Relative Performance Indicator - TrendSpider StyleRelative Performance Indicator - TrendSpider Style

📈 Overview

This Relative Performance (RP) indicator measures how your stock is performing compared to a benchmark index, displayed as a percentile ranking from 0-100. Based on TrendSpider's methodology, it answers the critical question: "Is this stock a leader or a laggard?"

Unlike simple ratio charts, this indicator uses percentile ranking to normalize relative performance, making it easy to identify when a stock is showing exceptional strength (>80) or concerning weakness (<20) compared to its historical relationship with the benchmark.

✨ Key Features

Three Calculation Modes:

Quarterly: 3-month relative performance for swing trading

Yearly: Weighted 4-quarter performance for position trading

TechRank: Composite of 6 technical indicators for multi-factor analysis

Clean Visual Design:

Green fills above 80 (strong outperformance)

Red fills below 20 (significant underperformance)

Dotted median line at 50 for quick reference

Current value label for instant reading

Flexible Benchmarks:

Compare against major indices (SPY, QQQ, IWM)

Sector ETFs for within-sector analysis

Custom symbols for specialized comparisons

Built-in Alerts:

Strong performance zone entry (>80)

Weak performance zone entry (<20)

Median crossovers (50 level)

📊 How To Use

Buy Signals:

RP crosses above 80: Stock entering leadership status

RP holding above 60: Maintaining relative strength

RP rising while price consolidating: Accumulation phase

Sell/Avoid Signals:

RP drops below 50: Losing relative strength

RP below 20: Significant underperformance

RP falling while price rising: Bearish divergence

Sector Rotation:

Compare multiple assets to find strongest sectors

Rotate into high RP assets (>70)

Exit low RP positions (<30)

🎯 Reading The Values

80-100: Exceptional outperformance - Strong buy/hold

60-80: Moderate outperformance - Hold positions

40-60: Market perform - No edge

20-40: Underperformance - Caution/reduce

0-20: Severe underperformance - Avoid/exit

⚙️ Calculation Method

Calculates percentage performance of both your stock and the benchmark

Finds the performance differential

Ranks this differential against historical values using percentile analysis

Normalizes to 0-100 scale for easy interpretation

This percentile approach adapts to different market conditions and volatility regimes, providing consistent signals whether in trending or choppy markets.

💡 Pro Tips

For Growth Stocks: Use quarterly mode with QQQ as benchmark

For Value Stocks: Use yearly mode with SPY as benchmark

For Small Caps: Compare against IWM, not SPY

For Sector Analysis: Use sector ETFs (XLK, XLF, XLE, etc.)

Combine with Price Action: High RP + price breakout = powerful signal

⚠️ Important Notes

RP is relative, not absolute - stocks can fall with high RP if the market falls harder

Choose appropriate benchmarks for meaningful comparisons

Best used in conjunction with price action and volume analysis

Historical lookback period affects sensitivity (adjustable in settings)

🔧 Customization

Fully customizable visual settings, thresholds, calculation periods, and smoothing options. Adjust the normalization lookback period (default 252 days) to fine-tune sensitivity to your trading timeframe.

📌 Credit

Inspired by TrendSpider's Relative Performance implementation, adapted for TradingView with enhanced customization options and Pine Script v6 optimization.

Tags to include: relativeperformance, relativestrength, percentile, ranking, sectorrotation, benchmark, outperformance, trendspider, marketbreadth, strengthindicator

Category: Momentum Indicators / Trend Analysis

Feel free to modify this description to match your style or add any specific points you want to emphasize!

Relativevolume

Trading Activity Index (Zeiierman)█ Overview

Trading Activity Index (Zeiierman) is a volume-based market activity meter that transforms dollar-volume into a smooth, normalized “activity index.”

It highlights when market participation is unusually low or high with a dynamic color gradient:

Light Blue → Low Activity (thin participation, low liquidity conditions)

Red/Orange → High Activity (active markets, large trades flowing in)

Additional percentile bands (20/40/60/80%) give context, helping you see whether the current activity level is in the bottom quintile, mid-range, or near historical extremes.

█ How It Works

⚪ Dollar Volume Transformation

Each bar, dollar volume is computed:

float dlrVol = close * volume

float dlrVolAvg = ta.sma(dlrVol, len_form)

Dollar volume = price × volume, smoothed by a configurable SMA window.

The result is log-transformed, compressing large outliers for a more stable signal.

⚪ Rolling Percentiles & Ranking

The log-dollar-volume series is compared to its rolling history (len_hist bars):

float p20 = ta.percentile_linear_interpolation(vscale, len_hist, 20)

float p40 = ta.percentile_linear_interpolation(vscale, len_hist, 40)

float p60 = ta.percentile_linear_interpolation(vscale, len_hist, 60)

float p80 = ta.percentile_linear_interpolation(vscale, len_hist, 80)

A normalized rank (0–1) is produced to color the main Trading Activity line.

█ How to Use

⚪ Detect High-Impact Sessions

Quickly see if today’s session is active or quiet relative to its own history — great for filtering setups that need activity.

⚪ Spot Breakouts & Traps

Combine with price action:

High activity near breakouts = strong follow-through likely.

Low activity breakouts = vulnerable to fake-outs.

⚪ Market Regime Context

Percentile bands help you assess whether participation is building up, in the middle of the range, or drying out — valuable for timing mean-reversion trades.

Above 80th percentile (red/orange) → Market is highly active, breakout trades and trend strategies are favored.

Below 20th percentile (light blue) → Market is quiet; fade moves or wait for expansion.

Watch transitions from blue → orange as a signal of growing institutional participation.

█ Settings

Formation Window (bars) – Number of bars used to average dollar volume before log transform.

History Window (bars) – Lookback period for percentile calculations and rank normalization.

-----------------

Disclaimer

The content provided in my scripts, indicators, ideas, algorithms, and systems is for educational and informational purposes only. It does not constitute financial advice, investment recommendations, or a solicitation to buy or sell any financial instruments. I will not accept liability for any loss or damage, including without limitation any loss of profit, which may arise directly or indirectly from the use of or reliance on such information.

