) True when pattern detected

bebLab(showLabel, labelColor, textColor) Produces "Bearish Engulfing" identifier label

Parameters:

showLabel : (bool) Shows label when input is true. Default is false

labelColor : (series color) Color of the label border and arrow

textColor : (series color) Text color

Returns: (series label) A label visible at the chart level intended for the title pattern

hammer(ratio, shadowPercent) Detects "Hammer" candle patterns

Parameters:

ratio : (float) The relationship of body to candle size (ie. body is 33% of total candle size). Default is 33%.

shadowPercent : (float) The maximum allowable top wick size as a percentage of body size. Default is 5%.

Returns: (series bool) True when pattern detected

hLab(showLabel, labelColor, textColor) Produces "Hammer" identifier label

Parameters:

showLabel : (bool) Shows label when input is true. Default is false

labelColor : (series color) Color of the label border and arrow

textColor : (series color) Text color

Returns: (series label) A label visible at the chart level intended for the title pattern

star(ratio, shadowPercent) Detects "Star" candle patterns

Parameters:

ratio : (float) The relationship of body to candle size (ie. body is 33% of total candle size). Default is 33%.

shadowPercent : (float) The maximum allowable bottom wick size as a percentage of body size. Default is 5%.

Returns: (series bool) True when pattern detected

ssLab(showLabel, labelColor, textColor) Produces "Star" identifier label

Parameters:

showLabel : (bool) Shows label when input is true. Default is false

labelColor : (series color) Color of the label border and arrow

textColor : (series color) Text color

Returns: (series label) A label visible at the chart level intended for the title pattern

dragonflyDoji() Detects "Dragonfly Doji" candle patterns

Returns: (series bool) True when pattern detected

ddLab(showLabel, labelColor) Produces "Dragonfly Doji" identifier label

Parameters:

showLabel : (bool) Shows label when input is true. Default is false

labelColor : (series color) Color of the label border and arrow

Returns: (series label) A label visible at the chart level intended for the title pattern

gravestoneDoji() Detects "Gravestone Doji" candle patterns

Returns: (series bool) True when pattern detected

gdLab(showLabel, labelColor, textColor) Produces "Gravestone Doji" identifier label

Parameters:

showLabel : (bool) Shows label when input is true. Default is false

labelColor : (series color) Color of the label border and arrow

textColor : (series color) Text color

Returns: (series label) A label visible at the chart level intended for the title pattern

tweezerBottom(closeUpperHalf) Detects "Tweezer Bottom" candle patterns

Parameters:

closeUpperHalf : (bool) input to only detect setups that close above the mid-point of the candle prior increasing its bullish tendancy. Default is false

Returns: (series bool) True when pattern detected

tbLab(showLabel, labelColor, textColor) Produces "Tweezer Bottom" identifier label

Parameters:

showLabel : (bool) Shows label when input is true. Default is false

labelColor : (series color) Color of the label border and arrow

textColor : (series color) Text color

Returns: (series label) A label visible at the chart level intended for the title pattern

tweezerTop(closeLowerHalf) Detects "TweezerTop" candle patterns

Parameters:

closeLowerHalf : (bool) input to only detect setups that close below the mid-point of the candle prior increasing its bearish tendancy. Default is false

Returns: (series bool) True when pattern detected

ttLab(showLabel, labelColor, textColor) Produces "TweezerTop" identifier label

Parameters:

showLabel : (bool) Shows label when input is true. Default is false

labelColor : (series color) Color of the label border and arrow

textColor : (series color) Text color

Returns: (series label) A label visible at the chart level intended for the title pattern

spinningTopBull(wickSize) Detects "Bullish Spinning Top" candle patterns

Parameters:

wickSize : (float) input to adjust detection of the size of the top wick/ bottom wick as a percent of total candle size. Default is 34%, which ensures the wicks are both larger than the body.

Returns: (series bool) True when pattern detected

stwLab(showLabel, labelColor, textColor) Produces "Bullish Spinning Top" identifier label

Parameters:

showLabel : (bool) Shows label when input is true. Default is false

labelColor : (series color) Color of the label border and arrow

textColor : (series color) Text color

Returns: (series label) A label visible at the chart level intended for the title pattern

spinningTopBear(wickSize) Detects "Bearish Spinning Top" candle patterns

Parameters:

wickSize : (float) input to adjust detection of the size of the top wick/ bottom wick as a percent of total candle size. Default is 34%, which ensures the wicks are both larger than the body.

Returns: (series bool) True when pattern detected

stbLab(showLabel, labelColor, textColor) Produces "Bearish Spinning Top" identifier label

Parameters:

showLabel : (bool) Shows label when input is true. Default is false

labelColor : (series color) Color of the label border and arrow

textColor : (series color) Text color

Returns: (series label) A label visible at the chart level intended for the title pattern

spinningTop(wickSize) Detects "Spinning Top" candle patterns

Parameters:

wickSize : (float) input to adjust detection of the size of the top wick/ bottom wick as a percent of total candle size. Default is 34%, which ensures the wicks are both larger than the body.