All investments involve risk, and the past performance of a security, industry, sector, market, financial product, trading strategy, backtest, or individual's trading does not guarantee future results or returns. Investors are fully responsible for any investment decisions they make. Such decisions should be based solely on an evaluation of their financial circumstances, investment objectives, risk tolerance, and liquidity needs.

Volume Stress Level V2Volume Stress Level V2, is designed to provide a nuanced view of "RECENT" trading volume by identifying different levels of volume stress relative to a smoothed average.

Key Features:

Dynamic Volume Stress Calculation: The indicator calculates volume stress based on a Simple Moving Average (SMA) of volume and its standard deviation. The length of the SMA and the multiplier for the standard deviation are fully customizable, allowing you to adapt the indicator to different market conditions and trading styles.

Visual Volume Zones: The script visually categorizes volume into distinct zones:

Low Volume Zone: Represented by a white background, indicating periods of lower-than-average trading activity.

Normal Volume Zone: Highlighted in blue, signifying typical trading volume.

Medium Volume Zone: Displayed in yellow, denoting a moderate increase in volume.

High Volume Zone: Shown in orange, indicating significant volume spikes.

Spike Volume Zone: Marked in black, representing extreme volume events.

Customizable Background: You have the option to enable or disable the colored background fill for these volume zones, providing flexibility in how you visualize the data.

Bar Coloring: The volume bars themselves are color-coded according to the identified volume stress level, offering an immediate visual cue on your chart.

Adjustable Parameters:

VSL Length: Controls the lookback period for the SMA and standard deviation calculations.

Multiplier: Adjusts the sensitivity of the standard deviation bands, thereby influencing the width of the volume zones.

How to Use:

This indicator can be valuable for identifying potential shifts in market sentiment, confirming breakouts, or spotting periods of accumulation and distribution. By observing the transitions between volume zones, traders can gain insights into the conviction behind price movements.

% of Average Volume% of Average Volume (RVOL)

What it is

This indicator measures cumulative volume during pre market and separately during the first 10 minutes of trading and compares it to the average 30 day volume. This matters as a high ratio of volume within the premarket and then during the first 10 minutes of trading can correlate to a stock that has a higher probability of trending in that direction throughout the day.

What it’s meant to do

Identify abnormally high or low participation early in the day.

Normalize volume by time of session, so 9:40 volume is compared to past 9:40 volume—not to the full-day total.

Provide consistent RVOL across 1–5–15–60 minute charts (the same market state yields similar readings).

Handle pre-market cleanly (optional) without inflating RVOL.

How it works (plain English)

Cumulative Intraday Volume: Adds up all bars from the session (or pre-market, if enabled) up to “now.”

Time-Matched Baseline: For each prior day in your lookback, it accumulates only up to the same intraday minute and averages those values.

RVOL %: RVOL = (Today cumulative / Average cumulative at same time) × 100.

This “like-for-like” approach prevents the classic mistakes that overstate RVOL in pre-market or make it drift with timeframe changes.

Works best on

Intraday charts: 1, 2, 3, 4, 5, 10, 15, 30, 45, 60 min

Regular & extended hours: NYSE/Nasdaq equities, futures, ETFs

Daily/weekly views are supported for reference, but the edge comes from intraday time-matched analysis.

Tip: For thin names or very early pre-market, expect more variability—lower liquidity increases noise.

Customization (Inputs → Settings)

Lookback Sessions (e.g., 20): How many prior trading days to build the average.

Include Pre-Market (on/off): If on, RVOL accumulates from pre-market start and compares to historical pre-market at the same time; if off, it begins at the regular session open only.

Session Timezone / Exchange Hours: Choose the session definition that matches your market (e.g., NYSE) so “time-matched” means the same thing every day.

Cutoff Minute (Optional): Fix a reference minute (e.g., 6:40 a.m. PT / 9:40 a.m. ET) to evaluate RVOL at a standard check-in time.

Smoothing (Optional): Apply a short moving average to the RVOL line to reduce jitter.

Thresholds & Colors: Set levels (e.g., 150%, 300%) to color the plot/labels and trigger alerts.

Show Labels/Debug: Toggle on-chart labels (current RVOL%, baseline vols) for quick audits.

On-chart visuals & alerts

RVOL% Line/Histogram: Color-coded by thresholds (e.g., >300% “exceptional”, >150% “elevated”).

Session Markers: Optional vertical lines for pre-market/regular open.

Alerts:

RVOL Crosses Above X% (e.g., 150%, 300%)

RVOL Crosses Below X%

RVOL Rising/Falling (slope-based, optional)

Good defaults to start

Lookback: 20 sessions

Pre-market: Off for large caps, On for momentum screens

Thresholds: 150% (notable), 300% (exceptional)

Smoothing: 0–3 bars (or off for fastest response)

Notes & best practices

Timeframe consistency: Because calculations are time-matched, RVOL should remain directionally consistent across intraday timeframes. If you see divergences, confirm your session hours & timezone match your instrument’s exchange.

Holiday/half days: These are included in history; you can shorten lookback or exclude such sessions if your workflow prefers.

Low-float names: Consider a slightly longer lookback to reduce outlier effects.

TL;DR

A time-matched RVOL that treats pre-market correctly, stays stable across intraday timeframes, and is fully customizable for your exchange hours, thresholds, and alerts—so you can spot real participation when it matters.

Burner Volume CandlesVisually see different candle colors based on volume relative to the look back period (default is last 20 candles).

This allows you to see if a current candle print is standard, high, or extreme sell/buy volume relative to the look back period.

This has been primarily used on the 30s timeframe on NQ.

It is also advised to take the NY open candle volume with a grain of salt as that is typically the extreme volume so it doesn't make this indicator as useful when it comes to those candles.

RVol - Time-based relative volumeImportant to see whether the stock has significantly more activity than usual.