Returns: (series bool) True when pattern detected

stLab(showLabel, labelColor, textColor) Produces "Spinning Top" identifier label

Parameters:

showLabel : (bool) Shows label when input is true. Default is false

labelColor : (series color) Color of the label border and arrow

textColor : (series color) Text color

Returns: (series label) A label visible at the chart level intended for the title pattern

morningStar() Detects "Bullish Morning Star" candle patterns

Returns: (series bool) True when pattern detected

msLab(showLabel, labelColor, textColor) Produces "Bullish Morning Star" identifier label

Parameters:

showLabel : (bool) Shows label when input is true. Default is false

labelColor : (series color) Color of the label border and arrow

textColor : (series color) Text color

Returns: (series label) A label visible at the chart level intended for the title pattern

eveningStar() Detects "Bearish Evening Star" candle patterns

Returns: (series bool) True when pattern detected

esLab(showLabel, labelColor, textColor) Produces "Bearish Evening Star" identifier label

Parameters:

showLabel : (bool) Shows label when input is true. Default is false

labelColor : (series color) Color of the label border and arrow

textColor : (series color) Text color

Returns: (series label) A label visible at the chart level intended for the title pattern

haramiBull() Detects "Bullish Harami" candle patterns

Returns: (series bool) True when pattern detected

hwLab(showLabel, labelColor, textColor) Produces "Bullish Harami" identifier label

Parameters:

showLabel : (bool) Shows label when input is true. Default is false

labelColor : (series color) Color of the label border and arrow

textColor : (series color) Text color

Returns: (series label) A label visible at the chart level intended for the title pattern

haramiBear() Detects "Bearish Harami" candle patterns

Returns: (series bool) True when pattern detected

hbLab(showLabel, labelColor, textColor) Produces "Bearish Harami" identifier label

Parameters:

showLabel : (bool) Shows label when input is true. Default is false

labelColor : (series color) Color of the label border and arrow

textColor : (series color) Text color

Returns: (series label) A label visible at the chart level intended for the title pattern

haramiBullCross() Detects "Bullish Harami Cross" candle patterns

Returns: (series bool) True when pattern detected

hcwLab(showLabel, labelColor, textColor) Produces "Bullish Harami Cross" identifier label

Parameters:

showLabel : (bool) Shows label when input is true. Default is false

labelColor : (series color) Color of the label border and arrow

textColor : (series color) Text color

Returns: (series label) A label visible at the chart level intended for the title pattern

haramiBearCross() Detects "Bearish Harami Cross" candle patterns

Returns: (series bool) True when pattern detected

hcbLab(showLabel, labelColor) Produces "Bearish Harami Cross" identifier label

Parameters:

showLabel : (bool) Shows label when input is true. Default is false

labelColor : (series color) Color of the label border and arrow

Returns: (series label) A label visible at the chart level intended for the title pattern

marubullzu() Detects "Bullish Marubozu" candle patterns

Returns: (series bool) True when pattern detected

mwLab(showLabel, labelColor, textColor) Produces "Bullish Marubozu" identifier label

Parameters:

showLabel : (bool) Shows label when input is true. Default is false

labelColor : (series color) Color of the label border and arrow

textColor : (series color) Text color

Returns: (series label) A label visible at the chart level intended for the title pattern

marubearzu() Detects "Bearish Marubozu" candle patterns

Returns: (series bool) True when pattern detected

mbLab(showLabel, labelColor, textColor) Produces "Bearish Marubozu" identifier label

Parameters:

showLabel : (bool) Shows label when input is true. Default is false

labelColor : (series color) Color of the label border and arrow

textColor : (series color) Text color

Returns: (series label) A label visible at the chart level intended for the title pattern

abandonedBull() Detects "Bullish Abandoned Baby" candle patterns

Returns: (series bool) True when pattern detected

abwLab(showLabel, labelColor, textColor) Produces "Bullish Abandoned Baby" identifier label

Parameters:

showLabel : (bool) Shows label when input is true. Default is false

labelColor : (series color) Color of the label border and arrow

textColor : (series color) Text color

Returns: (series label) A label visible at the chart level intended for the title pattern

abandonedBear() Detects "Bearish Abandoned Baby" candle patterns

Returns: (series bool) True when pattern detected

abbLab(showLabel, labelColor, textColor) Produces "Bearish Abandoned Baby" identifier label

Parameters:

showLabel : (bool) Shows label when input is true. Default is false

labelColor : (series color) Color of the label border and arrow

textColor : (series color) Text color

Returns: (series label) A label visible at the chart level intended for the title pattern

piercing() Detects "Piercing" candle patterns

Returns: (series bool) True when pattern detected