Alternatively you can use TradingView's built-in "Relative Volume At Time" indicator (anchor timeframe: 1 day, length: 10, calculation mode: cumulative, adjust unconfirmed: true), which is essentially the same - without the colorizing of the bars.

More infos: www.reddit.com

Advanced Volume Profile Pro Delta + POC + VAH/VAL# Advanced Volume Profile Pro - Delta + POC + VAH/VAL Analysis System

## WHAT THIS SCRIPT DOES

This script creates a comprehensive volume profile analysis system that combines traditional volume-at-price distribution with delta volume calculations, Point of Control (POC) identification, and Value Area (VAH/VAL) analysis. Unlike standard volume indicators that show only total volume over time, this script analyzes volume distribution across price levels and estimates buying vs selling pressure using multiple calculation methods to provide deeper market structure insights.

## WHY THIS COMBINATION IS ORIGINAL AND USEFUL

**The Problem Solved:** Traditional volume indicators show when volume occurs but not where price finds acceptance or rejection. Standalone volume profiles lack directional bias information, while basic delta calculations don't provide structural context. Traders need to understand both volume distribution AND directional sentiment at key price levels.

**The Solution:** This script implements an integrated approach that:

- Maps volume distribution across price levels using configurable row density

- Estimates delta (buying vs selling pressure) using three different methodologies

- Identifies Point of Control (highest volume price level) for key support/resistance

- Calculates Value Area boundaries where 70% of volume traded

- Provides real-time alerts for key level interactions and volume imbalances

**Unique Features:**

1. **Developing POC Visualization**: Real-time tracking of Point of Control migration throughout the session via blue dotted trail, revealing institutional accumulation/distribution patterns before they complete

2. **Multi-Method Delta Calculation**: Price Action-based, Bid/Ask estimation, and Cumulative methods for different market conditions

3. **Adaptive Timeframe System**: Auto-adjusts calculation parameters based on chart timeframe for optimal performance

4. **Flexible Profile Types**: N Bars Back (precise control), Days Back (calendar-based), and Session-based analysis modes

5. **Advanced Imbalance Detection**: Identifies and highlights significant buying/selling imbalances with configurable thresholds

6. **Comprehensive Alert System**: Monitors POC touches, Value Area entry/exit, and major volume imbalances

## HOW THE SCRIPT WORKS TECHNICALLY

### Core Volume Profile Methodology:

**1. Price Level Distribution:**

- Divides price range into user-defined rows (10-50 configurable)

- Calculates row height: `(Highest Price - Lowest Price) / Number of Rows`

- Distributes each bar's volume across price levels it touched proportionally

**2. Delta Volume Calculation Methods:**

**Price Action Method:**

```

Price Range = High - Low

Buy Pressure = (Close - Low) / Price Range

Sell Pressure = (High - Close) / Price Range

Buy Volume = Total Volume × Buy Pressure

Sell Volume = Total Volume × Sell Pressure

Delta = Buy Volume - Sell Volume

```

**Bid/Ask Estimation Method:**

```

Average Price = (High + Low + Close) / 3

Buy Volume = Close > Average ? Volume × 0.6 : Volume × 0.4

Sell Volume = Total Volume - Buy Volume

```

**Cumulative Method:**

```

Buy Volume = Close > Open ? Volume : Volume × 0.3

Sell Volume = Close ≤ Open ? Volume : Volume × 0.3

```

**3. Point of Control (POC) Identification:**

- Scans all price levels to find maximum volume concentration

- POC represents the price level with highest trading activity

- Acts as significant support/resistance level

- **Developing POC Feature**: Tracks POC evolution in real-time via blue dotted trail, showing how institutional interest migrates throughout the session. Upward POC migration indicates accumulation patterns, downward migration suggests distribution, providing early trend signals before price confirmation.

**4. Value Area Calculation:**

- Starts from POC and expands up/down to encompass 70% of total volume

- VAH (Value Area High): Upper boundary of value area

- VAL (Value Area Low): Lower boundary of value area

- Expansion algorithm prioritizes direction with higher volume

**5. Adaptive Range Selection:**

Based on profile type and timeframe optimization:

- **N Bars Back**: Fixed lookback period with performance optimization (20-500 bars)

- **Days Back**: Calendar-based analysis with automatic timeframe adjustment (1-365 days)

- **Session**: Current trading session or custom session times

### Performance Optimization Features:

- **Sampling Algorithm**: Reduces calculation load on large datasets while maintaining accuracy

- **Memory Management**: Clears previous drawings to prevent performance degradation

- **Safety Constraints**: Prevents excessive memory usage with configurable limits

## HOW TO USE THIS SCRIPT

### Initial Setup:

1. **Profile Configuration**: Select profile type based on trading style:

- N Bars Back: Precise control over data range

- Days Back: Intuitive calendar-based analysis

- Session: Real-time session development

2. **Row Density**: Set number of rows (30 default) - more rows = higher resolution, slower performance

3. **Delta Method**: Choose calculation method based on market type:

- Price Action: Best for trending markets

- Bid/Ask Estimate: Good for ranging markets

- Cumulative: Smoothed approach for volatile markets

4. **Visual Settings**: Configure colors, position (left/right), and display options

### Reading the Profile:

**Volume Bars:**

- **Length**: Represents relative volume at that price level

- **Color**: Green = net buying pressure, Red = net selling pressure

- **Intensity**: Darker colors indicate volume imbalances above threshold

**Key Levels:**

- **POC (Blue Line)**: Highest volume price - major support/resistance

- **VAH (Purple Dashed)**: Value Area High - upper boundary of fair value

- **VAL (Orange Dashed)**: Value Area Low - lower boundary of fair value

- **Value Area Fill**: Shaded region showing main trading range

**Developing POC Trail:**

- **Blue Dotted Lines**: Show real-time POC evolution throughout the session

- **Migration Patterns**: Upward trail indicates bullish accumulation, downward trail suggests bearish distribution

- **Early Signals**: POC movement often precedes price movement, providing advance warning of institutional activity

- **Institutional Footprints**: Reveals where smart money concentrated volume before final POC establishment

### Trading Applications:

**Support/Resistance Analysis:**

- POC acts as magnetic price level - expect reactions

- VAH/VAL provide intermediate support/resistance levels

- Profile edges show areas of low volume acceptance

**Developing POC Analysis:**

- **Upward Migration**: POC moving higher = institutional accumulation, bullish bias

- **Downward Migration**: POC moving lower = institutional distribution, bearish bias

- **Stable POC**: Tight clustering = balanced market, range-bound conditions

- **Early Trend Detection**: POC direction change often precedes price breakouts

**Entry Strategies:**

- Buy at VAL with POC as target (in uptrends)

- Sell at VAH with POC as target (in downtrends)

- Breakout plays above/below profile extremes

**Volume Imbalance Trading:**

- Strong buying imbalance (>60% threshold) suggests continued upward pressure

- Strong selling imbalance suggests continued downward pressure

- Imbalances near key levels provide high-probability setups

**Multi-Timeframe Context:**

- Use higher timeframe profiles for major levels

- Lower timeframe profiles for precise entries

- Session profiles for intraday trading structure

## SCRIPT SETTINGS EXPLANATION

### Volume Profile Settings:

- **Profile Type**: Determines data range for calculation

- N Bars Back: Exact number of bars (20-500 range)

- Days Back: Calendar days with timeframe adaptation (1-365 days)

- Session: Trading session-based (intraday focus)

- **Number of Rows**: Profile resolution (10-50 range)

- **Profile Width**: Visual width as chart percentage (10-50%)

- **Value Area %**: Volume percentage for VA calculation (50-90%, 70% standard)

- **Auto-Adjust**: Automatically optimizes for different timeframes

### Delta Volume Settings:

- **Show Delta Volume**: Enable/disable delta calculations

- **Delta Calculation Method**: Choose methodology based on market conditions

- **Highlight Imbalances**: Visual emphasis for significant volume imbalances

- **Imbalance Threshold**: Percentage for imbalance detection (50-90%)

### Session Settings:

- **Session Type**: Daily, Weekly, Monthly, or Custom periods

- **Custom Session Time**: Define specific trading hours

- **Previous Sessions**: Number of historical sessions to display

### Days Back Settings:

- **Lookback Days**: Number of calendar days to analyze (1-365)

- **Automatic Calculation**: Script automatically converts days to bars based on timeframe:

- Intraday: Accounts for 6.5 trading hours per day

- Daily: 1 bar per day

- Weekly/Monthly: Proportional adjustment

### N Bars Back Settings:

- **Lookback Bars**: Exact number of bars to analyze (20-500)

- **Precise Control**: Best for systematic analysis and backtesting

### Visual Customization:

- **Colors**: Bullish (green), Bearish (red), and level colors

- **Profile Position**: Left or Right side of chart

- **Profile Offset**: Distance from current price action

- **Labels**: Show/hide level labels and values

- **Smooth Profile Bars**: Enhanced visual appearance

### Alert Configuration:

- **POC Touch**: Alerts when price interacts with Point of Control

- **VA Entry/Exit**: Alerts for Value Area boundary interactions

- **Major Imbalance**: Alerts for significant volume imbalances

## VISUAL FEATURES

### Profile Display:

- **Horizontal Bars**: Volume distribution across price levels

- **Color Coding**: Delta-based coloring for directional bias

- **Smooth Rendering**: Optional smoothing for cleaner appearance

- **Transparency**: Configurable opacity for chart readability

### Level Lines:

- **POC**: Solid blue line with optional label

- **VAH/VAL**: Dashed colored lines with value displays

- **Extension**: Lines extend across relevant time periods

- **Value Area Fill**: Optional shaded region between VAH/VAL

### Information Table:

- **Current Values**: Real-time POC, VAH, VAL prices

- **VA Range**: Value Area width calculation

- **Positioning**: Multiple table positions available

- **Text Sizing**: Adjustable for different screen sizes

## IMPORTANT USAGE NOTES

**Realistic Expectations:**

- Volume profile analysis provides structural context, not trading signals

- Delta calculations are estimations based on price action, not actual order flow

- Past volume distribution does not guarantee future price behavior

- Combine with other analysis methods for comprehensive market view

**Best Practices:**

- Use appropriate profile types for your trading style:

- Day Trading: Session or Days Back (1-5 days)

- Swing Trading: Days Back (10-30 days) or N Bars Back

- Position Trading: Days Back (60-180 days)

- Consider market context (trending vs ranging conditions)

- Verify key levels with additional technical analysis

- Monitor profile development for changing market structure

**Performance Considerations:**

- Higher row counts increase calculation complexity

- Large lookback periods may affect chart performance

- Auto-adjust feature optimizes for most use cases

- Consider using session profiles for intraday efficiency

**Limitations:**

- Delta calculations are estimations, not actual transaction data

- Profile accuracy depends on available price/volume history

- Effectiveness varies across different instruments and market conditions

- Requires understanding of volume profile concepts for optimal use

**Data Requirements:**

- Requires volume data for accurate calculations

- Works best on liquid instruments with consistent volume

- May be less effective on very low volume or exotic instruments

This script serves as a comprehensive volume analysis tool for traders who need detailed market structure information with integrated directional bias analysis and real-time POC development tracking for informed trading decisions.

VSA - The Volume HUDVSA Volume HUD: Your At-a-Glance Volume Dashboard

Tired of cluttered charts with multiple indicators taking up screen space?

The VSA Volume HUD is a clean, powerful, and fully customisable Heads-Up Display that puts all the critical volume and price action data you need into one compact box, right on your chart.

Designed for traders who rely on Volume Spread Analysis (VSA), this tool helps you instantly gauge the strength, conviction, and context behind every price move as it happens.

Key Features

This indicator isn't just about showing the current volume; it provides a comprehensive, real-time analysis of the market's activity.

Real-time VSA Dashboard: A persistent on-screen table that updates with every tick, giving you instant feedback without needing to look away from the price. The HUD is fully draggable (hold Ctrl/Cmd + click and drag) to place it anywhere you like.

Essential Volume Metrics:

Current Volume: Displayed in a clean, abbreviated format (e.g., 1.25M for millions, 54.3K for thousands).

% Change (vs. Previous Bar): Instantly see if volume is expanding or contracting.

Vs Short-Term Average: Compare the current bar's volume to a moving average to spot unusual spikes.

Volume Velocity: Measures the rate of change in volume over a short period, helping you spot acceleration or deceleration in market interest.

Relative Volume (RVOL): See how the current volume compares to the average for that specific time of day, perfect for identifying abnormally high or low activity.

Price Action & Volatility Context:

Range vs. ATR: Quickly determine if the current bar's volatility is expanding or contracting compared to the recent average.

Price vs. VWAP: See how far the current price has deviated from the session's Volume-Weighted Average Price, a key level for institutional traders.

Deep Customization is Key

Tailor the HUD to perfectly match your trading style and chart aesthetic.

Display & Layout:

Compact Mode: Remove the metric labels for a sleek, minimalist view that saves screen space.

Bar Meters: Enable optional visual bars next to key metrics for a quick, graphical representation of strength.

Total Control: Toggle every single metric on or off to build the exact dashboard you need. Adjust text size, position, and background opacity with ease.

Smart Coloring & Visual Alerts:

Advanced VSA Coloring: This isn't just about up/down candles. The script intelligently colors volume based on confluence. It highlights increasing volume on a strong up-bar (bullish confirmation) or increasing volume on a down-bar (potential climax or distribution), giving you a deeper VSA context.

High Volume Highlight: Make standout bars impossible to miss! The entire HUD background can change color automatically when volume surges past a custom threshold (e.g., over 150% of the average), instantly drawing your attention to critical moments.

Full Color Customization: Change every color to match your chart's theme, including separate colors for bullish/bearish moves, the background, and the border.

How to Use It

The VSA Volume HUD is a powerful confirmation tool. Use it to:

Confirm Breakouts: Look for a spike in Volume vs. Average and RVOL as price breaks a key level.

Spot Exhaustion: Notice high volume on a narrow-range candle after a long trend, visible through the Range/ATR metric.

Gauge Conviction: Use the Advanced Coloring to see if volume is supporting the price move (e.g., green volume on a green candle) or diverging from it.

Projected 65min VolumeThe script provides relative volume for the first 5min candle after its close vs 14 avg and estimates projected volume for the first 65min candle in the trading session vs avg value.

!!!The indicator is designed to work only at 5min TF!!!

Buy & Sell Volume (OWI)📊 Buy & Sell Volume (OWI) Indicator Guide

The Buy & Sell Volume (OWI) indicator is designed to provide a visual breakdown of buying and selling pressure in each candle, helping traders identify volume surges and potential market moves. It also includes a time filter to focus analysis during key trading hours.

⚙️ Setup & Inputs

When adding the indicator to your chart, you'll see several configurable inputs:

SMA Length : Sets the period for the Simple Moving Average (SMA) of total volume.

Enable Time Filter : Toggles whether to restrict analysis to US market hours (Eastern Time). |

Start Hour/Minute : Defines the beginning of the time filter window (default: 9:45 ET). |

End Hour/Minute : Defines the end of the time filter window (default: 16:15 ET). |

📈 How It Works

🔍 Volume Breakdown

Buy Volume: Estimated volume attributed to buyers, calculated based on candle position.

Sell Volume: Estimated volume attributed to sellers.

Total Volume SMA: A moving average of total volume to benchmark current activity.

⏰ Time Filter (Optional)

When enabled, the indicator only highlights volume spikes during the specified US market hours. This helps filter out noise from pre-market or after-hours trading.

🚨 Highlight Conditions

The indicator flags significant volume spikes with labels above the volume bars:

| Label | Condition |

| V+ | Volume is between 1.5× and 2× the SMA, during market hours (if enabled). |

| V++ | Volume exceeds 2× the SMA, during market hours (if enabled). |

💡 Tips

- Use shorter SMA lengths for more reactive volume analysis.

- Change the time filter if you're trading outside US market hours.

- Combine with candlestick patttern to confirm breakout or reversal signals.

Relative Volume + Z-score + Normal Volume + Avg. VolumeA statistical way to visualize volume analytically compared to traditional volume. All Lookback Periods and Colors can be changed so user can make it feel personalized

- Relative Volume (RVOL) visualizer with the color of the histogram bar changing to represent exceeding a threshold specified by the user

For example --> (1.5 = Orange Bar) & (2 = Red Bar)

- Toggle View between RVOL visualization of volume vs. normal view of volume plot

- Z score lookback for volume across specified lookback per what user wants (dot/symbol above the bar)

- Average Volume Plot

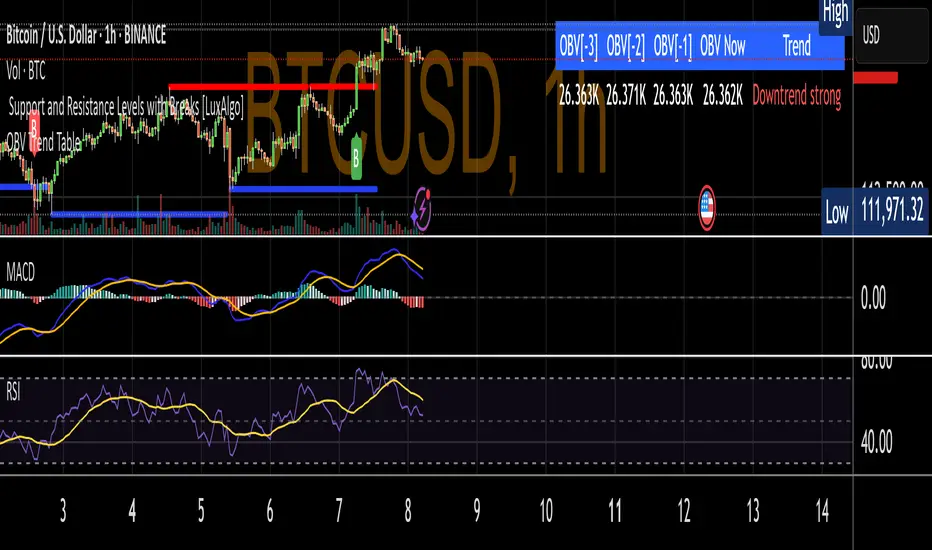

OBV Trend TableDisplays last 3 TF OBV values and current value of OBV. Also displays one of the trend values

- Uptrend healthy (price ↑ + OBV ↑)

- Downtrend strong (price ↓ + OBV ↓)

- Early reversal (price and OBV diverge)

- No clear trend (flat or mixed)

Volume Statistics - IntraweekVolume Statistics - Intraweek: For Orderflow Traders

This tool is designed for traders using volume footprint charts and orderflow methods.

Why it matters:

In orderflow trading, you care about the quality of volume behind each move. You’re not just watching price; you’re watching how much aggression is behind that price move. That’s where this indicator helps.

What to look at:

* Current Volume shows you how much volume is trading right now.

* Central Volume (median or average over 24h or 7D) gives you a baseline for what's normal volume VS abnormal volume.

* The Diff vs Central tells you immediately if current volume is above or below normal.

How this helps:

* If volume is above normal, it suggested elevated levels of buyer or seller aggression. Look for strong follow-through or continuation.

* If volume is below normal, it may signal low interest, passive participation, a lack of conviction, or a fake move.

* Use this context to decide if what you're seeing in the footprint (imbalances, absorption, traps) is actually worth acting on.

Extra context:

* The highest and lowest volume levels and their timestamps help you spot prior key reactions.

* Second and third highest bars help you see other major effort points in the recent window.

Comment with any suggestions on how to improve this indicator.

Previous VWAP Levels by Riotwolftrading The "Previous VWAP" indicator calculates and displays the previous session's Volume Weighted Average Price (VWAP) for five timeframes (Daily, Weekly, Monthly, Quarterly, Yearly).

Each VWAP is plotted as a horizontal line extending to the right edge of the chart, with customizable labels at the right to identify each level. The indicator is designed for traders who want to visualize key price levels from prior periods without cluttering the chart with current VWAPs or additional metrics like standard deviations.

**Functionality**:

- **Calculates Previous VWAPs**: Computes the VWAP for the previous session of each timeframe (Daily, Weekly, Monthly, Quarterly, Yearly) based on the input source (default: `hlc3`) and volume.

- **Visual Style** : Uses `line.new` to draw horizontal lines from five bars back to the current bar, ensuring the lines extend to the right edge of the chart. Labels are placed at the right edge using `label.new` for clear identification.

- **Customization** : Allows users to toggle visibility, adjust line styles, widths, colors, and label sizes, and choose between abbreviated or full label text.

- **Minimalist Design**: Focuses solely on previous VWAPs, omitting current VWAPs, rolling VWAPs, and standard deviation bands to keep the chart clean.

**Intended Use**: This indicator is useful for traders who rely on historical VWAP levels as support/resistance or reference points for trading decisions, particularly in strategies involving mean reversion or breakout trading.

---

### Rules and Features

*VWAP Calculation**:

- The VWAP is calculated as the cumulative sum of price (`src`) multiplied by volume (`sumSrcVol`) divided by the cumulative volume (`sumVol`) for each timeframe.

- The "previous VWAP" is the VWAP value from the prior session, captured when a new session begins (e.g., new day, week, month, etc.).

- The indicator uses the `hlc3` (average of high, low, close) as the default source, but users can modify this in the settings.

**Timeframes**:

- **Daily**: Previous day's VWAP.

- **Weekly**: Previous week's VWAP.

- **Monthly**: Previous month's VWAP.

- **Quarterly**: Previous quarter's VWAP (3 months).

- **Yearly**: Previous year's VWAP (12 months).

- New sessions are detected using `ta.change(time(period))` for each timeframe.

**Line Drawing**:

- Lines are drawn using `line.new` from `time ` (five bars back) to the current bar (`time`), ensuring they extend to the right edge of the chart.

- Lines are updated only on the last confirmed bar (`barstate.islast`) to optimize performance and avoid repainting.

- Previous lines are deleted (`line.delete`) to prevent overlapping or clutter.

**Labels**:

- Labels are drawn at the right edge (`x=time`, `xloc=xloc.bar_time`) with `label.new`.

- Users can choose between abbreviated labels (e.g., "pvD" for Previous Daily VWAP) or full labels (e.g., "Prev Daily VWAP").

- Label sizes are customizable (`tiny`, `small`, `normal`, `large`, `huge`).

- Labels are deleted (`label.delete`) on each update to maintain a clean chart.

5. **Customization Options**:

- **Visibility**: Toggle each VWAP (Daily, Weekly, Monthly, Quarterly, Yearly) on or off.

- **Colors**: Individual color settings for each VWAP line and label (default colors: Daily=#E12D7B, Weekly=#F67B52, Monthly=#EDCD3B, Quarterly=#3BBC54, Yearly=#2665BD).

- **Line Style**: Choose from `solid`, `dotted`, or `dashed` lines.

- **Line Width**: Adjustable from 1 to 4 pixels.

- **Label Settings**: Enable/disable labels, abbreviate text, and select label size.

- **Source**: Customize the price source (default: `hlc3`).

**Performance Optimization**:

- The indicator only updates lines and labels on the last confirmed bar to minimize computational overhead.

- Uses `var` to initialize variables and avoid unnecessary recalculations.

- Deletes previous lines and labels to prevent chart clutter.

---

### Usage Instructions

1. **Add to Chart**:

- In TradingView, go to the Pine Editor, paste the script, and click "Add to Chart."

- The indicator will overlay on the price chart, showing previous VWAP lines and labels.

2. **Configure Settings**:

- Open the indicator settings to customize:

- Toggle visibility of each VWAP timeframe.

- Adjust colors, line style, and width.

- Enable/disable labels, choose abbreviation, and set label size.

- Modify the source if needed (e.g., use `close` instead of `hlc3`).

3. **Interpretation**:

- **Previous VWAPs**: Act as dynamic support/resistance levels based on the prior session's volume-weighted price.

- **Timeframes**: Use shorter timeframes (Daily, Weekly) for intraday/swing trading, and longer timeframes (Monthly, Quarterly, Yearly) for positional trading.

- **Labels**: Identify each VWAP level at the right edge of the chart for quick reference.

4. **Best Practices**:

- Use on charts with sufficient volume data, as VWAP relies on volume (a warning is triggered if no volume data is available).

- Combine with other indicators (e.g., moving averages, RSI) for confirmation in trading strategies.

- Adjust line styles and colors to avoid visual overlap with other chart elements.

---

### Example Use Case

A trader using a 1-hour chart can add the "Previous VWAP" indicator to identify key levels from the prior day, week, or month. For example:

- The Previous Daily VWAP might act as a support level for a bullish trend.

- The Previous Weekly VWAP could serve as a target for a swing trade.

- Labels at the right edge make it easy to identify these levels without cluttering the chart.

This indicator provides a clean, customizable way to visualize previous VWAPs, making it ideal for traders who want historical price context with minimal chart noise. For the complete Pine Script code, refer to the artifact provided in the previous response.

JHW Volume Based Buy and Sell MomentumThe JHW Volume-Based Buy and Sell Momentum indicator is a custom momentum oscillator designed to capture market sentiment based on volume dynamics and price rate of change (ROC). It aims to identify bullish or bearish momentum by analyzing how price reacts to increasing or decreasing trading volume.

Core Logic:

The indicator calculates the Rate of Change (ROC) of the closing price.

It then accumulates this ROC separately based on whether the current volume is lower or higher than the previous bar:

If volume decreases, the ROC is added to a "negative volume index" accumulator.

If volume increases, the ROC is added to a "positive volume index" accumulator.

These two accumulators are combined to form a net momentum line.

Smoothing:

A Simple Moving Average (SMA) is applied to both accumulators over a user-defined period (default: 25 bars).

The sum of these smoothed values forms the signal line.

Visualization:

The indicator plots:

The net momentum line (yellow).

The smoothed signal line (blue).

The area between the two lines is filled with color:

Yellow when momentum is above the signal (bullish).

Blue when momentum is below the signal (bearish).

Bar colors are also adjusted to reflect the current momentum state.

Use Case:

This indicator helps traders:

Detect volume-driven momentum shifts.

Identify potential buy or sell zones based on volume behavior.

Confirm trends or spot early reversals.

Volume-Based Candle ShadingThe Volume Shading indicator dynamically adjusts the color brightness of each price bar based on relative volume levels. It helps traders quickly identify whether a candle formed on low, average, or high volume without needing to reference a separate volume pane.

Candles are shaded dynamically as they form, so you can watch volume flow into them in real time. This indicator is designed to be as minimally intrusive as possible, allowing you to visualize volume levels without extra clutter on your charts.

The additional volume indicator in the preview above is there just for a point of reference to allow you to see how the shading on the bars correlates to the volume.

⸻

SETTINGS:

Bullish and bearish base colors — These serve as the midpoint (average volume) for shading.

Brightness mapping direction — Optionally invert the shading so that either high volume appears darker or lighter.

Volume smoothing length — Defines how many bars are averaged to determine what constitutes “normal” volume.

Candles with volume above average will appear darker or lighter depending on user preference, while those with average volume will be painted the chosen colors, giving an intuitive gradient that enhances volume awareness directly on the chart.

⸻

USES:

Confirming price action: Highlight when breakout candles or reversal bars occur with high relative volume, strengthening signal conviction.

Spotting low-volume moves: Identify candles that lack volume support, potentially signaling weak continuation or false breakouts.

Enhancing visual analysis: Overlay volume dynamics directly onto price bars, reducing screen clutter and aiding faster decision-making.

Custom visual workflows: Adapt the visual behavior of candles to your trading style by choosing color direction and base tones.

Volume Spike AlertIndicator Features:

📊 Core Functionalities:

Exceptional Volume Detection:

Calculates volume in USD (volume × price)

Compares it against a 90-day average (3 months)

Configurable from 1 to 252 days

Visual Signals:

Green labels for bullish candles with high volume

Red labels for bearish candles with high volume

Displays excess percentage (e.g., +45.2%)

Dual Alert System:

AlertCondition: For manual alert configuration in TradingView

Alert(): Automated alerts with detailed information

⚙️ Available Settings:

Average Period: 1–252 days (default: 90 days)

Enable/Disable Alerts: Configurable checkbox

Show/Hide Labels: Visual control

Label Size: Tiny, Small, Normal, Large

Minimum Threshold: Minimum percentage required to trigger a signal

📋 Displayed Information:

On Labels:

Excess percentage (e.g., +67.3%)

Color based on candle direction

In the Table:

Current volume in millions USD

Average volume in millions USD

Excess percentage

Alert status (ACTIVE/NORMAL)

Calculation period

In Alerts:

Candle type (BULLISH 🟢 / BEARISH 🔴)

Symbol and current price

Current volume vs. average

Timeframe used

Volume Spike Analyzer(SMA10-Based)📊 **Volume Spike Analyzer (SMA10-Based)**

This indicator highlights abnormal volume activity by comparing current volume to the 10-period Simple Moving Average (SMA) of volume. It helps traders visually identify unusual activity that may precede breakouts, reversals, or news-driven moves.

---

🔧 **Features:**

• ✅ Colors volume bars:

• Green = Volume > SMA(10)

• Red = Volume ≤ SMA(10)

• ✅ Detects and labels spike levels:

• 🔶2x — Volume > 2x SMA(10)

• 🟢3x — Volume > 3x SMA(10)

• 🔴4x — Volume > 4x SMA(10)

• ✅ Built-in alerts for all 3 spike levels

---

📈 **Best Use Cases:**

• Confirm breakouts with strong volume

• Detect accumulation/distribution

• Filter low-volume setups

• Combine with VWAP/EMA for directional confirmation

---

⏱️ **Recommended Timeframes:**

• Intraday: 5m, 15m, 1h

• Also works on daily for swing trades

---

🧠 **Pro Tips:**

• Use with VWAP or EMA(20/50/200) for confluence

• Add SMA(Volume, 10) to your price chart for quick correlation

• Combine with candle pattern detection for signal validation

---

Time-Specific Volume AverageA volume indicator based on historic volume.

Checks for the average volume in the past few days at the same time of day. This helps you determine when there is truly volume in the markets.

We will see often see sustained volume above the average during a clear trend. If you see spikes in volume without it being sustained above the average, it is very likely that the trend will die off quickly.

This is very helpful in determining whether to trade based on a trend following system, or a range based system.

Settings are below:

Days to average: Number of days to look back(tradingview has limits depending on your plan)

SMA Length: Number of "volume averages" to look at. Keep this at 1 if you want the average volume at the exact moment in the day. If you increase it, will also average in the past few candles of "volume averages".

SMA Multiplier: Multiplies the SMA by this amount(helps to get higher quality trends)

Relative Volume Indicator (RVOL)Relative Volume Indicator (RVOL) is a powerful tool designed for intraday traders who want to quickly identify key areas of interest based on relative volume activity.

This indicator compares the current candle’s volume with the historical average volume over a customizable lookback period (default is 20). It highlights when volume is:

🔴 Below average

🟡 Average

🟢 Above average

🟣 Extremely high

⚙️ Customizable Settings:

Lookback period for average volume

Volume thresholds (average, above average, extreme)

Custom colors for each volume zone

🎯 Best suited for:

Scalping strategies

Breakout confirmation

Volume-based entries at key support/resistance levels

Spotting unusual or algorithmic trading activity

📈 Works across all timeframes.

🎨 Fully customizable from the settings panel.

🔔 Alerts coming in future versions.

VWAP Adaptive (RelVol-Adjusted)This indicator provides an Adaptive VWAP that adjusts volume weighting using RelVol (Relative Volume at Time), offering a more accurate and context-aware price reference during sessions with irregular volume behavior.

Classic VWAP calculates the average price weighted by raw volume, without considering the time of day. This becomes a serious limitation during major market events such as CPI releases, FOMC announcements, NFP, or large-cap earnings. These events often trigger massive volume spikes within one or two candles. As a result, the classic VWAP gets pulled toward those extreme prices and becomes permanently skewed for the rest of the session.

In such conditions, classic VWAP becomes unreliable. It no longer reflects fair value and often misleads traders relying on it for dynamic support, resistance, or reversion signals.

This Adaptive VWAP improves on that by using RelVol, which compares the current volume to the average volume seen at the same time over previous sessions. It gives more weight to price when volume is typical for that moment, and adjusts the influence when volume is statistically abnormal. This reduces the impact of isolated volume spikes and stabilizes the VWAP path, even in high-volatility environments.

For example, on SPY 1-minute or 5-minute charts during a CPI release, a massive spike in volume and price can occur within a single candle. Classic VWAP will immediately anchor itself to that spike. Adaptive VWAP using RelVol softens that effect and maintains a more realistic trajectory.

Key features:

- Adaptive VWAP weighted by time-adjusted Relative Volume (RelVol)

- Designed to maintain VWAP reliability during macroeconomic events

- Flexible anchoring: Session, Week, Month, Quarter, Earnings, etc.

- Optional display of Classic VWAP for comparison

- Up to 3 customizable deviation bands (standard deviation or percentage)

This tool is ideal for intraday traders who need a VWAP that remains usable and unbiased, even in volatile sessions. It adds robustness to VWAP-based strategies by incorporating time-sensitive volume normalization.

VOL & AVG OverlayCustom Session Volume Versus Average Volume

Description:

This indicator will create an overlay on your chart that will show you the following information:

Custom Session Volume

Average For Selected Session

Percentage Comparison

Options:

Set Custom Time Frame For Calculations

Set Custom Time Frame For Average Comparison

Set Custom Time Zone

Enable / Disable Each Value

Change Text Color

Change Background Color

Change Table location

Example:

Set indicator to 30 period average. Set custom time frame to 9:30am to 10:30am Eastern/New York.

When the time frame for the calculation is closed , the indicator will provide a comparison of the current days volume compared to the average of 30 previous days for that same time frame and display it as a percentage in the table.

In this example you could compare how the first hour of the trading day compares to the previous 30 day's average, aiding in evaluating the potential volume for the remainder of the day.

Notes:

Times must be entered in 24 hour format. (1pm = 13:00 etc.)

This indicator is for Intra-day time frames, not > Day.

If you prefer data in this format as opposed to a plotted line, check out my other indicator: ADR & ATR Overlay

On Balance Volume W DivergenceOBV With Divergence Indicator

A comprehensive On Balance Volume (OBV) indicator enhanced with divergence detection capabilities.

Core Features:

Classic OBV calculation with volume-based price movement tracking

Advanced divergence detection system

Multiple smoothing options for OBV

Bollinger Bands integration

Technical Components:

Volume-based price movement analysis

Pivot point detection for divergence

Customizable lookback periods

Adjustable divergence range parameters

Customization Options:

Multiple Moving Average types (SMA, EMA, SMMA, WMA, VWMA)

Bollinger Bands with adjustable standard deviation

Divergence sensitivity settings

Visual customization for signals and alerts

The indicator combines traditional OBV analysis with modern divergence detection, offering traders a powerful tool for identifying potential trend reversals and market momentum shifts.

Key Parameters:

- Pivot Lookback Right/Left: 5 (default)

- Divergence Range: 5-60 bars

- MA Length: 14 (default)

- BB StdDev: 2.0 (default)

Alert System:

- Bullish divergence alerts

- Bearish divergence alerts

- Customizable alert messages

Note: The indicator requires volume data to function properly and will display an error if volume data is not available.